Abstract

Poverty, inequality, unemployment, and unsustainable resource consumption are prevalent in Africa due to a lack of inclusive growth. The impacts of climate change are also considered to have hindered progress on achieving the Millennium Development Goals. Through literature reviews and policy analyses, this article presents suggestions on how inclusive growth can be attained in the post-2015 development agenda, and also presents a framework to enable microfinance institutions to promote both inclusive growth, and climate change mitigation and adaptation. The article shows that microfinance can support the mobilization of resources for climate change programs; hence, financial inclusion should be incorporated in climate change policies.

Keywords

Introduction

In the context of Africa, sustainable development could entail development that meets the people’s essential needs and aspirations for jobs, food, energy, water, and sanitation; ensures a sustainable level of population; conserves and enhances the continent’s resource bases; re-orientates technology and manages risks; and includes and combines environmental and economic consideration in decision-making (Perdan, 2011, pp. 5–6). Arguably, sustainable development can only be achieved when African countries attain inclusive growth. However, as it stands, in sub-Saharan Africa (SSA), the average income per capita in real terms is currently lower than it was at the end of the 1960s, and life expectancy is lower now than it was 30 years ago as incomes, assets, and access to essential services are unequally distributed (World Bank, 2013a).

Many countries in Africa are registering high levels of economic growth (average real Gross Domestic Product (GDP) growth per annum; Figure 1) and this has transformed Africa to become the world’s second fastest developing region. However, the pace of poverty reduction has been too slow to reach the poverty reduction target as stipulated in the Millennium Development Goals (MDGs) by 2015 because of high inequality, high population growth, recurring food price hikes, prevalent conflicts, weak governance, and climate change (UNECA, 2013). Consequently, the region is characterized by jobless growth, rising levels of inequality, low productivity, and poor working conditions for a majority of the African population (FAO, 2015; UNECA, 2012). In the light of these revelations, development practitioners and policymakers now seem to have recognized that development approaches, strategies, visions, models, and tools that were being implemented in some African countries have been successful in fostering economic growth but not inclusive growth.

In SSA, the inequalities which perpetuate poverty exist in the form of rural–urban differences in terms of average incomes and access to social services including education and health. Sadly, in some countries, the level of inequality has actually increased compared to the early 1990s (GoU, 2010; World Bank, 2013b). In addition to this, climate change is anticipated to increase disaster risks in the continent and hence can seriously hamper Africa’s future development and pose as an additional impediment to the achievement of the MDGs (Boko et al., 2007). Climate change may be considered as one of the most serious threats to sustainable development globally since studies have shown that about 90 percent of all natural disasters afflicting the world are related to severe weather and extreme climate change events. Additionally, rural households can take up to 10 years to recover from the effects of weather and climate shocks (FAO, 2015). Climate change and noninclusive growth are, therefore, significant impediments to Africa’s development aspirations. The interplay between these issues therefore requires further analysis in order to provide a better understanding to policymakers on how they can design and implement policies and solutions that can holistically address these issues.

The objective of this article is to encourage debates and discussions on how microfinance can simultaneously enhance inclusive growth and climate change resilience in Africa. The article proposes a framework that utilizes microfinance institutions as intermediaries to mobilize/leverage financial and nonfinancial resources from various sources and subsequently disburse the resources to various beneficiaries. Microfinance is a development tool and strategy that is considered to have positive impacts on poverty, income, savings, expenditure, and the accumulation of assets, as well as nonfinancial outcomes including health, nutrition, food security, education, women’s empowerment, housing, job creation, and social cohesion (Van Rooyen, Stewart, & De Wet, 2012). This makes microfinance an ideal tool and strategy that can address some of the challenges to inclusive growth in Africa.

