Abstract

Using microsimulation, we estimate the effects of three policy proposals that would alter Social Security’s eligibility rules or benefit structure to reflect changes in women’s labor force activity, marital patterns, and differential mortality among the aged. First, we estimate a set of options related to the duration of marriage required to receive divorced spouse and survivor benefits. Second, we estimate the effects of an earnings sharing proposal with survivor benefits, in which benefits are based entirely on earned benefits with spouses sharing their earnings during years of marriage. Third, we estimate the effects of adjusting benefits to reflect the increasing differential life expectancy by lifetime earnings. The results advance our understanding of the distributional effects of these alternative policy options on projected benefits and retirement income, including poverty and supplemental poverty status, of divorced and widowed women aged 60 or older in 2030.

Introduction

Demographic and socioeconomic changes are reshaping Social Security benefits and the retirement circumstances of women (Herd, 2005; Wu, Karamcheva, Munnell, & Purcell, 2013). Increasing labor force participation has raised women’s lifetime earnings and eligibility for Social Security benefits based on their own earnings history. At the same time, the increased likelihood of being divorced or never married has reduced women’s potential eligibility for spouse and survivor benefits, raising concerns about their retirement security, particularly among those with limited economic resources (Government Accountability Office [GAO], 2014; Harrington Meyer, Wolf, & Himes, 2006; Tamborini, Iams, & Whitman, 2009).

This changing demographic and socioeconomic context, coupled with system-financing challenges, raises a variety of issues for Social Security policy. One area of sustained interest is Social Security and women’s retirement income. Despite increasing labor force participation, earnings, and educational attainment, women continue to face a series of retirement challenges (Angel, Jimenez, & Angel, 2007; GAO, 2012; Zissimopoulos, Karney, & Rauer, 2015). Older women, particularly those unmarried, have lower retirement income and a higher risk of poverty than men have (Social Security Administration [SSA], 2016b; Tamborini, 2007). Women also have longer life expectancy in retirement (National Center for Health Statistics, 2014, table 18), which raises their income needs and the importance of Social Security benefits, most of all in advanced old age (Poterba, 2014).

A range of Social Security policy options has been discussed to address these issues. Proposals have ranged from altering eligibility rules for subgroups vulnerable to poverty, such as reducing the duration of marriage requirements for divorced spouses (Tamborini & Whitman, 2010), to changing the broader benefit structure, as in earnings sharing proposals (Iams, Reznik, & Tamborini, 2010). Caregiving credits (Favreault & Steuerle, 2007; Herd, 2006; Reno & Lavery, 2009), longevity indexing (Bipartisan Policy Center, 2010; Orszag & Diamond, 2003), longevity insurance (GAO, 2014), and increasing survivor benefits while reducing spouse benefits (GAO, 2012) have also been discussed, among many other options (Congressional Budget Office [CBO], 2010). Each option affects women differently; however, a common desire is to modernize the program to account for demographic trends over the past 50 years (Berkowitz, 2002; Favreault & Steuerle, 2007).

The objective of this article is to explore the distributional impact of introducing three types of Social Security policy options on women’s economic circumstance in retirement. Two are often discussed in the context of women’s changing work and marital patterns: (1) altering the 10-year marriage duration requirement for divorced auxiliary benefits and (2) incorporating earnings sharing in the benefit structure. The third attempts to improve income security of lower income groups by adjusting benefits to account for differential mortality by lifetime earnings.

We use the most recent version of the Modeling Income in the Near Term (MINT) model, a robust microsimulation model designed to project retirement outcomes and demographics of older Americans, to consider projected changes in Social Security benefits and retirement income under each policy alternative among women aged 60 or older in 2030. We limit our attention to divorced and widowed women to focus on two demographic groups with relatively high economic vulnerability and reliance on Social Security income in retirement (Butrica & Smith, 2012; SSA, 2016b, table 11.1; Weaver, 2010). In 2014, Social Security income constituted at least half of the family income for 56% of widows and 48% of divorced women aged 65 or older (SSA, 2016b, table 8.B3). The greater the importance of Social Security to a person’s income, the more likely their retirement security would be affected by policy changes.

The article makes several contributions to our understanding of the implications of Social Security reforms for women’s economic well-being in old age. Using the most recent MINT model, we assess multiple potential policy reforms that have not been analyzed together in a common analytical framework in the prior literature, as it relates to women’s old-age economic security. We also show important heterogeneity in each policy’s projected impact across different groups of women, paying particular attention to changes in poverty and alternative measures of poverty across key characteristics.

Literature Review

Design of Social Security Benefits

The U.S. Social Security retirement program is a social insurance system that provides benefits to workers based on their own work history but also to the spouses and survivors of qualified workers, including former spouses under certain conditions. In the program’s beginning years during the Great Depression, benefits were provided only to retired workers. However, in an effort to improve benefit adequacy for women and replace loss of income due to the death of a spouse, benefits were quickly extended to their widows (Weaver, 2010). Over subsequent decades, benefits became available to qualified spouses and to dependent divorced spouses or survivors (with 20 and later 10 years of marriage) of insured workers. 1 The design for these marriage-based benefits was based on the family structure typical in the Depression era, a “breadwinner” husband and full-time housewife in one marriage for a lifetime (DeWitt, Béland, & Berkowitz, 2008; Herd, 2005).

The basic orientation of Social Security’s retirement program to families has not drifted far from its inception, despite the fact that the life-course sequence of getting and staying married, along with low labor force participation among women, is increasingly less common (Brown & Lin, 2012). Under current law, receipt of retirement benefits is based on a person’s prior work record, their marital history, and the work record of current or former spouses. Retired worker benefits are based on a person’s work history, and to qualify, a worker must have earned at least 40 quarters (10 years) of coverage. The average of the highest 35 years of indexed earnings in covered employment (the average indexed monthly earnings [AIME]) is used to compute the basic benefit (the primary insurance amount [PIA]).

The spouses and survivors of insured workers may be entitled to auxiliary benefits based on the most recent marriage or on a prior marriage, depending on which entitlement gives the highest possible benefit. Spouse benefits may equal up to half the primary earner’s benefit, and survivor benefits may equal up to 100% of the deceased worker’s benefit. If a person is entitled to a retired worker benefit in addition to a higher auxiliary benefit, a person is dually entitled, and the retired worker benefit is supplemented to equal the auxiliary benefit level. If a person’s own retired worker benefit is higher than the auxiliary benefit, a person receives only the retired worker benefit and no auxiliary benefit. A person may be entitled to a divorced spouse or survivor benefit based on the work record of the ex-spouse if the marriage ended in divorce and if the marriage lasted at least 10 years.

While gender neutral, few men receive auxiliary benefits since men often have higher lifetime earnings than their wives. Although women increasingly receive benefits based on their own work histories, over half of female beneficiaries today receive some type of auxiliary benefit (Iams & Tamborini, 2012, chart 1). Moreover, while projections suggest continued increases in the share of women entitled to benefits based on their own work histories, these projections also show that many women will continue to receive auxiliary benefits, namely, as dually entitled survivors (Butrica & Smith, 2012; GAO, 2014). This is because women’s lifetime earnings are projected to remain lower than men’s, in part due to women taking more time out of the labor force and having lower annual earnings than men.

Social Security, Demographic Change, and Women

A prominent feature of the Social Security program is the dual goal of providing individual equity and social adequacy. The marriage-based benefits are often viewed as increasing program adequacy by providing income to an economically vulnerable segment of the population (Weaver, 2010). At the same time, concern has been raised about the inequities of these benefits. For example, a never-married woman with the same lifetime earnings as a married woman could receive a lower (retired worker) benefit than the (dually entitled spouse) benefit received by the married woman.

Several demographic changes are often viewed as challenging the program’s ability to balance equity and adequacy. One trend has been the rising labor force participation and earnings of women born after World War II (Goldin, 2006), resulting in successive generations of women reaching retirement age with more extensive earnings histories than in the past. Consequently, the percentage of women receiving benefits based solely on their own earnings record has risen, while the percentage receiving auxiliary benefits has declined (Iams & Tamborini, 2012, chart 1; Wu et al., 2013).

