Abstract

Governance and ownership structures are crucial to analyzing organizational risk, especially in emerging economies with changing legal frameworks. Board characteristics—turnover, diversity, size, CEO tenure and experience, directors’ international exposure, and financial expertise—impact corporate risk, while ownership structures—family, managerial, institutional, and state—moderate the effect. This study examined how governance systems and varied ownership forms affect company stability and risk. Data from 2013-2024 panel observations of 200 firms listed on the Pakistan Stock Exchange (PSX) was used in this quantitative study. Governance factors, ownership patterns, and company risk were examined using descriptive statistics, correlation analysis, heteroskedasticity tests, and multiple regression models. Interaction terms were used to investigate ownership structure moderating effects. Changes to the board, board size, CEO tenure, and director experience overseas all affect corporate risk. Only little important was directors’ money experience. Moderation was heavily influenced by ownership. Governance and risk were stronger when a company was controlled by a family or institution. Government-owned companies had varied results. Foreign and institutional ownership reduced risk, stabilizing things. By showing how board traits and ownership arrangements affect firm risk, this research advances corporate governance. Effective governance involves board composition and firm ownership structure. Policy implications indicate that regulators should focus on board composition reforms and ownership transparency to stabilize corporate risk in emerging markets such as Pakistan.

Introduction

Company governance is how it runs and controls itself. It seeks to align shareholder, management, and board interests. Corporate governance means shareholders obtain the most money and the company is fair and open. 1 Poor governance makes emerging countries like Pakistan more vulnerable to financial crises, whereas good governance strengthens them. 2 Board independence and ownership openness reduced bank risk-taking across regulatory frameworks. 3 Businesses use more advanced risk management systems due to the uncertain global economy. 4 Business operations are riskier due to inflation and rising energy prices. 5 Thus, business risk management is crucial for organizations to survive in challenging economic times. 6 This risky environment threatens corporate performance, investor trust, and market stability. 7

Businesses are struggling with financial, operational, and strategic risks as the global economy weakens. Supply chain, energy, and currency market changes have made organizations more conscious of systemic and unique risks. 8 Geopolitical conflicts like trade wars and sanctions make risk management difficult for multinational firms. 9 These global shifts have increased firms’ adoption of risk governance frameworks including scenario planning and stress testing to handle external shocks. 10 The International Monetary Fund reported inflation and economic slowdowns damaged businesses’ credit ratings worldwide. Attitudes toward risk have evolved. Epidemics have accelerated digital technology use and produced technological issues that have raised cybersecurity and data protection threats. 11 These hazards need firms to strengthen risk management and monitor the outside world to adjust their strategies promptly. 12 As part of this transformation, stakeholders and regulators urge enterprises to include environmental hazards in their risk frameworks. 13

International trade barriers change and international relations are unpredictable, making cross-border operations and supply chain resilience riskier. 14 Recent empirical studies show that increasing uncertainties demand adaptive governance frameworks in which boards actively manage risk and adjust ownership structures to enhance risk-aware decision-making. 15 Companies can’t predict how much customers will buy due to rising inflation and borrowing rates. All of them increase earnings volatility and capital structure concerns. 16 SMEs are finding it harder to borrow money and be flexible due to economic issues. This is due to limited access to finance markets. 17

Technological advancement and invention cycles have made products last less, making it riskier to be outdated and compete with other enterprises. 18 Companies with outdated risk management practices risk losing money and reputation, which can hurt market share and investor trust. 19 Natural resource and carbon-intensive companies are monitored and fined, increasing their risks. 20 Market risks arise from demographic and client choice changes that make demand uncertain and products less useful. 21

Businesses must enhance and update their risk management plans. Recent research suggests that diverse, autonomous boards and risk-reducing ownership frameworks are better at resolving these complicated concerns. Economic uncertainty has increased credit and liquidity risks in capital-intensive sectors and tightening monetary policy areas. 22 As global financial markets interact, corporations risk contagion from shocks in other economies or industries. Financial troubles can spread quickly through global networks, increasing firm risk beyond operational failures. 14

Board members’ understanding of finance, risk management, and key sectors strongly influences corporate risk behavior. Financial professionals and high-risk industry boards employ more advanced risk assessment frameworks to identify and mitigate risks. 21 Dynamic risk oversight boards encourage balanced risk-taking. These boards emphasize monitoring risk strategies and adapting them to market changes. 23 More board meetings and risk discussions improve supervision and risk control. 24

Problem statement

Board diversity, tenure, size, and financial expertise have been extensively studied, but how they interact with state, family, management, and institutional ownership arrangements to effect firm risk has not. Modern research often ignores the complex implications of ownership structure on board choices and risk outcomes in emerging economies where ownership concentration considerably affects risk profiles. The long-term impacts of board changes on business risk management and how good governance reduces them are unknown. 25 Due to new legislation, shareholder activism, and increasing responsibility, board members change frequently in today’s fast-paced business sector. New directors provide additional oversight and strategic advice, but they can also confuse and disrupt operations. This study addresses this deficit by examining board characteristics’ direct effects on business risk and ownership structures’ moderating effects. Thus, it examines how ownership and board-level governance affect risk-taking in economic and institutional environments.

Research gap

Most research on board changes and business risk focuses on established countries, where governance and market dynamics differ from emerging economies. 26 Board size, diversity, and CEO tenure are generally examined separately without considering how they affect business risk with varied ownership structures. Corporate risk assessments require understanding the complex link between governance frameworks and ownership structures, which this fragmented approach ignores. To understand how board composition and ownership affect business risk over time, longitudinal research is needed to detect trends that short-term studies miss. 25 In developing countries like Pakistan, with concentrated ownership and evolving government frameworks, these dynamics are more difficult. These qualities are crucial, but Pakistan lacks empirical data on how board and ownership structure changes affect business risk over time. This gap highlights the need for context-specific, longitudinal research on governance-risk nexus in these economies. 27

Research objectives

• To examine direct impact of board changes, board diversity, board size, CEO tenure, Director Foreign Experience and director financial expertise on firm risk. • To explore moderating effects of ownership structure in relationship between board characteristics and firm risk.

Research questions

(1) What is impact of board changes, board diversity, board size, CEO tenure, Director Foreign Experience and director financial expertise on firm risk? (2) Does ownership structure moderates’ relationship between board characteristics and firm risk?

Literature review

Corporate governance literature has extensively studied board features as risk factors. Board size, independence, CEO dual function, gender diversity, and financial abilities affect risk-taking and strategic decisions. Bigger boards can assess risks better due to their diverse talents and perspectives. If board is too huge, it may be tougher to collaborate and make decisions, putting the firm at risk. Al-Dhamari and Ismail 28 found that Malaysian enterprises with large boards took more risks due to poor oversight. Board independence is crucial for corporate risk reduction. Independent directors, who don’t operate the company, are more likely to monitor management and oppose risky initiatives. Nguyen et al. 29 suggest board independence significantly reduces market-based risk indicators in Asia, specifically stock return volatility. According to Chen et al., 30 firms with more independent directors had lower default rates and higher credit ratings. These findings support agency theory by showing that independent oversight reduces opportunistic executive behavior and organizational risk.

CEO duality—CEO as board chair—has been investigated in risk governance. CEO duality may simplify decision-making but may also reduce board oversight and business risk. Yousaf et al. 31 found a strong association between CEO duality and business risk in Pakistani banks, suggesting dual responsibilities hinder control. Chinese research suggests duality may help organizations adapt faster to market shifts. The risk impact of gender diversity on boards is becoming well acknowledged. 32 García-Sánchez et al. 17 found that boards with diverse genders tend to adopt conservative financial policies, reducing financial risk for European enterprises. Rahman et al. 33 found that gender diversity on boards reduced stock return volatility and operational risk in emerging economies, highlighting the importance of governance quality.

Risk management also requires money-savvy board members. Directors with finance or accounting backgrounds can better analyze financial statements, identify issues, and manage risk. Lee and Park 23 said money-savvy audit committee members improved risk controls and internal audit processes. A U-shaped association between board tenure and business risk in South Asian firms was found by Mahmood et al. 34 Long-term tenure reduced board independence and increased risk, while moderate tenure reduced risk. Technology-savvy board members reduce cybercrime and foster innovation. IT and cybersecurity boards are growing more crucial as digital disruption affects practically every company. Dey et al. 35 found that tech-savvy directors reduced cyber incidents and changed their organizations digitally safely, lowering risk over time. Crisis resilience and board adaptation are more relevant since COVID-19. Risks were reduced by boards that could quickly change processes, shift resources, and move things. Sadiq and Javed 36 claim that agile boards with diverse capabilities, decentralized authority, and scenario preparation minimized epidemic-related financial losses.