Some research that has explored the role of microfinance in addressing climate change issues with relevance to factors that can influence inclusive growth include DMFA (2009), whose study tried to identify possible synergies between the Clean Development Mechanism (CDM) and microfinance mechanisms; Rippey (2009), who analyzed the threats and opportunities for microfinance and climate change; and Becchetti and Castriota (2011), who analyzed the impact of microfinance by focusing on its effectiveness as a recovery tool after a natural disaster. Agrawala and Carraro (2010) explored the linkage between the top-down macro-financing for adaptation through international financial mechanisms and the bottom-up activities that can be implemented through microfinance. Morris et al. (2007) analyzed the use of microfinance to promote the diffusion of renewable energy technologies, and Hammill, Matthew, and McCarter (2008) explored the use of microfinance for adaptation. Hogarth (2012) looked at how FINCA (a microfinance institution in Uganda) could promote climate change mitigation by enhancing the deployment of solar lanterns/alternative technologies, and Nfah and Ngundam (2012) examined the role of various stakeholders including microfinance institutions in promoting access to renewable energy and supporting renewable energy enterprises. This article intends to contribute new perspectives to the existing body of literature on climate change management and microfinance. First, the article explores the avenues and opportunities which global and national policymakers can focus on in order to create a conducive environment to enable microfinance institutions to promote inclusive growth and enhance climate change resilience in Africa. Second, the article suggests a framework that can enhance microfinance resource mobilization, operations, and delivery channels in order to improve the sustainability, impact, and outreach of microfinance institutions.

The article is structured as follows. The next section provides an overview of strategies that will be implemented in the post-2015 development agenda in order to facilitate sustainable development. This is then followed, in the third section, by an analysis of the challenges related to food security in Africa and the influence to which microfinance may have to reduce food insecurity. The fourth section presents an argument on how empowering the youth and women in communities is essential to reduce social conflicts, and how empowering the youth and women can be achieved by increasing funding levels to entrepreneurs. A microfinance-inclusive growth framework focusing on creating jobs and harnessing Africa’s entrepreneurial talent is presented in the fifth section. A discussion in the sixth section highlights how the climate change financing arena is not only plagued by having insufficient resources for its activities but also how there are challenges to create effective delivery mechanisms that can channel climate change funds at the local level to reach communities that are the most vulnerable to the impacts of climate change. The roles to which microfinance could have in addressing both these shortfalls and the means to which these could be achieved are also elaborated in this section. Lastly, a conclusion, in the seventh section, is given which shows that various microfinance programs are already addressing climate change resilience issues, be it in fragmented ways, and hence, these activities can be scaled-up based on the microfinance-inclusive growth framework presented in this article.

Post-2015 Development Paradigms

Current literature and discussions on the post-2015 development agenda and framework suggest that different development strategies have to be deployed in different countries in order to reduce poverty in its many dimensions because various countries have divergent national circumstances and priorities (African Union, 2014; UNSD, 2015). This follows that the MDGs have been credited for mobilizing aid funds and directing aid toward particular sectors such as primary education, but have been criticized for the lack of participation involved in their formulation, lack of specific commitments for rich countries, and for neglecting key areas of importance for development such as improving energy access (Clemens, Kenny, & Moss, 2007; Melamed, 2012).

Following in from the successes and shortfalls of the MDG framework, the sustainable development goals (SDGs) (the 17 development goals and 169 associated targets) emphasize that global efforts to promote sustainable development should strive to end poverty while taking account of different national realities, capacities and levels of development, and respect to national policies and priorities (UNSD, 2015). The SDG framework therefore suggests that global and national development approaches, strategies, visions, models, and tools should:

ensure that all men and women have equal rights to economic resources, as well as access to basic services, ownership, and control over land and other forms of property, inheritance, natural resources, appropriate new technology, and financial services, including microfinance; and promote development-oriented policies that support productive activities, entrepreneurship, creativity, and innovation, and encourage the formalization and growth of micro-, small-, and medium-sized enterprises, including through access to financial services (UNSD, 2015). Since the accumulation of assets reduces poverty and the vulnerability of communities to climate change (Hallegatte et al., 2014), it can be argued within a context in which (a) and (b) are attained, and access to financial services for various uses is promoted, the vulnerability of communities to the impacts of climate change will be reduced and inclusive growth will be attained.

Promoting Food Security Through Microfinance

Food security in Africa can only be attained if communities at all times have both physical and economic access to sufficient food to meet their dietary needs for a productive and healthy life (FAO, 1996; USAID, 1992). Figure 2 suggests that attaining food security is not only a question of ensuring that farmers have access to land and farm inputs to grow certain crops, but that adequate provisions are put in place to ensure that various rural and urban communities simultaneously attain the three interrelated elements of food security throughout the whole year. The three interrelated elements of food security are to ensure (a) food availability (sufficient quantities available for consumption), (b) food access (adequate resources to obtain appropriate foods for a nutritious diet), and (c) food utilization (proper biological use of food, a diet providing sufficient energy and essential nutrients, potable water and adequate sanitation, as well as knowledge of food preparation, basic principles of nutrition, proper child care, and illness management) (USAID, 1992).

