Abstract

This paper presents a model of auditor-client relationship-building (RB). We find that the relation between RB and audit effort is nonmonotonic, that is, it can improve or impair audit effort. On the one hand, RB improves the usefulness of exerting effort and the auditor is then motivated to work harder. On the other hand, RB improves the precision of the signal received by the auditor and reduces her expected liability, which reduces her incentive to exert effort. Moreover, existing literature suggests that quasirents arising from long auditor tenure compromise auditor independence. In contrast to this conventional wisdom, this paper shows a positive effect of quasirents resulting from relationship-building on auditor independence under certain conditions. This is the first study modeling client relationship-building initiated by auditors. It enhances our understanding of the relationship between RB and audit effort as well as auditor-client negotiations.

Introduction

Audit firms often assign nondecision-making liaisons to engagements (i.e., relationship partners) to foster positive relationships with clients (Dodgson et al., 2021). 1 A professional relationship between clients and auditors can be beneficial for both parties throughout the audit process. However, relationship partners may engage in activities intended to entertain clients to build a close relationship. With such a relationship, audit firms may appear to be nonindependent. Audit firms however are required to be independent from their clients in both fact and appearance (PCAOB, 2016 AS 1005.03). Thus, the question arises: does professionally motivated investment in auditor-client relationship-building (RB) impair audit effort and auditor independence?

To answer this question, we build a two-period model to capture strategic interactions between auditors and managers. We analyze auditors’ choices regarding the extent of client RB and audit effort and their reporting decisions. Following prior literature, we define audit quality as the likelihood that an auditor both detects material misstatement in a client’s financial statements, and reports the breach (e.g., DeAngelo, 1981b). The conditional probability of reporting a discovered breach is a measure of an auditor’s independence from a given client (DeAngelo, 1981a). We also define this probability as the auditor’s reporting quality. Auditor independence includes two elements: (1) independence-in-fact, which is present when auditors attest to financial statements truthfully based on evidence collected, and (2) independence-in-appearance, which is present when auditors have only arm’s-length relationships, regardless of whether they actually report truthfully. Building a close relationship with a client may be a violation of independence-in-appearance, while the auditor is independent-in-fact. Auditor reporting quality is a function of whether the auditor is independent-in-fact, that is, once the auditor discovers a material misstatement, she reports it. Reducing RB is intended to maintain independence-in-fact by deterring auditors from violating independence-in-appearance.

However, we argue that RB is not detrimental necessarily. We first find that the relation between RB and audit effort is nonmonotone: if not too extensive, RB can enhance audit effort, but extensive RB diminishes it. On the one hand, RB boosts the usefulness of exerting effort and motivates the auditor to work harder. On the other hand, RB increases the precision of the signal received by the auditor, reducing her expected liability, and consequently her incentive to exert effort.

Moreover, we demonstrate that RB can either impair or improve auditors’ reporting quality. On the one hand, the incumbent auditor engaging in RB has an informational advantage over her competitors, increasing her quasirent. 2 When the quasirent increases, the auditor is more likely to acquiesce to a client-preferred inflated report in order to keep the company as her client. On the other hand, the auditor could successfully report independently in the first period if (1) the company prefers to engage in RB in the second period and (2) she credibly commits to eschew RB in the second period in case the company presses for an inflated report at the end of the first period. Such a commitment can be made credible by a regulator imposing more severe penalty on an auditor’s acquiescence to an inflated report in period one while engaging in RB in period two. Committing to eschewing RB in the second period drives the company to accept the independent report in the first period. Absent the commitment, a company with large quasirents would press for an inflated report to offset the discount from a rational capital market. The option of RB in the second period serves as a disciplinary mechanism (leverage) the auditor can use to elicit the company’s acquiescence to the independent report. In this case, the coincidence of higher quasirent with higher RB has a positive impact on auditor independence, in contrast to the negative impact implied by the existing literature.

RB is not uncommon in audit practice. Building an effective relationship with a client is a key skill that lies at the heart of the audit profession (CAAN, 2016; Knechel et al., 2020). Though there has been some analytical research on auditor independence, our study is the first to explore the impact of client relationship-building on audit quality (Ye, 2023). Antle (1984) develops a formal principal-agent model to investigate auditor independence. DeAngelo (1981a) examines whether low-balling in the first period of engagement impairs auditor independence. Magee and Tseng (1990) extend DeAngelo’s work on audit pricing and auditor independence. Zhang (1999) develops a bargaining model to formally analyze how quasirents can impair auditor independence. Arya and Glover (2014) stress the design of mechanisms that support independence of auditors from firm management. Ronen (2002) and Dontoh et al. (2013) suggest financial statement insurance to solve auditors’ conflicts of interest and lack of independence. Dye (1991), Teoh (1992), Kanodia and Mukherji (1994), Gigler and Penno (1995), and Lu (2006) analyze the relationship between auditor replacement and auditor independence. Simunic (1984) and Wu (2006) develop models to demonstrate the effect of consulting services on audit quality. These papers consider a client’s conferral of benefits on auditors such as to elicit a favorable report. Analyzing the auditor learning effect in a dynamic setting, Beck and Wu (2006) suggest the auditor may provide nonaudit service free of charge.

