Abstract

Executive movement to close rivals can have significant implications for firm competitiveness. While prior research has provided valuable insights into the antecedents of executive search and turnover in general, the theoretical understanding of where executives go when they move remains underdeveloped. We extend research in this area by introducing the concept of destination rivalry, defined as the degree of market commonality and resource similarity between an executive’s departure firm and destination firm. We then develop a theoretical model of key demand-side and supply-side factors associated with an executive’s position in the departure firm that explains movement to a closer versus more distant rivals. We theorize that among executives moving between firms, destination rivalry will be higher when the executive possesses competition-specific human capital (e.g., via core functional experience or corporate or divisional experience at the departure firm), has a larger pay gap to the CEO, and especially when both factors are present. Empirical tests of the theoretical model using a sample of executive movements from S&P 1500 firms to other public companies between 1993 and 2023 are largely consistent with these predictions. Our findings contribute to research on executive mobility and competitive strategy by providing novel insights into factors shaping the degree of rivalry in executive moves.

Over the last several decades, executive movement between firms has become increasingly common (Cappelli & Hamori, 2005; Frydman, 2019). A recent report found that 56 percent of executives plan to leave their current organization within the next two years, with just 17 percent of those departures due to retirement (Gartner, 2025). Coinciding with this trend, a growing literature has emerged to explore the demand-side and supply-side forces underlying individual executive search and mobility. This work underscores the two-sided matching that occurs in labor markets. On the demand side are factors that make executives more or less attractive to hiring firms. Here, research has especially emphasized how general (as opposed to specific) forms of human capital can increase executives’ opportunities in the external labor market (e.g., Cappelli & Hamori, 2014; Forbes & Piercy, 1991; Frydman, 2019; Won & Bidwell, 2023). On the supply side are factors shaping executives’ willingness to remain with or leave their current firms, including compensation and relational dynamics that drive turnover outcomes by influencing commitment or attachment to the organization (e.g., Andrus, Withers, Courtright, & Boivie, 2019; Cappelli & Hamori, 2014). Overall, this work highlights an important interplay between demand-side and supply-side forces in executive search and mobility.

Despite these insights, we know very little about where executives go once they depart a given firm (c.f., Aime, Hill, & Ridge, 2020; Harrison, Boivie, & Withers, 2022). Where a transitioning executive goes is of critical concern for organizations because it can have serious ramifications for the competitiveness of both the firm the executive leaves (the departure firm) and the firm to which the executive moves (the destination firm) (Bermiss & Murmann, 2015; Wezel, Cattani, & Pennings, 2006). This is especially true when executives take positions at close rivals of a departure firm, because their knowledge and experience can shift competitive advantage in favor of the rival destination firm (e.g., Wezel et al., 2006). For instance, when Walmart hired William White from Target to serve as its marketing chief (Boyle, 2020), or when Facebook poached Ian Spalter from YouTube and Kevin Weil from Twitter to redesign and manage Instagram (Shinal, 2017), the implications extended beyond filling leadership gaps, altering the competitive dynamics between these close rivals by affecting the competitive knowledge and experience available to them.

At the same time, executive movements can span the full spectrum of rivalry, from the head-to-head competitor moves illustrated previously to moves between more distant rivals. For example, David Thompson’s move from Symantec to Western Union (King, 2012) or Warren Jenson’s career transitions across Delta Airlines, Amazon, and Electronic Arts (Brannigan & Anders, 1999; Pham, 2002) illustrate how some executives move between firms with little competitive overlap. Despite the importance of this variation, extant theory on executive mobility rarely considers rivalry as a dimension of interfirm movements. The limited work that does address rivalry in these movements, whether for executives or for lower-level employees, has largely emphasized the competitive consequences of rival hiring (e.g., Somaya, Williamson, & Lorinkova, 2008; Wezel et al., 2006). We hence know little of the factors that drive such moves in the first place. Moreover, extant work has tended to conceptualize rivalry as a binary construct, where the departure firm and destination firm are conceptualized as either rivals or nonrivals. Such a coarse conceptualization conflicts with established theory in competitive strategy that views rivalry as the degree of overlap in resources and markets between two firms (Chen, 1996; Chen & Miller, 2012). Thus, not only has the executive mobility literature generally overlooked the central question of where executives go, but it has also constrained a key source of variance in interfirm mobility that has potentially profound competitive consequences, especially when considering the movement of firms’ top decision makers.

To build our understanding of these dynamics and better align executive mobility research with theory in competitive strategy, we introduce the concept of destination rivalry, which we define as the degree of market commonality and resource similarity between a transitioning executive’s departure firm and destination firm (Chen, 1996). We then develop a theoretical model considering demand- and supply-side factors associated with an executive’s position in the departure firm that explain movement to closer or more distant rivals. On the demand side, we emphasize what we refer to as competition-specific human capital, which reflects knowledge of how a firm operates and its key capabilities, markets, and the activities that shape its competitiveness. We argue that such experience, which we proxy via core functional experience and corporate or divisional experience in the departure firm, is particularly attractive to closer rivals because it represents human capital tied to overlapping markets and resources.

On the supply side, we focus on pay disparity in the departure firm, specifically in terms of the gap between the executive’s compensation and that of the CEO. Prior work suggests that a large pay gap relative to the CEO can generate competing motives for turnover in the first place (c.f., Pissaris, Heavey, & Golden, 2017; Ridge, Hill, & Aime, 2017). We argue that once an executive has decided to move on, such a gap increases their willingness to join closer rivals. This is due to both economic mechanisms—given closer rivals are more likely to offer compensation that addresses executives’ relative pay deprivation (e.g., Sturman, Walsh, & Cheramie, 2007)—and psychological processes that undermine attachment to the departure firm and reduce barriers to joining a close competitor (Breitsohl & Ruhle, 2013; Siegel & Hambrick, 2005). Together, these mechanisms suggest that transitioning executives with a larger pay gap to the CEO are more likely to view closer rivals as both materially and symbolically attractive destinations. We also expect these demand- and supply-side factors to have complementary effects in shaping destination rivalry. We test our theoretical model by tracking individual executive movements from S&P 1500 firms to other publicly listed companies between 1993 and 2023, assessing destination rivalry using a novel metric based on indicators of market commonality and resource similarity that apply across industries. Results provide substantial support for our theorizing.

Our research contributes to the literature on executive careers and mobility by explicitly focusing on where transitioning executives go when they depart and incorporating the continuous nature of interfirm rivalry into the conceptualization of that choice. By highlighting a more specialized form of human capital that is especially relevant to closer rivals, our arguments about the role of competition-specific human capital challenge and extend the common view in the literature that general forms of human capital are more valuable in the external labor market (e.g., Cappelli & Hamori, 2014; Forbes & Piercy, 1991; Frydman, 2019). We also extend behavioral research on executive mobility by demonstrating that pay inequality may not only drive executives out of their home firms (Messersmith, Guthrie, Yong-Yeon, & Jeong-Yeon, 2011; Pissaris et al., 2017), but that a larger gap to the CEO may also drive them specifically into the arms of closer rivals. Overall, some transitioning executives will be poached by close rivals, while others will move to more distant or nonrivals, and these decisions can have important consequences for both the departure firm and the destination firm (Bermiss & Murmann, 2015; Wezel et al., 2006). Our theoretical model illuminates the factors that push and pull transitioning executives and their destination firms one way or the other.

Theoretical Background

Competitive Consequences of Rival Moves

Executive movement between firms has been increasing over time (Cappelli & Hamori, 2005; Frydman, 2019), with no signs of slowing down (Gartner, 2025). This trend has important implications for firm competitiveness and survival, given executives’ central positions as strategic leaders and their understanding and involvement in their firms’ strategies and high-order routines (Bermiss & Murmann, 2015; Wezel et al., 2006)—knowledge that they carry with them when moving. This points to the importance of organizations shifting their focus from simply trying to retain key executives to considering how to limit the negative implications of interfirm moves when executives do decide to move on. In this regard, arguably one of the most theoretically and practically important attributes of a departing executive’s destination is the degree of rivalry between the departure firm and the destination firm.

Little research to date has explored where executives go when moving between firms (c.f., Aime et al., 2020; Harrison et al., 2022), let alone the degree of rivalry in those choices. But one early study in this area does point to the significant competitive implications of top decision makers moving to close rivals. In their study of Dutch accounting firms, Wezel et al. (2006) identified rivals based on discrete geographic markets and found that the risk of firm dissolution is greater when executives depart from a focal firm and take a position at another firm in the same province rather than a firm in a different province. Extending these findings, some work in the broader mobility literature has also explored related dynamics for lower-level employees, finding similar outcomes. For example, examining interfirm mobility of patent attorneys, Somaya et al. (2008) found that losing employees to rival firms, defined as law firms with links to the same client, was more detrimental to the focal firm than losing an employee to the client itself. In general, these effects are theorized to stem from the transfer of human and social capital from one firm to another, which has the potential to shift competitive advantage in favor of the rival destination firm.

Extending Theory on Executive Rival Moves

Despite the importance of rival moves to firms, little work has explored their antecedents. Instead, research has tended to focus on the competitive consequences of rival moves (Somaya et al., 2008; Wezel et al., 2006), on characteristics of departure and destination firms other than rivalry (Harrison et al., 2022), or on factors influencing broader executive search and turnover without considering characteristics of the destination firm at all (e.g., Andrus et al., 2019; Cappelli & Hamori, 2014; Won & Bidwell, 2023). Moreover, the little work that has explored the competitive implications of rival moves has tended to conceptualize and measure rivalry dichotomously. But such a coarse conceptualization is inconsistent with established theory on interfirm rivalry within competitive strategy.

