Abstract

Foreign subsidiaries in multinational corporations (MNCs) possess knowledge that has different sources (e.g., the firm itself or various sources in the environment). How such sources influence knowledge transfer is not well understood. Drawing on the “accommodation effect” from cognitive psychology, the authors argue that accumulation of externally sourced knowledge in a subsidiary may reduce the value of transferring that subsidiary’s knowledge to other parts of the MNC. The authors develop a parsimonious model of intrafirm knowledge transfer and test its predictions against a unique data set on subsidiary knowledge development that includes the sources of subsidiary knowledge and the extent of knowledge transfer to other MNC units. The authors show that a high level of externally sourced knowledge in a subsidiary is associated with a high level of knowledge transfer from that subsidiary only if a certain tipping point of internally sourced knowledge has been surpassed. This suggests that subsidiary knowledge stocks that are balanced in terms of their origins tend to be more valuable, congruous, and fungible, and therefore more likely to be transferred to other MNC units.

Various management literatures have argued that knowledge transfer between organizational units may serve to build knowledge-based competitive advantages (e.g., Argote & Ingram, 2000; Reagans & McEvily, 2003). In particular, a large segment of the international business literature argues that multinational corporations (MNCs) can derive advantages relative to purely domestic firms from their superior access to heterogeneously distributed knowledge (e.g., Bartlett & Ghoshal, 1989; Hedlund, 1986) and their ability to transfer and exploit such knowledge within the MNC (e.g., Kogut & Zander, 1993; Teece, 1977). The organizing framework in this literature has been that of the “bathtub metaphor” (Cohen & Levinthal, 1989, 1990; Decarolis & Deeds, 1999; Dierickx & Cool, 1989; Doraszelski, 2003), suggesting that firms and subsidiaries can be seen as possessing proprietary stocks of knowledge (like water in a bathtub) and that these stocks may be affected by (in and out)flows of knowledge, such as those caused by R&D, interfirm spillovers, and knowledge “depreciation.” This view of knowledge has been a powerful workhorse on which a vast body of important and influential research has been built.

The basic approach in this research stream has been to implicitly assume organizational knowledge stocks to change in a cumulative manner. The implication is that firms and their subunits accumulate knowledge, as long as their inflows are larger than their outflows, and thereby increase the economic value of their knowledge stocks. 1 This view contrasts with the psychology literature, which has emphasized that knowledge—unlike water in a bathtub—consists of multiple dimensions and elements that change one another. Different knowledge elements may even be in mutual conflict because they are based on dissonant cognitive schemas (Festinger, 1957). For example, when recipients acquire new knowledge that conflicts with their existing beliefs, they may inadvertently alter their existing knowledge structures—a process that cognitive constructivists call “accommodation” (Dole & Sinatra, 1998). In the context of the MNC, this may lead a foreign subsidiary to alter or discard preexisting knowledge that happened to be valuable to other MNC units. This implies that knowledge inflows from the environment may be value destroying, an effect that cannot be captured if we assume knowledge to be cumulative. A subsidiary’s increased absorption of knowledge from its external environment may therefore lead to less, rather than more, knowledge transfer to the rest of the MNC when accommodation to the knowledge sourced from the external environment impedes the subsidiary’s coherence with the rest of the MNC.

Knowledge in MNCs is to a large extent distributed across subsidiaries (e.g., Bartlett & Ghoshal, 1989; Birkinshaw, 1996; Gupta & Govindarajan, 2000; Hedlund, 1986). Knowledge heterogeneity arises partly because subsidiaries build knowledge assets, such as technological competencies, from different sources. For example, some subsidiaries may rely more on knowledge sourced from their local environments in the process of building valuable subsidiary-level knowledge (“external knowledge”), whereas others might build knowledge assets based on knowledge inputs from other subsidiaries or corporate headquarters (“internal knowledge”; see Frost, 2001). Such heterogeneity suggests that subsidiaries may differ not only in their ability to receive and utilize knowledge from their external environments (Cohen & Levinthal, 1989) but also in the amount of knowledge that they are able to successfully transfer to other subsidiaries within the MNC (Wong, Ho, & Lee, 2008). We argue that a foreign subsidiary needs to possess a certain minimum level (a “tipping point”) of knowledge received internally from other MNC units, for the rest of the MNC to benefit from the transfer of knowledge that the subsidiary acquires from its external environment.

We operationalize and test these ideas using a unique data set on foreign subsidiaries including information on stocks and flows of technological knowledge. Our findings suggest that the acquisition and exploitation of externally sourced knowledge are processes that are strongly related to the characteristics of the knowledge controlled by individual organizational units. Although our results relate directly to the current MNC literature, they have implications in more general settings. In particular, although we show that the MNC’s absorptive capacity (Cohen & Levinthal, 1989, 1990) is dependent on the knowledge characteristics of its individual organizational units, this argument is likely to apply to national firms as well.

Determinants of Knowledge Transfer in the Multinational Corporation

The notion that knowledge is a fundamental driver of value creation has become a key tenet in the strategic management literature (e.g., Barney, 1991; McEvily & Chakravarthy, 2002) as well as in the MNC literature (Gupta & Govindarajan, 1991, 1994, 2000; Hedlund, 1986; Kogut & Zander, 1993). Knowledge resources (e.g., production know-how) may be particularly strong drivers of value creation in MNCs because they can be transferred to overseas subsidiaries that do not yet possess them, yielding significant scale and scope economies across the MNC network. The MNC is viewed as a network of geographically separate but mutually linked nodes (or units), each possessing unique knowledge resources (Ambos, Ambos, & Schlegelmilch, 2006; Ghoshal & Bartlett, 1990; Ghoshal & Nohria, 1989; Håkanson & Nobel, 2001). Possibilities for combining complementary knowledge resources, and for supporting their transfer and subsequent combination, drive overall value creation (Fey & Birkinshaw, 2005; Yang, Mudambi, & Meyer, 2008).

At the same time, anecdotal evidence tells us that even intra-MNC knowledge transfer can be a source of managerial challenges. For example, when Acer America developed the Aspire, it encountered significant knowledge transfer barriers in its attempt to coordinate and leverage the innovation throughout the rest of the Taiwanese PC maker’s global organization, which was hesitant to take directions from the U.S. subsidiary (Bartlett & St. George, 1998). In general, the basic premise of much of the recent MNC literature—namely, that knowledge resources controlled by subsidiaries are heterogeneous—implies that intra-MNC transfer costs may vary depending on the characteristics of the transferred knowledge and the receiving unit (e.g., Kogut & Zander, 1993) and that the economic value of knowledge may be highly heterogeneous among different units within MNCs. This suggests that the amount of knowledge residing in a subsidiary is in itself of less importance than the dimensions of knowledge heterogeneity in determining the costs and benefits of knowledge transfer. Therefore, we need to consider these more subtle dimensions of knowledge heterogeneity to capture the cost and benefits of knowledge transfer. We argue that an understanding of these dimensions requires us to take one step further back and examine the sources of subsidiary knowledge heterogeneity.

Sources of Subsidiary Knowledge and Net Benefits of Knowledge Transfer

Subsidiary knowledge may originate from different sources (Frost, 2001). From the perspective of a focal unit, knowledge may derive from sources that are internal to the MNC in the sense that it has been transferred to the subsidiary from other MNC units (i.e., other subsidiaries or headquarters). For example, internal customers, suppliers, or R&D units may provide the subsidiary with the know-how it needs to perform its various functions in the firm. Alternatively, subsidiary knowledge sources can be external to the MNC. 2 For example, firms may acquire knowledge from interaction with external parties, such as host country customers or suppliers (Dyer & Nobeoka, 2000; Ford, 1990), or they may gain knowledge inputs from a well-educated workforce or local research institutions, such as technical universities, in industrial clusters (Porter, 1990; Porter & Sölvell, 1998).

