Abstract

A congruence model of organizational design suggests that the consistency among strategy, structure, and culture enhances organizational performance. In this study, the author attempts to understand which strategy-structure and strategy-culture contingencies facilitate superior postacquisition performance. From the perspective of task interdependence, the author argues that different acquisition strategies (i.e., unrelated, vertical, related) require different levels of headquarters centralization and interdivisional integration in the organizational structure, as well as different degrees of acculturation in the organizational culture. Based on input/output (I/O) analysis, the author develops theoretical measures for different acquisition strategies to test these arguments. The results from a two-stage model capture the author’s arguments by using a sample of 154 acquisitions in the Taiwanese electronics and information sector.

The acquisition–performance relationship assumes that the purpose of acquisitions is to improve performance (Cording, Christman, & King, 2008). Prior studies on this issue have addressed two sets of factors that affect acquisition performance. First, acquisition performance is proposed to depend largely on the acquirer’s acquisition strategy and the target’s resource characteristics (Makri, Hitt, & Lane, 2010) from the resource-based view of the firm. Second, successful acquisitions are argued to rely on effective organizational integration of both target and acquirer (Barkema & Schijven, 2008; Puranam, Singh, & Chaudhuri, 2009). The literature, however, neglects another factor, the collective effects of the firm’s acquisition strategy and organizational integration, which, as this study shows, may advance this study stream by adding new theoretical insights into the important issue of acquisition performance.

Although there is widespread agreement on the importance of firms’ acquisition integration decisions, whether or how these decisions affect acquisition performance remains unclear. For example, integration and resource reconfiguration are necessary for both target and acquirer to commercialize resources in a coordinated manner, yet the loss of autonomy that typically accompanies acquisition integration can be detrimental to the acquired firm’s capacity for continued innovation (Puranam & Srikanth, 2007). From an intermediate perspective, effects of acquisition integration decisions should be contingent on the acquirer’s acquisition strategy. As suggested by strategy-structure-performance studies (Hill, Hitt, & Hoskisson, 1992), acquisition strategy determines the level of acquisition integration because corporate strategy imposes operating requirements. For meeting these requirements, the administrative structure must provide an adequate climate. Based on Thompson’s (1967) theory of task interdependence, recent extensions of the present study have noted that related and vertical acquisitions enhance acquisition integration through reciprocal and sequential interdependent value chain activities, whereas unrelated acquisitions, relying on lower level of integration, can benefit from pooled interdependence (e.g., Aggarwal, Siggelkow, & Singh, 2011; Bailey, Leonardi, & Chong, 2010).

The ideas that acquisition performance can be influenced by proper strategy and integration choice, though theoretically reasonable, receive little empirical support and thus fail to predict performance. This failure can be derived from two research gaps in prior literature. First, effects of strategy and integration choice on acquisition performance are not simultaneously taken into consideration. Second, vertical, related, and unrelated acquisitions are not carefully differentiated. For the first gap, this study extends the prior literature on acquisition strategy and performance by including acquisition integration choice regarding organizational structure and acculturation processes. In response to the tension between potential benefits and risks associated with firms’ integration choices, I assess comparative perspective on the performance implication of different acquisition strategy. Specifically, I examine the fundamental arguments of the congruence model of organizational design (Tushman & Nadler, 1978), which focuses on the performance implications of the fit among firms’ acquisition strategy, structure, and acculturation (Hill et al., 1992). This study also recognizes that even though researchers account for the influences of strategy and integration, endogeneity is an important point that needs to be explained to understand the specific effects of each component on acquisition performance. If acquisition strategy influences both organizational integration and acquisition performance, a self-selection bias will occur and implications drawn from the analyses may be incorrect (e.g., Leiblein, Reuer, & Dalsace, 2002). Therefore, to explicitly explain the potential self-selection bias, I employ a series of two-stage designs that permit an integrative model capturing firms’ acquisition integration decisions as well as the strategic antecedents of these decisions and their performance implications. Regarding the second gap, I develop theoretical measures for different acquisition strategies based on input/output (I/O) analysis. Compared to the SIC-based measures of related and unrelated diversification, this study contributes to the literature by introducing a vertical index for two reasons. One is that the strategic intention of vertical acquisition, different from that of related and unrelated acquisitions, concerns specialized investments, which in turn generate productivity gains for the acquirer (Kretschmer & Puranam, 2008). The other reason is to reduce classification errors by using the traditional SIC construct (Fan & Lang, 2000).

This study highlights the importance of aligning acquisition strategy with acquisition integration and controlling endogeneity bias in assessments of acquisition strategy, integration, and performance outcomes. The contribution of this article is twofold. Theoretically, I extend acquisition studies by means of including integration choice regarding organization structure and acculturation process and explaining the collective effects of firms’ strategy, structure, and acculturation on acquisition performance. Methodologically, I develop measures of acquisition type, derived from a detailed I/O analysis of 161 industries. The adoption of a two-stage model effectively eliminates the potential self-selection bias regarding endogenous selection of acquisition strategy and integration choice. This empirical study captures my arguments by using a sample of 154 acquisitions over 7 years in the Taiwanese electronics and information sector.

Literature Review

Postacquisition Integration and Performance in the Combined Firm

Postacquisition integration, the level of interaction and coordination between the target and acquiring firms (Larsson & Finkelstein, 1999), brings the combination of activities within a common organizational boundary following an acquisition. While interaction postures are conducive to leveraging tacit knowledge embodied in physical artifacts, coordination postures provide superior access to the explicit knowledge embodied in documents and procedures (Puranam & Srikanth, 2007). As firms are combined within the common administrative boundaries, acquirers can use common authority, incentives, and processes to enhance coordination and mutual adaptation to reduce operational costs (Datta, 1991).

Although little empirical literature (e.g., Puranam, Singh, & Zollo, 2006) has examined whether acquisition integration choice affects performance, numerous case studies have described the potential advantages and risks of integration. Moreover, it is argued that the acquired firms’ autonomy in structure and culture preserves tacit and socially embedded technologies (Grabner, 2004). However, as autonomy restricts effective coordination, it thus harms the acquirer in leveraging acquired firms’ technologies. Puranam and Srikanth (2007: 807), observing that “integration enhances coordination at the expense of autonomy,” identify two major effects in acquisition integration, namely, coordination effect and loss of autonomy effect. In general, the coordination effect occurs by means of minimizing functional redundancy and joining daily activities, which helps the acquirer leverage the target firm’s capability. Moreover, the coordination effect may enhance reciprocal predictability of both sides’ actions through daily interaction and further strengthen mutual adjustment and adaptation (Galbraith, 1974). In addition to its effects on organizational structure, integration also shapes the informal processes (i.e., acculturation) that help to create organizational identity, common knowledge, and informal communication channels as well as bring the merging entity to cohesion. However, integration may also incur costs of “loss of autonomy effect” in several ways. First, the employees of the acquired firm may reduce their motivation and productivity after acquisition integration. Moreover, arguments from agency theory suggest that acquisition integration may weaken talented employees’ intrinsic motivation of participating in innovative activities because they are forced to cooperate in other colleagues’ tasks and therefore reduce their autonomy of concentrating on their own tasks. If free riding and agent opportunism further weaken the link between effort and reward, talented employees, especially those with hard-to-measure skills, could possibly leave (Kretschmer & Puranam, 2008). With regard to the acquired managers, as they lose their power and authority to make decisions, they may leave the merged organizations as well (Cartwright & Cooper, 1994). Ultimately, high turnover among the top management team and loss of human and social resources in the acquired firm will have a deleterious impact on acquisitions (Hambrick & Cannella, 1993). Also, as acquisition integration proceeds, the work practices in the acquired firm will change, which may also alter valuable organizational routines of the target firm and consequently leads to disruption (Puranam et al., 2009).