60 percent of the people in SSA are involved in agriculture thereby making the agriculture sector the largest economic activity in Africa, contributing more than 50 percent to GDP in most African countries (UNEP, 2014). Regardless of this, many African countries are still considered food insecure (UNECA, 2013). Moreover, increased climate variability and more frequent extreme events such as droughts and floods could significantly increase the risk of agricultural production failures and hence perpetuate food insecurity and disrupt rural livelihoods. Some research already points out that in comparison to developed countries, low-income countries such as those in Africa are the most vulnerable to current climate variability and future climate change (World Bank, 2013c) because of factors such as the higher exposure of low-income countries to climate risk due to a heavy reliance on agriculture for their livelihoods, Africa’s semi-arid climate or the concentration of populations in hazard zones, and Africa’s adaptation deficit as caused by a lack of institutional, financial, or technological capacity to adapt effectively to climate change (Bowen, Cochrane, & Fankhauser, 2012; Schumacher & Strobl, 2011). Some studies on cross-country factors influencing climate change adaptation highlight that factors such as wealth and access to extension services, credit, and climate information in Ethiopia; wealth, government farm support, access to fertile land, and access to credit in South Africa; and access to agricultural inputs and credit in Malawi influence farmers’ abilities to adapt to climate change (Bryan et al., 2009; Coulibaly et al., 2015). This suggests that there are no one-size-fits-all strategies for promoting adaptation of the agriculture sector across different countries and communities. Arguably, creating an enabling environment for adaptation should be tailored to meet the particular needs and constraints of different countries and groups of farmers possibly by increasing access to information, credit, and markets, and making a particular effort to reach small-scale subsistence farmers, with limited resources to confront climate change (Bryan et al., 2009). Following in from this, Fankhauser and McDermott (2014) point out that inclusive (and low-carbon) growth policies should be promoted as they can increase per capita income which leads to reduction in the impacts of extreme weather events and also increases the demand for substitutes to adaptation such as insurance cover. This can then ensure that Africa’s adaptation deficits can be reduced over time. Microfinance programs aimed at supporting inclusive growth by aiming at increasing the income levels of people and communities to enable them to improve their agricultural output and develop other off-farm income generating activities, which could therefore enhance food security and climate change resilience in Africa.

Some strategies that can boost agricultural production and increase the resilience of rural farmers to climate change include promoting new technologies, planting drought resistant crop varieties, practicing crop diversification, adopting improved farming systems, using different crop varieties, planting trees, promoting soil conservation, changing planting dates, and practicing irrigation. Microfinance institutions have been shown to promote climate resilient agricultural strategies such as conservation agriculture, drip irrigation, and organic farming (Frankfurt School, 2014) by providing credit and capacity building activities to communities. This has made microfinance to be an ideal mechanism to assist with addressing some financing and technical challenges that some rural farmers experience when trying to enhance their agricultural productivity and reduce their risks emanating from climate events in production activities.

The Case for Empowering the Youth and Women in Communities

Unemployment and particularly youth unemployment is a significant challenge that can affect the social and economic development of Africa (Momo, 2011; UNECA, 2012; UNECA, 2013). Unemployment among the unskilled population has been noted as a key source of crime, political violence, and social backwardness, hence creating more jobs for unskilled populations could be a plausible solution to minimize social unrest (Timilsina et al., 2010). Alternatively, unemployment can also be addressed through the implementation of well-targeted social policies tailored to the socio-political economy of various countries, and the development of financial mechanisms tailored to the needs and socio-political economy of various communities.

In addition to the aforementioned considerations, without the empowerment of women and the youth through jobs and economic opportunities, and the empowerment of women and the youth for decision-making within communities, inclusive growth might not be achieved. Women and the youth arguably need to be provided with the means and services that can stimulate the growth of their income and consumption so that they are empowered (i.e., have control over resources, participate in household and community decision-making and so on) and this might also lead to the reduction of vulnerability to and alleviation of poverty for women and the youth (Weber & Ahmad, 2014).

Some factors that hinder foreign direct investment (FDI) flows to Africa and indirectly impede the creation of jobs include political risk, low-skilled labor force, and a poor investment climate (Chirambo, 2014; Winkelman & Moore, 2011). Arguably, FDI inflows to the continent can be promoted by establishing effective governance structures, enhancing education and skills development, and improving infrastructure in the continent (Chirambo, 2014; WEF, 2015; Winkelman & Moore, 2011). Improved FDI flows to the continent could subsequently improve the prospects for creating inclusive jobs and developing various sectors such as energy, mining, construction, agriculture, and manufacturing.

