Abstract

This study proposes a new theoretical frame to explain intermarket differences in the follow-up firm’s market entry that determines the pioneer’s monopoly period (i.e., pioneer leadtime). The authors note that firms’ new market entry is reflective of their entry capabilities as well as entry motivations. More specifically, they argue that industry incumbency of both the pioneer and follow-up firms and product newness of the market may influence the follow-up firms’ entry capabilities and motivations, creating variance in pioneer leadtime. Their empirical findings generally support the theoretical frame and complement the conventional entry-barrier perspective. For example, for really new products, pioneer leadtime is shorter when the follow-up entrant has experiences from similar industries than when it does not. For incrementally new products, pioneer leadtime is longer when the pioneer has experiences from similar industries than when it does not.

Pioneer leadtime has appeared regularly in previous literature, as its strategic implications for competitive market entry have been noted (Cohen, Nelson, & Walsh, 2000; Levin, Klevorick, Nelson, & Winter, 1987). During the leadtime without competition, pioneers gain a temporary monopolist position, which secures higher profits than could be obtained in a competitive market (Kerin, Varadarajan, & Peterson, 1992; von Hippel, 1984), although the cost of introducing a new product can be high. A longer pioneer leadtime increases the pioneer’s advantages in terms of relative market share (Brown & Lattin, 1994; Huff & Robinson, 1994) 1 and survival rates (Robinson & Min, 2002; Shepherd, 1999). Previous studies on pioneer leadtime mainly draw on the entry-barriers perspective, focusing on the pioneer’s barrier-building capabilities and concomitant advantages (Bain, 1956; Karakaya & Stahl, 1991; Porter, 1980). In this study, we begin our discussion with real market examples that lead us to reconsider the pioneer’s capabilities in protecting a new market and extending pioneer leadtime.

In August 1993, Apple Inc. (Apple Computer at that time), a well-established industry incumbent, commercially introduced a highly innovative new product—a personal digital assistant (PDA) called the Newton. However, Apple’s monopoly did not last long. A few months later, at least three other firms introduced PDAs in the same market: Casio’s Z-7000, Sharp’s Expert Pad, and AT&T’s EO 440. Consider another example of highly innovative products—the Segway. The Segway is a two-wheeled, self-balancing transportation device commercialized by Segway Inc., a high-tech company established in 2001 without any previous industry experience in related fields. In contrast to Apple with its PDA, Segway Inc. has not confronted any substantial follow-up competitors up to this time (Sony has recently developed a similar technology but has not yet entered the market).

These examples reflect that an industry-experienced, strong pioneer (Apple Inc.) quickly faces competitors, whereas an inexperienced, small pioneer (Segway Inc.) can be free from competition for a while. How can this phenomenon be explained by the conventional view of entry barriers? The entry-barriers perspective predicts that a strong pioneer like Apple Inc. may build high entry barriers, whereas a small pioneer like Segway may not. It suggests a long monopoly period (or pioneer leadtime) for strong pioneers and a short one for small pioneers, which is contradictory to our example. An anomaly like this may suggest that pioneer leadtime and built-in entry barriers be revisited and examined through a different lens. As a response to this call, our study offers a complementary perspective to that of entry barriers to explain pioneer leadtime by incorporating follow-up entrants’ diverse entry motivations and capabilities.

While the entry-barriers perspective has provided sound theoretical basis and great opportunities for managerial applications for market entry research, its focus has been more on the pioneer’s barrier-building capabilities, and thereby a relatively limited attention to market followers’ challenging efforts and their different market entry motivations has been observed. This is an important issue as we conjecture that firms’ new product market entries are determined not only by their entry capabilities (i.e., ability to enter) but also by various motivations to enter, such as profit seeking, learning new technologies, and resource utilization (i.e., willingness to enter).

We note that the length of pioneer leadtime depends on when the potential follow-up entrants’ capabilities and entry motivations overcome the pioneer’s built-in entry barriers. In this sense, a better understanding of variations in pioneer leadtime can be obtained by adding the follower’s perspective in terms of its market entry capabilities and motivations into the existing entry-barriers view. Our study focuses on this issue and its contribution is along this line. Compared to its strategic importance, few research results so far have been reported on the follower’s view of new product market entry to explain pioneer leadtime. The most closely related research effort can be found in the studies of competitor responses to a focal firm’s strategic initiatives. These studies emphasize the capabilities and motivations of a focal firm to explain competitive dynamics among industry-incumbent firms (Aboulnasr, Narasimhan, Blair, & Chandy, 2008; Bowman & Gatignon, 1995; Chen & MacMillan, 1992).

For this study, our premise is that a follow-up firm with strong entry capability or motivation should enter the new product market faster, depending on the kind of product market it targets. Also, the pioneer’s reputation may reflect its barrier-keeping capabilities that deter follow-up entries or provide a reliable signal of the value of the new product market, again depending on what kind of product market it pioneers. With this premise, we submit that three dimensions of firm and product market characteristics, that is, (1) industry incumbency of the follow-up entrant, (2) industry incumbency of the market pioneer, 2 and (3) product newness, have an impact on pioneer leadtime. The follow-up firm’s industry incumbency, when considered together with the product newness of the market, mirrors the firm’s different levels of entry capabilities relative to entry motivations. Similarly, the pioneer’s industry incumbency, when combined with the market’s product newness, may imply the different levels and emphases of the pioneer’s barrier-keeping capabilities and reputation-based reliabilities.

The key contributions of this article are to offer a complementary view to entry barriers to explain pioneer leadtime and to provide supporting evidence that the motivation of the followers does indeed matter in the ways that could be expected, beyond the traditional view regarding barriers to entry. Any model that explains leadtime based solely on barriers to entry is likely to be incorrect due to omitted variable (e.g., entry motivation) bias. Similarly, any model that explains leadtime based only on followers’ motivation is also misspecified. In this context, we maintain that the impact of both barriers to entry and entry motivations must be analyzed to fully understand pioneer leadtime. In line with this argument and the previous market entry literature, we propose contentious hypotheses to examine the interrelated effects of the suggested three dimensions reflecting entry capabilities and motivations on pioneer leadtime. We provide empirical testing of the hypotheses using broad multi-industry data.

