Abstract

Hostile takeover attempts are considered a key external governance mechanism aimed at addressing perceived managerial underperformance in a target firm. Studies show that target chief executive officers (CEOs) are usually dismissed shortly after a takeover attempt, regardless of whether the bidder actually completes the acquisition. Yet, little is known about the investment behaviors of target CEOs who actually retain their positions in the wake of an unsuccessful hostile takeover attempt. Engaging with this underexplored governance context, we advance a behaviorally informed model of CEO investment behaviors in response to external governance as a function of the negative performance feedback event of the takeover attempt and the timing of the market’s attempt in terms of the stage of the target CEO’s tenure. Based on a matched-pair study of 71 failed takeover attempts from 1995 to 2006, we find evidence of a nonlinear relation between target CEO tenure and degree of uncertainty of expected returns in subsequent strategic investments in the wake of a failed hostile takeover attempt. We discuss the implications for research on external governance, behavioral agency, and executives’ influences on firm processes and outcomes.

Keywords

Market control contests, in particular, hostile takeovers, have been shown to serve as efficient vehicles for activating value-creating change in underperforming firms (Fama, 1980; Franks & Mayer, 1996; Kini, Kracaw, & Mian, 2004). Some have suggested that the market intervenes as a “court of last resort” when internal mechanisms are compromised, clumsy, or deficient (Chatterjee, Harrison, & Bergh, 2003; Daily, Dalton, & Cannella, 2003; Jensen, 1986, Shivdasani, 1993). As opposed to benign mergers and acquisitions, where parties consensually attempt to reach mutually beneficial arrangements (Jemison & Sitkin, 1986; Ranft & Lord, 2000), hostile takeover attempts are driven by a bidder’s belief that acquisition of a target firm’s resources, paired with a reshuffling of its management, can increase the target firm’s value (Jensen, 1988; Martin & McConnell, 1991). In attempting to buy something that is not for sale, hostile takeover bids signal a “managerial failure” to maximize value from the firm’s resources (Cremers & Nair, 2005). Target CEOs of hostile takeover attempts are subsequently scapegoated as “bad CEOs” and often end up being “disciplined” through dismissal (Kini et al., 2004; Wiesenfeld, Wurthmann, & Hambrick, 2008).

Being on the receiving end of a hostile takeover attempt is an undesirable event for CEOs as it brings about uncertain consequences. Previous research has focused on the disciplining role of the market by examining the choice and implications of replacing versus retaining target CEOs when firms are successfully acquired by a bidder (Bergh, 2001; Cannella & Hambrick, 1993; Walsh & Ellwood, 1991; Wulf & Singh, 2006) as well as the implications of replacing CEOs of target firms when they are not (Fee & Hadlock, 2004; Jensen, 1988; Singh & Harianto, 1989). However, hostile takeover attempts do not always result in either a successful acquisition of the target firm or dismissal of its CEO. Yet, very little is known about what happens next in this context where, based on traditional explanations (cf. Franks & Mayer, 1996; Jensen, 1988; Kini et al., 2004), external governance has failed.

The implications of retaining the CEO after a failed bid is not only an unexplored event, but retaining the CEO is also a strategically crucial decision for signaling the firm’s direction and future prospects to external constituents (Pfeffer & Salancik, 1977; Salancik & Pfeffer, 1980). By signaling a concrete reaction to the failed bid, CEO replacement may appease stakeholders by attributing fault to the ousted CEO (Gamson & Scotch, 1964; Gangloff, Connelly, & Shook, 2014). On the other hand, retaining the CEO after the market signals its dissatisfaction may be perceived by stakeholders as an indication of inertia, indifference, or even indecisiveness in a context that begs for action. Hence, examining the strategic investment behaviors of retained target CEOs in the aftermath of failed bids is an intriguing governance context from which we can infer how firms react when the court of last resort fails.

In this study, we engage with the overarching question: How do retained target CEOs behave when the market’s attempt at correcting managerial failure, fails? We advance a behaviorally informed model of CEO investment allocations in response to external governance as a function of (a) the negative performance feedback event of a takeover attempt (Cyert & March, 1963; Jordan & Audia, 2012; March & Simon, 1958) and (b) the timing of the market’s takeover attempt in terms of the “season” of the target CEO’s tenure (Hambrick & Fukutomi, 1991). Tackling this gap fills an important void in the literature in light of recent criticism on the efficacy of the takeover market as an external control mechanism (Dalton, Hitt, Certo, & Dalton, 2007) and of research showing that decision makers’ behaviors often reflect their career-specific paradigms rather than value-maximizing goals of stakeholders (Hambrick & Fukutomi, 1991; Matta & Beamish, 2008; Miller, 1991).

In taking the aforementioned approach, we seek to make several contributions. First, whereas prior research on external governance has largely drawn on agency perspectives to argue that external governors should intervene by dismissing target CEOs (Cannella & Hambrick, 1993; Franks & Mayer, 1996; Jensen & Meckling, 1976; Kini et al., 2004), we highlight that the market is not always successful in executing this verdict. Our behaviorally informed model offers a fresh way to carry extant theory on external governance forward, by highlighting how target firms and their agents react when the court of last resort fails. Highlighting this governance context is important, as takeover attempts signal that a target firm is underperforming its perceived potential and the choice of retaining (vs. replacing) the CEO shows how the firm will react to the market’s judgment (Gamson & Scotch, 1964; Pfeffer & Salancik, 1977; Salancik & Pfeffer, 1980). In doing so, we pick up the literature where traditional agency explanations end and boost research on external governance, which has generally been underemphasized in the broader governance literature (Daily et al., 2003).

Second, whereas behavioral research in corporate governance has traditionally been concerned with understanding managerial risk behaviors in relation to internal governance mechanisms (Sanders, 2001; Sanders & Carpenter, 2003; Wiseman & Gomez-Mejia, 1998), we contribute to this stream by suggesting that CEO risk behaviors are also sensitive to external mechanisms. We highlight a governance context where the market attempts to intervene as a court of last resort, presumably because these internal mechanisms are deemed unsatisfactory (Jensen, 1986; Shivdasani, 1993), but fails, and we theorize that the dispositions inherent in the stage of a CEO’s tenure will serve as a basis for informing her or his ensuing risk appetite (or lack thereof). As such, it is important to take the dispositions inherent in the tenure stage of the target CEO into account, as these may become accentuated in relation to external governance attempts and translated into heightened risk-seeking or risk-avoiding behaviors.

Finally, and relatedly, we also contribute by advancing research into executives’ influences on firm processes and outcomes more generally, by theorizing how different “seasons” of CEO tenure become reflected in patterns of strategic investments (Hambrick & Fukutomi, 1991; Miller, 1991; Miller & Shamsie, 2001). As prior research has shown that the effects of CEO tenure on firm-level outcomes are complex and may be contingent on contextual factors (Hambrick & Fukutomi, 1991; Simsek, 2007; Wu, Levitas, & Priem, 2005), we emphasize the role of external governance in activating the CEO tenure effect on firm-level processes and outcomes. Our findings, based on a matched-pair study of 71 failed hostile takeover bids among publicly listed U.S. firms during the 1995-to-2006 period, provide support for our model and show a U-shaped relation between CEO tenure and strategic investments with lower uncertainty of expected returns (capital expenditures) and an inverted U-shaped relation between CEO tenure and strategic investments with higher uncertainty of expected returns (research and development) (Kothari, Laguerre, & Leone, 2002). We add to the literature that the target CEOs’ behaviors in response to failed external governance are not uniform but, rather, vary in complex ways for CEOs in different “seasons” of their tenure.

