Abstract

We theorize about board decision making by introducing image theory, a descriptive theory of selection for decisions of more than routine importance, to research on CEO successor selection. We contend that directors’ current and future images of the firm typically revolve around their main responsibility, maximizing shareholder wealth. However, following discovery of misconduct, those images shift to the misconduct and to how it might be prevented. As such, ethical leadership dominates their criteria for a CEO successor. Evaluating candidates’ moral principles is nontrivial; there are few observable indicators. We develop arguments that, following organizational wrongdoing, directors are more likely to choose a CEO successor with a degree from a religiously affiliated university than they would under other conditions. We also find their intuition is correct: Choosing a CEO with a degree from a religious university reduces the likelihood of misconduct. In moderating analyses, we uncover a hidden irony: Directors in industries where misconduct is common are the least likely to choose, but the most likely to need, a CEO with a degree from a religious university. Results from analyses of S&P 1500 firms and a policy capturing study of actual directors support our hypotheses.

Management researchers have long sought to understand successor selection in the event of CEO turnover (Kunisch, Menz, & Cannella, 2019), with recent studies devoting particular emphasis to the special circumstance of CEO successor selection following corporate misconduct (Connelly, Ketchen, Gangloff, & Shook, 2016; Gomulya & Boeker, 2014). CEO turnover is common after the occurrence of misconduct (Arthaud-Day, Certo, Dalton, & Dalton, 2006), but the firm’s bad behavior complicates the question of who should be the next CEO (Gomulya & Mishina, 2017). Studies on the topic have yielded important insights, relying largely on signaling theory and symbolic management to explain decisions about choosing a CEO successor in the aftermath of misconduct (Gangloff, Connelly, & Shook, 2016; Gomulya, Wong, Ormiston, & Boeker, 2017).

Much of this work focuses on the initial reactions and impressions of external evaluators. We introduce image theory (Beach, 1993) to this literature, which allows us to develop arguments about the decision process directors undergo when making their choice of a CEO successor. Image theory is a descriptive theory of selection for “decisions of more than routine importance” (Beach & Mitchell, 1987). This theoretical perspective provides a way of understanding decision making that is not simply a degenerative version of expected utility maximization but, rather, is based on the evaluation of key cognitive schemata, or images (Miller, Galanter, & Pribram, 1986). In the wake of misconduct, ethical norms of behavior become especially salient and shape directors’ images about the company’s desired future state (i.e., one without misconduct) and the strategy for achieving it (i.e., hiring a CEO with high ethical standards). Finding a candidate who aligns with directors’ image of the ethical way the firm should operate going forward is daunting, because it is difficult to assess characteristics about integrity via externally observed factors (Morgeson, Campion, Dipboye, Hollenbeck, Murphy, & Schmitt, 2007).

To find a CEO successor that directors believe will successfully bring the firm toward a future state characterized by ethical business practice, they may look for clues about candidates’ moral values (Haselhuhn & Wong, 2012). Ethical theorists describe this as a process of deontological evaluation, or judging the extent to which candidates believe there is inherent good and bad in their actions, separate from the consequences of those actions (Laczniak & Murphy, 2006). There are many possible foundations of moral judgment, but scholars commonly acknowledge personal religiousness is an observable social factor that is closely linked to perceived ethical behavior (Parboteeah, Hoegl, & Cullen, 2008). Directors are unlikely to know the religious practices of candidates, but those that attended religiously affiliated universities communicate information about their religiosity (Lyon, Beaty, & Mixon, 2002). We, therefore, investigate the extent to which directors at firms that engaged in financial misconduct replace the CEO with a successor who has a degree from a university with an active religious mission.

Our work makes several contributions to the literature. First, we shift research on the succession decision from information economics to the way directors view the firm and what they envision for it. Discovery of misconduct puts directors in a precarious situation that affects their decisions, and few have delved into trying to understand directors’ thought processes in this situation. Second, we examine the extent to which the strategy of hiring a CEO with a degree from a religious university reduces misconduct (Dyreng, Mayew, & Williams, 2012; Hilary & Hui, 2009). Interestingly, our results show that directors of firms that operate in industries where misconduct is a relatively common occurrence are the least likely to choose, but the most likely to benefit from, a CEO with a degree from a religious university. Third, we build on recent studies that explore the extent to which a CEO’s early life experiences affect corporate outcomes (Bernile, Bhagwat, & Rau, 2017; Kish-Gephart & Campbell, 2015; Martin, Côté, & Woodruff, 2016).

Conceptual Development

Image Theory

Image theory describes how individuals make decisions (Beach, 1993). This theory stands in contrast to normative models of choice based on economic theory, which are often criticized for not representing the way decisions are actually made (Beach & Lipshitz, 2017). In the image theory framework, there are three different schematic knowledge structures that aid in choosing the best-fitting option in a choice set. The first is the value image, which lays the foundation for all decisions because it is composed of “self-evident truths about what [a decision maker], or the group or organization, stands for” (Beach & Connolly, 2005: 161). The value image includes the principles that are important to the decision maker. These principles inform the trajectory image, which consists of the decision maker’s goals and vision of an ideal future state. Third is the strategic image, where the decision maker matches goals from the trajectory image with a plan for goal attainment.

A decision maker uses the value, trajectory, and strategic images to make adoption decisions (and progress decisions, but those are not the focus of this study). Adoption decisions involve whether to add constituents to any of the three aforementioned images. For example, the process of choosing a CEO successor is an adoption decision in which a constituent is added to the strategic image in the hope of helping an organization reach a desired future state. As CEO candidates are evaluated, there is an assessment of their compatibility with the organization’s principles, goals, and existing strategic plans. This evaluation is a two-step process (Donnelly & Quirin, 2006). The first step is screening, where the decision maker eliminates options that are clearly incompatible with what they envision for the firm (Sekiguchi & Huber, 2011). The second step is profitability, where the decision maker chooses the most promising option among survivors of the screening phase, based on compatibility with their images of the firm.

Under normal operating conditions (i.e., absent revelations of misconduct), directors would likely create images about the firm that revolve around their main responsibility, which is to provide a return to shareholders. Their value image, therefore, would center on issues of performance, such as the firm’s productivity, growth, or profitability. Principles that reflect how the firm competes, such as their innovativeness (e.g., Tesla), efficiency (e.g., FedEx), or corporate culture (e.g., Southwest Airlines), underscore key aspects of directors’ value image (Schaffer, 2002). Their value image could also encompass moral principles, such as transparency and truthfulness, but competitive characteristics that have proven successful are likely to dominate. Directors are also likely to have a performance-based trajectory image where they define the future of the firm in terms of their position in the competitive marketplace. More often than not, trajectory images are optimistic because directors expect positive outcomes and are sanguine about the firm’s future (Fiske & Taylor, 2008). Conforming behavior remains largely unnoticed, so under normal operating conditions, there would be little reason for directors to question the firm’s moral principles.

Successor Selection

In this article, we are concerned with firms that have engaged in misconduct, which is the “organizational pursuit of any action considered illegitimate from an ethical, regulatory, or legal standpoint” (Harris & Bromiley, 2007: 351). The revelation of corporate misconduct forces directors to reconsider their images in view of recent expectancy violation (Floyd & Voloudakis, 1999). When firms and their managers deviate from commonly held expectations, it sends a shock that creates cognitive dissonance for directors, forcing them to attend to their images and recalibrate their expectations about the firm’s future state (T. Lee & Mitchell, 1994).

In this situation, framing becomes an essential part of the decision-making process. Framing describes the process of sensemaking, where the decision maker interprets the decision in view of the context in which they must make it (Beach, Puto, Heckler, Naylor, & Marble, 1996). Through framing, individuals can reduce the cognitive demands associated with decision making by focusing on relevant image components. Framing determines the salient aspects of the value image that drive the decision-making process (De Martino, Kumaran, Seymour, & Dolan, 2006). For example, directors at HealthSouth were thinking about the ethics component of the value image after the CEO, Richard Scrushy, had engaged in a multibillion-dollar accounting scandal from 1996 to 2002. Directors at Qwest Diagnostics likely had a similar reaction when they learned that their CEO, Joseph Nacchio, engaged in insider trading, illegally selling more than $50 million in stock in 2001.

As directors reassess the firm’s images in the wake of misconduct, we suggest that the moral principles under which the firm operates become especially salient. Moral principles refer to conduct associated with perceptions of right and wrong (Ambrose, Arnaud, & Schminke, 2008). Following organizational wrongdoing, the firm’s moral principles rise to the fore as a key element of their value image. With a focus on ethics, directors are likely to adopt a new trajectory image that includes conducting future operations with high moral standards.

One way for directors to focus on the ethical component of their value image and realize their new trajectory image of avoiding future misconduct is to appoint a new CEO with high moral standards. This, however, presents a problem: How can directors ascertain the morals of candidate CEO successors? This is difficult because candidates’ moral principles are not readily measured or outwardly visible. Directors and candidate CEOs operate in many of the same social circles, so directors will have extensive information about candidates, but reliably assessing their ethics is extremely challenging. Some have advocated for the use of integrity testing during selection, but the validity of such techniques is questionable at best (Morgeson et al., 2007). In the absence of reliable information about a candidate’s moral standards, directors may search for cues that reveal something about a candidate’s ethics (Gomulya et al., 2017).