A central tenet of competitive strategy research is that firms often compete in multiple markets using different strategies based on their resource endowments, such that the degree of rivalry between two firms can vary depending on the level of overlap in their resources and markets (Chen, 1996; Chen & Miller, 2012). Relative to discrete categorizations of rivalry, this view of rivalry as a continuous construct provides a stronger basis for understanding firms’ awareness, motivation, and capability to respond to one another’s strategic actions, which in turn facilitates more nuanced analyses of the competitive dynamics a pair of firms might experience within and across markets (Chen, Su, & Tsai, 2007). In our context, this further suggests that accounting for the degree of rivalry between a departure firm and destination firm can enrich our understanding of the factors influencing executive interfirm mobility.

Altogether, the foregoing discussion underscores the need for both a more refined conceptualization of rival moves—as a matter of degree rather than a discrete categorization—and additional theory focused on understanding what drives movement to closer or more distant rivals in the first place. We seek to address these issues in this study. We begin by formalizing a definition of destination rivalry that aligns more directly with theory from competitive strategy. Then, we develop a theoretical model outlining key demand-side and supply-side factors behind executive movement to closer or more distant rivals.

Theory and Hypotheses

Conceptualizing Destination Rivalry

We conceptualize destination rivalry as encompassing two central dimensions of competition: market commonality and resource similarity (Chen, 1996). The concept of market commonality is based on the understanding that firms compete in imperfectly overlapping markets, potentially competing with one group of firms for one segment of customers and a different group of firms for a different segment of customers (Yu & Cannella, 2013). The more points of competition two firms have in common in a multimarket setting, the greater the potential for firms to engage in intense rivalry, particularly in response to each other’s competitive moves (Young, Smith, Grimm, & Simon, 2000; Yu & Cannella, 2007). Consistent with Chen (1996: 106), we define market commonality as “the degree of presence that a competitor manifests in the markets it overlaps with the focal firm.”

The concept of resource similarity is based on the understanding that resources are heterogeneously distributed across firms and affect their strategic repertoires, such that a firm’s competitive position and advantage are determined by its unique resource endowments (Barney, 1991; Wernerfelt, 1984). To the extent that two firms share common resources, they are likely to view each other as stronger rivals (Chen, 1996). Not only does resource similarity with a competitor limit the uniqueness of a firm’s position in a given market, but it also increases the competitor’s ability to effectively respond to attacks by the focal firm (Chen et al., 2007). Resource similarity may be particularly important when considering executive interfirm mobility because executives familiarize themselves with resources over time, and more similar resources at a destination firm offer more opportunities for transitioning executives to leverage their expertise in their new roles. Again, consistent with Chen (1996: 107), we define resource similarity as “the extent to which a given competitor possesses strategic endowments comparable, in terms of both type and amount, to those of the focal firm.”

Taken together, we formally define destination rivalry as the degree of both market commonality and resource similarity between a transitioning executive’s departure firm and destination firm. Conceptualized this way, destination rivalry reflects a continuous construct where closer rivals are those with higher levels of market commonality and resource similarity with the departure firm, while more distant or nonrivals are those with few or no overlapping markets and little resource similarity with the departure firm. We use this definition to explain the mechanisms behind executive moves toward closer or more distant rivals.

Demand-Side and Supply-Side Factors Predicting Destination Rivalry

Extending prior literature on two-sided matching in executive labor markets, we argue that there will be demand- and supply-side factors associated with an executive’s position in the departure firm that explain movement to closer or more distant rivals. In a labor market, “demand side” refers to employers’ demand for labor, and “supply side” refers to employees’ willingness to supply their labor. On the demand side, potential employers value executives’ human capital to the extent that it can be translated into a competitive advantage. On the supply side, executives themselves are motivated to seek out firms where their human capital will be most valued and rewarded. Consistent with this view, we describe destination rivalry as a function of both executives’ human capital that is relevant to closer versus more distant rivals, as well as pay disparity in the departure firm, which limits attachment and motivates executives to move to closer rivals in pursuit of financial redress.

Competition-specific human capital and demand-side dynamics

External labor market demand for executives is generally dependent on their human capital, or the knowledge, skills, and experiences that they possess. Human capital can reflect all manner of experiences, with some experiences pertaining more to gaining a competitive advantage over rivals and other experiences pertaining more to general administrative tasks or managing internal organizational challenges. While all types of human capital have value, the more an executive understands about the activities central to a firm’s competitive advantage, the greater should be the demand-side interest in that executive among the firm’s closer rivals.

We define competition-specific human capital as knowledge and experience associated with a firm’s core capabilities, competitive markets, value-creating activities, and operations that are directly relevant to its competitiveness. Executives can develop this type of human capital through multiple pathways. A primary pathway consists of building experience in the core functional roles that shape a firm’s ability to compete at the business level (Menz, 2011; Porter, 1985). For instance, a marketing executive with expertise in price optimization and distribution channel strategy, or a research and development (R&D) leader with deep knowledge of product development cycles in a specific technological segment, will possess insights that map closely onto a firms’ unique capabilities, value-creating activities, and how they position themselves in competitive markets. Executives can also develop this knowledge through more general managerial roles, so long as they touch the competitive space. For instance, experience in corporate-level management roles (e.g., president, executive vice president) can foster a detailed understanding of the firm’s portfolio and expose them to a wide array of the firm’s operations, suppliers, and resource flows across its product markets. Or at lower levels, leading a division or business unit can promote a deep understanding of how a firm positions itself in specific competitive markets and how it tends to respond to competitors’ actions. In some cases, competition-specific human capital may also encompass sensitive information, such as knowledge of trade secrets or in-progress patent applications, although legal and institutional restrictions will generally limit the transferability of these particular types of knowledge (Marx, Strumsky, & Fleming, 2009; Starr, Prescott, & Bishara, 2021).

Competition-specific human capital is distinct from both firm-specific and general human capital. Firm-specific capital is tightly embedded in the routines and culture of a single firm and is therefore not transferable (Becker, 1964; Hashimoto, 1981). For example, familiarity with the firm’s internal politics or understanding how to work within its internal operating procedures can improve internal efficiencies, but such knowledge holds little value outside of the focal firm. At the other extreme, general human capital is broadly applicable across firms and industries but less directly tied to competition in a given product market (Becker, 1964; Castanias & Helfat, 1991). For instance, an accounting or finance officer may develop a deep understanding of financial structure and risk mitigation, or a human resource officer may develop capabilities in recruiting or designing incentive systems. While these are valuable skills, they tend to be less tightly linked to product-market competition or a firms’ competitive advantage. In contrast, competition-specific human capital combines elements of both specificity and transferability. It is sufficiently detailed and contextualized to provide insight into how a particular firm competes, yet also transferable to other firms operating in the same competitive markets. Thus, it is both valuable to a firm’s direct competitors and relatively rare in the broader labor market.

Because competition-specific human capital provides insights that are both highly relevant and directly applicable to direct competitors, executives who possess it are especially attractive to closer rivals of the departure firm. When market commonality is high between firms, a transitioning executive’s competition-specific human capital is directly relevant to the destination firm’s competitive challenges. For example, their understanding of pricing dynamics, customer segmentation approaches, or technology development priorities provides immediately applicable insights for firms operating in the same competitive arena. When resource similarity is high, the destination firm can effectively deploy this experience within its comparable resource base and competitive environment. Moreover, firms with high market commonality and resource similarity monitor one another more intensively and have greater capacity to extract value from competitive intelligence (Chen & Miller, 2012). Hiring an executive with competition-specific human capital thus provides dual sources of value creation. Defensively, it provides access to a nuanced understanding of a rival’s routines, priorities, and likely strategic responses. Offensively, it provides access to proven capabilities that can be deployed within the destination firm’s similar strategic context. Taken together, this logic suggests that executives with competition-specific human capital will not move randomly across the competitive landscape but will instead be disproportionately drawn toward firms whose rivalry with their former employer is most pronounced. In this way, competition-specific human capital represents a strong demand-side factor pulling transitioning executives toward closer rivals of the departure firm.

Hypothesis 1: Among executives moving between firms, the possession of competition-specific human capital is positively related to destination rivalry.

Pay gap relative to the CEO and supply-side dynamics

On the supply side of the two-sided matching process, executives moving between firms vary in the extent to which they are motivated and willing to join closer rivals relative to more distant or nonrivals. We argue that a primary supply-side factor shaping this willingness is the level of pay disparity they experience at the departure firm, specifically compared to the CEO. While a larger pay gap to the CEO can create conflicting incentives for turnover in general, we suggest that its motivational implications become clearer once an executive has decided to move on. At that point, executives with larger pay gaps to the CEO are more likely to join closer rivals.

