Abstract

Many state and local governments have responded to financial challenges facing their pension systems by cutting benefits or by shifting costs to employees. Will these changes make it harder for state and local governments to recruit highly skilled workers? This study explores this question by linking individual-level data from the Current Population Survey on worker transitions between the private and public sectors to measures of state and local pension generosity from the Public Plans Database. The results suggest that state and local employers with relatively generous pensions are better able to recruit high-wage workers from the private sector, but that this advantage is lost as workers are asked to contribute more from current paychecks to prefund those benefits. The findings help inform an ongoing debate over the role that state and local pensions play in shaping the public workforce.

Years of inadequate contributions and financial downturns have left many state and local pensions with large unfunded liabilities (Aubry, Crawford, and Munnell 2017). Nearly all of the large state and local retirement systems have responded by reducing the generosity of pension benefits, often for new hires, and by asking employees to contribute more toward prefunding those benefits (Aubry and Crawford 2017). In general, one expects that locations with more generous benefits, or benefits of equal value but paid for primarily by employers, to be able to attract higher-paid workers from the private sector. Consistent with this view, numerous studies in the private and public sectors document that generous employer pensions reduce worker quits and that people who value pensions are highly productive workers (e.g., Gustman, Mitchell, and Steinmeier 1994; Ippolito 2002; Quinby 2020).

What is not clear, however, is how prospective new hires value pension benefits relative to the cost of prefunding them. If employees value the longevity and inflation insurance provided by defined-benefit pensions more than the actuarial cost, then these plans remain productive tools for recruitment even if governments ask employees to contribute from their salaries to help fund benefits. To our knowledge, empirical evidence on this question is limited. Fitzpatrick (2015) provides the most direct answer, finding that Illinois teachers only value their pension benefits at twenty cents on the dollar; she concludes that deferred compensation is unlikely to attract new employees. Indirect evidence also suggests that public employees prefer wages to pensions. In surveys, public employees often state a preference for current salary over deferred benefits (Pew Charitable Trusts 2016, 2017). And, a growing body of work shows that the separation rate of public employees is inelastic with respect to pension generosity, which suggests that they do not value these benefits at their cost (e.g., K. M. Brown 2013; Knapp et al. 2016; Quinby and Wettstein 2018).

This study makes three contributions to the debate. First, it examines the direct relationship between public pension generosity and governments’ ability to recruit high-wage workers from the private sector. Second, it explores how the recruitment value of a more generous pension is reduced when employees are asked to contribute more toward prefunding those benefits. Third, it develops an empirical strategy for linking private-sector workers, transitioning between sectors, with their public pensions across a wide range of government occupations and geographies.

Determinants of Governments’ Ability to Recruit High-wage Workers

The question explored in this article is how pension generosity and the portion of pension benefits prefunded by employee contributions affect the ability of state and local governments to recruit workers. This section draws on prior literature to predict the factors that should influence recruitment and discusses how these factors are operationalized in the empirical analysis.

A key conceptual issue is how to measure the dependent variable: the earnings potential of government recruits. As its measure, this study uses the wage that new public-sector employees earned in the private sector previous to joining the government. Because factors aside from public-sector pensions will affect the ability of governments to recruit high-wage workers, the analysis uses a regression approach to isolate the effect of pensions. In this approach, measures of pension generosity serve as the independent variables of interest, with other independent variables included as controls. The remainder of this section first discusses the independent variables of interest and then those other controls.

Pension Accrual Rate

In a simple model of job search, increasing the generosity of compensation helps to attract highly skilled workers since job seekers only accept a job offer if the prospective compensation package meets or exceeds the expected value of continued search. 1 The model predicts that, all else equal, governments with generous pension benefits can hire workers who command high wages in the private sector.

The challenge is to find a summary measure of pension generosity that is easily interpretable. As a primary measure, this article uses the normal cost of the pension plan, which equals the present discounted value of lifetime benefits that an employee accrues during the fiscal year and is typically reported as a percent of the plan’s total payroll. 2 Periodically, the analysis differentiates between the employer-paid portion of the normal cost, which corresponds to employee compensation, and the total normal cost, which is also partially paid by employee contributions.