There are many motivations for moral behavior. One means by which individuals make assumptions or draw inferences about someone’s ethical standards is by evaluating their personal religiousness (Giacalone & Jurkiewicz, 2003). An indicator of personal religiousness is whether the candidate holds a degree from a religiously affiliated university. Information about where they attended university is a central feature of all CEO candidates. Schools such as Brigham Young University and Baylor have decidedly religious objectives, and many students self-select into such institutions, at least in part, as a reflection of their religiousness. Students can enhance their experience at these schools if they are willing to comply voluntarily with the norms of behavior of the denomination, and they are less likely to make it through to graduation if they outwardly oppose those standards (Scott, Bailey, & Kienzl, 2006).

This is important because directors do not have wide variance in their pool of candidates with respect to ethical violations (i.e., they do not have candidates with good and bad reputations). Rather, they face a candidate pool where, in all likelihood, all the individuals have no obvious record of organizational wrongdoing. If candidates have a history of prior ethical violations, or if reference checks reveal questions about moral standards, those individuals would not even pass the initial screen. Acquiring information related to the moral standards of those surviving the initial screening is likely difficult because there are few external indicators of integrity (Gomulya et al., 2017). For this reason, they must look deep to discern the candidates’ enduring ethical principles during the profitability stage of decision making, and there are few mechanisms for doing so.

These arguments suggest that directors choosing a new CEO after the firm has engaged in misconduct may consider whether candidates have a degree from a religious university. HealthSouth is a good example, as it brought in Jay Grinney, a graduate of Saint Olaf College (Lutheran) following its aforementioned accounting scandal. Such candidates align well with the ethics component of directors’ value image and their revised trajectory image in view of the recent misconduct (Donnelly & Quirin, 2006). We are not suggesting that a degree from a religiously affiliated university is necessarily the most important characteristic used by boards in making a succession decision. Rather, we argue that it becomes increasingly important in the wake of misconduct as opposed to under normal conditions. Therefore, we hypothesize the following:

Hypothesis 1: When choosing a CEO successor, directors are more likely to select a candidate with a degree from a religiously affiliated university if the firm had previously engaged in misconduct than they are if the firm had not engaged in misconduct.

There may be scenarios where misconduct is more, or less, common than other scenarios. Directors operate in a wide variety of industry environments, and ethical norms of behavior vary by industry (Greve, Palmer, & Pozner, 2010). For example, in industries such as financial services, health care, and construction, managerial misbehavior is far more common than the average for all industries. In fact, some have found that firms in financial services account for as much as 17% of all cases of fraud (Association of Certified Fraud Examiners, 2017), perhaps because it is easier to move money around on balance sheets than it is to engage in fraud when specific assets are at stake. Other industries, such as education, insurance, and wholesale trade, rarely see instances of fraudulent behavior.

In industries where misconduct is comparatively common, the gap between managerial misbehavior and the behavior that directors expect is not as great as in industries where misconduct is rare (Gomulya & Mishina, 2017). When misconduct is common in the industry, expectancy violation is not high, so directors are not likely to reevaluate the principles associated with their value image as a result of the misconduct (Beach & Mitchell, 1990). Instead, other aspects of the value image (e.g., those associated with performance or relationship building) could play a more prominent role. In these circumstances, the CEO succession decision is not as likely to be framed around misconduct as it is around other organizational objectives.

We predict that directors are less likely to be attuned to cues about candidates’ moral standards when they are choosing a new CEO in an industry where misconduct is relatively common compared to industries where misconduct is rare. The legitimacy of firms that engage in misconduct in high-misconduct industries is not in as much jeopardy as those who do so in low-misconduct industries, because legitimacy is defined by adherence to industry norms of behavior (Zimmerman & Zeitz, 2002). Therefore, the need for preventing future acts of misconduct may be less problematic in industries where misconduct is relatively common, as opposed to those where misconduct is rare. In high-misconduct industries, a degree from a religious university is not likely to make a strong impact on succession decisions. This leads us to hypothesize the following:

Hypothesis 2: The positive relationship between corporate misconduct and choosing a CEO successor with a degree from a religiously affiliated university is weaker in industries where misconduct is common than it is in industries where misconduct is rare.

Religiosity and Misconduct

One common denominator of studies on CEO successor selection following misconduct is that they do not investigate the supposed benefits of the firm’s successor choice. Most studies on this topic examine investor reactions to the board’s choice of successor (Gangloff et al., 2016; Gomulya et al., 2017), but few consider the consequences of making a particular choice.

There is some evidence to support the notion that religiousness is actually associated with high morals and ethical behavior (Kolodinsky, Giacalone, & Jurkiewicz, 2008; Neubert, Bradley, Ardianti, & Simiyu, 2017), in addition to perceptions of ethicality as we argued in our first hypothesis. For example, McCullough and Willoughby (2009) proposed that religiousness promotes self-control, influences self-regulation, and enhances self-monitoring. Subsequent empirical research has, in part, confirmed these propositions (Rounding, Lee, Jacobsen, & Ji, 2012), but the body of empirical research on this issue reveals mixed findings (Chan-Serafin, Brief, & George, 2013; Longenecker, McKinney, & Moore, 2004; Rounding et al., 2012). Thus, it is unclear whether and when the association of perceived religiosity and ethical behavior holds.

Weaver and Agle (2002) add a measure of clarity by introducing a symbolic interactionist perspective. These authors describe how the empirical inconsistencies scholars observe may arise because religion influences peoples’ self-identity in different ways, depending on how people define themselves in terms of the roles they serve (e.g., spouse, parent, employee). Individuals arrange each identity in a hierarchy so that the highest identities are the most salient and most influence one’s behavior (Stryker & Serpe, 1982). Religious affiliation may not necessarily affect behavior if the religious level of identity is not at or near the top of an individual’s self-identity hierarchy.

These authors go on to suggest that a key factor that can influence where individuals might situate religious identity in the self-identity hierarchy is their religious motivational orientation. Those who are intrinsically motivated are likely to live according to the prescribed morals of their religion (King & Crowther, 2004). Those who are extrinsically motivated view religion as a means for achieving social or economic goals. Recent studies support this distinction, as scholars have shown that individuals with intrinsically motivated religiousness exhibit positive characteristics typically associated with religiousness, more so than those who are extrinsically motivated (Stavrova & Siegers, 2014; Walker, Smither, & DeBode, 2012).

We argue that the decision to attend a religiously affiliated university could be an indicator of an individual’s intrinsic motivation for religiosity (Weaver & Agle, 2002). Religious universities impose a wide range of formal restrictions on student behavior, and there are even more restrictions that arise owing to students monitoring one another (Burdette, Ellison, Hill, & Glenn, 2009). This is not to say that wrongdoing does not occur at religious universities, but there are stringent rules about student behavior, and the most zealous students police others so that a culture of moral behavior is often evident (Regnerus, 2003). A culture that prioritizes moral principles can become a hallmark of these schools, so much so that students self-selecting into them are unlikely to do so unless they are intrinsically motivated to comply with established norms.

In addition to reflecting an individual’s moral principles, attendance at one of these schools may shape moral principles. Attending university, for either graduate or undergraduate education, constitutes a vulnerable time in a person’s life where they assimilate a tremendous amount of knowledge and learn principles about what is right and wrong (Kracher, Chatterjee, & Lundquist, 2002). Research shows that universities where college students choose to study powerfully affect those students’ espoused values (Finlay & Walther, 2003; Lyon et al., 2002). Consistent with this idea, Martin et al. (2016) recently showed that key aspects of managers’ upbringing influence their behavior and effectiveness as leaders. Thus, CEO candidates who studied at religious universities could have had their ethical principles shaped, in part, by their student experience.

The moral character of CEOs with degrees from religious universities could positively affect the organization’s culture so that others would be less likely to engage in fraud. Given that CEOs are at the helm of the firm and have ultimate decision-making responsibility, they have the power to reduce the likelihood of misconduct at their organization. CEOs are in the unique position of being able to implement policies and procedures that prevent fraud, and CEOs with a degree from a religious institution could avail themselves of this opportunity (Pfarrer, Smith, Bartol, Khanin, & Zhang, 2008). Consistent with this rationale, we suggest the following:

Hypothesis 3: The likelihood of misconduct will be lower when firms appoint a CEO successor with a degree from a religiously affiliated university than when they appoint a CEO successor without such a degree.

The extent to which misconduct occurs in an industry is likely to change the nature of the influence of CEOs with a degree from a religious institution. In industries where misconduct is rare, we argue there will be little difference between CEOs with degrees from religious universities and other CEOs. These industries already have strong norms behavior, and CEOs that operate in them will be well attuned to those expectations (Zahra, Priem, & Rasheed, 2005). The firm can ill afford to violate those norms of operation. Maintaining legitimacy will be of paramount concern for firms in these industries (Bundy, Pfarrer, Short, & Coombs, 2017), so ethical behavior will necessarily be the priority for any CEO that directors bring in as a successor. If the firm is going to continue to do business in these industries, there is no room for misbehavior. Therefore, we expect that in industries where misconduct is rare, CEOs with degrees from religious universities will behave ethically, but so will other CEOs because it is imperative that they do so.

