Abstract

In 2010, Virginia Commonwealth University (VCU) was granted a Clinical and Translational Science Award which prompted reorganization and expansion of their clinical research infrastructure. A case study approach is used to describe the implementation of a business and cost recovery model for clinical and translational research and the transformation of VCU’s General Clinical Research Center and Clinical Trials Office to a combined Clinical Research Services entity. We outline the use of a Plan, Do, Study, Act cycle that facilitated a thoughtful transition process, which included the identification of required changes and cost recovery processes for implementation. Through this process, the VCU Center for Clinical and Translational Research improved efficiency, increased revenue recovered, reduced costs, and brought a high level of fiscal responsibility through financial reporting.

Introduction

When Virginia Commonwealth University (VCU) was granted a Clinical and Translational Science Award (CTSA) in 2010, the Center for Clinical and Translational Research (CCTR), founded in 2007, received a highly visible and transformative boost that led to dramatic changes in the research organization of VCU. Nowhere is that more evident than in the restructuring of existing infrastructure to support clinical research. Prior to receipt of CTSA funding, VCU had both a Clinical Trials Office (CTO) and a General Clinical Research Center (GCRC), each designed to support elements of the clinical research enterprise. Receipt of the CTSA provided a unique opportunity to examine current systems and make changes where appropriate.

The purpose of the CTSA is to help institutions create an academic home for Clinical and Translational Science, an academic home with the resources and infrastructure to train and promote multidisciplinary and interdisciplinary investigators and provide access to research tools for applying new knowledge and techniques to patient care. In addition, the CTSA aims to increase the efficiency and speed of clinical and translational research (National Institutes of Health [NIH], 2009).The CTSA aligns with the goals of supporting the research enterprise at VCU.

A significant area of change resulting from the CTSA granted to VCU involved reorganization to streamline operations and a review of mechanisms for financial support of Clinical Research Services (CRS). The GCRC grant formerly provided staff, laboratory analysis, facility space, and informatics and provided resources to help investigative teams with direct financial support from the NIH National Center for Research Resources. The GCRC grant limited the proportion of industry trials conducted with GCRC resources, because it was an infrastructure grant to support research funded by the NIH. Rather than each center within NIH supporting clinical facilities and costs through individual grants, a GCRC was funded centrally to VCU to provide the needed resources for NIH clinical research: Individual grants would not provide those funds independently. To follow these requirements, the GCRC was restricted in the percentage of industry clinical trials it conducted. With the evolution to the CTSA grant, it was structured to provide institution-wide support for researchers and trainees not only in the conduct of the research but also in the development, design, biostatistics, research ethics, regulatory knowledge and support, community engagement, and education. Thus, the CTSA provided a much broader conceptual model for encouraging partnerships with foundations, industry, and communities to foster clinical and translational research. In addition, the CTSA mechanism included the expectation of a significant institutional commitment (NIH, 2009). With the new Request for Applications, the CTSA mechanism allowed for the creation of a model for cost recovery from federally funded research as well as unlimited work with industry-sponsored clinical trials (McCammon et al., 2012).

At the end of August 2011, after reviewing the current state of clinical trials with the GCRC and CTO in light of the new funding mechanism and goals, VCU created the CRS, an organizational unit that combined the efforts of the VCU CTO and GCRC. The mission and goal of the CRS is to increase the efficiency of research services by providing researchers with budget, planning, and regulatory submissions aid, study coordination, research-based laboratory services, a research unit and staff for Phases 1–4 studies, bionutrition services, and Biomedical Informatics. The changes in structure and processes of the clinical research enterprise at VCU required the leadership of the CCTR to perform a needs assessment and identify areas for improvement, including creating a cost recovery model and business plan for the CRS.

Method

This article presents a case study, including implementation of a business and cost recovery model for clinical and translational research and the transformation of a GCRC and CTO to a combined CRS entity. Specifically, we outline, the use of a Plan, Do, Study, Act (PDSA) cycle, which facilitated a thoughtful transition that included the identification of required changes identified and cost recovery processes for implementation (Deming, 1986, 1993).