We complement these studies by exploring the benefits relationship-building activities confer on clients. Our research contributes to this stream of literature by incorporating audit pricing, client retention, and auditor independence. More specifically, it focuses on RB initiated by audit firms that have no nonarm’s-length economic interest in the client and provides insights on auditor’s effort and reporting decisions. Most importantly, existing literature suggests that the quasirent has a negative effect on auditor independence. In contrast to this conventional wisdom, our paper shows a positive effect of quasirent resulting from RB if regulators properly sanction auditors’ RB. Analyzing the auditor-client negotiation and endogenizing the capital market effects, we show how an auditor’s credible commitment to discontinue RB in the second period induces the company to commit to truthful reporting with a consequent higher expected payoff in the first period. Furthermore, while prior analytical auditing research models one or two decisions, auditors in our model make three decisions: RB, audit effort, and reporting.

The sanction on EY by the Securities Exchange Commission (SEC) highlights the importance of auditor independence. 3 Our paper helps better understand the “threats” to independence and highlights the importance of distinguishing the effect of independence-in-appearance from independence-in-fact. To deter lying, penalizing violations of independence-in-fact may be useful, but disciplining independence-in-appearance requires more scrutiny. This research demonstrates the economic trade-offs of imposing a strict independence-in-appearance rule (such as sanctions on client RB) and provides relevant policy implications for regulating bodies such as the SEC. Harris and Raviv (2008) demonstrate that it is sometimes optimal to have insiders rather than independent directors in control of the board, because insider-control better exploits insiders’ information. Our analysis draws a similar conclusion in an auditing setting: auditors building relationships with clients can be beneficial.

Empirical research mostly examines whether consulting services will impair auditor independence. Schneider et al. (2006) provide a review on the literature regarding nonaudit services and auditor independence. Our study generates empirical predictions of the effect of client RB on audit effort and audit reporting quality. Based on our model assumptions, we predict a nonlinear relation between audit effort and RB.

This study also sheds light on the effect of mandatory audit firm rotation and adds to the existing literature in this area (Bleibtreu & Stefani, 2018; Lu & Sapra, 2009). We demonstrate that mandatory audit firm rotation is a double-edged sword. On the one hand, it improves auditor independence in the first period. On the other hand, it may reduce audit effort in the second period, as the new auditor does not have the informational advantages compared to the incumbent auditor.

The paper proceeds as follows. We describe the context of our research in Section 2. Section 3 presents the structure and ingredients of the model. Section 4 establishes the equilibrium. Section 5 reports on comparative statics analysis and discusses model implications. Section 6 concludes. We present all proofs in the Appendix.

RB in Auditing Practice and Modeling RB

A positive and strong working relationship is critical for audit firms, especially for client cooperation and assistance during the evidence-gathering process and when sensitive issues require resolution (Guenin-Paracini et al., 2015; Richard, 2006). Audit firms often assign senior leadership partners to engagements as relationship liaisons, frequently referred to as relationship partners. These liaisons do not hold any decision-making authority over the audit, but manage the relationships with the clients. Audit firms can enjoy potential benefits in return for relationship partner efforts during social exchanges. For instance, audit firms may engender a favorable working dynamic between the audit partner and client management and an avenue for amicable and quick resolution of issues (Dodgson et al., 2020). Relationship partners could help solving disagreements over estimates or accruals in which no clear-cut solution exists (Dodgson et al., 2021). The engagement partners can receive input from the relationship partners who may acquire private information from client senior executives through social exchanges.

One can think of three modeling choices for relationship-building. The first is that RB lengthens the period during which the client retains the auditor. The second is that RB decreases the marginal cost of the audit. And the third is that RB increases the marginal precision of the information the auditor gleans as a result of the audit. It is relatively easy to dispose of the first modeling choice. Unless there is a major audit failure or significant disagreement between the auditor and the client regarding some accounting choices, and in the absence of auditors’ mandatory rotation, the probability of termination of the auditor’s engagement would be negligible. Having made a significant investment in learning the client’s operations and the accounting system in the first years of audit, the auditor would likely perceive the client to be very reluctant to terminate the engagement. The client’s cost of retaining a new auditor who does not benefit from the learning investment made by the prior auditor would disincentivize the client from ending the relationship with the first auditor. In other words, the client may incur switching costs. These arguments are consistent with DeAngelo (1980), which shows that the incumbent auditor will always be retained in the presence of transaction costs of auditor switch. Hence, the auditor would have no incentive to invest in relationship-building.

