Abstract

Although organizational slack is a prominent construct in strategic management, it is often treated as an antecedent or enabler of other organizational outcomes, and thus our understanding of where slack comes from is underdeveloped. We draw on the behavioral theory of the firm to develop a better understanding about the antecedents of organizational slack. In so doing, we address a gap in the literature on the antecedents of slack by developing base models showing how and why performance feedback influences the three most common types of slack studied in the literature. Moreover, we contend that ownership is an important contingency that influences these relationships because different types of owners are motivated by different norms. Within a “communitarian” culture such as Japan, domestic owners generally have a multifaceted relationship with the firm and hence are motivated by norms of reciprocity and embeddedness, thereby allowing managers to adopt a stakeholder perspective. In contrast, foreign investors typically have only an arm’s-length relationship with the firm and are thus motivated by stock price, thereby putting “contractarian” pressures on managers to adopt a shareholder perspective. This domestic/foreign ownership distinction influences how resources are allocated and therefore the relationship between performance feedback and different types of slack in the firm. We further emphasize that these relationships will vary in accordance to where the slack resides: internal or external to the firm. We find general support for our hypotheses.

Keywords

Organizational slack is a crucial construct in the strategic management literature. Slack helps firms adapt to unfolding contingencies during periods of both strong and weak performance (Sharfman, Wolf, Chase, & Tansik, 1988), it influences experimentation and innovation (Nohria & Gulati, 1996), and ultimately it affects firm performance (Carnes, Xu, Sirmon, & Karadag, 2019). Despite slack’s prominence in the literature, it is generally relegated to the role of an enabler of certain behaviors (Shinkle, 2012), and research rarely considers the factors that influence a firm’s level of slack. Because slack influences firm performance, understanding why slack varies across firms helps address a canonical issue in strategic management: variability in firm performance. Enhancing our understanding of where slack comes from (i.e., its antecedents) is therefore an important goal for management research.

Developing such an understanding, however, poses two distinct challenges. First, although the construct of slack is employed in many empirical studies, slack is typically treated as an enabler of some other focal construct or action (Shinkle, 2012). Hence, we know little about the theoretical mechanisms that influence slack, since it is often treated as the mechanism itself. Second, there is a presumed (i.e., untested) relationship between performance and slack (e.g., Sharfman et al., 1988), but this presumption overlooks complexities inherent in decision-making processes. Specifically, decision-makers in different contexts abide by different decision-making norms, rules, and logics; as such, developing an understanding of the antecedents of slack necessitates consideration of the decision-making context.

We address this knowledge gap by developing a model rooted in Cyert and March’s (1963) behavioral theory of the firm (BTF) and its prescriptions regarding the antecedents of slack resources. A foundational premise of the BTF is that managers develop performance goals, or aspirations, that influence decision-making. When a firm exceeds its aspirations, management is motivated to stay the course, and as a result, excess resources tend to build up. As Cyert and March (1963: 189) put it, “in general, success tends to breed slack.” In contrast, when a firm falls short of its aspirations, managers are motivated to invest in risky activities to improve performance, which should typically result in a reduction of slack resources.

The seemingly simple relationship between performance relative to aspirations and slack belies the complexities inherent in the decision-making process, because as noted by Cyert and March (1963), decision-makers in different contexts have different rules or norms guiding their decision-making. For example, decision-making norms in contexts that emphasize contracts (i.e., “contractarian” systems, such as the United States) differ from those in contexts that emphasize the well-being of the overall community (i.e., “communitarian” systems, such as Japan) (David, O’Brien, Yoshikawa, & Delios, 2010). Societal norms in Japan traditionally place greater emphasis on taking care of a broader array of stakeholders relative to norms in most Western cultures (Ahmadjian & Robbins, 2005; Yoshikawa, Phan, & David, 2005). One manifestation of these norms is that many firms are deeply embedded in a network of linked firms that own significant percentages of each other (O’Brien & David, 2014).

Japan offers unique insights regarding how different norms can influence the relationship between performance relative to aspirations and slack because different kinds of ownership can reflect distinct norms that guide decision-making. In recent decades, Japanese managers have felt pressure to conform to contractarian norms in order to attract and retain foreign institutional investors. Hence, traditional communitarian norms compete with the more recently introduced contractarian norms. Research indicates that ownership by Japanese banks and trading partners (which, for brevity, we henceforth refer to as “domestic firms”) helps insulate the focal firm from these pressures and therefore makes them more likely to follow traditional communitarian norms (David et al., 2010). In this paper, we argue that the presence of domestic owners—that is, owners embedded in social and cultural ties and adhere to communitarian norms—influences the relationship between performance relative to aspirations and different types of slack.

We consider the three most studied types of slack—unabsorbed, absorbed, and potential (Bourgeois & Singh, 1983; Sharfman et al., 1988)—and note that they vary based on where they reside. Both unabsorbed and absorbed slack reside within the firm (e.g., cash, inventories, etc.), while potential slack is external to the firm because it refers to “resources that have not yet entered the firm” (Sharfman et al., 1988: 610), such as excess borrowing capacity. We argue that this internal versus external distinction influences who has primary control over the resources, to whom the benefits accrue when that particular type of slack rises, and who incurs the losses if those slack resources are reduced. Consequently, this internal versus external distinction is critical because different types of owners (and therefore decision-making norms) can influence the relationship between performance relative to aspirations and slack differently. Specifically, we argue that when norms of reciprocity prevail, demands on internal slack resources during performance shortfalls diminish due to greater availability of external slack resources.

Our study makes several important contributions to the literatures on organizational slack and the BTF. First, our study is one of the first to conceptually develop and then empirically examine slack as a phenomena to be explained. Although there is some conceptual work on the antecedents of slack (Sharfman et al., 1988), the empirical work is limited and typically considers the antecedents to slack only tangentially rather than as a focal element of the study (e.g., Greenley & Oktemgil, 1998; Singh, 1986). Consequently, there is little empirical knowledge about what influences slack. Hence, we develop arguments with regard to the three most commonly studied slack resources in the literature and empirically test Cyert and March’s (1963) exposition on the expected impact of performance relative to aspiration on slack resources in general. Although this is a “baseline” contribution (in that the relationship between performance feedback and slack has been proposed already, though it has not been tested), it enables us to set the stage for our other contributions.

Our second significant contribution is an answer to the call to explore how different institutional contexts impact the implications of the BTF (Vanacker, Collewaert, & Zahra, 2017; Vissa, Greve, & Chen, 2010). Despite Cyert and March’s (1963) assertion about the importance of differing norms (e.g., “[they] should be one of the major objects for study by students of organizational decision making,” p. 119), only a few studies examine how different institutional contexts provide novel insight to the BTF (O’Brien & David, 2014; Vanacker et al., 2017; Vissa et al., 2010). We theorize that different norms, as evidenced by domestic (vs. foreign) ownership, impact how slack changes in response to performance feedback. Specifically, we propose that domestic ownership mutes the responsiveness of available and absorbed slack but accentuates that of potential slack. Thus, a core focus of our study is to show how extending theory within the BTF tradition may require consideration of institutional context, due to its ability to influence decision-making processes.

Finally, the ability of stakeholders to extract benefits from their relationships with the firm influences the resources available to the firm (Coff, 1999). We add to this literature by showing that the impact of performance relative to aspirations on slack resources varies depending on both the nature of the stakeholders’ relationships with the firm (e.g., domestic owners) and the location of the resources in question (e.g., internal or external to the firm).

Theoretical Background and Hypotheses

Organizational Slack and Its Antecedents

In the neoclassical view, the owners receive the entire rent generated by a firm, and zero slack exists at any given time. However, Cyert and March (1963) noted that the assumption of zero slack does not represent reality. Resources in excess of those required to sustain the firm (i.e., slack) are held or consumed by the firm’s coalition members, and by activities within the organization. Empirical evidence indicates that there are a variety of benefits to holding slack resources: It reduces vulnerability to performance shortfalls (Gomez-Mejia, Patel, & Zellweger, 2018), influences a firm’s product search efforts (Greve, 2003a; Voss, Sirdeshmukh, & Voss, 2008), and is generally considered a valuable strategic asset (Kim & Bettis, 2014). However, the recognized value of slack belies the lack of emphasis placed on understanding its antecedents. To explore this issue, we examine the existing research on the antecedents of different types of slack and the ways that various types of slack resources differ from each other.

Cyert and March (1963: 189) developed a behavioral-process view of slack and were among the first to theorize that “success tends to breed slack.” Despite the early linkage established by Cyert and March (1963) between a firm’s performance relative to aspirations and slack, little research has investigated this aspect of the theory. The available empirical research on this issue tends to provide minimal theoretical development for a variety of reasons: Slack was simply a mediating mechanism within the broader empirical model (Singh, 1986), the sample size was small and only univariate statistical tests were conducted (Greenley & Oktemgil, 1998), or the study focused on only one form of slack—budgetary (Dunk & Nouri, 1998). The most detailed discussion of the antecedents of slack is the conceptual work of Sharfman et al. (1988), who proposed three primary antecedents: the environment, the organization itself, and the “values and beliefs” of the dominant coalition—the internal stakeholders of the firm. Sharfman et al. (1988) posited that different forms of slack are influenced distinctly by these antecedents. They asserted that greater performance leads to greater slack, especially in “calm environments,” as performance is associated with an enhanced ability to accumulate cash.

BTF

Cyert and March (1963) argued that managers compare firm performance to aspiration levels, and this influences subsequent risk-taking preferences (Hoskisson, Chirico, Zyung, & Gambeta, 2017), with search receiving the most scholarly attention. Performance below aspirations encourages risky search behavior meant to find a solution to the problem of underperformance, while performance above the aspiration is associated with complacency, or a tendency to stay the course and avoid risky activities (Greve, 1998). Thus, it is important to highlight that the focus of BTF research is typically performance relative to an aspiration level, and not simply performance feedback alone.