Organizational Structure and Performance in the Combined Firm

Chandler (1962) proposed that strategy–performance studies should emphasize the importance of implementation, for it determines whether a strategy results in superior performance. This model also suggests that firms should adopt different strategies in their life cycle to meet objectives of growth and profit. Thus, as firms diversify by acquisitions, superior performance is argued to be the outcome of establishing a correct fit between strategy and structure (Hill et al., 1992). Centralized multidivisional (CM-form) structure and decentralized multidivisional (M-form) structure are regarded as two classic organizational structures for achieving diversification strategy (e.g., Chandler, 1962; Harrison, Hitt, Hoskisson, & Ireland, 2001; Hoskisson, Hill, & Kim, 1993; Williamson, 1985). Based on Williamson’s (1985) study, a CM-form structure is multidivisional with high headquarters centralization and high interdivisional integration, whereas an M-form structure has low headquarters centralization and low interdivisional integration. Regarding divisional autonomy, the CM-form headquarters tend to constrain business-level strategies and operational decisions. In other words, the headquarters of CM-form firms are highly involved in operational activities of each division. As Hill et al. (1992) argue that related diversified firms should ensure resource sharing and skill transfer among the headquarters and divisions, a CM-form structure is thus suitable for related diversification (Hoskisson et al., 1993). In the M-form structure, the headquarters, on one hand, tend to delegate operational decisions to divisions. This extensive autonomy allows divisions to develop their own management systems and subcultures. On the other hand, the M-form headquarters must design appropriate incentive and control systems to supervise divisional performance and reallocate organizational resources to the most promising and expanding divisions. Such an M-form arrangement is argued to be appropriate for unrelated diversification (Hill et al., 1992).

Effects of Acculturation in the Combined Firm

Cultural integration, “the creation of positive attitudes toward the new organization and the emergence of a sense of shared identity and trust among organizational members” (Stahl & Voigt, 2008: 162), is argued to be the biggest challenge of acquisitions. As Larsson and Finkelstein (1999) have noted, the support from the acquired firm’s employees is contingent on proper cultural integration or the extent to which they perceive their culture to be compatible with the acquirer. Dissimilar or incompatible cultures may cause feelings of hostility and significant discomfort, which can hinder the acquired firm’s employees from committing to and coordinating with the acquirer. Besides, Stahl and Voigt (2008) argue that the execution of a well-designed cultural integration process is essential to minimize intercultural friction and capture expected acquisition gains.

The concept of acculturation was first introduced by Berry (1980), who studied the cultural integration process of individuals entering different ethnic or national cultures and afterward referred to acculturation as “the dual process of cultural and psychological change that takes place as a result of contact between two or more cultural groups and their individual members” (Berry, 2005: 698). Moreover, acculturation involves changes of social structure and cultural practices at the group level and changes of personal behavior at the individual level. Adopting Berry’s view of social anthropology, management researchers (e.g., Nahavandi & Malekzadeh, 1988) have proposed that postacquisition culture involves a dynamic tension between forces of cultural differentiation (the side of the acquired firm) and forces of organizational integration (the side of the acquirer). Larsson and Lubatkin (2001: 1574) further define acculturation in acquisitions as the “outcome of a cooperative process whereby the belief, assumptions and values of two previous independent work forces form a jointly determined culture” and find out that whether acculturation is achieved depends on how well the acquirer manages the acculturation process. This process also helps to explain pressures of conforming to the acquirer’s values and practices on the acquired employees, and reasons why the acquired employees tend to resist such cultural pressures. In addition, aspects of cultural integration, such as trust and mutual respect, will make capability transfer and resource sharing easier if a cultural integration is well executed (Berry, 2005). The acculturation process, nonetheless, is not always identical in all acquisition types. For example, in unrelated and vertical acquisitions where the domain and industry of two firms are dissimilar, the acquired firm is expected to maintain autonomous in culture, unaffected by the acquirer’s culture (Larsson & Finkelstein, 1999). As in related acquisitions, instead of having autonomy, acquired firms are expected to conform to the acquirer’s culture, for the acquirer believes that operating profits can be achieved through combination.

Theory and Hypotheses Setting

Task Interdependence Between Target and the Acquiring Firms

In avoidance of possible conflicts between target and acquirer, proper selection of acquisition integration regarding organizational structure and acculturation process is challenging for the acquirer (Puranam & Srikanth, 2007). As the execution of a well-designed integration process depends on the nature of task interdependence between target and acquirer, the needed extent of integration in different types of task interdependence have been central to theories concerning how to organize the combined organization after acquisition (Kretschmer & Puranam, 2008). Interdependence, the “value of performing one activity depends on how another activity is performed” (Puranam et al., 2009: 315), is argued to affect people’s action by determining the necessary extent of interaction, consultation, and material exchange. Along these lines, task interdependence is defined as the manner in which divisions interact and depend on one another for resources and knowledge to accomplish their tasks (Bailey et al., 2010).

From a coordination perspective, information processing activities and decisions on allocating tasks among people enable mutual adaptation between acquiring and target individuals. As long as employees of both sides can reach agreement through communication, decision making, and task implementation, they can continue their respective tasks and believe that the other’s task will be aligned to their own. Integration in acquisition presents the extent to which the target’s functions are linked to or aligned with the equivalent functions of the acquirer (Zollo & Singh, 2004). Drawing on Thompson’s (1967) pioneering work, the required extent of integration relies on degrees of task interdependence and capability transfer necessary for acquisition implementation. The model of pooled, sequential, and reciprocal interdependence indicates different levels of integration required in acquisitions, in which reciprocal interdependence is suggested to require the highest degree of integration, whereas pooled interdependence requires the lowest (Puranam et al., 2009).

Acquisition Strategy and Organizational Structure

In an unrelated acquisition, work does not flow between acquired and acquiring firms. Even though working independently, the acquired firm, as one part of the combined organization, contributes to the common good of the organization. In other words, the acquired unit behaves as a self-contained division “to the extent and degree that the conditions for carrying out its activities are independent of what is done in the other organizational units” (March & Simon, 1958: 28). When divisions (the target firms) are self-contained, each division should have its own set of support functions and control systems (Chandler, 1962) because a centralized set of support functions and control systems cannot satisfy the needs of different product divisions. The benefits of unrelated acquisition are mainly gained through pooled interdependence, which requires only minimal integration. As few information processing activities and day-to-day coordination are demanded among self-contained units, unrelated acquisitions have the lowest need for coordinating efforts of both merged firms. This also allows the acquired firm to have considerable autonomy and frees top managers of the acquirer from being involved in the daily activities of the acquired firm.