Some commentators point out that SSA is the region with by far the highest number of people involved in early-stage entrepreneurial activity (TEA), and Africa also leads the world in the number of women starting businesses, with almost equal levels of male and female entrepreneurs (Amorós & Bosma, 2014). Africa therefore possesses a significant number of entrepreneurs capable of starting small enterprises that have the potential to grow and provide employment to the continent’s population providing that market research and access to funding is improved (ibid.). The microfinance industry is noted to be transforming. The industry is now increasing its focus on financial sustainability and efficiency leading to a shift from donor-funded business models to commercially sustainable business models (i.e., second generation microfinance institutions are aiming for financial sustainability to avoid reliance on donor funding) thereby leading to increased competition among microfinance institutions and also the commercialization of microfinance (i.e., the interest of commercial banks and investors to finance microfinance institutions) (Rhyne & Otero, 2006; Weber & Ahmad, 2014). This does not only mean that microfinance institutions are increasing their outreach and impact but it also suggests that microfinance programs can be developed and implemented in countries and areas that might not be commercially attractive for highly risk averse foreign direct investors. Arguably, with the greater outreach of microfinance, microfinance institutions can be promoting new industries and investments in areas that were previously underfinanced or ignored. Microfinance institutions can therefore potentially fill in the financing gap that is caused by a lack of FDI to Africa. Moreover, microfinance institutions do not always only provide credit facilities to entrepreneurs and businesses, but they can also incorporate savings, insurance, money transfer services, and educational and health loans, and complementary services such as skills education and training, health and nutrition workshops, and advice on agricultural practices (Agrawala & Carraro, 2010). All these services can consequently greatly assist in capacity building and supporting the growth of African enterprises and incubating (youthful and female) entrepreneurs.

A distinctive feature of SSA is that it has a larger number of its population involved in the informal sectors in comparison to other regions. According to Dougherty-Choux (2014), in SSA micro and small business employ approximately 78 percent of the total population in comparison to 59 percent in South-Eastern Asia, 40 percent in the Middle East and Central Asia, 31 percent in Latin America and the Caribbean, 32 percent in North Africa, and 22 percent in Western Asia. In SSA, micro and small businesses account for 90 percent of all firms and make up about 25 percent of GDP (Soubeiga & Strauss, 2013). There are therefore suggestions that small businesses can play a greater role in enhancing climate change resilience as they are best suited to reach vulnerable communities in low-income countries since the majority of vulnerable populations rely on these businesses for their livelihoods and micro and small businesses are oftentimes the most direct contributors to a stable economy in low-income countries, providing a strong labor force, access to markets, and steady incomes (Dougherty-Choux, 2014). Microfinance is regarded as a means to empower developing countries by supporting base of pyramid (BOP) entrepreneurship and reducing (rural and urban) poverty, as in contrast to conventional development aid, microfinance involves and often even focuses on the informal sector (including those in slum areas) and may be an alternative to macro-economic solutions that are often used in development aid programs (Montgomery & Weiss, 2011; Mutisya & Yarime, 2014; Weber & Ahmad, 2014). To this effect, it may be concluded that the microfinance industries should be nurtured since microfinance is a development mechanisms that has been shown to have the means and outreach to actively encourage informal sectors to develop their capacities, which is in keeping with the socio-economic profiles of communities and businesses in Africa.

The Job Creation Revolving Loan Fund (JCRLF)

In some parts of Africa, knowledge and awareness of climate change issues is low (Lesolle, 2012), subsequently leading to various communities and stakeholders not to have the capacity to determine how best to address climate change issues or to be involved in climate change activities. Moreover, some suggestions point out that in less affluent areas, the quest for achieving economic growth precede the need to protect the environment (Marara et al., 2011) as such policies that seem to promote the creation of jobs and economic activity could be more likely to receive support from many stakeholders rather that those that could be considered to promote environmental conservation and constrain development. In a similar way, Ürge-Vorsatz and Herrero (2012) assert that climate change management alone might often not be a sufficient consideration or policy goal to be able to mobilize enough political will or adequate action for activities/programs related to protecting the environment and improving climate change resilience in some countries. The lack of climate change policies in many developing countries also means that the effective coordination, institutional harmonization, and implementation of climate change management is compromised and fragmented (CEPA, 2012). The Global Commission on the Economy and Climate however considers that countries at various stages of development can still achieve lasting economic growth and development concurrently whilst reducing the immense risks of climate change. This could be feasible if countries correct a range of market, government and policy failures, and new technologies, business models and financial innovations (including green bonds, risk-sharing instruments, co-investments, municipal finance, and crowd-funding) are implemented in order to facilitate the creation of jobs, investments, and growth (GCEC, 2014).

