Abstract

This study examines auditor resignations around a client firm’s stock price crash. Overall, the study suggests that a firm’s crash risk is one of the key factors influencing auditors’ client-retention decisions. A stock price crash increases the likelihood of lawsuits and financial restatements in the future. After controlling for risk factors that contribute to resignation decisions, I document a positive association between auditor resignations and stock price crashes. Further findings indicate that auditor size affects auditor–client relationship decisions before a crash occurs: Big auditors tend to resign more often from client firms with high crash risk compared with smaller auditors. However, auditor size becomes irrelevant once a crash occurs, as the client firms then become risky clients to both large and small auditors. This study therefore provides evidence that auditors of different sizes face different incentives to alter their relationship prior to a stock price crash and that these incentives change following a crash.

Introduction

Stock price is a widely used indicator that directly demonstrates the market reaction to new information about a firm’s future. In light of the 2008 financial crisis and a series of accounting scandals, both academics and practitioners have investigated the factors that may accelerate a sudden and dramatic decline in stock prices. To explain market crashes, accounting researchers have focused primarily on information asymmetry between managers and shareholders. They have argued that managers have incentives to overstate a firm’s performance and future prospects by strategically choosing to release good news to the market while withholding bad news. Then, once the accumulated bad news is released to the market, a stock price crash occurs.

This study examines auditor changes as they relate to stock price crashes. While engaging with client firms, auditors often gain in-depth knowledge about the firms. The knowledge that auditors obtain may contain valuable private information that cannot be easily acquired from firms’ financial statements, voluntary disclosures, or even highly sophisticated outside analyses. Because auditors have more information about a firm compared with outside investors and analysts, researchers view any change in auditor as an object of scrutiny and strive to uncover and comprehend the reasons behind the change. Researchers have contributed to the auditing literature by developing various explanations for auditor resignations. This study is motivated by prior literature that has investigated firm characteristics associated with auditor–client relationship decisions. 1 In this study, using a stock price crash event as a comprehensive market-based metric that reflects firms’ opacity, I examine the relationship between auditor changes and price crashes and whether auditor size affects client-retention decisions before and after crashes.

The first part of the analysis investigates the relationship between auditor resignations and stock price crashes by testing whether auditor resignation events precede or follow crashes. First, I expect auditor resignations to precede stock price crashes for two reasons. If the client firm is likely to experience a crash in the near future, then an auditor is more likely to resign beforehand to rebalance its risk associated with that audit engagement. It is also highly probable that dramatic stock market drops occur as a result of auditor resignations. Second, I hypothesize that auditor resignations may also follow a stock price crash because auditors consider a price crash an additional engagement risk. When firms tend to withhold bad news that leads to stock price crashes, it is more likely that they will encounter lawsuits or financial restatements in the future. If so, both channels can increase engagement risks for auditors, thus increasing the possibility of auditor resignations. 2 The regression results support the hypotheses. Results show that the likelihood of lawsuits and restatements increases after a stock price crash, and auditor resignations precede stock price crashes. Economically, the odds of a crash increase by 51% when a firm experienced an auditor resignation in the preceding year, indicating that market behavior correlates with auditor-resignation events. The test further shows that auditor resignations follow stock price crashes (odds ratio = 1.365), indicating that an auditor has an incentive to leave its client firm after that firm experiences a crash.

Next, I examine whether auditor size affects the resignation decision made shortly before or after crashes. I argue that compared with non-Big 4 auditors, Big 4 (PricewaterhouseCoopers, KPMG, Ernst & Young, and Deloitte Touche Tohmatsu Limited) are more likely to resign from client firms prior to crashes as Big 4 auditors are more sensitive to the risk associated with audit services and often exhibit more flexibility in adjusting their client portfolios (Catanach et al., 2011; Rama & Read, 2006). However, I predict that an auditor’s size will not affect its resignation decision after a firm experiences a crash. That is because, at the time of a crash, the firm will become a risky client for both large and small auditors; hence, incentives to walk away from the client firms become indifferent to both types of auditors. Consistent with these hypotheses, the regression results indicate that the odds of an auditor resignation before a crash increase by 141% when a predecessor auditor is a Big 4 auditor, whereas auditor size becomes irrelevant to auditor–client relationship decisions after crashes.

Finally, I examine the selection of successor auditors once these high-risk firms experience auditor changes. I hypothesize that Big 4 auditors are less likely to replace former auditors not only because Big 4 auditors are more selective in choosing client firms but also because firms consider large audit firms to be more conservative and less lenient in their audit services (Becker et al., 1998; Craswell et al., 1995). By comparing the resignation sample with firms without any auditor changes, I find that Big 4 auditors are less likely to become successor auditors if a potential client previously changed auditors either before or after a crash.

This study contributes to the literature in several ways. First, it contributes to the literature on auditor–client relationships by demonstrating that the market reacts to auditor resignations and that auditors do consider a stock price crash a risk factor when they make client-retention decisions. Prior studies have investigated various factors related to audit engagement risks, including litigation and financial restatement, yet there is little research on the effect of client firms’ stock return distribution on auditors’ client-retention decisions. The present study contributes to the literature by demonstrating that a crash risk is one of the key factors that change the auditor–client relationship while controlling for other factors. Moreover, by examining the different decisions made by Big 4 and non-Big 4 auditors and how auditors change around the time of stock price crashes, I provide evidence that shows how auditor type affects the decision-making of auditors with respect to such crashes. Similar to previous research, this study supports the argument that Big 4 auditors tend to adjust their client portfolios when confronted with high audit engagement risk, possibly because of their larger client base and reputation concerns. Furthermore, this study adds value to the capital markets literature that examines the relation between crash risk and firm opacity. Habib et al. (2018) examine the stock price crash literature and find that the majority of published studies focus on the determinants of crash risk. Rather than looking at the reason for a crash, this study sheds light on the consequences of stock price crashes by observing auditor resignations.

Section “Prior Literature and Development of the Hypotheses” highlights the prior literature on stock price crashes and auditor changes and proceeds to develop the hypotheses. Section “Research Design” outlines the research designs, including the sample selection methods. Section “Empirical Results” discusses the descriptive statistics followed by the empirical results, and Section “Conclusion” concludes the study.

Prior Literature and Development of the Hypotheses

Research on Auditor Changes

When engaging with clients and performing audit services, auditors are typically exposed to litigation risks in the event of an audit failure. Hence, they consider various risk factors when making client-retention decisions (Ghosh & Tang, 2015). Many researchers have examined auditors’ responses to the risks associated with audit engagements. Their studies find that with an increased risk, auditors adjust their audit plans and audit fees (Houston et al., 1999; Pratt & Stice, 1994), as well as increase audit efforts, as measured by audit hours (Cho et al., 2017; Houston, 1999; Jung, 2016). Moreover, Krishnan and Krishnan (1996) find that auditors tend to issue modified opinions in the presence of an increased risk. Along with changes in audit fees and audit opinions, auditors also rebalance client portfolios in an effort to reduce risks (Bockus & Gigler, 1998; Johnstone, 2000; Jones & Raghunandan, 1998; Krishnan & Krishnan, 1997; Shu, 2000). In a recent study, Huang and Scholz (2012) show that more auditor changes occur subsequent to financial restatement announcements, arguing that such changes are caused by an increase in auditors’ perceptions of audit risks due to restatements. Considered together, prior studies show that auditors rebalance portfolios for risk management purposes.