Examined how Industry 5.0 technologies and circular economy practices improve sustainable performance from the stakeholder theory perspective. The study found that disaster prevention practices and circular economy significantly strengthen organizational sustainability outcomes.

37

Investigated the relationship between corporate social responsibility (CSR) and sustainable firm performance. The findings revealed that employee wellbeing mediates this relationship, while supportive organizational culture positively moderates sustainable outcomes.

38

Explored the determinants influencing consumer purchase intention in the metaverse environment. The study highlighted that consumer flow experience significantly mediates the relationship between metaverse factors and purchase intention.

39

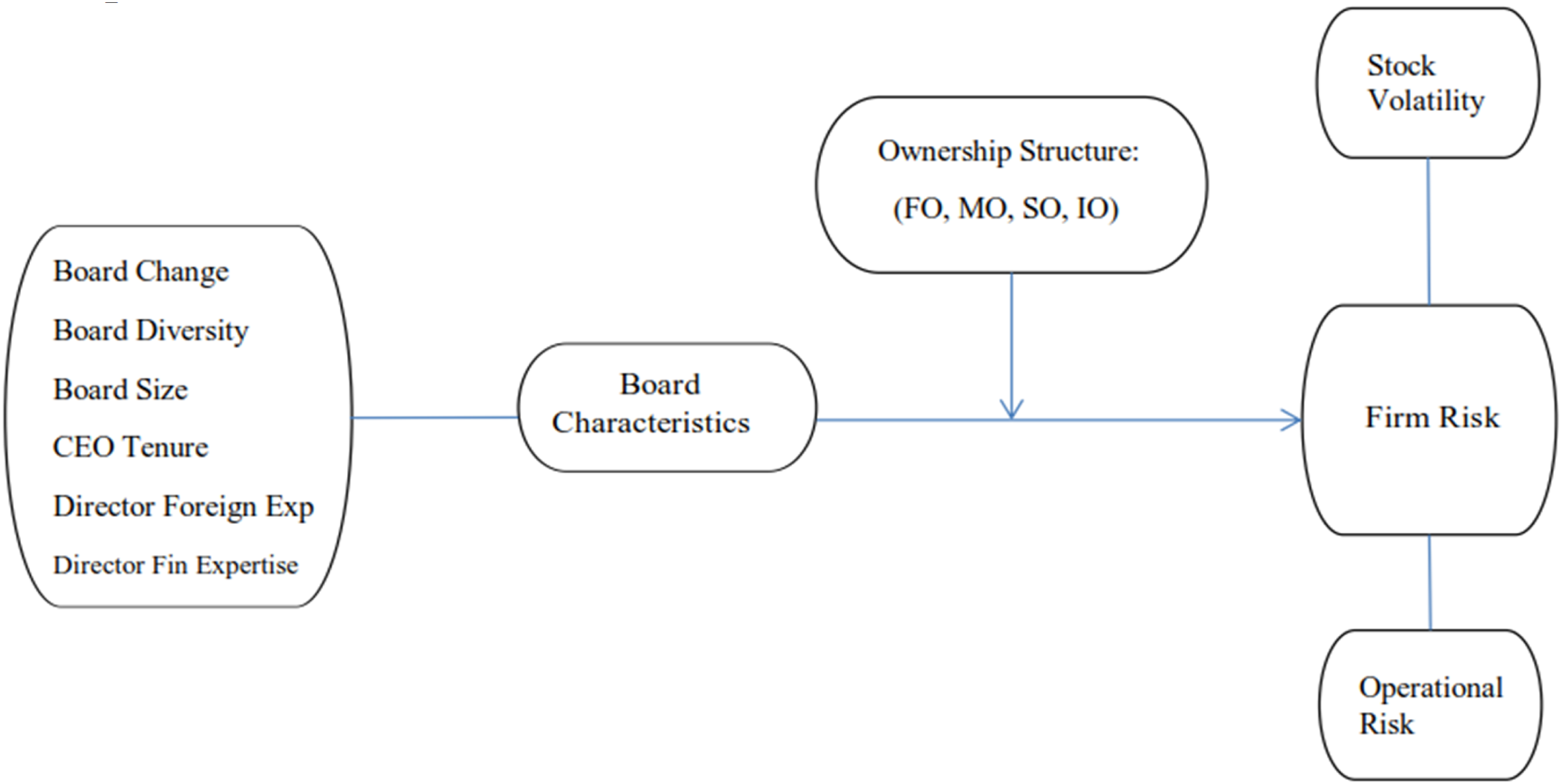

Analyzed the impact of service quality on customer satisfaction in the Chinese airline industry during COVID-19. The research concluded that improved service quality dimensions positively enhanced customer satisfaction and customer relationship management during the pandemic (Figure 1).

40

Conceptual framework.

Hypothesis

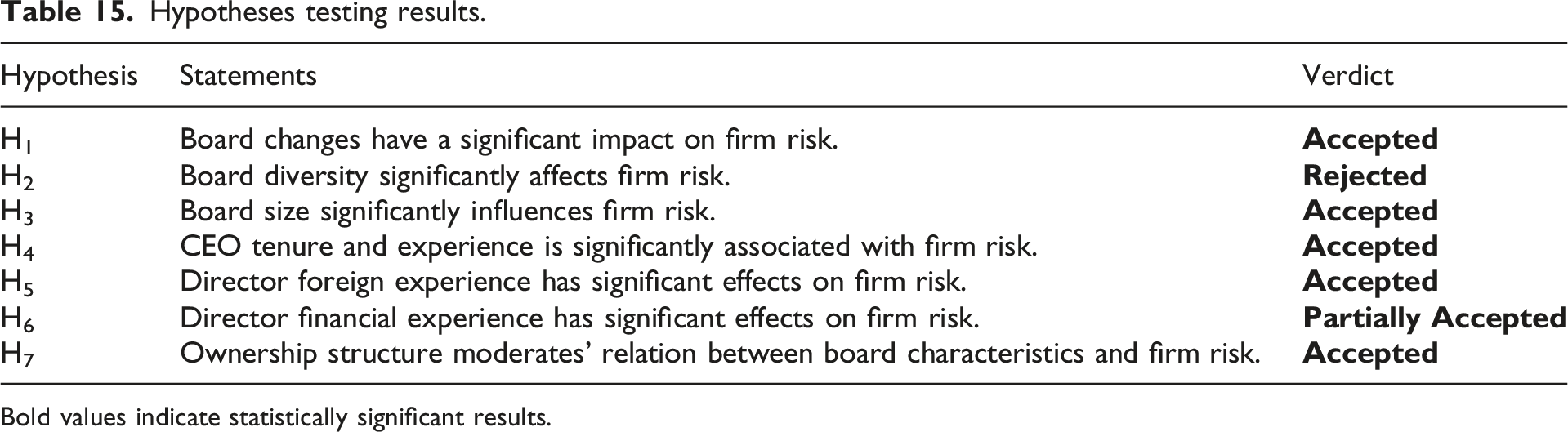

H1: Board changes have a significant impact on firm risk, as measured by Firmrisk 1 and Firmrisk 2. H2: Board diversity significantly affects firm risk H3: Board size significantly influences firm risk. H4: CEO tenure and experience is significantly associated with firm risk. H5: Director foreign experience has significant effects on firm risk. H6: Director financial experience has significant effects on firm risk. H7: Ownership structure moderates’ relation between board characteristics and firm risk.

Research methodology

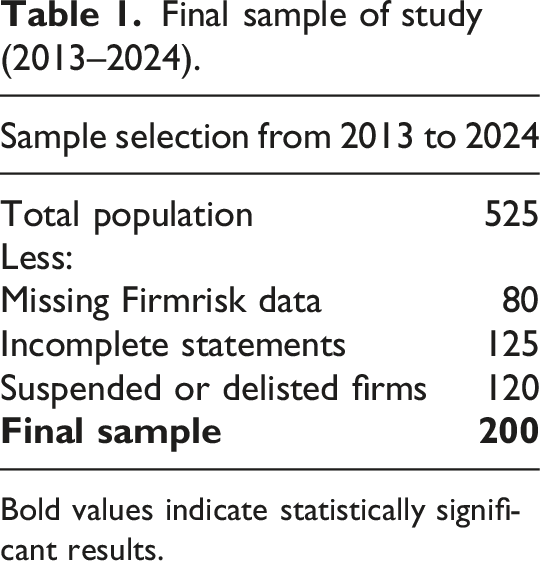

Final sample of study (2013–2024).

Bold values indicate statistically significant results.

