Abstract

We examine how labor-friendly institutional features (i.e., laborism) relate to corporate investment efficiency in labor in a sample of firms from 33 countries over 1996–2012. We consider three dimensions of laborism—the presence of a left-leaning government, rigidity of employee protection laws, and collectivist culture. Our evidence shows that firms operating in stronger laborism countries make less efficient labor investment decisions, which is consistent with higher labor adjustment costs associated with laborism.

Introduction

Building on Marx’s (1867) seminal work, Piketty (2014) documents how capital and labor have differentially contributed to value creation in modern economies. Contrasting these two key production factors has long been one of the most important issues in social science. Extending prior studies on the influence of country-level institutions to corporate behaviors (e.g., Baik et al., 2015; Chiang & Birtch, 2006; Gray et al., 2013), this article explores whether corporate hiring efficiency (or labor investment efficiency) is associated with country-level institutions reflecting labor friendliness. 1

Prior evidence on the relation between both firm- and country-level labor friendliness and firm performance is inconclusive. Some firm-level studies argue that labor-friendly corporate practices result in a stronger bond of loyalty to the company as well as lower absenteeism and voluntary turnover (Gellatly, 1995; Somers, 1995). Freeman and Medoff (1984), for example, find that labor friendliness is related to higher productivity and improved firm performance. In addition, Faleye and Trahan (2011) show that labor-friendly firms perform better than other firms in terms of stock returns and operating results. Edmans et al. (2014) also examine the relation between employee satisfaction and stock returns based on 14 countries and report a positive relation. They further show that the positive relation between employee satisfaction and stock returns exists primarily in countries with high labor market flexibility (i.e., easiness to hire or fire) such as the United States and the United Kingdom. In contrast, others document that pro-worker labor regulation leads to a decrease in manufacturing activities, lower labor force participation, and higher unemployment (Besley & Burgess, 2004; Botero et al., 2004; Holmes, 1998). Likewise, Besley and Burgess (2004) provide evidence based on Indian firms that pro-worker labor regulation is associated with lower output, aggregate employment, investment, and productivity in manufacturing industries.

However, little is known as to how country-level labor friendliness might affect corporate-level hiring decisions despite ample evidence that country-level institutions have significant impact on other corporate activities (e.g., Baik et al., 2015; Chiang & Birtch, 2006; Gray et al., 2013). A firm’s hiring decision can be an important channel through which institutional labor friendliness relates to firm value, given its impact on corporate operating performance and productivity (e.g., Jung et al., 2014). Using an empirical proxy for corporate hiring efficiency (Jung et al., 2014; Pinnuck & Lillis, 2007), we study the relation between country-level labor friendliness and firm-level employment efficiency. By doing so, we attempt to shed some light on the seemingly conflicting value implications of firm- and country-level labor friendliness.

We borrow our key construct, laborism, from Schumpeter (1942). Laborism reflects the degree to which both formal and informal institutions favor labor. We focus on this country-level measure of labor friendliness, as firms in different countries naturally have distinct hiring patterns depending on how much each country is protective of labor. For example, when the institution favors labor (i.e., employees) over capital providers, the firm might have to bear more labor costs by retaining and hiring more employees than needed. Accordingly, we expect that firms in countries with stronger laborism—a left-leaning government (LEFT), stronger employee protection laws (LABORLAW), or collectivist culture (COLLECTIVISM)—exhibit greater hiring inefficiency. We operationalize laborism in this manner, as left-leaning governments and rigid employment protection laws provide formal institutional support to labor (Botero et al., 2004; Julio & Yook, 2012), and more collectivist societies are likely to favor more labor-friendly institutions as they strive to avoid potential conflicts between management and labor (Hofstede, 2001).

We hypothesize that firms in economies with stronger laborism experience greater frictions in the labor market. In the presence of these frictions, firm employment can deviate from optimal levels due to higher costs of adjusting labor; thus, the labor market as a whole remains off-equilibrium. Under-hiring can occur when entrenched employees or unions extract excessive rents and exhaust resources that would otherwise be used for new employment (Jensen & Meckling, 1976; Montgomery, 1989). Research on labor unions tends to conclude that unionized firms reduce corporate investment, leading to a slower growth in employment and the eventual shrinkage of the union sector (Baldwin, 1983; Grout, 1984; Krol & Svorny, 2007). Over-hiring is also likely in the presence of pro-labor practices such as employment protection laws (i.e., the body of rules regarding the dismissal of employees), including procedural restrictions on layoffs and regulations regarding severance pay levels, which in turn imposes substantial employment costs. Banker et al. (2013) document that the strictness of employee protection laws imposes substantial firing costs on employers, and as a result, employers can be slow to divest workers even when corporate activity decreases and the net present value (NPV) of a worker turns negative.