Since unrelated acquisitions require high degrees of divisional autonomy and low degrees of coordination, an M-form structure is argued to be appropriate (Hill et al., 1992). Decentralized divisional managers, on one hand, are given autonomy by the headquarters for relevant operational decisions. On the other hand, the headquarters establish objective financial criteria for divisional performance, based on which each division is offered different levels of incentive (Hill et al., 1992). On this competitive basis, the headquarters can thus adopt the least cost behavior and capital flow for high-yield uses. To conclude, an M-form structure in unrelated acquisitions avoids performance ambiguities and bureaucratic costs that hinder divisional and organizational performance. Thus,

Hypothesis 1a: The interaction between unrelated acquisition and the degree of headquarters centralization is negatively related to postacquisition performance.

Hypothesis 1b: The interaction between unrelated acquisition and the degree of interdivisional integration is negatively related to postacquisition performance.

Vertical acquisition strategy is based on sequential interdependence where resources flow unidirectionally from one division to the other (Hoskisson et al., 1993). This is a high level of interdependence because the merged division and the acquirer’s preexisting divisions exchange resources and depend on others to have a better performance. Vertical acquisitions often provide opportunity for the acquirer to integrate resources and knowledge across different value chain activities. As benefits of vertical integration come from reducing transaction costs (Williamson, 1985), building entry barriers, and enriching product portfolios, firms usually invest in specialized assets (e.g., physical and human resource specificities). These specialized investments typically increase the specialization of organizational subunits, indicating that different divisions take on different subsets of organizational tasks (Kretschmer & Puranam, 2008). Specialization here refers to the condition that employees become proficient at dealing with given assignments, whereas specialized assets refer to investments on specialized devices to reduce cost of production. In general, as the specialization of tasks progresses, the interdependency of the specialized parts increases. Moreover, divisions across different value chain activities need to be tightly integrated owing to the need of resources to flow from one operating division to the next (Thompson, 1967). A coordination effect of integration in vertically combined firms occurs when proper incentives are provided (Kretschmer & Puranam, 2008). For instance, reward schemes that emphasize coordination rather than divisional performance can lead to cooperative behavior across divisions. A coordination effect also arises through shared experience and culture, so that members of both combined firms are willing to cooperate and pursue the common goals of the organization. Loss of autonomy effect is contrarily slight in vertical acquisitions because of the fact that the acquirer needs managers of the acquired firm to operate the business, at least for a time, until the acquirer becomes familiar with the operations. More important, vertical acquisitions are less likely to incur layoffs of the acquired employees (Harrison et al., 2001).

In consideration of sequential interdependence in vertical integration, Child (1984) argues that centralization is necessary to achieve coordination. Within the combined firm, interdivisional coordination is facilitated by three centralized mechanisms: programming, hierarchy, and feedback (Galbraith, 1974; March & Simon, 1958). Programming involves interdivisional arrangement and agreement on what (e.g., standards and procedures) and when (e.g., plans and schedules) actions must be implemented. Hierarchical mechanisms (e.g., centralized authority) enhance coordination by ordering individuals tasks of coordination and informing them about how differently those interdependent actors should behave. When daily programming is important, coordination mechanisms such as cross-divisional meetings and teamwork are necessary to provide feedback on an ongoing basis. Such daily feedback further enables mutual adjustment and adaptation across the target and acquirer. Thus, sequential interdependence in vertical acquisition encourages the headquarters to retain control over the target and adopt a CM-form structure.

Hypothesis 2a: The interaction between vertical acquisition and the degree of headquarters centralization is positively related to postacquisition performance.

Hypothesis 2b: The interaction between vertical acquisition and the degree of interdivisional integration is positively related to postacquisition performance.

Related acquisition strategy concerns the realization of economies of scope associated with reciprocal interdependence (Hoskisson et al., 1993). A coordination effect of integration between related combined firms can arise in two ways. First, in terms of inputs and outputs utilization of related activities, tangible (e.g., joint development of shared production) and intangible (e.g., knowledge transfer) interdependences between target and acquirer are exploited to achieve organizational tasks. Reciprocal interdependence tends to occur in a related combined organization with what Thompson (1967) has described intensive technologies, in which various products and services in combination are provided to its customers. Through interdivisional integration with sufficient coordination, related acquisitions can contribute to the acquirer’s goal of expanding its market to other related markets or product lines (Cording et al., 2008). Second, a coordination effect of a related acquisition may encompass all possible coordination effects of a vertical acquisition. For example, the design/manufacturing relationship (DMR), in which the purpose of sending designs to the manufacturing sector is to test whether these designs can be manufactured or need further modification, seems to be a sequential interdependence because products are typically manufactured after being designed. Nevertheless, from a broader perspective, DMR may be involved in new product development projects, in which not only design and manufacturing but also R&D and marketing have to be intensively coordinated in a reciprocal fashion. Moreover, each of these divisions will receive feedback from all the other divisions to manufacture a product fulfilling customer needs. In general, the reciprocal character can be considered as a higher order of interdependence, which encompasses a lower sequential interdependence.

The costs of loss of autonomy in related integration can be understood in two ways. First, firms of closely divisional interdependence may suffer from performance ambiguities (Harrison et al., 2001). Second, it is argued that takeover resistance is more likely to occur in related acquisitions. Because of high degrees of integration, functions of the acquired organization tend to be aligned or combined with the equivalent functions of the acquirer in related acquisitions (Zollo & Singh, 2004). It is thus likely that the acquirer might replace managers and lay off surplus employees. Because knowledge and experience are market and product specific, the success of market expansion usually depends on the retention of the target’s managers to understand how to integrate and coordinate the combined organization’s resources and subsequently turn them into new market opportunities (Cording et al., 2008). Given these costs from loss of autonomy, why do acquirers integrate related acquisitions instead of giving autonomy to related targets? Puranam et al. (2009) argue that gains from coordination will outweigh costs from loss of autonomy if high levels of interdependence between tasks underlie the target’s and the acquirer’s capabilities. In general, successful related acquisitions require intense coordination and functional experts to enhance horizontal and vertical communication between divisions and headquarters. Moreover, the acquirers can also avoid the loss of autonomy effect by means of establishing a reward scheme, emphasizing interdivisional coordination instead of divisional performance, and retaining talented employees of the acquired firms. Thus, a CM-form structure meets the strategic requirements of a related acquisition: tightly coupled divisions controlled by the centralized headquarters.

Hypothesis 3a: The interaction between related acquisition and the degree of headquarters centralization is positively related to postacquisition performance.

Hypothesis 3b: The interaction between related acquisition and the degree of interdivisional integration is positively related to postacquisition performance.

Acquisition Strategy and Postacquisition Acculturation

In unrelated acquisitions, associated with pooled interdependence, the maintenance of autonomous operations and business practices should be emphasized in the acquired firms (Hitt, Hoskisson, Ireland, & Harrison, 1991). Regarding organizational culture, the acquired employees wish to preserve their own culture in unrelated acquisitions (Larsson & Finkelstein, 1999). Furthermore, managers in headquarters see themselves as supporters, intending to further facilitate the development and growth of the acquired firms. As a result, they tend to minimize interference over the unrelated acquired firms and show tolerance or respect toward multiculturalism, which refers to “the degree to which an organization values cultural diversity and is willing to tolerate and encourage it” (Nahavandi & Malekzadeh, 1988: 83). In addition to operation and business practices, the acquired firms are permitted to maintain their values of autonomy and independency, and only a low level of postacquisition acculturation is necessary. So,

Hypothesis 4: The interaction between unrelated acquisition and the degree of postacquisition acculturation is negatively related to postacquisition performance.