As a present value measure, the normal cost is a function of various actuarial assumptions, particularly the discount rate. The higher the discount rate, the fewer funds must be put aside today to pay for benefits tomorrow. Thus, the empirical analysis in this study develops a standardized pension accrual rate variable that recalculates each plan’s reported normal cost using a 7.8 percent nominal discount rate (the average discount rate during the analysis period). Hence, the standardized pension accrual rate primarily reflects the variance in benefit generosity rather than the assumed rate of return. The first hypothesis of this article is that, holding other factors constant, a higher pension accrual rate is associated with the recruitment of higher-wage workers from the private sector.

Supplemental Table 1 in Supplemental Text 1 provides data over time on the average reported normal cost, the average standardized pension accrual rate, and the average assumed rate of return (discount rate). Despite the fact that many states have implemented pension reforms since the Great Recession, the average reported normal cost has not dropped substantially since 2007 (Aubry and Crawford 2017). The reason is twofold. First, most pension reforms apply only to new workers, a fact often due to state constitutional protections of pension benefits (J. R. Brown and Wilcox 2009; Munnell and Quinby 2012). And second, the average assumed rate of investment return also dropped from 7.8 percent in 2007 to 7.5 percent in 2016. Once the reported total normal cost has been recalculated using a common discount rate, the standardized pension accrual rate drops from 12.6 in 2007 to 11.7 in 2016.

Employee Contribution Rate

As discussed above, employee compensation becomes less generous when workers are asked to prefund the total pension accrual rate through payroll deductions. Table 1 uses data from the Public Plans Database (PPD), maintained by the Center for Retirement Research at Boston College, to show that the average employer contribution to the pension accrual rate has dropped even more than the total accrual rate. This decrease has been made up by increasing employee contributions—a cost-cutting reform that often applies to all workers, not just new employees. Between 2007 and 2016, employers’ contributions to the (standardized) normal cost dropped from 7.3 percent of payroll to 5.2 percent while employees’ contributions increased from 5.3 percent of payroll to 6.5 percent. The second hypothesis of this article is that plans requiring workers to prefund more of their own pensions lose some of the recruitment benefit of the plan and are less able to attract high-wage workers.

Mean Pension Accrual Rate (2001–2016).

Source: Authors’ calculations from the Public Plans Database (2001–2018).

Note: Normal cost has been standardized across plans and over time using a constant discount rate. All numbers shown are weighted by the number of regression sample members in the plan.

Actuarial Cost Method

The actuarial cost method used by public pensions to calculate their normal cost is a key control variable in the analysis. Some actuarial accounting frameworks (such as projected unit credit) backload costs while others (such as aggregate cost) do not differentiate between benefit accruals and the amortization of unfunded liabilities. This difference can cause the reported normal cost to be higher in some plans than others, even given the same level of underlying generosity (Munnell, Aubry, and Quinby 2010). Ideally, this study would recalculate the plans’ reported normal cost using a common actuarial cost method, similar to how it adjusted for the discount rate. However, since this type of recalculation cannot be performed using a simple rule of thumb, binary variables for each actuarial cost method used in the public sector will instead feature as control variables in the empirical analysis.

Relative Attractiveness of Public-sector Work

Aside from pensions, many other aspects of public-sector compensation may affect how easily governments recruit workers from the private sector. If these factors are correlated with the pension accrual rate, then failure to control for them will contaminate the estimated effect of pensions. For example, if public-sector employers with generous pensions also offer higher wages, then in the absence of a control for wages, the estimated effect of pension generosity would be biased upward. This article includes the following controls in an attempt to isolate the effect of pensions:

Private-sector wage level in state: By including this control for the median wage in the private sector in the worker’s state, the regression asks whether public employers with generous pensions recruit workers who are competitive in the local labor market. For example, whether the New York state government recruits workers whose private-sector wages are high in the state of New York rather than high nationally.

Public-sector wage premium: All else equal, workers will be more attracted to public-sector jobs that offer higher wages relative to the prevailing wage in the private sector (Borjas 2002; Katz and Krueger 2000). The wage premium is estimated for workers in the public and private sectors with similar demographic profiles in the same state.