The reduction in the marginal cost of an audit is another modeling option. Through RB, the auditor may become more efficient in planning and conducting the audit if she learns more about the company through private channels (Schultz & Hooks, 1998). Moreover, during the evidence collection stage, the client may be more accommodating, and sensitive issues can be resolved promptly. However, some may argue that such an effect from RB would be equivalent to investment in auditing technology that contributes to lowering the audit cost. To identify the unique effect coming from RB, we decide to focus on the third option.

The RB increases the marginal precision of the information (or the signal) obtained by the auditor via exerting effort on the quality and reliability of the financial statements. A close relationship with the client enables the auditor to build trust to allow the latter to obtain information that otherwise would be difficult to harvest. Specifically, this would be the kind of information that is not easy to glean from examining the accounting records, transaction documents, etc. Rather, this would be information solely possessed by the client’s senior officers, such as forecasts of events, future transactions, and trends, that potentially impact the content and reliability of the financial statements. In other words, RB facilitates the acquisition of higher-level information, which, by complementing the evidence obtained from the standard audit procedures, enhances the precision of the overall evidence or the signal about the correctness or quality of the financial statements. Through such relationship-building, the auditor may be able to obtain information from the client, making exerting effort more effective in obtaining more precise signal. Therefore, we model the effect of RB as a marginal enhancement of the signal’s precision.

Model

Consider a two-period model (t = 1, 2) in which the market for initial audit engagements in the first period is perfectly competitive since all potential auditors have identical capabilities. 4 The markets for the second period audits are not perfectly competitive because incumbent auditors may possess advantages over potential new auditors. Discount factor is assumed to be 1 for tractability purpose.

At the beginning of each period, a company prepares financial statements that provide information about its fundamental value. Denote the fundamental value of the company by

Audits are mandatory. In each period, an auditor chooses the amount of RB s

t

and audit effort e

t

(in collecting audit evidence) simultaneously, and obtains audit evidence y

t

about x

t

:

The audit evidence is an unbiased but noisy estimate of x

t

. The precision

We assume that the sum of auditor’s effort cost and RB cost in period t is:

When t = 1, the effort exerted creates learning benefits that decrease the total audit cost of later periods. Specifically, following DeAngelo (1981) and Magee and Tseng (1990), we assume that the later periods’ costs are reduced by a constant, denoted by l > 0 if effort is greater than zero. The auditor’s cost advantage in the second period stems from fixed start-up knowledge and system familiarity. That is, a part of the first-period information precision is retained by the incumbent auditor and can reduce second-period audit cost. To rule out an off-equilibrium result, we assume that l is not too large, that is, l < l∗, where l∗ is defined in the equilibrium discussions in Section 4.2.1. When l is not too large, the auditor will not be willing to accept the nonindependent report when the market beliefs the report is independent.

The cost multiplier k on RB captures the client’s aversion to engaging in RB, which could be the opportunity cost of their time. The higher the k, the more difficult and costly it is for the auditor to convince the client to participate in RB. This parameter is time invariant. We assume k > max (κ1, κ2) to ensure interior solutions. κ1, κ2 are defined in the proof.

Conditional on the audit evidence, y

t

, the auditor derives her best estimate of x

t

. The estimate is a weighted average of the prior mean

The auditor then proposes this estimate, r It , to the company as the candidate value to be reported externally. The company, in turn, proposes its own candidate value r t . If the auditor disagrees with r t , then r It will be issued as the final report. But the company may impose a cost on the auditor (Zhang, 1999). For example, the company may disengage from the auditor. This is possible since the client’s expected cost of hiring the incumbent auditor or switching to a new one could be the same in the second period. The auditor may agree with r t if the benefits of avoiding the cost imposed by the company outweigh the incremental liability resulting from issuing r t .

After the audited report r is issued at the end of period one, a competitive capital market forms the market price of the company, M(r), which satisfies

After the company’s first-period fundamental value is realized, the auditor and the company may suffer misstatement costs. Following the standard assumption in the literature (Antle & Nalebuff, 1991; Dye & Sridhar, 2004; Hillegeist, 1999; Narayanan, 1994), we assume that the audit firm will bear a cost of

At the beginning of the second period, the company decides whether to continue with the incumbent auditor or hire a new auditor. After being hired for an audit fee F2, the auditor chooses RB s2 and effort e2, and decides on the report rF2. We assume the incumbent auditor receives all the rent if this auditor can retain the client. Once the company’s second-period fundamental value is realized, the company and auditor share the misstatement costs.

