Abstract

This article examines the impact that external financial flows have on gross domestic product (GDP) growth in a new, small, and open economy—the Republic of Kosovo. Remittances, foreign direct investment (FDI), foreign debt, and net exports may affect GDP in different ways. In the context of a new, small, and open economy, these factors can be important determinants of economic development. This article examines the direct effect of these factors on economic development as represented by GDP growth in Kosovo, covering the period of 2012–2018. The relationships between remittances, net exports, FDI, external debt, and GDP are modeled based on theoretical arguments and empirical evidence. The results suggest that in Kosovo, remittances are the leading contributor to GDP growth. This contribution could be more valuable if remittances were invested in the manufacturing sector. These investments could have positive effects on job creation, thereby reducing the unemployment rate and Kosovo’s dependence on imports.

Keywords

Introduction

The various economic factors that influence gross domestic product (GDP) growth have been the subject of political and scientific debates for a long time. The research in this field does not provide the same results regarding the relationship between these factors and GDP. The research seems contradictory if country specifics (economic, social, and political conditions) are not taken into account.

This article analyzes the relationship between external financial flows and GDP growth in Kosovo, which as a new, small, and open economy depends to a large extent on these external factors. For this purpose, the article highlights the impact that foreign direct investment (FDI), remittances, net exports, external public debt, and external private debt have on GDP growth.

According to the World Bank (2018), Kosovo’s economic growth has consistently been above the Western Balkans’ average since the global financial crisis, despite its small base. But even though GDP per capita has increased, Kosovo remains the third poorest country in Europe.

The Bertelsmann Stiftung’s Transformation Index (BTI) Country Report on Kosovo (2018) reported that the primary sources of economic growth in Kosovo are public investment, the export-oriented mining industry, and remittances. The report showed a high unemployment rate of almost 33 percent in 2015. Diaspora investments mostly drive Kosovo’s economy but leave the economy to pay for imports instead of strengthening the development of the local economy. The national economy should be driven by investments and trade rather than remittances and consumption.

According to the International Fund for Agricultural Development (2015), Kosovo relies mostly on remittances from the Kosovar diaspora. In response to this situation, the International Organization for Migration (IOM) and the United Nations Development Programme (UNDP) have jointly implemented a Diaspora Engagement in Economic Development (DEED) project, which aims to increase the opportunities for members of the Kosovar diaspora and remittance-receiving households in Kosovo to participate in the country’s economic development through the investment of remittances in creating jobs and new businesses.

