Abstract

We examine how controlling owners’ family considerations affect their new industry entry decisions in family business groups in emerging economies. Drawing on the socioemotional wealth (SEW) approach, we conceive the new industry entry decision as controlling owners’ response to pursue various family interests. In particular, we distinguish two aspects of SEW, focused SEW and broad SEW, and theorize their opposing effects on the new industry entry decision. We propose that controlling owners’ likelihood to pursue new industry entry is negatively influenced by the exercise of family influence (a representative of the focused SEW) but is positively associated with the succession of family dynasty (a typical form of the broad SEW). Furthermore, we argue that the effects of SEW preservation on such decisions are contingent on controlling owners’ generation, with the effects to be stronger when the founder generation is in control. We test these hypotheses with a sample of Taiwanese family business groups and find general support for our predictions.

Keywords

Introduction

New industry entry is a key growth strategy pursued by business groups in emerging economies (Carney, Gedajlovic, Heugens, Van Essen, & Van Oosterhout, 2011; Khanna & Palepu, 1997). Previous studies examined such entries from the institutional environment perspective, such as market imperfection (Khanna & Palepu, 2000) and government intervention (Carney, 2008); and from the resource-based view of the firm, such as having access to labor, capital, and market (Guillen, 2000). What remains less understood is the role of the family in the decision making of new industry entry. This gap is significant given that families dominate the ownership and control of business groups in most emerging economies (Bertrand, Johnson, Samphantharak, & Schoar, 2008; Gedajlovic, Carney, Chrisman, & Kellermanns, 2012). Previous research found that family involvement has important implications on business group strategies, such as innovation (Hsieh, Yeh, & Chen, 2010) and internationalization (Chung, 2008). We intend to fill this gap by investigating how family involvement in group management affects the group’s new industry entry strategy.

Recent research in family businesses has highlighted socioemotional wealth (SEW) in explaining controlling owners’ strategic decision making (e.g., Berrone, Cruz, Gomez-Mejia, & Larraza-Kintana, 2010; Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson, & Moyano-Fuentes, 2007). According to the SEW approach, controlling owners of family businesses have distinct priorities and agendas compared with their nonfamily counterparts. Controlling owners are generally motivated by and committed to the preservation of their SEW, which is defined as the “non-financial aspects of the firm that meet the family’s affective needs” (Gomez-Mejia et al., 2007: 106). Controlling owners tend to use the gains or losses of SEW, rather than pure profitability, as a reference point when making strategic decisions (Berrone et al., 2010; Gomez-Mejia, Cruz, Berrone, & Castro, 2011).

Although the SEW approach provides important insights, the theoretical argument and empirical evidence on its role in controlling owners’ diversification decisions have been mixed. Some scholars posited that controlling owners of family businesses are less likely to diversify to avoid the loss of family influence, as diversification generally requires the involvement of nonfamily managers to oversee multiple business lines (Gomez-Mejia, Makri, & Kintana, 2010). As a trade-off, controlling owners are willing to bear the risks of concentration in a specific business (or sector) (Anderson & Reeb, 2003; Jones, Makri, & Gomez-Mejia, 2008). However, there is “an incentive for family business owners to diversify their personal investment portfolio by diversifying the business portfolio of the firm” (Miller, Le Breton-Miller, & Lester, 2010: 204-205). As controlling owners are exposed to the risks of holding a concentrated stake in the business, they are motivated to pursue risk reduction strategies, such as moving into different industries, to preserve the family assets (Kim, Kandemir, & Cavusgil, 2004; Zheng, 2002).

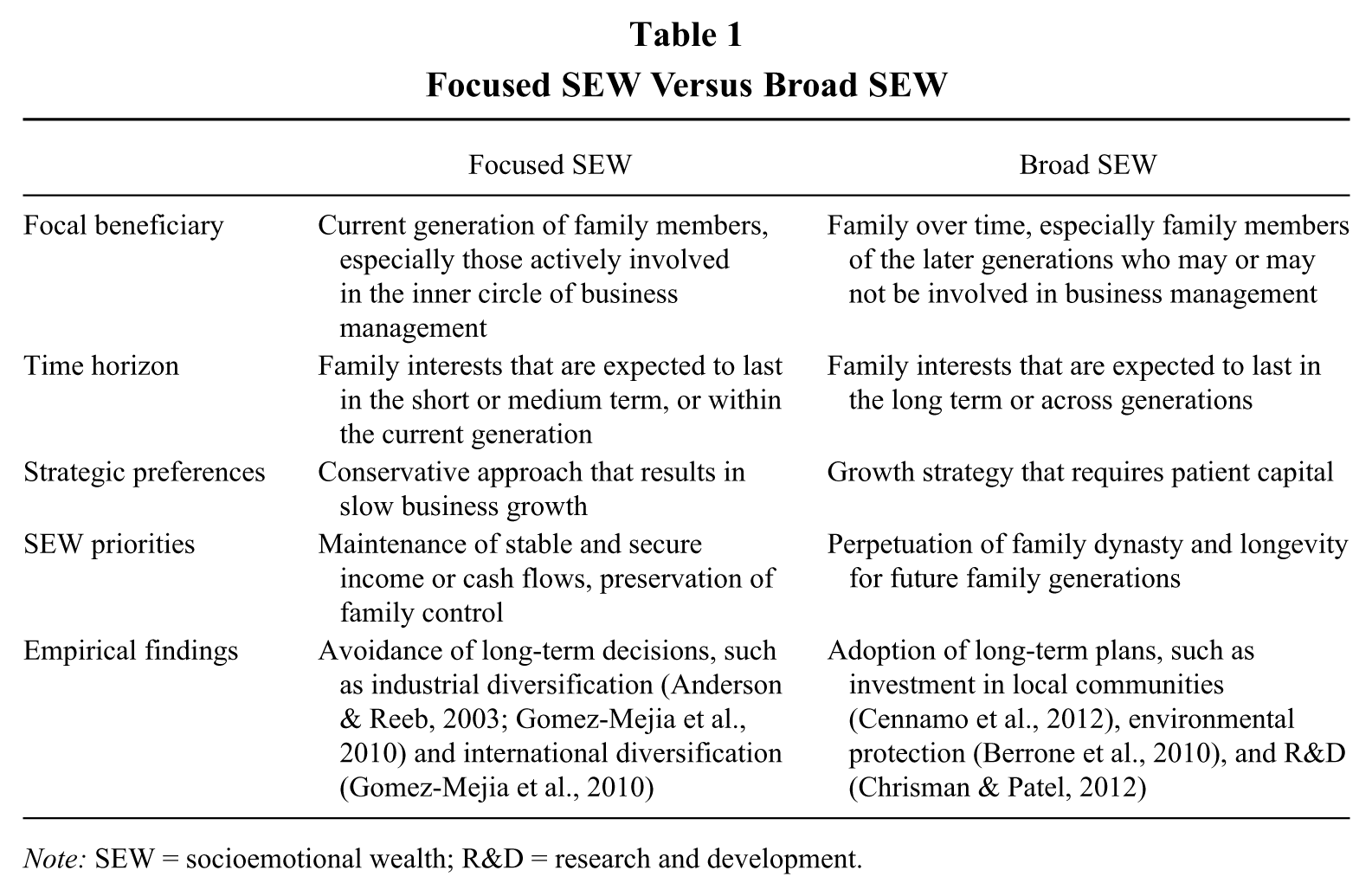

Two plausible reasons account for these inconclusive findings. First, previous research usually compared family firms with their nonfamily counterparts and assumed that family businesses are a homogeneous organizational form. Studies drawing on the SEW approach further assume that SEW is an identical goal that shapes controlling owners’ strategic preferences and generally overlook the complex variations among family businesses. This assumption is inconsistent with the fact that the SEW approach is an all-encompassing approach and “comes in a variety of related forms” (Gomez-Mejia et al., 2007: 108), such as family control and influence, renewal of family through succession, satisfaction of needs for belonging and intimacy, and conservation of social capital (Berrone, Cruz, & Gomez-Mejia, 2012; Gomez-Mejia et al., 2007). Different forms of SEW represent controlling owners’ distinct affective needs. Certain forms of SEW may shape the frame of reference to be favorable to the pursuit of diversification, whereas others may lead to the opposite direction. Second, affective attachment to the family businesses, defined as the degree of emotional bond the controlling owners feel for their family enterprises, forms the cognitive backdrop to the SEW pursuits and indirectly guides strategic decisions (Baumeister, Vohs, DeWall, & Zhang, 2007). However, there have been few systematic investigations into the effect of affective attachment among controlling owners. Given that controlling owners’ tendency to use SEW as the primary reference in their decision making depends on the levels of their emotional bond with the family businesses, it is important to consider the moderating effect of affective attachment in order to fully capture the heterogeneity of new industry entry decisions in family businesses.

