Abstract

Entry decisions—often critical to firm survival and growth, market evolution, and industry profitability—have been the subject of inquiry for decades. In particular, the timing of entry decisions, drawing primarily on the first-mover advantage (FMA) perspective, has emerged as a prominent area of study. While previous research confirms that entry timing is critical, a large number of contingencies create conceptual and methodological complexities that undermine the formation of a rigorous theory of entry timing. In this article, we review and synthesize management and marketing research on entry timing published in top-tier outlets from 1989 through 2013—the 25-year period that followed the publication of Lieberman and Montgomery’s seminal article on FMA. Distilling key lessons from this literature, our review tries to establish a foundational understanding of the conditions, methods, implications, and strategies of entry timing so that research might be reinvigorated in this domain. Our article concludes by offering a conceptual model of entry based on the lessons gleaned from the articles that we reviewed.

Many business decisions are complex, but entry choices are particularly thorny because they often reflect a shift in strategy, operations, or business model and are laden with uncertainty that stretches well beyond the boundaries of would-be entrants (Markman & Waldron, 2014). Entrants must consider diverse contingencies that differ in risk exposure, resource-capability commitment, and the amount of control over entry processes and outcomes. To name a few, entry choices include the mode of entry (e.g., organic vs. partner driven), the market context (e.g., new vs. established or domestic vs. international), and the timing of entry (e.g., first, second, early, or late). Such choices influence a firm’s path dependence, scale of operations, relations with partners, and industry position, all of which affect performance and survival (Carmeli & Markman, 2011; Peteraf, 1993).

While the form and context under which a firm enters a market are key considerations, the timing of entry—defined here as the order of entry into a new or existing space (e.g., market, industry, or geographic region), relative to competitors, technology development, product life cycle, or other contextual referents—has emerged as a prominent field of study in management (Ketchen, Snow, & Hoover, 2004), marketing (e.g., Boulding & Christen, 2003, 2008), and industrial organization economics (e.g., Klemperer, 1987). Scholars exploring timing of entry have largely drawn on the first-mover advantage (FMA) perspective, although extant research explores the advantages and disadvantages of a broad spectrum of temporal entry strategies ranging from first and early mover (e.g., Kerin, Varadarajan, & Peterson, 1992; Lieberman & Montgomery, 1988, 1998) to late mover (e.g., Cho, Kim, & Rhee, 1998; Shamsie, Phelps, & Kuperman, 2004; Shankar, Carpenter, & Krishnamurthi, 1998).

While research since Lieberman and Montgomery’s (1988) seminal paper has brought consensus that entry timing matters, the combination of numerous contingencies, challenging methodological issues, and varying conceptual lenses undermine the development of a theory of entry timing (Fosfuri, Lanzolla, & Suarez, 2013; Szymanski, Troy, & Bharadwaj, 1995; VanderWerf & Mahon, 1997). Indeed, as the empirical evidence in this review confirms, support for FMAs remains mixed and context specific with only a few regularities (Lieberman & Montgomery, 1998, 2013; Suarez & Lanzolla, 2007). In addition, and despite progress in event methodologies, entry is still a process, not an event (Markman & Waldron, 2014). In the pharmaceutical industry, for example, a product entry (as recorded in scholars’ data sets) is often preceded by years of costly R&D, trials, and perhaps even changes in resource-capability reconfigurations. Indeed, many firms use product, service, and, increasingly, business model innovations to facilitate entry, although research on innovation-entry relations is quite scarce (Markides & Sosa, 2013). Similarly, research on the link between a firm’s resource-capability mix and entry timing is particularly incomplete and appears to delay theory development. Such limitations are also troubling given that many managers and scholars have fallen for the elegance and simplicity of FMA and even perpetuate the myth of its efficacy for explaining successful entry.

Given these issues, it is appropriate to take stock, identify gaps, and, most importantly, synthesize and translate the enduring lessons of entry-timing research for wider consumption. Therefore, we first summarize the disparate and even balkanized entry-timing literature between 1989 and 2013 in order to provide an internally consistent, foundational body of knowledge on entry timing. First, we review 105 management and marketing articles to reveal gaps, differences in theory and methods, and key relationships that heretofore have not been fully discussed. Next, on the basis of our findings and additional research, we discuss how entry research might benefit scholars and managers, and we present a conceptual model of entry. Lastly, we feature new areas of research that can help develop more integrated theories and provide a pathway towards a more comprehensive and unified understanding of entry timing.

Twenty-Five Years of Research on Entry Timing

To assess the key issues and developments of entry-timing research, we analyzed the relevant literatures from 1989 through 2013. Our 25-year time frame includes research published since Lieberman and Montgomery’s (1988) seminal article on FMA, which has been cited in over 2,900 subsequent articles. 1 Because entry timing has been shaped principally by research in management and marketing, we focused our review on articles published in journals from both of these fields. Accordingly, we reviewed 15 top management and marketing journals in an effort to include the most influential and highest quality works available (Short, Payne, & Ketchen, 2008). 2 Our intention was not to be exhaustive of all articles published but to assess the most high-quality, well-scrutinized, rigorous research produced in the last 25 years.

For each journal, we searched for relevant studies with ABI/INFORM, EBSCOhost, and Google Scholar engines using the terms market entry timing, order of market entry, pioneering, first-mover advantage, early-mover advantage, and late-mover advantage. Our search also included derivatives of the keywords, such as pioneer advantage, entry, entry timing, market entry, and order of entry. The search yielded 105 original articles, after removing commentaries, literature reviews, and articles where “entry timing” was not a central focus. 3 Of these 105 articles, 91 were empirical and 14 were conceptual. Overwhelming emphasis on empirical studies highlights how the majority of the research has been aimed at exploring and testing a diverse set of entry-timing relationships rather than in-depth theory development per se.