Executives attend closely to relative pay comparisons and especially to how their compensation compares to that of the CEO. Prior research highlights the CEO as a uniquely salient reference point in the executive hierarchy (Connelly, Tihanyi, Crook, & Gangloff, 2013; Main, O’Reilly, & Wade, 1993; Wade, O’Reilly, & Pollock, 2006). Given that the CEO represents the apex of organizational status and success, even when social comparisons occur laterally among top executives, CEO compensation anchors these comparisons by defining the upper bound of rewards within the firm (Fredrickson, Davis-Blake, & Sanders, 2010). This makes executives’ pay relative to the CEO particularly informative for executives’ assessments of their standing and future prospects inside the firm (Connelly et al., 2013; Main et al., 1993). Yet prior research offers competing perspectives on how pay disparity with the CEO might affect the likelihood of executive turnover. From the perspective of tournament theory, a large pay gap can create tournament incentives that might encourage executives to remain with the firm and exert effort in pursuit of the CEO position and its associated rewards (Ridge et al., 2017). Alternatively, from the perspective of social comparison theory, these same dynamics can generate resentment and disharmony, motivating executives to seek opportunities elsewhere (Pissaris et al., 2017). Among executives who do decide to move, however, obtaining the tournament “prize” is no longer a relevant motivation, and what remains are supply-side considerations that generally increase executives’ openness to joining closer rivals of the departure firm.

The logic for this prediction rests on both economic and psychological mechanisms. Economically, executives who leave firms where they experienced greater pay disparity are naturally inclined to seek out new employers that correct unfavorable social comparisons (Aime et al., 2020). Given that closer rivals benefit more from an executive’s knowledge and experience (Campbell, Ganco, Franco, & Agarwal, 2012), they are more likely to offer higher compensation that would be especially attractive to such executives. 1 The potential for a significant pay jump increases supply-side interest in rival firms, and greater pay disparity to the CEO offers a greater opportunity for such a correction. In contrast, these processes will be less salient for executives whose compensation is more comparable to that of the CEO. For these executives, the need to seek out financial redress for pay disparities in the departure firm will be limited, so the supply-side pull of movement to a closer rival will not be as strong.

Psychologically, a larger pay gap to the CEO can also generate perceived inequity, dissatisfaction, and “resentment towards the [CEO] and possibly the firm itself” (Siegel & Hambrick, 2005: 262; see also Boivie, Bednar, & Barker, 2015). These reactions may be especially salient for executives, who attach high importance to status and achievement signals (Finkelstein, Hambrick, & Cannella, 2009). Perceived inequity and its associated negative emotions undermine commitment and organizational attachment (Colquitt, Conlon, Wesson, Porter, & Ng, 2001), weakening any residual loyalty that might otherwise constrain executives from joining direct competitors (c.f., Breitsohl & Ruhle, 2013). This psychological dynamic contrasts with that of executives whose pay is closer to that of the CEO, who are more likely to retain psychological attachment to the departure firm and avoid moves that risk alienating themselves from their former colleagues, such as joining a close rival. For executives facing a larger pay gap to the CEO, though, the combination of equity-driven discontent and the prospect of financial redress creates a powerful motivation to seek opportunities with closer rivals, which represent both symbolic validation of their worth and material compensation for past inequities.

Hypothesis 2: Among executives moving between firms, a larger pay gap to the CEO is positively related to destination rivalry.

The Complementary Effects of Supply- and Demand-Side Factors

Like any market, the market for executive labor is fundamentally shaped by two-sided matching (Bidwell & Mollick, 2015; Logan, 1996). Rival firms assess whether an executive’s knowledge and skills are valuable to their own competitive context, while executives decide whether the opportunities available are attractive enough to pursue. Thus, explaining transitioning executives’ choice of destination requires attention not only to each factor individually but also to how they reinforce one another. Moves to closer rivals are most likely when executives are simultaneously attractive and attracted to rivals.

In determining transitioning executives’ ultimate destination rivalry, competition-specific human capital and the pay gap to the CEO play complementary roles. Competition-specific human capital increases the likelihood that competing firms view an executive as a valuable hire, given the direct applicability of their knowledge and skills to overlapping markets and resources (Castanias & Helfat, 1991; Sturman et al., 2007). Yet attractiveness to rivals does not guarantee movement to those firms. Even executives who are sought after may hesitate to join close competitors if they perceive reputational risks or retain residual attachment to their former employer. Conversely, a larger pay gap to the CEO increases executives’ willingness to leave by creating financial incentives and symbolic dissatisfaction (Pissaris et al., 2017; Siegel & Hambrick, 2005). Yet motivation alone is insufficient; underpaid executives may want external validation, but unless they possess the knowledge and capabilities that rivals prize, their preferences may not translate into offers from those firms.

When these forces coincide, however, they reinforce one another. Competition-specific human capital creates opportunities by increasing rivals’ interest in recruiting an executive, while a larger pay gap to the CEO amplifies the executive’s willingness to act on such opportunities. Executives who combine both characteristics (valued human capital and strong motivation) are therefore in the best position to move closer to rivals. In this way, demand-side and supply-side factors do not merely operate in parallel but interact to create the conditions under which movement to closer rivals is most likely. Thus, we expect a positive interaction between competition-specific human capital and pay disparity to the CEO on the degree of rivalry between the departure firm and the destination firm.

Hypothesis 3: Among executives moving between firms, destination rivalry is highest for those with both competition-specific human capital and a higher pay gap to the CEO.

Methods

Sample and Data Collection

We test our hypotheses using a dataset of top executive movements from S&P 1500 firms to other publicly listed companies in the United States between 1993 and 2023. Data came primarily from Execucomp, BoardEx, and Compustat, with supplemental data taken from executive biographies sourced from various websites and company filings from the SEC’s EDGAR system. To identify executive movements, we first coded all departures for the executives in the initial sampling frame based on the date the executive left the focal firm. This information came from a combination of the leftco variable in Execucomp (when available) and the end date associated with an executive’s position from employment histories in BoardEx (Andrus et al., 2019). We coded 13,748 executive departures in our sampling frame using this approach. We then assessed movements as instances in which the departing executive took on an executive position at another publicly listed firm within one year of the departure date. We identified 3,205 such instances. 2 It was necessary to limit our sample to public firms to create our measure of destination rivalry, detailed later. Our final dataset consists of these 3,205 movements, which represent 2,969 unique executives moving from 1,506 distinct S&P 1500 firms (the departure firms) to 2,047 other public firms (the destination firms) between 1993 and 2023, inclusive.

Measuring Destination Rivalry

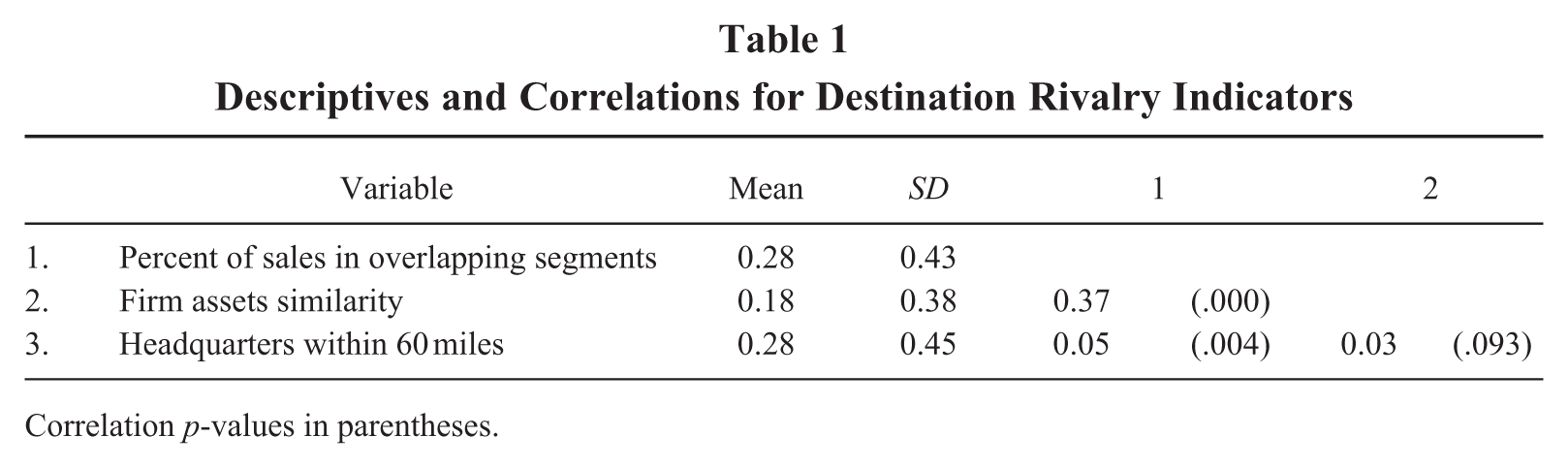

Research attempting to measure rivalry has tended to focus on single indicators (e.g., product similarity, Hoberg & Phillips, 2016) or to examine dyadic competition within very specialized industries—for example, Scottish knitwear (Porac, Thomas, Wilson, Paton, & Kanfer, 1995), California commuter airlines (Baum & Korn, 1996), and Dutch accounting firms (Wezel et al., 2006). A benefit of the latter approach is that it allows scholars to narrow their sample to a more manageable set of firms to identify indicators of interfirm rivalry (e.g., self-reported rivalry from questionnaires, overlapping routes for airlines, etc.). However, these indicators tend to be idiosyncratic to the industry and therefore not relevant to a multi-industry study such as ours. Moreover, measures based on a single indicator fail to account for both market commonality and resource similarity between firms, which are critical to the conceptualization of rivalry in the competitive strategy literature (Chen, 1996). Indeed, operationalizing both features requires an assessment of multiple dimensions, including the importance of different competitive markets to multidivisional firms, resource endowments, and access to labor markets (Baum & Mezias, 1992; Chen, 1996; Chen et al., 2007; Yu & Cannella, 2007). To address these issues, we create a novel measure of interfirm rivalry based on factors that are conceptually similar to those used in past work and reflect dimensions of resource similarity and market commonality that apply across industries. These include firm sales in overlapping business segments, similarity in firm assets, and geographic proximity of corporate headquarters.