Another stream of literature investigates the ways in which large and small audit firms differ when it comes to adjusting client portfolios. For example, prior studies noted that Big 4 auditors are more selective when deciding to engage risky clients and become more conservative with an increased number of resignation events after the Sarbanes–Oxley Act (SOX; Catanach et al., 2011; Government Accountability Office [GAO], 2006; Rama & Read, 2006). It is also well known that Big 4 auditors have characteristics different from non-Big 4 auditors. Researchers find that Big 4 auditors charge higher audit fees (Craswell et al., 1995) and are associated with lower discretionary accruals (Becker et al., 1998) and higher earnings response coefficients (Teoh & Wong, 1993). Overall, these papers suggest that larger auditors are generally different from smaller auditors but have become more conservative and risk averse, which has led to their more intensive efforts to manage audit engagement risks.

Researchers have also proposed explanations for client-initiated auditor changes. In particular, some studies have found that firms’ or auditors’ characteristics can influence auditor–client relationship decisions. For instance, Ettredge et al. (2007) examine the relation between audit fees and auditor dismissals and show that firms paying high audit fees tend to fire auditors more often in the post-SOX period. Conversely, Mande and Son (2013) find that the likelihood of dismissal increases after financial restatements, arguing that auditor changes can result from client firms’ tendency to blame their auditors for dishonorable events or in response to pressure from capital markets. Other studies find that firms are strategically changing their auditors for favorable audit opinions and audit practices (Davidson et al., 2006). Thus, as mentioned by DeFond and Francis (2005), auditor changes are often thought to occur for opportunistic reasons, including a firm’s hope to obtain a more lenient auditor.

Research on Stock Price Crashes

Stock price crashes are viewed as a sudden drop in market prices after accumulated negative information is leaked to the market once it reaches a certain threshold. They are thus represented by a negative skewness in the stock return distribution. Prior studies on stock price crashes suggest that they are closely related to various types of firm-specific risk factors.

There is an ample body of literature that examines how a firm’s new information about its future, especially with regard to the firm’s opacity, affects crash risk (e.g., Jin & Myers, 2006). Specifically, prior studies have found that a firm’s crash risk increases as accumulated accruals increase (Hutton et al., 2009; Zhu, 2016) and as the firm engages in real earnings management activities (B. Francis et al., 2016). Researchers have also shown that the crash risk increases with other aspects of a firm’s opacity, including its earnings smoothing, tax avoidance, and ambiguity in annual reports (Chen et al., 2017; Ertugrul et al., 2017; Kim et al., 2011), whereas it decreases with better disclosures about the firm’s corporate social responsibility, more conservative accounting policies, and better financial statement comparability (Kim et al., 2014; Kim, Li, et al., 2016; Kim & Zhang, 2016).

Furthermore, prior studies have argued that a manager’s incentive in corporate earnings also contributes to a higher future crash risk; that is, the crash risk increases if firms have overconfident and younger CEOs (Andreou et al., 2017; Kim, Wang, & Zhang, 2016). Prior literature also demonstrated that a sound corporate governance system and large holdings of dedicated institutional investors mitigate information asymmetry, thus reducing the crash risk (H. An & Zhang, 2013; Andreou et al., 2016; Hong & Lee, 2015). In line with the effect of corporate governance on crash risk, researchers have found that auditors’ client-specific knowledge, measured by tenure, and industry specialization reduce a firm’s crash risk as well (Callen & Fang, 2017; Robin & Zhang, 2015).

As noted by Habib et al. (2018), compared with the large body of literature on the determinants of a crash risk, few studies have focused on the consequences of crashes. Habib et al. (2018) point out that only two publications provide insights into what happens subsequent to crashes. Z. An et al. (2015) document that a firm’s speed of leverage adjustment changes as the crash risk increases. Meanwhile, Hackenbrack et al. (2014) find an increase in audit fees prior to stock price crashes, suggesting that the change in audit fees reflects client-specific information that auditors learn before the market does. Although not directly investigated in the study, Hackenbrack et al.’s (2014) work may suggest that an auditor may be switched due to an increase in audit fees for firms with a high crash risk. It is often the case that auditor dismissal is driven by higher audit fees, whereas auditor resignation decisions are driven by various risk factors associated with audit services. By examining auditors’ resignation decisions around crashes, this study adds to the stock price crash literature by identifying one of the consequences of stock price crashes.

Hypotheses Development

The auditing literature shows that auditors consider various risks when making client-retention decisions. Among all risk factors, the litigation risk can be very costly to auditors, as investors often try to recover a portion of their losses by suing the auditor. In fact, while prior studies have demonstrated many determinants of litigation risk (e.g., DeFond & Zhang, 2014), some researchers argue that the variability of stock returns and poor stock performances affect the likelihood of potential litigation against auditors (e.g., Lys & Watts, 1994). Because client firms’ stock price performance or volatile price movements can increase auditors’ litigation costs, I expect that a left skewness of stock returns—a stock price crash—will increase the litigation risk, thus raising the likelihood of auditor resignation. On the contrary, firms may misstate their financial statements to strategically withhold bad news, which will eventually lead to greater financial restatements. Auditors who audit these misstating firms with a high crash risk are expected to rebalance their client portfolio to lower their audit risk. For these reasons, I expect to see auditor resignations increase subsequent to stock price crashes.

Auditors adjust their client portfolios partially because they want to avoid increased audit risks and also to maintain their reputation. It is documented from prior studies that auditors have reputational concerns, especially during the engagement process, because firms consider reputation a key factor in selecting an auditor (Hilary & Lennox, 2005). Because of these concerns, along with auditors’ knowledge about client firms, auditors sometimes rebalance their portfolios to maintain risks at a reasonable level. In fact, Elder et al. (2009) show that auditors use various techniques to reduce their audit risks, and Hackenbrack et al. (2014) find that auditors increase their audit fees in advance due to future crash risk.

In this study, after controlling for firm characteristics, which include audit fees and audit opinions, I test whether auditors also respond to a client’s increased crash risk in another way. Given that auditors often gain in-depth knowledge about the client firm and industry and given their reputational concerns, I predict that auditors will resign from firms with high crash risks. Moreover, it is likely that the market views auditor resignation as a red flag, increasing the likelihood of a stock price crash in the future. Thus, I hypothesize that auditor resignations precede stock price crashes.

There have been significant changes in the risk dynamics of audit markets because of frequent regulatory interventions (DeFond & Zhang, 2014). Most notably, with the rapid increase in audit risk subsequent to SOX, auditors have faced changes in auditor–client relationships. For example, Raghunandan and Rama (2006) find that audit fees increased after SOX after controlling for auditor size. Moreover, Huang and Scholz (2012) show that both Big 4 and non-Big 4 auditors resign after financial restatement announcements. All these results support the notion that both non-Big 4 and Big 4 auditors respond to a high audit risk by adjusting their audit fees or making resignation decisions. Assuming that a firm becomes a risky client to any type of auditor once it had a crash, I predict that auditors, irrespective of whether they are Big 4 or non-Big 4 auditors, will adjust their client portfolios. Thus, I hypothesize that both Big 4 and non-Big 4 auditors are likely to walk away from client firms after a crash.