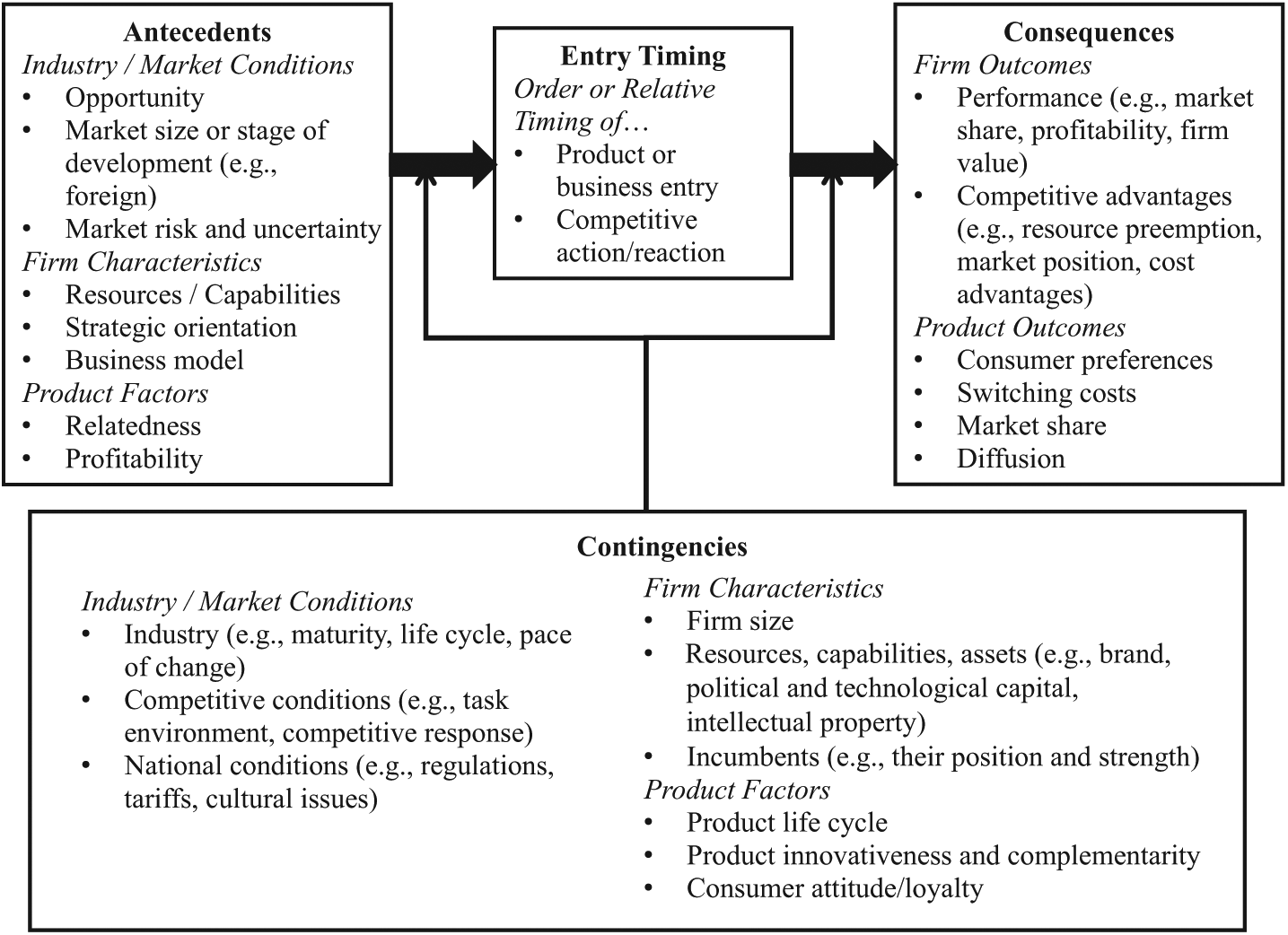

Our initial examination revealed that entry-timing research is ubiquitous across multiple contexts (e.g., products, industries, and geographical regions), focuses on various stages of market development (e.g., new/emerging vs. mature/established), and resides at multiple levels of analysis (e.g., product level, organizational level, country level). To better manage this wide breadth of research, we follow previous qualitative assessments of this type (Combs, Ketchen, Shook, & Short, 2011; Haleblian, Devers, McNamara, Carpenter, & Davison, 2009) and arrange our review around three key themes. As Figure 1 shows, these themes include (1) the outcomes or consequences of entry-timing decisions and actions, (2) the antecedents of entry timing (i.e., factors influencing entry timing), and (3) the contingencies that influence these two main relationships. We start by assessing entry outcomes because as the dependent variable, it signifies the primary focus in FMA logic. Additionally, to bring greater clarity, we distinguish between research directed at product-level entry and at firm-level entry.

Entry-Timing Literature Overview

Entry-Timing Consequences

In line with established first-mover arguments, the majority of the studies in our sample (65%) examined entry-timing decisions as an independent construct or variable. Most of these studies (51 of 70) investigate the predictive effects of different entry-timing strategies on product performance (e.g., customer preference, brand recall, product diffusion) or firm performance (e.g., market share, profitability). For instance, 72% and 67% of firm-level and product-level studies, respectively, find support for the early entry–to–performance relationship. The remaining studies generally offer mixed support, surfacing contingencies such as competitive conditions and product life cycle, which we discuss more fully in following sections.

Firm-Level Research

In an early effort to summarize the main relationship between entry timing and firm performance, Szymanski and colleagues (1995) conducted a meta-analysis of 16 articles published from 1980 through 1994. Their analysis reveals that, on average, early entry is positively associated with industry market share. Subsequent studies tend to support this general finding, although the reasons used to explain the entry timing–to–firm performance relationship may vary from study to study. Suarez and Lanzolla (2007) noted three general explanations: (1) resource-capability mix is the catalyst for entry-timing advantages; (2) isolating mechanism(s), such as technology leadership, preemptions, scarce resources, and switching costs, expand entry-timing advantages; and (3) contextual contingencies (e.g., industry and environmental factors) facilitate or hinder entry-timing advantages.

As to be expected, these explanations draw heavily from FMA logic, either as a stand-alone perspective or in conjunction with game theory (e.g., Narasimhan & Zhang, 2000; Tsurumi & Tsurumi, 1999), institutional theory (e.g., Dobrev & Gotsopoulos, 2010), and population ecology (e.g., Christensen, Suarez, & Utterback 1998). Despite support from other theories, FMA remains an anchor perspective to examine relationships between early entry and firm-level outcomes across contexts. For example, Robinson and Min (2002) investigate the relationship in the North American manufactured industrial goods industry, while H. Lee, Smith, Grimm, and Schomburg (2000) examine the long-distance telecommunications, personal computing, and brewing industries from 1975 to 1990. These are but a few studies that demonstrate the breadth of the FMA perspective, application, and general appeal.

While the majority of studies offer broad support for the early mover–to–performance relationship, conflicting or mixed results also intersperse the research. For instance, one question that researchers tried to address is under what conditions do long-term costs outweigh the long-term demand advantages of pioneering strategies? Testing this on business units, Boulding and Christen (2003) find that pioneering advantages erode after 12 to 14 years, except in cases where there are isolating mechanisms, such as customers’ limited ability to learn, where units retain a strong market share position, and/or the business has patent protection. Subsequent research by Boulding and Christen (2008) reports that early entrants enjoy cost advantages as a result of resource preemption and learning effects. They also demonstrate how firms with limited isolating mechanisms suffer disadvantages from follower imitation strategies, vintage effects, and demand orientation (similar to inertial effects).

In a similar way, Dobrev and Gotsopoulos (2010) suggest the importance of population ecology when considering entry timing. They argue that in an industry’s early years, when organizational form and functional requirements are not fully established, early entrants are more likely to fail than are early entrants into more mature industries. Overall, these scholars substantiate the link between environmental uncertainty and early-mover disadvantages by recognizing how ecological forces drive uncertainty. One key concern, highlighted through this group of studies, is that many of the explanations for why early movers achieve better outcomes (e.g., resource-capability mix, isolating mechanisms, and contextual contingencies) are also used to explain why later entrants often outperform first movers (Lévesque, Minniti, & Shepherd, 2013). This equivocality, along with a slew of contingencies, challenges FMA as a comprehensive framework for studying entry-timing effects.

Mixed findings have motivated several scholars to explore less traditional contexts and outcomes as a means of assessing entry-timing effects. For instance, Carow, Heron, and Saxton (2004) provide empirical evidence of abnormal returns for early movers within industry merger waves. Also, Robinson and Chiang (2002) demonstrate that order of entry has a lasting impact on product development strategies, as measured by product development, R&D intensity, new product sales, and new product sales intensity. According to this study, pioneering firms tend to be more incremental in their product development strategies.

Other scholars consider internationally relevant outcomes. For example, Wooster (2006) finds that early foreign direct investment (FDI) is a strong predictor of cumulative abnormal returns, and in the context of joint ventures, Isobe, Makino, and Montgomery (2000) demonstrate how early foreign entry has a positive effect on the perceived economic performance of a joint venture. Similarly, Luo (1998) observes that early investors in FDI tend to outperform later entrants in market growth in the host country. However, in line with traditional FMA studies, findings by Luo show that early investors in FDI also face greater operational risks than late movers in the start-up phase of international expansion. Furthermore, while early investors in FDI achieve superior asset efficiencies, they are disadvantaged in terms of overall profitability. Altogether, we find that—just as with domestic markets—early entry into foreign markets is often associated with various performance outcomes.

To summarize, at the firm level, entry-timing research offers general support for the early timing–to–performance relationship, but with caveats. A key concern is that mixed findings persist and that sizable deviations in how disparate contingencies influence the relationships make interpretations of such scholarship rather unstable. In the context of market creation, for example, pioneers’ greatest contingencies are chiefly internal (e.g., Do we have the resource-capability mix to form a market and attract customers?), whereas late movers face more external contingencies (e.g., How will incumbents and early entrants react to our forays?). It is also troublesome that the conceptual arguments that support FMA can be used to explain the success of late movers. One reason for this is a strong reliance on isolating mechanisms—and overlooking other factors such as resource-capability mixes—to explain antecedents to timing advantages. In addition, researchers have yet to fully integrate how innovation, tied to firm-level capabilities, affects entry (Fosfuri et al., 2013). Finally, entry failure is rarely glamorous and learning from past failure is valuable for subsequent entry efforts. Yet research on entry failure, entry learning, and reentry is clearly missing, which may be due to insufficient theory and, to reiterate an earlier point, because scholars tend to see entry as an event, not as a process.