Consider a focal foreign subsidiary that possesses a stock of technological knowledge, which may be either internally or externally sourced or some combination thereof. For example, it may possess blueprints and tacit knowledge elements that are a mixture of knowledge acquired from technical universities in its host country and from internal R&D labs in MNC units in other countries. This combination, in turn, affects the costs and benefits of transferring that knowledge from the subsidiary to other MNC units, including corporate headquarters and other foreign subsidiaries. Knowledge transfer benefits exist if economic value is created by transferring some of the knowledge resources of the focal subsidiary to other units within the MNC (e.g., if these receiving units can use it to produce and sell a technologically advanced product to their local customers at high margins). At the same time, however, knowledge transfer may be costly (Teece, 1977). A variety of economic and cognitive factors—namely, a lack of absorptive capacity (Lane & Lubatkin, 1998), distrust of the transferred knowledge (Katz & Allen, 1982), lack of retention on the part of the receiving unit (Szulanski, 1996), sending units’ lacking competence with respect to transferring knowledge (Martin & Salomon, 2003), low fungibility (Teece, 1982), and low congruity of the transferred knowledge with the knowledge held in the receiving unit (Schulz, 2003)—drive the costs of knowledge transfer (e.g., efforts to encode and decode the knowledge or costs of transportation and rotation of knowledge-bearing employees). There will be an incentive for MNE managers to facilitate such knowledge transfer only if the expected benefits of transferring the knowledge exceed these costs. We use formal notation to discuss how the marginal costs and benefits (

The uniqueness of external knowledge

Research indicates that unique knowledge may develop in the periphery of the firm’s knowledge structure (Andersson, Forsgren, & Holm, 2002; Lyles & Schwenk, 1992; Zahra, Ireland, & Hitt, 2000). Related research shows that external knowledge in foreign subsidiaries may be valuable to MNCs (Doz, Santos, & Williamson, 2001; Frost, Birkinshaw, & Ensign, 2002; Ghoshal, 1987). For example, the MNC may take advantage of interfirm spillovers of technological knowledge (Jaffe, Trajtenberg, & Henderson, 1993) that are captured by subsidiaries, or extract knowledge from sophisticated customers and skilled competitors by having specialized subsidiaries in strategic locations (Asmussen, Pedersen, & Dhanaraj, 2009; Dunning, 1996; Porter, 1998). The Acer Aspire is a case in point—being designed by a local Silicon Valley firm called Frog Design, championed by an American product manager, and shaped by extensive inputs from local retailers and consumers (Bartlett & St. George, 1998). External knowledge of this kind is likely to be different from the knowledge of other MNC units because geographical proximity is conducive to knowledge spillovers (Jaffe et al., 1993) and most of the potential MNC recipients reside in other locations where they do not have proximate access to the knowledge environment of the focal subsidiary. 4

In contrast, internal knowledge is likely to somewhat overlap with preexisting knowledge in a potential receiving unit because both sender and recipient have previously received their knowledge from some of the same sources (such as MNC headquarters or other subsidiaries). Thus, internal knowledge, when transferred, may be relatively redundant in the context of the knowledge already possessed by the receiving unit. We thus argue that the uniqueness of the subsidiary’s knowledge in an MNC context tends to be larger, ceteris paribus, if that knowledge is acquired in the subsidiary’s external host country environment rather than from other MNC units. This enhances the benefit of knowledge transfer as it may stimulate innovation by increasing diversity of knowledge in the receiving unit (Page, 2007).

Knowledge fungibility

Although the preceding analysis suggests that external knowledge increases marginal knowledge transfer benefits (formally, BKE > 0), other forces pull in the opposite direction. In particular, the value of transferring the knowledge of the subsidiary depends not only on the uniqueness of that knowledge but also on the degree to which it is specialized to its originating location. For example, production blueprints from a focal subsidiary may indeed be valuable to overseas MNC units, which can use them to manufacture products for their local customers—but only to the extent that the customers in those countries actually value the product described by the blueprint. This idea was first proposed by Teece (1982), who defined the fungibility of a resource as the extent to which the resource retains its value when applied in increasingly distant markets. Hence, highly fungible resources are those generalized, firm-specific capabilities that could potentially be used in a wide variety of markets (Teece, 1982; Wernerfelt & Montgomery, 1988). In an MNC context, the fungibility of the subsidiary knowledge stock should be an important determinant of the benefits of knowledge transfer.

Rugman and Verbeke (1992) stress the interaction of geographic distance and fungibility by distinguishing between location-bound (nonfungible) and non-location-bound (highly fungible) firm-specific advantages. Several factors may contribute to making a knowledge resource location bound. Often receiving units are poorly positioned to exploit knowledge simply because they are distant from the customers, suppliers, partners, or competitors for whom the knowledge was developed. This suggests that external knowledge is likely to be more difficult to apply in other MNC units, precisely because it has a more peripheral origin. It is less fungible than internal knowledge because it relates specifically to host country conditions and is, therefore, more context specific. External knowledge may therefore in fact be associated with lower benefits (BKE < 0) and increased costs (CKE > 0) of knowledge transfer.

Knowledge congruity

Furthermore, even if a focal subsidiary’s knowledge is highly fungible, it is not certain that potential recipient units possess the necessary complementary knowledge to absorb and utilize it (Cohen & Levinthal, 1990). This suggests that there is another aspect, in addition to the economic applicability of the knowledge to recipients’ markets, that matters to knowledge transfer benefits—a cognitive aspect that we refer to as the congruity of the subsidiary’s knowledge stock. Schulz (2003) noted that the relevance of a given knowledge stock to its recipient was a function of the extent to which the knowledge is related to and connected with the preexisting knowledge in the receiving unit. Consistent with that idea, we define knowledge congruity as the cognitive fit between the knowledge stocks of the focal subsidiary and those of potential recipients of that knowledge (e.g., HQ or a subsidiary in another location). One important antecedent to knowledge congruity is the combination of sources from where the knowledge of the subsidiary originates. If the knowledge originates within the MNC, it is likely to be reasonably congruous with that of a receiving MNC unit because both units have previously received their knowledge from some of the same sources and thereby have a foundation of shared knowledge on which to build. Conversely, external knowledge may be so far removed from the realities of the receiving unit that the personnel in this unit may not realize its value or fungibility or possess the necessary tacit complementary knowledge to exploit it (Yang et al., 2008) since the contexts of the sending and receiving subsidiaries differ. In other words, the receiving unit may not possess the relative absorptive capacity to utilize the external knowledge (Cohen & Levinthal, 1990; Lane & Lubatkin, 1998). Therefore, even if the knowledge reaches the intended recipient, it may lie dormant in that unit without being exploited to its full commercial potential, suggesting that BKE < 0 also for this reason.

Similarly, the congruity of the subsidiary’s knowledge with the knowledge held in the recipient units may influence the costs of knowledge transfer. If the knowledge stock is mainly internal, the overlap between the knowledge of the sender and recipient units is likely to be high. This implies low knowledge transfer costs (Reagans & McEvily, 2003): As the two units hold a certain amount of knowledge in common, less codification should be required because the transferred knowledge is easily recognized and understood and fewer costly misunderstandings occur. In contrast, external knowledge elements are likely to have fewer overlaps with other knowledge assets in the MNC. Therefore, even though other MNC units might benefit from this knowledge, their relative absorptive capacity to assimilate it is limited (Cohen & Levinthal, 1990; Lane & Lubatkin, 1998). In turn, this means that the encoding and decoding of this knowledge may require more effort and the need for face-to-face contact may be higher. These factors suggest that the costs of knowledge transfer will be higher if the subsidiary possesses more external knowledge (CKE > 0), an effect that compounds the effects of external knowledge on transfer benefits and reinforces its effects on fungibility.

Assimilation and accommodation as responses to external knowledge

Although the above arguments suggest an unambiguous amplifying effect of external knowledge on knowledge transfer costs, they offer conflicting predictions as to the effect of external knowledge on knowledge transfer benefits. In essence, external knowledge may make the focal subsidiary’s knowledge more unique and less applicable at the same time. The notion of a negative relationship between external knowledge and knowledge transfer benefits deserves elaboration as it may at first seem counterintuitive: How can more knowledge possibly lead to lower knowledge transfer benefits? Indeed, the tendency in the economics and management literatures is to see organizational knowledge stocks as cumulative, so that they can be augmented by acquiring additional external knowledge that stacks on top of the preexisting knowledge and adds to the value of that knowledge. Cognitive psychologists use the term assimilation to describe such a process, where recipients incorporate the learned knowledge into their existing knowledge stocks, which in turn are left largely unchallenged (Posner, Strike, Hewson, & Gertzog, 1982). Under knowledge assimilation, we would never expect to see a negative relationship between external knowledge and knowledge transfer benefits. In the worst case, acquired nonfungible and incongruous external knowledge would merely fail to increase knowledge transfer benefits further, but it should not destroy the benefits of transferring the subsidiary’s remaining knowledge, which would still be there, largely intact and valuable. 5 Therefore, there would always be, at worst, a flat relationship between external knowledge and marginal knowledge transfer benefits, so that BKE ≥ 0.

However, the cognitive psychology literature also recognizes that assimilation is only one part of the learning process and that a fundamentally different reaction pattern, called accommodation, may also occur in knowledge recipients (Dole & Sinatra, 1998; Vosniadou & Brewer, 1987). In the process of accommodation, the acquisition of new knowledge makes the recipients alter some of their existing knowledge structures. This process is described in detail in the psychology literature as pertaining to individuals (e.g., Piaget & Brown, 1985), and accommodation to host country knowledge may thus happen in subsidiary individuals such as country managers and R&D personnel. However, we suggest that it is likely to also be embedded on a higher level—the foreign subsidiary itself—since organizational learning “results in associations, cognitive systems, and memories that are developed and shared by members of the organization” (Fiol & Lyles, 1985: 804). Furthermore, even though accommodation is to some extent a natural part of the learning process in individuals, it may be problematic in the MNC context because acquired host country knowledge may lead subsidiaries to reinterpret and, possibly, discard internal MNC knowledge. Cognitive elements (whether at the individual or subsidiary level) may instead be infused with host country norms for what are best practices (e.g., What is considered a superior technology?) and host country perceptions of causal relationships (e.g., What determines the performance of a complicated product?). This could make the knowledge less congruous with and fungible for potential MNC recipients who do not share these norms and perceptions and thereby lead to lower knowledge transfer. This suggests a possible explanation for Acer’s problems, where units outside of the United States struggled with manufacturing the Aspire (suggesting low congruity of the American innovation with the rest of the MNC) and felt compelled to make significant and cost-increasing adaptations to it for their own markets (suggesting low fungibility). Effectively, there is a risk that the dominant logic (Prahalad & Bettis, 1986) of the subsidiary moves closer to that of its knowledge sources in the host country and further away from the dominant logic of the MNC. Therefore, the internal legitimacy of the subsidiary may be reduced because of the trade-off between internal and external legitimacy (Kostova & Zaheer, 1999). This may lead to increased subsidiary isolation and thus to reduced knowledge transfer, as pointed out by Monteiro, Arvidsson, and Birkinshaw (2008).

