Abstract

This study explores the Great Recession’s effect on the commitment by the city of Dallas, Texas, to its private partners in seventeen tax increment financing (TIF) districts. What effect did the recession have on private investment in public–private partnerships? Did the recession cause a loss of credibility in the city’s commitment, resulting in lower levels of private investment? Was there a lasting structural change in the determinants of private participation stemming from the recession? Results from a random effects Tobit model show that the city’s proposed budget for each TIF district was a significant determinant of the level of private investment. However, during the recession, the actual amount of investment by the city was essential to reassuring private investors of the city’s commitment.

Introduction

The Great Recession of 2007–2009 has had far reaching consequences on the perceived financial capacity of local governments. The overall weakening of the economy in combination with the increasingly vitriolic bureaucrat bashing has undermined the public’s faith in the fiscal solvency of public institutions. Public–private partnerships are particularly vulnerable to the disruptive effects of recessions because those relationships are built on trust, reciprocity, and the credibility of collaborators to meet their financial commitments (Ostrom 1998; Bovaird 2004). This article examines the Great Recession’s effect on the perceived commitment by the city of Dallas, Texas, to meet its financial obligations and the effect that perception has on participation by private developers in the city’s tax increment financing (TIF) districts.

Using data from seventeen of the city’s TIF districts drawn from a twenty-year period (1992–2011), we assess the Great Recession’s effect on the investment by private developers in these targeted areas of redevelopment. What factors affect private participation in these partnerships? Is there evidence that the city’s credible commitment affects participation by private developers? Did the recession cause structural changes in private participation that lingered into the postrecession period? TIF provides a fitting venue to answer these questions because a TIF district’s success depends on the fidelity of the host city to the prior commitments it has made to the collaborative venture.

While public–private collaboration has been studied extensively, little is known of the determinants of private sector participation in these collaborative ventures with the public sector. Private sector participants have different motives than the public sector that drive their participation. This article contends that the perceived credible commitment of the public partner is a key determinant of private sector participation. Recessions put that commitment to its greatest test. The Great Recession provides a fitting venue to test whether a city’s credibility suffers during fiscally stressful times and whether that stress adversely affects the city’s capacity to sustain its partnerships with other organizations.

This article begins with a discussion of public–private partnerships and the determinants of private sector participation followed by a brief discussion of the basics of TIF. That is followed by a theoretical discussion regarding the effects of credible commitment and of recessions on private sector participation in TIF districts. Next, we present a description of our methods and the data used in the analysis. This article ends with a discussion of the findings and their implications for public managers as they engage in partnerships with nonprofit and private firms.

Public–private Partnerships and TIF Districts

Public–private partnerships have gained considerable popularity over the past two decades, especially with cities as they have sought more cost-effective ways to deliver services. Now it is quite common for state and local governments, private businesses, and nonprofits to form partnerships that blend their distinctive strengths to finance and deliver public, and not-so-public, services. But we lack empirical evidence of the determinants of private sector participation in public–private partnerships. Using TIF, this study assesses the importance, if any, that a city’s perceived credible commitment has to the success of its partnerships with private businesses.

The motivation for public–private partnerships is the creation of what Klijn and Teisman (2005) call surplus value—outputs that exceed what would have been achieved in the absence of collaboration by the partners. In the case of TIF, the surplus value is increased economic activity in the targeted area that would not have occurred without the TIF—for example, growth in property values, in retail sales, and in employment. The cooperative arrangement is a form of coproduction in which the participants achieve greater returns working together than had they worked independently. All partners are necessary to the success of the venture, but none is sufficient on its own.

A key to a successful partnership is the credibility brought by, what Bryson, Crosby, and Stone (2006) call, the sponsor. A sponsor, such as the city of Dallas, brings “prestige, authority, and access to resources” to the partnership. Champions, on the other hand, such as private firms, provide the day-to-day business activity that “help the collaboration accomplish its goals” (Bryson, Crosby, and Stone 2006, 47).

Public–private partnerships also risk failure particularly in collaborative initiatives such as TIF where financial risk is shared by participants. Failure of the joint venture reverberates not only to the immediate partnership but also to future attempts at collaboration. As such, we define a public–private partnership as a formal or informal arrangement between a city and one or more private firms where participants share in the financial risk, and the benefits that accrue to each partner are dependent on the success of the other partners.

Although no prior study directly examines the determinants of private sector participation in public–private partnerships, insights can be gleaned from the research literature on collaboration and, specifically, studies of collective action. Collective action problems occur when rational individuals pursue their own self-interest, resulting in suboptimal social outcomes. In general, successful collaboration depends on goal congruence (Gray 1989; Rogers and Whetten 1982), shared values (Alter and Hage 1993; Fleishman 2009), leadership and managerial capacity (Agranoff and McGuire 2001; Bardach 1998; Ansell and Gash 2008; O’Leary and Bingham 2009), political entrepreneurs (Schneider and Teske 1992), low transaction costs (Feiock 2013; Feiock, Steinacker, and Park 2009), risk sharing (Boyne 1998; Brudney et al. 2005; Hawkins and Andrew 2010), and reputation (Ostrom 1990, 1998). However, this literature does not address directly the determinants of private sector participation where a government serves as the sponsor of the collaborative initiative.

The institutional collective action (ICA) framework provides further and more specific insights into the motivations and deterrents of private sector participation in public–private partnerships. The ICA framework treats institutions as individuals and holds that collaboration occurs when the benefits of collaboration outweigh the costs of not collaborating. Positive spillovers and benefits from economies of scale provide enough of an incentive for local governments to overcome regional collective action obstacles and collaborate with a third party (Feiock 2013). When the net benefits of collaborating are positive, transaction costs remain the primary barrier to collaboration (Feiock, Steinacker, and Park 2009).

Partnerships, such as TIF, are functional ICA problems where the logistics are complex and require specialized policy experts from different institutions (Feiock 2013). Any single institution may have the jurisdiction and resources, but it lacks all of the functional capabilities to resolve the logistical complexities. A partnership between public and private organizations provides the necessary expertise to assume the necessary roles that will bring net benefits to the collective that otherwise would not be possible if they had acted independently.