Product-Level Research

Research conducted at the product level also generally advocates that pioneers and early movers benefit from being first to market, with arguments commonly based on consumer preferences. Specifically, entrants that attract and capture customers early can influence how different product attributes are valued, along with the ideal configuration of such attributes (Carpenter & Nakamoto, 1989). Additionally, pioneers benefit from “branding” their products as the standard. A classic example is how, in 1924, Kimberly-Clark’s Kleenex brand replaced the generic facial tissue as the standard product label. Such eponymous advantages, however, are independent of product performance; TiVo is an early mover who earned a verb status (e.g., We TiVo’d last night’s show), but the company struggles as most of its revenues come not from selling its pioneering products but from suing rivals for patent infringement. Consumer preferences and branding are obviously important, but explaining entry-timing effects is more complicated than it may at first seem.

In a similar vein, Alpert and Kamins (1995) suggest that consumers have higher long-run preferences for pioneering brands as a result of positive product performance. This schema-based approach argues that consumers correlate pioneers with the idealized values of authenticity, innovativeness, and trustworthiness. In this sense, pioneering firms are rewarded by customers for lowering the uncertainties of an emerging offering. Also, Neidrich and Swain (2003) extend behavioral theories showing that a product’s order of entry in established markets is positively related to brand preferences. Together, their findings support both order-based (Carpenter & Nakamoto, 1989; Kardes & Kalyanaram, 1992) and schema-based (Alpert & Kamins) behavioral explanations of early-mover advantages.

Other research at the product level tends to more closely resemble the firm-level studies by linking early movers to advantages gained from the preemption of resources, capabilities, and market position. For instance, Kalra, Rajiv, and Srinivasan (1998) suggest that pioneers can leverage their early market position to impede the product quality signals of followers by lowering their price to just above the appropriate duopolistic price. Likewise, Dos Santos and Peffers (1995) argue that early movers benefit from the preemption of both tangible and intangible opportunities. Studying the adoption rates of automatic teller machines, they note that early adopters see greater market share and stronger performance as a result of preemption of scarce product placement (i.e., locations) and exclusive access to customers. Early movers also accumulate greater product-market knowledge via learning effects (Brown & Lattin, 1994).

As with firm-level research, scholars promoting the advantages of early product entry are not without criticism. In their historical analysis of 500 products in 50 different product categories, Golder and Tellis (1993) find that the average market share of pioneers was only 10%, with nearly half of the pioneers failing outright. In contrast, they also find that early followers showed remarkably higher average market shares (~28%) and significantly lower failure rates (~8%). Golder and Tellis conclude that early followers are more successful than pioneers because long-term survival and performance depend on the ability to acquire and leverage resources and capabilities for large-scale production of products. This view is supported by others who argue that first movers are often stymied by population-level uncertainty with regard to preferred organizational forms and functions (Dobrev & Gotsopoulos, 2010).

Fueling criticisms regarding FMA, Mascarenhas (1992a) argues that the pioneering–to–market share relationship is overestimated as a result of survival bias and can lead to costly misunderstandings. Specifically, he suggests that entering an existing market with a new product is less effective than entering a new geographical region with an existing product. Furthermore, there are localization effects that may reward native firms over foreign firms, although foreign firms can try to neutralize these effects with prior experience and by entering multiple markets simultaneously. Hence, multinational firms that sell their products in several markets may have advantages over local firms operating in a single market.

In summary, early product entrants enjoy a time advantage to accumulate more direct ties with customers and better knowledge about technology and products, but subsequent entrants have time to acquire information about competitors, suppliers, and market trends. The implication from a competitive dynamics perspective is that a later entrant can choose who to compete with or where to differentiate vis-à-vis an early entrant, whereas first entrants are often bound by incumbency and subject to the competitive choices of later entrants. Pioneers are not powerless, however; they can use their head start to forge ahead by continually redefining the market and reshaping customer purchasing criteria. Our concern, though, is with entry research that omits early value chain factors—particularly resource-capability mix and business model configurations—as drivers or antecedents of both product development and entry-timing options.

Antecedents to Entry Timing

Largely on the basis of the presumption that FMAs exist, many scholars have made efforts to better understand the antecedents to entry-timing decisions. Such efforts have been made more recently, with more than half (25 of 43) of these articles being published in the 21st century. And although a large number of antecedents have been researched, three principal categories arise: strategic intent/decision making, firm resources/capabilities, and market/industry conditions. Most studies that aim to explain entry-timing decisions invoke either resource-based arguments (e.g., resource-based view, competitive dynamics, organizational learning) or decision-making frameworks (e.g., game theory, managerial cognition, real options). The most noticeable differences, however, are between firm-level and product-level entry-timing antecedents, with firm-level research focusing more on firm resources and capabilities and product-level research emphasizing strategic intent and decision-making factors.

Firm-Level Research

As previously noted, research at the firm level focuses on resources and capabilities as key antecedents to entry-timing decisions (e.g., Boulding & Christen, 2003; Murthi, Srinivasan, & Kalyanaram, 1996). In an early example, Robinson, Fornell, and Sullivan (1992) argue that different capabilities support different entry-timing strategies; specifically, R&D capabilities predict early entry, while manufacturing capabilities predict early followers and marketing capabilities predict late entry. Subsequent research supports these basic arguments regarding capabilities but, not surprisingly, finds that entry timing does not play a uniform role across industries (Schoenecker & Cooper, 1998).

More recently, G. K. Lee (2008) added a new time component by dichotomizing capabilities into initial (i.e., catalyzing) and current (i.e., additive) capabilities and showing that initial capabilities affect entry timing through the development of later capabilities. Similarly, Hawk, Pacheco-De-Almeida, and Yeung (2013) demonstrate that a firm with greater intrinsic speed capabilities can wait longer to enter an emerging industry without significant negative consequences. Furthermore, Tan and Vertinsky (1996) demonstrate how prior experience influences the timing of FDI. Such findings link entry to latent firm capabilities, suggesting that entry timing is likely a second-order function of a firm’s dynamic capabilities (Teece, Pisano, & Shuen, 1997). Put more formally, we view entry order, entry timing, and entry-based advantages (i.e., FMAs, late-mover advantages) as symptomatic of antecedent factors (e.g., capabilities) that are appreciably more predictive of effective entry.

Beyond the resource advantage perspective, a number of studies demonstrate the importance of environmental conditions and strategic intents—considered either separately or together—in determining entry timing. For example, Folta and O’Brien (2004) suggest that industry characteristics, such as growth opportunities and uncertainty, act as antecedents to entry timing. Using real options theory, they argue that firms have the option to either defer or grow. In the face of uncertainty, the option to defer discourages entry, although high growth potential outweighs deferring entry, even at high levels of uncertainty.

Consistent with the strategic-groups research (e.g., Fiegenbaum & Thomas, 1995; Peteraf & Shanley, 1997), entry-timing decisions are also influenced by rivals’ actions (Debruyne & Reibstein, 2005). As Rose and Ito (2008) demonstrate, a contagion or bandwagon effect is frequently formed with firms racing to mimic rivals’ actions, including entry. However, research also shows that, for some firms, it is better to delay entry until after first entrants develop and grow their market (Lévesque et al., 2013). Furthermore, considerations should be given not only to the possible benefits gained by being early (or late) but also to the costs associated with rivals securing earlier (or later) positions (Narasimhan & Zhang, 2000). Also, some scholars link entry-timing decisions with the awareness-motivation-capability framework (M.-J. Chen & Miller, 2012), but as noted earlier, others tie entry-timing choices to mimetic forces, peer pressure, and herd mentality (Lieberman & Asaba, 2006).

Just as experience and market attractiveness are important antecedents to entry into domestic markets, they are also important in entry into foreign markets. In their study of U.S. Fortune 500 firms’ entry into China (from 1979 to 1996), Gaba, Pan, and Ungson (2002) find that larger, more internationally experienced firms are often early entrants. Similarly, Tan and Vertinsky (1996) observe that firms are more likely to engage in FDI earlier when they have experience in a particular market or in foreign operations. Our message is that antecedents—such as market size and stage of development (e.g., Mascarenhas, 1992b), opportunities and risks (e.g., Gaba et al.; Tan & Vertinsky), and competitive behaviors (e.g., Gaba et al.)—shape entry-timing decisions.

