Abstract

This research examines 130 government contracts for legal services, specifically focusing on how decisions to include various accountability clauses are influenced by previous relationships between the government and its private sector contractors. Overall, the findings illustrate that prior positive contract experiences decrease the use of clauses that facilitate disclosure of information but increase the use of contract details. The evidence suggests an important role for relationships in new governance: contracting with familiar contractors may reduce the cost and use of some forms of accountability but not necessarily reduce overall accountability.

How does a previous relationship between the government and its contractors affect contract design? More specifically, when the government and a contractor have worked together in the past, are contracts more or less likely to include formal mechanisms for accountability? This question is particularly relevant to debates on new governance, 1 given that the lines of accountability are becoming more obscured, monitoring is costly, and government resources are limited (Rosen 1998; Romzek and Johnston 2005; Rehfuss 1991). Previous relationships may reduce the need for strict controls, and thereby enhance efficiency (Uzzi 1997). Yet, critics question the upsurge of government officials awarding large contracts to organizations, such as Halliburton, with whom they may have personal connections (Verkuil 2007). No doubt government contracting officials can be “captured” much in the same way that regulators can be captured by those they regulate (DeHart-Davis and Kingsley 2005, 239).

While the significance of ongoing relationships is well documented in the literature (see Sclar 2000), the link between relational factors and contracting decisions is not fully understood. Some scholars argue that previous relationships increase trust, which in turn reduces the need for hierarchical controls (Granovetter 1985; Gulati 1995; Uzzi 1997). Others reason that relationships facilitate communication and learning, thereby making it easier to write more complete contracts (e.g., Poppo and Zenger 2002; Ryall and Sampson 2006). Although both explanations point to possible benefits in cultivating relationships, the logic points to opposite effects on contract design. The former implies that a previous relationship with the supplier will lead to less formal contracts and fewer control mechanisms. The latter implies that a previous relationship with the supplier will lead to more specified contracts, which are likely to include more formal accountability clauses.

To the authors’ knowledge, this research is the first to test the impact of relational characteristics on contract accountability in government contracts. There are two notable features of the data and analysis. First, the authors examine and code actual language of government contracts, focusing on specific clauses within 130 state government contracts for legal services. The clauses address standard principal–agent problems. Second, about half of the contracts included in the analysis are repeat dealings, most of which include information about the quality of the previous experience (e.g., contractor performed well in the past). This information provides unique leverage for analysis on the impact of relationships on contracting decisions.

The article proceeds as follows. First, the article provides a brief overview of contract accountability and develops the logic for testable hypotheses predicting the choice of different accountability mechanisms used in government contracts. Second, the article presents an overview of the empirical approach along with a presentation of the analytical results. The article concludes with a summary of key finds, a disclosure of research limitations, and a discussion of avenues for future research.

Accountability

In contracting, accountability is often achieved through a combination of political, legal, and professional forms (Romzek and Johnston 2005, 440). Political forms of accountability rest on the agency’s responsiveness to multiple principals and constituencies. By contrast, legal accountability is based on external authority. An agency decision to audit supplier records is an example of formal oversight associated with legal accountability (Light 1993; Bardach and Lesser 1996). Professional accountability emphasizes discretion and deference to expertise. The public manager’s goal is to recognize the appropriate form of accountability under the circumstances, while considering such factors as task complexity, compatibility with management strategy, and institutional context (Romzek and Dubnick 1987).

Effective contract accountability exists “when the relevant government agency has met the minimum conditions of ‘prudent purchasing’. . . that is, the capability to assess contractor performance and the potential to hold the contractor accountable” (Romzek and Johnston 2005, 437, citing Fossett et al. 2000). This definition suggests that relationships can play a key role is achieving effective contract accountability. Prior relationships may provide behavioral and performance assurances that reduce the need for more costly controls. Relationships can also facilitate accountability by increasing communication and learning, thereby making it easier (and less costly) to write more complete contracts.

The present research examines both legal and professional forms of accountability in state government contracts for legal services. Legal forms of accountability include monitoring-type clauses and clauses that specify work details. Monitoring-type clauses are vital to enforcement and decision making in that they prompt information disclosure, which is considered key in addressing principal–agent problems (Furlotti 2007; Jensen and Meckling 1976). Three types of clauses lead to information disclosure: clauses that give the government the right to access books and records, clauses that provide for audits of financial records, and reporting requirements. The government chooses to strategically manage expectations by inserting these clauses into the contract. The government relies on external legal authority for enforcement of these clauses (Dubnick and Romzek 1991). Work detail clauses can be either vague, noting only the expected outcome without elaborating on how the job is to be accomplished, or clearly specified, by enumerating milestones or interim activities. The former implies deference to expertise, which is consistent with professional forms of accountability, while the latter is more consistent with legal forms of accountability (Romzek and Johnston 2005).