Conceptual Background: Hostile Takeovers as an External Governance Mechanism

Shareholders rely on internal and external governance mechanisms to safeguard their due return on investments (Daily et al., 2003; Dalton et al., 2007; Walsh & Seward, 1990). Internal governance mechanisms typically comprise incentive packages (e.g., designing appropriate executive compensation) and monitoring (e.g., through board of directors’ independence and outside equity ownership) (Dalton et al., 2007). However, various corporate scandals have highlighted the limitations of overreliance on internal governance (Jensen, 1993). Consequently, research has turned to the role of market actors as external governance mechanisms (Jensen, 1993). These include financial analysts (Wiersema & Zhang, 2011), professional investors (Walsh & Kosnik, 1993), the media (Bednar, Boivie, & Prince, 2013), and ultimately, other firms through the market for corporate control to address the issue of firms underperforming their perceived potential.

The literature on acquisitions has acknowledged that hostile takeovers serve as key external governance mechanisms with the particular property of disciplining underperforming target managers through dismissal (Cremers & Nair, 2005; Kini et al., 2004; Scharfstein, 1988; Walsh & Kosnik, 1993). As Jensen (1986: 10) postulated, a takeover functions as a “court of last resort . . . when the corporation’s internal controls and board level control mechanisms are slow, clumsy, or deficient.” Building on Jensen, Franks and Mayer (1996) provided evidence that the role of the market in corporate control is one of disciplining underperforming managers, especially when internal control mechanisms are relatively weak or ineffective (see also Shivdasani, 1993). Similarly, Schranz (1993) argued that the threat of hostile takeovers serves as an important governance mechanism by keeping managers “on their toes” and that firms in markets with higher takeover activity tend to produce better financial results.

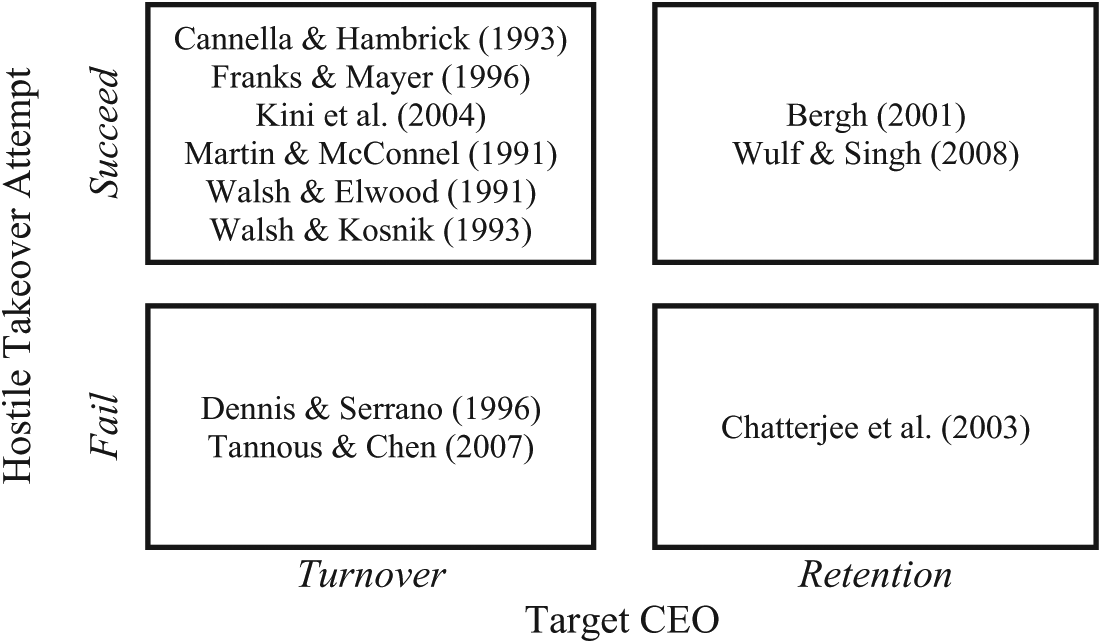

Yet the actual role of target firm managers remains unclear and largely unaddressed. Although some studies have examined the choice of replacing versus retaining target managers when takeovers succeed (Bergh, 2001; Cannella & Hambrick, 1993), as we summarize in Figure 1, still very little is known about the behaviors of target firms and their managers in the wake of a failed takeover attempt. The meager evidence in this broader area suggests that target firms of failed takeovers might be compelled to take action and implement the policies they believe would have been enacted by their bidders (Berger, Ofek, & Yermack, 1997; Chatterjee et al., 2003; Safieddine & Titman, 1999). As the market’s intervention would have probably resulted in target CEO dismissal (e.g., Kini et al., 2004), a core choice for the target firm when the takeover is unsuccessful is whether to replace or retain the CEO.

Representative Studies on Takeover Attempts and Career Consequences for Target CEOs

Some scholars have underscored that when firms perform poorly, they tend to replace the CEO not necessarily because they believe that the CEO is the only or most important cause of firm underperformance, but because they want to take a quick action that will signal to stakeholders that the board has taken action to address the firm’s performance concerns (e.g., Wiersema, 2002; Zhang, 2008). As the CEO is typically the most visible actor held accountable for an organization’s strategy, replacing the CEO may be perceived by stakeholders that the board acknowledges there is a problem and appears to be undertaking action to solve it (i.e., through dismissal of underperforming CEO). Accordingly, a few studies have documented that target CEOs are likely to face negative career consequences, such as dismissal, even when the takeover is unsuccessful (Denis & Serrano, 1996; Tannous & Cheng, 2007). 1

Conversely, retaining an “underperforming” target CEO creates a puzzling governance context that sends mixed signals to stakeholders (cf. Gangloff et al., 2014). On the one hand, in the governance context where a target CEO is retained in the aftermath of a failed takeover, a firm cannot simply disregard the fact that the market visibly thinks its CEO is not meeting the aspiration levels of critical external constituents—and thus the need for some form of adaptive change. On the other hand, retaining the CEO in this context may be perceived by stakeholders as an indication of inertia, indifference, or even indecisiveness in a context that calls for action. Retained target CEOs thus come under increased scrutiny and inflated expectations to engage in observable actions to send renewed signals of their competence and ability to exercise strategic leadership, creating a scenario where CEOs are compelled to undertake action to regain investor confidence.

Chatterjee et al. (2003) took a commendable preliminary step in this area and showed that target firms’ strategic behavior in this context depends on whether their boards of directors are independent from management or not. Specifically, whereas independent boards are likely to ignore the takeover attempt, firms with nonindependent boards are likely to view the hostile takeover attempt as a “wake-up call” and adjust their strategy through corporate refocusing. Yet, the premise from agency theory is that hostile takeovers actually emerge as a court of last resort to substitute deficiencies in these internal mechanisms (Jensen, 1986; Shivdasani, 1993). Thus, controlling for internal mechanisms, what kind of strategic behavior or reaction, if any, can we expect from retained target CEOs in the aftermath of a failed takeover attempt?

A Behavioral Approach to Retained Target CEO Conduct

Studies in the behavioral tradition have documented that decision makers adjust their risk behaviors in relation to performance feedback and engage actively in problem-solving behaviors to re-achieve par levels of acceptable performance (Cyert & March, 1963; Jordan & Audia, 2012; March & Simon, 1958). From a retained target CEO’s perspective, the market’s attempt to intervene represents an evaluation of her or his previous action and current expectations of her or his abilities to lead the firm into the future. As such, we conceptualize the takeover attempt as negative performance feedback and build on behavioral studies, which have documented that decision makers’ actions (especially their risk preferences) are sensitive to performance feedback.

