Abstract

Signaling theory suggests that firms send signals to stakeholders to reduce information asymmetry. Research, however, has rarely examined how investors interpret signals that are equivocal. We suggest that sensemaking serves as an important process by which investors interpret firm signals, and salient contextual cues influence the sensemaking process. We examine an equivocal signal, the adoption of a poison pill, as a means of examining investor interpretation of the signal and the role of contextual cues in influencing interpretation. Using a sample of 578 poison pill adoptions and controlling for self-selection, we find that investors react negatively to poison pills adopted to protect net operating losses (NOL poison pills) but positively to poison pills adopted when the firm is in receipt of a takeover offer (in-play poison pills). Assessing the role of contextual cues, our results suggest that CEO duality, the proportion of inside directors on the firm’s board, the firm’s R&D investments, and industry concentration also condition investor response to specific-purpose poison pill adoption. Our study contributes to research on signaling theory, sensemaking, and corporate governance by examining how investors interpret a firm’s equivocal governance decisions.

According to signaling theory, firms utilize signals to influence perceptions and responses to organizational actions (Connelly, Certo, Ireland, & Reutzel, 2011). Signals reduce information asymmetry between the firm and critical stakeholders (Akerlof, 1970; Elitzur & Gavious, 2003; Spence, 1973) and are sent, particularly to investors, to provide information regarding management’s quality and future intentions. Some signaling theory research examines positive signals communicated to convey firm attributes, for example, when management purchases firm stock to signal that strategies are value creating (e.g., Goranova, Alessandri, Brandes, & Dharwadkar, 2007). Firms may also send negative signals, such as announcing product recalls or firm name changes (Lee, 2001). An important aspect of the process, however, is that signal receivers, or stakeholders, must interpret and act upon signals from firms.

Signals, however, may be equivocal, leading receivers to enact a process whereby they interpret the signal’s meaning (Bolino, Kacmar, Turnley, & Gilstrap, 2008; Mills, 2003). While positive signals have received considerable attention, less research examines equivocal signals (Bell, Moore, & Al-Shammari, 2008; Connelly et al., 2011; Fischer & Reuber, 2007). Signaling theory offers little explanation as to how receivers interpret equivocal signals. We suggest that when signals are equivocal regarding the future value of the firm and managerial intentions, receivers are likely to undergo a sensemaking process to ascribe meaning to the signal.

Sensemaking is a process by which receivers interpret information to provide meaning as a precursor to action (Weick, Sutcliffe, & Obstfeld, 2005). Sensemaking processes rely upon situational cues to influence interpretation of a signal’s meaning (Mills, 2003; Weick et al., 2005; Zajac & Westphal, 2004); interpretation becomes important as receivers and signalers have competing interests (e.g., in adoption of poison pills). Sensemaking can thus serve as a means for stakeholders to deal with uncertainty (Mills, 2003).

One such signal that has received considerable attention is the adoption of poison pills (Straska & Waller, 2014). Poison pills generally provide rights to existing shareholders to purchase firm stock at discount prices in the event that the firm receives a hostile takeover offer or an outsider acquires a defined percentage of the firm’s shares. Poison pills are controversial to both practitioners and academics. Studies have found a negative relationship between poison pill adoption and abnormal stock returns (Bebchuk, Cohen, & Ferrell, 2009) or the likelihood of the firm being acquired (Borokhovich, Brunarski, & Parrino, 1997). Thus, researchers argue poison pills signal the firm entrenches ineffective managers from oversight by the market for corporate control. Despite this, research also notes poison pills may create value by allowing management to focus on long-term performance and providing the ability to extract greater acquisition premiums (Heron & Lie, 2006; Kacperczyk, 2009). Thus, we suggest that the positive and negative aspects of poison pills mean adoption is an equivocal signal for investor interpretation.

Traditionally, poison pills have been adopted on a “routine” basis to proactively ward off hostile takeovers. Given the negativity associated with poison pills, firms have responded by both repealing routine poison pills (Schepker & Oh, 2013) and adopting poison pills when there is a specific reason to do so (Boyson & Pichler, 2014; Laide, 2010). Specific-purpose poison pills attempt to overcome concerns regarding routine poison pills, as they are limited to the period during which the specific purpose is relevant (instead of a 10-year period for most routine poison pills). As such, specific-purpose poison pills are designed to communicate the adoption’s purpose and reframe it positively to shareholders, who can more closely monitor managerial behavior when the pill is in effect. Despite this, signaling theory suggests that such verbal declarations of intent are cheap signals and may not provide a means for firms to differentiate their adoptions (Spence, 1976). Therefore, specific-purpose poison pills present a research gap to examine how investors interpret and act upon an equivocal signal that is reframed positively with the goal of reducing information asymmetry regarding management’s intent in adopting the poison pill.

We draw on two types of specific-purpose poison pills: a net operating loss (NOL) carryforward poison pill and an in-play poison pill. NOL poison pills protect loss carryforwards for tax purposes, as U.S. tax law allows firms to carry forward losses to offset future taxable income. According to Internal Revenue Service (IRS) regulations, the benefits of NOLs are lost when firm ownership changes occur among blockholders. That is, such poison pills are adopted to protect existing NOLs, whose value is lost if a substantial change in the firm’s ownership occurs. Investor response to such adoptions, however, may be equivocal.

On the one hand, NOL carryforwards represent a valuable tax asset, and poison pills may allow managers with firm-specific knowledge to improve firm performance with limited threat of potential takeovers (positive interpretation). On the other hand, NOL poison pills could promote managerial entrenchment by limiting the efficacy of the market for corporate control toward underperforming managers (negative interpretation). Furthermore, there is no guarantee that the future gains from tax benefits would exceed gains provided by an acquirer. Thus, investors must consider whether they can gain more by letting incumbent managers attempt to improve performance or realize greater economic gains from an acquirer.

The second type of specific-purpose poison pill, an in-play poison pill, is adopted when the firm receives a tender offer or hostile takeover bid from a prospective acquirer (Laide, 2010). Proponents argue that they allow shareholders to realize higher acquisition premiums, as the board and management may utilize the poison pill as a negotiating chip (positive interpretation). In-play poison pills, however, could also entrench managers, as such poison pills increase the cost of acquiring the firm, buffering managers from the market for corporate control (negative interpretation). Thus, in-play poison pills could also be received equivocally.

Despite the trend toward specific-purpose poison pills, it remains unclear how investors interpret such adoptions (e.g., Sikes, Tian, & Wilson, 2014). Utilizing signaling theory and theory on sensemaking, we argue that the adoption of a poison pill is an equivocal signal for investors to interpret. By blending sensemaking with signaling theory, we illustrate how low-quality signals sent by management are interpreted through sensemaking processes by receivers and that these outcomes are not necessarily those desired by management. Further, we illustrate how sensemaking processes lead receivers to examine salient contextual cues to influence the interpretation of the signal and subsequent investor action. Thus, as poison pills could be an equivocal signal from management regarding its intentions (Crawford, 2003), shareholders examine additional informational cues to interpret specific-purpose poison pill adoption decisions. In particular, the firm’s governance context (Sundaramurthy, Mahoney, & Mahoney, 1997) and strategic context are likely to influence investor interpretation of the signal with regard to protecting shareholder interests (Hoskisson & Turk, 1990; Kosnik, 1990). Therefore, we argue that a poison pill’s specific purpose, an equivocal signal, influences investor reaction to its adoption, and the firm’s governance and strategic context will further influence this reaction.

We contribute to existing research as follows. First, we contribute to signaling theory by examining a signal that could be construed as equivocal depending on sensemaking. Limited research attention has been focused on what happens when a firm sends a signal that may be positive or negative. We extend early works on signaling theory suggesting that high-quality signals are necessary to credibly signal intent (Akerlof, 1970; Spence, 1973) by illustrating how signals influence investor response, particularly when context cues enhance interpretation. In blending signaling theory with sensemaking, we go beyond early works in signaling theory regarding the quality of the firm’s signal by considering the role of receivers in accepting the signal’s intent. This is important as firms understand how to reframe negative messages positively, particularly when communication is important to reduce information asymmetries.

Second, we contribute to signaling theory by examining how receivers interpret firm signals. We incorporate sensemaking as a process by which receivers derive meaning from firm signals and how this interpretation influences action. Whether receivers interpret signals consistent with a firm’s intentions has important consequences. We illustrate how receivers interpret equivocal signals positively when context cues exist that promote the positive meaning of the signal, while signals are discounted when information is not consistent with the firm’s signal. Thus, we go beyond early signaling theory explanations that “talk is cheap” by illustrating how low-cost signals may be valuable when supported by consistent contextual cues.

Third, we contribute to research on poison pills by examining investor response to specific-purpose poison pills. Given that such pills are strategic as they are adopted to convey the provision’s meaning, it is likely that investors respond differently to such poison pills than to routine poison pill adoption. Such poison pills exist to reduce information asymmetries regarding management’s intent following poison pill adoption; however, this intent may not be received positively by all stakeholders. Finally, we suggest that contextual cues are particularly important to receivers in interpreting signals that are particularly equivocal in nature.