Previous Research: Ambiguous and Inconsistent Findings

There is a large literature on the link between relational factors and contract design and accountability, but to date, the accompanying empirical evidence is ambiguous and mixed. One problem results from the decision to aggregates clauses, which makes it difficult to parse and decipher the true effects. For example, Poppo and Zenger (2002) focus on the overall complexity of the governance apparatus for their core dependent variable, while Anderson and Dekker (2005) consider the number of contract terms as a proxy for contract “extensiveness.” In the few studies where clauses are categorized as decision rights or monitoring rights, individual clauses within these groups are not differentiated. For example, Parkhe (1993) operationalizes his dependent variable as the number of contractual safeguards, whereas Arruñada, Garicano, and Vázquez (2001) focus on the total number of monitoring rights. Even where comparable measures can be identified, research findings are mixed. For example, Argyres, Bercovitz, and Mayer (2007) do not find a significant relationship between task description and prior deals with the same partner. In contrast, Ryall and Sampson (2006) find that a prior relationship with the same partner does lead to more detailed task descriptions.

Reconciling the Evidence

To better understand what drives the decision to use various accountability clauses, researchers should assume qualitative differences, even among clauses that ostensibly correct similar deficiencies, such as information asymmetry. In addition, there are reasons the parties may opt to include some but not all accountability clauses. A clause requiring the contractor to produce monthly reports is likely to be less costly than a clause requiring a formal audit of books and records. Reporting requirements can also be distinguished from access and audit requirements. Reporting is not necessarily about distrusting motives or preventing moral hazard; reporting is often required simply to keep a project on schedule. In addition, the cost of reporting is determined by the intervals associated with the requirements; weekly reports are more costly to complete (and monitor) than monthly reports. The effectiveness of reporting as a control often depends on a government official having a thorough understanding of the work required at different stages of the project. By contrast, the cost associated with the specification of work details is primarily concentrated at the earliest stages of contracting.

The treatment of various mechanisms of accountability as qualitatively different also fits with a key idea in transaction costs economics, that is, the governance structures are often not simple markets or hierarchies but rather sophisticated hybrid solutions (Stinchcombe 1990). While transactions vary in their attributes, governance structures (i.e., contracts) vary in their costs and competencies (Williamson 1996, 46-47). By focusing on the qualitative differences among contract clauses, it becomes clear that some factors, such as relationship history, will not necessarily have the same predicted effect on all contract provisions that increase accountability. For example, history may decrease the probability of observing mechanisms that facilitate disclosure of information, but it may increase the use of clauses that specify work details. The next section develops the logic for various contract choices drawing on transaction cost economics, the theory of social embeddedness, and the knowledge-based perspective.

Theoretical Logic

The Role of Relationships in Reducing Agency Costs

An agency relationship arises when government, the principal, hires a contractor, the agent, to perform a service. The theoretical rationale for designing contracts for accountability rests in the fundamental problem with all agency relationships, that is, how to keep the interests of the principal and agent aligned (Alchian and Demsetz 1972). In contracts between government and suppliers, the supplier’s profit motive may conflict with government’s goals. The agent is presumed to know more than the principal about the level of effort and the costs related to his contribution. This information asymmetry leads to goal incongruence, which in turn increases the probability of moral hazard on the part of the agent (Jensen and Meckling 1976). Additionally, agents may view information as a source of power (Waterman and Meier 1998). Agents sometimes avoid revealing information for strategic purposes and as a matter of practice (Marx 2006). Consequently, there are costs associated with getting the contractor to disclose information about his efforts.

Transaction cost economics adopts a similar assumption about the nature of humans and the potential for behavior to diverge from expectations. According to Williamson (1975, 26), humans are “self-interested with guile” so one should expect them to behave opportunistically. It follows that the main objective in crafting contract language is to protect against behavioral-type hazards. Although transaction cost economics does not specifically address the role of previous relationships, the theory does posit that “managers anticipate conditions and organize with respect to them” (Williamson 1996, 45). Thus, the theory leaves room for consideration of relationship factors. The theory also posits that managers decide among different governance options on the basis of efficiency. In the context of contracting, government officials deliberate on the necessity of various provisions based on what they know about the trading partner.