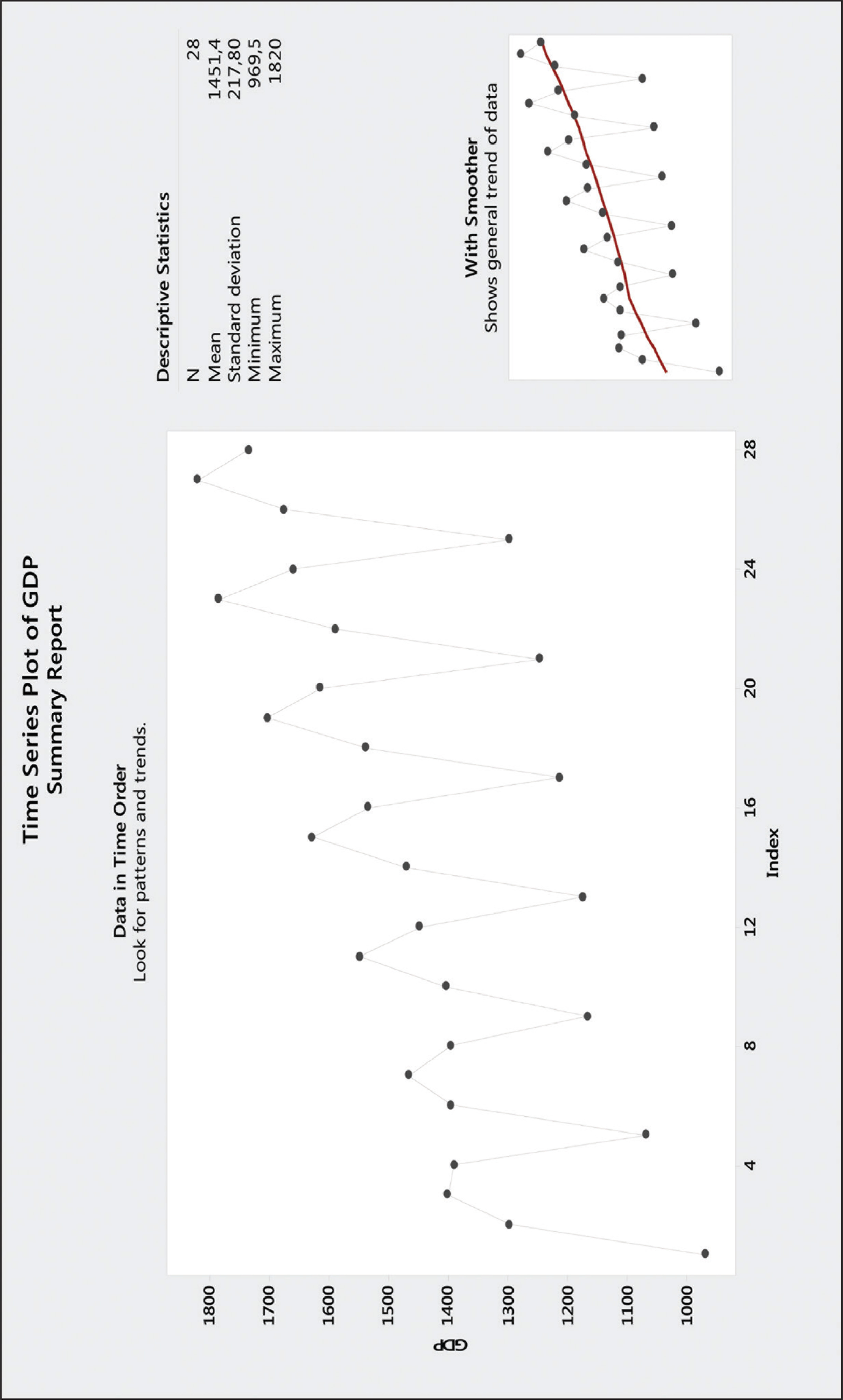

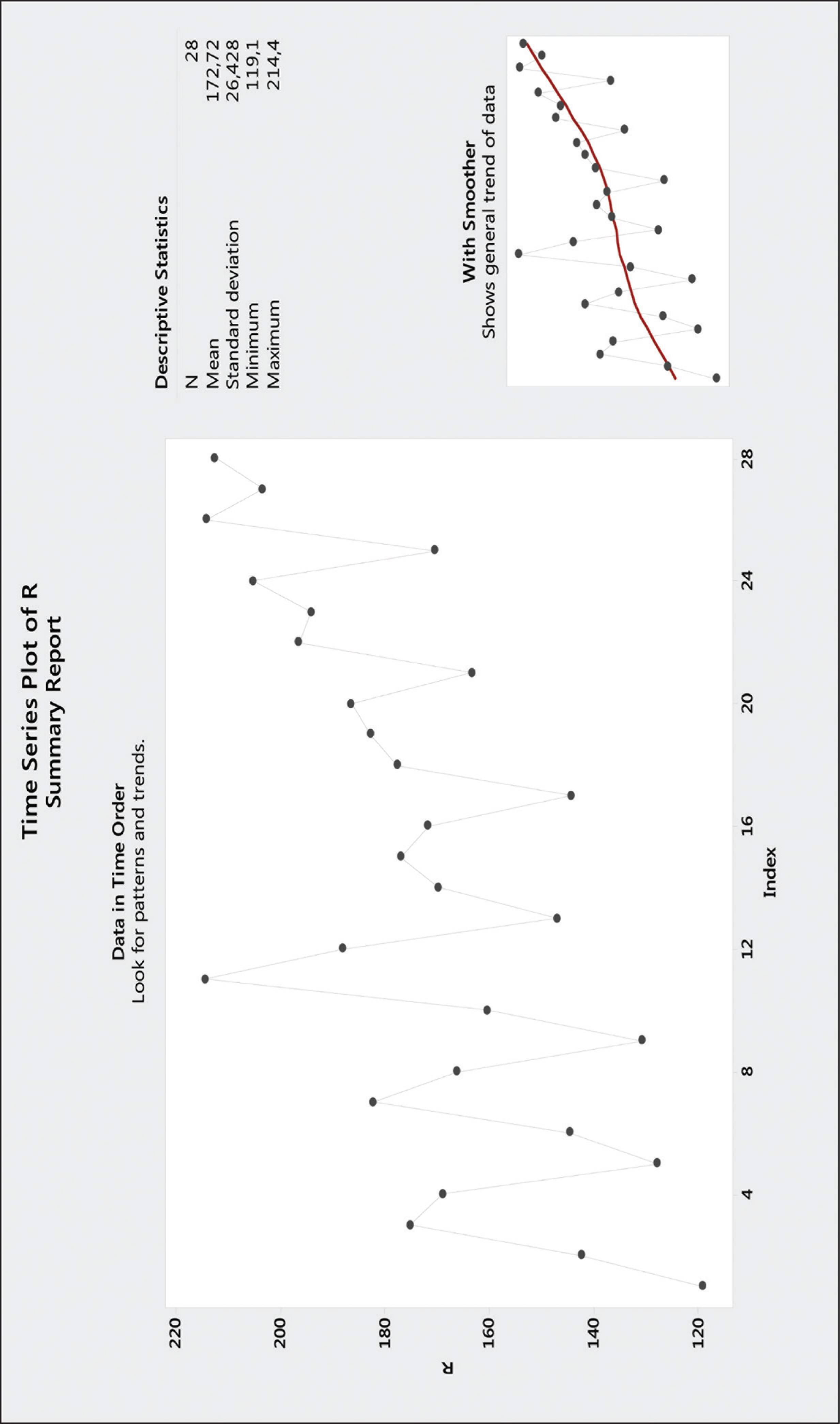

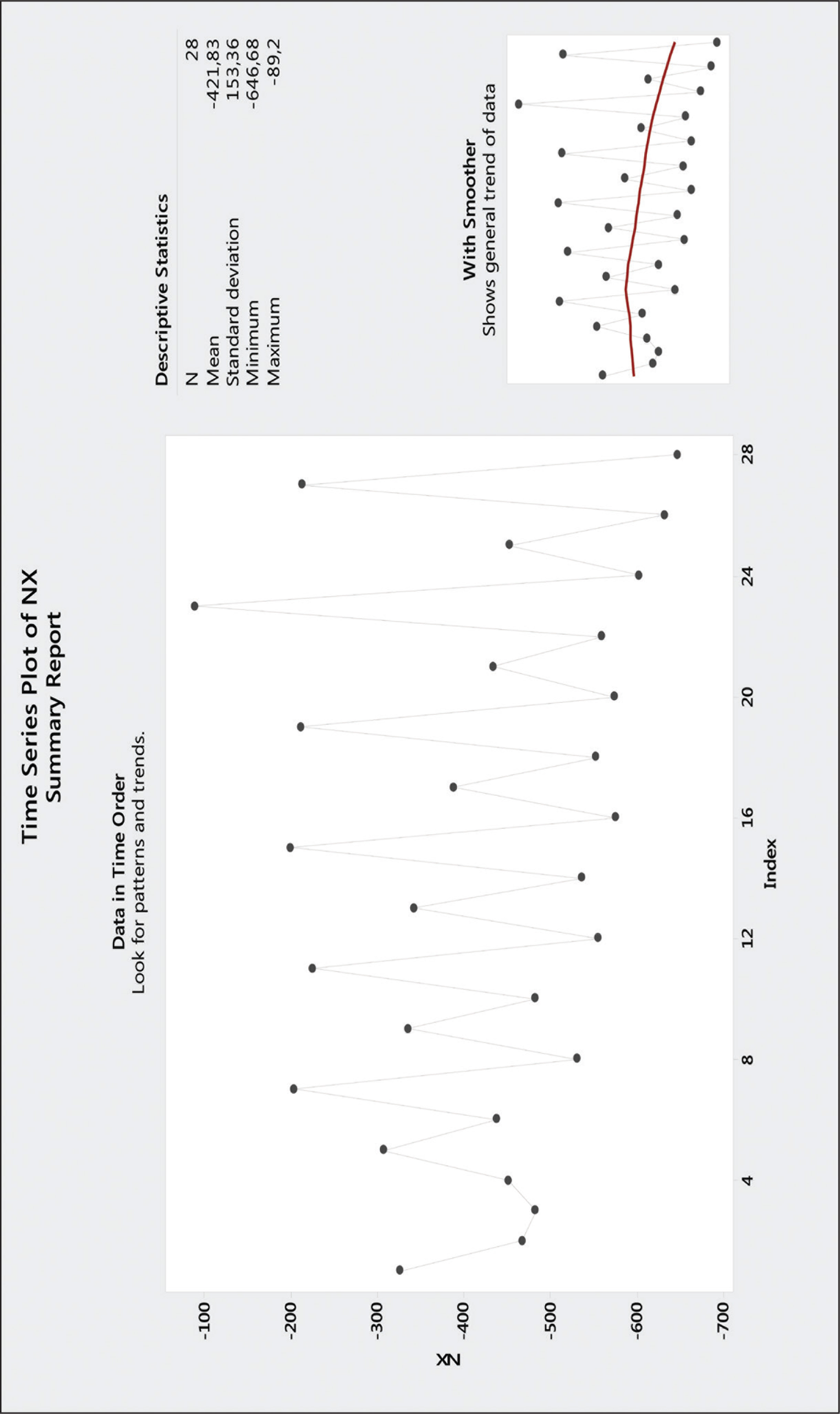

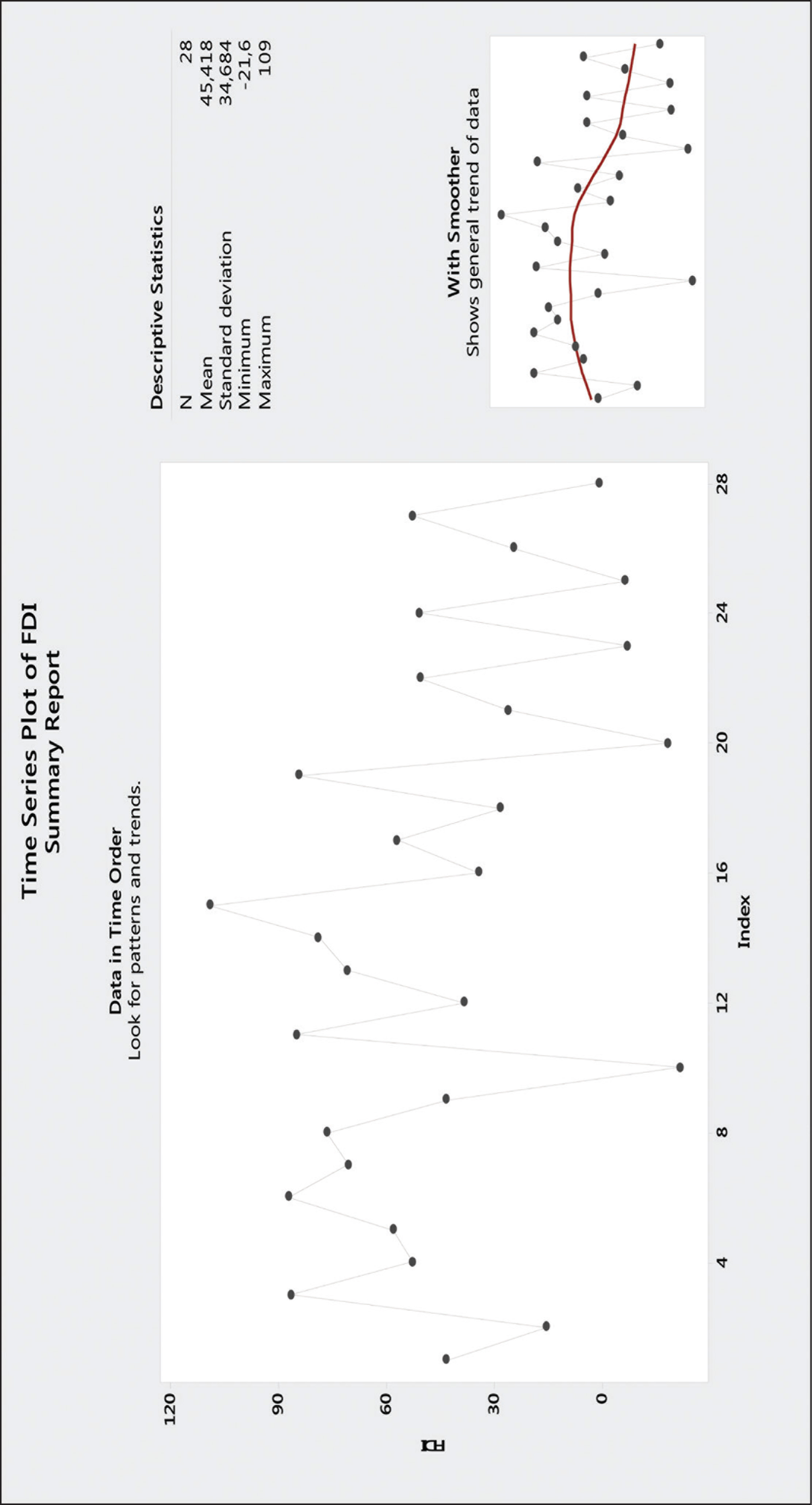

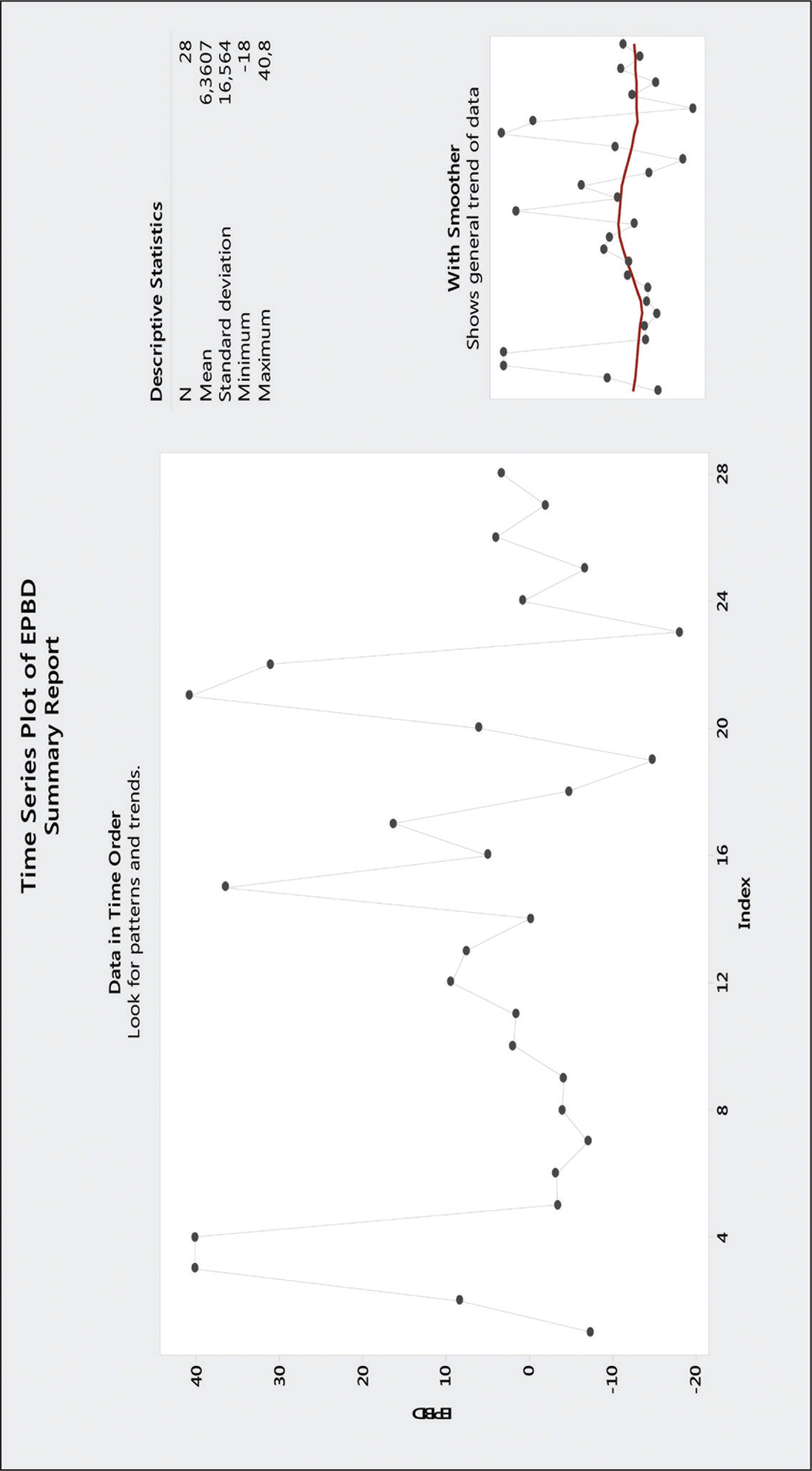

During the period from the first quarter of 2012 to the fourth quarter of 2018, Kosovo’s GDP and remittances have generally shown a steady upward trend (Figures 1 and 2). Net exports and FDIs initially showed a slight upward trend, but in the second half of the observed period, this trend decreased steadily (Figures 3 and 4). The same can be said for external private debt, but with a more pronounced trend in both directions (up and down) when compared to net exports and FDI (Figure 5). External public debt, unlike other variables, has a quite low downward trend (Figure 6).

In light of these trends, we examine the relationship between the independent variables and GDP as the dependent variable. The findings will hopefully serve as important indicators for policymakers in determining policies that improve the economic and social environment for sustainable economic development.