The PDSA cycle has four stages: Plan, Do, Study, and Act. The PDSA cycle is used to gather information, evaluate, and make appropriate changes in a system or process. During the Planning stage, the goal is to study processes, identify problems, and create a plan for improvement or change. In the Do part of the cycle, the plan is implemented on a test basis and results or improvement are measured and documented. The Study stage includes an evaluation process to determine whether the plan is achieving the desired goals and if any unintended consequences or new problems emerge. In the Act stage, the plan is fully implemented, areas for change are identified, and the cycle starts again at the plan stage (Deming, 1986, 1993).

Implementation, Decisions, and Change

Plan: Spring to Summer 2011

During the Spring of 2011, a leadership team was formed to include the Director of the CCTR, Directors of the former GCRC and the CTO, and the Director of Administration for the CCTR. In the dual roles of Director of CCTR and Associate Vice President for Research, the Director held authority to make decisions for evaluation and planning of the CCTR. Staff of both the GCRC and the CTO participated in the process designed to review and realign the structure and vision of the Center for future opportunities. The first unit of evaluation was the former GCRC. The GCRC was housed in the VCU Health System North Hospital with 10 registered nurses (RN), 11 patient beds, 3 outpatient rooms, a dietitian and staff, full metabolic kitchen, research laboratory, and other support staff. At the time of our analysis, the GCRC was recovering under US$50,000 in study billing from industry-sponsored research per year with an overall budget of 1.5 million dollars. Regulations governing the GCRC mechanism included defined limits on the proportion of clinical research supported by industry. With limited funding granted through the CTSA and the high expectation for rapid growth in other CCTR services, it was clear that if the CCTR was to continue to provide these essential services to the VCU research community, the GCRC component of CRS would need to become more financially self-sustaining. To become more financially self-sustaining, the CRS would need to rely less on the financial support of the CTSA grant and funding from the University and the CRS would need to generate additional financial support through a cost recovery model allowing the CRS to charge for services, such as nursing support and project coordination services.

Along with limited funding opportunities, most federal projects were experiencing reductions in federal awards (Eckelbecker, 2013). This put a high level of stress on the investigators to prioritize their limited funding. One investigator strategy found in our analysis was the escalating use of external laboratory services to preserve funds for personnel or supplies. Our entrepreneurial investigators had discovered that highly efficient private companies were processing samples at a fraction of the cost charged by our institution. It also became clear that investigators needed resources beyond the physical space of the GCRC, and VCU needed to assist research teams where they were located, while maintaining a full service clinical research hospital unit. Finally, the leadership team determined that existing staff would be able to meet current investigator needs. Figure 1 shows the parallel organizational structures of the CTO and GCRC.

Initial organizational structure of the CTO and GCRC. CTO = Clinical Trials Office; GCRC = General Clinical Research Center.

The CTO described in Figure 2 also provided needed services to the university. These services included Institutional Review Board (IRB) preparation, budget development and negotiation, and coordinator services, and the CTO acted as a primary point of contact for industry sponsors looking for potential sites for their clinical trials through feasibility assessments as well as identifying potential investigators conducting the studies. However, the CTO had not yet created a self-sustaining model through the use of cost recovery. Likewise tracking of coordinator time allocation to specific trials and tasks was not yet in place.