Theory Development and Hypotheses

Product Newness: Really New Versus Incrementally New Products

Based on recent studies by Agarwal and Bayus (2002) and by Min, Kalwani, and Robinson (2006), we note that profit- and risk-related product characteristics such as degree of product newness should affect the market entrant’s relative capabilities and motivations. We acknowledge that different ways of classifying innovations or product newness are suggested in the previous literature (cf. Garcia & Calantone, 2002; Gatignon, Tushman, Smith, & Anderson, 2002). In their comprehensive review of innovation typology and terminology, Garcia and Calantone recommended the typology of really new and incremental innovations, adding that radical innovations like the steam engine and telegraph are extremely rare. They suggest that most commercial new product innovations may belong to really new or incremental types (in this case, really new products include radical products; Garcia & Calantone, 2002, pp. 120-121). This dichotomy has been widely used by more recent studies of new product adoption (cf. Alexander, Lynch, & Wang, 2008; Herzenstein, Posavac, & Brakus, 2007) and new product survival (Min et al., 2006).

We adopt the definitions of really new and incrementally new products provided by Garcia and Calantone (2002), Min et al. (2006), and Urban, Weinberg, and Hauser (1996). Really new products are the ones that shift market structures, represent new technologies, require consumer learning, and induce behavior changes (Urban et al., 1996). They use new technologies to create new market needs (Min et al., 2006) and are often unreliable and costly when they first appear on the market (Agarwal & Bayus, 2002). Because of the high market and technological uncertainties surrounding them, really new products normally face slow customer acceptance and take a longer time to establish a technical standard or dominant product design in the market (Christensen, Suárez, & Utterback, 1998). Products like automobiles, personal computers, televisions, and jet engines are typical examples of really new products when they were first introduced (Olleros, 1986). Really new products generally entail high market and technological uncertainties and low survival opportunities (Lieberman & Montgomery, 1988; Min et al., 2006; Olleros, 1986).

In contrast, incrementally new products are designed to satisfy well-represented customer needs using an established technology base. In relation to this, Song and Montoya-Weiss (1998) clarify that an incrementally new product is introduced in the form of adaptation, refinement, and enhancement of the current product or process technologies. Incrementally new products involve much lower levels of market uncertainty because they normally provide incremental benefits to the felt market needs. Also, they carry limited technological uncertainty because the core technologies used are usually a refinement or extension of established technologies. Examples of incrementally new products include disposable mops, animal access doors, boat lights, and pickle-making machinery (Robinson & Min, 2002).

Implications of Product Newness for Follow-Up Entrants

We note that there exist ostensibly different levels of market or technological benefit expectations and uncertainties from really new products (high market expectations and risks) versus incrementally new products (low market expectations and risks; Min et al., 2006). Therefore, even with similar positions and profiles, the entry capabilities or motivations of potential followers may vary depending on the product newness of the market to enter. In the following, we discuss the logical background of our study to explain pioneer leadtime in terms of the market follower’s entry capabilities or motivations and the pioneer’s capability status, which are also influenced by the product newness of the market.

First, we assume that entry capability is the prerequisite to any new market entries for market followers. Although a follow-up firm’s entry motivation is strong, it cannot lead to actual market-entry behavior unless it is accompanied by the capabilities and resources required for entry. Therefore, for market followers, entry motivation becomes distinctive for a new market entry decision only after entry capability requirements are met. In this sense, we note that for really new product markets where superior technological and market knowledge create a major differentiating advantage and provide greater survival opportunities (Garcia & Calantone, 2002; Min et al., 2006), follow-up firms’ technological or market capabilities should be considered first to explain the interfirm differences in entry timing.

On the other hand, in incrementally new product markets, technological requirements are relatively easy to fulfill and the market demands are stable and predictable (Urban et al., 1996). In this case, the prerequisite entry capabilities will likely be more normalized across follow-up firms and will not be regarded as a major factor that determines different entry timing. Instead, follow-up firms’ entry decisions for incrementally new product markets will be more affected by their motivations, specifically based on financial profits or reasonable market share, and other entry motivations like technological learning opportunities will not be distinctive for these markets (Cohen & Levinthal, 1990; Geroski, 1995; Gort & Klepper, 1982).

Second, we note that the pioneering firm’s status may be perceived differently by market followers between really new and incrementally new product markets. In general, previous studies on entry barriers contend that a market pioneer that can establish tough entry requirements for potential followers in terms of various resources will effectively deter the follow-up firms’ new market entry (Harrigan, 1981; Karakaya & Stahl, 1989; Smiley, 1988). We agree that for market pioneers, because their barrier-related motivation is relatively self-evident and common—that is, protecting the new market from follow-up firms’ entry—their capabilities reflected by the reputation in the market or those of building and maintaining entry barriers will have greater implications for challenging market followers.

In this context, whether a capable pioneer is perceived as a reliable source of information or as a market entry deterrent will be determined, to some extent, by the product newness of the market. Specifically, we note that for really new product markets, the capable pioneer is considered more as a reliable entity to imitate than as a significant entry deterrent. For example, in uncertain and dynamic business environments like markets of really new products, because firms are not especially confident in their knowledge and ability to predict possible outcomes of specific strategic decisions, they tend to rely on information reflected by the actions of other reputable firms that move ahead of them (Bikhchandani, Hirshleifer, & Welch, 1992; Lieberman & Asaba, 2006).

Abrahamson and Rosenkopf (1997) and Haunschild and Miner (1997) also note that firms’ motivation to engage in reputation-based imitation becomes more distinctive when their strategic decisions are radical (e.g., entry into the market of a really new product), because radical decisions by nature bring about fatal impacts if they turn out to be wrong. In a similar vein, Aboulnasr et al. (2008) document that a reputable pioneer’s introduction for radical product innovation will increase (not decrease) competitive response by providing visions of market growth. Such a firm’s new market entry may also signal that firms that do not follow or respond to this firm’s behavior may eventually suffer business failure.