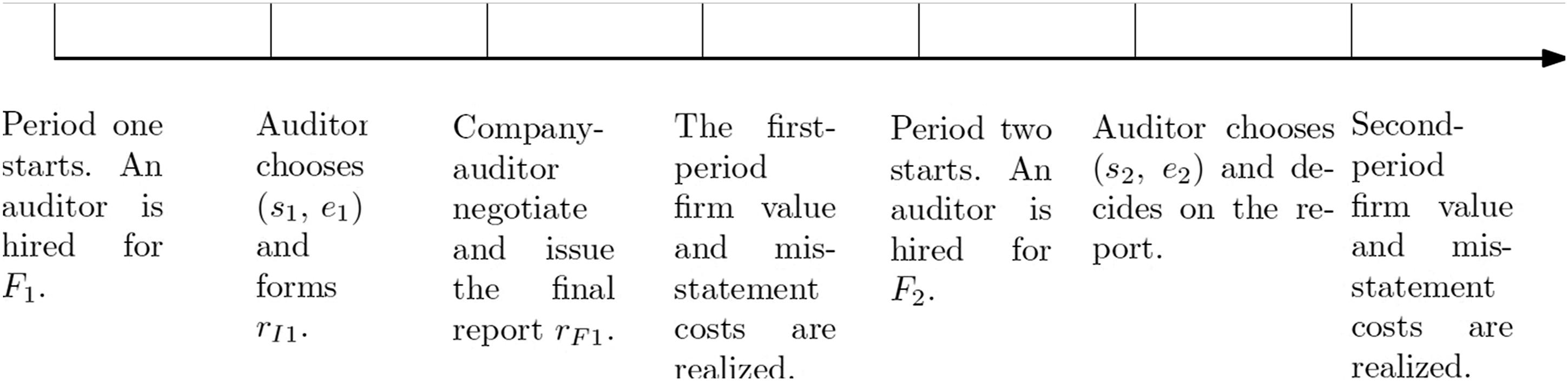

The sequence of events is as follows: • At the beginning of period one, the company offers an audit fee of F1, which is noncontingent on the audit report, and hires an audit firm from a competitive audit market. • The auditor decides simultaneously on the extent of client RB and her audit effort in collecting audit evidence y1, and estimates rI1. • The company proposes a value r1 to the auditor. The company-auditor interaction determines the final audited report rF1. The capital market forms the market price. • The company’s first-period fundamental value is realized. The auditor and the company may suffer misstatement costs. Period one ends. • At the beginning of period two, the company hires the incumbent audit firm or a new audit firm for an audit fee F2. • The auditor simultaneously decides on the extent of client RB and her audit effort in collecting audit evidence y2, estimates rI2, and reports rF2. • The company’s second-period fundamental value is realized. The auditor and the company may suffer misstatement costs.

Figure 1 summarizes the timeline. Timeline

Equilibrium

Benchmark: No RB

To analyze the effect of RB, we first solve a benchmark case when there is no RB, that is, s = 0. The equilibrium consists of the auditor’s effort and reporting decisions, and the company’s reporting choice in period 1 and the auditor’s effort decision in period 2. Since the game ends at the second period, there is no quasirent at that period. The auditor reports independently to the market, and there is no company-auditor negotiation.

The benefit of retaining the client is the quasirent (DeAngelo, 1981a) or value of incumbency (Magee & Tseng, 1990), denoted by Q. At the beginning of the second period, the incumbent’s audit fee is equal to its competitor’s demanded fee (cost), plus switching cost (which in this case is zero). The candidate auditor (competitor) breaks even by setting her fee at the sum of her expected audit cost plus the discounted value of incumbency pertaining to the future period (which is zero in this two-period model). In equilibrium, the value of incumbency in the second period is the cost difference between the incumbent auditor and the candidate auditor in the second period. To avoid confusion, in the rest of the paper, we use “quasirent” throughout to represent the value of incumbency. This quasirent is greater than zero because the incumbent auditor has a cost advantage compared to the new auditor due to learning. We summarize the result in the following lemma. The proof of this equilibrium is in the Appendix.

The auditor would not reduce effort ex ante in anticipation of the future reporting decision, because lower effort reduces her chance of discovering errors and receiving evidence to support her conclusions. Without audit effort, the auditor would not be able to learn the company and gain the learning benefit. The audit effort is not affected by the auditor’s reporting decision because even if the auditor agrees with an inflated report, the incremental misstatement costs resulting from the inflated report are not a function of the auditor’s effort. Moreover, when the auditor chooses reporting decision, her effort is sunk.