In industries where misconduct is comparatively common, the differences between CEOs with degrees from religious schools and other CEOs are more profound. In this case, establishing the firm’s ethical principles is only one component of the successor CEO’s charter and not necessarily among the highest priorities. Establishing the firm’s legitimacy may not be overly problematic given that the firm has not strayed far from industry norms even if they engaged in misconduct (Zahra et al., 2005). CEOs in these industries could have pressures on them for other outcomes, such as profitability, innovation, and growth, that outweigh pressures for ethical behavior. These industries highlight the differences between CEOs with degrees from religious universities, who are likely to maintain ethical behavior regardless of external demands, and other CEOs, who might succumb to such pressures.

Thus, although directors of firms in high-misconduct industries are the ones least likely to turn to CEOs with a degree from a religious university (i.e., Hypothesis 2), firms in industries where misconduct is more common could actually benefit the most from the heightened moral standards of these individuals (i.e., Hypothesis 4). Stated formally, the hypothesis is as follows:

Hypothesis 4: The negative relationship between choosing a CEO successor with a degree from a religiously affiliated university and the likelihood of misconduct is stronger in industries where misconduct is common than it is in industries where misconduct is rare.

Study 1: S&P 1500 Firms

Sample and Measures

The sample for our study starts with the S&P 1500 firms covered by ExecuComp over the years 2000 to 2013. We identified a total number of 2,709 CEO succession events for these firms during this sample frame. We dropped 388 CEO succession events of firms in the financial service industries because these firms follow different accounting reporting rules and face stringent regulation. We used BoardEx to identify CEOs and board members’ alma maters. Management Diagnostic Limited, which specializes in collecting and disseminating social network data, maintains the BoardEx database. We used data from the Integrated Postsecondary Education Data System (IPEDS) to identify religious affiliation (Hill, 2011; Saunders, 2008). We were unable to clearly identify and classify the educational background for 966 CEOs, leaving us with 1,355 CEO succession events. In addition, we removed 266 succession events from our sample due to unavailable control variables, leaving us with a final sample of 1,089 succession events.

First dependent variable: Religious-university CEO

The dependent variable for Hypotheses 1 and 2 is religious-university CEO, which is whether a CEO successor holds a degree from a religiously affiliated university (Hill, 2011). This variable receives a value of 1 if a CEO has a bachelor’s or master’s degree from a religiously affiliated university and 0 otherwise.

We use this measure as an observable indicator of personal religiousness, which reflect ethicality. The rationale is that there is a well-documented tendency for individuals to associate personal religiousness with high moral standards (Vitell, 2009). For instance, researchers have shown that individuals rate people described as religious as being more moral, ethical, and trustworthy than those who are not religious (Bailey & Young, 1986; Gervais, Shariff, & Norenzayan, 2011). Importantly, scholars have observed these effects both when one’s religiosity is explicitly stated and when it is implied via an external indicator (Galen, Smith, Knapp, & Wyngarden, 2011). Evidence suggests that individuals make inferences about religiosity subconsciously (Pichon, Boccato, & Saroglou, 2007). As a result, we suggest that religious school affiliation is a useful proxy for adherence to an ethical code of conduct.

To capture these data, we turn to the National Center for Education Statistics, which collects IPEDS data annually (Saunders, 2008). This covers every college, university, and vocational institution that participates in federal student financial aid programs. In addition to academic and admissions data, they also collect data on institutional characteristics, including the school’s mission and religious affiliation. The database shows universities with historical religious affiliations as not having active religious affiliations. Among 1,089 newly hired CEOs in our final sample, 178 of them received a degree from a religiously affiliated university. We checked which of these universities have obvious religious names (e.g., “Christian” or “Baptist” in the school name), because this could have signaling implications. However, only 1.5% of CEOs in our sample had degrees from universities that stated their religious affiliation in their school name.

Second dependent variable: Financial misconduct

The dependent variable for Hypotheses 3 and 4 is financial misconduct, which occurs when managers take actions that deceive investors or stakeholders. Financial fraud often involves corruption, lying about facts, failure to disclose material information, falsifying information about the firm’s performance, or covering up systematic problems. This is an apropos operationalization for our study because it reflects a breach of stakeholder trust, so scholars commonly use financial fraud as a measure of corporate misconduct (Arthaud-Day et al., 2006; Connelly, Shi, & Zyung, 2017; Shi, Connelly, & Sanders, 2016).

Despite the ubiquity of research examining financial fraud, there are multiple approaches to measuring when it has occurred. We, therefore, develop a comprehensive operationalization of financial misconduct by combining three well-established sources (including only one instance for events that occur in more than one source). The first is the Securities and Exchange Commission (SEC) Accounting and Auditing Enforcement Releases (AAERs). The SEC acts against firms that have violated required financial reporting requirements (Shi, Connelly, & Hoskisson, 2017). This component of our measure, therefore, mainly captures firms that have admitted restating earnings or have unusually large write-offs. The second is securities class action lawsuits, which captures instances where shareholders have been defrauded (Shi et al., 2016). We require lawsuits to have been settled for at least $2 million, which separates frivolous from meritorious lawsuits (Choi, 2007). This component of our measure represents another way of viewing financial misconduct because, rather than “cooking the books,” it uncovers other means by which executives may have cheated their shareholders. The third is instances of accounting malpractice, as found in the Audit Analytics database on Legal Case and Legal Parties. This is important because there are cases of accounting malpractice that do not result in an AAER, and there are AAERs that Audit Analytics does not list as malpractice. With this approach, there are 526 firm-year observations associated with commission of misconduct.

Independent variables

We have two independent variables in this study. The first, for Hypotheses 1 and 2, is financial misconduct. We use the same sources to identify misconduct. Here we are concerned with detection of misconduct because directors must know that the misconduct occurred (they might not know about situations where the CEO is cheating and getting away with it). For example, the SEC could announce in 2008 that misconduct occurred during the years 2005 to 2008. In this case, we would code misconduct as 1 for the years 2005 to 2008, but detection of misconduct is 1 only for 2008. Among 1,089 firm-year observations where CEO turnover occurred, 80 of them had misconduct detected in the prior year. The second independent variable, for Hypotheses 3 and 4, is religious-university CEO, as previously described.

Moderating variable

To measure the prevalence of financial misconduct in an industry, we counted the number of instances of misconduct (excluding the focal firm) in each industry for each year, based on the Fama-French 48-industry classification. We divided by the number of firms in the industry to determine average industry misconduct, labeled as industry misconduct intensity.

Control variables (Hypotheses 1 and 2)

When modeling whether a newly appointed CEO has a degree from a religiously affiliated university, we included a number of key firm-level variables that capture potential matching between firms and religious university CEOs. We first control for firm misconduct intensity. Firms that have frequently engaged in misconduct in the past may not find misconduct an issue. This control variable is measured as the running average of misconduct committed by firms during our sample period. We controlled for firm size using the natural logarithm of market value and firm performance using return on equity (ROE), which is the ratio of operating income after depreciation to total shareholders’ equity. In addition, we controlled for debt ratio (the ratio of the sum of long-term debt and debt in current liabilities to total assets) and cash-holding ratio (the ratio of cash and short-term investments to total assets). We also controlled for firm visibility (the ratio of advertising expenditure to total revenues) as more visible firms will find it more urgent to signal their commitment to misconduct prevention through hiring religious university CEOs.

We also included a number of CEO-level control variables. We controlled for MBA degree because an MBA degree may offset the potential positive effect on the directors’ image about CEO candidate’s image (Mintzberg, 1973). This control variable receives a value of 1 if a CEO holds an MBA degree and 0 otherwise. We controlled for CEO age and CEO gender, the latter of which receives a value of 1 for females and 0 for males. Last, we included CEO origin as a control variable (outsider vs. insider) because this can be an important consideration in the wake of misconduct. Consistent with prior research on CEO origin (Zhang & Rajagopalan, 2010), a CEO was considered as an outside CEO if he or she had firm tenure of less than 2 years when he or she assumed the CEO position. We also controlled for whether a predecessor CEO holds a degree from a religious university (religious-university predecessor) because predecessor characteristics can also affect CEO selection decisions (Kunisch et al., 2019).

At the board level, we controlled for the ratio of outside directors who hold a degree from a religiously affiliated university (religious-university outside director ratio) because boards with a large number of outside directors with degrees from religiously universities may be more likely to hire a CEO with a similar degree. For the same reason, we controlled for the ratio of non-CEO top managers who hold a degree from a religiously affiliated university (religious-university TMT ratio). Last, we controlled for industry, using the Fama-French 48-industry classifications, and year fixed effects.