3

Social Security coverage: Workers who are covered by social security have the additional benefit of employer contributions to that program (Quinby, Aubry, and Munnell Forthcoming).

Health insurance coverage gap: Nationally, state and local government employers are more likely to provide health insurance than the private sector (U.S. Bureau of Labor Statistics 2019). The difference in coverage rates is estimated for active employees in a person’s state.

Unionization gap: Workers may be more attracted to public-sector jobs with a high rate of unionization relative to the private sector since union coverage may be a proxy variable for unobserved job amenities (Freeman and Medoff 1984; Munnell et al. 2011). This variable is calculated in the same manner as the public-sector wage premium.

Worker Characteristics

Finally, the analysis controls for demographic variables that are standard in the labor economics literature on wage determination:

College degree: Education has been shown to generate higher wages (Card 1999) and may also be correlated with preference for retirement saving or the skills sought by government employers. Education is included in the analysis as two binary variables indicating whether the worker has completed some college or a college degree.

Age: Similarly, older workers tend to have more experience and higher wages (Weiss 1986) but also prioritize retirement saving (Pew Charitable Trusts 2016). Since age–wage profiles are not typically linear, the analysis controls flexibly for ten-year age ranges using a series of binary variables.

Male: Gender wage gaps have been well-documented in the labor market due to factors ranging from preferences for amenities over wages, discrimination, and time spent working in the home (Altonji and Blank 1999; Goldin 2014; Goldin et al. 2017; Goldin and Katz 2011).

Black: An equally large literature documents the wage penalty suffered by black workers (Altonji and Blank 1999; Fryer 2011).

Police officer or firefighter: Pensions for police and firefighters tend to have a higher normal cost than for other occupational groups because hazardous-duty workers often retire earlier (Aubry and Wandrei 2020).

Teacher: The educational requirements for teachers are often higher than for other government employees, suggesting that they could command higher private-sector wages.

Methods and Data

Model Specification

The main analysis takes a multiple linear regression approach, where each new recruit to the public sector enters the regression as one observation, and the dependent variable is the log of the individual’s wage the year before they transitioned to a public-sector job; the independent variables are as described above with a few additional notes. First, variables that measure rates (the pension accrual rate and employee contribution rate) are coded on a scale from 0 to 100, so a one-unit increase in these variables represents a 1 percentage point increase in the rate. Variables that reflect gaps between the public and private sectors (the public-sector wage premium, health insurance coverage gap, and unionization gap) are coded similarly to rates. And last, variables that reflect wage levels (the dependent variable and the private-sector wage level in state) are first adjusted for inflation and then coded as natural logs so as to facilitate a percent interpretation of the regression coefficients.

The main regression exploits variance in pension generosity and employee contributions across plans not within them. Exploiting this across-plan variance has a better chance of finding an effect since the variance of a plan’s accrual rate across time is small compared to the variance across plans at any point in time. However, because the control variables described above may not capture other unobservable aspects of the public-sector job which are correlated with both public pension benefits and a worker’s competitiveness on the labor market (e.g., work environment), a follow-on analysis shows results from a fixed effect regression. This analysis collapses the individual-level data on new recruits to the plan level so that there is one observation per pension per year. Each independent variable takes on the average value for that plan in that year (e.g., 40 percent of new hires had a college degree). The fixed effect regression then determines whether the average private-sector wage of new hires increases when the pension accrual rate also increases, relative to the average accrual rate for that plan over the entire analysis period. The regression is weighted by the number of new hires in the first year that the plan is observed in order to avoid the endogeneity that could arise if benefit reductions are also associated with reductions in the number of new hires.

Data

To estimate the relationship between pension generosity and the private-sector wage of workers entering the state and local sectors requires merging several data sets. The Current Population Survey Outgoing Rotation Group (CPS-ORG) is used to follow workers between the private and public sectors. However, these data contain no information about pension generosity. Thus, data on state and local pension generosity must be obtained from another source, in this case the PPD. Both of these data sets are described below, as is the process for merging data between them.