Since the incumbent auditor has a cost advantage compared to a new auditor, she sets audit fees at her cost plus the quasirent. Given the audit fee, the auditor chooses an effort to minimize her total cost

In the first period, prior to negotiating with the auditor, the company chooses r1 and audit fees to maximize its following objective:

Expression (5) says that the company benefits from a higher report, r1, where the benefit is the market price, M(r1), but incurs a misstatement cost of

We consider a Perfect Bayesian Equilibrium: (1) The company proposes a report r1 that maximizes expression (5), given the pricing function M(r), the company’s conjecture of audit evidence precision e1, and the audit evidence y1. It trades off the market price benefit against the expected misstatement costs to determine the optimal report. In choosing this optimal report, it needs to estimate the independent report rI1, which is a function of audit evidence precision e1. However, because the audit evidence precision e1 is a hidden action, the company must make a conjecture of the precision to derive the independent report. In equilibrium, the company’s conjecture of e1 is correct. (2) Given the final audited report rF1, and applying Bayes’ rule, the market price M(r) satisfies

The company and the auditor then negotiate by each proposing its preferred report (r1 and rI1 by the company and the auditor, respectively). It is assumed that the auditor’s proposed rI1, which is based on her audit evidence, is truthfully presented to the company.

7

If rI1 is greater than or equal to r1, the value proposed by the company, an agreement is reached and rI1 is issued as the final audited report (with a clean opinion), rF1. However, if rI1 is less than r1, the auditor compares the expected payoff from agreeing to report r1 with the expected payoff from insisting on reporting rI1 as the final audited report rF1. If there is no benefit from retaining the client, the auditor will report her proposed

Since the audit market is competitive in the first period, the audit fee is the auditor’s first period total audit cost minus the quasirent. The auditor chooses audit effort to minimize her total cost

Proposition 1. [Equilibrium (Benchmark)]

(i) In period 2, the final audited report is

(ii) In period 1, if the quasirent is less than β/(4 (1 − β)2), then the final audited report is

Main Analysis

In this section, we solve the equilibrium when the auditor can choose both audit effort and RB. Like in the benchmark case, in the second period, the auditor reports independently.

We next solve equilibrium in the first period. We will first analyze the company and auditor negotiation, and then the auditor’s choice of the amount of client RB, the precision e of the audit evidence (i.e., audit effort), and finally the audit fee F1.

Company-Auditor Negotiation Given RB

Similar to the benchmark case, the second period quasirent is the cost difference between the new auditor and the incumbent auditor. This rent is positive because of the RB effect in addition to the learning effect as identified in the benchmark case. Thus, the quasirent in the main analysis is higher than that under the benchmark case.

Now we move onto the auditor’s reporting decision. Compared to the benchmark case, the auditor’s expected liability given an independent report decreases due to the higher precision of audit evidence resulting from RB. At the first glance, this may in turn increase the incremental expected liability for nonindependent reporting, because holding the expected liability from nonindependent reporting constant, a reduction of the expected liability given an independent report will increase the difference between the expected liability from nonindependent reporting and that of independent reporting. The increase of incremental expected liability for nonindependent reporting will thus motivate the auditor to be less likely to report nonindependently. However, the expected liability for the nonindependent report will be reduced by the same amount because this liability consists of the squared difference between r1 and rI1 and the variance of firm value given the audit evidence. Due to the capital market’s rational expectations, r1 − rI1 remains the same and equals 1/(2 (1 − β)), while the latter component is decreased by the same amount. Therefore, the threshold value below which the auditor reports independently (β/(4 (1 − β)2)) remains unchanged. However, the quasirent with RB is higher than the quasirent without RB and RB increases the quasirent. Therefore, higher RB is more likely to induce nonindependent reporting.

We summarize the results below.

Proposition 2. [Period 1 Reporting Decision Given RB]

(i) If the quasirent is less than β/(4 (1 − β)2), then the final audited report rF1 is (ii) The auditor is more likely to accept the company proposed report given RB than given no RB.

Equilibrium Discussions

In equilibrium, when the market discounts the report and sets price equal to r1 − 1/[2 (1 − β)], the auditor and company agree with a report r1 = rI1 + 1/[2 (1 − β)]. Suppose the company deviates and would like a report

Next consider the case when the market thinks the auditor will remain independent and price the company at r1. Suppose the company deviates and would like the auditor to report

Given that the auditor’s quasirent Qm2 is less than β/[4 (1 − β)2], the auditor will be worse off if she agrees with rI1 + 1/[2 (1 − β)]. This is what sustains the market belief that the auditor will be independent and the market will accept r1 as an independent report. The auditor may deviate from the perceived report, but in equilibrium, beliefs about the auditor’s reporting choice and the actual choice must coincide (Bar-Yosef & Sarath, 2005).