Interaction of internal and external knowledge

As a result of the contrary effects of assimilation and accommodation, it is ambiguous how the external knowledge resources controlled by a subsidiary will affect the benefits of transferring knowledge to other MNC units. If the subsidiary merely assimilates external knowledge, more external knowledge can never be directly detrimental because the knowledge, at best, can be profitably exploited by receiving units and, at worst, is worthless to these units. In that case, we would expect that BKE ≥ 0. On the other hand, if external knowledge causes accommodation to take place in the subsidiary’s internal knowledge stock, which thereby becomes less congruous and fungible, a negative relationship between external knowledge and marginal knowledge transfer benefits may exist, because the composite knowledge of the subsidiary becomes less applicable in receiving units, that is, BKE < 0.

We argue that accommodation to external knowledge is more likely in subsidiaries that have low levels of internal knowledge, whereas subsidiaries with high levels of internal knowledge either reject new external knowledge or assimilate it by reshaping it to fit their existing internal knowledge structures. Hence, the interaction of external and internal knowledge is related to knowledge transfer benefits, such that the subsidiary’s “own internal know-how will increase the marginal returns to external knowledge acquisition strategies” (Cassiman & Veugelers, 2006: 68). There are three ways in which this can happen. First, for external knowledge to be combinable with knowledge in other MNC units, it has to be interpreted and formulated in such a way that it can be accessed by other units (Grant, 1996). This requires internal knowledge and may increase the congruity and fungibility of the subsidiary’s composite knowledge stock. In the absence of this interaction with internal knowledge, external knowledge may generate lower benefits in other parts of the MNC because it is too distant from the recipients’ preexisting knowledge. In other words, they may lack the absorptive capacity and the complementary knowledge to exploit it (as seemed to be the case for Acer’s market units in other regions). In contrast, having both internal and external knowledge in the technological knowledge stock of the subsidiary would be an ideal basis for intrafirm knowledge recombination (Ahuja & Katila, 2001) because the knowledge of the originating subsidiary is then neither too similar to the knowledge held by potential receiving units nor too different from it.

Second, internal and external knowledge resources can be complementary, so that they can be combined into a more valuable composite knowledge resource and subsequently transferred to other MNC units. A subsidiary might thus be able to combine technological stimuli from its host market with the proprietary technologies of the MNC before it transmits this knowledge to other MNC units. Arguably, if the U.S. subsidiary of Acer had possessed sufficient internal knowledge, it may have been able to push Frog Design to develop a product that fit not only with emerging consumer tastes but also with the manufacturing capabilities of Acer’s global organization.

Third, if the subsidiary possesses internal knowledge, it may be better able to screen the external environment (Arora & Gambardella, 1994; Cohen & Levinthal, 1989), enabling it to acquire external knowledge that is more fungible and congruous, and thereby more relevant to MNC recipients, in the first place. Internal knowledge can thereby empower the subsidiary as a “listening post” for the MNC—a role in which “receiver competence (assessing, filtering, and choosing information) and absorptive capacity (adapting inflows to fit firm-specific requirements) become crucial” (Mudambi & Navarra, 2004: 389). Taken together, these three mechanisms suggest a positive interaction between internal and external knowledge in the determination of the benefits of knowledge transfer, so that BKEI > 0.

As a highly stylized example of this process, consider a subsidiary that possesses a knowledge element A. Furthermore, suppose this knowledge element is fungible and congruous and (in the absence of more external knowledge) would therefore be associated with knowledge transfer benefits. What would happen if the subsidiary then increases its external knowledge level by acquiring a host country knowledge element B and combining it with A? If it has sufficient internal knowledge, it will reinterpret this new knowledge in the MNC context, in turn making both A and B useful to other units (an assimilation process leading to a positive relationship between external knowledge and knowledge transfer benefits). If the subsidiary has only a moderate level of internal knowledge, it may not be able to reinterpret the new knowledge in the MNC context and B may therefore be useless to other units (while A is still useful, leading to a flat relationship). Finally, if the subsidiary possesses low levels of internal knowledge, it may be so vulnerable to external influence that the new knowledge B leads it to inadvertently reinterpret A in a way that is specific to the host country (perhaps by discarding aspects of A that are unrelated to the local technologies embodied in B). This accommodation process decreases the usefulness of A to other MNC units. In that case, an increase in external knowledge actually leads to a decrease in knowledge transfer benefits.

Predicting Knowledge Transfer

The theoretical framework sketched out thus far describes the extent to which knowledge transfer may create costs and benefits for the MNC. We can generate predictions of actual levels of knowledge transfer by asking what happens if subsidiary and MNC managers are responsive to these costs and benefits, in other words, by submitting knowledge transfer to a “logic of consequences” (March, 1996: 283). If for now we treat the knowledge stock of the subsidiary (I and E) as exogenous, we can find the best level of knowledge transfer for any given level of internal and external knowledge. To do this, we solve for the level of knowledge transfer (denoted K*) that maximizes the net benefits from knowledge transfer (denoted NB):

The first- and second-order conditions for this maximization problem are as follows:

These conditions will be fulfilled if the marginal net benefits from knowledge transfer at some point begin to diminish and eventually reverse. Arguably, this is a reasonable assumption: At some point, either the benefits from further knowledge transfer are exhausted or the costs become prohibitive (Cohen & Levinthal, 1989). 6

For any given level of E, then, there will be a K* that satisfies Equation 2, and we can say that this equation therefore implicitly defines K* as a function of E. We use this feature to derive comparative statistics that show how changes in external knowledge levels affect the optimal level of knowledge transfer. By applying the implicit function theorem (see, e.g., Chiang, 1984: 208) to Equation 2, we arrive at, 7

As much of the literature identifies external knowledge as a source of MNC competitive advantage (Doz et al., 2001; Porter & Sölvell, 1998), one may be tempted to hypothesize that higher levels of external knowledge lead to more knowledge transfer, so that Equation 4 is positive. However, the denominator of Equation 4 is positive by virtue of the second-order condition, so the sign of K* E actually depends on the sign of the numerator BKE–CKE, which is indeterminate because of the dual impact of assimilation and accommodation. 8 Still, the assumption that BKEI > 0 implies that d(BKE) / dI > 0 and therefore also that d(BKE–CKE) / dI > 0 which, combined with Equation 4, implies that K*EI > 0. This is our first hypothesis:

Hypothesis 1: The interaction between the internal and external knowledge in a subsidiary is positively related to the level of knowledge transfer from that subsidiary to the rest of the MNC.

Based on this interaction effect, we can arrive at a conditional prediction of the relationship between external knowledge and knowledge transfer. If K*EI > 0, a sufficiently high level of internal knowledge will, ceteris paribus, increase the likelihood that the marginal benefits of external knowledge will be positive and also the likelihood that they will outweigh the marginal costs of that knowledge. This implies that there may exist a knowledge tipping point—a level of internal knowledge in a subsidiary that must be exceeded if the MNC is to benefit from knowledge that originates from that subsidiary’s external environment. We define this tipping point (denoted

Hypothesis 2: The relationship between external knowledge and knowledge transfer will be positive if the internal knowledge of the subsidiary lies above a certain tipping point,

Operationalizing the model

How can such a tipping point be estimated from actual data? To make the model amenable to empirical testing, we adopt the simplest polynomial approximation that fulfills our theoretical assumptions. This enables us to write the net benefit of transferring knowledge out of subsidiary j,

where

which can be solved for a prediction of K* j :

In this expression, γ

i

≡ gi / 2g4,

We can now estimate the level of internal knowledge that is required if external knowledge is to be beneficial. This level can be estimated by asking what level of I would ensure that (K*) E > 0: 12

Thus, the level of internal knowledge has to be above −γ1 / γ3 before external knowledge has a positive effect on the knowledge transfer out of the subsidiary. This tipping point can be estimated with data on E, I, and K.

Endogenous regressors

Although we have treated internal and external knowledge as exogenous variables in our framework, they could in fact be endogenous if MNC managers are simultaneously determining where to locate their subsidiaries, what knowledge to source internally and externally, and how much of that knowledge will be transferred. Therefore, if we estimated Equation 8 using ordinary least squares (OLS), we would run the risk of obtaining biased results and, consequently, a biased tipping point. In principle, if we could identify and observe all variables affecting K, we would be able to control for these variables and thereby solve the endogeneity problem (controlling for observables). However, in practice, we cannot a priori rule out the presence of unobserved variables that may affect both I and E, as well as K. For example, suppose that the disturbances ε1j were created by unobserved subsidiary-specific variables—such as tacit knowledge management capabilities—that affect both knowledge levels and knowledge transfer. In that case, I, E, and ε1j would be positively correlated (because they are affected by the same unobserved capabilities), which would lead to inflated estimates of γ in Equation 8 and thereby to a biased estimate of the tipping point in Equation 9.