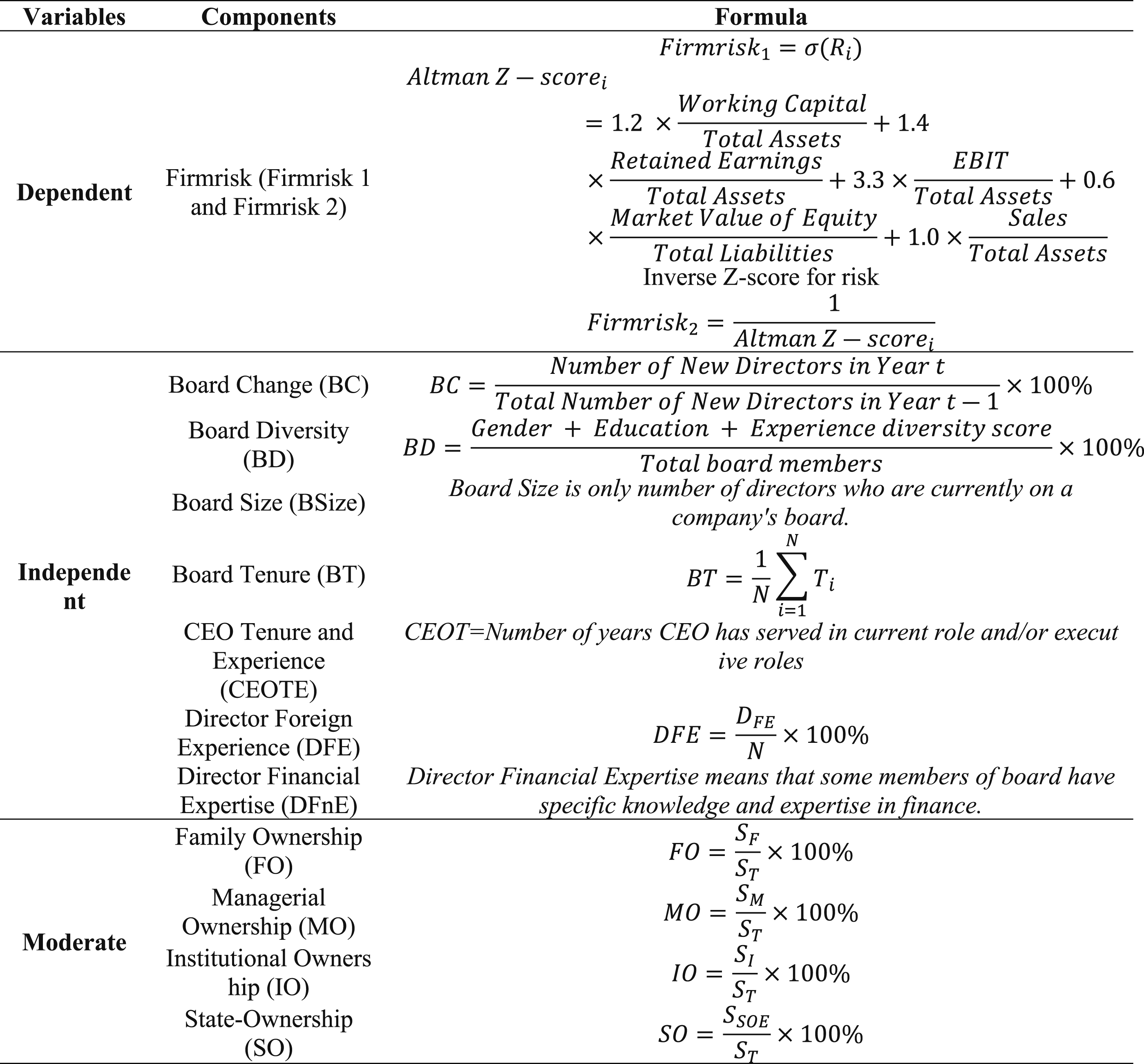

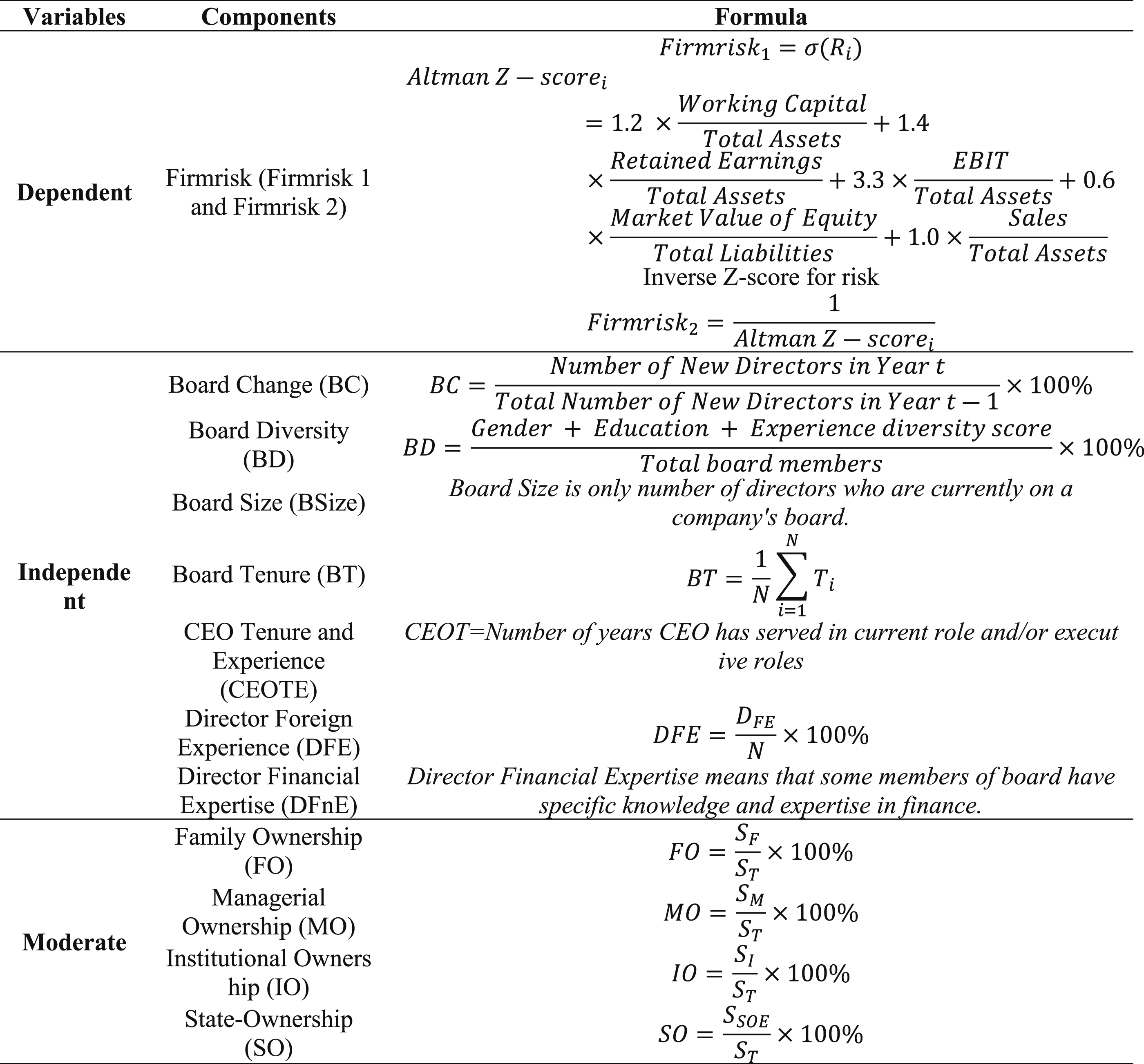

The sample size was presumably chosen to balance time, money, and ability to draw conclusions about more businesses. Pakistan Stock Exchange-listed companies from 2013 to 2024 are featured. 12-year period may have been chosen since 2013–2024 data is easy to collect, dependable, and consistent. Firm risk is measured using two proxies: (1) FR1 = Standard deviation of firm returns (σ(Ri)) (2) FR2 = Inverse Altman Z-score

Higher FR2 indicates higher bankruptcy risk due to inverse transformation of Z-score.