Theory suggests that slack plays a role in enabling search behavior. For example, Iyer and Miller (2008) found that unabsorbed slack is positively related to a firm’s acquisition activity, while Greve (2003a) found that absorbed slack is positively related to R&D intensity. We base our model on the premise that as performance increases relative to aspirations, then slack increases as well. In the following section, we discuss each form of slack separately as a form of baseline hypotheses, which are consistent with prior theory but have not been empirically examined. We formally hypothesize the relationships here so we can build upon them for our more theoretically novel contingency hypotheses regarding ownership.

Performance Below Aspiration and Unabsorbed, Absorbed, and Potential Slack

The most commonly studied forms of slack are unabsorbed, absorbed, and potential slack (Sharfman et al., 1988). We build on and extend prior work by highlighting the location of slack (Daniel, Lohrke, Fornaciari, & Turner, 2004), which may be internal to the firm (unabsorbed and absorbed slack), or external to the firm (potential slack) (Bourgeois, 1981; Bourgeois & Singh, 1983; Sharfman et al., 1988). Internal slack is under the control of management, while management has less discretion over external slack as it exists outside of the firm’s boundaries.

Unabsorbed slack consists of liquid, uncommitted cash and assets located within the firm (Love & Nohria, 2005). It has received the most attention in the economics and management literatures and has been shown to “foster appropriate adaptation to unfolding contingencies” and to shield managers from the “rigors of market governance” (O’Brien & Folta, 2009: 466). Managers can re-deploy it more easily than absorbed slack because doing so does not entail recovery of resources from other stakeholders, such as employees or business units. When performance falters, firms have an incentive to utilize unabsorbed slack and invest in efforts to reverse their poor performance. Since poor performance attenuates the possibility of paying for investments in search activities with cash flows, unabsorbed slack may be a primary source for funding search. Hence, unabsorbed slack will decrease as performance falls below aspirations.

Absorbed slack also resides within the firm and thus is subject to managerial discretion. Absorbed slack is recoverable and includes inventory and selling, general, and administrative expenses (Bourgeois & Singh, 1983). It represents resources that have been invested in building human capital or instituting redundancies within the system that may not be efficient but influence information flow, help with building capabilities, and can be beneficial for adapting to growth or changes in the marketplace (Cyert & March, 1963; Lant, 1985; Love & Nohria, 2005). We posit that when performance falls short of aspirations, organizations have an incentive to cut back on absorbed slack. For example, performance shortfalls can induce managers to forego or curtail bonuses, run leaner and trim inventories, not replace workers who quit or retire, or possibly even lay off some employees. Recovery of absorbed slack occurs by taking away resources from other internal stakeholders in the firm (e.g., employees, business units, etc.). Taking such actions can help free up capital to invest in the problematic search that performance below aspiration is likely to trigger, as well as help improve profitability in future periods. Accordingly, performance shortfalls will lead to a decline in absorbed slack.

Potential slack represents the ability of the firm to raise external funds—mainly debt or equity capital (Bourgeois, 1981). The ability to raise external financing is contingent on both current levels of debt and expectations regarding future performance, which are reflected in the market value of the firm’s equity. Managers have less discretion over potential slack than they do over the internal resources of absorbed and unabsorbed slack, as they have to rely on external stakeholders (such as other firms, institutions, banks, and bond or equity markets). When firms perform poorly, expectations about the firm’s future profitability decline, causing borrowing capacity to fall and also making new equity issues less appealing to investors. At the same time, if the firm lacks sufficient profits to cover expenses or fund investment opportunities, it may need to borrow more to cover its needs, leading to further declines in levels of potential slack. Consequently, a firm’s potential or external slack will shrink as performance falls. In consideration of the above discussion, we propose the following baseline hypotheses:

H1a: Unabsorbed slack declines as performance falls further below the aspiration level.

H1b: Absorbed slack declines as performance falls further below the aspiration level.

H1c: Potential slack declines as performance falls further below the aspiration level.

Performance Above Aspiration and Absorbed, Unabsorbed, and Potential Slack

Similarly, we also hypothesize that increases in performance relative to aspirations will be positively related to the three forms of slack. When performance is strong, managers will likely prioritize diversion of some of the excess profits toward an increase in unabsorbed slack because of its strategic value (Deb, David, & O’Brien, 2017; Kim & Bettis, 2014). Furthermore, to the extent that levels of unabsorbed slack may have fallen during previous periods of subpar performance, managers should seek to replenish the stock of unabsorbed slack as a precautionary move in the event of future performance shortfalls. However, we do not expect all excess profits conferred upon the firm by strong performance to be diverted to unabsorbed slack. Strong performance generally leads to investment in human capital, including raises and promotions, and hiring additional workers to both help manage future growth and develop new organizational capabilities. This is particularly salient because divisional and midlevel managers have incentives to barter for additional employees to grow their units, whether to insulate against future shocks, for personal pay and prestige, or simply because “many hands make light work.” Accordingly, in times of strong performance, absorbed slack will increase.

Finally, as performance increases relative to aspirations, the firm’s potential to raise external financing will grow as the valuation of the firm increases in the assessment of external investors (i.e., both shareholder and lenders). Likewise, firms in this position tend to use some of their profits to pay down existing debt (Myers & Majluf, 1984). Thus, strong performance relative to aspirations tends to increase a firm’s borrowing capacity while also reducing its existing debt. This, in turn, increases the ability of the firm to raise both debt and equity from external capital markets, thus resulting in increased potential slack. In sum, we propose the following three additional baseline hypotheses:

H2a: Unabsorbed slack increases as performance rises further above the aspiration level.

H2b: Absorbed slack increases as performance rises further above the aspiration level.

H2c: Potential slack increases as performance rises further above the aspiration level.

Domestic Ownership, Institutional Context, and Decision-Making Norms

Most BTF research suggests that firms respond in predictable patterns when performing above or below aspirations. However, these patterns rely on assumptions pertinent to specific institutional contexts, which is problematic because institutional contexts are heterogeneous (O’Brien & David, 2014). As noted by Cyert and March (1963), organizations have different norms and rules that govern their responses to performance feedback, yet little research considers how these different norms and rules influence firm action. Organizations are embedded in contexts with distinct institutional norms, and differences in these norms have implications for how firms respond to performance feedback, which represents an important area for research (Gavetti, Levinthal, & Ocasio, 2007). In other words, institutional norms are an important boundary to the predictions of BTF. Accordingly, we explore how the firm’s ownership structure can influence the institutional norms to which managers are exposed and thus exert a strong influence on the relationship between performance feedback and slack.

While various forms of embedded ownership exist in other contexts, including chaebols in South Korea and business groups in India and Europe (Kim, Kim, & Lee, 2008; Sundaram & Inkpen, 2004), Japan provides a particularly interesting context for studying how the preferences of owners can influence strategy (David et al., 2010). The preferences of domestic, embedded Japanese owners are a consequence of historical differences in the evolution of institutions in Japan versus in cultures like the United States and the United Kingdom. Due to labor strife after World War II, Japanese firms started guaranteeing lifetime employment to workers. This was done to make sure that firms had an uninterrupted supply of labor in order to ensure long-term growth (Ahmadjian & Robinson, 2001). Additionally, restrictions on shareholdings by banks (i.e., banks could only hold up to 5% in a firm) led them to develop a network of embedded relationships by acquiring stakes in companies (like life insurance companies and trusts) that held shares in the focal firms in which the banks could not own beyond a certain limit (Gerlach, 1992; Gilson & Roe, 1993).

In order to overcome regulatory restrictions, firms developed embedded relationships with other firms, such as trade partners, which over time evolved into a culture of institutional norms of ensuring growth of stakeholder groups like employees and reciprocity between firms in the embedded network. For example, in 1999, Nissan had over $4 billion of equity ownership in several companies. Up until the Asian financial crisis and subsequent merger with Renault, a major part of Nissan’s retained earnings was invested in creating and maintaining embedded relationships through ownership ties (Millikin & Fu, 2005). Consequently, many—but not all—Japanese firms are enmeshed in an embedded network of equity ownership and cross-shareholdings linking trading partners and financial institutions. Furthermore, since they intend to hold the equity in perpetuity and list it on their books at purchase price, stock price appreciation is generally a trivial concern for these owners relative to growth (O’Brien & David, 2014). Moreover, the cross-shareholdings provide a certain quid pro quo whereby managers of linked firms support each others’ desire to adhere to traditional norms.

An interesting “clash of capitalisms” occurred after Japanese financial markets liberalized regulations regarding foreign investment in the early 1990s (Ahmadjian & Robbins, 2001, 2005). The subsequent influx of foreign investors (mostly institutional investors in the United States and United Kingdom), coupled with slowing economic growth in the 1990s, left Japanese managers feeling pressured to attract and retain foreign investors by conforming to their expectations (Ahmadjian & Robbins, 2005). However, these foreign owners were very different from the domestic owners Japanese managers were used to. For example, foreign owners generally lacked business ties to the firm, and their primary motive for investing in the firm was stock price appreciation, and therefore stock price appreciation was the primary concern of these new owners. Notably, some research indicates that foreign owners possess significant power in these relationships and exert that power via disciplinary pressure on entrenched insiders (be they managers or owners), thereby promoting long-term stock appreciation (Bena, Ferreira, Matos, & Pires, 2017). Yet this underscores our fundamental assertion: Foreign owners are not motivated to adhere to entrenched communitarian norms that emphasize the growth and stability of the overall embedded network, rather than just the firm itself. Hence, Japanese managers who either had significant foreign investment or wanted (or needed) to attract it felt pressure to move away from the communitarian norms inherent in a stakeholder model and embrace the contractarian norms of the shareholder model.