Coordination problems, division costs, and defection risk create deterrents to collaboration (Feiock 2013). Coordination problems occur when a complex task requires interdependent execution of functions. As a collaborative effort gains complexity, the cost of not coordinating increases. Division costs occur when parties seek to accrue benefits from a partnership but have difficulty dividing the benefits in a satisfactory manner (Steinacker 2004). Coordination problems and division costs are not the primary concerns in a TIF district because (1) the activities of the partners are only minimally interconnected such that coordinating communication among partners is not essential to the partnership’s success and (2) the enabling legislation establishing a TIF district will define who receives what benefits.

However, the risk of defection poses the greatest threat to TIF partnerships because of the potential for opportunism by both public and private partners (Feiock 2013). Defection occurs when participants gain by reneging on their commitment to participate in the proposed partnership. Credible commitment provides a deterrent to defection by giving participants reliable information upfront when making a decision whether to join the partnership or not. Credible commitment lowers defection risk because of the increased trust among partners. When partners trust that the other partners will follow through on their commitments, then the need for higher level institutional assurances (e.g., an enforcing mechanism or third party oversight) is obviated (Ostrom 1990, 1998; Feiock 2013). Because participants in a TIF district do not have the option of a third party to compel participation, credible commitment provides the most viable long-term solution to minimizing defection and assuring that the partnership remains intact even during periods of economic stress.

Despite the extensive literature on determinants of collaboration, little is known about private sector participation in public–private partnerships. This study fills that gap by assessing the effects that credible commitment has on public–private partnerships in TIF.

Participation in a partnership gives private sector participants a competitive advantage when the collaboration allows them to benefit from economies of scale and public authority (e.g., access to eminent domain, expedited zoning changes, and public rights of way), and provides the private sector participants with learning opportunities that otherwise would not have occurred outside the partnership (Bovaird 2004). Koppenjan and Enserink (2009) identify the promise of a return on investment, mitigation of externalities, risk alleviation, and institutions limiting political uncertainty as important determinants of private sector participation in public infrastructure projects. Another determinant is scope management—the allocation of responsibilities in a partnership such that only the profitable components are in the purview of the private sector participants (Koppenjan and Enserink 2009). Johnstone and Wood (2001) found that scope management was a factor in private sector participation.

Private sector participation in a public–private partnership is driven by profit motivation and is most likely to occur when the partnership gives the private firm a competitive advantage coupled with a profit opportunity. The fact that public–private partnerships achieve socially beneficial outcomes is a positive externality of such partnerships.

TIF

TIF is a popular economic development tool used by local governments to attract private investment to a targeted region of a city or county. The redevelopment begins when a local government, using its authority granted by state law, establishes a TIF district, usually in an area where economic growth has lagged. States typically require that TIF districts be located in blighted areas, although statutes often leave blight undefined so as to make almost any area eligible. TIF districts range in size from just a few blocks up to several hundred acres.

When a TIF district is created, the host city may issue bonds, backed by the anticipated increment in property tax revenue from the redevelopment, to provide financing for the purchase, clearing, and preparation of land and for the installation of public infrastructure. Once prepared, the land is then sold to developers, often at a price below the cost of preparing the site, a technique known as a land write-down. The predevelopment costs, including write-downs, are later recouped by the district from property taxes generated by increased property values and from increased sales taxes over the life of the project (typically twenty years).

The incremental increase in property or sales taxes provides the funding for servicing the outstanding debt. TIF provides direct public funding for infrastructure improvements in the designated district, thereby lowering upfront investment costs to prospective business investors (Carroll 2008). A local government may construct some or all of the facilities and then lease them to private firms. The lease payments may provide additional funding for debt service obligations of the TIF district.

Although state statutes vary, either a TIF district has its own governing board appointed by the city or county council or it is governed directly by the council. Regardless of its governance structure, TIF districts typically prepare and send an operating and capital budget to their oversight body for approval. TIF districts with their own governing boards may even have the authority to issue bonds. A TIF district does not have the authority to levy a separate property or sales tax in the district. (Some types of improvement districts do possess separate taxing powers from a city or county.) Property in the TIF district is taxed at the same rate as all other property in the host city or county.

The property tax revenue in a TIF district is divided into two categories: (1) taxes on the predevelopment value of the tax base, which are kept by each overlapping taxing body (city, school district, special districts, and county) and (2) taxes generated from the increased value of the property resulting from redevelopment, which the district retains in a tax increment fund, giving rise to its name. (State laws may give overlapping local governments the option of opting out of the TIF district, in which case those governments retain all revenue generated in the district.) The TIF district’s governing board controls the revenues from the property tax increment and uses them (as well as, in some cases, sales tax revenues) to carry out the district’s redevelopment plan and pay for public improvements. Once a district reaches the end of its mandated term of existence, all liabilities are liquidated, the board is dissolved, and the taxable property in the district reverts to the tax rolls of the overlapping local governments.

Unlike tax abatements, which reduce tax liability on a case-by-case basis, TIF provides publicly funded improvements that benefit property owners in the TIF district. And TIF appears equitable since property owners within the district pay the same property tax rate as owners outside the district. Business investors also benefit from the public investment by having the incremental increases in their property taxes reinvested back into the district.

Politically, TIF enables a municipality to implement public improvements in the targeted area without raising tax rates on the whole municipality. It decreases or even eliminates certain redistributional burdens on the municipality’s remaining tax base by shifting the risk for development to those property owners in the district who benefit from the improvements. Local governments also use TIF to stimulate agglomeration economies in, and adjacent to, the redevelopment district, a strategy essential to building a sustainable local economy (Carlino 2011).

TIF is authorized in forty-eight states; it is not authorized in Arizona and no longer exists in California. Although California was the first to adopt TIF in 1952, in 2012 the state disbanded all 400-plus redevelopment agencies after a report by the Legislative Analyst’s Office found that TIF had not been effective at attracting business development to California (Kenyon, Langley, and Paquin 2012, 37). It appears that the real motive was a move by the state to take control of the revenue from the redevelopment districts to help balance the state’s structural budget deficit.

In Dallas, the TIF process begins with the city’s Office of Economic Development (OED) identifying neighborhoods, usually in the downtown area, where TIF may be an effective tool for stimulating redevelopment. The area may have suffered slow growth or even economic decline relative to other parts of the city, but the more important consideration is the area’s potential to attract private development. The OED prepares a preliminary budget that includes an estimate of the likely revenue from the property tax increment in the TIF district. The amount of city funding in the preliminary budget is driven by the projected property tax increment from the redevelopment.

