Abstract

We examine whether monitoring by the Internal Revenue Service (IRS) affects managers’ decisions to engage in fraudulent financial reporting. We argue that IRS monitoring provides a disciplining effect reducing managements’ incentives to engage in rent diversion activities such as costly financial statement misreporting. Using information on IRS audit rates and instances of fraud disclosed in Securities and Exchange Commission (SEC) Accounting and Auditing Enforcement Releases (AAERs), we find evidence consistent with IRS monitoring providing positive spillover effects in reducing the likelihood of accounting fraud. Our results are robust to using a matched sample of fraud and nonfraud firms. Altogether, we find evidence that tax authorities provide positive externalities in reducing agency costs through monitoring and enforcement.

Introduction

Tax authorities may be viewed as minority shareholders in the corporate organization (Desai et al., 2007). By looking after their own interests, they provide corporate oversight of potential rent diversion by managers. In particular, Internal Revenue Service (IRS) scrutiny may deter managers from manipulating financial data and limit the scope for inducing a favorable bias into reported earnings (Hanlon et al., 2014). However, given that there is only a loose connection between financial reporting and tax reporting, the role of IRS monitoring may not be a significant factor in deterring financial reporting fraud. In fact, some prior research has found that managers are willing to pay actual cash taxes on “fake” earnings to simultaneously misreport financial accounting income (Erickson et al., 2004). Furthermore, existing literature suggests the quality and ability of the external monitor is an important factor in the identification and addressing of financial fraud cases (e.g., Bayley & Taylor, 2007; Farber, 2005; Lennox & Pittman, 2010; Novack, 1998). As such, the IRS may lack the necessary sophistication and resources to adequately identify and address accounting fraud. As a result, it remains an empirical question as to whether IRS monitoring has a spillover effect on corporate managers’ decisions to engage in accounting fraud.

There are several potential reasons to expect that IRS monitoring can influence managers’ decisions on whether to commit financial reporting fraud. For example, managers may fear that in the event of a tax audit, the IRS will uncover evidence of financial reporting fraud and then report this information to other governmental agencies, such as the Securities and Exchange Commission (SEC), as is allowed under the Internal Revenue Code § 6103(i)(3). However, the threat of the IRS directly uncovering and sharing information regarding financial fraud is not a necessary condition. For instance, during tax audits, the tax authority often requests substantial documentation from the firm to justify the firm’s tax positions. If managers perceive the likelihood of a tax audit to be high, they may devote more care and attention to their financial record-keeping in anticipation of the tax audit’s information needs. With higher quality record-keeping and internal accounting systems, managers are likely to find it more difficult and costly to fraudulently misreport financial earnings. As such, monitoring by the IRS may have a spillover effect on instances of accounting fraud. However, given that the IRS does not directly monitor financial reporting and that the SEC and IRS are distinct and separate monitors, it is unclear whether IRS enforcement would have any effect on financial reporting decisions. Furthermore, even if IRS monitoring did have a spillover effect on financial reporting fraud, it is uncertain whether the spillover effect would be strong enough to be detected in empirical tests.

To investigate whether IRS monitoring influences the initiation of accounting fraud, we first construct proxies for IRS monitoring activity by combining data from publicly available IRS reports and from private reports by the Transactional Records Access Clearinghouse (TRAC) located at Syracuse University for years 1992 to 2010. Using these data, we calculate the likelihood a firm is audited by the IRS to capture a manager’s perceived IRS monitoring activity (El Ghoul et al., 2011; Guedhami & Pittman, 2008; Hanlon et al., 2014; Hoopes et al., 2012). We then combine these data with a comprehensive sample of accounting violations disclosed by the SEC on Accounting and Auditing Enforcement Releases (AAERs), and developed by Dechow et al. (2011).

Using this sample, we estimate the likelihood that a firm engages in accounting fraud in response to the perceived probability of an IRS audit. We specifically measure the decision to engage in accounting fraud using the first year that a firm misreports, as we expect that on the margin, the additional monitoring put forth by the IRS may serve as a deterrent to managers that are considering misreporting. 1 We find that as the IRS audit probability increases, there is a significant reduction in the likelihood that a firm engages in financial accounting fraud. Overall, our findings suggest that moving from the 25th to the 75th percentile of the probability of an IRS audit is associated with about a 14% decrease in the probability that a firm initiates misreporting that results in an AAER.

A concern when analyzing firms engaging in fraud activities is that unobserved firm characteristics are responsible for any observed effects, limiting the ability to identify an effect such as tax agency monitoring. To mitigate this concern and more clearly identify the effect IRS monitoring has on fraud activity, we use a matched sample to analyze how IRS monitoring influences the decision to engage in fraudulent activity for fraud firms as compared with a sample of nonfraud firms that are similar along many dimensions, including the propensity to engage in financial statement fraud activities, yet are not issued an AAER. The results from this analysis further confirm our main finding that IRS monitoring appears to act as a disciplining mechanism by discouraging managers from entering into fraudulent misreporting activities.

This article extends the existing literature on the effects of tax authority monitoring by documenting the effect of IRS monitoring on fraudulent misreporting decisions. Our findings compliment the results in Hoopes et al. (2012), which shows that tax authority monitoring plays an external governing role for firms by deterring tax aggressive behavior. In this vein of literature, our article is most closely related to Hanlon et al. (2014), which finds IRS monitoring affects financial reporting quality as measured by accrual quality (Dechow & Dichev, 2002; McNichols, 2002) and discretionary accruals (Dechow et al., 1995; Jones, 1991). We build on their study by analyzing instances of fraud as a measure of financial misreporting to analyze the most costly, egregious earning management cases (Palmrose et al., 2004), which also have been argued to be a more direct proxy for financial reporting manipulations as compared with discretionary accruals (Ball, 2009; DeFond, 2010; Lennox et al., 2013). Thus, we expand the existing literature to show that IRS monitoring reduces incentives to engage in violations of Generally Accepted Accounting Principles (GAAP) reporting in addition to earnings management that may abide by GAAP reporting standards.

