Abstract

Transparency is often cited as essential to the trust stakeholders place in organizations. However, a clear understanding of the meaning and significance of transparency has yet to emerge in the stakeholder literature. We synthesize prior research to advance a conceptual definition of transparency and articulate its dimensions, and posit how transparency contributes to trust in organization-stakeholder relationships. We draw from this analysis to explicate the mechanisms organizations can employ that influence transparency perceptions.

In the wake of a seemingly endless stream of corporate malfeasance, transparency is often invoked as a salve for the many maladies that accompany distressed relationships between an organization and its stakeholders through its presumed ability to reestablish stakeholder trust in the firm (e.g., Bennis, Goleman, & O’Toole, 2008; Fombrun & Rindova, 2000; Jahansoozi, 2006; Tapscott & Ticoll, 2003; Walumbwa, Avolio, Gardner, Wernsing, & Peterson, 2008). In fact, researchers who have called upon the transparency concept in organization-stakeholder relationships have consistently suggested its role in creating, maintaining, or repairing trust, either explicitly (Akkermans, Bogerd, & van Doremalen, 2004; Fleischmann & Wallace, 2005; Pirson & Malhotra, 2011; Rawlins, 2008) or implicitly (e.g., transparency in financial markets is important for enabling trust in the market system, even if the term trust was not mentioned directly; Bansal & Kistruck, 2006; Bhat, Hope, & Kang, 2006; Bushman, Piotroski, & Smith, 2004; Leuz & Oberholzer-Gee, 2006; Perotti & von Thadden, 2005).

To date, however, researchers touting the benefits of transparency in this context have relied on cursory assertions rather than rigorous theoretical development. Furthermore, to the extent that it has been examined empirically, the lack of a theoretically grounded consensus on the transparency construct is manifested in a patchwork of ad hoc operationalizations across areas of academic inquiry (see, for example, discrepant measures of transparency from Awad & Krishnan, 2006; Kaptein, 2008; Pirson & Malhotra, 2011; Rawlins, 2008; Walumbwa et al., 2008). In sum, the state of the extant literature on transparency suggests that it is not clear exactly how the construct should be conceptualized, how it relates to managing trust in the organization-stakeholder relationship, or how organizations manage it.

Therefore, in this article we have three objectives. First, we integrate the literature on transparency across academic disciplines to develop a more complete understanding of its meaning and dimensional structure. This analysis reveals that transparency is not a unidimensional construct as most researchers have commonly assumed. Rather, it is composed of three specific dimensions: information disclosure, clarity, and accuracy. Second, we turn to Mayer, Davis, and Schoorman’s (1995) model of trust to describe the impact of each dimension of transparency on organizational trustworthiness and stakeholder trust in the firm. Finally, we use this framework to describe several concrete mechanisms available to organizations to manage transparency.

The Meaning and Dimensional Structure of Transparency

There is currently very little convergence about the fundamental meaning of transparency. In an attempt to address this, we begin by synthesizing existing literature to compose a parsimonious definition of transparency. To examine the literature, we conducted a thorough search to trace common conceptualizations of the construct in line with suggestions from Shepherd and Sutcliffe (2011). An initial scan of the literature produced more than 500 articles that referenced to transparency. While the large number of articles reaffirms the broad relevance of the transparency concept, it at the same time makes a thorough review of the transparency discourse prohibitive within the scope of a single article. Hence, to reduce this number to a more manageable set, we retained only those articles that were published in academic journals with a relatively high impact factor (>3 for 5-year impact) or were cited more than 50 times through Google Scholar. Next, to include the practitioner voice, we scanned major practitioner-focused journals, including the Harvard Business Review and Sloan Management Review, to include articles that discussed transparency. We also reviewed several trade and professional books that discussed transparency.

Definition of Transparency

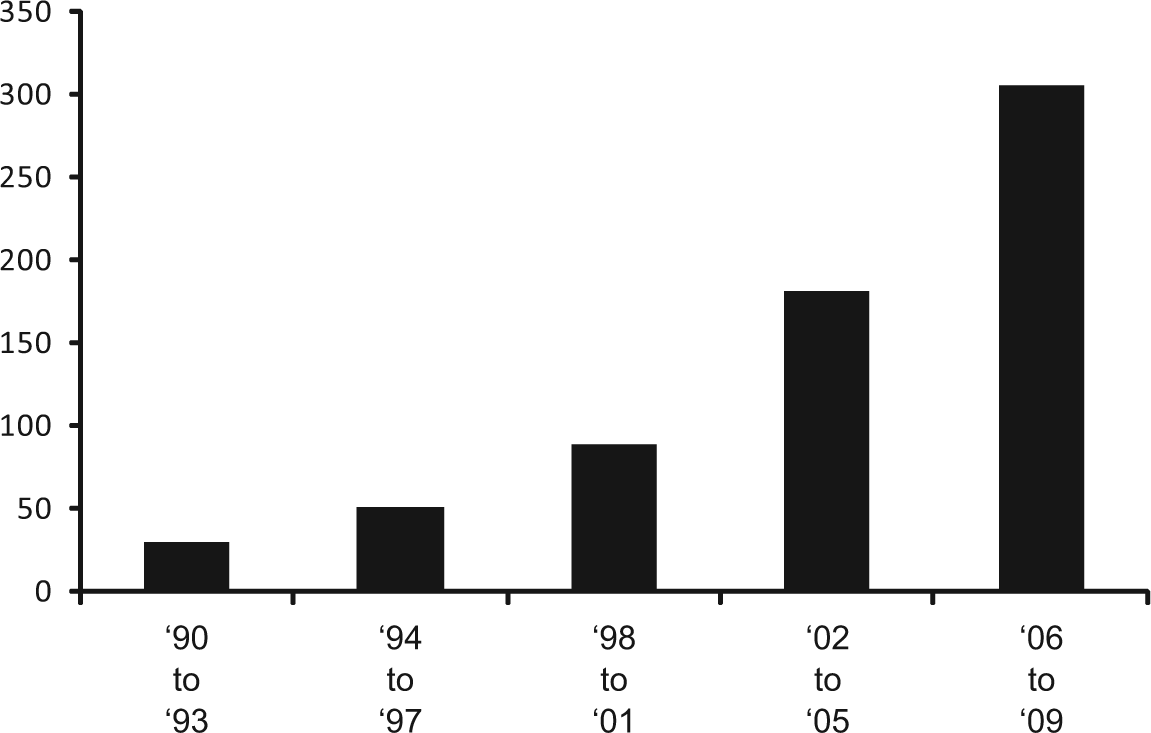

In the organization sciences, early reference to transparency can be traced back to discursive accounts of organizational roles and social conformity in the mid-20th century (e.g., Coser, 1961). Transparency remained a tangential concept most often summoned by organization theorists as a rhetorical device until the late 20th century. In the past two decades, a more formal interest in transparency has taken shape across domains of organizational research following a deluge of prominent corporate scandals (e.g., Enron in 2001, WorldCom in 2002, Lehman Brothers in 2008, and Madoff Investment Securities in 2009). Reflecting the increasing usage of the term among researchers, Figure 1 shows the number of articles from selected business journals referencing transparency in 4-year intervals from 1990 to 2009.