A second demographic trend is the retreat from marriage. Marriage has become less common, particularly among Black women, while divorce has become more common (Iams & Tamborini, 2012; Tamborini et al., 2009). Although divorce rates have leveled off somewhat since the 1970s, recent analysis by Kennedy and Ruggles (2014) suggests that divorce rates have continued to increase from 1990 to 2008, particularly among persons over the age of 35. Brown and Lin (2012) document the increasing prevalence of “gray divorce,” a trend marked by a doubling of the divorce rate among adults aged 50 or older between 1990 and 2010. Further, there is evidence of changes in the determinants of divorce over time, such as an increasing risk among those with lower levels of education (Özcan & Breen, 2012).

The trend away from marriage has implications for women’s retirement circumstance. First, divorced and never-married women represent a growing share of the elderly population (Tamborini, 2007; Tamborini & Whitman, 2010). Research has shown a strong relationship between marital history and economic resources among older women (Wilmoth & Koso, 2002; Zissimopoulos et al., 2015), including their life-course earnings trajectories (Couch, Tamborini, Reznik, & Phillips, 2013; Tamborini, Couch, & Reznik, 2015), Social Security claiming behavior (Couch et al., 2013; Gillen & Heath, 2014), and health (Hughes & Waite, 2009; Tamborini, Reznik, & Couch, (2016); Wood, Goesling, & Avellar, 2007).

The retreat from marriage has also led to a reduction in the percentage of aged women with potential entitlement to spouse and survivor benefits (Iams & Tamborini, 2012). From a social adequacy perspective, this raises concerns about increasing economic vulnerability among some unmarried women, especially those with lower levels of education and earnings, which is disproportionally correlated with being in a minority group (Angel, Prickett, & Angel, 2014; GAO, 2014; Harrington Meyer et al., 2006; Tamborini et al., 2009).

A third demographic trend is rising old-age longevity, coupled with increasing differential mortality by socioeconomic status (SES) (Manchester, Simpson, & Kim, 2014; Waldron, 2007). On average, life expectancy at age 65 in the United States has increased between 1940 and 2012 from 11.9 to 17.8 years for men and from 13.4 to 20.3 years for women (Board of Trustees, 2016, table V.A4). Increasing longevity has implications not only for Social Security costs but also for individuals’ work lives, savings plans, and reliance on Social Security income at advanced older ages, especially for women (Poterba, 2014).

Further, declining old-age mortality in the United States has not been uniform. Growing evidence suggests that mortality risks by SES have been widening over time, measured by income, education, and occupation (Bosworth & Burke, 2014 ; Bosworth & Zhang, 2015; Bound, Geronimus, Rodriguez, & Waidmann, 2014; Cristia, 2009; Goldman & Orszag, 2014; Masters, Hummer, & Powers, 2012; Montez, Hummer, Hayward, Woo, & Rogers, 2011; Olshansky et al., 2012; Preston, Stokes, Mehta, & Cao, 2014; Waldron, 2007, 2013). This leads to the policy concern that changing differentials in old-age mortality are making the Social Security system increasingly less generous to low-income individuals on a lifetime basis (Goldman & Orszag, 2014).

Against this backdrop, we estimate three types of Social Security policy options that could affect future female retirees differently. While the policies vary in their emphasis, each shares the goal of modernizing the program to help keep pace with demographic and socioeconomic changes that have occurred since its inception.

Research Design

Simulated Policy Alternatives

Altering the marriage duration requirement

The first type of policy option alters the marriage duration requirement for divorced spouse and survivor benefits. Current law requires at least 10 years of marriage to be eligible for divorced spouse or survivor benefits from an ex-spouse, a requirement that dates back to 1977 when it was changed from 20 years (SSA, 2016a, table 2.A21). We model three different provisions. First, we examine a counterfactual scenario wherein the length of marriage requirement was never reduced from 20 to 10 years. This simulation illustrates both the potential effects this policy change might have had if it had occurred today and the possible effects of going back to the prior rule. We expect that this provision would result in lower benefits for women, primarily divorced women, who would no longer qualify for higher auxiliary benefits as divorced spouses and survivors because their marriages did not last for enough years.

Second, we consider a commonly proposed provision reducing the requirement to 7 years, a means of raising the retirement incomes of aged women who do not currently meet the 10-year threshold for benefits (GAO, 2014, appendix II). Prior research demonstrated that this provision would affect only a small fraction of divorced women, but those affected would tend to experience a substantial improvement in their economic security (Tamborini & Whitman, 2010). Reexamining this provision using the updated MINT model, we expect it would increase benefits for women, primarily divorced women, who would now qualify for higher benefits as divorced spouses and survivors than as retired worker beneficiaries under current law.

Third, we estimate a provision allowing aged persons with less than 10 years of marriage to be eligible for benefits that are proportionally based on the length of the marriage. The proportions modeled are not linear to give more weight to longer lasting marriages up to 10 years. Specifically, a divorced spouse benefit would reflect an increasing proportion of the PIA of the ex-spouse based on the years of marriage: 1 year: 5%, 2 years: 10%, 3 years: 20%, 4 years: 25%, 5 years: 35%, 6 years: 40%, 7 years: 45%, 8 years: 47%, 9 years: 49%, and 10 years: 50%. These percentages are doubled for divorced survivor benefits. A version of this provision can be found in the “Retirement and Income Security Enhancements Act” (SSA, 2014). We expect that this provision would have similar results as reducing the requirement to 7 years but would affect more women.

Earnings sharing

The second type of policy option calls for the sharing of earnings between married persons during years of marriage, better known as “earnings sharing.” Earnings sharing plans propose a redesign in which the lifetime earnings record of each spouse would be credited with half of the couple’s combined earnings in years married and credited with one’s own earnings in years not married. In the case of multiple marriages, the sharing would occur with different spouses.

An overarching rationale for most earnings sharing proposals is that the economic resources acquired during a marriage, including Social Security credits, should be shared equally, regardless of the household division of labor. These proposals also have been cast as a strategy to achieve more individual equity in the system, as some have pointed to declining equity resulting from the rise in two-earner couples (Forman, 2006; Sandell & Iams, 1997; Steuerle & Bakija, 1994). Under earnings sharing, one- and two-earner couples would receive an equal benefit based on their contributions to the program.

We estimate the impact of an earnings sharing option where there are no spouse benefits, to focus the analysis on individual equity, but there are survivor benefits based on shared earnings (a surviving spouse can still receive the deceased spouse’s worker benefit). Previous analyses show that earnings sharing proposals without auxiliary benefits reduce benefits for women in the aggregate and especially for widows (Iams, Reznik, & Tamborini, 2009 , 2010). Using more recent data that account for changes in the population and national economy, we reassess a similar proposal focusing on divorced and widowed women. We expect that this option would have mixed results for divorced women, depending on the level of their earnings relative to the level of their ex-husband’s earnings and the length of their marriage. For widows, despite including survivor benefits as a possible way to alleviate some of the losses predicted by other proposals that do not include any auxiliary benefits, we still expect that this option would decrease survivor benefits for many widowed women because survivor benefits would no longer be based on the deceased husband’s nonshared earnings but rather on shared earnings.

Differential mortality by lifetime earnings

The third type of policy option attempts to mitigate changes in differential mortality by SES. This option builds on the idea that solely adjusting benefits to average life expectancy would not account for the fact that persons with high SES have exhibited the largest longevity gains (Bosworth & Zhang, 2015). As noted, greater life expectancy associates with characteristics of higher SES, and research shows that SES differentials in life expectancy of retirees have been increasing since World War II.