Finally, our results contribute to the broader literature on whether external monitoring affects instances of accounting fraud. As summarized in Dechow et al. (2010), several studies show that external monitoring decreases the probability that a firm commits accounting fraud, 2 whereas other studies show no link between external monitoring and accounting fraud. 3 Our results support the notion that external monitoring provides adequate oversight to reduce agency costs and thereby reduce the expropriation of shareholder wealth through accounting fraud. Our article also adds to the literature on whether the independence of a monitor affects the effectiveness of manager oversight (Geiger et al., 2008; Jo et al., 2007). Our results show that monitoring stakeholders, independent of the firm, can influence the likelihood that a manager chooses to commit accounting fraud.

The article proceeds as follows: Section “IRS Monitoring Activity and Accounting Fraud” presents the hypothesis development and literature review, section “Sample Selection and Research Design” presents the sample selection and research design used to test the hypothesis. Section “Results” presents the results of the empirical tests of the hypothesis. Section “Propensity Score Matching Analysis” presents the matching procedure and results using our matched sample, and section “Conclusion” presents the research conclusion.

IRS Monitoring Activity and Accounting Fraud

Existing literature on tax enforcement purports that tax authorities are minority owners in an organization and have similar incentives as outside stakeholders (e.g., Desai et al., 2007; Robinson, 1911). As such, tax enforcement, operating in its own interest, can serve as a monitoring mechanism for an organization suffering from agency conflict. Previous work finds evidence consistent with this theory showing tax authority oversight increases firm value and lowers the firm’s cost of capital due to a reduction in the private benefits extracted from controlling owners (Desai et al., 2007; Dyck & Zingales, 2004; El Ghoul et al., 2011; Guedhami & Pittman, 2008). Thus, prior evidence suggests tax authorities affect the governance in corporations and reduce agency costs through tax enforcement.

More recently, research has begun to explore the spillover effects of tax authority monitoring. For example, Hoopes et al. (2012) document the effect of tax authority monitoring on firms’ tax compliance decisions. The authors show that firms decrease their level of tax avoidance activity as the probability of an IRS audit increases, likely due to the potential costs from an IRS audit (e.g., tax audit adjustments, fines, and penalties) outweighing any benefits from taking tax aggressive positions. In the context of financial reporting, Hanlon et al. (2014) argue, and find, that increased oversight by a tax authority reduces management’s ability to manipulate financial earnings, as evidenced by improved financial reporting quality as the likelihood of a tax audit increases. The authors posit this is for at least three reasons.

First, because tax avoidance strategies require obfuscation of information (Desai et al., 2007), tax monitoring can reduce management’s ability to obfuscate rent-diverting activities, which can also limit management’s ability to manipulate earnings. 4 Second, with greater book-tax differences increasing the risk of a tax audit (Mills, 1998), firms have an increased incentive to align book and taxable income as the probability of a tax audit increases. To do so, firms are less likely to use nonconforming tax strategies, which would further increase the tax audit risk (Badertscher et al., 2009; Phillips et al., 2003). Therefore, as tax enforcement increases, firms are less likely to avoid tax through taxable income manipulation (Hoopes et al., 2012), which also reduces the manipulation of book income when tax and book income are closely aligned. Third, increased tax enforcement can lead to a greater risk of detection of financial misreporting (Erickson et al., 2004). This increased detection could be a result of the IRS disclosing information of financial fraud directly to the SEC, the board, or the audit committee. In any case, the increased probability of tax enforcement would almost certainly increase the detection risk of financial misreporting.

In addition to the mechanisms pointed out in Hanlon et al. (2014), it is possible that the threat of a tax audit influences management’s attention given to internal accounting systems. More specifically, during a tax audit, the IRS often requires the firm to provide substantial documentation to justify the firm’s tax positions. Therefore, as the likelihood of a tax audit increases, it becomes more cost-effective for the manager to preemptively devote more care and attention to their internal accounting record-keeping. The improved internal record-keeping results in improved information for both tax and financial audits, as well as for external auditors, and therefore limits management’s ability to manage earnings. Overall, we expect that tax enforcement and monitoring disciplines managers through any one, or many, of the previously mentioned avenues, thereby reducing instances of financial accounting fraud.

We extend Hanlon et al. (2014) and focus our study on the effect of tax monitoring on financial accounting fraud for several reasons. First, instances of financial accounting fraud, such as those disclosed in an SEC AAER, are argued to be the most deceptive forms of financial misreporting and are the costliest once detected (e.g., Lennox et al., 2013; Miller, 2006; Palmrose et al., 2004). Therefore, understanding possible deterrents of financial accounting fraud, such as tax enforcement, is increasingly important (Ball, 2009), especially with the consequences significantly affecting minority shareholders (e.g., Karpoff et al., 2008; Kedia & Philippon, 2009).