Number of Articles From Selected Business Journals Referencing Transparency (1990 to 2009)

Over the years, organization scientists have offered a number of definitions of transparency, with varying degrees of specificity. A review of common definitions of transparency is presented in Table 1. Overall, information systems researchers have investigated transparency in the context of business to consumer relationships and digital markets (e.g., Granados, Gupta, & Kauffman, 2005, 2006, 2008, 2010; Zhu 2004); organizational behavior researchers have explored transparency in the context of organizational trust development, organizational identity, perceptions of leadership, and organizational culture (e.g., Clair, Beatty, & MacLean, 2005; Fombrun & Rindova, 2000; Kaptein, 2008; Pirson & Malhotra, 2011; Walumbwa, Luthans, Avey, & Oke, 2011); researchers of finance and accounting have examined transparency in the context of financial markets, corporate disclosures, and monetary policy decision making (e.g., Bushman et al., 2004; Madhavan, Porter, & Weaver, 2005; Winkler, 2000); marketing researchers have studied transparency using related terms, such as product disclosure, in the context of consumer responses to nutrient and drug risk information (e.g., Cox, Cox, & Mantel, 2010; Howlett, Burton, Bates, & Huggins, 2009); and social psychologists have explored transparency in the context of negotiations (e.g., Garcia, 2002; Vorauer & Claude, 1998; Vorauer & Ross, 1999).

Definitions of Transparency

Note: Articles were included if they explicitly defined transparency and were published in academic journals (empirical or theoretical) with a relatively high impact factor (>3 for 5-year impact) or were cited more than 50 times through Google Scholar. Working papers, books, practitioner-oriented articles, and industry publications were omitted from this list.

These diverse applications suggest that, at its core, transparency neither exists within any single domain of research nor operates within any one context of study. Rather, the emerging consensus is that transparency can exist across contexts and domains of research. In addition, our review shows that most (but not all) managerially relevant applications of transparency exist at the organization level of analysis, specifically in relation to organization-stakeholder relationships (internal stakeholders, such as employees; see Kaptein, 2008; Walumbwa et al., 2011; as well as external stakeholders, such as shareholders, governments, and society; see Bloomfield & O’Hara, 1999; Bushman et al., 2004; Flood, Huisman, Koedijk, & Mahieu, 1999). Accordingly, a useful definition of transparency must be broad enough to enable theorists from a variety of management traditions to incorporate it into their study designs. At the same time, it must be specific enough to meaningfully inform management practice. For these reasons, we do not distinguish between contexts of study, levels of analysis, or domains of research in our definition but in the sections that follow, we adopt an organization level conception of transparency to draw examples from the literature that help us uncover its core theoretical properties and to elaborate on the aspects of its structure that are most relevant to management practice. Prior to this, however, we offer a definition of transparency and discuss the meaning of its individual components.

Transparency is the perceived quality of intentionally shared information from a sender.

This definition synthesizes a number of concepts from the literature. First, the emerging consensus is that transparency is about information. With rare exception, transparency is seen as a critical element of knowledge sharing such that increased transparency brings increased awareness, coherence, and comprehensibility to information exchanged between two parties (Pagano & Roell, 1996). For instance, Kaptein (2008) suggested that transparency is required to ensure that information about organizational conduct can be used by employees to modify or adjust their behaviors. In the context of external stakeholder relations, Madhavan et al. (2005) investigated transparency as the quantity of information released by financial institutions toward market participants. Similarly, Nicolaou and McKnight (2006) examined transparency in the setting of electronic information exchanges between organizations and stakeholders. 1

Second, most conceptualizations of transparency involve intentionally shared information such that ad hoc or unsystematic variations in information quality are not indicative of transparency. Rather, organizations hold the capacity to deliberately wield information in ways that increase or decrease transparency. For example, Rosengren (1999) has discussed different types of information held by financial firms that, if intentionally released, would increase the transparency in the banking system. In central banking, Winkler (2000) contends that more deliberate openness and clarity of monetary policies would increase the transparency of communications toward economic stakeholders. Others have similarly examined the factors that lead firms to intentionally materialize various types of information into speech acts, contracts, policies, and other communications toward stakeholders (e.g., Bloomfield & O’Hara, 1999; Granados et al., 2005; Larsson, Bengtsson, Henriksson, & Sparks, 1998; Winkler, 2000). These studies are based on the premise that, in absence of intentionality, transparency includes aspects of information sharing (e.g., unintended miscommunications) that dilute the practical and theoretical usefulness of the concept.

Third, our review suggests that transparency is a perception of received information, although organizations have the capacity to influence that perception through their information-sharing behaviors. To illustrate, some researchers study transparency as a perception of information that can be attributed to the senders of that information at different levels of analysis (e.g., toward another human being, a group of individuals, or an organization; see Larsson et al., 1998; Kaptein, 2008; Vorauer & Claude, 1998). Bushman et al. (2004), for example, have defined transparency as the availability of adequate information to stakeholders. Flood et al. (1999) have defined transparency as the ability of actors to clearly see outstanding price quotes. In electronic markets, Zhu (2004) has investigated transparency as the degree of visibility and accessibility of information. These views suggest that transparency is most appropriately conceptualized as a perception of information.

Finally, transparency perceptions vary according to the perceived quality of information. The importance of information quality is highlighted either explicitly or implicitly across virtually all of the studies we reviewed. For example, transparency has been measured as the perceived quality of information shared by an organization toward its employees (Rawlins, 2008), the perceived quality of information gathered by an organization about its customers (Awad & Krishnan, 2006), and the perceived quality of information shared by an organization toward its external stakeholders (Bushman et al., 2004). These studies operationalize transparency in a variety of ways. Nevertheless, they carry with them a core belief that information quality is central to transparency.

Gaps and Inconsistencies in the Literature

The apparent convergence around an emergent definition masks gaps and inconsistencies in the literature that hinder systematic theorizing of the transparency construct. We view these gaps and inconsistencies as opportunities for moving toward a more integrative theory of transparency. To develop these opportunities, we organize existing gaps and inconsistencies into three concerns that we believe are critical to resolve for a more theoretically meaningful and empirically useful conception of transparency. These include (a) concerns about the meaning of information quality, (b) concerns about the effects of transparency on organization-stakeholder relationships, and (c) concerns about the mechanisms that influence transparency perceptions. In the spirit of viewing each of these concerns as opportunities, we develop new theory that allows our ideas to be tested in future empirical research.

First, empirical applications of transparency have suffered from a great deal of conceptual variation as to what is exactly meant by information quality. Operational indications of transparency vary significantly across studies and include increased disclosure of information (e.g., Akkermans et al., 2004; Bushman et al., 2004; Eijffinger & Geraats, 2006), greater truthfulness and accuracy of information (e.g., Jordan, Peek, & Rosengren, 2000; Walumbwa et al., 2011), enhanced visibility and accessibility of information (e.g., Kaptein, 2008; Madhavan et al., 2005; Pagano & Roell, 1996; Prat, 2005; Zhu, 2004), increased clarity and understandability of information (e.g., Flood et al., 1999; McGaughey, 2002; Potosky, 2008), reduced information concealment (e.g., Granados et al., 2010; Larsson et al., 1998), and enhanced timeliness of information (e.g., Bloomfield & O’Hara, 1999; Jordan et al., 2000). Across these studies, some researchers favor combining all possible dimensions as formative inputs into a single additive transparency construct (e.g., Bushman et al., 2004; Khanna, Palepu, & Srinivasan, 2004; Patel, Balic, & Bwakira, 2002). Others argue that transparency is best viewed as an underlying latent construct without necessarily defining its dimensional structure (e.g., Kaptein, 2008; Pirson & Malhotra, 2011; Rawlins, 2008; Walumbwa et al., 2008). This state of affairs reveals that while researchers are clearly interested in transparency, there is no consensus as to exactly what factors differentiate higher-quality information from lower-quality information. As with any construct, meaningful insights about transparency will emerge only if scholars have a clear understanding of its definition and dimensional structure (e.g., Granados et al., 2010). Yet the lack of convergence around a unified explanation of the aspects of information quality that matter most to transparency has prohibited researchers from advancing a systematic theory of its antecedents and consequences.