CPS-ORG: The CPS is a joint effort between the U.S. Bureau of Labor Statistics and the U.S. Census Bureau and is the primary source of labor force statistics in the United States (U.S. Census Bureau 2001-2017). The CPS is a probability sample of addresses, with all eligible residents of a sampled address surveyed. For the purposes of this study, it provides demographic information on survey respondents including age, race, education, and state of residence and information on employment including class and sector of employment (private, state and local, federal, etc.), occupation, hours worked, health insurance coverage, and weekly earnings for some months.

Because of the timing of interviews conducted by the CPS, some individuals can be followed from one year to the next and transitions in sector of employment identified. When an address is selected for inclusion in the CPS, any eligible occupants will be interviewed eight times (unless they leave the address). These interviews are conducted nonconsecutively; interviews occur during the first four consecutive months, then eight months elapse, and interviews are restarted for an additional four consecutive months. An address’s fourth and sixteenth months in the survey are called “outgoing” months because its residents will either not be interviewed again for eight months (if in the fourth month) or will exit the sample entirely (if in the sixteenth month). Interviewees in the “ORG” are asked a more detailed set of questions than in other months—including their average weekly earnings. Because of the eight months off, individuals who remain at the same address have their outgoing interviews one year apart. If merged carefully, this longitudinal feature of the data can be used to determine whether individuals who were working in the state and local sector in a given year transitioned to the private sector in the following year and vice versa. 4

PPD: The PPD is a comprehensive database of financial, governance, and plan design information for approximately 180 state and local defined benefit plans, spanning the years 2001–2018. The data are maintained by the Center for Retirement Research at Boston College—in collaboration with the Center for State and Local Government Excellence and the National Association of State Retirement Administrators—and cover over 85 percent of state and local government employees in the United States. For the purposes of this study, the most important pieces of information collected by the PPD are the employers’ and the employees’ contribution to the total normal cost of the pension.

Ultimately, data from the PPD on pension generosity and cost sharing are merged onto the CPS data. For workers who transitioned to state employment, the PPD data are merged onto the CPS using a combination of information on the individual’s state of residence and their occupation (if their state has a specific plan for some workers, e.g., the Oklahoma Teachers Retirement Plan). For local workers, municipal plans were taken into account where possible. 5