Dallas uses a pay-as-you-go basis for its contribution to TIF districts. The OED markets the proposed TIF district to prospective developers and gauges their interest in the proposed redevelopment. Once sufficient private investment has been committed, the OED announces the creation of the district and the city’s proposed budget for the TIF district.

On rare occasions, the city’s financial advisor has recommended issuing bonds for TIF projects. Although the city’s approach to economic development is risk averse, it still shares risk with the private investors for the TIF district’s success, a strategy that constitutes a true public–private partnership (Bland 2013, 8).

The city of Dallas and private developers share in the financial risk of the partnership’s goal to achieve surplus value. Should the partnership fail, both public and private participants incur a loss. The city risks not receiving an increase in tax revenues from redevelopment and a loss of capital if its investment does not draw private investors. Private developers risk not recouping an investment return if the joint venture fails to meet their profit expectations. Thus, TIF provides a suitable venue to explore the distinctive roles, if any, of credible commitment among collaborators to create surplus value through a public–private partnership.

The popularity of TIF as a type of public–private partnership has attracted the investigative interest of public finance scholars. Prior studies, however, have not addressed the role of credible commitment in the success of TIF: what factors influence private firms to invest in a TIF district? How does a city’s credible commitment to TIF partnerships affect the willingness of private developers to invest in a TIF district? Did the recession cause structural changes in private participation that lingered into the postrecession period? These questions require a more in-depth case study of private investment in TIF districts and the changes, if any, caused by the Great Recession.

Theory

Public–private partnerships are not costless endeavors. Participants are drawn to the partnership because of the anticipated surplus value from the collaborative venture, particularly if those returns exceed what private investors could earn elsewhere in the market and if the social benefits exceed the investment cost for the host city. But surplus value is not assured, particularly in new collaborative ventures where the participants have no prior track record of working together, or during recessions when returns on investment may turn negative.

TIF provides an attractive investment opportunity to the extent the city’s participation reduces the risk of loss for investors and increases the prospect that their expected investment returns will be met. In the absence of a credible commitment by the city, private developers’ greatest fear is that the host city fails to meet its investment obligations. Public investment in a TIF district is predicated on increases in property values. However, if a TIF district does not generate the anticipated increase in property values, the city may have no recourse but to renege on its commitment. If that occurs, future collaboration between private investors and the city will be in jeopardy.

The key to successful public–private partnerships is credible commitment among participants—the degree to which participants trust each other to fulfill their obligations (Ostrom 1990, 1998; Koppenjan and Enserink 2009; Feiock 2013). The city’s reputation for fulfilling its obligations is central to building credible commitment in TIF districts. For a TIF district to successfully attract private investment, private developers must trust that the host city will follow through on its budget and projects proposed at the creation of the TIF district.

Private developers prepare their investment plans for the life of the district based on the city’s proposed budget for public improvements. They use this proposed budget to gauge the city’s commitment to the TIF district and to prepare an investment plan that optimizes the returns for their investors. That proposed budget provides essential information used by developers in planning their level of participation in the joint venture. The more credible the city’s budget, the more private developers are likely to invest in the venture.

In order to understand the role of credible commitment in TIF, it is necessary to understand the risks faced by private developers. Projects in a TIF district are financed from property taxes using incremental increases in property values. Because of the fluctuation in the business cycle, projects do not always add property value as planned. Consequently, the annual level of public investment in TIF district projects is volatile. Over the lifetime of a TIF district, however, public investment should approximate the level proposed by the host city in the original TIF plan.

Given the competition for private investment, we conjecture that private investors look for signals of credible commitment. For a city that has a record of meeting its investment commitments in TIF districts, that signal is the proposed budget for a new TIF district. Recessions, however, weaken investor confidence in that credible commitment, and they will seek reassurance that the city will uphold its commitment. We conjecture that, despite its volatility, investors will look to the actual level of spending by the city during recessions for reassurance of the city’s commitment.

A key determinant to attracting and keeping private sector participation in a TIF partnership is the degree to which investors perceive the city of Dallas to be committed to the capital improvement plan and budget for a TIF district. If Dallas has an erratic record of following its plans or if it has reneged on past commitments to a TIF plan, then investors will lack confidence in the city’s commitment. However, if the city has an unblemished record for meeting its commitments and timely completion of its projects, then private firms will perceive the city as having a high degree of credible commitment.

Based on this theory, in cases where credible commitment exists, we expect that the city’s proposed lifetime budget for a TIF district is associated with a positive increase in the level of private investment. Conversely, when a local government lacks credibility with its private partners, private developers will look for a more certain signal of the city’s commitment, namely its annual level of expenditures in the TIF district. These alternative perspectives lead to two testable hypotheses.

The Great Recession has had a lasting impact on the perceived fiscal strength of all levels of government. The depth of the recession and its protracted recovery in combination with the increasingly vitriolic bureaucrat bashing has undermined the public’s faith in the fiscal solvency of public institutions. We expect that the Great Recession weakened the perceived credible commitment of the city of Dallas to meet its funding obligations to its TIF districts. Given the volatility of the business cycle, during a recession investors will look to the actual level of spending by the city as a signal of the city’s commitment to meeting its obligations to the partnership. This leads to the following hypothesis.

The 2007–2009 recession jarred the American public, the economy, and the fiscal solvency of local governments. Although the recession officially ended in 2009, concerns linger regarding its lasting effects. The recession potentially caused a structural change in the way private developers view public entities. On the other hand, the negative effects of the recession might have been temporary. Did the recession cause a temporary or lasting change in the perceived credible commitment of the public sector?