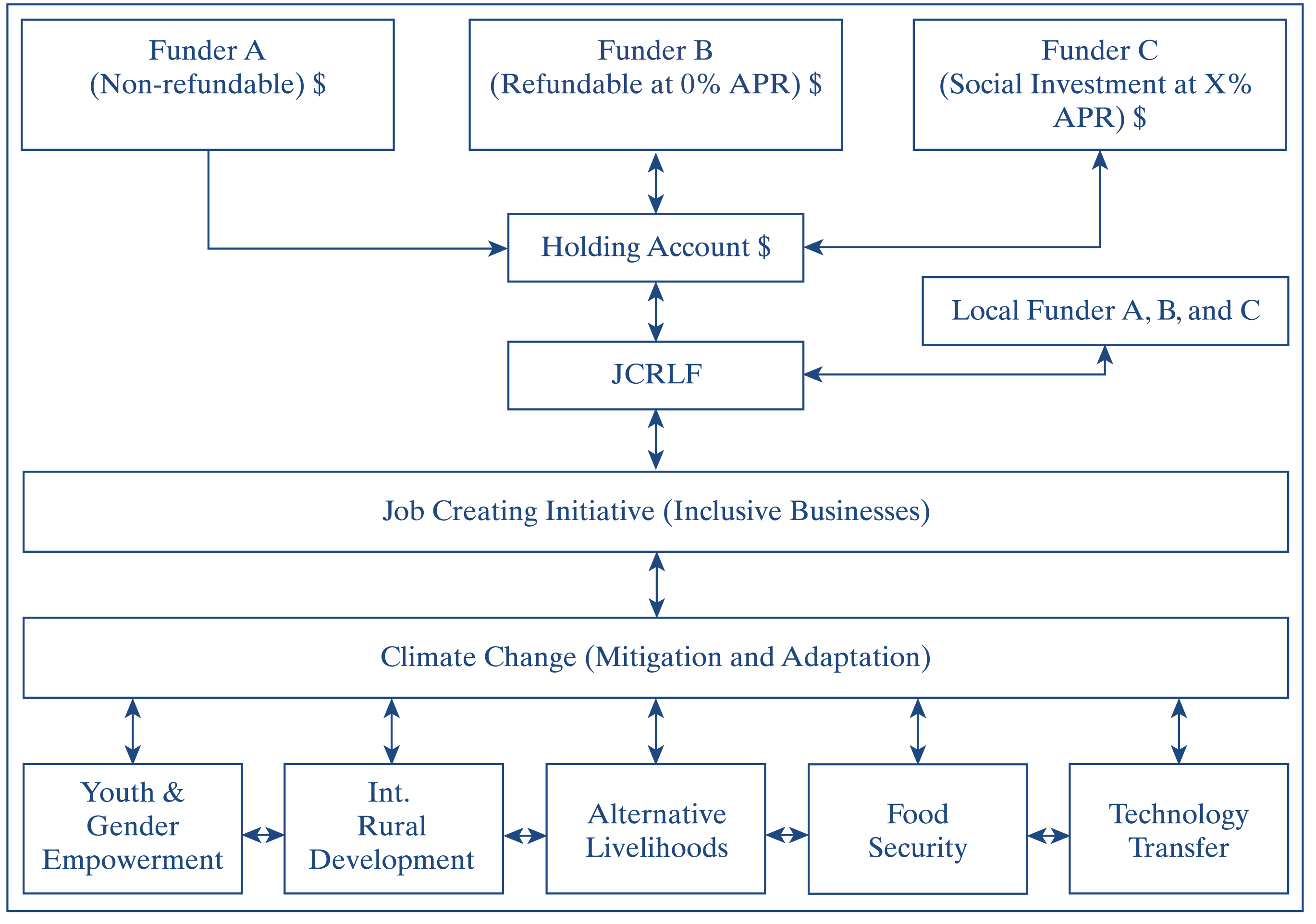

This section therefore illustrates a microfinance-inclusive growth framework that has a dual role of enabling microfinance institutions to be integrated into the climate finance domain by supporting activities related to improving the resilience of communities to the impacts of climate change, and promoting sustainable development by supporting the development of inclusive businesses which can create jobs and boost economic growth (Figure 3). The framework is based on the concept of a revolving credit fund. Revolving credit funds have been shown to be effective in easing credit constraints by reaching poorer communities, providing financial services to those households which rely on informal lending, and leveraging financial contributions from various sources (loan repayments from clients, loans from development agencies, and so on) (Menkhoff & Rungruxsirivorn, 2011; NREL, 2010). Revolving credit funds provide loans rather than grants thereby enabling microfinance institutions to become sustainable by recycling resources over and over again to deliver the ‘holy trinity’ of outreach, impact, and sustainability (Kotir & Obeng-Odoom, 2009); hence, this is in keeping with current microfinance practice which advocates for financial sustainability. As explained earlier on in this article, the creation of the right kind of jobs and opportunities and more importantly providing various financial services to the right type of households, enterprises and sectors could lead to inclusive growth and the empowerment of vulnerable groups. This may ultimately significantly improve Africa’s six development priority intervention areas of improving climate change resilience, enhancing food security, supporting youth and women empowerment, promoting technology transfers and diffusion, promoting alternative livelihoods, and facilitating integrated rural development. Revolving credit funds are therefore ideally suited to support these objectives in various contexts and socio-economic settings.

The framework aptly terms the revolving credit fund a Job Creation Revolving Loan Fund (JCRLF) so that its objectives can easily resonate with Africa’s need to create full and productive employment and decent work for its growing population, rather than being a general credit fund focusing on improving access to credit which can easily be linked to various other productive and nonproductive uses. The fund can therefore be easily set up as an independent project or programs within the operations of different microfinance institutions to specifically address one or more of the six priority areas as circumstances permit or it can be integrated into other operations of the microfinance institutions. The impact of the JCRLF can therefore be enhanced where the particular microfinance institutions also provide other financial and nonfinancial capacity building services to its clients (e.g., business training).