Despite this shifting landscape, not all firms were equally impacted by the influx of foreign investors. High degrees of ownership by domestic owners—who are more supportive of the traditional communitarian norms that emphasized close firm relationships, reciprocity, and lifetime employment (Ahmadjian & Robbins, 2001, 2005)—helped insulate managers from the pressures exerted by the contractarian norms of foreign investors, thus safeguarding traditional values (David et al., 2010; Yoshikawa et al., 2005). Though we chose Japan as our empirical context, our theorizing generalizes to other contexts where a significant proportion of owners are willing to embrace communitarian norms.

The Moderating Role of Ownership

Previous research has investigated differences between owners in terms of differences in their goals, and findings generally indicate that different owners do indeed have distinct preferences. For example, Hoskisson, Hitt, Johnson, and Grossman (2002: 697) argued that different types of owners influence corporate innovation strategies in distinct ways because “different types of owners often have their own distinct and potentially conflicting preferences.” Accordingly, Kim et al. (2008) found that ownership structure influences the relationship between financial slack and R&D investments, providing support for the notion that different types of owners have different preferences for how organizational slack is utilized.

Sharfman et al. (1988) highlighted the importance of considering the cultural backgrounds, beliefs, and preferences of key stakeholders in studying the antecedents of slack. Values and beliefs themselves are a function of the institutional norms that create the surrounding context in which decision-makers operate. For example, firms in the United States operate in a contractarian system, in which organizations are essentially conceptualized as a nexus of contracts among different stakeholder groups. In this context, organizations operate at arm’s length, and the primary tie between parties is the contract itself. In contrast, Japanese firms operate in an institutional context wherein firms often have close business relationships with many of their shareholders. According to prior literature on domestic ownership in the Japanese context, this nexus of embedded relationships among stakeholders is broadly referred to as a communitarian system and differs from contractarian systems in three important regards (David et al., 2010). First, firms adhere to norms of reciprocity—norms that dictate one gives something in return for something received (O’Brien & David, 2014)—which play an important role in how shareholders gain benefits. Second, there is a greater focus on the welfare of all stakeholders (i.e., customers, suppliers, employees, etc.). Third, growth of the embedded network of firms is prioritized over short-term profits for any one individual firm.

In consideration of these differences, there could be significant variation in the norms governing firm behavior for firms with high versus low levels of domestic ownership. Firms with low levels of domestic ownership will feel pressure to attract foreign investors and reflect the contractarian norms most commonly (and implicitly) theorized about in the BTF research, where the general charge of the firm is to fulfill its contractual obligations to its various stakeholders. However, firms with high levels of domestic ownership are embedded in a web of relationships and will therefore reflect the communitarian norms discussed above. As such, the duty of managers is enmeshed in a broader institutional context that emphasizes relationships between different stakeholders. These differing institutional norms play a critical role in the relationship between performance relative to aspirations and slack, which we will now discuss.

Performance Below Aspiration, Domestic Ownership, and Slack

As stated earlier, slack declines when performance relative to aspirations decreases. We now consider how different levels of domestic ownership, indicative of different norms that govern decision making in response to performance feedback, moderate this relationship. A critical consideration here is the location of slack. Whereas managers have relatively high discretion over internal forms of slack (i.e., absorbed and unabsorbed), managers must rely on external stakeholders such as banks and bond or equity markets to utilize external (i.e., potential) slack. This categorization of slack resources based on where it resides is relevant to our study because we theorize that having an embedded relationship with external stakeholders will influence both a firm’s ability to access resources that reside external to the firm as well as the firm’s tendencies to utilize slack resources located within the firm. Specifically, when performance falls below aspirations, the two forms of internal slack (i.e., unabsorbed and absorbed) will decline less in firms with greater domestic ownership.

In regards to unabsorbed slack, domestic ownership moderates this relationship for two primary reasons. The BTF suggests that when performance falls below aspirations, unabsorbed slack will be directed toward investments aimed at reversing the firm’s poor performance. However, because unabsorbed slack has multiple strategic benefits (Deb et al., 2017), managers prioritize sustaining sufficient levels. In times of need, firms with domestic owners have other methods to reduce their need to draw on unabsorbed slack. Due to norms of reciprocity and an emphasis on the growth of the network of firms, firms with high domestic ownership are embedded in a network of other firms that are a part of its value chain and can help the focal firm get more favorable terms on existing and new trade contracts. That is, flexibility in both delivery schedules and payment terms, as well as purchasing raw materials at subsidized costs, gives embedded firms the benefits of a pseudo-internal capital market (Lincoln, Gerlach, & Ahmadjian, 1996; Sheard, 1989). Indeed, if times have recently been good, the focal firm may have given overly generous terms to its trade partners, but now norms of reciprocity dictate that it receives beneficial terms.

Second, in addition to receiving more favorable trade terms, a firm with high domestic ownership has a greater ability to draw on external sources of financing at favorable terms during performance shortfalls, most notably potential slack (Sheard, 1989, 1994). Although it may seem unnecessary to take out new loans or draw on revolving lines of credit if the firm has cash reserves, the firm may prioritize maintaining cash reserves for a rainy day. In particular, even if the firm has an embedded relationship with its bank, credit can dry up during a recession, and a bank may be less able to help the firm despite its best intentions. Hence, prudent managers will try to preserve unabsorbed slack and instead utilize potential slack (i.e., loans or credit) if it is readily available on good terms. Furthermore, because debt has certain tax benefits, even cash-rich firms frequently issue debt (Worstall, 2013). Business groups in Japan often center on banks (Judge, Douglas, & Kutan, 2008), and Japanese banks tend to help their embedded clients even when performance shortfalls become serious and the firm faces default (David, O’Brien, & Yoshikawa, 2008). Similar findings about these banking practices, which contrast starkly with banking practices in the West, have also been documented in the Finance literature (see, e.g., Caballero, Hoshi, & Kashyap, 2008; Nakamura, 2016).

Furthermore, norms of reciprocity lead to both the expectation of outside help in times of need by the focal firm and the belief by other embedded firms that they will receive reciprocal benefits later (O’Brien & David, 2014). These norms of reciprocity between embedded firms reduces the need for the focal firm to deplete slack located within the firm because resources outside of the firm are more readily available and easily procured. Hence, firms that have higher domestic ownership will have access to favorable financing and contract terms during times of poor performance and therefore will have less need to draw down their unabsorbed slack. This does not suggest that these firms will not utilize unabsorbed slack resources at all but rather that they have access to, and support from, external sources during performance downturns and are apt to make use of these sources (at least to some extent) as opposed to primarily relying on unabsorbed slack during performance shortfalls. It is interesting to note that this contrasts with contractarian societies such as the United States and United Kingdom, which generally have relatively efficient external capital markets, but those markets are reluctant to provide funds on favorable terms to struggling firms, thus inducing managers to frequently forego attractive investment opportunities as opposed to raising external funds (Myers & Majluf, 1984).

H3: Unabsorbed slack will decline less as performance falls further below the aspiration level when domestic ownership is high.

As we argued previously, firms also have a tendency to draw down absorbed slack, via cutbacks and possibly even layoffs, when performance falls below the aspiration level. We contend this effect is diminished in firms with high domestic ownership for two reasons. First, domestic owners place greater emphasis on the long-run growth of the entire system of embedded firms. For example, David et al. (2010) showed that domestic owners seek growth rather than short-term profits from diversification and tend to promote greater employment growth following diversification. Reductions in absorbed slack may negatively influence long-run growth, as it would require decreases in human capital, structural changes, or the elimination of redundancies needed for information flows and potential future growth.

Second, because employee salaries constitute a major part of absorbed slack (Love & Nohria, 2005), domestic owners’ incentives are aligned with managers who prefer to preserve human capital investments, both because human capital investments are considered important for long-run growth and due to traditions like lifetime job guarantees (Gordon, 1985). The job guarantees common in Japan led to “norms against downsizing” (Ahmadjian & Robbins, 2005: 454). For example, Yoshikawa et al. (2005) and Ahmadjian and Robinson (2001) provided evidence of an implicit social contract in Japan whereby many firms consider the firing of employees to be unconscionable: “the chairman of Toshiba said that discharging employees ‘is the most serious sin’” (Yoshikawa et al., 2005: 285). Hence, when firms with high domestic ownership experience performance shortfalls, they are less prone to cut absorbed slack and instead will utilize potential slack or seek concessions from their trade partners.

H4: Absorbed slack will decline less as performance falls further below the aspiration level when domestic ownership is high.

Although we theorize that domestic ownership will weaken the positive relationship between performance relative to aspirations and unabsorbed and absorbed slack, we predict the opposite will be the case for potential slack. Generally, lenders are reluctant to invest in poorly performing firms, even though these firms may need to make critical investments to reverse their fortunes. However, our arguments are predicated upon norms of reciprocity to a larger network of stakeholders and not the norms of a contractarian system. Banks in Japan will readily lend to firms with whom they have an embedded relationship and which are experiencing performance shortfalls for three primary reasons. First, the loans are not viewed as risky because the bank expects the broader network of firms to help the focal firm turn things around, and as such, embedded firms are very resilient (David et al., 2008). Second, the bank is motivated to lend to the firm to help it turn things around because the bank makes most of its profits not from the loans but from the ancillary services (e.g., letters of credit, check clearance, and cash management) it provides to clients (Boot, 2000); helping the firm turn things around helps protect those cash streams. Third, as it is part of an embedded network, the bank also does business with many of the focal firm’s trade partners, who could be hurt if the bank did not help the focal firm improve its situation. Thus, firms with high domestic ownership in Japan have banks with which they have close relationships, and the firms can capitalize on this relationship to raise necessary financing (Hoshi, 2006; Sheard, 1989).

