Abstract

How do home country institutions influence cross-border postacquisition performance? We develop an institutional framework showing that informal and formal institutions not only have important individual effects but also work together in complex and interesting ways. While collectivism and humane orientation (two major informal institutions) can facilitate postacquisition integration and firm performance, shareholder orientation and property rights protection (two formal institutions) constrain postacquisition integration and firm performance. As acquirers are simultaneously embedded in their home countries’ informal and formal institutions, we further hypothesize that the positive effects of collectivism and humane orientation can be weakened by incompatible formal institutions that hamper postacquisition collaborative efforts. We find strong support for our hypotheses in a multilevel analysis of a sample of 12,021 cross-border acquisitions involving 43 home and target countries between 1995 and 2003.

Keywords

Cross-border acquisition (CBA) activities totaled US$1.6 trillion in 2015, a 27% increase over 2014 (Thomson Reuters, 2016). CBAs have increasingly become one of the most important international strategies for firms to enhance their performance (Anand & Delios, 1997; Erel, Liao, & Weisbach, 2012; Haleblian, Devers, McNamara, Carpenter, & Davison, 2009; Shimizu, Hitt, Vaidyanath, & Pisano, 2004). However, prior studies suggest that many acquirers fail to gain value from CBAs (Huang, Zhu, & Brass, 2016; Lebedev, Peng, Xie, & Stevens, 2015; Shimizu et al., 2004). Accordingly, the major task for strategic management research is to identify the key factors influencing firm performance (Haleblian et al., 2009; Peng, Wang, & Jiang, 2008). Scholars have since endeavored to explain postacquisition performance of CBAs. In particular, given the nature of CBAs, much has been written on how cultural distance and host countries affect postacquisition performance (Chakrabarti, Gupta-Mukherjee, & Jayaraman, 2009; Huang et al., 2016; Reus & Lamont, 2009; Zhu & Qian, 2015; Zhu, Xia, & Makino, 2015).

Indeed, prior research has significantly advanced our understandings of integrating the costs and benefits associated with cultural distance in CBAs from the transaction cost economics perspective, the resource-based view, and the institution-based view (Barney, 1991; Peng et al., 2008; Williamson, 1975). Yet it is important to emphasize that the extent to which acquirers could realize the benefits and reduce the costs of CBAs may differ significantly, depending on the acquirers’ postacquisition integration approaches. Acquirers, as the owner of the combined firm, decide how to integrate with acquired foreign targets and manage the combined firm, which leads to their success or failure in gaining value from acquisitions. For example, Puranam, Singh, and Zollo (2006) found that in domestic technological acquisitions, acquirers choose to take different postacquisition approaches resulting in varying postacquisition innovation outcomes.

In addition to firm heterogeneity, institutional research suggests that how acquirers from different countries integrate with and manage their acquired foreign targets is constrained by their home country institutions (North, 1990; Peng et al., 2008; Scott, 2007). However, scholars have paid scant attention to the effects of home country institutions on postacquisition performance of firms. One of the exceptions is Capron and Guillén (2009), who argued that acquirers’ postacquisition integration capabilities are constrained by national corporate governance institutions that affect how resources and powers are distributed among various stakeholders of the combined firm. While their research adds to the understanding of the processes and dynamics of postacquisition integration from a home country institutional perspective, their research has not theorized and tested the direct effect on postacquisition performance. Addressing this direct effect is a key task for strategy researchers and has far-reaching practical implications for managers. Marano, Arregle, Hitt, Ettore, and van Essen’s (2016) meta-analysis of the effects of home country institutions on firms’ international performance suggests that home country institutions affect CBA performance. Our study thus addresses an important but previously underexplored research question: How do acquirers’ home country institutions influence the postacquisition performance of CBAs?

Our study endeavors to make three contributions. First, it contributes to the CBA literature by directing our attention to a key predictor of CBA postacquisition performance: acquirers’ home institutions that shape their postacquisition behaviors and performance. Second, postacquisition value creation in CBAs results from the effective integration between acquiring and target firms (Cording, Christmann, & King, 2008). Such integration requires the “interdependence” perception of acquiring firms toward acquired foreign targets, which tends to be incorporated into acquirers’ behaviors and approaches in managing acquired target firms (Kale, Singh, & Raman, 2009). On the basis of the institution-based view and acquisition research, we propose an institutional framework that includes two informal institutions (collectivism and humane orientation) and two formal institutions (shareholder orientation and property rights protection) that can significantly influence the acquirers’ perceptions of interdependence (Chan, Isobe, & Makino, 2008; Makino, Isobe, & Chan, 2004; Peng, 2003; Peng et al., 2008). This institutional framework contributes to our knowledge of which home country institutions matter in CBA performance.

Lastly, the limited earlier attention on the effects of home country institutions may be a result of previous CBAs’ primarily originating from a single home country (often the United States), resulting in little variation of home countries of acquirers. Recently, many non-U.S. firms have started to acquire firms outside of their national borders (Ambrosini, Bowman, & Schoenberg, 2011; Barkema & Schijven, 2008; Erel et al., 2012; King, Dalton, Daily, & Covin, 2004; Kling, Ghobadian, Hitt, Weitzel, & O’Regan, 2014; Lebedev et al., 2015; Sun, Peng, Ren, & Yan, 2012; Zhu & Zhu, 2016). This provides us an ideal setting to theorize the effects of home country institutions on postacquisition performance of CBAs. With a large sample of 12,021 CBAs from 41 countries between 1995 and 2003, we use advanced multilevel modeling, which takes into account the nonindependence among firms within the same national institutional environment (Hitt, Beamish, Jackson, & Mathieu, 2007; Hox, 2002) and, thus, can better show the effects of institutions on firm outcomes. Our results support the idea that home country institutions influence postacquisition performance of CBAs.

Theory and Hypothesis Development

CBA Performance

Given the increasing popularity and importance of CBAs, scholars have devoted great efforts in understanding CBA performance, including short-term stock market returns and long-term performance (Ahern, Daminelli, & Fracassi, 2015; Alimov, 2015; Bertrand & Capron, 2015; Huang et al., 2016; Karolyi & Taboaa, 2015; Shimizu et al., 2004). Yet studies have found that many acquirers fail to create short-term or long-term value from their CBAs. Acquirers pay close attention to investors’ reactions to CBA announcements because of their effects on stock prices. However, prior research suggests that investors’ reactions to CBA announcements do not necessarily predict acquirers’ long-term CBA performance (Zollo & Meier, 2008). Acquirers’ long-term CBA performance is largely the result of very challenging postacquisition integration efforts that typically have not started when CBAs are announced. These postintegration challenges may not be easily predicted by investors in the short time span after CBA announcements. Scholars have therefore focused more on understanding of postacquisition long-term performance—the focus of our study—from different theoretical perspectives (Alimov, 2015; Huang et al., 2016).

Grounded in transaction cost economics and the resource-based view, earlier research argues that dominant U.S. acquirers in the 1990s could exploit their superior resources and internalize transaction costs through CBAs compared with other entry modes, such as greenfield investments (Barney, 1991; Morck & Yeung, 1992; Williamson, 1975). However, some studies show that these earlier CBAs underperformed because CBAs involve significant postacquisition integration challenges with foreign acquired targets (J. Li & Guisinger, 1991; Nitsch, Beamish, & Makino, 1996). One key cost is derived from cultural distance between home and host countries that largely results from the liability of foreignness as well as uncertainties and risks in targets and host countries (Stahl & Voigt, 2008). While some researchers proposed a negative effect of cultural distance on postacquisition performance (Stahl & Voigt, 2008), findings are mixed (Chakrabarti et al., 2009; Morosini, Shane, & Singh, 1998).

Taking an organizational learning perspective, scholars argue that acquirers can learn from acquired foreign targets located in culturally distant host countries and, thus, build new capabilities to survive (Reus & Lamont, 2009; Vermeulen & Barkema, 2001). These learning benefits could outweigh the cultural distance costs involved in CBAs. Acquirers could also learn about host countries from earlier CBA experience to reduce the liability of foreignness and, thus, could perform better (Barkema, Bell, & Pennings, 1996). This line of research has built up a solid foundation for us to further improve our understanding of long-term postacquisition performance of CBAs from a home country institutional perspective.