Although all auditors are likely to adjust client portfolios in response to an increased audit risk, many studies have demonstrated that larger auditors behave differently from smaller auditors in the presence of the same risk. Studies have shown not only that larger auditors provide high-quality audit services (Becker et al., 1998; J. R. Francis & Wang, 2008) but also that they can be more independent from client firms. For example, DeAngelo (1981) observes that larger auditors have a larger client base, which enables them to rebalance client portfolios more easily in cases of increased audit risks. Furthermore, as Jones and Raghunandan (1998) show, the likelihood that larger auditors will audit risky clients drops significantly as litigation costs increase. According to Rama and Read (2006), Big 4 auditors have also been found to resign more often in the post-SOX period. As Big 4 auditors can be more independent from clients due to a larger client pool, I expect them to resign more often when confronted with a higher crash risk. Thus, unlike Hypothesis 3, which relates to auditor resignation decisions after crashes, I hypothesize that when a client firm has a higher risk of experiencing a crash, Big 4 auditors are more likely than non-Big 4 auditors to walk away.

Finally, this study examines who takes the successor auditor role following auditor changes around stock price crashes. I predict that Big 4 auditors will be less likely to become successor auditors when they see auditor changes related to stock price crashes because larger auditors are more independent (DeAngelo, 1981) and more selective when making client-retention decisions compared with smaller auditors (Catanach et al., 2011; GAO, 2006). At the same time, risky firms are more likely to avoid Big 4 auditors, which prefer more conservative accounting practices, so I predict that firms will be less likely to hire Big 4 auditors after they experience auditor changes around crashes. Thus, I present the following hypotheses, which predict a negative relation between auditor size and auditor changes in two cases—auditor resignations that occur before a crash and those that occur after a crash:

Research Design

Sample and Data

Three databases are used in this study: stock price crashes are defined using the Center for Research in Security Prices (CRSP) daily stock file; information about auditors, including auditor–client relationship changes, is collected from Audit Analytics; and firm characteristics are gathered using Compustat. Table 1, Panel A, presents a brief summary of the sample selection process. I include only U.S.-incorporated firms and those that are not in the financial services industries (SIC Codes 6000–6999). Moreover, following Hutton et al. (2009), I exclude low-priced stocks (average price of less than US$2.50 for the year). To eliminate concerns related to auditor changes resulting from Arthur Anderson’s collapse in the early 2000s, my sample period is 2014–2013. A total of 4,766 firms (27,912 observations) are selected, of which 1,299 firms (1,522 observations) changed their auditors at least once during the sample period.

Sample Characteristics.

Note. Table 1 provides general information about the sample used in this study. Panel A presents the sample selection process, and Panel B shows the distribution of stock price crashes and auditor-resignation events by year. For Panel C, the focus is on firms with auditor-resignation events (266 observations). In Panel C, auditors are separated into two groups based on their size, their Big 4 and non-Big 4 affiliation, and which auditor firms rotate. CRSP = Center for Research in Security Prices.

Measurement of a Firm-Specific Stock Price Crash

Firms are defined as having a crash week when their firm-specific weekly return is more than 3.2 standard deviations below the mean over the entire fiscal year (e.g., Kim et al., 2011). To obtain firm-specific weekly returns and weekly market index returns, I summed daily returns and daily CRSP value-weighted market indices from Thursday to Wednesday. 3 Then, using the following market model regression, I gathered residual returns and defined them as firm-specific weekly returns, denoted as W, which is a natural log of one plus the residual returns.

The regression contains

Empirical Models

Before I study the relationship between auditor resignations and stock price crashes, I first examine whether a crash increases a likelihood of lawsuits or financial restatements in the future (subsequent 2 years) using the following regression model:

LAWSUIT is a binary variable that equals 1 if there was at least one instance of litigation against the company based on one of the Audit Analytics categories (Accounting and Auditing Enforcement Release, Accounting Malpractice, Class Action, Securities Law, and Tax), and 0 if there were no lawsuits against the company. Another dependent variable is RESTATE, which equals 1 if a firm restates a financial statement in which restating negatively affected the firm’s income number, and 0 otherwise. An independent variable of interest, CRASH, measures whether a firm experienced at least one crash week during a fiscal year. Twelve control variables are included in the regression to eliminate other factors that might trigger litigation or financial restatement events. All continuous variables in the regression are winsorized at the 1st and 99th percentiles, as these original variables had highly skewed distributions (e.g., K. Y. Lee, 2018).

Given the idea that auditors face a higher risk of lawsuit and restatement for firms with stock price crashes, I then examine whether auditor resignations are more likely following stock price crashes using the following regression model:

To determine the relation between stock price crashes and auditor resignations in the following year, AUDRES is measured at t+ 1, whereas CRASH is measured at t. Compared with Equation 2, I included one additional variable (RISK) to control for the level of risk that auditors encounter. Specifically, following Ghosh and Tang (2015), I form three variables for each of the risk factors (litigation risk, audit risk, and business risk) and then add these variables to construct an overall risk score. A firm has a high litigation risk score if it is in a high-tech industry, has low stock returns, and/or experienced a lawsuit or financial restatement. A firm’s audit risk increases if it has high discretionary accruals, market-to-book ratio, or external financing, if it is a small company, and/or if it has a weak internal control system. Finally, the business risk score is associated with a low Z score, low asset return, and more going-concern opinions. By definition, the overall risk score, RISK, ranges from 0 to 12, with a larger value representing a greater risk. After controlling for the level of risk, I expect a crash to provide incremental information regarding auditor resignation in a subsequent year: auditors are expected to resign from clients more often after stock price crashes (positive

Furthermore, to test whether auditor resignations are likely to precede stock price crashes, I model the relation between stock price crashes in a given year and auditor-resignation events in the previous year as follows:

While all 13 control variables in Equation 3 are included in Equation 4 to eliminate factors that might trigger firms’ stock price crashes, I also include CRASH measured at t− 1 as a control variable because the likelihood of a crash is fairly persistent. As mentioned in Hypothesis 2, I anticipate that auditor resignations will precede stock price crashes because of a negative market reaction to auditor resignation or because of auditors resigning before crashes resulting from a high audit risk. Thus, I expect the coefficient

Next, the subsample of firms that experienced a stock price crash at least once during the sample period and the subsample of firms that did not are used separately for the remaining analyses. As discussed in Hypothesis 3, I do not expect the incentives for large and small auditors to be different after a firm has experienced a crash. I test whether Big 4 auditors are more likely to resign after a crash compared with non-Big 4 auditors using the following model:

Once a crash occurs, auditors’ incentives to leave the client firm will increase. In other words, firms become risky clients to both Big 4 and non-Big 4 auditors after a crash; thus, the effect of auditor size on the decision to resign subsequent to a crash is unlikely to be significant. Therefore, I do not expect

Using Equation 6, I then examine whether auditor change decisions prior to crashes are affected by auditor size. To do so, I again use PBIG4 as a variable of interest and see whether Big 4 auditors, compared with smaller auditors, make different client-retention decisions for clients with a high crash risk. I expect to see a positive