The role of relationships on contract design can be further understood with reference to the sociological theory of embeddedness (Granovetter 1985). In this view, structural embeddedness can facilitate the development of trust by increasing the likelihood of repeated interaction between parities. Although the definition and operationalization of trust is subject to much debate, it is generally accepted that trust is accompanied by the positive expectation that one will not act to another’s detriment (Rousseau et al. 1998). Moreover, trusting parties are more willing than nontrusting parties to take risks based on that expectation (Mellewigt, Madhok, and Weibel 2007). Parties who trust each other become confident in each other’s motives and this confidence accrues as parties continue to honor commitments (Dyer and Singh 1998; Gulati 1995; Kalnins and Mayer 2004; Uzzi 1997). Combining these insights, some scholars propose that interaction may reduce the need for governance forms characterized by hierarchical controls (e.g., Gulati 1995).

Applied to the present research, when the government and the contractor do not have a prior working relationship, government officials will be more likely to include contract clauses that prompt information disclosure as a check on the contractor’s motives. However, when the parties do have a prior positive experience together, the government has some assurance that the contractor will behave in ways consistent with contract goals. In such cases, information disclosure becomes less important. In fact, given persistent budget constraints, government may prefer to contract with familiar parties so as to avoid the high cost associated with formal, legal forms of accountability.

Extending the same logic, transaction cost theory holds that the frequency of interaction matters, since it facilitates reputational effects and “make [s] the costs of specialized governance structures easier to recover for large transactions of a recurring kind” (Williamson 1985, 60). Likewise, organizational behavior scholars argue that the more parties interact, the more their values align (Ring and Van de Ven 1994). Value alignment decreases the likelihood of shirking. There is also empirical evidence indicating that the number of previous contracts is an important predictor of governance form (Anderson and Schmidtlein 1984). This leads to two related hypotheses:

Hypothesis 1a: A previous relationship between the contractor and the government will decrease the likelihood of observing accountability mechanisms aimed at facilitating or requiring information disclosure.

Hypothesis 1b: More frequent interaction between the contractor and the government will decrease the likelihood of observing accountability mechanisms aimed at facilitating or requiring information disclosure.

The Role of Relationships in Facilitating Learning

During interaction, parties not only learn about each other’s motives, they also develop more efficient avenues for communication. Parties who work together are likely to develop a common culture, common codes, and efficient channels of communication, which are important factors in both receiving information and reducing communication costs (Arrow 1974; Monteverde 1995). Kogut and Zander (1996, 503) describe how rules of communication can influence both information searches and learning. Parties who work together learn how to communicate; they come to understand the unique aspects of each other’s profession. The literature also tells us that the success of any information exchange depends in part on the intimacy and proximity of the source and recipient of the transfer (Arrow 1974). Similarly, Williamson notes that “specialized language develops as experience accumulates and nuances are signaled and received in a sensitive way” (1985, 62). Scholars applying this logic to contracts contend that interaction improves parties’ ability to draft more complete contracts (Poppo and Zenger 2002; Ryall and Sampson 2003). Consistent with this view, Argyres, Bercovitz, and Mayer (2007) find that more extensive relationship history leads to increases in contingency planning.

It is also plausible that parties will learn that some clauses are not necessary and delete them as they gain experience. Thus, evidence of learning effects can manifest in shorter contracts. Notwithstanding, some types of clauses are more likely to be valid indicators of learning. For example, clauses that detail work descriptions are more likely to show evidence of learning effects, than for example, auditing clauses. More specifically, contracts that include only brief descriptions of the work, such as “the contractor will provide legal representation for [case name],” provide evidence of the expected outcome for which the contractor is accountable. However, contracts that go beyond descriptions of the outcome and include details of output tasks (e.g., file response to complaint, conduct discovery, interview witnesses) provide evidence that the government has an understanding of the specific tasks associated with contract performance. More detail in subsequent contracts with the same contractor suggests that the government has developed this understanding over time. In contrast, a clause requiring an audit of the contractor’s books is more likely to be evidence of a perceived behavioral hazard or principal–agent problem than evidence of a learning effect. Auditing clauses are not as likely to be added to subsequent contracts when the exchange involves a repeat dealing with the same partner because if the contracting experience is negative, the government is more likely to contract with a different supplier in the future.