Home Country Institutions

While learning from foreign targets in host countries can affect CBA performance (Reus & Lamont, 2009; Vermeulen & Barkema, 2001), we suggest that the institutions of an acquirer’s home country may also affect CBA performance. Institutions capture the fundamental structure of a nation, which promotes or constrains certain behaviors of firms embedded in these nations (North, 1990; Scott, 2007). The institution-based view suggests that country institutions consist of two major categories: informal and formal institutions (Capron & Guillén, 2009; Martin, Cullen, Johnson, & Parboteeah, 2007; Meyer & Peng, 2016; North, 1990; Scott, 2007). While informal institutions (such as cultural values) represent noncodified norms, shared meanings, and collective understandings endured across generations within a country (Holmes, Miller, Hitt, & Salmador, 2013; Scott, 2007), formal institutions represent codified rules, laws, and regulations designed to regulate economic activities (North, 1990; Pinkham & Peng, 2016). Therefore, we examine how both informal and formal institutions in home countries affect acquirers’ integration with acquired foreign firms to create value.

We propose an integrated institutional framework that consists of the informal institutions collectivism and humane orientation as well as the formal institutions shareholder orientation and property rights protection. These informal and formal institutions shape the interdependence perceptions between acquirers and foreign targets and subsequently influence acquirers’ postacquisition integration behaviors and capabilities in CBAs. Collectivism refers to “the degree to which individuals express pride, loyalty, and cohesiveness in their organization” (House, Hanges, Javidan, Dorfman, & Gupta, 2004: 465). Humane orientation is defined as “the degree to which a collective encourages and rewards individuals for being fair, altruistic, generous, caring, and kind to others” (Hoppe, 2007: 1). While other informal institutions, such as performance orientation, uncertainty avoidance, and assertiveness, influence postacquisition integration and value creation, they may not shape acquirers’ interdependence perception in the same way as humane orientation and collectivism. For example, power distance may destroy the hierarchical relationship between acquirers and targets instead of an interdependent perception (Huang et al., 2016). Therefore, we focus on collectivism and humane orientation as informal institutions.

While prior research examined a variety of formal institutions, such as labor regulations and political institutions (Alimov, 2015; Capron & Guillén, 2009; Hall & Soskice, 2001; Henisz, 2003; Pinkham & Peng, 2016), two important formal institutions—shareholder orientation and property rights protection—are fundamental institutions across countries and tend to shape acquirers’ interdependence perceptions. Other formal institutions, such as political institutions, affect postacquisition performance in different ways, such as increased transaction costs in politically instable countries (Hall & Soskice, 2001; Henisz, 2003). Shareholder orientation and property rights protection are built upon the value maximization of shareholders regardless of other stakeholders and the ownership of acquiring firms over acquired targets (Capron & Guillén, 2009). Firms growing in these institutional environments tend to focus on the interests of a subgroup, such as shareholders, instead of the combined collective (Capron & Guillén, 2009). As a result, acquirers from home countries with different levels of these two formal institutions may form various postacquisition interdependence perceptions and, thus, adopt varying integration approaches resulting in different levels of postacquisition performance.

Importantly, informal and formal institutions do not work in isolation (Aguilera & Jackson, 2010; Hall & Soskice, 2001; Jackson & Deeg, 2008). We therefore examine how informal institutions interact with formal institutions that may strengthen or weaken the interdependence perceptions of acquiring firms in integrating with acquired foreign targets. Our research framework is presented in Figure 1.

Theoretical Model

Informal Institutions of Acquirers’ Home Countries

Home country collectivism

Acquirers that are shaped by home country collectivism have managers who view themselves as highly interdependent with their organizations. In particular, their job security and welfare depend on the success of their organizations, in which they express pride and loyalty and enjoy cohesiveness. These managers often have long-term contracts with the organization and lower mobility outside of their organizations (House et al., 2004). After CBAs, they are motivated to strive for the effective integration with acquired foreign targets (i.e., organizational goals) that are viewed by acquirers as an “interdependent” part of their organizations. Only successful integration with acquired targets can add value to acquirers (Djelic & Quack, 2008; Powell & Colyvas, 2008). Some of these managers may even be willing to sacrifice their personal interests in a short term to accomplish organizational goals (effective integration). In return for their personal sacrifice, managers expect their long-term job security and welfare. For example, Lenovo’s managers in China can tolerate their much lower salaries than their counterparts in the United States after Lenovo’s acquisition of IBM’s PC division, which facilitates the smooth postacquisition integration.

Viewing acquired targets as “interdependent” units and striving for collective value creation, such acquirers believe that it is their obligation to help acquired targets through sharing information with them, addressing their concerns, and lowering their great uncertainties after CBAs (Krug & Nigh, 2001; Very, Lubatkin, & Calori, 1996). For example, some Japanese firms invite foreign managers and employees to Japan before integration efforts begin (Brannen & Peterson, 2009). The Global Leadership and Organizational Behavior Effectiveness (GLOBE) study’s (House et al., 2004) culture and leadership research shows that managers of acquirers from collectivism cultures tend to collectively make decisions by taking into account different divisions’ interests. Treating acquired targets as new interdependent units, these managers tend to involve acquired targets in postacquisition decision making, respect their opinions, and value consensual decision making. As a result, collectivism-oriented acquirers are likely to foster effective cooperation and integration between acquiring and acquired firms (Chen, Peng, & Saparito, 2002).

On the other hand, acquirers that have been influenced by home country institutions with low levels of collectivism tend to strive for self-achievement (Chen et al., 2002; Markus & Kitayama, 1991) instead of collective goals (i.e., effective postacquisition integration). Because managers’ hiring and welfare are based on their personal competence and performance, their contracts with organizations are transactional, and they tend to have job opportunities outside of their organizations. However, in such a setting, organizational and personal goals tend to conflict in postacquisition integration processes. For example, managers from such acquirers value accountability and personal autonomy in their jobs, but postacquisition integration requires cooperation with acquired targets. This interdependence with acquired targets may blur personal accountability and autonomy because of heightened needs for collaboration. Furthermore, seeing that postacquisition integration is full of uncertainties and challenges, managers at the acquiring firm may exit the firm because of lower attachment to their organization. The increased turnovers at acquirers result in chaos and difficulties in postacquisition integration and value destruction.

Acquirers with lower levels of collectivism often view helping acquired targets as personal choices instead of obligations, leading them to carefully balance the costs and benefits of exerting efforts to help foreign targets (House et al., 2004). These acquirers are also less likely to seek help from others when they experience stress and encounter difficulties during postacquisition integration processes. Their independent, rather than interdependent, view of themselves may deter the communication and collaboration between acquirers and targets. Managers of these acquirers with individualistic goals are also often independent in decision making and less likely to involve acquired targets in postacquisition integration decisions. Furthermore, in spite of the uncertainties acquired targets encounter and the potential resistance of acquired targets towards the new owners, these managers may be more aggressive in unleashing postacquisition actions (such as mass layoffs). The result may be counterproductive in postacquisition performance (Krishnan, Hitt, & Park, 2007). Thus:

Hypothesis 1: There is a positive relationship between the level of an acquirer’s home country collectivism and its cross-border postacquisition performance.

Home country humane orientation

Informal institutions embodied in a home country’s humane orientation reward and encourage the support to others instead of self-enhancement in an organization. As a result, acquirers shaped by high levels of humane orientation can prioritize humane-oriented support to acquired targets in postacquisition integration processes. In contrast, firms with low levels of humane orientation tend to emphasize task efficiency with less consideration about acquired targets’ humane needs for support in postacquisition integration processes. The priority toward humane-oriented considerations of acquired targets may be vital in facilitating postacquisition integration and performance. Being acquired by foreign firms is highly stressful for acquired targets, which results in a sense of loss of control and alienation, antagonism, condescending attitudes, distrust, tension, and hostility toward acquiring firms (Brannen & Peterson, 2009; Larsson & Finkelstein, 1999). Prior studies demonstrated that such negative emotions of acquired targets are associated with lower commitment to and cooperation with acquiring firms (Very et al., 1996). Therefore, one of the first issues that acquirers need to address in postacquisition integration is to alleviate such negative emotions and destructive outcomes brought by negative emotions. Acquirers with high levels of humane orientation can provide such support (House et al., 2004; Reus, 2012). During postacquisition integration processes, such acquirers endeavor to understand targets’ uncertainties, stress, and needs.

