Abstract

The recent recession constitutes one of the macro forces that may have influenced workers’ retirement plans. We evaluate a multilevel model that addresses the influence of macro-, meso-, and micro-level factors on retirement plans, changes in these plans, and expected retirement age. Using data from Waves 8 and 9 of the Health and Retirement Study (N = 2,618), we find that individuals with defined benefit plans are more prone to change toward plans to stop work before the stock market declined, whereas the opposite trend holds for those without pensions. Debts, ability to reduce work hours, and firm unionization also influenced retirement plans. Findings suggest retirement planning education may be particularly important for workers without defined pensions, especially in times of economic volatility.

The recession that began at the end of 2007 created considerable interest in the effects of increased stock market fluctuations and heightened unemployment rates on the retirement plans of older workers (Bosworth & Burtless, 2010; Coe & Haverstick, 2010; Goda, Shoven, & Slavov, 2010, 2011; Sass, Monk, & Haverstick, 2010). Our research, using data from the 2006 and 2008 waves of the Health and Retirement Study (HRS), extends previous studies in several ways. First, we use a theoretical model that focuses on the interplay of macro-, meso-, and micro forces as predictors of retirement plans and planned retirement age. Prior studies relied on a more limited set of predictors making it difficult to interpret how the recession affected retirement plans. Second, whereas most studies addressed current retirement plans and expectations, we assess whether and how workers’ plans changed over time. Third, past research typically focused either on retirement plans or on expectations about the timing of the retirement transition (age at retirement); we link plan type (e.g., whether workers expect to stop working or to work in retirement) with expected retirement age.

Theoretical Framework and Literature Review

We apply a multilevel conceptual model of retirement transition processes Szinovacz, 2013) to distinguish among three main group of factors assumed to influence retirement transition processes; macro factors consisting of retirement institutions and societal structures such as the economy or culture, meso factors including organizational retirement policies and cultures as well as pertinent structures at the local or regional level such as labor markets, and micro factors pertaining to individuals’ retirement plans and decisions as well as their families, social networks, and personal characteristics (Szinovacz, 2013). We assume factors to be interrelated. For example, macro factors such as the economy can alter employer policies or influence changes in workers’ financial situation such as their pension portfolios.

Because this complex model cannot be captured by a single analysis, we adapt the model to reflect our emphasis on the potential impact of the recession and in regard to the availability of variables in the HRS. The macro factors considered in our analyses are indicators of the recession, specifically, changes in the Dow Jones Industrial Average (DJIA) and in the unemployment rate. Meso-level factors include firm characteristics (unionization and size), employee benefits offered by firms (pensions and health insurance), and work structures, especially opportunities to reduce work hours. The micro-level factors consist of individuals’ finances and health, both important predictors of retirement transitions, their work situation as well as selected demographic background characteristics as controls. Past research findings concerning each of these factors are described in the following sections.

Retirement has been institutionalized in modern societies and thus constitutes a normatively anticipated stage in the life course (cf. Szinovacz, 2013). However, retirement transitions have become increasingly blurred (Mutchler, Burr, Pienta, & Massagli, 1997), as many retirees engage in bridge jobs after leaving their career jobs (Cahill, Giandrea, & Quinn, 2006). Although most workers expect to retire at some point in their lives, their plans for how and when to retire develop over time and may be altered as circumstances demand.

Macro level

Both the 2000 stock market decline and the recession that began in late 2007/early 2008 led to steep drops in some retirement portfolios and assets (Eschtruth & Gemus, 2002; McFall, 2011), particularly for younger workers with defined contribution rather than defined benefit pension plans (Gustman, Steinmeier, & Tabatabai, 2009a). Stock market declines have been shown to lead workers to postpone the actual and expected timing of their retirement, although effects have been relatively small (Bosworth & Burtless, 2010; Coile & Levine, 2006, 2011; Goda et al., 2010, 2011; Munnell, Muldoon, & Sass, 2009). Rising unemployment during recessions can undermine workers’ opportunities to extend their working lives. Higher unemployment rates are associated with earlier retirement and expectations for earlier labor force exits (Bosworth & Burtless, 2010; Coile & Levine, 2011; Goda et al., 2010, 2011; Munnell et al., 2009).

Most important for our analyses are previous studies using the HRS. Goda, Shoven, and Slavov (2010, 2011) assessed the impact of the recession on retirement expectations through effects of changes in the Standard and Poor’s (S&P) 500 index, county-level unemployment rates, and changes in the state housing index. Decline in the S&P 500 index was significantly (p < .05) associated with a greater probability of working after age 62 but not the probability of working after age 65. Increases in regional unemployment contributed to higher probabilities of working past age 65, most likely to make up for financial losses suffered during the recession. Changes in housing values did not influence retirement expectations. Szinovacz, Martin, and Davey (2013) reporting on the same HRS questions about the probability of working past age 62 or 65 also found small effects of changes in the DJIA and in occupational unemployment rates, especially among workers who are older, closer to retirement, and among those with low or high education. Our analyses complement these earlier studies by addressing changes in retirement plans and expected retirement age linked to specific plans. We anchor stock market and unemployment dynamics with the timing of individual interviews.

Meso level

Research on the effect of firm characteristics on retirement planning is relatively scarce. Larger firms tend to have better benefits, whereas smaller firms may be more inclined to attend to their employee’s individual needs. Unionization has been linked to earlier work exits in times of economic downturns (Hardy & Hazelrigg, 1999).

Individuals with pensions, especially defined benefit plans, tend to expect earlier retirement and do retire earlier than those in jobs not covered by pensions (Mermin, Johnson, & Murphy, 2007). Provision of retiree health insurance tends to promote earlier retirement and retirement intentions although the strength of these effects remains under debate (Mermin et al., 2007; Yao & Park, 2012).

Age discriminatory employment practices and pressures on older workers to retire from employers and coworkers can reduce workers’ ability to postpone retirement (Dennis & Thomas, 2007; McCann & Giles, 2004). Work structures that offer older workers adaptations to reduce job demands or work hours, for example, work flexibility measured by the ability to reduce work hours, have been tied to postponement of retirement (Charles, 2007). U.S. employers have been reluctant to implement such practices (Eschtruth Sass, & Aubry, 2007; Szinovacz, 2013; Timmons, Hall, Fesko, & Migliore, 2011).

Micro level

Past research suggests that finances, health, and work conditions play an important role in workers’ retirement planning and decisions.

Pension wealth as well as asset wealth tend to induce earlier retirement (Aaron & Callan, 2011; Yao & Park, 2012). Because the shift to defined contribution accounts has placed a broader set of workers at risk of losing pension assets in times of economic downturns (Munnell, Cahill, & Jivan, 2003), workers with such plans may postpone retirement as may those experiencing significant losses to their asset wealth (McFall, 2011). Some recent research suggests that because a minority of workers invested in stocks and many older workers still have defined benefit plans, market changes had little effect on their financial situation (Goda et al., 2011; Gustman et al., 2009a; Gustman, Steinmeier, & Tabatabai, 2009b).

Studies indicate that individuals in poor health and those experiencing health shocks tend to leave the labor force earlier than their healthier counterparts (Coile, 2003; McGarry, 2004; Williamson & McNamara, 2003). Such health shocks can also lead to earlier than expected retirement (McGarry, 2004). Job stress and physical work demands can encourage earlier retirement (Johnson, Mermin, & Resseger, 2011).