Control variables (Hypotheses 3 and 4)

When modeling the likelihood of financial misconduct as our dependent variable, we used a slightly different set of control variables. At the firm level, we controlled for firm size using the natural logarithm of total market value and firm performance using ROE. Higher debt ratio may increase the probability of financial misconduct by providing incentives for firms to inflate reported earnings and other accounting measures to avoid violating debt covenants (Khanna, Kim, & Lu, 2015). Higher cash-holding ratio may weaken firms’ incentives to inflate their earnings because such firms are less financially constrained. Highly visible firms may face strong scrutiny from external stakeholders, which may prevent firms from engaging in misconduct, so we also controlled for firm visibility.

At the CEO level, we controlled for CEO ownership and CEO optional-pay ratio because a battery of studies show that equity incentives can affect financial misconduct (Efendi, Srivastava, & Swanson, 2007; Harris & Bromiley, 2007). CEO ownership is the percentage of ownership by the CEO to total shares outstanding, and CEO option-pay ratio is the ratio of total CEO option compensation value to total CEO compensation. We controlled for CEO duality (1 if the CEO is board chair) because CEOs who are board chair are less concerned about board monitoring, which could influence the likelihood of financial misconduct.

In addition, when misconduct is our dependent variable, we controlled for a number of factors that can influence the firm’s governance quality. The first is institutional ownership concentration because monitoring by institutional investors may reduce the likelihood of financial misconduct (Hadani, 2012). Institutional ownership concentration is a Herfindahl index of ownership percentages of institutional investors. As important information intermediaries, financial analysts play a significant role in monitoring top executives (Chen, Harford, & Lin, 2015), which could also reduce the likelihood of financial misconduct. We, therefore, controlled for the number of financial analysts covering a firm (analyst coverage). We included board independence as a predictor of financial misconduct because it is related to monitoring by board members, which is measured as the ratio of outside directors to board size. We controlled for religious-university outside director ratio and religious-university TMT ratio because having outsiders and top managers with degrees from religious universities could confound the influence of having a CEO from a religiously affiliated university. Last, we controlled for year fixed effects.

Estimation

To test our first two hypotheses, we used a cross-sectional data set that includes only observations associated with CEO successions. Given that the dependent variable is binary, we used probit regressions to test these two hypotheses, controlling for industry fixed effects. We did not control for firm fixed effects given the cross-sectional nature of the data set for these hypotheses.

Given that we use a sample of CEO succession firm years to test Hypotheses 1 and 2, this could lead to potential sample selection bias. Specifically, there can be unobservable firm characteristics that drive whether a firm experiences a succession event and the type of CEOs hired. To alleviate this concern, we conduct Heckman selection models. In the first-stage probit regression, we estimate the likelihood of a firm having a succession event. The predictors in the first-stage regression include firm size, firm performance, debt ratio, cash-holding ratio, firm visibility, year fixed effects, and industry fixed effects. In addition, we include a potentially exogenous variable that can predict whether a firm has a CEO succession event but may not predict what types of CEOs will be hired. Specifically, we calculate an industry CEO succession ratio, measured as the ratio of the number of CEO succession events in an industry year to the total number of firms in an industry. When CEO succession is frequent in an industry, this can increase the demand for CEO candidates and reduce the likelihood of a focal firm having a CEO succession event. However, the industry CEO succession ratio should not have a direct influence on the type of CEOs being hired. Consistent with our argument, we find that the coefficient estimate of industry CEO succession ratio is negative (b = −0.81, p = .024) in the first-stage regression. From the first-stage regression, we then calculate an inverse Mills ratio and control for it in the second stage.

To test Hypotheses 3 and 4, we do not constrain our sample to firm years associated with CEO successions. Given that the data set used to test Hypotheses 3 and 4 is structured as a panel, we conducted firm fixed-effects ordinary least squares (OLS) regressions to test these hypotheses. Firm fixed effects are also well suited to testing our hypotheses because they control for unobservable time-invariant firm heterogeneity that could shape firm financial misconduct. Firm fixed-effects regressions allow us to examine within-firm change, or the extent to which change in our independent variable relates to our dependent variable, which is consistent with our theory. More important, we can observe only misconduct that is detected, and the probability of detection should be relatively stable for any given firm that engages in misconduct. In this sense, within-firm estimation can help alleviate concern that heterogeneity in misconduct detection across firms biases our results. We measure financial misconduct at time t + 1 and the independent and control variables at time t.

Results

In Table 1, we present descriptive statistics and pairwise correlations for all variables. In Table 2, we present the probit regressions used to test our first two hypotheses. In Model 1, we include all the control variables. We find that several controls are significant, including religious-university predecessor, which is positive (β = 0.86, p < .01). In addition, the coefficient estimate of the inverse Mills ratio is positive (β = 5.06, p = .004). In Model 2, the coefficient estimate of financial misconduct is 0.54 (p = .005), consistent with Hypothesis 1. The marginal effect of financial misconduct on our dependent variable is 0.11 (p = .005), supporting Hypothesis 1. At firms that are choosing a new CEO, the likelihood of choosing a successor with a degree from a religious university is 13 percentage points higher for those that announced financial misconduct than for those that did not announce financial misconduct.

Descriptive Statistics and Correlations

Note: N = 10,207. TMT = top management team.

Probit Regression of New CEO Selection

Note: Coefficients shown with p values reported in brackets (two-tailed tests). TMT = top management team; FE = fixed effects.