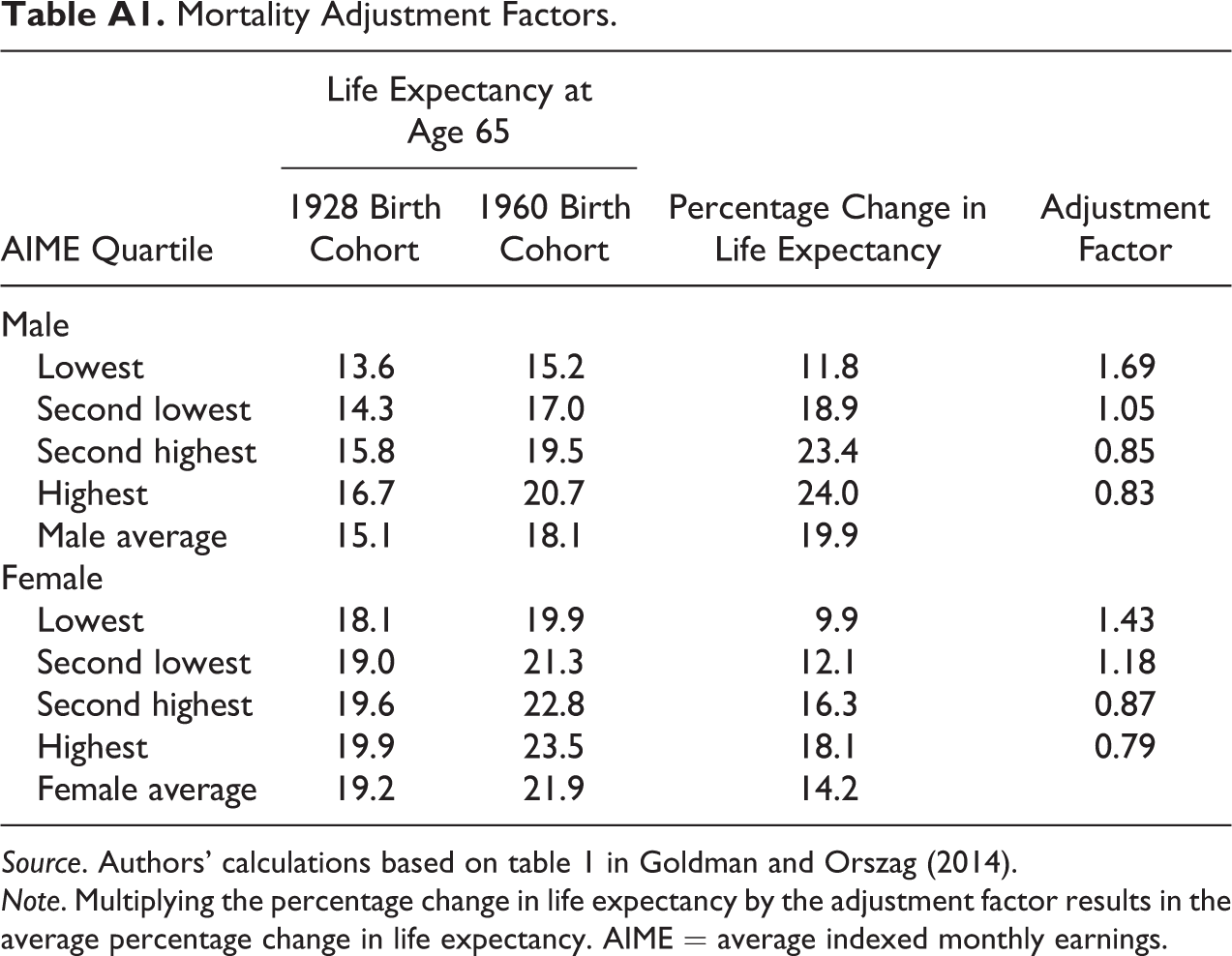

Growing policy attention has focused on possible ways that Social Security benefits could account for increasing differential mortality by SES (Waldron, 2013). Here, we examine an option that attempts to address the widening gap in mortality by lifetime earnings by adjusting the PIA using changes in gender-specific life expectancy by AIME quartile between a cohort born in 1928 and one born in the late baby boom (1960) as calculated by Goldman and Orszag (2014, table 1). Essentially, the adjustment increases the PIA for individuals in the lower AIME quartiles, who in general have had smaller improvements in life expectancy, and decreases the PIA for individuals in the higher AIME quartiles, who in general have had larger improvements in life expectancy. 2 Importantly, by making this adjustment to the PIA, rather than the final benefit, all related auxiliary benefits are also affected. It should be emphasized that this policy option would reduce the lifetime earnings differential in life expectancy for the aged population of 2030 to the level observed for the cohort retiring in the 1990s but does not aim to reduce the differential outright. We expect this option would have mixed results, increasing benefits for some women, and decreasing benefits for others, depending on whether they have characteristics related to low or high SES (e.g., education).

In sum, the three types of policy options will alter either Social Security’s eligibility rules or benefit structure. Each option has its own limitations, and each would affect divorced and widowed elderly women differently. Our analysis begins to disentangle the impact of each option on women under a unified framework using the most recent microsimulation methods available.

Method

There are various methods to disentangle the impacts of changes in Social Security’s rules and benefits, and microsimulation models are increasingly employed in this type of research (Mitton, Sutherland, & Weeks, 2000). Compared to the representative worker approach often used in the retirement literature, microsimulation techniques are better able to account for complexity in interactions between characteristics of individuals and families and complicated program rules. Microsimulation also provides a vehicle for assessing future trends in retirement income and benefits, while accounting for demographic and socioeconomic changes, and is a valuable tool for examining the distributional impacts of hypothetical policy changes.

We use the most recent version (Version 7) of SSA’s MINT microsimulation model developed by SSA’s Office of Research, Evaluation, and Statistics, with substantial assistance from the Brookings Institution, the RAND Corporation, and the Urban Institute. MINT7 is based on the 2004 and 2008 panels of the Survey of Income and Program Participation (SIPP) matched to SSA’s longitudinal earnings and benefit records. Detailed information on MINT7’s methodology can be found in Smith and Favreault (2013).

We examine the distributional effects of three types of policy options on the Social Security benefits and retirement income of the projected female population aged 60 or older in 2030 (born in 1970 and earlier), a time when almost all of the baby boom cohort (born 1946–1964) will have attained their Social Security full retirement age. 3 We focus on women projected to be divorced or widowed in 2030 and assume that the options were in effect their entire lives. Current marital status, as used herein, refers to the most recent marriage. Women in 2030 are classified as “divorced” if their last marriage ended via divorce, regardless of whether their ex-husbands are alive or dead, and classified as “widowed” if their last marriage ended via the death of their husband. We exclude women who ever received disability benefits. All results are weighted to reflect the national population.

