Abstract

Strategic human capital research has emphasized the importance of human capital as a resource for sustained competitive advantage, but firm investments in this intangible asset vary considerably. This article examines whether and how external pressures on firms from capital markets influence their human capital strategy. These pressures have increased over the past three decades due to banking deregulation, technological innovation, and the rise of institutional investors and new financial intermediaries. Against this backdrop, this study examines whether a firm’s capital structure as measured by share turnover, shareholder concentration, and financial leverage is associated with firm investment in strategic human capital. Based on survey and objective financial data from 221 establishments in the United States and Canada, our analysis indicates that firms with greater share turnover, higher shareholder concentration, and higher levels of financial leverage are less likely to invest in human resource systems that create strategic human capital. Differences in national financial systems also lead to differential effects for U.S. and Canadian firms.

More than 80 percent of some 400 executives questioned by the academics John Graham, Campbell R. Harvey, and Shivaram Rajgopal admitted they would reduce spending in important areas such as R&D, maintenance, and hiring in order to meet earnings targets.

Research in strategic human resource management has focused extensively on examining the relationship between investments in human resource (HR) systems and their impact on organizational performance. The central argument has been that firms that invest in these HR systems may increase employees’ stock of knowledge, skills, and abilities as a collective resource that has strategic value to the firm—or strategic human capital (Ployhart & Moliterno, 2011). This research builds on the resource-based theory (RBT) of the firm, which argues that human capital may be a strategic asset if it is valuable, rare, and hard to imitate (Barney, 1991; Wright & McMahan, 1992).

Human capital has been widely acknowledged as a source of sustainable competitive advantage since the 1980s, when the field of strategic HR management and the resource-based view of the firm emerged. Much research has been devoted to examining the relationship between investments in HR systems and organizational performance (Combs, Liu, Hall, & Ketchen, 2006), exploring other micro foundations of human capital’s strategic competitive advantage (Coff & Kryscynski, 2011), and evaluating the boundary conditions in which human capital provides such advantage (B. Campbell, Coff, & Kryscynski, 2012). Despite the consistent finding that investing in human capital improves organizational performance, only a minority of firms in North America compete on this basis (Posthuma, Campion, Masimova, & Campion, 2013), and very few studies focus on understanding why this pattern exists. The limited diffusion of investment in HR systems in practice appears to contradict the theory and empirical evidence on the strategic HR literature: Why do so few firms invest in the HR systems that create strategic human capital and, in turn, improve organizational performance?

In this article, we examine why so few firms invest in strategic human capital. That is, what explains variation in firm investments in strategic human capital? We consider this question by focusing on the dimensions of HR systems that firms use for this purpose. Three dimensions are particularly important as points of leverage. First, firms may invest directly in skills and training to create firm-specific human capital. Second, they may structure incentives to motivate employees to make long-term commitments to the firm and to use their human capital in the best interests of the organization. And third, they may design work in ways that create opportunities for employees to use their human capital effectively. Together, these points of leverage help develop collective human capital that is valuable, rare, and hard to imitate because it is characterized by asset specificity, social complexity, and causal ambiguity (Coff & Kryscynski, 2011).

We contribute to the literature in two ways. First, while a handful of studies have sought to explain the sources of variation in HR practices, they have focused on firm-level variables, such as business strategies, organizational values, work technologies, or complementary managerial practices (Batt, 2000; Toh, Morgeson, & Campion, 2008). We move beyond these firm-level explanations to consider the role of capital structures as a source of variation. By capital structure, we mean the relative mix of debt and equity and variation in the mix of shareholder investment. We focus on three characteristics of capital structure—share turnover, shareholder concentration, and financial leverage—because they reflect firm investment choices; and new types of investors and capital structures have emerged in the past three decades that influence the decisions of firms to invest in human capital versus other strategic assets. Share turnover—the rate at which shareholders buy and sell a company’s stock—has increased due to the rise of Internet-based and high frequency trading, the rise of discount brokerage services, and heightened use of defined contribution pension plans. Shareholder concentration has increased because institutional investors and wealthy individuals have grown in their relative importance. Financial leverage—the ratio of debt to equity—has risen as new financial instruments such as securitization have made debt more available and preferential tax treatment of debt encourages its use. To the extent that these changes increase the power of investors to shape firm investments in human capital, they reduce the degrees of freedom available to chief HR officers—that is, they undermine the “strategic” in strategic HR management.

Second, we contribute to the theoretical development of the literature by integrating the resource-based view of the firm with agency theory. While RBT articulates the argument for why human capital may serve as a strategic asset, it ignores the factors that influence its use. Shareholder influence has increased in part because top manager pay is increasingly linked to stock options and share price, in keeping with agency theory prescriptions; but returns to human capital investment are much more difficult to measure than the returns to other types of investment, suggesting that shareholders may discourage investment in these intangibles. Thus, agency theory—and the increased influence of shareholders in management decision making—may help explain why the resource-based view of strategic human capital is not more widely adopted by firms. By bringing in agency theory, we enrich the explanatory power of RBT. Similarly, by bringing RBT to agency theory, we expand the framework to show how the alignment of top managers with shareholders affects decisions deep in the organization—in this case, the management of human capital.

To examine these questions, we draw on a unique establishment level survey of customer service operations in the United States and Canada. We link these data to indicators of capital structures—share turnover, shareholder concentration, and financial leverage—based on several financial data sets from Standard & Poor’s Compustat.

Prior Literature

Human Resource Systems and Strategic Human Capital

Strategic HR management research relies heavily on RBT to argue that a firm’s unique resources and capabilities, especially human capital, create sustainable competitive advantage for firms (Barney, 1991; Peteraf, 1993; Wright, Dunford, & Snell, 2001; Wright & McMahan, 1992). Human capital can be a major source of sustainable advantage because, unlike more tangible assets, people are adaptable; they can develop the tacit knowledge, skills, and organizational routines needed to respond to changing business strategies and competitive conditions and to initiate innovations.

Organization-level human capital may be a source of sustainable competitive advantage if it includes three features: asset specificity, social complexity, and causal ambiguity (Barney, 1991; Coff & Kryscynski, 2011). If it is firm specific, it is valuable to the employer, it is less valuable in other contexts, and competitor firms are unable to acquire it directly. If it is embedded in complex social systems, it is difficult to replicate. And if it is causally ambiguous, it is hard to imitate because other firms cannot identify which employees or which routines are the critical links in producing superior performance (Lippman & Rumelt, 1982).

Firms can use different dimensions of HR systems to create human capital that is firm-specific, socially complex, and causally ambiguous. Research over the past two decades has identified models of high involvement or high performance work systems that have these features and produce better organizational results (Combs et al., 2006; Crook, Todd, Combs, Woehr, & Ketchen, 2011).

In spite of ample evidence that investment in these HR systems leads to better organizational performance, some may question whether these bundles of practices can adequately be the source of a firm’s competitive advantage because they appear to be codifiable and imitable. In view of this concern, Barney and Wright (1998) argue that human capital resources derived from similar managerial practices are highly idiosyncratic because they are rooted in an organization’s unique routines, culture, and history. If a firm is unable to copy these bundles of practices and their underlying organizational processes and structures, it cannot sufficiently develop human capital as a means to ensure parity with or to achieve competitive advantage over its competitors. In the same vein, Ployhart, Van Iddekinge, and MacKenzie (2011) argue that generic and organization-specific human resources are causally interdependent. That is, if a firm is unable to accumulate a high-quality stock of generic human capital, it cannot adequately build its organization-specific human capital. As HR systems often develop various forms of human capital simultaneously, this interconnectedness implies that competitors face increased inimitability because they would have to replicate the practices and reproduce the causal relationship between various forms of human capital (Dierickx & Cool, 1989).

