Abstract

We theorize that female candidates considering CEO roles will perceive greater termination vulnerability in such roles than their male counterparts. We further theorize that indicators of recent organizational distress will exacerbate female CEO candidates’ perceptions of termination vulnerability, while the presence of female leaders will mitigate these concerns. To test our arguments, we examine the initial values of newly appointed female and male CEOs’ severance agreements from 2007 to 2014. Results support our arguments and begin to shed light on the factors that influence female executives’ concerns about CEO roles and ultimately firms’ ability to appoint female CEOs.

Women are underrepresented at the CEO level, particularly in the most prominent U.S. firms. This disparity has long been attributed to the glass ceiling effect, or the invisible external barriers that restrict women from advancing into top corporate roles (Hymowitz & Schellhardt, 1986). However, in recent years, opportunities to progress to the upper echelon (UE) have opened for women, suggesting that the external barriers preventing women from advancing to the executive ranks may be slowly receding. Indeed, over the last two decades, the proportion of female CEOs in Standard and Poor’s (S&P) 500 firms has increased from <1% to 5% (Catalyst, 2018).

Despite this progress, the number of female CEOs remains low: “fewer large companies are run by women than by men named John” (Wolfers, 2015). Addressing this point, some have advanced a new explanation for the scarcity of women in the UE—the “opt-out revolution” hypothesis, which proposes that women are deliberately choosing not to pursue the very top executive positions (Belkin, 2003; Hoobler, Lemmon, & Wayne, 2014). For example, Gino, Wilmuth, and Brooks (2015) argued and found that, in general, although women find upper-level positions as equally attainable as their male counterparts do, they view those positions as less desirable. Likewise, the results of a recent survey revealed that while 64% of men aspire to obtain top executive roles, only 36% of women seek those same positions (Bellstrom, 2015). A recent Fortune article discussing the appointment of Susan Cameron as CEO of Reynolds American noted, “Cameron had no desire . . . to ever move up to CEO. (This is a stunningly common trait on the Fortune Most Powerful Women list; CEOs Ginni Rometty of IBM and Ellen Kullman of DuPont, among others, almost passed on promotions early in their careers, only to be pushed to lean in by their bosses or husbands.)” (Sellers, 2014). Most recently, some evidence appears to support women’s trepidations about taking the CEO role, as Gupta and colleagues (2020) showed that female CEOs are significantly more vulnerable to termination than male CEOs.

Although many women may be opting out of CEO roles, some clearly are opting in. However, given that UE scholars have paid little attention to the factors that female executives may deem important as they consider CEO roles, we know little about what drives their concerns about taking on those top roles or how firms seeking to hire a female CEO might attempt to overcome those concerns. Admittedly, until very recently, the sheer scarcity of female CEOs has limited scholars’ ability to examine gender in the UE. However, the recent increase (albeit somewhat small) in the number of female CEO appointments provides a novel opportunity to examine the contexts that affect female executives’ concerns about accepting CEO roles—which has implications for firms’ ability to appoint female CEOs.

In this study, we address these questions by integrating gender role research (Eagly, 1987; Eagly & Karau, 2002; Heilman, 2012; Oliver, Krause, Busenbark, & Kalm, 2018) and UE research (Almazan & Suarez, 2003; Cadman, Campbell, & Klasa, 2016; Cowen, Wilcox-King, & Marcel, 2016; Finkelstein, Hambrick, & Cannella, 2009; Rau & Xu, 2013). Prior work has shown that “gender biases, stereotypes and male-typed leadership schemas shape global normative expectations about women’s ability to lead and undermine the success of women in leadership roles” (Dwivedi, Joshi, & Misangyi, 2018: 379). Thus, women are likely to anticipate biased treatment and evaluations in top executive roles (Barbulescu & Bidwell, 2013; Ragins, Townsend, & Mattis, 1998). Building on this research, we argue that, in general, female candidates considering CEO roles will perceive greater vulnerability to termination in such roles than will their male counterparts. In addition, we expand our theorizing to argue that important contingencies will increase or decrease those perceptions of termination vulnerability.

We test our arguments by examining the initial severance agreements of newly appointed female and male CEOs. Initial severance agreements are negotiated between CEO candidates and boards of directors prior to appointment and specify the payments and benefits owed to CEOs if they are terminated. These agreements can reduce some of the future compensation and employment risk that CEOs perceive from potential involuntary termination (Almazan & Suarez, 2003; Cowen et al., 2016). 1 In this way, severance agreements function as a form of termination insurance for CEO candidates, “easing concerns that might otherwise prevent a mutually beneficial employment relationship” (Cowen et al., 2016: 155). Accordingly, guaranteed severance pay should reflect the termination risk that CEO candidates perceive prior to appointment.

Our results support our arguments and thus make several important contributions. First of all, we contribute to the emerging literature examining the factors that affect female CEO appointments (Cook & Glass, 2014, 2015; Ryan & Haslam, 2007; Zhang & Qu, 2016). We find that female CEOs tend to receive larger initial severance agreements than do male CEOs. This suggests that women perceive greater termination vulnerability from accepting CEO appointments than do male CEOs, which has important implications for boards. Specifically, boards seeking to hire female CEOs may need to address the latter’s heightened concerns about termination, which can lead women to “opt out” of such roles. Our results suggest that guaranteed severance pay can be effective in this regard by insuring CEOs against termination losses. Although prior severance research has acknowledged the benefit of using severance agreements as a recruitment tool (Cowen et al., 2016), very little empirical work has shown support for this argument (Klein, McSweeney, Devers, McNamara, & Blosser, 2017). Thus, our findings extend the severance literature (Cowen et al., 2016; Rau & Xu, 2013) and suggest that severance agreements can be viewed as an especially effective recruitment tool for female CEO candidates.

Second, we explore how factors related to female CEO candidates’ termination vulnerability can exacerbate or attenuate gender-based termination concerns (Fredrickson, Hambrick, & Baumrin, 1988; Zhang, 2008; Zhang & Qu, 2016). We show that the difference in severance agreements between incoming female and male CEOs is (1) larger in firms experiencing declining performance or where the prior CEO was dismissed early and (2) smaller in firms that have at least one female director or that operate in an industry with more female CEOs. These results suggest that female CEO candidates’ concerns about biased treatment are heightened when considering joining firms encountering organizational distress and reduced when other female leaders are present, whether on the firm’s board or as CEOs in its industry. Thus, our findings help extend our understanding of the specific conditions that seem to exacerbate and alleviate women’s perceptions of biased treatment, rather than simply insuring women against termination losses as severance agreements do. Together, these findings have the potential to advance the conversation about gender in the UE by providing some preliminary evidence that the perceptions and preferences of female leaders are more nuanced and complex than prevailing views allow for.

Third, in supplementary findings, we show that the total compensation and pay mix (variable vs. cash-based pay) of male and female CEOs are statistically indistinguishable—at least in our sample, incoming male and female CEOs receive comparable compensation, ceteris paribus. However, our results do show that the guaranteed severance pay that female CEOs receive in their initial contracts is significantly higher than that of male CEOs. This suggests that although female CEOs are, on average, able to secure greater severance guarantees, they do not appear to be trading cash- or incentive-based pay for severance. Rather, these results suggest that female CEO candidates may have previously unrecognized bargaining power in the employment negotiation process. 2

Theory and Hypotheses

CEO candidates face significant risk when considering CEO roles, due to the potential for termination. Indeed, there is much ambiguity regarding the demands of CEOs’ jobs (Allgood & Farrell, 2003; Zhang, 2008), as the typical objective metrics by which CEOs are evaluated (i.e., accounting and stock performance) fail to accurately reflect early-stage CEO performance (Finkelstein et al., 2009; Graffin, Boivie, & Carpenter, 2013; Kesner & Sebora, 1994). As a consequence, stakeholders must often rely on ambiguous and subjective information when evaluating recently appointed CEOs (Graffin et al., 2013; Holmstrom, 1982; Wade, Porac, Pollock, & Graffin, 2006). When executives are considering a CEO role, the possibility of termination and the subsequent adverse effects on financial, human, and social capital can create high perceptions of employment and compensation risk (Larraza-Kintana, Wiseman, Gomez-Mejia, & Welbourne, 2007; Wiesenfeld, Wurthmann, & Hambrick, 2008). Specifically, dismissed CEOs often face reputational damage (Finkelstein et al., 2009; Semadeni, Cannella, Fraser, & Lee, 2008), devaluation in the labor market, and, ultimately, costs to their future job prospects and pay (Fama, 1980; Sutton & Callahan, 1987; Wiesenfeld et al., 2008). Some evidence indicates that <12% of CEOs who are dismissed subsequently find new positions in public companies at any level; these jobs tend to be at smaller firms, with a lower compensation (Chang, Hayes, & Hillegeist, 2016; Fee & Hadlock, 2004).