FDI, the export of commodities, official development assistance (ODA), and remittance inflows are major influences of economic growth in Africa (Marwan et al., 2013), hence, these channels are the source funds that need to be harnessed in order to facilitate the growth of inclusive businesses and climate resilient growth in Africa. The JCRLF therefore has three main types of funders that have both commercial and noncommercial motives/incentives. Combining multiple funding sources can arguably enable the revolving fund to have a ‘lower cost of money’ and hence provide loans at concessionary interest rates, thereby overcoming the detrimental aspects to which high interest rates have on business growth and project development in Africa.

Funder As consists of individuals, investors, governments, multilateral and bilateral development banks, bilateral development cooperation agencies, the private sector, civil society, local communities, and research and development institutions that make donations to microfinance institutions as it is the case with many donations of philanthropy. Technological developments are making the sharing of information and transfer of money easier, hence, facilitating the growth of crowd-funding and peer-to-peer (P2P) lending/donating, whereby individuals and institutions can donate directly to other individuals and institutions; hence, the microfinance institutions have become mere intermediaries. For example, Microbanker (Uganda) uses its website to profile individuals and businesses that require funding; hence, it has been able to reach out to a global audience to enable it to continue supporting Ugandan enterprises regardless of periodic difficulties in attracting funding from institutional donors, governments, or companies (Microbanker, 2014).

Funder Bs consists of individuals, investors, governments, multilateral and bilateral development banks, bilateral development cooperation agencies, the private sector, civil society, local communities, and research and development institutions that support microfinance institutions through refundable donations. Refundable donations can enable microfinance institutions to borrow funds from the specified funders at zero percent interest and use the funds for their activities and return back to the funder after a specified time. This could increase the scope of available funders for the microfinance institutions since there could be instances where some potential funders could have ‘idle funds’ which can be temporarily available to be utilized for other purposes but not necessarily available for an outright nonrefundable donation. For example, Kiva Microfunds hosts a P2P crowd-funding platform where the Kiva lenders provide funds to various individuals and organization globally without anticipating a return on the money lent out when the money is returned to them after a specified time (Kiva Microfunds, 2014).

