Abstract

There is no theory in strategic management and other related fields for identifying decision problems that cannot be solved by organizations using rational analytical technologies of the type typically taught in MBA programs. Furthermore, some and perhaps many scholars in strategic management believe that the alternative of heuristics or “rules of thumb” is little more than crude guesses for decision making when compared to rational analytical technologies. This is reflected in a paucity of research in strategic management on heuristics. I propose a theory of “organizational intractability” based roughly on the metaphor provided by “computational intractability” in computer science. I demonstrate organizational intractability for a common model of the joint strategic planning and resource allocation decision problem. This raises the possibility that heuristics are necessary for deciding many important decisions that are intractable for organizations. This possibility parallels the extensive use of heuristics in artificial intelligence for computationally intractable problems, where heuristics are often the most powerful approach possible. Some important managerial heuristics are documented from both the finance and strategic management literatures. Based on all of this, I discuss some directions for theory of and research on organizational intractability and heuristics in strategic management.

Keywords

In theory, there is no difference between theory and practice. But in practice, there is.

Introduction

At least since and perhaps before the publication of Bower’s (1970) Managing the Resource Allocation Process over 45 years ago, serious questions have been raised in the management and strategy literatures concerning the frailty of the pure financial theory approach to allocating resources given the well-known cognitive and political limits on actual decision making by managers. At the same time, strategy scholars have generally agreed that there is an important logical connection between a divisional strategy and the corporate allocation of resources to achieve that strategy.

I address several topics. First I define “organizational intractability” of organizational decision making based on the metaphor provided by the theory of computational intractability in computer science (e.g., Moore & Mertens, 2011). 2 In general use, the term “intractable problem” means a problem that is hard to solve, but the definition of “computational intractability” in computer science and the definition of “organizational intractability” in this article are both more specific and detailed. For computational intractability, the amount of precise technical detail is large. Second, I demonstrate the organizational intractability of a normative strategic planning model and the related financial theory of resource allocation for a division in a diversified firm. My demonstration of organizational intractability parallels in important ways the insightful development of the computational intractability of the strategy formulation problem modeled as search on an NK landscape that was developed in Rivkin (2000). Unfortunately, since Rivkin’s paper this approach has largely lain fallow. I then review evidence for the extensive use of heuristics or “rules of thumb” by managers for both organizationally intractable decision problems and those that are constrained by time, information, and management attention.

Finally, this all leads to a more general consideration of both organizational intractability and the use of heuristics to make important decisions in organizations. I develop some preliminary suggestions for a theory and research on heuristics in strategic management and related areas. In some of the article I discuss the insightful heuristics literature from artificial intelligence in computer science that is generally unfamiliar to scholars in management. Heuristics are often viewed by many scholars in strategic management as seriously compromised relative to an array of rigorous analytical models and/or classical optimization methods. For such scholars, more models, more data, more calculations, and more optimization are viewed as always resulting in better decision making. I show that this is simply not the case. The arguments are developed logically, but not formally. No attempt is made to develop technical details or rigorous proofs. The article is written explicitly for a general audience in strategic management and other related fields.

Organizational Intractability

Organizations pursue intelligence. It is not a trivial goal. Its realization is imperfect and the pursuit is endless.

There is no theory in strategic management, organization theory, or economics regarding the intractability of important decision problems faced by managers in organizations. By contrast there are in some cases accepted theories, models, tools, and conventional wisdom that specify the “correct approach” to certain specific instances of decision making. Take for example the strategy theory of “fit” as the decision to select a consciously designed fit between the firm and its forecasted environment or the financial theory of net present value (NPV) as the theoretically correct way to decide the capital projects to be funded. MBA students are taught such “theories” and are equipped with the necessary technical apparatus for applying them directly to decision making in firms. The question of whether such theories or approaches are actually tractable for real managers working in real organizations under real-time constraints is never raised. Related in some ways to this article, there has been increasing scholarly interest in practice of strategy approaches that often go by the names “the practice-based view” or “strategy-as-practice.” See, for example, Jarzabkowski, Balogun, and Seidl (2007); Bromiley and Rau (2014); and Jarzabkowski and Kaplan (2015).

The theory of computational intractability 4 in computer science provides a metaphorical basis for the concept of “organizational intractability” developed in this article. Moore and Mertens (2011) provide a thorough development of computational intractability that is well motivated and without need of any substantial mathematics. At the same time, it is lengthy and not a casual read. Harel (2003) contains a very useful intuitive introduction. Harel and Feldman (2004) is intermediate between these two extremes. This theory starts from the obvious idea that computers may be fast but computation still takes time and memory. With certain problems, the time to complete the computation can become substantial to varying degrees. 5 It can take billions of years or even much more for a very fast computer to solve some problems, if they can be solved at all. 6 Take, for example, the “traveling salesman” problem that in various guises has many practical applications. This is usually described as the problem of finding the shortest route for a traveling salesman to cover all the cities that must be visited on a trip and finally return to the “home” city from which the tour started. Parameterized for 100 cities and with a computer that can check a million routes a second, it will take roughly 2.9 × 10142 centuries for the computer to check all routes and thereby be guaranteed to find the global shortest route (Yanofsky, 2013: 111-112).