In contrast, pioneer capability or reputation in incrementally new product markets may not be considered as much a credible sign of market attractiveness as it is for really new product markets. This is because relatively low technological and demand uncertainties in markets of incrementally new products will provide follow-up firms with confidence in their own assessment of the expected benefits and costs from new market entry (Cohen & Levinthal, 1990). In this context, for potential market followers, capable pioneers may not be interpreted as reliable sources to imitate but, rather, as major competitors to deal with. In these incrementally new markets, technological capabilities are not a critical concern as an entry barrier; rather, the pioneers’ greater capabilities in terms of operational efficiency or cost advantage will provide considerable entry barriers to potential follow-up firms (Geroski, 1995).

In summary, the different degrees of product newness may imply different levels of relative importance between entry capabilities and motivations for market followers. In really new product markets, potential followers’ capabilities are considered a distinctively important factor required to realize their new market entry. In incrementally new product markets, on the contrary, followers’ motivations like profit expectations and benefits of resource allocations may represent a major driving force for new market entry. The product newness of markets may also reflect different aspects of pioneer capabilities perceived by market followers. For really new product markets, the pioneer’s capabilities are more linked to its credibility or reputation to rely on and provide a signal of market attractiveness, instigating follow-up firms’ new market entry. In contrast, for incrementally new product markets, the pioneer’s capabilities are perceived in terms of its manufacturing efficiency and cost economies, deterring potential followers’ new market entry. Based on these theoretical and logical underpinnings, we develop hypotheses regarding pioneer leadtime, first in the market of really new products and then in the market of incrementally new products.

Pioneer Leadtime for Really New Products

Previous research indicates that firms with prior experience from similar industries will have more chances to enter a new market by leveraging their experience or reconfiguring their accumulated market or technological knowledge and resources (Helfat & Lieberman, 2002; King & Tucci, 2002; Scott Morton, 1999). In this sense, the follow-up entrant’s status of industry incumbency (i.e., industry-incumbent follower vs. start-up early follower) may reflect its capabilities for a new product market entry. Also, as discussed above, a follow-up entrant’s entry capabilities represent a more critical factor than other factors to market entry decisions for really new product markets.

Facing these environmental uncertainties and potential financial risks, firms in markets of really new products should be well equipped with capabilities based on diverse forms of resources for new market entry; otherwise, their survival opportunities will be minimal (Min et al., 2006). In relation to this, experienced followers may have more diverse resources than do start-up followers in terms of, for example, distribution channels built on existing products, multipurpose production equipment, and multifunctional management skills that can help overcome entry barriers in the markets of really new products (Helfat & Lieberman, 2002; Mitchell, 1991; Teece, 1986). These capabilities so far discussed will provide industry-incumbent (as opposed to start-up) followers with greater opportunities for early market entry into markets of really new products. Therefore we hypothesize:

Hypothesis 1a: In markets of really new products, pioneer leadtime is shorter when a follow-up entrant is an industry-incumbent firm than when it is a start-up firm.

Previous discussion posits that pioneer capability status in really new product markets represents a reliable market entity and information source that indicates attractive new markets for potential market followers. As a firm’s level of specific knowledge and reputation usually depend on its related industry experiences and merits (Helfat & Lieberman, 2002), experienced pioneers are more likely than start-up pioneers to act as a reliable signal of the value of entry in markets of really new products.

This expectation might not be based on the conventional entry-barrier perspective (e.g., Porter, 1980), which supports early market entry of follow-up firms that face a relatively less competent pioneer. In this context, we would propose that in markets of really new products, follow-up entrants will be more motivated to imitate a capable, industry-experienced pioneer than they will an inexperienced pioneer, and they are more willing to enter a new market pioneered by an industry-experienced firm. This argument leads to a faster market entry of follow-up entrants that confront the industry-incumbent pioneer.

Hypothesis 1b: In markets of really new products, pioneer leadtime is shorter when the market pioneer is an industry-incumbent firm than when it is a start-up firm.

Pioneer Leadtime for Incrementally New Products

As noted earlier, in incrementally new product markets, follow-up firms’ entry motivations such as new-market profit potentials and the efficient use of existing resources will be the most important factors influencing their market entry decisions. In relation to this, industry-incumbent (as compared to start-up) market followers, because of their relatively ample knowledge about different market alternatives and entry requirements, will be able to perform extensive profit–cost analyses with diverse resource allocation plans. For example, chances of low profits or extra expenses accompanied by a specific incremental product market entry may be more comprehensively examined by industry-incumbent firms than by start-up firms. Such a conservative decision-making process in industry-incumbent followers may delay their market entry.

On the other hand, start-up entrants may not be disadvantaged much by lack of resources for an incremental market entry. On top of that, compared to industry-incumbent firms, start-ups will have relatively less psychological burden in terms of resource allocation decisions because they do not have complicated resource portfolios for the current new market entry. This impact could also be observed for markets of really new products, but it might have been overridden by serious technological requirements that provide more tension to start-up followers in markets of really new products.

In summary, industry-incumbent followers’ resources and capabilities may enable their early market entry. But at the same time, we contend that their early entry motivation is rather low and their technological capabilities are not a significantly differentiating factor in markets of incrementally new products. While it is more likely an empirical question, we put forward a challenging hypothesis by arguing for the experienced follow-up entrants’ relatively slow market entry based on their low early entry motivation.

Hypothesis 2a: In markets of incrementally new products, pioneer leadtime is longer when a follow-up entrant is an industry-incumbent firm than when it is a start-up firm.

We discussed above that in incrementally new product markets, pioneer capabilities based on manufacturing efficiency and low operating or transaction costs form major entry barriers to potential market followers. In relation to this, experienced pioneers in incrementally new product markets have more diverse resources and generic capabilities compared to start-up pioneers in terms of, for example, multifunctional manufacturing processes, general transaction skills, and established distribution systems (Geroski, 1995). Therefore, potential follow-up firms will be more willing and able to join the new market created by a start-up pioneer than by an industry-incumbent pioneer, because they hope to maximize the utility of their specialized resources and assets without the pressure of having to cope with a generally well-equipped, competent pioneer.