Signaling Theory and Sensemaking Processes

Signaling theory explains how firms attempt to reduce information asymmetries with stakeholders (Akerlof, 1970; Connelly et al., 2011; Spence, 1973). Signals communicate information about the firm and its attributes or likely future behavior (Akerlof, 1970). Information asymmetries are particularly problematic when one party is concerned with the behavior and intentions of another party (Elitzur & Gavious, 2003), such as when firm ownership is separated from its management (Jensen & Meckling, 1976). As such, research on signaling theory often examines positive signals sent by organizations, such as top executives who purchase shares in their firm as signaling strategies are in the best interests of the firm’s investors (Goranova et al., 2007). In this sense, signals are an important mechanism for firms to utilize when attempting to influence stakeholder perceptions (Zajac & Westphal, 2004).

While the signaler and signals are an important aspect of the process, equally important is the receiver. Classical works in signaling theory focus primarily on the signal as a sign of quality designed to reduce information asymmetry; however, because signalers and receivers often have competing interests, signalers may have an incentive to provide false signals. For instance, Zajac and Westphal (2004) illustrate how firms adopt stock repurchase plans to influence investor response but often fail to implement such plans. Such signals may be low-cost “cheap talk” initiated by signalers to communicate false information. As such, shareholders prefer to validate information independently to lower the risk of managerial self-interest seeking (Crawford, 2003). Receivers not only identify signals but also interpret their meaning (Connelly et al., 2011). Largely absent from this research is whether receivers interpret the signals sent by firms in accordance with the signaler’s intent. Further, less research has focused on signals sent that are equivocal in nature. We suggest that receivers decipher the meaning behind an equivocal signal through sensemaking. Sensemaking serves as a process through which individuals develop plausible ideas to interpret events (Weick et al., 2005).

Sensemaking serves as a means by which individuals interpret and respond to an event. When action is critical, interpretation is a core phenomenon (Laroche, 1995; Weick, 1993). Furthermore, sensemaking is most relevant when equivocality exists, such that it can provide meaning regarding the message and reduces uncertainty (Mills, 2003). Finally, sensemaking is further aided by cognitive models and salient contextual cues, which help in the interpretation (Weick et al., 2005). Such cues become more important when signals are equivocal, as equivocality limits the effectiveness of heuristics in interpretation (Mills, 2003; Westphal & Zajac, 1998). As such, investor reactions to firm signals are likely to reflect interpretation of events that reduce uncertainty related to managerial motives (Westphal & Zajac, 1998).

Sensemaking is important to stakeholders who cannot observe managerial actions and intent. Stakeholders must consider the nature of the message provided by firms to understand its underlying meaning, as many signals sent by firms may have multiple interpretations. Thus, it is important to understand how stakeholders will respond to such messages and under which conditions signals will be positively received. We examine receiver sensemaking in the context of an equivocal firm signal: investor responses to the adoption of a poison pill, a controversial decision that has both positive and negative effects for shareholder value. Further, we suggest that context cues shape receiver interpretations of firm signals by further reducing information asymmetry regarding the signal sent. In turn, this interpretation enhances signal receptivity by investors. In doing so, we integrate the process of sensemaking into signaling theory by illustrating the important role of the receiver in discussing firm signals.

Specific-Purpose Poison Pill Adoption and Investor Response

Poison pills are adopted by the firm’s board and do not require shareholder consent (Walsh & Seward, 1990). Most research focuses on routine poison pill adoptions, typically valid for a 10-year period to proactively protect the firm from hostile takeovers. Poison pill benefits, however, have long been controversial (for detailed reviews, see Straska & Waller, 2014; Sundaramurthy, 2000). Some propose (e.g., Heron & Lie, 2006) that poison pills are beneficial, as they increase firm bargaining power to negotiate higher premiums during takeovers and signal bidders that the board will resist takeover attempts or demand a significant premium (Bebchuk et al., 2009). Poison pills also allow greater freedom to pursue long-term strategies that may create value (Kacperczyk, 2009). Others argue (e.g., Walsh & Seward, 1990) that by reducing the likelihood of a takeover attempt, poison pills insulate managers from the market for corporate control and lower shareholders’ ability to discipline ineffective managers (Bebchuk et al., 2009).

Research to date is mixed regarding stock market reaction to poison pill adoption. Studies have found positive (e.g., Brickley, Coles, & Terry, 1994) and negative (e.g., Malatesta & Walkling, 1988) market reactions to poison pill adoption, indicating that the adoption of a poison pill may be both a positive and a negative signal. Some research suggests poison pills reduce firm value (e.g., Borokhovich et al., 1997; Field & Karpoff, 2002; Pound, 1987), while others find that poison pills do not reduce the probability of takeover but do increase acquisition premiums (e.g., Comment & Schwert, 1995; Heron & Lie, 2006). This mixed empirical support suggests that poison pill adoption is likely to be an equivocal signal to investors. As such, to infer managerial intent relating to the adoption, investors must interpret the adoption’s meaning.

Changes in Poison Pill Adoption Practice

In recent years, boards of directors have come under greater scrutiny, reducing the likelihood of poison pill adoption and leading to many firms repealing poison pills (Schepker & Oh, 2013). Institutional and activist investors suggest that poison pills are “relics of the past” (Fontevecchia, 2013). While many firms adopt poison pills preemptively, such poison pills often are perceived as negative signals of future managerial behavior. Instead, firms now adopt poison pills for specific purposes (Laide, 2010). Specific-purpose poison pills are designed to signal positive intentions by responding to a specific threat and reduce information asymmetry regarding the intent of the poison pill’s adoption. However, given the prior negative association relating to poison pills, such signals may be equivocal to investors. Two types of specific-purpose poison pills have been increasingly adopted: NOL carryforward and in-play poison pills. During the 2000s, the adoption of routine poison pills declined significantly, from more than 120 in 2002 to fewer than 20 by 2010. In contrast, NOL and in-play poison pill adoptions increased from 11 such adoptions in 2002 to more than 30 such adoptions by 2008.

NOL poison pills are designed to protect a firm’s NOL carryforwards for tax purposes (Shargel & Monaco, 2011). When firms report NOLs, such losses can be either used to recover tax payments made in the past 2 to 3 years or carried forward to reduce tax burdens in the next 10 years. However, according to Section 382 of the Internal Revenue Code, companies that experience significant ownership changes of more than 50% in any blockholder group in a 3-year period can lose most or all of their NOLs. In response, firms began adopting NOL poison pills, which trigger typically at 4.99% ownership, as blockholders are entities that hold 5% or more of equity. In short, NOL poison pills make it more difficult for blockholders to change ownership as such changes will neutralize the value of NOLs for tax purposes. As such, NOL poison pills are designed to positively signal management is seeking to protect the firm’s valuable tax assets.

A second type of poison pill is adopted when the firm is “in play.” In-play poison pills are adopted upon receipt of a tender offer from a potential acquirer and act as a bargaining chip to gain higher takeover premiums or to reduce the likelihood of a takeover attempt. An in-play poison pill may serve as a means for management to signal positive intentions to enhance shareholder value through extracting greater acquisition premiums.

For both poison pills, management seeks to reframe equivocal perceptions of poison pill adoption to a positive signal of future intentions or behavior in line with shareholder interests. While these signals are designed to reduce information asymmetry, investor responses are likely to be conditioned based on how sensemaking processes influence their interpretation of the rationale for the poison pill’s adoption. At the same time, communicating the specific purpose of the poison pill is a low-cost signal. Both signaling theory and sensemaking suggest that investors may not rely solely on the firm’s low-cost signal to infer intent but may also rely on additional cues.

Specific-Purpose Poison Pills and Market Response

NOL poison pills are adopted to signal the firm’s desire to protect a deferred tax asset that is lost if ownership changes occur among blockholders. Investors should positively value NOL poison pills, as loss of such assets reduces the firm’s value. Despite this positive framing, proxy advisory firms oppose NOL poison pill adoption, as the typical 4.99% ownership trigger of an NOL pill is significantly lower than for routine poison pills, typically 10% (Deliso, 2009), and could lead to managerial entrenchment. As such, proxy advisory firms suggest that NOL poison pills are negative signals of future managerial behavior and intent.

Despite attempts to signal positive intentions, we suggest NOL poison pills are received and interpreted negatively by investors for three reasons. First, the existence of NOLs likely means the firm has performed poorly, which is an indication of lower-quality executives (Fee & Hadlock, 2004). Second, investors are likely to support large blockholders who may serve as a means to monitor managerial behavior, which may be most necessary when performance is poor. However, the lower trigger percentage for an NOL poison pill decreases the likelihood that blockholders would gain significant stakes in the firm. Such actions reduce the effectiveness of shareholder monitoring and efficacy of the market for corporate control. NOL poison pills could also serve as a means of entrenching managers against performance declines, earnings smoothing, and propping up profits resulting from tax benefits due to carryforwards of operating losses. Finally, investors are likely to be wary of managerial decisions that increase risk. The equivocal nature of poison pill adoption, even when promoted positively, may lead investors to err on the side of caution and discount the firm when an NOL poison pill is adopted.