Empirical studies support this line of argument. While it is true that some firms may be able to imitate some practices—a pattern documented in the steel industry research by Ichniowski, Shaw, and Prennushi (1997)—few are able to adopt a complex system of complementary practices and apply them in a way that enhances the human and production capabilities of a specific product or service. Despite years of diffusion of lean manufacturing, many firms still fail to implement it successfully; and despite years of research showing that HR systems create sustainable advantage for Southwest Airlines, most airlines have failed to imitate its approach (Gittell, 2003). That is because implementation is costly, takes considerable time to perfect, may lack top management support, may be undermined by employees who do not want to assume new responsibilities or skills, and needs to be continually reevaluated and reconfigured to respond to changing competitive conditions (Appelbaum & Batt, 1994). Industry-based studies illuminate why practices that appear generic or codifiable must be implemented in ways that uniquely address the specific human capital and production capabilities that a firm needs to compete (Appelbaum, Bailey, Berg, & Kalleberg, 2000; Appleyard & Brown, 2001; Arthur, 1994; Batt & Colvin, 2011; MacDuffie, 1995).

Compared to traditional HR systems, high involvement systems invest relatively more in skills and training; in incentives for organizational commitment and long-term relations; and in the design of work that enhances motivation, learning, and collective problem solving. When firms invest in training they create the kind of firm-specific human capital that cannot be bought on the external market. Firms that seek to achieve sustainable competitive advantages need to invest in formal and on-the-job training because market-based training does not deal with a firm’s specific technologies, work processes, products, and customers. Those firms that make serious and ongoing investments in training create a system of continuous learning to enable employees to work with complex value-added products and processes and to contribute to innovation and customization. Ongoing investments in training create firm-specific human capital that is rare, valuable, and hard to imitate.

To realize returns on training investments, firms need to encourage the long-term commitment of their employees. As Coff (1997) noted, labor is a special asset because it can walk out the door or demand higher pay as a condition for staying. Internal labor market theory and empirical research (Doeringer & Piore, 1971; Osterman, 1987) provide the logic and evidence behind this argument. Firms are willing to offer high wages and benefits (efficiency wages) relative to their competitors to motivate workers to perform well and stay with the firm. Providing full-time permanent jobs with implicit employment security convinces employees that the firm is committed to their long-term welfare. In firms where investments in long-term employee commitment create sustainable competitive advantage, employees are willing to help train novice employees and share their tacit knowledge with management because they are confident that the new employees they train will not take their jobs, and their suggestions for innovation will not lead to layoffs (Osterman, 1994). Employees choose not to leave because their firm-specific skill investments are worth less on the external market than internally; they are motivated to work hard in order not to lose these high-paying, secure jobs. Internal mobility opportunities that lead to more challenging or interesting job assignments also induce long-term commitment. Internal labor market practices are costly to the firm, but pay off because employees continue to accrue more valuable, firm-specific human capital; they are likely to be more loyal or committed to the firm than new employees (Meyer, Stanley, Herscovitch, & Topolnytsky, 2002); and that means their valuable, rare, and inimitable human capital continues to be deployed for the firm’s benefit.

How work is organized may also contribute to asset specificity, social complexity, and causal ambiguity. If jobs are engineered to be individually based and to require low or narrowly defined skills, then they are easily replicable and lack firm-specific attributes. By contrast, new forms of collaborative work allow employees to share knowledge, solve problems, learn from each other, and come up with innovative solutions. Empirical research has demonstrated the effectiveness of work group activity based on high levels of employee discretion over operational decisions plus opportunities to participate in group problem solving (Batt, 1999; Cohen & Bailey, 1997). But team learning and effectiveness are difficult to achieve and depend importantly on stable relationships of trust (Edmondson, 1999) and the development of transactive memory systems in which group members know “who knows what” (Lewis, Lange, & Gillis, 2005), which contribute to social complexity and causal ambiguity.

Taken together, these three dimensions of HR systems help firms attract, retain, and motivate employees to share their knowledge and make a long-term commitment to the organization. For firms that seek to use strategic human capital for sustainable advantage, high levels of employee turnover are particularly problematic as they are costly, reduce firm-specific human capital, which must be replaced, disrupt overall operations, and undermine complex social systems of trust and cooperation (Hausknecht, Trevor, & Howard, 2009; Kacmar, Andrews, Van Rooy, Steilberg, & Cerrone, 2006). Empirical research shows that high involvement systems increase commitment and reduce voluntary and overall turnover, leading to higher organizational performance (Batt & Colvin, 2011; Gardner, Wright, & Moynihan, 2011).

Yet few firms compete on the basis of the strategic use of human capital in North America (Posthuma et al., 2013). Why don’t more firms adopt these HR systems? Some point to the role of tax laws that privilege investments in physical capital, which are tax deductible, versus investments in human capital or training, which are not (Coff & Flamholtz, 1993). This research also highlights the influential role of capital market structures: The Japanese system is driven by a very different external capital structure that is far more supportive of the view of people as long run assets. Here, institutional investors own larger stakes (as opposed to speculative investors) and adopt longer time horizons for realizing returns. Accordingly, quarterly financial results are far less significant. (Coff & Flamholtz, 1993: 40)

More patient capital enables longer term investments in human capital.

In liberal or market-based economies such as the United States and Canada, however, capital markets exert more pressure on firms to return short-term profits, and these demands have accelerated over the past three decades (Davis, 2009). As we discuss in greater detail in the next section, agency theory has increasingly guided corporate behavior and has led firms to more closely align top managers to shareholder interests through compensation linked to stock options and share price (Jensen & Murphy, 1990). Within corporations, the decision-making authority of managers with operational expertise has given way to those with financial expertise, leading to greater focus on maximizing short-term shareholder value (Fligstein, 2001). There are complex reasons why this shift has occurred (Lowenstein, 2004), including the rise of institutional investors, the deregulation of financial services, the rise of discount brokerages and Internet trading, and the increase in the number of defined contribution pension plans that individuals manage themselves (Jacoby, 2005). These changes have brought about a departure from the “managerial capitalism” of the 1950s that was characterized by a high degree of separation between ownership and control (Davis, 2009).

Capital Structure and Strategic Human Capital

The central premise of agency theory is that shareholders and managers are in conflict over the appropriation of economic rents. The separation of ownership and control in corporations leads to lower shareholder returns because opportunistic managers appropriate for themselves the retained earnings, or profits of the corporation (Jensen & Meckling, 1976). To align managers’ interests with those of shareholders, agency theory prescribes greater shareholder monitoring and control of managers and that their pay be linked to stock performance (Jensen & Murphy, 1990). Critics argue that what appears to be “opportunistic” managerial behavior is often their use of retained earnings to invest in human capital and assets to create sustainable competitive advantage. Pay linked to stock performance leads them to act as self-interested shareholders, with an obsessive concern for short-term profits, rather than as professionals acting in the best interests of the organization. According to Lazonick (2009), this has led to a dramatic rise in the use of retained earnings for stock buybacks: For the period 2000 to 2007, 19 of the top 50 S&P 500 Corporations distributed more cash to shareholders through stock buybacks than they generated in net after-tax income. And the top technology corporations—Microsoft, Cisco, Intel, Oracle, Texas Instruments, IBM, HP, and Dell—had stock repurchase payouts that exceeded their investments in research and development (R&D) in the 2000s.