To correct this problem, we can replace the actual values of the endogenous regressors with instrumental variables or, preferably, with predicted values based on multiple instruments (Kennedy, 2003). First, we add the following two equations to our model,

where ε

j

are disturbances and

Empirical Analysis

Data Collection

The data for this article were collected mainly as part of the Centres of Excellence Project, which engaged researchers in the Nordic countries, the United Kingdom, Germany, Austria, Italy, Portugal, and Canada (see Holm & Pedersen, 2000). The project was launched to investigate headquarter–subsidiary relationships and the internal flow of knowledge in MNCs. To collect comparable quantitative data on the acquisition of subsidiary knowledge, it was decided to construct a questionnaire that could be used in all of the countries involved. This was accomplished after several project meetings and extensive reliability tests of the questionnaire with academics and business managers.

For practical reasons, all project members were responsible for gathering data on foreign-owned subsidiaries in their own country. Therefore, all subsidiaries in the database belong to MNCs. The data were gathered from subsidiary managers rather than headquarters. One advantage of using subsidiary respondents is that they are directly engaged in the operations on the market and are, therefore, more acquainted with the characteristics of the host country environment. Although any subsidiary might be expected to have a reliable awareness and understanding of its own knowledge resources, it would be advantageous to gather information on intra-MNC knowledge flows from other corporate units as well. However, identifying the appropriate subsidiaries in each country and then identifying and approaching relevant management units in the foreign subsidiaries would be an unmanageable task.

Description of the Data

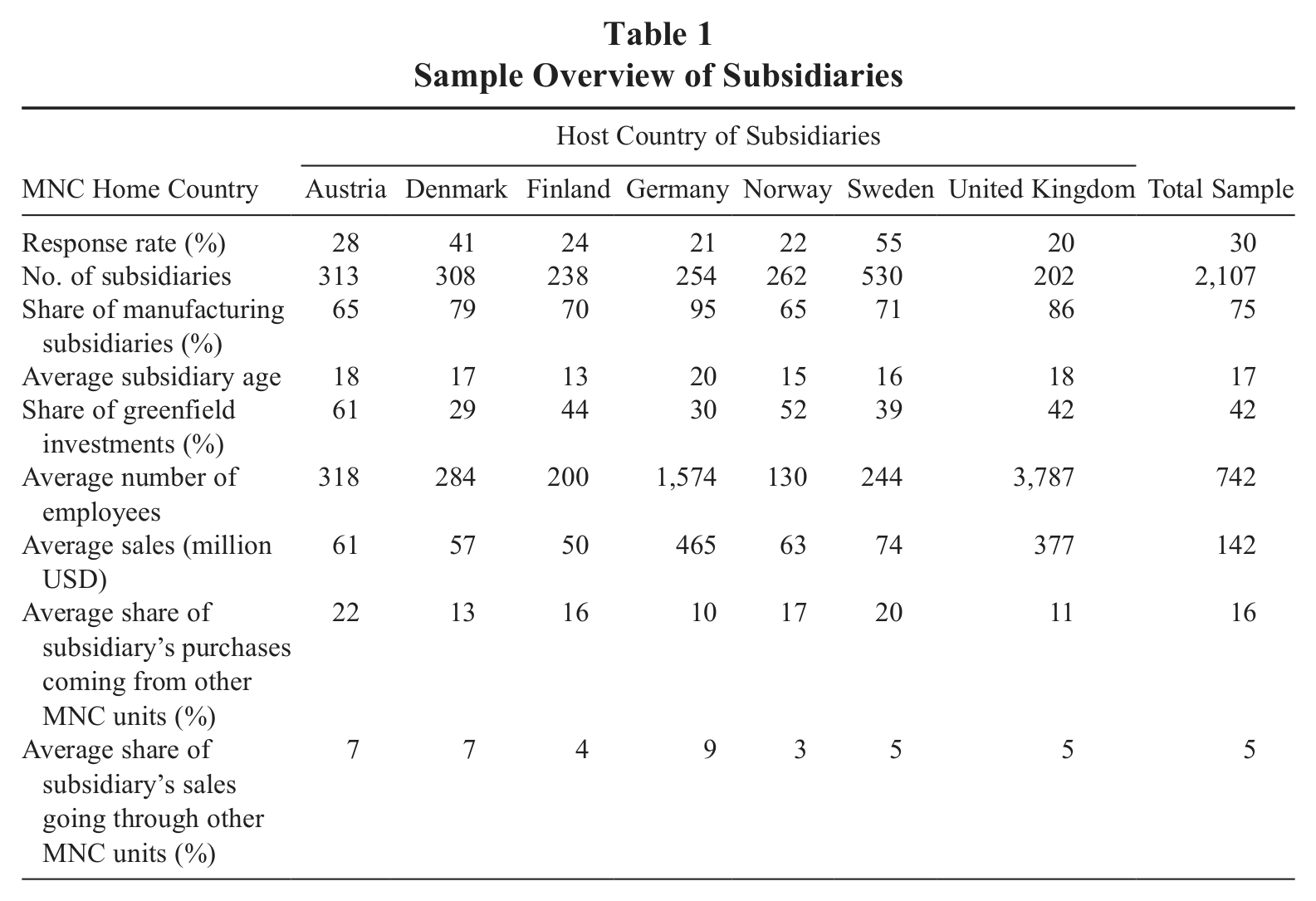

Our analysis is based on data from seven countries: Austria, Denmark, Finland, Germany, Norway, Sweden, and the United Kingdom. All countries are located in the northern part of Europe. The four Nordic countries are relatively small, whereas Germany and the United Kingdom are among the largest in Europe. Approximately 80% of the questionnaires were answered by subsidiary executive officers, whereas financial managers, marketing managers, or controllers in the subsidiaries answered the remaining 20%. The overall response rate was 30%, and the quality of the data was relatively high—the general level of missing values was not greater than 5%. Table 1 shows the sample properties segmented by country. Country variations emerge in the response rates, which ranged from 20% (in the United Kingdom) to 55% (in Sweden), and in the sizes of the subsidiaries, which tended to correlate with the sizes of the host countries and with subsidiary age. In general, the Nordic subsidiaries were younger and smaller than subsidiaries in other countries.

Sample Overview of Subsidiaries

The sample covers 2,107 subsidiaries and composes all types of subsidiaries in all fields of business. However, 75% of the subsidiaries conduct manufacturing activities across the seven countries. The average number of employees in the subsidiaries was 742, with a median of 102. Average annual subsidiary sales were US$142 million. The share of subsidiary sales going through other MNC units was on average 5%, whereas the average share of purchases coming from other MNC units amounted to 16%. The average subsidiary age at the time of the survey was 17 years. Of the subsidiaries, 42% were established as greenfield investments, whereas the remaining 58% were acquisitions. The sample size per country ranged from 202 (United Kingdom) to 530 (Sweden), and the sample sizes were generally similar, with the exception of Sweden. The average size of the subsidiaries in the five smaller countries was similar, whereas subsidiaries in Germany and the United Kingdom, because of the larger size of those markets, were substantially larger.