While all executives considering CEO roles are likely to be (at least) somewhat concerned about termination, evidence suggests that women perceive even greater personal and professional threats associated with accepting these roles as compared with their male peers. For example, Ragins et al. (1998) surveyed 1,251 Fortune 1000 female executives about the strategies that contributed to their career advancement: the authors found that the majority of women believed that to be successful, they must exceed performance expectations and act in ways that will not threaten their male coworkers or make them feel uncomfortable. Likewise, recent studies show that female executives anticipate more negative outcomes from high-level positions (Gino et al., 2015) and are thus less interested than men in becoming top executives because they perceive those roles as “disproportionately stressful” (LeanIn.Org & McKinsey & Company, 2015).

Considerable gender role research indicates that the heightened challenges that female executives face largely stem from the inconsistencies between the characteristics that observers expect leaders to exhibit and those that they expect from women (Eagly & Karau, 2002; Heilman, 2012). Specifically, prior work demonstrates that people tend to associate leaders with agentic qualities, such as assertiveness, aggressiveness, independence, and confidence (Koenig, Eagly, Mitchell, & Ristikari, 2011; Ryan, Haslam, Hersby, & Bongiorno, 2011; Schein, 1973). This association is problematic for women because, although people generally expect men to exhibit agentic qualities, they largely expect women to exhibit communal qualities, such as compassion, nurturance, kindness, sensitivity, and caregiving (Bakan, 1966; Diekman & Eagly, 2000; Eagly, 1987). The resulting inconsistency often causes female leaders who exhibit agentic behaviors to be seen as violating their stereotypical communal gender role, whereas those who demonstrate communal behaviors are seen as lacking the agentic qualities expected of successful leaders (Eagly & Karau, 2002; Heilman, 1983, 1995; Heilman & Okimoto, 2007; Rudman & Glick, 2001). This leads observers to judge male leaders as being more effective than female leaders, even under similar performance levels (Heilman, 2012; Koenig et al., 2011), which can undermine the success of female leaders, particularly those in executive-level roles (Dwivedi et al., 2018).

In support, Bigelow, Lundmark, Parks, and Wuebker (2014) demonstrated that external observers presume that female CEOs are less capable than male CEOs during initial public offerings, even when they have the same qualifications and manage similar firms. Similarly, Lee and James (2007) and Jeong and Harrison (2017) showed that the market responds more negatively to female CEO appointments than to male CEO appointments. Other research indicates that female CEOs are more likely than their male counterparts to be blamed for their missteps, causing them to face greater negative media coverage and damage to their reputations (Park & Westphal, 2013). Most recently, Gupta and colleagues (2020) found that female CEOs are more likely to be terminated than male CEOs, ceteris paribus. Finally, anecdotal evidence offers additional support for these findings. For example, Indra Nooya, who stepped down as PepsiCo’s CEO in 2018, stated, “When you become a CEO and you’re a woman, you are looked at differently . . . . You are held to a different standard. There’s no question about it” (Kolhatkar, 2018).

Although female executives have overcome many constraints related to gender bias and male-type leadership schemas to reach their positions, stepping into a CEO position is often considered a big leap for executives because the CEO role differs substantially from any other executive role. Indeed, it is widely believed that the CEO position requires agentic qualities and behavior, which are mostly inconsistent with the traditional female gender role and lead to downwardly biased evaluations of women’s performance in such a leadership position (Eagly & Karau, 2002; Jeong & Harrison, 2017). CEOs are also subjected to heightened visibility and exposure (Graffin et al., 2013; Kesner & Sebora, 1994; Zhang & Rajagopalan, 2004): the CEO is inescapably perceived as the leader of the firm, which again conflicts with the female gender role and can result in significant career penalties for those who are deemed unsuccessful. Given this research, we theorize that, as compared with male executives, female executives perceive greater termination vulnerability when considering CEO positions.

CEO Gender-Based Perceptions of Termination Vulnerability and Severance

In this study, we consider the initial severance agreements granted to incoming female and male CEOs. Initial CEO severance agreements are negotiated between boards and CEO candidates prior to appointment and specify the payments and benefits promised to CEOs upon termination. The severance payments that these agreements promise are far from trivial. For example, for incoming CEOs in our sample, annual salary—which many argue is the safest form of compensation—averages approximately $700,000, whereas guaranteed severance pay averages $4.3 million.

Although CEOs and directors often face criticism over severance agreements (Bebchuk & Fried, 2004; Dash, 2007), advocates argue that such agreements offer several important benefits related to CEO succession (Almazan & Suarez, 2003; Cowen et al., 2016). Specifically, as stated earlier, when executives are considering a CEO offer, the threat of dismissal can generate high perceptions of employment and compensation risk (Larraza-Kintana et al., 2007). The greater the perceptions of this risk, the more likely it is that qualified candidates will decline CEO offers. Scholars have argued that severance agreements can provide some insurance against involuntary termination for CEO candidates, thus mitigating the personal cost of termination (Cadman et al., 2016; Cowen et al., 2016; Lys, Rusticus, & Sletten, 2007; van Dalsem, 2010). Accordingly, severance agreements can help CEO candidates commit to a position that may otherwise be perceived as presenting too much termination risk. By offering termination-related insurance to potential CEOs and facilitating directors’ ability to attract CEO candidates who may have reservations about joining their firms, severance agreements can serve the interests of CEO candidates and boards. 3 Building on this work, we argue that the value of incoming CEOs’ severance agreements should reflect the level of termination risk that they associate with those positions.

Previous research suggests that due to inherent gender bias and male-type leadership schemas, female executives perceive greater vulnerability to termination when accepting CEO roles as compared with their male counterparts. Since a severance agreement is the only instrument that pays off if and only if the CEO is terminated, it is by definition the most efficient compensation-related instrument to alleviate termination-based concerns (see Cowen et al., 2016; Ju, Leland, & Senbet, 2014; Rau & Xu, 2013). By contrast, the components of an executive’s annual compensation package, such as salary and stock option pay, are granted only as long as the CEO is still in office, 4 and they play other purposes than insuring the CEO against termination risk. As a result, we believe that severance agreements will be especially useful in addressing the heightened termination concerns of female CEO candidates.

Qualitative evidence provides preliminary support for the idea that severance agreements will tend to be more valuable for incoming female CEOs than incoming male CEOs. For example, Apple’s 2015 proxy statement stated, “Aside from the arrangement with Ms. Ahrendts [senior vice president for retail and online], which was offered to encourage her to join the Company, the Company does not generally enter into severance arrangements with its named executive officers” (Apple Inc., 2015: 48). Likewise, Johnson & Johnson’s 2013 proxy statement suggests that it offered its only female top management team executive, Ms. Peterson (“Group Worldwide Chair”), an agreement when she first entered the company that was different from that of the other top executives (Johnson & Johnson, 2013: 70). Consequently, we propose that guaranteed severance pay will be larger for incoming female rather than incoming male CEOs—thus,

Hypothesis 1: All else equal, the value of female CEOs’ initial severance agreements will tend to exceed those of male CEOs.

Gender-Based Contingencies in Perceptions of Termination Vulnerability

With our first hypothesis, we proposed that female CEO candidates perceive higher termination vulnerability than do their male counterparts. In this section, we explore the contextual factors that could exacerbate or attenuate female candidates’ perceptions of vulnerability in CEO roles as compared with male candidates.

First, UE scholars have argued that declining firm performance and early dismissal of the prior CEO, or “recent organizational distress,” make CEOs more vulnerable to dismissal in the early years of their tenure (Fredrickson et al., 1988, Martin, Gomez-Mejia, & Wiseman 2013; Zhang, 2008). Building on this work and on role congruity theory, we argue that these factors exacerbate female CEO candidates’ termination concerns as compared with those of male CEO candidates. Second, scholars have argued that women are less vulnerable to biased treatment in CEO roles when other women are present (Oliver et al., 2018; Zhang & Qu, 2016). In fact, Valian (1998: 323) argued that one of the most effective ways for women leaders “to evade the negative consequences of gender schemas and accumulate advantage” is to “try to work in fields and organizations where women are well-represented.” Extending this work, we propose that the presence of female leaders on the firm’s board and as other CEOs in the firm’s industry will attenuate female CEO candidates’ termination concerns as compared with those of male CEO candidates.

Recent organizational distress

A priori, we would expect CEO candidates to be concerned about termination when considering a firm with recent organizational distress; however, we argue here that women’s termination concerns will be heightened as compared with men’s due to stereotypes about gender and leadership.