In the present study, we distinguish two SEW aspects and demonstrate their contrasting effects on controlling families’ tendency to pursue new industry entry: focused SEW and broad SEW. Although both the focused and the broad SEW are associated with nonfinancial and family-centric goals, they differ in terms of the scope of the beneficiaries and the time horizon. The focused SEW emphasizes the welfare of a restricted group of family members who are actively involved in the business management with a temporary timeline. Conversely, the broad SEW is concerned about the interests of an extended group of family members in a longer time horizon with a futuristic orientation. We argue that the different emphases between the focused SEW and the broad SEW differently affect controlling owners’ evaluations of investment opportunities. In particular, we perceive the exercise of family influence as a form of the focused SEW and the succession of family dynasty as a form of the broad SEW. The exercise of family influence refers to the goal of family members to retain control over strategic decisions (Berrone et al., 2012; Gomez-Mejia et al., 2007). Family influence is typically associated with “a dominant family coalition” that serves in the inner circle of business management, such as a CEO or chairman of the board (Berrone et al., 2012: 262). In comparison, the succession of family dynasty refers to the goal to achieve a smooth transition of the family businesses to future generations (Berrone et al., 2012; Cennamo, Berrone, Cruz, & Gomez-Mejia, 2012; Gomez-Mejia et al., 2007). Family dynasty succession involves a larger group of family members who may or may not be involved in the business management and is usually associated with long-term strategic investment that can be bequeathed to multigeneration descendants (Sirmon & Hitt, 2003).

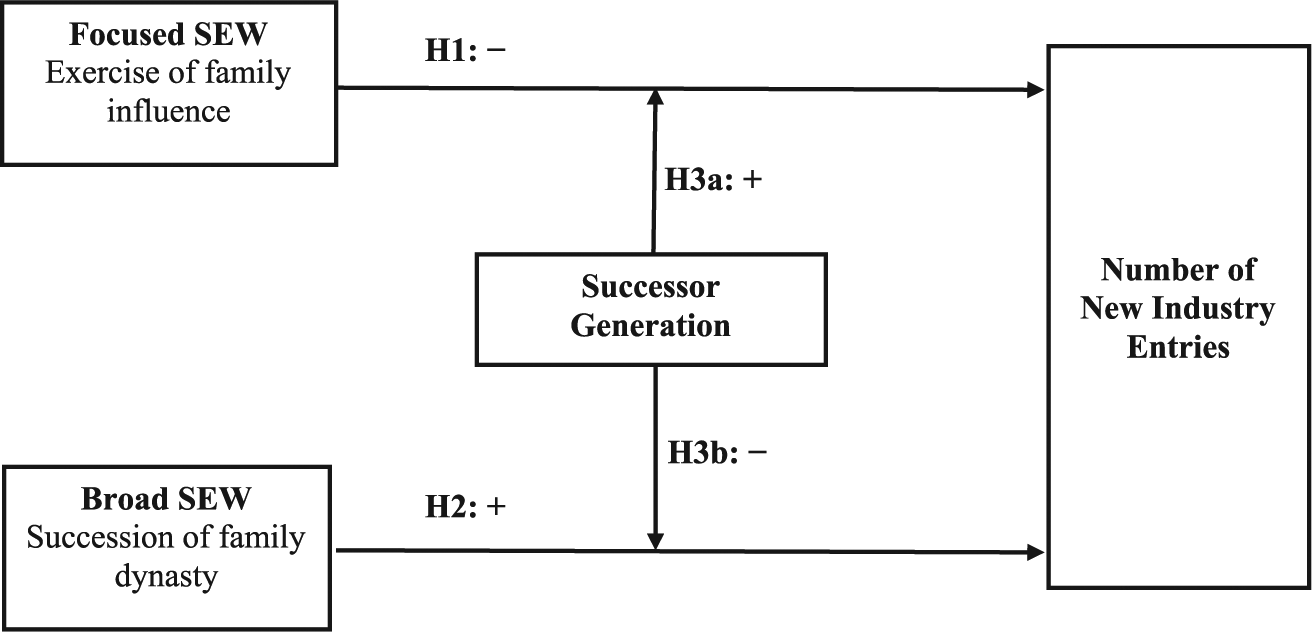

We theorize and demonstrate that controlling owners are likely to reduce new industry entries to exercise their family influence but do the opposite to resolve the challenge of family dynasty succession. In addition, we propose that the aforementioned relationships are contingent on the controlling owners’ generation, which differs in terms of their affective attachment to the family businesses. The effects of the exercise of family influence and the succession of family dynasty on diversification decisions are likely to be stronger for the founder generation than for the successor generation. Refer to Figure 1 for an integrative model of our hypotheses.

Effect of SEW on the Number of New Industry Entries

We use a sample of Taiwanese business groups, defined as a collection of legally independent firms bound together through persistent formal (e.g., equity) and informal (e.g., family) ties (Granovetter, 1995), from 1980 to 2000 to test our argument. Overall, our argument and hypotheses receive empirical supports.

The present study makes several contributions. First, we fine-tune the SEW approach by sharpening the causal relationship between various SEW motives and its behavioral consequences. Despite the common interests of preserving SEW, controlling owners’ strategic preferences can vary, depending on their prioritization of the different SEW aspects and on their generation. By showing the opposing effects of the focused SEW (through the exercise of family influence) and the broad SEW (through the succession of family dynasty), we offer a fine-grained SEW approach. The proposed SEW approach helps address the concern of the single-dimensional and “oversimplified” SEW construct in previous research (Berrone et al., 2012) and reconcile the mixed findings on diversified entry strategies in family businesses. Such a fine-grained approach also contributes to the general family business literature. A recent review of family firm research indicated that the decision-making time horizon of family executives is a critical determinant of the firms’ strategy, but “there has been relatively little research on its firm-level antecedents” (Gedajlovic et al., 2012: 1030). In this study, we theorize and demonstrate how the orientations of long-term versus short-term time horizons are linked to the different socioemotional needs of the family and exert contrasting effects on the family firms’ diversified entry decisions.

Second, we integrate cognitive psychology in the study of new industry entry, a central topic in strategic management literature. Strategy scholarship has relied on explanatory mechanisms such as market equilibrium and efficiency and has overlooked the reality of cognition and emotion in the practice of executive judgment (Denrell, Fang, & Winter, 2003). By showing how affective attachment differs between generations and moderates the effects of SEW aspects on new industry entry decisions, we respond to the recent call to “go beyond cognitive biases to produce useful frameworks that integrate psychology and strategy practice” (Powell, Lovallo, & Fox, 2011: 1370).

Third, new market entry in business groups has been considered a result of market inefficiency (Khanna & Palepu, 1997), government intervention (Carney, 2008), and generic resources and capabilities (Guillen, 2000). By examining the role of the family in new industry entry, the present study advances the understanding of the emergence, evolution, and persistence of business groups in emerging economies (Khanna & Yafeh, 2007).

Theory and Hypotheses

Organizations with family involvement have been documented to have different priorities and agenda compared with nonfamily businesses. Controlling owners are likely to serve family interests and cater to family value, identity, and social status in strategic decision making. This tendency generates loyalty and commitment among family members (Schulze, Lubatkin, Dino, & Buchholtz, 2001). Gomez-Mejia and his coauthors (2007) labeled these priorities as SEW. They proposed that controlling owners use SEW preservation or enhancement as a key criterion during the decision-making process, such as executive compensation (Gomez-Mejia, Larraza-Kintana, & Makri, 2003), composition of top management teams (Cruz, Gomez-Mejia, & Becerra, 2010), corporate social responsibility (Berrone et al., 2010), and CEO succession (Minichilli, Nordqvist, Corbetta, & Amore, 2014).

Although insightful, SEW is an all-encompassing construct that includes multiple forms of affective needs. Certain forms of SEW emphasize benefits that mainly concern a restricted group of family members and last within a relatively short time frame. We refer to these priorities as the focused SEW. The focused SEW may include securing careers for family members who are in the inner circle of business management, preserving their dominant control and influence, and achieving sustainable cash flows in the family business (Naldi, Cennamo, Corbetta, & Gomez-Mejia, 2013). When the focused SEW is used as the primary reference in decision making, controlling owners are likely to adopt a conservative investment approach. For example, controlling owners are inclined to avoid uncertain and long-term investments, such as corporate diversification and internationalization (Anderson & Reeb, 2003; Chrisman, Chua, & Sharma, 1997; Gomez-Mejia et al., 2010), as these may cause more potential losses, take longer time to pay off, deprive the family of a current stable income, and, more importantly, risk the family members’ control of the business (Miller, Le Breton-Miller, & Lester, 2011). Instead, controlling owners are more committed to maintaining the status quo of family control and constraining the influences from outsiders who are necessary to the diversification pursuit.

In comparison, other forms of SEW mainly concern the affective needs of a larger pool of family members that can be sustained for an extended time frame with futuristic orientations. We refer to such other forms as the broad SEW. The broad SEW may include the perpetuation of a family dynasty, preservation of family identity and status, maintenance of transgenerational sustainability, and conservation of family social capital (Arregle, Hitt, Sirmon, & Very, 2007; Berrone et al., 2010). To achieve the broad SEW objectives, controlling owners are likely to pursue growth strategies with an extended time frame (Gedajlovic et al., 2012). For example, to perpetuate the family legacy over generations, controlling owners are likely to exhibit a high level of corporate social responsibility. They are willing to respond to demands of environmental preservation (Berrone et al., 2010) or invest in communities where the family businesses are embedded (Cennamo et al., 2012). To ensure sustainable dynastic succession, controlling owners are motivated to pursue a “generational investment strategy that creates patient capital (i.e. financial capital invested without threat of liquidation for long periods)” (Sirmon and Hitt, 2003: 343), such as investments in research and development (R&D) and innovations (Chrisman & Patel, 2012). Table 1 summarizes the key differences between the focused SEW and the broad SEW.

Focused SEW Versus Broad SEW

Note: SEW = socioemotional wealth; R&D = research and development.