We measure firm-level labor investment efficiency based on Jung et al. (2014) who build an expectation model to estimate the optimal level of hiring based on various fundamental factors which affect managers’ hiring decisions (e.g., sales growth, leverage, profitability, liquidity, and firm size). Following their approach, we consider each firm-year observation’s residual as a deviation from the optimal level, and thus inefficiency in labor investment. Over-hiring (under-hiring) is when the residual is positive (negative), and it suggests that a firm hires more (less) than the optimal level.

We test our hypothesis based on a sample consisting of 99,649 firm-year observations from 33 countries. Our first main finding is that the deviation from the optimal level of hiring (i.e., abnormal hiring) is significantly and positively related to all three laborism variables as well as their composite measure. This suggests that both formal (LEFT and LABORLAW) and informal (COLLECTIVISM) institutional factors are associated with hiring inefficiency. Second, in both over-hiring (i.e., positive residuals from the employment regression) and under-hiring (i.e., negative residuals from the employment regression) cases, laborism is associated with inefficient hiring practices. Each laborism measure has similar coefficient estimates in the two subsamples in terms of both magnitude and statistical significance. This confirms that the non-trivial labor adjustment costs exist in both directions in the presence of strong laborism (Botero et al., 2004).

This study makes several contributions to the literature. First, this is a pioneering study to document cross-country variations in labor investment efficiency. These findings advance our understanding on how hiring decisions, one of the most important, yet understudied corporate decisions, are made not only based on firm-level considerations but also are heavily influenced by legal, social, and political factors. As such, the study highlights how corporate decisions are interwoven with the institutional environments in which firms operate. Second, we ambitiously incorporate the measurement of laborism into our context. Building on Botero et al. (2004), a number of papers investigate employee protection laws across countries as a formal institution favoring labor. However, to our knowledge, no prior studies have extended the discussion to informal institutions such as culture. Considering both formal and informal institutions simultaneously provides a deeper understanding on the nature of laborism. Our evidence suggests that future research examining corporate hiring efficiency should incorporate both formal and informal institutional factors.

This study is organized as follows. In the next section, we review related studies and develop an empirically testable hypothesis. In the “Research Design” section, we explain research design. In the “Sample and Empirical Results” section, we describe the sample and discuss results. We conclude in the “Conclusion” section.

Literature Review and Hypothesis Development

Constraints of Operating Labor to Employment Efficiency

Rigidity in employment works as operating risk given that labor is a key element in production (Chen et al., 2011). For example, prior studies suggest that labor unions reduce a firm’s flexibility in investment and financing activities (D. Bronars & Deere, 1991; S. G. Bronars & Deere, 1993; Hirsch, 1991, 1992). Related research examines cross-country variation in employee protection laws and argues that the provisions of employment protection legislation are a source of considerable labor adjustment costs and hence a constraint in operating labor (Long & Siebert, 1983). The employment protection laws are the body of rules regarding the dismissal of employees, including procedural restrictions on layoffs and regulations regarding severance pay levels. As such, employee protection imposes operating risk and incurs adjustment costs, thereby causing inefficiency in employment decisions.

Laborism and Employment Efficiency

Schumpeter (1942) defines socialist society or socialism as “an institutional pattern in which the control over means of production and over production itself is vested with a central authority” (p. 167). To the extent that a central government (or state) has more control over employment in each firm, firms have less flexibility in operating manpower. Schumpeter (1942) also claims that laborism is the last stage of capitalist society in which labor interest is predominant (Swedberg, 1997).