In addition, our analyses control for selected demographic characteristics that have been tied to retirement planning. Closeness to retirement, measured by age crystallizes retirement plans (Ekerdt, Hackney, Kosloski, & DeViney, 2001) and leads to greater responsiveness of retirement plans to stock market fluctuations (Coile & Levine, 2009; Goda et al., 2011), although plans may become vague again once workers reach the typical retirement age (Abraham & Houseman, 2004). Experiences of job loss or unemployment spells tend to hasten retirement (Chan & Stevens, 2002), most likely because older workers face considerable reemployment barriers (Adler & Hilber, 2009). Men tend to retire later than women and may thus be more inclined to opt for postretirement work (Mermin et al., 2007). Individuals of lower socioeconomic status and minorities have been shown to retire earlier than higher status workers and Whites, partly due to less amenable work environments and poorer health (Aaron & Callan, 2011; Warner, Hayward, & Hardy, 2010).

Hypotheses

The theoretical framework outlined previously leads to a number of testable hypotheses that focus on the effects of the economy (macro level) and individuals’ finances (micro level) on plans to stop or continue working past retirement, although other predictors suggested by the conceptual framework are included in the analyses models. Based on the assumption of cross-level interlinkages, we hypothesize selected interaction effects among the main variables of interest.

Method

Sample

We use Waves 8 and 9 (2006–2008) of the HRS (Heeringa & Connor, 1995). Our analyses were restricted to individuals aged 50–64 who were employed in 2006 and 2008 to obtain changes in retirement plans over time. We excluded proxy respondents and individuals who reported being partly or completely retired. These selections yield a sample size of 2,618 respondents.

Measures

Most of our measures are derived from HRS public data files. However, for selected variables (especially wealth), we use imputed HRS data available through files developed by the RAND Corporation. Dependent variables for analyses are retirement plans, changes in such plans, and expected age of retirement.

Retirement plans

Respondents were asked: “Do you plan to stop working altogether or reduce work hours at a particular date or age, have you not given it much thought, or what?” Answer categories were stop work altogether, never stop work, not given much thought, no current plans, reduce work hours, change kind of work, work for myself, and work until my health fails. Because three answer categories were implied in the question (stop work, reduce work hours, and no thought), most answers fell into these three groups. Because the other categories have low frequencies and also ambivalent meanings (e.g., no plans may imply that respondents hadn’t yet started to plan or that they did not plan to retire at all), we focus our analyses of retirement plans on the three main answer categories. This selection covers 82.64% of 2008 plans (N = 2,261) and 80.67% of 2006 plans (n = 2,029).

Change in retirement plans

The measure of change in plans focuses on the three main plan categories (stop, reduce hours, and no thought). Changes in plans were coded into four groups: no change, change toward reduced hours, change toward stopping, and change toward no thought. Change toward stopping refers to those who indicated that they planned to stop working in 2008 but had mentioned a different plan in 2006. Change toward reduced hours was assigned to respondents who planned to reduce hours in 2008 but had either planned to stop work or had no plans, no thought, or “other” plans in 2006. We exclude individuals who changed from other work categories (i.e., work for self, change jobs, never retire, work until health fails), so that change is only indicated when a clear transition to a different type of plan occurred. Change toward no thought comprises those individuals who either transitioned from plans to stop working in 2006 to having no thoughts in 2008 or who indicated any plans to work in 2006 but no thought in 2008. Also included are workers who had no thoughts about retirement in 2008 but “other” plans in 2006, whereas individuals transitioning from “no plans” in 2006 to “no thought” in 2008 were excluded, given the ambiguity of the no plans category.

Expected retirement age

Individuals who indicated plans to stop working or to change their work in some way (reduce hours, change job, work for self) were then asked at what age they intended to make this transition. Our analyses focus on expected age of stopping work and expected age of reducing work hours. Respondents who answered “never” to these questions were excluded from the analyses.

Change in expected retirement age

We considered predictors of changes in expected retirement age by including expected retirement age in 2006 as predictor in the analyses. This has the statistical advantage of providing estimated effects independent of (i.e., orthogonal to) baseline expectations. These analyses were restricted to those individuals who did not change plans between waves.

Based on our conceptual framework, we distinguish among three sets of predictor variables (macro, meso, and micro level).

Macro level

The macro-level predictors refer to changes in the economy, namely, in the stock market and in the unemployment rate. We calculated 12-month percentage changes in the DJIA, based on average monthly values. These changes were coded to refer to the time period prior to the 2008/2009 wave interview month. Changes in unemployment were measured through the percentage change in industry-specific monthly unemployment rates. We matched HRS workers’ industry data (partly based on restricted data) with the industries used by the Bureau of Labor Statistics for reporting unemployment statistics for specific time periods (http://www.bls.gov/iag/tgs/iag_index_naics.htm). Because interviews were conducted from February 2008 through February 2009, there is considerable variability in the economic climate among respondents. For example, changes in the DJIA ranged from 64% to 100% (a 36% decline compared to no change), and percentage changes in unemployment rates ranged from 35% (a 65% decline) to 274% (more than doubling over the 1-year period).

Meso level

Meso-level factors include firm characteristics, employee benefits, and work structures. The two firm characteristics are unionization and firm size. Unionization was coded as a dummy variable (1 = yes, 0 = no). Firm size was coded into six categories (1–4, 5–14, 15–24, 25–99, 100–499, and 500+ employees).

Employee benefits include pensions and health insurance. We capture pensions through two dummy variables indicating coverage through a defined benefit plan or a defined contribution plan (1 = yes/0 = no). Those without pensions serve as reference group. Health insurance was divided into four dummy variables: has employer health insurance that continues into retirement (1 = yes, 0 = no), has employer health insurance without coverage in retirement (1 = yes, 0 = no), has government health insurance such as Medicaid or VA/CHAMPUS, (1 = yes, 0 = no), and coverage through spouse’s health insurance (1 = yes, 0 = no). Those without any insurance served as reference.

The single variable used as measure of work structure reflects potential barriers to late-life employment. We used the HRS question: Could you reduce the number of paid hours in your regular work schedule (1 = yes, 0 = no)? Because this question was not asked of self-employed workers, the self-employed were assigned a score of 0 and self-employment was entered as an additional dummy variable in the analyses. Employees who cannot reduce hours serve as reference.

Micro level

The micro-level factors consist of finances other than benefits, work situation, health, and demographic controls. Several indicators of finances were used. Wealth was captured by investments, debts, and changes in the net home value. Total investments were derived by summing RAND imputed values for stocks, bonds, IRAs, checking, Certificates of Deposit (CDs), and other savings. This variable was then coded in US$1,000 and logged. Extremely high values were Winsorized to the 99th percentile, that is, values above the 99th percentile were recoded to the value of the 99th percentile. Debts were recoded into three dummy variables: those who have negative net assets, those who have low debts, and those with high debts. High and low debts were assigned based on the percentage of debts (excluding mortgages) relative to total assets (total investments plus the value of businesses and real estate other than residences). Those with debts under 15% of investments were considered to have low debts and those with debts of 15% of investments or more were treated as having high debts. Individuals without debts serve as reference group. In addition, we included change in debts, total investments, and home value (including the net value of primary and secondary residences) since the previous wave (in US$1,000 with extreme values Winsorized at the 1st and 99th percentiles). All three variables were derived by subtracting 2006 values from 2008 values. Imputed earnings from RAND were used. The variable was then divided by 1,000 and logged.