First, we consider the moderating effect of performance decline at the firm where the CEO is appointed. One of the most important predictors of CEO termination is poor firm performance (Coughlan & Schmidt, 1985; Fredrickson et al., 1988; Gilson, 1989; Kaplan & Minton, 2012; Murphy & Zimmerman, 1993). Thus, CEO candidates are likely sensitive to signals of performance decline and look for such markers when evaluating CEO offers. In particular, scholars have argued that if a firm has had a consistent performance decline, it will be very hard for a new CEO to turn it around (Chen, 2015). For example, Barker and Patterson (1996) showed that only about 30% of declining organizations actually achieve turnaround. The reason is that a firm’s downward spiral tends to be persistent (Hambrick & D’Aveni, 1988, 1992). Thus, as compared with healthy firms, declining firms often face a high risk of failure (Jiang, Cannella, Xia, & Semadeni, 2017). If a firm fails during a CEO’s tenure, even if the problems were inherited from the predecessor, the CEO may be viewed as personally responsible (Carpenter, Geletkanycz, & Sanders, 2004; Semadeni et al., 2008). Admittedly, accepting a CEO role at a declining firm could be appealing to some CEO candidates given that turning around the firm’s fortune can result in the CEO making a name for himself or herself and gaining significant prestige (Chen, 2015). However, the likelihood of this occurring is very low (Bibeault, 1982; Chen & Hambrick, 2012). Thus, CEO candidates are likely to perceive a heightened possibility of termination when considering a position at a declining firm (Chang et al., 2016).

While all CEO candidates may be apprehensive about joining a firm on a declining performance trend, female CEOs are likely to be more concerned. The reason is that a man’s competence is often assumed in leadership roles, whereas a woman’s competence is generally questioned (Heilman 2001, 2012), consistent with role congruity research (Eagly & Karau, 2002). In particular, when a woman makes a mistake, gender bias is heightened, given that “salient mistakes create ambiguity” and “stereotyping thrives on ambiguity” (Brescoll, Dawson, & Uhlmann, 2010: 1640). Consequently, female CEOs often face greater blame for a firm’s poor performance than do male CEOs (Brescoll et al., 2010; Haslam, Ryan, Kulich, Trojanowski, & Atkins, 2010), resulting in greater negative media coverage and reputational damage for them (Park & Westphal, 2013). Recent evidence also shows that female CEOs tend to encounter greater public displays of dissatisfaction from activist investors (Gupta, Han, Mortal, Silveri, & Turban, 2018), which matters to women considering a CEO position at firms on a declining trajectory, since activist investors have a stronger propensity to target poorly performing companies (Bethel, Liebeskind, & Opler, 1998).

In addition, a firm on a declining trajectory will often require decisive corrective actions, such as downsizing or retrenchment (Weitzel & Jonsson, 1989), which are often perceived as incongruent with the communal expectations of the female gender role. As such, role congruity theory suggests that such actions are likely to elicit more negative evaluations for female CEOs than for male CEOs (Eagly & Karau, 2002). In sum, female CEO candidates will likely perceive greater termination vulnerability when accepting CEO roles in firms with declining performance trends than will male CEOs.

By contrast, some male executives may even perceive benefits from being appointed CEO of a firm on a declining performance trend, as this provides them with an opportunity to exhibit behaviors congruent with the male gender role, such as “forcefulness” and “assertiveness” (Eagly, 1987; Vandello & Bosson, 2013). Besides, even poor performance by a male executive is less likely to be attributed to his ability as a leader but instead to outside factors, such as bad luck or market or industry conditions (Park & Westphal, 2013; Swim & Sanna, 1996). This suggests that male CEO candidates will likely be less concerned than female CEO candidates about accepting a position at a firm with a declining performance trajectory. Thus, we expect the following:

Hypothesis 2: The relation between gender and the value of CEOs’ initial severance agreements is moderated by firm performance prior to CEO appointment such that sustained declining performance strengthens the positive relation between female CEO and severance value.

Second, we consider how the early termination of the previous CEO of the appointing firm may affect the relation between CEO gender and initial severance agreements. Prior work has shown that new CEOs appointed to firms in which the predecessor was dismissed, particularly in a short period following appointment, are especially vulnerable to early dismissal (Fredrickson et al., 1988; Zhang, 2008). The reason is that the failure of these CEOs often causes a firm to have to bypass the normal succession process and select a new CEO in an unplanned manner, which can aggravate an already disruptive process (Zhang & Qu, 2016: 1848). As Shen (2003: 469) discussed, “dismissing new CEOs before they can fully demonstrate their leadership potentials is not only a waste of executive talent but very disruptive to the firm, because it hinders the establishment of reliable and predictable routines that are highly regarded by inside and outside stakeholders (Hannan & Freeman, 1984).” Ultimately, this worsens the situation faced by the successor (Shen & Cannella, 2002b) and increases the likelihood that he or she may also be dismissed (Zhang, 2008). Thus, CEO candidates may view a prior CEO’s early dismissal as indicative of the challenges that they will face at a firm (Gillan, Hartzell, & Parrino, 2009). They could also view it as a signal of a “trigger-happy board” that expects to see results materialize quickly or a board that is prone to terminate a CEO in response to negative short-term organizational events (Shen, 2003). For all these reasons, the early dismissal of the prior CEO can heighten concerns about termination when candidates consider CEO roles.

Yet, female CEO candidates are likely to be more concerned than male CEO candidates about an early dismissal of the prior CEO. While all new CEOs face a “liability of newness,” leading to some disruption as the new CEO takes over, a new female CEO is more disruptive given the rarity of women in such roles and the expectation that her management style will differ from that of traditional (male) leaders (Ashcraft, 1999; Zhang & Qu, 2016). Recent evidence indeed indicates that appointing a female CEO, especially after a predecessor departed early, “may amplify the disruption of the CEO succession process and increase the challenges faced by the successor” (Zhang & Qu, 2016: 1862). Ultimately, this can make it harder for a woman to succeed in an already challenging role.

Furthermore, given role congruity bias, women often face greater skepticism regarding their fitness for CEO roles (Eagly & Karau, 2002). Consistent with this argument, Jeong and Harrison (2017: 1226) argued that negative stakeholder evaluations of female CEOs are likely to be “captured in short-term market returns, which largely reflect investor beliefs and cognitions about future share price (Lamin & Zaheer, 2012; Schijven & Hitt, 2012), rather than long-term financial returns to business operations.” In addition, female CEOs are more likely to take a strategic, collaborative, and cautious approach, which should take more time to bear fruit, ultimately affecting long-term firm performance rather than short-term performance (Ibarra & Obodaru, 2009; Jeong & Harrison, 2017). Thus, the early dismissal of the previous CEO—which indicates that the firm’s board is looking for a quick turnaround and is prone to respond to negative short-term signals and events by terminating a CEO (Zhang, 2008)—may be particularly concerning for women.

In contrast, we believe that this effect will be weaker for male CEO candidates. First, men are already seen as leaders (Eagly & Karau, 2002); in addition, the majority of CEOs are men. Thus, the appointment of a male CEO is more likely to be viewed as “normal,” creating less disruption for the firm (Zhang & Qu, 2016). Second, when firms led by male CEOs experience negative events, those situations are likely to be attributed to external factors and luck rather than to the CEO (Park & Westphal, 2013; Swim & Sanna, 1996). Thus, male CEO candidates may be more likely to believe that they will be given the benefit of the doubt by boards early in their tenure. Hence, we propose the following:

Hypothesis 3: The relation between gender and the value of CEOs’ initial severance agreements is moderated by the early dismissal of the prior CEO such that an early dismissal strengthens the positive relation between female CEO and severance value.

Female leader presence

Prior research argues that the presence of female leaders in a firm’s environment should decrease the biased treatment faced by a female CEO (Eagly & Karau, 2002; Oliver et al., 2018; Valian, 1998; Zhang & Qu, 2016). Extending this work, we argue that the presence of female CEOs in the focal firm’s industry or on its board of directors will reduce female candidates’ perceptions of termination vulnerability associated with accepting CEO roles.

We first consider the moderating effect of female CEOs in the focal firm’s industry. Although observers tend to associate the CEO position with the male gender role, evidence suggests that the presence of top female leaders can begin to weaken gender and leader stereotypes (Beaman, Chattopadhyay, Duflo, Pande, & Topalova, 2009; Dasgupta & Asgari, 2004; Dasgupta & Greenwald, 2001; Fiske & Neuberg, 1990; Heilman & Caleo, 2018; Kwan, Yap, & Chiu, 2015). The reason is that exposure to female leaders can facilitate “updating of impressions based on new observations (e.g., Weber and Crocker, 1983)” (Koenig et al., 2011: 619). Thus, in situations in which female leaders are more prevalent, observers tend to ascribe more agentic qualities to women and less masculine qualities to leaders, reducing the incongruity between the female gender role and leadership roles (Dasgupta & Asgari, 2004; Diekman & Eagly, 2000; Duehr & Bono, 2006; Koenig et al., 2011). In turn, this can lead observers to view women as being more suitable for leadership roles (Beaman et al., 2009; Dasgupta & Asgari, 2004; Eagly & Carli, 2007; Kanter, 1977; Valian, 1998).