Sales in overlapping segments

Our primary indicator of market commonality reflects the degree of overlap in the competitive markets shared between the departure firm and destination firm. Data on firms’ competitive markets come from Compustat’s Segments dataset and include each firm’s sales across each specific industry segment in which they operate, at the four-digit SIC level. When assessing competitive market overlap, we specifically focus on the percentage of the departure firm’s total sales that come from segments in which the destination firm also operates. This allows us to assess the importance of the overlapping markets to the departure firm. Using the departure firm’s segments as the basis for comparison also means that this component reflects the level of rivalry from the departure firm’s perspective rather than the destination firm’s perspective. 3 This is important because perceptions of interfirm rivalry can be asymmetric (Chen, 1996; Chen et al., 2007), and considering the departure firm’s perspective aligns with our initial motivation in the introduction regarding the potential negative implications to the departure firm of losing an executive to a close rival. 4

Firm assets similarity

Corporate assets are a strong indicator of firms’ resource endowments (Josefy, Kuban, Ireland, & Hitt, 2015). Firms with similar asset values operating in the same general industry category are especially likely to hold similar resources, both in terms of amount and type (e.g., similar plant, equipment, supporting technologies, supply chain capabilities, etc.). To capture both aspects of resource similarity, we compare the reported asset values of the departure and destination firms when they operate in the same primary industry group (i.e., two-digit SIC). We begin by calculating the natural log of total assets for each firm each year. We then create a measure capturing its quartile rank on this value within its broader primary industry group (1 = top quartile, 2 = second quartile, 3 = third quartile, and 4 = bottom quartile), using all firms included in Compustat during the year. Our measure of firm assets similarity takes a value of 1 if the departure firm and destination firm are within the same industry quartile of firm assets, and 0 if the firms are in the same industry group but in different quartiles or are in different industry groups altogether.

Headquarters’ geographic overlap

Geographic proximity affects interfirm rivalry by increasing managers’ awareness of competitors and intensifying local firms’ competition over customers, labor, and other resources (Chen, 1996; Zhao, 2018). This is true even for large, geography-spanning firms like those in our sample (Yu & Cannella, 2007). Moreover, because top executives tend to be located around firm headquarters, competitors with headquarters in close proximity will be especially salient to one another for poaching executive talent and will be in a better position to do so. Consistent with work on local market density and executive labor markets (e.g., Zhao, 2018), we assess geographic overlap by identifying whether the departure firm’s and destination firm’s headquarters are located within 60 miles of each other. The variable takes the value of 1 when the firms are located within this distance, and 0 otherwise.

Rivalry index

Our final measure of destination rivalry is calculated as the summed standardized values of the three components. 5 We used the sum of standardized values because the overall scale should reflect a formative measure, where each component contributes additively to the overall level of rivalry between firms (see DiStefano, Zhu, & Mindrila, 2009). As demonstrated in Table 1, correlations among the three components are all positive, providing evidence that the measures covary in the data. At the same time, the correlations are not so high as to suggest a reflective measure, where each component is driven by the latent construct. Rather, they reflect distinct dimensions that contribute uniquely and additively to the construct (Coltman, Devinney, Midgley, & Venaik, 2008). Analysis of variance inflation factors (VIFs) provides further support for the formative measure. VIFs for the three factors range from 1.00 to 1.16, with an average VIF of 1.11, suggesting they are not collinear.

Descriptives and Correlations for Destination Rivalry Indicators

Correlation p-values in parentheses.

Competition-Specific Human Capital

As described in our theorizing, competition-specific human capital reflects executives’ experience and knowledge regarding a firm’s core capabilities, competitive markets, value-creating activities, and overall operations. To capture this construct empirically, we coded executives’ employment histories from Execucomp and BoardEx, which provide detailed information on executives’ titles and roles held across their careers. From these data, we derived two separate measures of competition-specific human capital—core functional experience and corporate or division experience in the departure firm.

Executives are more likely to possess competition-specific knowledge when they have experience in core functional areas directly tied to the firm’s value chain and competitive advantage. Following Hambrick and Mason (1984), we define these core areas as the firm’s throughput and output functions, including operations and engineering, marketing and sales, and R&D or business development. Experience in these core areas contrasts with experience in peripheral functions such as finance, accounting, or human resources that may also be of general value in the labor market but are less directly tied to competition in a firm’s product markets. Thus, the variable core functional experience takes the value 1 when an executive’s dominant experience was in one of the throughput or output functions, and 0 when the dominant experience was in peripheral functions (e.g., finance or accounting, human resources, law or investor relations, information systems) or in general management roles not tied to a specific function. 6

Executives may also develop competition-specific human capital in roles that provide holistic knowledge of how the firm operates and competes in particular markets. This can come from corporate or division experience in the departure firm, which exposes executives to key supplier relationships, resource allocation decisions, and competitive positioning across markets. Thus, we code corporate or division experience when their primary experience in the departure firm involved corporate management (e.g., president, executive vice president, senior vice president) or leading specific divisions or business units (e.g., division president or vice president, group president or vice president). The variable takes the value 1 when the executive’s dominant experience in the departure firm was in such roles, and 0 when it was primarily in a functional area or in broad administrative positions not directly linked to markets or business units (e.g., chief administrative officer, chief governance officer, secretary).

Pay Gap to the CEO

Our theory also emphasizes pay relative to the CEO as a key supply-side factor driving departing executives toward closer rivals. Pay is based on the TDC1 field in Execucomp, which reflects executives’ total annual compensation, comprising salary, bonuses, other annual compensation, restricted stock grants, and long-term incentives. After capturing this for each CEO and executive, we calculated pay gap to CEO as the difference between CEO’s total pay and that of the focal executive (Gnyawali, Offstein, & Lau, 2008), in millions of U.S. dollars. Thus, higher values indicate a larger pay gap, while smaller values indicate a smaller pay gap or instances where the executive is paid more comparably to the CEO. To reduce the influence of outliers, we winsorized this variable at the 1-percent level for both high and low values.

Control Variables

We control for factors at multiple levels that may be related to our focal relationships. At the state level, we control for the adoption or rejection of the Inevitable Disclosure Doctrine (IDD) in employment law (Flammer & Kacperczyk, 2019; Na, 2020). The IDD restricts employees from joining competitors when such moves would inevitably lead to disclosure of trade secrets, making it a strong indicator of the enforceability of noncompete provisions that could constrain executive movement to close rivals. We code State IDD as 1 in years when the doctrine was adopted and active in the departure firm’s headquarters state, and 0 otherwise, based on state-level court rulings that were staggered across the sample period.

Industry norms related to rival poaching may also be more common in some industries than others. Thus, we control for industry poaching, which equals the average level of rivalry between departure firms and destination firms for executive moves within the departure firm’s primary industry from t − 3 to t − 1, where industries are based on four-digit SIC codes. 7 We also control for local labor market density as the number of other public firms within a 60-mile radius of the departure firm (in hundreds) (Andrus, Lee, & Hom, 2024; Yonker, 2017; Zhao, 2018).

At the firm level, we control for departure firm profitability, size, and market leadership, as each can shape executives’ opportunities in the external labor market (Boivie, Graffin, & Pollock, 2012; Lange, Boivie, & Westphal, 2015). Firm profitability is measured as industry-adjusted net income in t − 1 (in millions of U.S. dollars). To limit overlap with the asset-based component of our rivalry index, we control for firm size using the log of employees. Market leaders are identified as the top four in market share within their four-digit SIC industry.

At the individual level, we control for executive age, whether the executive is female, their tenure in the departure firm, whether they held a board position in the departure firm, and the number of shares owned by the executive (in thousands). To account for scaling in shares owned, we include the firms’ total common shares outstanding (in millions). We also control for executives’ network size to account for informal social factors that may influence interfirm mobility. Network size reflects the number of external ties an executive has to other executives and directors in the sample, based on overlapping tenure in prior executive roles (Harrison et al., 2022). In addition, we control for whether the executive was appointed CEO at the destination firm, as CEO appointments may reflect distinct incentives shaping destination choices.

Finally, we control for additional pay comparisons that may shape executives’ mobility decisions. While our primary measure captures vertical pay comparisons with the CEO, executives may also engage in horizontal comparisons internally with other top management team (TMT) members and externally with industry peers (Ridge et al., 2017). We account for internal comparisons using pay disparity to the TMT, calculated as the difference between the focal executive’s pay and the average pay of other non-CEO executives in a given year. External comparisons are captured using pay disparity to industry peers, calculated as the difference between the focal executive’s compensation and the average compensation of executives at the same hierarchical level within the same four-digit SIC industry during the year. Hierarchical levels follow Hambrick, Humphrey, and Gupta (2015). For all pay measures, higher values indicate greater disparity, while lower or negative values indicate smaller gaps or cases in which the executive is paid above peers. All pay variables are winsorized at the 1 percent level to mitigate outliers.