Work situation indicators include RAND job tenure in years, work hours, and employee job stress and physical demands. The latter was measured based on agreement or disagreement with questions whether one’s job requires lots of physical effort and whether it involves a lot of stress. For the first statement, workers were asked whether this was true all or almost all of the time, most of the time, some of the time, or none or almost none of the time. For the statement regarding stress, workers responded by agreeing or disagreeing with the statement. Scores could range from 1 (none of the time, strongly disagree) to 4 (all of the time, strongly agree). We dichotomized both variables. In the case of physical work demands, those answering all of the time or most of the time were coded 1, the others 0. For job stress, those agreeing were coded 1 and those disagreeing 0.

Health was measured through self-reported health coded into a dummy variable (excellent, very good, and good = 1, fair and poor = 0). We also included the number of chronic conditions, a measure developed by RAND based on the count of whether or not respondents had ever been diagnosed with the following: high blood pressure, diabetes, cancer except skin cancer, chronic lung disease, heart attack, coronary heart disease, angina, congestive heart failure, or other heart problems, stroke, emotional, nervous, or psychiatric problems, and arthritis or rheumatism. Changes in self-reported health and chronic conditions were obtained by subtracting 2006 from 2008 values.

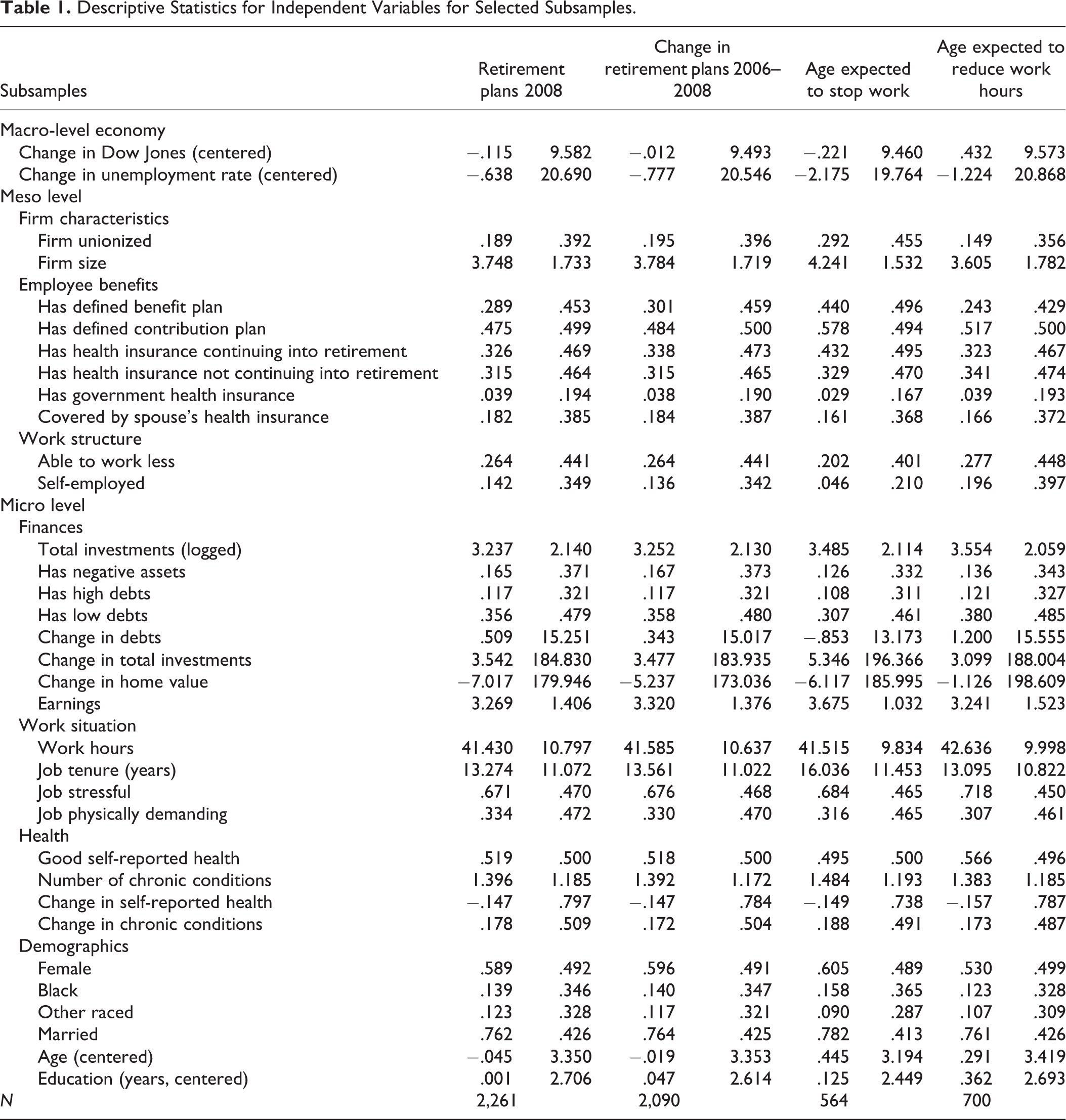

The demographic control variables gender, race/ethnicity, and marital status were coded as dummy variables (female = 1, male = 0; Black = 1, Hispanic = 1, other race = 1; White = 0; married = 1, not married = 0). Age was coded in years. For socioeconomic status, we used education (in years, range 0–17). We also include work hours and tenure in the present job (in years). Means and standard deviations for all independent variables are shown in Table 1.

Descriptive Statistics for Independent Variables for Selected Subsamples.

Analyses

Given the categorical nature of our dependent variables, we used multinomial logistic regressions for the analyses of retirement plans and changes in plans. Ordinary least squares (OLS) regressions were used for expected retirement age and changes in expected retirement age. The two indicators of the economy (stock market changes and unemployment rates) were entered in separate equations because they are highly correlated (r = −.56, p < .01). However, we report them in the same tables for space reasons. The coefficients for the other variables are always taken from the equations including the change in the DJIA, but these effects remained the same in the equations with unemployment. We imputed missing data through 10 multiple imputations using multiple imputations via chained equation procedures. Analyses adjust for the clustered nature of the design using the cluster variance estimator that is robust to misspecification and within-cluster correlation. Average variance inflation (VIF) was 1.44 and no single variable had a VIF value over 2.5, suggesting no multicollinearity in the models. The analyses rely on unweighted data.

Results

We first describe the distribution of retirement plans and their association with expected retirement age and then proceed to the analyses of predictors of plans and expected retirement age in accordance with our conceptual framework.

