Abstract

This article is the first to study the relation between financial restatements and restatement firms’ demand for trade credit as a source of financing. Using a sample of U.S.-listed firms for the 2000–2016 period, we find that restatement firms tend to use more trade credit in the year following the restatement disclosure year than do non-restatement firms. Moreover, we find evidence that restatement firms use trade credit to substitute for the reduced reliance on short- and long-term loans. Our further analysis reveals that restatement firms can obtain more trade credit when the firms promptly change the CEOs as a signal for firms’ attempt to repair damaged organizational legitimacy. Taken together, our findings suggest that restatement firms experiencing difficulties in obtaining conventional borrowings tend to resort to trade credit as an alternative source of financing.

Introduction

Trade credit is a regular component of market transactions and is considered to be one of the main sources of short-term financing. About 80% of U.S. firms offer their products on trade credit (Tirole, 2006), and, from 1992 to 2007, trade credit represents about 10% of the total assets of U.S.-listed firms (Aktas et al., 2012). Motivated by the substantial role of trade credit in providing short-term financing, we investigate whether restatement firms seek trade credit as a source of short-term financing when facing difficulties in borrowing from financial institutions.

A financial restatement is perhaps the most significant indication of an accounting failure since it is a breakdown in the system that involves management, audit committees, auditors, and the U.S. Securities and Exchange Commission (SEC). The inability to provide reliable financial statements may shake investor confidence and raise concerns about the overall health of a company. Moreover, financial restatements may cast doubt on management integrity and expose the company to regulatory scrutiny or litigation. As such, restatement announcements often lead to a significant drop in the market value and a confidence crisis among outside investors. In 2003, a Government Accounting Office (GAO) report documents a marked increase in the total number of restatements from 1997 to 2002 and a detrimental impact of these restatements on financial markets, as evident by an estimated total loss of US$100 billion in market capitalization in the intermediate period after the restatement announcement (GAO, 2003).

The extant literature focuses on the consequences of restatements on restating firms’ equity and debt financing. To date, there is no evidence on the impact of financial restatements on the firms’ trade credit financing. Our article attempts to fill this gap. Trade credit is not a pure form of financing and it is very different from the traditional debts from financial institutions. Trade credit is offered by non-financial entities and is limited to the purchase of goods. While trade credit is generally considered to be an expensive alternative to bank debt, it is the largest and most important source of short-term financing and plays a critical role in providing liquidity to the economy. Why firms are willing to use trade credit even though it is a costly financing source? There are currently two competing hypotheses that attempt to answer this long-standing question in the trade credit literature. The first hypothesis, known as the substitution hypothesis, argues trade credit and bank loans are imperfect substitutes, that is, firms rely more on trade credit when they face difficulties in obtaining bank financing (Petersen & Rajan, 1997). The second hypothesis, known as the signaling hypothesis, argues the reason that buyers use trade credit, despite its costly nature, is to signal their quality. Since suppliers possess an informational advantage over financial institutions to judge the financial health of their buyers, if a seller is willing to extend trade credit to a buyer, and thus to bear the default risk of the buyer, it must be that the former has good information about the latter. On observing this, the bank may update positively its beliefs about the buyer, and therefore agrees to lend. In other words, trade credit is viewed as a sign of firms’ good quality, making it easier for them to access bank loans. As a result, trade credit and bank lending would not necessarily be substitutes, but might be complements (Biais & Gollier, 1997).

We ask two related main questions about statement firms’ use of trade credit in this study. First, do restatement firms rely more on trade credit after restatement announcement years? Second, if restatement firms use more trade credit, do they use trade credit as an alternative source of financing to substitute for traditional debt or as a signal of their quality to have access to traditional debt? Regarding the first question, we examine two alternative views. The first view predicts that restatement firms rely more on trade credit after restatements because these firms tend to have higher degrees of uncertainty, information asymmetry, and hence more limited access to other sources of financing. Because of their advantage over financial institutions in evaluating and controlling the credit risk of their buyers, suppliers may be willing to finance these firms even if their credit quality is suspect. The alternative view, however, suggests that due to restatement firms’ lower credit quality, their demand for trade credit may not be matched by suppliers’ willingness to lend. Put differently, this view contends that restatement firms maintain a lower level of trade credit after the restatement announcement year. Regarding the second question, if restatement firms use trade credit as an alternative source of financing, we should expect them to use less debt and more trade credit as suggested by the substitution hypothesis. However, if trade credit is used as a signal of quality, we should expect restatement firms to increase the use of trade credit while having more debt as suggested by the signaling hypothesis.

Using a sample of 5,904 unique firms (of which 1,817 firms restated their financial statements) for the period from 2000 to 2016, we first examine the difference in the use of trade credit between restatement and non-restatement firms. We find strong evidence that restatement firms are likely to use more trade credit in the year following the restatement disclosure year than do non-restatement firms, and relative to the pre-restatement announcement period, restatement firms’ level of trade credit is higher in the post-restatement period. Moreover, we find evidence that restatement firms that experience a decline in the use of short-term loans and long-term loans after the restatement disclosures tend to use more trade credit. The results are consistent with the substitution hypothesis that because of limited access to other sources of financing, restatement firms use trade credit as an alternative source of financing and suppliers are willing to lend to these firms even if their credit quality has deteriorated.

Furthermore, we follow Hennes et al. (2008) and classify whether a restatement is due to irregularity or an accounting error. We find firms with irregular restatements tend to use more trade credit than do other firms with accounting error restatements. Using market reactions and dollar restatement amount as measures of restatement severity, we show the likelihood of using trade credit is higher for firms with more severe restatements. Our additional analysis also suggests that restatement firms’ ability to obtain more trade credit extension is higher when the firms change their CEO. The result supports the argument that management turnover in the post-restatement period signals restatement firms’ attempt to resolve information problems and investors’ trust (Desai et al., 2006), which in turn, influences suppliers’ willingness to grant trade credit.

Our findings on the association between financial restatements and trade credit may be biased by potential endogeneity problems. To alleviate this endogeneity concern, we use firm fixed effect specification and instrumental variable approach in our regressions. The results are consistent with our main finding that restatement firms rely more on trade credit after the announcement year. Our results are also robust when we use an alternative measure of trade credit and limit the sample to the post–Sarbanes-Oxley Act (SOX) period.

This study offers several major contributions. First, our article is the first to provide evidence on how restatements affect firms’ use of trade credit, one of the primary short-term financing sources of corporations, and thus contributes to the restatement literature that has mainly focused on debt and equity financing for restatement firms. Second, our study contributes to the trade credit literature by providing direct empirical evidence to support the substitution hypothesis and complements earlier studies of trade credit policies in small businesses based on the National Survey of Small Business Finance (NSSBF) (e.g., Petersen & Rajan, 1997). However, the NSSBF data are mainly restricted to a pooled cross-section and are only available over a limited number of periods. By using a sample of restatement firms in a much longer period, we examine the two competing hypotheses (substitution and signaling hypotheses) in the trade credit literature in a different setting than previous studies that rely on the NSSBF data.

Third, our article contributes to a growing debate on the impact of accounting quality on trade credit policy. By looking at the association between trade credit and financial restatements, which is a very significant event that indicates an accounting failure, we can examine the relation between trade credit and accounting quality from a different perspective since the evidence is mixed in the literature when using accrued based measure of accounting quality. For example, Chen et al. (2017) present evidence that accounting quality is negatively associated with trade credit, while García-Teruel et al. (2014) report that firms with higher accrual quality tend to obtain more trade credit from suppliers. A financial restatement is different from the accrual-based measure of earnings quality because of its reputational effect and restatement firms’ signaling motivation subsequent to a financial restatement (Wiedman & Hendricks, 2013). Therefore, while the financial restatement is an indication of a firm’s poor accounting quality, suppliers may predict future improvements in the restatement firm’s earnings quality and extend more trade credit to the firm. Moreover, compared with the accrual-based proxy of financial reporting quality, a restatement is a more objective measure of financial reporting quality (Archambeault et al., 2008). Also, a financial restatement may lead suppliers to raise questions about the validity of their trade credit granting decision which was previously based on the originally released financial information that contains material misstatements. Meanwhile, the accrual-based measure of financial reporting may not be subject to such questions. In addition, different from prior studies on the association between accounting quality and trade credit, our study shows that even though a financial restatement is a serious event that damages restatement firms’ reputation and reduces investors’ confidence in the firms’ financial information, restatement firms’ prompt action to repair the damaged organizational legitimacy (through changing the CEO associated with the restatement) enables the firms to increase their trade credit financing.