Given the incentive of managers to reduce their employment risk in the face of prior losses (Crawford, 2003; Walsh & Seward, 1990), we posit that a poison pill adopted with the intention of protecting NOLs will be negatively received by the market particularly as it may reduce the efficacy of the market for corporate control. As such, our arguments suggest that while management attempts to reframe the poison pill adoption as a positive signal, investors will interpret the signal negatively, resulting in actions that reduce the firm’s stock price.

Hypothesis 1: Announcements of poison pills designed to protect NOL carryforwards will be negatively associated with stock market reaction compared to the announcement of routine poison pill adoptions.

An in-play poison pill adoption presents different interpretation challenges. In-play poison pills increase the difficulty or cost for acquirers to complete the acquisition once a tender offer is received. On the one hand, in-play poison pills may serve as negative signals as they may entrench management by reducing the likelihood of a potential takeover event (Pound, 1987). Acquirers may discount firm value for entrenchment, reducing investor valuations. On the other hand, in-play poison pills may serve as positive signals, as several studies suggest that poison pills increase bid premiums while not decreasing the likelihood of takeover attempts (Comment & Schwert, 1995; Heron & Lie, 2006). The board’s responsibility is to ensure that fair value is received for the firm, and an in-play poison pill can be used as a negotiating chip to increase an acquisition premium. Therefore, we suggest that an in-play poison pill reduces information asymmetries with regard to poison pill adoption by sending a stronger signal regarding the board’s intention to extract value for shareholders from prospective acquirers.

Hypothesis 2: Announcements of in-play poison pills will be positively associated with stock market reaction compared to the announcement of routine poison pill adoptions.

The Moderating Role of Context Cues

While the adoption of specific-purpose poison pills may signal investors, it is also a relatively low-cost, equivocal signal. Sensemaking and signaling theory suggest that when signals are equivocal, informational cues enhance interpretation of the event (Weick et al., 2005). Such cues increase signal strength by providing information, which reduces information asymmetries and enhances diagnosticity of an event’s meaning (Chung & Kalnins, 2001; Fischer & Reuber, 2007). Furthermore, they help receivers determine whether the signaler’s qualities are associated with the positive or negative intentions tied to the signal (Durcikova & Gray, 2009).

Specific-purpose poison pills yield equivocal interpretations as investors are unsure of whether the adoption would promote shareholder interests or yield managerial entrenchment. Relying on managerial intent to evaluate adoptions is difficult, as managers have incentives to misrepresent intent (Crawford, 2003). Consistent with poison pills as equivocal signals, studies on routine poison pill adoptions find that investors respond positively when the firm has strong governance and negatively when governance is weak (Brickley et al., 1994; Sundaramurthy et al., 1997). We suggest that shareholders seek out cues related to the firm’s governance and strategic contexts to enhance interpretation of a specific-purpose poison pill’s adoption. Corporate governance provides indications of the degree to which the board is able to protect shareholder interests (Hoskisson & Turk, 1990; Kosnik, 1990; Lorsch & MacIver, 1989). The firm’s strategic context reduces information asymmetries by providing information regarding management’s prior behaviors and the nature of its competitive environment.

Firm governance cues

Corporate governance is likely to provide cues that condition investors’ interpretation of managerial decisions, as decisions by firms with poor governance are likely to be construed negatively (Sundaramurthy et al., 1997; Walsh & Seward, 1990). Two important characteristics are the CEO’s structural power relative to the board and the degree to which inside managers are involved in board strategic decisions.

Structural power enhances the CEO’s authority over the decision to adopt a poison pill. CEOs with the dual role of chairman of the board have greater power. The ability of the board to effectively monitor such CEOs is lower (Walsh & Seward, 1990), thereby increasing monitoring and control costs (Sundaramurthy et al., 1997). Stronger, more powerful boards vis-à-vis the CEO are likely to assuage investor apprehension regarding specific-purpose poison pill adoption by illustrating that the adoption is less related to the interests of a powerful CEO. For instance, when the firm receives a takeover offer, non-CEO-dominated boards may be construed as adopting an in-play poison pill to increase bargaining power rather than to entrench management and reduce CEO employment risk. Similarly, when a firm has NOLs, non-CEO-dominated boards ensure monitoring and also provide resources and counsel to improve performance.

Furthermore, Finkelstein and D’Aveni (1994) suggest that CEO duality may increase managerial entrenchment but also may provide for unity of command. As such, managerial discretion of the CEO is likely to be higher under CEO duality. While powerful CEOs may be able to adopt specific-purpose poison pills to protect long-term firm investments (Kacperczyk, 2009), investors should respond negatively to increased managerial discretion in the face of antitakeover provisions that insulate potentially ineffective managers. Given negative signals associated with potential entrenchment and increased discretion, we suggest that investors will react more negatively to specific-purpose poison pill adoption when the CEO has duality.

Hypothesis 3a: The negative association between an NOL poison pill adoption and stock market reaction is exacerbated in the presence of CEO duality.

Hypothesis 3b: The positive association between an in-play poison pill adoption and stock market reaction is attenuated in the presence of CEO duality.

The composition of the firm’s board of directors also likely influences sensemaking. Outside directors play a fundamental role in monitoring managerial behavior (Sundaramurthy et al., 1997). However, outside directors also have limited knowledge of the firm and its industry (Carter & Lorsch, 2004). Given this knowledge differential, inside directors, or members of management, have more information about firm capabilities than outside board members (Baysinger & Hoskisson, 1990; Shen & Cannella, 2002). This better enables inside directors to know the firm’s true value and allows inside directors to involve themselves more in board deliberations (Finkelstein, Hambrick, & Cannella, 2009).

With regard to NOLs, inside board members likely better understand the true value of a firm’s NOLs. Due to greater firm-specific knowledge of inside directors, investors may interpret the adoption of an NOL poison pill as a positive signal aimed to protect tax assets. A significant advantage of adopting an in-play poison pill is to vest managers with the power to negotiate with bidders, which is especially effective when shareholders are dispersed (DeAngelo & Rice, 1983; Straska & Waller, 2014). Investors should respond positively to in-play poison pills when the firm has directors with greater knowledge of the firm’s value, which should provide negotiating benefits. Thus, we propose that a specific-purpose poison pill’s adoption will be interpreted as a positive signal when the firm has a higher percentage of inside directors on the board.

Hypothesis 3c: The negative association between an NOL poison pill adoption and stock market reaction is ameliorated under a high proportion of inside directors.

Hypothesis 3d: The positive association between an in-play poison pill adoption and stock market reaction is strengthened under a high proportion of inside directors.

Firm strategic context

While governance indicates the potential to limit problems of managerial opportunism, the firm’s strategic context provides information regarding strategic actions undertaken and the environment in which the firm operates, which may assist in the interpretation of the signal. Prior strategic investments are likely to be indicative of the degree to which the firm targets long-term value-creating strategies or those designed for short-term payoffs. In particular, R&D investments are indicative of strategies with long-term payoffs (Barker & Mueller, 2002), which may signal the firm’s commitments.

R&D investments may serve as a negative signal when firms adopt NOL poison pills. Under high levels of R&D investments, investors may believe NOLs exist due to unsuccessful R&D investments. R&D investments also have high outcome uncertainty in the future. As such, an NOL poison pill under high R&D investments may be interpreted as a signal that executives are making high-risk bets. Further, given prior losses, investors may believe R&D investments will not pay off. If firms fail to achieve profitability, value will not be appropriated from NOLs, and a poison pill would only entrench managers. In short, NOL poison pill adoption allows managers to “buy time” to make excuses for past unsuccessful investments. Thus, we suggest investors will respond negatively to NOL poison pills in the presence of higher R&D intensity.

In-play poison pills may protect specific knowledge that may be undervalued at the time of the tender offer due to investments in long-term strategies (Kacperczyk, 2009; Mahoney, Sundaramurthy, & Mahoney, 1997). In-play poison pills are a positive signal under higher R&D investments, as firms protect undervalued assets or obtain higher acquisition premiums given R&D investments presumed to pay off in the future. An in-play poison pill signals bidders that R&D investments should be reflected in acquisition premiums. As such, investors will respond more positively to in-play poison pills when R&D intensity is higher.