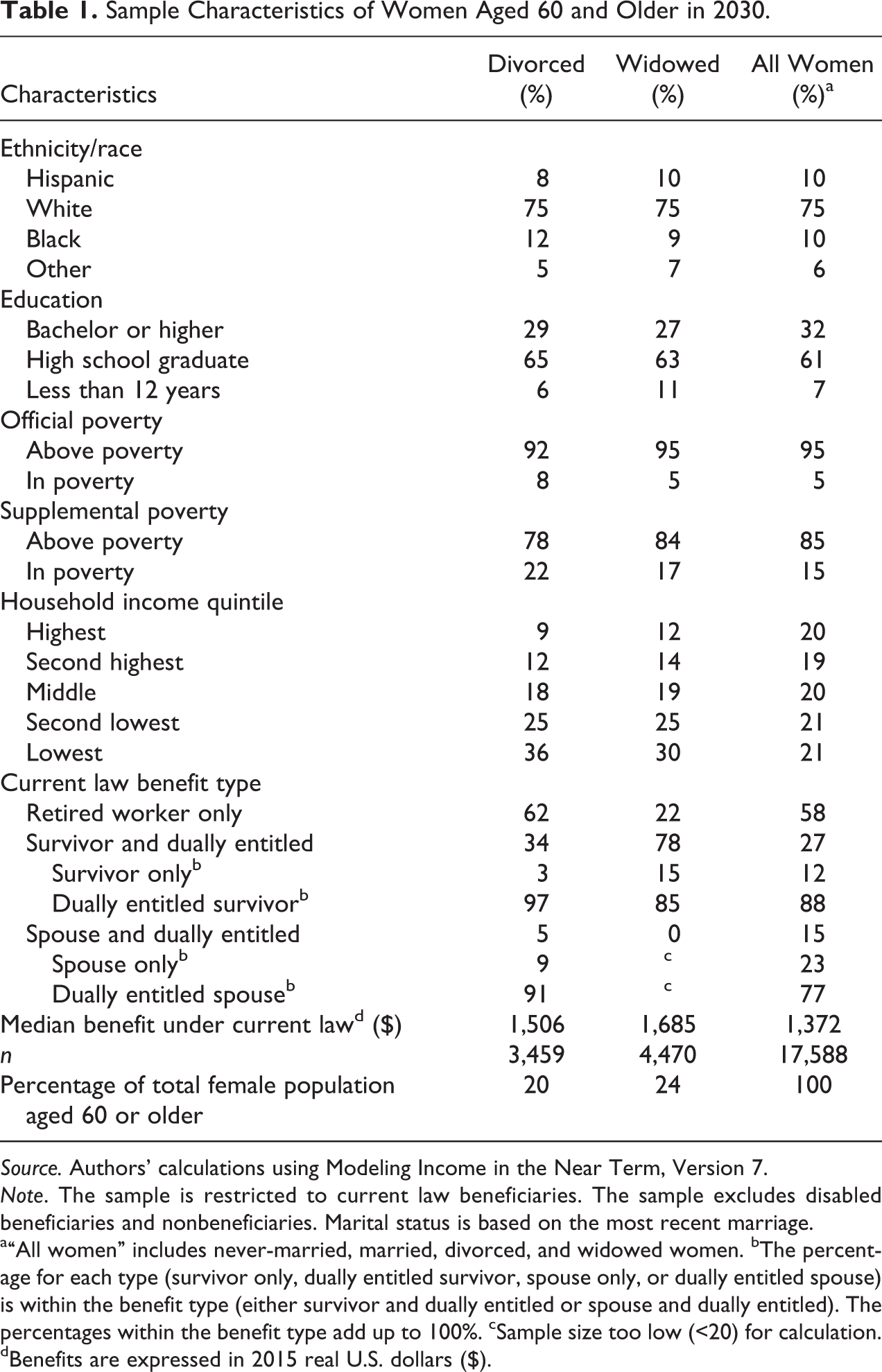

We contrast several outcomes relative to current law. A main outcome of interest is the percentage of women, divorced or widowed, experiencing an increase or a decrease in their individual Social Security benefit levels. We also analyze the extent of the change among the affected population across key demographic subgroups. One key subgroup is the type of benefit received in 2030 under current law, whether retired worker only, survivor only, dually entitled survivor, spouse only, or dually entitled spouse. To gauge how the policies might affect women’s economic vulnerability, we examine the change in the projected official poverty rate (OPR) and supplemental poverty rate (SPR), an alternative measure of poverty developed by the Census Bureau that accounts for resources other than cash income and for additional expenses (Fox, Wimer, Garfinkel, Kaushal, & Waldfogel, 2015; Haveman, Blank, Moffitt, Smeeding, & Wallace, 2015; Short, 2013). Generally, the SPR is higher than the OPR for the aged because it includes out-of-pocket medical expenses, an important component of living expenses for many of the elderly (Bridges & Gesumaria, 2014; Levitan et al., 2010; Zedlewski, Gianarelli, & Wheaton, 2010). Furthermore, MINT7 assumes the OPR and SPR thresholds increase by prices and wages, respectively, and wages are assumed to grow about 1% faster per year than prices. 4 Table 1 presents the descriptive statistics of our sample population based on MINT7 projections.

Sample Characteristics of Women Aged 60 and Older in 2030.

Source. Authors’ calculations using Modeling Income in the Near Term, Version 7.

Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

a“All women” includes never-married, married, divorced, and widowed women. bThe percentage for each type (survivor only, dually entitled survivor, spouse only, or dually entitled spouse) is within the benefit type (either survivor and dually entitled or spouse and dually entitled). The percentages within the benefit type add up to 100%. cSample size too low (<20) for calculation. dBenefits are expressed in 2015 real U.S. dollars ($).

Results

Altering the Marriage Duration Requirement

The first type of policy option alters the required years of marriage to receive divorced spouse and survivor benefits. Three different provisions are assessed. Because these provisions primarily affect the divorced, we only discuss estimates for that group.

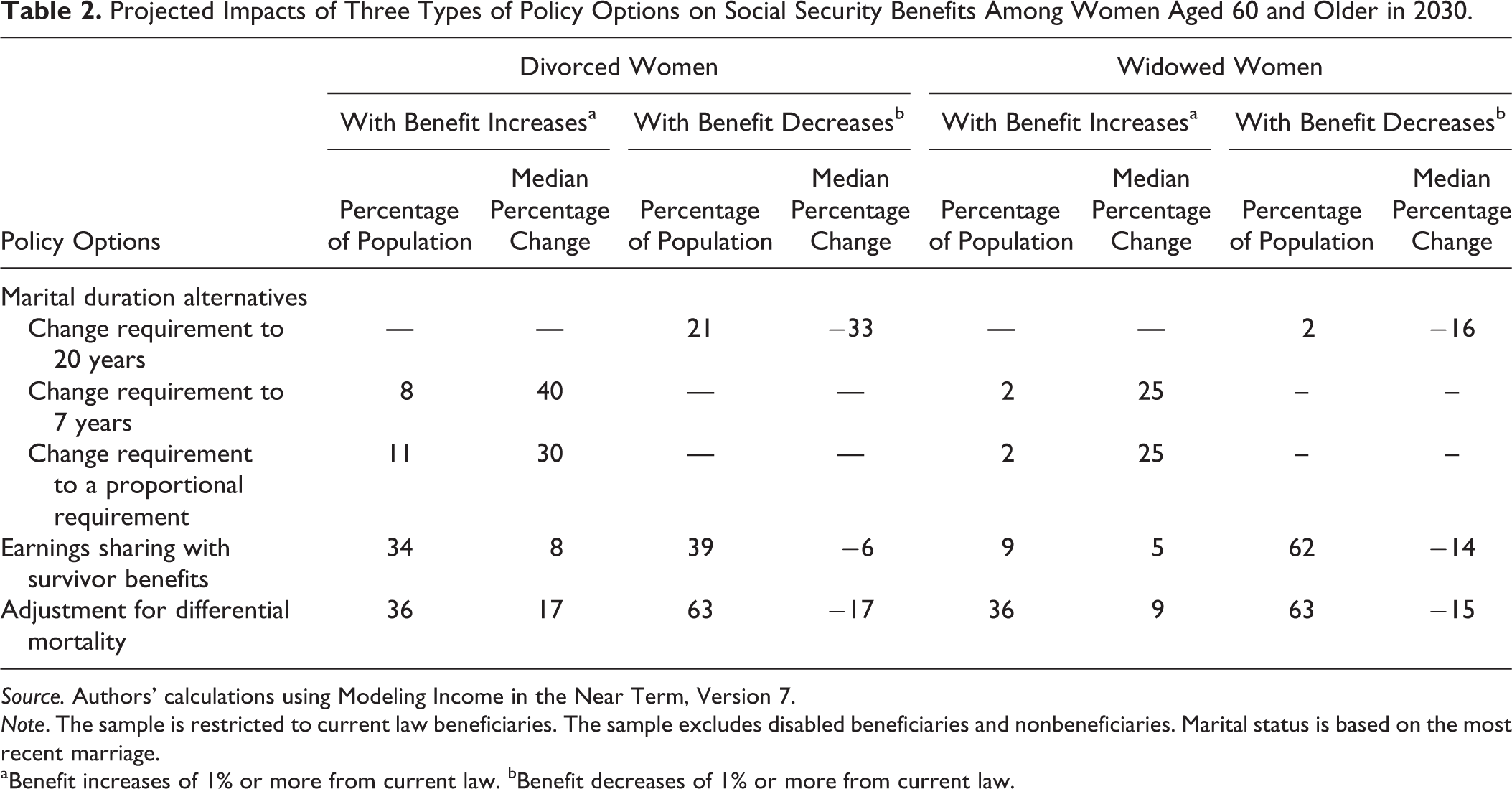

Overall, the counterfactual option (i.e., going from 10 to 20 years) would have a much larger impact than the other provisions (Table 2). In particular, about a fifth (21%) would have lower benefits under a 20-year requirement. In contrast, reducing the 10-year requirement to a 7-year requirement and the proportional provision would increase benefits of about 8% and 11% of divorced women, respectively.