The behavioral theory of the firm acknowledges that complex decisions with uncertain outcomes, such as corporate strategic investment decisions, are largely due to “bounded rationality” rather than rational calculation in view of economic value maximization (Cyert & March, 1963; Hambrick & Mason, 1985; March & Simon, 1958; Simon, 1965). The concept of bounded rationality implies that decision makers have cognitive limitations. Due to such limitations, they react to external stimuli on the basis of a “paradigm,” which is derived from their experience (or background) and contextual conditions in which their preferences, career concerns, and biases are situated (Barker & Mueller, 2002; Carpenter, Geletkanycz, & Sanders, 2004). In particular, research has highlighted that CEOs may exhibit different behaviors depending on the stage of their tenure and that their commitment to paradigms are likely to vary over time (Hambrick & Fukutomi, 1991; Miller, 1991; Miller & Shamsie, 2001). Accordingly, we argue that CEOs are likely to react differently to negative performance feedback in different stages of their tenure.

Prior research informs us that CEOs in different stages of their tenure have different career concerns and will have developed clearer versus more uncertain causal linkages between their actions and expectations about payoffs. Examples are CEO learning and adaptive reaction (Henderson, Miller, & Hambrick, 2006; Miller & Shamsie, 2001) and entrepreneurial initiatives (Simsek, 2007). As such, reactions to events that affect the career prospects of CEOs may be contingent on the stage in the tenure of the CEO, as this accentuates CEOs’ concerns about how current actions may affect future opportunities. Consequently, in the aftermath of an event that is likely to reflect negatively on CEOs, such as a failed hostile takeover for retained target CEOs, the stage in the tenure of target CEOs is important for theorizing how they will behave in terms of subsequent strategic investments.

The Role of CEO Tenure

The literature on CEO tenure informs us that CEOs in an early stage in their tenure cycle are under political and social pressure to respond to initial mandate expectations and show tangible results (Hambrick & Fukutomi, 1991). Early-tenure CEOs are likely to show motivation to take action and “make their case,” that is, develop a track record and legitimacy, since they are still in a relatively vulnerable position (Fredrickson, Hambrick, & Baumrin, 1988). CEOs during this stage are likely to take action predominantly in the domains where they have built expertise (Gabarro, 1987), that is, the domains where they feel more confident or certain about expected returns. As previous research documents, early-tenure CEOs are most likely to take conservative actions, such as focusing on low-uncertainty projects as opposed to taking risks, because the CEOs’ future career opportunities are contingent on the tangible performance evidence they display in the early stages (Murphy & Zimmerman, 1993). After a failed takeover attempt, early-tenure CEOs may be increasingly motivated to take actions to counter potential perceptions of managerial underperformance or failure, as these CEOs are likely to be sensitive to career concerns and susceptible to exhibit greater conformity and risk aversion (Chevalier & Ellison, 1999; Nam, Wang, & Zhang, 2008). As a result, target CEOs with relatively short tenure are likely to take action focusing on strategic investments having a relatively low uncertainty of expected returns. That is, we expect a failed hostile takeover attempt to accentuate the previously described proclivity of early-tenure CEOs to take action in a low-uncertainty direction.

However, as CEOs progress in their tenure beyond their liability of newness, they establish a track record, are likely to have developed confidence and power (Hambrick & Fukutomi, 1991; Ocasio, 1994), and may subsequently entrench themselves in the CEO position (Shleifer & Vishny, 1989). In entrenching themselves as the CEO, they reduce career concerns and increase job security, endowing them with more leeway for experimentation and forming the basis for making bold moves that can cement their distinctive legacy. Accordingly, mid-tenure CEOs are likely to exhibit greater openness to uncertainty, learning, and experimentation (Hambrick & Fukutomi, 1991). As a result, mid-tenure CEOs are likely to be involved in ongoing strategic investment projects of a more uncertain nature in terms of expected returns. After a failed hostile takeover attempt, mid-tenure CEOs are likely to be aware that it is costly for corporate shareholders to replace them, while already having the proclivity to engage in a behavior entailing greater uncertainty. Therefore, failed takeover attempts may further reinforce mid-tenure CEOs’ inclination toward higher-uncertainty investment behavior. That is, we expect a failed hostile takeover attempt to accentuate target mid-tenure CEOs’ proclivity for higher-uncertainty investment allocations.

The literature on CEO tenure also informs us that CEOs in a late-tenure stage can grow “stale in the saddle” (Miller, 1991), exhibiting an increased commitment to existing strategies (Hambrick & Fukutomi, 1991). That is, late-tenure CEOs become increasingly tied to the status quo, impeding investments in innovative strategies (Henderson et al., 2006). In addition, prior research documents that late-tenure CEOs are less involved in acts of substance and more involved in impression management and symbolic actions with which they are comfortable, that is, actions implying low substantive uncertainty (Romanelli & Tushman, 1983). In the aftermath of a failed hostile takeover attempt, retained late-tenure CEOs may be strongly inclined to take action to preserve their legacy (Kahneman & Lovallo, 1993). They may engage in actions that show increasing risk avoidance and decreased willingness to learn (Henderson et al., 2006). This is because late-tenure target CEOs may expect not to remain in office for long and thus avoid engaging in projects with higher uncertainty of expected returns, as they are likely to prefer, at this later stage of their tenure, to show strong accounting and market earnings (McClelland, Barker, & Oh, 2012). Preserving their legacy will increase their postcareer opportunities, for instance, as board directors and/or advisors (Brickley, Linck, & Coles, 1999; Gibbons & Murphy, 1992; Matta & Beamish, 2008). Therefore, late-tenure CEOs may be increasingly inclined to act by investing in strategies with low uncertainty of expected returns, aimed at restoring and preserving their legacy. That is, a failed hostile takeover may accentuate late-tenure target CEOs’ inclination toward low-uncertainty actions.

Taken together, the aforementioned arguments suggest that in the wake of a failed hostile takeover, target CEO tenure will have a nonlinear effect on subsequent strategic investment behavior. Early-tenure target CEOs and late-tenure target CEOs will favor strategic investments that are likely to have a relatively low uncertainty of expected returns. In contrast, mid-tenure target CEOs will undertake strategic investments that are likely to have relatively higher uncertainty of expected returns. The above arguments suggest the following two hypotheses that distinguish between strategic investment behavior entailing low uncertainty of expected returns, on the one hand, and behaviors entailing high uncertainty of expected returns, on the other. These two mirroring hypotheses predict the direction in which target CEO tenure relates to strategic investments with lower or higher uncertainty of expected returns after a failed takeover attempt.

Hypothesis 1: In the wake of a failed takeover attempt, target CEO tenure will have a U-shaped effect on subsequent investments with lower uncertainty of expected returns.

Hypothesis 2: In the wake of a failed takeover attempt, target CEO tenure will have an inverted U-shaped effect on subsequent investments with higher uncertainty of expected returns.

Data and Method

Research Design

We adopt a matched-pair research design to analyze the population of publicly listed U.S. firms that were targets of failed hostile takeover bids from 1995 to 2006. Matched-pair designs follow a quasiexperimental logic that allows for an effective way to sample the occurrence of a well-specified but nonrandom event (i.e., a failed hostile takeover bid where the CEO of the target firm retains her or his position). Pair matching allows for variance reduction among potentially influential unobserved factors while maximizing variance in the constructs of interest so as to isolate specific effects and relations (Dunlap, Cortina, Vaslow, & Burke, 1996). Pair matching has the added benefit that it also allows for a priori mitigation of endogeneity concerns, as it provides built-in controls for confounding factors that are inherent in the noise surrounding random sampling of these types of events. The entire data set includes an equally weighted portfolio of publicly listed U.S. companies subject to a failed takeover attempt and their respective paired matches.