This work suggests that female CEO candidates should perceive that their gender will be less salient to evaluators in industries with a larger presence of female CEOs than in male-dominated industries (Cook & Glass, 2011; Kanter, 1977; Koch, D’Mello, & Sackett, 2015), thereby mitigating female CEO candidates’ fear of negatively biased treatment and evaluation. Some studies also suggest that new female CEOs should feel more comfortable and supported in their roles in the presence of female peers (Ely, 1994; Kanter, 1977). 5 Building on this work, we propose that female CEO candidates will perceive lower termination vulnerability in industries where the presence of female CEOs is higher. However, we do not believe that this factor will have a substantial effect on male CEO candidates’ termination concerns. The reason is that the majority of CEOs are men (Catalyst, 2018). As a result, we suggest that men are less prone to perceive role congruity–related biases, especially at the current levels of female CEOs, even in industries in which the proportion of women leaders is higher. Thus, we propose the following:

Hypothesis 4: The relation between gender and the value of CEOs’ initial severance agreements is moderated by the presence of female CEOs in the focal firm’s industry such that a larger presence of female CEOs weakens the positive relation between female CEO and severance value.

Last, we consider the moderating effect of female director presence. One of the main roles of a company’s board is to appoint, oversee, and occasionally terminate the company’s executives (Matsa & Miller, 2011). We argue here that the presence of female CEOs in the focal firm’s industry can reduce female candidates’ termination concerns, as it makes the gender of a new female CEO less salient to evaluators. Similar evidence indicates that female director presence can decrease the likelihood of gender stereotyping against female CEOs (Oliver et al., 2018). This results from the increased exposure and contact with female leaders (Pettigrew & Tropp, 2006; Zhu & Westphal, 2014), which signal that women are valued and can perform well in leadership roles at the firm (Zhang & Qu, 2016). In addition, given their own experience with gender bias (Kulich, Trojanowski, Ryan, Haslam, & Renneboog, 2011; Main & Gregory-Smith, 2018), female directors are likely more equipped to recognize any biased treatment that female CEOs may face and to help them overcome such challenges (Cook & Glass, 2015; Matsa & Miller, 2011). This could be achieved directly via mentoring and sharing of information with the CEO (Amore, Garofalo, & Minichilli, 2014; Cook & Glass, 2015) or more indirectly by calling out biased treatment during board meetings. Prior evidence supports the idea that female CEOs benefit from female directors’ presence, as it has been shown to improve the postsuccession profitability of female CEOs in family-controlled firms in Italy (Amore et al., 2014) and in Fortune 500 U.S. firms (Cook & Glass, 2015). Thus, we argue that female CEO candidates appointed to firms with female director presence will likely perceive the potential of having a powerful ally on their side and thus perceive less termination vulnerability.

Together, the work discussed so far suggests that female director presence should alleviate female candidates’ termination concerns in CEO roles. However, since the majority of board members are still men (Gupta et al., 2020; Zhang & Qu, 2016), we do not believe that female director presence at the current levels will substantially affect male CEO candidates’ concerns. Indeed, male candidates are unlikely to perceive that they will face role congruity bias and thus be at a disadvantage in a CEO role when a woman is present on the board. Thus, we predict the following:

Hypothesis 5: The relation between gender and the value of CEOs’ initial severance agreements is moderated by female director presence such that the latter weakens the positive relation between female CEO and severance value.

Methods

Data

We collected data from a variety of sources for this study. First, given that our study focuses on new CEO appointments, we identified all new CEOs for all publicly traded U.S. firms during 2007 to 2014 using the S&P ExecuComp database. We excluded any “interim” CEOs as identified in their titles, similar to Oliver et al. (2018). Given the imperfections of the ExecuComp database with regard to severance agreements documented by Cadman et al. (2016), we searched for the proxy statement (DEF 14A) of each firm identified as having a new CEO and hand-coded its incoming CEO’s initial guaranteed severance dollar value for involuntary termination. Specifically, we obtained each firm’s proxy statement from the Securities and Exchange Commission’s website. We then searched for guaranteed severance pay information for each CEO and coded the total dollar value of guaranteed involuntary termination pay. Some firms listed these data in a table; for these firms, we simply coded the value. When this information was not directly provided, we calculated these values using text descriptions of guaranteed involuntary termination value and compensation summary tables, as severance agreements are often based on a combination of different forms of total compensation, including base salary, lump-sum cash, vested and unvested stock and stock options, insurance coverage, pension plan acceleration, among other items (Zhao, 2013). Following Cadman et al. (2016), we did not include already earned or already “vested” compensation (we subtracted these amounts from the total severance value).

Firm- and individual-level characteristic variables were gathered from ExecuComp and Compustat, except for governance data, which were gathered from RiskMetrics. Similar to previous studies on CEO dismissal (e.g., Cannella & Lubatkin, 1993; Jenter & Kanaan, 2015; Shen & Cannella, 2002a, 2002b), we obtained news reports and press releases surrounding early departures of CEOs to determine whether the CEO was dismissed. Given that our sample includes only CEOs who were appointed between 2007 and 2014, our analysis is based on 870 observations.

Dependent Variable

We examined the guaranteed dollar values of severance payments contained in CEOs’ initial severance agreements (negotiated at the time of appointment). We used the total dollar value of guaranteed severance pay for involuntary termination collected from proxy statements, as specified in each incoming CEO’s initial severance agreement. For CEOs without an agreement, we coded the value as zero, adding one before logging it. We then logged this measure, as is commonly the case for executive compensation studies.

Independent Variable

The predictor variable in our study is CEO gender, coded as 1 for female and 0 for male.

Moderators

Declining firm performance

As in prior research, firms had to experience multiple years of declining firm performance to be characterized as declining (Bruton, Ahlstrom, & Wan, 2003; Morrow, Johnson, & Busenitz, 2004; Pearce & Robbins, 1993; Wiseman & Bromiley, 1991). Specifically, we constructed a dummy variable that equaled 1 if return on equity (ROE) declined for three consecutive years prior to CEO appointment and 0 otherwise. The hypothesized result for declining firm performance is robust to using return on assets instead of ROE and to operationalizing declining firm performance as four or five consecutive years of declining ROE prior to appointment instead of three.

Early dismissal of prior CEO

In line with prior research using news reports and press releases surrounding the departure of the previous CEO, we defined the prior CEO as being dismissed early if he or she was terminated within a short period, defined as ≤3 years after appointment (Finkelstein & Hambrick, 1996; Zhang, 2008) and “all officership and directorship connections between the firm and its outgoing CEO were severed at the time of succession” (Cannella & Lubatkin, 1993: 777). Specifically, we created a dummy variable equal to 1 if the outgoing CEO’s tenure was within 1 to 3 years, given that CEOs with tenure <1 year are likely to be interim CEOs, and all connections with the firm were cut off at the time of termination. We coded this variable as 0 if the prior CEO did not depart early, if his or her tenure was <1 year, or if the prior CEO remained connected to the firm after termination via directorship, officership, advisorship, or consulting positions, as mentioned in news reports or press releases related to the CEO’s departure.

This definition of “dismissal” is particularly relevant to our study on female CEOs given the importance of a mentoring and partnering relationship with the predecessor for a female CEO’s success (Dwivedi et al., 2018). In addition, although the male gender role is often associated with independence, the female gender role is associated with communal qualities. If the prior CEO is no longer involved, the new CEO becomes the sole (independent) leader of the firm, thus potentially increasing perceptions of role incongruity. Last, we focus on “early” dismissal given that a CEO dismissed after a long tenure could simply be a manifestation of the need for periodical renewal, as is the case, for example, in CEO successions that involve an heir apparent (Cannella & Shen, 2001), which should not be especially concerning to female CEO candidates.

Presence of female CEOs in the focal firm’s industry

This variable is defined as the proportion of female CEOs in the industry in the prior year, based on the two-digit SIC code (Cook & Glass, 2011).

Female director presence

We operationalized female director presence as a dichotomous variable equal to 1 if there was at least one female director on the board in the year prior to the CEO appointment and 0 otherwise, similar to previous studies (Geiler & Renneboog, 2015; Zhang & Qu, 2016). 6

Controls

We included several CEO- and firm-level control variables that may influence CEOs’ initial severance agreements, as identified by previous studies (e.g., Bodolica & Spraggon, 2009; Cadman et al., 2016; Rau & Xu, 2013). Because initial severance agreements are negotiated at the time of CEO appointment, we lagged our firm-level controls. We dropped all observations that were missing, resulting in our final sample of 870 observations.