The differences between the focused and the broad SEW reflect the multidimensional nature of controlling owners’ affective endowments and the importance of using “more direct, multifaceted, and finer-grained measures of SEW” (Miller & Le Breton-Miller, 2014: 718). We attempt to do so by considering the exercise of family influence as a form of the focused SEW and the succession of family dynasty as a form of the broad SEW. The exercise of family influence is one of the most commonly applied frames of reference in the pursuit of family interests (Gomez-Mejia et al., 2007; Naldi et al., 2013). It emphasizes controlling owners’ direct or indirect control and is usually associated with the family’s representation in ownership, top management, and board (Bertrand et al., 2008). The exercise of family influence indicates the power, discretion, and status of controlling owners and their dominant family coalition within the organization. By contrast, the succession of family dynasty refers to the transition of the family businesses to future generations. It has been considered “a key goal for family firms” (Berrone et al., 2012: 264) and reflects controlling owners’ transgenerational intention toward long-term perpetuation (Chrisman, Chua, Pearson, & Barnett, 2012). As the succession of family dynasty becomes more complex and challenging, controlling owners are more likely to perceive the future benefits for the family as a priority and use it as a primary reference point in their decision making. Drawing on the context of family business group, we elaborate in the next section how these two SEW dimensions shape the priorities of controlling owners and lead to distinct new industry entry decisions and patterns.

In addition, we propose that the degree to which SEW is prioritized in the decision-making process is contingent on the controlling owners’ generation. According to previous research, controlling owners from different generations vary in terms of their affective attachment to the family business (Gomez-Mejia et al., 2007; Zellweger, Kellermanns, Chrisman, & Chua, 2012). Affective attachment gradually accumulates as family dynamics and business growth interact over time (Berrone et al., 2012). Affective attachment largely functions as an instructive feedback system, and its main direct effect is to stimulate cognitive processing, not behavior (Baumeister et al., 2007; Nifadkar, Tsui, & Ashforth, 2012). For example, Cardon, Wincent, Singh, and Drnovsek (2009) proposed that entrepreneurial passion influences the effectiveness of behavioral engagement by triggering the self-regulation cognition process directed toward the pursuit of entrepreneurial goal. Similarly, by stimulating controlling owners’ cognitive processing, affective attachment modifies controlling owners’ willingness to conform to familial norms or satisfy the family’s SEW needs (Chung & Luo, 2008a). In recent studies on family businesses, scholars have paid attention to the role of controlling owners’ affective attachment in influencing their management behaviors. Similar constructs, such as emotional capital (Sharma, 2004) and emotional value (Zellweger & Astrachan, 2008), have been proposed to capture the effects of affective attachment on family businesses. In the “Affective Attachment as a Contingency” section below, we argue how controlling owners’ affective attachment to family businesses varies across generations and how it modifies the relationships between the SEW pursuits and new industry entries.

Exercise of Family Influence and New Industry Entry in Family Business Groups

As a typical form of the focused SEW, the exercise of family influence is highly valued by controlling owners (Cennamo et al., 2012). The exercise of family influence usually concerns a small number of key family members (Berrone et al., 2012) and involves appointing the dominant family coalition to key managerial positions and maintaining their discretions over strategic decisions (Schulze, Lubatkin, & Dino, 2003b). The exercise of family influence can restrain controlling owners from incorporating outside executives (Gomez-Mejia et al., 2011) and expanding their business scopes (Berrone et al., 2010; Hoskisson, Johnson, Tihanyi, & White, 2005). We argue that the pursuit of family influence decreases controlling owners’ likelihood of entering new industries.

First, dominant family control in business groups can limit the organization’s reach for nonfamily managers who are key to the pursuit of industrial diversification. Chung (2006) argued that the social capital possessed by business group managers plays a critical role in the business group’s decision to enter a newly deregulated industry. Yabushita and Suehiro (2014) also pointed out the importance of hiring managers from outside when family business groups enter new businesses.

To maintain the dominant control of the group, the controlling family is likely to maintain a centralized management style and to be personally involved in both key decision making and daily operation (Chung & Luo, 2008b; Kim et al., 2004). Such domination and engagement reduce availability of the executive positions to nonfamily managers. The domination and engagement also discourage existing nonfamily managers because they are unlikely to reach the top management positions (Bertrand & Schoar, 2006). However, the talents and inputs of nonfamily managers are particularly valuable for the pursuit of new industry entry, which, by nature, deviates from the group’s existing businesses and requires knowledge, skills, and experience beyond the reach of the controlling family. The exclusion of nonfamily managers from the core management limits the family business groups’ capability to diversify (Hoskisson, Hitt, Johnson, & Grossman, 2002).

In addition to managerial knowledge and skills, another critical resource for new industry entry is capital that can be raised externally or internally (Chatterjee & Singh, 1999). Typically, external funds are raised through debt and equity financing. Family owners generally shy away from borrowing external funds because controlling owners perceive high leverage as high dependence on outsiders and escalated bankruptcy risks (Morck, Wolfenzon, & Yeung, 2005). Controlling owners “would be more reluctant to borrow funds to support an active diversification program” (Gomez-Mejia et al., 2010: 227). As to equity financing, controlling owners usually need to concede certain ownership and control to outsiders, such as institutional investors. The presence of such external owners or board members is usually associated with a more independent governance structure that monitors and constrains the controlling family. For example, Desender, Aguilera, Crespi, and Garcia-Cestona (2013) found that firms with more nonexecutive board members are more likely to engage external auditors to monitor the management. Such a structure may also enforce accounting, financial, and human resource practices that minimize controlling owners’ prerogative (Arikan & Capron, 2010). Therefore, external financing constrains controlling owners (Gomez-Mejia et al., 2010) and may lead to goal conflicts between outsiders and the controlling family (Schulze et al., 2001).

Internal financing, which builds on the intragroup capital market, is another source of funding that can support new industry entry of family business groups (Gomez-Mejia et al., 2010). Previous research documented the pyramidal structure as a common structure of intragroup capital market. Pyramidal structure refers to a chain of ownership relationship in which the family directly controls several group firms, each of which controls yet more group firms, and so forth (Almeida & Wolfenzon, 2006). The pyramidal structure creates a wedge between controlling owners’ cash flow rights and control rights (La Porta, Lopez-De-Silanes, & Shleifer, 1999), which may enable controlling owners to finance new industry entry with resources tunneled from minority shareholders. Although controlling owners may encounter less control loss with this tunneling approach, they may not prefer this option because of its negative effects on family reputation and status. As market intermediaries (e.g., stock analysts and business media) and government regulations (e.g., protection laws for minority shareholders) gradually build up during institutional transition, the risks of tunneling substantially increase, making financing through intragroup tunneling less attractive (Morck et al., 2005).

In sum, controlling owners who consider the exercise of family influence—a form of the focused SEW—as a priority perceive high risks for the pursuit of new industry entry. They are concerned with the loss of their status quo, power, and control, and thus are reluctant to leverage nonfamily managerial talents and external financing. As a trade-off, they are likely to avoid new industry entry and choose to bear the risks of slow growth instead.

Hypothesis 1 (H1): There is a negative relationship between controlling owners’ family influence and the number of new industry entries in family business groups.

Succession of Family Dynasty and New Industry Entry in Family Business Groups

The succession of family dynasty refers to the goal of ensuring the smooth transition of family businesses to future generations (Berrone et al., 2012; Cennamo et al., 2012; Gomez-Mejia et al., 2007). It implies “a long-term investment horizon” that involves transgenerational continuity and represents a typical form of the broad SEW (Naldi et al., 2013). Although the succession of family dynasty is a common goal of controlling owners (Handler, 1994), its effects on their strategic decisions may vary according to the level of complexity that controlling owners encounter during the succession process. When a larger number of family members are involved in the business, more potential conflicts and a greater challenge in achieving a smooth succession are expected. This challenge prompts controlling owners to apply family dynasty succession as the primary frame of reference in their decision making and to prioritize the strategic choices, such as new industry entry, that can reduce family tension and conflicts in the succession process.

First, as the number of family members increases and more people become involved in the distribution of family assets (Bertrand & Schoar, 2006), family dynasty succession becomes a greater and more complex challenge. Family members are more likely to form coalitions and raise conflicts among one another because of their different objectives and goals (Cennamo et al., 2012). These conflicts are particularly salient in the context in which the rule of equal inheritance of family assets applies (Bertrand & Schoar, 2006). The rule of equal inheritance considers each household (jia) as a basic unit of the kinship system. All children of each household, in some cases all sons (chuan nan bu chuan nu), receive equal shares of the family assets (fen jia) after the father passes away (Wong, 1985). Wang You-theng, a Taiwanese tycoon, once said, “If one family member gets a Mercedes-Benz, I will make sure every other family member will also have one” (Wealth Magazine, 1991). Compared with a system in which the eldest child takes the reign, the institution of equal inheritance induces more complexities and conflicts.

The escalated conflicts within the family can be detrimental to the longevity of family business (LaRocca & De Feis, 2015). New industry entry can be a solution that resolves the challenges of family dynasty succession. It carves out a specific business sector for each of the entitled children, satisfies their needs for autonomy, and thus reduces conflicts and facilitates harmony in the controlling family (McMullen & Warnick, 2015). According to a founder of a Taiwanese business group,

In 1970s, I found all my sons became mature. If all of them joined the same business, it would be risky and conflicts would be inevitable. I therefore diversified our business to different areas. For instance, since my eldest son has good connections and experience in semiconductor production, I went into this field and made him responsible for it. My second son has an interest in button production and he was then assigned to take charge of this area. My third and fourth sons lead the property investment firm. Each son has his own territory. (Zheng, 2002: 305-306)

Second, new industry entry creates a learning platform and provides career opportunities for descendants. The descendants, especially those who are novice to the family businesses, are able to enhance their management skills without impairing the core business (Miller et al., 2010). In addition, they can be better prepared for the succession by establishing their leadership and enhancing their status in their respective organization. As pointed out by the founder of Veronesi Group, one of the top players in the food industry in Italy, the purpose of diversifying into the financial sector is “to enhance the succession process by giving shares to all my five children and in particular an increasing responsibility to the three males, who were actively involved in the business” (Lassini & Salvato, 2010: 74).