Also, if industry-incumbent pioneers promptly achieve large-scale production with their manufacturing skills accumulated from previous experience, following entrants may have to operate at a suboptimal scale, as market demand is limited (Geroski & Mazzucato, 2001). Such subscale operations will decrease follow-up firms’ expected profits and therefore reduce their profit-based entry motivation for markets of incrementally new products (Lieberman, 1989; Robinson & McDougall, 2001). In contrast, follow-up firms may enjoy time to increase production efficiency and get scale economy before a start-up pioneer fully establishes its pioneer advantage in terms of production cost-efficiency (Debruyne & Reibstein, 2005; King & Tucci, 2002; Tyagi, 2000). Based on the discussions above, we expect that follow-up entrants have greater motivation to enter the start-up pioneer’s market than the industry-incumbent pioneer’s market, causing them to enter the start-up pioneer’s market faster. We submit:

Hypothesis 2b: In markets of incrementally new products, pioneer leadtime is longer when the market pioneer is an industry-incumbent firm than when it is a start-up firm.

Pioneer Leadtime for Really New Products Versus Incrementally New Products

One of the ongoing but yet-to-be-validated discussions in entry literature pertains to whether markets of really new products or incrementally new products attract follow-up entries earlier. A tacit assumption of previous studies suggests that firms tend to delay market entry more for really new products than for incrementally new products because the firms confront higher demand uncertainty and greater technological barriers (Levin et al., 1987; MacMillan, McCaffery, & van Wijk, 1985). Regarding technological barriers faced by follow-up entrants, Levin et al. argue that duplicating major innovations incurs more costs and takes more time than duplicating incremental innovations, so the innovator’s leadtime should be longer for major innovation markets (i.e., markets of really new products). This view is also consistent with the entry-barriers perspective, which asserts that a market environment of great technological changes significantly deters follow-up entries, as it accompanies large technological investments and capital requirements from potential entrants (Bain, 1956; Reinganum, 1983).

On the other hand, authors of other studies argue that higher expected postentry profits actually motivate firms’ new market entry, and although really new products such as personal computers and transistors are costly to develop and difficult to imitate, they have greater profit potentials than do incrementally new products (Cohen & Levinthal, 1990; Geroski, 1995; Gort & Klepper, 1982). Specifically, in modern industries where the radical technology-based premiums bring about competitive superiority and greater chances of commercial success, really new products may attract more attention from both industry-experienced and start-up firms (Gatignon et al., 2002; Lee, Smith, & Grimm, 2003). In addition, technological diversity based on really new products (e.g., various application opportunities of semiconductors) plays an important role in attracting follow-up entrants that hope to achieve future business diversification (Holbrook, Cohen, Hounshell, & Klepper, 2000). In this regard, Cohen and Levinthal further argue that large technological spillovers, which are more typical of high-technology or really new products, provide strong incentives for a potential entrant to follow the pioneer for the purpose of exploiting these spillovers.

In summary, there is a prevalent prediction of longer pioneer leadtime for really new products than for incrementally new products. However, there is also growing evidence that implies a shorter pioneer leadtime for really new products than for incrementally new products. What contributes to these inconclusive, contrasting predictions? Are pioneer leadtimes shorter or longer for really new products than for incrementally new products? Based on our previous argument—pioneer leadtime depends on the incumbency of market pioneer and follow-up entrant—we propose that the comparison of pioneer leadtime between really new and incrementally new products should control for the incumbency of market pioneer and follow-up entrant. For example, for markets of really new products, the pioneer leadtime will be shorter when market pioneer and follow-up entrant are industry incumbents than when they are start-up firms (Hypotheses 1a and 1b). Also, for markets of incrementally new products, the leadtime will be longer when market pioneer and follow-up entrant are industry incumbents than when they are start-up firms (Hypotheses 2a and 2b). Seeing these four hypotheses, we may conjecture that pioneer leadtime will be shorter for really new products than for incrementally new products when both market pioneer and follow-up entrant are industry incumbents. The predictions based on our hypotheses are summarized in Table 1. Although there are four combinations of industry incumbency of market pioneer and follow-up entrant (2 × 2) that should be considered, we build hypotheses for two distinctive cases of incumbent pioneer, incumbent follower and start-up pioneer, start-up follower in which the predictions are clearly opposite. General interpretations of interaction effects between the market entrants’ industry incumbency and product newness are provided in the Discussion section.

Predictions of the Length of Pioneer Leadtime

First, consider the case of markets of new products where both pioneer and follower are industry incumbents. Our study submits that, in markets of really new products, potential entrants tend to interpret such a credible pioneer’s (e.g., the industry-incumbent pioneer’s) market entry as encouraging information or a signal of the existence of great potential benefits (monetary or nonmonetary, as discussed above) for the new market. Furthermore, based on the view of entry barriers, an industry-experienced follower equipped with related industry knowledge and resources may overcome the high market entry barriers of really new products more easily than can a start-up follower. Thus, as long as both pioneers and followers have great capabilities for a new product market entry (e.g., both are industry-incumbent firms), really new products provide greater entry motivations for the followers than do incrementally new products so that the pioneer leadtime for really new products will be shorter than for incrementally new products. Also, in a market for an incrementally new product, an industry-incumbent pioneer may effectively build entry barriers based on cost advantages, while an industry-incumbent follower is often less motivated to enter because of possible negative impact on its product portfolio (e.g., cannibalization) and low potential profits from the new product. We formally submit:

Hypothesis 3a: Pioneer leadtime is shorter for really new products than for incrementally new products when both the market pioneer and follow-up entrant are industry incumbents.

On the other hand, when both the market pioneer and follow-up entrant are start-up firms, we expect a longer pioneer leadtime for really new products than for incrementally new products. When the market pioneer is not reputed in the related industries (e.g., start-up pioneer) and therefore its entrance into the new product market is not necessarily a reliable signal of a profitable market, market followers will be more concerned about the potential risks than about the benefits expected from the new product market. It would be even more so for inexperienced market followers (e.g., start-up followers). In this case of a lack of reliable market information, really new products normally imply more risks, so start-up followers will take more time in making entry decisions into markets of really new products than into markets of incrementally new products. Furthermore, start-up entrants that attempt to enter the market of a really new product have to overcome higher technological or R&D entry barriers than do start-up entrants that enter a market of incrementally new product. Therefore, when both the market pioneer and follow-up entrant are start-ups, we expect that pioneer leadtime is longer for really new products than for incrementally new products. We formally submit:

Hypothesis 3b: Pioneer leadtime is longer for really new products than for incrementally new products when both the market pioneer and follow-up entrant are start-up firms.