Distribution of Retirement Plans

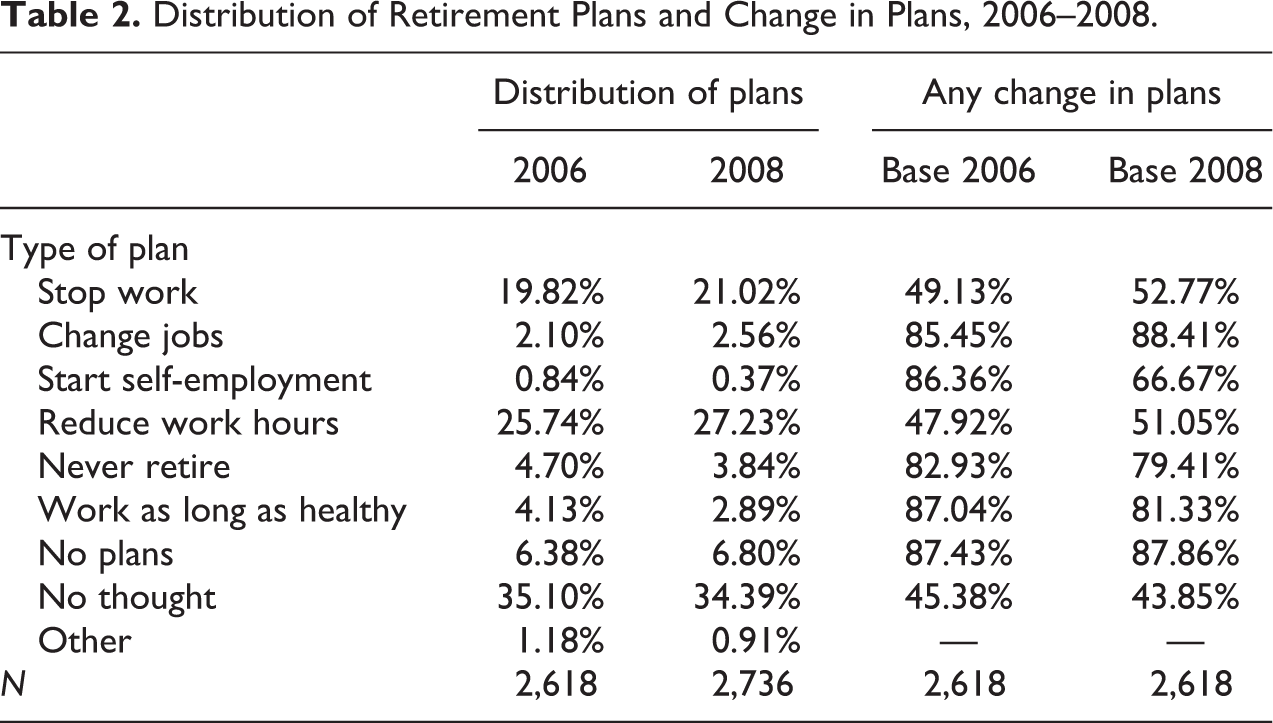

The distribution of retirement plans for 2006 and 2008 and changes in plans between 2006 and 2008 are shown in Table 2. The most common responses (perhaps partly due to how the question was asked in the HRS) are stopping work, reducing work hours, and not having given retirement much thought. Over one third of workers express some intention to work in retirement or to work in their later years, whereas only about a fifth expects to stop working after retirement. However, over a third of workers aged 50 and over has not yet thought about their retirement.

Distribution of Retirement Plans and Change in Plans, 2006–2008.

Even though the distributions are quite similar for 2006 and 2008, over half of the respondents (52.3%) made some change in plans. Such changes in plans differ considerably by plan type. The third and fourth columns in Table 2 indicate the percentage of workers who changed plans. The numbers for base 2006 refer to changes from the specified plans in 2006, whereas base 2008 indicates changes to specific plans in 2008. For example, 49.1% of workers who planned to stop working in 2006 had changed their plans by 2008, whereas 52.8% of workers mentioning plans to stop work in 2008 had indicated different plans in 2006. Change seems more common for the plan categories mentioned by fewer workers, perhaps due to the wording of the HRS question or the small N’s for these groups.

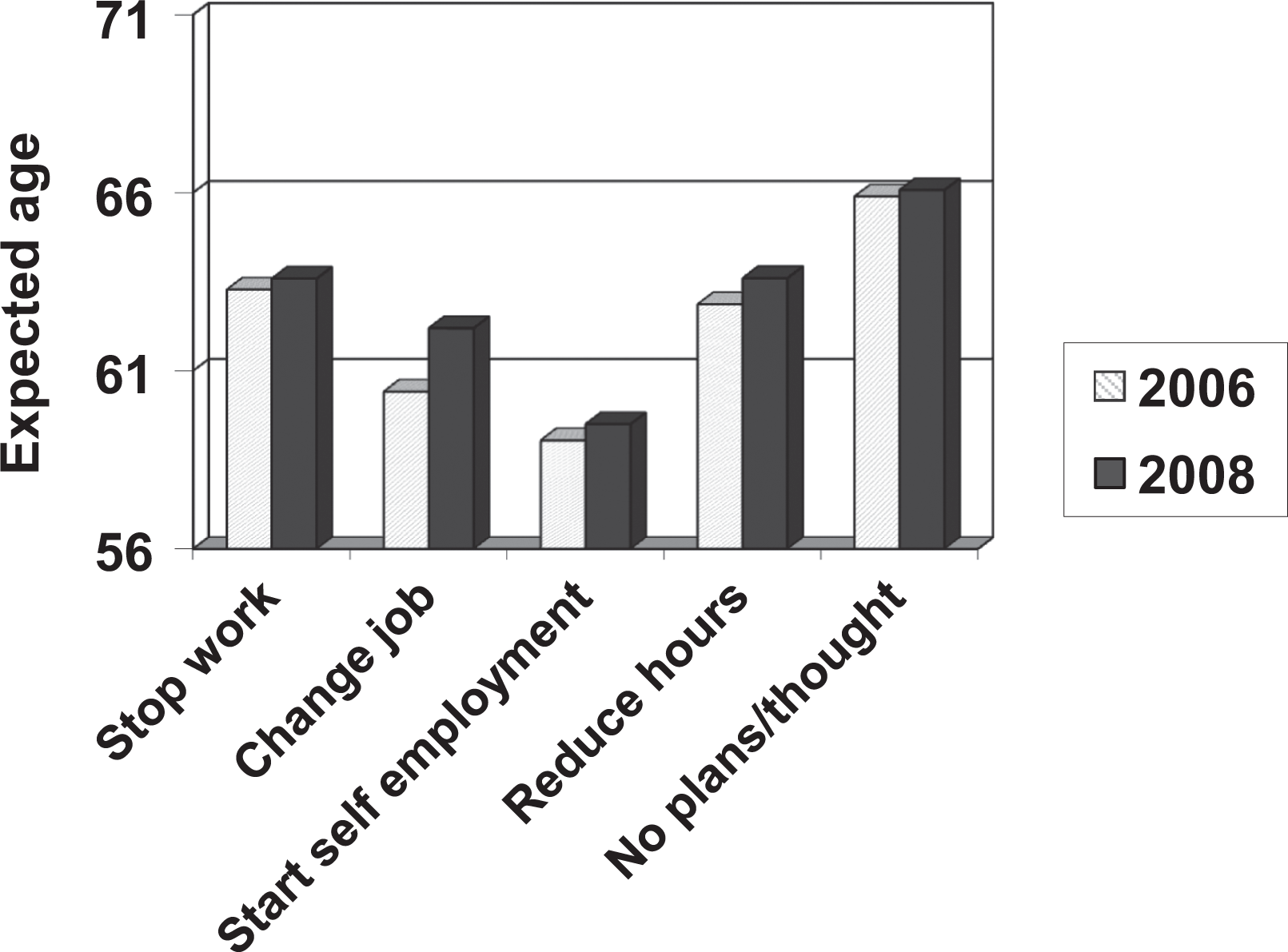

To assess whether expected retirement age differed among the various types of retirement plans, we calculated the mean expected retirement age given for specific plans. Results are shown in Figure 1.

Expected retirement age by type of retirement plan and year.