Firms vertically integrate because the division of labor and specialization of productive activities increase manufacturing productivity. In a vertically merged firm, divisions of sequential interdependence must devote themselves to corporate performance rather than divisional performance. Flexibility and cost advantages are achieved by combining design and manufacturing in all value chain activities. To cope with keen competition, vertical integration in manufacturing industries usually includes joint design and joint development functions to reduce the time spent on preparing for mass production. In this business model, head offices have to integrate their various operation processes and inside suppliers. Thus, gains of vertical integration cannot be realized without the help of the target’s and the acquirer’s managers. In addition to its impact on formal structure and systems of the merged unit, organizational integration also shapes informal processes by means of creating informal communication channels and group identity, which helps to share values and transfer knowledge (Puranam et al., 2009). These informal influences may be strengthened if organizational integration also brings forth high degrees of interaction between the merging firms with a coordinated effort into the quality of interaction (Larsson & Finkelstein, 1999). Thus, a high degree of acculturation is required in vertical acquisition.

Hypothesis 5: The interaction between vertical acquisition and the degree of postacquisition acculturation is positively related to postacquisition performance.

In related acquisitions, especially when the acquired unit offers supplementary capacities to the acquirer and possesses unique technical advantages, a high degree of integration will be necessary to promote divisional coordination and knowledge transfer within the new organization (Håkanson, 1995). Because of a lack of autonomy, activities of the acquired firm increasingly depend on operational and strategic decisions by the acquirer, which may accompany redirection and redefinition of missions and objectives as well as destroy the acquired firm’s previous identity and culture. A similar perspective by Larsson and Lubatkin (2001) also indicates that superior performance in related diversification over a prolonged period requires a strong and adaptive uniculture, in which managers should not only emphasize the uniqueness of employee values, norms, and rewards systems but also aim to achieve consistency in corporate goals, strategies, and practices among the acquiring and acquired firms. Consequently, the acquired firm is expected to be fully acculturated into the culture and practice of the dominant acquirer if target and acquirer have reciprocal interdependence (Cartwright & Cooper, 1994).

Hypothesis 6: The interaction between related acquisition and the degree of postacquisition acculturation is positively related to postacquisition performance.

Method

Possible Self-Selection Biases and the Two-Stage Analytic Technique

This study investigates the impact of acquisition strategy and organizational integration on acquisition performance. Here the endogenous selection of acquisition type and organizational integration is important in acquisition performance studies (Shaver, 1998). If acquisition strategy influences both organizational integration and acquisition performance, a self-selection bias can occur and the analyses may lead to incorrect implications (Miller, 2006). As the typical sequence of acquisitions is that the acquirer (a) chooses the acquisition strategy and (b) determines the level of integration, the need for postacquisition integration is primarily bounded by the acquirer’s strategy (Datta, 1991). Since the firms are able to self-select the observed level of acquisition integration based on their performance-maximizing analyses, it is probable that the observed acquisition performance is conditional on acquisition type, which influences the acquirer’s choices regarding organization structure and acculturation process. To correct the potential self-selection biases, I employ a two-stage technique that contains a first-stage integration choice model and a second-stage performance model (Heckman, 1979). The two-stage models can be summarized as reestimating regression coefficients by adding an adjustment term, the inverse Mills ratio, to the performance model. In this study, the intuition is to correct the estimates in the performance model by controlling for the tendency of the firm to select a choice of high acquisition integration (i.e., acquisition integration choice [high]).

Theoretically, one first estimates a first-stage probit model to introduce a selection equation and then calculates the inverse Mills ratio, which is introduced as a control variable in the second-stage regression analyses (Leiblein et al., 2002). Specifically, I estimate the most likely value for acquisition integration choice (high) for a given acquisition, using the probit model Prob(Yi = 1) = Φ(β’Xi), where Yi is the acquisition integration choice variable for the ith observation, Xi is a vector of characteristics surrounding the acquisition, β is a vector of estimated coefficients for the characteristics, and Φ(·) is the standard normal cumulative density function. The inverse Mills ratio (λji) is defined as λ1i = (ϕ (β’Xi)) / (Φ(β’Xi)) for observations that adopt a high level of acquisition integration (i.e., j = 1) and λ0i = − ϕ (β’Xi))/([1-Φ(β’Xi)]) for observations that do not select high acquisition integration (i.e., j = 0). In both cases, ϕ (·) is the standard normal probability density function. The two-stage models that introduce this correction of self-selection biases provide consistent and unbiased estimates of regression coefficients (Heckman, 1979).

Data Collection

I collected data at the financial, organizational, and industrial levels of acquisitions in the Taiwanese electronics and information industry. Corporate financial data were collected from the databases in Securities and Futures Commission, Ministry of Finance, Taiwan. Industrial data and I/O tables were obtained from the Directorate General of Budget, Accounting and Statistics, Taiwan. 1 Organizational-level data were drawn from the top 1,000 Taiwanese electronics and information firms reported by China Credit Information Service, an authorized credit-rating company in Taiwan. In the research period (2002–2008), 397 of the top 1,000 firms had undertaken acquisition. Because sufficient time to complete postacquisition integration may be required (Puranam et al., 2006), and because the main point of this study is to examine the effects of integrating organizational structure and culture after acquisition, I thus define the acquisition year (t = 0) as the year that the acquisition happens, the preacquisition year (t = −1) as one year before the acquisition, and the postacquisition year (t = +1) as one year after the acquisition. Questionnaires that contain descriptions of organizational structure and acculturation after acquisition integration were distributed to general managers of these 397 target firms one year after the acquisition has completed (t = +1), and 154 were returned. Questionnaires were distributed to managers of target firms because only managers of acquired firms actually know how intensely the target firm is integrated with the acquirer. Data of unrelated/vertical/related acquisitions were collected and calculated from industry I/O tables, and control variables were collected from the acquirer’s data in databases.

Measures

Acquisition performance

Strategic management studies on diversification and acquisition performance have sought to refine the measures of performance. For examining the diversification–performance relationship, Palich, Cardinal, and Miller (2000) investigate meta-analytic data from 55 previously published studies. In their regression work, the set of correlations based on accounting performance measures are analyzed separately from the set of correlations based on market measures. The results show that market-based performance measures are more relevant to diversification and acquisition research since they capture expectations of future returns, as opposed to past outcomes reflected in accounting-based measures. The primary dependent variable in the second-stage performance model is market value, calculated as log (price of outstanding common shares × number of shares + book value of preferred stock + book value of debt) (Miller, 2006). The adoption of market value is also common in finance studies on diversification, which suggests that using market-based measures of performance allows better controls of potential endogeneity than using accounting-based measures (Mansi & Reeb, 2002).