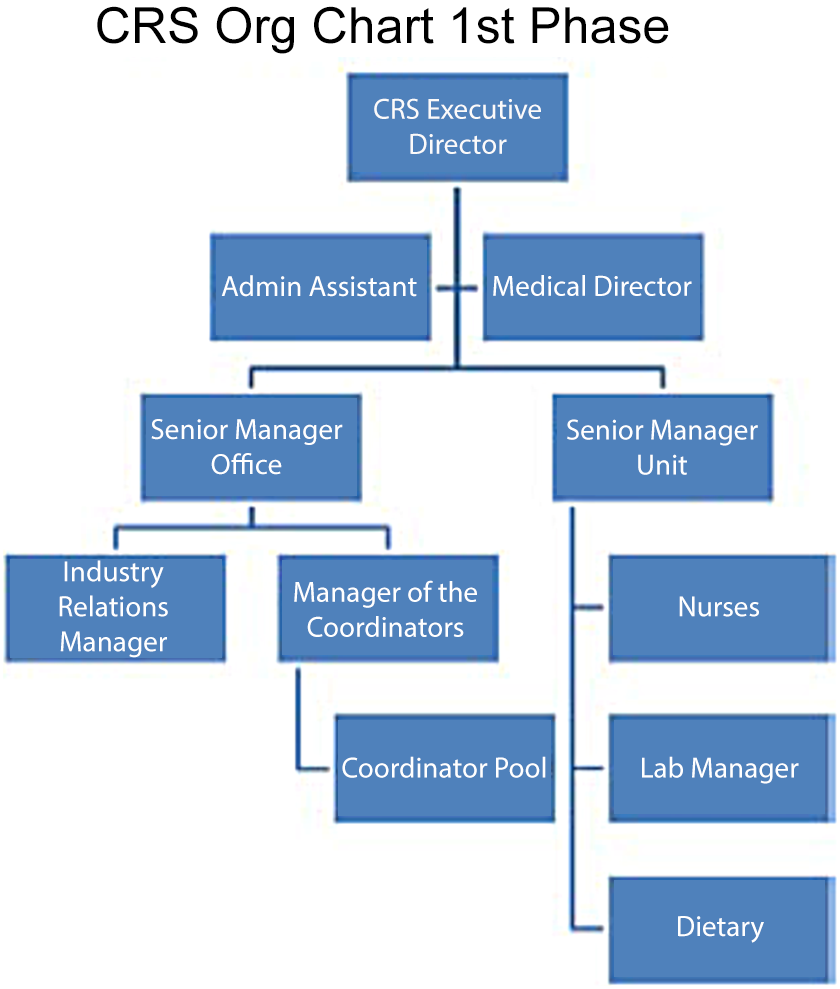

Phase 1 of the CRS organizational structure. CRS = Clinical Research Services.

With a better understanding of the customer base and staff, a tactical business strategy was needed. The initial review indicated that the revenue stream was in considerable flux, with little of the consistency needed for accurate budgeting. In addition, there were no clear procedures for processing invoices, and invoicing was completed on a quarterly basis. This delayed accounting of incoming revenue and in turn delayed financial decisions. Moreover, no revenue or financial reports were being created to track invoicing or cost recovery. As was true for many GCRCs, several computer-based systems were used to manage day-to-day activities. These programs included iCAMP© to manage study participants, locally created systems for bed scheduling, an Access© database for tracking incoming participants, and Lawson©, for billing of patients for standard of care services.

The leadership team reviewed the evaluation of both the CTO and the GCRC noting duplications in services and administration as well as strengths of each system. It was determined that combining the two systems to create a new organizational unit, CRS, would allow: (a) fewer duplicated or conflicting services and (b) decreases in fixed costs of operation through shared leadership and administration. This would enable the VCU CCTR to become a one-stop shop for all services relating to clinical trials. Figure 2 shows Phase 1 of the CRS structure. This phase eliminated one administrative assistant and aligned the reporting structure.

After review of the CTO and GCRC, it was clear that an invoicing and financial process/system was needed to manage the CRS and cost recovery for the CCTR. The main areas that needed to be reconciled were: (1) the disparity between a large budget and low cost recovery of the GCRC and (2) a commitment to provide resources to our investigators. To achieve these goals, the CCTR continued to provide the same services as those offered through the GCRC and CTO mechanisms while transitioning that base to a new business model. While it was important to increase the amount that the former GCRC and CTO could recover and to standardize the rates; a reduction in costs, through an increase in revenue, could be obtained through an increase in the number of industry studies using the CRS.

The next area to be addressed was the establishment of a consistent pricing structure and management. Highly productive meetings with representatives from the Vice President of Health Sciences, Vice President of Research, the University Controllers Office, and the affiliated Health System resulted in a common basis and uniform structure upon which budgets could be reliably created. It was determined that costs for ongoing studies would be honored at previously agreed upon rates. A business plan was designed to guide future planning, maintain focus on the long-term goals and mission of the CCTR, and to develop a new system that would enable tracking of all costs and revenues to help in evaluating the success of the CCTR.

Key actions taken during the Plan stage included:

Merge the GCRC and CTO to streamline resources.

Create a business plan.

Establish standard charges for CRS resources.

Develop a method for tracking invoicing and collecting bills for resources.

With the primary expectation of the planning stage complete, the leadership team set forth to implement the new strategies through the Do portion of the PDSA model.