Yet, evidence of learning effects vis-à-vis the inclusion of more task detail does not change the fact that such language also increases accountability (Crocker and Reynolds 1993; Furlotti 2007). Behavior safeguards are manifest through details and stipulations (Saussier 2000). By breaking down a project into specific tasks or milestones, the government is clarifying responsibilities and boundaries, making it more difficult to claim misunderstandings. Although less detailed contracts pose fewer transaction costs, they also increase the risk of opportunism. The value of adding contract detail is increased when partners have an incentive to behave opportunistically (Mellewigt, Madhok, and Weibel 2007). Like monitoring clauses, task detail clauses are consistent with legal forms of accountability. Omitting such detail and leaving the specific means for accomplishing results to the discretion of the contractor is consistent with professional forms of accountability. Given the importance of contract details to accountability, an important goal is to understand how prior interaction and relationships might lead to learning and how that learning might manifest in contract details. This leads us to specific predictions about the inclusion of contract details:

Hypothesis 2a: A prior contracting history between the agency and the contractor will increase the likelihood of observing accountability mechanisms that describe work tasks.

Hypothesis 2b: More frequent interaction between the contractor and the government will increase the likelihood of observing accountability mechanisms that describe work tasks.

Data and Method

Sample and Data 2

The units of analysis for this study include the total population (N = 130) of legal contracts entered into by five different Indiana state government agencies over the past decade. The five agencies include the Department of Family and Social Services, The Indiana Regulatory Commission, the Office of the Secretary of State, the Attorney General, and the Indiana Gaming Commission. The selection of five agencies, which differ significantly in their missions, is intended to protect against generalizability concerns (Gulati 1995). The ten-year period was necessary to achieve a sample size sufficient for the statistical analysis and to provide an acceptable level of confidence in results. Examples of the types of legal services under contract include representation of pending lawsuits, debt collection, preparation of reports for the General Assembly, review of bids, and administrative law judge services. The average contract amount of contracts in the sample is $127,452. The maximum contract award is $900,000. Some contracts extend up to three years but most are entered into for a one-year period. The selection of legal contracts is motivated by the fact that government agencies tend to develop long-term relationships with law firms, similar to the way in which individuals come to rely on a single attorney for their entire adult lives. In this sense, law firms are truly agents of the state in the way depicted by much of the new governance literature. Approximately half of the contracts in the sample are between agencies and law firms that have previously worked together.

The included contract provisions are good candidates for analysis, since they comport with the literature on accountability and because Indiana requires a level of standardization for all professional service contracts. Agency officials use a contracting manual provided by the Indiana Department of Administration when specifying contracts. The manual specifies the overall contract structure and placement of clauses and also provides boilerplate language for different clauses.

Content Analysis

The authors took several steps to ensure the validity and reliability of the contract coding. First the authors consulted three persons with experience in negotiating contracts with the Indiana government and asked them to identify from a random sample of contracts all those provisions they believed were intended to hold the contractor accountable. All three uniformly selected provisions for reporting, auditing, and access to records. The variations in the language contained in these clauses did not change their opinion that the clauses were properly labeled as “mechanisms for accountability.” Work description clauses that went beyond simple work statements and that contained detail on roles or responsibilities were consistently selected by two of the three persons for all five contracts. However, after discussion, all three agreed that the more elaborate work descriptions were intended to increase contractor accountability. Thus, the authors are confident that the clauses originally selected based on a literature review of accountability are consistent with those clauses actually used in practice to achieve accountability.

The authors then engaged three different coders to identify the presence or absence of the clauses identified by the experts. The clauses are referred to as access, audits, reports, and details.The aim in coding access, audits, and reportswas simply to detect the presence or absence of the clause. No judgment is made as to the degree of accountability. To code contract details, the coders looked beyond the clause heading “work description” to the language contained within the clause; simple statements of work were distinguished from more fully detailed roles and responsibilities. 3

Dependent Variables

To minimize measurement error, the analysis includes dichotomous measures for the presence (value = 1) or absence (value = 0) of provisions; no judgment is made as to the degree of accountability. The audits variable measures whether the State requires an audit or may require an audit in the future. The access variable measures whether the contractor must grant the State access to its records and information either now or in the future. The reports variable denotes whether the contractor is required to provide the State with progress reports at any interval (weekly, monthly, etc.). Finally, the details variable is a measure of whether the contract includes provisions documenting specific work tasks, roles, and/or responsibilities of the contractor.