Variables description

Econometrics model

To address dynamic persistence in firm risk, a lagged dependent variable model is also estimated:

This allows capturing adjustment effects in firm risk over time. The regression model incorporates moderate to isolate effect of board change on firm risk. Equation can be specified as follows:

Equation (1) becomes:

This study employs a panel data econometric framework. The estimation is conducted using: • Pooled Ordinary Least Squares (Pooled OLS) • Fixed Effects Model (FEM) • Random Effects Model (REM)

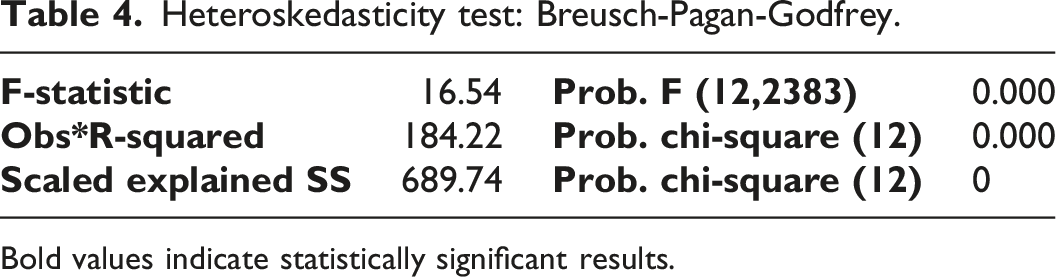

Hausman specification test is used to determine the appropriate model. Robust standard errors are applied to control heteroskedasticity.

Results and discussion

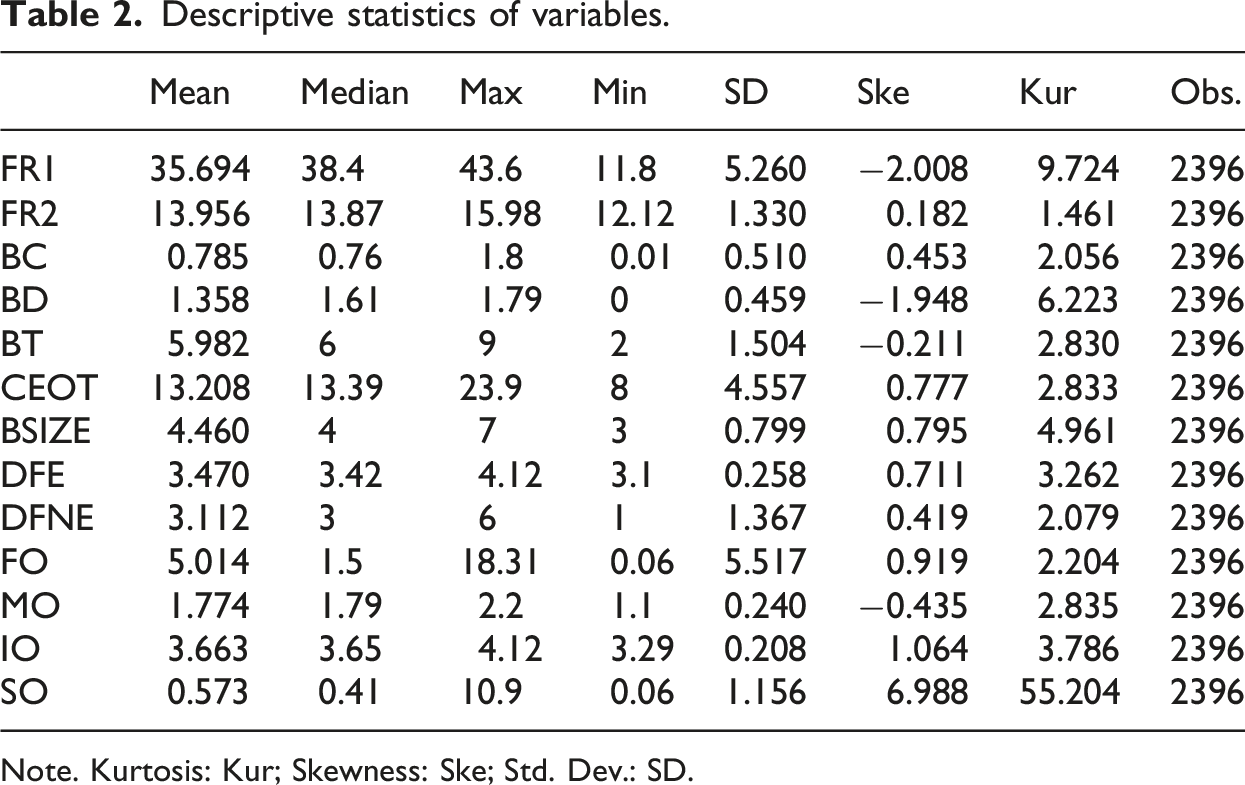

Descriptive statistics of variables.

Note. Kurtosis: Kur; Skewness: Ske; Std. Dev.: SD.

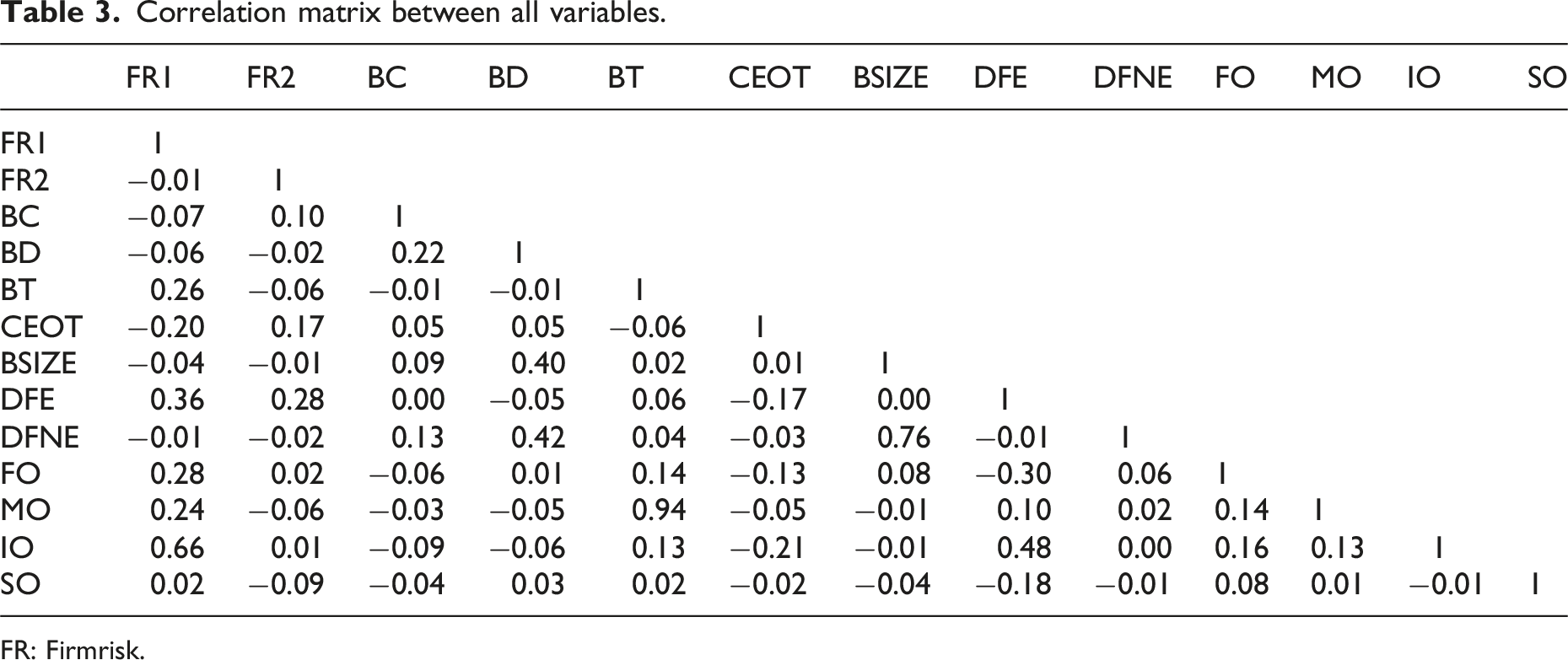

Correlation matrix between all variables.

FR: Firmrisk.

Heteroskedasticity test: Breusch-Pagan-Godfrey.

Bold values indicate statistically significant results.