We leave the other two cases—start-up follower versus incumbent pioneer and incumbent follower versus start-up pioneer—as empirical questions. This is because the predictions based on our previous argument are rather inconclusive for these two cases. For example, consider the market contingency of start-up follower versus industry-incumbent pioneer. For start-up follower, our predictions are a longer leadtime for really new products (Hypothesis 1a) and a shorter leadtime for incrementally new products (Hypothesis 2a). However, for an industry-incumbent pioneer, we expect a shorter leadtime for really new products (Hypothesis 1b) and a longer leadtime for incrementally new products (Hypothesis 2b). Consequently, for one specific market situation composed of start-up follower and industry-incumbent pioneer, the two prediction results do not converge and even could be opposite to each other, allowing no logical conjecture on this type of contingencies.

Method

Data, Measures, and Sample Description

We use data from numerous editions of the Thomas Register of American Manufacturers to identify new products and to measure pioneer leadtime for each of the new products launched in the 1960s, 1970s, 1980s, and 1990s. The Thomas Register is an annually published national buying guide encompassing a wide range of the products manufactured in the United States. Since its first annual edition in 1905, it has become the most comprehensive directory for American manufacturers and their products. Its 2003 edition, for example, contains information about 173,000 firms and more than 65,000 product categories. Compared to other sources of data, the Thomas Register has unique merits in that it clearly delineates product market boundaries to help potential buyers find a product by grouping product categories from the buyer’s perspective. In this sense, the Thomas Register reveals “consumer-driven” product market structure rather than a firm’s subjective interpretation of it. Relative to its comprehensive coverage of multiple industries’ product market information, the Thomas Register takes a conservative position in listing market entry. It lists a new entrant only when a firm commercially introduces a product at the level of regional markets or above. For these reasons among others, the Thomas Register data have been used in many academic studies pertaining to the dynamics of industry and product market evolution and firm entries and exits (cf. Agarwal, 1996, 1997; Agarwal & Bayus, 2002; Agarwal & Gort, 1996, 2001; Gort & Klepper, 1982; Min et al., 2006).

New products were identified by comparing various annual editions of the Thomas Register from the 1960s to the 1990s in storage at a university library. Product headings are listed in alphabetical order in the product sections of the Thomas Register. Thus, in order to obtain a random sample of new products, product headings of a specific year were compared with those of previous years’ editions in alphabetical order. The first year a product is listed in the Thomas Register was identified by comparing the annual editions of the Thomas Register over the years. Furthermore, the years for which the annual editions compared were constantly switched from the 1960s to the 1970s, 1980s, 1990s and back to the 1960s in order to obtain fairly distributed sample across the decades. This random selection covered products whose first letter begins with A through W, such as “Absorptometers” and “Washers: Fiberglass.” Because only a few service markets were identified, we excluded those from the sample. Therefore, our sample includes only market entrants for manufactured goods. Table 2 describes the sample in terms of two-digit standard industrial classification (SIC) codes. The sample covers most of the manufacturing industries in the United States. Reflecting the important portions of the U.S. manufacturing businesses, Machinery and Computer Equipment (SIC code 35), Electronic and Electrical Equipment (SIC code 36), and Measuring, Analyzing, and Controlling Equipment (SIC code 38) markets comprise 28%, 14%, and 16% of the sample, respectively.

Sample by Two-Digit Standard Industrial Classification (SIC) Code

Market pioneer is defined as the first firm that enters a new market in the year of its market inception (Schmalensee, 1982; Urban, Carter, Gaskin, & Mucha, 1986). Accordingly, it should be identified as the unique entrant in the first year the product is listed in the Thomas Register. Each new market is traced forward to identify the second entrant, which we call, along with others that entered in the same year, follow-up entrants. The final sample includes 264 new products with 264 unique market pioneers and 486 follow-up entrants. 3 Pioneer leadtime, the duration in years between the pioneer’s entry and the follow-up entrant’s entry, is measured for each product market.

Whether a specific market entrant is an industry incumbent or start-up is identified by examining the annual records of company profile sections from the Thomas Register. A market entrant represents an industry-incumbent entrant if it is listed in the Thomas Register in the years prior to its current market entry and the description of its previous business covers the same industry boundary as that of its current new market in terms of two-digit SIC code levels. A start-up entrant is identified by finding that the company has never appeared before the year of its current market entry in the Thomas Register’s company profile section or that, although it has, the business description of the company’s prior market industry does not overlap with the industry boundary of the currently entered product market in terms of two-digit SIC code levels.

Expert survey was used to classify products into really new versus incrementally new products, following the definitions of Garcia and Calantone (2002), Min et al. (2006), and Urban et al. (1996) previously discussed (i.e., the former shifts market structures, represents new technologies, requires consumer learning, and induces behavior changes, whereas the latter satisfies a felt market need and uses or refines currently available technology). Thirty-nine industry and research experts evaluated 264 product categories related to their own expertise and identified a specific category as a really new versus incrementally new product at the point in time at which it was first commercially introduced. To establish the internal consistency of the experts’ ratings across different product categories (i.e., to control for the individual expert’s bias of consistently low or high ratings for the degree of product newness), some well-known really new products verified from prior research were provided to serve as benchmarks. The average score of these well-known really new products was calculated for each expert as his or her benchmark score. For each expert, a specific product was considered a really new product when the raw score given to the product was greater than or equal to that expert’s benchmark score. Final category classification was based on the majority agreement for each of the given products, yielding 66 really new products and 198 incrementally new products. Really new products include the laser mirror, radar detector, parylene, microfilm, reader-printer, video tape motion analysis system, and so on. Incrementally new products include the prefabricated chimney, air-operated door, magnifying lamp, boat loader, and snow melting mat, among others.

We analyze the follower sample (N = 486) instead of the market pioneer sample to measure pioneer leadtime because testing our hypotheses requires dyadic information—that is, the status of industry incumbency of the market pioneer and the follow-up entrants for each pioneer leadtime. All the pioneer–follower relationships are based on unique pairs, except for six relationships that involve the same pairs of firms in four different industries. Since the sample data come from the early 1960s to the mid-1990s, all of the observations have complete spells. In addition to our main explanatory dimensions—the market entrants’ industry incumbency and pioneer or follower status—other factors may also have an impact on pioneer leadtime. To test the suggested hypotheses of our study and analyze the net effects of industry incumbency and pioneer or follower contingencies, we should control for other factors that might affect pioneer leadtime. We deal with this by introducing several control variables in the next section while discussing model specification.