Second, there is general consensus that the likelihood of observing a positive effect of organizational transparency on performance outcomes (Berggren & Bernshteyn, 2007; Bernstein, 2012; Christmann, 2004; Larsson et al., 1998) is dependent in part on how transparency influences the firm’s relationship with its stakeholders. For instance, many theorists have contemplated an association between organizational transparency and stakeholder trust in the firm to theorize more generally about its effects on firm performance outcomes (e.g., Akkermans et al., 2004; Pirson & Malhotra, 2011; Walumbwa et al., 2011; Williams, 2005). However, the majority of this work is characterized by cursory assertion rather than rigorous development of precisely how these constructs are theoretically related. Empirical examination is even less common and is characterized by mixed evidence as to how transparency actually influences trust. One study found compelling evidence of a positive relationship between organizational transparency and stakeholder trust (e.g., Rawlins, 2008), while another found only marginal support for the proposition that transparency is positively related to trust (e.g., Pirson & Malhotra, 2011). These incongruent findings suggest a need for further theoretical clarification of the transparency-trust relationship.

Third, no formal consensus has emerged to describe how organizations actually manage transparency perceptions. To illustrate, Bernardi and LaCross (2005) examined transparency in the context of code of ethics disclosures on organizational websites. Bernstein (2012) suggested that transparency varies according to the extent to which organizations use encryption (e.g., industry jargon) and shift visibility (e.g., private vs. open offices). Still others have examined transparency as a function of the methods used by organizations to convey information related to organizational governance and financing to stakeholders (Bhat et al., 2006; Bushman et al., 2004). Overall, the lack of a formal integration of the transparency literature has limited our ability to articulate the mechanisms available to organizations to manage it.

The Meaning of Information Quality

Theorists have come to disparate conclusions as to the aspects of information quality that are most important to conceptualize the dimensional structure of transparency. Though most theorists have measured transparency as a unidimensional construct (e.g., Pirson & Malhotra, 2011; Rawlins, 2008; Walumbwa et al., 2008), discordant applications across domains of organizational research have cultivated a proliferation of views regarding the most appropriate conceptualization and imply the need for a multidimensional structure. A closer examination of this collective body of work suggests that researchers have conceptualized transparency in three primary ways: disclosure, clarity, and accuracy. Based on a review of articles that discuss the underlying characteristics of transparency, Table 2 illustrates that common conceptualizations are subsumed within the perception of these three dimensions. This leads us to expect that each of these dimensions is a distinct critical factor that explains a fundamental aspect of transparency. Specifically, each contributes a unique perspective on the meaning of information quality such that together they provide a parsimonious foundation upon which to study transparency.

Overlap of Transparency Dimensions

Note: Articles were included if they explicitly discussed the characteristics of transparency and were published in academic journals (empirical or theoretical) with a relatively high impact factor (>3 for 5-year impact) or were cited more than 50 times through Google Scholar. Working papers, books, practitioner-oriented articles, and industry publications were omitted from this list.

Disclosure

Disclosure is defined as the perception that relevant information is received in a timely manner (e.g., Bloomfield & O’Hara, 1999; Williams, 2008). In the literature, a variety of studies advocate for the use of disclosure as a central dimension of transparency (e.g., Bushman et al., 2004; Finel & Lord, 1999; Madhavan et al., 2005; Nicolaou & McKnight, 2006; Pagano & Roell, 1996). Pirson and Malhotra (2011), for instance, measure transparency explicitly as a stakeholder’s perception that firms openly share all relevant information. Perotti and von Thadden (2005) suggest that perceptions of transparency are built around a stakeholder’s ability to gather needed information about a firm. These views are based on the premise that inaccessible information delimits the stakeholder’s ability to gain a full picture of the organization (Zhu, 2004).

The concept of disclosure implies that information must be openly shared for it to be considered transparent. Yet disclosure is more than the open transfer of all available information. It also warrants a careful consideration of the most relevant information to disclose. To illustrate, Williams (2008) has suggested four specific processes associated with disclosure: analysis (e.g., target audience identification), interpretation (e.g., determination of relevant information), documentation (e.g., encoding of information), and communication (e.g., distribution of information to internal and external audiences). Of these, only documentation and communication are associated with the open release of information. The other two processes (analysis and interpretation) are needed to differentiate relevant information from irrelevant information.

A number of theorists have discussed similar constructs as pivotal to transparency using several synonyms. Granados et al. (2010) have used the words availability and accessibility to describe fundamental aspects of transparency. Others have used the words visibility (Kaptein, 2008) or observability (Bernstein, 2012) to describe transparency. Similarly, Bloomfield and O’Hara (1999) have used the term real time to define transparency. All of these are similar to disclosure in the current conceptualization. Whereas visibility, availability, accessibility, and observability refer to aspects of open information sharing, the term real time suggests timeliness in our definition.

Intriguingly, we also found that information relevance was only passively incorporated into many conceptualizations of transparency. Most researchers define transparency narrowly (e.g., as trade and quote information in finance or as information regarding current order and production status in operations) such that information relevance is assured by the construct definition. This is clearly problematic for developing a systematic theory of transparency because not all researchers operating from diverse theoretical backgrounds will converge on a common conception of relevant information. To remedy this, we specify the importance of relevance while leaving space for variation in empirical application by emphasizing the broader concept of disclosure (e.g., Williams, 2008).

Clarity

Clarity is defined as the perceived level of lucidity and comprehensibility of information received from a sender. In the literature, Winkler (2000) contends that organizations must present information more clearly for it to be considered transparent. Similarly, Street and Meister (2004) have argued that organizational information must be understandable for it to be considered transparent. Daft and Lengel (1986) have found that a major problem for managers is a lack of informational clarity rather than a lack of sheer data. The importance of clarity is based on the premise that information consisting of industry jargon (Nicolaou & McKnight, 2006), unknown foreign languages (Larsson et al., 1998), and complicated mathematical algorithms (Granados et al., 2010) cannot be considered transparent even if it is highly disclosed. For instance, in the realm of financial markets, Flood et al. (1999) have argued that information must be disclosed and clear for market participants to fully ascertain its value.

Clarity differs from disclosure in that it is largely about the seamless transfer of meaning from sender to receiver rather than the amount or relevance of information shared. Accordingly, clarity relies on the skillful use of linguistic devices, such as pragmatics, to achieve higher levels of understandability (Watzlawick, Beavin, & Jackson, 1967). For instance, within uttered representations, clarity is a function of the perceived comprehensibility of both locutionary and illocutionary acts (Austin, 1962; Chomsky, 1995). Locutionary acts refers to the phonology of the utterance and its ostensible meaning, and illocutionary acts refers to the intended meaning of the utterance (Schiffer, 1972). Clarity is also a function of the proper application of verbal paralanguage, such as grunts, giggles, laughs, and sobs (Wilson, 2000); nonverbal paralanguage, such as turn taking (Sacks, Schegloff, & Jefferson, 1974); and the interpretation of nonverbal behavior related to body movements (Birdwhistell, 1970). In written communication, clarity is a matter of perceived grammatical and semantic coherence. For example, the use of abstract images (e.g., company logos) can delimit an observer from disentangling signifiers (words, images, and symbols) from denotata (what signifiers stand for) to render the image less clear (e.g., a picture worth a thousand words is veritably unclear).