The final regression models are used to determine whether Big 4 auditors are less likely to become successor auditors after an auditor resignation around crashes. First, I examine which auditors take a job after auditor resignations prior to crashes using following model:

Because I am focusing on auditor changes prior to a crash, AUDRES is measured at t− 1, a year before a crash happens, whereas the control variables are measured at t− 2. The dependent variable is SBIG4, which is an indicator variable that equals 1 if a successor auditor is a Big 4 auditor and 0 otherwise. I predict that different types of auditors will make different decisions regarding whether they accept a position as a successor auditor following an auditor change. Because Big 4 auditors are more selective in audit engagements, a negative

I also investigate the type of successor auditor, focusing on auditor change events subsequent to crashes, using Equation 8, where AUDRES is measured at t+ 1, a year after a crash. For auditor changes subsequent to crashes, I also argue that smaller auditors are more likely to replace former auditors, as Big 4 auditors will be less likely to take such jobs due to their low tolerance for audit risk after auditor changes subsequent to stock price crashes. Thus, I expect to observe a negative

Empirical Results

Descriptive Statistics

Table 1 provides general information about the sample characteristics. The sample selection procedure is illustrated in Panel A, which shows how the final 27,912 observations (4,766 firms) were selected. In the sample, 6,514 observations include firms that experienced stock price crashes, and 1,522 observations include firms with auditor-change events, about 17% of which are attributed to resignations and 83% are dismissals. Panel B shows the distributions of stock price crashes and auditor resignations by year. In the sample period (2004–2013), crashes occurred more often in the earlier years, with a peak in 2008. In addition, auditors walked away from their clients more often in the earlier years of the sample period, with a subsequent downward trend. Panel C of Table 1 shows a closer analysis of the sample firms with auditor resignations. In Panel C, predecessor and successor auditors are each separated into two groups, Big 4 and non-Big 4. I then divide the auditor-resignation sample into four categories: Big 4 to Big 4, Big 4 to non-Big 4, non-Big 4 to Big 4, and non-Big 4 to non-Big 4. Most of the firms in which the auditors resigned switched from Big 4 to non-Big 4 auditors (more than 47%), whereas fewer firms changed their non-Big 4 auditors (about 35%).

Panel A of Table 2 presents the descriptive statistics for the variables used in the study. I break the sample down into an auditor-resignation group and a no-change group. On average, 23% of the firms in the sample experienced a crash, whereas of those that experienced auditor resignation, about 27% also experienced a crash. This suggests that firms with auditor resignations tend to experience a crash more often than those without any auditor changes. Compared with firms without any auditor changes, firms whose auditors resigned tend to be smaller (SIZE) and less profitable (ROA). They are also more likely to have weaker internal control (IC) and a going-concern opinion (GC), and, on average, they are more likely to be a riskier company (RISK). Moreover, the resignation group tends to have a shorter relationship with auditors (TENURE) and is less likely to have large (BIG4) or industry-specialist (SPECIAL) auditors. They also tend to take up a large proportion of the auditor’s portfolio (PCTFEE).

Descriptive Statistics and Correlations.

Notes. Panel A presents the descriptive statistics for the sample of firms for 2004–2013. In Panel A, the firms are separated into two groups: 266 firm-years in which their auditors resigned and 26,390 firm-years without any auditor changes. The mean differences between the two groups are tested using t statistics from a nonpaired test of means, assuming unequal variances. In Panel B, a Pearson (top right) and a Spearman (bottom left) correlation table is provided for the key variables. The statistical significance at the 1%, 5%, and 10% levels is denoted by ***, **, and *, respectively. See the appendix for the variable definitions.

Next, Pearson and Spearman correlations of the main variables are presented in Panel B. As the purpose of the study is to examine auditor resignations around crash events, the correlations between AUDRES at t+ 1 or t− 1 and CRASH at t are shown in Panel B. The correlation between AUDRES at t+ 1 and CRASH is 1.7%, significant at the 1% level, indicating a strong relationship between stock price crashes and auditor resignations in the subsequent year. However, the correlation between AUDRES at t− 1 and CRASH is positive but insignificant.

Empirical Results

The purpose of this study is to examine changes in auditor–client relationships around firms’ stock price crashes. To better understand auditors’ incentives to alter their relationships with clients, the study separately reports the empirical results for the auditor-resignations that occurred a year before or after stock price crashes in Tables 4 to 6. Industry and year fixed effects are included in all regressions, and standard errors are clustered at the firm level.