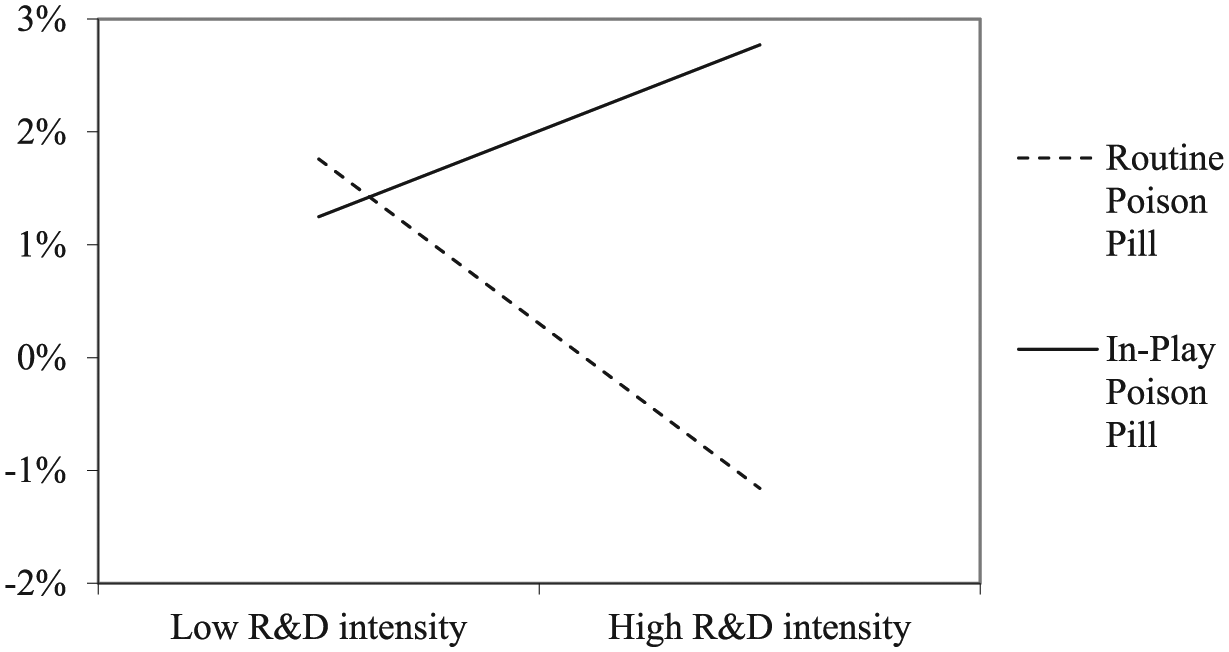

Hypothesis 4a: The negative association between an NOL poison pill adoption and stock market reaction is strengthened under high R&D intensity.

Hypothesis 4b: The positive association between an in-play poison pill adoption and stock market reaction is strengthened under high R&D intensity.

The competitive environment also provides insight as to potential intentions in the future. In particular, the industry’s concentration influences the level and degree of competition (e.g., Palmer & Wiseman, 1999). Highly concentrated industries have several large players that control significant industry output. When firms are similar in size, competition may be intense as firms compete for small changes in market share.

Concentration may influence investor interpretations in several ways. High industry concentration is associated with lower complexity (Dess & Beard, 1984), as the major players are known, and strategic actions of competitors can be easily monitored. As a result, ability to take advantage of NOLs is higher as firms typically avoid head-on competition in a concentrated industry (Ketchen, Snow, & Hoover, 2004). Thus, firm attempts to improve value by adopting a poison pill are more likely to be successful in a high-concentration industry. Further, this leads to greater reduction in information asymmetries as investors can more easily identify strategic moves by industry competitors, thus reducing uncertainty regarding managerial intentions. Finally, highly concentrated industries have higher exit costs. An NOL poison pill adoption may signal that management is digging in to fight to improve its strategic position in the industry and desires to protect its valuable assets (cf. Anderson & Tushman, 2001). In short, NOL poison pills can be a strong signal to investors when industry concentration is high, as investors may make a more informed decision regarding managerial intent for the poison pill’s adoption.

On the other hand, an in-play poison pill increases bargaining power of target firms, as they are one of the few options acquirers have for growth. In-play poison pills are interpreted as value creating due to an improved bargaining position under high concentration. Under low concentration, an in-play poison pill may signal managerial entrenchment. The low concentration provides many alternative firms for the acquirer to negotiate with, reducing the bargaining power of the focal firm and thereby the effectiveness of the in-play poison pill.

Hypothesis 4c: The negative association between an NOL poison pill adoption and stock market reaction is attenuated under high industry concentration.

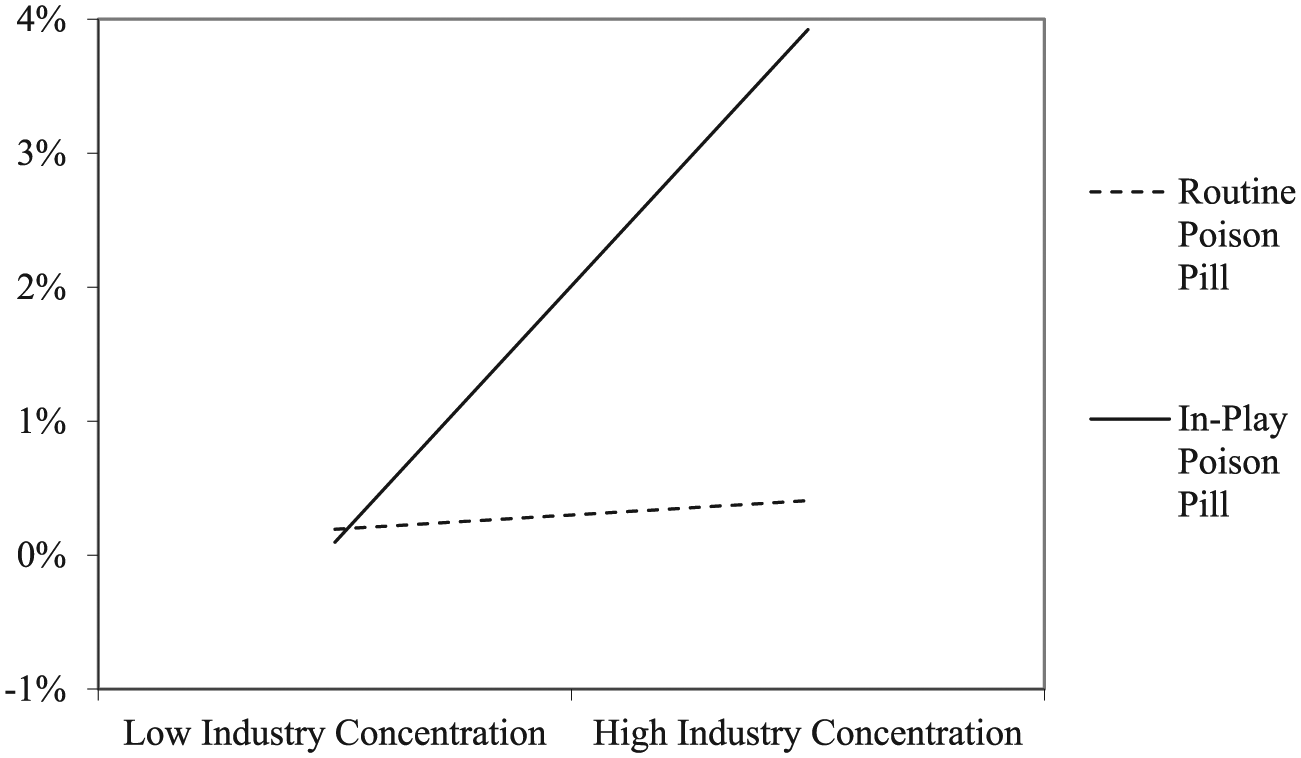

Hypothesis 4d: The positive association between an in-play poison pill adoption and stock market reaction is strengthened under high industry concentration.

Method

Data and Sample

Our sample was drawn from U.S.-based firms that adopted a poison pill between 2002 and 2011. Data on poison pill adoption were obtained from FactSet SharkRepellent (www.sharkrepellent.net), a research company specializing in takeover defense mechanisms. There were approximately 1,100 poison pill adoptions during our study period. Following prior studies (Rhee & Fiss, 2014), we did not include adoptions by mutual funds, real estate investment trusts, and investment companies. Also, we excluded cases where other confounding events, such as announcements of acquisitions, occurred during the event window of our study. We used a number of archival sources (i.e., COMPUSTAT, GMI Ratings), firm annual reports, and firm proxy statements to collect firm data. Investors’ stock market reaction data (cumulative abnormal returns [CARs]) were collected from EVENTUS.

After applying the filters, our sample consists of 578 poison pill adoptions with complete data. The sample size is comparable to prior studies on poison pill adoption (Rhee & Fiss, 2014). In our sample, 40 firms adopted poison pills for NOL tax purposes, whereas 108 firms adopted in-play poison pills. Six firms adopted poison pills that were classified as serving both purposes. The remaining 436 poison pills were classified as routine poison pill adoptions, which are poison pills that were adopted not in response to a specific threat or expectation of tax benefits but as a blanket provision that proactively protects the firm from hostile takeover.