While most theorists explicitly name clarity as a significant component of transparency (e.g., Flood et al., 1999; Potosky, 2008), several researchers have used closely related terms to describe the construct. McGaughey (2002) has used the term understandability to conceptualize clarity. In the context of information quality, Miller (1996) has used the term coherence to describe the degree to which information avoids confusion and promotes understanding. Nicolaou and McKnight (2006) have similarly used the term interpretability to refer to the perceived quality of information shared between two parties, and Briscoe and Murphy (2012) have suggested that information must be simple enough to be easily apprehended. These terms are similar to our conceptualization of clarity. Specifically, clarity implies that received information will “hang together” in a way that limits ambiguity.

Accuracy

Accuracy is defined as the perception that information is correct to the extent possible given the relationship between sender and receiver. The importance of accuracy stems from the perspective that information cannot be considered transparent if it is purposefully biased or unfoundedly contrived (Walumbwa et al., 2011). However, accuracy does not imply that information must be completely correct ex post for it to be considered transparent. Such a standard would be an impossible end to apply to exchanges of necessarily imperfect information (e.g., Taylor & Van Every, 2000). Instead, accuracy suggests that material claims should reflect precise qualifications about their expected validity for information to be considered transparent. In the literature, Vorauer and Claude (1998) and others (e.g., Granados et al., 2006) have argued that accuracy is a pivotal component of transparency. In fact, Akhigbe and Martin (2006) have suggested that inaccurate disclosures play a pivotal role in reducing corporate transparency and prompting corporate scandals. Within manufacturing firms, Bernstein (2012) has found that information accuracy is a cornerstone of workplace transparency.

Accuracy is unique to disclosure and clarity in that it is about information reliability rather than completeness or understandability (e.g., Angulo, Nachtmann, & Waller, 2004). With this in mind, a number of theorists have used related words to conceptualize accuracy in their assessments of transparency. Philippe and Durand (2011) have suggested that an organization’s claims related to its environmental footprint must be precise enough for external stakeholders to ascertain its actual ecological impact. Bushman et al. (2004) have suggested that information must be valid for it to be considered transparent. Similarly, Williams (2005) and Nicolaou and McKnight (2006) have suggested that organizational information must be seen as reliable for it to be considered transparent. These terms are similar to our conceptualization of accuracy.

Importantly, several authors have discussed related aspects of accuracy that fall outside of our current definition. For instance, Walumbwa et al. (2011) have defined transparency as a perception of leader behaviors that reveal his or her true thoughts and feelings. Although Walumbwa et al. emphasize disclosure as a conduit by which to assess leader behaviors, we contend that transparency is ultimately about information, and constructs such as truthfulness and honesty are more appropriately defined in reference to individual behavior. Accordingly, truthfulness and honesty are critical elements associated with individual behaviors that have the capacity to influence information accuracy but fall outside the focal content area of the transparency construct.

In sum, transparency appears to be a function of three theoretically viable and managerially relevant factors: disclosure, clarity, and accuracy. Disclosure is increased as stakeholders perceive information as more relevant and timely; clarity is increased as stakeholders perceive information as more understandable; and accuracy is increased as stakeholders perceive information as more reliable. Each of these dimensions contributes uniquely to overall levels of transparency by increasing stakeholder confidence in the quality of information received from the organization.

Transparency and Trust in the Organization-Stakeholder Relationship

Having described the dimensional structure of transparency, we now turn our attention to posit how transparency dimensions relate to stakeholder trust in the organization. Assertions of an association between transparency and the establishment or repair of trust in organization-stakeholder relationships are common, especially in response to a series of high-profile business scandals (e.g., Eijffinger & Geraats, 2006; Herdman, 2001; Kramer & Lewicki, 2010; Seidman, 2009a, 2009b, 2009c; Sheppard & Sherman, 1998; Vishwanath & Kaufmann, 2001). These views imply that organizational transparency is an antecedent to stakeholder trust. Yet these claims have been made without rigorous theoretical development, so it is unclear exactly how transparency and trust relate.

Mayer et al.’s (1995) trust theory postulates that trust refers to the willingness of stakeholders to be vulnerable to the actions of the organization. The proximal determinant of trust is the perceived trustworthiness of the organization, which is evaluated along three dimensions: ability, benevolence, and integrity. Ability refers to “the group of skills, competencies, and characteristics that enable a party to have influence within some specific domain” (Mayer et al., 1995: 717). For example, investors might rely on investment advice received from a wealth management firm because that firm is seen as having expertise in helping clients meet their financial goals. Benevolence refers to “the extent to which a trustee is believed to want to do good to the trustor, aside from an egocentric profit motive” (Mayer et al., 1995: 718). For example, investors might perceive a wealth management firm as being more benevolent when that firm does not tie advisor pay to the client’s choice of specific investments; in this case, clients are more likely to view the advice they receive as unbiased by the advisor’s own financial incentives (which might otherwise be at odds with the client’s investment goals). Rather, advice is more likely to be interpreted as being in the client’s best interests. Integrity refers to “the trustor’s perception that the trustee adheres to a set of principles that the trustor finds acceptable” (Mayer et al., 1995: 719). For example, a wealth management firm can foster perceptions of integrity with a reputation for high ethical standards and behavior (e.g., characterized by fairness, honesty, reliability, etc.). This theory has received extensive empirical support (Colquitt, Scott, & LePine, 2007; J. Davis, Schoorman, Mayer, & Tan, 2000; Mayer & Gavin, 2005), yet it did not specify the antecedents of trustworthiness perceptions, and very few empirical studies have examined this issue (Frazier, Johnson, Gavin, Gooty, & Snow, 2010).

In the only empirical study to date examining the role of transparency in the trustworthiness-trust relationship, Pirson and Malhotra (2011) assumed transparency to be a dimension of trustworthiness. Their findings indicated marginal support for the effect of organizational transparency on stakeholder trust when modeled with other trustworthiness dimensions. In other words, at conventional significance levels, there was no effect of transparency on trust when simultaneously accounting for established dimensions of trustworthiness (ability, benevolence, and integrity). These findings could mean that transparency (as a dimension of trustworthiness) is not actually related to trust, or it is inaccurately specified as a dimension of trustworthiness. In an attempt to clarify how transparency relates to stakeholder trust in the firm, we integrate our conceptual analysis of transparency with Mayer et al.’s (1995) trust theory to develop formal propositions regarding the role of transparency in managing trust in organization-stakeholder relationships.