Research Design

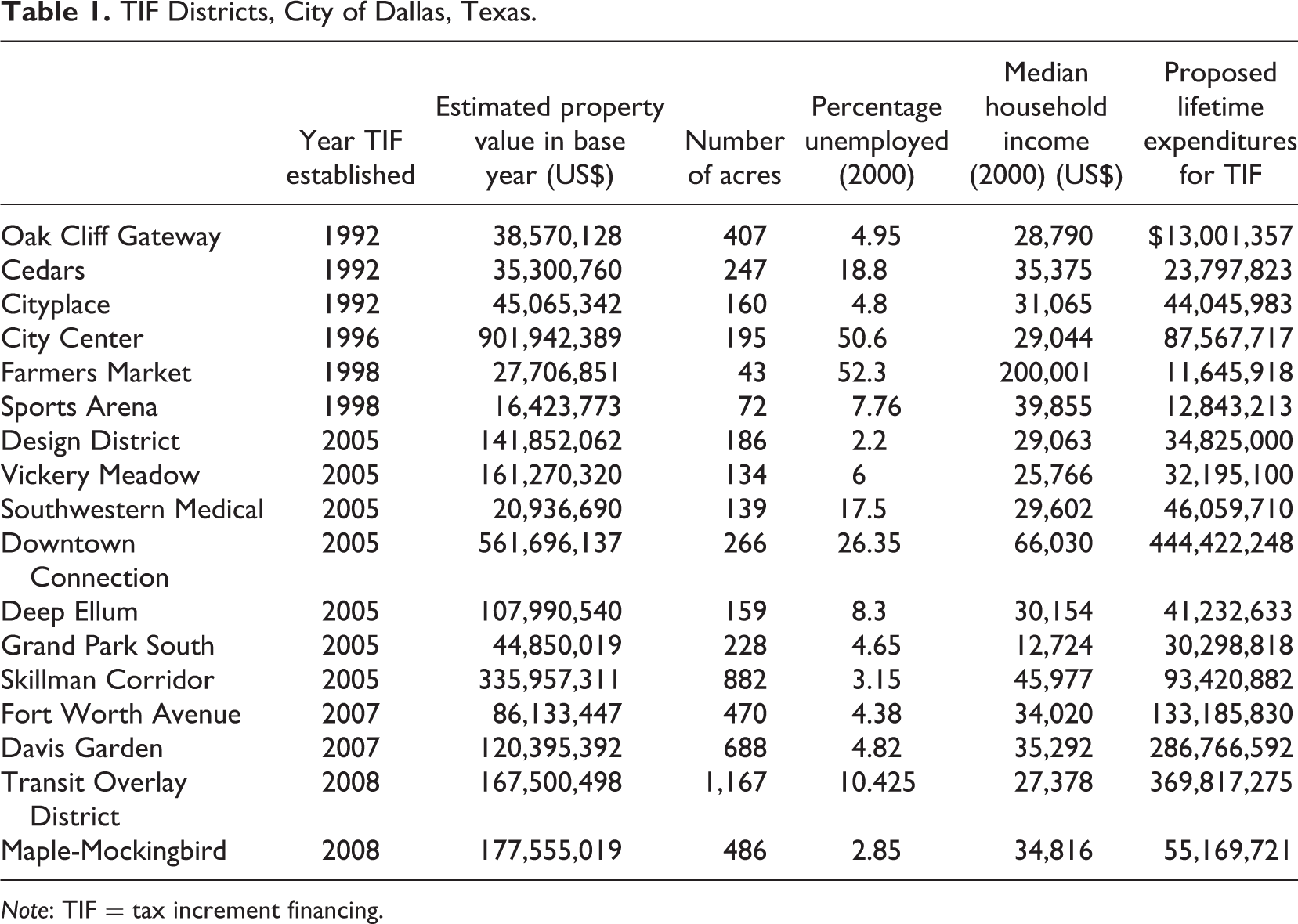

This study examines the impact of the recession on the perceived credible commitment of the city of Dallas using private sector participation in seventeen TIF districts. (The first TIF district established by the city of Dallas was excluded from the sample because the city had not yet adopted the practice of preparing a lifetime budget for the project.) Previous TIF studies have examined the impact of TIF either at a macro level where property values at the city level are the unit of analysis or at a micro level where the parcel of land is the unit of analysis. This study uses the TIF districts themselves as the unit of analysis. Table 1 provides a brief description of each district. Data were collected between 1992 and 2011 for the years that a TIF district was operational ranging in age from nineteen years (e.g., Oak Cliff) to four years (e.g., Maple-Mockingbird). The final set of observations constitutes an unbalanced panel data set with 188 observations.

TIF Districts, City of Dallas, Texas.

Note: TIF = tax increment financing.

Limiting the analysis to one city controls for administrative and policy differences that vary across municipalities and impact TIF implementation. It also has enabled collection of more detailed data at the TIF district level thereby allowing us to ask theoretically richer questions. On the other hand, restricting the analysis to just one city does limit the generalizability of the findings.