Sampling Procedure

We constructed a database on which to test our model in two stages. The first stage dealt with the firms to be sampled based on the event and the second stage dealt with finding suitable matches with which to pair these firms. In the initial stage, we drew up a list of firms that, from 1995 to 2006, were targets of a hostile takeover bid in which the bidder sought to amass more than 50% of the controlling shares. Data for these firms were collected using the Deals Analysis Module in the Thomson One Banker database. Firms from heavily regulated industries (e.g., railroads and utilities) and financial firms were excluded because they are subject to special accounting and regulatory requirements, making them difficult to compare with other firms. Following prior procedures, this was effected by excluding the companies with the Standard Industrial Classification (SIC) codes 4000 to 4999 (regulated companies) and 6000 to 6999 (financial companies) from the sample (Ahn & Walker, 2007). This approach provided us with 92 potential cases.

Then, we selected the cases in which (a) both bidder and target were incorporated in the U.S., as studies have shown that national governance institutions could account for unobserved heterogeneity (Capron & Guillén, 2009) and (b) the hostile bid occurred and failed within the same fiscal year in which the bid was made, as it was necessary for the purposes of the study for the CEO to know whether the bid would fail or succeed and whether she or he would subsequently keep her or his position. This is a necessary condition to activate the theorized behavioral mechanisms of interest. We also (c) selected cases that were not targets of multiple bidders simultaneously. 2 Next, since we were interested in the CEOs who retained their positions, the CEO of the target firm must have had her or his position as CEO at least for the full fiscal year of the failed takeover bid, and subsequently must have kept her or his position at least two fiscal years after the year of the takeover bid. The information was obtained from proxy statements and annual reports. This stage led to the selection of 71 focal cases.

In the next stage, we turned to pairing the selected focal cases with comparable firms that were not subjected to a hostile takeover bid during the period of observation of the focal cases. To do so, we first compiled a shortlist of potential pairs based on three-digit SIC codes by selecting the five firms that were closest to each focal case in terms of total assets, as per data obtained from Compustat. We dug deeply into each candidate firm to understand its specific context and to establish if the conditions previously identified could be satisfied, which required in-depth case-by-case inspection of pair candidates to determine that no CEO turnover took place in the relevant observation years of our analysis, and finally to ensure that these firms had not been targets of hostile bids themselves during the respective period. The candidates were rank ordered by the researchers, and in the odd case when multiple near matches were the top-ranked candidate, we selected the closest possible alternative based on mutual agreement.

This approach resulted in 71 matched cases for which suitable near matches were identified. The matching criteria and the size of the number of matched cases are comparable to prior research employing a matched-pair research design (e.g., Bruton, Oviatt, & White, 1994; Singh & Harianto, 1989; Walsh & Kosnik, 1993). To further test the adequacy of our matching procedure, we conducted independent-samples t tests to see if there were significant a priori differences between the means of the focal firms and their matched pairs in the matching year (t0). No significant differences were diagnosed when looking at the matching criteria and the main dependent, independent, and control variables of interest, with the exception of age (target CEOs were three years older on average). The cause of termination of the bid is not reported in the Deals Analysis Module of Thomson One Banker for most of the firms, and we sought this information in archives of newspapers and articles. In our sample, 29.35% of the bids were rejected by target shareholders, whereas another 29.35% were repelled by the target. For 21.74% of the failed takeovers, no specific reason could be identified, 11.95% were withdrawn by the bidder, and 7.61% failed due to miscellaneous reasons, like failures of takeovers due to specific reasons, such as government disapproval or breach of contract. The final data set consisted of 142 observations.

Variables

Dependent variables

To distinguish between strategic investment behavior entailing low uncertainty of expected returns and behavior entailing high uncertainty of expected returns, we focused our attention on two accounting measures (as listed in the Compustat database) of strategic investments that have been shown to be at the discretion of the firm’s CEO and can be compared across firms: capital expenditures (CAPEX) and research-and-development expenditures (R&D). Investing in CAPEX entails less uncertainty of expected returns, whereas investing in R&D entails more uncertainty of expected returns, since prior research has shown the return volatility for these accounting measures to be less and more volatile, respectively (Barker & Mueller, 2002; Kothari et al., 2002). As Kothari et al. (2002: 357) note, “future benefits from R&D investments are more uncertain than those from capital expenditures.” CAPEX is depreciated over the useful life of property, plants, and equipment, and each depreciable amount is charged to the income statement in the year the item has helped generate profit (Istvan, 1961). Thus, these two accounting measures are both measures of strategic investment behavior but with differential levels of uncertainty of expected returns.

The dependent measures we employed were operationalized as the log (to tackle skewness in the distributions when taking $ units) of the industry median-adjusted level of CAPEX at t+1 and similarly the log (to tackle skewness in the distributions when taking $ units) of the industry median-adjusted level of R&D at t+1 based on data from Compustat. We took the industry median-adjusted level for both dependent variables in order to mitigate unobserved industry-level effects, given the heterogeneous sectors represented in our sample.

Observing the dependent variables at t+1 is in line with relevant prior research. Specifically, Gabarro (1987) has documented that a new CEO needs about 2 to 2.5 years to have an impact on her or his organization, especially if the new CEO is an outsider (often the case when the predecessor was dismissed due to underperformance; e.g., Boeker & Goodstein, 1993). In the context of our study, we focus on CEOs who retain their position after the failed takeover attempt; hence they are “insiders,” and as a result, it is reasonable to expect to observe an earlier impact (or even a much earlier impact) than the 2 to 2.5 years. The context of our study, that is, failed takeover attempts after which the CEO is retained, may further enhance the necessity for quicker action; therefore we reasonably expect patterns of investment behaviors to become visible at t+1.

Explanatory variables

Data on CEO tenure were collected from proxy statements available in the Securities and Exchange Commission (SEC) database and annual reports of the companies. CEO tenure indicates accumulated tenure in number of years at t0. Our research reports a mean of 9.91 for target CEO tenure at the time of the takeover attempt, consistent with Buchholtz and Ribbens (1994), for instance, who reported a mean of 9.10 for CEO tenure at the time of the takeover attempt. The average CEO tenure for our entire sample was 10.07 years. To test for the curvilinear relationship between CEO tenure and investment behavior after a failed takeover attempt, we created a variable by taking the square of the mean-centered CEO tenure variable, and then we constructed an interaction term for this variable with a dummy variable identifying the 71 focal cases of failed hostile takeover attempts. As high levels of multicollinearity can be expected with the interaction of categorical and continuous variables in linear models (Aiken & West, 1991), we residual-centered all the interaction terms used (see Zhang & Rajagopalan, 2010, for an application of this procedure).

Control variables

To isolate the effect of our hypothesized predictors on the dependent variables, we controlled for several important factors identified in the literature. The control variables were measured at t0. Of particular importance was board independence, as identified by Chatterjee et al. (2003). Board independence captures some of the effect of whether the takeover threat is considered a sign of managerial failure or not. We measured board independence with the percentage of outside directors sitting on the firm’s board (Beatty & Zajac, 1994; Masulis, Wang, & Xie, 2007). We also included a dummy indicating CEO/chair duality, which might account for CEO power, and hence why the CEO kept her or his job after the failed bid (Iyengar & Zampelli, 2009; Rechner & Dalton, 1991). We controlled for institutional ownership, measured by the percentage of equity held by institutional investors (Goranova, Alessandri, Brandes, & Dharwadkar, 2007); CEO ownership, measured by the percentage of equity held by the CEO (Goranova et al., 2007; Shleifer & Vishny, 1986); and CEO variable compensation, measured by the percentage of the equity-based component of the CEO’s compensation (Matta & Beamish, 2008). We accounted for the potential effects of CEO social capital by including the number of external board directorships held by the CEO (Geletkanycz, Boyd, & Finkelstein, 2001). Furthermore, we controlled for CEO age (McClelland et al., 2012), CEO technical background as a dummy if the CEO had formal educational training in the STEM (science, technology, engineering, and mathematics) fields, and finally, a dummy for CEO advanced education if the CEO had a formally attained master’s degree or higher level of education. Data on CEO background were collected from SEC reports, corporate profiles, and the business press (e.g., Forbes and Fortune).