Funder Cs are various types of individual and institutional social investors who provide funds to microfinance institutions on condition that the microfinance institutions use the money for programs related to reducing poverty and assisting socio-economic development whilst anticipating a return/interest on the funds provided. For example, Myc4 A/S (Denmark) uses a similar model to mobilize funds and disburse funds. Myc4 A/S collects funds globally from various private and institutional investors, and subsequently remits the funds to various microfinance institutions that are its partners in different African countries. Through such an arrangement, the organization has been able to raise and disburse over €23,772,392 from 20,712 investors from 120 countries (Myc4, 2014).

The framework also suggests that microfinance organizations should have a holding account in a country where most of its foreign funds come from or have an arrangement with another foreign organization so that the other organization can receive and temporarily keep funds on behalf of the pertinent microfinance institution. This arrangement can encourage remittances and reduce transaction costs. Research indicates that even though remittances play a vital role in supporting health, education, food security, and productive investment in agriculture, many of the benefits of remittance transfers are lost in intermediation as a result of high charges, since remittance charges to and within Africa are almost double the global average (Watkins & Quattri, 2014). Consequently, if money transfer operators, banks, and other intermediaries reduced remittance charges to reach the world average levels and the five percent G8 target, remittance transfers would increase by USD1.8 billion annually (ibid.). In addition to this, some estimates suggest that there are many African migrants scattered around the world who currently provide around USD40 billion a year in officially recorded remittances. These migrants have the potential to provide more than USD100 billion a year to help develop Africa and there is also an estimated USD50 billion in diaspora savings that could be leveraged for low-cost project finance (Arezki & Brückner, 2012). Not surprisingly, Goal 10 of the SDGs which aims to reduce inequality within and among countries has a target to reduce to less than three percent the transaction costs of migrant remittances and eliminate remittance corridors with costs higher than five percent by the year 2030 (UNSD, 2015). Since mechanisms that can lower remittance charges can potentially increase remittance flows and amounts, the holding account is therefore aimed at reducing the transaction costs for international funders A, B, and C as their donations and investments would be subject to no or minimal fees as local deposits/donations, whilst the microfinance institutions will periodically remit the funds to the host country at a later date after amalgamating donations/investments from various sources to have bigger sums to transfer preferably through commercial banks, 1 which generally have lower charges than money transfer operators.

Discussion

It has been reported that climate change policy debates have largely focused upon estimating adaptation costs, ways to raise and to scale-up funding for adaptation, and the design of the international institutional architecture for adaptation financing, consequently ignoring discussion on actual delivery mechanisms to channel these resources at the subnational level, particularly to target the poor who are also often the most vulnerable to the impacts of climate change (Agrawala & Carraro, 2010; Bodansky & Diringer, 2014; Hyder, 2008; Rong, 2010). As elaborated earlier on in this article, microfinance institutions are capable of designing and implementing various types of interventions that are context sensitive and adapted to local needs, and hence can play a great role in ensuring that Africa is able to achieve and sustain inclusive growth based on the six mutually reinforcing pillars of enhancing climate change resilience, food security, technology transfers and diffusion, empowerment of vulnerable groups, creating alternative livelihoods, and integrated rural development/rural diversification. In order to enhance the effectiveness of microfinance programs aimed at facilitating climate resilient inclusive growth, it may be necessary for microfinance programs to be designed to support ODA and national planning and poverty alleviation processes. This follows that, the aforementioned development strategies have also got a role in creating macro-economic stability, reducing poverty, and facilitating climate change management by reducing a country’s vulnerability to external trade shocks, enhancing country investment capacity, and promoting social cohesion and political stability.

Microfinance may be considered as one of the most sustainable, effective, and flexible strategies in the fight against global poverty possibly due to its potential to be implemented on a massive scale necessary to respond to the urgent needs of the world’s poor (Kotir & Obeng-Odoom, 2009). This article has presented a framework which highlights the roles to which microfinance could have in promoting inclusive growth and more particularly mitigating the risks as presented by climate change, hence addressing arguably two of Africa’s greatest development challenges. However, for microfinance to have a more prominent role in promoting climate resilient inclusive growth, Africa’s rates of financial inclusion have to be increased. For example, in SSA, an average of only 24 percent of the population has an account with a formal financial institution (in contrast to 55 percent of adults in East Asia, 35 percent in Eastern Europe, 39 percent in Latin America, and 33 percent in South Asia), subsequently leading to reduced female empowerment and productive investment in the region (Aga & Peria, 2014).