Second, acquirers with humane orientation may establish rapport with and win acquired targets’ trust by supporting acquired targets. Under such circumstances, acquirers can start to integrate with acquired targets that view themselves as interdependent with acquirers (Bresman, Birkinshaw, & Nobel, 2010; Kale et al., 2009). Managers of acquirers with high levels of humane orientation are less likely to emphasize their self-achievement and enhancement but are more willing to involve managers of acquired targets in postacquisition decision making in creating value for the combined firms. In contrast, when acquirers with low levels of humane orientation ignore acquired targets’ humane needs and merely emphasize the implementation of integration tasks, acquired targets’ negative emotions, such as sense of loss of control and alienation, are likely to become stronger (Brannen & Peterson, 2009). As a result, there may be acquired targets’ resistance to the integration and even high rates of turnover that may undermine postacquisition performance.

Hypothesis 2: There is a positive relationship between the level of an acquirer’s home country humane orientation value and its cross-border postacquisition performance.

Formal Institutions of Acquirers’ Home Countries

Home country shareholder orientation

Countries may be categorized into shareholder oriented or stakeholder oriented (Hall & Soskice, 2001; Kacperczyk, 2009). Shareholder-oriented countries prioritize the interests of shareholders over other stakeholders, such as customers, employees, and communities. In contrast, stakeholder-oriented countries promote the interests of stakeholders more generally, of which shareholders are only one constituent.

Acquirers that have been influenced by home country institutions reflecting strong shareholder orientation are more likely to pay primary attention towards the interests of shareholders, in particular paying close attention to short-term shareholder value (Capron & Guillén, 2009). These acquirers may be pressured by shareholders to extract value from foreign targets, which raises the share price and appeases shareholder pressures (Connelly, Tihanyi, Certo, & Hitt, 2010). Acquirers may therefore endeavor to keep short-term costs under control through layoffs and divestitures to improve efficiency (Capron & Guillén, 2009). However, following narrow shareholder pressures may not necessarily improve postacquisition performance. For instance, acquirers typically have limited knowledge of targets, which largely constrains acquirers’ ability to identify key employees and managers to achieve successful integration (Cannella & Hambrick, 1993). Thus, the restructuring of assets and top management teams may lead to the turnover of key managers of the acquired targets who are dissatisfied with the postacquisition integration plans (Cannella & Hambrick, 1993; Krug, 2003). The loss of key personnel in targets may significantly reduce acquirers’ abilities to reap value from acquired foreign targets (Cannella & Hambrick, 1993).

In contrast, acquirers from home countries with lower levels of shareholder orientation may be better able to cater to all stakeholders because they are less constrained by narrow shareholder pressures (Kacperczyk, 2009). This allows acquirers to spend the necessary time and resources to understand the acquired targets’ customers, employees, and communities. Moreover, acquirers can establish trust with acquired targets before restructuring the combined firms if more stakeholder interests are considered (Freeman, Wicks, & Parmar, 2004; Kale et al., 2009). Not exclusively focusing on shareholders thus enables acquirers to build relationships with more nonshareholder stakeholders of acquired targets. Therefore, such stakeholders are more likely to cooperate and integrate to achieve better postacquisition performance. Thus:

Hypothesis 3: There is a negative relationship between the level of an acquirer’s home country shareholder orientation and its cross-border postacquisition performance.

Home country property rights protection

Property rights protection refers to the extent to which property rights are clearly defined and effectively enforced in a country (Carruthers & Ariovich, 2004; Hart & Moore, 1990; North, 1990). Property rights consist of the rights to possess, use, consume, and obtain income from a target that is perceived to be owned (Foss & Foss, 2005). Shaped by strong property rights protection institutions, acquirers in CBAs obtain their property rights over acquired targets in order to gain high payoffs from such investments (North, 1990; Tsang & Yip, 2007). These acquirers have a strong sense of ownership over acquired targets (Pierce, Kostova, & Dirks, 2001). They strongly believe that they have the right to decide how to manage and integrate with acquired targets to create value and how to distribute the newly created value between acquirers and acquired targets (Mahoney, Asher, & Mahoney, 2004). This postacquisition integration and value distribution decision making is less likely to involve acquired foreign targets. However, acquired targets’ dissatisfaction with acquirers’ postacquisition integration and value distribution may negatively affect whether and how much acquirers could create value from CBAs through targets’ high turnovers, tardiness, and tacit resistance.

In contrast, acquirers from weak property rights protection countries, based on their home country experience, often believe that in addition to owners, other stakeholders can also play a critical role in firms’ profit making (Henisz, 2003; Holburn & Zelner, 2010). Transferring such experience to CBAs, acquirers are more likely to recognize that acquired targets, as nonseparable interdependent units, are important stakeholders (rather than objects that can be owned and exploited). These acquirers are likely to see targets’ involvement and assistance in postacquisition periods as an important role in improving postacquisition performance. These acquirers thus may respect acquired targets’ opinions, fulfill their needs and expectations, and humbly learn from them to create more value in the combined firms. Thus:

Hypothesis 4: There is a negative relationship between the level of an acquirer’s home country property rights protection and its cross-border postacquisition performance.

Joint Influence of Acquirers’ Home Country Informal and Formal Institutions

In addition to the direct effects proposed earlier, we suggest that formal institutions may also weaken the effects of informal institutions on postacquisition performance (Holmes et al., 2013; Yamagishi, Cook, & Watabe, 1998). Transmitted from one generation to the next, informal institutions are often “durable, long-lasting, and relatively stable, with incremental changes occurring slowly” (Holmes et al., 2013: 533). Formal institutions, on the other hand, are established as a response to problems in a society, but the logic and rationale according to which formal institutions are designed are often influenced by informal institutions in that society (Yamagishi et al., 1998). For example, property rights protections as formal institutions are built upon individualism in the United States (Hall & Soskice, 2001). However, some countries in recent years have imported from abroad formal institutions such as shareholder orientation and property rights protection because these formal institutions have been demonstrated to facilitate economic growth (Weber, Davis, & Lounsbury, 2009). These imported formal institutions may be inconsistent with the prevailing informal institutions (Hall & Soskice, 2001). Such incompatible formal institutions may promote unintended behaviors that undermine the positive effects of informal institutions (Aguilera & Jackson, 2010; Chan et al., 2008; Jackson & Deeg, 2008; Peng, 2003). Given the coexistence of long-lasting informal institutions and potentially incompatible formal institutions, we further examine their joint effects on CBA performance.

Collectivism × Shareholder Orientation

Collectivism facilitates the shared interests and collaboration in the postacquisition combined firms. However, high levels of shareholder orientation may disrupt this collective spirit and interdependent identity through prioritizing shareholders’ demands for short-term returns from acquisitions. Specifically, while collectivism-oriented acquirers may prefer to help acquired targets to identify and integrate with the acquiring firms (House et al., 2004), the pressures to increase share price in the short term due to strong shareholder orientation do not allow them to prioritize the establishment of an interdependent identity within the postacquisition combined firm. On the contrary, shareholder pressures may force collectivistic-oriented acquirers to take immediate actions to cut costs through mass layoffs and divestitures—one of the easiest and quickest ways to generate profits (Krishnan et al., 2007). While collectivism-oriented acquirers are hesitant to behave in this shortsighted manner, which is against their collectivistic values, they may have to do so because they face the threat of being punished by impatient stockholders. The conflicting institutions result in the collectivism-oriented acquirers’ espousing noncollectivistic behaviors, which are in direct conflict with each other. These contradictory actions may confuse stakeholders such as employees at acquired firms, who may become further distressed after the acquisitions. As a consequence, these stakeholders may become more hesitant to collaborate with acquirers, which hinders postacquisition performance.