We posit that the institutional environment in which a firm operates plays a dominant role in shaping laborism. Specifically, we consider three laborism proxies that potentially aggravate labor investment efficiency. First, left-leaning governments favor labor, while right-leaning governments are more market-friendly (e.g., Julio & Yook, 2012). World Bank refers to various sources, including Political Handbook, to identify party orientation with respect to economic policy (Keefer, 2008). World Bank classifies a government as right-leaning if the current political party is defined as conservative, Christian democratic, or right wing. Left-leaning parties are those that are defined as communist, socialist, social democratic, or left wing, and they would often protect employees from dismissals justified by economic reasons which would otherwise be an optimal choice for firms. By doing so, left-leaning governments put employees’ interests ahead of economic forces. Next, we consider the rigidity of employment protection laws in each country. Although left-leaning governments are known to provide directional support for laborism-inclined institutions, it is not clear how it causes inefficiency. Prior research in labor economics (e.g., Bentolila & Bertola, 1990; Botero et al., 2004; Lazear, 1990) documents that employment protection laws are a major source of employee-firing costs that have important macroeconomic implications such as unemployment and decline in long-term productivity.

The above two variables are formal country-level institutions. In contrast, informal institutions, including culture, have received much less attention in the labor economics literature. Li et al. (2013) and Shao et al. (2013) are two exceptions, albeit they are not directly related to our investigation. Both studies explore the relation between national culture and risk-taking in terms of capital investments or R&D expenditures, given that people in more collectivist societies tend to work harder for group interest and harmony. Building on these studies, we expect that the voice of employees will be heard more, and managers will strive harder to avoid potential conflicts with labor forces in more collectivist countries. Thus, we adopt the degree of collectivist culture as another proxy for laborism. The above arguments lead to the following hypothesis:

Research Design

Because we predict that higher laborism leads to less efficient hiring decision by managers, we should observe a positive relation between laborism and the level of deviation from the optimal hiring (i.e., hiring inefficiency). To test this prediction, we first estimate each firm’s optimal level of hiring by using the model developed in Jung et al. (2014). Then we examine the relation between laborism and hiring efficiency.

Estimating the Optimal Level of Hiring

If there is no market friction such as information asymmetry between managers and shareholders and agency problems, similar to capital expenditure and R&D expense, managers’ hiring decisions would be determined mainly based on investment opportunities (such as sales growth or Tobin’s Q), which managers privately observe (Pinnuck & Lillis, 2007). However, as the market is not complete, we also need to consider various factors that affect the actual level of investments in human resource. Some prior studies (e.g., Jung et al., 2014; Pinnuck & Lillis, 2007) attempt to develop a model to estimate managers’ expected demand for human resources or managers’ expected hiring decisions based on various fundamentals. Similar to Jung et al. (2014), we first run the following equation 1 (1) to estimate the expected (or normal) level of managers’ hiring decision:

Note that all variables are defined in the same manner as those in Pinnuck and Lillis (2007) and Jung et al. (2014). The literature shows that PSALEGROW, sales growth in the previous year, is the most important determinant of managers’ hiring decisions. As sales growth reflects the change in demand for a firm’s products and services and the change in demand affects changes in production factors, we expect a positive relation between sales growth and the change in hiring. We also include SALEGROW, the change in sales in the current year (i.e., year t), because managers’ hiring decisions are also influenced by their private information about future growth. RET, annualized stock returns, also represents expected future growth, which is not captured by sales growth measures. Thus, we expect a positive relation between ΔHIRE and RET. The effect of SIZE on ΔHIRE is twofold. On one hand, as larger firms are more mature in life cycle, and thus tend to have lower investment opportunities, SIZE would be negatively correlated with ΔHIRE. On the other hand, larger firms are generally less likely to face financial constraints for investments, and thus the relation would be positive. Therefore, we do not have a predicted sign on SIZE. Both PQUICK and PCQUICK are based on the quick ratio in the previous period and generally reflect a firm’s liquidity problem related to investments. As firms with higher quick ratios are less likely to have liquidity problems, we predict that both are positively related to ΔHIRE. However, as more hiring would lower the quick ratio in the same year due to cash payments of wages and salaries, there would be a mechanical negative relation between CQUICK and ΔHIRE. Thus, the relation between CQUICK and ΔHIRE depends on which direction dominates. As profitability in the prior year, PCROA, is more likely to lead to more hiring in the next year, we predict a positive relation. However, similar to a mechanical negative relation between CQUICK and ΔHIRE, the effect of CROA, profitability in the current year, on ΔHIRE is not clear. On one hand, managers of firms expecting better performance are more likely to hire, and thus there may be a positive relation. On the other hand, there could also be a mechanically negative relation because an increase (decrease) in hiring negatively (positively) affects net income in the same year due to an increase (decrease) in wage and salary expenses. Again, the sign of the relation depends on which factor of two dominates. As the literature (e.g., Myers, 1977) generally documents that leverage dampens overall investment activities, we expect a negative relation between PLEV and ΔHIRE. Loss indicator variables such as LOSS1, LOSS2, LOSS3, LOSS4, and LOSS5 are included to control for the effect of loss occurrence on managers’ firing decisions. Pinnuck and Lillis (2007) show that accounting losses play a significant role in reducing labor forces. Thus, we predict that coefficients on loss indicator variables are significantly negative. Industry dummies are also added to control for any other omitted firm characteristics related to each industry in which a firm belongs. We also include year fixed effects to control for the effect of overall macroeconomic changes on managers’ hiring decisions. For example, when macroeconomic conditions are good (bad), managers are more likely to increase (decrease) employee hiring.