Independent Variables

The analysis includes two relational variables. The dichotomous variable history indicates that the agency and the contractor have worked together in the past. Notably, in this data set, the measure also indicates that the experience was positive. More specifically, the government requires the agency to justify the selection of the vendor in professional service contracts (found on the cover sheet of the contract). The two primary justifications are history and expertise. In just over half of the contracts, previous history is the primary justification (e.g., contractor performed well in the past). Therefore, the contractor is not only a previous agent for the state but also performed well in that capacity. The second relational variable, number, is a count of the number of contracts the law firm has had with the agency over this ten-year period. Based on the review of the literature, the more frequent the interactions, the more likely a relationship will develop.

In addition to the main independent variables, the analysis includes control variables to capture additional heterogeneity in the contracts and across the organizations. The dichotomous variable complex is intended to capture the perceived difficulty associated with the work tasks. The literature on the transfer of information suggests that knowledge involving complex tasks is especially costly to gather and also to communicate (Polanyi 1966; Simon 1962). Technical problems are often solved at one site because they involve “sticky information” that is not so easily transferred between sites (von Hippel 1994). When knowledge has tacit elements, transfer often involves numerous exchanges (Nonaka 1994). The main measure for task complexity is perceptual. Specifically, in about 46 percent of the contracts, the parties use the term “complex” or “difficult” in either the work description or in their explanation for choosing a particular vendor. For example, the contract may indicate that the agreement involves a “complex appeal” or that the vendor was selected because of its expertise in “difficult regulatory filings.” It is reasonable to assume that the parties use these terms when they perceive the complexity or uncertainty of the work to be relevant to the terms of the deal. Contracts that include these terms were coded as a 1 and 0 otherwise.

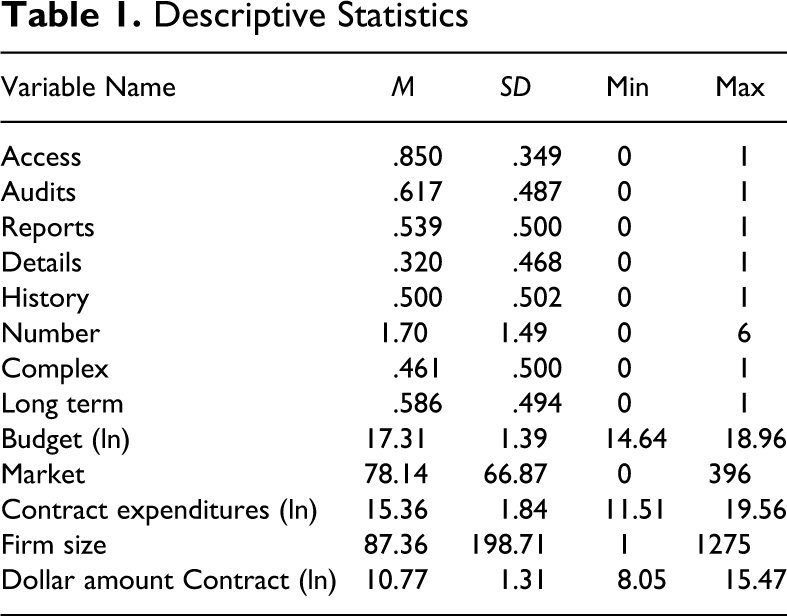

To capture any potential qualitative differences in the contract beyond complexity, the analysis includes several controls. The variable long-term denotes any contract with a duration that exceeds one year, since duration may affect accountability decisions. The variable dollar amount controls for the possibility that larger contracts may warrant additional accountability. Other controls account for organizational variation associated with the agency or the law firm. The variable budget is included because more agency capacity may be associated with increased oversight or more contract specification. The variable contract expenditures is intended to pick up any variation related to the agency's contract experience as well as its propensity to contract for professional services during the same year of the contract. To measure variation across law firms, the analysis includes firm size, which measures the number of employees working for the law firm. To control for the size of the market for legal services (and the potential for competition), the authors obtained a count of the number of law firms in the metro area that provide the same type of legal service indicated in the work description of the contract from the Martindale Hubbell Legal Directory. Finally, the analysis includes two sets of dummy variables for the year of the contract and the identification of the agency under contract. Presumably, the propensity to control contractors might increase or decrease over time, given changes in the political and economic environments. It is also possible that agency fixed effects, which are currently not accounted for by the other independent variable, may affect the propensity to include accountability provisions. Table 1 provides a summary of the descriptive statistics for the dependent and independent varialbes.

Descriptive Statistics

Results

The contracts under study exhibit a number of interesting aggregate qualities. First, the variation in the use of such clauses along with variation in language within these clauses suggests that parties do deliberate on options for the circumstances at hand. Only 24 percent of the contracts stipulated all four accountability mechanisms (i.e., the four dichotomous dependent variables). Less than half (45 percent) of the contracts included all three monitoring-type provisions (i.e., access, audits, and reports).