Taken together, the larger the number of family members, the more complex the challenge of achieving a smooth family dynasty succession to the controlling owners. To reduce intrafamily conflicts and ensure a smooth succession, controlling owners are likely to favor the diversified entry strategy. By doing so, they are better able to prepare for the division of family assets, hone the management skills of descendants, protect the descendants from fighting against each other, and ultimately enhance the longevity of the family business. Therefore, we propose the following:

Hypothesis 2 (H2): There is a positive relationship between controlling owners’ number of family members and the number of new industry entries in family business groups.

Affective Attachment as a Contingency

Although the focused and the broad SEW dimensions may have distinct effects on new industry entry, their strength may rely on the affective attachment of decision makers to the family business. In this section, we argue that the level of affective attachment varies according to the generations of controlling owners. Controlling owners’ generation represents different stages of the life cycle of the family and the business. While the founder generation may wish to maintain a robust and coherent business and pass it to future generations, the successor generation may prefer a different career path or enjoy the achieved wealth and status (Miller & Le Breton-Miller, 2014).

Compared with the successor generation, the effects of both the focused and the broad SEW on the level of new industry entries are stronger when the controlling owners are the founder generation than when they are not. Founder-generation controlling owners are strongly attached to the family business because it usually reflects their lifelong adventure and endeavor, bears their own names, and involves their personal investments (Le Breton- Miller, Miller, & Lester, 2010). Their affective attachment arises from and evolves through a history of shared experiences with family members and business partners (Berrone et al., 2012). To the founder generation, the family business represents a self-identity that connects them with “a desirable past self (e.g., memories), a present self (me now), or a future self (who I am becoming)” (Kleine, Kleine, & Allen, 1995: 328). They tend to monitor and influence organizational management and recognize a high cost associated with shutting down the business (Gomez-Mejia et al., 2007). They are generally committed to preserve the family interests and those of long-term employees who have followed the founder since the beginning and are treated as “pseudo family members” (Le Breton-Miller et al., 2010). With the same level of family influence, the founder generation is more likely to avoid hiring new employees and undertaking organizational restructuring to protect family members and loyal employees, and thus is less willing to enter new industries.

In comparison, the successor generation usually has not experienced the challenges and hard work during the start-up process and, thus, enjoys less privilege and status than the founder generation. Many of the successor generation may prefer to pursue personal interests and careers outside the family business. In the present research context, Taiwanese successors usually take over the family businesses because of filial piety, family tradition, or social pressure (Yu, Lin, & Chang, 2009). Therefore, the successors are less satisfied with the nature of their work or the level of their responsibility in the family businesses and are less motivated to be actively and personally involved in business management and control (Handler, 1990). Consistently, Gomez-Mejia et al. (2007) demonstrated that the successor generation is more willing to relinquish control of the family-owned olive oil mills in exchange for better financial performance. Therefore, the successors are less sensitive to the negative bearing of the new industry entry on family influence, and thus a weaker relationship exists between their pursuit of family influence and their tendency to enter new industries.

In sum, affective attachment serves as the trigger and booster for controlling owners’ cognitive processing directed toward strategic decisions (Baumeister et al., 2007; Cardon et al., 2009). With a lower degree of affective attachment to the family business, the successor generation is less inclined to conform to familial norms and place SEW as its primary frame of reference when making strategic decisions. The effects of the exercise of family influence on the level of diversified entries are weaker for the successor generation than for the founder generation.

Hypothesis 3a (H3a): The negative effects of controlling owners’ family influence on the number of new industry entries are weaker when the controlling owners are the successor generation than when they are the founder generation.

The founder generation’s strong affective attachment to the family business also increases the importance of family dynasty succession in the diversified entry decisions. To the founder generation, the family business is not only a financial source to provide for descendants but also an achievement of their lifetime endeavor. The successful transition of leadership demonstrates that the founder’s lifetime achievement will continue into the future generations and glorify himself or herself and the family name. The founder-generation controlling owners perceive a strong desire and obligation to sustain the family businesses and are likely to prefer strategies that reduce potential family conflicts and ensure smooth succession. They prefer to adopt a “paternalistic” management style characterized by concentrated management control, authoritarian hierarchy, and distrust of outsiders (Ansari, Goergen, & Mira, 2014).

By contrast, the successor-generation controlling owners are usually on a special track designed by the founder and take the crown at a relatively young age (Chung & Luo, 2008a). They commonly lack a close bond with and respect from existing business stakeholders (Le Breton-Miller et al., 2010). They also face constant power contests among siblings and other family members (Schulze et al., 2003b), especially when the practice of family dynasty succession follows the rule of equal inheritance (Chung & Luo, 2008a). As a result, members of the successor generation tend to be more concerned about their own welfare and utilities than those of their siblings (Schulze, Lubatkin, & Dino, 2003a). Consistently, the successor generation is more likely to employ formal human resource policies to ensure transparency and democracy in business management than the founder generation (Ansari et al., 2014). The successor generation is also more likely to dismiss family executives when the family business performs poorly (Gomez-Mejia, Nuñez-Nickel, & Gutierrez, 2001).

For these reasons, we expect that compared with the founder generation, the successor-generation controlling owners are less sensitive to the need to provide family assets and career opportunities to their family members during the family dynasty succession. The relationship between family dynasty succession and the level of diversified entry weakens under the leadership of the successor generation.

Hypothesis 3b (H3b): The positive effects of controlling owners’ number of family members on the number of new industry entries are weaker when the controlling owners are the successor generation than when they are the founder generation.

Method

Sample

Our research setting is the Taiwanese business groups from 1980 to 2000. 1 The sample was derived from the biennial directory Business Groups in Taiwan (BGT) compiled by China Credit Information Service, the oldest and the most prestigious credit rating agency in Taiwan and an affiliate of Standard & Poor in the United States. This directory provides financial and product information of the top 100 groups (in terms of sales) and controlling owners’ family background, such as the names of their spouses, siblings, and children, as well as their managerial positions (if any) in the groups. The BGT directory has been used in previous studies on business groups in Taiwan (e.g., Luo & Chung, 2005).

The initial sample contains 101 distinct business groups over the period of 20 years. The data are unbalanced as some groups were dropped when they did not satisfy the size criterion and others were added because they grew large enough. We excluded 18 business groups that did not have any family involvement in management positions, such as holding executive positions or board seats in any group firms. As we used lags for the independent and the control variables, we lost another three business groups that appeared at only one time point in our dataset. Thus, our final sample comprised 413 observations and 80 distinct family business groups. Each group had an average of 10.4 years of data (5.2 time points as the directory is published every two years).

Taiwanese business groups are an ideal context for this study for three reasons. First, Taiwanese business groups are typically featured with different diversification levels (Chang, 2006). In particular, new industry entry by establishing a new firm has been considered a driving force for business group formation (Khanna & Yafeh, 2007). The sufficient variation of new industry entry among business groups enables us to test the hypotheses.

Second, family involvement through ownership and control pervades business groups in Taiwan and plays a central role in shaping various strategic decisions (e.g., Bertrand et al., 2008). Hamilton and Biggart (1988) found that the top 100 largest business groups in Taiwan are subject to various degrees of family influence. This variation enables us to investigate the family influences on controlling owners’ diversified entry decisions.

Third, Taiwan experienced a significant market-oriented institutional transition from 1980 to 2000. Scholars estimate that Taiwan introduced more regulatory measures between 1988 and 1993 than in the previous two decades (Cheng & Chu, 2002). The changes include deregulation of monopolized industries, privatization of state enterprises, large-scale reductions of import control, and liberalization for foreign investment and financial market. The large-scale economic transformation is typical of emerging economies, thus making our findings generalizable to other similar contexts (Sachs & Warner, 1995).

Dependent Variable

Following prior research (Zhu & Chung, 2014), we measured the number of new industry entries by counting the number of entries into a new four-digit standard industrial classification (SIC) code that each family business group invested in each year. We identified the new industry entry in each group by manually surveying the development trajectories documented in the BGT directory. As the BGT directory has no ready-to-use industry coding, the industry code of each new industry entry was hand coded using the SIC scheme published by the Taiwanese government in 2006 (http://eng.stat.gov.tw/). 2 Two coders independently coded the industries with a consistency rate of .83. Business histories of the group firms were consulted to resolve the differences between the two coders.

Independent Variable

Previous literature emphasized the role of the board in controlling owners’ exercise of family influence (Dalton, Certo, & Roengpitya, 2003; Hoskisson et al., 2002). The board of directors is considered a vehicle to reinforce family influence and pursue family objectives (Gomez-Mejia et al., 2011). Following Chung and Luo (2008b), we measured the level of family influence by a factor score from two variables. The first variable, chair overlap, is measured by the Herfindahl Index:

We captured the variation in the pursuit of family dynasty succession with the number of family members of the controlling owner. A large number of family members entitled to family assets increases the conflicts and complexity in family dynasty successions (Bertrand & Schoar, 2006) which are likely to become the primary reference of controlling owners’ decision process of diversified entry. 3

The BGT directory asks business group firms to identify the most important decision maker in their group and generates a list of controlling owners. In addition, the BGT directory provides a photo and biographical description of each controlling owner. The controlling owner generally meets three conditions: (1) the person is the founder of the family business group or the family member of the founder, (2) the person is the largest shareholder of the core firm and other group firms, (3) the person usually serves as the board chairman of many group affiliates.