We also controlled for specific characteristics of the failed bidder, given that the credibility of the (failed) takeover may vary and, subsequently, the firm’s strategic behavior in terms of our dependent variables. 3 Specifically, we controlled, first, for whether the bidder was a private firm, with a dichotomous variable that equals 1 and 0 otherwise. Private firms are considered to be better governed, experiencing much lower agency costs (Jensen, 1989). Second, we controlled for the track record of the bidder in terms of successful bids up to 3 years before the focal failed bid. This is a dichotomous variable with values of 1 when the bidder was a publicly traded firm and had a 100% successful record in all its bids for the prior 3 years and 0 otherwise. Third, we controlled for the size of the bidder, given that larger organizations typically have greater visibility and resources, in terms of total assets relative to the size of the target firm, with a dichotomous variable equaling 1 when the bidder was a publicly traded firm and was larger than the target firm. We also controlled for the duration of the takeover bid in months, as bids that take longer might be indicative of powerful bidders that are more difficult to avert and might elicit different internal processes or disagreements as to the merits of the takeover. Data on the identity and the characteristics of the failed bidder were collected from Thomson One Banker, Zephyr, and the business press.

We also included controls to account for the firm’s CAPEX expenditures and R&D expenditures at t0 by taking the log of the corresponding industry median-adjusted level of expenditures (same as the operationalization of the dependent variables at t+1). This is because prior level of firm expenditures, depending on the industry within which it operates, could influence subsequent expenditures, and prior investments may make it difficult to change strategies due to strategic momentum and inertia. In addition, we controlled for firm size by employing the log of total employees (Chatterjee & Wernerfelt, 1991), firm sales as the most fundamental and visible indicator of firm financial performance, firm leverage by employing the debt-to-equity ratio (Gibbs, 1993), firm profitability by employing an industry-adjusted measure of earnings per share (Masulis et al., 2007), dividends paid at t0, and time effects by including year dummies.

Results

Descriptive Statistics

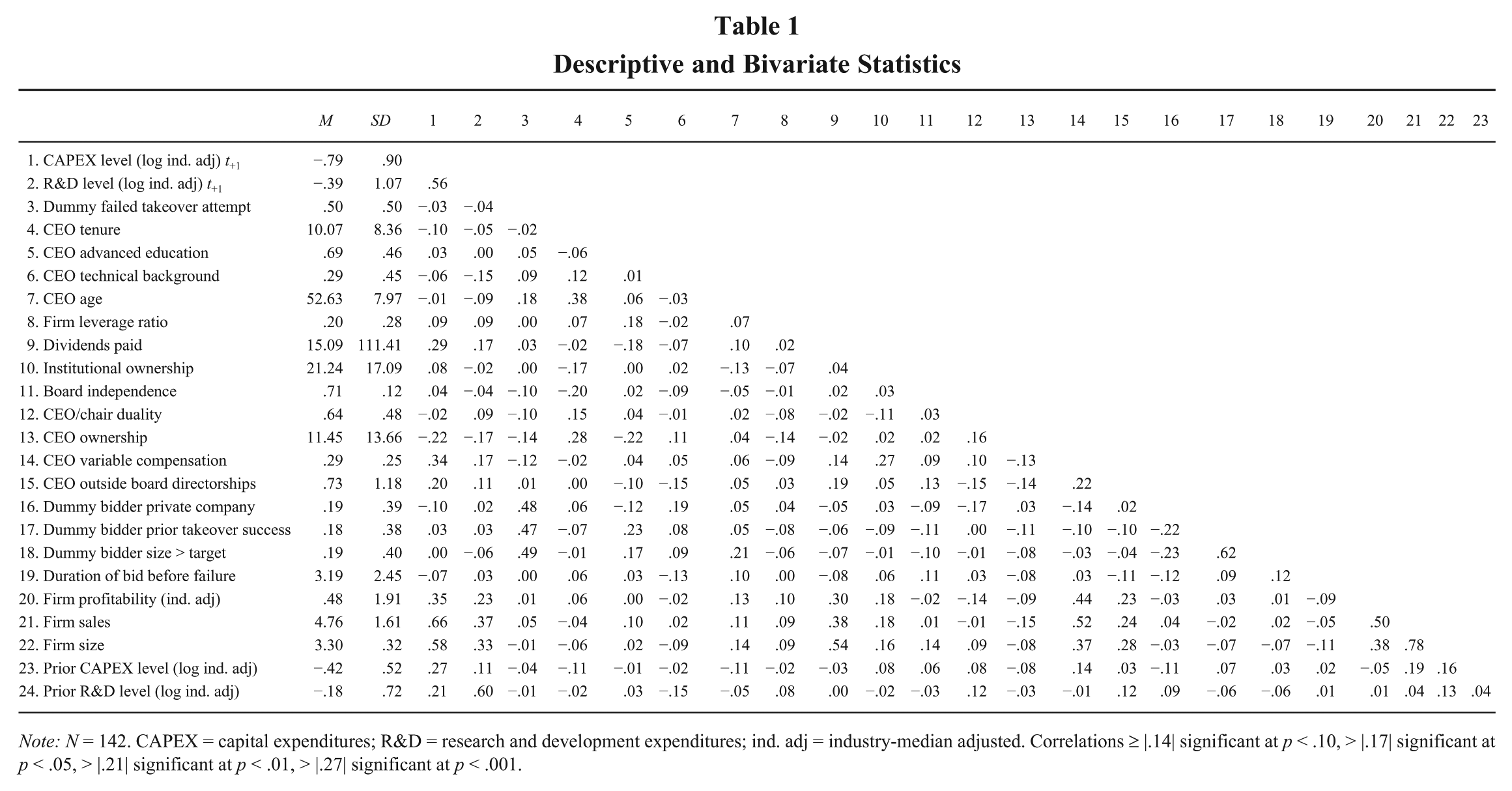

Table 1 shows the overall means, standard deviations, and bivariate correlations for the variables used in the subsequent multivariate analyses.

Descriptive and Bivariate Statistics

Note: N = 142. CAPEX = capital expenditures; R&D = research and development expenditures; ind. adj = industry-median adjusted. Correlations ≥ |.14| significant at p < .10, > |.17| significant at p < .05, > |.21| significant at p < .01, > |.27| significant at p < .001.