Conversely, weak shareholder orientation may promote the collective spirit and interests, as collectivism does. In particular, weak shareholder orientation in home countries may impose fewer pressures on acquirers to boost share price immediately after acquisitions, which may enable collectivism-oriented acquirers to spend sufficient time on building a collective identity. Large-scale restructurings during the postacquisition period to create value for the combined firm are likely to be acceptable in the long run. Therefore, weak shareholder orientation may reinforce the positive effects of collectivism on the interdependence, collaboration, and integration with acquired foreign firms to create value. Thus:

Hypothesis 5a: An acquirer’s home country shareholder orientation negatively moderates the positive relationship between the level of the acquirer’s home country collectivism and its cross-border postacquisition performance.

Humane Orientation × Shareholder Orientation

As discussed earlier, humane-oriented acquirers extend their support to acquired targets during and after the acquisition and, thus, help to facilitate the collaboration and integration with acquired targets (House et al., 2004). However, strong shareholder orientation may disrupt the collaborative tendency fostered by humane orientation. Humane-oriented acquiring firms influenced by home country shareholder orientation may be forced to direct their attention and resources from how to support acquired targets to increasing share price after the acquisition. If acquiring firms do not take actions to increase the share price, they are likely to be penalized by stock markets with lower share prices and face threats of being acquired themselves (Walsh & Kosnik, 1993). From the standpoint of postacquisition integration, the actions to increase share price in the short term are often harmful and may cause chaos within the postacquisition combined firms (Capron & Guillén, 2009). Such actions may also cause acquired firms to doubt the humane-oriented support from acquiring firms, which shakes the trust and cooperation from the acquired firms.

In contrast, weak shareholder orientation does not shape acquirers to view shareholder interests as the primary goal. Instead, such acquirers may focus more on promoting the interests of acquired targets as one of the key contributors in the combined firm. As a result, humane-oriented support received by the acquired targets may be reinforced instead of being reduced or undermined in the postacquisition integration processes. Thus,

Hypothesis 5b: An acquirer’s home country shareholder orientation negatively moderates the positive relationship between the level of the acquirer’s home country humane orientation value and its cross-border postacquisition performance.

Humane Orientation × Property Rights Protection

We expect that acquirers shaped by both strong home country humane orientation and property rights protection reduce postacquisition performance. As discussed earlier, humane-oriented acquirers may extend the support toward acquired targets and facilitate the formation of intraorganizational interdependence as well as shared identity in combined firms for postacquisition integration and value creation. However, the coexistence of strong property rights protection that shapes the perception of acquired firms as independently owned units, at least in the short term, may change the perception of humane orientation of acquirers. In particular, these acquirers may change the mind-set and dominant logic to take it for granted that acquiring firms, as new owners, possess the rights to make their own decisions to manage acquired targets and that acquired targets have to follow the rules of the game imposed by the new owners. As a consequence, these acquirers become less considerate toward acquired targets and less likely to take into account acquired targets’ needs in postacquisition integration processes. Targets that go through uncertain and stressful postacquisition periods may become alienated and are hesitant to cooperate with acquiring firms, which will suppress the positive effects of humane orientation.

On the other hand, acquirers influenced by weak property rights institutions may strengthen the belief of humane-oriented acquirers that the acquired targets are critical and interdependent stakeholders in postacquisition integration and value creation. For example, seeing acquired targets such as IBM’s PC division under great stress and anxieties after the acquisition, acquirers such as China’s Lenovo tend to take every action (e.g., promise not to lower salaries) to reduce anxieties and fulfill the needs of foreign targets because they are perceived as interconnected units (G.-G. Li & Xu, 2010). As a result, acquired targets become closer to acquirers and more willing to cooperate with their new owners. The interdependence and integration facilitated by humane orientation are further strengthened rather than reduced. Thus:

Hypothesis 6: An acquirer’s home country property rights protection negatively moderates the positive relationship between the level of the acquirer’s home country humane orientation and its cross-border postacquisition performance.

Method

Sample and Data Collection

We used three criteria to amass a data set on a worldwide basis. First, acquirers and targets should be located in any 2 of the 50 countries/regions on which we have full information. Second, the announcement dates of CBAs must be between 1995 and 2003 (inclusive). During this period, many governments with varying levels of institutional development were liberalizing their economies to foreign investors. As a result, the number of CBAs grew significantly. Thus, our examination of the effects of home country informal and formal institutions on CBA performance is not only theoretically important but also practically relevant and timely. Third, acquirers should be publicly listed firms so that we could access their financial information.

We collected annual financial data for acquirers and targets from Datastream, home and host countries’ collectivism and humane orientation from the GLOBE study (House et al., 2004), home and host countries’ property rights protection from Economic Freedom of the World (Gwartney et al., 2009), and shareholder orientation from Djankov, La Porta, Lopez-de-Silanes, and Shleifer (2008). Because Datastream does not provide all financial information for all acquirers and targets, we did not include CBAs for which acquirers’ financial data are not available. The final sample includes 12,021 CBAs involving 4,130 acquirers in 41 home countries and 11,096 targets in 43 host countries in the 8-year period.

Variables

Dependent variable

Consistent with prior studies of firm performance in international markets (Chan et al., 2008) and of postacquisition performance (Cording et al., 2008; Hult et al., 2008; Kapoor & Lim, 2007; Krishnan et al., 2007; Laamanen & Keil, 2008), our study measured CBA performance by using acquirers’ return on sales (ROS) 3 years after CBA announcements. Because ROS includes two flow measures (pretax income and net sales), it is less influenced by inflation and accounting standards than return on assets (Chan et al., 2008). Therefore, acquirers’ ROS can more accurately reflect their CBA performance than return on assets.

Independent variables

To measure collectivism in the home country, we used organizational in-group collectivism, which captures “the degree to which individuals express pride, loyalty, and cohesiveness in their organization” (House et al., 2004: 46). For humane orientation in the home country, we used “the degree to which a collective encourages and rewards individuals for being fair, altruistic, generous, caring, and kind to others” (Hoppe, 2007: 1). We used the GLOBE scales to measure these two informal institutions in the home country (House et al., 2004). Also, we used a time-invariant measure of informal institutions because although formal rules change, informal institutions change much slower (Greif & Tabellini, 2010; Hofstede, 2007). Furthermore, prior studies have demonstrated the construct reliability and validity of the GLOBE measures (Gupta, Sully de Luque, & House, 2004; Rossi, Wright, & Anderson, 1983; Webb, Campbell, Schwartz, & Sechrest, 2000).

Shareholder orientation in the home country

We employed the anti-self-dealing index developed by Djankov et al. (2008) to measure the shareholder orientation in the home country. This index captures the effectiveness of shareholder orientation. Djankov et al. also found that the anti-self-dealing index has a significant effect on stock market development. As such, we expect that the stronger the shareholder orientation, the more likely shareholders assert their rights. Because laws do not change significantly over time, we used the cross-sectional index for 2003 to measure shareholder orientation in this study.

Property rights protection in the home country

Following Meyer, Estrin, Bhaumik, and Peng (2009) and Ashby, Bueno, and McMahon (2011), we used the legal structure and security of the property rights index from Economic Freedom of the World (Gwartney et al., 2009) to measure property rights protection in the home country. This index is based on seven components: (1) judicial independence, (2) impartial courts, (3) protection of property rights, (4) military interference in rule of law and political process, (5) integrity of the legal system, (6) legal enforcement of contracts, and (7) regulatory restrictions on the sale of real property (Gwartney et al., 2009). These seven ratings were then averaged to arrive at the final index of property rights protection. While this source presents data for 1995 and for the years from 2000 to 2003, it does not contain data for the 1996 to 1999 period. To compensate for this, we linearly interpolated intervening years (Marquis & Huang, 2010).

Control variables

We have controls across country, industry, firm, deal, and year levels:

As host country institutions may affect acquirers’ CBA performance (Capron & Guillén, 2009; Reus & Lamont, 2009), we controlled for the host country collectivistic cultural value, humane orientation, shareholder orientation, and property rights protection. The institutions in host countries were measured the same way as those in home countries.

We controlled for gross domestic product (GDP) per capita of home and host countries because economic development in home and host countries is likely to affect firms’ international performance.

We controlled for acquirers’ host country acquisition experience, which is measured by acquirers’ total number of acquisitions within the focal host country in the 3-year period prior to the focal CBA announcement. Previous research suggests that firms’ acquisition experience in the focal host country can influence acquirers’ CBA performance (Haleblian & Finkelstein, 1999).