Projected Impacts of Three Types of Policy Options on Social Security Benefits Among Women Aged 60 and Older in 2030.

Source. Authors’ calculations using Modeling Income in the Near Term, Version 7.

Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

aBenefit increases of 1% or more from current law. bBenefit decreases of 1% or more from current law.

We find a substantial change in benefit levels among those affected by each of the provisions. Among divorced women affected by the shift from 10 to 20 years, the typical benefit reduction would be about 33%. Likewise, among divorced women affected by a shift from 10 to 7 years and by the proportional provision, the typical gain in benefits would be quite large, at about 40% and 30%, respectively.

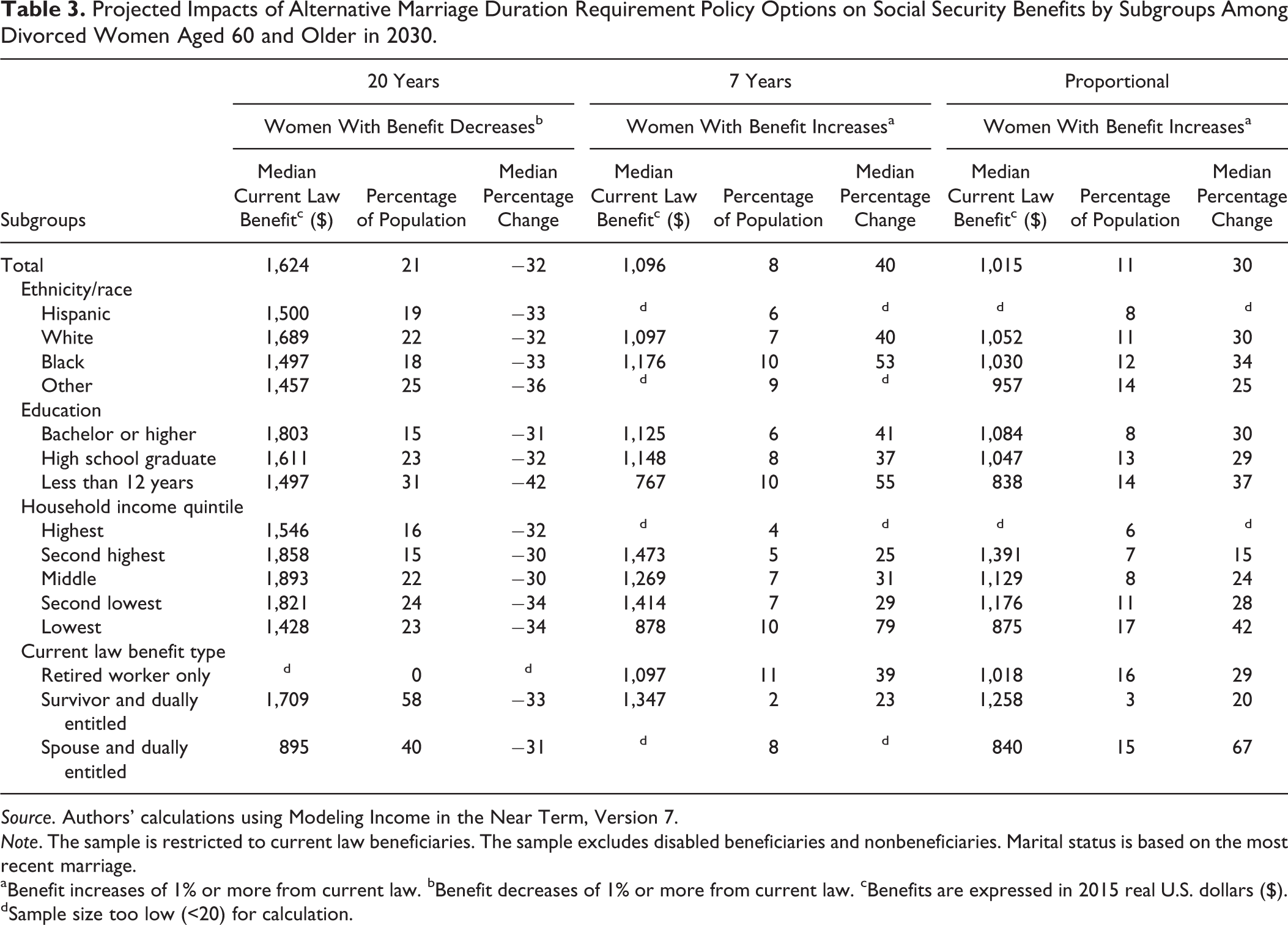

Table 3 displays the distributional implications across key subgroups for divorced women affected by each of these provisions. Overall, the impact would be greatest among those with lower socioeconomic attainment, such as less education or lower income. For example, the 20-year requirement shows that higher shares of less educated women and women with lower household incomes would experience benefit decreases relative to current law.

Projected Impacts of Alternative Marriage Duration Requirement Policy Options on Social Security Benefits by Subgroups Among Divorced Women Aged 60 and Older in 2030.

Source. Authors’ calculations using Modeling Income in the Near Term, Version 7.

Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

aBenefit increases of 1% or more from current law. bBenefit decreases of 1% or more from current law. cBenefits are expressed in 2015 real U.S. dollars ($). dSample size too low (<20) for calculation.

The distribution of benefit increases under the other two provisions (7-year requirement and proportional benefits) also appears to be concentrated among more economically vulnerable subgroups. For example, the 7-year requirement would raise the benefits of 10% of divorced women in the lowest income quintile relative to 4% of those in the highest. Additionally, those in the lowest income quintile would experience a greater increase in benefits (79%) than those in the higher quintiles. A similar pattern is observed for the proportional provision.