Prior research has shown that firm risk is associated with the value of the severance agreement, given that being employed at a firm with greater risk is likely to increase one’s termination vulnerability (Cadman et al., 2016; Rau & Xu, 2013). We used two common measures of firm risk: return volatility and leverage. Specifically, we controlled for return volatility, defined as the lagged annualized standard deviation of the log of daily stock returns, multiplied by 252(1/2) (Cadman et al., 2016), and firm leverage, defined as a firm’s lagged total liabilities divided by lagged liabilities plus lagged stockholders’ equity. We also controlled for firm size using the natural logarithm of lagged total sales because it may be an important determinant of the use and size of severance agreements (Rau & Xu, 2013; Rusticus, 2006). In addition, since better-performing firms tend to offer higher pay (Bertrand & Hallock, 2001), we took into account firm performance by controlling for the lagged 3-year average of ROE (Cook & Glass, 2014). We also controlled for industry performance using the 3-year industry (two-digit SIC code [Standard Industrial Classification]) average of ROE and a stock measure of performance by controlling for lagged total shareholder return.

Similar to past severance studies (e.g., Bodolica & Spraggon, 2009), we controlled for board independence using the lagged proportion of independent board members. Because firms that pay more may offer higher guaranteed severance, we also partialed out the effect of CEO compensation using the natural logarithm of annual total pay (TDC1), defined as the sum of salary, bonus, stock, stock options, nonequity incentive pay, deferred compensation earnings, and other pay (Rau & Xu, 2013; Schwab & Thomas, 2006). Prior research has also shown that internal appointees tend to receive smaller severance agreements than do external appointees (Gillan et al., 2009; Rusticus, 2006). Thus, we controlled for internal appointee, a dummy variable that equals 1 if the incoming CEO had been employed by the firm for ≥2 years and 0 otherwise (Cannella & Lubatkin, 1993; Harris & Helfat, 1997). In addition, younger CEOs tend to demand higher guaranteed severance pay: as they do not have an established track record, it is more difficult for them to find a comparable job in case they are dismissed. Thus, we controlled for the effect of CEO age (Rau & Xu, 2013). We also controlled for CEO duality (coded 1 if a new CEO also had the title of chairman, 0 otherwise), as this may decrease the likelihood of CEO dismissal (Zhang, 2008). Last, we included a control for CEO ownership, defined as the lagged percentage of total shares outstanding held by the CEO, given that CEOs who own less of the firm’s equity often have larger severance agreements (Cadman et al., 2016). 7

Analysis

To analyze the data, we standardized predictor variables, except for dichotomous variables, before creating the interaction terms. Given the structure of our data, we used ordinary least squares models with year dummies and two-digit industry clustering. 8 However, our results are also robust to industry random effects models. Variance inflation factor scores indicated that multicollinearity was not an issue in any model, as all of those scores were <5 and the mean scores were <2.

Results

Summary Statistics and Empirical Results

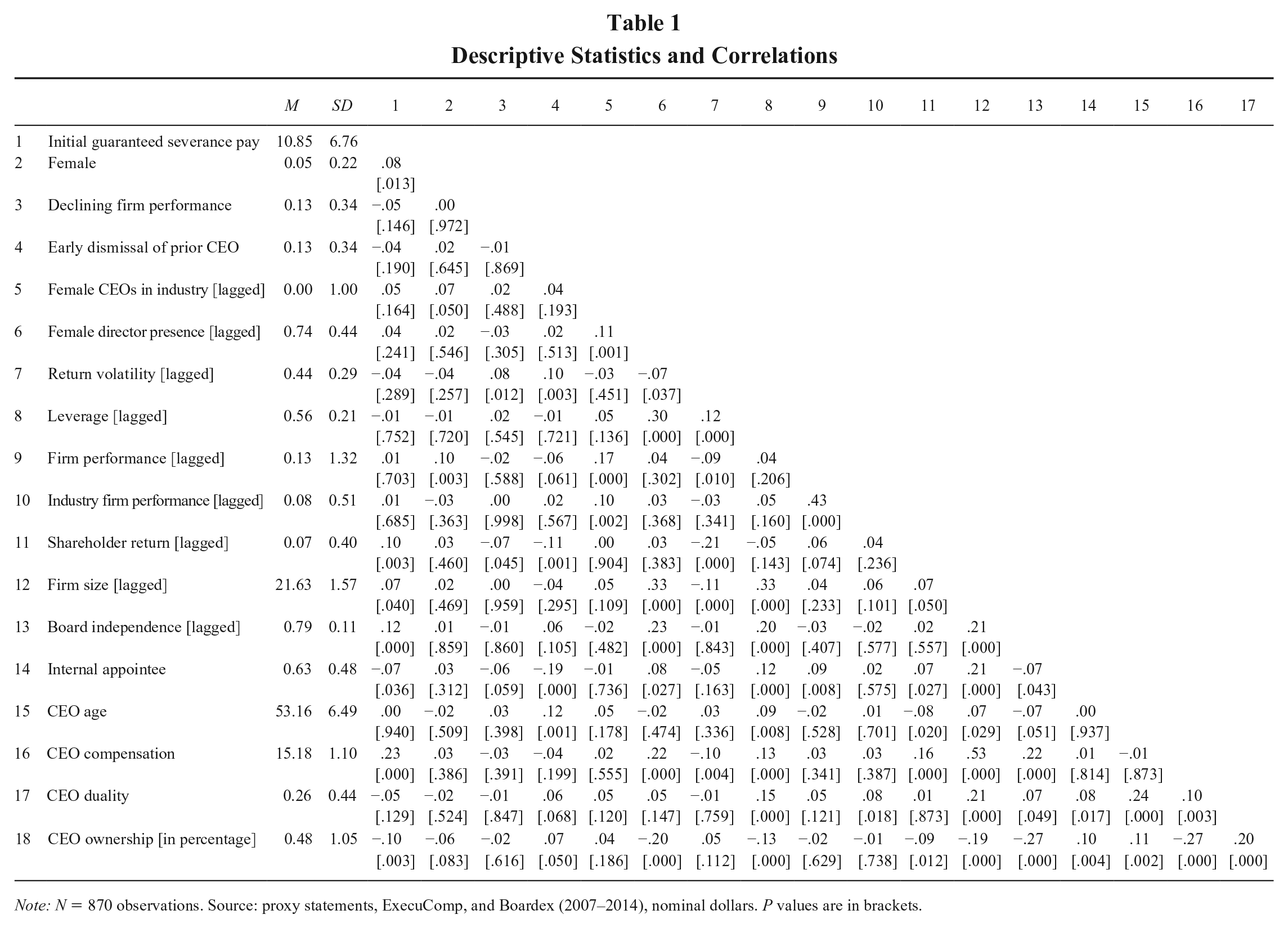

Table 1 presents the summary statistics for all CEO appointments from 2007 to 2014. Approximately 5% of incoming CEOs in our sample are women. Additionally, roughly 73% of incoming CEOs have a severance agreement, with a mean guaranteed payment of $4.3 million and median of $1.9 million.

Descriptive Statistics and Correlations

Note: N = 870 observations. Source: proxy statements, ExecuComp, and Boardex (2007–2014), nominal dollars. P values are in brackets.