On the basis of previous findings that the method of payment for an acquisition (cash or stock) may influence CBA performance (King et al., 2004), we created a dummy variable to control for method of payment. We coded cash payments as 0 and use of shares as 1, and if acquirers use both methods, we coded the dominant method of payment.

Following Haleblian and Finkelstein (1999), we adopted a continuous measure of relatedness to control acquirer-to-target product relatedness because firms pursuing related diversification strategies tend to outperform those pursuing unrelated strategies. If Standard Industrial Classification (SIC) codes of the acquirer and target match, the acquisition was assigned a 2 at the two-digit level, a 3 at the three-digit level, and a 4 at the four-digit level match. If there are no matches, the acquisition was assigned a 1.

Following Krishnan et al. (2007) and McDonald, Westphal, and Graebner (2008), we controlled for acquirer slack, measured as the debt-to-equity ratio at the end of the year prior to a CBA announcement.

We controlled for acquirer performance, measured as the average of acquirers’ ROS in the preceding 3 years prior to the announcement date of the CBA (McDonald et al., 2008) because firms with better financial performance are more likely to achieve acquisition success (Morck, Shleifer, & Vishny, 1990).

We controlled for the percentage of target firms’ shares acquirers own after the acquisition, which is likely to influence how the gains are shared between acquirers and targets and, thus, affect the integration between them and CBA performance.

We controlled for the cultural distance between home and host countries (Kogut & Singh, 1988). Country culture scores, excluding those of collectivism and humane orientation, were obtained from GLOBE (House et al., 2004). We used a Euclidean distance measure to represent cultural distance.

We controlled for industry effects by including acquirers’ two-digit primary SIC codes (McDonald et al., 2008) and for period effects by including the linear time trend variable that ranges from Year 0 to Year 8 to represent the year of CBA announcement (Dobbin & Dowd, 1997).

Hierarchical Linear Modeling (HLM)

We adopted HLM to test hypotheses because acquirers and targets are nested in home and host countries and because HLM takes into account nonindependence among firms within the same country’s institutional environment (Hitt et al., 2007; Hox, 2002). Since we were mainly interested in testing the main and interactive effects of home country institutions (Level 2) on acquirers’ CBA performance, we used random-intercept HLM models.

Moreover, because CBAs involving the same home and host countries are influenced by the same institutional environment (home and host country institutions), we classified CBAs involving the same home and host country in the same Level 2 cluster. Thus, 739 Level 2 clusters are ordered home-host country dyads.

We centered Level 1 variables at the grand mean to reduce the correlation between the intercept and slope estimates across Level 2 dyads. By doing so, we alleviated potential Level 2 estimation problems due to multicollinearity (Hofmann & Gavin, 1998). We also centered Level 2 variables at the grand mean (i.e., the mean across the sample) to test interaction effects at Level 2, which helps to avoid multicollinearity and estimation difficulties, and to facilitate interpretation (Bryk & Raudenbush, 1992; Cohen, Cohen, West, & Aiken, 2003).

Results

Table 1 presents descriptive statistics and correlations. Property rights protection and collectivism are highly correlated. Given their high correlations, we controlled for and tested their effects in separate models (Cohen et al., 2003). As such, we minimized the multicollinearity caused by including these two highly correlated institutions in the same model and ensured that our results and interpretation are valid. We further examined variation inflation factors (VIFs) of predictors for each hypothesis test. The average VIF score is 1.21, and the range of VIF scores of predictors is between 1.02 and 3.92. These results suggest that multicollinearity is not a major concern.

Descriptive Statistics and Correlations

Note: N = 12,021. ROS = return on sales; SIC = Standard Industrial Classification; GDP = gross domestic product.

Absolute value of the number was multiplied by 100.

p < .10.

p < .05.

p < .01.

p < .001.

The null model, in which neither Level 1 nor Level 2 variables were specified, was tested to determine whether there are statistically significant between–Level 2 (ordered home-host country dyad) variances in the dependent variable. Results show that between–Level 2 dyads variance is statistically significant (sigma_u = 0.032, p < .001). Thus, we can proceed to test hypotheses by using multilevel modeling.

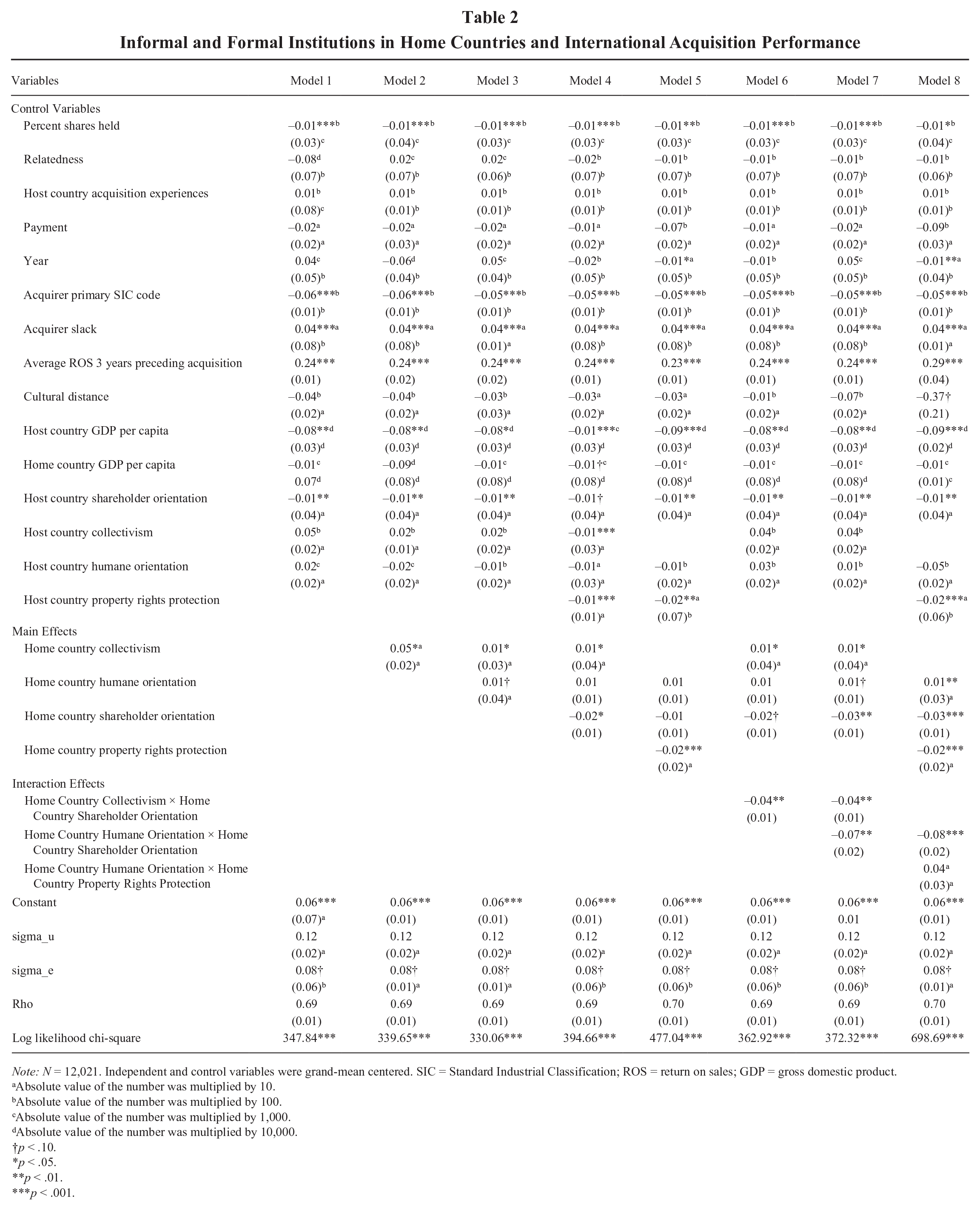

Table 2 shows the results of HLM analyses. For Hypothesis 1, we expected that an emphasis on collectivism in home countries leads to enhanced acquirers’ CBA performance. Model 2 indicates that the coefficient for collectivism in home countries is positive and statistically significant (p < .05). Therefore, Hypothesis 1 is supported. Furthermore, Hypothesis 2 predicted a positive relationship between acquirers’ humane orientation in home countries and acquirers’ CBA performance. In Model 3, the coefficient for humane orientation in home countries is positive and statistically significant (p < .10). Thus, Hypothesis 2 receives support.