Those who have not yet made plans for retirement or thought about it indicate the highest expected retirement age, hovering around age 66. We tested whether these expectations differed for those indicating “no plans” for retirement and those reporting that they had given it “no thought” and found quite similar responses. It should also be noted that a sizable group of those mentioning no plans or no thought say that they will “never” retire (21.6% and 18.0%, respectively, for 2008 and 28.8% and 15.3%, respectively, for 2006). Those intending to stop working expect to retire somewhere between ages 62 and 65 (M = 63.3 and 63.6 for 2006 and 2008, respectively). Expected age of retirement among those planning to reduce hours is also around age 63 (62.9 and 63.6 for 2006 and 2008, respectively), whereas those planning to change jobs and especially those aiming to work for themselves expect to make these transitions earlier. It is notable that expected retirement age is slightly higher for 2008 than 2006 across all plans, and this difference is most pronounced among those planning to change jobs.

Predictors of Retirement Plan and Changes in Plans

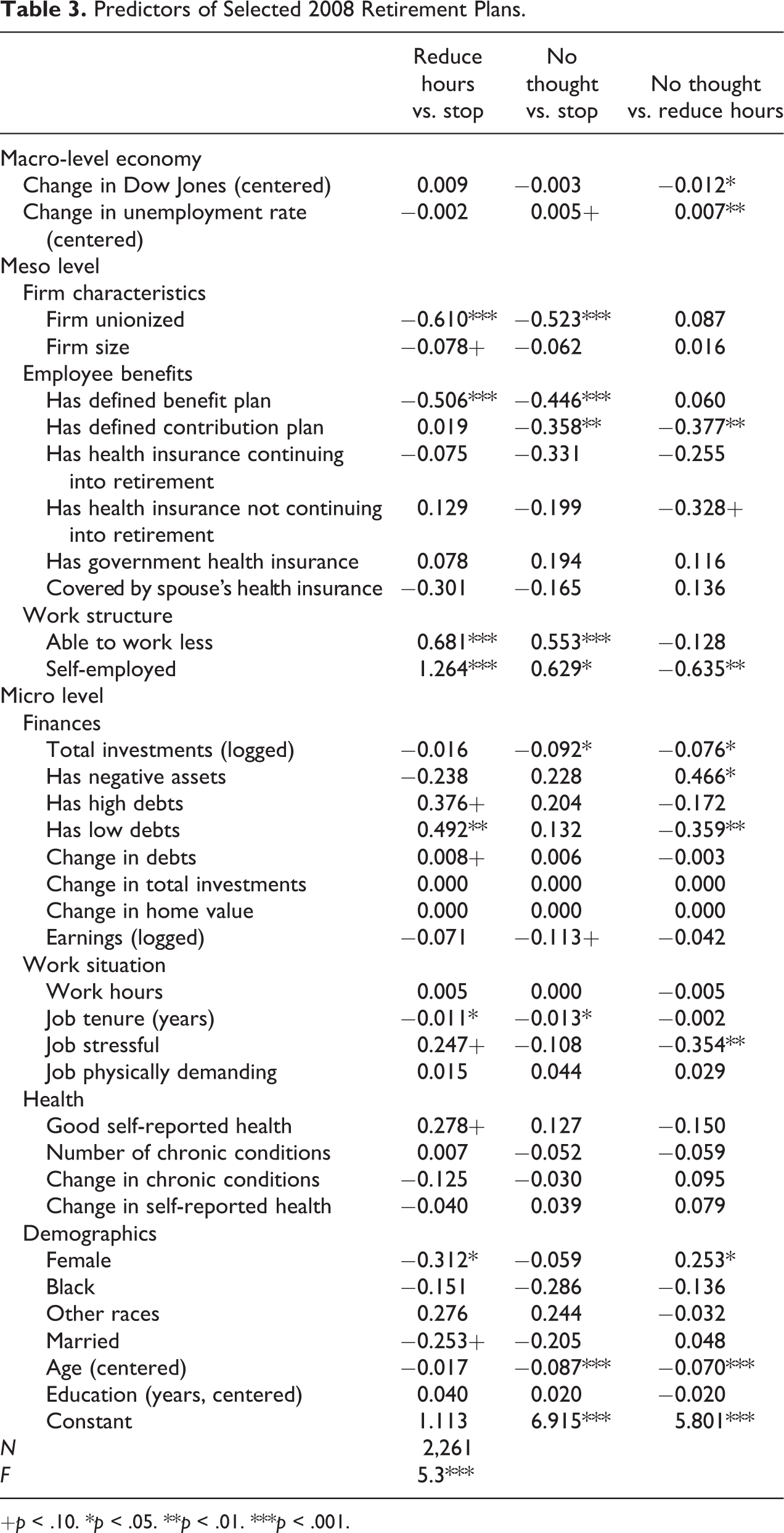

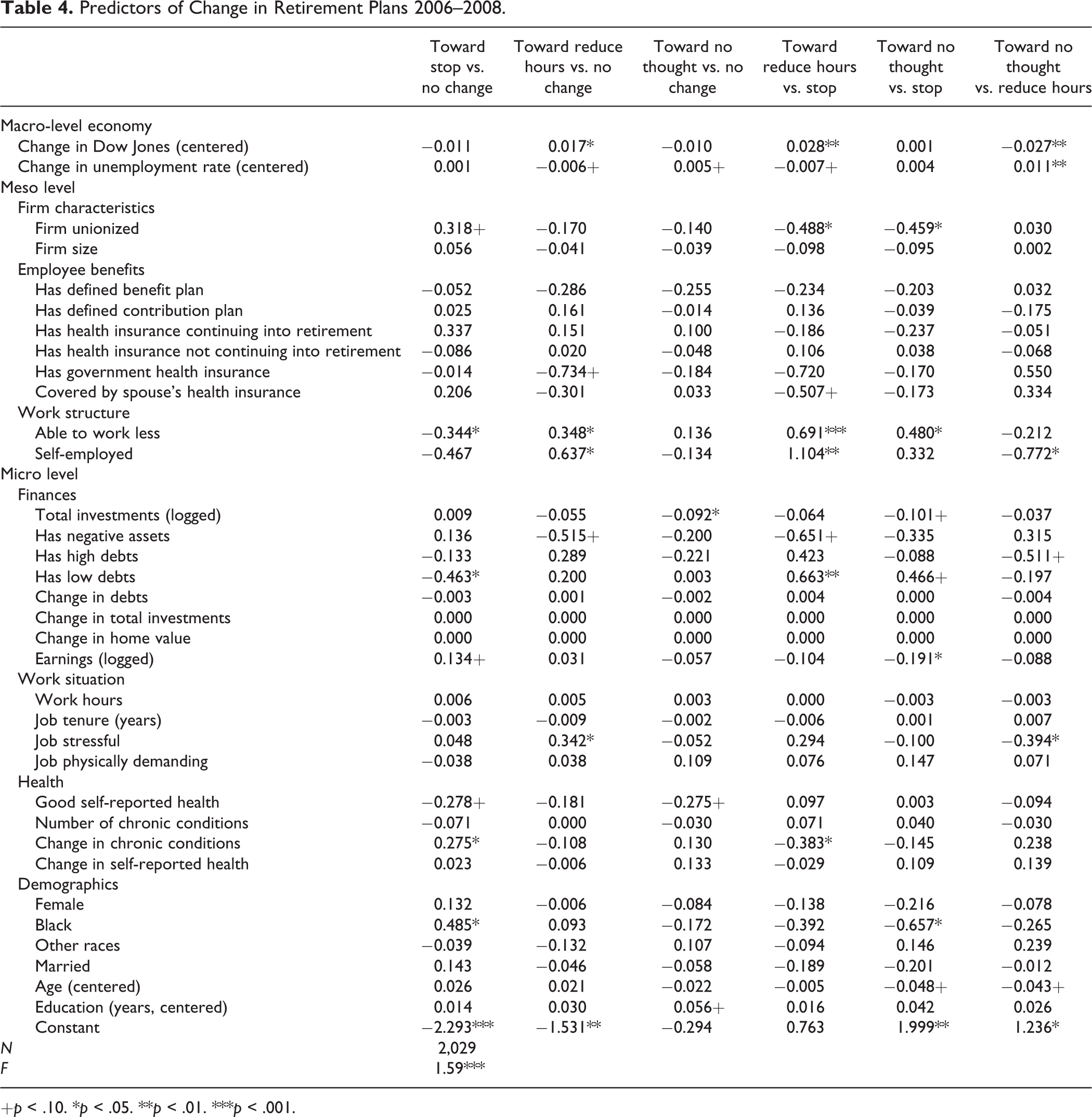

The multinomial logistic regression results for retirement plans in 2008 are reported in Table 3 and the regressions for changes in plans are reported in Table 4. We first address our hypotheses and then comment briefly on effects of other predictors. To aid interpretation, we present different parameterizations of the same equation using different base (reference) categories in order to see differences between categories that would be difficult to compare using only “stop work” as the reference category. The first two columns in Table 3 use plans to stop working as base category, whereas the third column uses plans to reduce hours as base category. A similar approach was used to present the different contrasts for changes in retirement plans. Because unemployment rates and changes in the DJIA are partly interdependent, we estimated separate regressions including changes either in the DJIA or in unemployment rates. As the other parameters in the models remain essentially the same, we display the regressions conducted with DJIA changes in the model but show the regression coefficients for unemployment rates in a separate row in the same table.

Predictors of Selected 2008 Retirement Plans.

+p < .10. *p < .05. **p < .01. ***p < .001.

Predictors of Change in Retirement Plans 2006–2008.

+p < .10. *p < .05. **p < .01. ***p < .001.

Our first hypothesis referred to the effects of the stock market on retirement plans. In interpreting the results shown in the tables, it is important to remember that high scores on the DJIA indicate an increase (or stability) in the stock market, whereas lower scores indicate a decline in stock market values. We find that declines in the DJIA are associated with a greater probability of having given retirement plans no thought when plans to reduce hours are used as reference category, suggesting that a decline in the stock market increases insecurity in or postponement of retirement planning (Table 3). For changes in plans (Table 4), we find that respondents exposed to lower stock market values were less prone to change retirement plans toward reduction of work hours. These results contradict our hypothesis (1) that declines in the DJIA would be associated with plans to work in retirement. Rather, workers either maintained their previous plans or postponed retirement planning. Plans to stop working seem unaffected by stock market changes.

Our second hypothesis that increases in unemployment should be associated with more plans to stop working is also not supported, as we find no influence of unemployment rates on intentions to stop working. Instead, findings for changes in unemployment rates parallel the results for stock market changes. As unemployment increased, workers were more prone to have given retirement no thought rather than planning for reducing work hours, suggesting again that a volatile job market increases uncertainty in retirement planning.

Our third hypothesis addressed meso-level factors, especially in the form of employee benefits. The assumption that coverage by a defined benefit plan would foster abrupt retirement is supported by the data. Individuals with defined benefit plans are more likely to plan on stopping work rather than continuing work into retirement. In addition, those with defined contribution plans are particularly unlikely not to have thought about retirement. Changes in retirement plans are not affected by pension plans. In contrast to the hypothesis, we also find little evidence for effects of health insurance on retirement plans or changes in plans.