Acquisition integration choice

The primary dependent variable in the first-stage probit model is the acquisition integration choice. To examine hypotheses that acquisition performance differs based on the different levels of acquisition integration selected, I define the variable acquisition integration choice (high) equal to one for those firms that select a high level of postacquisition integration (firms that score above the average score on headquarters centralization, interdivisional, integration, and acculturation), and otherwise equal to zero for other choices. The use of acquisition integration choice (high) as a dummy variable also matches the management studies (e.g., Miller, 2006) that adopt the two-stage technique proposed by Heckman (1979). The underlying assumption of the present study is that firms are assigned exogenous acquisition types (unrelated, vertical, or related acquisition) and then select the level and type of acquisition integration (structure and acculturation).

Unrelated, vertical, and related acquisition

I develop measures of vertical, horizontal, and unrelated indexes in acquisitions by theory of I/O analysis. The maximal and minimal related acquisition index values for the sample are 1.00 and 0.00, the maximal and minimal vertical acquisition index values are 0.53 and 0.00, and maximal and minimal unrelated acquisition index values are 0.96 and 0.00. For detailed definitions of these indexes, please see the appendix.

Organizational structure

Two variables can be used to characterize CM-form firms: headquarters centralization and interdivisional integration (Hill et al., 1992). An organization is regarded as CM-form when degrees of centralization and integration are both high. According to the centralization dimension developed by Ghoshal and Nohria (1989: 336), headquarters centralization in this study is measured by divisional managers estimating the degree to which the head office influences divisional (a) introduction of new products, (b) changes in product design, (c) changes in manufacturing processes, and (d) career development plans for senior managers (5-point scale, Cronbach’s α = .85). In the dimension of integration, interdivisional integration, containing operational integration and strategic integration (Burgelman & Doz, 2001), is measured by divisional managers estimating the degree of interdivisional activities in (a) joint procurement, (b) sharing a sales force, (c) sharing production information, (d) sharing best practices in various administrative processes, and (e) involving the combination of resources from different divisions to create new business (5-point scale, Cronbach’s α = .87).

Acculturation

Acculturation is a cultural process through which employees of the target firm are acculturated to the acquirer’s belief, assumptions, and values (Larsson & Lubatkin, 2001). Based on Håkanson (1995) and Larsson and Lubatkin (2001), acculturation is measured by the acquired firm’s managers concerning the level of (a) jointly shared meanings fostering cooperation between joining firms, (b) a joint organizational culture through activities such as cross-visit, celebrations, and other rituals, and (c) the existing culture in the acquired firm being forced to change (5-point scale, Cronbach’s α = .84).

Control variables

As diversification performance studies have suggested, four variables (leverage, preacquisition firm profitability, R&D intensity, change in the overall market) are used to reduce possible endogeneity biases (Miller, 2006). Leverage is measured as the ratio of the book value of debt to market value, as defined in the dependent variable (Mansi & Reeb, 2002). The acquirer’s preacquisition firm profitability is measured as the 3-year average return on assets (ROA) covering the past 3 years (t = −1, t = −2, and t = −3) before the acquisition (Hambrick & Cannella, 1993). It is examined as industry-adjusted profitability by subtracting industry average profitability (industry 3-year average ROA). R&D intensity is the target’s R&D expenditure over total assets in the year before the acquisition (Miller, 2006). Based on the overall stock appreciation for the Taiwanese market, change in the overall market is measured as the overall market value in the postacquisition year (t = +1) minus the overall market value in the preacquisition year (t = −1). Shaver (1998) argues that change in the overall market should be controlled in studies of acquisition performance because it may simultaneously affect acquirers’ performance on market value, as well as their willingness to acquire firms in industries that are growing or recessive.

This study also concerns other control variables. Relative size has been found to positively affect predicting acquisition performance (Datta, 1991). It is measured as the ratio of the sales of the acquired firm to that of the acquirer in the year before acquisition. It seems reasonable to expect a relationship between acquisition experience and acquisition capabilities (Barkema & Schijven, 2008). Acquisition experience is measured as the number of acquisitions completed by the acquirer in the 10 years preceding the observed acquisition. Foreign target, also controlled in this study, is coded as 1 if the target is not from Taiwan and 0 otherwise. Finally, considering that macroeconomic factors might have impact on profitability, 6-year dummy variables are created in the sample with the omitted year 2002. These dummies are not significant in the sample, indicating no significant difference on integration choice and performance across time periods.