Informal and Formal Institutions in Home Countries and International Acquisition Performance

Note: N = 12,021. Independent and control variables were grand-mean centered. SIC = Standard Industrial Classification; ROS = return on sales; GDP = gross domestic product.

Absolute value of the number was multiplied by 10.

Absolute value of the number was multiplied by 100.

Absolute value of the number was multiplied by 1,000.

Absolute value of the number was multiplied by 10,000.

p < .10.

p < .05.

p < .01.

p < .001.

We also expected that shareholder orientation in home countries is negatively associated with postacquisition performance. Model 4 shows that the coefficient for shareholder orientation in home countries is negative and statistically significant (p < .05). Thus, Hypothesis 3 is supported. The effects of property rights protection in home countries on postacquisition performance are shown in Model 5 to be negative and statistically significant (p < .001). This result supports Hypothesis 4.

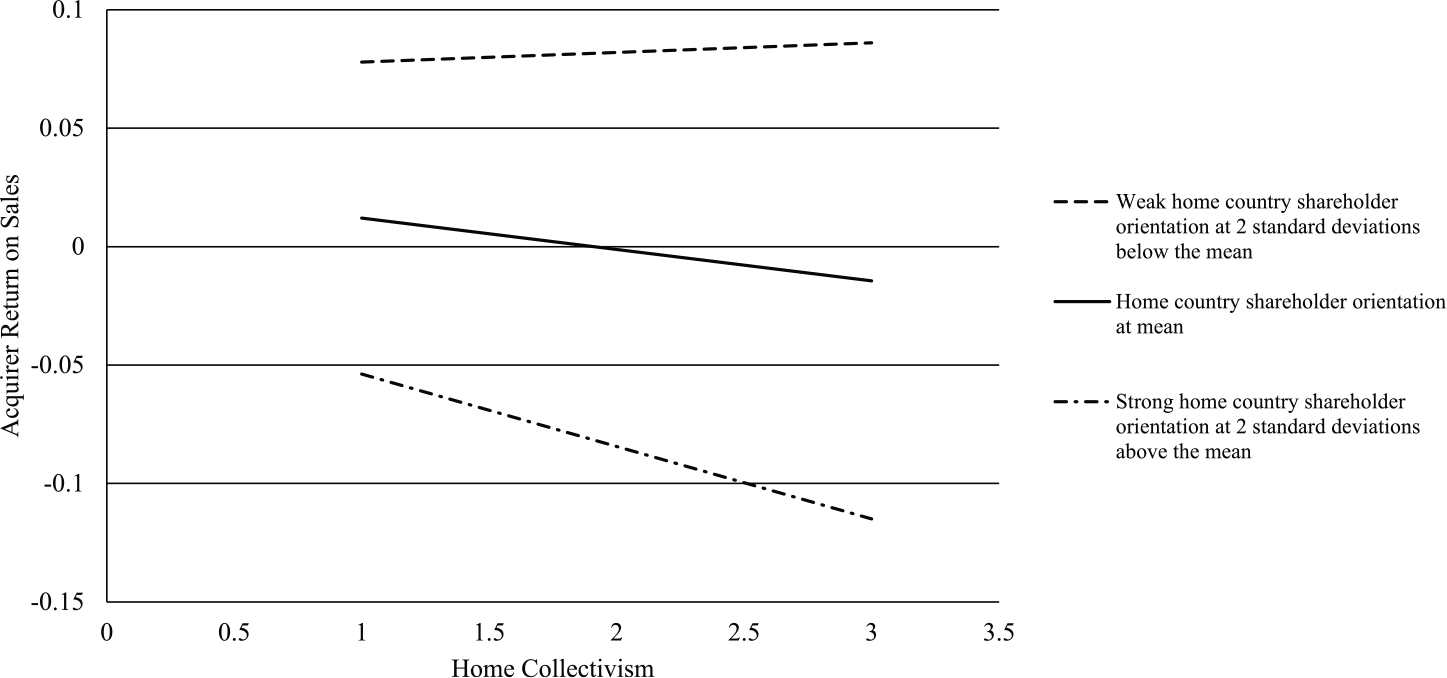

Hypothesis 5a predicted the moderating effects of shareholder orientation in home countries on the positive relationship between collectivism in home countries and acquirers’ CBA performance. In Model 6, the coefficient for collectivism in home countries is positive and statistically significant (p < .05), the coefficient for shareholder orientation in home countries is negative and statistically significant (p < .10), and the coefficient for the product term of collectivism and shareholder orientation in home countries is negative and statistically significant (p < .01).

Accordingly, Figure 2 shows that when shareholder orientation in home countries is weak, collectivism in home countries is positively related to acquirers’ CBA performance. Yet when home country shareholder orientation is strong, the relationship becomes negative. Overall, these results consistently and strongly support Hypothesis 5a.

Shareholder Orientation as a Moderator of the Relationship Between Collectivism and Cross-Border Acquisition Performance

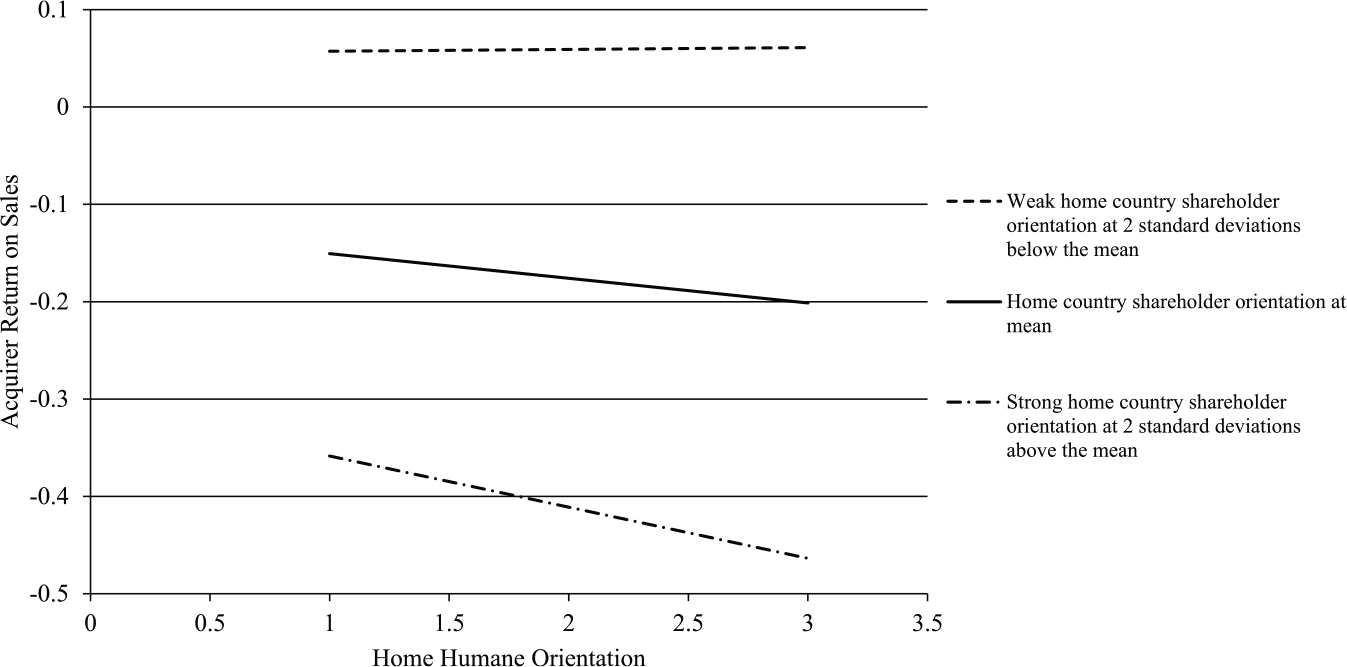

In Model 7, the coefficient for humane orientation in home countries is positive and statistically significant (p < .10), the coefficient for shareholder orientation in home countries is negative and statistically significant (p < .01), and the coefficient for the product term of humane orientation and shareholder orientation in home countries is negative and statistically significant (p < .01). Hence, these results strongly support Hypothesis 5b. Furthermore, as Figure 3 illustrates, under conditions of weak shareholder orientation in home countries, the cultural value of humane orientation is a predictor of positive CBA performance. In contrast, when home countries’ shareholder orientation is strong, humane orientation is negatively related to CBA performance. Overall, these results consistently and strongly support Hypothesis 5b.