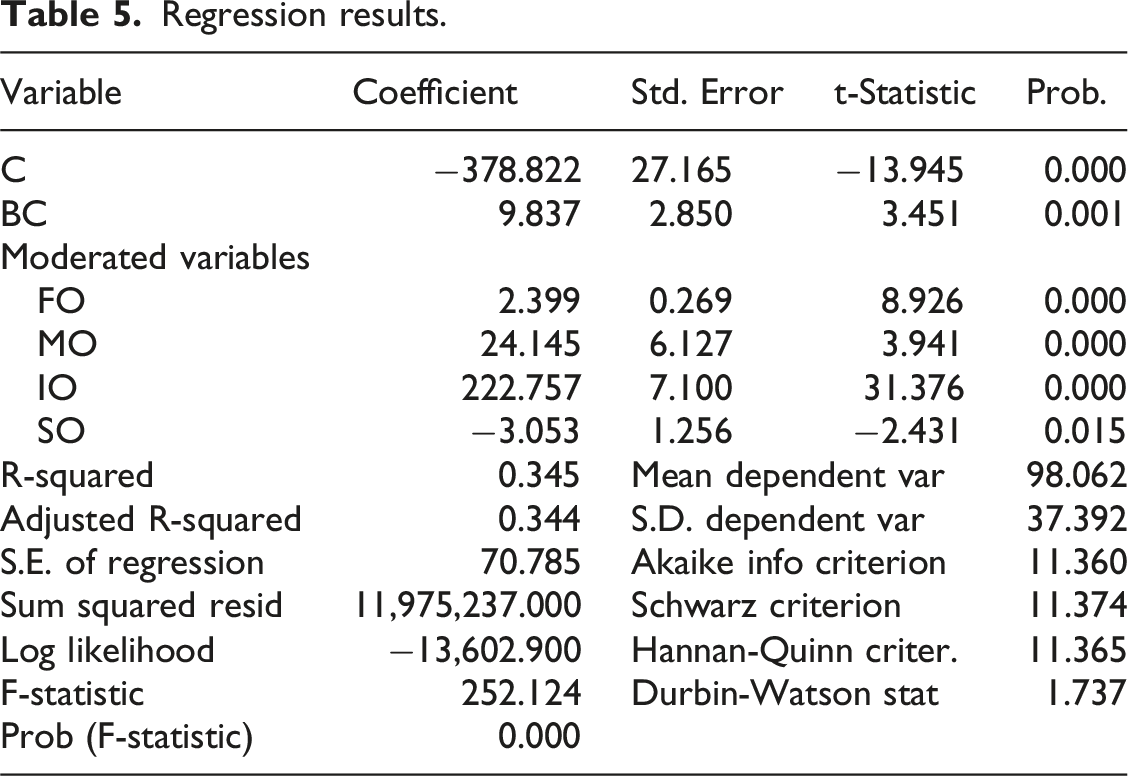

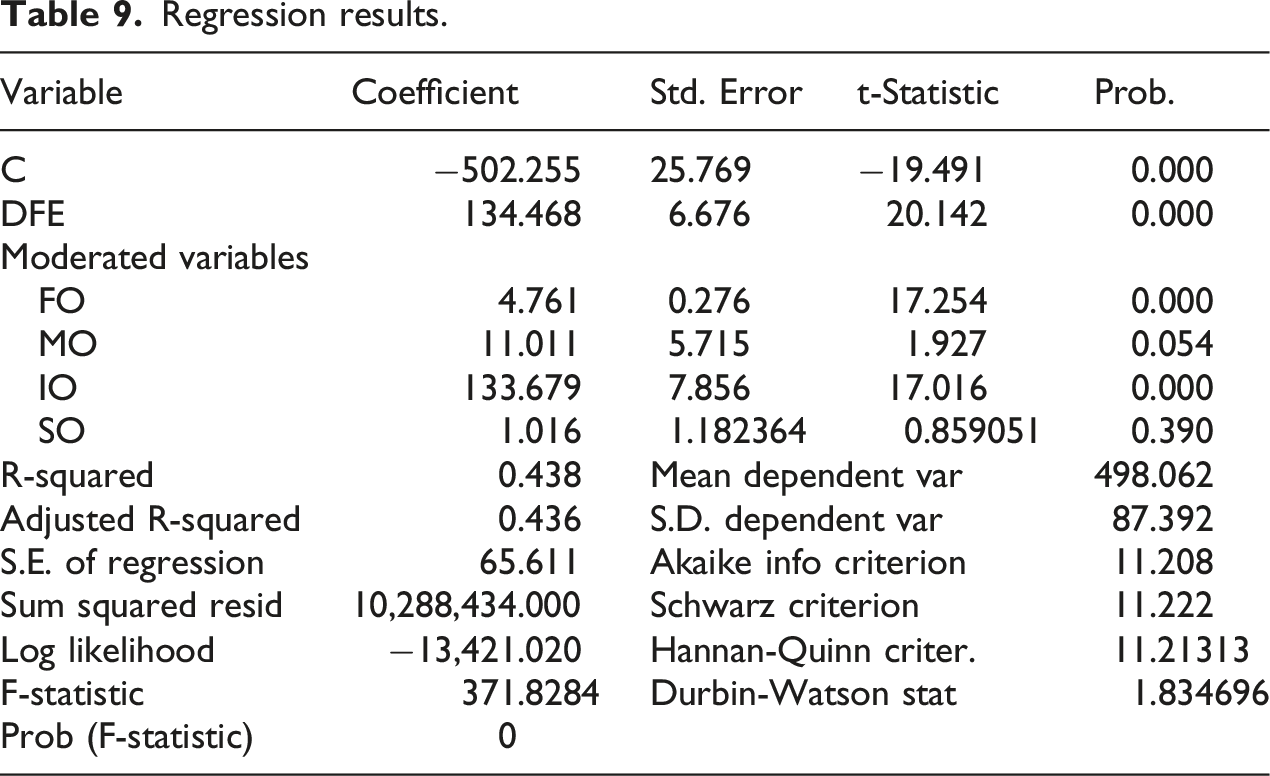

Regression results.