In addition, our study provides insights into whether the degree of severity of financial restatements influences firms’ demand for trade credit. Our study should be of interest to restatement firms, firms with low-quality financial reporting, or firms facing difficulties borrowing from financial institutions. Restatement firms or any firms with an interest in looking for an alternative source of financing would benefit from realizing that trade credit can be a source of short-term financing and a substitute for the difficult-to-borrow loans from conventional financial institutions.

The remainder of the article is organized as follows. The next section provides the literature review and develops our hypotheses. Then we describe the sample design and sample selection process. Next, we will present the results of our main analyses and discuss additional tests. The conclusion section summarizes our results and discusses the limitations of our study.

Literature Review and Hypothesis Development

Our article combines two strands of literature: (a) costly consequences of financial restatements and (b) the relationship between restatement firms, trade credit, and other external financing choices. We review related articles along these lines and then present our hypotheses.

The Costly Consequences of Financial Restatements

A financial restatement and its consequences are becoming an important issue among the investors, corporate managers, regulators, and accounting firms, particularly in the aftermath of the SOX of 2002 (GAO, 2003, 2006). Prior research shows that restatements can be very costly to a firm. For example, Palmrose et al. (2004) find a significantly negative market response (−9.2%) for a 2-day window beginning the day of the restatement announcement. In addition, the negative market response to fraud-related restatements (i.e., deliberate misreporting) is −20% but is only −6% for non-fraud restatements. Besides the negative stock price reaction, financial restatements lead to long-term consequences. Wilson (2008) provides further evidence by showing a decline in the earnings response coefficient for restatement firms, indicating a negative impact of restatements on investors’ perceptions about firms’ earnings quality. Barniv and Cao (2009) find that investors in restatement firms rely more on analyst characteristics associated with the forecast accuracy than do investors in non-restatement firms. Desai et al. (2006) investigate the impact on adverse managerial reputations and penalties imposed by both the labor market and regulators. Srinivasan (2005) also shows that directors of companies that have restatements face significant labor market penalties. Lambert et al. (2007) construct a theoretical model and show that the cost of capital increases when the quality of accounting information decreases. Hribar and Jenkins (2004) document a positive relation between accounting restatement and the cost of capital. Chen et al. (2013) find that after issuing restatements, firms experience difficulties in raising external capital and become financially constrained. Overall, a large body of empirical evidence indicates that financial restatements are bad news events and costly to firms. Financial restatements reflect the low-quality accounting information and high information asymmetry, thereby reducing shareholders’ value and increasing external financing costs.

Financial Restatement, Trade Credit, and Other External Financing Choices

Many accounting studies provide support to the important role of accounting information quality in a firm’s value and external financing choices. For example, firms with high-quality accounting information have better access to capital markets, because high-quality financial information reduces information asymmetry (e.g., Bhattacharya et al., 2013). In contrast, firms with lower-quality financial reporting tend to prefer bank loans (i.e., private debt), because banks possess superior information and have processing abilities, both of which result in a decrease in adverse selection costs for borrowers (Bharath et al., 2008). Chen et al. (2013) document that firms rely more on debt financing (especially, private debt financing) and less on equity financing in the period following restatements. Graham et al. (2008) document that because of the increased risk and information asymmetry arising from financial problems, banks use tighter loan contracts with restatement firms. Specifically, bank loans in the post-restatement period have remarkably higher spreads, shorter maturities, a higher likelihood of being secured, and more covenant restrictions than do those in the pre-restatement period.

Briefly, studies that examine the relation between financial restatements and external financing choices usually focus on debt and equity financing. The use of trade credit as a means of financing for restatement firms remains unexplored. Much of the trade credit literature ponders the question that why firms extend trade credit to their customers when more specialized financial institutions such as banks could provide the financing. Literature suggests several motives that explain the existence and the supply of trade credit. For example, suppliers may have an advantage over traditional financial institutions in evaluating the creditworthiness of their customers since suppliers can visit the premises of the buyers more often and thus acquire more and cheaper information about buyers than financial institutions can (Brennan et al., 1988). Suppliers may also have advantages over financial institutions in monitoring and in enforcing the repayment of credit because they can threaten to cut future orders to ensure repayment of credit. When terminating the relationship is costly, customers are less likely to default (Cuñat, 2007; Ng et al., 1999). In addition, suppliers may have advantages over financial institutions in liquidating the goods in the case of buyer default because they can seize the goods and resell the goods more easily than financial institutions can due to their strong network in the industry, leading to lower repossessing and resale costs (Mian & Smith, 1992).

Trade credit can also be used to price discriminate even if the supplier has no financing advantage over financial institutions (Brennan et al., 1988; Mian & Smith, 1992; Petersen & Rajan, 1997). In addition, trade credit is a very efficient payment method that provides for the separation of payment from delivery and reduces uncertainty (Ferris, 1981). When a supplier does not have a reputation in the product market, the supplier can offer trade credit until the buyer can ascertain the product quality, and therefore, will bear the cost of financing until having built up a reputation in the market (Long et al., 1993).

The above studies explain the existence of trade credit from the supply side’s perspective. From the demand side’s perspective, there are currently two competing hypotheses that attempt to explain why firms use trade credit even though it is a costly source of financing. The first hypothesis, known as the substitution hypothesis, argues that trade credit and bank loans are substitutes, that is, the reliance on trade credit increases when firms face difficulties in obtaining bank financing (Petersen & Rajan, 1997). The second hypothesis, known as the signaling hypothesis, argues that trade credit might play a signaling role for banks, thus mitigating adverse selection problems and credit rationing. As Biais and Gollier (1997) suggest that if the seller is willing to extend trade credit, and thus to bear the default risk of the buyer, it must be that it has good information about the latter. On observing this, the bank updates positively its beliefs about the buyer, and therefore agrees to lend. In other words, trade credit enables the private information of the seller to be used in the lending relationship, and this additional information can alleviate credit rationing due to adverse selection. From this perspective, trade credit and bank lending would not necessarily be substitutes, but might be complements. This argument is supported by Cook (1999). More specifically, Cook (1999) documents that uninformed banks seem more inclined to lend to firms accessing trade credit. Alternatively, suppliers, by extending trade credit, seem to be disclosing favorable information to potentially less-informed lenders.

Hypothesis Development

As discussed previously, firms with restatement announcements may experience difficulties in borrowing from financial institutions, because of the increased information asymmetry between the restatement firms and the financial institutions. In contrast, suppliers use different information than financial institutions and do not appear to rely on information provided by lending relationships. Measures of the strength of institutional relationships or the risk premium on institutional loans granted have little effect on how much trade credit a firm is offered. More specifically, suppliers may have more advantages than banks in evaluating and controlling the credit risk of their customers. Suppliers may also use trade credit to price discriminate different groups of customers when direct price discrimination is not legal. Trade credit may be useful in reducing transaction costs or in providing a guarantee about suppliers’ product quality. Therefore, suppliers may still be willing to extend trade credit to restatement firms even if these firms are facing financial constraints from the capital market. Therefore, following the restatement announcements, we expect restatement firms to use more trade credit than do non-restatement firms. Our first hypothesis is stated as follows:

According to the pecking order theory (Myers & Majluf, 1984), firms that seek to minimize their cost of capital will try everything from the cheapest financing method to the most expensive one. That is, first, they will use their internal cash, then borrow from banks, followed by raising public debt, and finally issue equity. Trade credit is not considered in the pecking order theory. However, because of its implicitly high interest rate, trade credit is generally considered an expensive alternative to bank debt. Therefore, as suggested by the substitution hypothesis, we argue that firms resort to trade credit financing only when they experience difficulties in borrowing from financial institutions. In other words, when restatement firms are more financially constrained, they tend to use more trade credit. Our next two hypotheses are as follows:

Research Design and Sample Selection

Research Design

To test H1, we consider the following regression model for the full sample that includes both restatement firms and non-restatement firms:

We follow prior research and include firms’ characteristics that could be related to trade credit as discussed in the literature (e.g., Chen et al., 2017; Dass et al., 2015). We include liquidation costs (LIQUIDCOST) because suppliers may be unwilling to offer trade credit if it is difficult or costly for the suppliers to liquidate the borrower firms’ assets (Petersen & Rajan, 1997). To control for credit quality, we include firm size (LOGASSET), firm age (LOG_AGE), and credit rating (PREDRATING) in our primary model. We control for market power by adding MKTSHARE to the primary regression model. Because the demand for trade credit is higher when firms have greater growth opportunities (Dass et al., 2015), we control for firm growth by including positive and negative changes in sales (POS_CHGSALE, NEG_CHGSALE) and market-to-book ratio (MTB). Prior research reveals that suppliers are more willing to offer trade credit to more profitable firms (Petersen & Rajan, 1997) and that the demand for trade credit is lower for more profitable firms (Dass et al., 2015). To control for firms’ profitability, we include return on assets (ROA). Prior literature provides mixed evidence on the complementary and substitutability effects of bank loans and trade credit (e.g., Sáiz et al., 2017); therefore, we include leverage (LEVERAGE) in Equation 1. Because Chen et al. (2017) find that firms having more current liabilities that exclude accounts payable use more trade credit, we also include the ratio of current liabilities excluding accounts payable to total assets (CL_XTRADE).