Multivariate Results

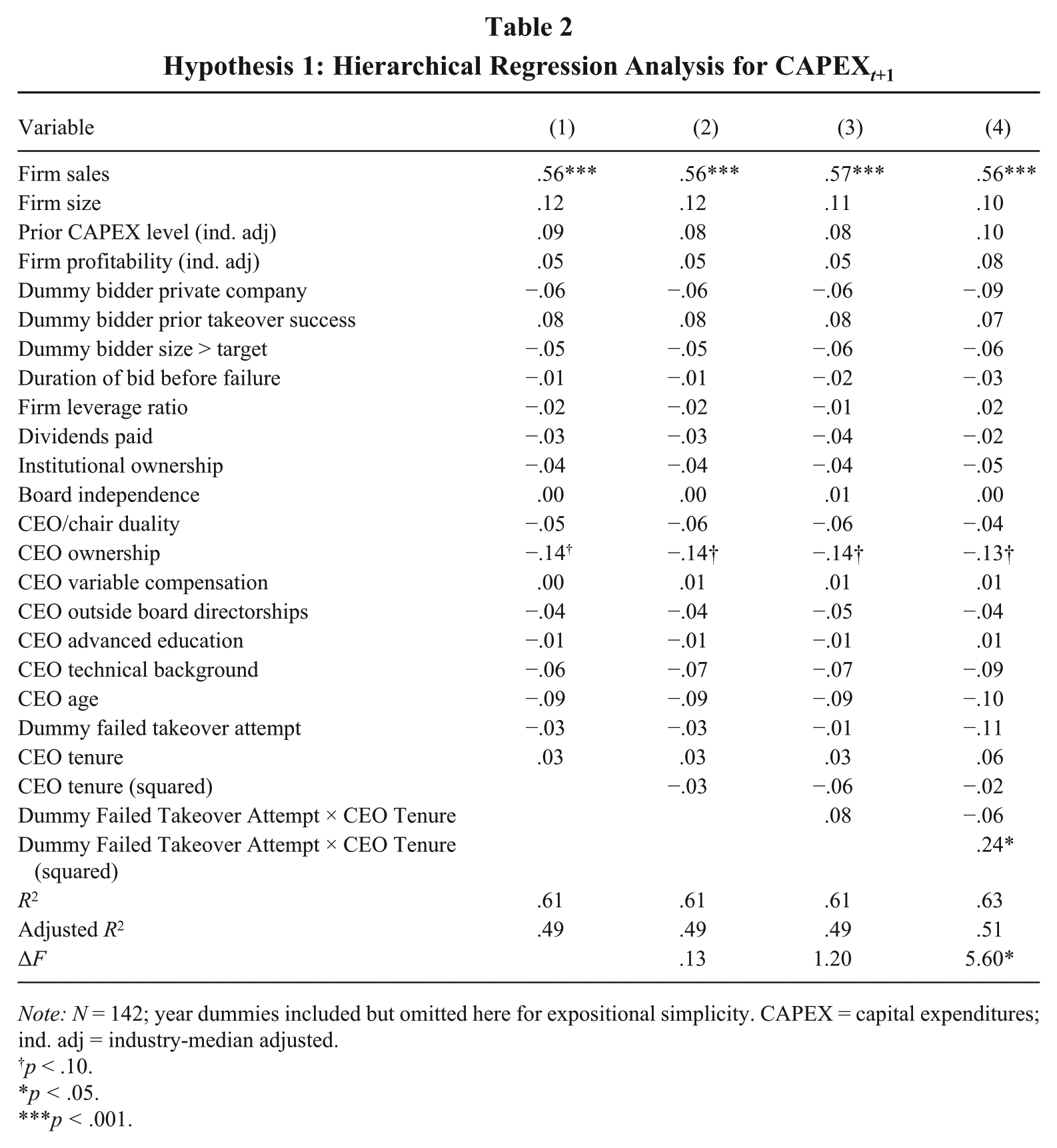

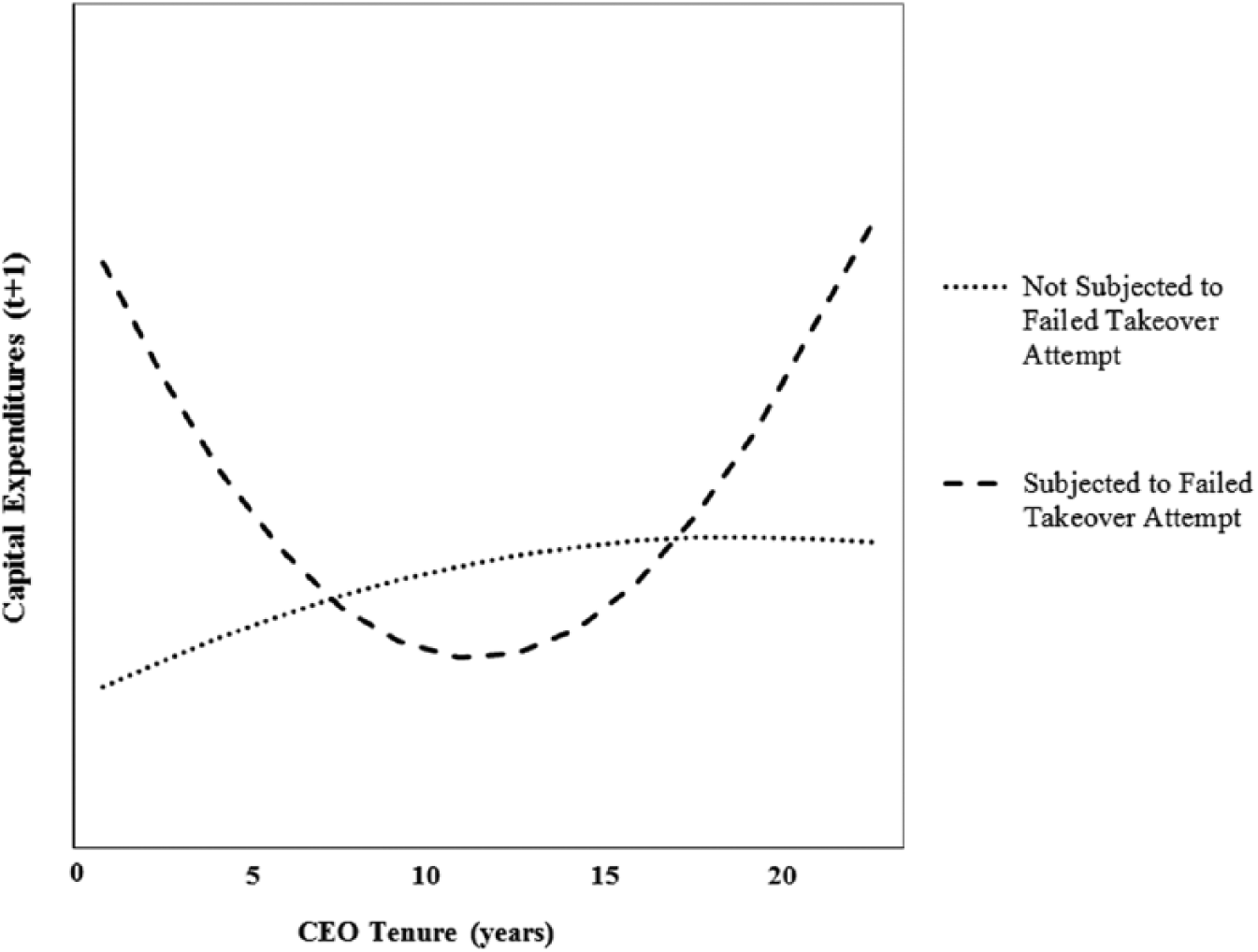

We tested our hypotheses adopting an ordinary least squares hierarchical regression approach where we included substantive variables in four additive stages, following convention, as shown in Table 2 and Table 3. Our interpretations for both hypotheses are based on the final full model in both Table 2 and Table 3. The full CAPEX model in Table 2 shows a good overall fit (R2 = .63), improving significantly from the previous stage (ΔF = 5.60; p < .05). Several control variables have a significant effect. We find that firm sales is positive and highly significant (β = .56; p < .001) and CEO ownership is negative and (marginally) significant (β = –.13, p < .10). For the main parameter of theoretical interest corresponding to the hypotheses, we find that the interaction between failed takeover attempt and CEO tenure squared exerts a significant effect at the p < .05 level in the predicted (positive) direction (β = .24). This suggests support for Hypothesis 1 that, in the wake of a failed takeover attempt, target CEO tenure will have a U-shaped effect on subsequent investments with lower uncertainty of expected returns (i.e., level of CAPEX at t+1), as visually depicted in Figure 2, plotted in line with the suggestions of Dawson (2014). As shown in Figure 2, we observe a downward sloping curve for the subsample of CEOs subjected to a failed takeover with the inflection point around 10.88 years, attesting to the nonlinear nature of the theorized relations in our sample.