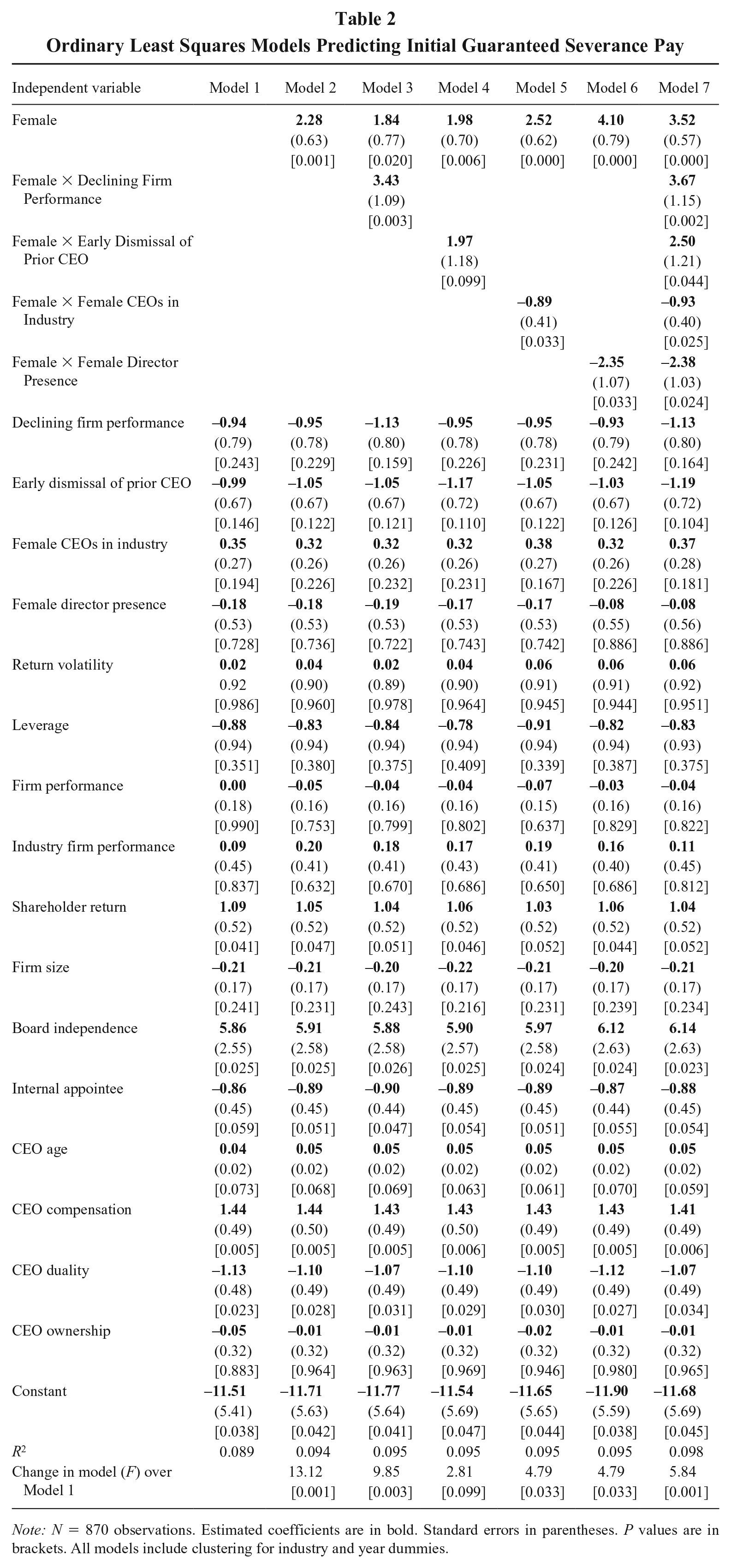

Table 2 presents the results of the regressions used to test Hypotheses 1 through 5, controlling for standard determinants of severance agreements. Model 1 includes only the control variables. In Model 2, we examine the influence of CEO gender on CEOs’ initial severance agreements by including the female dummy. The results indicate that guaranteed severance payments tend to be larger for incoming female CEOs rather than incoming male CEOs (b = 2.28, p = .001), supporting Hypothesis 1. By assessing the magnitude of this effect (based on Model 2), the predicted guaranteed severance pay is $5.2 million for incoming female CEOs and $0.8 million for incoming male CEOs, all else equal.

Ordinary Least Squares Models Predicting Initial Guaranteed Severance Pay

Note: N = 870 observations. Estimated coefficients are in bold. Standard errors in parentheses. P values are in brackets. All models include clustering for industry and year dummies.

Models 3 to 6 present each interaction individually, and Model 7 presents the test of our interaction hypotheses. Hypothesis 2 predicted that a firm’s declining performance would strengthen the positive relation between CEO gender and guaranteed severance pay. The coefficient for the Female Dummy × Declining Firm Performance interaction term is positive in Model 7 (b = 3.67, p = .002), consistent with Hypothesis 2. Hypothesis 3 predicted that the early dismissal of the prior CEO would also strengthen the relation between CEO gender and guaranteed severance pay. We find support for this hypothesis (b = 2.50, p = .044). 9 Consistent with Hypothesis 4, we find that the presence of female CEOs in the focal firm’s industry prior to appointment weakens the relation between CEO gender and guaranteed severance pay (b = −0.93, p = .025). Last, Hypothesis 5 predicted that female director presence prior to appointment weakens the relation. We also find support for this hypothesis (b = −2.38, p = .024).

Finally, considering the economic significance of our moderators while controlling for other factors, the estimated percentage increase in guaranteed severance pay for incoming female CEOs in firms with declining performance (Model 3) is 897% (to put this number in perspective, the predicted guaranteed severance pay for incoming female CEOs is $1.0 million in nondeclining firms and $12.8 million in declining firms). In firms where the prior CEO was dismissed early, incoming female CEOs’ guaranteed severance pay increases by 123% (Model 4). For a one–standard deviation increase in the proportion of female CEOs in the firm’s industry, incoming female CEOs’ guaranteed severance pay decreases by 40% and by 91% in firms with female directors (Models 5 and 6, respectively).

Supplemental Analyses

Gender-based difference in severance by termination event

While our empirical analysis examined severance agreements in the case of involuntary termination, an analysis of proxy statements (DEF 14A) reveals that severance agreements are negotiated for a number of other involuntary and voluntary termination events beyond involuntary termination—namely, (1) voluntary retirement, (2) resignation without good reason, (3) voluntary termination for good reason, (4) involuntary termination without cause, and (5) involuntary termination with cause. Voluntary retirement and resignation without good reason occur when CEOs either retire or leave on their own volition, and voluntary termination with good reason occurs in response to changes in employment terms (e.g., relocation of headquarters; Bodolica & Spraggon, 2009: 988). Involuntary termination is often triggered by unsatisfactory performance, while involuntary termination with cause is generally defined by events such as felony, fraud, embezzlement, neglect of duties, or violation of noncompete provisions (Schwab & Thomas, 2006). If female executives perceive greater vulnerability to termination in a CEO role due to downwardly biased evaluations, then incoming female CEOs should have higher guaranteed severance pay than male CEOs only for termination events that are performance related and outside the control of the CEO. The only event that falls into this category is involuntary termination.

To explore this, we hand-collected the guaranteed severance dollar values for all five termination events listed earlier from Fortune 500 and S&P 500 firms’ proxy statements. Due to the arduous and time-consuming task of hand-coding proxy data, we collected these data from 2010, which falls in the middle of our sample time frame. 10 We then regressed the logged value of guaranteed severance pay for each termination event on the female dummy variable and all the controls included in the main analysis at the time of appointment (resulting in 320 observations). As seen in Appendix A, the guaranteed severance pay of female CEOs is larger than that of male CEOs for involuntary termination—and involuntary termination only (b = 4.60, p = .033). Thus, these results provide additional support that female candidates perceive greater involuntary termination vulnerability in CEO roles than do male candidates.

Endogeneity checks

Next, we wanted to examine how strong a correlated omitted variable would need to be to overturn our results, by calculating the impact threshold of a confounding variable for our main model (Frank, 2000). We find that an omitted variable would have to be correlated at .246 with CEOs’ initial severance agreement value and .246 with CEO gender to invalidate our results, corresponding to an “impact” of .0604. Given that the largest impact of our observed covariates is .0068 based on unconditional correlations and .0031 based on partial correlations, the “impact” of an omitted variable would thus need to be much larger than any of the variables that we already included in our model. If we assume that we have a reasonable set of control variables, this suggests that the results are likely not driven by a correlated omitted variable.

In addition, to ensure the robustness of our findings, we empirically tested that hiring a female CEO is not endogenous, by performing a Durbin-Wu-Hausman test (cf. Davidson & MacKinnon, 1993). The test includes the residuals of potentially endogenous right-hand-side variables, as a function of the instrumental variables and the exogenous variables in a regression of the original model (Jiang et al., 2017). This test allows us to assess whether the estimates obtained by ordinary least squares are consistent. Using the lagged number of female executives excluding the CEO as the instrumental variable in the first regression, we found the coefficient on residuals to be nonsignificant (p = .646) in the second-step regression, indicating that the endogeneity of the CEO’s gender is unlikely to be an issue.