Firms with more current assets (excluding cash) tend to have a higher need for trade credit financing (Petersen & Rajan, 1997). To control for this, we add the ratio of non-cash current assets to the book value of total assets (CA) to our primary model. We control for firms’ liquidity by adding CASHHOLD (Sáiz et al., 2017). García-Teruel et al. (2014) show that trade credit is negatively associated with the operating cycle. Thus, we control for firms’ operating cycle by including OPERATINGCYCLE. Dass et al. (2015) indicate that firms with more fixed assets are less likely to use trade credit because those firms can use fixed assets as collateral for external financing. To control for firms’ tangibility, we include the tangibility ratio (TANGIBILITY) in our primary model. Chen et al. (2017) find that firms with lower accounting quality use more trade credit; thus, we include the absolute value of abnormal accruals (AQ). The appendix contains detailed descriptions of all variables used in this study.

To test H2 and H3, we consider the following regressions for the sample of restatement firms:

We also include industry and year dummy variables to account for industry-specific and year-specific effects on trade credit in all regressions. The standard errors are two-way clustered at the firm and year levels to correct for the serial correlation in the error terms.

Sample Selection

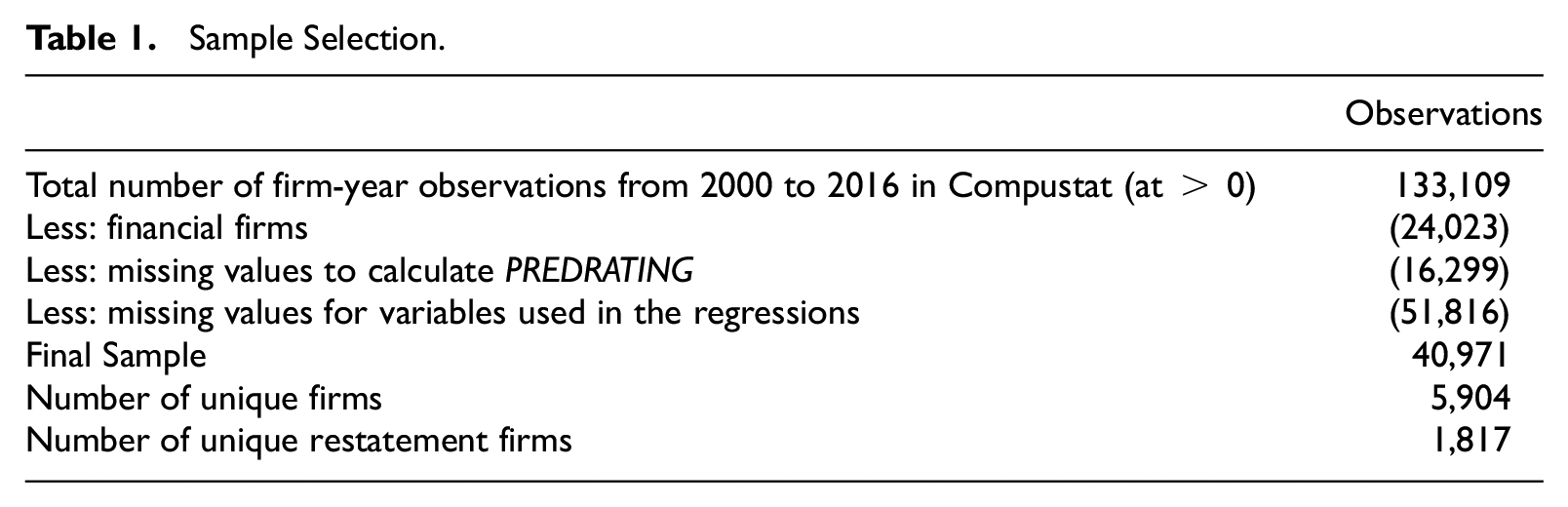

Table 1, Panel A, describes our sample selection process. We start with 133,109 firm-year observations with positive total assets in the Compustat database for the period 2000–2016. Following the literature, we then delete financial firms and foreign firms listed in the United States because these firms may have different legal and operational environments. We also eliminate firms that lack data to calculate all variables used in our regressions. Our final sample has 40,971 firm-year observations for 5,904 unique firms.

Sample Selection.

We then use the Audit Analytics database to identify firms in the above sample that restate their financial statements. In this study, we focus on analyzing only restatements that correct materially misstated financial statements. Our final restatement subsample consists of 2,728 firm-year observations representing 1,817 unique firms. On average, the number of firm-year observations in our restatement subsample is about 6.66% of the full sample, which is comparable to previous studies (e.g., Mande & Son, 2013).

In the Internet Appendix I, we find that the industry composition of the full sample is relatively similar to that of the restatement sample. Both samples cover a wide range of industries with the business services industry being the most represented one (15.71% and 15.43% for the full sample and the restatement sample, respectively).