Measurement of Variables

Dependent variable

As poison pill adoption conveys information to the stock market (Brickley et al., 1994), we used abnormal stock returns (CARs) around the announcement of a poison pill adoption as the dependent variable. CARs as a standard event study methodology have been extensively used in poison pill research (e.g., Agrawal & Mandelker, 1990; Rhee & Fiss, 2014; Sundaramurthy et al., 1997). As news of the poison pill may leak (the day before the announcement) and because the stock market could take time to assess the poison pill’s adoption, we use a window of −1 to +1. Longer windows could be confounded by other firm-related news.

The standard event study methodology of market model (MM) was used. Compared to market adjusted model or comparison period mean-adjusted returns, the MM is comprehensive (e.g., MacKinlay, 1997). The firm’s predicted stock return was calculated on trading day t = −170 to ending day t = −21 to estimate daily returns. Any abnormal return was then calculated using

where rt is daily return for the firm on day t, and rmt is the daily return for the value-weighted Russell 3000 market index, α and β are firm-specific parameters, and ε t is independent and identically distributed. Using α and β, we predict daily return, Rt, on day t, or the day of the announcement. We then subtract predicted return Rt from actual return, rt. The cumulative abnormal return is the abnormal return over the window between (t − 1) and (t + 1), or [−1, +1]. Abnormal returns are represented as percentages in our data.

Independent variables

Two types of specific-purpose poison pills are examined in our study: (a) adoptions to protect NOLs (NOL poison pill) and (b) adoptions in response to an acquisition offer (in-play poison pill). Due to prior losses, an NOL poison pill is designed to create the opportunity to offset future tax liabilities with a firm’s deferred tax assets. For example, Eastman Kodak announced an NOL poison pill to protect the use of its tax assets valued at about $2.9 billion (August 11, 2011). An in-play poison pill is adopted when the firm is the subject of specific or publicly announced takeover threats. For example, Clorox adopted a poison pill in response to an unsolicited acquisition offer from Carl Icahn, a 9.4% shareholder (July 18, 2011). Each type of specific-purpose poison pill adoption was coded as a dummy variable. All other poison pills adopted were coded as 0 and represent routine poison pill adoptions. All poison pill adoptions were classified as to their purpose by FactSet SharkRepellent.

Moderating variables

We have two sets of moderators reflecting firm governance cues and strategic context. For firm governance cues, we used CEO duality and proportion of inside directors. CEO duality, a dummy variable, is coded as 1 if the CEO was also chair of the board, 0 otherwise. Proportion of inside directors is the number of inside directors divided by the total number of board members. These were measured on the date of poison pill adoption. For strategic context, we used R&D intensity and industry concentration. R&D intensity is the firm’s R&D spending as a percentage of sales, and it was transformed logarithmically due to the positively skewed distribution. This variable was collected 1 year prior to the adoption of the poison pill. Industry concentration was calculated using the eight-firm concentration ratio (CR8), or the total market share of the eight largest firms in an industry at the two-digit Standard Industrial Classification level. Industry concentration was measured as of the year of poison pill adoption.

Control variables

We controlled for other firm, governance, and poison pill characteristics that could influence investor reactions. All variables, except prior net operating income, were gathered at the time of poison pill adoption. First, we controlled for firm-level characteristics. Firm data were collected from COMPUSTAT. Prior studies (e.g., Sundaramurthy et al., 1997) found that investors react more negatively for larger firms’ adoption of poison pills. Thus, we controlled for firm size, measured by taking the logarithm of a firm’s total sales. Since firms with low market capitalization relative to their book value are at a higher risk of takeover, we included market-to-book ratio, calculated as total market value divided by the firm’s book value. As firms with a greater level of debt are less attractive to potential acquirers, we further controlled for debt ratio, measured as the ratio of long-term debt to total assets (Schepker & Oh, 2013). Since the level of prior NOL is important for future tax purposes, we controlled for prior net operating income, measured as the 3-year average value of net operating income (loss) relative to the firm’s total assets before the poison pill’s adoption.

In addition, corporate governance characteristics, such as ownership, board structure, other antitakeover provisions adopted, and executive compensation, also affect investor reaction (Agrawal & Mandelker, 1990; Sundaramurthy et al., 1997). We controlled for blockholder ownership, since a negative reaction will be lower in the presence of large blockholders (Brickley, Lease, & Smith, 1988). Blockholder ownership (%) was calculated by the total percentage of shares held by investors who hold more than 5% of the firm’s outstanding shares. Data were collected from GMI Ratings and firm proxy statements. We also controlled for the proportion of non-interdependent directors, those nominated by the current CEO. Non-interdependent directors was measured by the proportion of the firm’s directors on the board who were not nominated by the incumbent CEO.

We also controlled for poison pill renewal, creating a dummy variable coded 1 if the adoption is the replacement of an existing poison pill (that expired or was due to expire shortly) and 0 if the adoption was original. The market cue by adopting a poison pill may be stronger for an original adoption. In our sample, 220 adoptions were renewals and 358 were new adoptions. This information was obtained from FactSet SharkRepellent. We also controlled for the number of other antitakeover provisions. Similar to previous studies (e.g., Schepker & Oh, 2013), we measured the sum of six antitakeover protections at the time of adoption: (a) classified board provision, (b) dual-class stock, (c) supermajority merger approval provision, (d) bylaw amendment vote, (e) corporate charter amendment vote, and (f) golden parachute. This information was collected from GMI Ratings, Execucomp, and firm proxy statements. Since CEO compensation impacts shareholder wealth (Brickley, Bhagat, & Lease, 1985), we included CEO long-term incentive pay, measured by the proportion of long-term variable pay (e.g., stock-based compensation and long-term incentive plan) to total compensation. Last, we included the inverse Mills ratio in order to correct for nonrandom sampling bias, as described below.

Analysis

Following prior studies on stock market reaction to poison pill adoption (Rhee & Fiss, 2014; Sundaramurthy et al., 1997), we used ordinary least squares (OLS) regression analysis. We mean-centered variables and measured variance inflation factors (VIFs), which ranged from 1.05 to 1.49. Since VIFs are under the conventional threshold level of 10 suggested by Belsley, Kuh, and Welsh (1980), our sample does not show evidence of multicollinearity.

Given that our sample includes only firms that adopted poison pills, sample selection bias may exist, as firms who adopt poison pills may evoke different investor responses. Thus, we used a Heckman selection model (Heckman, 1979), a two-staged procedure that corrects for sample selection bias. First, we estimated the likelihood of poison pill adoption over our study period using a probit regression model. We combined our sample (N = 578) and randomly selected firms that did not adopt poison pills from 2002 to 2011 from the GMI Ratings database (N = 582). We drew on a series of predictors identified through reviewing research related to poison pill adoptions.

At the firm level, we used firm size (e.g., Vijh & Yang, 2013), liquidity in machinery and equipment (e.g., Schlingemann, Stulz, & Walkling, 2002), leasing expenditures (Campello & Giambona, 2010), and ratio of employees to cost of goods sold. These variables suggest flexibility in strategic decision making following poison pill adoption. We also used prior firm performance as a predictor. For firm governance, we examined family firm ownership due to differing motives of such firms (e.g., Block, 2012; Gomez-Mejia, Cruz, Berrone, & De Castro, 2011), state of incorporation (e.g., Field & Karpoff, 2002), proportion of outside directors, board size, and number of other antitakeover provisions adopted (e.g., Mallette & Fowler, 1992). Results of the first-stage model are available from the authors upon request. The first-stage selection model generated the inverse Mill’s ratio, which was included as an additional control variable in our second-stage regression model predicting stock market reaction. The inclusion of the inverse Mills ratio controls for self-selection bias due to nonrandom sampling.