Hypothesis 1: Hierarchical Regression Analysis for CAPEXt+1

Note: N = 142; year dummies included but omitted here for expositional simplicity. CAPEX = capital expenditures; ind. adj = industry-median adjusted.

p < .10.

p < .05.

p < .001.

Hypothesis 2: Hierarchical Regression Analysis for R&Dt+1

Note: N = 142; year dummies included but omitted here for expositional simplicity. R&D = research and development expenditures; ind. adj = industry-median adjusted.

p < .10.

p < .05.

p < .01.

p < .001.

Effect of Target CEO Tenure on Capital Expenditures

The full R&D model in Table 3 shows a good overall fit (R2 = .63), improving significantly (ΔF = 7.61, p < .01) from the previous stage. Several control variables show significant effects as well. We find that firm sales and prior level of R&D investments are positive and significant (β = .35, p < .01, and β = .59, p < .001, respectively), whereas CEO ownership, CEO outside board directorships, and the squared term for CEO tenure are negative and marginally significant at the p < .10 level (β = –.13, β = –.15, and β = –.13, respectively). CEO age is negative and significant at the p < .05 level (β = –.18), and the interaction between the dummy for the takeover event and the linear term of CEO tenure is positive and significant (β = .23, p < .05). As for the second hypothesis, the parameter of focal theoretical concern, the interaction between failed takeover attempt and CEO tenure squared exerts a significant effect at the p < .01 level and in the predicted direction (β = –.31). This supports Hypothesis 2 that, in the wake of a failed takeover attempt, target CEO tenure will have an inverted U-shaped effect on subsequent investments with higher uncertainty of expected returns (i.e., level of R&D expenditures at t+1), as visually depicted in Figure 3, plotted in line with the suggestions of Dawson (2014). As shown in Figure 3, we can observe an initially upward-sloping curve for the subsample of CEOs subjected to a failed takeover with the inflection point around 12.63 years, attesting to the nonlinear nature of the theorized relations in our sample.

Effect of Target CEO Tenure on Research and Development Expenditures

Overall, these results are consistent with our theory of retained target CEO responses to failed external governance attempts. Taken together, they provide support for our proposed model that, in the wake of a failed hostile takeover attempt, target CEO tenure will have a nonlinear effect on subsequent strategic investments with different degrees of uncertainty of expected returns.

Discussion

Researchers have argued that the market for corporate control can serve as an important external governance mechanism aimed at addressing target firm (and CEO) underperformance relative to perceived potential (Chatterjee et al., 2003; Fama & Jensen, 1983; Franks & Mayer, 1996). In this study, we have carried this discussion forward by focusing on an understudied governance context: failed takeover attempts with retained target CEOs (visually depicted in Figure 1). This is an important advancement, as agency explanations suggest that the market steps in (through hostile takeover attempts) as a court of last resort aimed at disciplining underperforming managers. However, as dismissal is the prescribed course of action, we still lack understanding on what we can expect in a governance context where (a) the takeover fails and (b) the target CEO is still not dismissed.

To tackle this void in the literature, we have conceptualized hostile takeover attempts as an externally visible negative performance feedback event, from the perspective of the CEO on the receiving end. Advancing a behaviorally informed model, we have argued that target CEO responses are not homogenous in the wake of a failed hostile takeover attempt. Rather, whether and how target CEOs undertake action will reflect the dispositions inherent in the stage of their tenure. Specifically, we developed mirroring hypotheses to predict the direction in which target CEO tenure relates to strategic investments with lower or higher uncertainty of expected returns after a failed takeover attempt. Our study reveals the complex nonlinearities in CEO strategic investment behaviors with different payoff structures, as induced by the interplay between the stages of CEOs along their tenure and failed hostile takeover event.

We discuss some important contributions to and implications for the limited research on external governance (Bergh, 2001; Cannella & Hambrick, 1993; Franks & Mayer, 1996; Walsh & Ellwood, 1991; Wiersema & Zhang, 2011), behavioral research in the upper ranks of organizations (Sanders, 2001; Sanders & Carpenter, 2003; Wiseman & Gomez-Mejia, 1998), and research on the career life cycle of top executives (Hambrick & Fukutomi, 1991; Miller, 1991; Miller & Shamsie, 2001; Simsek, 2007; Wu et al., 2005).

Implications and Contributions

External governance

We first make an important contribution to prior research on external corporate governance mechanisms. Whereas various corporate scandals have highlighted the limitations of overreliance on internal governance, research has also turned to the role of market actors who can act as an external governance mechanism to address firm (and CEO) underperformance (Franks & Mayer, 1996; Walsh & Kosnik, 1993; Wiersema & Zhang, 2011). Although our understanding regarding the outcomes of replacing versus retaining CEOs after successful takeovers has advanced (Bergh, 2001; Cannella & Hambrick, 1993), as has our knowledge of the consequences of replacing CEOs after failed takeovers (Denis & Serrano, 1996; Tannous & Cheng, 2007), little is known about the implications of failed takeovers for target firms when target CEOs retain their positions. In this context, Chatterjee et al. (2003) showed the importance of internal governance in firm behavior; that is, the retained target CEO operating under a nonindependent board is more likely to strategically refocus the corporate portfolio.

With regard to internal governance, in comparison to Chatterjee et al. (2003), we found that board independence did not exert a significant effect in either the R&D or the CAPEX model. One reason for this could be that Chatterjee et al. did not adopt a matched-pair research design to contrast their findings, as we do in this study, and estimated a probabilistic model with a discrete choice outcome. Our model goes beyond a discrete choice of whether to change strategy or not, to capture more subtle adaptive patterns of strategically important resource allocation behaviors. That is, the act of refocusing is likely to be a relatively drastic strategic course of action, and this is unlikely to be led by the current CEO (Zhang & Rajagopalan, 2010), whereas investment patterns of resource allocation are important in understanding the future options and adaptive choices of the firm. Controlling for internal governance factors, we contribute to the literature by uncovering the pattern of resource allocation in two important strategic investments that have been shown to be at the discretion of the CEO, and that have differential levels of uncertainty of expected returns (i.e., CAPEX and R&D), after an external governance mechanism aiming at disciplining the (retained) target CEO fails. In doing so, we highlight heterogeneity in investments from target firms that retained their CEOs in the aftermath of a failed takeover attempt.

Furthermore, this specific governance context is one that has been fairly neglected in the literature. Yet, it is theoretically very relevant, as this empirical domain represents a governance context where traditional agency explanations on the disciplining role of the market reach a dead end (cf. Jensen, 1986; Kini et al., 2004). From an agency perspective, this governance scenario typically implies a context where the market’s attempt to step in and correct managerial failure has failed. Yet, as “correction” of managerial failure through dismissal is the prescribed solution from the market, agency theoretic explanations may not be sufficient to understand a scenario of CEO retention in the aftermath of a failed takeover attempt—and what happens next. Our study is pioneering in this specific dimension of the larger conversation on external governance (see Figure 1). We believe that focusing on this governance context is important for a more comprehensive understanding of different external governance contexts, as some have questioned the efficacy of the market for corporate control (Dalton et al., 2007).