Empirical Findings

Univariate Analyses and Descriptive Statistics

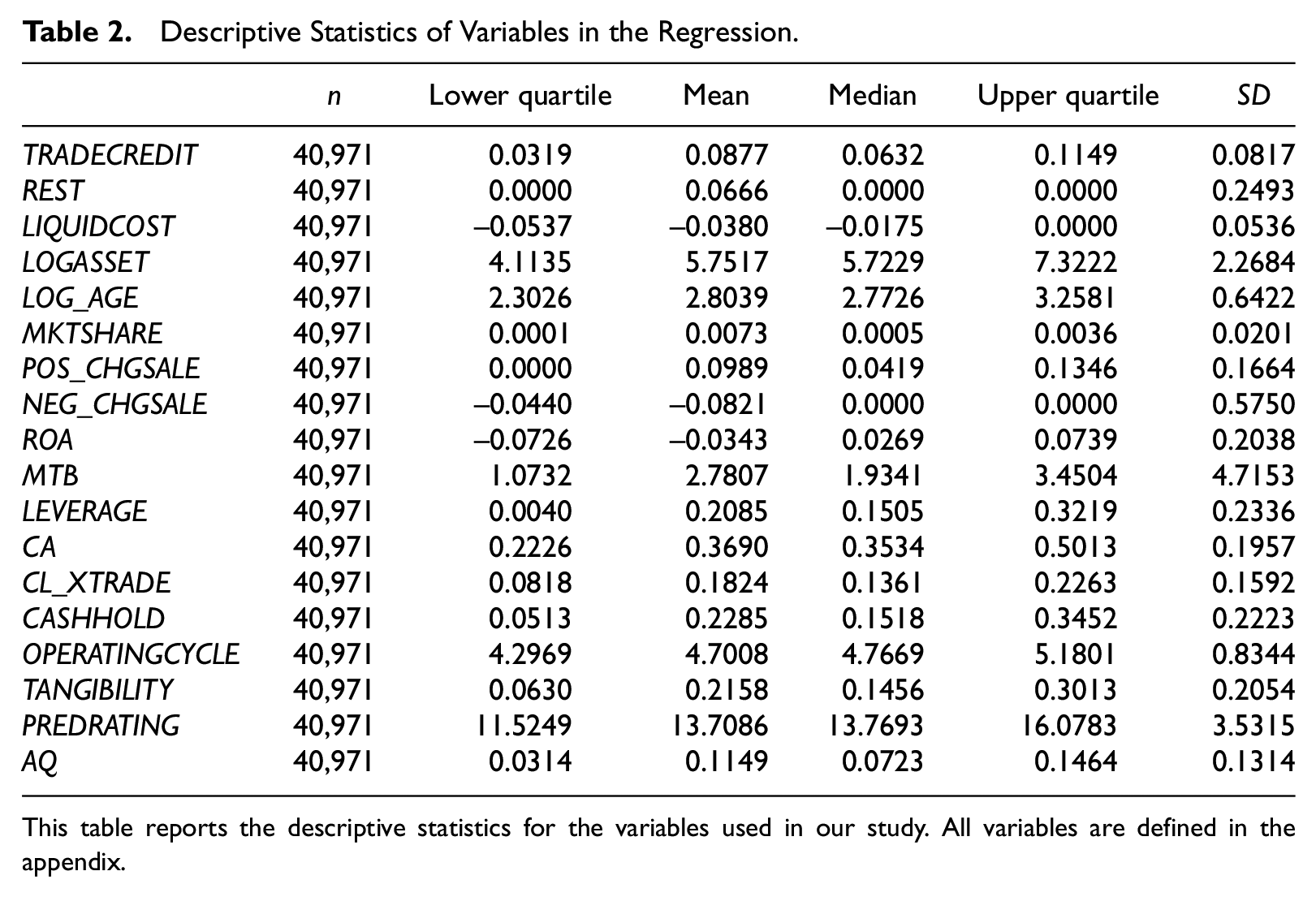

Table 2 reports descriptive statistics for the variables used in our primary regressions. All the continuous variables are winsorized at the 1% and 99% levels to reduce the effect of outliers. The average trade credit is about 8.77% of firms’ total assets in the year preceding the restatement disclosure year, which is consistent with prior studies on trade credit (e.g., Chen et al., 2017). For brevity, we do not discuss the descriptive statistics of the remaining control variables because the values are also consistent with Chen et al. (2017).

Descriptive Statistics of Variables in the Regression.

This table reports the descriptive statistics for the variables used in our study. All variables are defined in the appendix.

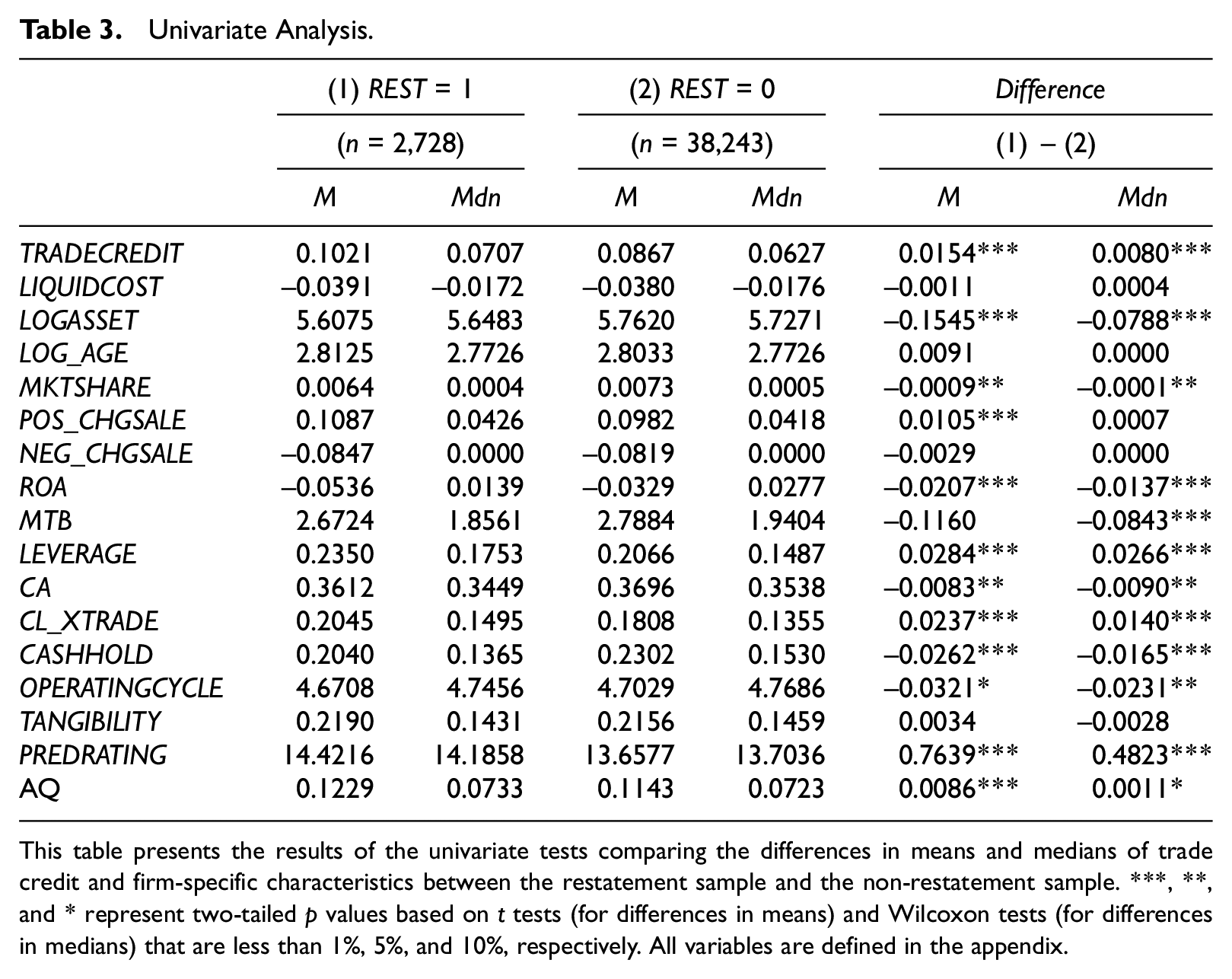

Table 3 provides univariate evidence on the differences in trade credit and other firm characteristics between the restatement and non-restatement samples. The results show that restatement firms use more trade credit than non-restatement firms do in the post-disclosure year, which is consistent with H1. We also find that, relative to non-restatement firms, restatement firms are smaller in size (LOGASSET), less profitable firms (ROA), more likely to have liquidity problems (CASHHOLD), have a lower market share (MKTSHARE), less current assets excluding cash (CA), and shorter operating cycle (OPERATINGCYCLE). The univariate tests of differences also show that growth opportunities (POS_CHGSALE) are greater for restatement firms. In addition, restatement firms are high-leveraged firms (LEVERAGE), have a greater ratio of current liabilities excluding accounts payable-to-total assets (CL_XTRADE), lower credit quality (PREDRATING), and lower accounting quality (AQ). Our univariate results are consistent with the strand of literature that suggests a negative association between firms’ accounting quality and the use of trade credit.

Univariate Analysis.

This table presents the results of the univariate tests comparing the differences in means and medians of trade credit and firm-specific characteristics between the restatement sample and the non-restatement sample. ***, **, and * represent two-tailed p values based on t tests (for differences in means) and Wilcoxon tests (for differences in medians) that are less than 1%, 5%, and 10%, respectively. All variables are defined in the appendix.