Many studies on the timing of entry into international markets rely on first-mover arguments (e.g., Dunning, 1977; Hymer, 1976), along with geographical dispersion perspectives (e.g., Bass, 1969). For instance, Paul and Wooster (2008) show that advertising intensity, strong recent sales, and overall firm size predict international entry motives and, subsequently, entry timing. They also observe that firms in concentrated industries—wherein opportunities for growth are limited—are more likely to enter new geographical regions earlier, particularly by using higher-equity modes of entry. Gaba and colleagues (2002) consider international experience, firm size, scope of market offerings, and nonequity modes of entry, while at the country level, they show that greater political and business risk delay market entry. These authors also note that firms are more likely to enter an international market earlier when more competitors enter early, which is consistent with theories of imitation (Lieberman & Asaba, 2006) and bandwagon effects (Knickerbocker, 1973).

Product-Level Research

Much akin to the firm-level research, antecedents of entry timing at the product level include resources and capabilities, intentions, modes of entry, market prospects, and contexts (e.g., country-level factors). In many cases, scholars rely on game theory to understand entry timing, where entry decisions are based upon rivals’ behavior and the strength of competing products. For instance, Krider and Weinberg (1998) use a sample of movies in North America to study the benefits of releasing a movie earlier given the potential of a competing movie. Similarly, Ethiraj and Zhu (2008) argue that the entry timing of imitators is a function of information asymmetry, where the unavailability of information regarding a pioneer’s product increases the follower’s benefit on delaying entry. Such studies rightfully recognize that entry-timing decisions occur in dynamic competitive contexts, but many continue to rely on duopolistic competition modeling, which, while empirically simpler, is an unreasonable assumption in most competitive contexts. Indeed, lucrative, munificent markets tend to attract a high number of diverse, and often less predictable, entrants even in the face of barriers to entry (Markman & Waldron, 2014).

As a unique aspect of product-level research on antecedents, several studies consider factors that influence the timing of introducing product extensions. Building on the idea of cannibalization and instances where firms forgo being first to market (Connor, 1988), Wilson and Norton (1989) ask when it is best to introduce a new line extension. They suggest that a line extension tends to lower per unit profit margins while cannibalizing on existing product(s), but it may also help to expand the market and subsequently increase sales growth. Hence, it is often better to introduce a line extension early in a product’s life cycle or not at all. Considering the trade-offs between positive (i.e., leverage) and negative (i.e., backlash) social influence effects, we see that even in the face of a negative backlash, it is often advisable to enter a new market anyway (Joshi, Reibstein, & Zhang, 2009). However, this logic is tempered too because, as we now know, entry outcomes are contingent on a diverse set of factors, including the extent of market penetration.

In summary, research on entry timing is fairly consistent across product-level and firm-level studies, with studies showing that both internal (i.e., resources and capabilities, strategic intent) and external (i.e., market, industry, country) antecedents are key to explaining entry timing. Although many studies imply that being a first entrant is a desirable objective, this assumption is quite suspect. Rather, we found that advantages resulting from entry order (i.e., early and late entry) appear to be indicative of a deeper level of strategic fit. That is, timing advantage represents a firm matching its resource-capability mix with product and market contexts, which are subject to significant variation across time and space. As such, even entry timing can be framed as a contingency, so researchers need to cast a holistic net and consider the broader and more diverse set of contingencies, which is the topic we address next.

Contingencies

Contingencies moderate the relationships between antecedents and outcomes, and they are important because in addition to the trio of antecedents, entry timing, and consequences, nearly half of the studies in our review (50 of 105) find support for contingency effects. Interestingly, we view many contingency studies as the field’s reaction to inconsistent or counterintuitive findings regarding FMAs. Overall, contingency studies tend to support the view that because FMA is dynamic, it is best specified through interactions as opposed to direct effects (Lieberman & Montgomery, 1998, 2013).

Contingencies: The Relationship Between Entry Timing and Outcomes

Contingencies of the entry timing–to–outcomes relationship, either product-based or firm-based studies, included a wide variety of moderators, including those based on product attributes (e.g., product line breadth, customer synergies, product imitation by competitors), firm attributes (e.g., firm resources and capabilities, lead time over competitors, advertising and marketing expenditures, strategic orientation, luck), and industry attributes (e.g., market uncertainty, pace of industry change, industry competition). As such, there is a high degree of complexity associated with many of these studies because of the theoretical and empirical issues in dealing with multiple levels of analysis. Furthermore, only a few contingencies have been repeatedly examined across different contexts, which may draw into question the robustness of certain findings. So, while the empirical testing of a variety of moderators has helped identify important boundary conditions, the lack of replication across contexts of time and space may support the notion that entry timing is a context-specific construct, thus reinforcing the need for a general theory of entry.

Of the various entry-timing studies, many tested contingencies are based on product or brand attributes or strategies. For example, in their extensive study of 75 product line extensions of 34 brands of cigarettes over 20 years, Reddy, Holak, and Bhat (1994) find that the strength of the parent brand, combined with early entry, firm size, and marketing competencies, is positively associated with the success of a line extension. In addition to brand strength, other product contingencies include product line breadth (Szymanski et al., 1995), product life cycle (Lilien & Yoon, 1990), and the extent to which the value of a product increases with adoption (Srinivasan, Lilien, & Rangaswamy, 2004). Strategies related to product lines also affect entry-timing outcomes. For instance, according to Boulding and Christen (2009), businesses with a broad product line benefit from pioneering only when invoking a versioning strategy wherein incremental product variety is created from a standard product offering to meet anticipated demand. Alternatively, firms following a tailoring strategy, where products are customized to meet customer demand, could face a cost disadvantage that might offset pioneering advantages.

Firm attributes (e.g., size, structure) were relatively common contingencies, with many studies conceptually relying on a resources-and-capabilities perspective. However, as mentioned earlier, these studies often use the same resource-based logic to make predictions regarding both early- and late-entry advantages, although some types of attributes tend to fit better with certain timing strategies than others. Resources that increase pioneering or early-mover advantages include patent protection (Boulding & Christen, 2003), network size (Varadarajan, Yadev, & Shankar, 2008), and knowledge competencies (Li & Calantone, 1998). Most notably, R&D and marketing capabilities are among the strongest moderators of the entry timing–to–performance relationship (e.g., Franco, Sarkar, Agarwal, & Echambadi, 2009). For late movers, resources and capabilities that strengthen the timing-to-outcomes relationship include relevance and size of a resource base (Shamsie et al., 2004), as well as innovation capabilities (Shankar et al., 1998).

As to be expected, resources and capabilities also facilitate international market entry. In their study of Korean FDI, Chang and Rhee (2011) find that the speed of FDI expansion is more strongly related to firm return on invested capital for firms with considerable marketing knowledge, strong brand equity, and slack resources. As another example, Frynas, Mellahi, and Pigman (2006) argue that early movers in emerging markets can reap advantages so long as they can leverage strong political resources. Such studies emphasize the importance of early entry, particularly with regard to a firm’s ability to develop a robust set of capabilities, including securing favorable positions in factor (Markman, Gianiodis, & Buchholtz, 2009) and political (Capron & Chatain, 2008) markets.

Industry or market conditions are also important contingencies. For instance, in a comprehensive study of four different products’ entry into 16 different countries, Ganesh, Kumar, and Subramaniam (1997) report that products diffuse faster in countries that are culturally and economically similar to the first country being entered. Furthermore, diffusion of product adoption is accelerated when there is a longer time between product introduction in the initial country and product introduction in countries entered subsequently. More recent research, which is consistent with the view that FMAs rarely hold in fast-paced industries (Christensen et al., 1998; McGrath, 2013), argues that FMAs depend upon the pace of market and technological evolution (Suarez & Lanzolla, 2007). Additionally, the nature of competition related to speed of competitive actions and responses (Ferrier, Smith, & Grimm, 1999), commitment level of each competitor (M.-J. Chen & Miller, 2012), and robustness of competitive repertoire, just to name a few, are important factors. Krider and Weinberg (1998), for example, note that firms facing stronger competitor offerings are better off delaying entry. Overall, these studies resonate with Kerin and colleagues (1992), who noted, over two decades ago, that entry effects should be examined in the context of market strategy and marketplace variables.

In summary, many of the studies in our sample corroborate the view that entry timing and performance are not easily explained by simple, direct relationships. Moreover, we see that studies consider an increasing number of contingencies and a wider selection of contextual factors that either support (e.g., marketing capabilities) or refute (e.g., network externalities) early-entry predictions. An important finding, therefore, is that scholarship in this area might progress faster and bring greater clarity by deviating from the FMA view. As noted earlier, instead of focusing on entry timing as a core predictor of performance, a more nuanced understanding of entry requires researchers to consider entry timing as a contingency factor.