Do: August 2011

Because of the long-held organizational identity of the GCRC and a more recent push for name recognition and valued service by the CTO, reorganizing the GCRC and CTO into a new entity was a sensitive endeavor. Both organizations were collapsed into a new enterprise called CRS, to include the Clinical Research Services Unit (CRSU) and the Clinical Research Services Office (CRSO). The former GCRC Director became the CRS Executive Director, with the leaders of the CRSO and the CRSU serving as Senior Managers. The administrative unit of the CTO was absorbed by the CCTR Administration, achieving economies of scale and realized cost savings in the administrative area of over US$50,000. The financial management responsibilities of the CTO were also combined with the CCTR, which created a consistency in reporting for the CCTR. Reorganization allowed the CRS to offer services including clinical trial budget planning and negotiation, IRB and regulatory preparation, coordinator support, full hospital support with a full nursing staff, patient beds, the ability to support clinical trials 24/7, dietary support, laboratory and sample analysis, and study closeout.

While formation of the CRS was taking place, the leadership team began to implement the business model. In order to comply with university regulations, the new enterprise would need to be created as a service center, an organizational unit involved directly in revenue generation and providing support services to other organizational units or subunits. The basic elements of a business model were generated along with the charges and accounting plans for the new enterprise. The service center was placed at the Center (CCTR) level. This permitted the inclusion of additional CCTR core services including Biomedical Informatics.

Based on the activities and the uniqueness of the services provided, five new lines of business were identified: (1) coordination and nursing, (2) laboratory services, (3) research facilities, (4) bio nutrition, (5) and administration for budget development, negotiation, regulatory and IRB services. These five allow for tracking the major activities of the CRS. Later, a sixth line of business was added for the Biomedical Informatics Core for Research Electronic Data Capture database creation and customized tools designed in a new system called the BIC portal.

These new lines of business and billing structure were an important milestone to enable consistent billing across all services and all types of trials. A billing system that would accommodate the budget structure of trials and CRS services would need to be created. This was most apparent in the billing structure of the coordinator pool. For NIH or nonindustry studies, it was important to charge for coordinator services based on effort since most trials were based on a flat dollar amount and a set effort for the coordinators (e.g., 40%). For industry trials, it was important for the coordinators to be charged for activities completed, per visit, per activity. It was not possible to charge a coordinator at a set effort on a trial that was not able to accrue patients. The new structure entailed the creation of a model that had each activity of the coordinator and the budget and negotiation personnel priced at a level of simple, moderate, and complex. Protocol review included a determination of coordinator activity and level of complexity as well as identification of procedures and time. This new pricing structure allowed the CRS to have a standard model for all studies. A CRS billing specialist was hired to help develop and operate a financial system that allowed the CRS to track its activity and cost recovery, including a system to track overall revenues/budget and expenses of the Center. This was accomplished by creating two separate financial reports to account for differing fiscal years (University and NIH) for the purpose of budgeting and reporting. While this report was being created, a separate set of reports was created to track revenue for each of the six lines of business.

Since the service center was created as a university resource and the funds generated were being credited to VCU, it was important to conform to other university bookkeeping and revenue tracking based on the university fiscal year and to start invoicing on a monthly basis. This provided many advantages, including timeliness of billing and accounting. By moving to monthly invoicing, study teams were able to more immediately match invoices to previous activities, it allowed for more data to see trends in activity and spikes or valleys in usage.

Once the expense and revenue tracking reports were completed, a report was created that matched expenses for each of the fiscal years and the revenues generated. Since the fiscal reports would not match the revenues reported, due to CTSA grant funding cycles or to different fiscal years, it was determined that the best reporting would be to compare recovery to date to expenses to date. Leadership was afforded the opportunity to compare running totals that allow calculations of the percentage of cost recovery to date and to determine the level of cost recovery that will be acceptable and necessary to allow growth with limited university funding.

Finally, a system to inform investigators about resource allocation and costs for a particular study was developed. A detailed letter including all approved resources for the six lines of business and their costs is sent to each investigator with a requirement that they acknowledge and accept the costs and allocation. For nonindustry studies, the costs are reported to the investigator in the letter but are not billed to the investigator, noting support from the CCTR.

Key activities completed during the Do stage include:

Established the CRS;

Hired a billing specialist;

Determined all costs for the CRS resources;

Determined how coordinator work on a study would be billed;

Created a tracking and invoicing system;

Created a letter to inform investigator of costs, approved resources, and have them acknowledge;

Created reporting mechanisms to track expenses and revenues.