Analysis Strategy

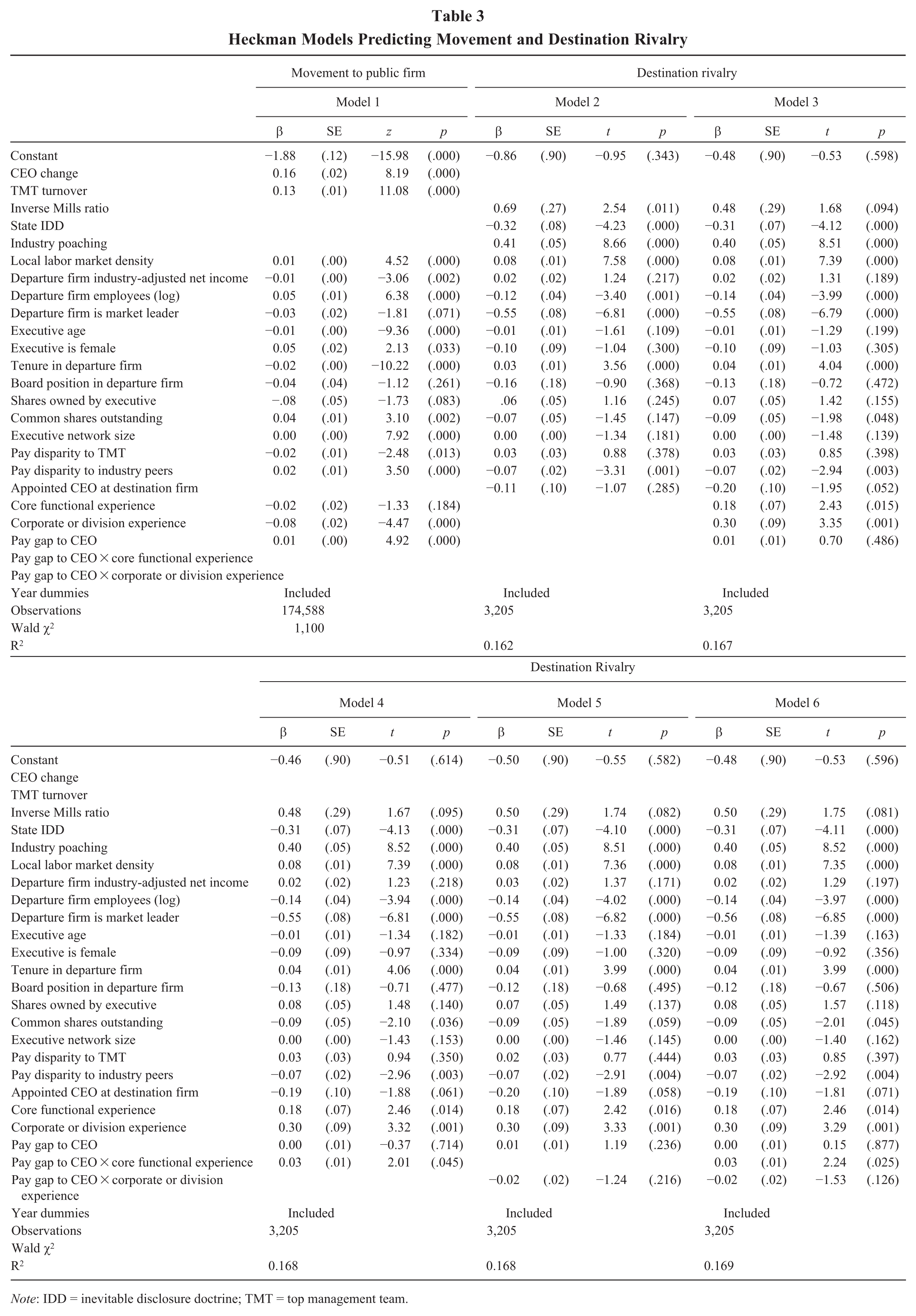

We test our hypotheses using two-stage Heckman (1979) models. This approach helps to address potential sample-induced endogeneity (Bascle, 2008; Certo, Busenbark, Woo, & Semadeni, 2016), which may stem from our inability to calculate destination rivalry for all transitioning executives and the fact that executive movement is a nonrandom event. In the first stage of the Heckman analysis, we estimate a probit model predicting executive movement to any public company. Our exclusion criteria in the first stage model are CEO change, which reflects whether there was a CEO succession event in the departure firm during the year, and TMT turnover, which reflects the number of other TMT members who left the company during the year, excluding the focal executive and the CEO. These are theoretically relevant exclusion criteria because they each reflect relational shocks that should influence individual executive turnover or movement (Andrus et al., 2019), but not necessarily the degree of rivalry between the departure firm and the destination firm. Empirical analyses confirm this assumption and further demonstrate the appropriateness of CEO change and TMT turnover as exclusion criteria. 8 Based on the first-stage model, we then calculate the inverse Mills ratio to include in second-stage models predicting destination rivalry. We estimate second-stage models using ordinary least squares (OLS) regression, including robust standard errors clustered on the firm. All models include year fixed effects. We use Stata 19 for all analyses.

Results

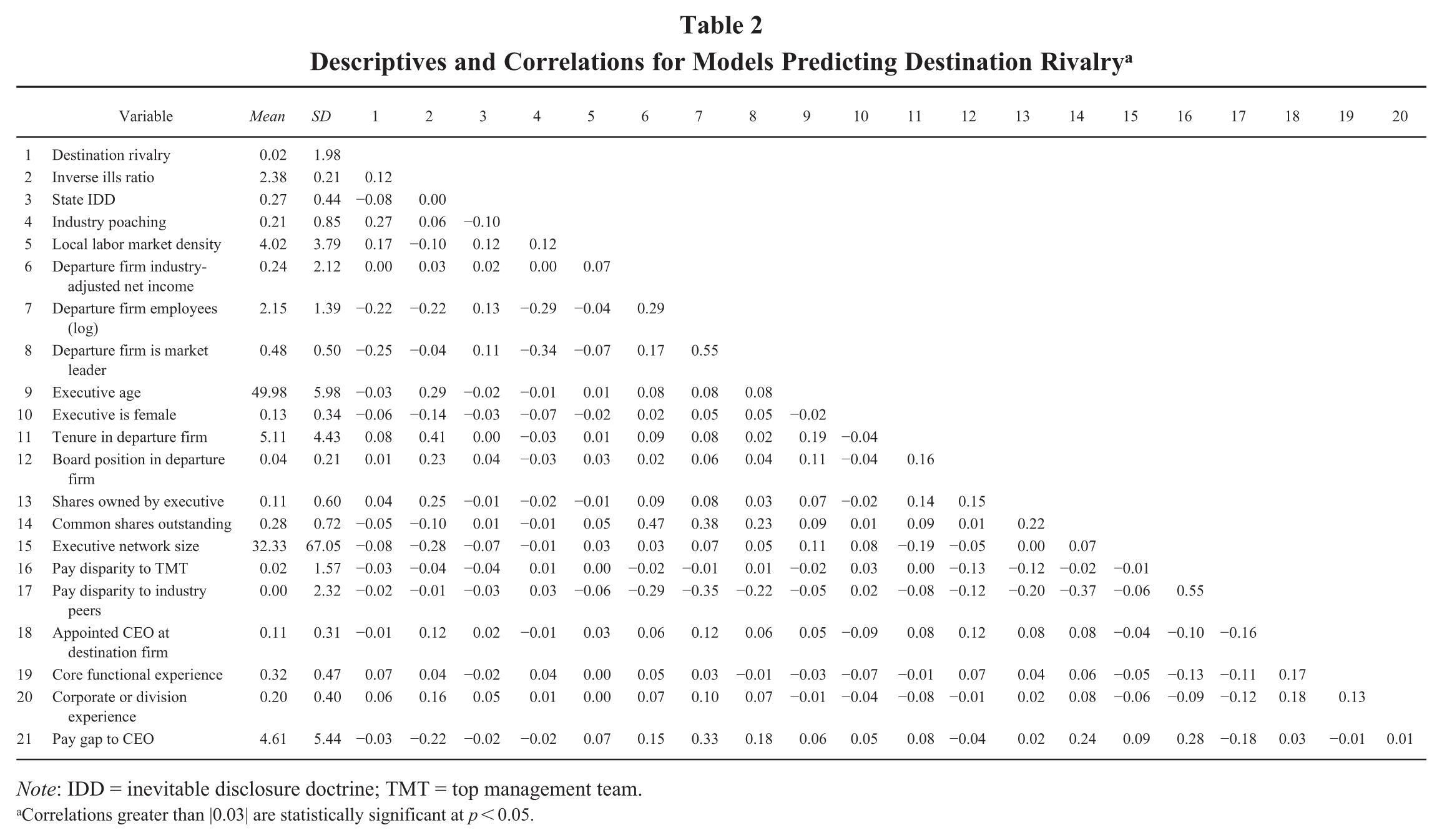

Table 2 presents summary statistics and correlations for our sample of transitioning executives. Correlations among study variables and controls are generally low, with an average correlation below |.08|, suggestive that multicollinearity is not driving our results. The highest correlation among study variables and controls is .33 between the pay gap to the CEO and the number of employees. Among control variables, number of employees is also highly correlated with market leadership (r = .55), common shares outstanding (r = .38), and pay disparity to industry peers (r = .35). Strong positive correlations are expected in each case, given larger firms are more likely to be market leaders, issue more shares, have larger pay dispersion among non-CEO executives, and pay the CEO more compared to other executives. Reestimating models excluding highly correlated variables does not substantively change our results, suggesting that these relatively higher correlations do not bias the estimates. VIF diagnostics reinforce these conclusions. In the full model, the average VIF is 1.44, and the high is 2.66, each well below the conventional threshold of 10 used to indicate multicollinearity (Kennedy, 2008). Overall, these values suggest that multicollinearity is unlikely to be a major concern in our analyses.