Data

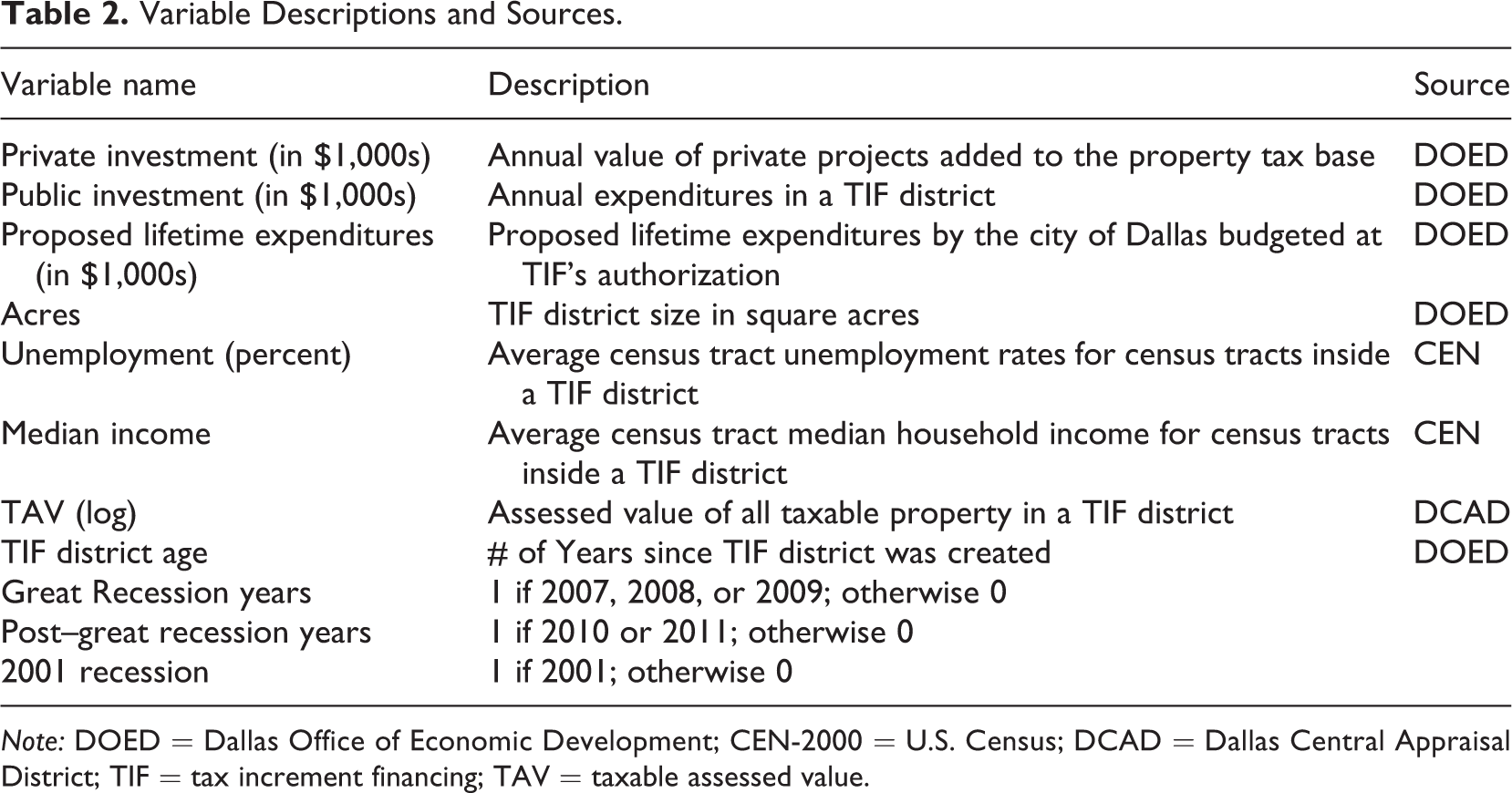

Data for this analysis were collected from the Dallas OED, the Dallas Central Appraisal District (DCAD), and the U.S. Census Bureau. Data on public investment, private investment, and the proposed lifetime expenditure budget of each TIF district were collected from the annual TIF district reports published by the OED as was the acreage of each TIF district. The annual taxable assessed values (TAVs) for each TIF district were collected from the DCAD. Data for unemployment rates and the median household income were collected from the 2000 Census. Private investment, public investment, median household income, and proposed lifetime expenditure budget were adjusted for inflation. Table 2 contains a full description of the variables and their sources.

Variable Descriptions and Sources.

Note: DOED = Dallas Office of Economic Development; CEN-2000 = U.S. Census; DCAD = Dallas Central Appraisal District; TIF = tax increment financing; TAV = taxable assessed value.

Dependent Variable

The dependent variable is the amount of private investment added annually to a TIF district. Private investment is the approximate value in dollars of the private projects completed annually in a district. This estimate is reported by the OED in its annual report for each TIF district.

The OED estimates this value using the DCAD appraised value of the project in the year it is completed and added to the tax rolls, which under Texas law is based on fair market value. Only completed projects are included in the tally. Excluded is spending on project development and design not directly connected to the district and on partially completed projects. By restricting the dependent variable to include only completed projects, we are measuring the degree of private participation by fully vested private sector participants.

The amount of private investment added annually to a TIF district is well suited to measure private sector participation. It represents the overall financial commitment made by private developers. Though financial commitment does not capture all of the ways that private developers participate in TIF districts, measuring their financial commitment does have advantages. First, financial commitment can be compared across developers and across TIF districts. Participation in other ways (i.e., attending TIF district annual budget meetings, public hearings, or planning meetings) is likely to vary among developers and across TIF districts.

Another advantage is that private investment directly measures the degree of risk that developers, in the aggregate, are willing to take in a TIF district. Putting dollars on the table does not constitute “cheap talk.” Unlike nonmonetary forms of participation, the sunk costs associated with private investment in a failed public–private partnership have far-reaching consequences for the private developer and its stockholders. In short, private investment shows a developer’s relative commitment and the degree of risk they are willing to accept.

Explanatory Variables

The two explanatory variables central to this analysis are public investment and the proposed lifetime expenditures (budget) by the city in a TIF district. Public investment is the actual amount spent annually by the city of Dallas in each TIF district. It is operationalized as the sum of a TIF district’s annual expenditures for administration, interest, capital, and other expenditures as reported in the annual report prepared by OED for each TIF district. Expenditures for services in the TIF district but paid out of the city’s general fund were not included.

The proposed lifetime budget is the estimated aggregate expenditures by the city of Dallas over the expected life of the TIF district. After preliminary discussions with developers, a list of capital projects is prepared. The city’s contribution to project costs, including the installation of infrastructure, is used to estimate the TIF budget. The proposed expenditure budget is generated before the TIF district is approved and does not change thereafter.

However, the proposed budget does not obligate the city to the proposed projects or the level of spending specified in the budget. The city’s financial contribution is contingent on the TIF district generating revenue from the incremental increases in taxable value above the base level of value projected in the expenditure budget. If property values fail to increase at the expected rates and property (or sales) tax revenue falls short of projections, the city will modify its actual spending accordingly. The proposed budget is not legally binding on the city. The perceived validity of a TIF district’s proposed lifetime expenditures to a private developer is contingent on the credibility of the commitment made by Dallas and not on any legally binding obligations.

Previous research has found that urban blight is an important determinant of both TIF adoption (Dye and Merriman 2000) and TIF success (Byrne 2006). Urban blight generates negative externalities that have detrimental effects on property values in a neighborhood. It is also a major obstacle to attracting private investment. TIF is used to counter blight’s effects and attract private investors to an area with business potential.

A key control variable used to measure blight is the annual TAV of each TIF district. TAV captures the overall wealth of a TIF district. The DCAD annually prepares an appraisal of the taxable value of the individual properties in each district. The summed TAV of all properties in the TIF district is then logged in order to normalize the variable. Texas law requires that appraisals be at 100 percent of fair market value and reappraisal occurs annually. TIF districts with higher TAV are expected to have greater levels of private investment because developers will view those districts as safer investments.

Two other variables are included to account for urban blight: unemployment rate and median household income. Data on these measures were obtained by census tract from the 2000 U.S. Census. Because the boundaries of census tracts and TIF districts are not coterminous, a two-step process was used to construct the measure. First, a map with Dallas County census tracts was overlaid with a map of the seventeen TIF districts. Second, the observed blight values for the census tracts encompassing a TIF district were then averaged across tracts.