Contingencies: The Relationship Between Antecedents and Entry Timing

A few studies examined contingencies between market entry timing and its antecedents. Most such studies explore factors that moderate the relationship between strategic intent or industry opportunities and the option to enter first or delay entry. For instance, Bayus, Jain, and Rao (1997) argue that the relationship between firms’ competitive insights (i.e., leader foresight) and entry-timing decisions under duopolistic conditions is moderated by market estimates and development efficiencies. Firms that estimate markets better and have stronger capabilities to develop efficiencies are better served by entering a product market first. Folta and O’Brien (2004) hold that the relationship between industry uncertainty and entry timing is contingent upon the irreversibility of the investment required for market entry, which increases the option value of deferring entry until there is greater clarity on growth opportunities and potential early-entry advantages. Alternatively, Hawk and colleagues (2013) report that firms with speed capabilities can wait longer before entering a market, allowing time for uncertainty to decrease while avoiding preemption risks. This relationship becomes more salient as investment commitment increases and the option value of waiting increases accordingly.

In summary, the extant literature demonstrates that various firm- and industry-level contingencies incent or deter firms from entering a market early. However, product offering characteristics and the potential for above-market gains influence these contingencies as well, confirming the complex and multifaceted nature of entry-timing decisions. Overall, we see considerable research opportunities to uncover commonality among contingencies and consider them more holistically as they relate to the relationship between antecedents and entry timing.

Methodological Trends

One of the positive findings of our review was the overall level of sophistication and rigor utilized in the methods and statistics. On the whole, the data, methods, and statistical techniques show a high level of competence and creativity, especially in the last decade; this seems fitting given the rather complex nature of the entry phenomena and advancements in statistical techniques. We noticed that studies utilize longitudinal data (48%) and analyze them with survival/event study methods (29%) or regression models (60%), commonly making the necessary statistical compensations for modeling nonnormal and/or nonlinear data (e.g., logistic, probit, Poisson). However, we also noticed some general limitations, including a strong reliance on (exclusively) archival data (57%), a persistent dependence on nominal measures for entry timing (48%), and a dominance of North American samples (54%).

Firm-Level Entry-Timing Empirical Research

In our sample, 60 of the 73 firm-level entry-timing articles were empirical. Of the 60 empirical studies, 45 were published in management journals and largely consider the role of entry timing as an independent variable (28 of 45 studies). Marketing demonstrates a similar pattern, with 10 of the 15 empirical articles using entry timing as an independent variable. For management and marketing, entry timing is modeled as a moderator relatively rarely—in only 5 of the 60 studies.

Nearly half of the studies operationalize entry timing as a continuous variable (47%), typically measuring the time (in varying units) between market or industry formation and entry (e.g., G. K. Lee, 2007, 2008; Mitchell, 1991) or time from first entry (e.g., Green, Barclay, & Ryans, 1995; Schoenecker & Cooper, 1998). Even still, a comparatively large number of studies measure entry timing as a nominal variable (43%). Typically, the nominal measure indicates whether a firm is first to market or not (e.g., Mascarenhas, 1992a; Murthi et al., 1996) or whether a firm entered a market as an event in longitudinal designs (e.g., Hawk et al., 2013). Many of these studies rely on PIMS (Profit Impact of Market Strategy) data and their nominal measure of market pioneering, which has been called into question because it is based on single-source self-report surveys and omits nonsurvivors (e.g., Boulding & Christen, 2003, 2008; Moore, Boulding, & Goodstein, 1991; Robinson & Chiang, 2002). Also, the PIMS definition of pioneering is inconsistent with more contemporary research (e.g., Golder & Tellis, 1993; Lieberman & Montgomery, 1998). Interestingly, given the emphasis on order of entry, only a few studies utilize ordinal measures of timing (5%). Overall, the preference for continuous measures of entry timing, which have the highest measurement precision among other data forms (Hair, Black, Babin, & Anderson, 2010), is an encouraging revelation among firm-level entry-timing research.

Over half of the empirical firm-level entry-timing studies rely on regression-based methods of data analysis (53%). While many studies use more traditional regressions with ordinary least squares assumptions (often rightly so), a comparatively equal number of studies invoke more nuanced regression techniques to compensate for violations of such assumptions (i.e., nonnormal and/or correlated residuals, etc.). Alternative approaches include logistic/probit regression (e.g., Paul & Wooster, 2008), multinomial logistic regression (e.g., Robinson et al., 1992), and two- and three-stage least squares regression (e.g., Han, Kim, & Kim, 2001). More flexible, generalized forms of family distributions, such as Poisson (e.g., Gielens & Dekimpe, 2007) and negative binomial distributions (e.g., Lavie, Lechner, & Singh, 2007), are also utilized. Second to regression, many studies approach entry timing using event or survival techniques (28%), including historical analysis (e.g., Dobrev & Gotsopoulos, 2010) and Cox hazard models (e.g., Debruyne & Reibstein, 2005). A minority of studies rely on structural equations modeling (e.g., Calantone & Schatzel, 2000), econometric/time series modeling (e.g., Boulding & Christen, 2008), or Bayesian methods (e.g., Tsurumi & Tsurumi, 1999). The diversity and sophistication of analytical techniques is encouraging as it demonstrates both competence and rigor.

Product-Level Entry-Timing Empirical Research

Of the 37 articles on product-level entry, 31 are empirical. The majority of these studies come from marketing journals (65%), consider entry timing as a predictor variable (77%), and measure entry timing nominally (55%)—either as a binomial variable (i.e., first mover vs. all others) or in multiple categories. Indeed, 6 product-level studies rely on multicategorical measures of entry timing in which the timing of entry corresponds to several categories. For example, Atuahene-Gima and Ko asked respondents to “indicate whether the firm was first to market, an early follower, a late follower, or a late entrant with the new product” (2001: 63). Although less frequent than nominal measures of entry timing, scholars also use continuous measures, often directly as time (e.g., days, months, years). For example, Brown and Lattin (1994) studied the effects of time in market on the development of pioneering advantages by measuring the number of months a pioneer’s product was in a market before follower entry. Similar to firm-level studies, ordinal measures were less common.

Encouragingly, most product-level empirical research invokes longitudinal or repeated-measures designs, with seven studies that investigated predictive effects of entry-timing strategies using repeated-measures data. Understandably, studies examining entry timing as a dependent variable more commonly rely on cross-sectional or simple longitudinal data (i.e., over time). Only two product-level studies test the moderating effects of entry timing; one uses a longitudinal design (Shankar, Carpenter, & Krishnamurthi, 1999) and the other uses simulation (Ali, Kalwani, & Kovenock, 1993).

The majority of product-level entry-timing studies collect data from archival sources, commonly within the pharmaceutical and medical devices industries (e.g., Ethiraj & Zhu, 2008), the computer components and software industries (e.g., Franco et al., 2009), or the consumer manufactured goods industry (e.g., Kim & Min, 2012). Consistent with the calls of Kalyanaram, Robinson, and Urban (1995) and Lieberman and Montgomery (1998), many of the product-level studies examine entry timing in other contexts, such as the mutual fund industry (Makadok, 1998) and the movie industry (Krider & Weinberg, 1998). Furthermore, with a few exceptions (e.g., Atuahene-Gima & Ko, 2001; Lilien & Yoon, 1990), product-level entry-timing research largely ignores geographical regions beyond North America, despite the strong likelihood of country and/or cultural effects.

A number of other product-level studies rely on observational or survey data. Most of the studies use observational techniques: either laboratory experiments in which the effects of entry order are tested on consumer memory/judgment (e.g., Kardes & Kalyanaram, 1992) and product preference (e.g., Carpenter & Nakamoto, 1989) or case studies of product-market pioneers (e.g., Bayus, Jain, & Rao, 1997, 2001). Similarly, studies using surveys are mostly aimed at establishing the effects of order entry on brand preferences and other qualitative judgments about a product and its features.

We observed a greater variety of analytical methodologies in research on product-level entry timing than firm level. Such analytical diversity is owing to methodological differences in consumer-based versus producer-based research. For instance, studies that focus on entry-timing advantages bestowed on firms by consumer attitudes, cognitions, or behaviors rely more on experimental or survey methods, thus commonly invoking analysis of variance (e.g., Alpert & Kamins, 1995) or structural equation modeling techniques (e.g., Kuester, Homburg, & Robertson, 1999). Conversely, studies investigating the effects of product or brand attributes on the efficacy of entry-timing strategies more often rely on archival data and various regression techniques (e.g., Y. Chen & Xie, 2007), conjoint analyses (e.g., Carpenter & Nakamoto, 1989), survival analyses (e.g., Srinivasan et al., 2004), or mathematical modeling (e.g., Bayus et al., 1997, 2001).