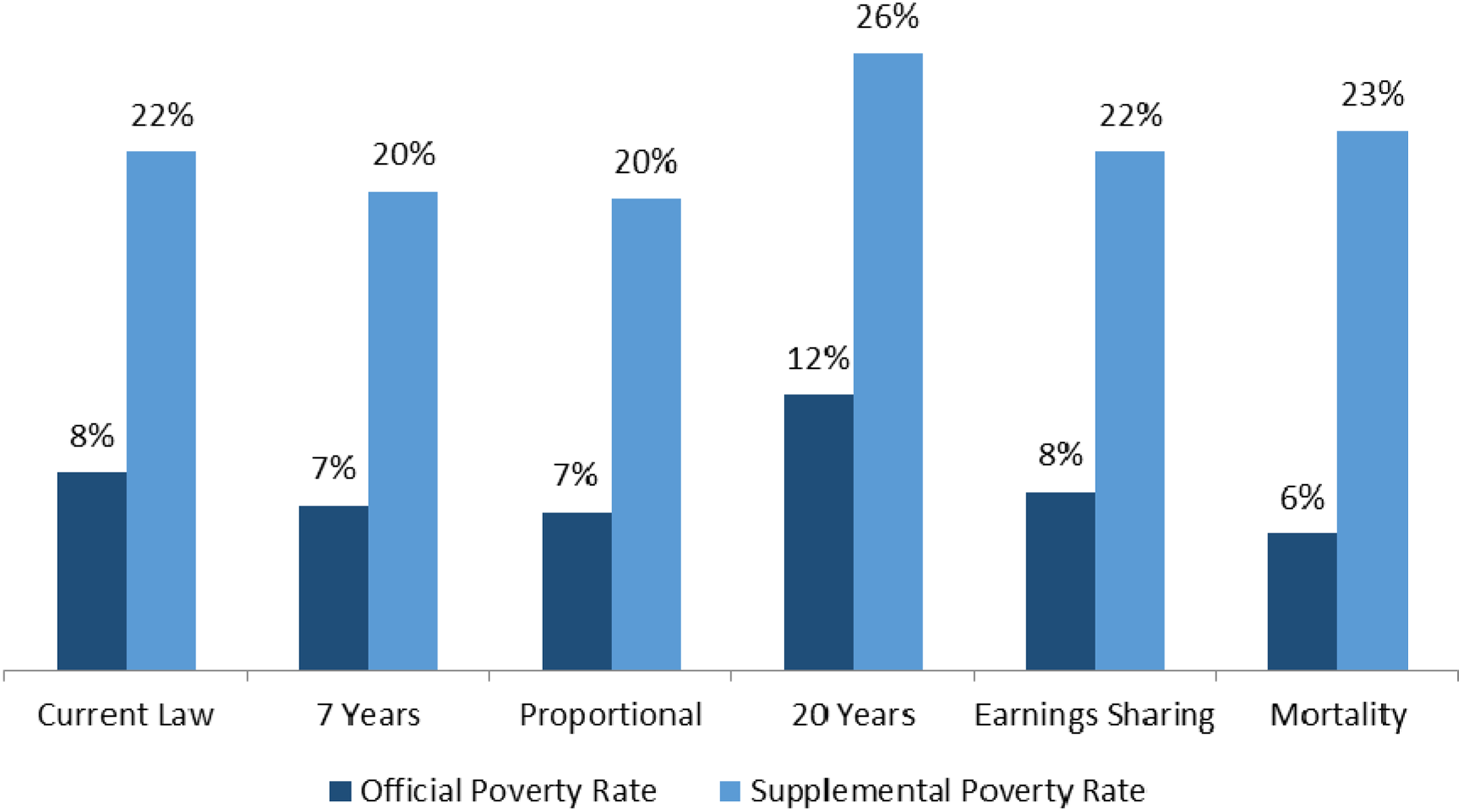

In terms of economic vulnerability, we see that each provision has appreciable, though varied, effects on poverty (Figure 1). Under the 20-year requirement, we find a substantial increase of about 4 percentage points in their OPR (approximately 237,000 additional women [not shown]) and SPR (approximately 298,000 additional women [not shown]). The 7-year and proportional provisions would reduce the poverty rates by roughly 1–2 percentage points. 5

Projected official and supplemental poverty rates under various policy options among divorced women aged 60 and older in 2030. Source. Authors’ calculations using Modeling Income in the Near Term, Version 7 (MINT7). Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

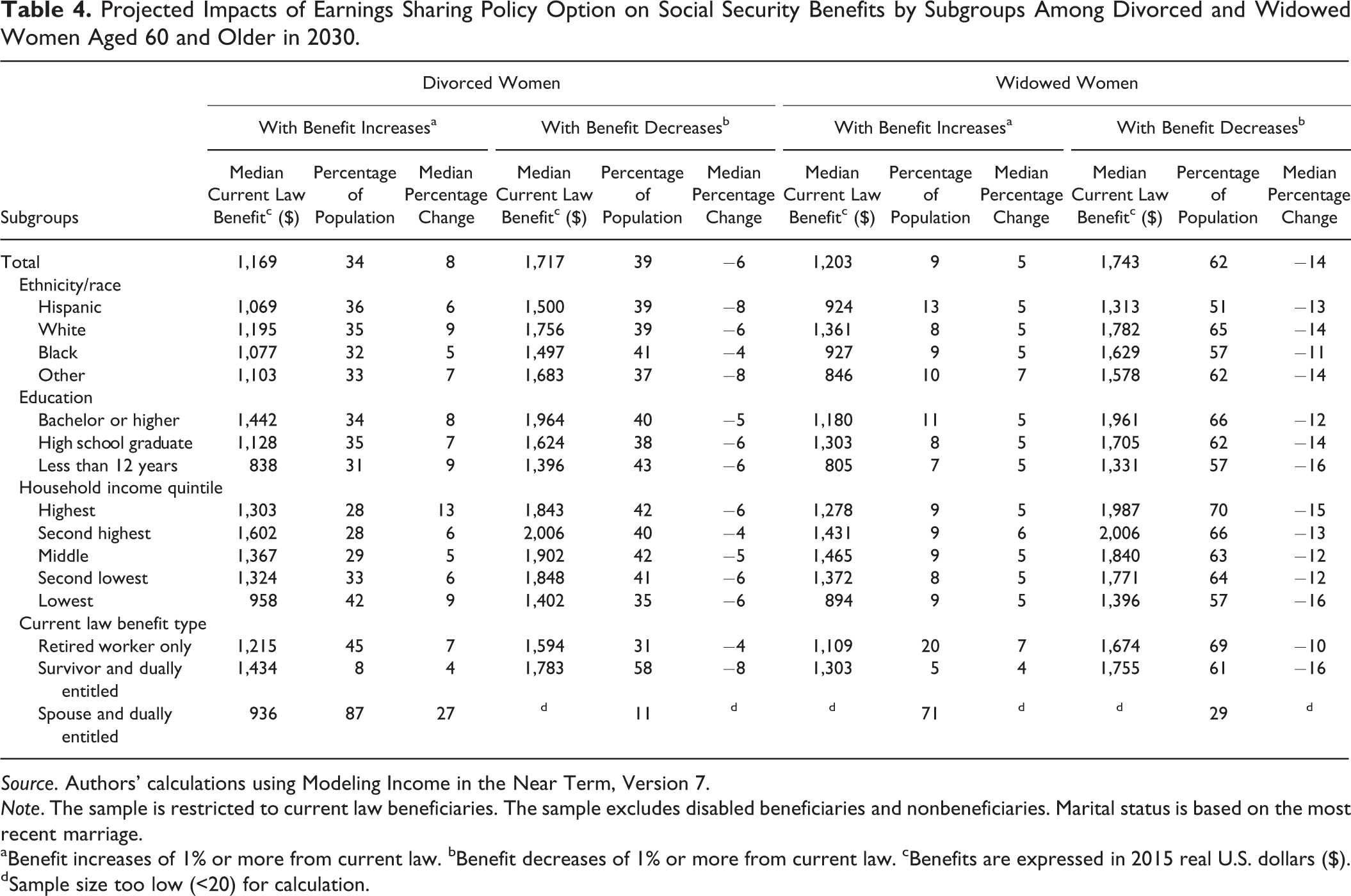

Earnings Sharing

Table 2 shows the projected impact of earnings sharing for divorced and widowed women. Under earnings sharing, benefit amounts are altered in complex ways for about three quarters of divorced (73%) and widowed (71%) women. Among the divorced, benefits are about equally likely to decrease (39%) as increase (34%), depending on their level of earnings relative to their ex-husband’s and whether he is alive.

In contrast, benefits would decline for the majority (62%) of widows, with few experiencing increases (9%). The large share of widows experiencing losses results from basing the survivor benefit under earnings sharing on the deceased husband’s “shared earnings” during marriage, as opposed to his full earnings record. This sharing of earnings during marriage reduces the lifetime earnings used in the husband’s benefit calculation, leading to a reduced survivor benefit. Moreover, for women negatively affected, the relative change in benefits is sharper for widows than for divorced women.

Table 4 shows diverse consequences across subgroups of divorced and widowed women. A key characteristic is benefit type. Survivor beneficiaries, including dually entitled survivors, would often experience declines in benefits (58% for divorced women and 61% for widows). As explained above, this is because sharing earnings during years of marriage reduces the deceased husband’s PIA, the basis of the survivor benefit, whether divorced or widowed. By contrast, divorced spouse and dually entitled beneficiaries, an uncommon benefit type, would experience increases in benefits (87%) and few reductions (11%). These benefit gains are attributable to an increase in lifetime earnings due to sharing earnings with their higher earning ex-husbands in years of marriage and the likely switch to receiving benefits as retired worker beneficiaries.

Projected Impacts of Earnings Sharing Policy Option on Social Security Benefits by Subgroups Among Divorced and Widowed Women Aged 60 and Older in 2030.

Source. Authors’ calculations using Modeling Income in the Near Term, Version 7.

Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

aBenefit increases of 1% or more from current law. bBenefit decreases of 1% or more from current law. cBenefits are expressed in 2015 real U.S. dollars ($). dSample size too low (<20) for calculation.

Among retired worker beneficiaries, almost half (45%) of the divorced and only a fifth (20%) of widows would experience benefit increases, as their earned benefits increase due to the addition of shared earnings in years of marriage in cases where the husband had higher earnings. At the same time, almost a third (31%) of divorced and more than two thirds (69%) of widowed retired worker beneficiaries would receive reduced benefits. This may appear counterintuitive at first, but in this case, the divorced or widowed retired worker beneficiary had higher earnings than her former or deceased husband did during the years of marriage, and under earnings sharing, these higher earnings are shared with the lower earning husband, resulting in a lower benefit.