Because the analysis is restricted to one city, we can more accurately measure whether experience using TIF has an effect on the performance of public–private partnerships. We use TIF district age—the number of years a TIF district is operational—as a surrogate for the acquisition of knowledge in the development, implementation, and management of a TIF district. As a TIF district ages, its administrators gain operational experience to solve problems idiosyncratic to that district. This operational knowledge should directly translate into better outcomes for both private developers and the host city. Thus, we anticipate that an increase in TIF age results in an increase in private investment due to the increased administrative capacity of that district to generate better economic benefits for private developers.

Two dummy variables were added to account for the effects of the recession on private investment. The first is coded 1 for the years of the Great Recession (2007–2009) and 0 otherwise. The second is for the postrecession years and is coded 1 for each year in the sample after the recession (2010 and 2011) and 0 otherwise. The postrecession measure tests for structural changes caused by the recession. We are interested in determining whether the effects of the recession on credible commitment lingered beyond the recession creating a structural change in the way private developers view the city or whether credible commitment returned to prerecession levels.

Research Methods

Panel data require analytic methods that take into account both the cross-section variation and the variation across time. The more commonly used methods are fixed effects (FEs) and random effects (REs) estimation methods. FE models cannot estimate time-invariant explanatory variables. Since one key explanatory variable in this analysis is time-invariant—proposed lifetime expenditures—RE models are used to generate the estimates.

The dependent variable is the annual amount of private investment in a TIF district. Private investment is censored below zero; that is, it is impossible for a private investor to invest negative amounts in a TIF district. Estimation using standard linear models would result in biased and inefficient estimates (Tobin 1958). While most variables can be considered theoretically censored, not all variables have enough observations at the threshold value to validate the use of a Tobit model. Private investment, however, has eighty-six observations at zero, roughly 46 percent of the sample, making Tobit the appropriate methodology for estimating the effects on this dependent variable. To account for both the panel data issues and the censored dependent variable, an RE Tobit model is used to generate the estimates.