Shareholder Orientation as a Moderator of the Relationship Between Humane Orientation and Cross-Border Acquisition Performance

As presented in Model 8, the coefficient for humane orientation in home countries is significantly positive (p < .01), and the coefficient for property rights protection in home countries is significantly negative (p < .001). While the coefficient for the product term of humane orientation and property rights protection in home countries is not statistically significant, the coefficient of the product term is smaller than the coefficient of humane orientation in home countries, which indicates home property rights protection weakens the effects of humane orientation. Hence, Hypothesis 6 is partially supported.

Robustness Tests

We also conducted a series of robustness checks. In the first set of robustness checks, we used several alternative dependent variables in different time windows after the acquisitions to test our hypotheses. First, we used ROS at 2-, 4-, and 5-year windows to measure the CBA performance. The results largely support our hypotheses. Second, we adopted acquirers’ Tobin’s q at 2, 3, and 5 years after the acquisitions. Results are largely consistent with our results in the primary tests. Using Tobin’s q at 3 and 4 years after acquisitions, results support all hypotheses except the main effects of collectivism and shareholder orientation. As we use Tobin’s q at 5 years after the acquisition, all hypotheses are supported except the main effect of humane orientation and the joint influence of property rights protection and humane orientation. It seems that different dimensions of institutions may play their roles in postacquisition performance in different stages of postacquisition processes. Consistent with our theory, humane orientation tends to play an important role in the early stage of postacquisition integration. While collectivism starts to play a role in postacquisition integration, its role becomes more pronounced in the later stages. Third, we measured postacquisition performance by using the change of acquirers’ ROS at 3 years after the acquisitions from the average of ROS in the previous 3 years before the acquisition. Results are consistent with and strongly support our findings. Overall, alternative measures of postacquisition performance provide strong support for our theory.

In the second set of robustness tests, we used an alternative measure of shareholder orientation to test the main effects of shareholder orientation in home countries and their moderation effects of informal institutions. We retrieved the yearly stock market capitalization as the percentage of GDP from World Competitiveness Online to measure shareholder orientation. The results support our hypotheses. For property rights protection, we collected additional data—free property rights from Heritage Foundation—to measure property rights protection in order to test its main effect and moderation effects on the relationship between humane orientation and international acquisition performance. The results strongly support the hypotheses.

The third set of robustness tests has seven components. First, to control for the confounding events occurring between acquisition announcement and postacquisition performance, we calculated the number of acquisitions and divestitures that acquirers conducted between the announcement date and the year of calculating performance. The results support our hypotheses. Second, because there are a lot of missing transaction values, we identified those 5,928 deals with an identifiable transaction value and controlled for transaction value to test hypotheses. The results are consistent with our main findings except the main effect of home humane orientation and the moderation effect of shareholder rights protection on humane orientation, but the sign is consistent. Third, we also identified the first deal that the acquirers conducted between 1995 and 2003 and included these deals only in the hypotheses testing, resulting in 4,130 deals. Results are consistent with our main findings except for the main effect of collectivism and humane orientation. The signs of the main effects are positive. Fourth, because there are missing values regarding acquired targets’ size, we identified those deals with information about the target size, resulting in a sample of 3,545. Then we calculated the relative size and controlled for it. Results support all hypotheses except the main effect of collectivism.

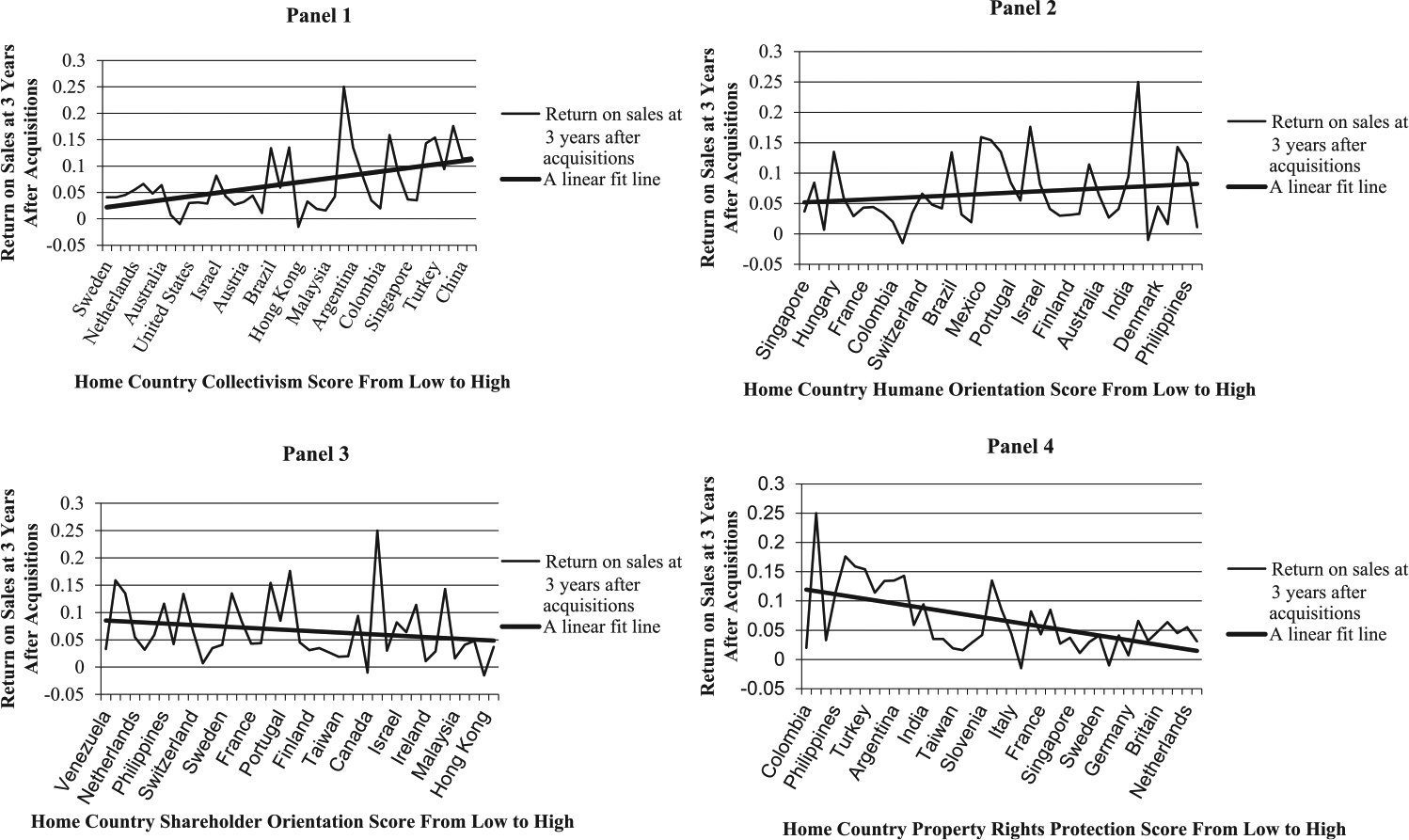

For the fifth component, we retrieved exchange rates and consumer price indexes from Economist Intelligence Unit and control for these rates in both home and host countries. Results are consistent with our main findings. Sixth, we excluded U.S. acquirers’ CBAs to conduct robustness checks. Results strongly support all hypotheses. Seven, to substantiate our findings that firms from certain home institutional contexts enjoy comparative acquisition capability advantage, we provided a descriptive table. As shown in Table 3 and Figure 4, acquirers from collectivism- and humane-oriented countries have performed better in postacquisition value creation, and firms from strong shareholder orientation and property rights protection may be less capable of extracting value through integrating with acquired foreign targets. Overall, all 16 robustness tests strongly support our hypotheses, significantly enhancing our confidence in the explanatory and predictive power of our theory.