Multivariate Analyses

Regression results: Financial restatements and trade credit

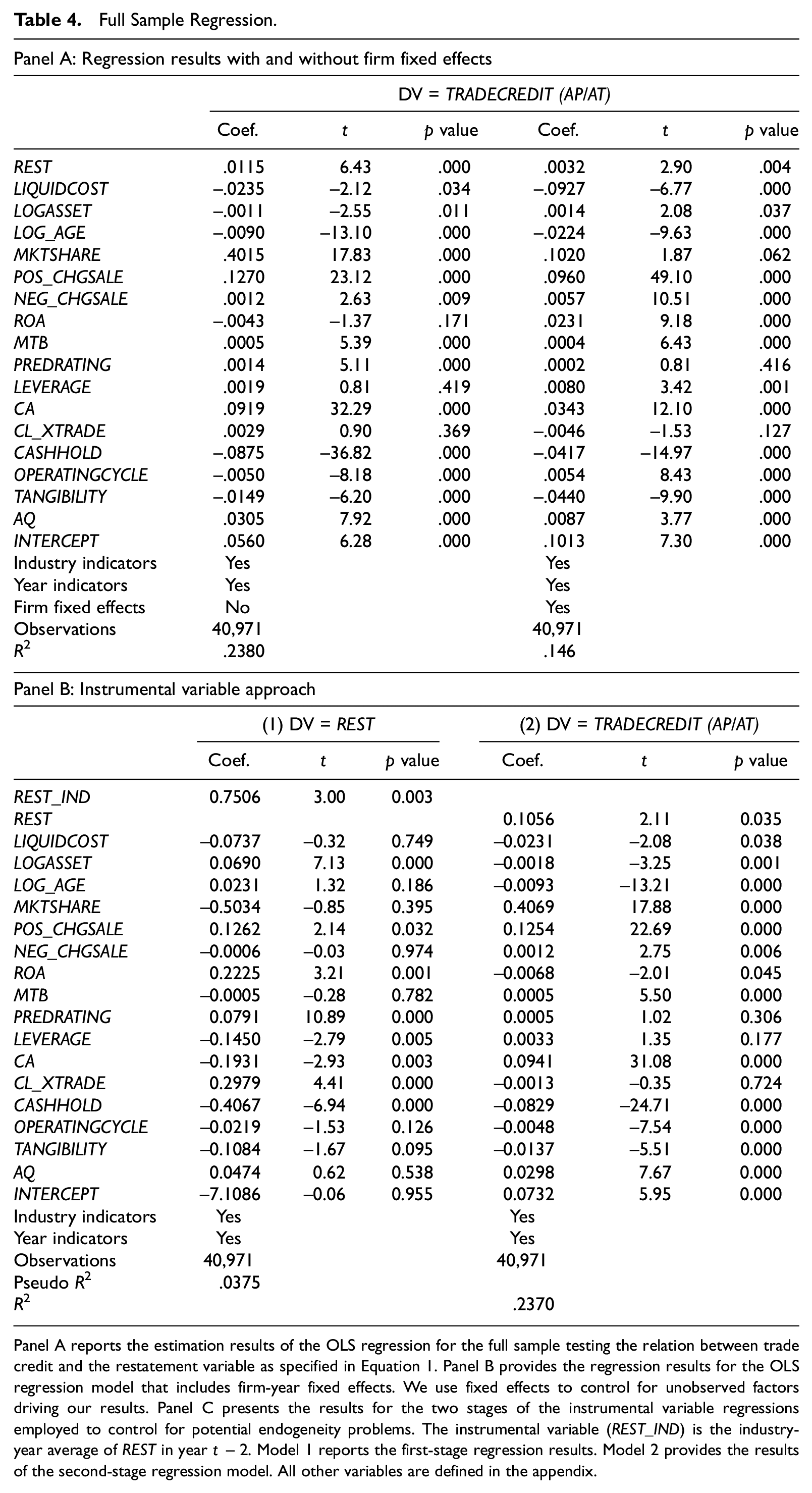

Table 4 provides the results for our H1. In the first three columns of Panel A, we present the results of the ordinary least squares (OLS) regression model. We find that the coefficient on the variable

Full Sample Regression.

Panel A reports the estimation results of the OLS regression for the full sample testing the relation between trade credit and the restatement variable as specified in Equation 1. Panel B provides the regression results for the OLS regression model that includes firm-year fixed effects. We use fixed effects to control for unobserved factors driving our results. Panel C presents the results for the two stages of the instrumental variable regressions employed to control for potential endogeneity problems. The instrumental variable (REST_IND) is the industry-year average of REST in year t− 2. Model 1 reports the first-stage regression results. Model 2 provides the results of the second-stage regression model. All other variables are defined in the appendix.

Our findings on the association between financial restatements and trade credit may be biased by potential endogeneity problems. Specifically, there may be unobserved factors that are correlated with restatements and trade credit. We account for the possibility of omitted variables by using a firm, industry, and year fixed effect specification and instrumental variable approach in our regressions. The last three columns of Panel A present the results of the estimation of Equation 1 that includes firm fixed effects. The results are still consistent with our main findings on the positive relation between restatements and trade credit.

Panel B of Table 4 reports the results of the two-stage instrumental variable approach to address potential endogeneity problems. We use the industry (i.e., 2-Digit SIC) average of the probability of restatements in the previous fiscal year (REST_IND) as the instrument. We believe that the use of the past industry averages is a valid instrument in our setting because this instrument is likely to be exogenous to the probability of firms restating their financial statements in the current year. In the first stage, we regress the probability of financial restatements (REST) on the instrumental variable and control variables from our primary model. In the second stage, we regress trade credit on the predicted value of the probability of financial restatements and control variables. As shown in Panel B of Table 4, the instrumental variable results are consistent with those in Panel A of Table 4. Briefly, the results of the regression model that includes firm fixed effects and the instrumental variable regression reinforce our reported OLS findings.

As additional tests, we perform change analyses for both the full sample and the restatement sample. For the full sample, we use the same Equation 1 with all dependent and independent variables being in changes form. The dependent variable, CHANGE_TRADECREDIT, is the change in trade credit from the year prior to the restatement disclosure year to the year after the restatement disclosure year. The variable of interest, CHANGE_REST, is an indicator variable equal to 1 when a firm changed from not restating their financial statements to restating their financial statements. We report the results in Panel A Table 5. We find that the coefficient on CHANGE_REST is positive and significant, which indicates that the level of trade credit is higher for firms that changed from not restating their financial statements in year t−2 to restating their financial statements in year t−1 as compared with other firms. Panel B Table 5 provides the results of analyzing the change in trade credit for the restatement sample. In this model, the interest variable, POST, is an indicator variable equal to 1 for the year after the restatement year and 0 otherwise. We find that POST is positively and significantly associated with TRADECREDIT. This suggests that relative to the pre-restatement period, restatement firms have a higher level of trade credit in the post-restatement period. Briefly, the results in Table 5 further confirm our conclusion that restatement firms use more trade credit than non-restatement firms. The results provide additional evidence on the restatement firms’ increase in the level of trade credit in the post-restatement period compared with the pre-restatement period.

Change Analyses.

Panel A presents the changes analysis of the full sample. In the changes model, all the dependent variable, the interest variable, and control variables are in changes form. The dependent variable (CHANGE_TRADECREDIT) is the change in trade credit from the year prior to the restatement disclosure year to the year after the restatement disclosure year. The variable of interest, CHANGE_REST, is an indicator variable equal to 1 when a firm changed from not restating their financial statements in year t−2 to restating their financial statements in year t−1. Panel B reports the change analysis of the restatement sample. Assuming that the restatement disclosure year is year t−1, the dependent variable (TRADECREDIT) is the amount of trade credit in the year after the restatement disclosure year (year t) scaled by total assets in the year before the restatement year (year t−2). The variable of interest, POST, is an indicator variable equal to 1 for the year after the restatement disclosure year (year t), and 0 otherwise. All other variables are defined in the appendix. All models include industry and year indicators. Standard errors are clustered at the firm and year levels to correct for serial correlation. Values of p are based on two-tailed t tests.