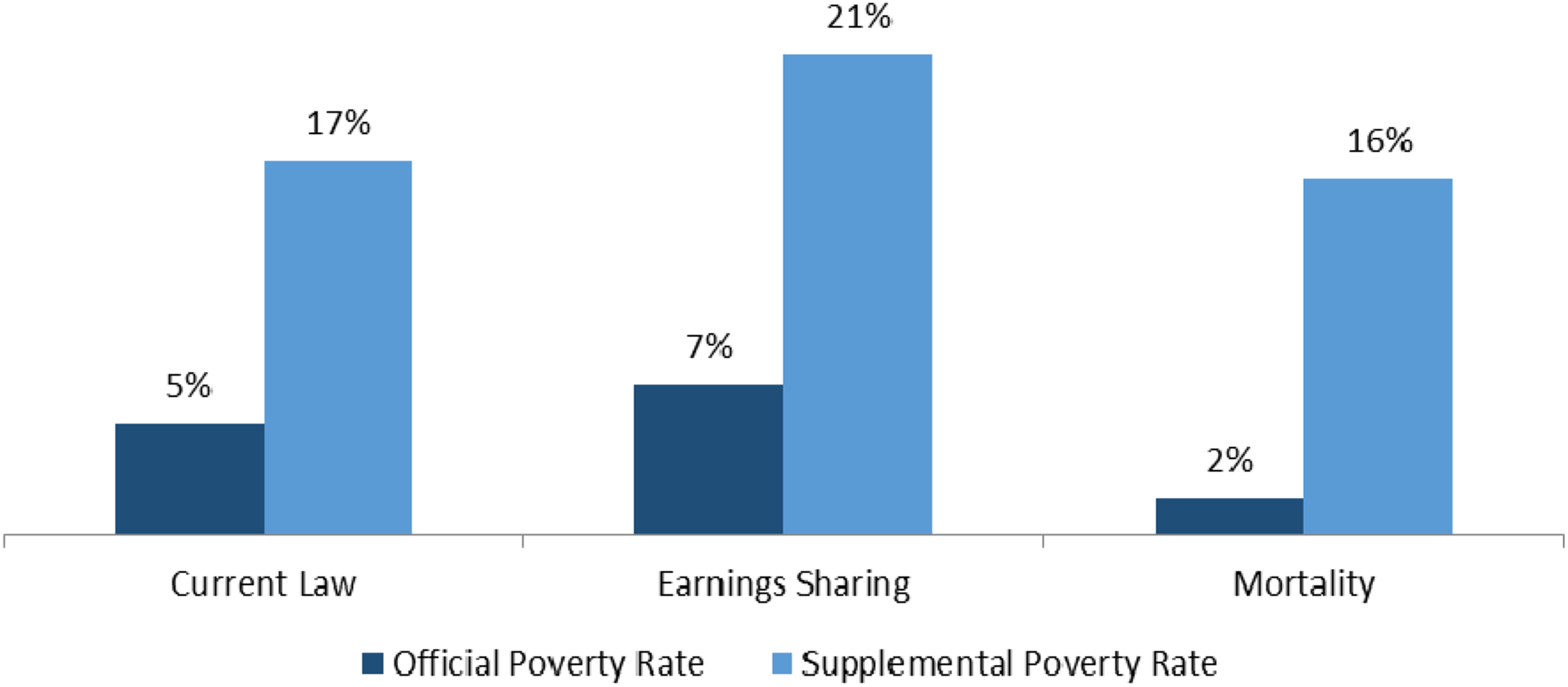

In terms of economic vulnerability, a higher share of divorced women in the lowest income quintile would experience benefit increases, at around 42%, relative to those in the highest income quintile, at 28%. The majority of widows, including those in the lowest income quintile (57%), would experience benefit reductions. With regard to poverty, earnings sharing would have almost no impact on the overall poverty rates for divorced women (Figure 1). However, it would substantially reduce financial security among widows (Figure 2), as indicated by an increase in their OPR of about 2 percentage points (approximately 153,000 additional women [not shown]) and SPR of about 4 percentage points (approximately 402,000 additional women [not shown]).

Projected official and supplemental poverty rates under various policy options among widowed women aged 60 and older in 2030. Source. Authors’ calculations using Modeling Income in the Near Term, Version 7 (MINT7). Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

Differential Mortality by Lifetime Earnings

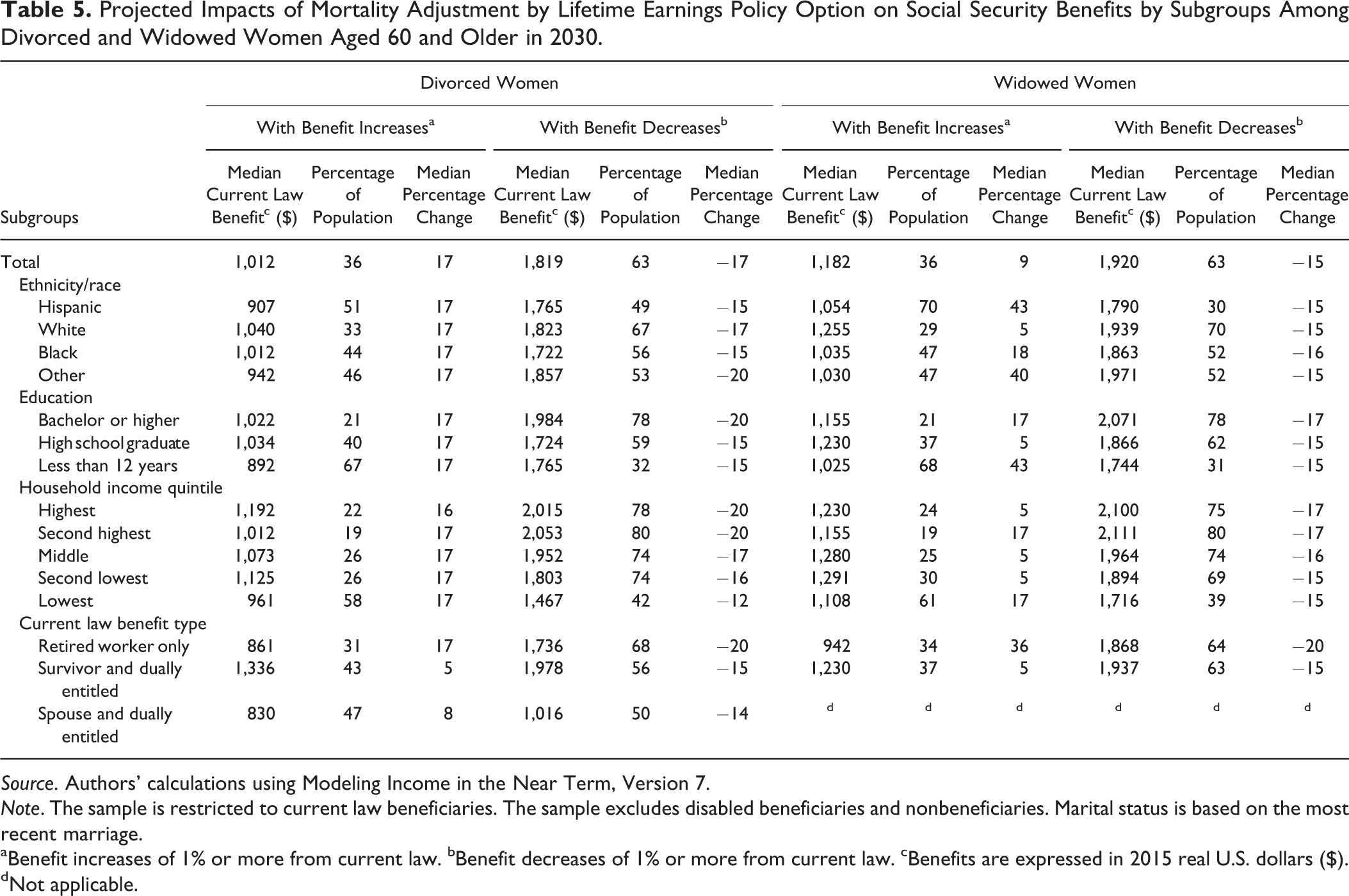

The adjustment for the increasing gradient in mortality by lifetime earnings would affect virtually all divorced and widowed women (Table 2). We find increased benefits for 36% and decreased benefits for 63% of divorced women and widows. Even though these patterns are similar for divorced and widowed women, the trends underlying them are likely to be different. For divorced women, reduced benefits would be expected for women with high lifetime earnings who are also retired worker beneficiaries. For widows, reduced benefits would more likely be due to having been married to a now-deceased husband with high lifetime earnings. The typical benefit reduction would be around 15–17% for these women. For those experiencing benefit increases, the typical increase would be 17% for divorced women and 9% for widows.