I seek to demonstrate that the divisional strategic planning decision problem and the associated resource allocation decision problem by the corporate office as per the MBA introductory course level are both intractable for organizations as defined directly below. 7

Definition of Organizational Intractability

I first introduce the concept of “organizational intractability.” This concept is intended to apply to important managerial decision making based on rational analytical technologies. By organizationally intractable, I mean that for organizationally important decision making (e.g., strategic decisions) based on rational analytical technologies, the total time required for an organization to organize the decision-making process, gather the required information, perform the necessary analytical and judgment tasks to arrive at a logically justifiable analysis (sufficiently rigorous and comprehensive), and make the decision is long enough to preclude the possibility of arriving at a solution before the decision problem has changed in important ways or has become irrelevant.

By rational analytical technologies, I mean approaches such as classic optimization techniques, analytical models, formal decision theory, strategic planning, and game theory. Generally, these are what March (2006: 202) calls “model-based rational logic.” It should be noted that organizational intractability does not address the question of the accuracy of a rational analytical technology as applied in organizations. This is a separate issue that becomes totally irrelevant if the technology is organizationally intractable as defined above. Furthermore, the analysis must be of “sufficient rigor and comprehensiveness” to be logically justifiable. This obviously requires some level of judgment. This phrase is intended to indicate that the analysis should not be abbreviated, simplified, or altered to the point where objective, knowledgeable scholars believe that it compromises the “rational analytical technology” being used.

The proposed definition of organizational intractability also avoids the rather obvious issue of organizational deadlines. Important organizational decision problems have deadlines that must be met, and these are usually measured in hours, days, weeks, or a few months but not years. The deadline limit set by the definition is the “has changed substantially or has become irrelevant” component in the above definition. Also, “organizational intractability” does not address the issue of whether or not participants in the decision-making processes are satisfied with the process and/or its outcome (e.g., Garbuio, Lovallo, & Sibony, 2015). This is an entirely separate matter. Furthermore, in some and perhaps many cases, even at substantially lower levels of rigor and comprehensiveness, the decision making based on rational analytical technologies may turn out to be organizationally intractable, thereby negating the need to prove this result for higher levels of rigor and comprehensiveness, which would take longer, and perhaps much longer, to execute. The case examined below is one such example.

Demonstration of Organizational Intractability

Environments are often complicated, endogenous, subjective and contested.

No matter how detailed, the business scenarios used in planning are generally inadequate.

In the demonstration of organizational intractability, I rely on one approach to strategy formulation that is often taught in introductory MBA and undergraduate classes. This is sometimes referred to as strategic planning in both courses and firms. It is a model of strategic planning that is often considered a normative or conventional analytic view. Often, this seems to include a 5-year time frame, but this is largely arbitrary. Readers can consider any reasonable time frame from a couple of years to 10 or 20 years.

I consider one and only one aspect of this strategy formulation or strategic planning problem—forecasting the future environment(s) of a business division (or a single business firm) so that an appropriate strategy can be fitted to this forecast. This single aspect will be demonstrated to be organizationally intractable, making the entire strategic planning problem using forecasting organizationally intractable. In this demonstration, I will usually refer to the singular “environment” of a firm to include all the relevant environments that actually compose the environment of the firm. In this regard the singular “environment” is meant to include the industry, competitive, supplier, customer, regulatory, social, technological, cultural, political, macroeconomic, and other constituent environments.

It is reasonable to question the accuracy of any forecast of the entire environment of a firm that involves more than a few months into the future. However, I ignore this and other relevant issues and concentrate on the amount of time necessary to develop the forecast of the environment of the firm with sufficient rigor and comprehensiveness. Such a forecast would be rationally defensible as an analytical process even though there would still be important questions about the degree of inherent accuracy of the forecast. I seek to demonstrate that under the conditions above the development of a forecast of the environment is organizationally intractable. If this is so, then the entire strategic planning process is intractable.

Forecasting the environment actually amounts to finding the most likely future environment of the firm in the forecast problem space so that a business or divisional strategy can be designed to “fit” this future environment. 10 By problem space in this context, I simply mean a managerial representation of the problem thought likely to include all the important future states of the firm or division environment. An all-seeing and all-knowing entity would be able to specify the actual complete problem space.

Notice that this definition ignores the fact that a strategy based on this forecast becomes endogenous to the environment when executed and will alter it in a fashion not easily determined. 11 The analysis will demonstrate organizational intractability without introducing this complication. Consistency of the analysis demands that the forecasted environment selected from within the problem space be logically consistent with, if not identical to, the environmental forecast assumptions behind the estimated cash flows used to calculate the theoretically correct NPV of the strategy and/or the new resource commitments that the strategy entails. Inconsistency in either direction represents a flaw and logically invalidates the combined strategy and associated resource allocation decision problem. Hence, I assert that the forecasting component of both a strategy and the associated NPV calculation for new resources are logically coupled and cannot be considered independently. The environmental forecast will be used to determine a strategy that “fits” the future environment, and hence, the NPV of resource commitments inherent in this strategy should be consistent with this forecast.