Regression results: The influence of external financing

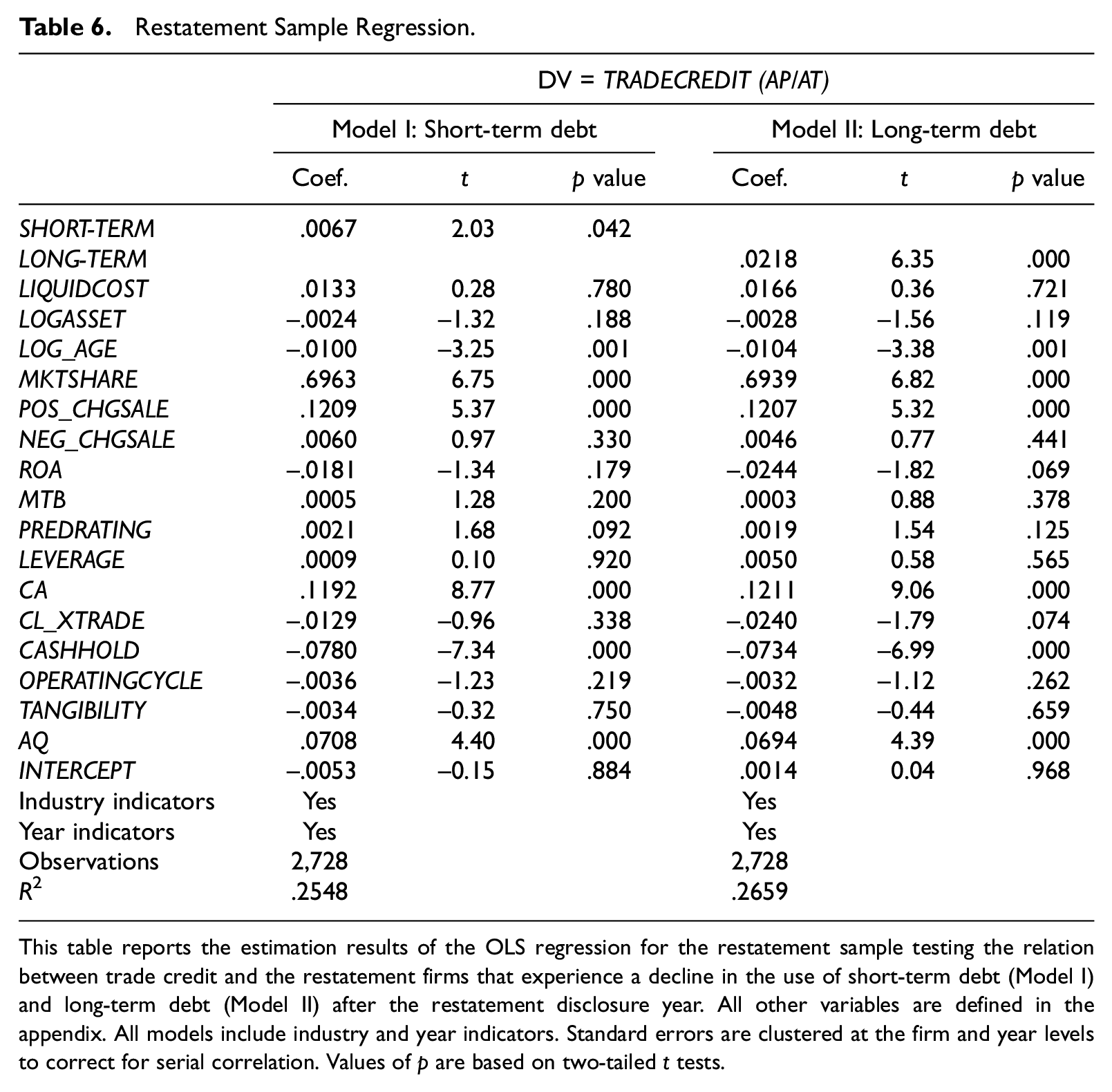

Table 6 presents the estimation results for the equations (2) and (3) to test H2 and H3. In the first three columns, the dummy variable SHORT-TERM is significantly positive, indicating that restatement firms that use less short-term debt in the post-disclosure year than in the disclosure year are likely to use more trade credit. The result of the LONG-TERM dummy variable in the last three columns of Table 6 is also similar. The results for control variables are relatively similar to those in Table 5. Here, the results support H2 and H3, which predict that when restatement firms are more financially constrained with financial institutions (i.e., using less short-term debt and long-term debt after the disclosure year), they are likely to turn to suppliers for trade credit financing.

Restatement Sample Regression.

This table reports the estimation results of the OLS regression for the restatement sample testing the relation between trade credit and the restatement firms that experience a decline in the use of short-term debt (Model I) and long-term debt (Model II) after the restatement disclosure year. All other variables are defined in the appendix. All models include industry and year indicators. Standard errors are clustered at the firm and year levels to correct for serial correlation. Values of p are based on two-tailed t tests.

Additional Analyses: Financing Choices by Restatement Types

Accounting error versus irregularity restatements

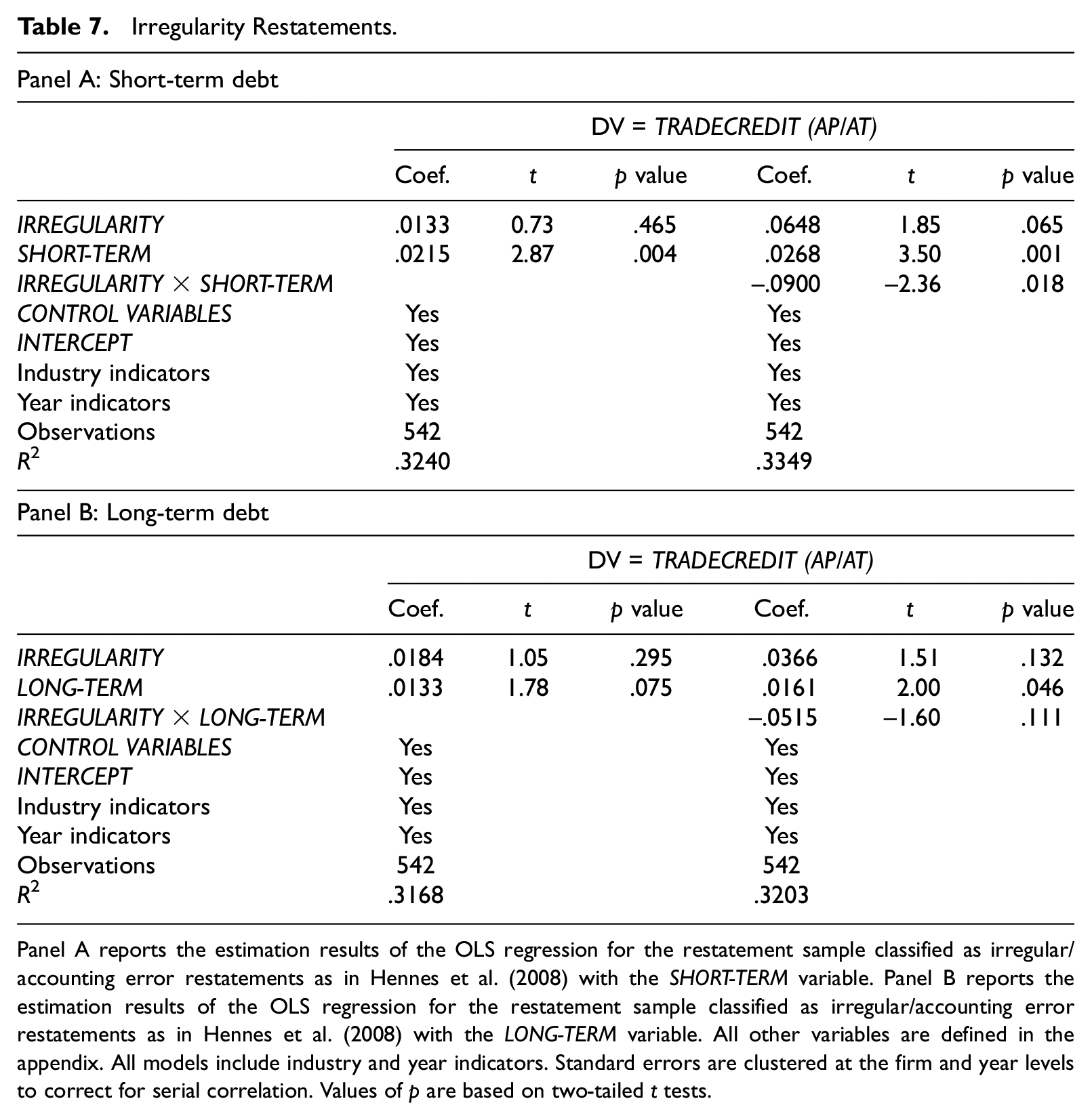

Hennes et al. (2008) show that it is important to distinguish between errors (unintentional misstatements) and irregularities (intentional misstatements) by using restatement data. Restatements that involve accounting irregularities entail more serious consequences than do restatements that involve accounting errors. We employ the irregularity versus accounting error restatement data set used in their study, and the results are reported in Table 7. 1 Panel A shows the results for the SHORT-TERM debt dummy variable, and Panel B shows the results for the LONG-TERM debt dummy variable. IRREGULARITY is a dummy variable equal to 1 if a restatement is classified as an irregularity restatement, and 0 otherwise. As shown, IRREGULARITY is only significant in one of the four models in Table 7, its coefficient is positive in all models. The results provide some evidence on the prediction that firms with irregularity restatements, which are more severe, are likely to use more trade credit than are firms with accounting errors, which are less severe restatements. However, the negative and significant coefficient on the interaction term IRREGULARITY×SHORT-TERM indicates that firms with both irregularity restatements and limited access to short-term financing from financial institutions rely less on supplier financing. The coefficient of the interaction variable IRREGULARITY×LONG-TERM is not significant, suggesting that firms with irregularity restatements may not have their trade credit financing extended if they experience difficulties in obtaining long-term external capital (i.e., using less long-term debt in the post-disclosure year).