Literature Review

There are a number of studies on the relationship between GDP and other factors that may affect GDP and economic growth. Elmendorf and Mankiw (1998) present the conventional theory of government debt and have continued examining the theory and empirical evidence of debt neutrality which is called Ricardian equivalence. Reinhart and Rogoff (2010) have found that across both advanced countries and emerging markets, high debt/GDP levels are associated with lower growth outcomes. They have found no coherent relationship between high debt levels and inflation in advanced economies. On the contrary, in emerging market countries, higher public debt levels are associated with higher inflation rates.

The general theoretical assumption is that at a low public debt level, the effect on growth is positive, whereas, beyond a certain debt level, the negative effect on growth prevails, as has been proved by Mencinger, Aristovnik, and Verbic (2014, 2015). They found that the positive impact of accumulated public debt turned into negative effect between 80 percent and 94 percent in the European Union (the EU without the new member states). The hypothesis that the public debt may have a significant impact on GDP, in some cases, a negative impact depending on country-specific differences, has been confirmed by Ribeiro, Vaicekauskas, and Lakstutiene (2012). In other cases, the GDP has been affected positively by public debt.

Concerning private debt and private credit flows, the results show positive effects on the economy, suggesting that private debt is more efficient than public debt. Also, the effects that the openness of the economy and inward FDI have on GDP vary due to the different characteristics of the countries. Egert (2012) has found some evidence favoring a negative linear relationship between debt and growth, using nonlinear threshold models. According to Egert, these results were sensitive to the time dimension, the country coverage considered, data frequency, and assumptions on the minimum number of observations required in each nonlinear regime.

Akalpler and Shamadeen’s (2017) study confirms that a positive relationship exists between net exports and economic growth, supported by the positive influence of gross fixed capital formation, and a negative relationship between imports and economic growth in the USA. Lee and Zhang (2019) have explored the possible links between export structure and economic growth and their volatility in a low-income and small countries, using a range of export concentration indices that vary across industries. Their results show that export diversification can boost economic growth and reduce economic volatility depending on the size of the country and the level of income. Ronit and Divya (2014) in their study of the relationship between export growth and GDP growth, in the case of India, concluded that there is evidence against the export-led growth hypothesis. Through the impulse response function, they prove that the shocks to GDP growth affect the growth of exports. The reason for this specific relationship between export growth and GDP growth is India’s large domestic market.

Abbes, Mostefa, Seghir, and Zakarya (2015), based on their study of the relationship between FDI and economic growth in 65 countries, have concluded that FDI is positively and significantly related to economic growth. Their results about FDI and growth demonstrate a strong long-run relationship between the two, and show the importance of FDI for economic growth in these countries. Simionescu (2016) has investigated the relationship between FDI inflow and economic growth in the EU-28 during the financial crisis period (2008–2014), concluding that there was inverse relationship between economic growth and FDI starting at the beginning of the crisis. Puri and Sengupta (2018) have proved the association between FDI and GDP, and the role of the individual economic policies of countries in explaining the difference in the quantity of the flow of FDI.

Alfaro (2003) examined the relationship between FDI and growth and concluded that the benefits of FDI vary widely across sectors. The results of Alfaro’s research show that FDI in the primary sector tends to have a negative effect. On the contrary, this research shows FDI in the manufacturing sector has had a positive effect on growth, while evidence in the services sector has been ambiguous. Iamsiraroj and Doucouliagos (2015) investigated the impact of economic growth on FDI. In their analysis, which consists of 946 observations from 140 comparable empirical studies, they conclude that there was a robust positive correlation between growth and FDI. This correlation was slightly higher in developing countries than all countries combined, but with no practical importance.

There are many debates and studies on the relationship between remittances and GDP in developing countries (Lubambu, 2014). After FDI, remittances represent the second most important source of external financing for developing country economies. In Albania, for example, remittances surpass export, net FDI, and official development assistance. When considering remittances as a percentage of GDP, the World Bank ranks Albania among the first in Eastern Europe and the former countries of the Soviet Union, whereas, in Kosovo, they represent approximately 20–30 percent of the country’s GDP (Anghel, Piracha, & Randazzo, 2015). Hassan and Shakur (2017) have found a nonlinear relationship between remittances and economic growth. The estimated positive and significant coefficient on the square of the remittances variable implies that remittance flows decrease the per capita GDP growth rate in the initial phase but increase the growth in later stages. In the early periods, remittances are sent for unproductive use, but in later periods they tend to be used for more productive purposes. Paul and Das (2011), in their research, found a long-run positive relationship between remittances and GDP in Bangladesh but no evidence of remittance-led growth in the short run. They also noticed that the impact of GDP in remittances was much stronger than of remittances in GDP.