In the case of strategic management, managerial construction of the problem space of the forecast usually involves specifying the future of a variety of market structure variables, government policies, technological evolution, social trends, macroeconomic trends, and other relevant variables perhaps in multiple regions of a country and/or areas of the world. In the conventional approach this is complemented by an analysis of the resources, capabilities, structure, systems, and policies of the firm, and what changes will be needed to accomplish the new strategy. Reflecting on these internal and external analyses, it is then imperative to design a strategy and organization structure, resources, rules, and systems that “fit” the forecasted environment. 12 Hence, again the point is that the NPV rule of capital budgeting should be used based on a forecast of future cash flows from the strategy when implemented and based on a theoretically correct discount rate (firm or division cost of capital) and the fit of the strategy with the future environments. Instead, for finance in practice this often means embedding “estimated” future cash flows as the means of well-behaved Gaussian distributions. It is unclear in theory how such cash flows are estimated. I have on numerous occasions in the classroom had MBA students with experience as financial analysts in firms and investment banks cite incidents where they were told to alter the cash flows to “make the numbers work.” It should also be noted that the strategic and financial analyses can come up with inconsistent results that of logical necessity should be reconciled before executing the strategic plan and allocating the associated capital expenditures.

To demonstrate the organizational intractability of this forecasting approach to planning, I use a simple example of forecasting the future environment of a specific type of hypothetical firm that might be expected in formulating a strategy for a business or division. To do this, I first develop a specific environmental forecasting problem space that will have to be constructed, in order to arrive at a forecast. To this point, Table 1 lists 20 major environmental variables for the forecasting problem space as a part of the strategy development process for a hypothetical global fast food hamburger chain. 13

Example Problem Space Variables for Organizational Intractability Demonstration

I could easily introduce more relevant components into the forecast problem space, but 20 will be adequate for the demonstration. I could reduce the dimensions to some “more manageable” number, but then it gets increasingly harder to claim that the sample problem space is an adequate approximation. In fact it also makes it easier analytically to ignore potentially important future developments. Although the example is entirely hypothetical, the reader might want to think of an actual company like McDonald’s Corporation to give the demonstration useful context.

At this point, I introduce a vital issue regarding the demonstration: the large scale interdependency often called complexity. The 20 variables of our example problem space are obviously interdependent to varying degrees. Forecast values of each variable cannot simply be considered separately and then added together to construct a forecast of the overall environment. At least some of the variables will likely be highly interdependent, but almost all will have some interdependencies. I will use the term “complexity” throughout this article to mean large-scale interdependency such that the values of any particular variable will depend directly and/or indirectly on the values of several or many other variables. As an example, consider the network of relationships between the forecast variables in the present case. A change in the level of any variable will reverberate through many variables and be subjected to various feedback loops. 14 This simple definition is used to ensure that my use of “complexity” is not confused with many different kinds and definitions of complexity.

It is also necessary to specify a number of potential future values for each variable. This is a nontrivial task since each cannot be specified independently of others due to complexity. It is unclear how this could actually be done since there is no way for determining or even reasonably estimating the actual interdependence structure. The result in terms of organizational intractability is the same if we assume no interdependency structure. Hence, I do not use any interdependence structure in the analysis.

Also, it seems reasonable to associate some probability level or distribution with every future level of each variable. In reality, this gets severely tangled in the assumed interdependence structure. However, again I choose not to introduce this important refinement. This does not impact the result in terms of organizational intractability.

Table 2 shows the time required for nine different cases of the demonstration environmental forecast.

Calculation of Time Required for Demonstration Analysis Subject to Number of Variables and Cases

Calculated by dividing total environmental forecasts by (360 x 24) = 8640.

The number of variables in the problem space is allowed to vary from initially assumed 20 down to 15 and 10. The number of values for each variable in the forecasts is allowed to vary from five to three to two. The total environmental forecasts necessary for each of the variable/level forecasts is a simple combinatorial and calculated as the number of levels tried for each variable in the forecast raised to the power corresponding to the number of variables. From this number the total person-years is calculated based on an assumed 1 hour for an individual to examine each resultant forecast and determine the ranking relative to the other forecasts in terms of some measure of likelihood. Obviously, this makes the wildly optimistic assumption that 1 hour is adequate to develop an understanding of the forecast and make an informed judgment on relative likelihood compared to many (billions in some cases) of other forecasts. It does not include the time to organize the project, develop the forecasts, and fit the strategy to the most likely forecast after it is determined. Undoubtedly these would all take substantial time.

The results in Table 2 easily rule out all the 20 and 15 variable cases. For the most rigorous and comprehensive example of 20 variables and 5 levels of each, it will take over 11 billion years (24 hours a day 360 days a year with no coffee breaks or sleeping allowed!). By contrast, planet earth is only about 4.5 billion years old. Rigor and comprehensiveness can certainly take time. I would rule out all of the 10-variable cases on the basis that these would all be insufficiently rigorous and comprehensive as per the definition and discussion earlier for “organizational intractability.”

Aside from the issue of organizational intractability, this demonstration has made numerous simplifications. Among these are ignoring the endogeneity of the firm to the environment, eliminating consideration of the interdependence structure of the forecasted future environment, eliminating probabilities until each forecast environment is evaluated, ignoring the time to gather data, ignoring the many judgments that would have to be made very quickly by executives and analysts, and ignoring the coordination time required for the project. I also point out that all of this is just a necessary precursor to the design of a strategy to fit the forecasted environment.