Key Methodological and Empirical Challenges

While generally positive in terms of rigor, some methodological and empirical challenges (related to entry timing) remain. In particular, greater attention is needed to (1) parameterize and measure entry times and windows; (2) identify all relevant “players” (i.e., entrants, rivals, consumers, stakeholders) who operate in or are affected by an industry or market, including an unambiguous identification of failed firms; (3) decrease causal ambiguity through greater use of repeated-measures study designs and/or qualitative data; (4) determine the appropriate measures of advantage (i.e., market share vs. profitability vs. survival); (5) understand the multilevel and cross-level entry-timing effects better; and, as mentioned previously, (6) account for antecedents and contingencies.

Our view is that despite the progress made thus far, the literature is hamstrung by an interplay between theory and method (cf. Van Maanen, Sorensen, & Mitchell, 2007), which has evolved over time but has yet to overcome the challenges we note above. And while the use of diverse methodologies and creative construct parameterization show progress, the literature continues to report inconsistent and, too often, countervailing findings. Some notable challenges associated with the entry-timing research are summarized in Table 1, along with some basic suggestions for overcoming them.

Summary of Key Empirical Challenges and Research Opportunities

Discussion

This review article synthesizes, consolidates, reconciles, and reintegrates the collective wisdom on entry timing from 105 articles that were published in top-tier management and marketing journals from 1989 through 2013. At a broad conceptual level, we can see the importance of, arguably, the most valuable and scarcest resource of all: time. For first or early movers, extra time over later entrants allows for the capture of customers and the building of capabilities that can advance and perpetuate early gains. However, time can also benefit later entrants by helping to improve risk estimations, clear uncertainties, remove capability gaps, and facilitate learning, particularly from the costly activities (and mistakes) of earlier entrants. Thus, a recurring concern that we substantiated with this review is that the logic that explains why first movers achieve better outcomes is often also being invoked to explicate why later entrants displace first movers (Lévesque et al., 2013).

The studies we reviewed collectively challenge the conceptual purity or simplicity of FMA thinking. Specifically, we note that because most entry choices are linked to a sundry of contingencies that interact with firm-specific heterogeneity (e.g., rivals, consumers, opportunities, market risks, and technological uncertainties), FMA and follower advantage can coexist (Lieberman & Montgomery, 2013). Furthermore, the complexity associated with entry timing is exacerbated by its dynamic and multidimensional nature. For instance, a firm might be a late mover with a product introduction but a pioneer with a business model. Indeed, many of the recent articles in our sample do not prescribe to a purist FMA perspective, nor do they seek to test it without explicit attention to antecedents and contingencies (e.g., Dobrev & Gotsopoulos, 2010).

Overall, our review suggests that while FMA serves as a cognitive shortcut to explain entry-timing decisions, FMA may also be a red herring, misleading or diverting attention away from more important and more nuanced entry considerations. So, although the FMA logic sees timing (i.e., being first) as a core predictor of performance (i.e., advantage), our synthesis suggests that scholars and practitioners should consider entry timing as just one of many contingency factors. Indeed, we agree with Lieberman and Montgomery, who recently acknowledged that they “have a strong preference for the term, ‘entry timing effects’ rather than ‘first-mover advantage and disadvantage’” (2013: 317).

With these key considerations in mind, we now discuss the most persistent conceptual and practical takeaways from this body of knowledge. Then, drawing on our findings, we provide directions for future research, which include the presentation of a comprehensive conceptual framework that integrates the various contingencies associated with entry.

Enduring Lessons

A theory is often judged by the diversity of contexts in which it maintains its predictive and explanatory power. Discovering that the main prescripts of the FMA thinking endure, despite 25 years of research showing that the direct-effect logic of FMA is invalid without attention to scores of contingencies (and antecedents), was surprising. The revelatory power of contingencies is perhaps best illustrated by contexts in which FMA and follower advantage coexist or where both incumbents and entrants enjoy superior performance (Markman & Waldron, 2014). To use another example, entry-timing choices shape and are shaped by mimetic behavior and bandwagon effects, where firms are more likely to enter a market after seeing rivals do so (e.g., McNamara, Haleblian, & Dykes, 2008; Rose & Ito, 2008). Our point is that diverse contingencies, ranging from firm characteristics (e.g., Robinson et al., 1992), to market dynamics (e.g., Debruyne & Reibstein, 2005; Narasimhan & Zhang, 2000), and even idiosyncratic industry contexts (e.g., Folta & O’Brien, 2004), can individually and collectively influence entry-timing decisions and effects (Lieberman & Montgomery, 2013).

Just as with contingencies, we also advocate complementing FMA thinking with an explicit attention to antecedents. For example, we observed that entrants’ capabilities and experience, as well as competitors’ characteristics, are prominent antecedents to entry timing. Of particular interest is the possible substitutability between an early-entry strategy and a firm’s capability. For example, some firms mobilize resources to displace early movers in product markets (Markman et al., 2009), whereas others choose to forfeit a first-mover position but use speed capabilities to catch up with, and even leapfrog, first entrants (Hawk et al., 2013).

Another consistent finding is that entry timing—much like rivalry, competitive advantage, and performance—is imbedded in relativity. Entry is neither relative to clock time nor independent but, instead, relative to a broader context, including entrants’ resources and capabilities, incumbents’ strength, market attributes, and industry dynamics. As such, we generally see the timing of entry as a sequential act relative to some contextual anchors, and the length of time separating actions, outcomes, and reactions is important. In fact, identifying the contextual anchors without myopically assuming they should be limited to the first entrant is the next important evolutionary step for empirical and conceptual research in this literature.

Entry is also not a rare or an anomalous event but, rather, a common, frequent, and ongoing process where attempts occur far more frequently than successful penetrations (Markman & Waldron, 2014). Many firms have a mandate to pursue growth opportunities, but given that entry is risky and failure is a likely outcome, the rate of entry is perhaps higher than what would be considered a rational behavior (Lieberman & Asaba, 2006). Consistent with entrepreneurship research, de novo entry attempts are more frequent than entry by diversified (de alio) players, but the latter is often more successful (Morris, 2009). And as articulated before, entry-order effects and superior performance outcomes are impermanent; they diminish over time by competitor actions (Lieberman & Montgomery, 2013).

We also noticed that most entrant-incumbent research does not delve too much into the implications of firm size disparity, but a recent effort reveals that severe size asymmetry can explain meaningful deviations from the traditional predictions made by mutual forbearance and resource partitioning theories (Markman & Waldron, 2014). Unlike their smaller counterparts, large, multibusiness enterprises exploit slack resources and complementary capabilities to scale up their operation and bypass early entrants (Markides & Geroski, 2005). For example, in the 1990s, Microsoft overtook Netscape’s Web browser, despite Netscape’s FMA. More recently, Google Earth undermined Garmin’s first-mover position in global positioning system applications. The impermanence of FMA is not a new consideration; rather, we interpret this literature as indicating that having a size advantage, either a large or small size advantage, is more fitting for a late or early entry, respectively. This logic is yet to be articulated theoretically or confirmed empirically in the literature.

Collectively, the articles we reviewed generally acknowledge the view that entry is a dynamic process. Recognizing this temporality, Lieberman and Montgomery (1998) suggested that first movers might extend their advantage by applying logic consistent with industrial organization economics theory: control scarce resources, retain technology leadership, increase customers’ switching costs, and develop network effects. Unfortunately, these basic tenets are not unique to first or early movers; our review unequivocally shows that these strategies work equally well to benefit late movers.