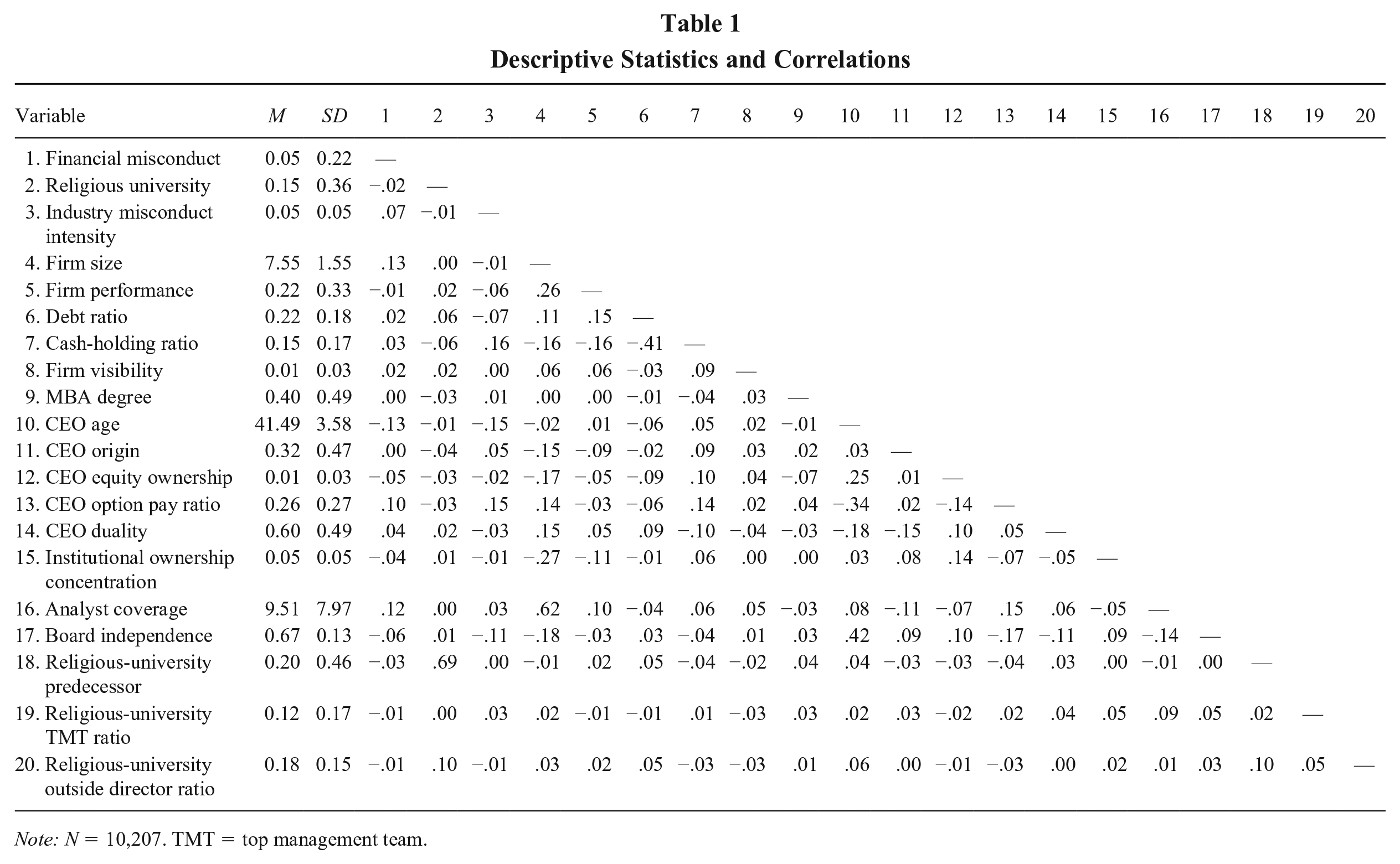

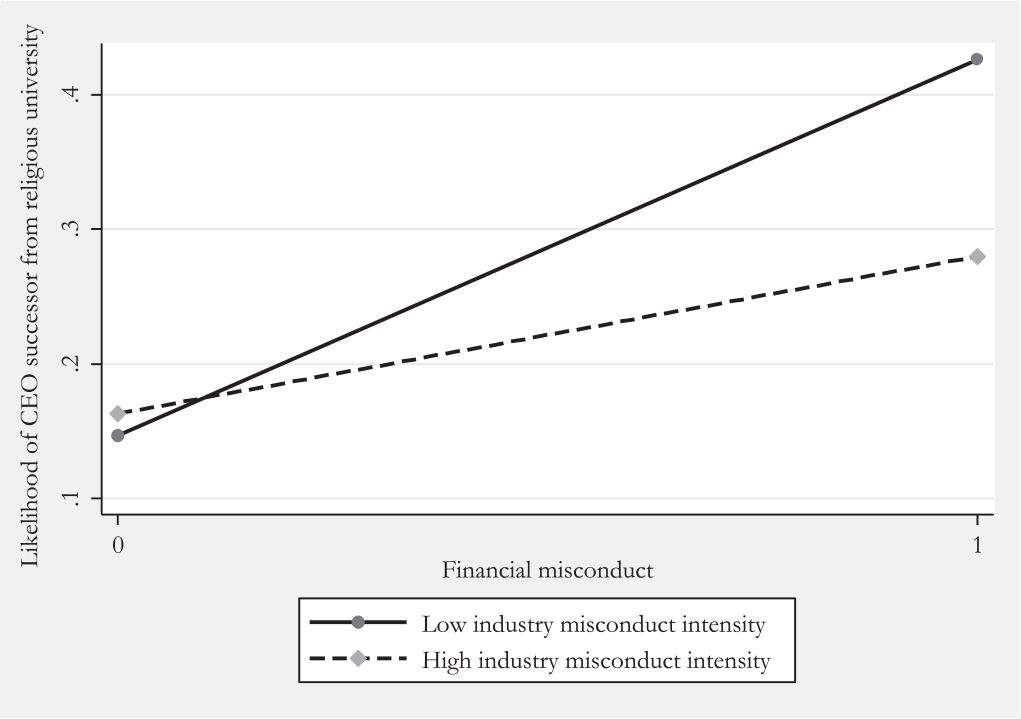

In Model 3, we test the direct effect of our moderator, which is not significant (β = −0.47, p = .668). In Model 4, we examine its moderating effect and find that the coefficient estimate of Financial Misconduct × Industry Misconduct Intensity is negative (β = −5.15, p = .042). The coefficients of interaction terms in nonlinear models do not always represent the true interactions (Hoetker, 2007; Wiersema & Bowen, 2009). Thus, we follow Wiersema and Bowen (2009) to consider the moderating influence by examining the marginal effect of the interacted variables. The marginal effect of financial misconduct on the likelihood of appointing a CEO successor with a degree from a religious university is stronger when industry misconduct intensity takes its mean minus one standard deviation (b = 0.18, p = .001) than when industry misconduct intensity takes its mean plus one standard deviation (b = 0.08, p = .050), supporting Hypothesis 2.

We also calculate and graph the magnitude of the moderating effect. When industry misconduct is rare (mean minus one standard deviation), the likelihood of choosing a successor with a degree from a religious university is 24 percentage points higher for observations with financial misconduct than those without financial misconduct. However, when industry misconduct is common (mean plus one standard deviation), the same likelihood is 9 percentage points higher for observations with financial misconduct than those without misconduct. We graph this interaction in Figure 1. The positive relationship between misconduct and the likelihood of appointing a CEO with a degree from a religious university is stronger for firms in industries with low incidences of misconduct (solid line). The relationship is less pronounced for firms in industries where misconduct is common (dotted line).

Moderating Effect of Industry Misconduct (Archival Study)

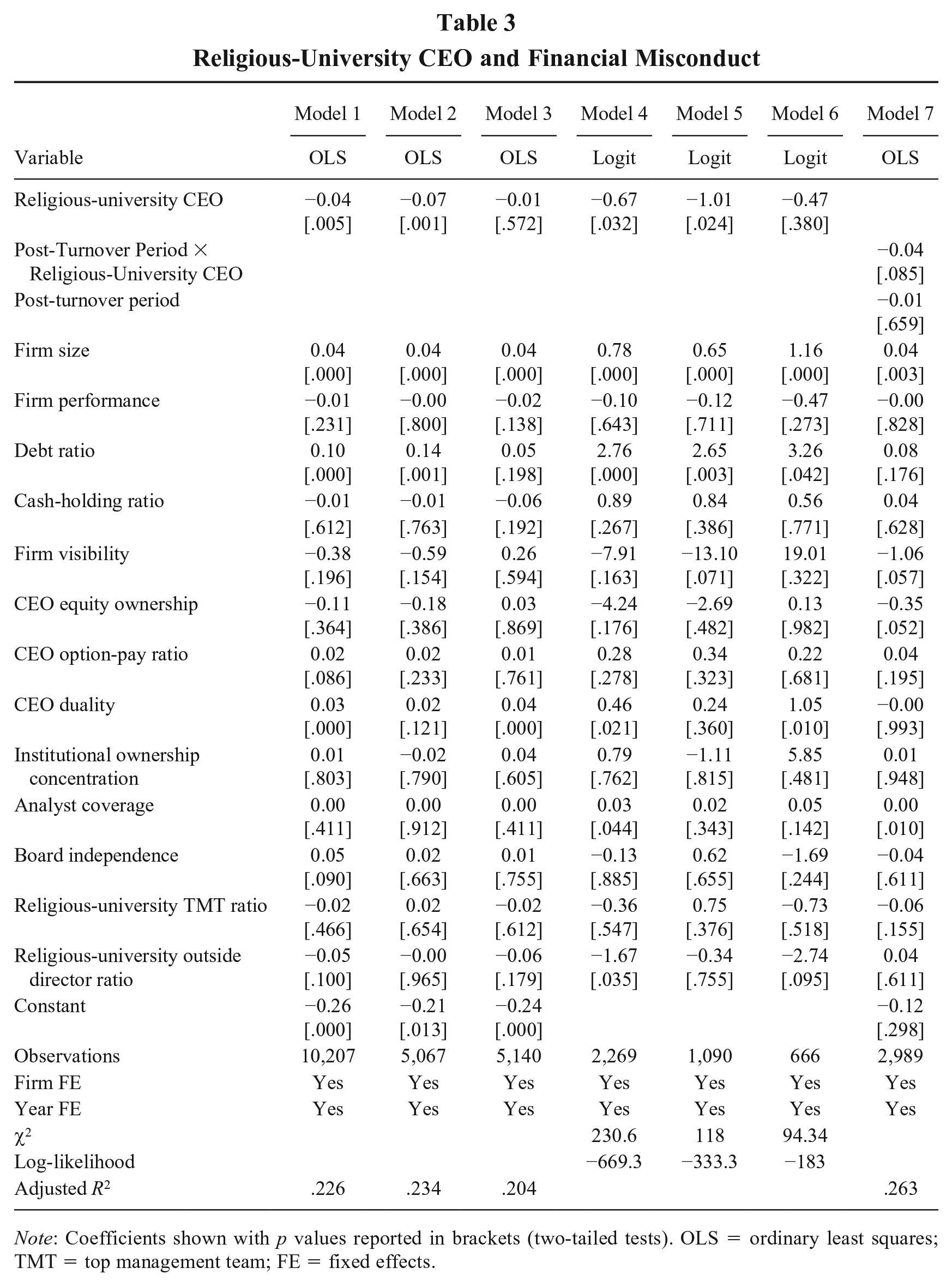

The models in Table 3 test Hypotheses 3 and 4. Models 1 through 3 present results from firm fixed-effects OLS regressions. In Model 1, the coefficient estimate of religious-university CEO is negative (β = −0.04, p = .005), consistent with Hypothesis 3. The likelihood of misconduct reduces by 4 percentage points after a religious university CEO succeeds a non-religious-university CEO.

Religious-University CEO and Financial Misconduct

Note: Coefficients shown with p values reported in brackets (two-tailed tests). OLS = ordinary least squares; TMT = top management team; FE = fixed effects.

We evaluate Hypothesis 4 by splitting the sample at the industry median and report the results in Table 3. The reason for conducting a split sample analyses is that industry misconduct intensity does not change much over time, so we cannot include it as a variable in our firm fixed-effects regression models (in unreported results, we find that the coefficient estimate of Religious-University CEO × Industry Misconduct Intensity is statistically not significant using the whole sample). In Model 2 of Table 3, we see that for firms operating in industries where misconduct is common, the relationship described by Hypothesis 3 holds. That is, choosing a CEO successor with a degree from a religious institution is a negative predictor of misconduct (β = −0.07, p = .001). Model 3 shows that for firms operating in industries where misconduct is rare, the relationship described by Hypothesis 3 no longer holds (β = −0.01, p = .572). These results lend support to Hypothesis 4. Models 4 through 6 present results from firm fixed-effects logistic regressions, which by nature of the analysis include only firms that have a time-variant dependent variable. With this analysis, we continue to find support for Hypotheses 3 and 4.