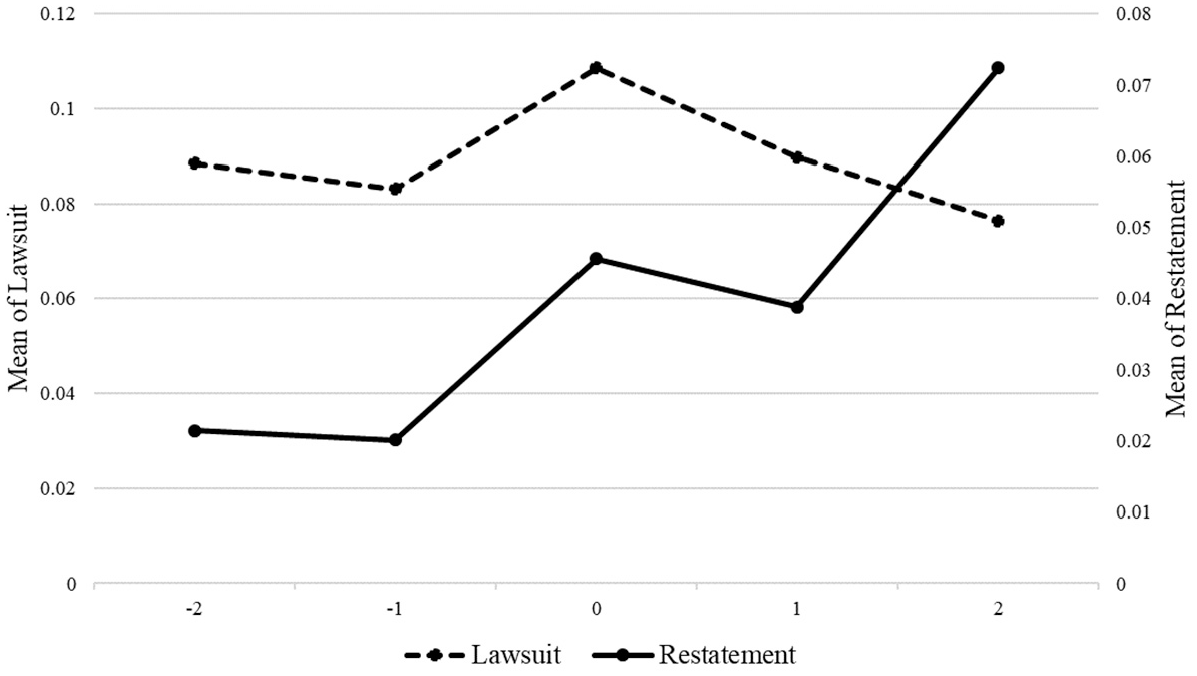

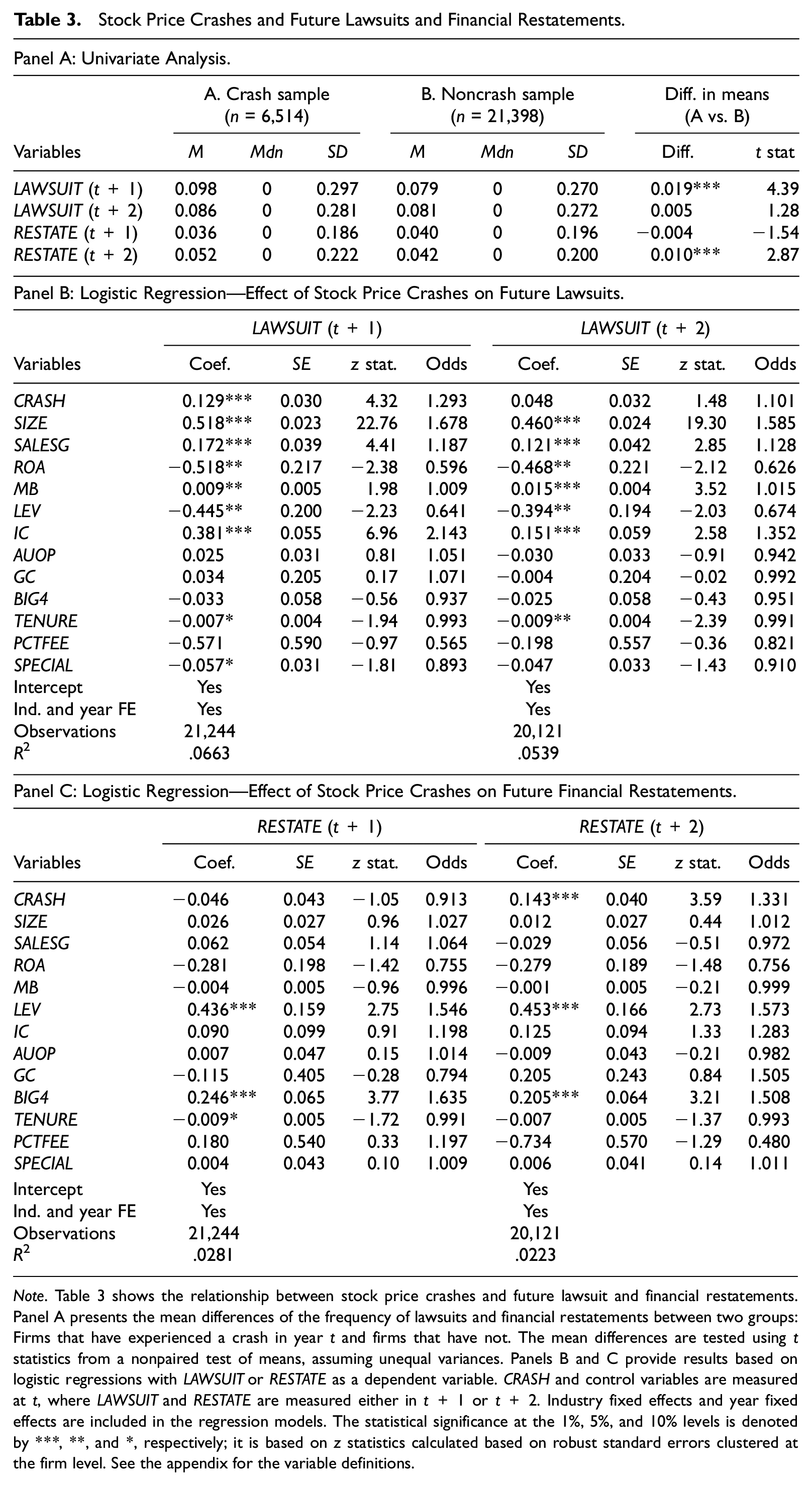

First, I examine the channels that can link stock price crashes to auditor resignations. The first channel I look into is future lawsuits. When a firm’s return distribution is negatively skewed, it is more likely to be exposed to a greater litigation risk in the future, thus leading an auditor to consider rebalancing its client portfolio. On the contrary, the second channel that can affect auditors’ decisions is financial restatements. Firms that have a tendency to withhold bad news by misstating financial statements are more likely to experience a crash. As financial restatements impose a greater risk to auditors, the chance of auditor resignation will increase for firms with a high crash risk. Figure 1 shows how the likelihood of lawsuits and restatements changes around crashes. Lawsuits and restatements show different trends: the chance of a lawsuit jumps in the year of a crash and decreases over time, whereas financial restatements lead to a huge increase in the 2 years after the crash. Univariate tests yield similar results (Table 3, Panel A): compared with firms that do not have a crash, the crash sample tends to have a greater likelihood of lawsuits in the next year and a greater possibility of restating financial statements in the 2 years after a crash. Table 3, Panel B, shows consistent results after controlling for firm and auditor characteristics in a regression setting. Thus, this study confirms a positive relation between stock price crashes and future lawsuits and financial restatements.

Lawsuits and financial restatements around stock price crashes.

Stock Price Crashes and Future Lawsuits and Financial Restatements.

Note. Table 3 shows the relationship between stock price crashes and future lawsuit and financial restatements. Panel A presents the mean differences of the frequency of lawsuits and financial restatements between two groups: Firms that have experienced a crash in year t and firms that have not. The mean differences are tested using t statistics from a nonpaired test of means, assuming unequal variances. Panels B and C provide results based on logistic regressions with LAWSUIT or RESTATE as a dependent variable. CRASH and control variables are measured at t, where LAWSUIT and RESTATE are measured either in t+ 1 or t+ 2. Industry fixed effects and year fixed effects are included in the regression models. The statistical significance at the 1%, 5%, and 10% levels is denoted by ***, **, and *, respectively; it is based on z statistics calculated based on robust standard errors clustered at the firm level. See the appendix for the variable definitions.

Table 4 provides the results of the test regarding whether auditors resign before or after stock price crash events. Panel A presents the results regarding the effect of crashes subsequent to auditor resignations. Using Equation 3, I find that the coefficient on CRASH is positive and significant at the 10% level, suggesting that auditor resignations follow stock price crashes. Economically, the result represents a 37% increase in the odds of an auditor resignation once a firm experiences a crash. Coefficients on control variables show that auditors are more likely to resign from smaller firms (SIZE), high-growth firms (ROA), and firms with more debt (LEV) or weaker internal control (IC). Auditors tend to resign more often if they are short-term auditors (TENURE) and as the client firm’s proportion within the auditor’s portfolio increases (PCTFEE). Generally, the results represent auditors’ tendency to walk away from client firms if there is a high audit risk. I further test whether auditor resignations predict future crashes by testing the relation between auditor resignations and stock price crashes in the following year. As shown in Table 4, Panel B, I find that the coefficient on AUDRES measured at t− 1 is positive and significant at the 5% level, which shows that auditors resign before a crash occurs. In addition, I find that firms are more likely to experience a crash when they have a high growth rate (SALESG) and are audited by larger auditors (BIG4). I also find a consistent likelihood of crashes (CRASH).

Logistic Regression Models for Auditor Resignations and Stock Price Crashes.