Examining Whether Laborism Constrains Hiring Efficiency

After estimating equation 1, we compute the residual value of hiring for each firm-year observation, which is equal to actual hiring in the current year minus the fitted value of hiring estimated from equation 1 (i.e., the expected level of hiring). We consider the residual value as abnormal (or unexpected or unpredicted) investments in employment—abnormal hiring. A zero residual indicates that a firm’s actual hiring is equal to the predicted level based on various firm fundamentals. If the residual value is positive (i.e., its actual level is higher than the expected level), it indicates over-investment in employment (i.e., over-hiring), labeled as OVER_HIRE. If the residual value is negative (i.e., its actual level is lower than the expected level), it indicates under-investment in employment (i.e., under-hiring), labeled as UNDER_HIRE. Thus, the absolute value of the residual—OVER_HIRE or UNDER_HIRE—reflects how much an individual firm’s hiring deviates from the optimal (or expected) level of hiring based on fundamentals. We label the absolute value of residual as ABSHIRE. To examine how laborism affects hiring efficiency, we estimate the following equation 2:

where:

ABSHIRE = the absolute value of the difference between the actual level of hiring and the expected level of hiring, which is estimated from equation 1;

LNGDP = natural log value of gross domestic product (GDP) per capita;

UKLAW = common law dummy: 1 for common law country, 0 otherwise;

ANTISD = anti-self-dealing index. It is measured as the average of ex-ante and ex-post private control of self-dealing from Djankov et al. (2008);

CREDITOR = creditor right index from La Porta et al. (1998);

LABORISM = we employ three proxies for laborism: LEFT, LABORLAW, and COLLECTIVISM. LABORISM is equal to the standardized average values of COLLECTIVISM, LEFT, and LABORLAW. Specifically, we standardize the average of the three variables in a country by subtracting the mean value of the measure and dividing by the standard deviation of the measure in our sample;

LEFT = leftism government tradition measure from Botero et al. (2004);

LABORLAW = A composite index of labor laws, which is equal to the average value of three labor-related laws (EMP, UNION, and SOCSEC). EMP measures the difficulty and the costs of reducing wages and working hours, and covers regulations concerning overtime and use of temporary workers. UNION assesses the legal protection of labor unions and the regulation of collective disputes. SOCSEC measures the strength of social security laws. These three variables are all measured at the country level and time invariant. They are from Botero et al. (2004);

COLLECTIVISM = 1 – Individualism index (Hofstede, 2001) divided by 100.

Note that we borrow definitions for other variables either from the previous equation 1 or from Jung et al. (2014). Countries in different law systems deal with employment issues using different approaches. Common law countries tend to rely on market and contracts, whereas civil and socialist laws are more likely to use regulation and state ownership (Botero et al., 2004). The difference of dealing with employment issues may result in a difference in hiring efficiency. We also consider the effect of country wealth. A country with high GDP per capita is likely to be associated with high education attainment and a high level of labor productivity. Prior studies (e.g., Atanassov & Kim, 2009) suggest that investors and creditors tend to put more pressure on management to take corrective measures when their firm’s performance is not satisfactory. One implication is that investors’ and creditors’ rights have a potential impact on firms’ employment policies and, in turn, affect employment efficiency. To account for these possibilities, we include both country-level investor protection index (ANTISD) and creditor right index (CREDITOR) in equation 2.