There is also a trend of prior relationships in choosing contract partners. Sixty-four contracts (about half of the sample) are between parties that have worked together in the past. Sixteen of the sixty-four contracts are between parties that have more than two prior dealings. Eleven contracts are between firms that have six prior dealings. The contract electronic summary document (EDS) attached to each contract also illustrates that the experiences between partners were generally positive because the reason for vendor selection includes language such as “chosen because of prior dealings.” Only six contracts between the same partners do not include any statement about the nature or quality of prior dealings either in the EDS or in the contract.

Results from t-tests provide some general information about the variation in contracts based on the supplier/law firm, including the possibility that influential law firms are more likely to receive longer contracts or larger contracts. 4 The results suggest that the mean difference in contract duration for the three largest law firms (twelve in sample) against all others is not statistically different from zero. However, the total amount of contract awards is statistically different for the two groups. The average dollar amount of contracts for the largest firms is $76,152; for other firms, the average amount is $183,269. Yet, this result does not hold when controlling for the size of the supplier market. In addition, no statistical difference in means was found between the average contract durations and average contract amounts associated with firms that are registered lobbyists and firms that are not registered lobbyists. Thus, it appears that the size of the contract is driven by the market of available suppliers, not the size of the firm or lobbyist registration.

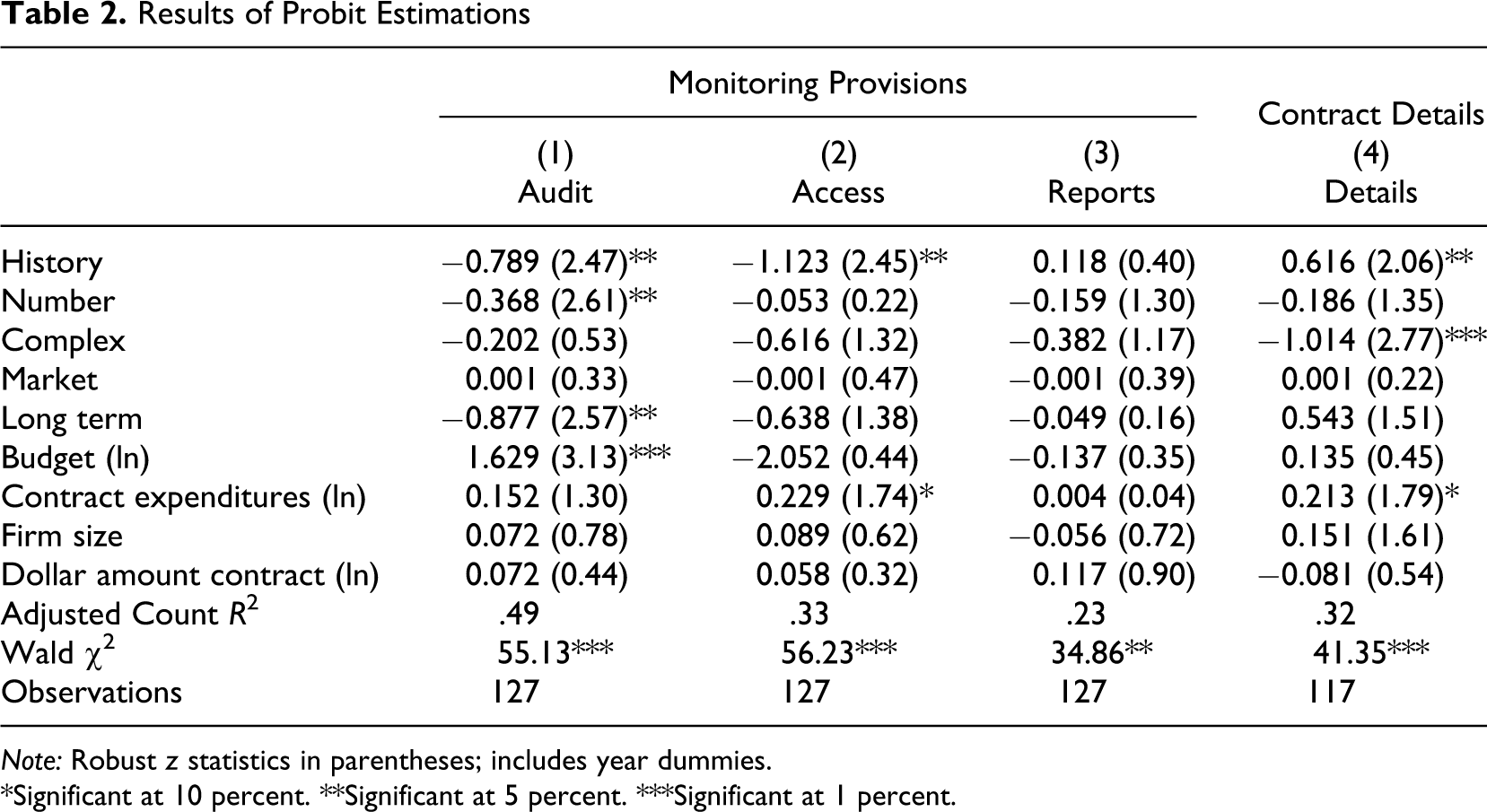

Table 2 reports the results of the multivariate analysis, specifically highlighting how relationship history affects accountability terms in government contracts for legal services, while controlling for other factors. Given the dichotomous nature of the dependent variables, the analysis employs binary choice models (probits) to estimate the outcomes (Greene 2007). As noted earlier, there are two general accountability categories included in the analysis: monitoring (access, audits, and reports) and contract details (specific roles and responsibilities). There appears to be no statistical rationale (e.g., Cronbach’s α and factor analysis) for combining the three monitoring provisions into a single measure. However, access and auditing are highly correlated, which suggests a common underlying logic associated with their use. This makes sense, given that both provisions prompt disclosure of information, a problem associated with principal–agent relationships. Reporting requirments, on the other hand, may be included in the contract to address other concerns, for example, keeping the project on schedule. 5 Since the reporting requirement variable is not correlated with the other monitoring variables, the analysis reports each monitoring-type dependent variable separately.

Results of Probit Estimations

Note:Robust z statistics in parentheses; includes year dummies.

*Significant at 10 percent. **Significant at 5 percent. ***Significant at 1 percent.