The fourth hypothesis focused on micro-level factors, particularly wealth. Individuals with higher investments tend to have thought more about retirement than their less wealthy counterparts, but they are as likely to plan to stop working as to plan on reducing work hours. Furthermore, changes in investment values have no effect on retirement plans. However, individuals with low debts (rather than no debts) are particularly prone to plan on reducing work hours, and a similar trend (p < .10) is evident for those with high debts. In contrast, individuals with negative assets are more likely to have given retirement no thought than to plan on reducing work hours. Earnings have no significant effect on plans.

As far as change in plans is concerned, individuals with high investments are less prone to have not thought about retirement than to have maintained their previous plans. Neither negative assets nor high debts significantly influence changes in plans, whereas individuals with low debts are more likely to change toward plans to reduce work hours than either not changing plans or changing toward plans to stop working. Changes in any of the wealth indicators have no effect on plan changes. Individuals with high earnings are less likely to change toward no thoughts than toward stopping work.

Hypothesis 5 addressed interactions between the macro-level factors and pension benefits (data not shown). We find no significant interaction for 2008 retirement plans but significant interactions for change in plans. The interaction between the DJIA and defined benefit plans is significant (b = .034, p < .05). Individuals with defined benefit plans were somewhat more prone to move toward plans to stop working when the DJIA was still relatively high than when it had decreased, whereas the opposite trend holds for respondents without pensions. We also find a significant interaction between changes in the unemployment rate and defined contribution plans for the contrast between moving toward no thought and no change in retirement plans (b = .014, p < .05). Specifically, under conditions of high unemployment, individuals with defined contribution plans are significantly more likely to maintain their previous retirement plans than to move to no thoughts about retirement when compared to respondents without pensions. Given the number of interactions tested and the relatively weak interaction effects, both findings should be taken with some caution. Furthermore, neither interaction supports our hypotheses.

In addition to the hypothesized relationships, we explored the effects of other meso- and micro-level factors on retirement plans (see Tables 3 and 4). Among the meso-level factors, we find both effects of firm characteristics and work structure. Workers in unionized and large firms are more likely than other workers to expect to stop working. Furthermore, workers in unionized firms are less likely to have changed plans toward reducing hours or giving retirement no thought than toward stop working. Individuals who can work less or who are self-employed are significantly less likely to plan on stopping work. The self-employed are also less prone to not have thought about retirement than to plan on reducing hours. Having the option to work less also contributes to changes in retirement plans toward reducing work hours and away from plans to stop work, whereas self-employment is significantly associated with changes in plans toward reduction of work hours.

The first set of micro-level factors other than finances concerns the work situation. Workers with longer job tenure are more inclined to plan on stopping work, but job tenure is not significantly related to plan changes. Having a stressful job seems to promote plans to reduce hours rather than giving retirement no thought and also to change toward plans to reduce hours.

None of the health indicators exerts a significant influence on retirement plans. However, individuals are more inclined to change plans toward stopping work when they experienced increases in chronic health conditions.

Among the demographic factors, we find significant effects of gender and age on retirement plans as well as of race on changes in plans. Women are less likely to plan on working in retirement than men. Having not thought about retirement is more common among younger workers. African Americans are more prone to change their plans toward stopping work.