Regarding the relationship between economic growth and remittances, studies show that higher economic growth increases with the level of remittances. Also, per capita income and the size of the economy affect remittance flows (Niimi & Ozden, 2008). When considering the channels of remittance effect on the economic growth, direct estimates of the remittance effect in the investment to GDP ratio show that about 50 percent of the impact of remittances on growth derives from an increased rate of domestic investment (Acosta, Calderon, Fajnzylber, & Lopez, 2008).

Methodology

The following estimated regression model we developed relates quarterly data on GDP (dependent variable), remittances, FDIs, net exports, external public debt, and external private debt (independent variables). The sample consists of 28 observations, covering the period from the first quarter of 2012 to the fourth quarter of 2018. The formula is GDPt = α + β1FDIt + β2Rt + β3EPbDt + β4EPrDt + β5NXt + εt. where the unknown parameters are:

α—the constant; βk—the coefficients; and εt—the error term, which represents other factors that influence the dependent variable.

The dependent variable is GDP t —represented by GDP at current price, estimated quarterly.

The independent variables are:

FDI

t

—FDI represents the increase or decrease in total incoming direct investment amount; Rt—remittances are the quarterly amount of migrant transfers inflow; EPbD

t

—external public debt, which represents the increase or decrease in the amount of public and publicly guaranteed external debt of the general government and central bank at the nominal value outstanding at the end of the quarters; EPrD

t

—external private debt represents the increase or decrease of the external debt of the private sector not publicly guaranteed by deposit-taking corporations (excluding the central bank), other sectors, and intercompany borrowing; and NX

t

—net export includes the export and import of goods and services. Model selection is based on the following main indicators: R2, R2 (adjusted), R2 (predicted), Mallows’ Cp, S value, Pearson correlation, Spearman’s rho correlation, Durbin–Watson statistic, and Grubbs’ test.