Table 2 provides results for each regression equation. Models 1–3 present the results of the regression predicting the inclusion of monitoring provisions (dependent variables: audit, access,and reports). The adjusted count R 2 statistics range from .49 in model 1 to .23 in model 3. Overall, the results provide general support for Hypotheses 1a and 1b in regressions 1 and 2. Relationship history decreases the likelihood of including information requirements in the contract. Specifically, an acknowledged history between the parties decreases the likelihood of observing an audit and mandating access (marginal effects = .30 and .11, respectively). Similarly, increases in the number of contracts a firm has had with the State decreases the probability of requiring an audit (marginal effect = .07). For auditing, significance occurs once the parties have had at least two prior dealings (pr = .023). For reporting requirements, there is a significant association (pr = .07) once there are at least three prior dealings. For both auditing and reporting comparable levels of significance hold as familiarity increases (four plus dealings, etc.). Interestingly, for both auditing and reporting, results also show that no familiarity impacts the decision to add requirements more than familiarityimpacts the decision to forego auditing. Decisions to forego some formal auditing requirments appear to be made reluctantly—especially as the parties become more familiar with each other and in light of positive experiences. However, this result is not consistent for all provisions. The number of contracts (or degree of familiarity) has no statistically significant effect on the likelihood of mandating access to information. The relational variables also have no statistically significant effect on the likelihood of observing a reporting requirements. Thus, there appears to be something qualitatively different between reporting and the other two accountability/monitoring variables. There is also a consistent pattern between the length of the contract, the dollar amount of the contract, and the probability of observing all of the monitoring-type clauses. In general as contacts increase in length, dollar amount, or both, the probability of observing each monitoring provision increases, all other variables held at their means. Probabilities range from .28 to .38 for contracts one year or shorter that are of the smallest dollar amounts (under $5000) and from .76 to .95 for contracts that are longer than one year for the highest dollar amounts ($900,000).

Model 4 presents the results of the probit estimates of provisions associated with the dependent variable details. The adjusted count R2 statistic for model 1 is .32. The results provide some support for Hypothesis 2; a relationship history will increase the likelihood of adding contract details. When the parties have worked together in the past, the probability that the contract will describe the work in detail is .42; when there is no history between the parties, the probability is .21 (the marginal effect is .21). However, there is no statistical evidence that the number of contracts between the parties influences the level of task detail. Therefore, the results support Hypothesis 2a but not Hypothesis 2b.