Behavioral governance and managerial agency

Our study also informs behavioral perspectives on managerial risk behaviors in relation to corporate governance (Wiseman & Gomez-Mejia, 1998; see also Hambrick, Werder, & Zajac, 2008). Although prior studies have documented managerial risk sensitivities to internal governance mechanisms, such as stock ownership, stock options, and performance targets (Sanders, 2001; Sanders & Carpenter, 2003), our model contributes evidence for variation in managerial risk behaviors beyond these internal governance arrangements by focusing on external governance mechanisms. This is an important addition to studies in behavioral agency as we introduce an external dimension of governance to which target managers, CEOs in particular, adjust their risk-seeking or risk-avoiding inclinations.

We have conceptualized a takeover attempt as negative performance feedback experienced by a target CEO. Accordingly, this negative performance feedback activates risk sensitivities that become evident in subsequent strategic investments with different payoff structures, as the CEO engages in actions to send renewed signals to stakeholders of her or his competence and ability to exercise strategic leadership. However, we argue that behavioral responses will not be homogenous. Instead, we theorize that the behaviors of boundedly rational CEOs will be subjected to the biases, dispositions, and career concerns inherent in the stage of their tenure (Hambrick & Fukutomi, 1991). As such, the dispositions inherent in the career stage of the target CEO have to be taken into account, as they may become accentuated in this governance context and translated into heightened risk-seeking or risk-avoiding behaviors.

Taken together, we believe that our focal governance context is particularly promising to increase our understanding of managerial risk behaviors and how they are informed when internal governance mechanisms are in question (Jensen, 1986). Expanding behavioral agency models to account for the role of external governance also has managerial implications. From a practitioner’s perspective, the issue of whether a target CEO should be retained or dismissed remains of critical importance. Given the strategic objectives of each given firm, our study provides a framework for understanding how a retained target CEO acts in relation to external governance attempts—and important career-specific contingencies have to be taken into account. As such, we complement Bergh’s (2001) insights into when target CEOs of acquired firms are most valuable by revealing some aspects of what we can expect from retained target CEOs. Uncovering this issue can help investors, boards, and consultants to make more informed decisions about whether maintaining or dismissing the target CEO is congruent with their objectives.

CEO life cycle and tenure

We also believe that our study offers a significant contribution to research on top executives’ influences on firms’ processes and outcomes (Hambrick & Mason, 1984), the effect of CEOs on organizations (Fitza, 2014; Mackey, 2008), and CEO life cycle theories in particular (Hambrick & Fukutomi, 1991; Miller, 1991; Miller & Shamsie, 2001; Simsek, 2007; Wu et al., 2005). Our model and subsequent evidence contribute to an understanding of the many ways in which CEO tenure influences a firm’s strategic behavior, as prior research has shown that the effects of CEO tenure on firm-level outcomes are complex and may be contingent on contextual factors (Simsek, 2007; Wu et al., 2005; Zhang & Rajagopalan, 2010). Indeed, prior research has shown that CEO tenure has a direct effect on a variety of firm outcomes. For instance, CEO tenure has a downward-sloping linear effect on firm adaptation (Miller, 1991), a mirroring positive effect on commitment to the status quo (Hambrick, Geletkanycz, & Fredrickson, 1993; McClelland, Liang, & Barker, 2010; Miller, 1991), and an inverted U-shape on risk-taking propensity (Simsek, 2007). Furthermore, prior research documents more complex interdependencies, in that CEO tenure interacts with a variety of factors to influence firm outcomes. For instance, CEO tenure has an inverted U-shaped effect on company invention, contingent on technological dynamism (Wu et al., 2005); a negative effect on performance in dynamic environments; and an inverted U-shaped effect on performance in stable ones (Henderson et al., 2006). According to Zhang and Rajagopalan (2010), the level of strategic change has an inverted U-shaped effect on performance when the firm’s CEO has tenure shorter than or equal to 3 years.

Attesting to the complexities of the CEO tenure effect, our findings provide support for the notion that target CEO tenure would have a U-shaped effect on subsequent strategic investments with lower uncertainty of expected returns (i.e., CAPEX), and conversely, target CEO tenure would have an inverted U-shaped effect on subsequent strategic investments with higher uncertainty of expected returns (R&D). Specifically, our nonlinear effects resonate with recent studies on CEO career life cycle. For instance, Brookman and Thistle (2009) found that CEOs’ risk of termination increases until about 13 years and subsequently decreases. Our inflection points are consistent with this observation, with risk-seeking peaking between 10 and 13 years (highest R&D, lowest CAPEX). Taken together, the results of our study extend our understanding of the effects of target CEO tenure on strategic investment behavior by theorizing how dispositions, biases, and career concerns inherent in different career stages are accentuated in relation to an external governance attempt and provides us with a better understanding on how the “seasons” of a CEO’s tenure are manifested in different strategic investment behaviors.

Future Research and Limitations

As with all research, our study has some limitations. We have considered two dependent measures to capture variations in the strategic behavior of CEOs through investments with differential uncertainty of expected returns. Future studies could consider other aspects of a firm’s strategy in the aftermath of a failed takeover attempt that may reflect variations in risk behavior, such as financial diversification (Castañer & Kavadis, 2013). In the same vein, we have focused on one important factor characterizing the bounded rationality of target CEOs (i.e., tenure). Future inquiries may expand the investigation to other factors, for instance, the information-search behaviors used to inform subsequent decisions (Heyden, Van Doorn, Reimer, Van Den Bosch, & Volberda, 2013; McDonald & Westphal, 2003). In our study, we also accounted for factors that may be indicative of the credibility of the (failed) takeover. We were unable, however, to fully account for such factors due to data availability limitations. We believe that future research may more directly examine the question of what factors are likely to make a takeover threat more or less credible and potentially refine our understanding of subsequent behaviors and even further research on why some takeovers are successfully resisted whereas others are not.

There may be some differences between the length of tenure of our sample CEOs and recent trends about CEO tenure in the general population of CEOs—that CEO tenure is decreasing and we increasingly observe CEOs to leave office when they are still early tenured (McClelland et al., 2012). Therefore, we recommend that researchers interpreting the seasons of a CEO’s career, as well as our empirical results, consider the specific confines of the context of our study, namely, firms that retain their CEO in the aftermath of a failed takeover attempt, and be cautious with overgeneralizations. Although our results offer a basis for more extended inquiries, attention to issues of external validity might be important before transferring our insights to different contexts. Comparative and, particularly, cross-national approaches might offer elucidating insights, given, for instance, that CEO strategic behavior tends to differ depending on the institutional context (Abdi & Aulakh, 2014; Crossland & Hambrick, 2007; Kwee, Van Den Bosch, & Volberda, 2011).

Furthermore, in our study, we do not expand on subsequent performance outcomes. Although important, we caution that many new contingencies have to be taken into account as the changes in investment patterns may affect other organizational practices as well. Of particular interest would be whether and how the market reacts to different investment responses and whether another takeover attempt is launched. For instance, increases in R&D may make some target firms even more attractive for prospective acquirers (Heeley, King, & Covin, 2006). Finally, research could benefit from further considering the temporal nature of changes, as the full magnitude of changes in this governance context might become visible only over a longer period of time and across a broader range of variables (Ployhart & Vandenberg, 2010). However, this in itself warrants theorizing as there are confounding factors that arise from the changes made during t+1 that would have to be taken into account. These may include changes in personnel (to cope with the new R&D demands) and/or organizational structure and management control systems (as a result of changes in capital expenditures).

Footnotes

Acknowledgements

This article was accepted under the editorship of Deborah E. Rupp. The authors would like to thank associate editor Annette Ranft and the anonymous reviewers for their constructive comments and suggestions throughout the review process. The authors would also like to thank Markus Fitza, YuChen Hung, and Bo Nielsen for invaluable comments on previous drafts of this manuscript as well as Jo Killmister and Lana Prendergast for editing assistance. All remaining errors and omissions are our own.