Note. Table 4 presents results that show a relationship between stock price crashes and auditor-resignations. Panel A presents results based on logistic regression to test whether the auditor resignations follow the crashes. The dependent variable is auditor resignation (AUDRES), measured at t+ 1, where CRASH and other control variables are all measured at t. In Panel B, I test whether auditor resignations precede crashes. The dependent variable is CRASH at year t, and auditor-resignation events and control variables are measured at t − 1. Industry fixed effects and year fixed effects are included in the regression models. The statistical significance at the 1%, 5%, and 10% levels is denoted by ***, **, and *, respectively; it is based on z statistics calculated based on robust standard errors clustered at the firm level. See the appendix for the variable definitions.

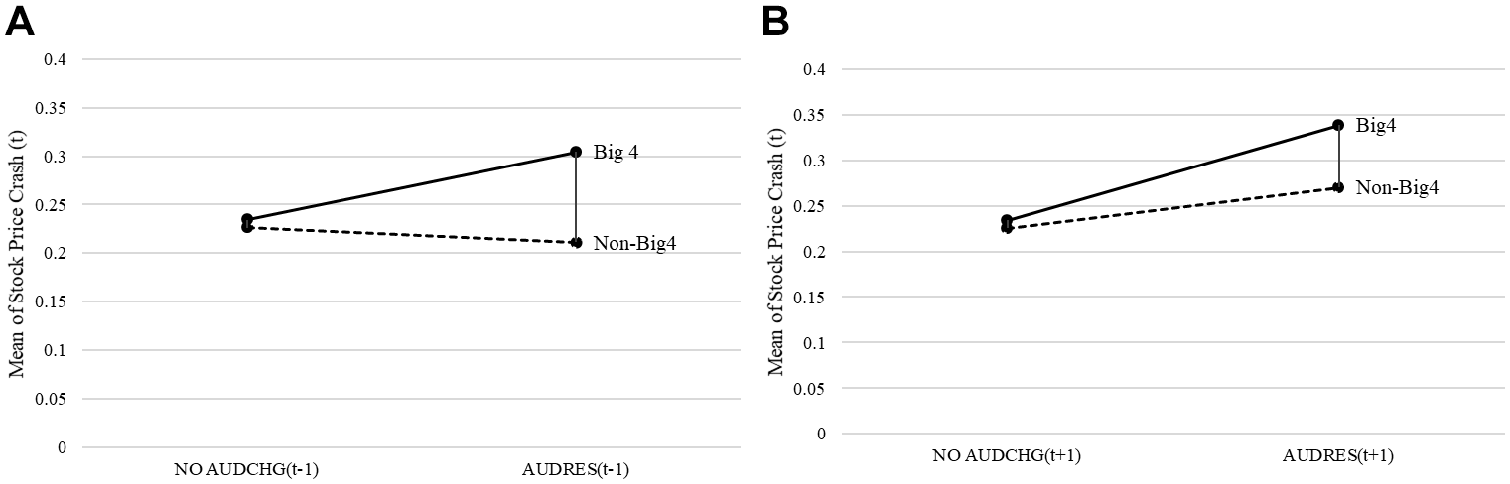

Next, I test whether auditor size affects auditors’ resignation decisions. In Figure 2, I draw interaction plots between auditor size and resignation events to visually illustrate how the likelihood of a crash changes depending on the types of auditors that resigned. Panel A shows an increase in the gap between two lines, representing Big 4 and non-Big 4 predecessor auditors, indicating that it is more likely that auditor resignations will lead to stock price crashes when the predecessor auditor is one of the large audit firms. On the contrary, when I focus on auditor resignations subsequent to crashes, the gap between the two lines is smaller, as shown in Panel B, which indicates that the effect of auditor size on its resignation decision is reduced once a crash occurs. Thus, Figure 2 provides evidence consistent with Hypotheses 3 and 4.

Predecessor auditor and resignation event interaction plots. Panel A: Auditor resignations prior to stock price crashes; Panel B: Auditor resignations following stock price crashes.