Results

First-Stage Acquisition Integration Choice Estimates

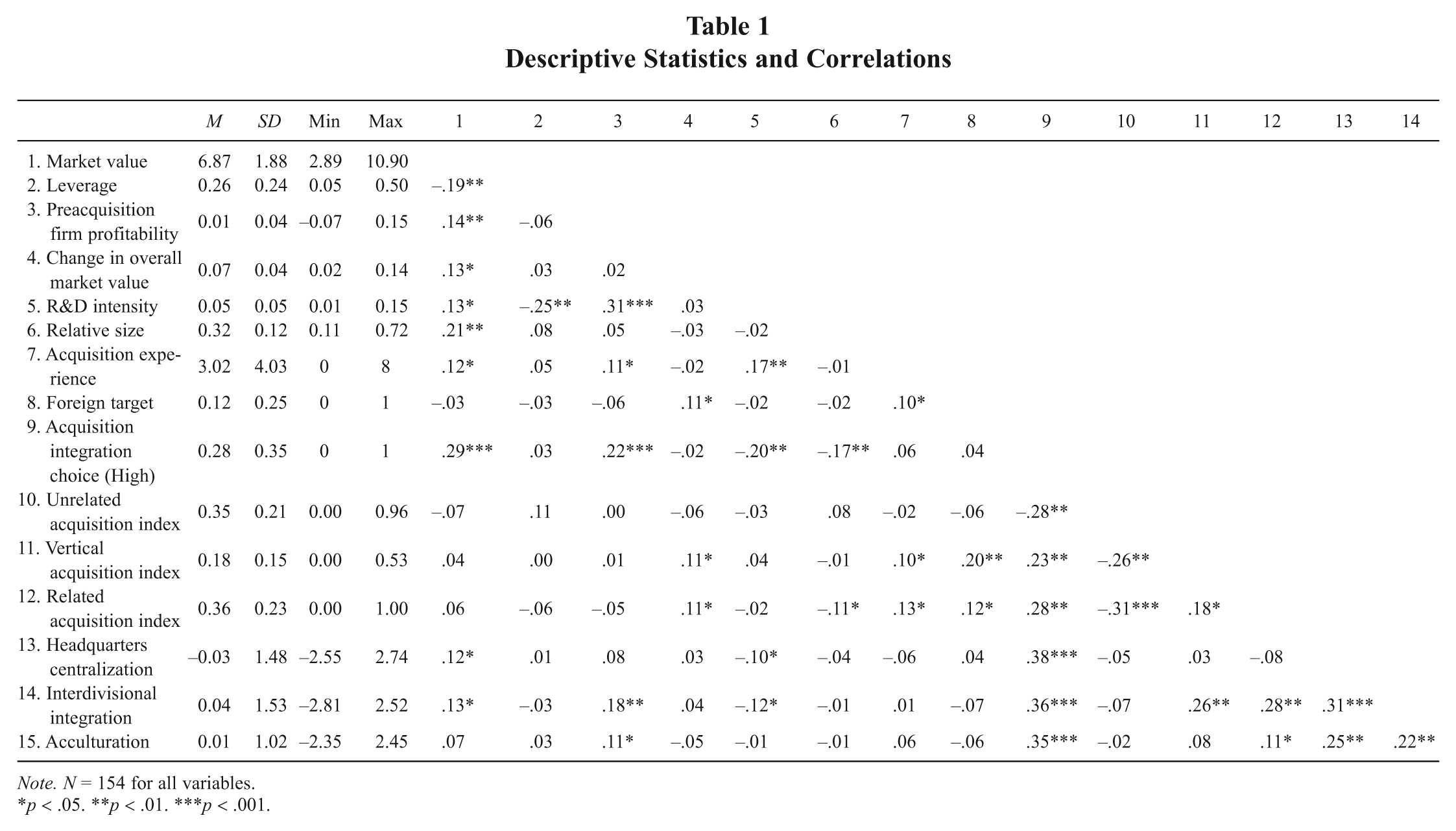

Table 1 provides summary and correlation statistics for all variables. Table 2 presents the result from two potential acquisition integration choice models. The use of acquisition integration choice (high) as an indicator variable makes it relatively straightforward to introduce a choice model (Heckman, 1979). The probit Model 1 in the first step presents a baseline model that includes an intercept and the following variables: preacquisition firm profitability, R&D intensity, and relative size. Consistent with Larsson and Lubatkin’s (2001) findings, the acquirer with superior preacquisition performance tends to impose its organizational structure and management practices on the acquired firm for its knowledge or financial advantages. The acquirer’s culture therefore tries to dominate the acquired firm’s culture. These reasons also increase the probability that firms choose high degrees of postacquisition integration. The negative coefficients associated with the target’s R&D intensity and relative size are also consistent with expectations and the results in the literature. For instance, Puranam et al. (2009) argue that too much acquisition integration is unnecessary for acquiring technological firms. Datta (1991) also indicates that relative size is a predictor of acquisition integration because it may affect the governance choice of resource combination in the postacquisition stage.

Descriptive Statistics and Correlations

Note. N = 154 for all variables.

p < .05. **p < .01. ***p < .001.

Results of First-Stage Probit Regressions Predicting Acquisition Integration Choice (high)

Note. N = 154. Positive coefficients indicate a greater probability of high-level acquisition integration. Dummy variables for each year are not shown, since none of these variables are significant.

Standard errors in parentheses.

Appropriate degrees of freedom are reported in parentheses.

p < .05. **p < .01. ***p < .001.

Model 2 introduces measures of related, vertical, and unrelated acquisition, which are viewed as exogenous variables in second-stage performance model. As suggested by strategy-structure-fit studies (Hill et al., 1992), a firm’s level of acquisition integration shall follow its acquisition strategy. Acquisition strategy must dominate the design of organizational acculturation because “the strategy imposes operating requirements and, in turn, the administrative structure must provide the climate for meeting them” (Ansoff, 1965: 7). Results of Model 2 also confirm the perspective that “structure follows strategy” (Chandler, 1962: 297) and show that acquisition strategy determines the level of consequent organizational integration. The positively significant coefficients of related and vertical indexes reveal that firms undertaking related and vertical acquisition are more probable to select high levels of acquisition integration. Conversely, the negatively significant coefficient of unrelated index reveals that firms undertaking unrelated acquisitions are less probable to select high levels of acquisition integration. The inverse Mills ratio from this model is introduced as a control variable in the second-stage performance model.

Second-Stage Acquisition Performance Estimates

Tables 3 and 4 record results of second-stage regressions designed to illuminate the relationships between acquisition strategy, acquisition integration, and performance. To assess the problem of multicollinearity, variance inflation factors (VIFs) were calculated for each coefficient. VIFs of all associated coefficients range from 1.10 to 3.49, which implies minor multicollinearity. The Durbin–Watson statistics for regression models range from 2.09 to 2.65, also suggesting that autocorrelation does not bias the parameter estimates. As for year dummy variables, I include six dummy variables for each year (except 2002) to control any time-specific variations. Since none of these variables are significant, dummy variables for each year are not shown in the Tables. In Table 3, Model 3 presents a baseline specification including an intercept term, control variables, strategy and structure variables, and a dummy variable of acquisition integration choice (high). While Model 3 does not control self-selection biases, I present the results to demonstrate how the correction for self-selection influences the coefficient of acquisition integration choice (high). The inverse Mills ratio from first-stage probit model is added as a control variable (λ) in Models 4 and 5. The coefficient for λ is significant at the α = .01 level, and its introduction removes significance from acquisition integration choice (high). The significance of coefficient for λ also indicates that firms have self-selected the most favorable type and level of acquisition integration.

Results of Second-Stage Regressions Predicting Market Value

Note. N = 154. Unstandardized regression coefficients reported. Year dummy variables are not shown. Standard errors in parentheses.

All continuous variables used in interaction terms are centered. Results are similar if uncentered.

p < .1. *p < .05. **p < .01. ***p < .001.