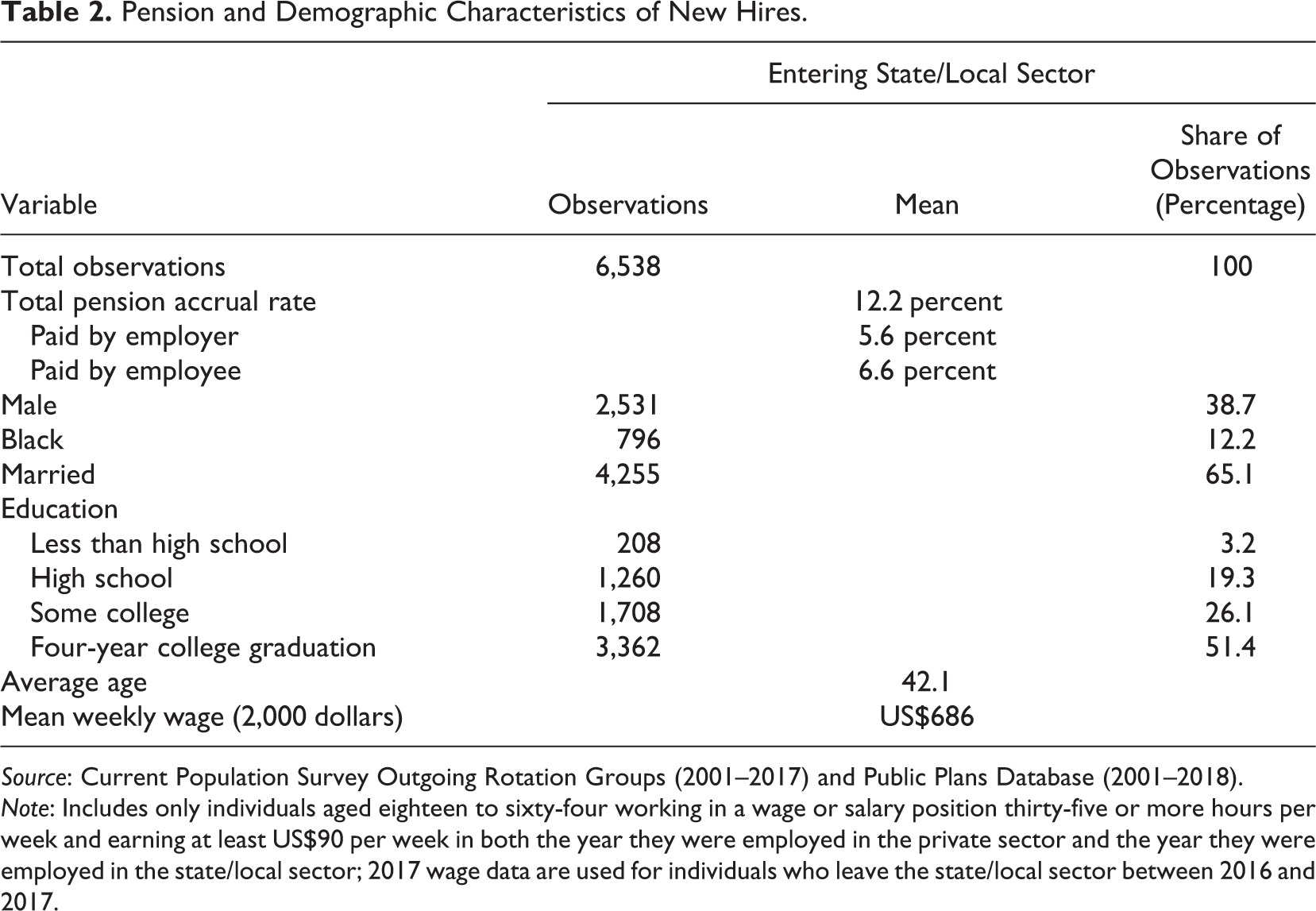

In the end, the article focuses on the private-sector wages of 6,538 full-time workers aged 18–64 who were successfully merged onto normal cost data from the PPD and who were just entering the state or local sector from the private sector (new hires). Table 2 summarizes the demographic characteristics of new hires for the period 2001–2016; the sample is 39 percent male, 12 percent black, and 65 percent married. Slightly more than half of new hires had at least a four-year college degree.

Pension and Demographic Characteristics of New Hires.

Source: Current Population Survey Outgoing Rotation Groups (2001–2017) and Public Plans Database (2001–2018).

Note: Includes only individuals aged eighteen to sixty-four working in a wage or salary position thirty-five or more hours per week and earning at least US$90 per week in both the year they were employed in the private sector and the year they were employed in the state/local sector; 2017 wage data are used for individuals who leave the state/local sector between 2016 and 2017.

Empirical Results

Results from the linear regression appear in Table 3. Column (1) supports the intuition that generous pension benefits recruit high-wage workers from the private sector. A 1 percentage point increase in the employer pension accrual rate is associated with a 0.48 percent increase in the mean private-sector wage of new hires, and the coefficient is highly statistically significant. Reassuringly, the coefficients on other job attributes, such as the public-sector wage premium and health insurance gap, are also in the anticipated direction and often statistically significant.

Determinants of the Private-sector Wage of Newly Hired State and Local Government Employees.

Source: Authors’ estimates from the Current Population Survey Outgoing Rotation Groups (2001–2017) and Public Plans Database (2001–2018).

Note: Numbers in parentheses are robust standard errors with clustering at the state-year level.

* Significance at the 10-percent level.

** Significance at the 5-percent level.

*** Significance at the 1-percent level.

The story becomes more interesting in column (2) when the employer pension accrual rate is replaced with the total pension accrual rate and the employee contribution rate is added as an explanatory variable. As before, when employers bear the entire cost of the pension, a 1 percentage point increase in the total pension accrual rate is associated with a 0.47 percent increase in the mean private-sector wage of new hires. Yet, each percentage point increase in the employee contribution rate is associated with private-sector wages that are 0.53 percent lower. These offsetting coefficients suggest that a pension enhancement fully funded by employee contributions should have little effect on recruitment. Both coefficients are statistically significant at the 5 percent level. Supplemental Tables 3, 4, and 5 in Supplemental Text 1 perform several robustness tests on this main result, including testing the sensitivity of the coefficients to model specification.