Results

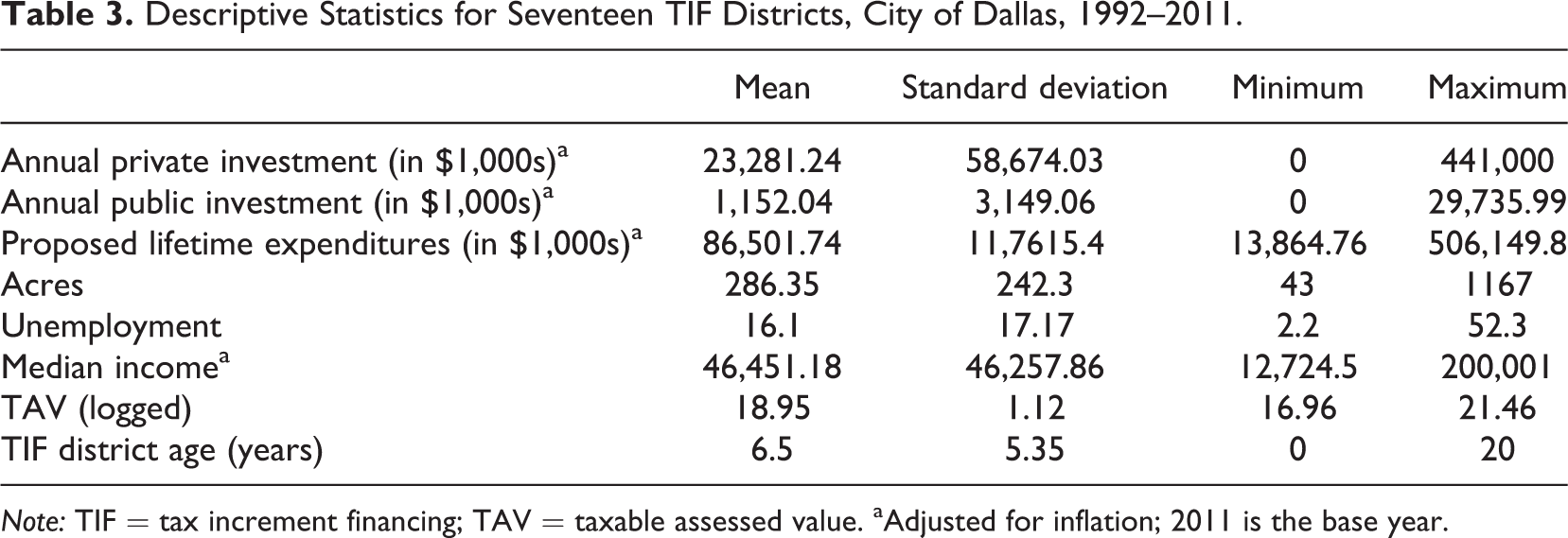

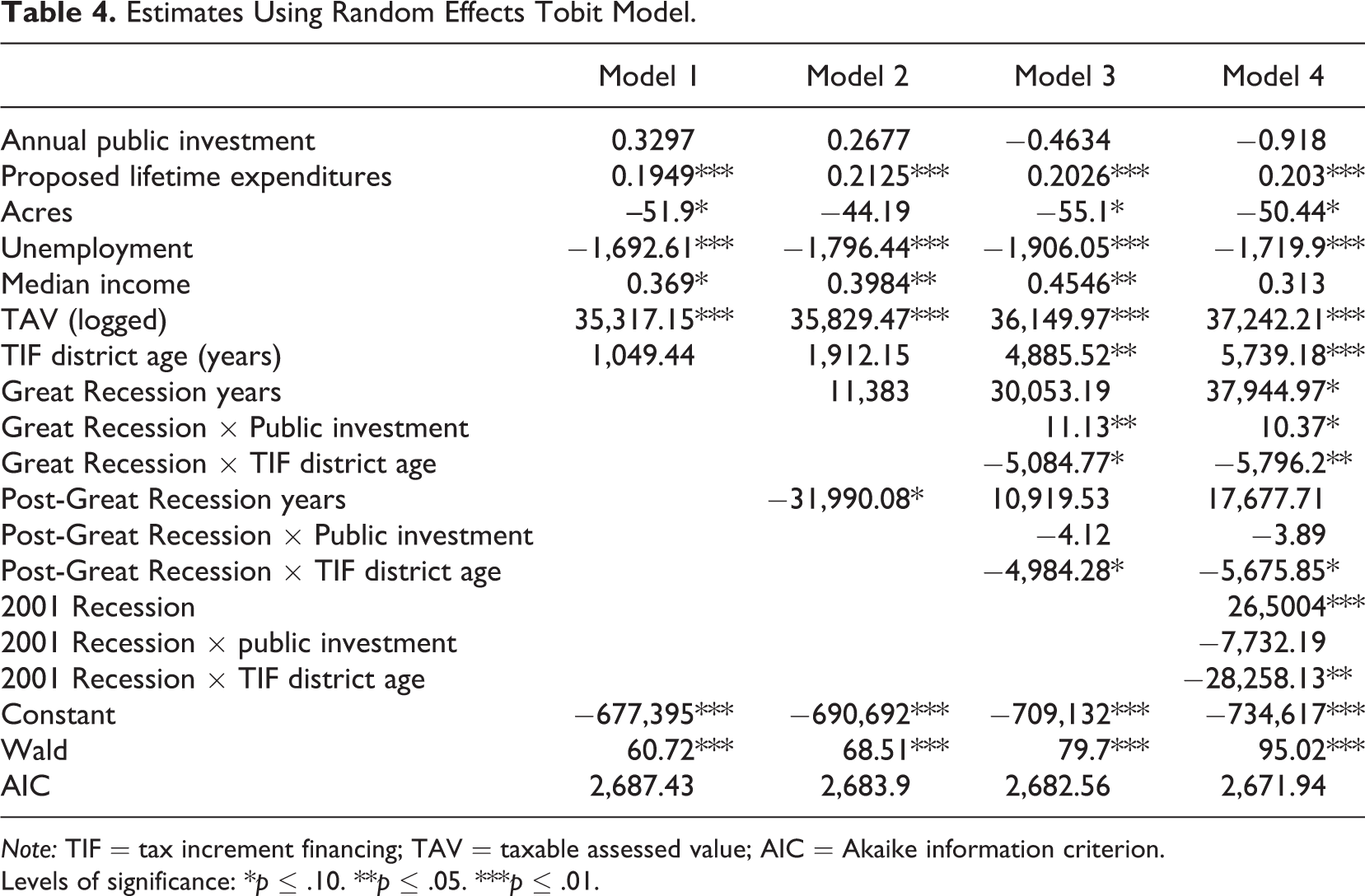

Table 3 reports the descriptive statistics for the variables used in this analysis. The results of the RE Tobit models are reported in Table 4. The Wald test statistics indicate that the joint significance of the independent variables in each model was statistically significant at the 99 percent confidence level.

Descriptive Statistics for Seventeen TIF Districts, City of Dallas, 1992–2011.

Note: TIF = tax increment financing; TAV = taxable assessed value. aAdjusted for inflation; 2011 is the base year.

Estimates Using Random Effects Tobit Model.

Note: TIF = tax increment financing; TAV = taxable assessed value; AIC = Akaike information criterion.

Levels of significance: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

Model 1 provides baseline estimates for the predictors of theoretical interest, which are all significant except public investment and the age of the TIF district. Model 2 adds a dummy for the Great Recession years and another for the postrecession years. Model 3 adds the following four interaction terms: (1) the Great Recession with public investment, (2) the Great Recession with TIF district age, (3) the postrecession years with public investment, and (4) the postrecession years with TIF district age. The fourth model, which is discussed more fully later, tests whether the effects of the Great Recession held up during the earlier and less severe recession of 2001.

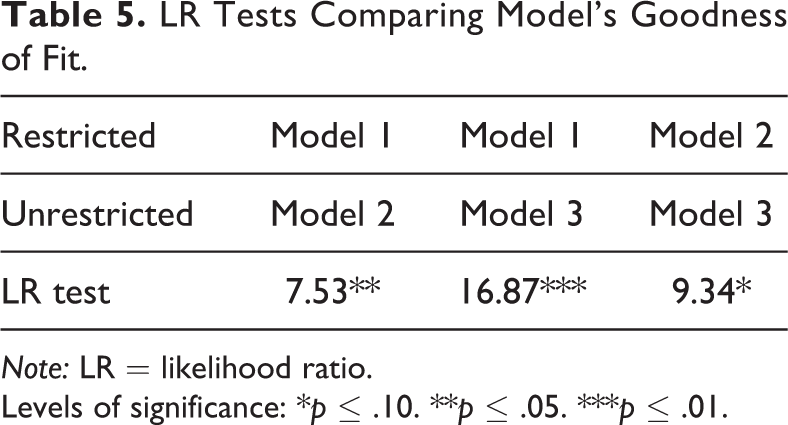

The likelihood ratio (LR) tests reported in Table 5 corroborate the statistical importance of the dummy variables and interaction terms. LR tests comparing the three models are all statistically significant. These findings indicate that the addition of dummy variables and interaction terms in models 2 and 3 adds predictive power to the model. Overall, model 3 is the best fitting model of the three.

LR Tests Comparing Model’s Goodness of Fit.

Note: LR = likelihood ratio.

Levels of significance: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

Since the regression results were estimated using RE Tobit models, the coefficients cannot be easily and substantively interpreted. Only their statistical significance and direction can be easily extrapolated. This limitation does not inhibit our inference of the results. Statistical significance and direction of the relationship are the central characteristics of the variables required to understand the association between our independent and dependent variables. While substantive interpretation of the estimates can be helpful to understanding the marginal effects of predictors on the dependent variable, those interpretations are not essential for hypothesis testing.

The results in all four models support Hypothesis 1, namely that, in the presence of credible commitment, the city’s announced budget for each TIF district was a highly significant factor in promoting private investment in TIF partnerships. The coefficients for the proposed lifetime expenditures in a TIF district are positive and statistically significant at a 99 percent confidence level. According to model 3, at the average values of all the independent variables, a US$1 increase in the proposed level of public expenditures in a TIF district results in an average 20 cent increase in private investment, holding all other variables constant. This represents a substantial level of investment for a nonlegally binding proposal. Overall, the findings provide statistical evidence that TIF district proposals by the city of Dallas were viewed as credible commitments by private developers.

On the other hand, Hypothesis 2 is not supported by any of the four models. Annual public expenditures in the TIF districts had no significant effect on the amount of private investment in these seventeen TIF districts. Model 3 corroborates these findings, but must be interpreted conditionally due to the interaction terms that include public investment. According to the estimates in model 3, an increase in public investment had no impact on the level of private investment in a TIF district before the recession.