Second, our focus on financial accounting fraud allows for a more precise identification of the effect of tax enforcement on financial reporting. Contrary to existing literature, financial accounting fraud represents actual events, which have been argued to be a better proxy for poor accounting quality because they do not suffer from measurement error in the same way discretionary accruals do (e.g., Ball, 2009; DeFond, 2010; Lennox et al., 2013). Finally, managers that engage in fraud activities may have an altogether different mindset than managers that engage in nonfraud earnings management or no earnings management at all. For example, Schrand and Zechman (2012) find that fraudulent managers are overconfident, believing they can avoid detection by outsmarting the auditors. Thus, analyzing the effect of tax enforcement on instances of accounting fraud provides a more robust analysis for understanding the spillover effects of tax monitoring.

While existing literature would suggest tax enforcement may reduce instances of accounting fraud, it is unclear ex ante whether tax enforcement alters managers’ decisions to engage in fraudulent financial misreporting. Because accrual-based earnings management measures include both fraud and nonfraud earnings management, it may be that tax enforcement has no impact on financial accounting fraud and only affects nonfraud earnings management (e.g., Hanlon et al., 2014). Thus, we may observe no association between tax enforcement and instances of fraud.

It also may be the case that firms engaging in fraud activities take steps to avoid tax authority scrutiny. For instance, Erickson et al. (2004) show firms are willing to pay additional tax on fraudulently overstated financial earnings to avoid scrutiny by the IRS, SEC, or other outside investors. Specifically, they show that a sample of firms accused of committing accounting fraud overpaid their taxes by 11 cents per dollar of fraudulent earnings to avoid detection suggesting “managers may willingly have their firms pay taxes on earnings over-statements to avoid raising the suspicion of . . . the Internal Revenue Service.” As such, a higher likelihood of tax authority monitoring may not be associated with a decreased level of accounting fraud as the benefit from inflated earnings outweighs the additional tax cost.

In addition, prior research shows that the quality of the external monitor matters greatly in deterring managers from committing accounting fraud (e.g., Beasley, 1996; Farber, 2005; Lennox & Pittman, 2010). This literature would suggest the quality of the monitor, and not necessarily just its existence, is important in deterring instances of fraud, which may call into question the ability of a tax authority, such as the IRS (Novack, 1998), to appropriately identify financial accounting fraud. For example, the IRS is understaffed to such a degree that according to the former IRS commissioner Charles Rossotti, “The IRS simply does not have enough resources to cover even the most serious [tax] compliance cases.” Empirical research supports this view, finding that lower levels of IRS resources limit the scope of tax audits, which leads to smaller tax deficiencies and less tax revenue (Nessa et al., 2020). Given the lack of resources to engage in tax collection, it is unlikely the IRS has the resources necessary to identify instances of accounting fraud.

Furthermore, it is unclear whether the IRS would actually provide information to the SEC in the event the IRS were to uncover evidence of accounting fraud. In fact, even though the IRS is permitted to disclose information related to financial fraud to agencies such as the SEC under § 6103(i)(3) of the Internal Revenue Code, according to the AAERs from 1982 to 2005 collected by Dechow et al. (2010), there has yet to be a single firm accused of accounting fraud due to the SEC receiving a tip from the IRS. 5 Therefore, it is unclear whether increased tax enforcement poses a corresponding increased threat of SEC enforcement of financial fraud.

Finally, because the IRS does not directly influence financial reporting or oversee cases of financial misreporting, any spillover effect of tax enforcement on instances of financial accounting fraud may be too small to detect. Following this line of reasoning, we may observe that authority monitoring has little to no impact on instances of financial accounting fraud. Therefore, it remains an empirical question as to whether the probability of tax enforcement is associated with firms’ decisions to engage in fraudulent financial reporting activities. As such, we state our hypothesis in the null form as follows:

Sample Selection and Research Design

Tax Monitoring and Enforcement

To test our hypothesis, we first construct a measure of tax monitoring and enforcement using data on tax examinations. The data on tax enforcement are gathered from the TRAC located at Syracuse University. Data in the TRAC database are obtained from a variety of sources, including the IRS’ internal management database, which is used to internally track statistics of tax audits and other metrics to provide necessary reports for various government offices, as well as from publicly available Data Book reports, which are issued by the IRS in March of the year following the tax year for which the report pertains. 6 The credibility of the TRAC data is evident in the use by the IRS Oversight Board and the Finance and Permanent Subcommittee on Investigations in the U.S. Senate, as well as respected media outlets (Guedhami & Pittman, 2008).

From these data, we gather information on the number of corporate tax return audits performed and the number of corporate tax returns received by the IRS. This information is available based upon the IRS’ firm size groupings and the year the audit is performed. The TRAC data report audits performed within a given band of firms by amount of assets. For example, the IRS audit statistics are reported for firms in the lowest size band with assets of less than US$250,000. The next size band accounts for firms with assets between US$250,000 and US$1 million. From there, the next size bands for reporting audit statistics are for firms with assets from US$1 to US$5 million, US$5 to US$10 million, US$10 to US$50 million, US$50 to 100 million, and US$100 to US$250 million. The last size band encompasses audit statistics for firms with assets in excess of US$250 million. The IRS labels firms below US$10 million in assets as “small” corporations, whereas firms above US$10 million in assets are “large” corporations. In our study, we are most interested in large firms with assets above US$10 million as we anticipate the costs and benefits of financial misreporting to be heightened in such firms. Furthermore, restricting our sample to large corporations enables us to more clearly identify the variation in IRS audit statistics among these firms (Hoopes et al., 2012).