Table 4 shows the results from the fixed effect regression that takes advantage of within-plan variance in generosity. Consistent with the main analysis, column (1) shows that a 1 percentage point increase in the employer pension accrual rate is associated with a 0.7 percent increase in the average private-sector wage of new hires. Column (2) replaces the employer pension accrual rate variable with variables measuring the total pension accrual rate and the employee contribution rate and finds the same offset described in the main analysis. However, a relative lack of within-plan variance in the employee contribution rate worsens the statistical significance of that variable.

Relationship between Within-plan Changes in Select Variables and Change in the Private-sector Wage of Newly Hired State and Local Government Employees.

Source: Authors’ estimates are from the Current Population Survey Outgoing Rotation Groups (2001–2017) and Public Plans Database (2001–2018).

Note: Numbers in parentheses are robust standard errors with clustering at the plan level. Variables that do not change within a plan over time are dropped from the regressions. The regression is weighted by the number of new hires in each plan during the first year that the plan is merged with the Current Population Survey Outgoing Rotation Groups.

* Significance at the 10-percent level.

** Significance at the 5-percent level.

*** Significance at the 1-percent level.

Ultimately, these results suggest that many state and local governments currently ask their employees to pay too much for their pension benefits to reap a positive effect on recruitment. Recall from Table 1 that employees contributed about 56 percent of the total pension accrual rate in 2016, on average. Enhancing the total pension accrual rate by 1 percentage point while maintaining this cost-sharing arrangement is only associated with a statistically insignificant 0.15 percent increase in the private-sector wage of new hires. The regression results also allow an estimate of how much the changes that have occurred over the last decade have reduced state and local government’s ability to recruit workers from the private sector. From 2001 to 2016, the total normal cost of public pensions decreased by 0.6 percentage points and the employees’ share of those costs increased by 1.6 percentage points. Combined, and without a compensating wage increase, the effect is to reduce the private-sector wages of workers entering the public sector by just over 1 percent. This decrease is statistically significant and nontrivial relative to the overall public–private pay difference; according to the public–private wage differentials described above, public-sector workers make 4 percent less than similar private-sector workers.

Conclusion

States and localities have reduced the generosity of their pensions for new hires while increasing the share of those pensions paid by employees. This article asks a simple question: what will the impact of these changes be on state and local governments’ ability to recruit highly skilled workers from the private sector?

The analysis suggests that the changes may be detrimental. Reducing the monetary value of future pension benefits is associated with lower private-sector wages among new recruits, as is increasing the required employee contribution rate. Taken together, these findings imply that workers value generous pensions but are not willing to pay for them out of current salaries. Although pensions may not be the most efficient way to recruit high-wage workers from the private sector, the analysis does not speak to the other benefits that employers gain by offering a pension, for example, the ability to better control the timing of workers’ retirement or to retain workers at certain points in their careers.

This article should sound a note of caution for states and localities reforming their pension benefits. Reducing those benefits while simultaneously maintaining or even increasing the employees’ contribution—as has occurred over the last decade and a half—will likely reduce governments’ ability to hire high-wage individuals from the private sector unless the changes are offset with salary enhancements. Future research should consider how the changes to date have affected the performance of the public workforce and should keep an eye on future changes.

Supplemental Material

Supplemental Material, SLGR_19-0086R3,_Text_1_Supplement - Do Pensions Matter for Recruiting State and Local Workers?

Supplemental Material, SLGR_19-0086R3,_Text_1_Supplement for Do Pensions Matter for Recruiting State and Local Workers? by Laura D. Quinby and Geoffrey T. Sanzenbacher in State and Local Government Review

Footnotes

Authors’ Note

The findings and conclusions expressed are solely those of the authors and do not represent the views of the Center for Retirement Research or Boston College. Any mistakes are those of the authors.

Acknowledgment

The authors thank Mark Rider and attendants at the National Tax Association Annual Conference’s session on “Decision Making in State and Local Public Finance” for helpful comments.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

The supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.