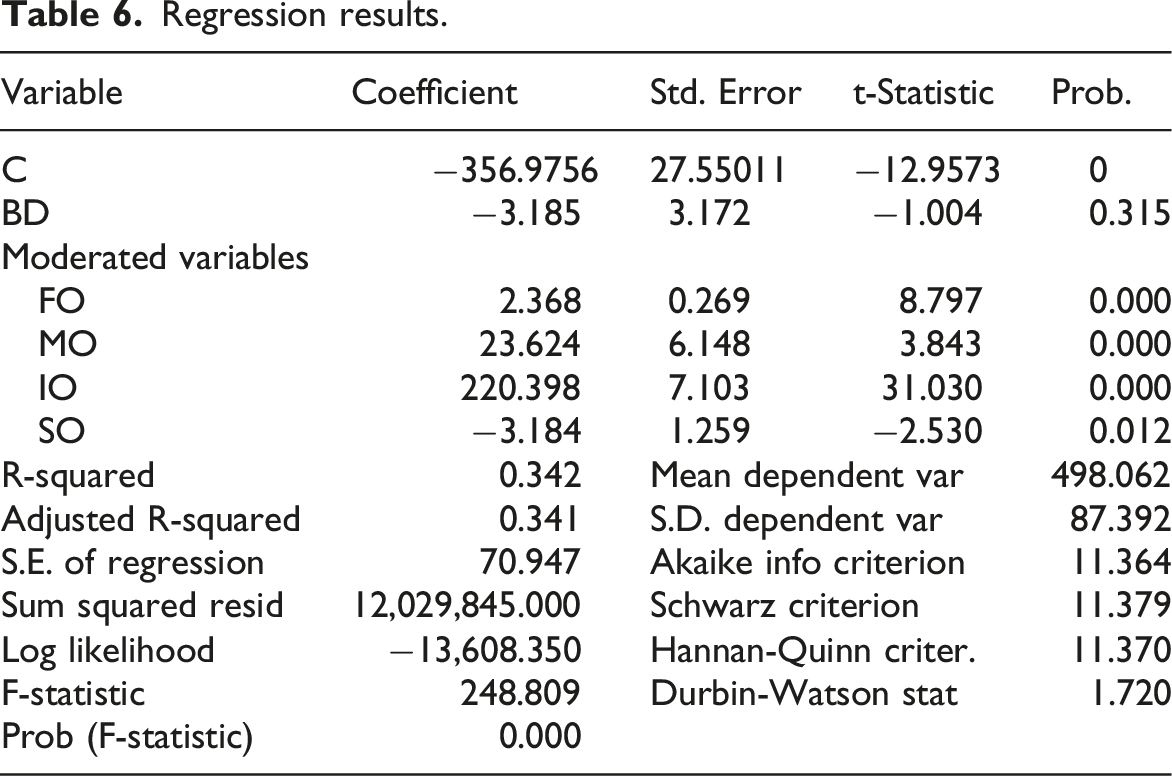

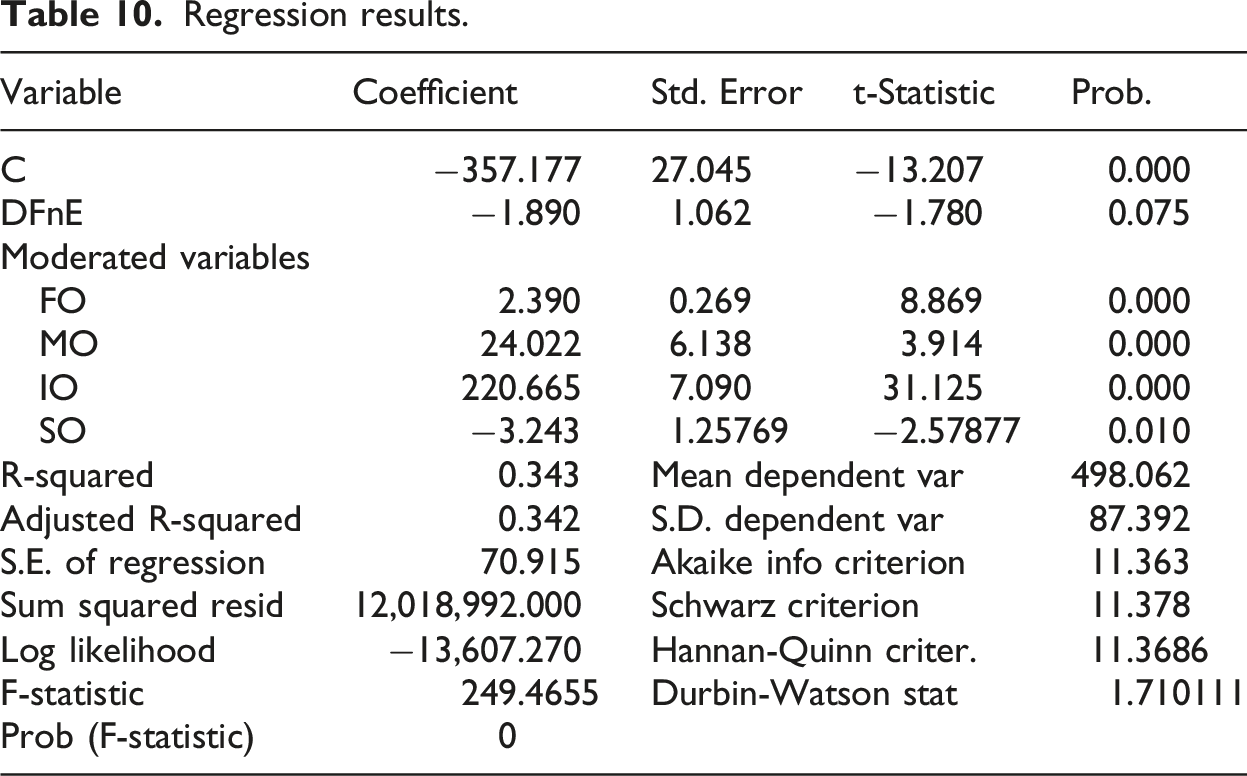

Regression results.

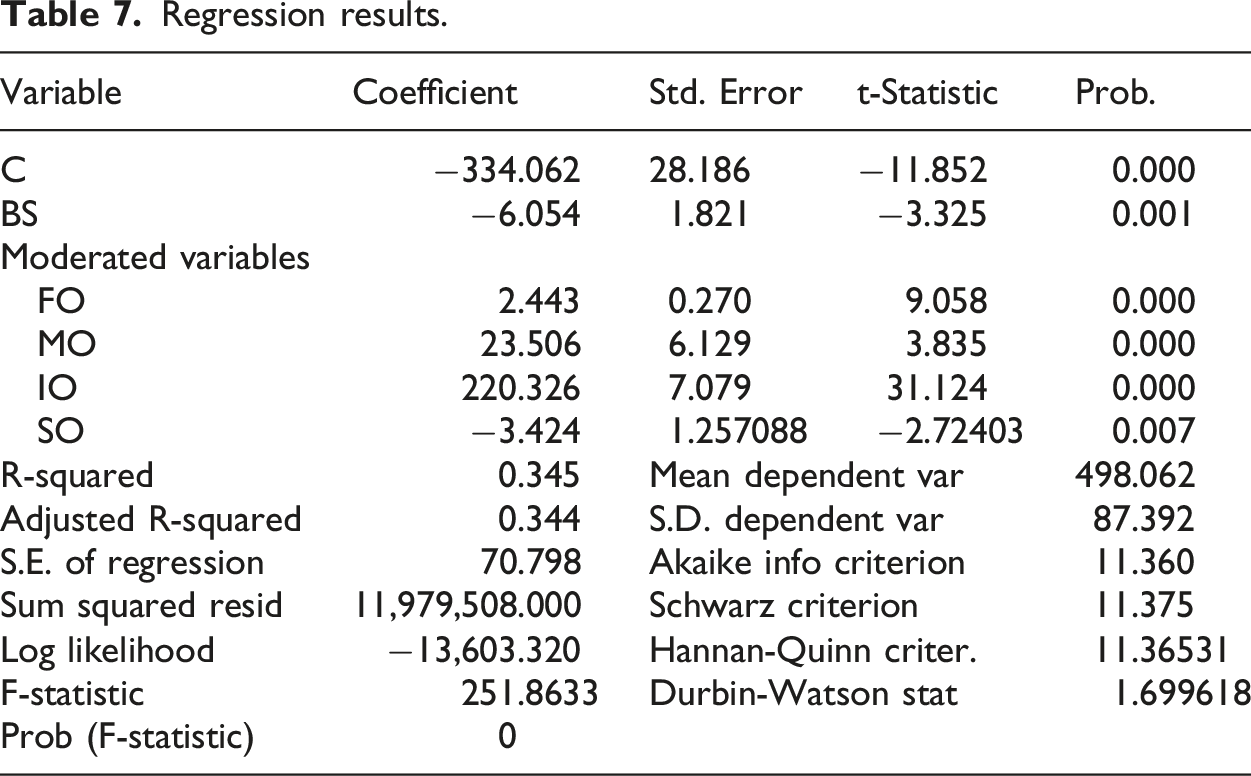

Regression results.

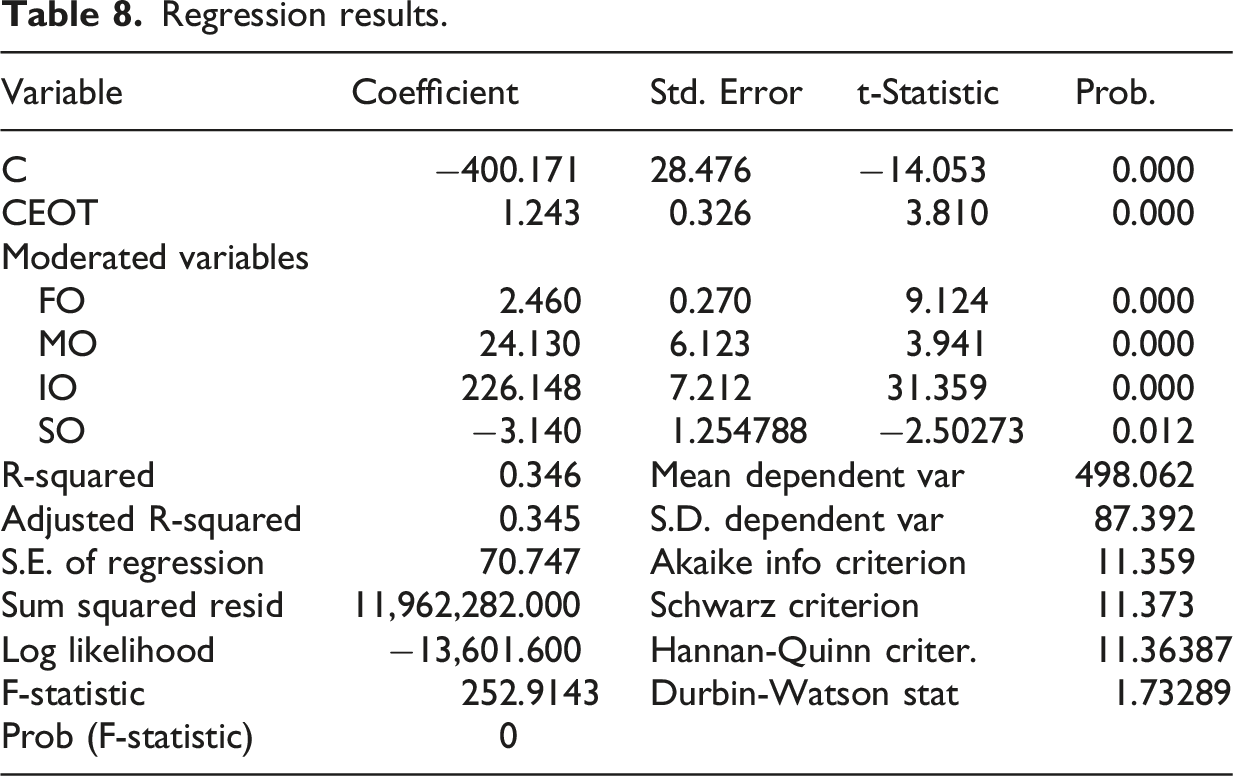

Regression results.