Using this information, we calculate a proxy for tax enforcement, Audit Prob, defined as the number of corporate tax returns audited by the IRS for each grouping of firms based on the total asset size in a given fiscal year divided by the total number of corporate tax returns received by the IRS from firms in the same size group in the previous fiscal year. 7 As in Hoopes et al. (2012) and Hanlon et al. (2014), we use a denominator of the previous year’s corporate tax returns received. To the extent there is a delay in a firm’s decision to either abstain or engage in fraudulent financial reporting, in response to the probability of being audited by the IRS, it would bias against us finding a significant association between tax enforcement and financial accounting fraud. Our measure of IRS audit probability spans fiscal years 1992 to 2010. 8

It is important to point out that for the probability of a tax audit to influence managers’ decisions to engage in fraudulent financial accounting activities, it must be that managers are aware of the IRS audit statistics. Blank and Levin (2010) find that information made publicly available by the IRS is intended to influence taxpayer behavior. 9 Thus, managers perceiving IRS tax audit risk statistics from publicly available information may alter the fraud decision. However, even if managers may not access the IRS tax audit statistics, it is possible that either through their own experience at their firm or through conversations with managers at peer firms, managers may be aware of the likelihood of undergoing an IRS audit.

Financial Accounting Fraud

To identify instances of financial accounting fraud, we gather information on the SEC’s enforcement of financial statement violations reported in AAERs made available through the University of California, Berkeley Center for Financial Reporting and Management (CFRM). Each release represents a separate violation involving accountants indicating the beginning and ending dates of financial misconduct (Karpoff et al., 2017). Karpoff et al. (2017) raise concerns regarding the various data sources used to identify fraud for academic research purposes. However, they state that AAERs are appropriate when analyzing the full narrative of the misconduct such as the beginning and ending dates of the fraud behavior, yet fall short when analyzing specific dates that information about the misconduct becomes available to investors. Because we are interested in how the probability of an IRS audit affects the decision to engage in fraudulent financial reporting, AAERs appear to be the most appropriate source to identify fraud firms and the inception of the fraud activity.

In some instances, the SEC enforcement results in multiple AAERs being filed against a firm, or individual at the firm. 10 We follow existing literature and exclude AAERs that pertain to nonaccounting frauds (Erickson et al., 2006; Lennox & Pittman, 2010; Miller, 2006). Consistent with our data on IRS enforcement, we restrict our sample to include only AAERs where the fraud activity began after 1992. Table 1 shows the number of AAERs in our sample by the year the fraud began. We have 144 firm-year observations that entered into fraudulent financial reporting with the bulk of the sample occurring during the late 1990s and early 2000s. This is consistent with Cohen et al. (2008), which shows a significant decrease in earnings management, and likely fraudulent misreporting, after the passage of the Sarbanes–Oxley Act (SOX).

Fraud Cases Initiated by Year.

Note. This table provides information on our sample of fraud cases by the year the financial statement misreporting began. Using Accounting and Auditing Enforcement Releases (AAERs) made available through the University of California, Berkeley Center for Financial Reporting and Management (CFRM), we identify the year the fraud activity began based on the disclosed violation period from the AAER.

It is worth noting that using AAERs to identify accounting fraud has potential disadvantages. Due to a limited budget, the SEC typically brings enforcement on only the most egregious violators of GAAP (Dechow et al., 2011). Thus, there may be instances where firms commit accounting fraud through less obvious departures from GAAP and are less likely to receive an AAER from the SEC. To the extent these firms remain undetected in our sample, this would bias against us rejecting our null hypothesis. To mitigate this concern, we perform a robustness analysis using a matching methodology to match firms receiving an AAER with firms that do not to compare firms that are known to engage in accounting fraud with firms that may have similar incentives to engage in accounting fraud yet do not or remain undetected. Discussion of our full sample selection is in the following section, while the discussion of our matching methodology and analysis is contained in section “Propensity Score Matching Analysis”.

Sample Selection

We combine our measure of the probability of a tax audit and instances of accounting fraud with firm-specific data from Compustat for fiscal years 1992 to 2010. 11 We restrict our sample to include only firms incorporated and headquartered in one of the 50 U.S. states or the District of Columbia. Furthermore, we limit our sample to include only C corporations as IRS data on tax enforcement contained in the Data Book are organized by entity type with data on flow-through entities, such as partnerships and S corporations, being generally unavailable. In addition, if the probability of a tax audit alters the decision to engage in fraud, then we would expect this to be more prevalent in public corporations that suffer from more extensive agency costs (Jensen, 1989). In addition, we restrict our sample to include firms with positive pretax income and exclude all firm-year observations that have missing values for size and other firm-level control variables.

To combine our tax enforcement data with firm-specific information, we match firm-years to the IRS tax audit data based on total assets and fiscal year. The IRS Data Book contains statistics on tax audits and tax returns received for groups of firms ranging from less than US$250,000 in total assets to corporations that have greater than US$250 million in total assets. The size groups formed by the IRS range in size anywhere from US$750,000 between the smallest and largest firms in the group to groups that span US$15 million in total assets. 12 As a result, for each firm-year observation, we have a corresponding tax audit probability based upon the firms’ fiscal year and total assets. As we are most interested in larger firms, we further restrict our sample to include “large” corporations with greater than US$10 million in total assets defined by the IRS Data Book. 13 After these restrictions and data set combinations, we are left with a total of 144 unique firm-year observations that are associated with the initiation of an accounting fraud in year t. Table 1 shows the number of fraud firms by the year the fraud began according to the AAER. Our full sample consists of 44,596 firm-year observations, with Table 2 providing summary statistics for our full sample. The additional control variables used in our analysis along with descriptions of all variable sources and calculations are described in more detail in Appendix.