Firms with high domestic ownership are not only more capable of drawing on potential slack during tough times, they are also more inclined to do so. As we argued above, firms experiencing performance shortfalls should generally prefer to preserve unabsorbed slack and capitalize on their ability to raise external financing, if available, thus reducing the extent of potential slack. Furthermore, due to cultural norms of protecting stakeholders such as employees and investing in long-term growth (David et al., 2010; O’Brien & David, 2014; Yoshikawa et al., 2005), domestic owners support the firm’s resistance to eroding absorbed slack during tough times and will prefer to use external financing, thus reducing potential slack. Hence, struggling firms with high domestic ownership have both a greater propensity and capacity for utilizing potential slack to facilitate adaptive investments during performance shortfalls.

H5: Potential slack will decline more as performance falls further below the aspiration level when domestic ownership is high.

Performance Above Aspirations, Domestic Ownership, and Slack

We argued that norms of reciprocity encourage concessions by external stakeholders (e.g., partner firms and banks) when the focal firm is performing poorly relative to aspirations, leading to less reduction in levels of absorbed and unabsorbed slack. Conversely, as performance increases above aspirations, domestic owners will want the firm to reciprocate and help other stakeholders who are in need or to repay those who had helped the firm previously (O’Brien & David, 2014). Due to the existence of reciprocal commitments and obligations that are derived from cultural norms of reciprocity (Bradley, Schipani, Sundaram, & Walsh, 1999; David et al., 2010), firms performing well are obliged to “share the wealth” with partner firms and will thus have fewer available resources to accumulate internally. In addition, if firms can rely on external resources when performance declines, then the urgency and need to build up both absorbed or unabsorbed slack when performance is strong also decreases. As a result, the positive relationship between strong performance and both unabsorbed and absorbed slack weakens in firms with high domestic ownership. As excess profits are diverted toward benefiting the domestic partners, either because the other firms are in need or because the focal firm is paying them back or creating and maintaining new embedded ties, firms with greater domestic ownership will accrue lower levels of both unabsorbed or absorbed slack.

H6: Unabsorbed slack will increase less as performance rises further above the aspiration level when domestic ownership is high.

H7: Absorbed slack will increase less as performance rises further above the aspiration level when domestic ownership is high.

We noted earlier that when performance is above aspirations, firms (1) have extra free cash flow, thereby improving expectations about the firm’s future performance, and (2) tend to pay down debt. In such cases, the firm’s level of potential slack, as reflected in its ability to raise external funds, increases. The tendency to pay back debt when performance is above aspirations is particularly pronounced when domestic ownership is high. Due to norms of reciprocity, the bank will readily lend to a domestic client that experiences performance shortfalls, but the bank will also expect to be repaid promptly when things turn around. Prompt repayment, in turn, allows the bank to reallocate those funds from relatively low-profit loans to more profitable opportunities or, alternatively, to lend those funds to other firms within the embedded network that may need the extra financial support. David et al. (2010) noted that embedded lenders profit more from their investments in business relationships than from the loans. Prompt repayment from a firm experiencing strong performance therefore enables the bank to further develop relationships with other firms. Together, these findings suggest that domestic ownership strengthens the relationship between performance above aspirations and potential slack.

H8: Potential slack will increase more as performance rises further above the aspiration level when domestic ownership is high.

The Responsiveness of Internal and External Slack to Performance Feedback

We hypothesized differences in the relationship between performance feedback and slack depending on the type of slack, with a critical distinction being whether slack is internal or external to the firm. This, however, raises the question of whether all forms of slack are equally responsive to performance feedback, and consideration of the location of slack helps illuminate this question. Although our theoretical arguments varied according to whether performance was above or below aspirations, we generally hypothesized—within each type of slack—similar relationships for above and below the aspiration. However, for the general responsiveness of the different types of slack to performance feedback, distinguishing between performance above and below aspirations is not theoretically critical. Hence, to simplify this analysis, we focus more generally on performance relative to aspirations. And as we explain below, the types of slack that are most responsive to performance feedback will heavily depend on ownership structure.

Dedicated domestic owners help to stabilize a firm’s stock price and insulate managers from concerns about short-term fluctuations in stock price. However, when domestic ownership is low, managers have to be much more concerned about attracting and retaining foreign investors, and thus the focal firm is more subject to contractarian norms. Accordingly, firms with low domestic ownership will behave similarly to U.S. firms in that unabsorbed slack will be the primary source for funding search during tough times but will replenish during good times. Thus, when domestic ownership is low, unabsorbed slack will be more responsive to performance feedback than other forms of slack. In contrast, when domestic ownership is high, these tendencies are muted because—as argued above—the focal firm is both motivated and able to maintain relatively stable internal slack levels during times of both poor and strong performance. These firms instead rely on the readily available (external) potential slack during tough times but repay it quickly during good times. Hence, when domestic ownership is high, potential slack is the most responsive to performance feedback, and we thus predict:

H9: When domestic ownership is low, unabsorbed slack is the most responsive form of slack to performance relative to aspirations.

H10: When domestic ownership is high, potential slack is the most responsive form of slack to performance relative to aspirations.

Methods

Data Sources and Sample

We utilize the Pacific-Basin Capital Markets (PACAP) database for Japanese firms to test our hypotheses. Our initial sample included all manufacturing companies over the period from 1974 to 2010. We limited the sample to manufacturing firms in order to maintain comparability across industries. For example, common definitions of available slack may have very different interpretations in financial industries, potential slack may be less pertinent in service industries that invest in few tangible assets, and firms may have less discretion over slack in more heavily regulated industries. Additionally, since small firms may be locked out of the foreign securities markets, we do not include firms with a book value of equity less than three billion Yen (Anderson & Makhija, 1999), which is approximately US$19 million using the average exchange rate over our sample period. After applying the above criteria, and accounting for missing values for all variables in our regression equations, the final unbalanced panel data sample consists of 1,340 firms. Due to differences in availability of data for the three dependent variables, we have different numbers of firm-year observations for each. The total numbers of firm-year observations in models where unabsorbed slack, absorbed slack, and potential slack are the dependent variables are 28,569, 28,565, and 28,633, respectively.

Variables

Dependent variables.

We follow prior literature (Bourgeois & Singh, 1983; Greve, 2003a; Singh, 1986) to calculate the three different types of slack about which we hypothesize. Unabsorbed slack is measured as the ratio of cash and marketable securities to current liabilities. Absorbed slack is measured as the ratio of selling and administrative expenses to sales. Potential slack is measured as the ratio of debt to the market value of the firm (calculated as the sum of the book value of debt plus the market value of equity) subtracted from one. A decrease in either absorbed or unabsorbed slack indicates a decline in the stock of internal slack resources; a decrease in potential slack indicates a decline in the ability of the firm to raise external financing.

Independent variables and controls.

Previous research has argued and found that the relationship between performance relative to aspirations and firm search can be different above and below the aspiration (Greve, 2003a). Similarly, our theoretical arguments posit slightly different mechanisms driving the relationship between performance relative to aspirations and slack for above and below the aspiration point. Thus, in order to test our hypotheses related to the direct impact of variations in performance relative to aspirations on the three types of slack, for most of our models we employ spline regressions and calculate two independent variables: performance below aspiration (Perf<A) and performance above aspiration (Perf>A).

In order to calculate performance below and above aspiration (Perf<A and Perf>A, respectively), we first calculate performance relative to aspiration as the difference between the focal year’s performance and the performance aspiration levels (Perf-A). The firm’s performance is measured by its return on assets (ROA), calculated as the ratio of operating income to total firm assets. Our proxy for performance aspiration level (A) is a function of firm’s historical (HA) and social aspirations (SA) (Greve, 2003a, 2003b). In equation (1) below, A(t) stands for aspiration level, HA(t) stands for historical aspiration, and SA(t) stands for social aspiration. The variable wt1 stands for the proportion by which historical and social aspirations are weighted.

Social aspiration (SA) is calculated as the average ROA of all other firms operating in the focal firm’s industry. Our final measure of aspiration level is a weighted average of historical aspiration and social aspiration. We measure historical aspiration as a weighted sum of past years’ performance and past historical aspiration, using the following formula:

HA stands for historical aspiration. Perf is the performance of the focal firm measured as ROA. The variable wt2 represents the proportion by which the most recent past performance is weighted. We assume that the most recent past performance, Perf (t-1), should be weighted equal to or greater than past historical aspiration as more recent performance tends to have a larger impact on managerial decision making than performance in preceding years. Accordingly, wt2 can take the values between 0.5 and 1.0. In order to determine the values of wt1 and wt2, we run empirical models for all possible values with increments of 0.1. Hence, we run fixed-effects models, in which wt1 can take values between 0.0 and 1.0 with increments of 0.1 and wt2 can take values between 0.5 and 1.0 with increments of 0.1.