Model Specification

We specify a regression model for each of the really new and incrementally new product samples, as follows:

where i indicates a specific product market, and ε i is a disturbance term. We take a natural logarithm of pioneer leadtime, as our model estimation uses right-skewed time duration data. For about 90% of the products, the pioneer leadtime is less than 5 years, while for just a few products, pioneer leadtime extends to 9 to 10 years in our data. A log transformation of data stabilizes the variance of this type of skewed dependent variable by making right-skewed data into more symmetrical ones distributed around zero (usually creating a normal distribution; Mosteller & Tukey, 1977). Industry-incumbent follower is a dummy variable indicating an industry-incumbent follow-up entrant. The industry-incumbent pioneer variable is also a dummy variable for an industry-incumbent market pioneer. The estimate of β1 enables us to test Hypotheses 1a and 2a, and β2 tests Hypotheses 1b and 2b. In Table 3, we feature the definitions and descriptive statistics of the variables we use in the regression analyses for both types of markets.

Variable Definitions and Descriptive Statistics

Note: The reported statistics are mean values; standard errors are in parentheses.

p < .01.

As discussed above, we control for four other factors that might affect the pioneer leadtime as in the following. We expect calendar year market started to reduce pioneer leadtime, partly because of the easier transfer of knowledge and skills for recent years as a result of increased mobility of skilled labor, rapid diffusion of technical information through research publications, greater access to plant tours, and increased reverse engineering (Agarwal & Gort, 2001; Chandler, 1990). Utterback (1994) also observes relatively long leadtimes in older markets, such as typewriters and electric lights, and relatively short leadtimes in younger markets, such as transistors and electronic calculators. Product patent effectiveness should increase the innovator’s monopoly, resulting in longer pioneer leadtime. Levin et al. (1987) report that only 6% of patented products (relative to 19% of unpatented products) could be duplicated within one year. For typical new products, 34% of patented products compared with 66% of unpatented products could be duplicated within one year. Because the Thomas Register sample includes various manufacturing industries (e.g., chemicals, machinery, electronics, instruments), the effectiveness of patent production varies. We obtain product patent effectiveness for each industry from Levin et al.’s survey results; in their study, respondents evaluated their industries’ patent effectiveness on a scale of 1 to 7.

Higher industry capital intensity (i.e., industry fixed asset-to-sales ratio) should increase pioneer leadtime because the barrier to entry imposed by capital requirements should become stronger as the volume of capital requirements increases. Scale economies are important to market entry, not only because the supply of a significant fraction of industry output is required for efficiency but also because large absolute capital investments are necessary. Such high sunk costs demanded for market entry can be a serious entry barrier in capital-intensive markets. High industry R&D intensity (greater R&D activities) results in more innovations that bring in diverse technologies and trajectories to the industry (Dosi, 1982). These various technology learning opportunities may attract potential entrants’ market entries (Gort & Klepper, 1982), reducing pioneer leadtime. Holbrook et al. (2000) empirically show that technological diversity in the semiconductor industry played an important role in its rapid evolution. To measure R&D intensity, we use the annual survey results of industry R&D performance provided by the National Science Foundation.

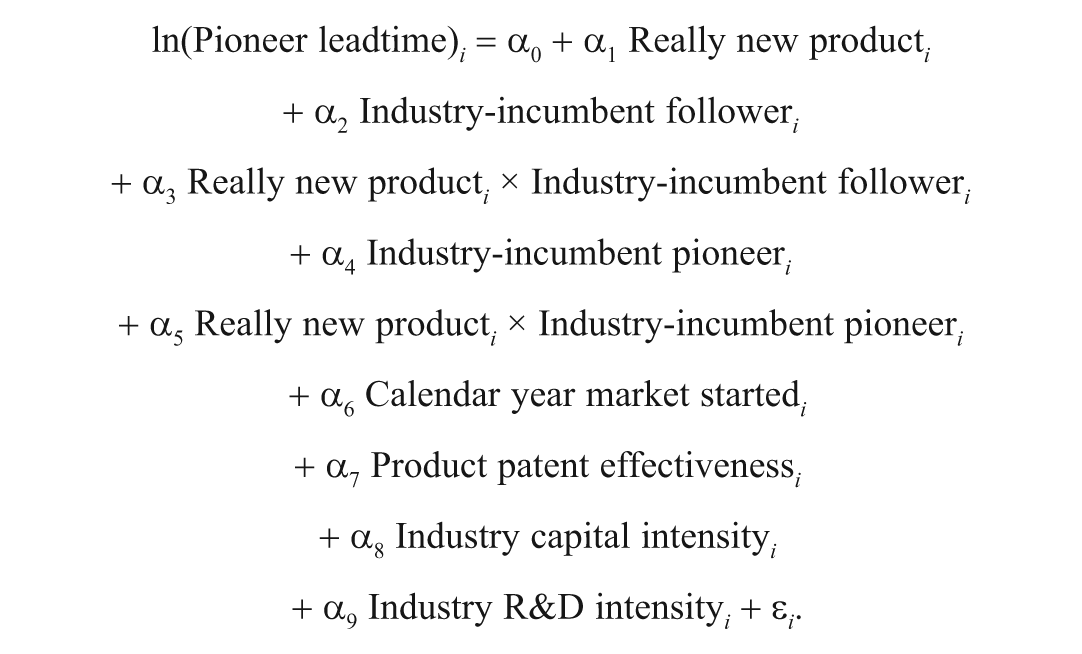

To compare pioneer leadtime across the two types of product markets (Hypotheses 3a and 3b), we specify a pooled-sample regression model for each product market i as follows:

Equation 2 thus adds three new dummy variables to Equation 1: one for really new product and two for the interactions of really new product with industry-incumbent follower and industry-incumbent pioneer. To test Hypothesis 3a, we estimate Equation 2, assuming that the market pioneer and follow-up entrant are industry incumbents (i.e., α3 = α5 = 1). Thus, a negative estimate of α1 + α3 + α5 would support Hypothesis 3a and suggest that a shorter pioneer leadtime occurs for really new products compared with incrementally new products when both the market pioneer and follow-up entrant are industry incumbents. For the test of Hypothesis 3b, comparison of pioneer leadtime between really new products and incrementally new products when both the market pioneer and follow-up entrant are start-ups (i.e., α3 = α5 = 0), we check the coefficient estimate of α1. A positive sign of α1 estimate will support Hypothesis 3b.