Irregularity Restatements.

Panel A reports the estimation results of the OLS regression for the restatement sample classified as irregular/accounting error restatements as in Hennes et al. (2008) with the SHORT-TERM variable. Panel B reports the estimation results of the OLS regression for the restatement sample classified as irregular/accounting error restatements as in Hennes et al. (2008) with the LONG-TERM variable. All other variables are defined in the appendix. All models include industry and year indicators. Standard errors are clustered at the firm and year levels to correct for serial correlation. Values of p are based on two-tailed t tests.

Market reaction to restatement announcements

Some other studies (e.g., Burks, 2010; Wilson, 2008) use market reaction to the restatement announcement as a measure of the perceived severity of a restatement. A restatement is considered more severe if the market reaction around the announcement date is more negative. Table 8 reports the results for the market reaction to restatement disclosures. CAR denotes the cumulative market-adjusted abnormal returns for the 3-day window (i.e., [−1, 1]) surrounding the restatement announcement date and is calculated by subtracting the Center for Research in Security Prices (CRSP) equal-weighted market return from the firm’s holding returns on each day and summing these returns over 3 days. CAR is negative and significant in Panel A and Model 1 of Panel B. The coefficient on CAR in Model 2 of Panel B is not significant but still is negative, which is consistent with the remaining models of Table 8. The results suggest that firms with more severe restatements (i.e., more negative CAR) are likely to use more trade credit. However, similar to the interaction variables in Table 7, the interaction variables CAR×SHORT-TERM and CAR×LONG-TERM in Table 8 are not significant. This indicates that restatement firms with more negative CAR may not be able to substitute long-term debt and short-term debt for trade credit financing.

Effect of Market Reaction.

Panel A reports the estimation results of the OLS regression for the restatement sample classified by the market reaction to restatement disclosures with the SHORT-TERM variable. Panel B reports the estimation results of the OLS regression for the restatement sample classified by market reaction to restatement disclosure with the LONG-TERM variable. All other variables are defined in the appendix. All models include industry and year indicators. Standard errors are clustered at the firm and year level to correct for serial correlation. Values of p are based on two-tailed t tests.

Material errors versus immaterial errors

To further examine whether the severity of financial restatements is related to restatement firms’ financing choice, we follow Choudhary et al. (2019) and classify restatements by materiality. Internet Appendix II presents the results of the model classifying restatements due to material and immaterial errors. The variable of interest in both Panels A and B, MATERIAL_ERRORS, is an indicator variable equal to 1 if a firm discloses its restatements with material errors, and 0 otherwise. As shown in the panels, the coefficient on MATERIAL_ERRORS is negative and significant in all models. The results indicate that firms disclosing restatements with material errors, which is a more severe financial restatement than restatements due to immaterial errors, have a lower level of trade credit than other firms. The results are opposite the previous results using other classifications of restatements (i.e., classifying the severity of restatement by irregularity restatements and market reactions to restatement announcements). A possible explanation for the results is that suppliers may perceive restatements with material errors to be more severe than other classifications of restatement severity. Turning to the two models with interaction variables in Internet Appendix II, we find no significant association between trade credit and the two interaction terms MATERIAL_ERRORS×SHORT-TERM and MATERIAL_ERRORS×LONG-TERM. The results of the interaction variables are consistent with those in Tables 7 and 8, suggesting that firms with more severe financial restatements may have limited access to both conventional loans and trade credit.

The severity of restatements by the restatement amount

Finally, we use the restatement amount (RESTAMT), which is the cumulative change in net income scaled by the book value of total assets, to measure the severity of restatements and examine its relation with trade credit. We report the results in Internet Appendix III. The results show that RESTAMT is positive and significant in all models in both Panel A and Panel B in the Appendix III, indicating that restatement firms with more severe financial restatements measured by the high dollar value of restatement amount are more likely to seek trade credit extension for short-term financing. The insignificant results of the interaction variables between RESTAMT and SHORT-TERM and LONG-TERM are in line with the previous results. The results support the conclusion that the severity of financial restatements and the difficulty in obtaining external capital from financial institutions may be important factors contributing to restatement firms’ inability to obtain trade credit extension.

Additional Analysis: CEO Turnover Effect

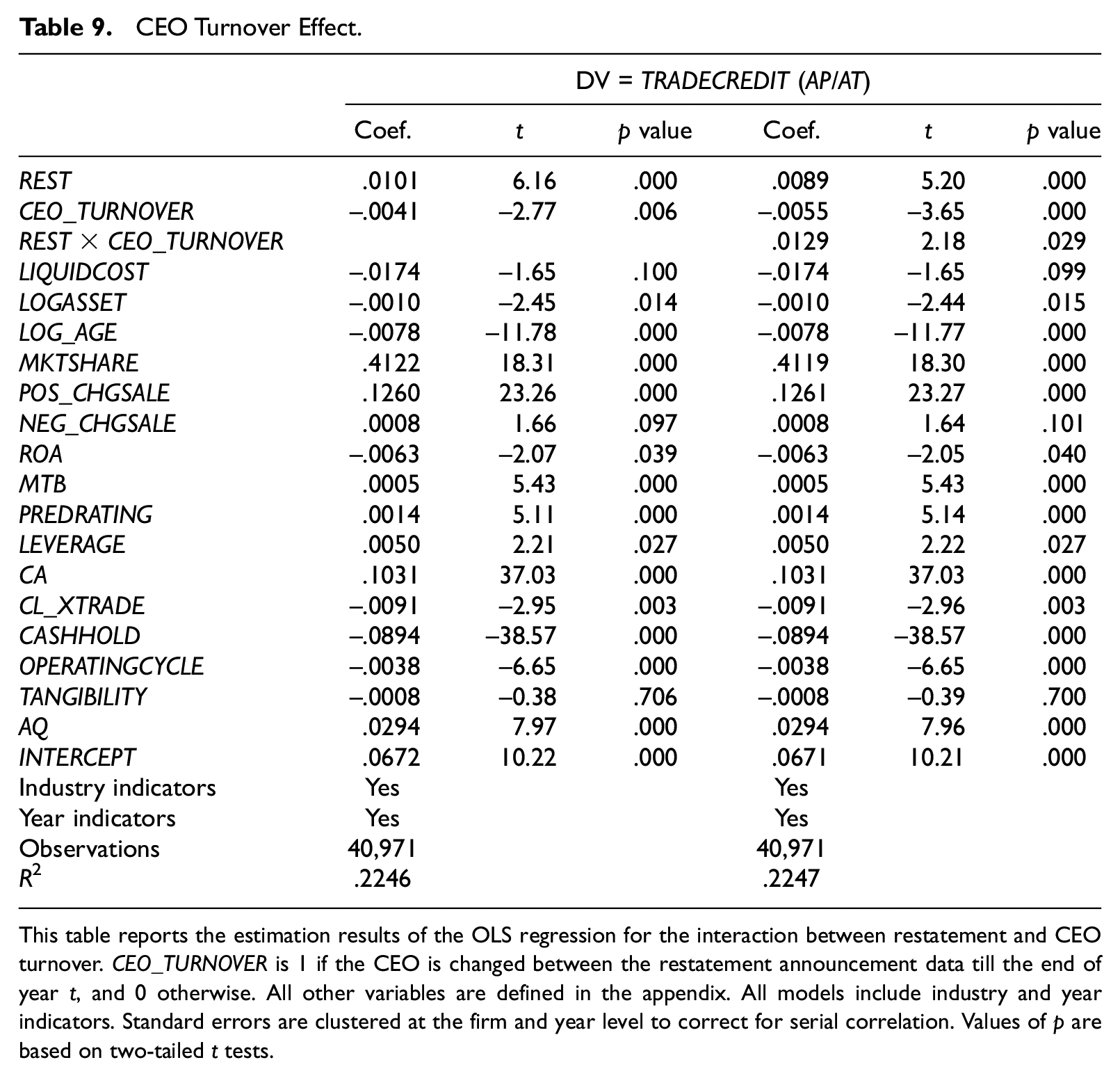

Desai et al. (2006) indicate that restatements lead to significant damage to firm reputation, which in turn motivates firms to change the management to restore investors’ faith in the firms and to recover firms’ reputation. Similarly, Kryzanowski and Zhang (2013) add that the higher probability of CEO turnovers in the post-restatement period signals the market about restatement firms’ intention to deal with the impact of agency problems on cash flow uncertainties. Accordingly, our additional test examines whether the CEO turnover event after a restatement announcement (CEO_TURNOVER) helps restatement firms to resolve information problems and thus influences suppliers’ willingness to grant trade credit. Specifically, we add an interaction between CEO_TURNOVER and restatements (REST) to our primary regression model. We provide the results in Table 9. We find that REST is positively associated with TRADECREDIT, further supporting our main results. The results also show a positive and significant coefficient on the interaction term (REST×CEO_TURNOVER), suggesting restatement firms can enhance their ability to obtain trade credit through changing the CEO in the post-restatement period.