If laborism leads to more inefficient (i.e., less efficient) hiring decision by managers, the coefficient on LABORISM would be significantly negative. Similar to Jung et al. (2014), we expect that hiring efficiency is higher (lower) for firms with better financial reporting quality, dividend paying firms, and larger, less leveraged, and more tangible firms (loss firms, fast-growing firms, more liquid firms, labor-intensive firms, and firms with higher volatilities of cash flow from operations, sales, and employees) in an international setting.

Sample and Empirical Results

Sample

We construct our sample by combining several databases. We obtain international financial data from the Compustat Global Industrial and Commercial file and North America financial data from Compustat for the period from 1996 to 2012. To gauge the difference of reporting currencies in the Compustat data, we translate all currencies into U.S. dollars for consistency. We winsorize all the continuous firm-level variables at their top and bottom 1% levels to mitigate the effect of outliers. We extract macroeconomic data (e.g., GDP per capita) from World Bank, investor protection and creditor right indices from La Porta et al. (2006), governmental ideology tradition and labor laws indices from Botero et al. (2004), and culture index from Hofstede (2001). To be included in our final sample, we require firms (a) in non-financial industries; (b) with positive values for sales, total assets, and the number of employees; (c) without missing values for all the variables of our tests; and (d) at least 10 observations in each country-year to ensure meaningful comparisons. After this screening procedure, our final sample consists of 99,649 observations from 33 countries.