One question can obviously be raised about the demonstration: Why not use a very fast supercomputer with the appropriate algorithm to automate this whole process of forecasting? To address this, it is only necessary to consider the two items technically necessary to describe an algorithmic problem: (a) a definition of the set of all legal inputs and (b) a precise description of the required output as a function of the input (e.g., Harel & Feldman, 2004: 14). 15 The biggest problem here, but certainly not the only one, is that the precisely defined function that describes the output as a function of the input is highly ambiguous. For example, it requires the function to precisely define algorithmically “judgment” in evaluating the myriad of individual forecasts and assigning likelihoods to them in a manner consistent with probability theory. Overall, this is not a well-structured problem. Rather, it is an ill-structured (e.g., Simon, 1996) and/or a wicked problem (e.g., Camillus, 2008; Rittel & Webber, 1973). Such problems are notoriously difficult to precisely specify without substantially or completely altering the fundamental nature of the problem (e.g., Churchman, 1967).

The Inevitability and Virtues of Heuristics

Heuristics! Patient rules of thumb, So often scorned: Sloppy! Dumb! Yet, slowly common sense become.

The discussion and demonstration of organizational intractability of environmental forecasting raises important questions regarding any strategy development process based on forecasting the environment. It also raises similar questions about the forecasting origins of the cash flows for NPV calculations to justify the new resources required by the strategy. For both decisions the demonstration strongly suggests that something else is happening. It is logically a short step from this demonstration to considering the alternative possibility of heuristics that economize on information, time, and managerial attention when considering any organizationally important decision-making (e.g., strategic decisions).

As an example of heuristics, consider the traveling salesman problem as discussed earlier and parameterized for 100 cities. As noted above, for a very fast computer this problem will take roughly 2.9 × 10142 centuries to find the global shortest route. One heuristic for constructing a feasible solution is simply to start at any particular city and go to the nearest city, then from that city to the nearest city that has not been visited, and so forth until all cities have been visited and the salesman has returned to the city from which he started. This “nearest neighbor” or “greedy” heuristic does surprisingly well and will obviously take very little time to calculate (Johnson & McGeoch, 1997). On the other hand, it will generally not find a global optimum and on occasion will perform poorly. One estimate is that it will on average come up with a path about 25% longer than the shortest path for large numbers of cities and random distances (Johnson & McGeoch, 1997). There are more sophisticated algorithms based on refinements of the nearest neighbor heuristic that perform substantially better than this. “Branch and bound” algorithms can actually find optimal solutions but only for specific cases that are much smaller than 100 cities.

The study of heuristics for problem solving originated in the most logically rigorous discipline in the academy, mathematics. Polya’s (1945) book, How to Solve It, emphasized the role of heuristics in proving mathematical theorems and solving mathematical problems.

The heuristics research most familiar to management and strategy scholars is in psychology. It is generally accepted that there are two broad approaches to heuristics in the psychology literature. The first and by far the most widely known and researched “heuristics and biases” approach sprang from the Nobel Prize–winning work of Kahneman and Tversky (e.g., Kahneman, 2011; Tversky & Kahneman, 1974). The general approach is that “people rely on a limited number of heuristic principles which reduce complex tasks of assessing probabilities and predicting values to simpler judgmental operations. In general, these heuristics are quite useful, but on occasion they lead to severe and systematic errors” (Tversky & Kahneman, 1974: 1124). Although acknowledging the usefulness of heuristics, much of this research has concentrated on finding “severe and systematic errors.” For an interesting example of this research applied to managerial decision making, see Lovallo and Kahneman (2003).

The other major psychological approach is associated with Gigerenzer and associates (e.g., Gigerenzer & Selton, 2002). Gigerenzer’s approach emphasizes the positive and adaptive character of heuristics in the presence of Knightian uncertainty (Knight, 1921) 17 and ecological rationality (e.g., Todd & Gigerenzer, 2012). Heuristics are seen as ignoring available information and focusing on a few key pieces of information as a way to make better and faster decisions (Todd & Gigerenzer, 2012: 7). For an example of this research applied to managerial decision making, see Mousavi and Gigerenzer (2014). This approach to heuristics is generally consistent with the approach taken in the paper.

There have been occasional insightful articles in the strategic management literature where heuristics are viewed neutrally or positively. See, for example, Alvarez and Busenitz (2001), Amit and Schoemaker (1993), Eisenhardt and Zbaracki (1992), Schwenk (1984), and Stubbart (1989). More recently, there has been increasing and consistent interest in the adaptive character of heuristics. See, for example, Bingham and Eisenhardt (2011); Bingham and Haleblian (2012); Davis, Eisenhardt, and Bingham (2009); and Eisenhardt and Sull (2001). Loock and Hinnen (2015) contain a fine review of the heuristics research in organization and management theory.

The earliest substantial work I can find explicitly naming and discussing the importance of heuristics in strategy is An Evolutionary Theory of Economic Change (Nelson & Winter, 1982). It is hard to understand how this important work on heuristics in combination with the earlier work of Simon, Cyert, and March (e.g., Cyert & March, 1963; Simon, 1955) did not immediately stimulate considerable research on the topic in strategic management research during its formative period in the early 1980s. It is worth noting that there are many heuristics in theories related to strategy and especially behavioral approaches to strategy. For example, consider concepts such as “search for a set of possible outcomes” (Simon, 1955: 106), or “stop searching when a satisfactory solution is found,” or “search near a problem” (Cyert & March, 1963), or the theory of adaptive aspirations (Cyert & March, 1963). All of these are theories in the form of heuristics that attempt to represent real heuristic processes.