The values of wt1 and wt2 are determined by estimating the models with different values and determining the value that best fits the data (as determined by the overall model fit, as indicated by the F statistic), which is consistent with other BTF research (Audia & Greve, 2006; Greve, 2003b; Lungeanu, Stern, & Zajac, 2016). This technique relies on using available data to estimate aspiration weights and is appropriate for large sample studies such as ours. For our models where absorbed slack is the dependent variable, we found wt1 to be equal to 0.4 and wt2 to be equal to 0.5. For our models where unabsorbed slack is the dependent variable, wt1 is equal to 0.0, and wt2 is equal to 0.5. For our models where potential slack is the dependent variable, wt1 is equal to 0.4, and wt2 is equal to 0.9. Subsequently, we subtract the aspiration level, A(t), from the firm’s current period ROA to calculate performance relative to aspiration (Perf-A). We calculate performance below aspiration, Perf<A, as being equal to performance relative to aspiration (Perf-A) when Perf-A is less than equal to zero, and equal to zero otherwise. Similarly, we calculate performance above aspiration, Perf>A, to be equal to performance relative to aspiration (Perf-A) when Perf-A is greater than zero, and zero otherwise. We note, however, that Perf-A was used to test H9 and H10, since they employed similar logic for Perf<A and Perf>A.

The most critical consideration concerning ownership is whether the owners have other business ties to the firm and are therefore incentivized to care about more than just the stock price. Following prior literature (David et al., 2010; O’Brien & David, 2014; Yoshikawa et al., 2005), domestic ownership is calculated as the total number of shares owned by Japanese financial institutions and other Japanese business corporations divided by total shares outstanding. The financial institutions include banks that lend money to the firm and insurance companies that underwrite insurance policies for the firm, and the Japanese corporate owners are largely suppliers and customers (Yoshikawa et al., 2005). For both types of owners, ownership is typically a means for bolstering business and other ties (Gedajlovic & Shapiro, 2002), and as such, the shares are generally held for the long term—often reciprocally—and are rarely sold (Gerlach, 1992). The higher the value of this variable, the greater the influence of domestic owners, indicating that the firm will adhere more closely to the communitarian norms (O’Brien & David, 2014). We note, however, that our measure of domestic ownership only includes firms that are likely to have an embedded relationship with the focal firm and does not encompass all domestic owners. Specifically, the measure excludes ownership by the government, securities companies (typically investors with an arm’s-length relationship), and ownership by individuals.

We also controlled for several other factors that could influence the level of slack. First, in each model, we controlled for the lagged value of all the three types of slack—absorbed, unabsorbed, and potential. Because large firms tend to have more slack (Audia & Greve, 2006), we control for firm size with the natural logarithm of total firm assets. Volatility in performance may impact a firm’s access to resources and its inclination to engage in reciprocal behavior. Hence, we control for the stability of the firm’s earnings with the variable performance volatility, which we measured as the standard deviation of ROA over the previous 5 years. We control for the influence of foreign owners, which in Japan are primarily institutional investors from the United States and United Kingdom (Ahmadjian & Robbins, 2005), who together account for 70% of foreign shareholdings (Yoshikawa et al., 2005). They do not share the same cultural norms as Japanese investors, have only an arm’s-length contractarian relationship with Japanese firms, and hence primarily care about stock price (David et al., 2010). The influence of these contractarian owners on the firm may impact our proposed relationships. Hence, we control for foreign ownership, which is the total number of shares owned by foreigners divided by total shares outstanding. Results are substantively similar, however, if we exclude this control.

Accessibility of certain resources may depend on the amount of investments in net fixed assets and intangible assets. Hence, we control for fixed assets, calculated as the ratio of plant, property, and equipment owned by the firm to total assets. Intangible assets are calculated as the ratio of the sum of goodwill, patent rights, design rights, mining rights, etc., to total assets. Changes in revenue may influence the extent of slack available to the firm, so we control for sales growth, which is calculated as the natural logarithm of the ratio of sales to the previous year’s sales. Furthermore, we control for several time-varying industry characteristics that may impact our dependent variables. Industry competition may influence the availability of slack resources available in the industry and hence we control for industry competition by calculating the entropy measure of industry competition as per the formula below. Pi is the ratio of sales of firm i to sum of sales of all firms in the industry of N firms.

Additionally, we control for growth opportunities in the industry with the variable industry growth, which is calculated as the market-to-book ratio of the median firm operating in that industry. Industries with volatile sales may use and keep slack to a different extent than industries that have stable sales. We therefore control for industry volatility, calculated as the standard deviation of sales of all firms in the industry in a particular year. We also control for industry potential slack, industry absorbed slack, and industry unabsorbed slack as the average potential slack, average absorbed slack, and average unabsorbed slack (respectively) in the industry in a particular year. These industry-level controls help us account for time-varying differences in the industry that might impact our results. Also, all independent variables are lagged by 1 year and all models specified firm, industry, and year fixed effects, although the industry fixed effects were generally dropped because of collinearity.

Analysis

We account for firm heterogeneity that is stable over time with firm fixed effects. We control for the lag of the dependent variable because prior levels of slack may influence current levels. Furthermore, including the lag of the dependent variable as a predictor variable also helps to account for time-variant firm heterogeneity. However, including the lag of the dependent variable as a predictor variable also introduces bias into the model (see Nickell, 1981). Fortunately, Bruno (2005) describes a method for correcting this bias in unbalanced dynamic panel data models employing firm fixed effects. Accordingly, we use Bruno’s (2005) corrected least squares dummy variable (LSDVC) approach, which we implement via the XTLSDVC command in Stata (for more details, see Bruno, 2005). Although all three methods for correcting the bias reviewed by Bruno (2005) yielded similar results, we use the Arellano-Bond method (Arellano & Bond, 1991) because it is appropriate for handling problems of unobserved heterogeneity and endogeneity in a dynamic panel data with a relatively small number of time periods but a large number of firms, as is the case in our data. Hence, this estimation technique is well suited to a dynamic panel data model with a modest number of time periods and a large number of firms, when unobserved heterogeneity is a concern.

Results

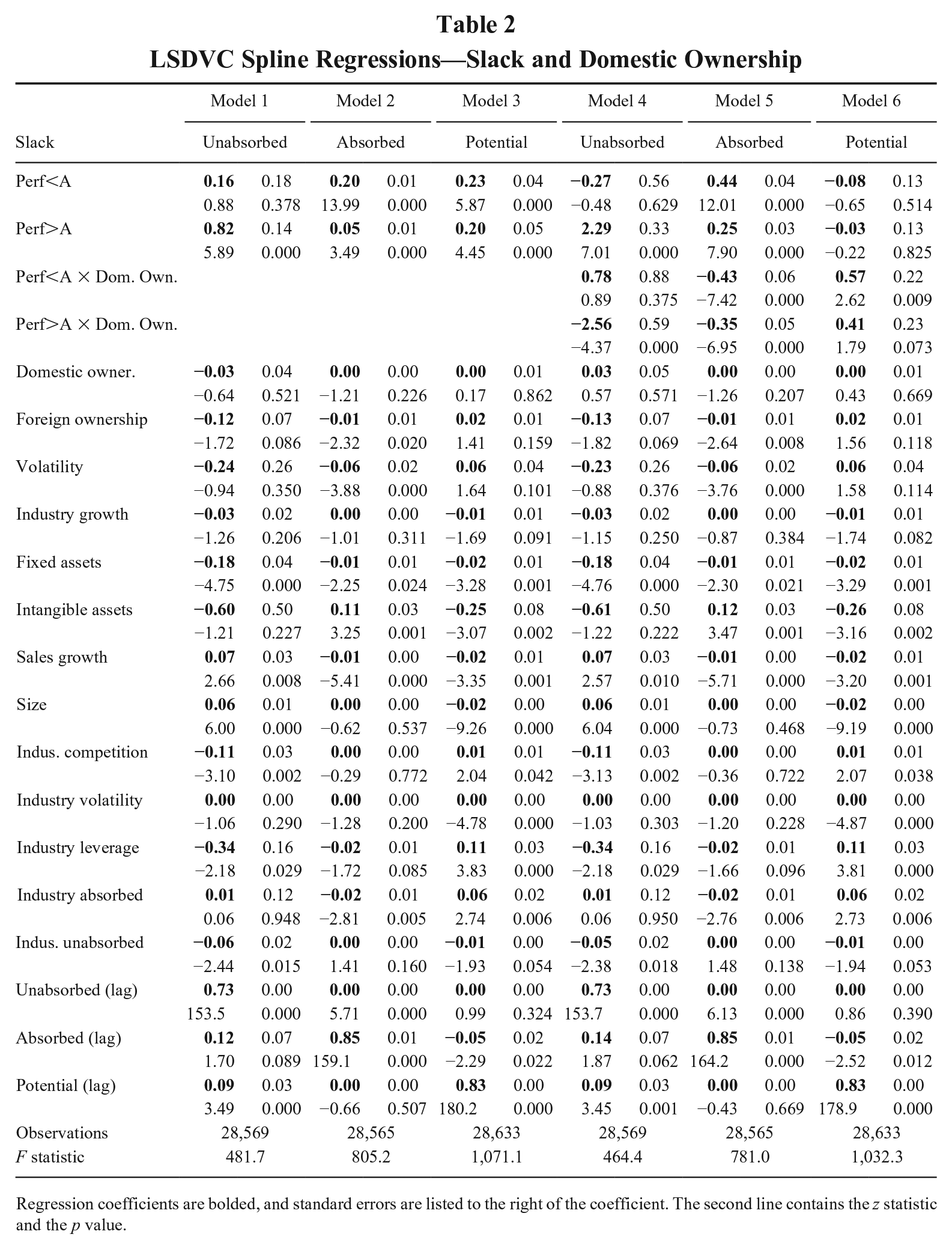

Table 1 displays the descriptive statistics of our data, and Table 2 displays the results of our hypotheses tests. For all models, the Wald Chi-Squared test was highly significant (p ≈ 0.000). Hypotheses 1a-c argued that as performance falls below aspirations (Perf<A), the extent of unabsorbed, absorbed, and potential slack (respectively) would decline. While the positive and significant (p ≈ 0.000) coefficients on Perf<A for absorbed (Model 2) and potential (Model 3) slack support Hypotheses 1b and 1c, we fail to find support for Hypothesis 1a regarding unabsorbed slack (Model 1). Hypotheses 2a, 2b, and 2c argued that as performance increases above aspirations (Perf>A), the extent of unabsorbed, absorbed, and potential slack (respectively) would increase. The positive and significant (p ≈ 0.000) coefficients on Perf>A in Models 1, 2, and 3 support all three hypotheses.