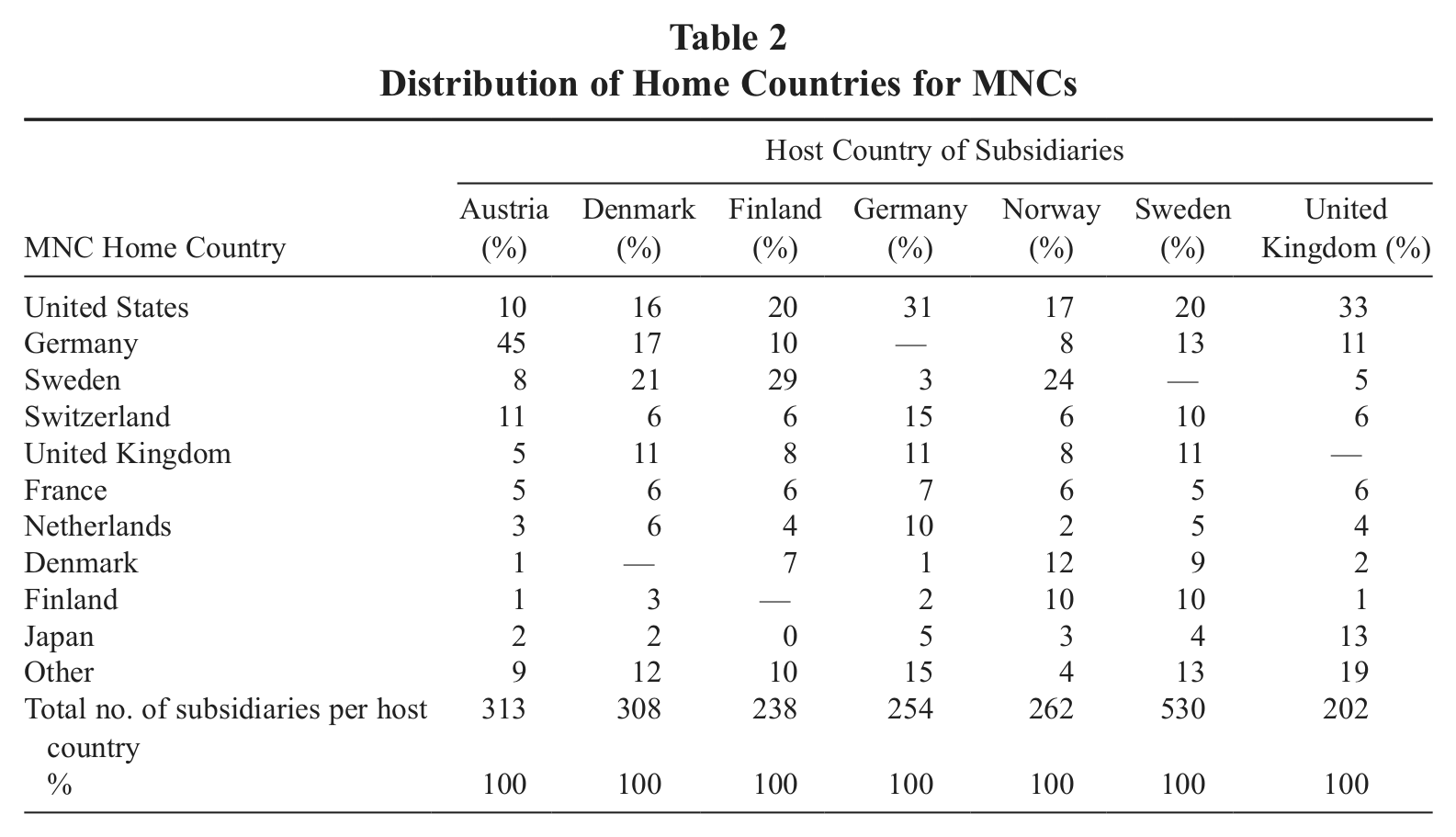

Table 2 lists the distribution of MNC home countries for the 2,107 subsidiaries that are the focal unit of analysis for this study. There are some notable differences in the dominant MNC home country for subsidiaries in the seven host countries. Of the foreign-owned subsidiaries in Austria, 45% and 11% are German and Swiss owned, respectively, whereas Swedish owners are dominating among the foreign-owned subsidiaries in Finland (29%), Norway (24%), and Denmark (21%). MNCs from the United States control a prominent share of foreign-owned firms in all seven countries but are particularly dominating in the United Kingdom (33%), Germany (31%), and Sweden (20%). Japanese MNCs seem to control only minor shares except in the United Kingdom, where 13% of the foreign-owned subsidiaries have Japanese owners.

Distribution of Home Countries for MNCs

Measures

Data were collected both from secondary sources and through the questionnaire. Some items in the latter, such as the number of employees, were measured using actual values, whereas most variables are multi-item measures that were measured using 7-point Likert-type scales. 13

Survey measures have both advantages and disadvantages compared to patents, which have become a popular way to operationalize knowledge transfer (see, e.g., Singh, 2007). On one hand, survey measures can capture transferred knowledge that is used in final products or processes in the recipient units, whereas patent citations cannot pick up knowledge transfer unless the recipient unit itself engages in innovative activity and takes out a patent in which citations can appear. Also, unlike patent data, perceptual data are suitable for capturing tacit as well as codified knowledge (Kaiser, 2002), and it is relatively industry agnostic (Archibugi & Pianta, 1996). On the other hand, it is well known that survey data may contain measurement errors that violate econometric assumptions because of social desirability and other respondent biases (Bertrand & Mullainathan, 2001). We have assessed and addressed the possibility of such biases in a number of ways in our study. First, to detect potential common method bias problems in the data (i.e., the risk that the correlations between variables might be inflated), we performed Harman’s single-factor test for all dependent and independent variables (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003), but found no indication of such a bias. Following Podsakoff et al. (2003), we also ran a partial least squares (PLS) model, which included a common method factor whose items encompassed all of the constructs’ items. This PLS model provided information on each item’s variances, substantively explained by the constructs and by the common method factor. The average substantively explained variance of the items is between 0.59 and 0.69 for the different models, whereas the average method-based variance is around 0.01. The ratio of substantive variance to method variance is, therefore, very high, which indicates that the potential common method bias is relatively small. In combination, these statistical tests suggest that our results are not driven predominantly by common method bias, especially as our main hypotheses are based on a moderating effect, which is rather unlikely to emerge exclusively as a result of such bias (Chang, Van Witteloostuijn, & Eden, 2010; Siemsen, Roth, & Oliveira, 2010).

Finally, as explained below, we also attempt to control statistically for error covariances with our instrumental variables 3SLS model. All in all, although these precautions do not eliminate the threat of potential biases stemming from the use of survey data, they do raise the hope that such biases have been largely contained. 14 The next sections describe the measurement of the individual variables in our data set.

Knowledge transfer

Davenport and Prusak (1998) argue that knowledge transfer involves not just the transmission of knowledge but also the practical application and use of the knowledge by the receiver. Accordingly our measure of (successful) knowledge transfer captures the use of the subsidiary knowledge in other MNC units. The subsidiaries were asked about the extent to which technological knowledge under their control had been of use to other MNC units on a 7-point Likert-type scale, where 1 was defined as to no use at all for other units and 7 was defined as very useful for other units. The transfer of technological knowledge was measured in terms of the average usefulness of three types of knowledge, research (basic and applied), development (of products and processes), and production (of goods and services), and this scale showed acceptable reliability with Cronbach’s alpha = .65.

Internal knowledge

The “internal knowledge” construct captures the knowledge developed through interaction with other MNC units. To measure the knowledge inputs from other MNC units, respondents were asked to assess the impact of various internal organizations on the development of the subsidiary’s competences, where 1 equaled no impact at all and 7 equaled very decisive impact. Internal technological knowledge was thus measured as the impact of internal MNC R&D units on the subsidiary’s competences.

External knowledge

The “external knowledge” construct (i.e., subsidiary-level knowledge built mainly from external knowledge inputs) captures the importance of external parties. The inputs from external partners were measured by asking respondents to assess the impact of various external organizations on the development of the subsidiary’s competences, where 1 equaled no impact at all and 7 equaled very decisive impact. External technological knowledge was then measured as the impact of external R&D units on the subsidiary’s competences.

Predictors of internal knowledge

As predictors of internal knowledge in Equation 10, we include a number of variables suggested by theory. First, we obtained measures of subsidiary dependency, which captures the extent to which the focal subsidiary is dependent on knowledge from other MNC units. It was measured by asking respondents, “What would be the consequences for the subsidiary if it no longer had access to the competencies of other MNC units?” (1 = no consequences and 7 = very significant consequences). We believe that a subsidiary that perceives itself as being highly dependent on other MNC units would also be more motivated to receive knowledge from these units. Second, we included the subsidiary’s mode of formation (0 = greenfield, 1 = acquisition). We would have liked a more fine-grained measure including, for example, information about joint venture partners, but this information was not available. We nevertheless believe our dummy variable captures an important distinction: A subsidiary that is acquired as an independent firm and subsequently integrated into the MNC may be more reluctant to receive knowledge from its parent and other subsidiaries than one that is designed and staffed by the MNC from inception, for example because of the not-invented-here syndrome (Katz & Allen, 1982). Third, we included the age of the subsidiary (in years), which captures the duration of time the subsidiary has been exposed to MNC policies and internal knowledge. Arguably, internal knowledge may be more readily absorbed when the subsidiary has well-developed channels, routines, and organizational structures for exchanging information with other units, and building such an infrastructure is subject to time compression diseconomies (Dierickx & Cool, 1989). The passing of time itself may also enable employees to become more strongly identified with the firm and develop trust in the internal network, which facilitates internal knowledge acquisition.

Predictors of external knowledge

Extant research has suggested several factors that may influence subsidiary acquisition of external knowledge. In particular, host country characteristics have been shown to be important predictors of subsidiary innovation (Almeida & Phene, 2004). We obtained several measures to gauge these characteristics and, especially, the quality of the knowledge in the external business environment, which might enhance the external technological opportunities (Cohen & Levinthal, 1989) of the subsidiary. First, we constructed measures of science per capita for each host country in which our subsidiaries are located. This was calculated as the number of scientific and technical journal articles published in the relevant host country (sourced via the World Development Indicators database from the World Bank), normalized by dividing with the population of each country. Second, although knowledge environments differ from country to country, they also vary across localities and industries within a country (Porter, 1990). We therefore also used Porter’s (1990) diamond model as a more fine-tuned measure of location effects. We asked respondents for their assessment of cluster factors along the following dimensions: availability of business professionals, availability of supply material, quality of suppliers, level of competition, government support, legal environment, and existence of research institutions (1 = very low quality and 7 = very high quality). Porter’s (1990) emphasis on the holistic nature of the model and the high intercorrelation between many of the items motivated us to construct a composite index (Cronbach’s α = .67). These cluster factors extend the science per capita measure as they contain both country-specific effects and industry-specific effects and some level of interaction between them. Third, we asked the respondents to evaluate the institutional environment in the host country. If institutional conditions are perceived as favorable, the subsidiary may be more willing to open up and engage actively with the surrounding environment, for example, collaborating with host country partners, without an expectation of disputes or intellectual property appropriation. This, in turn, would lead to better opportunities for external knowledge sourcing.