Regression results.

Regression results.

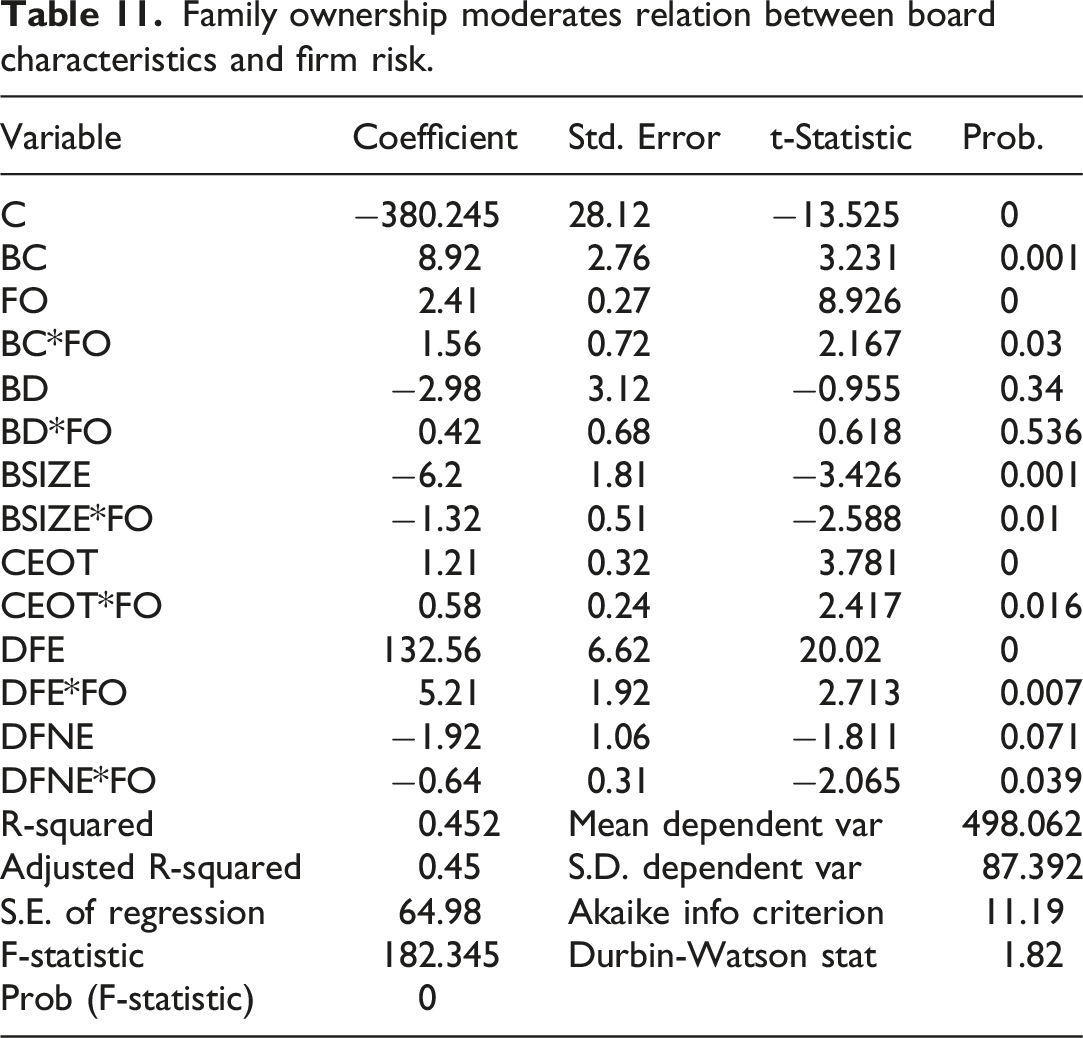

Family ownership moderates relation between board characteristics and firm risk.

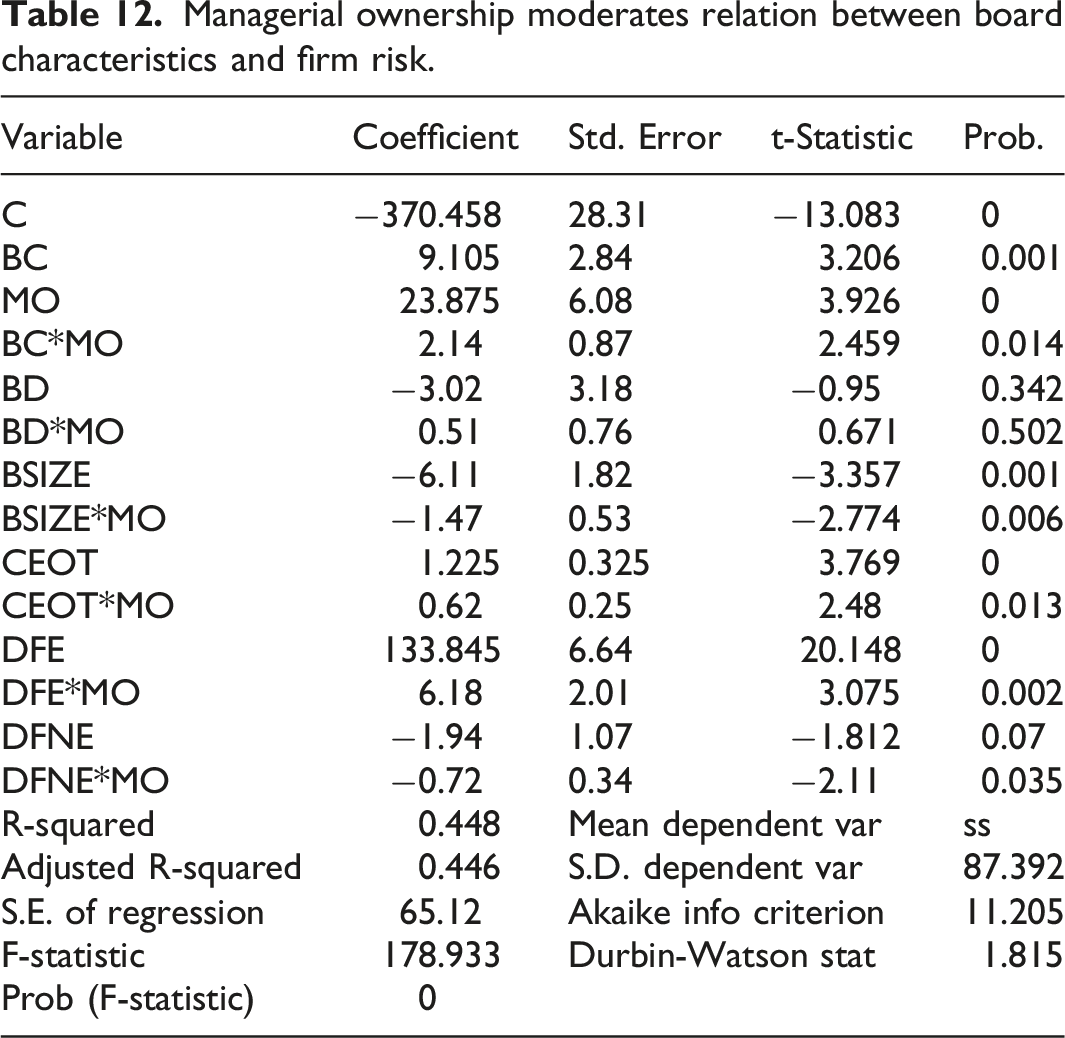

Managerial ownership moderates relation between board characteristics and firm risk.