Heuristics, often search heuristics, are an important research area in computer science, operations research, and engineering. Consider for example Pearl’s seminal 1984 book, Heuristics: Problem-Solving Strategies and the Nature of Heuristics. In the prologue to this book, Pearl cites his inspiration for the book as the complex tasks that humans can accomplish with simple unreliable information. Pearl subsequently won the Turing Award for his work in computer heuristics and other areas. A recent textbook on artificial intelligence states that heuristics are one of the most central topics the book covers and that heuristics are more intuitive, human-like approaches based on insight, experience, and know how (Lucci & Kopec, 2013: 79). It is ironic that while strategic management researchers often cite optimization results or adopt classic optimization techniques, artificial intelligence researchers seek to imitate powerful human heuristics to find solutions in large complex problem spaces.

It is relevant to note that Herbert Simon based his satisficing theory of bounded rationality largely on the heuristic “search till a satisfactory solution is found.” Interestingly, he made important contributions to artificial intelligence and was a Turing Award winner jointly with Allen Newell for their work on artificial intelligence. Their work in artificial intelligence is considered foundational. In their Turing Award acceptance speech they make the following relevant observation: “Our analysis of intelligence equated it with the ability to extract and use information about the structure of the problem space, so as to enable a problem solution to be generated as quickly and directly as possible.” (Newell & Simon, 1976: 124). In this quote, it is worthwhile to note the phrase “a problem solution” instead of “the problem solution.”

It is likely that many decision problems of importance to strategic management involve large complex problem spaces that severely violate the very narrow assumptions necessary for the usual methods of optimization to be workable. The artificial intelligence literature addresses such problem spaces with heuristics. The managerial and organizational use of heuristics therefore seems to have a strong basis in the presence of large, complex problem spaces in strategy. There is no other way to address issues of decision making in the presence of some and likely many realistic strategic decision problem spaces. The demonstration above of organizational intractability hopefully illustrates this.

There are two specific sets of managerial and organizational heuristics in the scholarly literature that are of interest for the present article—those used for capital budgeting and those used for simultaneously determining divisional strategy and the associated resource allocations (capital budgeting). I start with the capital budgeting issue.