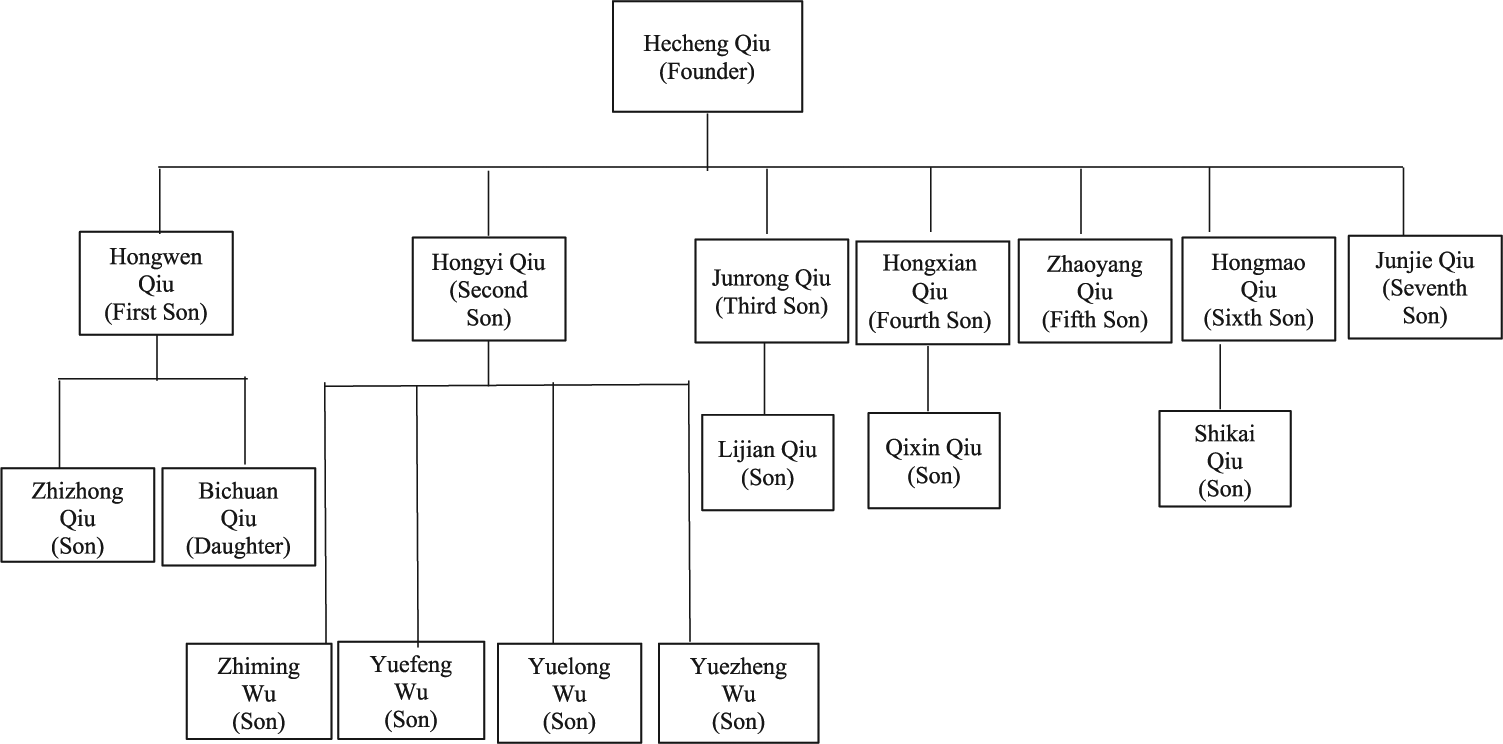

We followed the method applied by Bertrand et al. (2008) to capture controlling owners’ family size. We supplemented the family background data of the BGT directory by going through various local business magazines and newspapers, such as Wealth Magazine (1974-2000). We also referred to the group founders’ autobiographies and the monographs and dissertations devoted to this topic. We started coding the family data from the founder of each family business group. Afterward, we tracked all direct descendants of the founder generation up to the last generation that is currently active in business. We coded the founder generation as the first generation, the children of the founder generation as the successor generation, and so on. For all family members, we collected information on their gender, relationship with the controlling owner, and managerial positions (if any) in the family business group. Furthermore, we obtained information on the educational and business backgrounds of the controlling owner. We kept track of changes in the family business group members and their descendants over the years.

Figure 2 demonstrates a sample of a family tree published in the BGT directory. The Qiu family owns and manages the Hecheng Group, which is Taiwan’s leading manufacturer of bathroom fixtures, building materials, precision ceramics, and kitchen facilities. The family business started as a small pottery workshop in 1931. Hecheng Qiu was coded as the first generation in our data. He had seven sons and nine family members as the family reached the third generation. Shikai Qiu is now the controlling owner of the family business.

Qiu Family, Controlling Family of Hecheng Group

Generation is a dummy variable that equals 1 if the controlling owner is the founder of the business group and 2 otherwise (successor generation). As most of the Taiwanese business groups under investigation were founded after the 1950s, the majority of the groups are now under control by either the founders or the second-generation successors.

Control Variable

We included a set of variables that have been found to affect diversified entry decisions. We included two variables for controlling owners’ demographics: age of controlling owner and foreign education of controlling owner. The top management team literature has documented the critical role of controlling owners’ age and education in business decision making (Finkelstein & Hambrick, 1996). In particular, exposure to foreign education raises controlling owners’ awareness of organizational practices outside their primary institutional environment. Such an exposure may shape their perspectives on the approach to manage the business, such as diversification discount prevalent in American businesses (Chung & Luo, 2008a). We measured foreign education of controlling owner with a dummy variable, which equals 1 if the controlling owner has experienced foreign education and 0 otherwise. In most cases, foreign education is at the graduate level in American business schools.

We controlled for six group-level variables and one industry-level variable. Previous empirical studies demonstrated that group age affects group strategy partly because of the increased legitimacy and reliability, and partly because of the experience that business groups accumulate overtime (Carroll & Delacroix, 1982). We controlled for group age based on the year that the first group member firm was established. In addition, we controlled for group size using the log transformation of group assets.

Afterward, we included total diversification to control for the influences of the previous “stock” of diversification at the group level. We calculated total diversification using Palepu’s (1985) entropy measure:

We used return on asset (ROA) to gauge business group performance. ROA reflects the business groups’ efficiency in employing organizational assets and their profitability. ROA is equal to the sum of the net income of all group firms deflated by their total assets. Net incomes and assets that were cross-held between group firms were calculated only once to avoid double counting. Following previous studies (Chakrabarti, Singh, & Mahmood, 2007), we used the log transformation of ROA in the regression models. 4 Debt ratio indicates that the business groups’ financial conditions can shape new industry entry decision making. Debt ratio was calculated as the ratio of group debts to group net worth in percentage terms. In addition to tangible ones, we also controlled for intangible resources for new industry entry. Organizations with a larger stock of innovation are more likely to pursue new industry entry (Wu, 2013). Accordingly, we measured business groups’ innovation with a count of U.S. patents that family business groups were granted each year. The patent information was collected from the U.S. Patent Office Classification. U.S. patent is a valid measure for innovation as the United States is a highly desirable market in which firms around the world tend to file their most important innovations (Mahmood & Mitchell, 2004). The patent measure was log transformed to enhance normality.

Lastly, growth opportunities in an organization’s current industry affect its diversified entry decision into other sectors (Stowe & Xing, 2006). Accordingly, we first identified the industry of the core firm in each business group. Then, we calculated the average sales of each industry by aggregating all the core firms of all business groups and used the year-over-year growth rate in sales to capture industry growth (O’Brien, David, Yoshikawa, & Delios, 2014).

Analytic Model

The no. of new industry entry is a count measure that takes only nonnegative integer values. As the standard deviation of the no. of new industry entries is close to the mean and thus displays no signs of overdispersion, we used the Poisson model to address the discrete nature of the variable. We specified the Poisson regression model as

We used the fixed-effect model to account for within-group variations over time. The estimated coefficients are unbiased by the unobserved time-invariant heterogeneity among business groups (Greene, 2012). We used robust standard errors in all models to test our hypotheses.

A concern of our empirical examination is the potential endogeneity of controlling owners’ family influence, which could be affected by certain organizational and individual attributes related to information processing and coordination. For example, cross-shareholding and pyramid have been considered as two important control-enhancing mechanisms in business groups (La Porta et al., 1999; Masulis, Pham, & Zein, 2011). Cross-shareholding can be generated by share exchanges between two group firms, which may or may not involve the significant reallocation of internal capital (Masulis et al., 2011). Conversely, the pyramidal structure is an ownership arrangement in which a family controls several private and listed firms, each of which controls yet more other firms (Morck et al., 2005). Both cross-shareholding and the pyramidal structure help create a wedge between controlling owners’ control and cash flow rights. The wedge may amplify controlling owners’ influences within the group by enabling them to control a large number of group member firms in which the family has only limited cash-flow rights (Claessens, Djankov, & Lang, 2000; Morck et al., 2005). Controlling owners’ age can also affect their openness to board independence, the board’s monitoring of the controlling family, and eventually the family’s dominance in the organization’s decision-making process (Zajac & Westphal, 1996).