Table 5 shows diverse impacts across subgroups. In general, the results suggest that economically vulnerable divorced and widowed women are more likely to gain from the mortality adjustment, as expected. By education, a greater percentage of divorced women without a college degree would experience benefit increases (40% and 67%, respectively) than those with one (21%). This is expected insofar as these women, as well as their ex-husbands, are likely to have lower lifetime earnings. The median gain would be about 17%. We see a similar pattern among widows; however, the median benefit increase would be greater in some cases, particularly for high school dropouts. Additionally, advantaged groups, for example, those with higher household income, are more likely to experience benefit decreases than those from more disadvantaged groups.

Projected Impacts of Mortality Adjustment by Lifetime Earnings Policy Option on Social Security Benefits by Subgroups Among Divorced and Widowed Women Aged 60 and Older in 2030.

Source. Authors’ calculations using Modeling Income in the Near Term, Version 7.

Note. The sample is restricted to current law beneficiaries. The sample excludes disabled beneficiaries and nonbeneficiaries. Marital status is based on the most recent marriage.

aBenefit increases of 1% or more from current law. bBenefit decreases of 1% or more from current law. cBenefits are expressed in 2015 real U.S. dollars ($). dNot applicable.

The impact on economic vulnerability is greater for widows than for divorced women. The OPR for divorced women would decrease 2 percentage points (approximately 180,000 fewer women [not shown]), but the SPR would increase by 1 percentage point (approximately 60,000 additional women [not shown]; Figure 1). For widows (Figure 2), the OPR would decrease by 3 percentage points (from 5% to 2%; approximately 279,000 fewer women [not shown]). The effects on the SPR are more negligible.

Discussion and Conclusion

Using the most recent version of SSA’s MINT microsimulation model, we assessed the distributional impacts of three types of Social Security policy options, focusing on aged divorced and widowed women in 2030. The analysis provides a unified set of results using a common method in order to contrast the possible effects of these options. The results confirm that these options would have substantial impacts on the Social Security benefits and retirement income of divorced and widowed women, but each policy would affect them differently. We also find varied consequences across diverse subgroups of divorced and widowed women.

In terms of the marriage duration requirement, we find that returning to a 20-year threshold for divorced auxiliary benefits would have a greater impact than the other two provisions examined in the share of affected divorced women and in the magnitude of changes in their poverty status. Thus, in relation to Social Security’s program goals, reducing the requirement from 20 to 10 years in 1977 can be seen as a modification that improved the social adequacy of the program for generations of divorced women, principally those with low lifetime earnings.

In addition, reducing the requirement to 7 years or allowing proportional benefits would improve the economic security of disadvantaged divorced women without qualifying marriages under current law, namely, those in the lower income quintiles and those without a college degree. This suggests that further reducing the requirement or introducing proportional benefits would likely improve the social adequacy of the program for divorced women, particularly those with characteristics that are associated with low SES. At the same time, such provisions may raise a new set of equity concerns related to the program’s treatment of marriage since additional women would qualify for marriage-based benefits, potentially exacerbating the current inequities in the auxiliary benefit structure.

An important finding related to the earnings sharing option is the substantial impact on some divorced women and on many widows. About 87% of divorced women with a spouse or dually entitled spouse benefit type would experience higher benefits, but this subgroup represents only about 5% of the divorced population. Poverty rates would be higher for widows, and about 62% of widows would experience lower benefits, even though survivor benefits based on shared earnings were retained. The main factor driving these reductions is that the vast majority of widows receive 100% of their husband’s PIA, and under earnings sharing, the husband’s PIA incorporates half the couple’s shared earnings during marriage, which is often lower than his PIA based only on his own lifetime earnings as under current law. In relation to program goals, earnings sharing would improve individual equity within the system and may improve adequacy for a very small segment of divorced women (i.e., divorced spouse beneficiaries), but at the cost of reduced adequacy for a substantial share of widows and surviving divorced beneficiaries.

The option that would adjust for the increasing differentials in life expectancy by lifetime earnings would affect virtually all divorced and widowed women. Overall, this option would lead to higher benefits for over a third of divorced women and widows, but lower benefits for almost two thirds of them. These reductions are largely due to the often-unforeseen complexity in adjusting benefits for mortality by lifetime earnings based on the primary benefit payee. For example, lower benefits could occur if either the woman, if she is a retired worker beneficiary, or the ex-husband, if she receives auxiliary benefits based on his PIA, is a high lifetime earner and thus subjected to the downward adjustment for high earners.

The results also highlight diverse consequences of the mortality adjustment across different groups of women. Women in lower socioeconomic groups exhibited rising benefits more often than women in higher socioeconomic groups. This is expected, even though the husband’s lifetime earnings are used as the basis of the adjustment for many women, since marriage often occurs between individuals in the same SES (Schwartz, 2013). As such, this option improves the retirement security of more vulnerable subgroups of women, improving benefit adequacy, as well as individual equity, on a lifetime basis.

The study contains several noteworthy limitations. First, we examined the distributional impact of each option leaving aside the effects on Social Security system finances. To be sure, each option would have differing effects on Social Security’s actuarial deficit (CBO, 2010). Second, we did not analyze other groups of women (e.g., married or never-married women) or men. Earnings sharing and the mortality adjustment would have substantial impacts on these groups. Third, the possible reform options are extensive, and here, we only examine several approaches with a specific focus on divorced and widowed women. Fourth, we excluded women who received disability benefits, but they may also be affected. Finally, projections could have measurement error that could reduce the precision of our estimates.

The future will bring further demographic and socioeconomic changes in the American population that will reshape the retirement experience of today’s working-age population when they reach retirement age and could lead to a future need for changes in Social Security’s program structure. This article provides one approach to examining both possible policy responses to alter the Social Security system in response to historical changes in American society using microsimulation methods and a path to evaluating similar changes encountered in the future.

Footnotes

Appendix

Mortality Adjustment Factors.

| AIME Quartile | Life Expectancy at Age 65 | Percentage Change in Life Expectancy | Adjustment Factor | |

|---|---|---|---|---|

| 1928 Birth Cohort | 1960 Birth Cohort | |||

| Male | ||||

| Lowest | 13.6 | 15.2 | 11.8 | 1.69 |

| Second lowest | 14.3 | 17.0 | 18.9 | 1.05 |

| Second highest | 15.8 | 19.5 | 23.4 | 0.85 |

| Highest | 16.7 | 20.7 | 24.0 | 0.83 |

| Male average | 15.1 | 18.1 | 19.9 | |

| Female | ||||

| Lowest | 18.1 | 19.9 | 9.9 | 1.43 |

| Second lowest | 19.0 | 21.3 | 12.1 | 1.18 |

| Second highest | 19.6 | 22.8 | 16.3 | 0.87 |

| Highest | 19.9 | 23.5 | 18.1 | 0.79 |

| Female average | 19.2 | 21.9 | 14.2 | |

Source. Authors’ calculations based on table 1 in Goldman and Orszag (2014).

Note. Multiplying the percentage change in life expectancy by the adjustment factor results in the average percentage change in life expectancy. AIME = average indexed monthly earnings.

Acknowledgments

The authors thank Glenn Springstead, Dave Shoffner, Karen Glenn, Mark Sarney, and Natalie Lu for their helpful comments and suggestions. The findings and conclusions presented here are those of the authors and do not necessarily represent the views of the Social Security Administration.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.