Alternative explanations

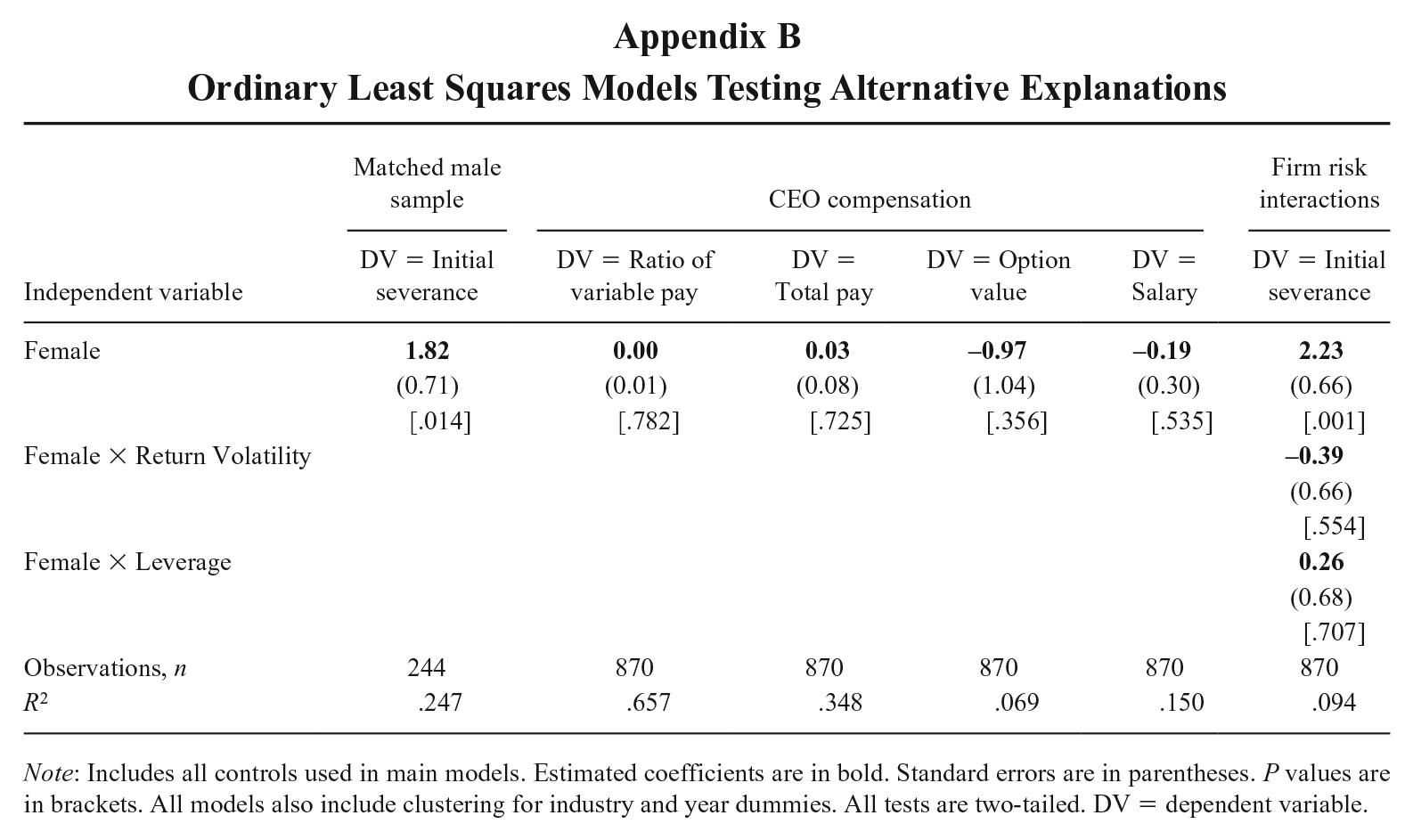

We performed several supplemental analyses to rule out alternative explanations for our main finding that new female CEOs tend to have larger severance agreements than new male CEOs. First, we ran our main models on a matched sample of incoming male CEOs. Propensity score matching ensures that the matched group (incoming male CEOs) is as similar as possible to the treatment group (incoming female CEOs) on observable characteristics (Amore et al., 2014). Following other studies (e.g., Amore et al., 2014; Cook & Glass, 2014), we estimated the propensity score with firm performance, firm size, industry, and percentage of female outside board members. We then used the nearest neighbor method to obtain our matched sample of incoming male CEOs (Li, 2012), and we ran the same models as presented in Model 2 of Table 2. Matching on five males for each female CEO (n = 244), we find no material differences between this analysis and our main model (b = 1.82, p = .014). These results are displayed in Appendix B. Thus, gender-based sorting does not appear to explain our results.

Second, it could be that male and female CEOs receive very different compensation contracts so that the effect of gender differences in severance agreements in facilitating female CEO appointments might be overstated. To investigate this possibility, we examined whether incoming female CEOs’ pay structures were composed of lower levels of “at risk” pay than incoming male CEOs’. We also explored whether differences in total pay or cash-based pay existed. To do so, we ran regressions similar to those presented in Model 2 of Table 2, using the ratio of variable pay to total pay (defined as stock, stock options, and nonequity incentive pay divided by the total of salary, bonus, stock, stock options, nonequity incentive pay, deferred compensation earnings, and other compensation), total annual pay, the value of yearly stock options, and salary as the dependent variables. 11 As seen in Appendix B, we do not find gender differences for the proportion of variable pay (b = 0.00, p = .782), total annual pay (b = 0.03, p = .725), stock option value (b = −0.97, p = .356), or salary (b = −0.19, p = .535). These results indicate that the total amount and structure of the compensation packages of comparable male and female CEOs are statistically indistinguishable at the time of appointment.

Last, while our theory suggests that recent organizational distress can heighten female CEO candidates’ termination concerns, there is some evidence that women tend to be more risk averse than men (e.g., Croson & Gneezy 2009; Eckel & Grossman, 2008, Jianakoplos & Bernasek, 1998), including firm executives (Jeong & Harrison, 2017). Thus, although we controlled for measures of firm risk (stock price volatility and leverage) in our main models, it is possible that female CEOs are more risk averse than male CEOs, which could be driving the gender difference in the initial severance agreements. To explore this, we studied whether stock return volatility and leverage also have a moderating effect on the difference in severance agreements between women and men. We find that measures of firm risk do not have a statistically significant moderating effect (b = −0.39, p = .554; b = 0.26, p = .707), as displayed in Appendix B. Thus, typical measures of firm risk do not appear to heighten female CEO candidates’ perceptions of termination vulnerability as compared with male candidates’, suggesting that our results are not driven by gender differences in risk aversion.

Discussion

In this study, we propose that, due to inherent gender bias and male-type leadership schemas, female executives will perceive heightened termination vulnerability when considering a CEO role. We further theorize that certain contingencies will heighten or alleviate women’s termination concerns. Specifically, we argue that indicators of recent organizational distress should heighten female candidates’ perceptions of bias in CEO roles and thus further increase their termination concerns. In contrast, the presence of female leaders is likely to decrease their perceptions of bias and thus attenuate those concerns. Our results support our arguments and have theoretical and practical implications.

First, our findings contribute to recent literature that studies the factors that affect the appointment of female CEOs (Cook & Glass, 2014; Zhang & Qu, 2016). Specifically, we find that incoming female CEOs receive larger severance agreements than do incoming male CEOs, or a “gender severance gap” in favor of female CEO candidates. On its own, this result contributes to the gender gap literature, which typically documents “gaps” in favor of men (Bertrand & Hallock, 2001; Blau & Kahn, 2017; Joshi, Son, & Hoh, 2015). More broadly, this result supports our argument that women perceive greater termination vulnerability than men do when considering CEO roles—thus, the advantageous gender gap in severance agreements emanates from an initial disadvantage. This has important implications for corporate governance and recruiting. In particular, although prior literature has argued that severance agreements can function as a recruitment tool (Cowen et al., 2016; Rau & Xu, 2013), empirical work has yet to provide support for this argument (Klein et al., 2017). Consistent with gender and UE research, female leaders’ heightened termination concerns likely lead some women to “opt out” from assuming executive roles. Although severance agreements cannot reduce women’s perceptions of termination vulnerability, they can insure against termination losses, thereby at least partly mitigating female CEO candidates’ termination concerns. As such, we argue that more valuable severance agreements can be particularly useful in the recruitment of female executive candidates.

We further show that the magnitude of the difference in severance agreements between incoming female and male CEOs appears to vary with factors affecting female candidates’ perceptions of termination vulnerability in CEO roles. Specifically, we find that this difference is (1) larger in organizations on a declining performance trend or where the prior CEO was dismissed early and (2) smaller in firms that have at least one female director or operate in industries with more female CEOs. These findings provide some preliminary evidence about the specific conditions that seem to exacerbate and alleviate women’s perceptions of biased treatment, rather than simply insuring them against termination losses as severance agreements do.

We also show in our supplemental analyses that the structure and total annual compensation of new female and male CEOs are statistically undistinguishable, which stands in contrast with our finding that female CEOs do receive more valuable initial severance agreements than do men. While a large literature indicates that women face greater challenges in top executive roles than men (Eagly & Karau, 2002; Park & Westphal, 2013), the findings here suggest that these challenges may actually give women an advantage when bargaining with boards, which has not yet been recognized by prior research. Indeed, scholars and the media have been paying more attention to the biases and challenges faced by women in top leadership positions (Dixon-Fowler, Ellstrand, & Johnson, 2013) and to the fact that women are rarely appointed as CEOs (Catalyst, 2018). As a result, some boards may already be very attuned to the concerns of women considering CEO roles and offering higher levels of guaranteed severance pay to female candidates, relative to male candidates, to encourage them to accept those roles. Specifically, when the board and the CEO candidate are both aware of the greater obstacles faced by a CEO because of her gender, a female CEO candidate is likely to be more credible at the negotiation stage when she asks for a more generous severance agreement—the board might be less receptive to similar demands formulated by a male CEO candidate. Nevertheless, to better understand the drivers of the difference in severance agreements between women and men, future research could develop a better understanding of the negotiation process between CEO candidates and the board—for example, by using experiments, surveys of female and male CEOs, and/or interviews with boards of directors, compensation consultants, and CEO candidates.