Summary Statistics—Full Sample.

Note. This table provides descriptive statistics for variables used in our empirical analysis. Initial Fraud is defined as taking the value of 1 for firms that are identified and issued an Accounting and Auditing Enforcement Releases (AAERs) by the SEC, which is made available through the University of California, Berkeley Center for Financial Reporting and Management (CFRM). We define the probability of an IRS audit, Audit Prob, as the ratio of the number of returns in the current year that the IRS audits for each IRS firm size group scaled by the total number of returns received in the previous year and in the same IRS size grouping. The sources and construction of each variable are disclosed in Appendix. IRS = Internal Revenue Service; SEC = Securities and Exchange Commission.

Research Design

Our hypothesis, in the null form, suggests monitoring and enforcement by the IRS will have no effect on the probability a manager chooses to commit fraud. To test this hypothesis, we use a logistic regression predicting the likelihood that a firm engages in accounting fraud while simultaneously considering other factors that may influence the fraud decision. We estimate the following empirical model:

The dependent variable, Initiate Fraud, takes the value of 1 if firm i begins the accounting fraud disclosed in the AAER in the current period t and 0 otherwise. Audit Prob is the tax audit statistic calculated as the total tax returns audited in the current fiscal year, t, for a given size grouping divided by the total tax returns received by the IRS in the previous year, t−1, for the same firm size grouping disclosed in the IRS Data Book and TRAC data on IRS audit rates. Following Hanlon et al. (2014), we account for firms that are in the Coordinated Industry Case (CIC) program, and thus under continuous IRS examination, by setting the audit probability to 1 for the largest 1,000 firms in our sample per year based on total assets in year t.

To account for other firm-level characteristics that may influence managers’ incentives to engage in fraud, we include in our empirical model, X, which is a vector of control variables capturing the operating and financial characteristics that have been shown to influence incentives to engage in corporate fraud. Included as controls are measures of firm leverage, Leverage, shown to be higher for fraud firms (Burns & Kedia, 2006), and market-to-book ratio, MB, which is higher for fraud firms (Dechow et al., 2011). We account for the effect that firm performance has on the decision to engage in fraud using a firm’s return on assets, ROA, which has been shown to affect financial reporting quality and incentives to engage in fraudulent misreporting (Dechow et al., 2011; Erickson et al., 2006; Hanlon et al., 2014). 14 We also include controls for both firm age and size of the firm, which have been shown to be significantly associated with fraud activity (Lennox & Pittman, 2010). In addition, controlling for firm size further accounts for the fact that our variable of interest, Audit Prob, is in part a function of firm size as the information in IRS audit rates is broken out by total assets and year (Hanlon et al., 2014; Hoopes et al., 2012).

We also account for operational considerations of the firm that may dictate the incentives to engage in fraud including performance or external financing needs. We include the firm’s level of cash, Cash, and sales growth, SalesGrowth, as well as whether the firm experienced a net loss, Loss, shown to be associated with instances of fraud (Beneish, 1997; Lennox & Pittman, 2010). To consider whether firms manipulate financial accounting figures to aid in raising capital, we include a proxy for firms suffering financial distress using an indicator variable, NegativeBE, taking the value of 1 if the firm has negative book equity (Maksimovic & Titman, 1991).

In addition to firm-specific characteristics, Lennox and Pittman (2010) show the quality of the auditor affects the likelihood that a firm engages in fraud activities, while Myers et al. (2005) find the tenure of the audit firm significantly affects the likelihood of material restatements. To account for these factors, we include an indicator variable, BigN, which takes the value of 1 if the auditor is a Big N auditor and 0 otherwise, as well as a variable for auditor tenure, AuditTenure, measured as the number of years the firm has had the current auditor. Furthermore, to account for unobserved time trends affecting fraud decisions, we include year fixed effects in our analysis (Davidson, 2011). Specifically, each of our variables is measured as follows:

Audit Prob represents the probability of being audited by the IRS based on the firm’s size (as measured by total assets) and year of observation. The probability is set to 1 for the largest 1,000 firms in our sample based on total assets in the current period following Hanlon et al. (2014).

Initiate Fraud is a binary variable equal to 1 in year that the fraud was initiated according to the SEC’s AAER and 0 otherwise.

Leverage is calculated as total long-term debt (Compustat #9) divided by total assets (Compustat #6).

ROA is calculated as pretax income (Compustat #170) divided by lagged total assets (Compustat #6).

MB is equal to the market value of equity over the book value of equity, where the market value of equity is defined as the share price at the end of the fiscal year (Compustat #199) multiplied by the number of shares outstanding (Compustat #25), and the book value of equity is the book value of equity from Compustat (Compustat #60)

BigN is a binary variable equal to 1 if the firm has a Big N auditor and 0 otherwise.

Age is equal to the logarithm of age, where age is the current year the firm first appears on Compustat

Size is equal to the log of the market value of equity, where the market value of equity is defined as the share price at the end of the fiscal year (Compustat #199) multiplied by the number of shares outstanding (Compustat #25).

AuditTenure is equal to the number of consecutive years that the firm has had their current auditor.

Cash is equal to the amount of cash and cash equivalents (Compustat #1) the firm has divided by total assets (Compustat #6).

Negative Book Equity is a binary variable equal to 1 if total liabilities (Compustat #181) are greater than total assets (Compustat #6) and 0 otherwise.

SalesGrowth is calculated as the ratio of current year’s sales (Compustat #12) divided by the previous year’s sales (Compustat #12), minus 1.