Future Research

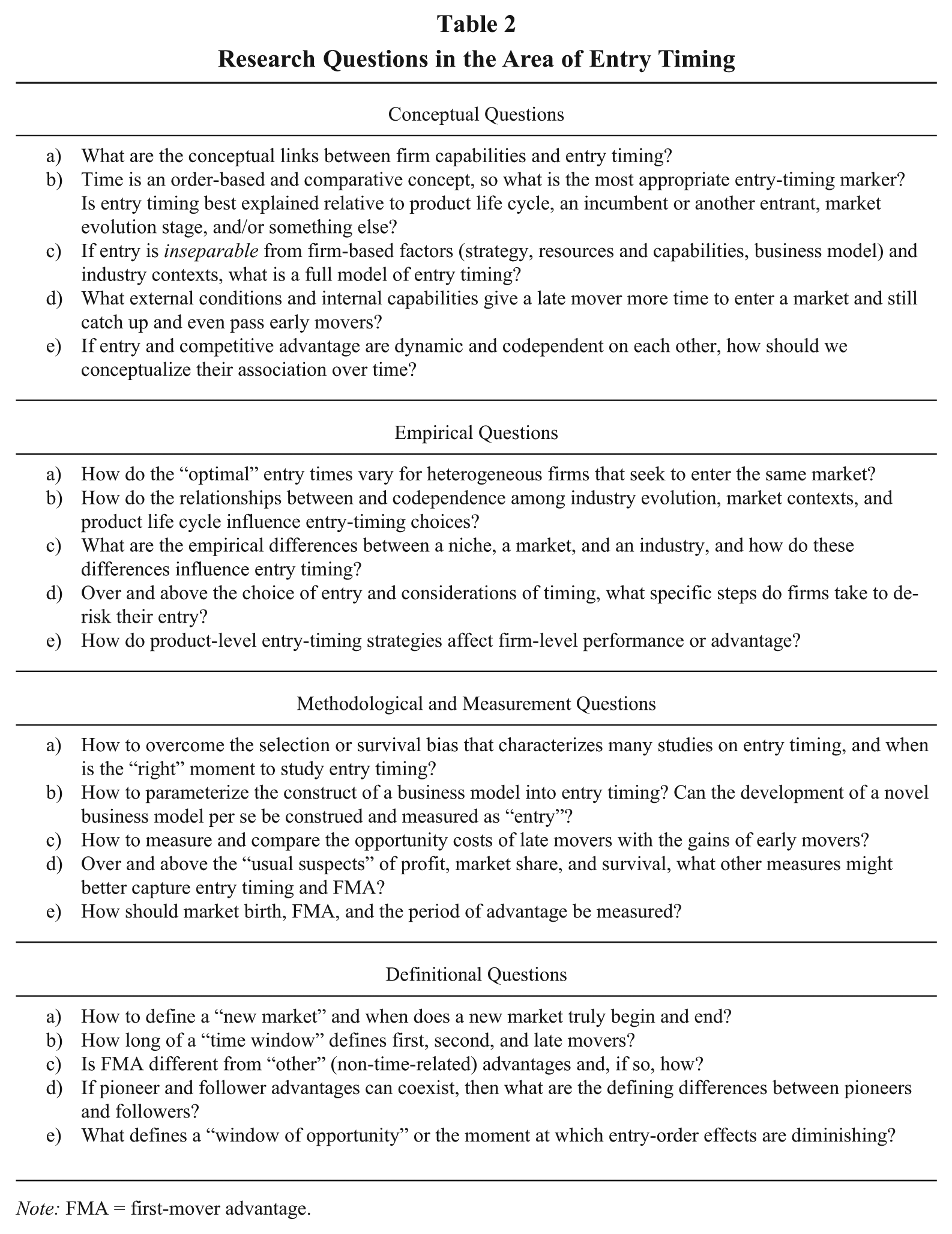

Given the literature’s maturity and how its conceptual development and empirical findings complement parallel literatures, our review reveals several gaps and irregularities that need to be addressed. All in all, this line of inquiry is hungry for new ideas, theories, methods, and techniques for exploring entry timing. This section explicates the main challenges and research opportunities, and Table 2 features key conceptual, empirical, methodological, and definitional questions that should guide future entry-timing research.

Research Questions in the Area of Entry Timing

Note: FMA = first-mover advantage.

As with any proliferating scholarship stream, the most obvious gaps often stem from inconsistent definitions, imprecise sampling, deficient methodology, and underconstruction of theory. For example, markets are in a constant state of change with fluctuating levels of unrest and uncertainty; such volatility introduces empirical ambiguities and raises concerns regarding construct validity. While construct validity should be explicitly and consistently addressed, it is difficult to conceptualize and measure some key constructs, such as market birth and age, size and scope of a market space, or industry boundaries. Consider, for example, the first mechanical typewriters, which were displaced by electronic typewriters, which were then dislodged by PCs, laptops, and now smartphones and tablets; it is difficult to identify which, if any, of these products represents the “birth” of a new market. Given that performance is the net outcome of many forces—for example, early- and late-entrant dynamics, incumbent reactions, market conditions, consumer behavior, technological and environmental changes, and government regulations (Lieberman & Montgomery, 2013)—it is not surprising that entry timing plays a contingent role in shaping performance. Entry timing is therefore a multifaceted construct that needs research attention in the context of other contingencies.

Sampling challenges and limitations of statistical techniques also force scholars to omit important variables from firm-, market-, and industry-level data. As Dobrev and Gotsopoulos note, “Tracking down early entrants and recreating their complete histories poses a daunting task [since] such firms are small and obscure, their products often cumbersome and quixotic, and the records they leave behind incomplete” (2010: 1168). Indeed, many studies we reviewed acknowledge the possibility of not knowing about the first entrants who failed to survive, which is consistent with Golder and Tellis’ (1993) and Mascarenhas’ (1992b) concerns about survival bias. However, entry timing will continue to be an important area of inquiry, and with the advent of more sophisticated statistical techniques, we are quite certain that scholars will be able to address various aspects of the survival bias. In short, just as research on start-up failure is contributing greatly to the field of entrepreneurship, more research on entry failure will improve our understanding of entry choices and timing effects.

A related issue that is innately a part of research on entry timing is the multilevel nature of most entry research. Throughout our review, the research questions posed by scholars typically involved multiple levels, including products, firms, industries, and countries, yet such questions were seldom addressed conceptually or empirically. As a result of the inherently nested nature of entry research, the theories, data, and analytical methods used to explain and predict relationships must consider hierarchical effects (Klein, Dansereau, & Hall, 1994). Hence, following similar calls (e.g., Hitt, Beamish, Jackson, & Mathieu, 2007; Kozlowski & Klein, 2000), there is a need to more explicitly consider how the various levels are nested and how each level affects the process of entry and its outcomes differently. Not considering multilevel factors can result in a variety of errors, such as conceptual misspecification and methodological violations, which delay the development of accurate models of entry timing. Despite some challenges, the conceptual foundation for making multilevel inferences has been established (e.g., Klein et al.; Kozlowski & Klein; Rousseau, 1985), and there are a growing number of techniques that allow for the use of multilevel concepts and data (Bliese, Chan, & Ployhart, 2007; Payne, Moore, Griffis, & Autry, 2011).

The majority of research reviewed considers the timing effects of entry of a single product into a single market, industry, or geographical region. However, important questions that address the aggregate effects of entry timing have been largely neglected. For example, as noted in Table 2, what are the firm-level performance effects of the cumulative entry-timing strategies for a basket of goods and services? Or to what extent does the utilization of different configurations of product-market entry-timing strategies for multiple goods and services aggregate into organizational competitive advantages? In addition, how might simultaneous entry of the same product into different geographical markets, or successive entry of products and complementary goods and services into different product markets, affect both firm- and corporate-level performance? Furthermore, how might intrinsic speed or other entry capabilities be developed and refined over a series of entry decisions, and how might these capabilities affect the pace of entry? Such inquiries would galvanize (or challenge) the view that an advantage in product-market entries can bring about firm-level advantages and, perhaps, strategic orientations toward approaching entry in a consistent way over time. Recent work on temporal orientations (e.g., Brigham, Lumpkin, Payne, & Zachary, 2014; Souder & Bromiley, 2012) may be particularly applicable with regard to how organizations strategically approach entry over time.