Control variable effects are also notable. In particular, complex exchanges lead to less work detail. Specifically, the marginal effect of the complex variable is −.37. When the contract is coded complex, the likelihood of observing contract details is just .13. This finding is not surprising, given that task complexity impedes information exchange and obfuscates planning. Complex tasks may be difficult to comprehend and therefore to communicate and specify in writing. However, complexity has no statistically significant effect on the monitoring dependent variables. This finding is somewhat inconsistent with previous research. Brown and Potoski (2003), for example, found that measurement difficulties (a form of complexity) led to additional monitoring in local service delivery. In addition, agencies that contract more (measured by higher contract expenditures) are more likely to add details as well as require the contractor to provide access to a firm’s books and records, whereas agencies with larger overall budgets (natural log) tend to require more audits. A possible explanation is that larger agencies, both in terms of contracting and overall budget, simply have more contract management capacity. That is, they are better equiped to require additional control due to their contracting experience and resources. The number of suppliers also does not appear to affect either the inclusion of monitoring-type provisions or the decision to add task detail to the contract, controlling for other factors. Finally, longer contracts are less likely to entail auditing clauses.

Discussion and Conclusion

A main goal of this research was to produce evidence of what new governance looks like, particularly as it relates to the effect of relationships on accountability. To authors’ knowledge, this research is the first to test the impact of relational characteristics on contract accountability in government contracts. Two aspects of this research set it apart from previous work. First, the authors code actual contract language from government contracts. Second, positive experiences are typically assumed in research on the effect of repeat dealings; the authors were able to incorporate information on the quality of previous experiences between the contracting parties. Although this research is not able to fully uncover the causal mechanisms behind contract choices, the results generally support both the trust accounts and the learning effects attributed to relationships in previous research. This adds to the body of work linking relational factors more generally to contract design.

Overall, the weight of evidence from the analysis suggests an important role for relationships in new governance: contracting with familiar suppliers may reduce the cost of accountability and also enhance government’s capacity to write more tailored contracts that facilitate accountability. In choosing to rely on contractors with whom they have a previous relationship, government relies less on strict controls and more heavily on the detailed specification of tasks necessary to achieve results. Viewed through the lens of previous public administration scholarship on accountability (e.g., Romzek and Johnston 2005), reliance on one form of accountability over another does not necessarily mean a reduction in net accountability.

Evidence further suggests that government is cautious in its decisions to forego monitoring; both the degree of familiarity with the contractor and the availability of agency resources appear to be part of the decision calculus. Although the decision to forego scheduled audits and access to books and records is more frequent when there is a history with the contractor, reduction in these controls often occurs only after two (and sometimes three) positive experiences. In addition, the agencies that do choose the more stringent (and costly) monitoring approaches are those with more resources (larger budgets). Thus, on the surface, the accountability strategy appears both rational (efficiency-based) and credible. Together the findings imply government aims to be a “prudent purchaser” (Fossett et al. 2000), even if it does increasingly rely on contracts. This interpretation is bolstered by the fact that the results provide no conclusive evidence that political influence is driving decisions to forego formal monitoring. This stands in contrast to the discussions on new governance that paint a negative picture of the evolving ways in which government carries out its responsibilities: Extensive contracting is often described as the path to a “hollowed out” government, one in which authority is diminished, accountability problems abound, and democratic values are compromised.

The evidence that the parties learn to specify contracts as they interact, which in turn enhances contractor accountability, suggests an added benefit to working with familiar parties. The result is consistent with learning effects and the role of relationships in facilitating information exchange and knowledge transfer (Arrow 1974; Monteverde 1995). One unexpected but interesting finding is that learning occurs in more than one way. Specifically, agencies that write more contracts also write more detailed contracts, regardless of who they write them with. This suggests that an agency’s general contracting experience may provide just as much leverage for enhancing accountability vis-à-vis specification as agency experience working with the same parties repeatedly. However, contracts involving more complex tasks do appear to present challenges for writing detailed contracts. This is an area for additional research.

Finally, the findings are subject to limitations. The relevance of results to professional services, other than legal services, remains an open question. Moreover, while it is clear to us that the government relies on different forms of accountability when it deals with familiar parties, the efficacy of those choices requires further research. In addition, this research focused on very specific forms of accountability evident in contract design. In reality, contract decisions are part of a broader system of accountability. Intergovernmental relationships and the overarching political environment are two of many factors that interact with contract choices and ultimately define the level of accountability associated with any decision.

Footnotes

The authors appear in alphabetical order; the authors have contributed equally to this manuscript.

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The authors received no financial support for the research, authorship, and/or publication of this article.