The next stage of the PDSA model was to study the changes that had been made to determine the next course of action.

Study: March 2012

In March 2012, the leadership team reviewed studies for which the CRS was providing services without collecting program income. With the exception of documenting the type of studies and services provided, no financial tracking was taking place. It was determined by the leadership team that the CRS should expand fiscal reporting to include studies that were being 100% subsidized. This would be important to document the level of support that the CRS was providing from institutional resources. It was determined that the investigators would receive detailed letters showing the support investigators were receiving. The CRS began to send monthly invoices to all studies, even if the costs were not actually being recovered due to cost sharing. This served two purposes: (1) investigators were able to see the cost of the protocols they were creating and in some cases remove unnecessary procedures and (2) CRS would now have a complete view of the work that was being performed and the costs associated with the work. It was intended that this should (1) lead to more efficient, streamlined protocols, without compromising scientific intent and (2) permit the CRS to review all pricing, to ensure that costs are reasonable.

Act: June 2012

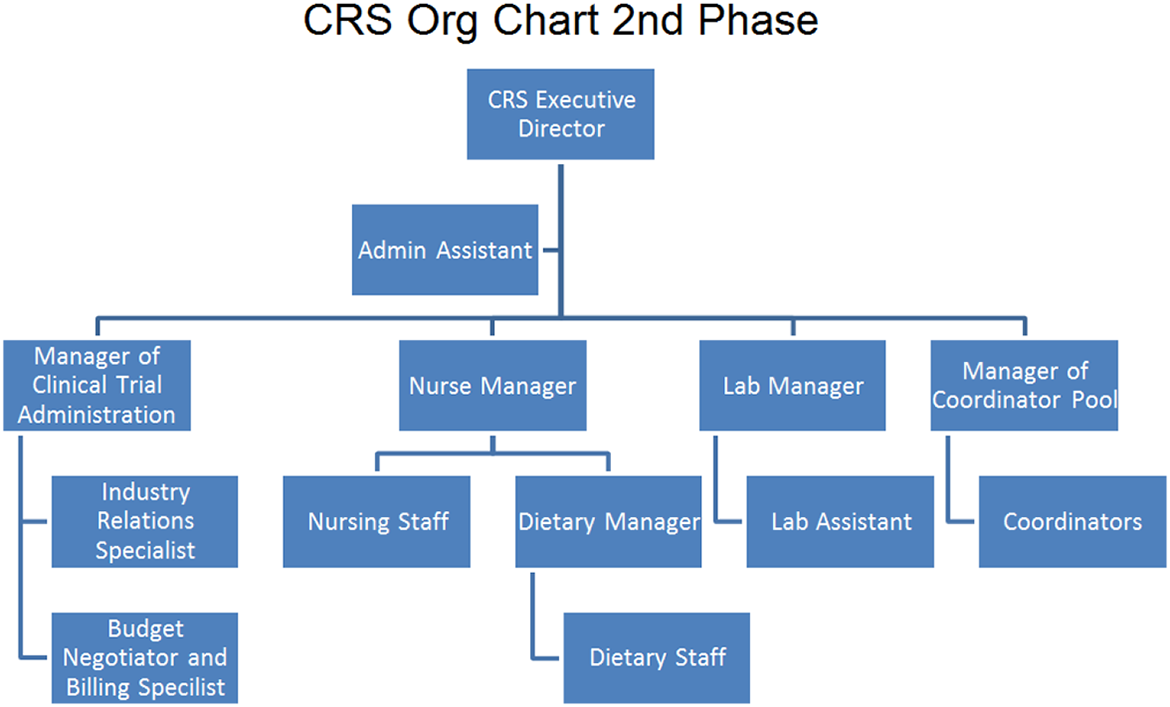

After studying the actions taking place, the leadership team reorganized the management structure of the CRS. Figure 3 shows the Phase 2 organization and reporting structure. By eliminating one of the senior manager positions and having the budget/negotiation and regulatory person, the coordinator manager, and one senior manager reporting directly to the CRS Executive Director, the CRS became one united organization. Cost savings were realized and a more direct reporting structure to the CRS Executive Director was established through the elimination of the medical director position.

Phase 2 of the CRS organizational structure. CRS = Clinical Research Services.