Investors may object to investments in human capital because of information asymmetry, differing time horizons, and conflicting interests in the appropriation of economic rents (Jensen & Meckling, 1976). Because human capital is tacit, idiosyncratic, and difficult to evaluate, shareholders and creditors lack information they need to assess its role in firm performance. For example, laws to enhance market transparency and protection for minority investors prevent large shareholders from private communications with managers about the company’s nonfinancial indicators of future earnings, such as staffing plans or new product development. This significantly weakens large shareholders’ incentives and abilities to monitor firm decisions (Bhide, 1994). These restrictions also make it more difficult for managers to convey “nuance and complexity” to shareholders (Fox & Lorsch, 2012: 54). In a survey of corporate executives, Graham, Harvey, and Rajgopal (2005: 59) also reported that GAAP-based financial reporting downplayed the values of intangible assets such as “people, processes and brand position.” As a result, these executives underestimated the value of intangible human capital and, in turn, their willingness to invest in HR systems that create it.

In addition, as we have argued, the accumulation of strategic human capital requires a relatively long time horizon, but shareholders and creditors are risk averse toward long-term investments that do not produce shorter-term gains. They generally prefer liquidity and flexibility; profit maximization is the desired objective (Berle & Means, 1932). They worry that investments in HR systems that cannot be accurately measured simply increase agency costs and serve the self-interests of managers and employees who gain higher pay, job security, power, and prestige (Amihud & Kamin, 1979).

Three characteristics of capital structures may shape top management decisions regarding investments in HR systems that build human capital: share turnover, shareholder concentration, and financial leverage. We draw on theory and previous empirical research to outline our hypotheses regarding their relationships with investment in these HR systems. We then consider whether the relationships between capital structure and investment in human capital differ across countries (United States and Canada) with somewhat different financial institutions.

Share turnover

Share turnover refers to the rate at which shareholders buy and sell shares of stock. While shareholders tend to have shorter time horizons than what is ideal for the accumulation of strategic human capital, they nonetheless vary in their time preferences. Transient shareholders and speculative investors believe they will profit more from frequent stock trading than from a firm’s long-term growth. Hedge funds are emblematic of this approach as they typically seek to exit investments in less than 18 months. New forms of high frequency trading at low costs have intensified these short-time horizons: Software systems identify and capitalize on tiny price differences across stocks and make trades in seconds or milliseconds. In 2012, high frequency trading accounted for 51% of the daily number of trades in the U.S. stock market (New York Times, 2012) and 42% in the Canadian market (Financial Post, 2012). Since the 1950s, the average holding period for an equity traded on the NYSE has decreased from 7 years to 6 months in 2012 (Fox & Lorsch, 2012).

Under intense pressure to increase stock price and avoid earnings disappointments, top management may take actions that produce short-term gains but at the expense of long-term value. In a longitudinal study of 100 U.S. large companies, for example, Bange and De Bondt (1998) found that firms with high share turnover were more likely to reduce R&D budgets to close the anticipated gap between analysts’ earnings forecasts and reported income. Bushee (1998) found that when a firm’s institutional investors had high share turnover and were momentum traders, the firm had a higher probability of reducing R&D expenditure to reverse an earnings decline. In addition, studies of finance and HR practices have found that volatility in stock markets is related to market-based employment practices such as shorter job tenures and performance-based compensation (Black, Gospel, & Pendleton, 2008).

By contrast, firms with lower share turnover have more degrees of freedom to invest in HR systems because their equity financing is more stable. These firms may have better strategies for communicating with their investors, providing more complete information, and building their loyalty. Investors with longer time horizons may simply be more passive or more satisfied with slow but steady growth profiles. In sum, theory and evidence suggest that firms with low relative share turnover will invest more in HR systems that build human capital.

Hypothesis 1: Share turnover is negatively related to investments in human capital.

Shareholder concentration

Agency theory states that whether managers will act in shareholders’ interests depends on shareholders’ relative power to monitor and control management actions. Shareholder or ownership concentration refers to the proportion of a firm’s stock owned by individual or large shareholders (with at least 5% equity ownership). When concentration levels are high, managers face stronger monitoring and control from shareholders because they have higher incentives to protect their large investments. They are likely to have a disproportionate impact on firm strategy (Shleifer & Vishny, 1986). As large shareholders put pressure on managers to maximize short-term returns, managers are under pressure to improve internal efficiencies and reduce costs, as opposed to investing longer-term in human capital.

Corporate executives are worried about responding to large shareholder activists, as illustrated in the power of hedge funds that control large pools of private capital. They have influenced target firms either by insisting on changes in governance or operational policies or by bringing about a takeover of the firm. Greenwood and Schor (2009) analyzed the demands of large shareholders of public corporations from 1993 to 2006, as indicated in their Schedule 13D filings with the Securities and Exchange Commission (SEC). They found that hedge fund activism was 4 times the level of non-hedge-fund investors, and it increased dramatically from the late 1990s onward. Hedge fund activists influenced nine categories of initiatives, including capital structures, governance issues, business strategies, sales of assets, merger and acquisition activity, and proxy contests (Greenwood & Schor, 2009). These activists also increased the likelihood of a takeover by 11%. Another study, using the same SEC data for 2003 to 2005, found that hedge funds were successful in implementing 60% of the 151 initiatives they attempted (Klein & Zur, 2009).

In contrast to companies with concentrated ownership, those with a diffuse shareholder base face fewer activists. Managers have more autonomy to make decisions regarding investments in technologies, innovation, or HR systems because shareholders with smaller equity stakes have little incentive or power to closely monitor and discipline top executives (Shleifer & Vishny, 1986). In addition, organizing dispersed owners to exert collective power over management incurs substantial coordination costs. Therefore, managers in these firms worry less about shareholder demands. Several empirical studies have reported a negative relationship between concentrated ownership and investment in long-term, intangible assets such as R&D, advertising, and product diversification (Graves & Waddock, 1990). Only a few studies have examined the implications of increased shareholder ownership on HR practices. For example, Bethel and Liebeskind (1993) found that concentrated ownership was a significant cause of employment downsizing based on a sample of large, publicly traded companies. Nevertheless, these earlier studies have not examined the effect of shareholder concentration on a firm’s investment in strategic human capital.

Hypothesis 2: Shareholder concentration is negatively related to investments in human capital.

Financial leverage

Agency theory also argues that managers should use debt rather than retained earnings to finance new investment because this subjects investment projects to review by financial firms and to a market test for efficiency. Markets rather than managers should allocate capital. The extent to which firms rely on debt to finance investments affects management decisions because debt disciplines managers to strive for efficiencies to service the loans and keeps them focused on maximizing shareholder value (Jensen, 1986; Jensen & Meckling, 1976). The popularization of low-interest loans and preferential tax treatment of debt have further encouraged the extensive use of debt.

High debt loads, however, may increase the cost of capital, limit funds available for investment, and increase creditors’ perceptions of risk (Harris & Raviv, 1991). Firms with high leverage risk financial distress and have higher bankruptcy rates. In the extreme case of highly leveraged, private equity-owned companies, the bankruptcy rates are twice as high as for comparable publicly traded corporations (Strömberg, 2008). After the financial crisis, default rates for highly leveraged public and privately held companies increased to 25% (Hotchkiss, Smith, & Strömberg, 2011). Moreover, the costs of going through insolvency are high—an estimated 10% to 20% of a firm’s value (Andrade & Kaplan, 1998).

These high debt levels put pressure on managers to cut costs or increase short-term revenues to service the debt and avoid financial distress. Obligations to creditors may lead managers to forgo investment in strategic assets that would benefit long-term growth and sustainability. Past research has shown, for example, that the share of debt in a firm’s capital structure is associated with decreased investment in R&D (Jordan, Lowe, & Taylor, 2003; Simerly & Li, 1999).