Expected Retirement Age

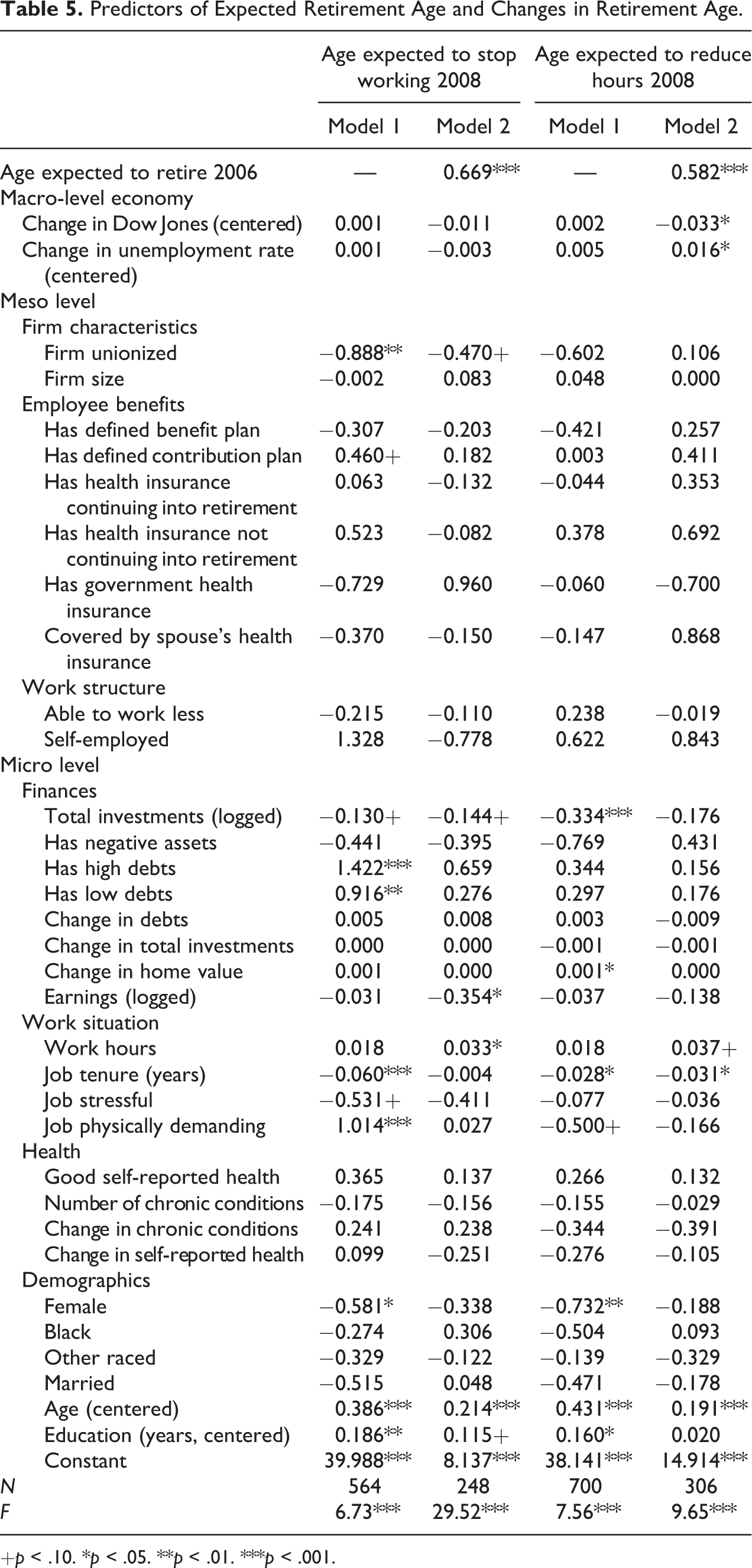

The OLS regressions for expected retirement age are shown in Table 5. We first address hypothesized effects and then comment on other predictors in our conceptual model. Given the relatively small number of cases for the regressions, we did not test interaction effects for expected retirement age. Model 1 refers to the effects of the predictors on current (2008) expected retirement age, whereas Model 2 pertains to change in expected retirement age as we control for retirement age expectations in 2006.

Predictors of Expected Retirement Age and Changes in Retirement Age.

+p < .10. *p < .05. **p < .01. ***p < .001.

Neither changes in the DJIA nor in the unemployment rate significantly affect expected age to stop working or changes in these expectations, thus providing little support for Hypotheses 1 and 2. Similarly, there are no significant effects of DJIA or unemployment changes on current expected age of reducing work hours. However, changes in expected age of reducing work hours are significantly influenced by both the stock market and unemployment. As expected (Hypothesis 1), decreases in the DJIA are associated with change toward later age of reducing work. However, the data are in the opposite direction than predicted by Hypothesis 2. Increases in the unemployment rate are associated with postponement of reducing work hours.

Hypothesis 3 is not supported. Neither expected age of stopping work nor of reducing work hours is significantly related to benefit plans.

Hypothesis 4 addressed effects of wealth on retirement plans. We find no significant effect of total investments on expected age of stopping work. However, there is a trend (p < .10) toward lower expected age of stopping work as investments increase. Furthermore, persons with low or high debts (but not with negative assets) are significantly more likely to expect to stop later than those without debts. Individuals with high investments are significantly less prone to postpone age of reducing work hours. These findings provide partial support for Hypothesis 4. In contradiction to the hypothesis, we find a positive association between expected age of reducing work hours and changes in home value. Earnings are negatively related to changes in expected age of stopping work, suggesting again that individuals with more financial resources opt for earlier retirement.

Among the meso-level factors not directly addressed by our hypotheses, only firm unionization has a significant effect on expected age of stopping work. Individuals in unionized firms expect to stop working earlier than their counterparts in nonunionized firms.

Several of the micro-level factors other than finances influence expected retirement age. Individuals with longer work hours are significantly more likely to have increased their expected retirement age since the 2006 wave. In contrast, longer job tenure seems to encourage earlier expected age of stopping work as well as of reducing work hours and of having decreased expected age of reducing work hours since the previous wave. Although physical job demands had no significant effect on type of retirement plans, they significantly influence expected age of stopping work although not in the expected direction: Workers in more physically demanding jobs expect to stop working later than those in less physically demanding jobs. Health has no significant effect on expected age of stopping work or reducing work hours.

The demographic characteristics significantly related to expected retirement age are gender, age, and education. Women tend toward expectations of retiring earlier than men both in regard to stopping work and reducing work hours. Expected retirement age increases with age as does change in such expectations since 2006. Better educated workers tend toward expectations of retiring later than the less educated.

Conclusion

The main aim of this study was to assess whether and how workers changed their retirement plans and expected age of retirement during the recent recession.

Overall, we found that about one half of the workers in the main plan categories (stop work, reduce hours, no thought) maintained their plans over the 2006–2008 time period. Change was more common for the other types, perhaps because they were not implied in the HRS question. When changes did occur, they were foremost toward working or no thought/no plans rather than toward stopping work. Increased uncertainty seemed almost equally prevalent as a change toward working, suggesting that the economic downturn may lead at least some workers to question their previous plans.

The data support a multilevel model of retirement planning. They demonstrate that retirement plans are influenced by macro-, meso-, and micro-level factors. We will first discuss the macro-, meso-, and micro-level factors addressed by our hypotheses (economy, benefits, individuals’ finances), but several other predictors deserve notion as well.