Transparency and Trustworthiness

Given the central role of trustworthiness perceptions in determining trust, it becomes important to explain how these perceptions are formed. We argue that transparency perceptions (an evaluation of the quality of information provided by the organization) are used in determining trustworthiness perceptions (conclusions about the organization’s ability, benevolence, and integrity). Perception research has demonstrated that individuals rely on visible manifestations of an actor’s traits when forming perceptions of those traits (Bruner & Tagiuri, 1954; Estes, 1937). An application of this finding in the performance appraisal domain is the use of multisource feedback tools (which often include self-appraisal) to provide managers with performance-relevant information that would otherwise not be available to inform their evaluation of subordinates (Borman, 1997). Therefore, assessment of an actor’s traits can be facilitated by exposure to stimuli relevant to diagnosing those traits, especially when those stimuli come directly from the actor. Insofar as perceivers believe that organizations possess the capacity to shape and share information with varying degrees of quality, the perception of information quality from an organization should facilitate evaluations of the organization’s trustworthiness. Consistent with this argument, Mayer and Davis (1999) found that employee perceptions of information accuracy in the performance appraisal system were positively and directly related to their assessment of top management trustworthiness. Other studies have similarly shown that information-sharing practices can precede the development of global trustworthiness perceptions (Nakayachi & Watabe, 2005; Sonenshein, Herzenstein, & Dholakia, 2011).

Taken together, these studies suggest that transparency is an antecedent (rather than a dimension) of trustworthiness. In the sections that follow, we posit specific relationships between each dimension of transparency and each dimension of trustworthiness.

Disclosure

Disclosure of information entails the risk that this information might be subsequently used against the one making the disclosure (Derlega & Chaikin, 1977; Kelly, 1966); this risk increases with the degree of disclosure. Voluntary disclosure of information by organizations conveys a willingness to assume this risk in order to benefit the recipient in some way (e.g., allowing investors to make more informed decisions in their best interest guided by sufficient, relevant data). Information disclosure is central in the creation of integrative agreements reflecting a commitment to maximizing joint (instead of self) gain (Lewicki, Barry, & Saunders, 2010). Greater disclosure is therefore a signal that the one making the disclosure is doing so out of a desire to help the trustor in a way that exceeds purely egocentric concerns (Ganesan, 1997; Mayer et al., 1995).

Proposition 1a: Stakeholder perceptions of an organization’s information disclosure are positively related to perceptions of the organization’s benevolence.

In addition, to the degree that disclosed information has the potential to neutralize or impede the discloser’s egoistic motives, disclosure reflects fair dealing. Organizations may recognize that divulging some types of information to stakeholders is appropriate because it allows stakeholders to make informed decisions; yet this information might even be inherently threatening to the organization’s interests. The decision to disclose the information nonetheless is a decision to do “the right thing” rather than conceal the information to maintain unfair advantage. Insofar as disclosure indicates the firm’s intent to adhere to moral and ethical principles related to openness and information sharing, it stands as a signal of the organization’s integrity (Colquitt et al., 2007; Mayer et al., 1995).

Proposition 1b: Stakeholder perceptions of an organization’s information disclosure are positively related to perceptions of the organization’s integrity.

Clarity

Clarity refers to information provided in a way that is deemed coherent and lucid. The extent to which organizations convey information in a manner that can be readily understood by stakeholders should relate to perceptions of the organization’s ability. Conveying information with clarity involves understanding the perspective of the stakeholder audience(s). Unlike organizational insiders, stakeholders often have unique interests, needs, and concerns. They may also not be as familiar with internal organizational processes, routines, and jargon. When organizations carefully package and tailor information in a way that can be readily digested by stakeholders, they establish their ability to communicate effectively. Mayer et al. (1995) refer to ability as perceived expertise reflecting high aptitude in a technical or interpersonal domain. Other trust researchers have described ability in similar terms, including the knowledge, interpersonal skills, and communication skills to perform successfully (Colquitt et al., 2007; Gabarro, 1978).

Proposition 2: Stakeholder perceptions of an organization’s information clarity are positively related to perceptions of the organization’s ability.

Accuracy

Accuracy refers to information that is regarded to be correct. Providing fully correct information is a challenge for organizations operating in a complex, turbulent environment. Stakeholders often desire information that is highly technical and subject to compliance with a myriad of reporting regulations and standards (e.g., reporting on executive pay or pension plan details; Milkovich, Newman, & Gerhart, 2011). Organizations perceived to convey accurate information should influence perceptions of their ability to successfully navigate complex data and master the technical aspects of compiling needed data to develop reliable information. Consistent with this line of reasoning, one study found that customer evaluations of online sellers’ trustworthiness were predicted by the degree to which the seller processed their transaction correctly (Singh & Sirdeshmukh, 2000).

Proposition 3a: Stakeholder perceptions of an organization’s information accuracy are positively related to perceptions of the organization’s ability.

Accuracy also indicates the truthfulness behind information and, hence, the honesty of the organization. Integrity perceptions refers to the degree to which the organization enacts values that stakeholders find acceptable, including honesty (Dietz & Den Hartog, 2006; Larzelere & Huston, 1980). Particularly when information refers to issues that might be detrimental to the organization, accurate accounts signal honesty to stakeholders and hence reflect positively on the firm’s values. More generally, accuracy signals a basic aversion to engage in manipulative practices toward stakeholders, enhancing stakeholder perceptions of the firm’s integrity.

Proposition 3b: Stakeholder perceptions of an organization’s information accuracy are positively related to perceptions of the organization’s integrity.

Transparency and Trust

We posit that greater transparency from organizations (in the form of greater disclosure, clarity, and accuracy) will facilitate higher stakeholder trust in the organization. This is because trust reflects a willingness to be vulnerable to a trustee based on confident positive expectations of the trustee’s intentions and behaviors (Lewicki & Bunker, 1995, 1996); information quality (i.e., disclosure, clarity, and accuracy) shapes these expectations. Disclosure, clarity, and accuracy also enable accountability, whereby the organization can be rewarded for trustworthy behavior and punished for untrustworthy behavior; these factors also contribute to trust judgments (Lewicki & Bunker, 1995, 1996). Other researchers have also suggested that transparency and trust are positively related (e.g., Akkermans et al., 2004; Bennis et al., 2008; Fleischmann & Wallace, 2005), and there is some empirical evidence of this relationship. A field experiment in a downsizing company found that leadership transparency influenced followers’ level of trust and evaluations of leader effectiveness (Norman, Avolio, & Luthans, 2010). Another study found that transparency was instrumental for repairing damaged trust among stakeholders after a breach by the organization (Jahansoozi, 2006).

Proposition 4: Stakeholder perceptions of an organization’s information disclosure, clarity, and accuracy are positively related to trust in the organization.

Transparency, Trustworthiness, and Trust

Finally, we consider the relationships among transparency, trustworthiness, and trust. As we have stated earlier, we contend that transparency is an antecedent to trustworthiness, not a dimension of trustworthiness. Furthermore, we argue that transparency influences trust via its effect on trustworthiness perceptions. Specifically, transparency refers to characteristics of information, whereas trustworthiness refers to characteristics of the organization. Thus, transparency (i.e., information quality) informs the extent to which an organization is regarded as trustworthy (refer to Propositions 1 through 3). In turn, trustworthiness is the proximal predictor of trust: We place trust in those who are perceived to be worthy of that trust (Mayer et al., 1995). As a result, the relationship between transparency (of information) and trust (in the firm) should be due to trustworthiness perceptions (of the firm). This line of reasoning extends prior research indicating that trustworthiness is an antecedent to trust (e.g., Chou, Wang, Wang, Huang, & Cheng, 2008; Mayer & Davis, 1999) by explaining how trustworthiness perceptions are formed and how trustworthiness is the mechanism that facilitates the effect of transparency on trust.

Proposition 5: The effect of stakeholder perceptions of an organization’s transparency on trust in the organization is mediated by stakeholder perceptions of the organization’s ability, benevolence, and integrity.