The concept of inclusive growth is multifaceted and has financial inclusion as one of its main building blocks. The provision of appropriate and quality financing that is both accessible and affordable to low-income and other vulnerable households can allow developing countries to harness the untapped potential of those individuals and businesses currently excluded from the formal financial sector, and enable communities to manage risks associated with their livelihoods (Triki & Faye, 2013). African countries should therefore demonstrate clear policy signals and political support to prioritize financial inclusion since that can also improve the outreach of microfinance institutions, hence supporting effective climate change management and inclusive growth (and its ancillary benefits).

Lastly, microfinance works differently in different regions. Factors such as population density, attitudes to debt, group-cohesion, enterprise development, and financial literacy can influence the impact of microfinance projects (Van Rooyen et al., 2012). On the other hand, microfinance sophistication, financial resources, mission, market, management information systems, and the regulatory environment can influence the ability of microfinance institutions to diversify and develop new products (Rippey, 2009). It should therefore not be assumed that microfinance can provide all the answers to support the growth and sustainability of inclusive businesses. Since the practice of microfinance itself varies enormously and is available to a wide range of people in a variety of contexts, accordingly, there will always be a need to consider what we know about the different types and models of microfinance and whether or not they work, for whom and in what circumstances (Van Rooyen et al., 2012). These assertions reinforce the need to continuously develop various microfinance programs and projects that can explore and test the effectiveness of microfinance in addressing the development challenges as presented by climate change, population growth, and economic growth.

Conclusion

The challenge of achieving sustainable development in Africa is enormous. This follows that various models and strategies have been implemented in various African countries to promote socio-economic development but have achieved varying levels of success. Africa manages to register high economic growth rates but this has neither translated into inclusive growth that substantially reduces poverty nor created sufficient jobs of good quality for its population. In addition to this, climate change is anticipated to lead to more frequent extreme events such as droughts and floods which could significantly increase the risk of agricultural production failures, thereby perpetuating food insecurity and disrupting rural livelihoods.

Microfinance is a development tool that has been shown to reduce poverty by improving access to financial services to vulnerable groups, thereby enabling them to increase their incomes, investments in small businesses, assets, and reduce their vulnerability to drought and crop failures. This makes microfinance an ideal tool to be utilized in order to foster inclusive growth and enhance climate change resilience. A microfinance-inclusive growth framework with six mutually reinforcing pillars of enhancing climate change resilience, enhancing food security, promoting technology transfers and diffusion, empowering vulnerable groups, promoting alternative livelihoods, and facilitating integrated rural development/rural diversification was presented in this article. An inclusive growth framework, with a focus on creating jobs and stimulating entrepreneurship in rural and urban settings in both informal and formal settings, was shown to be able to have the scope to attract institutional and private funding for microfinance activities, and more importantly minimize some of the barriers to remittances and the flow of funds between different countries.

The priority areas and contextualization of emerging development challenges as presented in the SDGs highlights what could be a fundamental shift on how development and poverty reduction will be financed and addressed in the future. Financing and funding modalities for the 8 MDGs and associated 18 targets and 48 technical indicators to measure progress toward the goals were not a prominent aspect in the MDG framework, arguably due to the premise that ODA would be provided in sufficient amounts to achieve the goals. However, most of the SDGs and associated targets contain various aspects related to resource mobilization and financial services. Arguably, this highlights how microfinance could have a greater part toward promoting sustainable development not only by leveraging funds from private and institutional sources to complement public funding for development but also by assisting in effectively channeling resources to communities and segments of society that were excluded and marginalized by formal financial institutions. This means microfinance could have a significant bearing on promoting inclusive growth and enhanced climate change management.

All in all, climate resilient inclusive growth strategies are desirable yet unattainable without sustainable financing mechanisms that can address the livelihood needs of people in developing countries. The microfinance-inclusive growth framework and JCRLF, as presented in this article, offers a dynamic framework that can sustainably stimulate both the demand and supply aspects of adaptation and mitigation actions, whilst creating the much needed jobs in developing countries. Using this framework, funds from grants, donations, social investments, and crowd-funding can be leveraged together to enhance the institutional, financial, and technological capacity of various stakeholders to implement context- specific adaptation and mitigation actions that can enable African countries to promote sustainable development, reduce poverty and inequality, and minimize the adverse impacts of climate change regardless of the country’s existing national realities, capacities, and levels of development.