Knowledge transfer control variables

Finally, when predicting knowledge transfer in Equation 8 we included a number of variables related to the role of the subsidiary in the MNC network. When a subsidiary has a mandate as a strategic asset-seeking unit (Dunning, 1993), a competence-creating subsidiary (Cantwell & Mudambi, 2005), or a center of excellence (Frost et al., 2002; Holm & Pedersen, 2000), its knowledge is likely to be formally and informally recognized and valued by headquarters, by other units, and by subsidiary employees. This, in itself, may encourage the subsidiary to transfer more knowledge regardless of its actual knowledge levels. We therefore controlled for the MNC’s formal recognition of and dependency on the knowledge residing in the subsidiary, as well as the subsidiary’s own investments in and assessments of its competences. Formal recognition was measured by asking whether the indicated competencies of the subsidiary were formally recognized by the MNC headquarters. Respondents could answer yes or no to the following three activities: research, development, and production (the sum of which measured formal recognition of technological knowledge, from 0 to 3).

The MNC dependency on the knowledge of the focal subsidiary was measured using the following question: “What would be the consequences for other units in the foreign company if they no longer had access to the competencies of the subsidiary?” (1 = no consequences and 7 = very significant consequences). The subsidiaries’ own investments were measured by asking respondents to assess the level of investments in the subsidiary in the past 3 years, where 1 = very limited and 7 = substantial. Like formal recognition, the level of investments was assessed for the three technological activities (and averaged to determine investments in technological knowledge; Cronbach’s α = .69). In a similar way, the subsidiaries’ own assessment of their technological knowledge was captured by asking respondents to indicate the level of subsidiary competencies for these same activities (on a 7-point scale; Cronbach’s α for assessment of technological knowledge = .71). The subsidiaries vary in size, and their ability to absorb and exploit knowledge might be related to size, for example, in terms of employees. Therefore, we included a size measure of logarithm of total number of subsidiary employees as a control variable. Finally, we controlled for geographic distance with a dummy variable measuring whether the parent MNC was headquartered in Europe.

The correlation coefficients and descriptive data (mean values, standard deviations, and normality statistics) on all variables are provided in Table 3.

Correlation Matrix

Note: N = 2,107. All correlations > .04 or < –.04 are significant at the 5% level.

The bivariate correlations between knowledge transfer and both internal and external knowledge are positive and highly significant. Five control variables (MNC dependency, formal recognition, own competencies, subsidiary investments, and subsidiary employees) are also positive and significantly related to transfer of knowledge. Surprisingly, the sixth control variable, EU headquarters, seems not to be related to any of the other variables in the data set. It is also noticeable that none of the correlation coefficients among the independent variables indicate the possibility of multicollinearity (i.e., r > .5). Our dependent variable, knowledge transfer, has a low mean (about 2), which implies technological knowledge that has been of low to moderate use to other units, but the standard deviation and skewness suggest a long right tail. This suggests that a substantial number of subsidiaries indicate that their knowledge is of no use at all to other units (1), whereas a few see their knowledge as more or less useful (2–6) or even very useful (7). In fact, 101 subsidiaries (about 5% of the sample) answered either 6 or 7 on the 7-point Likert-type scale. This is surprising but could be interpreted as an indication of a “star system” pertaining to reverse knowledge transfer, where a few subsidiaries claim a disproportionate share of top management attention (Blomkvist, Kappen, & Zander, 2010). Finally, we can see from Table 3 that internal knowledge (mean of about 2.9) seems to be more important to the subsidiaries than external knowledge (2.1), perhaps reflecting barriers that subsidiaries with limited absorptive capacity face when sourcing knowledge from their host markets.

Evaluation of Instrumental Variables Approach

To address the problem of endogeneity through an instrumental variables approach, one would need an instrument (or set of instruments) that is correlated with the endogenous variable but that is not correlated with the error from the regression in which the endogenous regressor appears (Stock, Wright, & Yogo, 2002). From an a priori theoretical perspective, it seems likely that the “objective” instruments in our model—science per capita, subsidiary age, and formation—pass this test. Since the former is at the country level and collected outside the survey instrument and the latter two variables are irreversibly set at the founding of the subsidiary, it is unlikely that they will be significantly influenced by the current knowledge structures and organizational arrangements in the subsidiary. This means that they work as plausibly exogenous instruments. On the other hand, our perceptual instruments—cluster factors, institutional environment, and subsidiary dependency—may be less obvious candidates for instrumental variables. We believe that host country characteristics should be largely exogenous to the knowledge processes in an individual subsidiary since they exist independently of the subsidiary context. Subsidiary dependency does not, but it has the attractive property (for an instrument) that it is theoretically more strongly related to the accumulation of internal knowledge in the subsidiary than to the level of knowledge transfer out of the subsidiary (since it captures only one direction of the power relationships between the subsidiary and its peers). Still, if only because all three measures are perceptual, we cannot completely rule out the risk that they are at least simultaneous to the process that drives knowledge transfer, as would happen for example if there were unobserved capabilities that influenced both knowledge transfer and respondent perceptions.

From an a posteriori empirical perspective, nevertheless, there seems to be limited evidence of such a problem. Judging from Table 3, almost all instrumental variables predicting internal and external knowledge (Variables 4 to 9) are much more strongly correlated with their corresponding knowledge type (2 or 3) than they are with knowledge transfer (1). The weakest instrument seems to be cluster factors (for E), whereas the strongest ones seems to be subsidiary dependency (for I) and science per capita (for E). More importantly, however, is that they work well as a group, explaining an acceptable 13% to 15% of the variance in the endogenous regressors (as reported in Table 5). Furthermore, to test for overidentifying restrictions, we regress the residual from the knowledge transfer equation on the instruments for the model (Sargan, 1958). The R-squared value in this regression is very low (.0045), and none of the predictors are statistically significant. Basmann (1960) independently developed a method that is computationally different from but similar in spirit and asymptotically equivalent to the Sargan test (Kirby & Bollen, 2009). This test also led us to reject the hypothesis of a significant relationship between instruments and residuals (F = 0.78, p = .67), which is a quite strong result considering the size of our sample, which directly scales the test statistic. We also inspected the bivariate correlations between instruments and residuals, all of which were insignificant and close to 0. In combination, these tests do not provide absolute proof of the absence of endogeneity, but they do suggest that the problem has been addressed in our model.

Results

We did not mean-center our independent variables around 0, as this approach would complicate the interpretation of the tipping point—our focal interest—without improving the stability of the estimated coefficients (Echambadi & Hess, 2007). The Hausman test for endogeneity implied that the OLS estimates did indeed suffer from endogenous regressors (test statistics = 39.92, p < .001). This suggests the use of either 2SLS or 3SLS as a remedy against endogeneity bias. The main benefit of 3SLS is that it is asymptotically more efficient than 2SLS and thereby yields more precise parameter estimates in large samples if the error terms are correlated; in fact, “the performance of 3SLS always bests that of 2SLS as the sample size increases indefinitely” (Belsley, 1988: 29). This benefit has to be weighed against the potential drawbacks of 3SLS, which are that it is more computationally demanding and that it increases the severity of potential misspecification biases by allowing these to “contaminate” the whole system of equations (Zellner & Theil, 1962). We ultimately choose 3SLS because (a) we have a large sample that allows us to leverage the asymptotic efficiency of 3SLS and (b) the correlation of the error variances in our model cannot be ignored (in fact, they vary between .07 and .38), which means that the estimates would be less accurate if we restrict them to 0, as 2SLS implicitly does. We suspect that these error covariances may stem from the previously described measurement error in our survey data. We therefore refer to the 3SLS estimates (although they are very similar to the 2SLS estimates) in the following.

Although all exogenous variables were used to predict internal and external knowledge in the first stage, we report only the main (third-stage) predictors of these two variables in the interest of conciseness and clarity. Our results are reported in Tables 4 and 5.

Three-Stage Least Squares Models and Incremental F Tests

Note: N = 2,107. Standard errors are shown in parentheses. Coefficients on control variables are suppressed (but shown in Table 3 for the final model).

p < .01.

Three-Stage Least Squares Model for Technological Knowledge

Note: N = 2,107. Instrumented values of internal and external knowledge are based on all exogenous variables. Standard errors are shown in parentheses, and standardized beta estimates (how many standard deviations the dependent variable changes for each standard deviation change in the independent variable) are listed in italics.

p < .05. **p < .01.