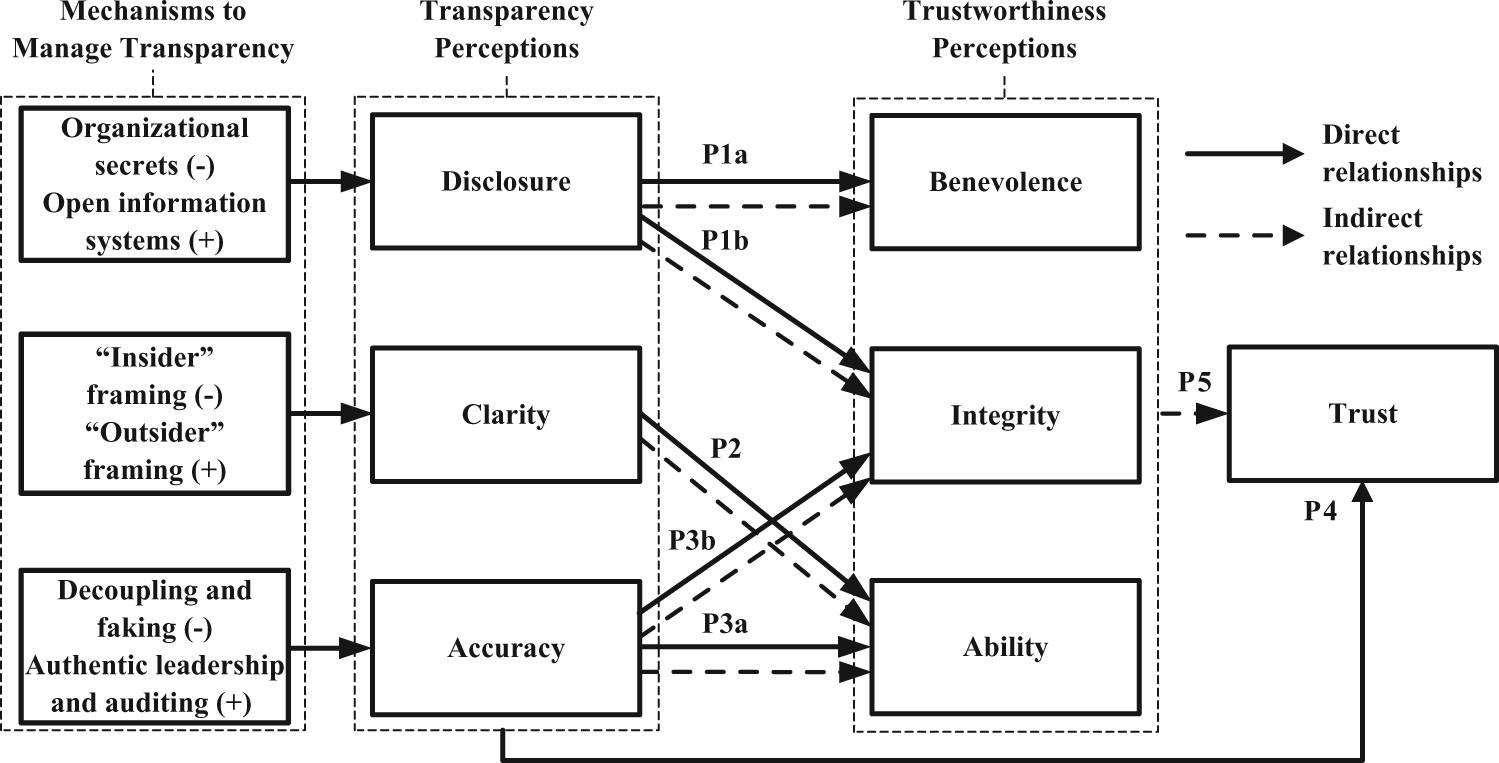

Mechanisms to Manage Transparency

In this section, we extend discussions related to the theoretical dimensions of transparency by examining specific ways in which organizations can manage it. This discussion is rooted in the understanding that when organization-stakeholder interests are misaligned, organizations might face incentives to strategically support or suppress transparency perceptions (e.g., Eisenberg, 1984; Gaa, 2009; Hannan, Polos, & Carroll, 2003). A firm’s stock of internal knowledge and effort to manage impressions toward its stakeholders give it some (but not ultimate) power to manage stakeholder perceptions. Firms carry the capacity to sway transparency perceptions through their tactical repertoires to manipulate information quality. For example, competitive advantages are often gleaned from the strategic withholding of information on the one hand (e.g., organizational trade secrets) and the strategic releasing of information on the other (e.g., partnerships or joint ventures) (e.g., Ndofor & Levitas, 2004). Consistent with this, Granados et al. (2005, 2008, 2010) suggest that the concept of transparency strategy—defined as organizational attempts to reveal, conceal, bias, or otherwise distort information shared with stakeholders—can be used to explain the tactics applied by firms to manage transparency. To formalize an intuition of the mechanisms that allow organizations to accomplish this, we discuss a number of common approaches adopted by firms to manage transparency next.

Mechanisms to Manage Disclosure

Organizations can reduce disclosure through the keeping of secrets, on the one hand, or increase disclosure through the use of open information systems, on the other. For instance, many researchers have noted that managers have a tendency to conceal negative organizational information (e.g., Abrahamson & Park, 1994; Eisenberg & Witten, 1987). Based on the widely accepted premise that organizations can produce rents from withholding proprietary knowledge (Liebeskind, 1997), case studies have revealed a number of examples of nondisclosure by corporate officers toward uninformed shareholders for the purposes of maintaining secrets (Starbuck, Greve, & Hedberg, 1978; Sutton & Callahan, 1987). Building on these studies, empirical findings suggest that organizations can hold one of two kinds of secrets: sanctioned and unsanctioned (Anand & Rosen, 2008).

Sanctioned secrets are intentionally maintained by the organization for the purposes of competitive advantage. Sanctioned secrets are “sanctioned” because they are generally considered legitimate by the firm’s stakeholders (e.g., Coca-Cola keeping its proprietary beverage formula confidential). Unsanctioned secrets, on the other hand, are considered illegitimate in the eyes of stakeholders (e.g., concealment of negative organizational performance information from stockholders) and can result from the need to maintain competitiveness in the midst of internal organizational crises (Starbuck et al., 1978). An example would be the shredding of material documents by Enron Corporation prior to its downfall (Sims & Brinkmann, 2003). Researchers have found that firms are particularly likely to engage in this form of nondisclosure when they are failing (Agnew, Piquero, & Cullen, 2009) or confronting resource scarcities (Finney & Lesieur, 1982). Taken together, the use of sanctioned and unsanctioned secrets allows organizations to strategically reduce transparency through nondisclosure.

The strategic use of secrets can be juxtaposed against the use of open information systems as a method to increase disclosure. Setia, Rajagopalan, Sambamurthy, and Calantone (2010) have found that organizations are progressively integrating open-source procedures as a means to share otherwise private information with stakeholders. Having a firm grasp on the information requirements of stakeholders is important to successfully increase disclosure through open information systems. To accomplish this, Web 2.0 technologies, such as social bookmarking (i.e., publicly viewable lists of bookmarks), can be used to move ideas and knowledge from one context to another (Peter, Salvatore, & Bala, 2011). Similarly, Wikis (i.e., websites that anyone can edit) provide opportunities for organizations to collaborate and share knowledge with stakeholders (Kane & Fichman, 2009).