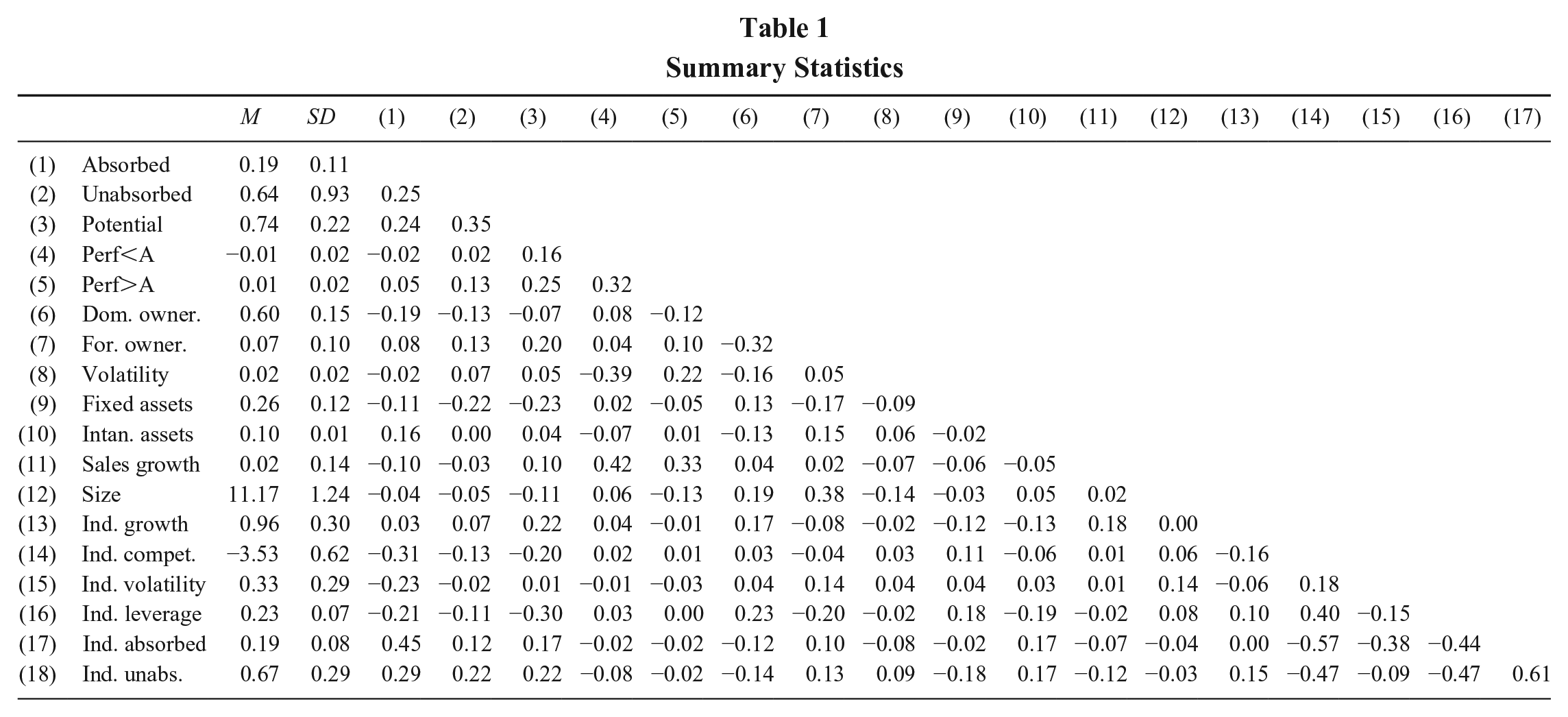

Summary Statistics

LSDVC Spline Regressions—Slack and Domestic Ownership

Regression coefficients are bolded, and standard errors are listed to the right of the coefficient. The second line contains the z statistic and the p value.

In H3 and H4, we argued that as performance falls below aspiration, unabsorbed and absorbed slack (respectively) will decline less in firms with higher domestic ownership. The insignificant coefficient (p = 0.375) for the interaction between Domestic Ownership and Perf<A in Model 4 indicates a lack of support for H3. However, the negative and significant (p ≈ 0.000) coefficient on the interaction between domestic ownership and Perf<A in Model 5 supports our assertion with respect to absorbed slack, and hence H4 is supported. In Hypothesis H5, we argued that as performance declines below aspiration, potential slack declines more in firms with greater domestic ownership, as these firms tend to utilize resources external to the firm. The positive and significant coefficient in Model 6 on the interaction between performance below aspiration and domestic ownership (p = 0.009) lends support to H5.

In Hypotheses H6 and H7, we argued that when performance increases above aspiration, both unabsorbed and absorbed slack (respectively) will increase less in firms with higher domestic ownership. The negative and significant (p ≈ 0.000) coefficients on the interactions between domestic ownership and Perf>A in Models 4 and 5 support both hypotheses. In H8, we argued that in firms with greater domestic ownership, increases in performance above aspiration will lead to a greater increase in the extent of potential slack. We find modest support for this hypothesis in Model 6 (z = 1.79, p = 0.073).

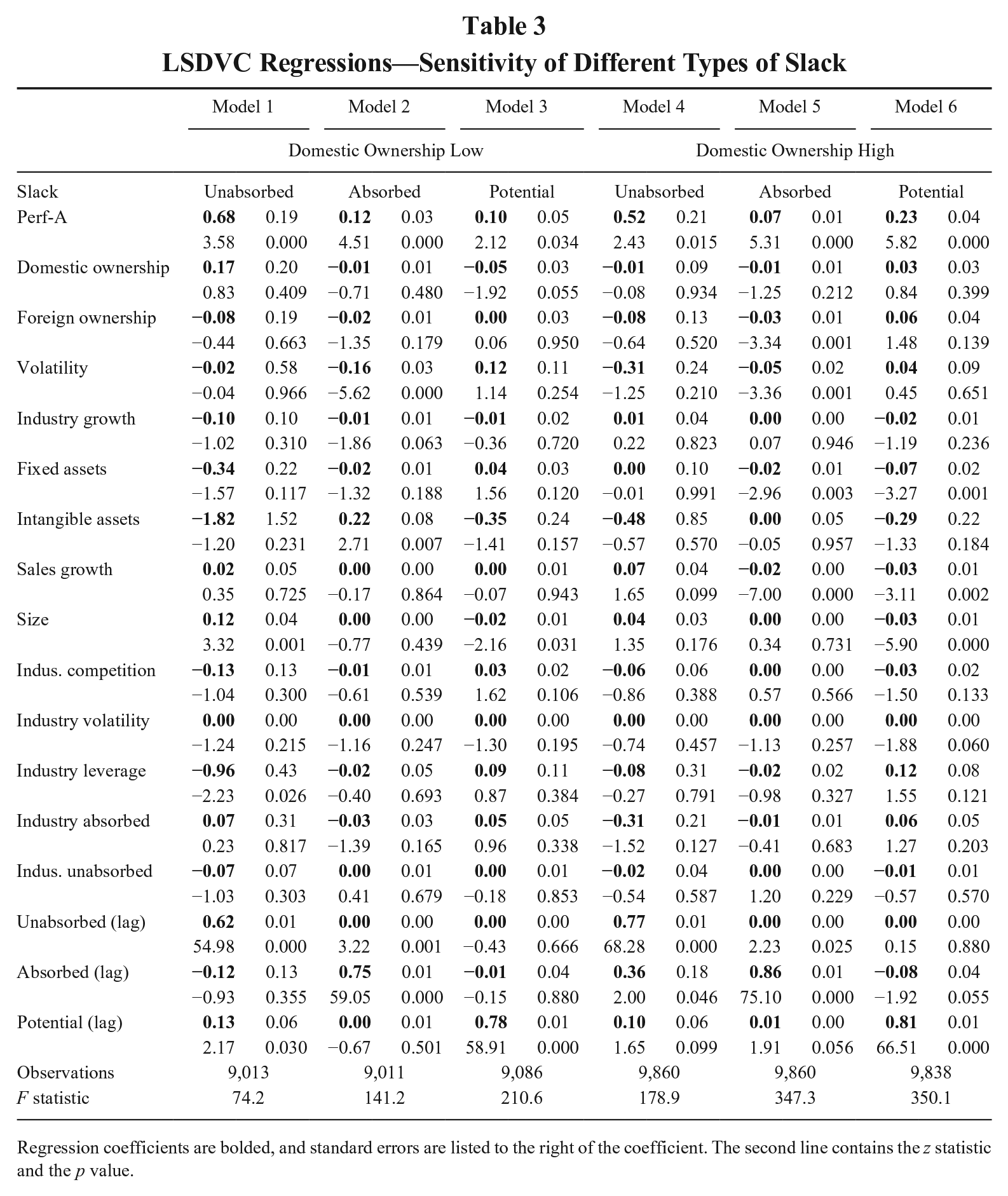

Table 3 presents our analysis of Hypotheses 9 and 10, which predicted that the form of slack that is most sensitive to changes in performance relative to aspirations will vary according to the level of domestic ownership. Since our arguments for these hypotheses were similar for performance both above and below the aspiration, and in order to simplify the analysis, we focus on Perf-A instead of Perf<A and Perf>A. Models 1 through 3 show the results for firms with low domestic ownership. As predicted by H9, the coefficient for the effect of Perf-A on unabsorbed slack (Model 1) is several times greater than it is for both absorbed slack (z = 2.91, p = 0.004) and potential slack (z = 2.96, p = 0.003). However, in regards to firms with high domestic ownership (Models 4-6), we find mixed support for H10. Although the coefficient for the impact of Perf-A on potential slack is significantly larger than it is for absorbed slack (z = 3.76, p ≈ 0.000), it is not significantly different than the effect of Perf-A on unabsorbed slack (z = −1.33, p = 0.183).