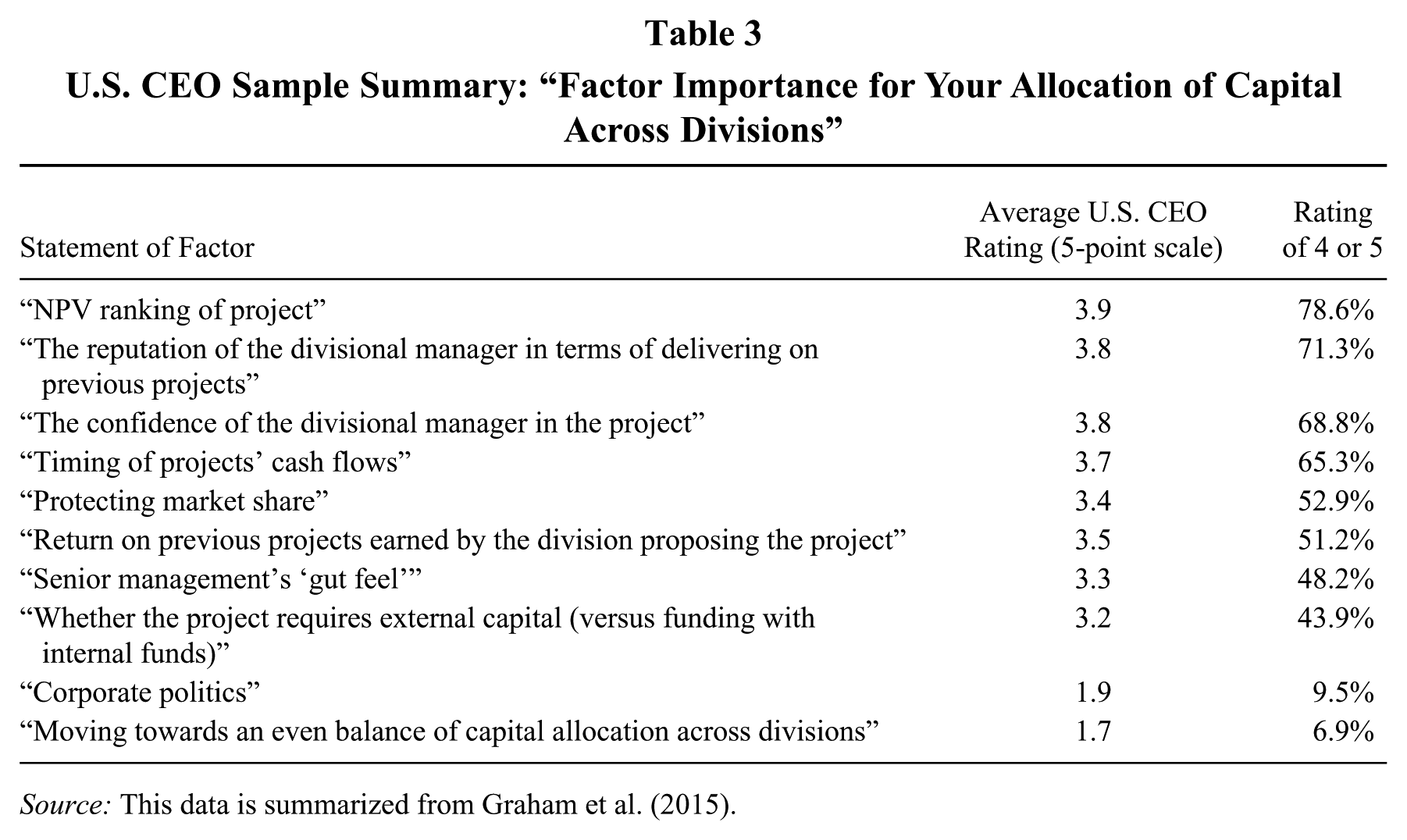

A recent study of capital budgeting surveys the use of various approaches to the capital budgeting problem (Graham, Harvey, & Puri, 2015). The article uses anonymous data from around the world of more than 1,000 chief executive officers (CEOs) and chief financial officers (CFOs). This is an extraordinarily rich survey with many results. While encouraging readers to carefully examine this entire article, I focus on only one set of results, the decision criteria U.S. CEOs used for capital allocation to division mangers. Table 3 lists both the criteria and the full wording of the survey choices available.

U.S. CEO Sample Summary: “Factor Importance for Your Allocation of Capital Across Divisions”

Source: This data is summarized from Graham et al. (2015).

The theoretically correct NPV ranking is listed, but so are other criteria such as “gut feel,” “previous return,” (division) “manager reputation,” and (division) “manager confidence.” Looking at the full list, the term “heuristic” comes readily to mind. The scale used was 1 to 5, with 1 representing being not important at all and 5 being very important. A level of 4 was deemed important. With this in mind, Table 3 lists the percent of U.S. CEOs choosing either 4 or 5 for each criteria. Not surprisingly, the average ranking for NPV was the highest, with a mean of 3.9 with 78.6% saying it was important or very important. The next four were manager reputation (3.8/71.3%), manager confidence (3.8/68.8%), cash flow timing (3.7/65.3%), market share (3.4/52.9%), previous return (3.5/51.2%), and gut feel (3.3/48.2%). It is stunning from a financial theory perspective that over 20% of CEOs ranked NPV as less than important. It is also theoretically extraordinary that “division manager reputation” and “division manager confidence” both averaged 3.8, only 0.1 below NPV. These results overall are indicative of the widespread use of various heuristics by CEOs in the allocation of capital to divisions.

There is a closely related group of heuristics that jointly addresses the divisional (or strategic business unit) strategy and financial cross-subsidization across different categories of businesses. These are known by a variety of names such as corporate portfolio analysis, the business portfolio, or the strategic business unit (SBU) concept. Interestingly, these heuristics arose as the result of conscious efforts primarily by consulting firms to design systems for managing diversified firms. The catalyst for these heuristic approaches was likely the substantial firm diversification in the USA that occurred in the 1960s. According to Pidun, Rubner, Krühler, Untiedt, and Nippa (2011), these approaches originated in 1970 with the introduction of the Boston Consulting Group (BCG) growth-share matrix of four categories. Similar heuristics were introduced jointly by McKinsey / General Electric and by Arthur D. Little using multiple measures for the two dimensions of the matrix. A variety of other variants on these matrices then quickly appeared. The McKinsey/GE matrix used multiple measures of industry attractiveness and competitive position in a nine-bloc matrix. For all of these grids, generic strategic and cash-usage/generation roles were defined. Names such as “cash cows,” “stars,” “questions marks,” and “dogs” were assigned to denote their strategic and cash generation, cash use roles. In some firms the grids were used as a tool of analysis, and in others they became complete management systems (Bettis & Hall, 1981). An excellent description of the BCG grid can be found in Hedley (1977). There has been a wide and deep criticism of these approaches by scholars in strategic management. They seldom are even mentioned in current corporate strategy research, although they still appear in some strategic management textbooks. See Nippa, Pidun, and Rubner (2011) and Untiedt, Nippa, and Pidum (2012) for summaries of the criticism and the authors’ associated rebuttals with suggestion for future research. I take no position with respect to the effectiveness of these techniques, except to note that they are heuristics that seek to economize on information, time, and managerial attention, and that managers still find them quite useful. There is also a substantial recent survey of the use of these concepts that suggest they are still used extensively in practice.

Pidun et al. (2011) surveyed a global sample of senior executives in 1,403 companies regarding the portfolio concept. Approximately 60% of the responding companies had over $5 billion in sales. The results were complemented by in-person and telephone interviews with 50 senior executive and 100 major client engagements involving portfolio assessments undertaken by the BCG between 2004 and 2009. (For details of the many results, readers should refer to the paper.) The results suggest that, though these concepts have evolved some, they are still an important part of the strategic decision-making technology in many firms. For example, of 183 respondents to one set of questions, 37% responded that “CPM (Corporate Portfolio Management) is a major part of our ongoing management process.” In addition, 30% responded that “we regularly use CPM for planning and strategic decisions.” It is unclear if this represents a random sample and what role self-selection played, but the percentage of affirming regular usage still seems large. It is clear that many senior executives find these techniques useful.

In sum, there is credible evidence of the substantial use of heuristics in the case of NPV analysis and, in the case of the connection between strategy and resource allocation (cross-subsidization), for corporate strategy in diversified firms. This suggests a more theoretical consideration of the role of heuristics in strategic management (and, perhaps, corporate finance) may be in order.

Toward a Theory of Strategic Management Heuristics

The broad ideas that shape the most critical high-level decisions of a business enterprise may also be viewed as heuristics—they are principles that are believed to shorten the average search to solution of the problems of survival and profitability. Much discussion of heuristics of this sort has been carried under the rubric “corporate strategy.”