The Relation Between Laborism and Hiring Efficiency

Descriptive statistics

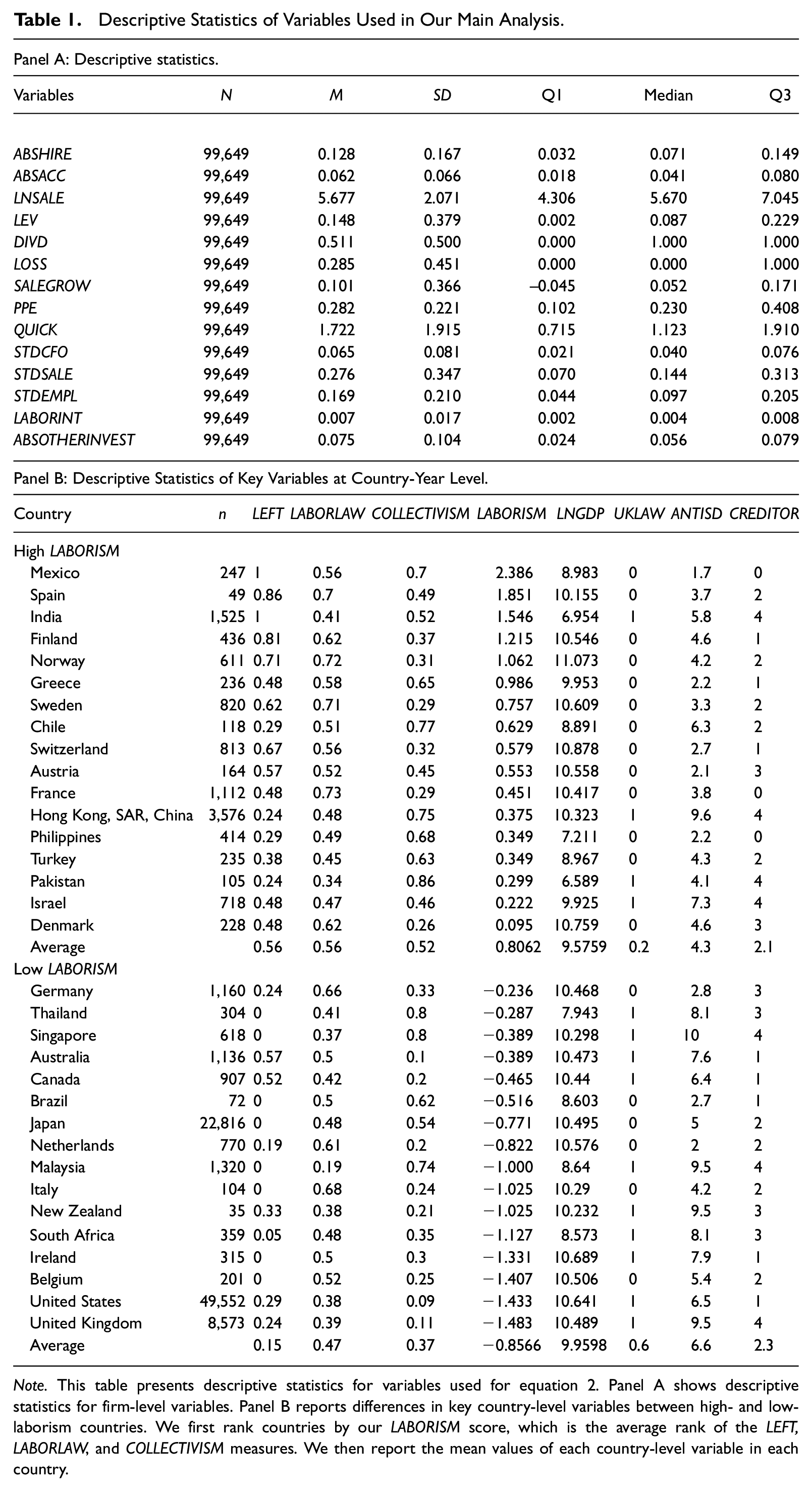

Table 1 presents descriptive statistics for variables used in equation 2. Panel A shows that the mean (median) of hiring inefficiency, ABSHIRE, is 0.1275 (0.0708), with a standard deviation of 0.1670. The large standard deviation of ABSHIRE relative to their respective mean value suggests that our sample has a large range of variation in hiring inefficiency. 3 The mean (median) leverage of our sample firms is 14.8% (8.7%) of total assets. On average, half of our sample firms pay dividends, while 28.5% of sample firms experience loss. The mean (median) of sales growth is 10% (5%). The average ratio of property, plant, and equipment to total assets is 28.21%, while the mean (median) of the quick ratio is 1.722 (1.123).

Descriptive Statistics of Variables Used in Our Main Analysis.

Note. This table presents descriptive statistics for variables used for equation 2. Panel A shows descriptive statistics for firm-level variables. Panel B reports differences in key country-level variables between high- and low-laborism countries. We first rank countries by our LABORISM score, which is the average rank of the LEFT, LABORLAW, and COLLECTIVISM measures. We then report the mean values of each country-level variable in each country.

Panel B reports differences in key country-level variables between high- and low-laborism countries. We first rank countries by our LABORISM score. Recall that the LABORISM score is calculated as the average of the LEFT, LABORLAW, and COLLECTIVISM measures. Countries with a high score of LABORISM are Mexico, Spain, India, Finland, and Norway. Countries with a low score of LABORISM are the United Kingdom, the United States, Belgium, Ireland, and South Africa. The average score of LABORISM for countries with high laborism is 0.8062, while the average score of LABORISM for countries with low laborism is –0.8566. The three components of LABORISM in high- and low-laborism countries are as follows: 0.56 versus 0.15 for LEFT; 0.56 versus 0.47 for LABORLAW; and 0.52 versus 0.37 for COLLECTIVISM. LNGDP, UKLAW, ANTISD, and CREDITOR are higher for low-laborism countries, indicating that lower laborism countries are wealthier, are common law based, and have a higher anti-self-dealing index and creditor right index. It suggests that these variables are related to laborism, and thus may affect the relation between laborism and hiring efficiency, highlighting the importance of including these variables as control variables in equation 2.