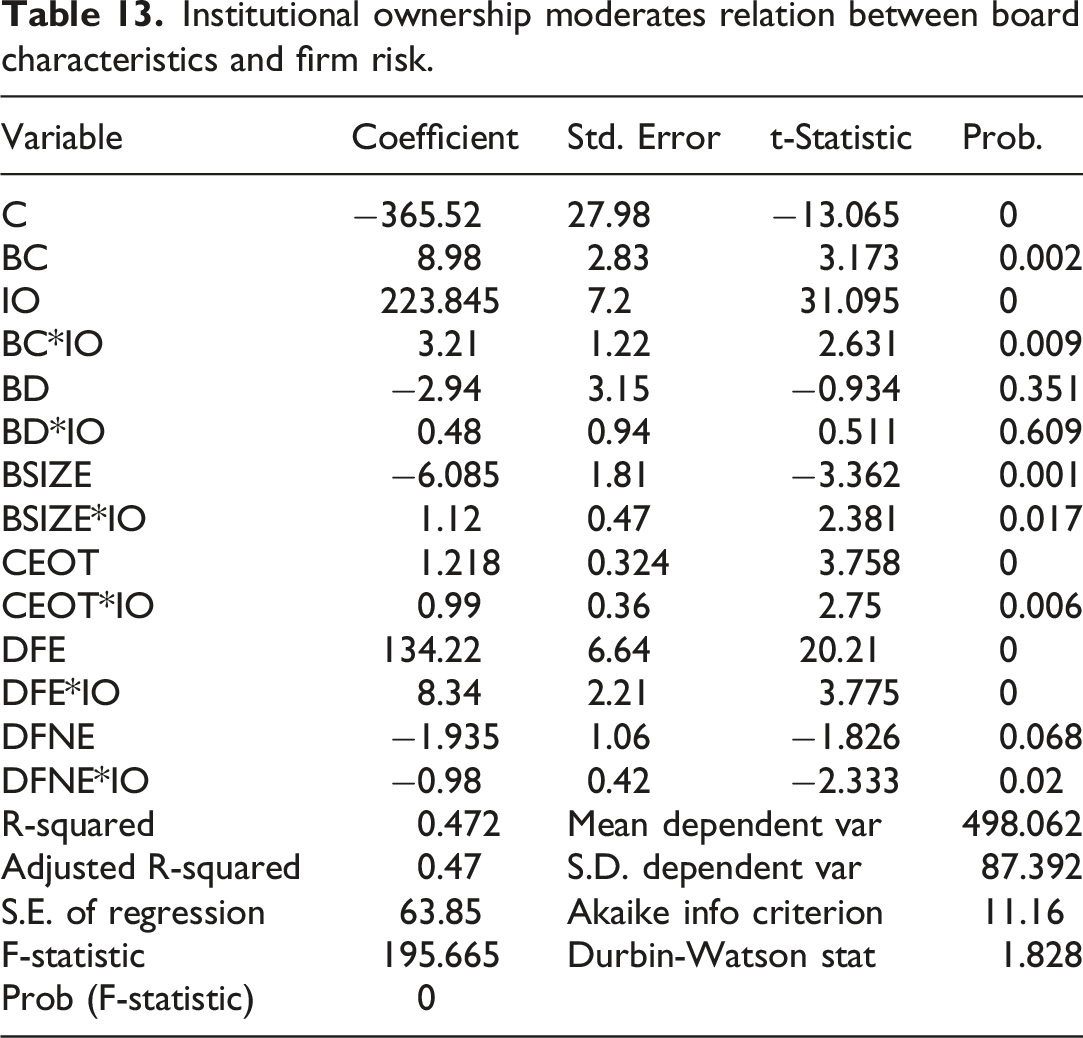

Institutional ownership moderates relation between board characteristics and firm risk.

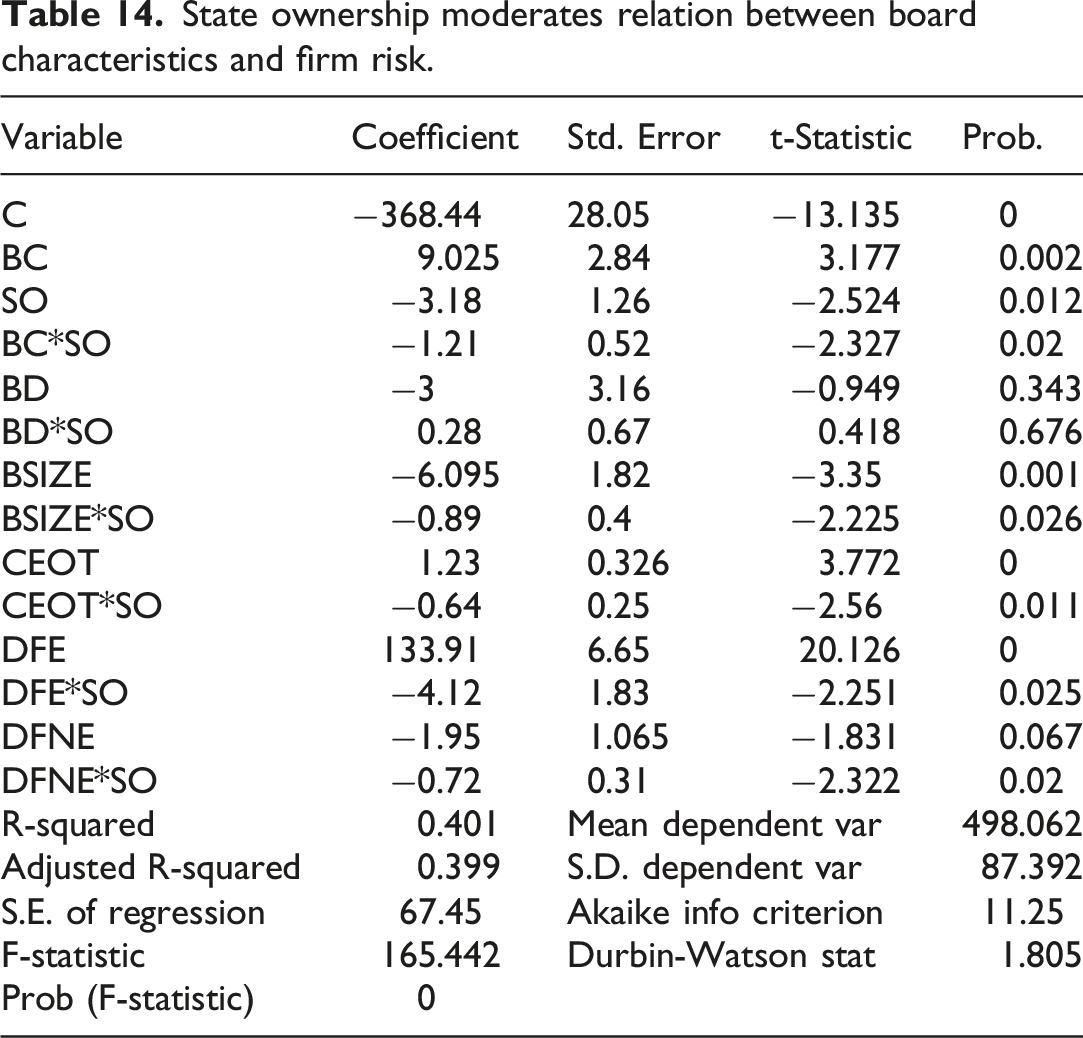

State ownership moderates relation between board characteristics and firm risk.

Hypotheses testing results.

Bold values indicate statistically significant results.

Conclusion and recommendation

The insignificant relationship between board diversity and firm risk suggests that diversity alone does not automatically translate into effective risk governance in emerging economies. In Pakistan’s institutional environment, symbolic diversity may exist without functional influence on decision-making. Additionally, concentrated ownership structures may override board-level heterogeneity, limiting the practical impact of diverse boards.

The study examined how board qualities and ownership arrangements affect corporate risk, with family, management, institutional, and state ownership moderating. Results support most current research suggesting board dynamics and ownership arrangements affect business risk. A bigger board can reduce risk, but board and CEO competence changes usually increase risk. Director with foreign experience increases firm risk and shows global strategy emphasis. However, financial expertise is less significant.

Moderated by ownership, governance results are contextual, highlighting corporate governance–risk complexity. BC positively and significantly affects firm risk in all models, supporting the assumption that leadership changes increase risk. BD Showed a negative but small influence, suggesting that diversity alone may not generate hazardous outcomes in the organizations examined. Size has a negative and significant influence; therefore, larger boards reduce firm risk by enhancing monitoring and control. CEOT exhibited a positive effect, suggesting that experienced CEOs are more risk-taking. DFE Positive and significant, showing that exposure to other countries increases risk-taking. DFNE has a small negative influence on business risk. FO, MO, IO, and SO greatly affected board characteristics and company risk.

Researchers might examine longitudinal data from different organizations and nations to discover if this study’s findings apply across institutions. Interviews and case studies can show how boardroom decisions affect risk. Study will benefit from independent directors, women on boards, and board committee structure. Private equity, foreign direct investments, and cross-holdings might complicate board-risk dynamics.

Policy implications

• Regulators should strengthen board appointment frameworks to ensure functional independence. • Ownership transparency should be improved to reduce excessive control effects. • Institutional investors should be encouraged to adopt active monitoring roles. • State ownership requires governance reforms to balance control and efficiency.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.