To address the potential endogeneity issue, we followed a two-stage procedure to capture the variations in controlling owners’ influences in family business groups that are exogenous to the aforementioned organizational and individual attributes (Wiersema & Zhang, 2013; Yu, 2008). First, we estimated family influence with a set of predictors, including cross-shareholding tie, pyramidal depth, and age of controlling owner. Cross-shareholding tie refers to the total number of ties through which two of the group firms exchange shares with each other. Pyramidal depth was measured with the largest number of vertical ownership links among firms within a family business group (Bertrand et al., 2008). Second, we used the residual from the first regression as the proxy for controlling owners’ family influence to test our hypotheses. The residual can be considered as a component of controlling owners’ family influence that is uncorrelated with the included predictors (Wiersema & Zhang, 2013). This approach removes the potential endogeneity between family influence and the factors that are likely to affect their dominance in the board.

Results

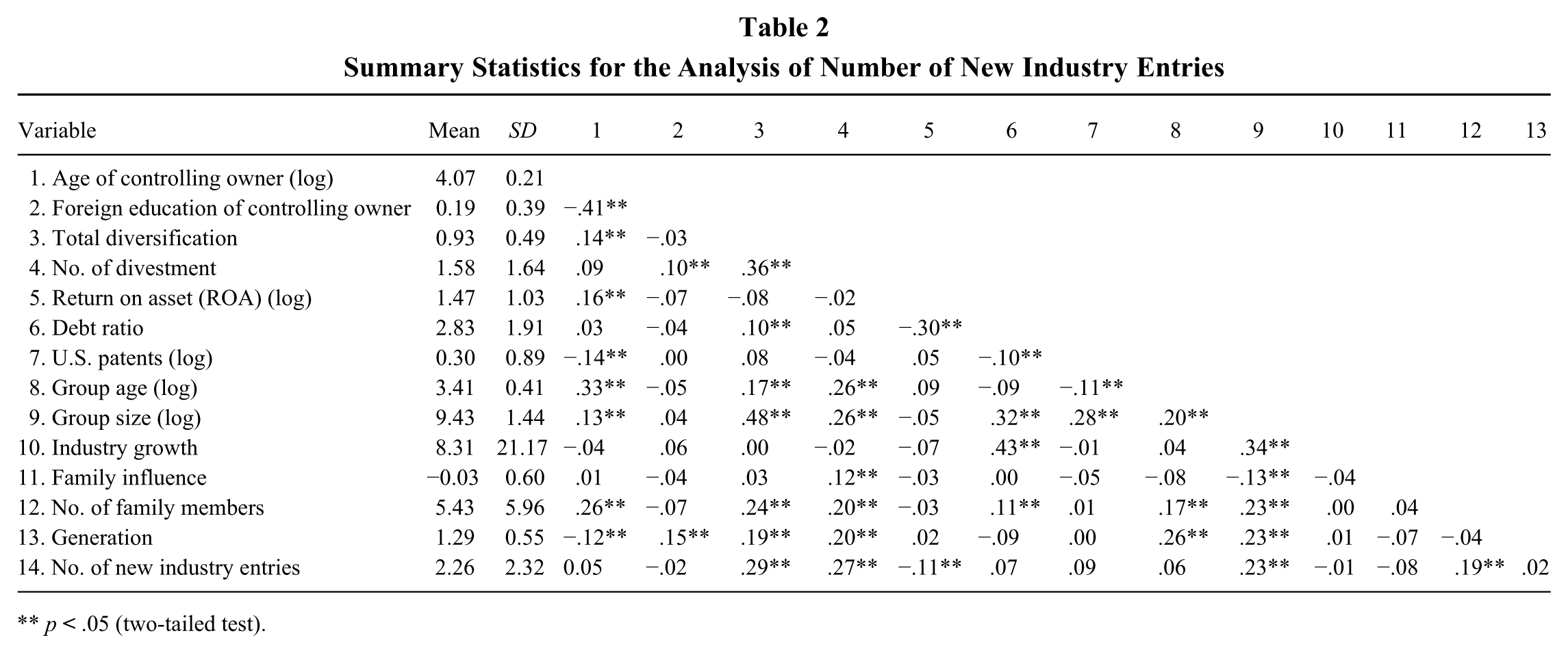

Table 2 reports the descriptive statistics of the variables included in the analyses. Our independent variables and control variables have no especially high correlations. To statistically test for the presence of multicollinearity, we checked the variance inflation factor (VIF) value. The VIF values of all independent and control variables range between 1.06 and 1.99, which suggest that multicollinearity is not likely a concern in the present study (Greene, 2012).

Summary Statistics for the Analysis of Number of New Industry Entries

p

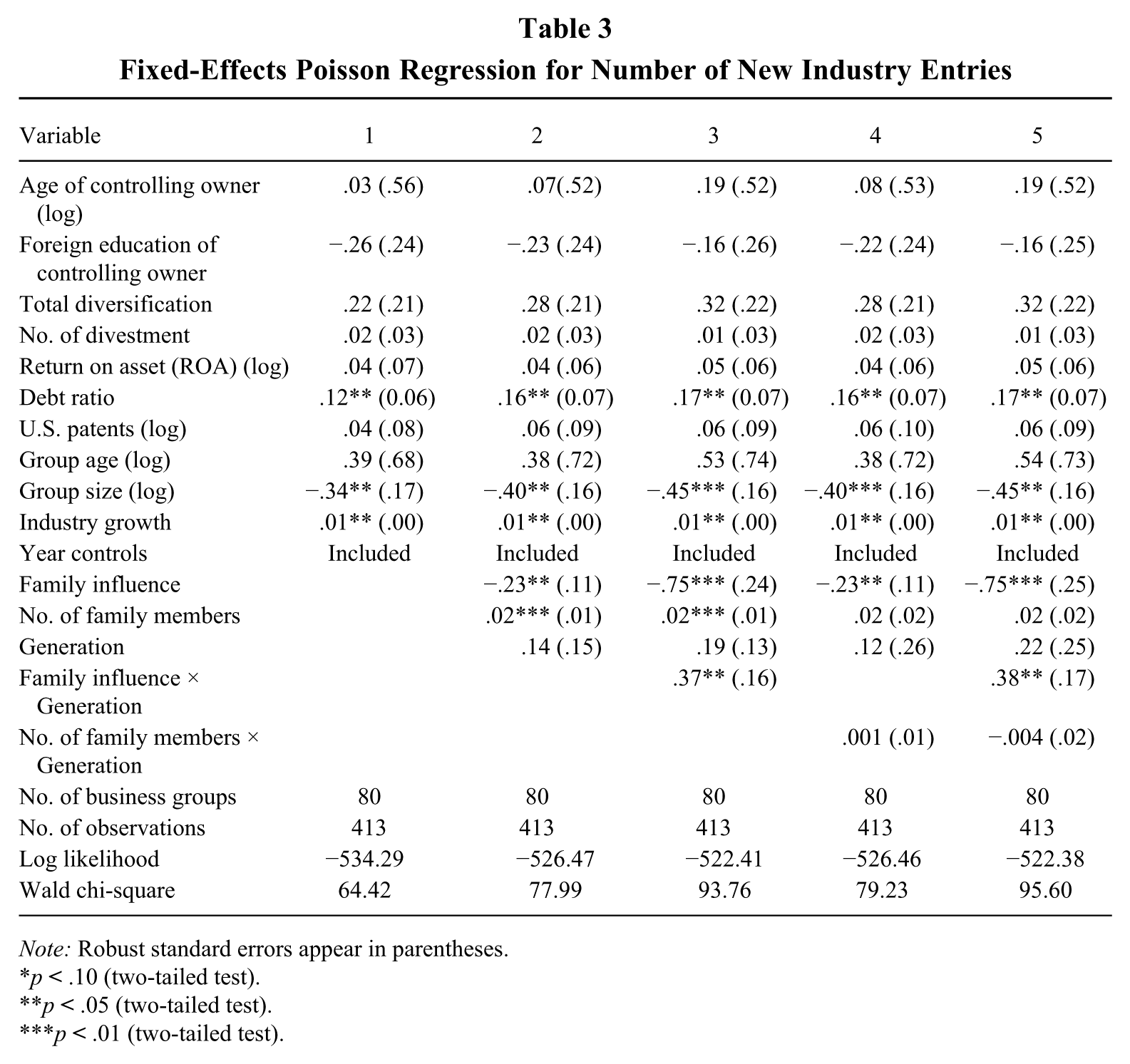

We presented the empirical testing results for the no. of new industry entries in Table 3. Model 1 is the base model with only the control variables. To observe the changes in the explanatory power, we sequentially added the independent variables and the interaction terms. We also conducted the likelihood ratio test to check for model improvement. Except for Model 4, the results show a statistically significant model improvement as we added the independent variables and the interactions in the regressions.