LSDVC Regressions—Sensitivity of Different Types of Slack

Regression coefficients are bolded, and standard errors are listed to the right of the coefficient. The second line contains the z statistic and the p value.

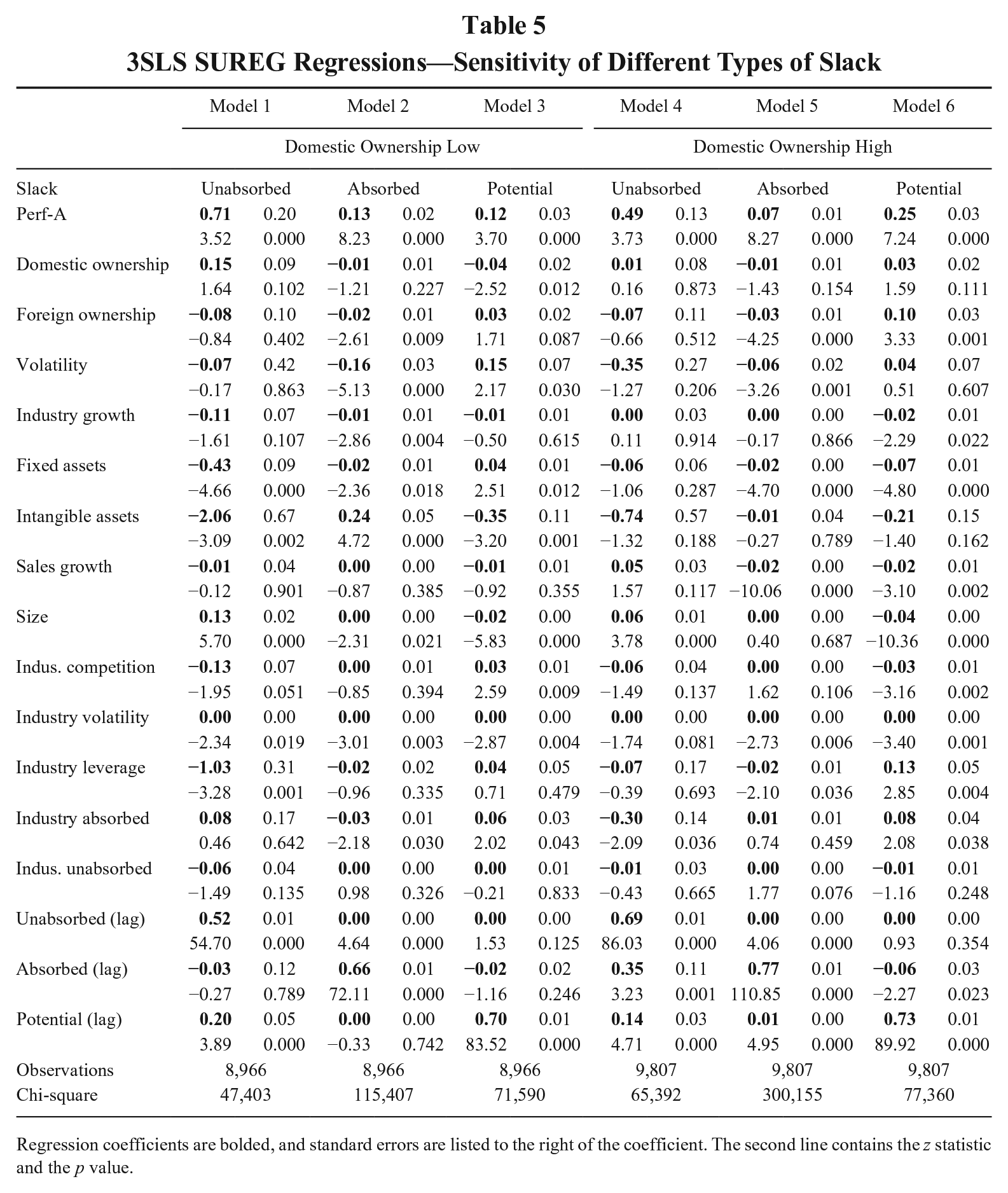

As a robustness check, we repeat the analysis of Tables 2 and 3 by modeling the three forms of slack with a simultaneous system of equations using three stage least squares regressions (3SLS). Specifically, we use the REG3 command in Stata with firm fixed effects while treating ownership and all forms of slack as endogenous (using all exogenous variables as instruments). As Tables 4 and 5 reveal, the results are very similar to our LSDVC models.

3SLS SUREG Regressions—Slack and Domestic Ownership

Regression coefficients are bolded, and standard errors are listed to the right of the coefficient. The second line contains the z statistic and the p value.

3SLS SUREG Regressions—Sensitivity of Different Types of Slack

Regression coefficients are bolded, and standard errors are listed to the right of the coefficient. The second line contains the z statistic and the p value.

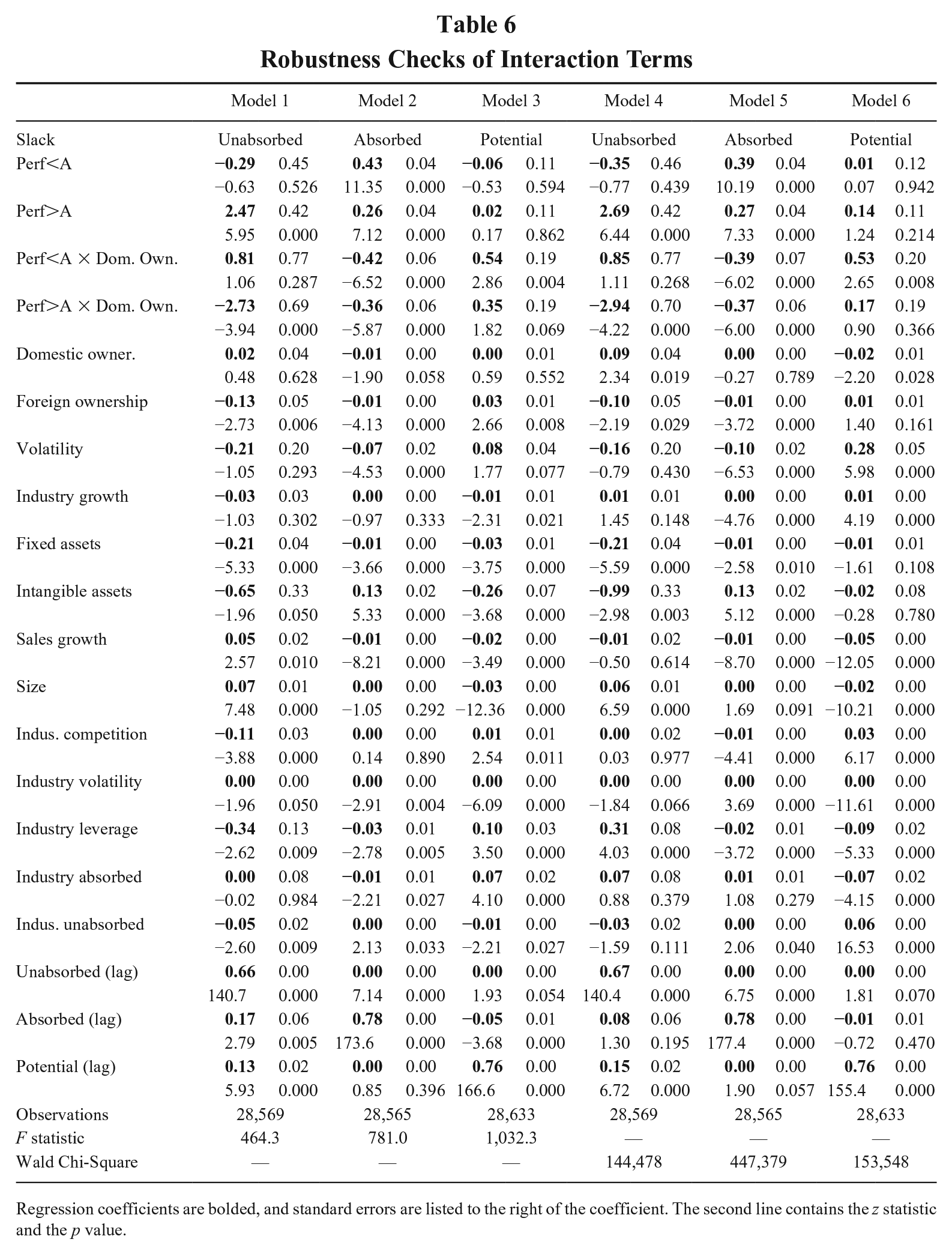

We followed theoretical and empirical precedent (David et al., 2010; O’Brien & David, 2014; Yoshikawa et al., 2005) in defining domestic ownership as ownership by Japanese financial institutions and other Japanese business corporations. However, the government also sometimes owns shares in Japanese corporations, and it could be argued that they are stable, embedded owners. Hence, we verify that the interactions presented in Table 2 hold if we also include government ownership in constructing Domestic Ownership. As Models 1-3 in Table 6 reveal, results are very similar to those of Models 4-6 of Table 2.