Loss is a binary variable equal to 1 if net income (Compustat #172) is less than 0, and equal to 0 otherwise.

Results

Table 2 presents the summary statistics for our full sample. The mean (median) audit probability in our sample is 44% (32%), and audit probability exhibits significant variation, ranging from a low of 20.8% for the 25th percentile of observations to 54.6% for the 75th percentile of observations. As expected, in our full sample analysis, we observe that a very small percentage of firms initiate an accounting fraud in a given year, with only 0.3% of the sample initiating a fraud in year t. 15 Consistent with prior research, we find that the majority of observations in our sample (75%) utilize a BigN auditor. We also find that the majority of the firms in our sample are profitable, with a mean (median) ROA of 15.8% (8.9%).

To test our hypothesis, while accounting for the multiple factors that may influence the likelihood of engaging in fraudulent misreporting, we estimate our empirical model, Model (1), on our full sample of firm-year observations. Table 3 presents the results from this estimation. Consistent with our predictions, we observe a statistically significant association between the likelihood that a firm engages in fraudulent financial reporting and the probability of an IRS audit. In terms of magnitude, our results suggest that moving from the 25th to the 75th percentile of the probability of an IRS audit is associated with about a 14% decrease in the probability that a firm initiates misreporting that results in an AAER. This is consistent with a spillover effect on fraudulent misreporting that can occur when managers perceive they are more likely to receive an IRS audit, thus supporting the potential oversight role that the IRS can play in disciplining managers.

Analysis of IRS Monitoring and Accounting Fraud—Full Sample.

Note. This table reports the estimation results from our estimation of fraud on IRS audit probabilities and other firm characteristics using our full sample of firms. The dependent variable in each estimation is our variable Initiate Fraud, which takes the value of 1 for firm-years the fraudulent activity began according to the AAER and 0 otherwise. Audit Prob is defined as the ratio of the number of returns in the current year that the IRS audits for each IRS firm size group scaled by the total number of returns received in the previous year and in the same IRS size grouping. The sources and construction of each variable are disclosed in Appendix. T-statistics are presented in parentheses with *** and ** indicating statistical significance at the 1% and 5% levels, respectively. IRS = Internal Revenue Service; DV = dependent variable; AAER = Accounting and Auditing Enforcement Release.

The results from this estimation also support existing literature showing firm size and leverage are positively associated with fraudulent misreporting, whereas firm age and level of cash are negatively associated with fraud activity. We also find a significantly positive association between ROA and the likelihood that a firm engages in fraudulent misreporting. This may suggest that higher levels of firm performance induce greater SEC scrutiny and/or heightened levels of fraud detection by the SEC. Interestingly, we also find that firms with higher growth in sales are more likely to engage in fraud activity. This suggests managers respond to market pressures to show continued growth in revenues year over year by engaging in fraudulent misreporting (Graham et al., 2005). Furthermore, our results are robust to controlling for year fixed effects and robust standard errors clustered by firm (Petersen, 2009).

Propensity Score Matching Analysis

As with any fraud or litigation study, documenting an effect on fraud behavior can be problematic due to issues regarding identification. For instance, any observed effect may be due to potential unobserved firm characteristics or the probability of detection. To more clearly identify the effect that tax authority monitoring has on fraud behavior and to account for the endogeneity concern of unmeasurable or unobserved factors affecting our findings, we perform our analysis using a propensity score matching technique. By comparing fraud firms with firms that have a similar propensity to commit financial accounting fraud yet do not, we are able to better isolate the effects of IRS monitoring on the likelihood that firms engage in financial reporting fraud.

To create our matched sample, we first estimate Model (1) predicting the likelihood that a firm engages in fraudulent financial reporting dependent upon a number of firm characteristics, which includes firm performance as a main determinant of fraud activity (Rogers & Van Buskirk, 2009), while excluding the IRS audit probability. Following Shipman et al. (2017), the prediction model we use to create our matched sample is identical to the multivariate model we then use in the second-stage regression predicting the effect of IRS monitoring on fraud activity, with the exception of the treatment variable itself, Audit Prob. From this estimation, we then generate a propensity score for each fraud and nonfraud firm. Using the propensity scores, we create two separate matched samples by matching fraud firms to either one or two nonfraud firms using the nearest neighbor or the nearest two neighbors, in terms of the propensity to engage in financial reporting fraud, with replacement. Our matched samples consist of 144 fraud firm-years and 144 nonfraud firms-years for our one-to-one match and 286 nonfraud firm-years for our match using the nearest two neighbors.