An argument can be made that private investment drives public investment. As private investors commit to new projects in the TIF district, the city must respond with new investment in infrastructure. However, this causal direction does not hold for two reasons. First, TIF districts are created because private investment has lagged behind what is potentially possible, at least from the perspective of city planners. The city’s investment is needed to jump-start investment in the district. Second, if private investment was the driver for public investment, then estimates for public investment would be significant for all the models in Table 4, which is not the case. We conclude that the city of Dallas has established credible commitment with private developers who look to the city’s proposed lifetime expenditures, not the annual amount of public spending, when making their investment decisions, at least those decisions before and after the Great Recession.

As for the Hypothesis 3, model 3 provides interesting findings. The statistical significance of the interaction term between the Great Recession and public investment shows that during the recession an increase in public investment resulted in an increase in private investment. According to model 3, at the average values of all the independent variables, a US$1 increase in public investment in a TIF district during the Great Recession results in an average US$11.13 increase in private investment, holding all other variables constant.

The insignificant estimate for the interaction between post-Great Recession and public investment, however, reaffirms that, in the years following the Great Recession, private investors once again looked to other signals for the city’s commitment to the partnership. While public investment had no effect on the level of private investment before and after the recession, the level of public investment by the city of Dallas during the Great Recession was positive and statistically significant. A reasonable explanation is that actual annual public spending during the Great Recession reassures private investors of the city’s commitment at a time when investors may have doubts about that commitment.

Models 1–3 paint a vivid picture of the role of public investment before, during, and after the Great Recession and of the city’s proposed lifetime expenditures for each TIF district in fostering private investment. Before and after the recession, the annual expenditures by the city of Dallas are not statistically related to the annual amount invested by private developers in a TIF district. However, the recession caused enough doubt in the fiscal solvency of the city that during the Great Recession private developers invested in TIF districts where the city was investing. Then after the recession, the city’s actual expenditures were once again an insignificant signal to private developers, implying that during times of perceived fiscal stress, private developers look for reassurance of the city’s commitment. During periods of severe economic stress, they require more than just words but also that the city “put its money where its mouth is.”

The insignificant estimates for the Great Recession years in models 2 and 3 indicate that the level of private investment in a TIF district was not directly affected by the recession. However, the interaction of the Great Recession with public investment in model 3 shows that the recession has a mediating impact on private investment through other variables. The insignificant estimates for both postrecession years and its interaction with public investment in model 3 suggest that those effects disappeared in the postrecession years.

The relationship between TIF age and private investment is complex. Models 1–3 provide conflicting statistical evidence regarding the impact of TIF age on private investment. In models 1 and 2, the insignificant estimates for TIF district age imply that the age of a TIF district is not correlated with the level of private investment in that TIF district. However, with the addition of the interaction terms in model 3, the coefficient is positive and statistically significant. The coefficient for the interaction term between TIF age and the recession is negative and statistically significant, implying that older TIF districts received less private investment during the recession.

Furthermore, the negative and significant interaction between TIF district age and the dummy for postrecession years indicates a structural change in private investment that persisted after the Great Recession. Older TIF districts would have been planned and financed from a prerecession mind-set. There is an intuitively appealing lesson, albeit based on conjecture, in this explanation: older institutions no longer provide the investment returns expected by private investors and no longer engender the credible commitment that newer institutions do. Newly designed TIF districts can take into account all of the lessons from previous TIF districts, in addition to taking into consideration the recession-tempered fears and expectations of private developers.

The models do not provide conclusive evidence on the nature of the relationship between TIF district acreage and private investment. First, models 1, 3, and 4 indicate that acres are statistically significant while model 2 indicates insignificance. Second, the sign of acre’s coefficient when the variable is statistically significant is negative, suggesting a possible inverse relationship between TIF district size and private investment. We speculate that larger TIF districts may lie further out from the urban core and provide lower rates of return to investors, thereby attracting less private investment.

The control variables for blight provide consistent results that operate as expected. Lower unemployment rates, higher median incomes, and higher TAV are associated with higher levels of private investment. Both the coefficients and the statistical significance remain constant for unemployment, median income, and TAV for all the models. Both TAV and unemployment are statistically significant. Intuitively, lower median incomes, higher unemployment rates, and lower TAV values suggest fewer resources in a TIF district and, thus, less appealing to developers looking to maximize profits. The widely held assumption among economic development circles that blight is a barrier to private investment is corroborated by this analysis.

As a test for the validity of our theories, model 4 examines the response of private investment to the 2001 recession. The 2001 recession is interacted with both TIF district age and public investment. The Wald test statistic of 95.02 indicates that the model is statistically significant. Few differences exist in the signs or significance of the estimates in model 4 from those of model 3. The most significant point is public investment and the proposed lifetime expenditures in a TIF district behave the same in the 2001 recession as they did in the Great Recession (model 3).

While the 2001 recession did affect private investment (both directly and through its interaction with TIF district age), its impact on the economy was not as strong or as prolonged as the Great Recession. But the lower severity and duration of the 2001 recession did not weaken the city’s credible commitment when compared to the Great Recession. While the interaction terms with TIF age for both the Great Recession and the 2001 recession were statistically significant, only the Great Recession had a lingering effect.

Conclusion

The results of the analysis of panel data for seventeen TIF districts for a twenty-year period (1992–2011) show that the Great Recession had an impact on the perceived credible commitment of Dallas to meet its financial commitments. Before and after the recession, private sector participation was driven by the proposed lifetime expenditures by the city in a TIF district and not by its annual expenditure levels. We conclude that the city’s initial budgets were seen as credible commitments by developers who used that information to prepare their development plans and expected investment returns over the life of the TIF district. However, during the recession, annual expenditures by the city of Dallas became a key driver in private sector participation, indicating that the recession weakened Dallas’ credible commitment enough for private developers to expect Dallas to “put its money where its mouth is.”

Furthermore, the Great Recession altered the relationship between older TIF districts and private investment. One explanation is that older TIF districts were designed with a different set of assumptions of what private developers expected from their public partners. If true, public managers leading public–private partnerships should carefully examine the parameters of older TIF districts to ensure that those partnerships can handle the evolving needs of private sector participants.

However, broad recommendations on these findings should be approached cautiously due to the limited sample frame. These findings serve as a starting point for a greater discussion regarding the credible commitment and the lasting effects of the recession on private sector participation in public–private partnerships.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.