Mechanisms to Manage Clarity

Organizations can influence clarity through the strategic use of frames to (a) bring coherence and understanding to stakeholders or (b) stimulate tactical confusion and ambiguity (e.g., Druckman, 2001; Kahneman & Tversky, 1984; Kuhberger, 1998; Levin, Schneider, & Gaeth, 1998; Tversky & Kahneman, 1981). The study of frames and framing has its origins in the work of Goffman (1974), who analyzed the cognitive processes that enable individuals to label and articulate experiences in terms of socially meaningful and familiar categories. In the domain of social movements, theorists have greatly advanced our understanding of frames as devices used to selectively punctuate and encode events in order to render them meaningful (Gamson, Fireman, & Rytina, 1982). In this way, frames are tools used by organizations to build collective momentum around shared interpretations of social activity (Hunt, Benford, & Snow, 1994). Consistent with this, we use the term framing to connote organizational attempts to alter the meaning of information content in ways that render it more or less understandable.

To increase clarity, one alternative is for organizations to compose “outsider” frames that reflect the interests and information requirements of specific stakeholder groups. Similar to managing disclosure, having an understanding of the information requirements of stakeholders is important to build frames that unambiguously transfer knowledge. For example, research on technology acceptance suggests that organizations can increase interest in new technology by constructing frames that appear lucid and straightforward to end users (e.g., F. Davis, 1989; Venkatesh & Davis, 2000). In a similar vein, organizations can use outsider frames to more clearly communicate with stakeholders through messages that accommodate the knowledge and information requirements of the stakeholder (Wolfe & Putler, 2002).

Alternatively, interest-driven actors can strategically distort information shared with stakeholders through “insider” frames that interrupt the stakeholder’s ability to decipher the meaning of received information (e.g., Campbell, 2004; Fiss & Zajac, 2006; Ronde, 2001). For example, Walker, Martin, and McCarthy (2008) have found that organizations alter their tactical repertoires, including their framing strategies, as they confront different stakeholders. Similarly, Kaplan (2008) has argued that frames are resources that politically savvy actors can use to alter the meaning of information. Consistent with this, organizations can tactically distort information by framing it as context specific (e.g., legalese or medical jargon; see Castro, Wilson, Wang, & Schillinger, 2007), socially embedded (e.g., foreign languages), or technically altered (e.g., modified typeface or small print; see Hagtvedt, 2011).

Mechanisms to Manage Accuracy

Organizations can decrease accuracy through faking and decoupling, on the one hand, or increase accuracy through candid interactions with stakeholders, on the other. With regard to the former, institutional theorists have elaborated a number of conditions that lead organizations to reduce accuracy by decoupling symbolic expressions of conduct from actual behaviors (e.g., Westphal & Zajac, 1998, 2001). For instance, Fiss and Zajac (2006) have found that managers often decouple espousal from actual implementation of strategic change initiatives to accommodate the interests of divergent stakeholder groups. Others have used the term faking to describe the condition that exists when individuals misrepresent known facts in an effort to appear competent and legitimate to the outside world (Komar, Brown, Komar, & Robie, 2008; McFarland & Ryan, 2000, 2006).

Greenwood, Oliver, Sahlin, and Suddaby (2008: 25) suggest that decoupling reveals “the dark side” of symbolic behavior when it reflects a willful manipulation of stakeholder perceptions in order to increase organizational performance. For example, Enron Corporation was successful in falsifying documents to preserve images of prosperity prior to its collapse in 2001 (Sims & Brinkmann, 2003). In the context of transparency strategy, faking and decoupling are forms of manipulation that reduce accuracy by diminishing the extent to which information conforms to the beliefs, logic structures, and lived experiences of the source.

The strategic use of decoupling and faking can be contrasted with organizational tactics to candidly share information with stakeholders (e.g., O’Toole & Bennis, 2009). To build a capacity for candid interactions with stakeholders, Serpa (1985) suggests that organizations must promote honesty across all levels of the firm by, for example, hiring authentic leaders (Walumbwa et al., 2011). Evans, Hannan, Krishnan, and Moser (2001) have found that organizations can cultivate honesty in management by offering employment contracts that allocate a greater share of total surplus to managers. With regard to external stakeholder relations, Pany and Smith (1982) have found that audited financial statements are perceived as more reliable by stakeholders than nonaudited financial statements. Taken together, managers appear to have a variety of leadership, resource allocation, and third-party alternatives to influence accuracy.

The above sections discussed a number of independent mechanisms that can be used to strategically manage transparency. These mechanisms are by no means an exhaustive list of alternatives available to organizations to manage transparency perceptions, nor are they meant to operate in complete isolation. Rather, they represent an initial set of approaches available to firms to manage specific aspects of transparency. In practice, organizations regularly implement policies that impact more than one dimension at a time. For instance, the development of a new website might increase disclosure but reduce clarity toward outside stakeholders if the information presented on the website is highly contextualized (e.g., industry specific). In addition, organizations often face resource constraints and competitive dynamics that render efforts toward complete transparency difficult to achieve (e.g., Chen & Miller, 2012). Taken together, these factors suggest that managing transparency is a complicated endeavor requiring organizations to balance internally defined objectives against the interests of divergent stakeholder groups. The mechanisms we propose above are offered as a first step toward future research on managing transparency in firms.

Our conceptual model of the mechanisms available to organizations to manage transparency and the proposed relationships discussed in the previous section is provided in Figure 2.

Conceptual Model of Mechanisms to Manage Transparency and the Association Between Transparency, Trustworthiness, and Trust

Discussion

Notwithstanding growing interest in the topic of transparency, researchers have thus far made little progress toward a unified definition of the construct. Moreover, despite the fact that researchers have operationalized transparency in a variety of different ways, it has continued to be regarded as a unidimensional construct. Theorists, practitioners, and pundits have increasingly called for greater transparency to curtail corporate malfeasance (e.g., Bennis et al., 2008; Fombrun & Rindova, 2000; Herdman, 2001; Jahansoozi, 2006; Tapscott & Ticoll, 2003), yet very little is known about how organizations actually manage it. To complicate matters, while many claims have been made about the relationship between transparency and trust (e.g., Eijffinger & Geraats, 2006; Kramer & Lewicki, 2010; Seidman, 2009a, 2009b, 2009c; Sheppard & Sherman, 1998), these have been devoid of rigorous theoretical development. Just as the transparency literature has been vague about how it relates to trust (the relationship has rarely been specified, and when it has, transparency has been viewed as a dimension of trustworthiness), the trust literature has ignored seemingly important questions related to the antecedents of trustworthiness (Elsbach, 2004).

Against this backdrop, this article takes initial steps toward a theory of transparency by systematically integrating the literature to compose a unified definition of the construct. This analysis addresses inconsistencies in the literature by illustrating overall consensus that transparency is best viewed as a perception of the quality of intentionally shared information from a sender (e.g., Akkermans et al., 2004; Bloomfield & O’Hara, 1999; Nicolaou & McKnight, 2006). Building on this emergent definition, we extend existing research on transparency by distinguishing between three of its underlying dimensions. Specifically, we suggest that transparency can be meaningfully conceptualized as the degree of information disclosure, clarity, and accuracy.