The leadership team reviewed staffing and determined that the current staff was adequate but that the high costs of RN are cost prohibitive for some trials. The CRS continued to maintain sufficient numbers of RN to care for research patients which required RN skills, while positions created by turnover were, if possible, replaced by less expensive providers (licensed practical nurses and patient care technicians).

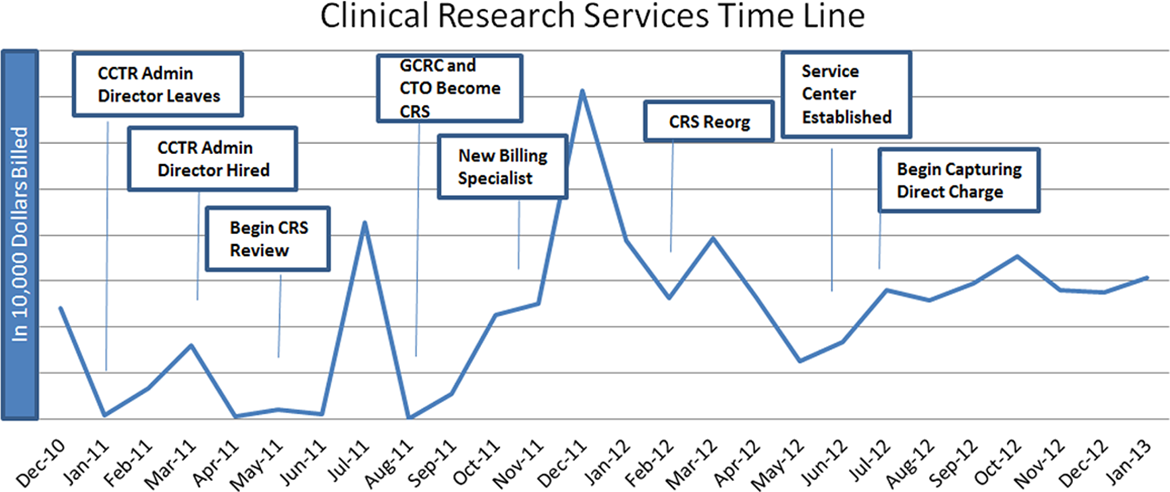

The net of management reorganization and maintaining current RN staff levels was found to be cost neutral and placed the CRS on sound financial footing to move forward as a critical component of the CCTR. Figure 4 shows the timeline for development of the CRS and the cost recovery overtime. The graph is presented in dollars billed compared to time. This shows how the use of the PDSA model, the implementation of reorganization strategies, and a business model affected the revenue generating aspects of the CCTR. As the activities took place, a higher level of funds was recovered and the revenue stream became more consistent and predictable providing projection and regression analysis to be possible.

Clinical Research Services timeline and cost recovery.

Conclusion

The PDSA model allows organizations to continue to improve processes and allows them to continue to modify systems and organizational structure to meet the changing demands of today’s clinical trials environment. Through the use of the PDSA model, the CCTR was able to remodel the VCU organization from a GCRC and CTO to a CRS. The CCTR improved efficiency; increased revenue recovered, reduced costs, and brought a high level of fiscal responsibility through financial reporting. With expanded offerings of the CRS and inclusion of Biomedical Informatics billing, the VCU CCTR saw over a 300% increase in the average revenues recovered from the first 7 months of data available to the most recent 7 months of data.

While every academic institution with a CTSA is part of the national CTSA consortium, many with similar needs as ours, we recognize that each will have unique qualities to be taken into account as a cost recovery model is developed. The PDSA process helped VCU to transform the VCU CCTR. It allows for continuous evaluation and improvement in the CRS system (Deming, 1986, 1993; Nelson & Batalden, 1999; Quinn, 1992). Assessment of the current program for positive and negative attributes is essential as is an examination for missing processes for compliance and efficiency. Consideration of the many stakeholders is also important. Once decisions are made, they must be explained clearly to investigators and staff, and finally, it is vital that processes are continually evaluated and adjusted to a changing research climate changes.

Footnotes

Authors’ Note

Its contents are solely the responsibility of the authors and do not necessarily represent official views of the National Center for Advancing Translational Sciences or the National Institutes of Health.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This publication described was supported by CTSA award No. UL1TR000058 from the National Center for Advancing Translational Sciences.