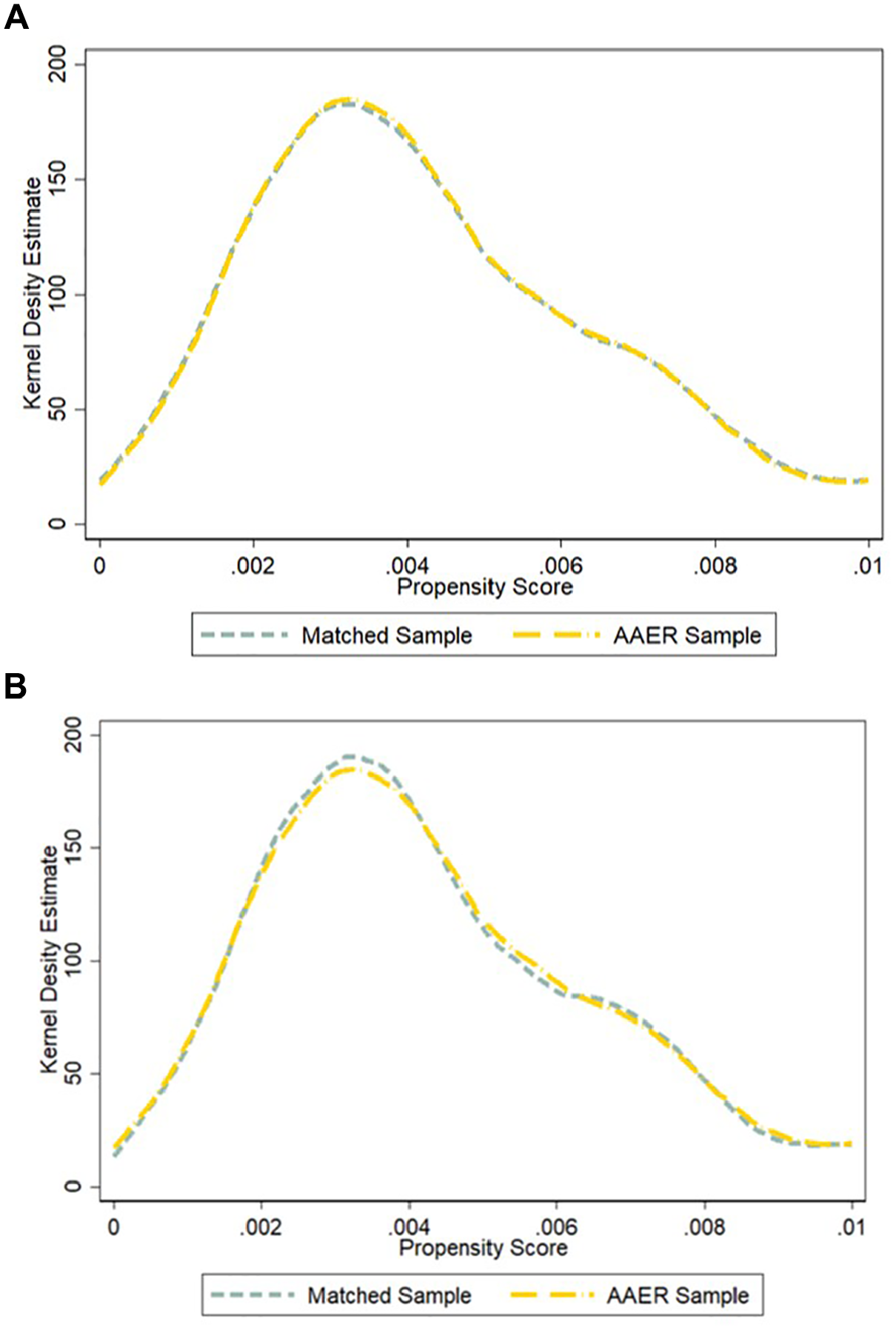

To ensure the validity of our matched sample and assess the necessary covariate balance between our treated and control groups (Shipman et al., 2017), we first compare our fraud and nonfraud samples in terms of firm characteristics predicting fraud activity. The results of this comparison are presented in Table 4. We find that our sample of matched nonfraud firms appear to be generally indistinguishable from fraud firms except for firms’ market-to-book ratio and sales growth. 16 These similarities remain consistent across both matched samples, for example, nearest neighbor and nearest two neighbors. As a further test of our covariate balance, we estimate the probability density function of the propensity scores for both the treated and control sample using a kernel density estimation (Shipman et al., 2017). From this estimation, we then graphically compare our two samples and present the illustrations in Panels A and B of Figure 1. Consistent with our comparison of means, we find significant similarities in the density functions of each samples’ propensity to engage in fraud activities. 17 Given the similarities between our fraud and nonfraud firms, we believe our subsequent analysis comparing the likelihood of fraud due to IRS monitoring activity is adequate in accounting for unobserved firm characteristics.

Comparison of Matched Sample.

Note. This table presents descriptive statistics and comparisons of means for fraud firms and a sample of matched nonfraud firms. We define a firm as a fraud firm by the year the fraudulent activity began according the AAER. We match each fraud firm to a firm that has not engaged in fraudulent activity by the propensity to be a fraud firm based on the listed firm characteristics. Panel A presents a comparison of our matched control firms and fraud firms when using the single closest match in terms of the propensity score to engage in financial misreporting. Panel B presents a comparison of means for our fraud firms and the nearest two nonfraud firms based on the propensity to engage in fraudulent misreporting. Each variable is measured at time t with the beginning of the fraud occurring at time t+1 to capture variables that predict the initiation of the fraud. The sources and construction of these variables are disclosed in Appendix. T-statistics are presented in parentheses with *** and ** indicating statistical significance at the 1% and 5% levels, respectively. AAER = Accounting and Auditing Enforcement Release.

Kernel density estimation for treated and control groups. Panel A: sample estimation using one-to-one match. Panel B: sample estimation using two-to-one match.

Using these matched samples, we reestimate Model (1) and present the results in Table 5. Importantly, we include all covariates used in our propensity score model to account for possible remaining differences between our treated and matched sample and to ensure our results are “doubly robust” (Shipman et al., 2017). Columns 1 and 2 display results for our one-to-one and nearest two neighbors matched samples, respectively. Consistent with our main findings using the full sample, we observe a statistically significant reduction in the likelihood that a firm engages in fraudulent financial statement reporting as the level of IRS audit probability increases. This again supports our hypothesis that IRS monitoring provides a spillover effect on the decision to engage in fraud activities, even after accounting for possible unobserved characteristics confounding our previous results. 18

Analysis of IRS Monitoring and Accounting Fraud—Matched Sample.