The purposes of this section are to sketch some issues relevant to a possible theory of heuristics in strategic management and other areas and to make some related research suggestions. We actually know very little about the use of heuristics in strategic management, although heuristics are seemingly a common feature of senior executive decision making and inconsistent with more theoretical, optimal, or model-based approaches.

A Proposed Definition of Heuristics

The first issue with a theory of heuristics in strategic management and management generally is simply that the widely used “rules of thumb” definition lacks usefulness and precision. As an alternative, I suggest using the definition used by Pearl (1984: 3): Heuristics are criteria, methods, or principles for deciding which among several alternative courses of action promises to be the most effective in order to achieve some goal. They represent compromises between two requirements: the need to make such criteria simple, and at the same time, the desire to see them discriminate correctly between good and bad choices.

This definition seems to have many virtues. It is focused on decision making. It uses the action verb deciding as one of choosing between alternative courses of action. It frames choosing in the context of a “goal.” This goal must be apparent. Furthermore, it explicitly acknowledges the need for both “simplicity” and the need to discriminate between “good and bad” choices. This implies that “choices” are fundamental to the analysis. Both goals and choices may be subject to political manipulation including misrepresentation, but this is a separate issue from defining the term “heuristics.” Relatedly, note that obviously a finding of organizational intractability for a rational analytical decision process suggests the necessity of heuristics of some sort. Perhaps in such situations heuristics are actually being used while the “appearance” of a rational decision process is maintained for the purpose of legitimacy with relevant internal and external audiences. Research is needed to address this point.

I now introduce two rather different types of heuristics: those learned from experience with the environment of the organization and those designed by managers or consultants. There may be many kinds of heuristics and ways to categorize them, but the two types discussed arise from different processes and seem particularly relevant to strategic decision making in firms.

Type I Heuristics: Learning Directly From the Environment

In real-world environments an almost limitless number of distinct possible situations may occur. A useful learning capability therefore always needs to provide a significant component of generalization; a learned behavior has to be effective not only in situations that are identical to ones previously experienced, but also in any number of novel ones.

It is impossible to discuss learned managerial heuristics divorced from the environment of the firm. In the case of strategic management, senior managers make repeated strategic decisions (e.g., new products, acquisitions, technology changes, capital investments, new strategies) and observe feedback from the environment from which they draw conclusions. This experiential learning is complemented by observation of decisions and their outcomes in competitors and other firms. Both direct experiential learning and learning from observing others can result in heuristics individually or jointly. These heuristics may then be diffused among managers by inclusion in decisions, memos, reports, briefings, meetings, rules, procedures, routines, and informal discussions.

This learning is obviously a process of induction by managers. Initially, such an induction is based on a very limited sample, perhaps just a single case, and may never reach or even approach the sample sizes typical of the probabilistic inductions of statistical studies. Furthermore, it will never include the controls typically found in statistical studies. The resultant heuristic will likely be applied to decision situations that differ in varying degrees of novelty from the limited samples of experience on which they are originally based. This will be particularly true of decisions that managers conclude are in some way(s) similar to the original situations on which a heuristic is based. Induction based learning is the fundamental basis of human intelligence. It is a process of trying to discover meaningful regularities in our environment. We all engage in it from the moment we are born. Millennia of evolution have honed it into a powerful tool of human intelligence.

However, such adaptive learning processes are obviously far from problem-free (March, 2010). Environments are complex and stochastic, so learning is imperfect. In such learning from feedback, not all of the instances of feedback are treated equally (Kiesler & Sproull, 1982). Some are much more memorable than others and, hence, likely to be more influential. However, even with such problems, managerial heuristics are developed that are thought to be useful in decision making. Apparently, some and perhaps many of them are often used and found to be useful.

In a sense, the environment is teaching the manager or organization how to use bounded rationality to make better decisions. Perhaps more flatteringly for the author, readers, and managers, human intelligence is being applied though experiential learning to discover regularities in the environment that can be expressed as useful heuristics. Various mechanisms of environmental selection will directly eliminate some of these heuristics that are inappropriate or unreliable. Furthermore, managers or organizations that on average learn and use inappropriate or unreliable strategic heuristics are more likely to be selected out by the environment over long enough time periods. Also, as Nelson and Winter (1982: 132-133) point out, such heuristics will vary with the functional background of executives and may arrive and depart with executive hires and departures. They also note that heuristics often are stored and used as routinized behavior or routines. All of this raises an important issue—to what degree heuristics can be updated across time as more learning occurs or the environmental state changes. In this regard, the dynamic capabilities literature (e.g., Winter, 2003) is evocative of the evolution of simple heuristics into more sophisticated rule sets.

In a totally random environment, there are by definition no real regularities. Real environments obviously have regularities. Casual observation suggests that environments generally have lots of regularities. A firm environment will obviously have regularities that will allow managers in the firm to learn heuristics from experience with the environment. However, the cognitive processes for separating regularities from randomness and complexity in environments are not well understood. Furthermore, environments can obviously change in randomness, complexity structure, and nature of regularities. Changes in regularities can alter the value of heuristics learned in a previous environmental state. Environments are inherently dynamic and complex. They are complex adaptive systems and can move through a variety of unpredictable environmental states across time. This raises many important issues regarding identification of managerial/organization heuristics and their robustness to various changes in environmental states.