Descriptives and Correlations for Models Predicting Destination Rivalry a

Note: IDD = inevitable disclosure doctrine; TMT = top management team.

Correlations greater than |0.03| are statistically significant at p < 0.05.

Table 3 reports our primary results. Model 1 is the first-stage model predicting movement to another public company (i.e., sample inclusion), while Models 2 through 6 present results related to our hypotheses on destination rivalry. Hypothesis 1 predicts that, among transitioning executives, competition-specific human capital will positively relate to the degree of rivalry between the departure firm and the destination firm. In Model 3, we find positive coefficients for both core functional experience (β = 0.18, p = .015) and corporate or division experience (β = 0.30, p = .001). We interpret these effects by comparing estimated values of destination rivalry for transitioning executives with and without primary experience in these areas. To get a better sense of the size of the effects, we report effect sizes in terms of standard deviation (SD) changes in destination rivalry. Among executives moving between firms, destination rivalry is .09 SD higher for executives with core functional experience and .15 SD higher for executives with corporate or division experience, as compared to those without primary experience in these roles. These results are consistent with Hypothesis 1.

Heckman Models Predicting Movement and Destination Rivalry

Note: IDD = inevitable disclosure doctrine; TMT = top management team.

Hypothesis 2 proposes that a larger pay gap to the CEO will be positively related to destination rivalry. As part of our theorizing, we also outline prior work that has suggested that high pay gaps to the CEO can have competing implications for movement in the first place. Results from the first stage (Model 1) show that a larger pay gap is positively related to movement to another public company (β = 0.01, p = .000). Thus, within our sample, results seem to support a social comparisons view of vertical pay disparity (where large gaps create discontent that drives executives to leave), rather than a tournament theory view (where large gaps motivate executives to remain and compete for the top prize). However, Model 3 shows no statistically significant main effect of the pay gap to the CEO on destination rivalry. This indicates that higher pay gaps to the CEO are not, on their own, meaningfully related to destination rivalry.

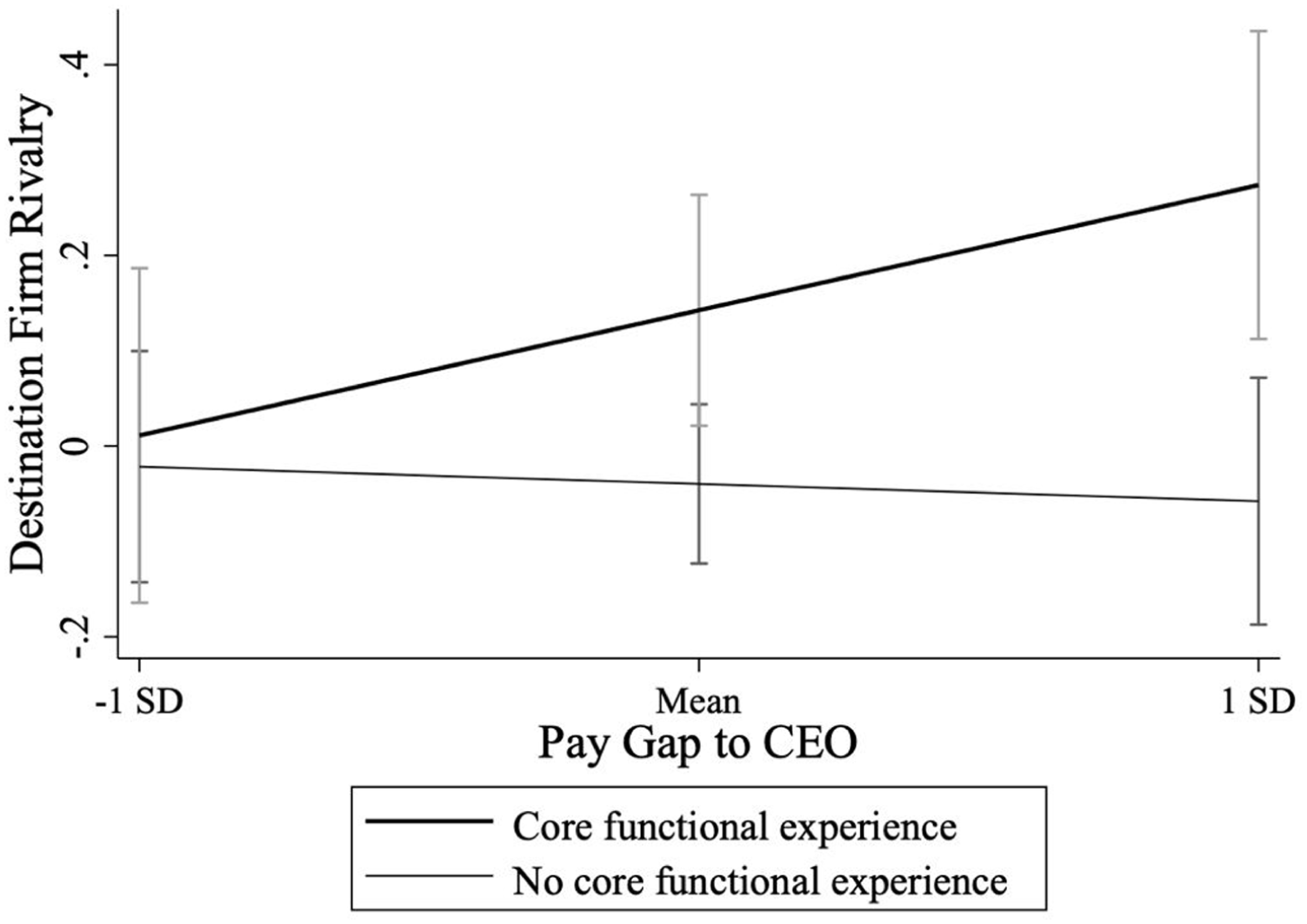

Finally, Hypothesis 3 predicts a positive interaction between executives’ competition-specific human capital and pay gap to the CEO on destination rivalry. When competition-specific human capital is measured by corporate or division experience, the interaction is not statistically significant. But consistent with Hypothesis 3, when competition-specific human capital is measured by core functional experience, the interaction term is positive and significant (β = 0.03, p = .045 in Model 4; β = 0.03, p = .025 in Model 6). This suggests that destination rivalry is highest for executives who have both primary experience in core functions and a high pay gap to the CEO. Figure 1 reinforces this idea and further illustrates the nature of this relationship. Among transitioning executives with core functional experience, destination rivalry is .17 SD higher for those with a high pay gap to the CEO compared to those with a low pay gap to the CEO. In contrast, the effect of pay gap to the CEO is essentially null for executives without core functional experience. This is consistent with our argument in Hypothesis 3 that competitively relevant human capital and vertical pay deprivation act as complementary demand-side and supply-side predictors of destination rivalry.