To evaluate the impact of the hypothesized variables, we ran a series of models that were hierarchically nested within another, in the sense that each new model was obtained by adding explanatory variables to the previous one. The results of this process are reported in Table 4. Model 1 included only the control variables in Equation 8; Model 2 added the direct effects of the independent variables, and Model 3 also included the interaction effect. As demonstrated by the R-squared values in the table, the control variables explained 55% of the variation in knowledge transfer, whereas the direct effects explained an additional 3% and the interaction effect an additional 10%. The strong explanatory power of our control variables is not unexpected given their high correlation with knowledge transfer and their strong conceptual link to this variable, and it suggests that we have adequately controlled for other factors besides our hypothesized variables. In comparison, the limited explanatory power of the direct effects alone, and their insignificant coefficients in Model 2, may at first seem surprising. However, it becomes clear that this apparent insignificance conceals an omitted variable bias as soon as the interaction is added. Theoretically, this means that we cannot say anything universal about the effect of external knowledge independently of internal knowledge since the direction of the impact of external knowledge is contingent on the level of internal knowledge.

The incremental F tests in Table 4 show that the increase in R-squared resulting from each new addition to the model is highly significant and suggest that we can therefore proceed with Model 3 for hypothesis testing. Table 5 shows the full model with all three equations and control variable coefficients. Overall, the equation system works well with many significant variables and reasonably high R-squared values. The instruments for internal and external knowledge are all significant and explain 13% to 15% of the variation in those variables. The standardized beta coefficients indicate that subsidiary age and dependency are the most important predictors of internal knowledge and that the perceptions of the host country environment in terms of cluster factors and institutions have the strongest impact on external knowledge. Conversely, although science per capita is highly significant, its effect on external knowledge is smaller, perhaps because this measure (unlike the perceptual ones) implicitly aggregates the technological environment up to the country level and thereby fail to capture knowledge spillovers on a more localized level (Jaffe et al., 1993). Among the control variables in the knowledge transfer equation, formal (MNC) recognition of subsidiary knowledge and subsidiary investments are the most important judging from the standardized estimates—one standard deviation change in each of these variables is associated with a change in knowledge transfer of 0.44 and 0.37 standard deviations, respectively. This indicates, as expected, that a high level of knowledge accumulation in a subsidiary is associated with a high level of knowledge transfer to the rest of the MNC network. Having European headquarters has no effect on knowledge transfer, suggesting that the subsidiaries are able to transmit technological knowledge over long as well as shorter distances.

Our two hypotheses are tested by the coefficients on the two knowledge sources and their interaction, which is marked in bold in Table 5. Hypothesis 1 is supported by the positive and significant coefficient of the interaction effect, as well as by the significant incremental F-test reported above. With a standardized beta of 0.60 and an increase of 0.10 in R-squared—almost three times the increase provided by the direct effects alone (cf. Table 4); this interaction clearly has strong explanatory power in our model. This suggests that the complementarity between internal and external knowledge is crucial to building fungible competences on a subunit level and that failing to account for this complementarity would seriously obscure the mechanisms behind knowledge transfer.

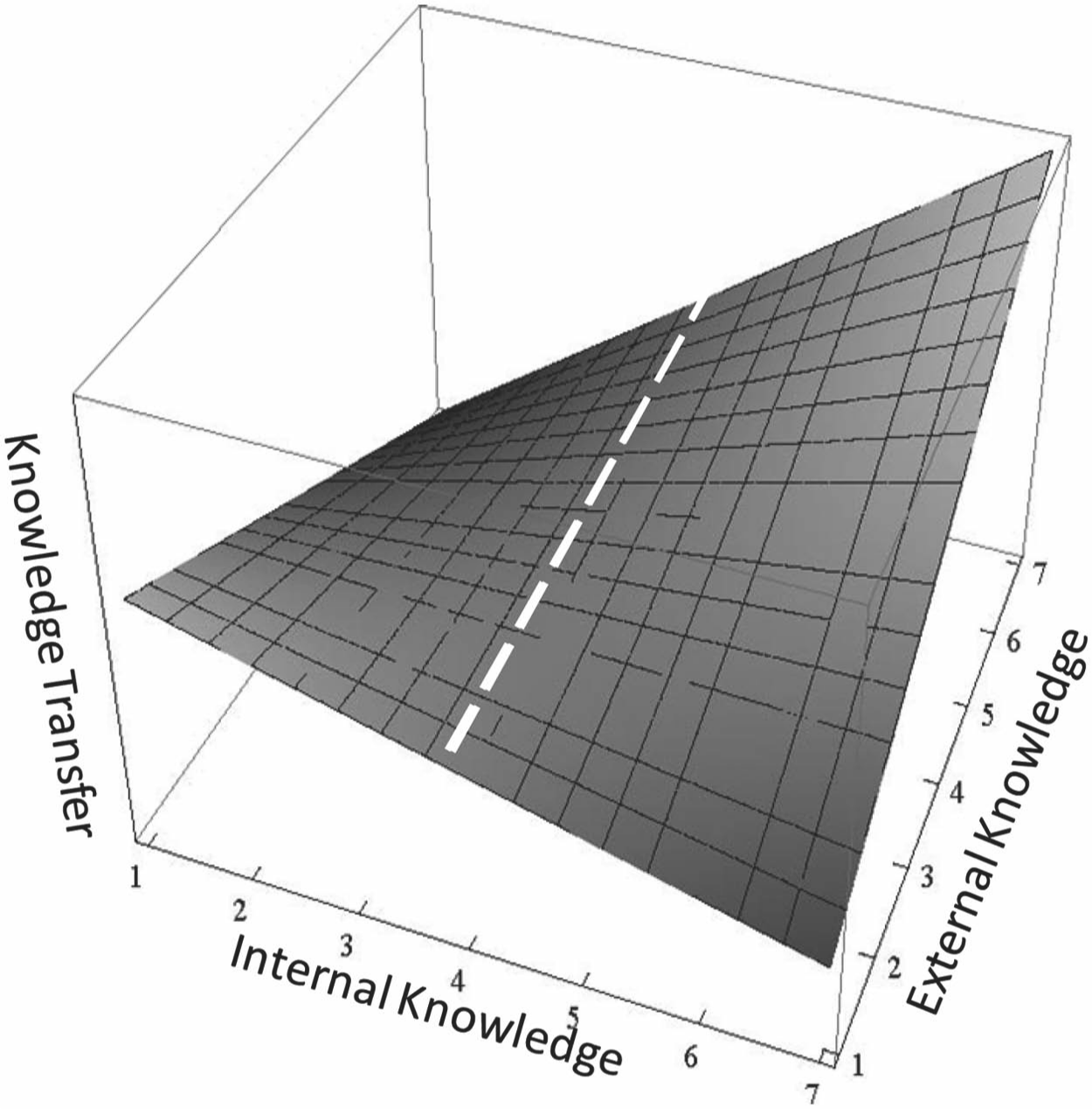

Hypothesis 2 expresses the idea that the accumulation of external subsidiary knowledge is associated with knowledge transfer only when internal knowledge is above a certain tipping point, as suggested by our theoretical discussion of accommodation and assimilation. The hypothesis is evaluated by applying Equation 9 to the estimated coefficients on external knowledge and the interaction effect, leading to an estimated tipping point of

Tipping Point (

The tipping point is shown as a dotted white line where the relationship between external knowledge and knowledge transfer “tips” from a negative to a positive one. A segmentation of our sample subsidiaries around this point illustrates the managerial implications of our results. Only 34% of the subsidiaries in our sample have reported a level of internal knowledge above (in Figure 1, to the right of) this tipping point; these subsidiaries can be considered potential scanning units or centers of excellence for external knowledge sourcing. This leaves the remaining majority of the subsidiaries (66%) who have internal knowledge below the tipping point (to the left of the dotted line). The more external knowledge these subsidiaries possess, the less they tend to transfer to the rest of the MNC. Although we cannot directly observe the cognitive processes going on in these subsidiaries, this result is consistent with accommodation taking place. The configuration that is least conducive to knowledge transfer is (I,E) = (1,7), whereas the most conducive is (I,E) = (7,7), and going from the former to the latter is associated with an increase in knowledge transfer of almost 3—sufficient to turn a completely isolated subsidiary into a subsidiary whose knowledge is in fact moderately useful to other MNC units.

As a post hoc estimation, we conducted an ANOVA analysis on the two groups of subsidiaries clustered by the tipping point, namely those above the tipping point (I > 3.8) and those below the tipping point (I < 3.8). Table 6 reports the results of this analysis, which indicates a remarkable and statistically significant difference between the two groups. In particular, the group of subsidiaries above the tipping point is characterized by higher transfer of technological knowledge, higher external knowledge, higher subsidiary investments, and a stronger tendency for its knowledge to be formally recognized and for the rest of the MNC to be dependent on this knowledge. Generally, these variables are also the ones that were the most significant in the 3SLS model. In contrast, there is no significant difference in the propensity of the subsidiaries to belong to a European MNC, as both groups have 70% of their subsidiaries reporting headquarters in Europe. Also, somewhat surprisingly, the two groups do not differ in their assessment of own technological knowledge. This may indicate that merely having knowledge is not sufficient: Before a subsidiary can provide value to its peer units, this knowledge must be fungible and congruous in relation to the rest of the MNC. This is apparently quite difficult to accomplish since only one third of the subsidiaries in our sample have enough internal technological knowledge to achieve it.