Prior empirical attempts to explain the impact of transparency on stakeholder trust have been met with mixed results. For example, one study found a positive relationship between organizational transparency and stakeholder trust in the firm (Rawlins, 2008), while another found only marginal evidence of such a relationship between transparency and trust when transparency was assumed to be a dimension of trustworthiness (Pirson & Malhotra, 2011). In this article, we draw on Mayer et al.’s (1995) framework of trust to propose new associations that illustrate how disclosure, clarity, and accuracy of information (i.e., transparency) are distinct from, and lead to greater stakeholder perceptions of, organizational ability, benevolence, and integrity (i.e., trustworthiness). We further propose that transparency leads to greater trust in the firm through its effects on stakeholder perceptions of organizational trustworthiness. Importantly, these propositions contribute equally to the trust literature by describing new mechanisms that can be used to increase trustworthiness.

To further elaborate the transparency concept, we describe common mechanisms used by organizations to manage disclosure, clarity, and accuracy. We suggest that organizations can decrease disclosure toward stakeholders through the keeping of sanctioned and unsanctioned secrets (e.g., Anand & Rosen, 2008) or increase disclosure toward stakeholders through the tactical use of open information systems (e.g., Peter et al., 2011; Setia et al., 2010). Firms can also decrease clarity toward stakeholders through the use of “insider” frames to bring confusion and distortion (e.g., Kaplan, 2008) or increase clarity toward stakeholders through the use of “outsider” frames to bring coherence and understanding (e.g., Hunt et al., 1994). Additionally, organizations can decrease accuracy toward stakeholders through decoupling and faking (e.g., McFarland & Ryan, 2006; Westphal & Zajac, 2001) or increase accuracy toward stakeholders through authentic leadership and auditing (e.g., Evans et al., 2001; Serpa, 1985). Together, these mechanisms compose an initial set of factors that can be used by researchers to examine how organizations influence transparency by positioning it within a broader nomological network of antecedent conditions.

We discuss the theoretical, management, and research implications of our framework of transparency in the sections that follow.

Theoretical Implications

We integrate the literature to provide a clear conceptual definition and build the case for a three-dimensional model of transparency. Our analysis illustrates that transparency is best viewed as a perception of the quality of intentionally shared information from a sender (e.g., Akkermans et al., 2004; Bloomfield & O’Hara, 1999) and emphasizes that transparency is a function of information disclosure, clarity, and accuracy. In this way, we provide a considerable step forward in the transparency literature through a new framework that has the capacity to be applied across contexts of organizational research. Next, we clearly distinguish between transparency perceptions and trustworthiness perceptions to crystallize an intuition of the role of transparency in the trustworthiness-trust relationship. Our analysis separates transparency from trustworthiness and trust to assert a new theory of transparency as a stand-alone concept ripe for further theoretical and empirical advancement. Although our ultimate objective is to systematically develop the transparency concept, our integrative framework of transparency and trust suggests a new category of antecedents of trustworthiness. We then explicate concrete mechanisms available to organizations to manage transparency perceptions. These mechanisms contribute to our theoretical development of “transparency strategy” (Granados et al., 2005, 2010) insofar as they outline specific approaches to manage information for deliberate changes in transparency.

Management Implications

The primary management implications of this article are threefold. First, the definition and dimensions of transparency offer managers a set of categories to increase transparency towards their internal and external stakeholders (Kochan & Robinstein, 2000; Mitchell, Agle, & Wood, 1997). Recent changes in organization-stakeholder relations indicate a trend toward interactions governed less by face-to-face communication and more by technology-enabled exchanges of information that can develop over great distances and intervals of time (e.g., via e-mails and letters; see Daft & Lengel, 1984; Daft, Lengel, & Trevino, 1987). Having an awareness of the meaning and dimensions of transparency should allow managers to maximize information quality given the specific nature of the organization’s relationship with its stakeholders.

Second, existing theory is insufficient to adequately explain the trust development process in environments characterized by arm’s-length exchanges of information. As a consequence, managers know little about how to avert large-scale organizational failures (e.g., Lehman Brothers) that are impacted greatly by dramatic shifts in outside stakeholder perceptions of trustworthiness. The framework presented in Figure 2 suggests that organizations can use information to increase stakeholder perceptions of organizational trustworthiness and trust even when the stakeholder does not have direct (i.e., face-to-face) interaction with the organization. This framework has the potential to be especially important in environments where (a) the firm is attempting to quell stakeholder unrest related to unsubstantiated claims of corporate malfeasance, (b) a breach of trust has already occurred (Kramer & Lewicki, 2010), or (c) the organization is interacting with a stakeholder for the first time.

Third, we offer concrete approaches to toggle between higher and lower levels of disclosure, clarity, and accuracy. In the management discourse, the framing of transparency as a strategic initiative has become ubiquitous (e.g., Bennis et al., 2008; Granados et al., 2010; O’Toole & Bennis, 2009; Zhu, 2004) yet we know very little about how organizations actually manage transparency. The mechanisms described in this article are offered as an initial set of approaches to increase or decrease transparency toward stakeholders.

Research Implications

Our theoretical framework suggests a number of directions for future research. First, and perhaps most obviously, it highlights the need for researchers to further investigate the role of transparency as a means to manage stakeholder relations. In this article, we have discussed the meaning, dimensionality, enabling mechanisms, and consequences of transparency in an effort to provide interested researchers with ample opportunities to empirically examine the role of transparency in organization-stakeholder relationships. For example, future research might examine our claim that transparency is indeed more appropriately viewed as a perception of information rather than a perception of the organization’s trustworthiness and that the former is an antecedent to the latter. Our work also points to the use of distinct measures of transparency and trustworthiness, with distinct referents (information and organization, respectively). Future studies should be designed to model and capture the mediating process we propose as well.

Second, subsequent research might also examine potential interrelationships among transparency dimensions. Each of these dimensions is posited to be a distinct factor of information quality (i.e., transparency) and, hence, may vary independently of the others. Other than suggesting that an organization perceived as high on all three dimensions is regarded as high in transparency (and an organization perceived as low on all three dimensions is regarded as low in transparency), it is beyond the scope of our article to contemplate minimum levels of each dimension necessary to create a perception of transparency or to articulate how these dimensions might interact with each other (cf. Mayer et al.’s [1995] analogous discussion in relation to trustworthiness dimensions). Yet this may be a fruitful area for future research.

Third, we have suggested a number of mechanisms to influence disclosure, clarity, and accuracy. Yet it is possible that other mechanisms might also influence each dimension of transparency. More research is needed to verify the influence of the mechanisms described in this article as well as to identify new mechanisms used to manage transparency.

Fourth, while most managerially relevant applications of transparency materialize at the organization level, our review of the literature suggests that transparency can develop across contexts of study and levels of analysis (e.g., between a firm and its suppliers or a government and its citizens). Our integrated definition and dimensions leave space for application at different levels of analysis, opening room for additional research opportunities.

Fifth, given the reciprocal nature of organization-stakeholder relationships (e.g., Pfarrer, Decelles, Smith, & Taylor, 2008; Rowley & Moldoveanu, 2003), we should also consider the role of stakeholder trust as an enabler of organizational transparency. For example, do organizations increase transparency when they perceive high stakeholder trust in the firm? This should allow us to further distinguish the influence of stakeholder groups on organizational conduct and policy.

Footnotes

Acknowledgements

This article was accepted under the editorship of Deborah E. Rupp. We would like to thank Corinne Coen, Susan Case, David Kolb, Ronald Fry, and the two anonymous reviewers for their thoughtful comments on earlier drafts of this article.