Home Country Institutions and Cross-Border Acquisition Performance

Note: ROS = return on sales.

Home Country Institutions and Postacquisition Performance

Discussion

Contributions to the Institution-Based View

Our study contributes to the institution-based view in five significant ways. First, we propose an integrated institutional framework that consists of two informal institutions (collectivism and humane orientation) and two formal institutions (shareholder orientation and property rights protection). Our theory and results show that this integrated institutional framework in home countries is powerful in explaining postacquisition performance because this framework shapes acquirers’ interdependence perception toward acquired targets in different degrees and corresponding postacquisition integration approaches as detailed below.

Second, the findings that home country collectivism and humane orientation positively influence CBA performance demonstrate that institutions do matter for firm activities beyond national borders through CBAs (Marano et al., 2016; North, 1990; Peng et al., 2008; Peng, Sun, Pinkham, & Chen, 2009). In CBAs, collectivism and humane orientation shape acquirers’ management logics to believe that stakeholders’ interests are interdependent (Powell & Colyvas, 2008), and such “interdependence” logics are extended to manage acquired targets in postacquisition combined firms. These acquirers view acquired targets as interdependent units, prioritize support to acquired targets, promote growth and success, and welcome acquired targets to participate in postacquisition integration decision making (House et al., 2004). Our theory and evidence suggest that these logics and postacquisition management approaches of acquirers shaped by their home country institutions are useful means to create value from CBAs.

Third, postacquisition integration requires collective efforts of both acquiring and acquired firms. However, strong shareholder orientation merely highlights the interests of shareholders of acquirers and de-emphasizes other important stakeholders. This formal institution provides different stakeholders conflicting and potentially counterproductive incentives needed for effective postacquisition integration. Moreover, acquirers in strong property rights protection countries, as new owners, may impose their ways of managing firms on acquired targets and are less likely to take acquired targets’ needs into account. Our findings suggest that acquirers embedded in these two formal institutions may be less able to create value from CBAs. These findings similarly demonstrate that institutions can be extended to affect firm activities beyond national borders through CBAs (Djelic & Quack, 2008).

Fourth, although scholars have addressed the joint influence of formal and informal institutions (Yamagishi et al., 1998), this study represents one of the first studies in the setting of CBAs. We posit that home country informal and formal institutions can jointly influence acquirers’ perceptions and approaches of managing acquired targets. While informal institutions exert their influences on acquirers’ interdependence perceptions, formal institutions may reshape such perceptions. We find partial support for the moderation effects of property rights protection on the positive relationship between humane orientation and CBA performance. As strong property rights protection shapes acquirers not to consider the interests and opinions of targets during postacquisition integration processes, this approach tends to be resisted by targets. Acquirers with humane orientation tend to be very sensitive to such resistance. In addition, humane-oriented acquirers may not be willing to change their altruism behavior toward acquired targets because these acquirers with strong property rights protection also desire effective integration and better returns from such cross-border investments. This may explain why we did not find full support for the moderation effects. Considering the influence of both formal and informal institutions, our study provides a more complete understanding of institutional influence on postacquisition processes and performance.

Finally, our theory and findings extend recent institutional work on the source of firm performance variance (Chan et al., 2008; Peng et al., 2008; Peng et al., 2009) by showing that national institutions are a source of value creation for firms that not only operate in their home countries but also expand to foreign markets. As such, this research significantly enriches the institution-based view of strategy (Ahuja & Yayavaram, 2011; Holmes et al., 2013; Lin, Peng, Yang, & Sun, 2009; Meyer et al., 2009; Meyer & Peng, 2016; Peng, Ahlstrom, Carraher, & Shi, in press).

Contributions to CBA Research

Our results make two significant contributions to CBA research. First, our results shed light on the influence of informal institutions on CBA performance. We go beyond the current embodiment of informal institutions in terms of differences between home and host countries (Chakrabarti et al., 2009; Morosini et al., 1998) by introducing home country informal institutions as a key explanatory variable. Our findings indicate that acquirers’ home country collectivism and humane orientation exert substantial influence on CBA performance.

Second, this study not only echoes but also goes beyond recent studies that show that formal institutions, including shareholder orientation, influence postacquisition performance (Capron & Guillén, 2009). We contribute by highlighting the joint influence of informal and formal institutions. While informal institutions can exert influence on acquirers, such influence is constrained by formal institutional forces. Our theory and findings provide a fine-grained understanding of how informal and formal institutions simultaneously affect the performance of CBAs (Kogut, Walker, & Anand, 2002; Lebedev et al., 2015; Lin et al., 2009; Wan & Hoskisson, 2003; Yang, Lin, & Peng, 2011; Zhu & Zhu, 2016).

Managerial and Public Policy Implications

From a managerial perspective, our findings suggest the important practices that are particularly helpful to facilitate the coordination, cooperation, and integration between acquirers and targets. Our study shows that shareholder orientation and property rights protection, despite their generally noted positive features, may be less helpful in promoting cooperative actions between acquiring and acquired firms. It stands to reason that certain actions (e.g., downsizing) driven by concerns for shareholder rights may be oriented toward yielding high returns in the short term rather than toward building long-term value. Therefore, our findings make acquirers aware of institutional influences and allow managers to adequately respond (Hoskisson, Wright, Filatotchev, & Peng, 2013). Additionally, policy makers may refine formal shareholder rights to promote firms’ long-term strategic investment and value creation potential. For example, new policies can be designed to induce shareholders to focus on long-term value and therefore complement informal institutions that provide collective incentives for acquirers.

Limitations and Future Research Directions

There are several limitations of this study that can also offer opportunities for future research. First, given our use of archival data of CBAs among 50 countries, we are not able to directly measure the postacquisition processes or mediating mechanisms through which collectivism and humane orientation affect postacquisition performance. Researchers may supplement our findings through surveys conducted to substantiate the integration advantages of these two informal institutions. In particular, it may be feasible for researchers to conduct such surveys in one host country where acquirers from a variety of countries are interested in acquiring local firms.

Second, we focus only on the joint influence of collectivism/humane orientation and shareholder orientation/property rights protection on CBA performance. Future work may identify other informal and formal rules and examine how they combine to influence CBA performance (Estrin & Prevezer, 2011) and also other settings, such as international joint ventures (Pinkham & Peng, 2016; Tong, Reuer, & Peng, 2008; Yang et al., 2011).

Finally, given the mixed findings of cultural distance in existing studies, it is very likely that certain dimensions of cultural values have stronger influence on postacquisition performance. Yet cultural distance incorporating each dimension of cultures may complicate the effects. Future research could examine how specific dimensions of cultural distance and/or formal institutional distance exert their strong influence on postacquisition performance (Huang et al., 2016; Zhu & Zhu, 2016). Similarly, it may also be interesting to investigate the influence of specific host country institutions.

Conclusion

In conclusion, this study proposes an integrated institutional framework that consists of two informal institutions (collectivism and humane orientation) and two formal institutions (shareholder orientation and property rights protection) and demonstrates its explanatory power behind postacquisition performance. Future research can use this framework to examine other strategies that require interdependence perception and collaborative approaches. Furthermore, we provide an initial investigation of the individual and joint influences of informal and formal institutions in the home countries of acquirers on CBA performance. We find that collectivism and humane orientation in home countries can exert positive influences on postacquisition performance. Moreover, such effects are constrained by surrounding formal institutions when these formal institutions are incompatible with the prevailing informal institutions. In doing so, we extend institutional research to the context of CBAs. We hope this study will serve as a starting point for additional institution-based research on acquisitions because the various mixes of informal and formal institutions in different countries present fertile grounds for significant progress in developing an institution-based view of acquisitions.

Footnotes

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright. We appreciate the constructive guidance from Sucheta Nadkarni (editor) and three reviewers. This study was supported by two grants from the Research Grants Council of the Hong Kong Special Administrative Region (Projects 14501714 and 14504715) and by the Jindal Chair, University of Texas at Dallas.