Interaction of Pay Gap to CEO and Core Functional Experience

Endogeneity

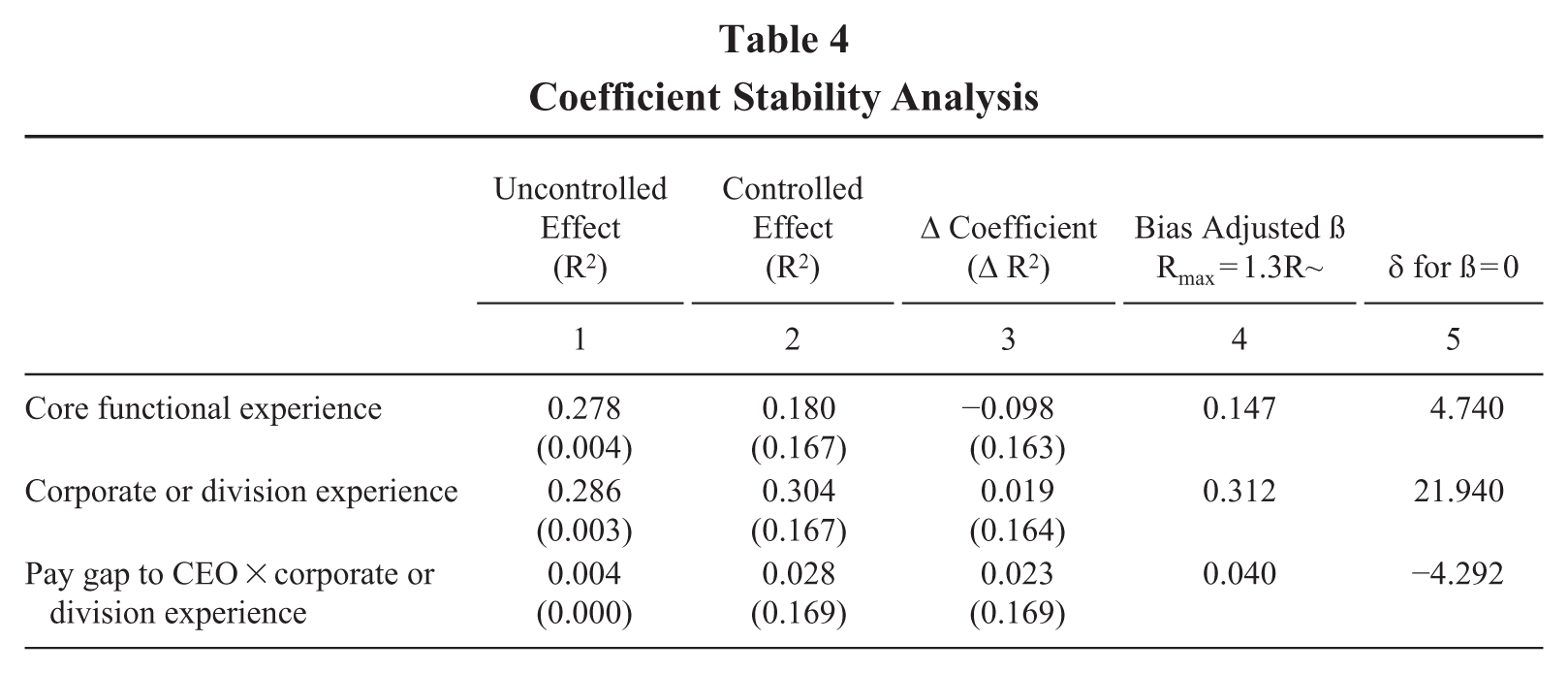

We conducted several tests to mitigate concerns about potential endogeneity. First, we implemented a coefficient stability test following Oster (2019) using the pscalc command in Stata 19. This approach evaluates the extent to which omitted variable bias may influence our estimates by comparing coefficient movements and changes in R2 between uncontrolled and controlled models. It then extrapolates what the coefficient would be if selection on unobservables were proportional to selection on observables.

Table 4 reports the coefficients and R2 values for both uncontrolled and controlled models, as well as the bias-adjusted treatment effect (β) for δ = 1 and the implied proportional selection coefficient δ when the treatment effect is set to zero. The results show relatively small changes in coefficients accompanied by much larger increases in R2 when controls are added. The bias-adjusted coefficients are generally similar to the controlled effects. Moreover, the proportional selection coefficients δ exceed the common threshold of |1| for each effect, implying that selection on unobservables would need to be substantially stronger than selection on observables for the treatment effect to be eliminated. Taken together, these results suggest that our findings are unlikely to be driven by omitted variable bias. Given consistency between controlled and uncontrolled effects, they also further support the idea that our results are not being driven by multicollinearity with included controls.

Coefficient Stability Analysis

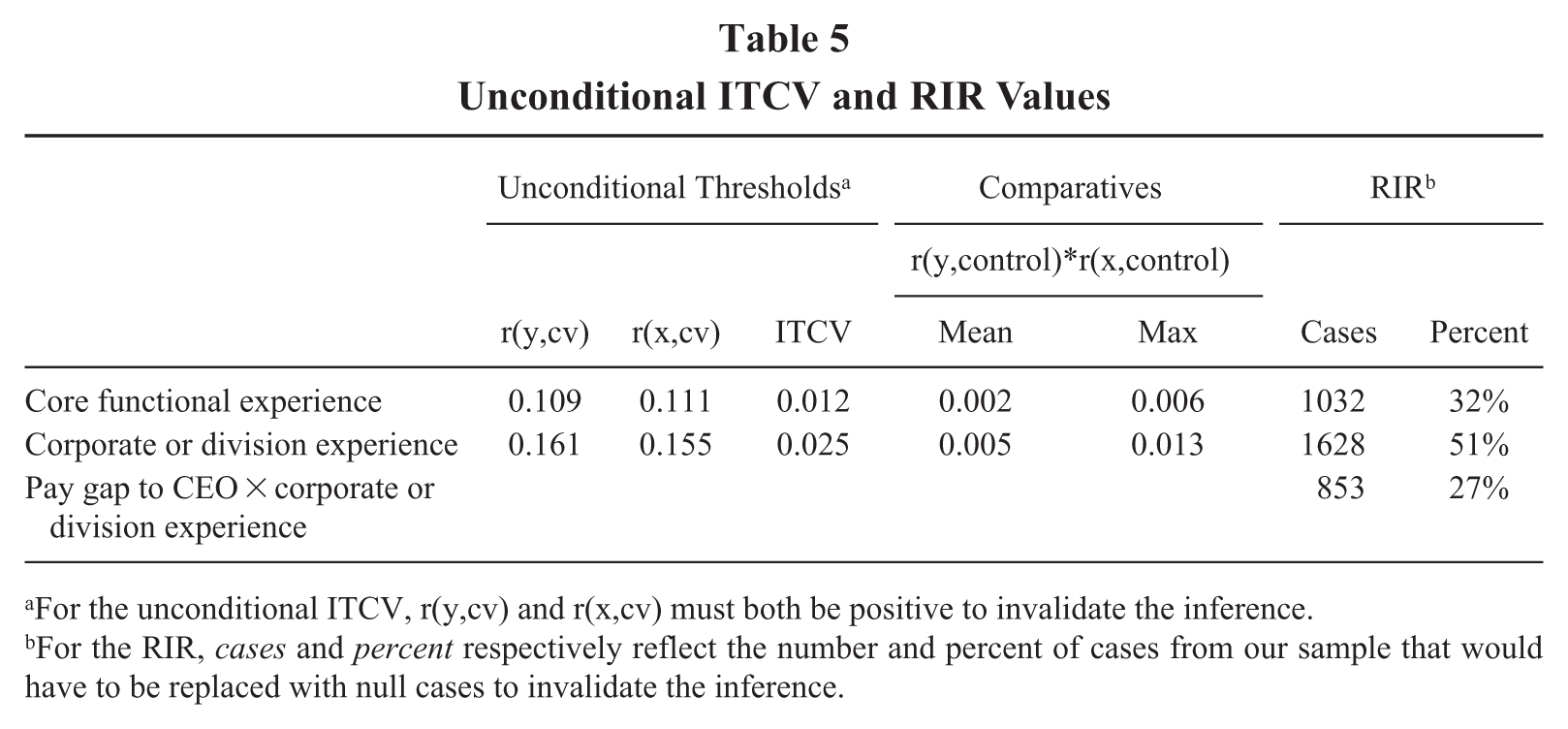

Second, we examined the impact threshold of a confounding variable (ITCV) and the robustness of inference to replacement (RIR) (Busenbark, Frank, Maroulis, Xu, & Lin, 2021; Frank, 2000) using the konfound command in Stata 19. The ITCV estimates the minimum strength of correlation that an unobserved confounder would need with both the independent variable, r(x,cv), and the outcome, r(y,cv), to fully explain away an observed effect, calculated as the product r(y,cv) × r(x,cv). We report ITCV values for statistically significant main effects on the left-hand side of Table 5. To interpret these values, we compare them to benchmarks derived from the partial correlations between our control variables and both the independent and dependent variables. Specifically, for each independent effect, we calculated r(y,control) × r(x,control) for every control variable, then identified the mean and maximum values of these products as points of comparison with the ITCV. Following current best practice, we report unconditional ITCV values (Lonati & Wulff, 2024), as default ITCVs are not directly comparable to control variable correlations due to scale differences. Results from the ITCV analysis further suggest the robustness of our results, as the ITCV values exceed both the mean and maximum benchmark values for each significant effect in our main results.

Unconditional ITCV and RIR Values

For the unconditional ITCV, r(y,cv) and r(x,cv) must both be positive to invalidate the inference.

For the RIR, cases and percent respectively reflect the number and percent of cases from our sample that would have to be replaced with null cases to invalidate the inference.

The RIR analysis complements these findings and allows us to assess the robustness of the interaction effect, which the ITCV does not accommodate (Busenbark et al., 2021). The RIR calculates the percentage of cases that would need to be replaced with cases showing a null effect to invalidate the inference. Across our focal independent variables, between 853 cases (27 percent) and 1,628 cases (51 percent) would need to be replaced to invalidate our inferences. Taken together with the coefficient stability tests reported above, these results provide evidence that our findings are unlikely to be driven by omitted variable bias.

Finally, while our primary models correct for potential sample selection bias by predicting the likelihood of moving to another public company in the first stage, they do not explicitly account for general turnover. We estimated additional models to account for turnover by applying inverse probability weighting (IPW). In the first step, we estimated models predicting executive turnover in the full sample and generated predicted probabilities of exit. These probabilities were then used to construct stabilized IPWs, calculated as the ratio of the overall probability of turnover (

Discussion

This paper seeks to extend research on executive mobility by conceptualizing and explaining the destination choices of executives in terms of the degree of rivalry between the departure and destination firms. We theorized that competition-specific human capital and a large pay gap to the CEO positively impact destination rivalry for executives transitioning from one firm to another. We find that competition-specific human capital is positively associated with the degree of rivalry between the departure firm and destination firm, and that destination rivalry is highest for transitioning executives with a combination of core functional experience and a large pay gap to the CEO. Next we describe how our theory and findings contribute back to the literature from which we draw, as well as their implications for practice. We conclude by outlining some limitations of our work that may provide fruitful avenues for future research.