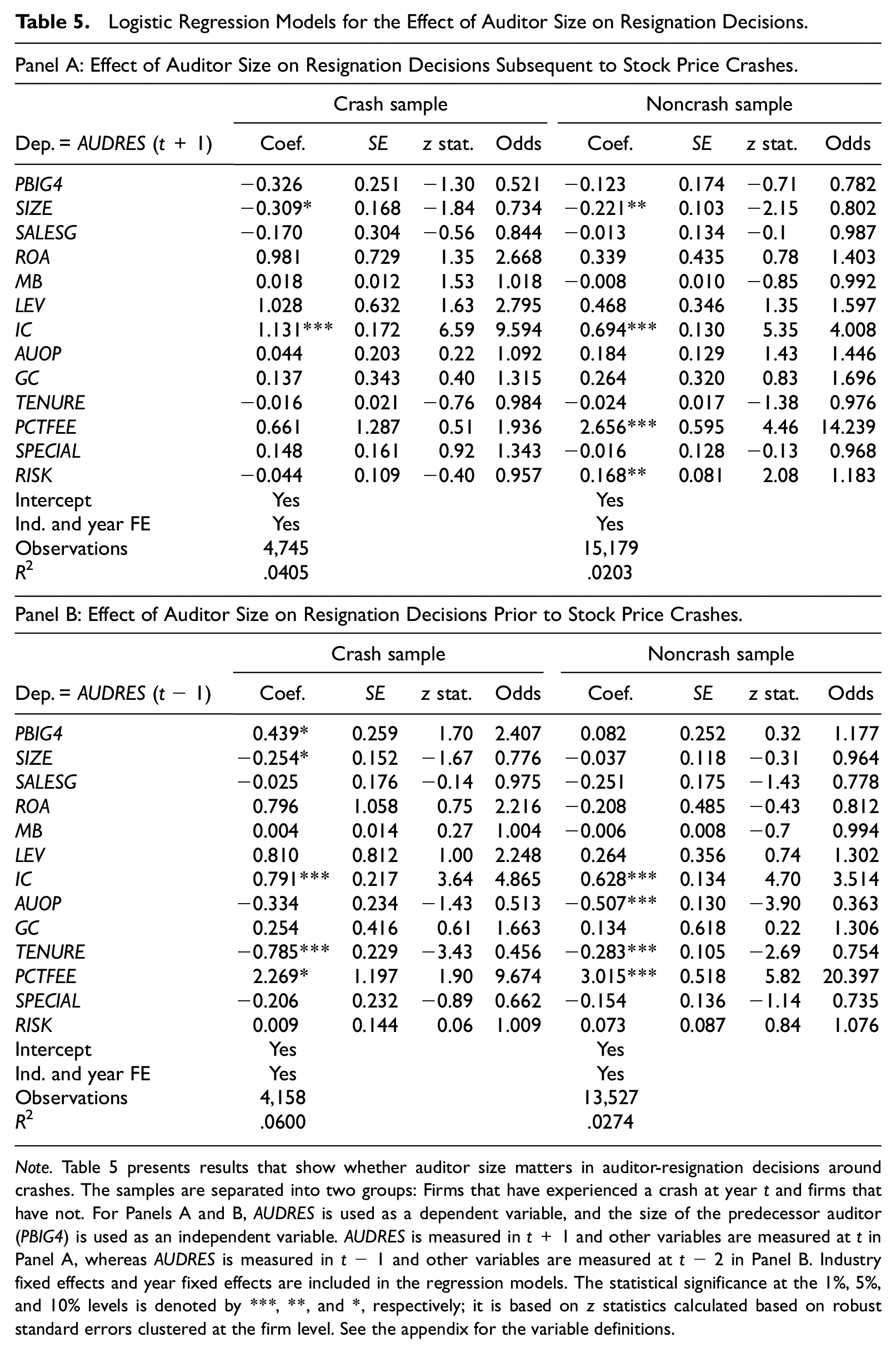

Table 5 reports these implications in a regression setting in which firms are separated into two groups: those that experienced a crash and those that did not. Consistent with my conjecture that auditor size does not matter as much once the client firm experiences a crash, I find an insignificant coefficient on PBIG4 (Panel A) for both groups. The next question I ask is if resignation decisions prior to a crash are affected by whether auditors are Big 4 auditors. Specifically, I argue that unlike smaller auditors, Big 4 auditors are more likely to resign before a crash because they have more flexibility in adjusting their client portfolio. Moreover, once a Big 4 auditor leaves its client, a crash is more likely to occur due to a negative market reaction. Table 5, Panel B, shows that the coefficient on PBIG4 is positive and significant at the 10% level, with an odds ratio of 2.407 in the crash sample. Economically, when a predecessor auditor is a Big 4 auditor, there is a 141% increase in the odds of an auditor resignation prior to a crash. However, with the no-crash sample, I do not find a strong relationship between auditor size and resignation decision in a year prior to the crash. The results shown in Table 5 suggest that, compared with non-Big 4 auditors, Big 4 auditors are more likely to walk away before a crash event, but that auditor size becomes irrelevant when it comes to resignation decisions after the crash because the firm will then become a risky client for both Big 4 and non-Big 4 auditors.

Logistic Regression Models for the Effect of Auditor Size on Resignation Decisions.

Note. Table 5 presents results that show whether auditor size matters in auditor-resignation decisions around crashes. The samples are separated into two groups: Firms that have experienced a crash at year t and firms that have not. For Panels A and B, AUDRES is used as a dependent variable, and the size of the predecessor auditor (PBIG4) is used as an independent variable. AUDRES is measured in t+ 1 and other variables are measured at t in Panel A, whereas AUDRES is measured in t − 1 and other variables are measured at t − 2 in Panel B. Industry fixed effects and year fixed effects are included in the regression models. The statistical significance at the 1%, 5%, and 10% levels is denoted by ***, **, and *, respectively; it is based on z statistics calculated based on robust standard errors clustered at the firm level. See the appendix for the variable definitions.

Finally, Table 6 presents the results for successor-auditor selection. I find that once firms have changed their auditor around crashes, small auditors tend to become successor auditors. Specifically, I find that the coefficient on AUDRES at t+ 1 is negative and significant at the 1% level (Panel A). This shows that when auditors resign after crashes, it is more likely that non-Big 4 auditors will become successor auditors. Furthermore, the coefficient on AUDRES at t− 1 is negative and significant at the 1% level (Panel B), suggesting that once firms have changed their auditors prior to crashes, Big 4 auditors are less likely to replace the former auditors. Economically, the odds of hiring Big 4 auditors as a successor decrease by 95% once firms experience an auditor resignation around a crash event. I also find that the chance of Big 4 auditors becoming a successor increases for larger firms (SIZE), firms with a lower growth rate (ROA), and firms with predecessor auditors who are industry-specialist (SPECIAL) or those with a longer relationship with the client (TENURE).

Successor Auditor Selection.

Note. Table 6 presents results that show who becomes a successor auditor after an auditor-resignation event. The samples are separated into two groups: Firms that have experienced a crash at year t and firms that have not. For Panels A and B, the dependent variable is SBIG4. AUDRES is measured at t+ 1 and other control variables are measured at t in Panel A, whereas AUDRES is measured at t− 1 and other variables are measured at t− 2 in Panel B. Industry fixed effects and year fixed effects are included in the regression models. The statistical significance at the 1%, 5%, and 10% levels is denoted by ***, **, and *, respectively, and is based on z statistics calculated based on robust standard errors clustered at the firm level. See the appendix for the variable definitions.

Overall, the empirical evidence presented in this study suggests that auditor resignation is positively associated with stock price crashes. I show that auditor resignation precedes and follows crashes and that Big 4 auditors, compared with non-Big 4 auditors, are more likely to walk away from clients prior to the crashes. Once a crash hits the firm, it becomes a risky client for both Big 4 and non-Big 4 auditors, so auditor size becomes irrelevant. Finally, this study identifies which auditors become successor auditors after auditor changes around crashes. Regardless of when an auditor resignation occurs, either before or after a crash, Big 4 auditors are less likely to replace former auditors, possibly due to high audit risk.

Conclusion

Many factors can potentially affect auditors’ decisions to alter their relationships with clients. Among these factors, this study focuses on a firm’s crash risk, examining its relationship with auditor resignations and asking how auditor type affects auditor–client relationship decisions around crash events. Specifically, the results show that litigations and financial restatements are more likely to occur once a firm experiences a crash. After controlling for the risk factors that influence an auditor’s client-retention decisions, the results show that auditor resignations precede and follow crashes and that Big 4 auditors tend to walk away prior to crashes more often than non-Big 4 auditors do. This indicates that Big 4 auditors are more likely to rebalance their client portfolios because they have a larger client base and superior knowledge about the client firms. However, once firms experience a crash, auditor size becomes irrelevant in resignation decisions. That is because, once a crash occurs, the inclination to resign will not differ between Big 4 and non-Big 4 auditors, as both will view the firm as a risky client. Moreover, I find that Big 4 auditors are reluctant to become successor auditors if other auditors have resigned shortly before or after the client firm’s stock price has crashed.

Robustness tests are performed to ensure that the results are not sensitive to the various specifications used in the research design. First, following prior studies (e.g., Kim et al., 2014), I re-run the regressions with two alternative measures of stock price crashes, NCSKEW and DUVOL; NCSKEW captures the negative conditional skewness of firm-specific weekly returns, whereas DUVOL is a natural logarithm of the ratio of the standard deviation in the down weeks to the standard deviation in the up weeks. I confirm that the main results are robust to different crash variables. Second, a different measure of industry-specialist auditors is used for robustness. All the analyses performed in this study are based on the market share approach, where it considers the audit firm to be a specialist if it has the largest share within a particular industry. On the contrary, the portfolio share approach measures whether the auditor generates most of its audit fees from a particular industry. Because these two definitions are very different, I test the hypotheses with a specialist-auditor variable based on the portfolio share approach and confirm that the main findings remain consistent. The results of the robustness tests are not reported due to space considerations.

In summary, this study provides evidence that the stock market responds to auditor-resignation events and that the crash itself can also be an important determinant of auditor resignations because a crash increases the likelihood of lawsuits and financial restatements. Furthermore, the findings suggest that auditor type plays a significant role in auditors’ client-retention decisions. This study is subject to several limitations, including the fact that what it documents is associations among variables rather than causal relationships. To minimize the risk of overlooking other factors that could correlate with auditor–client relationship decisions, further research should examine alternative explanations for these results.