CEO Turnover Effect.

This table reports the estimation results of the OLS regression for the interaction between restatement and CEO turnover. CEO_TURNOVER is 1 if the CEO is changed between the restatement announcement data till the end of year t, and 0 otherwise. All other variables are defined in the appendix. All models include industry and year indicators. Standard errors are clustered at the firm and year level to correct for serial correlation. Values of p are based on two-tailed t tests.

Robustness Tests

Alternative measure of trade credit

In this section, we also employ another measure of trade credit (i.e., the ratio of accounts payable to the book value of long-term debt) and re-estimate Equations 1, 2, and 3. The results are very similar. 2 Specifically, we document that the coefficients of the dummy variables REST, SHORT-TERM, and LONG-TERM are positive and significant, providing additional evidence to support our hypotheses. Overall, the results suggest that firms with more severe restatements may use more trade credit as a source of financing. However, we do not document any evidence that restatement severity affects restatement firms’ financing choices between traditional short-term or long-term debt and trade credit financing.

Limiting sample to post-SOX period

Prior studies on restatements show that in the post-SOX period, market reactions to restatement announcements are significantly less negative than the pre-SOX period (e.g., Scholz, 2008). This may be because financial restatements in this period appear to be less severe and involve lower dollar amounts, unintentional errors, and non-core accounts (Hennes et al., 2008; Plumlee & Yohn, 2010). Therefore, firms’ use of trade credit may be different between the pre- and post-SOX periods. As a robustness check, we re-estimate our regression using the post-SOX sample. The untabulated results are consistent with our main findings, suggesting that regardless of the pre- and post-SOX, restatement firms tend to rely more on trade credit financing than other firms.

Conclusion

Despite the extensive literature discussing the consequences of financial restatements and the difficulties experienced by restatement firms in obtaining borrowings from financial institutions, no research has examined the association between financial restatements and the restatement firms’ use of trade credit. Our article fills in this gap in the literature by investigating whether restatement firms are more likely to use trade credit as a source of financing and whether restatement firms with a decrease in conventional types of debts (short-term and long-term loans) tend to use more trade credit.

We find evidence that firms restating their financial reports tend to demand more trade credit in the year following the restatement disclosure year compared with non-restatement firms. We also find that relative to the pre-restatement announcement period, restatement firms’ level of trade credit is higher in the post-restatement period. These findings are consistent with our expectations that restatement firms are more likely to seek trade credit as an alternative source of financing. Financial institutions are more reluctant to provide capital to such firms, whereas suppliers are willing to extend trade credit because suppliers are better positioned to obtain information about the creditworthiness of a customer. We also document that restatement firms that use fewer short-term loans and long-term loans are more likely to use trade credit. Our additional tests show that firms with more severe financial restatements (classified by accounting errors versus irregularity restatements, market reaction to the restatement, and restatement amount) tend to seek trade credit contracts from suppliers. Nevertheless, when we employ material errors versus immaterial errors as the criteria to evaluate the severity of financial restatements, we find that firms disclosing restatements due to material errors (i.e., a more severe type of financial restatements) use less trade credit financing. These different results between the classification of restatements using the materiality of restatement errors and other methods of restatement classifications may be due to suppliers’ perception of restatement with material errors to be more severe than other types of restatements and thus are less willing to offer trade credit extensions. In addition, we do not find evidence about how the severity of financial restatements influences firms’ choices between trade credit and conventional loans. This article provides initial insights into the association between financial restatements and the use of trade credit. Future research should use a more extensive sample of restatement firms to examine the impact of restatement types on the restatement firms’ choice of financing.

Supplemental Material

sj-docx-1-jaf-10.1177_0148558X221096369 – Supplemental material for Financial Restatements and the Demand for Trade Credit

Supplemental material, sj-docx-1-jaf-10.1177_0148558X221096369 for Financial Restatements and the Demand for Trade Credit by Mai Dao, Duong Nguyen and Hongkang Xu in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Variable Definitions.

| Variable | Definition |

|---|---|

| Main variables | |

| TRADECREDITt | The ratio of accounts payable to the book value of total assets in the year t (i.e., the year after the restatement disclosure year) |

| RESTt-1 | Equals 1 if the firm restates its financial statements in year t− 1, and 0 otherwise |

| SHORT-TERMt | Equals 1 if a restatement firm decreases its use of short-term debt from year t− 1 (restatement disclosure year) to year t, and 0 otherwise. Short-term debt is the ratio of debt in current liabilities to total assets. Debt in current liabilities, which is obtained from the Compustat database, is the sum of long-term debt due in 1 year and notes payable |

| LONG-TERMt | Equals 1 if a restatement firm decreases its use of long-term debt from year t− 1 (restatement disclosure year) to year t, and 0 otherwise |

| IRREGULARITYt-1 | Equals 1 for an irregular restatement, and 0 otherwise. We follow Hennes et al. (2008) definition of irregularity |

| CARt-1 | The cumulative market-adjusted abnormal returns for the 3-day window surrounding the restatement announcement date; is calculated by subtracting the CRSP equal-weighted market return from the firm’s holding returns on each day and summing these returns over 3 days |

| MATERIAL_ERRORSt-1 | 1 if the firm discloses its restatements with material errors, and 0 otherwise |

| RESTAMTt-1 | Cumulative change in net income scaled by the book value of total assets |

| CEO_TURNOVERt-1, t | 1 if CEO is changed between the restatement announcement data and the end of year t, and 0 otherwise |

| Control variables | |

| LIQUIDCOSTt | Liquidation costs are calculated as the ratio of raw materials to total assets and multiplied by −1 |

| LOGASSETt | The natural logarithm of the book value of total assets |

| LOG_AGEt | The natural logarithm of a firm’s age plus 1 |

| MKTSHAREt | A firm’s market share is calculated as the ratio of the firm’s sales over total industry sales, where industry classification is based on two-digit SIC codes |

| POS_CHGSALEt | Positive changes in sales, scaled by the book value of total assets |

| NEG_CHGSALEt | Negative changes in sales, scaled by the book value of total assets |

| ROAt | Return on assets, calculated as the ratio of net income over total assets |

| MTBt | The ratio of the market value of equity to the book value of net assets |

| PREDRATINGt | S&P credit rating from Compustat. If the rating is not available for a firm-year, then we estimate a credit rating following Beatty et al. (2008). The larger the value of the predicted rating, the lower the credit quality |

| LEVERAGEt | The ratio of long-term debt and debt in current liabilities to the book value of assets |

| CAt | The ratio of non-cash current assets to the book value of total assets |

| CL_XTRADEt | Current liabilities excluding accounts payable over total assets |

| CASHHOLDt | The ratio of cash and marketable securities to total assets |

| OPERATINGCYCLEt | The natural logarithm of days of accounts receivable plus days of inventories |

| TANGIBILITYt | The ratio of net property, plant, and equipment to assets |

| AQt | The absolute value of abnormal accruals computed using the Jones (1991) model modified by Dechow et al. (1995) |

| REST_INDt-2 | The industry-year average of the REST in year t− 2 |

Acknowledgements

We thank the editors and an anonymous referee for valuable comments that have greatly improved this article, as well as participants at the 2020 American Accounting Association Management Accounting Section Midyear Meeting.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.