In contrast to Hypotheses 1 and 2, workers seemed more prone toward uncertainty (no thought) and less prone to plan on reducing work hours as the recession deepened. In addition, those who maintained plans to reduce work hours became more inclined to postpone this transition during the 2006–2008 period, suggesting that workers respond to the general economy rather than to specific economic changes such as stock market declines or unemployment rates. We find no effects of the economic indicators on plans to stop working or on expected age to stop working. These results differ from those of earlier HRS studies that reported that stock market and unemployment changes influenced the probability of working past age 62 and 65 (Goda et al., 2010, 2011); however, we excluded partial retirees, whereas past research using the HRS did not. More research is needed to explore why the recession seems to have had little impact on plans to stop working or the age at which workers plan to stop. Perhaps such plans are more driven by considerations about benefits and eligibility issues than by the economic climate.

We find, in line with Hypothesis 3, that workers with defined benefit plans are more inclined to plan on stopping work altogether, whereas those with defined contribution plans seem more prone to have some plans, regardless of whether these plans involve stopping work or reducing work hours. We find no effect of benefits on change in retirement plans or expected retirement age. Having defined contribution plans seems to promote crystallization of retirement plans, perhaps because such plans induce workers to stay more involved in decisions about their pension portfolios. There was little evidence that workers adjust their retirement plans to health insurance coverage.

Hypothesis 4, which addressed the influence of workers’ financial status on retirement plans, received mixed support. We find no evidence that high investments are associated with plans to stop working or to stop work earlier. However, persons with higher investments are less prone not to have thought about retirement and intend to reduce work hours at a younger age than those with fewer investments. Increases in uncertainty or postponement of plans to reduce work hours prevail among those with low investments, suggesting that lower income workers may be caught in a catch-22 situation, where financial need to continue working is counterbalanced by the recognition that jobs may not be available to do so. Changes in investments have no effect on plans or expected retirement age, and the effect of changes in home value is not in the expected direction.

Debts influence retirement plans. Those with low debts are more likely to plan on reducing work hours than individuals with no debts, and they are also less likely to change their plans toward stopping work. In contrast, individuals with negative assets are more likely to have given no thought to retirement than on planning to reduce hours. In addition, individuals with low or high debts (but not with negative assets) expect to stop working later than those without debts. This suggests that different debt scenarios are associated with divergent retirement plans. That reduction in work hours is foremost related to low debts suggests that workers may extend their working lives through bridge jobs in order to deal with their indebtedness. That a similar effect does not occur for those with high debts or negative assets requires further investigation.

We find little support for the hypothesis predicting interaction effects between the economic indicators and benefits. Individuals with defined benefit plans are more prone to change toward plans to stop work before the stock market declined, whereas the opposite trend holds for those without pensions. It is conceivable that respondents with defined benefit plans are in more secure work environments than those without pensions and thus more able to continue work in times of economic crises. In addition, individuals with defined contribution plans were particularly unlikely to change toward no thoughts about retirement under conditions of high unemployment, perhaps because such plans require greater involvement on the part of beneficiaries.

Meso-level indicators seem especially important. Firm unionization encourages plans to stop working and at a younger age. Opportunities for work flexibility (ability to reduce hours or self-employment) apparently encourage plans to work in retirement. This suggests that employer policies may play an important role in shaping workers’ retirement plans.

We also find some effects of micro-level factors other than finances. Those with long job tenure are more prone to plan on stopping work, perhaps because they have been able to accumulate more pension funds or because of work fatigue. Job stress seems to encourage changes in plans to move toward reduced work hours, presumably to alleviate some stress. Health shocks in the form of increased chronic conditions seem to further move toward plans to stop working, a finding corroborating similar results from research on retirement timing and transitions (Coile, 2003). Women are more inclined to plan on stopping work and to retire earlier than men, whereas African Americans were more prone to move toward plans to stop working since the previous wave. Given our controls for socioeconomic and marital status, this suggests that women and minorities approach retirement differently than men and Whites, supporting the need to better conceptualize diversity in retirement transitions (Calasanti, 1996).

Our findings have implications for policy and future research. Studies using different questions about retirement planning (expected age of retirement, intentions to save or work more, type of retirement transition) yield divergent results. Both qualitative and quantitative research may be necessary to shed more light on these discrepancies. Do workers indicating that they plan to work in retirement (and, given the wording of the HRS answer categories, especially reduce work hours) mean that they want to remain in their jobs but work less (as our finding regarding ability to reduce work hours in one’s current job might suggest) or are they also thinking of job and employer changes? Similarly, are answers to questions about the probability of retiring at a certain age referring to retirement from one’s career job or one’s bridge job?

Another avenue for future research is to better understand the diverse effects of an economic recession on workers’ retirement plans. It seems essential to conduct research that delves further into the reasons why workers pursue specific retirement plans or change their previous plans and whether such reasons differ among diverse population groups such as lower- versus higher level workers or those who are only moderately compared to those who are strongly affected by stock market fluctuations or rising unemployment. Furthermore, it is not clear to what extent retirement plan changes lag behind economic change or depend on the duration of a recession. It is conceivable that the effects of the current recession on retirement planning will only become evident in later waves of the HRS. Thus, future research is needed to replicate this study with more recent HRS waves.

Our analyses suggest that debts play an important role in retirement plans. These results also have implications for financial planners and policy makers. Most retirement planners focus on investment portfolios, perhaps because of a vested interest in selling their products (Ekerdt & Clark, 2001). Debt reduction constitutes an important motivation to postpone retirement or work in retirement. Low debts seem to encourage bridge employment, whereas high debts seem to encourage postponement of labor force exits. These findings suggest that certain types of consumer debt (e.g., credit card debt) may be good predictors of future retirement trends. Clearly, more research is needed to explore which types and amounts of debts lead to prolongation of work life.

Workers’ retirement plans are also influenced by the work environment. Ability to reduce work hours promotes plans to work in retirement. Employer initiatives to provide more flexible workplaces and, perhaps, union initiatives promoting and facilitating postponement of retirement may very well be essential to successfully implement government policies geared toward extending work into the later years (Organization for Economic Co-operation and Development, 2005; Szinovacz, 2011). Of some concern is our finding that plans to work in retirement prevail among workers in nonunionized firms, especially since we control for benefits often associated with unionization. It is conceivable that unions create a culture of “making place for younger workers” that discourages postretirement work. However, such a culture is not supported by evidence about the relationship between youth unemployment and late-life work (Gruber, Milligan, & Wise, 2009).

Workers covered by pensions seem to have more crystallized plans for retirement than their counterparts without pensions. Perhaps pension coverage and contributions to pension plans may inadvertently encourage concrete retirement plans by creating a workplace culture around planning (Ekerdt, Kosloski, & DeViney, 2000), whereas workers without pension options may be further disadvantaged because of their limited exposure to such a planning culture. Further exploration of whether pension coverage and other saving options encourage earlier retirement planning is needed to inform policies that attempt to promote workers’ retirement planning and savings.

Perhaps the most important conclusion from this research is the importance of considering societal and work contexts in research on retirement planning. Previous research has been dominated by a micro approach. Our findings demonstrate, instead, that both economic volatility and work environments affect retirement planning and plan formation, although individual factors play an important role as well.

Footnotes

Authors’ Note

The opinions and conclusions expressed in this article are solely those of the authors and do not represent the opinions or policy of the National Institutes of Health or the HRS.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was funded by a grant from the National Institute of Aging R01AG013180 to Maximiliane E. Szinovacz, PI. The Health and Retirement Study is conducted by the University of Michigan’s Institute for Social Research and funded by the National Institutes of Health (grant number NIA U01AG009740).