Supplementary Analyses

Endogeneity

To mitigate endogeneity concerns, we conduct a difference-in-differences analysis, comparing financial misconduct before and after transitions from having a CEO with a religiously affiliated degree to one without such a degree, using a control sample of firms that transition from a CEO without a religiously affiliated degree to another CEO without such a degree.

There are two advantages associated with difference-in-differences. First, it requires a CEO to be in power for a durable period, alleviating any unique effects of CEO turnover. We require that a CEO be in power for at least 3 years so that he or she can have sufficient time to influence firm decisions. Second, we use transitions from CEOs without a religiously affiliated degree to another CEO without a religiously affiliated degree as a control group, which conditions our test on the occurrence of CEO turnover of any kind. Specifically, we conduct the following regression:

where i indexes firm and t indexes time; Yi,t+1 is the dependent variable of interest (financial misconduct); α t and δ i are year and firm fixed effects, respectively; Xi, t is a vector of control variables to rule out potential confounding effects; ε it is an error term; Religious i is an indicator variable for whether firm i has a transition from a CEO without a religiously affiliated degree to one with a religiously affiliated degree; and Posti,t+1 is an indicator variable for whether year t + 1 is after the CEO transition. Because the specification includes firm fixed effects, it is not necessary to include a religious dummy variable (Huang & Kisgen, 2013). We conducted firm fixed-effects OLS regressions with financial misconduct as the dependent variable.

We present the results from these analyses in Model 4 of Table 3. The coefficient estimate of Post-Turnover Period × Religious-University CEO is negative (β = −0.04, p = .085), indicating that CEOs with a degree from a religiously affiliated university reduce the likelihood of financial misconduct more than other CEOs. We can interpret the coefficient estimate of the interaction term as an approximate indicator of the percentage decrease in the likelihood of misconduct. During the 3 years after transition to a CEO with a degree a religiously affiliated university, the likelihood a firm engages in misconduct is 4 percentage points lower than for a firm that transitions to having another CEO without a religious degree.

Bivariate probit regressions with partial observability

Studies that investigate fraudulent behavior of any kind have to deal with a common problem: One observes only misconduct that is actually detected. There is no expedient mechanism for observing misconduct that is committed but not detected. We account for this potential concern by reanalyzing our data using bivariate probit analysis with partial observability (Wang, 2013; Wang, Winton, & Yu, 2010). To do so, we model managerial misconduct as the combined result of two latent variables: misconduct commitment, P(M), and misconduct detection given commitment, P(D|M). These models are useful from a theoretical perspective (Wang, 2013), but they are empirically challenging because they suffer from a loss of efficiency and estimation failures are commonplace (Poirier, 1980). They can be useful as a supplementary analysis of the likelihood of misconduct because they attempt to parse out the likelihood of committing misconduct, as opposed to detecting. To be clear, though, these models are only predictive; we do not actually know which firms are committing misconduct without being detected. We use bivariate probit regressions with partial observability only as a robustness check.

There are two main requirements to achieve full identification for these models (Poirier, 1980). First, variables used to test detection of misconduct and commitment of misconduct must not include the same variables. Second, the predictors should have significant variation. Based on these requirements, the model is better identified if variables in commitment of misconduct and detection of misconduct use continuous, as opposed to binary or dummy, variables (Wang, 2013). Therefore, we leave out the firm fixed effects and year fixed effects for these models because including them leads to an inability to estimate parameters.

In Models 1 and 2 of Table 4, we use different control variables for P(M) and P(D|M). To model P(M), we control for firm size, firm performance (ROE), debt ratio, cash-holding ratio, CEO equity ownership, CEO option ratio, CEO duality, religious-university TMT ratio, and religious-university outside director ratio. To model P(D|M), we control for a subset of those variables that are most likely to predict detection. The first is stock returns, because underperforming firms would be one of the more obvious red flags for misconduct. We also control for stock return volatility, as it reflects a firm’s level of risks, which can motivate misconduct detection. In addition, we control for firm visibility, as more visible firms receive more attention from stakeholders. We control for industry misconduct intensity, because firms from industries with more intensive misconduct activities are more likely to become targets of misconduct detection. We also control for a number of governance variables (institutional ownership concentration, analyst coverage, board independence, and CEO duality) that may influence misconduct detection.

Bivariate Probit Regressions With Partial Observability

Note: Coefficients shown with p values reported in brackets (two-tailed tests). P(M) = misconduct commitment; P(D|M) = misconduct detection given commitment; TMT = top management team.

Model 1 shows the results from bivariate probit regressions of P(M), and Model 2 shows P(D|M). The coefficient for religious university CEO is positive (β = −0.13, p = .074) in Model 1, consistent with Hypothesis 3.

Prestigious universities

To gain a deeper insight into the role of religious-university degrees in CEO succession, we classify religious universities into two types based on their prestige. We use the school’s acceptance rate as a measure of university prestige (Wiersema & Bird, 1993). Using the median acceptance rate of all universities covered in our sample, we classify religious universities with an acceptance rate below the median as more prestigious and those with an acceptance rate above the median as less prestigious. In unreported (but available) results, we find support for Hypotheses 1 and 2 if we use religious universities with low prestige as the dependent variable but not if we use religious universities with high prestige as the dependent variable. One possibility for this finding could be that directors assume all candidates with a degree from a prestigious school have strong ethics, so religious affiliation does not add information about the candidate’s ethics. Alternatively, directors might ignore religious affiliation for candidates from prestigious institutions because they want their human capital, regardless of the candidate’s ethics.

Variation in religiousness

To consider potential differences in the degree of religiousness, we measure whether a religious group originally founded a university, finding that religious groups founded about 40% of the universities in our sample (e.g., Dartmouth, which was originally Puritan Congregationalist but is now nonsectarian). We conducted analyses by examining CEOs with a degree from a university that a religious group founded. In unreported results, we found only marginal support for Hypothesis 1 and no support for our other hypotheses. This illustrates that the current religious affiliation of a CEO’s degree-granting institution is a pertinent measure, as opposed to the affiliation of the degree-granting institution at founding, which is not pertinent.

Schools might signal religious affiliation in the title of their school. Some may not recognize that Santa Clara University is a Roman Catholic school (in the Jesuit tradition), but there is no mistaking the affiliation of Ouachita Baptist University. To address the influence of signaling via the school name, we coded our data for obvious indicators of religious affiliation, such as Christian, Baptist, Catholic, and a wide range of other obvious denominations and religions. What we found, though, was that only a very small percentage of CEOs in our sample had degrees from universities that stated their religious affiliation in their title. Relatedly, there could be a range of schools, such as Notre Dame and Brigham Young University, that do not explicitly state their religious affiliation in the school name, but many people know they are religious. The difficulty here is there is not agreement among who recognizes the religious affiliation of many schools, such as Santa Clara or the University of Dayton, both of which are Roman Catholic. Thus, there is an assumption in our work that for the schools within the subset of CEO candidates, directors will know at least for that limited number of schools whether they have a religious affiliation.

Alternative operationalization

We tested our results using Wiersema and Zhang’s (2011) classification of CEO dismissals, but there are much fewer of these (231 firm-year observations). The results did not hold, we expect owing to the considerably reduced sample size. Nonetheless, we contend that it is more appropriate to our analysis to include all instances of CEO turnover in the wake of misconduct because doing so is consistent with our image theory rationale.

Alternative explanation

An alternative reason the board of directors could hire a CEO with a degree from a religiously affiliated university could be to trigger positive shareholder reactions (Gomulya & Boeker, 2014). However, this alternative explanation assumes that stock markets would react positively to the announcement of a successor with a religiously affiliated degree (Bergh, Connelly, Ketchen, & Shannon, 2014). To consider this alternative explanation, we examine stock market reaction to CEO appointment announcements in the aftermath of misconduct.

To conduct such an analysis, we collected the specific dates of all CEO appointment announcements. We were able to identify exact dates for 234 of the CEO appointments in our sample. This allowed us to examine whether the interaction between discovery of financial misconduct and subsequent announcement of CEO turnover with a successor that has a degree from a religiously affiliated institution is positively associated with cumulative abnormal returns (using a window of 3 days [−1, +1]). In unreported results, the coefficient estimate of this interaction term is statistically not significant (β = −0.05, ns). Thus, the empirical evidence does not favor a market-signaling explanation for choosing a CEO successor with a degree from a religiously affiliated university because there is no positive feedback for the signal (Bergh et al., 2014).