Relatedly, although we do not find statistically significant differences between incoming male and female CEOs for standard forms of compensation, we believe that addressing how CEOs may trade off severance against other forms of compensation or other aspects of the employment contract would also be beneficial for pushing research on severance agreements forward. For example, it is possible that some CEOs forgo pension benefits and perquisites to enhance their contractual severance payment when negotiating their employment contracts. An alternative hypothesis advanced by Bebchuk and Fried (2004) is that some CEOs will attempt to extract more benefits from the firm by “camouflaging” their compensation into items not reflected in their “annual compensation”—in which case, they will obtain more generous severance agreements as well as additional benefits. Additional research is needed to explore this question, as well as if and how men and women trade off compensation in different ways.

Consistent with our theory, the fear of biased treatment leads female candidates to perceive greater termination vulnerability from accepting CEO roles as compared with their male counterparts. The reason is that, not only do they perceive that they will face more negative reactions to their appointment than will male CEOs (Jeong & Harrison, 2017; Lee & James, 2007), but they also expect biased evaluations of their actions over time (Gupta et al., 2018; Park & Westphal, 2013). Given that these concerns are inextricably linked, we argue that female CEO candidates will be more likely than their male counterparts to require severance agreements to accept CEO roles. However, although boards may perceive severance as a recruitment tool, they may also view it as a tool for aligning CEOs’ interests with those of shareholders postappointment (Almazan & Suarez, 2003; Cadman et al., 2016). This raises an interesting question of if and/or how boards’ interest alignment concerns may influence incumbent CEOs’ severance values throughout their tenures and, further, whether gender-related severance gaps persist over time (Klein et al., 2017). Although this question is beyond the scope of this study, examining the factors that may affect CEOs’ postappointment severance values and gender-related severance gaps offers interesting avenues for scholars to pursue.

As discussed earlier, we found that factors that increase women’s expectations of bias in CEO roles—namely, recent organizational distress—heighten the difference in severance between incoming male and female CEOs. Interestingly, our theory and our empirical findings suggest that female CEOs are not merely more averse than men to adverse circumstances, such as a declining firm performance, when considering a CEO position. Instead, our findings indicate that male CEOs tend not to get more valuable severance agreements when appointed to firms with a declining performance or to firms where the previous CEO was prematurely dismissed, as evidenced by the nonsignificant main effect of declining firm performance and prior CEO dismissal in Table 2 (Model 7). To the extent that severance agreements reflect termination concerns, men seem to be unfazed by these adverse circumstances. This may seem somewhat surprising in light of conventional arguments but is consistent with our role congruity perspective. This subset of findings is also consistent with prior work showing that male executives are often more overconfident than female executives (Barber & Odean, 2001; Huang & Kisgen, 2013). Future research could build on our findings by continuing to (1) uncover situations in which male CEOs and female CEOs may interpret stimuli differently and (2) further explore if there are situations where male CEOs perceive greater termination vulnerability than do female CEOs.

Furthermore, as explained so far, neither our theoretical arguments nor our empirical results indicate that the presence of female leaders at their current levels affect men’s termination concerns. This might however be different if women were as dominant as men currently are in firms’ UEs. It is thus an open question if and at what point men’s termination concerns begin to change as women occupy more and more UE roles to such an extent that gender roles are redefined. This does not imply that female leaders are systematically at a disadvantage nowadays: studies referenced by Eagly, Karau, and Makhijani (1995) found that female leaders tend to be viewed as more effective than male leaders in educational, governmental, and social service organizations, as leader roles have a more feminine definition in these organizations. Thus, it seems that female CEOs could be at an advantage in corporations that resemble nonprofit organizations along some dimensions, including the gender makeup. Admittedly, it is arduous to measure such differences, even though more qualitative studies might be able to capture them—scholars have argued that for-profit and nonprofit organizations are more similar than is often believed (e.g., Brody, 1996). We believe that this question provides a fruitful opportunity for additional research designed for developing a deeper understanding of female and male CEOs’ termination concerns in different types of organizations and among various industries with different gendered leadership concentrations.

Finally, although we theorize and show evidence consistent with the notion that the presence of other female leaders plays an important role in allaying the concerns that women may have about experiencing biased treatment in CEO roles, we do not address the policies and practices that can lead to a greater presence of female leaders. Other research, however, provides guidance on this important issue. For instance, some have argued that gender quotas for top management teams and boards may help to “break the structures that endogenously favor the inequality” (Kogut, Colomer, & Belinky, 2014: 892). Thus, quotas, which mandate a target for a certain group, can help achieve a critical mass of female corporate leaders (Kogut et al., 2014). Accordingly, several European countries have adopted gender quotas for corporate boards. For example, Germany recently passed legislation requiring firms to raise the percentage of women on the board of directors to 30% (Smale & Miller, 2015). Similar legal requirements are in effect in Norway, Spain, France, Belgium, Italy, Iceland, and the Netherlands. We contribute to this debate by showing that increasing female leader representation may lower women’s concerns about biased treatment in CEO roles. Yet, additional research is needed to explore the consequences of quotas and other ways to increase the presence of women in UE roles. In addition, the aforementioned countries could provide an interesting context to understand if and how men’s concerns change as the presence of female leaders increases in firms’ UEs. Last, prior work has argued that directors’ experience or familiarity with certain events can influence the type of events to which they pay attention and their evaluations of such events (Johnson, Schnatterly, & Hill, 2013). Thus, it is possible that women’s termination concerns will be mitigated in firms where directors have prior experience working with a female CEO in their own “home firms” or at other firms where they are directors. This “familiarity hypothesis” could be explored in future studies.

Conclusion

Severance payments are often viewed as a pernicious form of rent extraction or even insurance for incompetence (Bebchuk & Fried, 2004; Dalton, Daily, & Kesner, 1993; Morrison, 1982). This article contributes to a literature that argues that firms may benefit from the use of severance agreements in certain situations. Specifically, our findings suggest that severance agreements, which insure CEOs against involuntary termination, play an important role in the appointments of female CEOs. We identified two important factors—declining firm performance and the early dismissal of a previous CEO—that heighten female CEO candidates’ concerns regarding a CEO role. We also identified two factors—the presence of female CEOs in the focal firm’s industry and the presence of female directors on its board—that alleviate their concerns. We have argued that these factors affect women’s perceptions of biased treatment in CEO roles. We hope that our findings help to provide a stronger foundation on which scholars can build to provide a deeper theoretical and empirical understanding of the factors that enhance or reduce female executives’ proclivity to pursue and accept top leadership roles.

Footnotes

Appendix

Ordinary Least Squares Models Testing Alternative Explanations

| Matched male sample | CEO compensation | Firm risk interactions | ||||

|---|---|---|---|---|---|---|

| Independent variable | DV = Initial severance | DV = Ratio of variable pay | DV = Total pay | DV = Option value | DV = Salary | DV = Initial severance |

| Female |

|

|

|

|

|

|

| (0.71) | (0.01) | (0.08) | (1.04) | (0.30) | (0.66) | |

| [.014] | [.782] | [.725] | [.356] | [.535] | [.001] | |

| Female × Return Volatility |

|

|||||

| (0.66) | ||||||

| [.554] | ||||||

| Female × Leverage |

|

|||||

| (0.68) | ||||||

| [.707] | ||||||

| Observations, n | 244 | 870 | 870 | 870 | 870 | 870 |

| R 2 | .247 | .657 | .348 | .069 | .150 | .094 |

Note: Includes all controls used in main models. Estimated coefficients are in bold. Standard errors are in parentheses. P values are in brackets. All models also include clustering for industry and year dummies. All tests are two-tailed. DV = dependent variable.

Acknowledgements

We would like to thank our editor, Karen Schnatterly, and three anonymous reviewers for their constructive and developmental feedback during the review process. We are also grateful to Jeremy Bernerth, Kevin Hallock, Mevan Jayasinghe, Gerry McNamara, Danny Miller, Daniel Rush, Taekjin Shin, Maite Tapia, Michael Withers, and participants of the Reputation Symposium at Oxford University’s Centre for Corporate Reputation for their helpful comments on earlier versions of the paper.