In this context, firms find it difficult to justify investments in HR systems that do not generate immediate financial returns. Instead, firms with high relative debt are more likely to adjust employment levels to business cycles, to use contingent workers to replace regular workers, to lower wages, and to reduce contributions to employee pension plans (Hanka, 1998; Sharpe, 1994). Similarly, one study of 358 firms found that when highly leveraged firms experienced short-term distress, they had a strong propensity to reduce 10% or more of their workforce over the year (Ofek, 1993). Echoing this pattern, a study of 10 major U.S. airlines from 1987 to 2005 also found that a firm’s debt ratio was positively associated with layoffs (Gittell, Cameron, Lim, & Rivas, 2006). By contrast, firms with low financial leverage have the resource slack to buffer cash flow volatility and sustain employment levels and investments in human capital even during difficult times. In sum, theory and empirical evidence suggest that high debt levels undermine a firm’s ability to invest in human capital.

Hypothesis 3: Financial leverage is negatively related to the investments in human capital.

Capital Market Differences Between the United States and Canada

Although agency theory helps explain how and why shareholders influence managerial decisions, it fails to account for cross-national differences in financial systems that affect shareholder power (Aguilera & Jackson, 2003). We compare the United States and Canada because, although both are classified as liberal market economies (Hall & Soskice, 2001), their financial regulations and banking systems are different enough to affect shareholder behavior and its impact on firm decisions (La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 2000).

Although Canadian corporate and securities regulations have their origins in U.S. regulations, significant differences exist in the enforcement of regulations between the two countries. In particular, Canada is viewed as having much weaker enforcement of insider trading laws than the United States (King & Segal, 2003; McNally & Smith, 2003). Moreover, Canadian capital markets are less liquid and less transparent (Dyl, Witte, & Gorman, 2002; Mittoo, 2003). As a result, Canadian investors are forced to bear higher levels of idiosyncratic risk, and because of this they require an additional return premium and demand higher returns from the firms in which they invest.

In addition, differences in the U.S. and Canadian banking systems affect the impact of debt in the two countries. The U.S. banking system consists of over 9,000 locally fragmented commercial banks. This atomistic institutional structure leads to high levels of competition among banks and lowers the costs of debt financing. In Canada, by contrast, six major banks dominate the banking system, leading to a focus on stability and more conservative banking practices (Brean, Kryzanowski, & Roberts, 2011) and raising the cost of debt. The higher cost of debt puts more financial pressure on firms to cover higher interest payments.

These two features—weaker security regulation enforcement and a more concentrated banking industry—combine to produce a higher cost of capital and more expensive debt in Canada. These forces, in turn, increase the pressure on management from shareholders and creditors. As a result, given their higher sensitivity to capital market pressures, Canadian firms are more likely to underinvest in strategic human capital than are their U.S. counterparts when pressures induced by a firm’s capital structure are high. Therefore, we predict that share turnover, shareholder concentration, and financial leverage have a greater impact on Canadian firms’ investment in human capital than on U.S. firms.

Hypothesis 4: The negative relationship between capital structures (share turnover, shareholder concentration, and financial leverage) and investment in human capital will be stronger in Canada than it is in the United States.

Method

Sample

We analyze data from an establishment level survey of call centers with 10 or more employees in the United States and Canada. 1 The survey covered questions regarding market conditions, organizational characteristics, and HR practices. Each respondent, the general manager, answered questions about the “core” occupational group, customer service agents.

The U.S. sample is a stratified random sample consisting of 60% from a Call Center Magazine list representing centers across a broad array of industries and sectors and 40% from a Dun & Bradstreet listing of telecommunications establishments. The response rate for the U.S. survey was 68%. The Canadian sample includes 508 call centers compiled from industry experts, Internet research, and the membership lists of call center associations. The 70% response rate produced 406 usable cases. Both the U.S. and Canadian samples cover all geographic regions in each country and represent a wide cross section of industries. These samples are fairly comparable with two exceptions. The U.S. study oversampled telecommunications centers and the Canadian sample contains a higher proportion of call center vendors that provide specialized outsourcing services.

To gather capital structure data, we traced the establishments in our data sets to their parent companies. For each establishment, we researched their corporate structure using company websites, electronic databases from Hoover’s Company Records and Ward’s Business Directory, and industry experts. We classified each parent company into one of two categories: either listed on a North American stock exchange or nonlisted (i.e., privately owned). We included only those listed on a North American stock exchange in our analysis. The final sample includes 221 establishments in 26 two-digit SIC industry groups. The U.S. sample includes 135 establishments representing 69 listed firms, while the Canadian sample includes 86 establishments representing 50 publicly traded companies.

Measures

Dependent variables

We evaluate a firm’s investment in the creation of strategic human capital with three indices of HR systems representing investments in (a) firm-specific training, (b) long-term commitment, and (c) high involvement work organization. The measures capture actual use of objective HR practices. Following the convention in strategic HR research, we measure these as additive indices because some practices may be substitutes for one another, and they are not latent factors requiring confirmatory factor analysis (Delery, 1998). All three measures have been linked to superior performance in previous work, including lower turnover, higher customer satisfaction, and the agility to cope with competitive dynamics (Batt & Colvin, 2011; Lepak, Takeuchi, & Snell, 2003; Shaw, Dineen, Fang, & Vellella, 2009). Appendix A summarizes these measures.

Investment in firm-specific training is an additive index of initial on-the-job training and ongoing training. On-the-job training measures the number of days that a typical new hire needs to become fully competent. The longer this training period, the more the firm has designed jobs that require substantial firm-specific and tacit knowledge. This measure represents a substantial investment by employers because they are paying new hires full wages when they are not fully productive. Ongoing training measures the number of formal training days a typical core employee receives after the first year, including online, vendor, classroom, and other formal training. Both practices contribute to a firm’s strategic human capital by creating firm-specific skill that is valuable and not deployable in other firms.

Investment in long-term commitment captures an employer’s choice of salary and benefit levels, internal mobility opportunities, and degree of employment security offered to employees. Good pay and benefits, promotion and transfer opportunities, and a long-term employment contract together encourage employees to continuously invest in firm-specific skills and knowledge and to use them to advance the organization’s outcomes. Salary measures gross annual earnings for the typical full-time employee before deductions and taxes, including bonuses, commissions, profit sharing, and overtime pay. We asked respondents for the median salary level to reduce the influence of especially well-paid or especially low-paid employees in a given establishment. We used a logarithm transformation on this variable to account for its skewed distribution. Benefits measures the total value of discretionary benefits (as opposed to legislatively mandated ones) paid by the employer to a typical core employee as a proportion of gross annual earnings. Internal mobility opportunities measures the percentage of core employees promoted or transferred within the larger organization in the past 12 months. Employment security captures the percentage of workers who are full-time and permanent employees, rather than part-time or temporary. The long-term commitment index is the mean of the standardized values for salary, benefits, internal mobility opportunities, and employment security.

Investment in high involvement work organization consists of three variables: the extent of employee discretion on the job, the percentage of employees who participate in problem-solving groups, and the percentage of employees working in self-directed teams (Batt, 2002; Batt & Colvin, 2011). Employee discretion is a seven-item index that captures employee discretion over both the task and their interactions with customers, measured on 5-point Likert-type scales from none to complete (α = .74; Batt, 2002; MacDuffie, 1995). Problem-solving groups is the percentage of workers involved in offline groups with supervisors to discuss work related issues. Self-directed teams is the percentage of workers organized into online, semiautonomous work groups. The high involvement work organization index is the mean of the standardized values for employee discretion, problem-solving groups, and self-directed teams.