ANOVA for Subsidiaries Above and Below Tipping Point

Note: N = 2,107.

p < .05. **p < .01.

Concluding Discussion

Contributions

This work advances our knowledge of intrafirm knowledge transfers, specifically intra-MNC knowledge transfers, by building on two key ideas. The first one is that there is a meaningful distinction between knowledge in MNC subsidiaries that mainly stems from internal sources and knowledge that mainly stems from external sources, and that these two kinds of knowledge may interact. Although this idea is not new per se (Frost, 2001), our theoretical exploration and mathematical formulation of this idea yield new implications, particularly in the context of the distinction between accommodation and assimilation effects. Thus, we show that a sufficiently high level of internal knowledge increases (ceteris paribus) the likelihood that the marginal benefits of external knowledge will be positive and also the likelihood that they will outweigh the marginal costs of that knowledge. The wider ramification of this idea—which is embodied in our first hypothesis—is that the complementarity between internal and external knowledge is crucial to building fungible and congruous knowledge on a subunit level and that failing to account for this complementarity may hamper our understanding of knowledge transfer in MNCs.

The second key idea is the distinction between “assimilation” (where recipients incorporate the learned knowledge into their existing knowledge stocks, leaving these largely intact) and “accommodation” (where the acquisition of new knowledge makes the recipients alter some of their existing knowledge structures) effects from cognitive psychology (Dole & Sinatra, 1998; Vosniadou & Brewer, 1987). Applying this distinction in the MNC context made us question whether external knowledge sourcing by subsidiaries is conducive to knowledge transfer, as accommodation effects in subsidiaries may lead to knowledge in that subsidiary becoming less relevant to the rest of the MNC network. This also implies the existence of a tipping point, that is, a level of internal knowledge in a subsidiary that must be exceeded if the (rest of the) MNC is to benefit from knowledge that originates from that subsidiary’s external environment (cf. Hypothesis 2). We identified this tipping point on the basis of data on external and internal knowledge and knowledge transfer from the subsidiary. Our findings reveal that only 34% of the subsidiaries in our sample have reported a level of internal knowledge above this tipping point.

Relations to the Extant Literature

In the literature, a high level of similarity between the sender and receiver of knowledge is often seen as conducive to knowledge transfer (e.g., Reagans & McEvily, 2003). We challenge this view by showing that neither a high nor a low level of similarity is associated with a high level of knowledge transfer. We find that an intermediate level, in which a combination of internal and external knowledge is present, is most highly associated with knowledge transfer. If the knowledge of the subsidiary is too similar to the knowledge held in the rest of the MNC, it may become redundant in the MNC context and be associated with a diminished level of potential innovation and inhibit knowledge transfer. Therefore, our findings are consistent with the idea of dual institutional pressures (Kostova & Zaheer, 1999; Rosenzweig & Singh, 1991), which force the subsidiary to balance its similarity to the host country environment with its similarity to the internal MNC environment. To the extent that the legitimacy obtained from such a balance enables the subsidiary to acquire knowledge from both the internal environment and the external environments, it would be positively associated with reverse knowledge transfer, according to our model. Hence, a balanced approach to subsidiary isomorphism is not only necessary for the subsidiary to obtain the resources it needs to survive but also important in the MNC context, as it increases the benefits that other MNC units can reap from the subsidiary’s knowledge. These benefits are maximized through a combination of internal and external knowledge, where enough overlap exists to make the transferred knowledge useful to the recipient, but not enough to make it redundant. 15

Our study also adds to earlier research into the determinants of knowledge transfer from MNC subsidiaries. For example, Monteiro et al. (2008) hypothesized and found a correlation between internal knowledge inflows (in our model, I) and internal knowledge outflows (K). Although they offered organizational explanations of this correlation (reciprocity and the existence of internal communication channels), our explanation emphasizes the mediating role of the host country environment: Internal knowledge inflows in a subsidiary enable the subsidiary to acquire congruous and fungible external knowledge, which in turn facilitates knowledge outflows. Our study thereby has implications for the notion of absorptive capacity (Cohen & Levinthal, 1990) in the sense that we link subsidiary-level absorptive capacity to overall (MNC-wide) absorptive capacity. For example, if an MNC wishes to establish a subsidiary “listening post” in a lead market (Mudambi & Navarra, 2004) on the basis of a knowledge-seeking motive (Barkema & Vermeulen, 1998; Doz et al., 2001; Ghoshal, 1987) to extract knowledge from competitors and demanding customers (Porter, 1998), it would seem helpful to install local competences in sales and marketing so that the subsidiary can absorb knowledge in a way that is useful for the rest of the MNC. Otherwise, it is conceivable that potentially relevant external knowledge fails to get transferred to other MNC units because of a too low level of internal knowledge. If management suspects that this is the case, internal knowledge may be fostered by, for example, expatriate management or by establishing liaison mechanisms between subsidiaries. Indeed, a lack of internal knowledge was eventually identified as the main reason behind the problems with the Aspire, reflected by Acer America’s design of a product with no standard Acer parts and expressed in concerns that they “didn’t understand Taiwan operations very well” (Bartlett & St. George, 1998: 10). Top management was ultimately able to improve on the situation by sending expatriate executives and engineers to the United States to increase the internal knowledge level of Acer America, as our model would suggest. Although our study is silent on the ultimate effects of knowledge transfer on MNC performance, it does suggest that the task of identifying and obtaining the right balance in knowledge development and acquisition is a difficult and, perhaps, underestimated task faced by internationalizing firms.

Implications for Future Research

This research has some limitations that we hope will be addressed in future research. First, we have no direct measures of the costs and benefits of knowledge transfer but infer them from the knowledge stocks and flows chosen by MNC managers. We do this based on the argument that the proportions of costs and benefits create incentives for managerial action. Therefore, if managers respond rationally to these incentives, a cost–benefit approach is both useful and powerful. Nevertheless, this is not a rejection of the importance of developing more realistic theories about how managers actually make decisions regarding MNC knowledge transfer. Such theories, which could draw on agency theory, behavioral theories of decision making, theories that stress legitimacy, and so on, would be a welcome contribution to our cost–benefit analysis.

Second, our framework is distinct in that we abstract from widely studied knowledge dimensions such as tacitness and complexity (e.g., Kogut & Zander, 1993) and focus instead on the sources of subsidiary knowledge and their implications for knowledge transfer costs and benefits. Although this is a deliberate choice that enables us to focus on less studied, but important, dimensions of knowledge, we do not dispute that other dimensions also matter. Future studies could combine these complementary lenses on knowledge to examine the interaction among fungibility, congruity, tacitness, and complexity.

Third, we have relied on perceptual data to measure knowledge stocks and flows. As mentioned above, the strengths of survey measures are balanced by a number of weaknesses, such as the risk of social desirability biases. A possible avenue for future research could be to try to operationalize our theoretical framework using patent data instead of or, ideally, by combining survey and patent measures. For example, one could measure a subsidiary’s internal and external knowledge by its citations to patents originating inside and outside the firm, respectively, while measuring knowledge transfer with a survey instrument similar to the one we have been using here—an approach that would at the same time eliminate any risk of common method bias.

Finally, the validity of our conclusions is to some extent limited by the strength of our instrumental variables. Although we have made every effort to control for endogeneity, and although no ex post statistical evidence of such endogeneity could be found in our final empirical model, we cannot completely rule out a risk that our estimated tipping point could be biased (although it is not clear in which direction such a bias would occur). It remains a formidable challenge for scholars of the knowledge-based view of the firm to identify appropriate natural or seminatural experiments that would enable us to instrument for organizational knowledge. In combination with our cross-sectional research design, this also makes it difficult to establish econometrically that the relations among knowledge types, complementarities, and knowledge transfer are in fact causal relations.

Nevertheless, whereas we view the idea of knowledge tipping points to be of considerable managerial interest, the tipping point we have estimated is in any case likely to be specific to our sample. The purpose of this article has not been to prescribe a given internal knowledge level but rather to draw attention to the possible existence of an accommodation effect in external knowledge sourcing and to analyze theoretically and empirically the implications of such an effect for foreign subsidiaries and MNCs. In fact, although we suspect that the existence of a tipping point is a generalizable phenomenon, the extent to which the location of such a point is universal is, of course, questionable. This raises theoretical and empirical questions of interest for MNC and international strategy scholars. For example, does the tipping point capture a liability of foreignness in local knowledge acquisition, and how does this liability vary with diversity and distance between home and host country? Are tipping points industry specific? And so on. Building on the approach we present in this article, such questions could be tackled in future research.

Footnotes

Acknowledgements

We thank (without implicating) Mark Casson, Alan Rugman, Rajneesh Narula, Ram Mudambi, and Steven Tallman, as well as seminar audiences at Reading University and Copenhagen Business School, for their comments on earlier versions of this article. Comments from Ulf Andersson and Mia Reinholt in the late stages helped us sharpen the theoretical framework. We are indebted to editor Michael Leiblein for his guidance and to the two anonymous Journal of Management reviewers for multiple rounds of insightful comments that inspired many significant improvements to the article.