Results

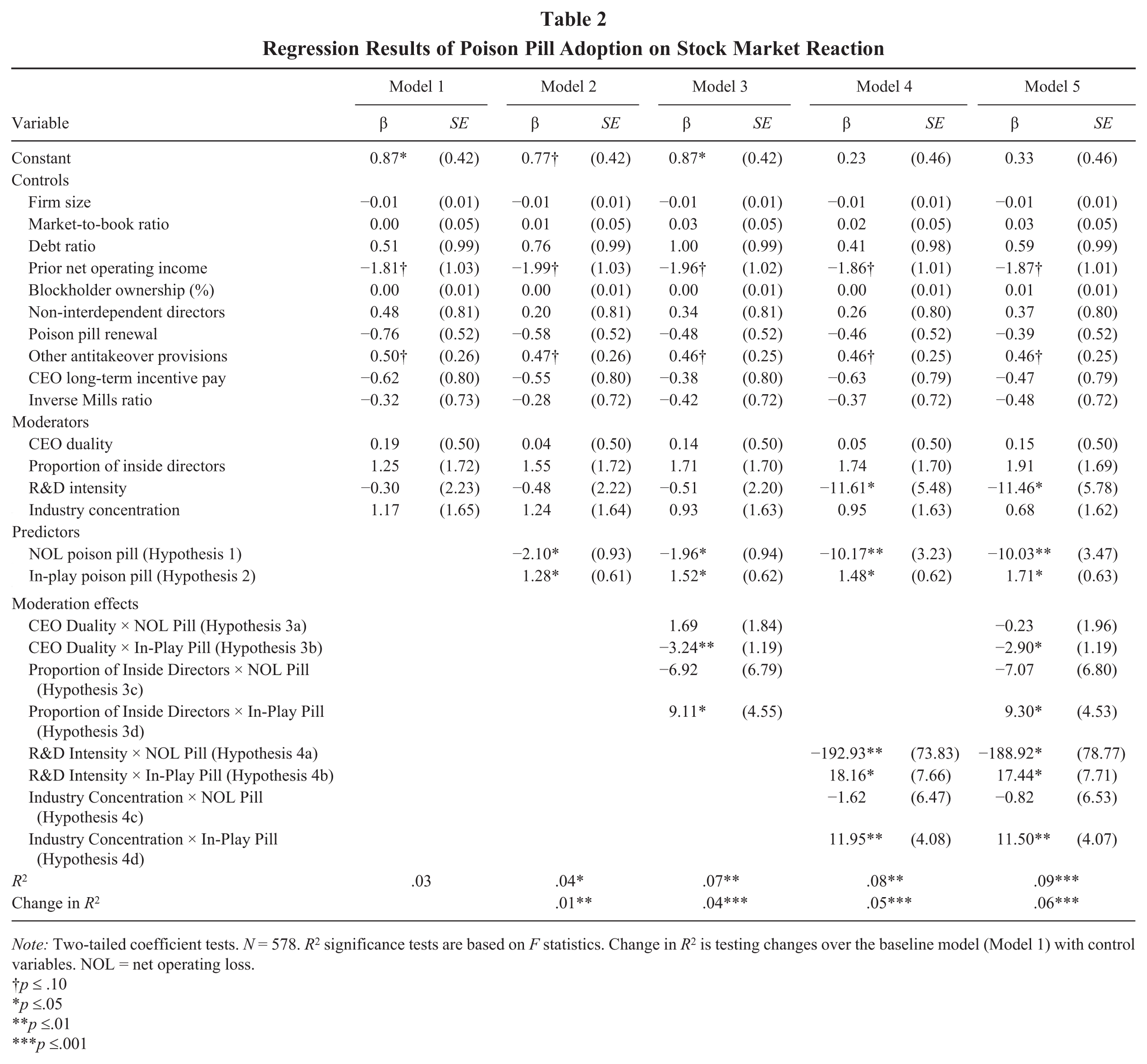

Table 1 shows descriptive statistics, including means, standard deviations, and correlations of our study variables. Table 2 shows the results of our analyses. Model 1 presents the baseline model with control variables, while Model 2 tests the main effects of NOL and in-play poison pill adoption. Models 3 and 4 examine the moderating effects of firm governance cues and firm strategic context for each type of poison pill. Model 5 is the fully specified model.

Means, Standard Deviations, and Correlations

Note: Two-tailed coefficient tests. Correlations with absolute values greater than .08 are significant at p ≤ .05 level and absolute values greater than .11 are significant at p ≤ .01 level. N = 578. NOL = net operating loss.

Regression Results of Poison Pill Adoption on Stock Market Reaction

Note: Two-tailed coefficient tests. N = 578. R2 significance tests are based on F statistics. Change in R2 is testing changes over the baseline model (Model 1) with control variables. NOL = net operating loss.

p ≤ .10

p ≤.05

p ≤.01

p ≤.001

We predict that investors will react negatively to an NOL poison pill (Hypothesis 1), while they will react positively to an in-play poison pill (Hypothesis 2). In Model 2, the adoption of an NOL poison pill is negatively associated with the stock market’s reaction (p ≤ .05) compared to a routine poison pill adoption; thus Hypothesis 1 is supported. Also, the adoption of an in-play poison pill is positively related to the stock market’s reaction (p ≤ .05) compared to routine poison pill adoption, supporting for Hypothesis 2. To understand the significance of our effects, we calculated the change in market capitalization associated with specific-purpose poison pill adoption. In our sample, the average market capitalization was $1049.18 million. The adoption of an NOL poison pill thus leads to a decline in market capitalization of $22.03 million (2.10% × $1049.18), while the adoption of an in-play poison pill increases market capitalization by $13.43 million (1.28% × $1049.18) in comparison to routine poison pill adoptions.

In Hypotheses 3a and 3b, we argue that CEO duality moderates the relationship between specific-purpose poison pill adoption and investor reaction. We do not find significant interactive effects for an NOL poison pill adoption and CEO duality (p > .10); thus Hypothesis 3a is not supported. However, results from both Model 3 and Model 5 provide support for Hypothesis 3b (p ≤ .01), indicating that the stock market reacts more negatively for the adoption of an in-play poison pill when the CEO is also the board chairperson. Hypotheses 3c and 3d predict that the proportion of inside directors on the board positively moderates the effects of NOL poison pills and in-play poison pills on stock market reaction. In Models 3 and 5, the interactive effects between NOL poison pill adoption and the proportion of inside directors are not significant. Therefore, Hypothesis 3c is not supported. However, the coefficients of the interaction terms of in-play poison pill and proportion of inside directors are significant (p ≤ .05), supporting Hypothesis 3d. To understand the significance of these effects, we calculated their economic value when duality exists versus does not exist and at one standard deviation above and below the mean of the proportion of inside directors. Upon adopting in-play poison pills, when the CEO has duality, market capitalization is reduced by $32.52 million compared to firms who do not have duality. At the same time, having a proportion of inside directors one standard deviation above average results in market capitalization of $31.73 million greater than firms who adopt in-play poison pills with a proportion of inside directors one standard deviation below average.

We proposed the moderating effects of R&D intensity on the relationship between poison pill adoption and stock market reaction. The coefficients of the interaction terms of NOL poison pill and R&D intensity (p ≤ .01) and of in-play poison pill and R&D intensity (p ≤ .05) are significant, providing support for Hypotheses 4a and 4b. In terms of economic significance, our results suggest that when adopting an NOL poison pill, market capitalization is reduced by $557.85 million for firms with R&D intensity one standard deviation above the mean compared to one standard deviation below. This decline in firm value must be interpreted with caution, as a large number of firms do not invest in R&D (Koh & Reeb, 2015); in such firms, R&D would be tied strongly to growth prospects and result in a stronger market reaction. When adopting an in-play poison pill, higher R&D investments result in market capitalization of $18.00 million greater than firms with low R&D investments.

In Hypotheses 4c and 4d, we propose the interaction effects of poison pill adoption and industry concentration on investor reaction. We do not find significant effects for NOL poison pill adoption and industry concentration (p > .10). Thus, Hypothesis 4c is not supported. Results from both Models 4 and 5 (p ≤ .01) support Hypothesis 4d, indicating that the positive effects of an in-play poison pill on investor reaction is stronger under higher industry concentration. Adopting an in-play poison pill increases market capitalization by $43.31 million when industry concentration is high compared to low levels of industry concentration.