Time can also be considered a level of analysis and, thus, should be more explicitly addressed both conceptually and empirically. Because of its potential to affect the who, what, where, how, and when of entry strategies, we think it is unwise to separate the timing of entry decision from the mechanisms or modalities used for entry, as it would divorce strategy formulation from implementation (Mintzberg & Waters, 1985). Although we acknowledge the extensive efforts made with regard to time-sensitive empirics, such as the use of survival analyses, hazard models, and event history analyses, the role of time has not been integrated into theory beyond simple linear views (Short & Payne, 2008). As George and Jones (2000) suggest, to make entry-timing research more robust and lead to a more unified and dynamic theoretical understanding, scholars need time-based boundary conditions, such as the time of first product/service introduction to a launch of subsequent offerings, the onset of market maturity, or some other clearly defined inflection point after which the study of entry timing is conceptually and empirically inapplicable (Suarez & Lanzolla, 2007). Future research should advance theory and better integrate new methodological techniques to develop and test entry-timing questions. For example, there is a rich literature that explores population ecology that uses markers such as niche width, resource partitioning, and density dependence (e.g., Dobrev & Gotsopoulos, 2010; Dowell & Swaminathan, 2006; Hannan & Freeman, 1989). We sense that anchoring constructs in dynamic contexts (e.g., smartphones) can advance understanding of entry-timing effects.

A related issue that delays progress is endogeneity—the interdependence between cause and effect. For example, entrants change their strategy in response to market conditions, while market conditions shift as a result of entry. A pioneering firm may succeed not because of its order of entry per se but because of other reasons, such as its R&D and supply chain capabilities or because it uses bracketing patents that undermine would-be followers. As a number of studies we reviewed show, an optimal choice between first mover and follower is often linked to a firm’s resource-capability mix as well as market and industry conditions. Notwithstanding attention to the various contingencies of entry—who, where, what, how, and when—the field lacks clarity about the conditions under which various combinations (e.g., firm capabilities, market, and/or industry forces) are most and least promising for a strong entry. In this sense, entry-timing research greatly parallels the challenges embedded in various theories of resource-based advantages (Kraaijenbrink, Spender, & Groen, 2010). Hence, we offer a word of caution to researchers who seek to theoretically ground their entry-timing study in resource-based logic.

The strong interrelatedness of the contingencies surrounding entry timing and advantage (and disadvantage) begs the question of whether research can and should attempt to disentangle the configural nature of the entry-timing phenomenon. In other words, is there a direct relationship between entry timing and firm advantages not obscured by contingencies, and is entry timing the strongest predictor of performance? The answer to these two questions, on the basis of our review, is no and, hence, our advice to view entry timing as a contingency factor rather than a stand-alone variable. Future scholars should consider entry timing, including its antecedents, contingencies, and consequences, from a configurations perspective, which might suggest that entry-timing relationships are best explained through situational archetypes. Configurations theory suggests that organizational phenomena are better understood by grouping organizations on the basis of configurations of attributes to form archetypes or gestalts that can be generalized across contexts (Short et al., 2008). All in all, entry timing and outcomes are better understood, explained, and predicted by examining such factors dynamically and holistically rather than piecemeal. Furthermore, a configurations perspective may be useful by examining whether optimal configurations of entry characteristics exist or whether equifinality is present (Payne, 2006).

Our review also found insufficient research on postentry strategies, and we sense that this area is ripe for research and integration with parallel literatures (cf. Ketchen et al., 2004). As consumers, products, firms, markets, and industries evolve—hence, our penchant to view the concept of entry as a process, not an event—even the best entrants must quickly develop a postentry plan; this is what D’Aveni, Dagnino, and Smith (2010) term the first, second, . . . sixth dynamic strategic interactions. To use an analogy, there is a wealth of information on the antecedents, contingencies, and consequences of mergers and acquisitions but not nearly enough on post–merger and acquisition activity, such as operational integration, product and service synergies, and cultural harmonization (Markman & Venzin, 2014). Another research domain that may offer conceptual and empirical pathways is a burgeoning literature on serial entrepreneurship that compares/contrasts first-time versus serial entrepreneurs (e.g., Plehn-Dujowich, 2010). In our context, studies on postentry and repeat entry are clearly missing and provide an excellent pathway to enrich the literature.

One theory that may hold considerable promise for understanding the cyclical timing of decisions that firms make is organizational entrainment theory. The theory argues that firms are best served when they match the timing of internal processes and actions (e.g., product development and release, diversification) with a dominant external pacer or “zeitgeber” such as institutional forces, calendar events, or geopolitical happenings (Pérez-Nordtvedt, Payne, Short, & Kedia, 2008). An entrainment view of entry timing may help to explain the success versus failure of repeated entry-timing decisions made by firms because it anchors timing decisions not just on competitors but also on external pacers, such as seasonal events or economic forces.

Finally, another research gap relates to resource-based competition (Markman et al., 2009). Consider, for example, how studies on FMAs have proven to be much more prevalent in consumer goods industries as opposed to producer goods industries, and none of the 105 studies surveyed sought to explore entry timing in factor markets. This is not very surprising given the empirical and methodological challenges that are associated with studying factor-market rivalry. Still, given that resource and product markets are characterized by different conditions—that explain why firms compete very differently in product and factor markets—it seems plausible that entry timing would unfold differently in each of these market types. Hence, we encourage greater research on entry into resource markets beyond general modeling of R&D, mergers and acquisitions, FDI, or other types of slack resource allocations.

Integrative Model of Entry Contingencies

The challenges to FMA logic and calls to integrate antecedents and contingencies with entry-timing logic are not entirely new, but we reiterate them in the above discussion to highlight the need to develop a more holistic framework of entry—one that integrates timing with other important entry considerations. As a first step towards this end, we offer a general model (shown in Figure 2) that suggests that any entry choice depends on five interlinked forces: (1) who—the relevant players (e.g., entrants, incumbents, buyers, partners, stakeholders, regulators); (2) where—the area that is entered (e.g., technology corridors, product spaces, markets, industries, or geographical locations); (3) what—the type of entry (e.g., product, service, resource, or business model entry); (4) how—the strategies, resources, capabilities, and assets needed to enter; and (5) when—the contextual timing for entry (e.g., first mover, second mover, early mover, early follower, late mover, late follower). These five categorizations are representative of the various contingencies that have been examined in the extant literature and should be considered simultaneously and dynamically in the process of entry.

The Five Contingencies of Entry

Although a full theoretical narrative, with regard to the model shown in Figure 2, is beyond the scope of this article, we believe that such an amalgamated framework is needed for the field to progress. Indeed, while we heralded several studies that use longitudinal data, large samples of entrants and incumbents, and sophisticated statistical procedures, most entry-timing studies offer an incomplete view because they neither investigate the full spectrum of contingencies nor consider their interdependencies fully. Therefore, the research, to date, may be analogous with the proverbial tale of the blind men and the elephant, where each man described the elephant differently, according to the various body parts touched. Here, researchers are analyzing the same phenomena and reporting valuable lessons but do not provide a holistic understanding of entry decisions and actions.

Specifically addressing this need, our model offers a starting point for better understanding entry in a more comprehensive way. We hope that additional research can provide a more thorough grounding for appropriating and developing the model. As is, the model reflects a cross-sectional summation of collective wisdom featured in the articles that we reviewed. So if validated and expanded by future research, this model could help unify the diverse conceptualizations and findings associated with entry choices, including timing. For example, our model does not suggest an order of impact for the five entry forces; it is possible that considerations of the “when” contingency should come into play only after firms address the “who” and the “how” contingencies. These, and other key concerns, represent strong opportunities for future conceptual and empirical work in this important area of research.

Conclusion

As we reviewed the articles in the extant literature over the previous 25 years, it was clear that entry timing does matter but equally unclear how or under what conditions. We learned that timing, while important, may not be a primary, and certainly not the sole, consideration for making entry decisions. Rather, timing is more likely a secondary or tertiary consideration because of the many contingencies that also influence entry decisions. Hence, we advocate more attention to how timing, as one of several contingencies, might be better integrated into entry research both theoretically (i.e., beyond FMA) and empirically. We owe it to the field, and to the managers who we advise, to broaden our thinking about entry considerations or we will just perpetuate the myth that “being first creates a competitive advantage” without the caveat that when to enter is only one of at least four additional considerations. As demonstrated in Figure 2, other necessary considerations, besides when, include who (e.g., considering the entrants, incumbents, buyers, partners, and stakeholders), where (the actual space where entry might unfold), what (whether the entry entails product, resources, business model innovation), and how (how entrants might use strategy, resources, and capabilities).

Footnotes

Acknowledgements

This article was accepted under the editorship of Deborah E. Rupp. We thank Jeremy Short, the associate editor, and two anonymous reviewers for their insightful and developmental feedback. We seek forgiveness from the many scholars whose work we wanted to cite but were unable to as a result of space limitations. Authors contributed equally; they are listed in a reversed order of seniority.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.