For the test of the hypotheses we use the matched sample of 486 pairs of pioneers and follow-up entrants instead of the 264-pioneer sample. The 486-pair sample is obtained because we take the followers’ perspectives to analyze pioneer leadtime, and there are quite a few product markets with multiple follow-up entrants that have the same leadtime in our Thomas Register data. About 47% of 264 product markets listed multiple follow-up entrants. On average, therefore, there are 1.84 (= 486/264) follow-up entrants for one product market in our data. If one product market has multiple observations, there may be a problem to take care of because one observation (i.e., pioneer leadtime) would be counted as many times as the number of follow-up entrants in that specific market. In this case, a conventional regression estimation such as ordinary least squares estimation would yield biased estimates by overly reflecting those markets that have multiple follow-up entrants. Because of this potential problem, we have adopted weighted least squares to estimate the parameters with the inverse weight of the number of follow-up entrants. For instance, if one market has three follow-up entrants, we give each pair of the observation one-third weight to estimate the parameter coefficients so that the concerned market is weighted equally with other product markets.

Findings

We provide the estimation results from the regression analyses based on two separate market samples (really new and incrementally new products) in Table 4.

Weighted Regression Results for Separate Samples

Note: The t-statistics are reported in parentheses. The dependent variable is the natural logarithm of pioneer leadtime.

p <.10; **p <.05; ***p <.01.

For the really new product sample, the negative and significant coefficient of industry-incumbent follower (−0.31, p < .01) indicates that industry-incumbent followers provide shorter pioneer leadtimes than do start-up followers, in support of Hypothesis 1a. The coefficient of industry-incumbent pioneer, which is negative and marginally significant (−0.17, p < .10), also reflects that pioneer leadtime is shorter with an industry-incumbent pioneer than with a start-up pioneer, marginally supporting Hypothesis 1b at the .10 level.

For the incrementally new product sample, we find a significant positive coefficient for industry-incumbent pioneer (0.19, p < .05), which indicates that pioneer leadtime is longer for an industry-incumbent pioneer than for a start-up pioneer in incrementally new product markets. The coefficient for industry-incumbent follower is not statistically significant. Therefore, Hypothesis 2b receives support, but Hypothesis 2a does not. A possible reason for this insignificant test result in the case of Hypothesis 2a is that industry-incumbent followers’ conservative entry decision process makes them delay new market entry, but at the same time their diverse entry capabilities help them enter quickly. These two contrasting forces that affect industry-incumbent followers’ market entry may have neutralized the total impact on their early entry decision.

We report the estimation results from the pooled sample regression in Table 5. The estimation results without industry incumbency variables are reported in the first column (I). The coefficient estimate for a dummy variable of really new product is significantly negative (−0.18, p < .05), which is a consistent result with the preliminary mean comparison in Table 3. However, these results do not take into account the effects of industry incumbencies. The hypothesis testing for Hypotheses 3a and 3b requires us to control for industry incumbency of market pioneers and follow-up entrants. The second column (II) of Table 5 adds two interaction effects of industry experience variables. For the case when both the market pioneer and follow-up entrant are industry incumbents, the difference in pioneer leadtime between really new and incrementally new products is measured by (0.30) + (−0.27 × Industry-incumbent follower) + (−0.42 × Industry-incumbent pioneer), which is −0.39 (p < .01), showing that the pioneer leadtime for really new products is shorter than that for incrementally new products. This result supports Hypothesis 3a. On the other hand, the positive coefficient of really new product (0.30, p < .10) indicates that the pioneer leadtime for really new products is longer than that for incrementally new products when both the pioneer and follow-up entrant are start-ups. Therefore, Hypothesis 3b is also supported at .10 level. For the case of (a) start-up follower and industry-incumbent pioneer, and (b) industry-incumbent follower and start-up pioneer, the pioneer leadtime differentials between really new products over incrementally new products are −0.12 (= 0.30 − 0.42) and 0.03 (= 0.30 − 0.27), respectively. As we discussed in the previous section, neither of these two cases provides significant empirical results.

Weighted Regression Results for the Pooled Sample (n = 486)

Note: The t-statistics are reported in parentheses. The dependent variable is the natural logarithm of pioneer leadtime.

p <.10; **>p <.05; ***p <.01.

From the regression results in Tables 4 and 5, we note that all the control factors are significant in explaining pioneer leadtime except for industry R&D intensity. Possibly the most influential control variable is calendar year market started. Our empirical results of negative impact of this variable on pioneer leadtime thus show that pioneer leadtime has shortened from the 1960s to the 1990s, consistent with the study by Agarwal and Gort (2001). We also empirically confirm that the industries of high capital intensity and those in which patent protection is effective tend to experience longer pioneer leadtime. This result is consistent with the theory of entry barriers.

Discussion and Conclusion

Although frequent interfirm knowledge transfer is currently possible based on the development of communications technology, entry barriers still persist and the pioneer advantages remain distinctive. For example, firms’ new market entry is often found to be a difficult and challenging task because the introduction of a new product requires nontrivial commercialization efforts—for example, trials of pilot plants or a full-scale marketing of the new product beyond test markets—even after a technological completion of the new product (Mansfield & Wagner, 1975).

Despite its theoretical and managerial contributions to a comprehensive understanding of a firm’s new market entry behaviors, previous entry-barrier research mainly focused on the pioneer’s capabilities to maintain its built-in market advantages and market dominance (Huff & Robinson, 1994; Kerin et al., 1992; Lieberman & Montgomery, 1988). Consequently, the capabilities and various motivations of the pioneer’s counterpart—follow-up entrants—for new market entry have been rarely examined. Our study suggests a complementary view to conventional entry barriers and analyzes pioneer leadtime from the follow-up market entrant’s point of view. More specifically, this study intends to provide contributions to the existing literature in terms of the following.