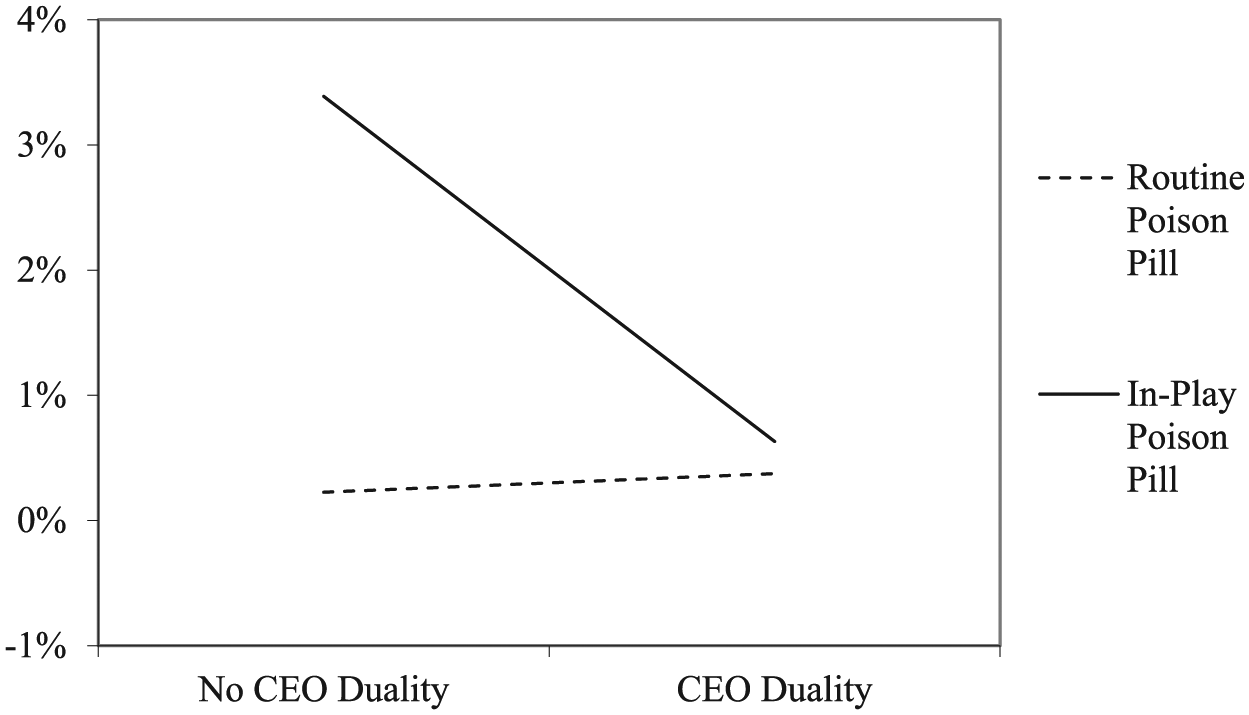

To illustrate the moderating effects, we plotted the effects of specific-purpose poison pill adoption on investor reaction at different conditions of governance cues and strategic context in Figures 1 through 5. The vertical axis represents stock market reaction (CARs) of the firms that adopt poison pills. Figure 1 shows that investors more favorably react to in-play poison pills when there is separation of the CEO and chairperson. For routine poison pill adoption, duality does not appear to affect investor response. Figure 2 shows positive effects of in-play poison pill adoption when there is a higher proportion of inside directors. As with duality, investors do not respond more strongly for routine poison pills under an increasing proportion of inside directors.

Interaction Between In-Play Poison Pill and CEO Duality (Hypothesis 3b)

Interaction Between In-Play Poison Pill and Proportion of Inside Directors (Hypothesis 3d)

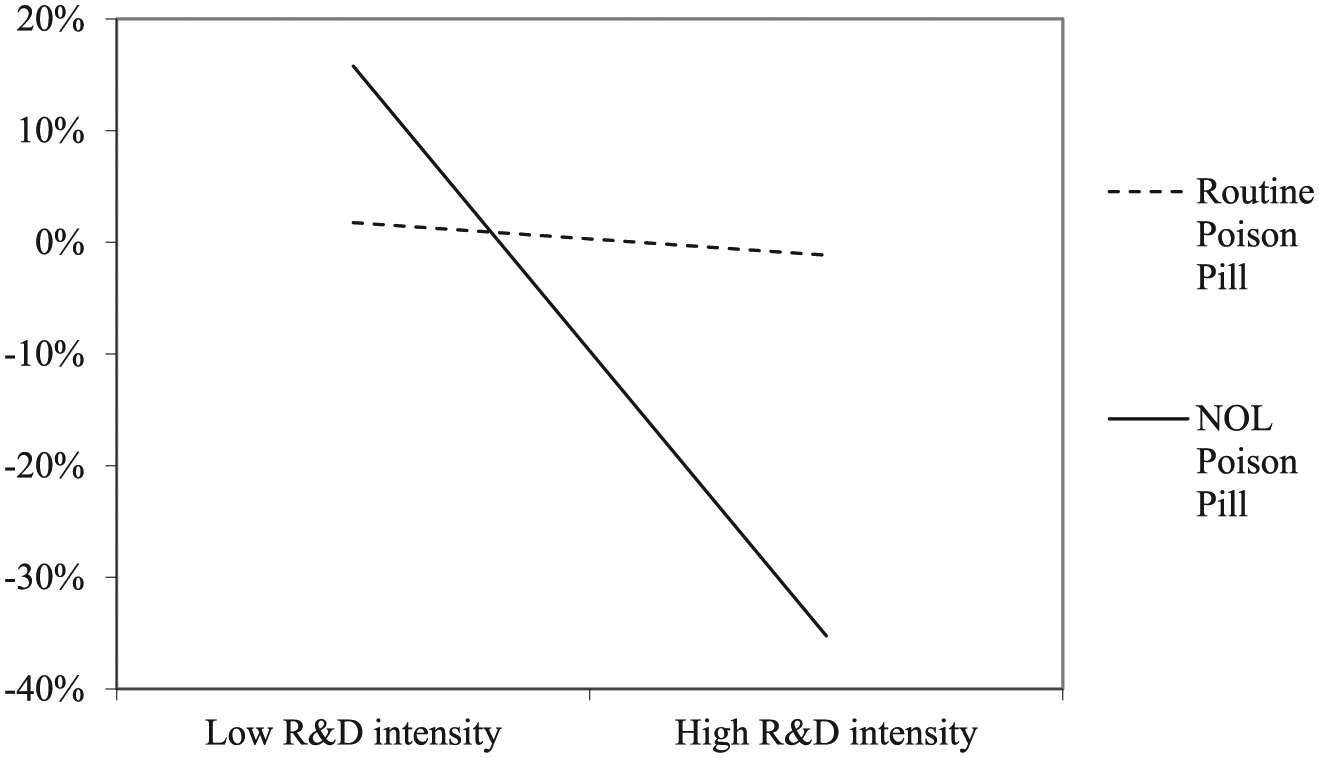

Interaction Between Net Operating Loss Poison Pill and R&D Intensity (Hypothesis 4a)

Interaction Between In-Play Poison Pill and R&D Intensity (Hypothesis 4b)

Interaction Between In-Play Poison Pill and Industry Concentration (Hypothesis 4d)

In terms of strategic context, Figure 3 shows the negative effects of NOL poison pill adoption when there is high R&D intensity. These effects are particularly strong for NOL poison pills; however, for routine poison pill adoptions, the level of a firm’s R&D intensity does not make a difference. Figure 4 shows the moderating effects of R&D intensity on the relationship between in-play poison pills and CARs. Investors more favorably react to in-play poison pills if the firm has a high level of R&D investments. In Figure 5, under high industry concentration, investors react positively for in-play poison pills, but this pattern is not observed for routine poison pills. In totality, these figures suggest that salient cues related to a firm’s governance and strategic context influence investor responses to specific-purpose poison pills, but not routine poison pills, such that context cues are particularly valuable to verify low-cost firm signals.

Supplemental Analyses

We conducted a number of supplemental analyses to examine the robustness of our findings. First, to control for time and industry effects on stock market reaction, we ran analyses using year and industry dummy variables. This analysis did not change the pattern of findings reported. We also tested hypotheses using alternative event windows including [−1, +2] and [−1, +3]. Our findings for Hypotheses 1, 2, 4a, 4b, and 4d are all confirmed across these event windows in magnitude, direction, and significance. Hypotheses 3b and 3d were consistent in magnitude and direction but were marginally significant (p ≤ .10) in the full models. Last, we conducted additional analyses for the first-stage Heckman selection model with alternative selection variables; however, results are not different from our reported ones.

Discussion

Signaling theory suggests that firms send signals to convey positive attributes. Seminal works on signaling theory (Akerlof, 1970; Spence, 1973) highlight the importance of signals in overcoming information asymmetries through communicating such attributes. The ability of signals to suggest intentions is based on the cost of the signal sent. However, firms may also undertake decisions that signal equivocal managerial intentions. In such cases, firms must actively manage the impressions of stakeholders to influence how they interpret the signal’s meaning. Little empirical research, however, focuses on the role of the receiver in interpreting equivocal signals. While early signaling theory suggests low-cost signals have little value (Akerlof, 1970; Spence, 1973), we suggest that such signals yield positive interpretations when considered with context cues that support positive aspects of the signal through sensemaking.

In this article, we examine firm decisions to adopt poison pills. Given that poison pills have mixed effects on stock market reaction and firm performance, we suggest that adoptions are equivocal signals regarding future management intentions. To reduce equivocality, firms adopt specific-purpose poison pills to signal positive intentions. However, receivers are left to interpret whether such signals indicate positive intentions or may be potentially harmful. In examining investor responses to poison pills as a signal of managerial intentions, we blend signaling theory with sensemaking to make several contributions to existing research.

First, we illustrate the importance of the receiver in interpreting equivocal signals. It is important to understand how receivers interpret and act upon signals that have multiple interpretations. Sensemaking is a process by which receivers interpret the firm’s decision, provide meaning, and act. Furthermore, we illustrate that when equivocality exists, receivers examine additional salient context cues to provide meaning for the decision. Context cues enhance the quality of the signal sent by firms and reduce uncertainty. Integrating sensemaking with signaling theory provides a theoretical lens through which to examine situations where investors receive signals in a manner inconsistent with how the firm frames such signals.