Since the company utility increases by 1/[4 (1 − β)] if the market believes the audited report is an independent report, the company may attempt to persuade the auditor to accept the nonindependent report by proposing to share with her a part (γ ∈ (0, 1)) of the gain 1/[4 (1 − β)]. The auditor’s payoff will then be Qm2 + γ/[4 (1 − β)] − β/[4 (1 − β)2]. She will only accept a nonindependent report if the gain exceeds the loss, that is, Qm2 + γ/[4 (1 − β)] > β/[4 (1 − β)2]. However, we assume that l is not too large, that is,

Audit Evidence Precision and RB

Before the company-auditor negotiation, the auditor privately chooses her desired precision in collecting audit evidence and decides on the amount of RB, in anticipation of the bargaining process. In the bargaining subgame, the company makes a conjecture

Formally, the auditor chooses audit effort and RB to minimize

The benefit of higher audit effort is to obtain more-precise audit evidence about the fundamental value of the company and thus, reduce the possibility of costly misstatements. Higher precision requires a larger audit resource cost,

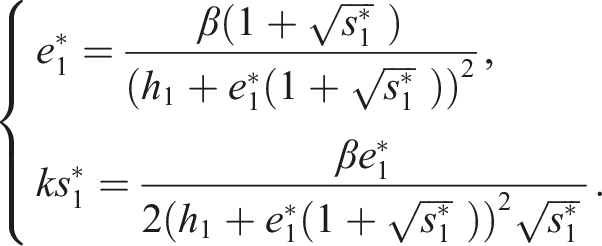

Proposition 3. [Period 1 RB and Audit Evidence Precision] The audit firm’s optimal choice of RB and evidence precision are determined by the following:

Audit Fees

In the first period, all auditors are the same, and the audit market is competitive; the auditor earns zero profit. The first-period audit fee minus the first-period audit cost plus the future quasirents should be zero, that is,

Corollary 1. [Audit Fees] The equilibrium first-period audit fee is as follows:

Comparative Statics Analysis and Implications

In this section, we analyze how RB affects the auditor’s effort and discuss regulatory and empirical implications.