First, we suggest that the potential new market entrants’ industry incumbency (industry-incumbent vs. start-up firms) and the product newness of target market (really new vs. incrementally new products) relate to their varying entry capabilities and motivations. We provide a theoretical basis for this argument by integrating well-developed theories in previous literature pertaining to firms’ resource capabilities (Helfat & Lieberman, 2002; Mitchell, 1991), motivations for imitation (Lieberman & Asaba, 2006), market protection (King & Tucci, 2002), and profit expectations (Gort & Klepper, 1982), as well as theories related to entry barriers (cf. Karakaya & Stahl, 1989). In this logic, our study takes the follower’s perspective instead of the pioneer’s and emphasizes the interaction of the follower’s industry incumbency and product newness that affects its capabilities and motivations for a new product market entry. This view is considered to complement the conventional view of entry barriers that focuses on the pioneer’s barrier-building and -maintaining capabilities as discussed above. It is therefore noted that analyzing only firms’ industry incumbency (i.e., without considering product newness) may create misleading interpretations about the impact of industry incumbency on follow-up market entry.

Second, we submit that a follow-up firm’s entry capabilities are the prerequisite to its new product market entry, which is consistent with a view of entry barriers. A follow-up firm’s entry decision may depend on its entry motivations like expected new market benefits if the required entry capabilities are rather homogeneous or easily obtained and therefore no longer a major concern among competing firms. With this theoretical background, we put forward hypotheses regarding pioneer leadtime based on a conceptual scheme that a follow-up firm’s capabilities and motivations, as well as the relative emphasis between these two, are influenced by the firm’s industry incumbency and the product newness of the newly entered market.

Finally, but no less important, we demonstrate that pioneer capabilities or status may be interpreted differently by potential market followers depending on the market situation. According to the view of entry barriers, the established market status or great capabilities of the pioneering firm are regarded as a formidable entry barrier. But on the other hand, we note that they could also be perceived as a signal of new market attractiveness for follow-up entrants. Again, we provide and empirically validate hypotheses based on our understanding that such different perceptions of pioneer capabilities or statuses are affected by the product newness of the new market. For really new products, the pioneer’s capabilities or reliable status reflected by industry incumbency encourages imitation by followers and motivates their market entry. For incrementally new products, as technological capabilities or uncertainties are not a major concern, the pioneer’s capabilities based on operational superiority may work as a barrier to follow-up entrants.

Managerial Implications

This study offers several implications for firms that engage in new product development and market entry. First, it provides more insight for an important strategic dimension, industry incumbency, which may contribute to efforts to manage relative market competitiveness. Because pioneer leadtime is closely related to the sustainability of pioneer competitive advantage, managerial focus previously has centered on the order-of-entry dimension. This study indicates that the existence of market entrants’ prior industry experience is a significant strategic factor that affects market competitiveness for both market pioneers and followers.

Second, the current study helps explain intense competition among industry-experienced entrants for really new products. Such competition deserves more attention because of the increasing number of experienced competitors that develop and introduce really new products for new markets (Geroski, 1995). Anecdotal evidences about such entry-based competition are observed. After Sony launched its first e-book reader—the Sony Reader—in 2006, Amazon.com followed immediately by introducing its own e-book device brand—the Amazon Kindle. Similarly, just after Apple’s iPhone was introduced in summer 2007, industry-experienced firms including LG and Samsung rushed into the market. These cases reflect that competing firms with prior industry experience monitor one another’s innovation activities (Debruyne & Reibstein, 2005). They may have strong monetary and nonmonetary motivations and capabilities to join new businesses when competitors successfully pioneer really new product markets.

Limitations and Future Research

This study is not free from limitations. First, the logic behind our suggested hypotheses is that the three explanatory dimensions of entrant and product characteristics—entry status, industry incumbency status, and product newness—reflect different types or levels of entry capabilities and motivations, which eventually cause variations in the follower’s market entry. Although this logic is built on and complements the well-established view of entry barriers and the empirical results support the logic, the current study has not provided direct measures of entry capabilities and motivations. Future research efforts to deal with this issue are warranted.

Second, this study treats pioneering as an extraneous (or given) event and focuses on follow-up entrants’ entry capabilities and motivations without considering pioneers’ entry. The concepts of entry capabilities and motivations can be applied to market pioneers as well. Although most existing studies investigate the pioneer’s resource profile (e.g., Robinson, Fornell, & Sullivan, 1992), only a few uncover its entry motivations, such as expectation of high probability of postentry survival (e.g., Christensen et al., 1998). Additional studies should include both entry capabilities and entry motivations of market pioneers to explain their entry timing.

Third, this study uses a proxy measure for patent effectiveness. Due to the lack of data availability, we use the survey measures by Levin et al. (1987). Future studies could use more comprehensive data that include the pricing policies of market pioneers and the patent effectiveness of new products. Similarly, the measures of R&D intensity and capital intensity in this study are based on the two- and four-digit SIC codes of industry classification, respectively, for the year of the new market’s inception. Although this type of industry measure is normally accepted for industry research (e.g., Dosi, 1982), survey-based data collected at the firm level will provide more direct and useful information on the level of firm resources.

Fourth, further research could investigate a firm’s entry capabilities and motivations with a microlevel approach and analyze the firm’s intraorganizational dynamics for market-entry decisions. Existing motivation theories for individual behaviors, including governance pattern and power structures, might be applied to studies on a firm’s entry motivation. Related to this, Chen, Su, and Tsai (2007) suggest the perceptions and opinions of corporate executives as one of the unexplored critical issues in competitive dynamic research (p. 103). Combining inter- and intrafirm aspects of entry capabilities and motivations could provide more comprehensive explanations of a firm’s competitive market entry decision.

Footnotes

Acknowledgements

This article was accepted under the editorship of Talya N. Bauer. We thank Manu Kalwani, Bill Robinson, Gerard Tellis, Rajesh Chandy, Peter Golder, the associate editor, and the two anonymous reviewers for their insightful comments on previous versions of this article. The first author acknowledges the research support of the Hong Kong Polytechnic University’s Central Research Grant (G-YH76).