Note. This table reports the estimation results from our estimation of fraud on IRS audit probabilities and other firm characteristics using our sample of matched firms by nearest neighbor in Column 1 or the nearest two neighbors in Column 2. The dependent variable in each estimation is our variable Initiate Fraud, which takes the value of 1 for firm-years the fraudulent activity began according to the AAER and 0 otherwise. Audit Prob is defined as the ratio of the number of returns in the current year that the IRS audits for each IRS firm size group scaled by the total number of returns received in the previous year and in the same IRS size grouping. The sources and construction of each variable are disclosed in Appendix. T-statistics are presented in parentheses with ***, **, and * indicating statistical significance at the 1%, 5%, and 10% levels, respectively. IRS = Internal Revenue Service; DV = dependent variable; AAER = Accounting and Auditing Enforcement Release.

Similar to our results utilizing the full sample of observations, we find firm sales growth is significantly positively associated with the likelihood of fraud. This again suggests managers seek to meet or beat sales growth expectations by engaging in fraudulent misreporting. Unlike our previous results, we find limited variation in firm characteristics affecting the likelihood of engaging in fraud. This is not surprising, given our matching procedure along these firm characteristic dimensions, and further suggests our matching procedure is effective in capturing control firms that are similar in firm characteristics and the propensity to engage in fraud activities. Altogether, our results using a matched sample provide compelling evidence on the effect of IRS oversight on managers’ engagement in fraudulent financial reporting.

To ensure our findings when using propensity score matching are not sensitive to the matching procedure used, we follow the recommendations of Shipman et al. (2017) and DeFond et al. (2018) and perform a series of robustness tests using varied matching methodologies. First, we match firms that receive an AAER to the nearest control firm, in terms of the propensity to engage in fraud, without replacement. In the next three models, we similarly match firms that engage in fraud to the nearest three, five, and 10 neighboring control firms with replacement. Using these samples of treated and matched control firms, we then reestimate Model (1). The results from these specifications are presented in Table 6. We again find that a higher IRS audit probability is associated with a significantly lower likelihood that a firm initiates financial reporting fraud. Thus, regardless of the matching procedure, we find consistent evidence supporting the notion that IRS monitoring has a spillover effect on firms’ decisions to engage in fraudulent misreporting.

Analysis of IRS Monitoring and Accounting Fraud—Various Matched Samples.

Note. This table reports the estimation results from our estimation of fraud on IRS audit probabilities and other firm characteristics using a series of matching methodologies. Column 1 uses a one-to-one matching method for the nearest neighbor without replacement in terms of the propensity to engage in fraud based on the propensity score. Columns 2 through 4 use a matched sample created by matching the nearest three, five, and 10 neighbors, with replacement, respectively. The dependent variable in each estimation is our variable Initiate Fraud, which takes the value of 1 for firm-years the fraudulent activity began according to the AAER and 0 otherwise. Audit Prob is defined as the ratio of the number of returns in the current year that the IRS audits for each IRS firm size group scaled by the total number of returns received in the previous year and in the same IRS size grouping. The sources and construction of each variable are disclosed in Appendix. T-statistics are presented in parentheses with ***, **, and * indicating statistical significance at the 1%, 5%, and 10% levels, respectively. IRS = Internal Revenue Service; DV = dependent variable; AAER = Accounting and Auditing Enforcement Release.

Conclusion

In this study, we examine whether monitoring by tax authorities affects managers’ decision to engage in fraudulent financial misreporting. Desai et al. (2007) argue that tax authorities are minority shareholders of corporate organizations and benefit from reducing the agency costs inherent in such firms by monitoring manager behavior. Existing literature has expanded this notion by documenting empirically a positive spillover effect of monitoring by tax authorities on the financial information of the firm (El Ghoul et al., 2011; Guedhami & Pittman, 2008; Hanlon et al., 2014). We expand this literature by assessing whether the positive spillover effect of tax authority monitoring extends to fraudulent misreporting behavior. In doing so, we can determine whether IRS monitoring influences even the most egregious financial reporting violations.

Using a sample of the SEC’s enforcement of financial statement violations reported in AAERs, we document a significant decrease in the likelihood that a firm engages in fraudulent financial misreporting as the level of IRS monitoring increases. Our findings are robust to a propensity score matching methodology and the comparison of the likelihood of fraud on IRS monitoring for firms that are similar in terms of firm characteristics. We conjecture that our results could be a result of various mechanisms, including manager’s fear that the IRS will report to the SEC fraud it has identified in a tax audit, or a result of firms investing more in record-keeping and internal controls as the threat of a tax audit increases, which in turn constrains the ability of managers to fraudulently report earnings.

Overall, we find strong evidence that monitoring by the IRS acts as a governance mechanism to reduce managers’ incentives to engage in fraudulent misreporting. Thus, our study extends the existing literature documenting the effects of tax authority monitoring while also providing new evidence on the factors that can influence managers’ decisions to fraudulently misreport.

Footnotes

Appendix

Acknowledgements

We are grateful to David Guenther, Jing Huang, Pei Hui, Chris Kim, Linda Krull, Steve Matsunaga, Keun Jae Park, Hai Tran, Jason Turkiela, Shan Wang, and workshop participants at the University of Oregon for detailed comments and encouragement. All errors and omissions are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Financial support for this project was provided by the Hankamer School of Business at Baylor University and the Kelley School of Business at Indiana University.