Contributions to Theory and Research

First, we align executive mobility research more closely with theory on competitive strategy by conceptualizing transitioning executives’ destination choices on a spectrum of rivalry with the departure firm (Chen, 1996). This approach has several theoretical and empirical benefits. From a theoretical standpoint, rapidly shifting competitive landscapes have made categorical rival designations increasingly problematic for both scholars and practitioners. Rather than assigning firms to the category of rival or nonrival and risk omitting key players or including peripheral ones, scholars can use our concept and measure of destination rivalry to account for competition in a more holistic way across industries. More in-depth examination of the degree of rivalry in the executive mobility literature might illuminate labor movement and competition patterns that to this point have remained hidden due to data or conceptual limitations.

In addition, the demonstrated positive association between executives’ competition-specific human capital and destination rivalry reflects an important extension of theory and research on human capital and individual mobility. Most prior work at both the executive level and lower levels of analysis has emphasized the role of general human capital in job search and mobility (e.g., Cappelli & Hamori, 2014; Schönberg, 2007). From this perspective, general human capital increases external search and mobility because it provides individuals with a greater array of external opportunities (Becker, 1964; Cappelli & Hamori, 2014; Won & Bidwell, 2023). In contrast, executives’ specific human capital, while relevant to their home firms’ competitive advantage, is generally thought to be less transferable and therefore limiting in executive mobility (Becker, 1964; Starr, Ganco, & Campbell, 2018). While this logic may apply when considering an individual executive’s general likelihood of search or the breadth of opportunities that may be available to them, more specific forms of human capital can still have value in labor markets (Mackey, Molloy, & Morris, 2014; Sturman et al., 2007). Our findings extend research in this area by suggesting that, conditional upon moving, competition-specific human capital may be particularly relevant to closer rivals of the departure firm, with important implications for firm competitiveness (Campbell et al., 2012).

Finally, our findings contribute to research on executive compensation, particularly work that has approached compensation from the perspective of tournament theory (Connelly et al., 2013). Tournament theory describes individual and group behavior when reward structures are relative (e.g., based on rank or comparison) rather than based on objective output (Connelly et al., 2013). It has been used extensively in research on executive compensation, primarily in comparing CEO pay to that of executives at the next hierarchical level (Eriksson, 1999; O’Reilly, Main, & Crystal, 1988). Most research on vertical pay disparity emphasizes its potential to incentivize executives to remain at the firm and compete for promotion. However, our results highlight the potential downsides of large pay gaps to the CEO. Such gaps show a strong positive association with executive turnover in our sample of S&P 1500 firms. In addition, while pay gaps to the CEO exhibit no main effect on destination rivalry, our findings indicate that they do motivate transitioning executives with core functional experience (who are attractive to rival firms) to move to closer rivals. This finding also suggests that the demand-side pull of competition-specific human capital must be present for pay gaps to drive rival movement, offering strong support for our third hypothesis while clarifying the boundary conditions under which large pay gaps to the CEO become particularly problematic for firms.

Our findings also have implications for broader research on executive (horizontal) pay comparisons (Andrus et al., 2024; Pissaris et al., 2017; Ridge et al., 2017). Among our controls, we find that pay disparity to other TMT members is not significantly related to rivalry between the departure and destination firms, and supplemental analyses reveal no interaction between this form of disparity and competition-specific human capital on destination rivalry. These null effects underscore the distinctive role of vertical pay gaps to the CEO in shaping rival moves. Moreover, while our theory deals with internal pay dynamics that might shape executives’ willingness to move to closer rivals, we also control for external pay comparisons. We observe that pay disparity to industry peers is positively related to first-stage movement but negatively related to destination rivalry. This is a somewhat unexpected but potentially important finding, as the latter effect seems contrary to a supply-side logic. One plausible interpretation is that, when considering transitioning executives’ destinations, industry peer comparisons operate more as a demand-side signal than a deprivation-based motivator. Specifically, while larger pay disparities to industry peers may reflect external labor market comparisons that motivate general job search (e.g., Andrus et al., 2024), it may also signal lower perceived quality to close rivals (Finkelstein et al., 2009; Spence, 1973). In this sense, industry pay disparity may encourage general mobility while simultaneously reducing the likelihood of moves to close rivals. We encourage future research exploring how different pay comparison reference points function as supply-side motivators versus demand-side signals in shaping executive mobility.

Implications for Practice

Our study also has important implications for business practice. As average organizational tenures decline, a recent global survey before and after the onset of the Covid-19 pandemic found that CEOs believe retaining talent is the top threat to their business (Greenshields, 2020). One factor contributing to this is that the “new normal” increases job mobility for employees working remotely or from home. Our work directly ties into this issue by identifying relative pay as one factor that may be effective at preventing talent from joining rival firms. Contractual noncompetes, which reflect a more traditional way for firms to prevent rival movements, have recently come under significant legal fire. In many states, noncompete clauses are illegal or simply not enforceable (Marx, Singh, & Fleming, 2015), reducing the efficacy of noncompetes in terms of providing meaningful protection against rival poaching. Given these legal trends, along with the fact that employee mobility is only likely to increase in the coming years, firms may need to look to alternative methods to prevent poaching by rival firms. Our findings related to executive pay and incentives may well offer a promising alternative to keep transitioning executives and other employees from moving to rival firms.

Limitations

Our study has some limitations that create opportunities for future research. From a theoretical standpoint, our model adopts a rational, market-based interpretation of executive mobility. While this is consistent with much of the literature (e.g., Cappelli & Hamori, 2014; Forbes & Piercy, 1991; Frydman, 2019; Won & Bidwell, 2023), it necessarily omits the relational dynamics that research has shown also influence labor market decisions, including at the executive level (e.g., Andrus et al., 2019; Harrison et al., 2022). We attempt to control for some of these effects using the size of executives’ professional networks. However, this is an important boundary condition of our theory. Future smaller-scale or qualitative work could build on our study by focusing more squarely on relational factors affecting destination rivalry, either independently or in combination with market factors.

Empirically, there are some limitations associated with our choice of sample and measures. Although our measure of destination rivalry allows us to use a broad sample of firms across industries, it requires data that are only systematically available for publicly traded companies. In general, closer rivals for members of the S&P 1500 are likely to come from the population of other prominent, publicly traded companies, suggesting that we have a relevant set of destination firms from which to assess destination rivalry. Still, this constraint prevents us from exploring whether the dynamics we examine differ in smaller and/or private firms. For example, an executive may have a greater impact or play more roles in small or private companies, which might alter what constitutes competition-specific human capital to closer rivals. A sample that includes private firms would help clarify the boundaries of our theory.

The measure of destination rivalry is, itself, also subject to some limitations. As proxies for theoretical dimensions, the components of our formative index only imperfectly capture the factors that together constitute market commonality and resource similarity. For example, while assessing departure and destinations firms’ assets provides a consistent and scalable indicator of resource similarity that can be applied across industries, it remains only an approximation of the underlying construct, as resources are multifaceted and inherently difficult to measure directly. Similarly, geographic proximity contributes to rivalry between firms, but it can also facilitate executive relocation (Andrus et al., 2024), which may confound its role in our setting. While we attempt to mitigate these issues through alternative specifications (e.g., excluding geographic proximity, controlling for precise differences in assets), there is still the potential for measurement error. Along similar lines, our measure emphasizes structural sources of rivalry but captures only limited perceptual sources. Additional perceptual dimensions, such as those created by cultural dimensions or performance aspirations, are likely important and represent a promising avenue for future research.

The measures of competition-specific human capital, while demonstrating predictive value, are also necessarily constrained by the type of data available in archival sources. Beyond core functional roles and corporate or division leadership, executives may possess competition-specific human capital in other forms—for example, through access to trade secrets or involvement in in-progress innovations. Conversely, contractual barriers such as noncompete or nondisclosure agreements may inhibit the transfer of this knowledge, reducing its value to rivals. These factors lie outside the scope of what we can observe systematically, but they represent important boundary conditions. We view our measures as a meaningful step toward capturing competition-specific human capital in large-sample studies, while encouraging future qualitative or small-scale research to examine additional dimensions in greater depth.

Conclusion

Whereas research on executive mobility has yielded important insights into the antecedents of executive search and turnover, theoretical understanding of where executives go when moving between firms has lagged. Scholars have generally not considered the degree of rivalry between departure and destination firms, with few studies examining rivalry as a destination attribute at all. We introduce the concept of destination rivalry as the degree of market commonality and resource similarity between a transitioning executive’s departure firm and destination firm. We find that destination rivalry is higher for executives who have competition-specific human capital, and especially when they have a large pay gap to the CEO. Our theory and findings contribute novel insights to the literature on executive mobility and competitive strategy, with implications for how the two literatures can be integrated more fully.

Supplemental Material

sj-docx-1-jom-10.1177_01492063261428060 – Supplemental material for Where Do Transitioning Executives Go? Exploring Demand-Side and Supply-Side Drivers of Destination Rivalry

Supplemental material, sj-docx-1-jom-10.1177_01492063261428060 for Where Do Transitioning Executives Go? Exploring Demand-Side and Supply-Side Drivers of Destination Rivalry by Joseph S. Harrison, Ryan Krause, René M. Bakker and Zhiyan Wu in Journal of Management

Footnotes

Acknowledgements

The authors would like to acknowledge instrumental feedback and editorial guidance from Hermann Ndofor and two anonymous reviewers during the development of this research.

Supplemental material for this article is available with the manuscript on the JOM website.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge financial support from the Major Project of National Social Science Fund of China (24&ZD073).

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.