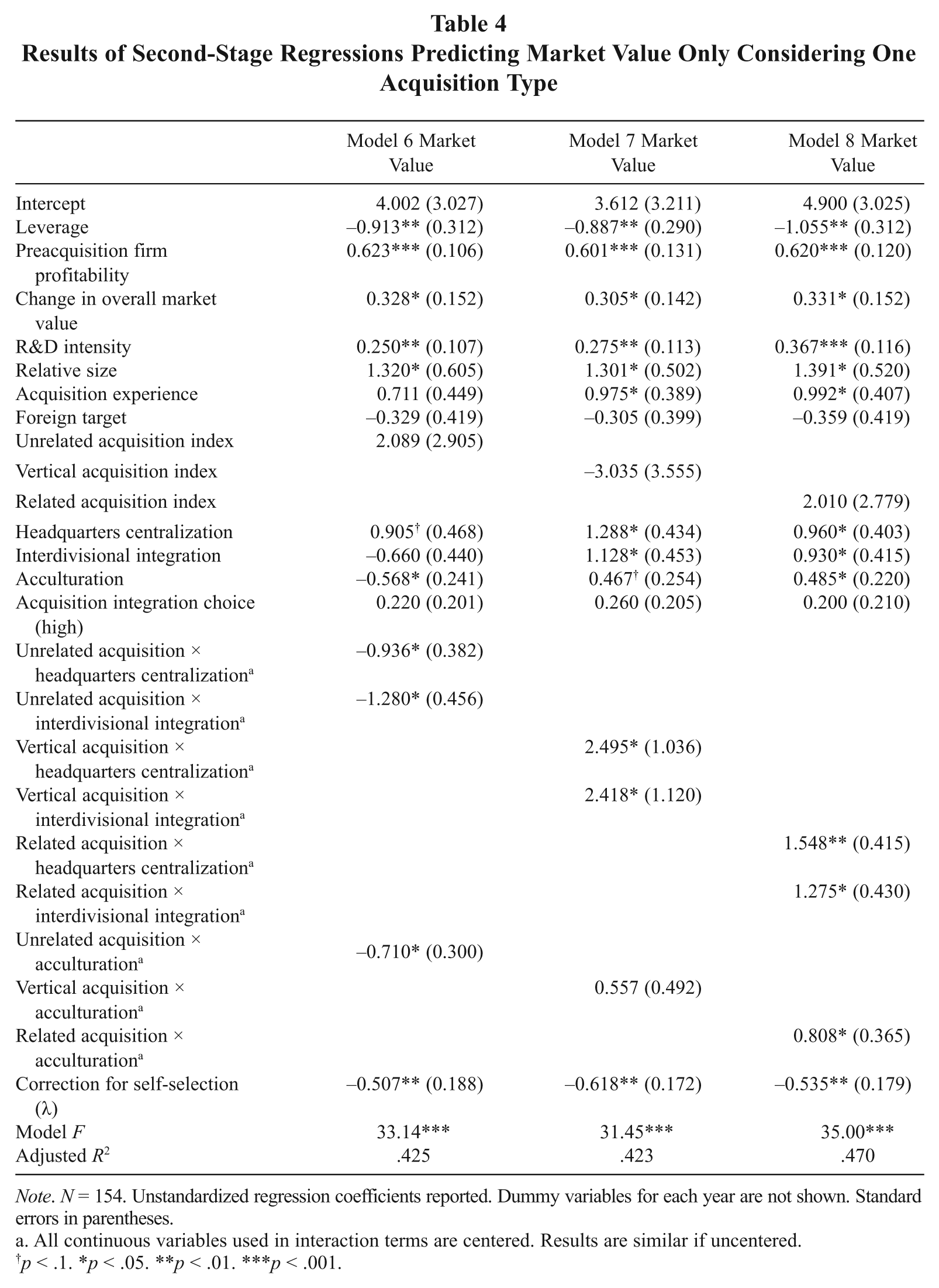

Results of Second-Stage Regressions Predicting Market Value Only Considering One Acquisition Type

Note. N = 154. Unstandardized regression coefficients reported. Dummy variables for each year are not shown. Standard errors in parentheses.

All continuous variables used in interaction terms are centered. Results are similar if uncentered.

p < .1. *p < .05. **p < .01. ***p < .001.

In Model 5, I insert the interaction terms to assess the effects of acquisition strategy × organizational structure and acquisition strategy × acculturation on postacquisition performance. The statistically significant negative interaction terms between unrelated acquisition and headquarters centralization (p < .05) and between unrelated acquisition and interdivisional integration (p < .05) indicate that an M-form structure is beneficial for unrelated acquisitions to achieve high acquisition performance. Hypotheses 1a and 1b are therefore supported. Moreover, the statistically significant positive interaction terms between vertical acquisition and headquarters centralization (p < .05) and between vertical acquisition and interdivisional integration (p < .05) indicate that a CM-form structure is beneficial for vertical acquisitions to achieve high acquisition performance. Hypotheses 2a and 2b are thus supported. The statistically significant positive interaction terms between related acquisition and headquarters centralization (p < .01) and between related acquisition and interdivisional integration (p < .05) suggest a CM-form structure is beneficial for related acquisitions to achieve high acquisition performance. These results also support Hypotheses 3a and 3b. In testing Hypotheses 4 to 6, the statistically significant negative interaction terms between unrelated acquisition and acculturation (p < .05) and the statistically significant positive interaction terms between related acquisition and acculturation (p < .05) support Hypotheses 4 and 6 but not Hypothesis 5.

For carefully examining the interaction terms of each acquisition type, Table 4 further examines interactions, in which only one acquisition type is considered. When concerning unrelated acquisition only, as shown in Model 6, the positively significant coefficient of headquarters centralization (p < .1) indicates a direct effect of headquarters centralization on postacquisition performance (market value). A negatively significant coefficient of unrelated acquisition × headquarters centralization (p < .05) also reveals a negative moderating effect of unrelated acquisition strategy. As shown in Figure 1, the relationship between centralization and acquisition performance will be positive if firms have low degrees of unrelated acquisition index (firms that scored below the average score on unrelated acquisition index). However, the relationship between centralization and acquisition performance will inversely change to be negative if firms have high degrees of unrelated acquisition index (firms that scored above the average score on unrelated acquisition index). With regard to interdivisional integration and acculturation, the results are similar. That is, unrelated acquisition negatively moderates the relationship between interdivisional integration and acquisition performance, as well as the relationship between acculturation and acquisition performance.

Moderating Effect of Unrelated Acquisition on the Relationship Between Headquarters Centralization and Market Value

When concerning vertical acquisition only, as shown in Model 7, the positively significant coefficient of headquarters centralization (p < .05) indicates a direct effect of headquarters centralization on acquisition performance (market value). A positively significant coefficient of vertical acquisition × headquarters centralization (p < .05) also reveals a positive moderating effect of vertical acquisition strategy. In other words, there exists a relatively weakened positive relationship between centralization and acquisition performance in firms with low degrees of vertical acquisition. However, this positive relationship will be enhanced if firms have high degrees of vertical acquisition. With regard to interdivisional integration, the results are similar. That is, vertical acquisition positively moderates the relationship between interdivisional integration and performance.

When concerning related acquisitions only, as shown in Model 8, the positively significant coefficient of headquarters centralization (p < .05) indicates a direct effect of headquarters centralization on postacquisition performance (market value). A positively significant coefficient of related acquisition × headquarters centralization (p < .01) also reveals a positive moderating effect of related acquisition strategy. That is, there exists a relatively weakened positive relationship between centralization and acquisition performance in firms with low degrees of related acquisition. Nevertheless, this positive relationship will be enhanced if firms have high degrees of related acquisition. With regard to interdivisional integration and acculturation, the results are similar. That is, related acquisition positively moderates the relationship between interdivisional integration and acquisition performance, as well as the relationship between acculturation and performance.

Discussion

The fields of strategic and organizational management involve three major research streams. One focuses on the preacquisition stage and finds out that superior acquisition performance strongly depends on cautious selection of target firms (Larsson & Finkelstein, 1999). The other pays attention to the implementation stage in the acquisition processes (Puranam et al., 2006; Puranam et al., 2009), indicating that even with a careful selection of target firms, superior performance still depends on sufficient and effective integration (Barkema & Schijven, 2008). The third emphasizes the difficulties that two organizations face when they combine the existing business units and resolve conflicts between dissimilar cultures, suggesting that the acquisition performance depends on the acquirer–target relationship and proper degrees of acculturation (e.g., Larsson & Lubatkin, 2001; Stahl & Voigt, 2008). By integrating these research streams, I suggest that acquisition strategy and firms’ integration choice interactively influence postacquisition performance. To obtain unbiased results, empirical analyses must address firms’ acquisition integration choice as well as their drivers and performance implications. As self-selection biases could affect normative implications drawn from studies on the performance implication of firms’ diversification decisions (Miller, 2006), the two-stage analysis approach can reduce potential endogeneity problems and allow researchers to develop integrated models of firms’ managerial decisions as well as the antecedents and consequences of these decisions. It could be widely applied to topics such as firms’ governance decisions (Leiblein et al., 2002), market entry decisions (Shaver, 1998), and diversification performance (Miller, 2006).