Independent variables

Our independent variables include share turnover, shareholder concentration, and financial leverage. Share turnover measures the liquidity of a company’s stock by dividing the aggregated trading volume by the average number of shares outstanding over a period of time (J. Campbell, Grossman, & Wang, 1993; LeBaron, 1992). To control for time-sensitive spurious events, we calculate a firm’s average share turnover over a 3-year period prior to data collection. We then subtract the mean value of share turnover based on a two-digit SIC industry groups from each firm’s share turnover to create industry-adjusted share turnover indicators (Hoskisson, Hitt, Johnson, & Grossman, 2002).

Based on previous research (Baysinger, Kosnik, & Turk, 1991; Hill & Snell, 1989), we measure shareholder concentration as the normalized Herfindahl–Hirschman Index (HHI) in the previous fiscal year based on data from the Thompson Financial 13F Institutional Holdings database, which is part of Compustat. The normalized HHI is calculated as in

Financial leverage refers to the amount of debt used to finance a firm’s assets. A firm with significantly more debt than equity is considered highly leveraged. We measure financial leverage as the ratio between debt and common equity (i.e., debt-equity ratio, including short-term and long-term debt) (Hanka, 1998). To reduce temporal bias related to spurious events, we calculate the average debt ratio for each firm over a three-year period prior to data collection. Moreover, because the capital structures of firms within an industry are more alike than those in different industries (Harris & Raviv, 1991), we then subtract the mean value of debt ratio based on two-digit SIC industry groups from each firm’s debt ratio to create industry-adjusted debt ratios. Therefore, we measure a firm’s financial leverage relative to other firms competing in the same industry, rather than the absolute degree of debt.

Control variables

We control for characteristics that may influence our dependent variables, including the size of the core workforce, whether or not the establishment is unionized, the percentage of the workforce that is female, and the average education level of the core workforce. We do this because large, nonunionized establishments with more female and fewer educated workers are more likely to implement control-focused HR practices (Batt & Colvin, 2011; van Jaarsveld, Kwon, & Frost, 2009).

We also included several control variables to account for a firm’s financial standing and investment opportunities that are considered influential. We measured firm size as a log of total assets, financial performance as the ratio of the firm’s market value to its total asset value (i.e., Tobin’s Q ratio), capital intensity as measured by capital expenditure to sales ratio, and growth opportunities as measured by dividend yield (Budros, 1997; Hill & Snell, 1989; Sharpe, 1994). In addition, we included primary stock exchange dummies (i.e., New York Stock Exchange, NASDAQ, and Toronto Stock Exchange) to control for the effects of trading mechanism and listing requirements as well as industry dummies (i.e., telecommunications, financial services) to account for external regulation and market competition factors.

Data Analysis Procedures

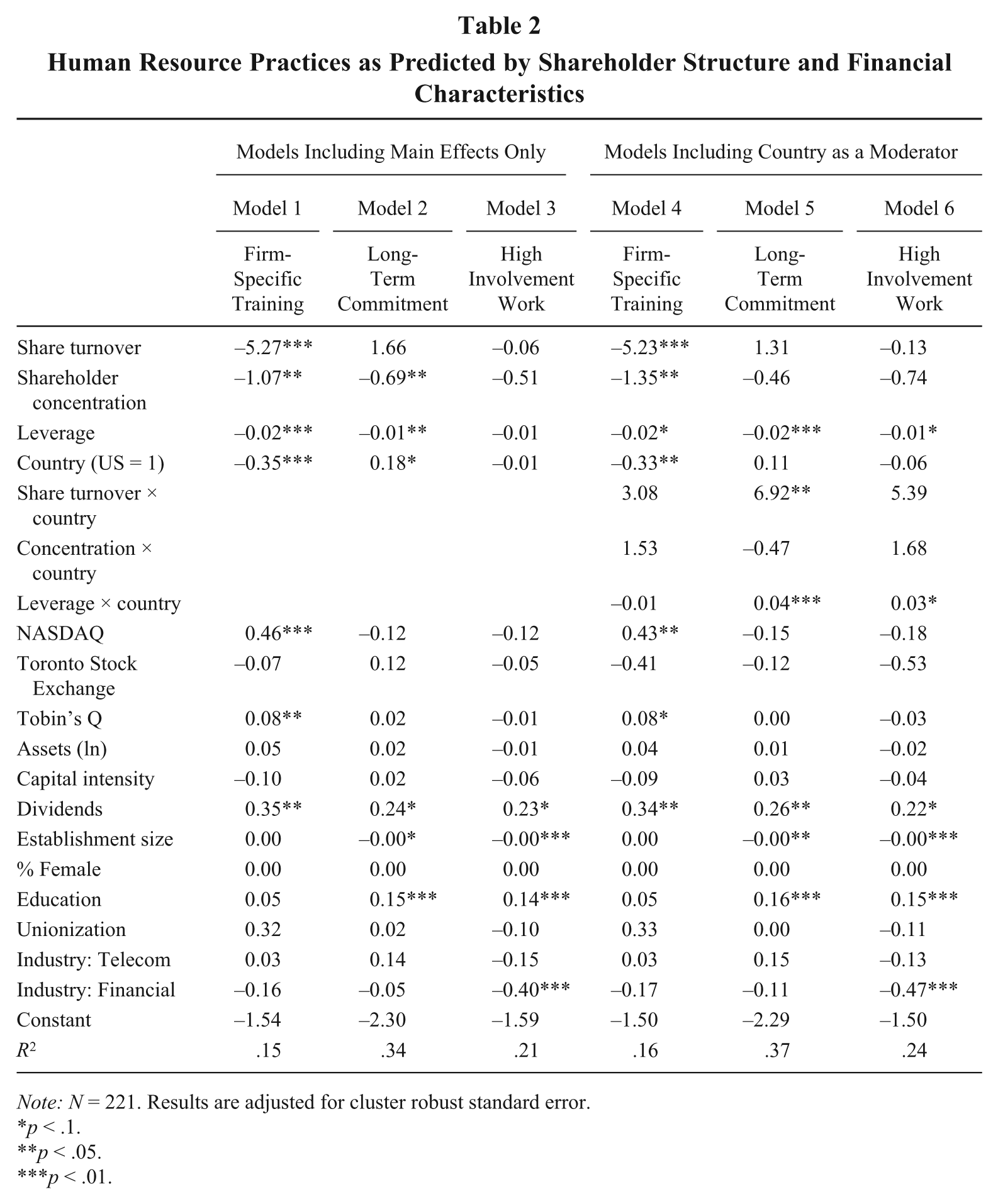

We fit a set of multivariate regression models to examine the effects of a firm’s capital structure on its investments in firm-specific training, in long-term commitment, and in high involvement work organization. Specifically, we regressed each of the three indices with share turnover, shareholder concentration, financial leverage, and the controls. Then we included country as a moderator to examine whether the effect of capital structure on investment in human capital varies between the United States and Canada. Following Aguinis, Beaty, Boik, and Pierce’s (2005) recommendations, we used moderated multiple regression to test whether there is a slope difference between countries. Additional analyses (not reported) indicate that alternative estimation methods such as subgroup analyses produce consistent results. To mitigate the concern that standard errors are biased because some establishments were affiliated with the same listed parent company, we adjusted the model by computing a cluster robust standard error for the coefficients in all analyses (Greene, 2003). Finally, we examined the results of a set of regression models that include each single human capital investment as a dependent variable (Appendix B). Our three measures of capital structure have negative relationships with most of the single measures, and many of them are statistically significant.

Results

Table 1 provides descriptive statistics and correlations for all variables. Table 2 reports the regression results. We ran the same models for the three dimensions of HR systems. Models 1, 2, and 3 test the main effects for the independent variables. Models 4, 5, and 6 include the moderating effect of country.