Furthermore, our findings also contribute at the intersection of research on sensemaking and signaling theory. While signaling theory assumes that signals are costly to generate and are usually transmitted unequivocally to receivers, signal receivers in the stock market consider additional cues when interpreting signals to increase coherence in developing an understanding of the signal’s intended meaning. Signals and cues are considered jointly to develop a more refined understanding and reduce ambiguity. Taking into account the signalee illustrates how declarations of intent regarding a poison pill’s purpose may be received positively when additional information exists that supports the signal provided. This extends the work of signaling theorists, such as Akerlof and Spence, by illustrating that low-cost signals may be valuable when prior decisions are consistent with the signal’s message.

Second, utilizing signaling theory allows us to contribute to research on antitakeover provisions. We show the growing adoption rate of specific-purpose poison pills as a means to attempt to reframe an equivocal signal to a positive signal by promoting positive managerial intentions. However, in utilizing theory on sensemaking, we illustrate why investors may accept or reject the firm’s signal that is positively framed. Our results suggest that specific-purpose poison pills evoke different reactions from investors than routine poison pill adoptions, indicating that it is important to understand the specific purpose for adopting the poison pill. In comparison to routine poison pills, the market more favorably responds to poison pills adopted when the firm is in receipt of a hostile takeover offer. For NOL poison pills, investors react negatively compared to routine poison pill adoptions, an action that is counter to management’s intentions in adopting the poison pill. Our theory and context illustrate means by which firms attempt to reduce information asymmetries regarding controversial decisions and the process by which investors are willing to accept or reject management’s explanations.

Third, we illustrate the role of context cues in investor evaluation of equivocal signals. We suggest that a firm’s governance and strategic contexts influence investors’ interpretation of equivocal signals. Our empirical results provide significant support for our hypotheses and suggest that these cues influence investors’ reactions to specific-purpose poison pills. With regard to in-play poison pills, such poison pills can be used to extract greater takeover premiums or to reduce the effectiveness of a takeover attempt, providing equivocality regarding managerial intentions. Consistent with sensemaking theory, our results indicate that the market interprets an in-play poison pill poorly when the board has weak oversight due to CEO duality. CEO duality allows the CEO to control the board’s agenda and limits the board’s effectiveness in monitoring.

Furthermore, a greater proportion of inside directors on the board is positively perceived by investors in case of an in-play poison pill adoption. Investors reward firms for adopting in-play poison pills when management is in a strong position to extract greater takeover premiums. Alternatively, investors could be punishing boards with a higher proportion of outside directors even more when adopting an in-play poison pill, counter to prior studies (Brickley et al., 1994; Sundaramurthy et al., 1997). As seen in Figures 1 and 2, our results illustrate that governance has a significant association with market reaction only in the case of in-play poison pills.

The lack of results for governance effects moderating the relationship between market reaction and NOL poison pill adoption is likely due to investors’ negative reaction to NOL poison pills (Sikes et al., 2014). An NOL poison pill may not be equivocal, leading to negative reactions by shareholders without additional cues. Alternatively, governance cues may be less informative when poison pills are adopted to protect prior tax losses. For instance, CEO duality could be harmful to future performance by entrenching ineffective managers, but it may also be beneficial in allowing unity of command, which improves decision making. As such, governance may not appropriately signal the intention behind NOL poison pill adoptions. Instead, information regarding why losses occurred may be particularly informative, as shown in the interactive effects between the firm’s R&D investments and reaction to NOL poison pill adoptions. This relationship is consistent with the recommendations of proxy advisory firms that oppose NOL poison pills (Deliso, 2009). It may be that in-play poison pills are truly equivocal in nature due to concerns about negotiating higher takeover premiums versus thwarting acquisition attempts, while investors perceive NOL poison pills directly as negative signals.

For the firm’s strategic context, we find a significant moderating effect of R&D intensity on both NOL and in-play poison pill adoption and CARs, while finding industry concentration influences responses to in-play poison pills. In particular, R&D investments result in an adverse effect of investor perceptions when an NOL poison pill is adopted, due to either a perception that R&D has failed or a belief that future R&D will be unsuccessful. Investors may desire to retain an effective market for corporate control to improve performance.

For in-play poison pills, the market responds more positively with higher R&D investment and industry concentration. Investors may perceive management as attempting to protect knowledge related to the firm’s innovation pipeline or an undervalued balance sheet. Investments may also signal intent to extract greater acquisition premiums. For high industry concentration, investors may positively perceive management’s intentions to extract greater premiums by improving bargaining power in an industry in which few options exist for acquirers. Thus, investors may perceive an in-play poison pill positively when they believe the likelihood of acquisition is high, but such an acquisition will result in greater investor premiums.

Practical and Theoretical Implications

Our results along with recent research on poison pill repeal (Schepker & Oh, 2013) suggest that changes have occurred with respect to antitakeover provisions. Firms are more nuanced in how they approach adopting such provisions and influence how these provisions are received. Specific-purpose poison pills allow firms to gain the benefits of poison pills while limiting concerns regarding managerial entrenchment. Practically, such changes suggest that managers adapt to changing environmental conditions to influence investor response. However, management must be attuned to shareholder perceptions of such adoptions. While management may intend to send positive signals, our results illustrate that in some cases these signals are received negatively. The market’s negative reaction may indicate it is safer for management to communicate with shareholders appropriately regarding the need to protect NOLs.

Furthermore, our results have practical implications as they suggest that investors seek additional contextual cues to interpret firm decisions. Firms must be aware of the cues sent through decisions such as long-term firm investments, composition of the board of directors, and the industries in which the firm competes. As investors seek to reduce information asymmetries, they will seek to identify cues that reduce equivocality regarding managerial motives.

Finally, our study has practical implications for investors. Given information asymmetries, investors must understand how changing business needs have led to the creation and adoption of new antitakeover provisions. Further, our results suggest that investors are considering these types of poison pills separately from routine poison pill adoptions and that contextual cues strongly play a role in influencing the evaluation of specific-purpose poison pill adoptions. Investors should continue to monitor managerial actions to understand and evaluate behaviors that are designed to send positive signals to fully understand managerial intentions. Investors should not always assume such intentions are neither positive nor negative.

Our results also provide theoretical implications. The firm-specific context of an event sends a strong cue to investors regarding intent of the firm’s actions. Managers must be aware that investors pay attention to not only their words (e.g., Rhee & Fiss, 2014) but also the context in which firms take actions. Furthermore, consideration of the signal’s receiver is also important to future research. While a litany of prior research focuses on positive signals, firm decisions are often equivocal in nature. Understanding how receivers interpret events can have important implications for impression management techniques firms may use. Our results suggest that positive framing alone is not enough to limit information asymmetries. Future research may further examine how receivers interpret both high-quality and low-quality signals when equivocality or negative information exists.

Researchers must also be aware of changes in corporate governance practices to understand how and why firms engage in new corporate governance strategies. In particular, it appears that changes in the regulatory environment and with economic troubles have led to firms’ adoption of new types of poison pills. Given that investors are naturally wary of management’s communication due to information asymmetries, future researchers should examine the role that publicly verifiable information sources play in influencing investor responses to firm decisions. Finally, examining additional variables that influence the perception of firm decision making could help understand how investors interpret managerial intent.

Limitations

Our study is also not without its limitations. First, we rely on publicly available information on poison pills. However, we do not have access to board deliberations for poison pill adoption, nor do we have process data on postadoption strategic decision making. Having access to such discussions may provide meaningful information regarding intent. Such data are not publicly available, and we call on future studies to focus on a smaller sample to draw inferences from process data.

Second, postadoption data related to negotiations with prospective acquirers or strategic investments undertaken to take advantage of NOL carryforwards could further inform managerial actions undertaken to realize economic benefit from specific-purpose poison pill adoption. Also, aggressiveness in the covenants of in-play poison pills could backfire, despite short-term positive stock market reactions. In other words, additional cues, such as the target firm’s profitability and synergies with potential acquirer’s resources, could influence investor response. Management’s need to extract higher premium could also lower the attractiveness of the firm. Thus, future studies can benefit from examining the long-term consequences of specific-purpose poison pill adoption using postadoption data.

Last, our measures of governance, while widely used, do not directly measure the nature and extent of board members’ involvement in governance. Instead, these proxies are meant to define the level of power between the board and CEO as well as the depth of knowledge regarding the firm’s true value among board members. Other influences among board members, including diversity, conflict, and team processes, may more strongly influence board decision making. We encourage future research to continue to delve deeper into understanding how board processes work in poison pill adoption decisions.

Conclusion

In conclusion, our study aims to contribute to research on corporate governance, poison pills, and investor reactions by illustrating the role that governance context, R&D investments, and industry concentration play in the market’s response to specific-purpose poison pill adoptions. Our study illustrates how advances in corporate governance relating to specific-purpose poison pills in response to changing regulatory environments require further attention from researchers, as they elicit different responses depending on the purpose identified.

Footnotes

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright. The authors would like to thank Yasemin Kor for her helpful comments to develop this article. We also gratefully acknowledge John Laide for data provided by FactSet SharkRepellent from FactSet Research Systems, Inc., as well as research support provided by the Haskayne School of Business at the University of Calgary.