Fixed-Effects Poisson Regression for Number of New Industry Entries

Note: Robust standard errors appear in parentheses.

p

p

p

We propose that the exercise of family influence reduces the no. of new industry entries in H1. Consistent with our hypothesis, the coefficient of family influence is negative and significant in Model 2 (b = −.23, p < .05). H2 predicts that the succession of family dynasty will have a positive effect on the number of new industry entries. The positive coefficient of the no. of family members in Model 2 lends support to the hypothesis (b = .02, p < .01). H3a asserts a positive moderating effect of generation on the negative relationship between the family influence and the no. of new industry entries. The coefficients of the interactions in Models 3 (b = .37, p < .05) and 5 (b = .38, p < .05) are positive and significant. To facilitate the interpretation of the coefficients in a nonlinear model, we followed the simulation-based approach suggested by Zelner (2009), and used the intgph routine in Stata to graph the interaction. Figure 3 demonstrates the estimated relationship between the family influence and the no. of new industry entries with different generations of family leadership. As predicted, the negative slope of the family influence is steeper when the controlling owners are the founder generation. It indicates that the founder generation is more sensitive and reactive to the need of exercising family influences than the successor generation. The founder generation is more likely to reduce its diversified entries to preserve their SEW than the successor generation. Therefore, the results support H3a.

Number of New Industry Entries, Exercise of Family Influence and Generation

We propose that the positive effect of the no. of family members on the no. of new industry entries is mitigated by generation in H3b. The coefficients of the interactions in Models 4 (b = .001, p > .1) and 5 (b = −.004, p > .1) are insignificant, thus failing to support H3b. The insignificant finding is probably due to the lack of sufficient within-group cross-generation variations in the no. of family members. We have an average of 10.4 years of coverage for each family business group. This time span enables us to account for the family variations within business groups and their influences on controlling owners’ new industry entry decisions. However, the time span may not be long enough to fully capture the differences in family sizes within business groups that went through different generations of family leadership.

Robustness Check

We conducted a set of sensitivity tests to make sure that our results were robust. First, we used alternative measures for the dependent variable no. of new industry entries. We constructed the no. of two-digit new industry entries and the no. of three-digit new industry entries by calculating the number of new industry entries based on two-digit and three-digit SIC codes, respectively. We also changed the count measure of no. of new industry entries into a dummy variable. The measure was coded as 0 if the family business group did not pursue any four-digit new industry entries in the focal year and 1 otherwise. The results are similar to our findings.

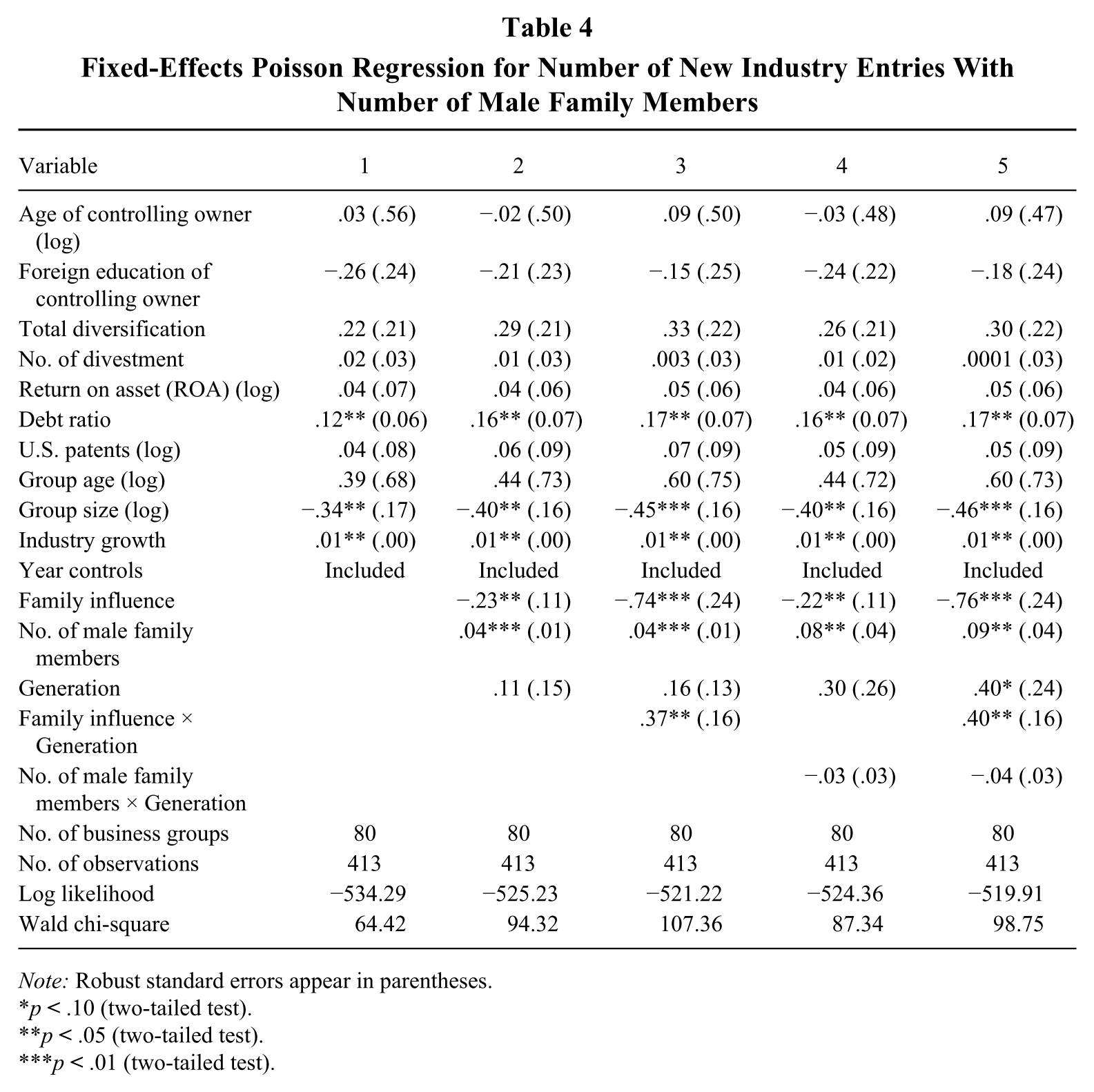

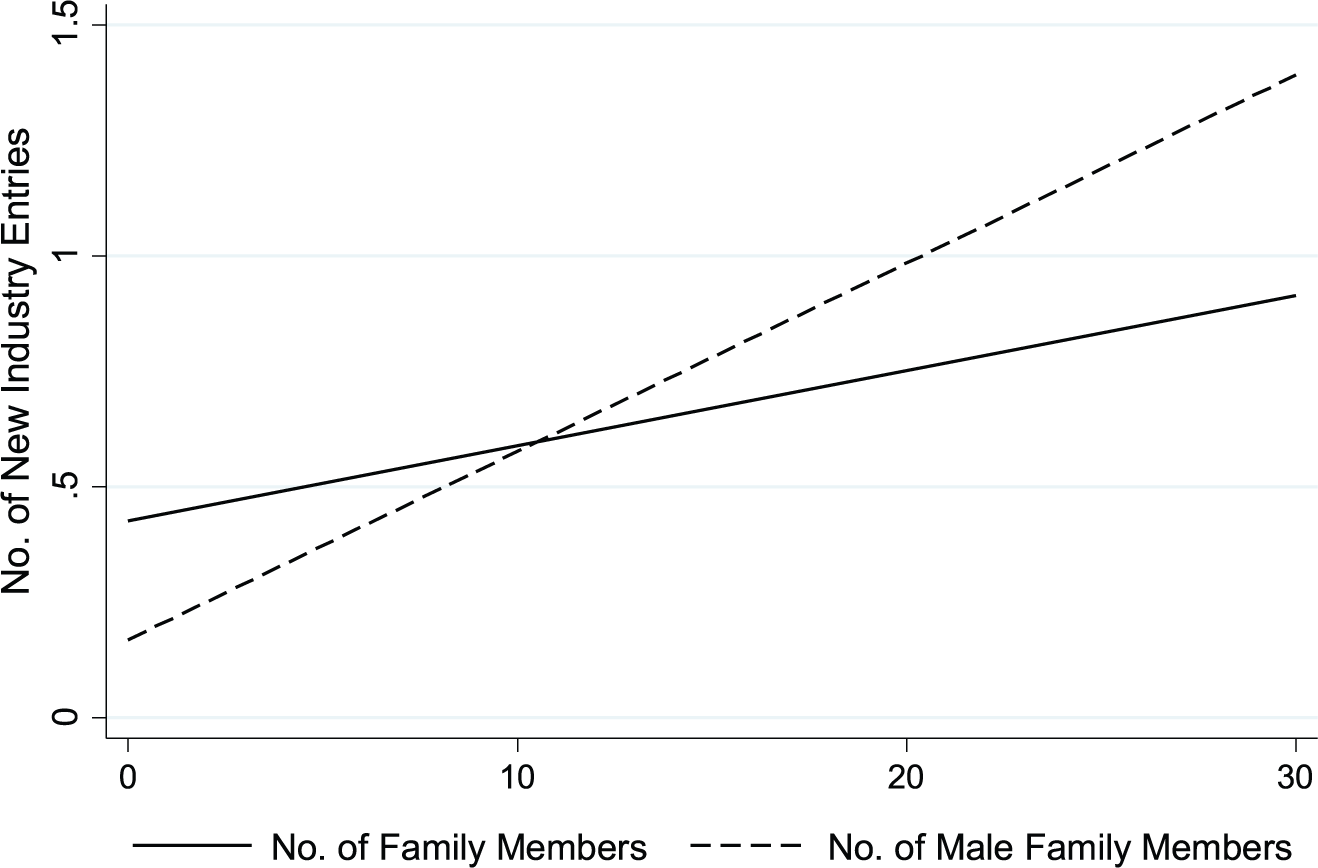

Second, we constructed the no. of male family members as an alternative measure for the no. of family members. This measure is the total number of male family members of the controlling owner, and can be considered as a subset of the no. of family members. Consistent with our hypotheses, the no. of male family members has a significant and positive effect on the no. of new industry entries (see Table 4). Moreover, we find that the coefficients of this alternative measure are consistently larger than those of the original measure (no. of family members) in all models. We plotted the effects of the no. of family members (based on Model 2 in Table 3) and the no. of male family members (based on Model 2 in Table 4) on the number of diversified entries. As shown in Figure 4, the slope of the no. of male family members is steeper than that of the no. of family members. The figure indicates that with every unit increase in the no. of male family members, controlling owners’ new industry entry decision will have greater change. This stronger effect of male family members on controlling owners’ diversified entry decision is consistent with the previous findings on the patrilineal preference in family business succession (Bertrand & Schoar, 2006). Male descendants impose high imperatives on controlling owners to resolve family conflicts and use family insiders to perpetuate the family dynasty, thus driving controlling owners to pursue new industry entries. This result further confirms our argument that the influence of SEW is not homogeneous and that it varies when controlling owners’ priorities are associated with different SEW aspects.