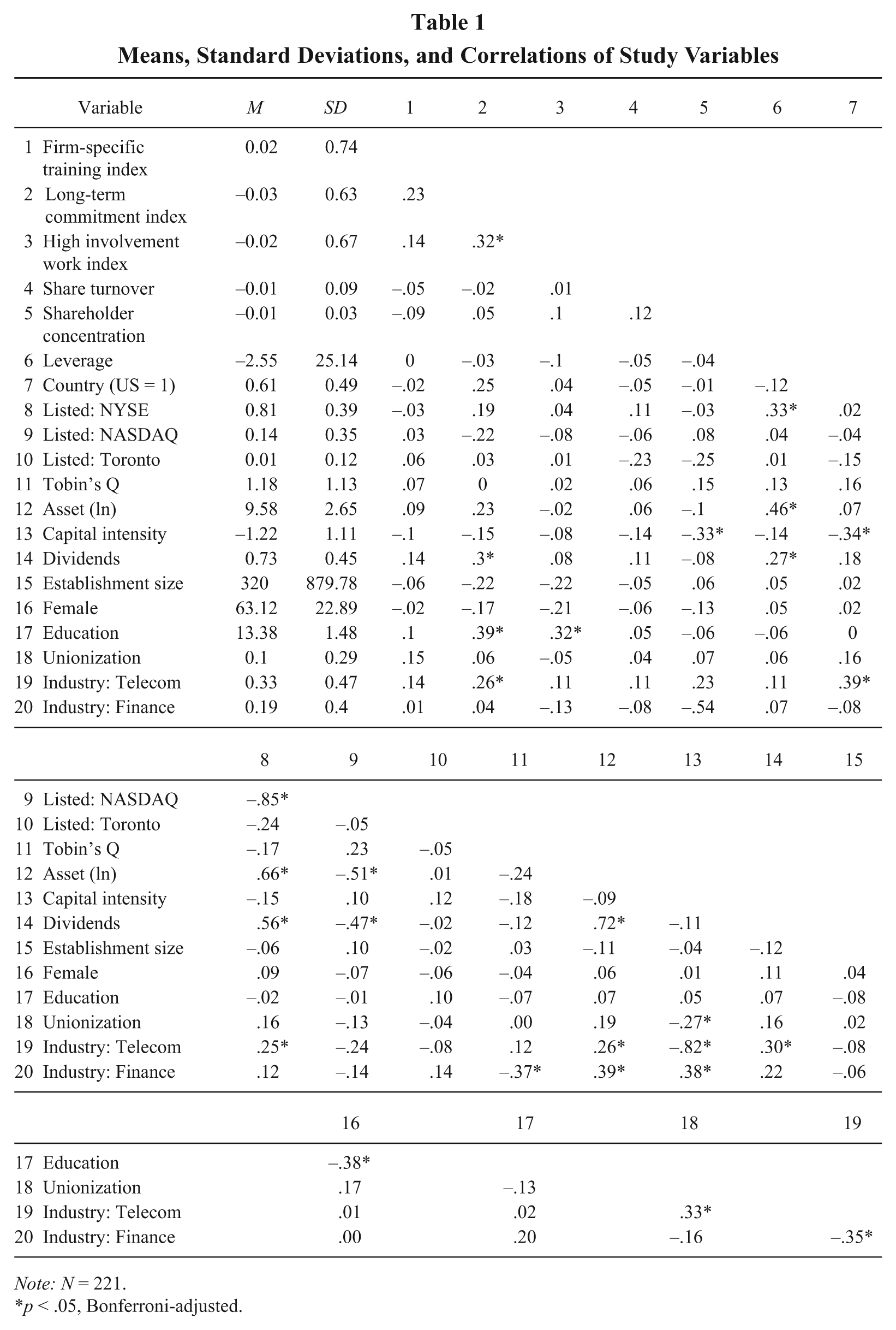

Means, Standard Deviations, and Correlations of Study Variables

Note: N = 221.

p < .05, Bonferroni-adjusted.

Human Resource Practices as Predicted by Shareholder Structure and Financial Characteristics

Note: N = 221. Results are adjusted for cluster robust standard error.

p < .1.

p < .05.

p < .01.

In Hypothesis 1, we expect that higher relative share turnover negatively relates to investment in human capital. Model 1 reports that share turnover significantly decreases investment in firm-specific training (–5.27, p < .01), although its effects on investments to increase long-term commitment (Model 2) and high involvement work organization (Model 3) are not statistically significant. Hypothesis 1 is partially supported.

Hypothesis 2 proposes a negative relationship between shareholder concentration and investment in human capital. The results indicate that a 1-unit increase in the transformed Herfindahl measure of shareholder concentration is associated with a 1.07-unit decrease in investment in firm-specific training (p < .05; Model 1), as well as a 0.69-unit decrease in the long-term commitment index (p < .05; Model 2). This finding is consistent with Hypothesis 2. It suggests that firms with relatively higher share turnover and shareholder concentration are under greater pressure to reduce investments in skill development and in incentives that build long-term commitment. The effect of shareholder concentration on investment in high involvement work organization, however, is not statistically significant (Model 3). Therefore, Hypothesis 2 is largely supported.

Hypothesis 3 predicts that investments in human capital are constrained by a firm’s financial stress as measured by financial leverage. As shown in the results, we found that a firm’s financial leverage relative to its competitors is negatively associated with investments in firm-specific training (–0.02, p < .01; Model 1) and investment in long-term commitment (–0.01, p < .05; Model 2). This evidence supports Hypothesis 3.