Audit Evidence Precision

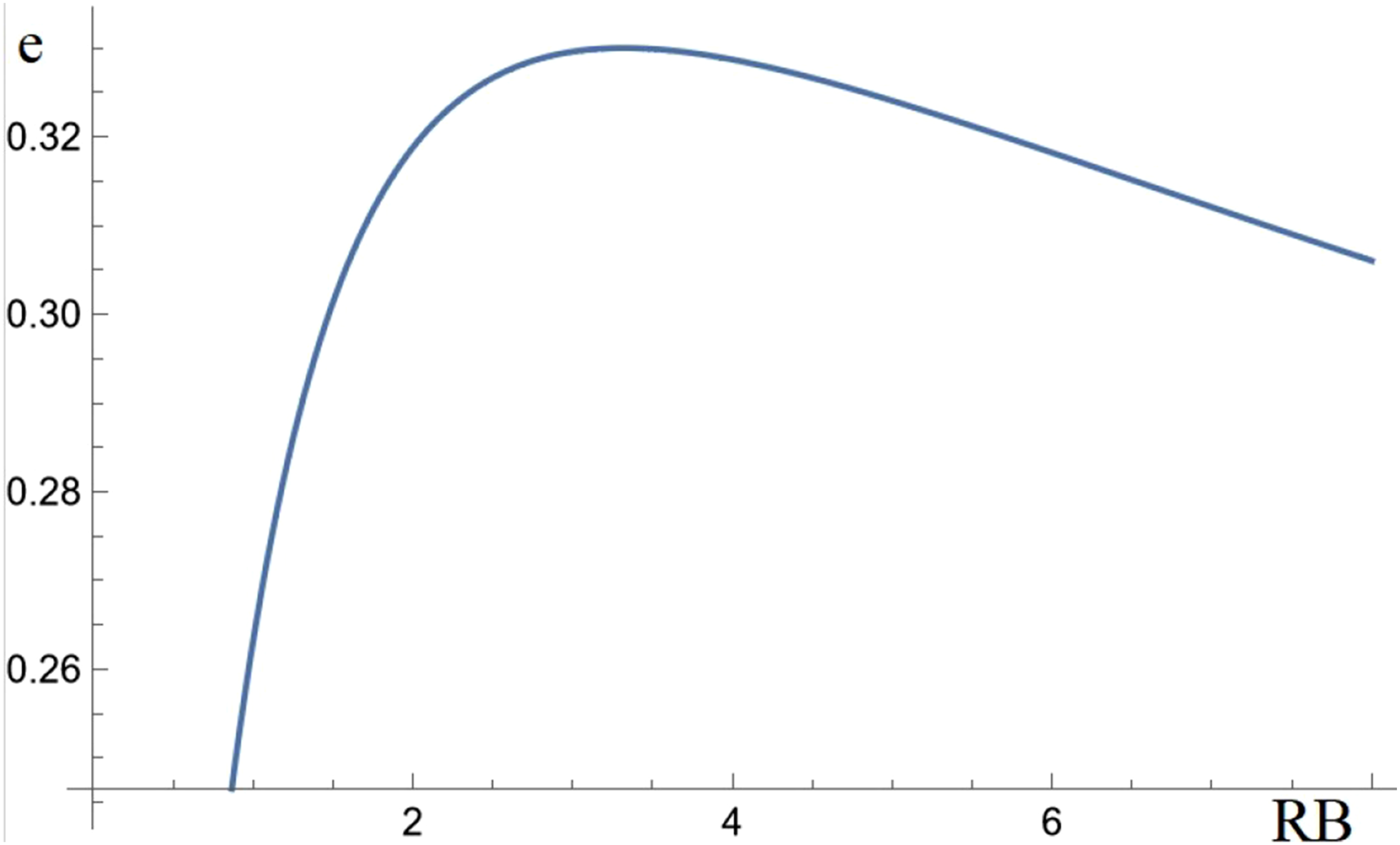

Proposition 3 shows the equilibrium audit evidence precision and RB. We now show how changes of RB (exogenously) will affect the audit evidence precision. On the one hand, it is plausible that within a good relationship, the auditor gains trust from the client and obtains more private information. Hence, RB improves the precision of the signal received by the auditor and reduces her expected liability, which reduces her incentive to exert effort. On the other hand, RB improves the usefulness of exerting effort and the auditor is then motivated to work harder. Therefore, the effect of RB on audit effort could be positive or negative and we find this relationship is nonmonotonic.

Proposition 4. [Audit Effort and RB] The relationship between audit effort and RB is nonmonotonic.

Figure 2 illustrates this relation using a numerical example. In this figure, the x-axis is RB, Audit effort and RB

This proposition can shed light on the empirical examination of auditors’ commercial effort (such as developing sales proposals, attending networking events) and professional effort (Ciconte et al., 2025). If RB effort can be proxied by commercial effort, we predict that RB first increases and then decreases professional effort.

Regulatory Policies

The above analysis shows that RB causes higher quasirent and auditors are more likely to be nonindependent than under the benchmark case without RB. To induce independent reporting, should RB be completely banned? If not, can a regulator sanction the auditor such that the net effect of RB will be positive? For example, the regulator may impose a more severe penalty on the auditor if the auditor agrees with an inflated report in the first period and engages RB in the second. 8 Exhibiting seeming lack of independence by engaging in RB in the second period in addition to the report-inflating strengthens the allegations against the auditor because the RB speaks to intent in addition to opportunity (consider the sanctions imposed by SEC on the EY partners). 9

Under this condition, the auditor will be able to commit to not engaging in RB in the second period if the company presses for a higher report (hereafter: “the commitment”). This commitment is credible because the auditor will be punished severely by the regulator for engaging in RB in the second period in combination with nonindependent reporting in the first period.

We find that the auditor’s expected payoff is higher when she makes the commitment. The company also prefers the commitment, because an independent report reduces its expected liability and the second-period RB enhances its credibility of committing to an independent report and the market price will be higher.

The proof of Proposition 2 shows that the auditor’s reporting choice is affected by the amount of quasirent, which decreases when the auditor reduces the first-period RB (Lemma 3). If the reduction of RB is so large that the quasirent becomes less than the threshold β/[4 (1 − β)2], then the auditor will behave as if she is independent. This result is consistent with the regulator’s motivation in requiring independence-in-appearance. However, further analysis shows this result may not hold for all companies. The quasirent includes the learning cost differences between the incumbent auditor and the new auditor. Large clients typically have larger learning cost, and the incumbent auditor obtains more quasirent from these clients. The reduction of quasirent due to less RB may not be large enough to drive the quasirent below the threshold. In that case a reduction of RB would actually compromise auditor independence. This is because the auditor loses the commitment device and the company loses the utility gained from RB in the second period and will not go along with a lower report. The following proposition summarizes this discussion.

Proposition 5. [Auditor Independence] Forbidding RB can reduce the likelihood of auditor independence.

This proposition highlights that quasirents resulting from RB can have a positive impact on auditor independence given that the regulator imposes severe penalty if the auditor agreed with an inflated report in the first period and built RB in the second period. The company is able to commit to truthful reporting and to gain a higher expected payoff due to the auditor’s ability to commit to discontinuing RB in the second period if the company presses for an inflated report. Note that our results do not imply that more RB is necessarily good for improving auditor independence. We emphasize that a complete ban on RB would actually impair auditor independence in companies with large quasirents, typically large companies. We suggest that selective ban on RB is a better way to improve auditor independence.