Robustness Checks of Interaction Terms

Regression coefficients are bolded, and standard errors are listed to the right of the coefficient. The second line contains the z statistic and the p value.

Our main analysis employs firm fixed effects, but one shortcoming of fixed-effects models is that interaction terms in these models confound between-firm variance with the (more desirable) within-firm variance (Shaver, 2019). Accordingly, we verify that our results are robust to using Allison’s (2005) hybrid model, which can parcel out within- versus between-firm variance (Certo, Withers, & Semadeni, 2017). In Models 4-6 of Table 6, we report the strictly within-firm variance for the interaction models, as given by Allison’s hybrid model (using XTHYBRID in Stata). Once again, the results are very similar to those in Table 2.

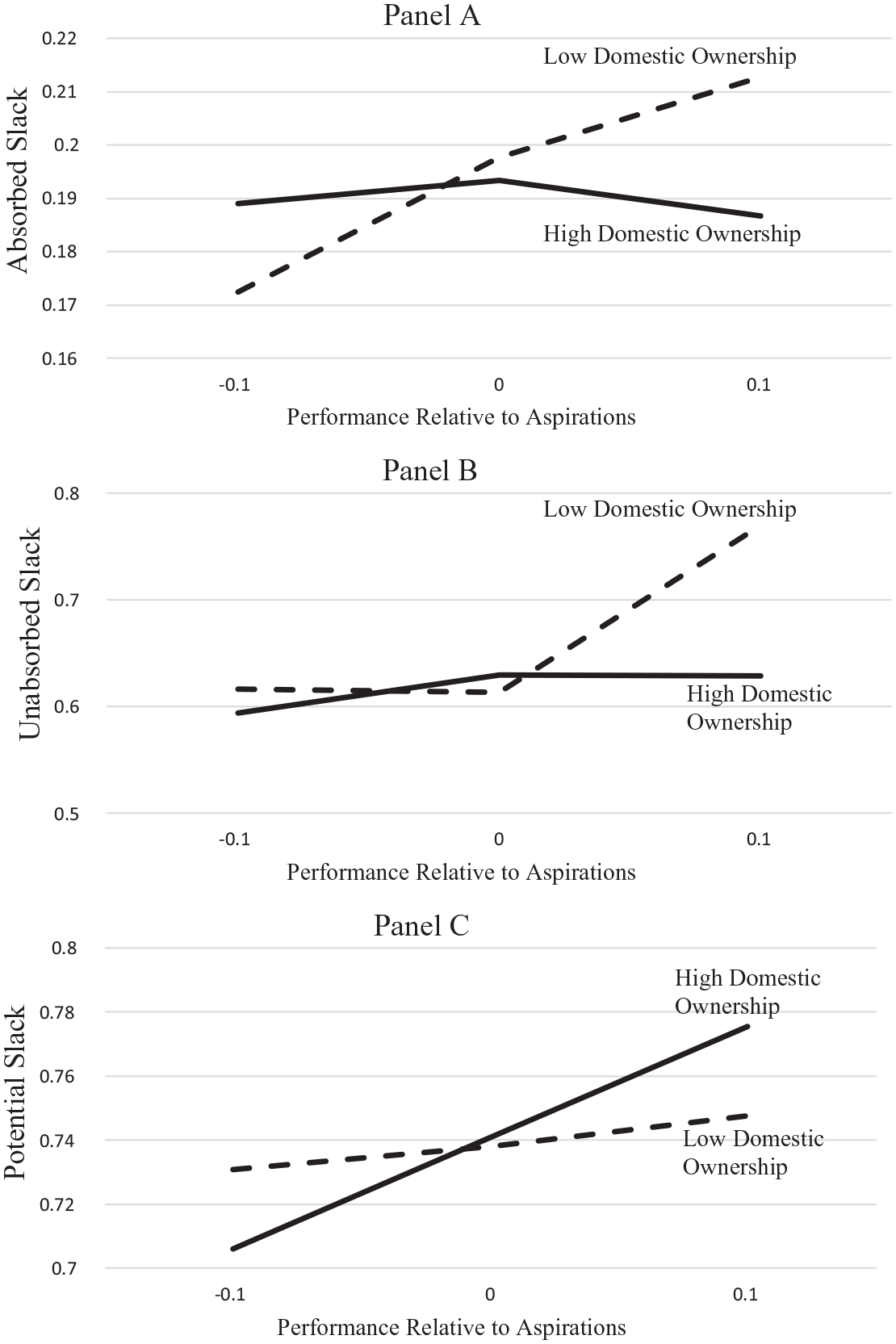

Finally, in order to examine the economic significance of our results, we plot the relationships between domestic ownership, performance relative to aspiration, and the extent of absorbed, unabsorbed slack, and potential slack in Figure 1. Panels A and B illustrate that levels of both absorbed and unabsorbed slack remain relatively stable despite changes in performance relative to aspirations when domestic ownership is high, consistent with our theory. In contrast, when domestic ownership is low, absorbed slack will increase by about 25% as performance goes from poor (lowest one percentile) to strong (top one percentile) and 15% if performance goes from poor (lowest one percentile) to performance equal to aspiration. Similarly, unabsorbed slack increases by about 25% as performance goes from the aspiration level to relatively strong (top one percentile). Finally, Panel C illustrates that potential slack is approximately four times more responsive to changes in performance relative to aspirations when domestic ownership is high than when domestic ownership is low.

Predicted Slack.

Discussion and Conclusion

Slack is a central construct in the strategic management literature, yet the knowledge base regarding the antecedents of slack is largely populated by untested theorizing. Our study highlights the complexity underlying a seemingly simple relationship—while performance may indeed breed slack within certain institutional contexts (Cyert & March, 1963), other contexts may dictate different rules that govern the relationship between performance feedback and slack. There are three major theoretical implications of our study.

First, value capture by stakeholders drives resource availability through arm’s-length contracts and bargaining (Coff, 1999). We extend this reasoning and show that when institutional norms of reciprocity are prevalent, embedded institutional investors influence the slack available to the firm. Second, we develop a conceptual model rooted in the process view advanced by the BTF to explain the extent of slack resources as a function of performance feedback and characteristics of the specific slack resource under consideration. A benefit of examining slack as a dependent variable, while considering characteristics of where slack resources reside, is that slack can be analyzed as a heterogeneous construct in which antecedents may influence each type of slack differently. Third, researchers interested in studying the antecedents to slack resources can employ our development of characteristics of slack resources, such as where the slack resources reside and to whom the benefits/losses accrue, to generate other antecedents that can directly impact these characteristics. For example, extensions of our research could examine how different types of owners, like venture capitalists, suppliers, or family ownership in family-run firms, all have distinct implications for different types of slack.

Our study also has implications for managers and investors. Firms tend to have different types of slack resources—some that are easily available and ready to use; some that need to be recovered, if needed, from employees and business units; and some that reside with external stakeholders, which in some contexts may be more readily available than in other contexts. While there is a general tendency for these resources to diminish when performance declines and increase when performance increases relative to aspirations, managers need to decide which type of resource to employ first when need for these resources arises. Hence, it is important to understand the nature of each type of resource in terms of the costs and benefits of recovery. Our paper helps managers understand the characteristics of these different slack resources and will aid in the managerial assessment of these resources. Furthermore, our paper shows that when the need for resources arises, pressure for recovery of internal resources might be less if firms have relationships that can help them in need. However, long-term sustenance of such relationships also requires reciprocal commitments.

There are also limitations to our study that should be discussed. First, we test our arguments in a specific context, so the results must be generalized carefully. Domestic institutional ownership in contexts outside of Japan cannot always be considered to represent embedded ownership. However, even though embedded relationships may not be as common in other contexts, they do occur in a wide variety of contexts, including the United States (Uzzi, 1996). To the extent one can proxy for influential external stakeholders who are part of an embedded system of firms driven by norms, such as norms of reciprocity and long-term value of the system of stakeholders, we should expect similar results. Second, our results for potential slack are driven by a context in which banks are usually a part of an embedded network of firms. Hence, our findings are most generalizable to other bank-centric economies (e.g., Germany). The extent to which they generalize to other firm-bank relationships will likely vary with the extent to which they develop an embedded versus arm’s-length relationship.

The advantage of using Japanese firms is that it enables us to investigate how embedded ownership influences different forms of slack due to the ways these owners create and extract value. Future research could build on these insights and study how slack resources drive firm adaptability in different contexts as a function of how different influential stakeholders benefit from their relationships with the firm. Inquiry in this direction can open new research questions on firm adaptability driven by the management of different slack resources. For example, one could consider institutional stakeholders who are both owners and suppliers of products to firms’ employees (e.g., insurance companies). In this scenario, the influential owner is extracting value through two mediums—for example, an embedded insurance company that has an ownership stake in the focal firm extracts value by being an owner but also through being able to sell financial services to firm employees. Does this then restrict the ability of the firm to downsize when the need for adaptability due to poor performance arises? Consequently, do these firms then tend to invest less in human capital and more in automation for fear of not being able to adjust human capital costs, thereby leading to lesser increases in human capital slack when performance increases? Finally, while we focused on the types of slack most often discussed in the literature, recent studies have examined other types of slack, like human resource slack (Vanacker et al., 2017). Future research could extend this study by looking at these and other types of slack resources.

In conclusion, our study adds critical nuance to the literature on firm slack resources, as we show that different types of slack resources can vary depending on who benefits from a relationship with the firm (i.e., domestic institutional owners), how they benefit from it (i.e., norms of reciprocity in communitarian institutional systems), and when they benefit (i.e., when performance is above or below aspirations).