Multivariate analysis

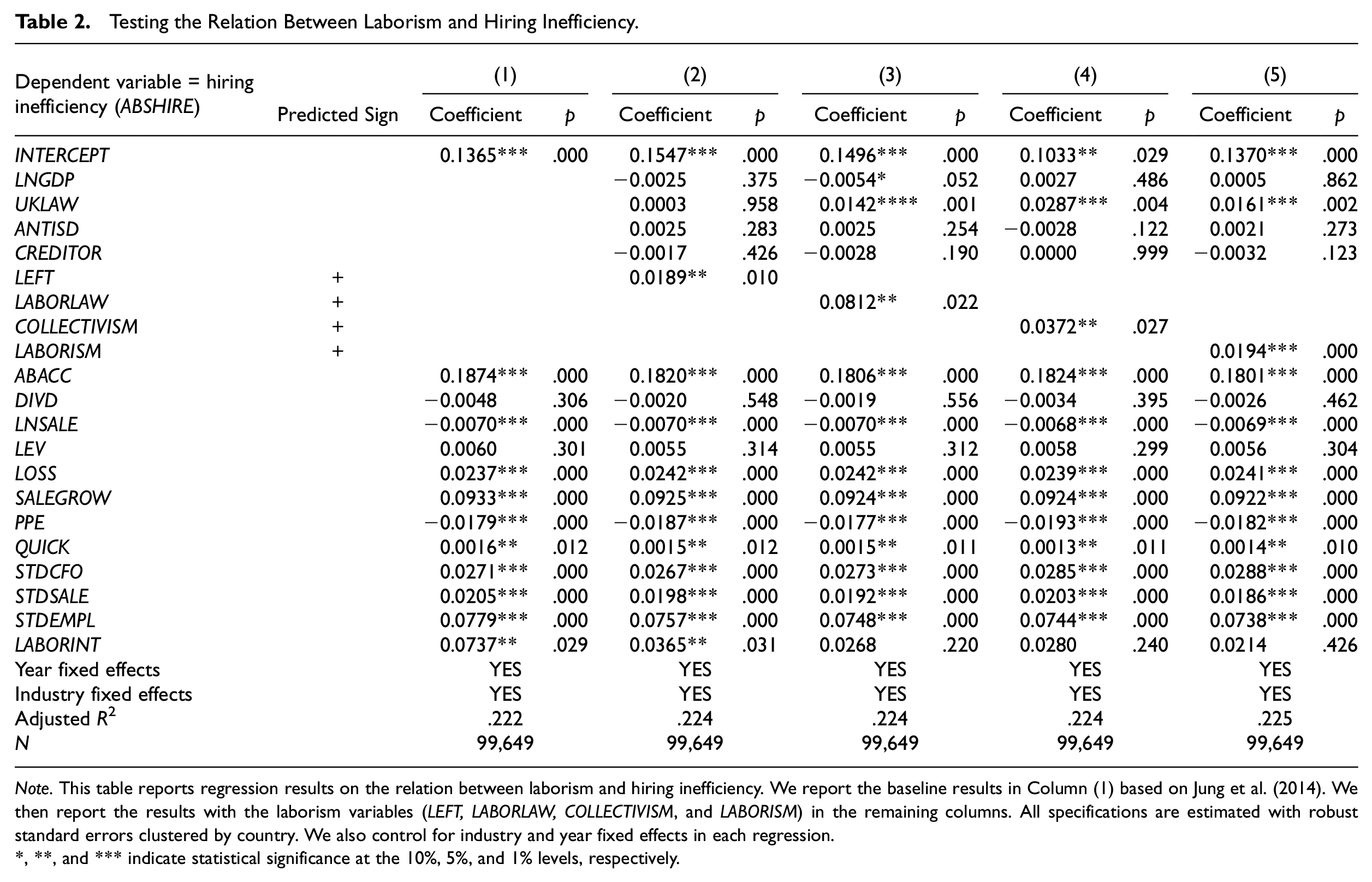

To test whether laborism positively or negatively affects managers’ hiring decisions based on multivariate analysis, we estimate equation 2. If country-level laborism enhances (hinders) managers’ hiring decisions, we would observe a positive (negative) coefficient on laborism measures. The results are reported in Table 2. To confirm the results in Jung et al. (2014) with international data, we first estimate equation 2 without country-level variables such as LNGDP, UKLAW, ANTISD, CREDITOR, and laborism measures. We present the results in Column (1). Our results based on international setting are generally consistent with Jung et al. (2014). Specifically, consistent with Jung et al. (2014), the coefficient on ABACC is significantly positive (p = .0001), suggesting that better financial reporting practices improve firm-level hiring efficiency even in countries other than the United States. ABSHIRE is also significantly positively (negatively) associated with LOSS, SALEGROW, QUICK, STDCFO, STDSALE, and STDEMPL (LNSALE and PPE), suggesting that hiring efficiency is lower (higher) for loss firms, fast-growing firms, more liquid firms, and firms with higher volatilities of cash flow from operation, sales, and employment (larger firms and more capital intensive firms).

Testing the Relation Between Laborism and Hiring Inefficiency.

Note. This table reports regression results on the relation between laborism and hiring inefficiency. We report the baseline results in Column (1) based on Jung et al. (2014). We then report the results with the laborism variables (LEFT, LABORLAW, COLLECTIVISM, and LABORISM) in the remaining columns. All specifications are estimated with robust standard errors clustered by country. We also control for industry and year fixed effects in each regression.

*, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Columns (2) through (5) present the results of estimating equation 2 with laborism measures. Before employing the composite measure of laborism, LABORISM, we first use each proxy of laborism. Column (2) reports the results when LEFT is a proxy for laborism. The coefficient on LEFT is significantly positive (p = .010), suggesting that laborism, as reflected in LEFT, increases hiring inefficiency. In Column (3), we use LABORLAW as a measure of laborism. The coefficient on LABORLAW is also significantly positive (p = .022). In Column (4), in which we use COLLECTIVISM as another proxy for laborism, the coefficient on COLLECTIVISM is, again, significantly positive (p = .027). Finally, in Column (5), we use a composite measure of laborism, LABORISM. Its coefficient is still significantly positive (p < .01), which is consistent with the results based on the individual measures reported above. 4 Thus, the results support our hypothesis that managers of firms operating in countries with higher laborism tend to have less efficient hiring decisions. In other words, laborism (or pro-labor institutional systems) hinders managers’ efficient hiring decisions.

We further examine how laborism constrains hiring efficiency by separately considering over-hiring and under-hiring cases. Laborism may result in more abnormal hiring by over-hiring, under-hiring, or both. To examine whether the positive relation between laborism and hiring inefficiency is driven by over-hiring or under-hiring cases, we first split the entire sample into two groups—firms that are more likely to experience over-investment in labor (i.e., over-hiring) and firms that are more likely to experience under-investment in labor (i.e., under-hiring). For firms where the residual value from estimating equation 1 is greater (less) than zero, we consider them as firms that over-hire (under-hire). The number of firm-year observations with over-hiring (under-hiring) cases is 40,445 (59,204). Then, we run equation 2 to the two groups, separately. The (untabulated) results confirm that laborism hinders managers’ efficient hiring decisions by inducing both over-hiring and under-hiring problems.

Conclusion

Strong laborism implies that firms are under pressure from various institutional forces (e.g., government, laws, and society) to retain existing employees and to continue to hire labor. This pressure can induce managers’ hiring decisions to deviate from the optimal level of firm employment. Eventually, this inefficiency in corporate hiring can lead to decreased profitability. The goal of our article is to examine hiring inefficiency in the presence of strong laborism, which constrains the flexibility in managers’ hiring decisions. Consistent with our hypothesis, we document that laborism related to both formal and informal institutional forces, such as left-leaning governments, rigid employee protection laws, and collectivism culture, is associated with inefficient corporate hiring decisions.

Caveats are in order. First, as per labor market consequences of labor-friendly institutions, we should have considered both quantity (i.e., employment level) and price (i.e., wages) components of labor costs wherever possible. An analysis also incorporating the wage component would provide a more complete picture on the relation between laborism and hiring because laborism may result in rigidity in wages, hiring, or both. In addition, managers’ hiring decisions are significantly affected by the wage component. Unfortunately, wage data for our sample firms are, for the most part, unavailable. We leave this analysis to future research.

Second, one unstated premise of our study is that the optimal hiring model that Jung et al. (2014) set up for U.S. firms works equally well in cross-country analyses. We admit, however, that a single model of estimating the optimal level of hiring may not hold across countries. As a result, the possible presence of country-level omitted variables would make it difficult to interpret over- and under-hiring as a form of inefficiency in labor investment. More specifically, in our empirical analyses, we unwillingly and, to some extent, inevitably ignore the fact that each institution has been built on its own grounds. Addressing our research question requires enormous institutional knowledge on economic outcomes, labor codes, and government enforcement in every country because countries with stronger laborism should have their own reasons for which formal and informal laborism has developed to its current form. For example, the rigidity of employee protection laws depends not only on the letter of the labor code but also on its effective implementation. Institutions in charge of implementation such as labor courts might determine their efforts based on the letter of the law and the performance of the labor market. As such, the degree of laborism in each country can be in equilibrium, in which employment efficiency is rationally sacrificed for potential benefits unidentified in this study. Given the above, we caution readers that our findings are only suggestive of the causal relationship between laborism and employment efficiency. We call for more innovative endeavors to push this line of literature forward.

Footnotes

Acknowledgements

We thank Shirley Daniel, Dongyoung Lee, David Weber, and seminar participants at McGill University, University of Hawaii at Manoa, 2015 European Accounting Association Annual Congress, and 2015 Japan Accounting Association Conference for helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Lee appreciates financial support from the Institute of Management Research at Seoul National University.