Study 2: Corporate Directors

We conducted a second study as an experimental complement to consider our ideas in a different way. Our dependent variable for this second study is about not whom respondents would choose as a successor in a given scenario but rather how important is their image of the firm to their decision making about a successor. We used a policy-capturing approach for our second study because it has advantages and limitations that are essentially orthogonal to our prior analysis of archival data (Hitt, Ahlstrom, Dacin, Levitas, & Svobodina, 2004). For organizational misconduct, archival data cannot reveal the extent to which directors might be influenced, for example, by the media or people around them. Policy capturing helps obviate this problem by manipulating only the predictor variables and not providing respondents with cues about what others are saying or thinking. A limitation of policy capturing, though, is that it relies on a small sample and does not assess actual behavior in the marketplace.

Sample and Measures

The sample for our second study uses actual directors. We recruited former students from a highly ranked executive MBA program (EMBA). We sent invitations to EMBA recent alumni, requesting participation from those who have experience on a public or private (but not nonprofit) board of directors. Our sample included 32 respondents, seven of which are female and five of which are ethnic minorities. All respondents confirmed their board experience, and the average experience as a director was 8 years.

Dependent variable

We asked respondents to imagine they were on the board of directors of a publicly traded company and that it was time for them to select a new CEO. The dependent variable was the importance of future misconduct prevention as a criterion for CEO successor selection. We asked participants to rank in order of importance nine decision-making criteria as they pertained to the CEO successor selection decision for each scenario. We coded responses as an ordinal variable based on participants’ reported importance ranking of the “likelihood the new CEO might misstate earnings in the future,” with 1 being least important and 9 being most important.

We identified the nine decision-making criteria by performing a review of the succession literature. Our review uncovered seven main criteria for succession decisions under normal conditions (i.e., misconduct has not occurred) and two additional criteria that are especially pertinent following misconduct. During a normal succession, we found that potential stock market (Graffin, Boivie, & Carpenter, 2013; Zhang & Wiersema, 2009) and media/analyst (Gomulya & Boeker, 2014; Wiersema & Zhang, 2011) reactions to the announcement of a successor are important. There is also evidence that boards choose successors that can help the company grow and perform well (Georgakakis & Ruigrok, 2017; Shen & Cannella, 2002). We separated growth and performance because investing in growth can have different connotations than focusing on performance (Cowling, 2006; S. Lee, 2014). We also separated short-term from long-term firm performance, because some boards could be myopic about their selection whereas others are more strategic (Ballinger & Marcel, 2010). In addition, there is evidence that boards sometimes choose industry insiders to help maintain or develop supply chain and partnership relationships. Employee reactions may also be important because stakeholder primacy theory suggests that boards should be cognizant of employee needs (Ballinger, Lehman, & Schoorman, 2010). Two additional criteria address decision making in the wake of misconduct. One pertains to signaling to external stakeholders that future misconduct will not happen. The last one tests future misconduct prevention to assess the relevance of image theory.

Our resulting nine criteria are “likelihood the stock market might react positively/negatively to your selection”; “likelihood the media or financial analysts might react positively/negatively to your selection”; “likelihood the new CEO might produce/fail to produce the expected market growth”; “likelihood the new CEO might deliver/not deliver positive short-term financial performance”; “likelihood the new CEO might deliver/not deliver positive long-term financial performance”; “likelihood the new CEO might develop/fail to develop relationships with customers, suppliers, and other stakeholders”; “likelihood current employees might react positively/negatively to your selection”; “likelihood the new CEO might/might not signal to external stakeholders that future misconduct will not occur”; and “likelihood the new CEO might/might not misstate earnings in the future.”

Independent variable

The independent variable for our second study is financial misconduct. For scenarios in which the company had discovered financial misconduct, coded as 1, we included the following statement: “Your company was forced to issue an earnings restatement during the prior year.” We also provided a definition of “earnings restatement,” noting that it “occurs when a company has to reissue financial statements, such as their annual earnings report. This often occurs due to fraudulent misuse of accounting procedures, lack of oversight, or misinterpretation of accounting rules.” Other scenarios, coded as 0, did not include this statement.

Moderating variable

The moderating variable was industry misconduct intensity. For scenarios in which the company operated in an industry with high levels of misconduct, coded as 1, we included the following statement: “In this scenario, imagine that issuing an earnings restatement is something that is common in your industry. Companies in your industry have to do it all the time.” Other scenarios, coded as 0, did not include this statement.

Control variables

We also included a number of control variables that might influence respondents’ selection decisions in a succession context. Some studies show that female executives may be less likely to engage in misconduct (Cumming, Leung, & Rui, 2015), so we controlled for female respondent as a binary variable, with 1 being female. Directors with considerable experience may be cognizant of key factors in successor selection (Beasley, 1996), so we controlled for director experience using a continuous variable for the number of years. A respondent’s personal religiousness might also affect the extent to which they focus on choosing a CEO that will reduce the likelihood of misconduct (Neubert et al., 2017). We asked, “How important are your religious beliefs to you?” with responses on a 5-point Likert scale ranging from extremely important to not at all important. Education level may influence strategic decisions (Knippen, Shen, & Zhu, 2019), so we controlled for the level of director education, which was coded as 3 for doctorate degrees, 2 for master’s degrees, 1 for bachelor’s degrees, and 0 otherwise. Some directors may be more comfortable with risk than others, which could affect the importance of the likelihood a CEO would engage in financial misconduct. We therefore controlled for personal risk propensity using a composite measure of seven items developed by Lion and Meertens (2001). Following these authors, we combined these items into a single 7-point variable ranging from 7 for a risk seeker to 1 for a risk avoider. Last, we controlled for directors’ religious education background using a binary variable, which was coded as 1 if the director attended a religious college or university for any degree and 0 otherwise.

Estimation and Results

We analyzed the data using hierarchical linear modeling (HLM) to account for both within-person and between-person variance. We used the xtmixed command in Stata 15.0. This command fits linear mixed models and contains both fixed and random effects. Its model is

for i = 1, . . . , 4 scenarios and j = 1, . . . , 32 respondents. Y represents respondents’ ratings of the questions after each scenario (i.e., decision-making criteria). X represents treatment of the events and other control variables for each respondent. The fixed portion of the model, β0 + β1Xij, captures the population average. The random effect is captured by µ j according to each respondent, and random effects occur at the respondent level.

In Model 1 of Table 5, we show the direct effect of financial misconduct on the importance of misconduct prevention to directors’ decision making about a successor. Consistent with the arguments of Hypothesis 1, we see a significant positive relationship (β = 1.22, p < .001) for scenarios where the firm has engaged in prior misconduct.

Hierarchical Linear Modeling Regression of Prevention of Misconduct as Decision-Making Criterion

Note: Coefficients shown with p values reported in brackets (two-tailed tests).

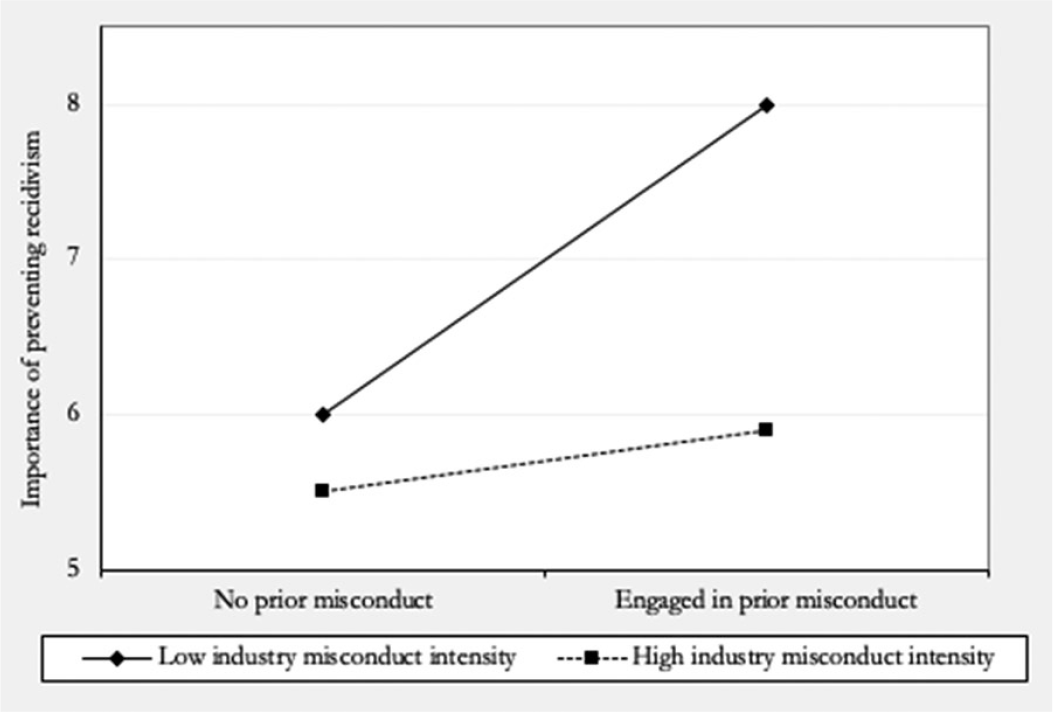

In Model 2, the direct effect of industry misconduct is negative and not significant (β = −0.53, p = .307). The interaction term is negative and significant (β = −1.62, p = .027), consistent with the arguments of Hypothesis 2. We graphed the interaction effect in Figure 2, which shows the positive relationship between prior financial misconduct and the importance of preventing misconduct is strong when a firm operates in an industry where misconduct is rare (solid line). The relationship is less strong in industries where misconduct is comparatively common (dotted line).