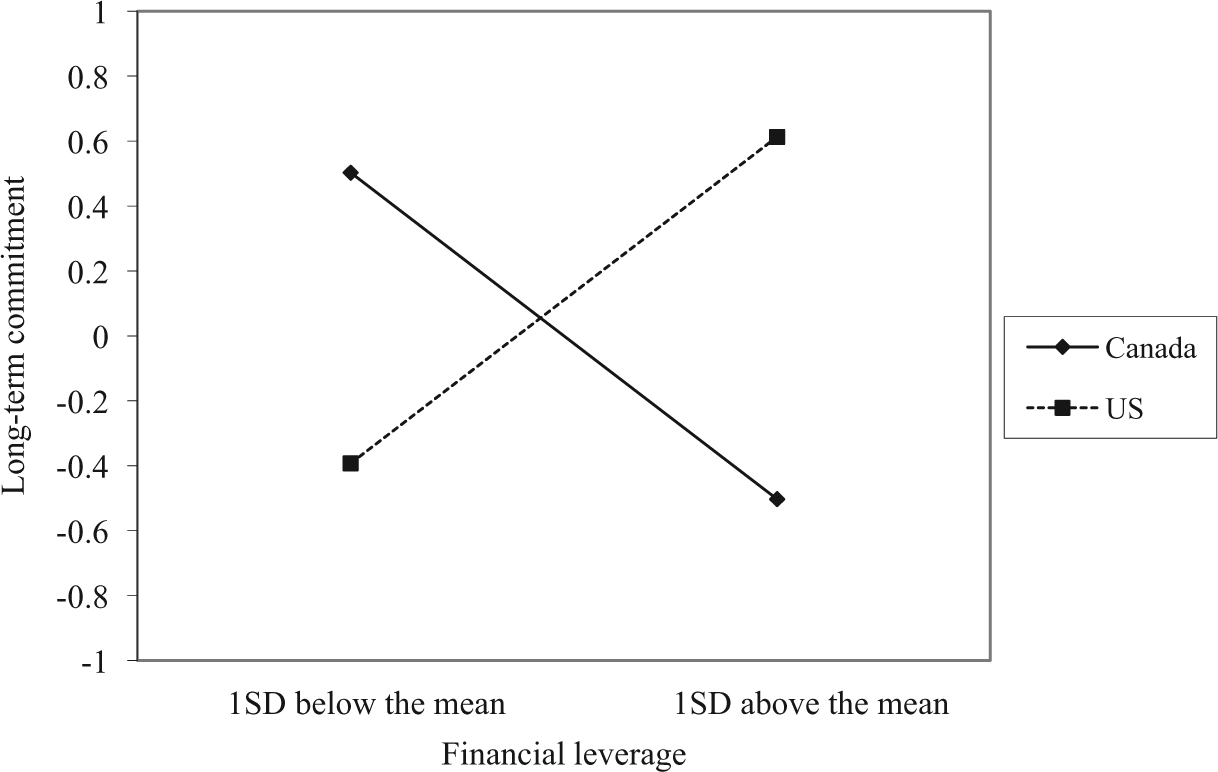

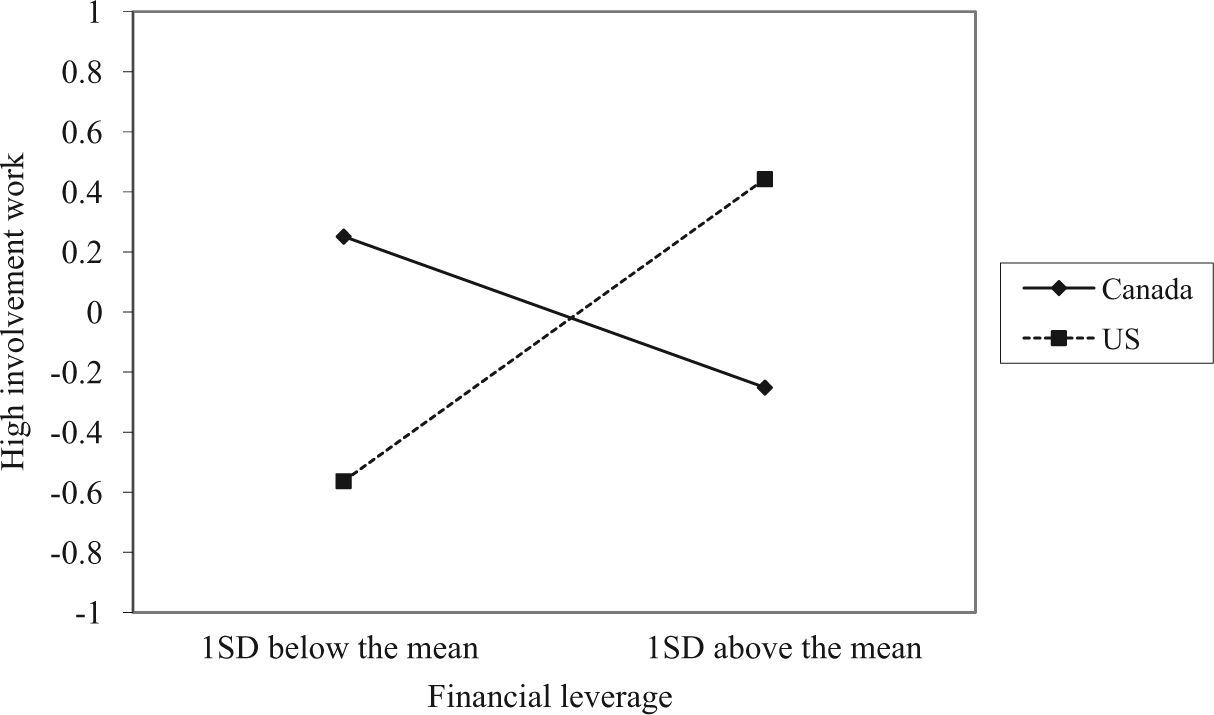

Hypothesis 4 posits that the effects of capital structure on a firm’s investment in human capital vary depending on the country where an establishment operates. The results indicate that the moderating effect of country is statistically significant and positive. In particular, while the main effect of a firm’s financial leverage ratio is relatively weak for all firms in the sample (Models 2-3), for Canadian establishments it is significantly associated with a 0.02-unit decrease in investment in long-term commitment and a 0.01-unit decrease in investment in high involvement work organization (Models 5-6). In other words, the negative effects of capital market pressures on investment in human capital are significantly stronger among Canadian establishments. These findings support our argument that as compared to U.S. firms, Canadian firms raise capital at higher costs from limited financing sources; and this financial stress as measured by financial leverage impairs managers’ tendencies to invest in human capital that has strategic value. We illustrate these interactions in Figures 1, 2, and 3.

Interaction Effect Between Share Turnover and Country in Predicting Long-Term Commitment

Interaction Effect Between Financial Leverage and Country in Predicting Long-Term Commitment

Interaction Effect Between Financial Leverage and Country in Predicting High Involvement Work Organization

Discussion

In this study, we examined whether variation in capital structure is related to investment in strategic human capital to address the question of why, despite consistent evidence showing the benefits, few firms are investing in HR systems that create strategic human capital. We examined dimensions of a firm’s capital structure that prior theory and empirical research have emphasized as important to managerial decision making, but which have yet to be analyzed with respect to their influence on investments in human capital. Our findings indicate that firms with greater share turnover, more concentrated share ownership, and higher financial leverage are more likely to respond to external demands for maximizing short-term returns. These demands, in turn, lead managers to reduce their investments in skills and wages and other benefits that build long-term commitment—HR practices that create strategic human capital.

Our study offers several contributions. First, we move beyond firm-level explanations to show how capital structure can influence variation in investment in strategic human capital among firms. This perspective is a useful one because although we know that investing in strategic human capital is beneficial for firms, in practice evidence suggests a low level of investment in human capital among firms in North America (Blasi & Kruse, 2006; Godard, 2001; Posthuma et al., 2013). Researchers continue to question the disconnect between the growing evidence demonstrating the benefits of investing in HR systems and the low level of adoption in practice; yet we know far less about the factors influencing this decision than we know about the consequences of investing in these practices (Huselid & Becker, 2011). Our analysis suggests that researchers need to consider the capital structure of firms as a potential explanation for why so few firms invest in strategic human capital.

Second, we incorporate agency theory into our theoretical framework to help address the limitations of strategic HR management and the RBT of the firm. Both have primarily focused on a firm’s internal environment, especially the means by which resource accumulation and deployment leads to sustainable competitive advantage. Although RBT scholars have explained why resources and capabilities are the basis for a firm’s long-term success, they generally have neglected the factors that discourage the development of human capital as a strategic asset. In particular, they have overlooked how shareholder preferences and pressures limit managerial discretion over resource allocations within the firm. We extend the RBT of the firm by incorporating agency theory into our model to explain variation in firm adoption of the RBT approach. To the extent that investors increasingly prefer asset liquidity and short-term earnings, managers face heightened pressure to reduce investment in strategic resources that generate benefits over time. Integrating RBT into agency theory also expands its scope as it has tended to oversimplify the interests of shareholders and has focused primarily on the alignment of shareholder and managerial interests, assuming that this alignment will maximize shareholder value. Agency theory has ignored the additional—perhaps unintended—consequences of this alignment on investment in human capital and on the long-term capabilities of the firm to create sustainable competitive advantage. More broadly, by bringing together agency theory and RBT, we respond to recent calls for a more integrated framework for understanding the relationships among shareholders, managers, and employees, and in turn, their implications for the management of human capital at the organizational level (Bidwell, Briscoe, Fernandez-Mateo, & Sterling, 2013).