Studies on organizational integration pay attention to the benefits and costs of acquisition integration (Puranam et al., 2009). Integration can enhance the ability to coordinate task interdependence but simultaneously cause the costs of disruption to the acquired firm. The acquirer is therefore in a dilemma between coordination and autonomy (Puranam et al., 2006). This study concerns the nature and strength of different interdependence (i.e., pooled, sequential, reciprocal), arguing that the gains of coordination through acquisition integration can dominate the costs of disruption if activities between the target and acquiring firm, as in related and vertical acquisitions, are highly interdependent. In the case of interdependence, formal integration, the integration through organizations’ combination within the common administrative boundaries (Puranam et al., 2009), explicitly enacts routines, schedules, and plans, hoping to maximize coordination effect (gains) and minimize loss of autonomy effect (costs). Informal integration, the cooperative acculturation process to form a jointly determined culture (Larsson & Lubatkin, 2001), also implicitly coordinates work by anticipating the actions of the interdependent actors and sharing a common set of norms, values, and beliefs. As acquisition is associated with personnel change, disrupted career prospects, loss of identity and security, and alteration in working practice and culture, lack of understanding acculturation has been blamed for unsatisfied acquisition performance (Cartwright & Cooper, 1994). If the acculturation process is smooth, the acquired firm’s members will feel that the implementation of an acculturation can help them adapt to the new organization. However, if two firms fail to agree on the degree of acculturation, stress and resistance from employees will occur (Nahavandi & Malekzadeh, 1988).

The findings of this study suggest that unrelated acquisitions demand only low levels of acculturation since this strategy realizes economies of internal capital markets. Partners of two sides are relatively independent, in which business in different divisions will be conducted in a “hands-off” manner, and share a financial governance system with minimal cultural exchange. Regarding organizational structure, as different acquisitions require different organizational structures to achieve economic benefits, this study argues that the postacquisition organization in unrelated acquisitions should adopt an M-form structure. As for related acquisitions, the findings suggest that the establishment of effective interdivisional integration and a similar culture is required since economic performance is enhanced through shared values and the utilization of joint inputs or activities. High acculturation occurs when the acquirer’s culture is considered attractive and individual autonomy in the acquired members is less valued. As the acquirer tends to impose its culture on the acquired firm owing to its knowledge-based and technological advantages, the acquired managers may leave the merged organization, for they lose their power and decision-making authority. Thus, how to reduce cultural clashes becomes important for related combinations. Moreover, this study argues that a CM-form structure is appropriate in related acquisitions because of the need of interdivisional coordination based on the nature of reciprocal task interdependence.

In vertical acquisitions, the findings support only arguments of high centralization and high integration but not those of high acculturation. One of the reasons may be that vertical acquisitions involve two firms in different industries but focusing on linked value chain activities in the production process. Their operations and practices are therefore different (e.g., one focusing on manufacturing and the other on marketing). Hence, managers in the merged division need autonomy to apply their specialized knowledge into the business domain, and the acquired firm prefers to preserve its valuable practices and routines. Therefore, high acculturation is not appropriate for the target’s employees because of their professionalism and familiarity in the specialized value chain activities.

Limitations and Suggestions for Future Research

This study has limitations, which in turn provides opportunities for future research. One limitation is the use of a short-term cross-sectional research design in this study. Several authors have used congruence models to argue that the type of fit varies in different organizational life cycles (Hill et al., 1992). Therefore, managers are responsible for designing organizations in ways that best fit environmental and strategic challenges. As long as strategy, structure, culture, and individuals can work together to provide a highly congruent system, a successful organization will be possible. Nevertheless, the results of this study show only short-term performance. The structure and culture that foster success in the current life cycle may cause congruence to be a “managerial trap” (O’Reilly & Tushman, 2004), which becomes a significant barrier to change.

The second limitation concerns the focal industries—high-tech industries—investigated in this study. Because of the fact that all sample firms in this study are in the Taiwanese electronic and information industry, the results are informative in the electronic and information industry and can be generalized only to acquisitions in other technological industries. Moreover, as “technology is an important component of the acquired firm’s assets” in high-tech industries (Ahuja & Katila, 2001: 197), firms adopting technology acquisitions tend to pay more attention to technology interdependence (e.g., intangible technological resources and innovative capacity of the acquired firms), instead of the nature of task interdependence or resource interdependence. Since this study does not discuss technology interdependence but task interdependence, the results do not show significant differences between vertical and related acquisitions. Therefore, a typology concerning the interdependence of target’s and acquirer’s technology may be worthy for future research.

Concerning limitations in measures, one of them is that since the measures in this article are at the industry level, it is possible that the results cannot entirely reflect strategies or conditions at the firm level. With regard to financial performance, while financial performance is generally recognized as a critical indicator for firms, innovation performance (e.g., R&D and patent intensities) is particularly important in technological acquisitions (Hitt et al., 1991). Organizational designs that drive different types of performance are therefore not the same. For example, a mechanistic organizational structure may produce manufacturing efficiency at a low cost, whereas an organic structure enhances technological innovation and growth. When two acquisitions are undertaken simultaneously, with one acquisition for production efficiency and another for innovation, how shall these seemingly inconsistent design elements be resolved? Research on ambidextrous organization (Gibson & Birkinshaw, 2004) does provide a possible clue to understanding how seemingly conflicting designs can coexist in an organization and actually promote long-term success. As both exploitation and exploration are required to achieve persistent success, an ambidextrous organization is generated simultaneously in both tight and loose coupling and composed of highly differentiated and loosely integrated subunits. Therefore, exploratory efforts may be configured as “structurally independent units, each having its own processes, structures, and cultures but integrated into the existing senior management hierarchy” (O’Reilly & Tushman, 2004: 76). Conversely, exploitative efforts that focus on decreasing variance as well as increasing efficiency and control may require enhanced coordination and integration. Although a culture with tight or loose elements requires recruiting new workers to deal with its ambidexterity, the pursuit of ambidexterity is particularly important for long-term adaptation when acquiring firms in multiple, loosely connected domains (Gibson & Birkinshaw, 2004).

Conclusion

This study examines the relationship among strategy, organizational integration, and performance while controlling the endogeneity of acquisition strategy type and integration choice. Conforming to the idea that “structure follows strategy” (e.g., Chandler, 1962; Galan & Sanchez-Bueno, 2009; Hill et al., 1992), the empirical results based on Taiwanese electronics and information sectors indicate (a) tighter acculturation with higher interdivisional integration and headquarters centralization relates to superior performance in related acquisitions, (b) looser acculturation with lower interdivisional integration and headquarters centralization relates to superior performance in unrelated acquisitions, and (c) in vertical acquisitions, only high degrees of interdivisional integration and headquarters centralization facilitate superior performance. Furthermore, this study contributes to the prior literature by considering integration choice of both organization structure and acculturation process as well as explaining the collective effects of organizational strategy, structure, and acculturation on acquisition performance. Methodologically, measures based on I/O construct help to distinguish vertical, related, and unrelated acquisitions, allowing management scholars to classify and investigate different strategies of firms’ diversification and acquisition.

Footnotes

Appendix

Acknowledgements

The author thanks Editor Michael Leiblein and the reviewers for their constructive feedback and Wei-Hsin (Eugenia) Lin for editorial assistance.