Fixed-Effects Poisson Regression for Number of New Industry Entries With Number of Male Family Members

Note: Robust standard errors appear in parentheses.

p

p

p

Number of New Industry Entries, Family Members, and Male Family Members

Third, we captured family influence with three alternative measures: the chair overlap calculated by the Herfindahl Index, the percentage of board chairmen held by the controlling family, and the family ownership at the group level (Chung & Luo, 2008b). The chair overlap calculated by the Herfindahl Index captures the level of family influences that is concentrated on one individual family member. The percentage of board chairmen reflects the aggregated influences of all family members who are involved in the group management. Family ownership at the group level was gauged by a weighted average (weighted by sales of the group firm as a percentage of total group sales) of family ownership in all group firms. Family ownership in each group firm is the percentage of shares owned by family members and other group firms controlled by the family. The results of all these alternative measures remain consistent with our findings.

Fourth, the no. of family members may be driven by business group performance or controlling owners’ demographics. For instance, the owner may think that he or she needs more descendants to prosper the business empire as the family business group progresses in both scale and scope. To address this endogeneity concern, we employed the two-stage procedure mentioned earlier (Wiersema & Zhang, 2013; Yu, 2008) that first regressed the no. of family members against a set of predictors (group age [log], group size [log], controlling owner’s age, foreign education, and generation) to generate residuals as a component of the no. of family members. Afterward, we used the residuals as a proxy for the no. of family members to predict the no. of new industry entries. This proxy is uncorrelated with the predictors included in the first stage and is considered exogenous to the attributes pertaining to the business groups and the controlling owners. The adjusted results correspond to the results reported in Table 3. Furthermore, the no. of family members may be influenced by the controlling owners’ generation or the family business groups’ sizes. To reduce the estimation bias, we first tested the effect of no. of family members in the subsamples divided by generation. Then, we tested our predictions in the subsamples divided on the basis of the group size’s mean. The signs of our independent variables in the models are consistent with our hypotheses although not all of the coefficients are significant. The insignificance is probably due to the smaller number of observations in the subsamples.

Additional Analysis: Organizational Approach of New Industry Entry

The exercise of family influence not only affects controlling owners’ pursuit of diversified entry but also the way the new industry entry is structured. Specifically, the new business unit can be organized as a new division within an existing group firm or a legally separated new firm, both of which are within the boundary of a family business group (Lee & Lieberman, 2010).

Following our previous argument, we expect that new industry entry through a new division offers important advantages to controlling owners who prioritize their exercise of family influences. In particular, the setup of a new division usually requires less initial resource commitments, such as those made in human resources, information systems, or financial structures. The setup of a new division reduces the risks of external scrutiny and financial distress (Gomez-Mejia et al., 2010), and thus better protects family control from being diluted.

In comparison, new industry entry by establishing a new firm is conducive to perpetuating family dynasty for two reasons. First, diversified entry through a new firm provides more opportunities to nurture family descendants and creates more space to promote them (Gomez-Mejia et al., 2001). Second, compared with partitioning one company into multiple portions, creating a collection of legally independent firms during family succession incurs fewer family conflicts and less erosion of the established businesses. Therefore, when facing an increasing challenge to perpetuate the family dynasty during succession, controlling owners are more likely to structure the diversified entry through a new firm rather than a new division in the existing firms.

To test our arguments, we constructed the approach of new industry entry with a dummy variable, which equals 1 if the diversified entry is conducted through a new firm and 0 if through a new division. Table 5 demonstrates the results based on Logit regression. 5 The significant coefficients of the family influence and the no. of family members are consistent with our predictions and provide additional support to our hypotheses on the distinct effects of the focused SEW and the broad SEW (H1 and H2, respectively).

Logit Regression for Approach of New Industry Entry

Note: Robust standard errors appear in parentheses.

p

p

p

Discussion and Conclusion

Our study examines how controlling owners’ family socioemotional needs affect their pursuit of new industry entry. Drawing on the SEW approach, we consider new industry entry as controlling owners’ response to the pursuit of different SEW aspects. Specifically, we distinguish controlling owners’ affective needs of a restricted group of family members who are involved in the business management from the ones that relate to a larger number of family members and span a relatively longer time horizon. We refer to the former as the focused SEW and the latter as the broad SEW and demonstrate their opposing effects on new industry entries. Further, we propose that the effects of SEW aspects are contingent on owners’ generation. The effects of both the focused and the broad SEWs are stronger when the controlling owners are the founder generation.

Our results offer several contributions to the current literature. First, recent studies employing the SEW approach tended to treat SEW as an aggregated and homogeneous construct (Berrone et al., 2010; Gomez-Mejia et al., 2007). Although this approach is insightful, it has been criticized for oversimplifying controlling owners’ decision-making process and leading to mixed findings (Miller & Le Breton-Miller, 2014). By showing how different SEW aspects can impose distinct effects on controlling owners’ diversified entry decisions and how the relationships are modified by their affective attachment to the family businesses, we clarify the causal relationships between SEW aspects and family business strategies. Our study modifies the conventional approach that treats SEW as a latent explanatory construct and shifts the research direction toward directly theorizing and measuring its various aspects. It also adds precision to the SEW construct and helps reconcile previous ambiguous findings on family business diversification (Anderson & Reeb, 2003; Boyd & Solarino, 2016; Gomez-Mejia et al., 2010; Jones et al., 2008). In addition, our study responds to the call for advancing the understanding of different decision time horizons of executives in family firms (Gedajlovic et al., 2012). The opposing effects of the exercise of family influence and the succession of family dynasty on new industry entry decisions confirm the importance of decision-making time horizons and extend the existing family business research that has mainly focused on the effects of CEO age, tenure, or capital market pressures (Antia, Pantzalis, & Park, 2010; Walsh & Seward, 1990).

Second, the lack of psychological grounding has been a limitation in strategic management literature (Powell et al., 2011). By incorporating research on affective and cognitive processing in the explanation of the moderating effect of family business generation, we attempt to “bring realistic assumptions about human cognition, emotion, and social behavior” (Powell et al., 2011: 1371) to the understanding of the organization’s strategic choices, such as new industry entry.

Third, one core agenda in the business group literature is why and how business groups emerge and survive through diversified entries (Khanna & Palepu, 2000). Previous research offered different explanations, such as market inefficiency (Khanna & Palepu, 2000), government intervention (Carney, 2008), and generic resources and capabilities (Guillen, 2000). Our results provide an alternative explanation, that is, the role of controlling owners’ SEW needs. By demonstrating a path through which family firms can evolve from family entrepreneurs to larger family-owned entities and eventually to business groups, the present study illustrates the extent to which family considerations influence firm evolution.

Our findings can be extended in a number of ways. First, we point out the importance of distinguishing various SEW aspects and propose a tentative dichotomy to associate different SEW aspects with divergent strategic preferences in family businesses. Future studies can extend our approach by examining different forms of focused and broad SEW and their distinct implications to other strategic decisions. For example, one can consider the desire to secure cash flows for family members as a form of focused SEW and the goal to ensure business survival as a form of broad SEW. Differentiating these SEW forms and their various implications on strategic choices such as R&D expenditure and international expansion helps advance the SEW literature.

Second, we capture the affective attachment with the measure of generation, and it is worthy of further examination with other proxies such as family executives’ tenure, unique experience, or social relationships in the family firm. More importantly, more research is required to integrate cognitive and social psychology with strategic management theory to advance our understanding of behavioral decisions in family businesses.

Third, new industry entry takes various organizational forms as we explore in the additional analysis. Our preliminary findings suggest that new industry entry by adding a new division within a group can be used by the controlling owners to maintain their family influence and that diversification through establishing a new firm (a legally separate corporate entity) can be a tool to facilitate family dynasty succession. Future studies can further test such relationships by examining how strategies shaped by SEW also influence other corresponding organizational forms, such as strategic alliances, joint ventures, and wholly owned organizations.

As with any study that utilizes a single country as research context, our results can be limited in application scope. It would be useful to examine if the SEW aspects theorized and tested in the present study could be applied to other contexts. Furthermore, a possible explanation for the insignificant finding for H3b is our limited data span. The finding warrants further investigation using longitudinal data over a longer time period. In addition, our study does not examine the role of institutional investors in the family businesses’ decision making due to data constraints. Future research may further investigate how controlling owners interact with institutional investors and how such interactions affect strategic decisions and ultimately their business performance.

Footnotes

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright. The authors would like to thank Dr. William P. Wan and two anonymous reviewers for their insightful comments.