Much more research is needed on all of these issues. The NK landscape model (Levinthal, 1997) might be useful in such research, but in the usual formulation it is totally random. Hence, it would be necessary to introduce some regularities and uncertainties that characterize real environments.

Type II Heuristics: Consciously Designed

At this point it is useful to introduce a second kind of heuristic, Type II Heuristics, that has a very different origin from Type I Heuristics. Above we discussed Type I Heuristics, those organizational heuristics that are directly the natural result of managers learning from experience. By contrast, Type II Heuristics are those heuristics that are consciously designed by consultants and/or firm managers rather than being the direct product of some form of induction process. Of course, it may be that design takes advantage of what managers believe they have already learned through induction about regularities in various environments.

Industrial organization economics, strategic management, and other fields have identified what can obviously be described as regularities in the environments of firms in variables such as market share, acquisitions, innovation, R&D, competitor preferences, and alliance types. Often these regularities have been related to various performance measures and other outcome measures. Obviously such regularities can be used to design potentially useful heuristics. Furthermore, this has likely happened before and will continue to happen. Such designed heuristics might lack the rigor, boundary conditions, and control variables of the original empirical work that is their origin, but they economize on time, information, and managerial attention.

To illustrate this possibility, we suggest how the BCG Portfolio Grid (e.g., Hedley, 1977) could have been developed. At the time it was “designed,” there were already well-established empirical regularities from economic studies tying market share within an industry to business performance, and industry growth rate to business performance and cash generation or usage. These can be easily mapped to the two dimensions of the grid: relative market share and relative growth rate. Bubbles sized to the sales or assets of each business can then be used to plot the businesses of the firm. It is an important design insight that the four quadrants can then lead to defining strategy and cash generation/usage roles for each of the businesses of a diversified firm and also lead to looking at the dynamics of the portfolio of businesses among the quadrants across life cycles. It is also worth noting that at this time the firms that extensively diversified during the conglomerate wave that started in the 1960s were encountering substantial problems managing their portfolio of businesses. This grid was likely seen as very useful in dealing effectively with such problems. In other words, there was a demand side to the story. This all leads to an obvious conjecture. Empirical academic research in industrial organization economics and strategic management may have substantial potential application not only in the possibility of directly informing managerial decisions directly as widely assumed by academics, but perhaps more importantly, allowing useful heuristics to be designed by consultants and managers that can inform managerial decision making while economizing on time, information, and managerial attention.

It is interesting to note that the portfolio grids discussed just above and earlier in the article seem to have survived selection pressures and thrived for about 46 years at the time of this article. This certainly seems to be a very long time in terms of relevant selection pressures.

Conclusion

This article addresses two major topics. First, some important decision problems that managers in organizations need to “decide” are likely intractable for organizations using the rational analytical decision technologies that are often prescribed. The concept of “organizational intractability” is intended to make it possible to identify such decision problems faced by organizations. Hopefully, others will use this theoretical approach to identify further examples of rational analytical technologies that are organizationally intractable.

Second, heuristics are appropriate, and probably the only appropriate approach, for organizationally intractable decision problems. More generally, heuristics are appropriate anywhere the need to economize on information, time, and management attention is important. Furthermore, heuristics are highly unlikely to result in a global optimum for strategic decision problems. In fact, as briefly discussed earlier, strategic decision problems tend to be “ill-structured” and/or “wicked problems.” For such problems, it is generally impossible to find optimal solutions without changing the nature of the problem so as to make the solution less meaningful or meaningless to the original problem. Thus, it is usually foolish to talk about optimal solutions to such problems since the problems are inherently so ambiguous. On these bases, a theory of strategic heuristics is a fundamental and necessary aspect of any comprehensive future theory of strategic management.

Finally, this article overall is suggestive of two major issues of broad and deep importance to strategic management. First, it is likely that a significant and perhaps substantial amount of strategic and other decision making relies on heuristics. Second, this suggests that firms may compete strategically to some important degree on the basis of the relative effectiveness of their strategic decision heuristics. Importantly, Amit and Schoemaker (1993) emphasize the heuristic nature of organizational rent creation. This raises important questions. Is a set of highly effective strategic heuristics a valuable firm resource? How does such a set of heuristics originate in a firm? How unique can such a set be? How reliable can such a set be? How robust are each of these heuristics to varying degrees of novelty in decision problems? How can these heuristics be maintained and updated across time without value destroying imitation or unconscious transfer to other firms?

Footnotes

Acknowledgements

I want especially to thank Phil Bromiley, for extensive and insightful comments at an early stage that were extremely helpful in developing the article. At a later stage, Michael Nippa provided many insightful comments that helped further develop the article and caused me to think deeply about a myriad of important issues beyond the scope of the current work. Travis Howell and Ling Xiao helped me construct the demonstration of organizational intractability and later provided useful comments on the article. Loock Moritz, Honggi Lee, Dani Blettner, Songcui Hu, Aleks Rebeka, and Kevin Miceli all provided useful comments. I also want to thank my department chair, Chris Bingham, and our senior associate dean at the time, Jennifer Conrad, for allowing me to use overload teaching credits to free up time to work on this article and several others. Finally, I particularly want to thank Cathy Maritan and Gwen Lee for their kind invitation to write an article for this special edition of the Journal of Management. This invitation ultimately stimulated a new stream of research, with this as the first article. This article is dedicated to Connor T. Bettis, my first grandchild, who was about 17 months old when I finished the final draft. He has already learned various social heuristics for successfully navigating his parental environment.