Third, we interpret our findings as offering important insights into the constraints that the leadership within firms has to contend with that strategic HR management research often overlooks. To the extent that shareholder behavior and debt financing lead firms to reduce their investments in strategic human capital, they reduce the capacity of chief HR officers to act “strategically”—to use their expert knowledge, skills, and abilities to make the right decisions for the growth and sustainability of the enterprise. Investor activism takes the “strategic” out of strategic HR management and is a force that is growing in power (Davis, 2009). Chief HR officers have fewer degrees of freedom to enact their strategic visions. With these findings, we are able to help explain why firms vary in their adoption of HR systems that create strategic human capital—among those that are more or less constrained by capital market structures. The results shed light on why many firms fail to invest in strategic human capital, despite the fact that empirical research shows that it contributes to firm performance.

Fourth, our findings inform recent debates concerning the evolution of financial systems in liberal market economies and its implications for managers and employees. Prior to the 1970s, the prevailing managerial model of decision making in large firms privileged the authority of professional managers who had deep industry expertise and firm-specific skills and knowledge (Chandler, 1990). Managers used retained earnings to invest in the assets they believed were essential for firm growth and sustainability, including investments in innovations, technologies, and long-term employment relations (Jacoby, 2005). Maximizing shareholder returns through dividends or improvements in share price was among several primary concerns, but it was not the overriding priority for managers. In recent decades, however, institutional changes coupled with agency theory prescriptions have led firms to pay more attention to the demands of shareholders and to align top management pay to stock options and share price. Pressure to return retained earnings to shareholders rather than invest in strategic assets has accelerated. Accordingly, managers pass these risks and uncertainties onto workers as the company diminishes the use of HR systems that encourage employees to increase skills, develop attachment to the employer, and participate in workplace decisions.

Fifth, our findings regarding the differences between the United States and Canada provide further support for our argument linking variation in capital structure to investments in human capital. In Canada, where share turnover is higher than in the United States, firms are under even more pressure to reduce investments in wages and other benefits that support long-term commitment. In addition, because the cost of debt is higher in Canada, Canadian firms are under more financial pressure to pay off the interest on debt and repay loans. This leads them to invest significantly less than do U.S. firms in long-term commitment and high involvement work organization.

Future Directions

Several research opportunities exist that could improve our understanding of these relationships. First, future research could examine the identity of large shareholders and their relative degree of power. Indeed, a possible reason for the weak relationship between shareholder concentration and investment in human capital observed in this study is that powerful shareholders may have divergent interests in a firm’s long-term investments. Future studies may evaluate who the largest owners are, whether they are hedge funds, sovereign wealth funds, institutions representing retail owners, or pension funds, and could yield important insights about which types of investors represent more patient capital and which ones prefer exit or voice when they are dissatisfied with management’s directions (Ryan & Schneider, 2002). Gospel and Pendleton (2003), for example, reported that directly managed pension funds tend to participate in active corporate governance as opposed to exit, whereas mutual funds are more likely to exit. Hoskisson et al. (2002) found that the managers of public pension funds had a longer-term orientation to investment than those of professional investment funds. Following this line of research, future studies may examine whether the identity and investment orientation of shareholders may affect corporate investment in human capital.

Second, our cross-national comparison is based on liberal market economies, and even here we found that relatively small differences in national financial systems led to significant differences in shareholder influence on firm behavior. Future research should expand the analysis to include countries from emerging markets, as well as coordinated market economies that have more concentrated ownership structures, greater reliance on banks for debt financing, and stable long-term relationships between shareholders and managers. According to some research, these characteristics produce an insider-style of monitoring management, which appear to motivate greater investment in human capital (Poutsma & Braam, 2005). Labor institutions and collective bargaining also exert greater influences in these countries, which may further strengthen the role of human capital.

Third, as noted earlier, our establishment-level survey data cover a period of economic expansion. A longitudinal approach encompassing periods of economic expansion and contraction could help us isolate how economic conditions affect the relationships we find. A longitudinal approach could also help shed light on causality.

Limitations

This study has limitations that require the results to be interpreted cautiously. First, while we find significant relationships between capital structure and investments in human capital, the causal story needs further development. We used a rigorous research design by matching objective data on firm characteristics from Compustat at Time 1 (a 3-year average of capital structure prior to the survey administration) to survey data collected at Time 2. We also controlled for other explanations of investments in human capital, including firm financial performance at Time 1 (which provides resources for higher levels of investments), industry variation, workforce characteristics, and unionization. Workforce characteristics and unionization were particularly significant in their relationship to investments in human capital indices. While these strategies help to mitigate concerns about reverse causality, they do not completely address them.

Second, our research design privileges internal validity over external validity by focusing on the core occupational group in one type of service operation. This choice reduces confounding alternative explanations. Moreover, our choice of call center agents as a subject is appropriate for this study because when firms are under pressure to cut costs, they are likely to start with operations they consider to be marginal to firm profits—as call centers are widely viewed. Thus, while we are able to demonstrate that variation in capital structures does influence HR practices deep in an organization, it is plausible that this finding would not hold for occupations or productive activities that are viewed as more critical or of strategic value for the firm. A useful design for future research would be to compare investments in human capital across multiple employee groups in one firm and their relationships with the firm’s capital structure. A plausible expectation is that some occupational groups within firms, that is, those jobs that are considered to be of high strategic value to the firm and require high uniqueness of knowledge (Lepak & Snell, 1999) might be less exposed to pressures from shareholders than others.

Third, among studies of human capital considerable variation exists in how human capital is conceptualized (Crook et al., 2011). To build on our research, we encourage future studies to use a direct measure of strategic human capital and to differentiate between investments in firm-specific human capital and general human capital.

Practical Implications

Our findings have important implications for strategic HR management. As we have argued at the theoretical level, capital structures that exert more financial pressure on firms limit the capacity of chief HR officers to enact their strategic vision. Their power to use HR strategy to affect competitive advantage is reduced. This means that top HR managers not only need to be trained in business strategy, as HR scholars have argued, but also must be sophisticated in their knowledge of how capital markets and institutions affect the range of strategies they can pursue.

Our findings indicate that managers need to pay close attention to the ownership and capital structures of their firms and how these may influence their decision-making power. If top management pay is linked to stock performance, then top HR executives may be satisfied to accept the strategic direction suggested by activist shareholders or imposed by lenders. This, however, may create a new agency problem, as top managers may be guided more by their interests and identities as shareholders than their interests and identities as organizational managers. In these circumstances, the long-term competitiveness of the firm may suffer. In addition, if top managers have lower levels of discretionary power, these companies may find it difficult to attract and retain, the most talented managers in the field—those who seek opportunities to exercise their own creativity and innovation as professional managers.

Conclusion

The relationship between strategic human capital and competitive advantage is important for understanding how firms can position themselves in the market. Through our integration of agency theory and the resource-based view of the firm, we help explain why firms in the United States and Canada may encounter challenges in trying to adopt and implement the kinds of HR systems that increase the human capital of the workforce. While the majority of research has focused on the consequences of investing in strategic human capital, we argue that the factors that influence adoption—particularly capital market structures—need greater attention. Clearly, human capital has a fundamental role in creating competitive advantage for firms, but important contextual factors need to be considered to ensure that firms can realize this competitive advantage.

Footnotes

Appendix A

Appendix B

Acknowledgements

Funding for this project came from the Russell Sage Foundation, the Alfred P. Sloan Foundation, and the Social Sciences and Humanities Research Council of Canada. We are grateful to Russell Coff and two anonymous reviewers for their constructive and insightful comments. We would also like to acknowledge valuable feedback from seminar participants at Cornell University, Pennsylvania State University, University of Toronto, and the Industry Studies Association 2012 annual meeting.