Footnotes

Appendix

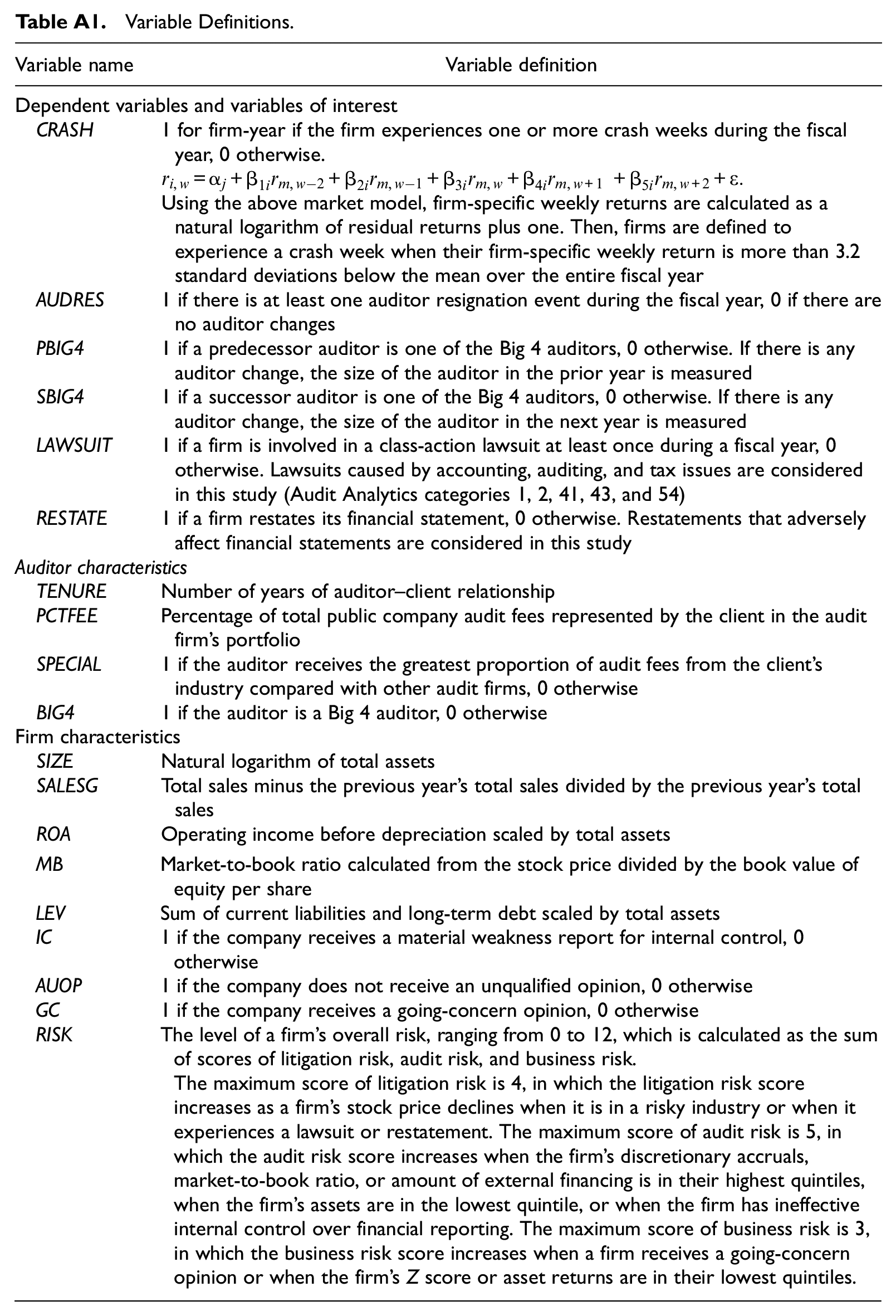

Variable Definitions.

| Variable name | Variable definition |

|---|---|

| Dependent variables and variables of interest | |

| CRASH | 1 for firm-year if the firm experiences one or more crash weeks during the fiscal year, 0 otherwise. Using the above market model, firm-specific weekly returns are calculated as a natural logarithm of residual returns plus one. Then, firms are defined to experience a crash week when their firm-specific weekly return is more than 3.2 standard deviations below the mean over the entire fiscal year |

| AUDRES | 1 if there is at least one auditor resignation event during the fiscal year, 0 if there are no auditor changes |

| PBIG4 | 1 if a predecessor auditor is one of the Big 4 auditors, 0 otherwise. If there is any auditor change, the size of the auditor in the prior year is measured |

| SBIG4 | 1 if a successor auditor is one of the Big 4 auditors, 0 otherwise. If there is any auditor change, the size of the auditor in the next year is measured |

| LAWSUIT | 1 if a firm is involved in a class-action lawsuit at least once during a fiscal year, 0 otherwise. Lawsuits caused by accounting, auditing, and tax issues are considered in this study (Audit Analytics categories 1, 2, 41, 43, and 54) |

| RESTATE | 1 if a firm restates its financial statement, 0 otherwise. Restatements that adversely affect financial statements are considered in this study |

| Auditor characteristics | |

| TENURE | Number of years of auditor–client relationship |

| PCTFEE | Percentage of total public company audit fees represented by the client in the audit firm’s portfolio |

| SPECIAL | 1 if the auditor receives the greatest proportion of audit fees from the client’s industry compared with other audit firms, 0 otherwise |

| BIG4 | 1 if the auditor is a Big 4 auditor, 0 otherwise |

| Firm characteristics | |

| SIZE | Natural logarithm of total assets |

| SALESG | Total sales minus the previous year’s total sales divided by the previous year’s total sales |

| ROA | Operating income before depreciation scaled by total assets |

| MB | Market-to-book ratio calculated from the stock price divided by the book value of equity per share |

| LEV | Sum of current liabilities and long-term debt scaled by total assets |

| IC | 1 if the company receives a material weakness report for internal control, 0 otherwise |

| AUOP | 1 if the company does not receive an unqualified opinion, 0 otherwise |

| GC | 1 if the company receives a going-concern opinion, 0 otherwise |

| RISK | The level of a firm’s overall risk, ranging from 0 to 12, which is calculated as the sum of scores of litigation risk, audit risk, and business risk. The maximum score of litigation risk is 4, in which the litigation risk score increases as a firm’s stock price declines when it is in a risky industry or when it experiences a lawsuit or restatement. The maximum score of audit risk is 5, in which the audit risk score increases when the firm’s discretionary accruals, market-to-book ratio, or amount of external financing is in their highest quintiles, when the firm’s assets are in the lowest quintile, or when the firm has ineffective internal control over financial reporting. The maximum score of business risk is 3, in which the business risk score increases when a firm receives a going-concern opinion or when the firm’s Z score or asset returns are in their lowest quintiles. |

Acknowledgements

This study is based on my doctoral thesis (K. Y. Lee, 2017). I gratefully acknowledge the support of my dissertation committee at Purdue University: Mark Bagnoli (co-chair), Susan Watts (co-chair), P.J. Hoffman, and Yeejin Jang. I also thank the audiences at the Purdue Accounting Research Workshop for their invaluable suggestions and helpful comments. This paper has benefited greatly from the comments of Dr. Bharat Sarath (editor) and two anonymous reviewers.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.