Mandatory Audit Firm Rotation

Mandatory audit firm rotation has been on the audit regulator’s agenda for a while. For example, in 2011, the PCAOB issued a concept release on auditor independence and audit firm rotation and requested public comments on this release. However, the PCAOB abandoned this project in 2014, after only a 3-year pursuit. A direct implication from the above analysis is that mandatory audit firm rotation can reduce the second period audit effort, since the new auditor will provide a lower effort than the incumbent. The informational advantage the incumbent gains from relationship-building in the first period allows her to exert more effort than the new auditor. However, mandatory rotation will eliminate the quasirent, and make auditors independent in the first period. Audit effort in the first period is not affected by this rule, as quasirent does not affect auditor effort in the first period. This is because, when the auditor chooses her effort, she is only concerned with the expected liability if reporting nonindependently. The reporting decision occurs after the effort decision. She will only accept an inflated report if the quasirent can compensate the incremental penalties resulting from an inflated report. We summarize these discussions in the following Corollary.

Corollary 2. [Mandatory rotation] Mandatory rotation can reduce audit effort in the second period. The first period audit effort is not affected, and the auditor is independent in the first period.

This corollary demonstrates that mandatory audit firm rotation is a double-edged sword. On the one hand, consistent with the PCAOB’s intention, it improves auditor independence in the first period. On the other hand, it may reduce audit effort in the second period, since the new auditor does not have informational advantage compared to the incumbent auditor. This finding complements the existing analytical literature on mandatory audit firm rotation. Lu and Sivaramakrishnan (2009) analyze the effect of mandatory rotation on companies investment decisions. Bleibtreu and Stefani (2018) extend the market matching model of Salop (1979) to an audit market and shows that client importance and audit market concentration are in direct conflict. Patterson et al. (2019) show that audit tenure reduces fraud. Dordzhieva (2022) demonstrates conditions under which mandatory rotation could actually impair auditor independence. Our analysis considers market competition, quasirent, and information differences resulting from longer tenure and client RB.

Alternative Benchmarks

In this section, we analyze two alternative benchmark cases: (1) no learning benefit (cost savings) through the first-period effort l = 0 while no RB is allowed; and (2) forbidding RB only in the first period of the engagement s1 = 0.

No RB and l = 0

Again, in the second period, there is no quasirent because the game ends. The auditor reports independently to the market, and there is no company-auditor negotiation. In contrast to the prior analyses, the incumbent and the new auditor will have the same cost in the second period since there is no learning effect resulting from the first period audit effort (l = 0) and no RB is allowed. The company is indifferent to which of the two auditors is hired in the second period and no quasirent is generated in the first period. Therefore, the auditor reports independently in the first period as well. The market price equals the audited report’s number and audit fees constitute the total audit cost. We summarize the equilibrium results in the following remark.

Remark 1

(i) In period 2, the final audited report is (ii) In period 1, the final audited report is

No RB in the First Year Engagement

In this benchmark case, instead of both s1 = 0 and s2 = 0, we examine the case where only s1 = 0. That is, rather than banning RB completely, the regulator may ban RB in the first-year audit engagement but allow RB in the second-year engagement. If the candidate auditor wins the engagement in the second period, it would be her first engagement, barring her from engaging in RB. However, if the incumbent auditor wins the second period engagement, she will be able to engage in RB as per the stipulation in the benchmark. Therefore, due to the second-period RB and the cost savings resulting from the first-period effort l learning effect, the incumbent auditor continues to enjoy the quasirent. Therefore, we obtain a similar equilibrium as in the main analysis.

Remark 2

(i) In period 2, the final audited report is (ii) In period 1, If the quasirent is less than β/[4 (1 − β)2], then the final audited report rF1 is

Moreover, allowing second period RB can still be useful in achieving auditor independence because the effect of being able to commit to no RB in the second period continues to be operative. We summarize it in the following remark.

Remark 3. Forbidding RB in the second period can reduce the likelihood of auditor independence.

Conclusion

This paper develops a theory of client RB and analyzes its impact on audit effort and auditor-client negotiation. Increasing RB may improve audit effort initially, but decrease audit effort if RB is too large. In addition, we highlight another unintended consequence: auditors are likely to be more inclined to agree to a higher report for clients with high quasirents, that is, large clients. When RB is allowed, the existence of second-period RB allows the clients to credibly commit to a truthful report. Forbidding RB removes this benefit, and clients will demand a higher report. Auditors will acquiesce to a high report when the quasirent is high. As long as there is any RB benefit enjoyed by the company, which the auditor can take away if the company disagrees with an independent report, and the regulator can impose proper penalties, our results still hold. Our theory advances the current theoretical literature on auditor independence and audit quality, and provides timely and relevant policy implications for regulators.

Footnotes

Acknowledgements

We appreciate the helpful comments by Mingcherng Deng (discussant), Aysa Dordzhieva (discussant), Steve Fortin, Jonathan Glover, Evelyn Patterson, and participants at the JAAF conference 2024, the Canadian Academic Accounting Association Annual Conference, the 13th Workshop on Accounting and Economics, and the Junior Accounting Theory Conference. We gratefully acknowledge the financial support of the Social Sciences and Humanities Research Council of Canada.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge the financial support of the Social Sciences and Humanities Research Council of Canada.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.