Moderating Effect of Industry Misconduct (Policy Capturing)

Supplementary Analyses

Ethicality of successors

It was not possible to test Hypotheses 3 and 4 using policy capturing because the dependent variable is misconduct. However, we included two additional scenarios at the end of our study where we presented participants with two CEO successor candidates, alike in all details except their university degree, and asked them to choose the one that they believed would be most ethical. We then conducted an additional HLM regression, this time using a degree from a religious university as the predictor and expected ethicality as the dependent variable. This is akin to testing Hypothesis 3, but we cannot measure whether the CEO candidates engage in misconduct, just whether participants think they might. The results (unreported) were marginally significant (β = 0.31, p < .10). Since there were only two scenarios for our 32 participants with this analysis, the sample size is only 64, so our marginally significant result shows some support for the influence of having a religious degree on perceived ethicality.

Signal to stakeholders

We also sought to consider the extent to which directors wanted to use the CEO successor choice to signal to external stakeholders that they are serious about preventing misconduct. To do so, we recoded the dependent variable to test for the ranked importance of signaling to external stakeholders (i.e., “likelihood the new CEO might/might not signal to external stakeholders that future misconduct will not occur”). We conducted the same analyses with the same control variables as our main analysis, finding substantively similar results. Our approach here is not a direct test of signaling theory, because we do not distinguish between high- and low-quality signalers (Connelly, Certo, Ireland, & Reutzel, 2011). However, these additional results may indicate that directors choose a new CEO not only with prevention of misconduct in mind but also with a view toward communicating their sincerity to outside entities.

Discussion

We develop theory explaining why directors choosing a CEO successor following firm misconduct consider the religious affiliation of the candidate’s university. Results confirm our theory: Directors of firms that recently announced misconduct are more likely to choose a CEO successor with a degree from a religiously affiliated institution than are directors of firms where there was no misconduct. This effect is especially strong for directors of firms operating in industries where misconduct is rare. A policy-capturing survey of actual directors reinforces our image theory logic. In addition, we tested the extent to which the strategy of hiring a CEO with a degree from a religious school actually works. That is, are CEOs with degrees from religiously affiliated institutions less likely to engage in misconduct than other CEOs? We found they are. Again here, the effect holds only for CEOs operating in industries where misconduct is common, because these industries allow CEOs with degrees from religious universities to stand out from their counterparts without such degrees.

Implications for Research and Practice

Our study adds to the literature on board decision making by incorporating an image theory perspective into a literature that has been historically dominated by normative decision theory and expected utility. Doing so shifts the emphasis of their decision from the reaction of external evaluators (Gangloff et al., 2016) to the mind of directors who have recently undergone a traumatic change in their perception of the firm and its outlook (Marcel & Cowen, 2014). Stated differently, we move the discussion of CEO successor selection from the information economics of the decision to the way directors view the firm and what they envision for it. Discovery of misconduct puts directors in a precarious situation that affects their decisions, and few have delved into trying to understand directors’ thought processes in this situation. This is important because directors lie at the heart of many important firm decisions, but extant studies focus more on what everybody else will think, as opposed to what the directors themselves are thinking, about their decisions.

We also complement existing research on executive succession (Berns & Klarner, 2017). It is natural to evaluate a CEO successor choice in terms of observable metrics, such as how capital markets react to the choice or how information intermediaries interpret the selection. These are, after all, important proxies of the quality of the choice that directors made and reliable indicators of the likelihood that the new CEO will be successful (Shen & Cannella, 2002). These metrics, though, do not take into account how directors feel after their firm has engaged in misconduct or how those feelings might affect their decision making when choosing a new CEO. Image theory helps capture director responses to the situation by explaining how their changing image of the firm’s value and trajectory images might shape their choice of who will be the next person to run the firm.

We build on recent studies that explore the extent to which a CEO’s early life experiences affect corporate outcomes (Bernile et al., 2017; Kish-Gephart & Campbell, 2015; Martin et al., 2016). Prior studies have focused on issues such as family income/social standing, military experience, and elite education (Benmelech & Frydman, 2015). We add to this body of work by incorporating exposure to a religious environment at a young and impressionable age. Like other studies in this area, our findings indicate that early life experiences may affect a leader’s ability to generate specific outcomes for their organization.

Our findings provide insights into the effect of CEO successor selection on the likelihood of misconduct, which may be important for at least two key reasons. The first pertains to protecting the firm from future misconduct. Following an instance of corporate misconduct, directors are responsible for identifying and correcting problems. Our findings show they can increase the effectiveness of executive succession as a corrective mechanism (Hersel, Helmuth, Zorn, Shropshire, & Ridge, 2019). The second pertains to protecting directors from the adverse consequences of choosing the wrong successor. Following misconduct, directors are motivated to choose a successor that will resolve systemic problems and steer the ship away from nefarious behavior. Their choice has consequences for their own careers because choosing a CEO that later engages in misconduct could spell an end to a director’s career (Marcel, Cowen, & Ballinger, 2017).

Limitations and Future Research

One limitation of our work pertains to our sample. The small sample size of Study 2 is not ideal. Future research might attempt to improve on this by incorporating a snowball sampling technique. It is also important to note that our Study 2 sample was more diverse in terms of gender and race than the composition of a typical board of directors. This might call into question the generalizability of our findings to boards that are more homogenous than the respondents in our sample. Study 1 also has a sampling limitation in that we were unable to obtain from archival sources the educational background of a fairly large number of CEOs. Future research could seek to extend our findings by carefully seeking historical information for each CEO not in our educational database (e.g., via individualized searches, phone calls, and alumni databases).

Another limitation is that we cannot measure the cognitive schema of directors. We develop arguments about aspects of the value image that will be salient (e.g., ethics, performance) to directors and the changing nature of their trajectory image, but we cannot assess the images directly. As a result, we are limited to (a) confirming that the predictions of image theory align with what is happening in the marketplace and (b) testing the thought process in our second study. Neither of these approaches incorporates direct measures of images directors form following organizational misconduct. We expect a qualitative study with in-depth interviews of directors and open-ended questions about the images they form would be a good approach to addressing this problem. A qualitative study would also help address the concern that our financial misconduct measure can capture only misconduct that is both committed and detected, not misconduct that goes undetected.

The nature of our data collection did not allow us to measure the personal religiousness of CEOs (we ask about the religiousness of the directors in our policy capturing as a control variable). Studies on religiosity show that when denominations maintain stringent requirements for members of their group (e.g., abstention from alcohol, mandatory attendance), individuals adhere to the denomination’s moral code of conduct (Sosis & Bressler, 2003). Future research might consider differences between types of affiliations. Relatedly, we rely on university affiliation as a measure of religiousness. We cannot be sure the extent to which this would correlate with direct measures if we surveyed CEOs. For example, the World Values Survey (www.worldvaluessurvey.org) uses a range of measures to capture religiosity on a national level, which could be a useful starting point for an individual-level survey. The spiritual well-being measure (Bormann, Liu, Thorp, & Lang, 2012) provides another possible avenue for surveying CEOs about religiousness. Future research might leverage these tools for direct measures of CEO religiosity.

Similarly, scholars might build on our ideas to incorporate other indicators of moral principles beyond religion, such as charitable work or care for the environment. For example, Payne Moore, Bell, and Zachary (2013) describe how CEOs use rhetoric to establish an organizational virtue orientation. This line of study could inform the successor selection literature because CEO candidates’ espoused ethics are likely to be important to directors. Researchers can use annual statements to shareholders or transcripts of earnings calls to qualitatively assess a CEO’s ethical tone (McKenny, Aguinis, Short, & Anglin, 2018). The virtue orientation CEOs adopt may not be an accurate predictor of their ethical principles (Bergh et al., 2014), but it could be something directors consider when choosing a CEO. Future studies could examine, for instance, data on corporate social responsibility either as an added control or as an alternative explanatory mechanism.

A final limitation of our work pertains to the potential for nonrandom assignment in our moderating hypothesis. If there is something fundamentally different about CEO selection in one industry as opposed to another, it could change our results. For instance, it could be that CEO selection is a more common decision that directors have to make in some industries because they are more likely to remove the CEO for misconduct. We partially address this with our difference-in-differences supplementary analysis, because we show that nonrandom assignment across industries is not biasing our results. However, to address this fully would require us to know more about whether the decision directors face about CEO selection in industries where misconduct is common is different, in some meaningful way, from the same decision in industries where misconduct is rare. It is difficult for us to do so with the data we have.

Conclusion

Directors have a dearth of reliable information about candidates’ moral principles. As a result, we find that in the aftermath of corporate misconduct, they attend to the religious affiliation of candidates’ alma maters, and that strategy is effective. Moreover, directors of firms that operate in industries where misconduct is a relatively common occurrence are the least likely to choose, but the most likely to benefit from, a CEO with a degree from a religious university.