Findings and Discussion

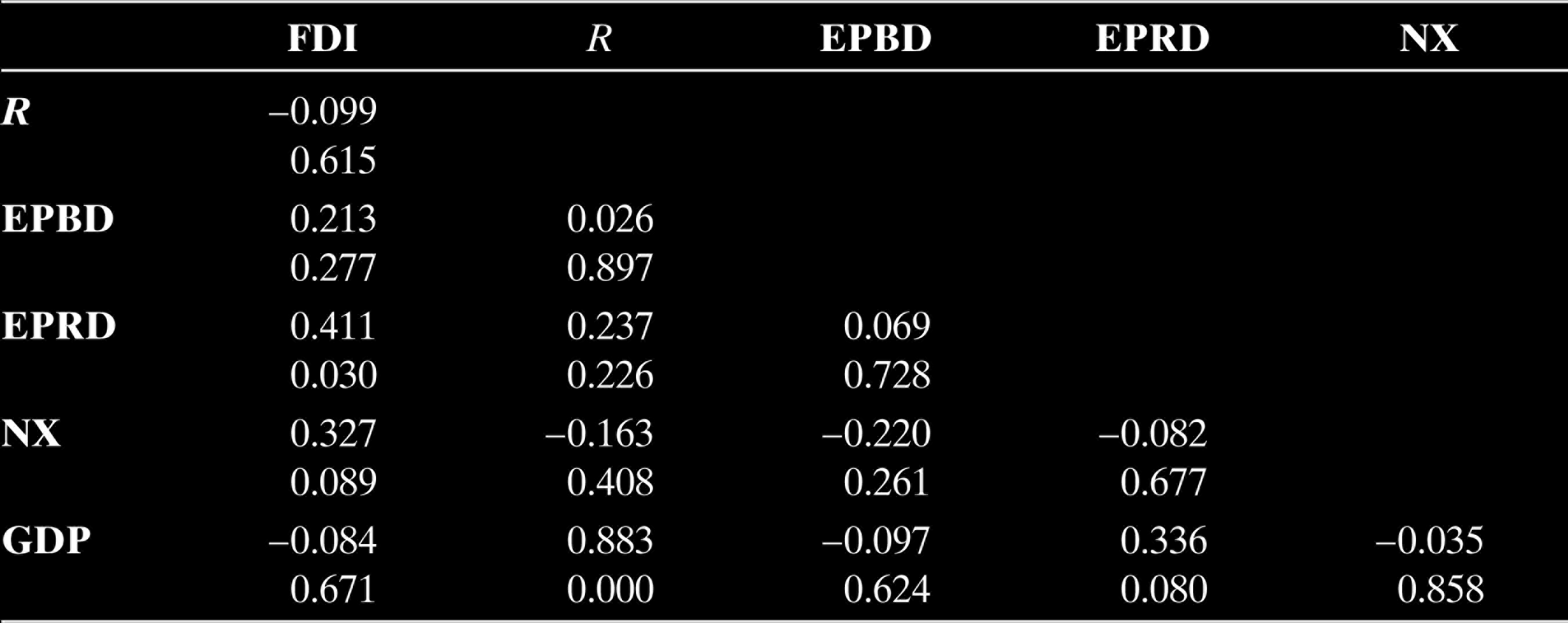

To see the strength and direction of the linear and monotonic relationship between the variables, we used the Pearson correlation and the Spearman’s rho correlation. Based on the Pearson correlation, our research indicates FDI shows a low negative relationship with remittances and with GDP, and a weak positive relationship with external public debt. But there is a significant moderate positive relationship with external private debt and a moderate positive relationship with net exports. The weak positive linear relationship between remittances and external debt (public and private) and the low negative relationship between remittances and net exports are statistically not significant. The correlation coefficient between remittances and GDP indicates a strong positive relationship.

There is a low negative relationship between external public debt and net exports and GDP, and a weak positive correlation with external private debt, statistically no significant. External private debt has a weak negative correlation with net exports, and a moderate positive correlation with GDP, whereas, net exports have a low negative relationship with GDP (Table 1).

Pearson Correlation

Spearman’s Rank-order Correlation

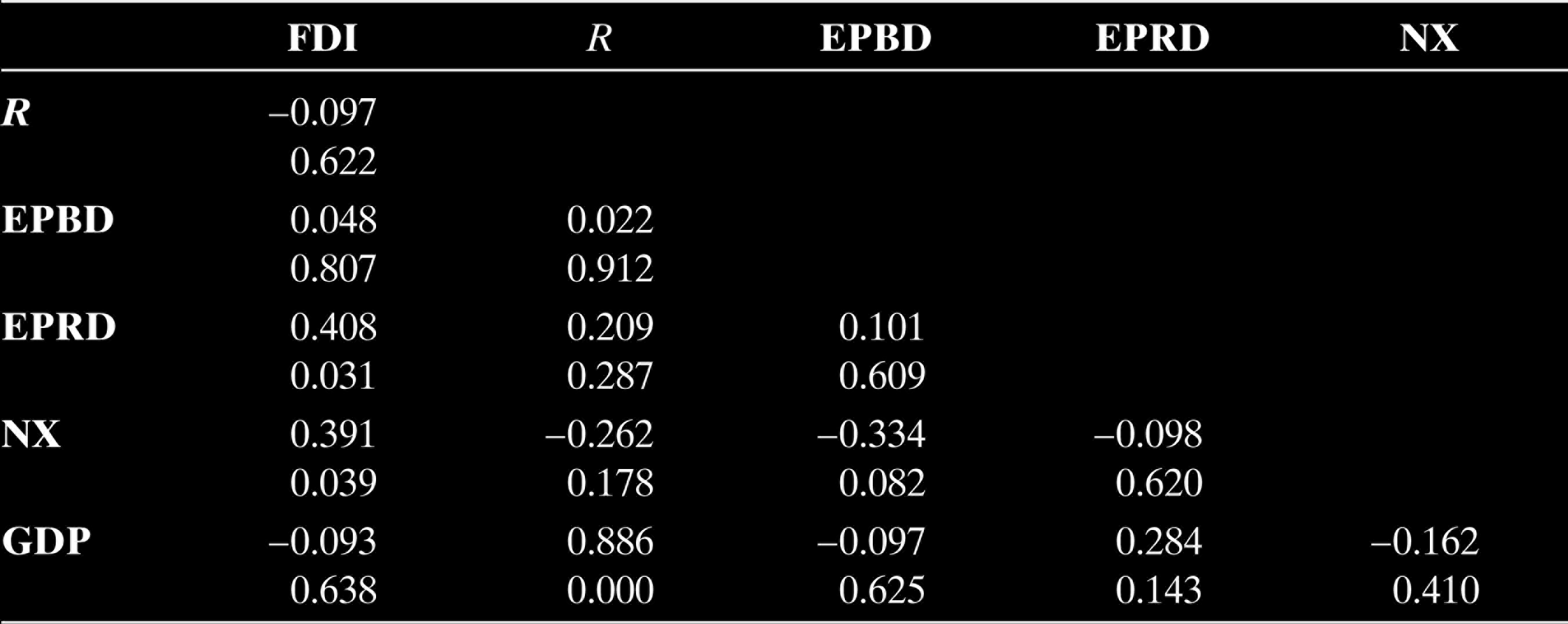

The Spearman’s rank-order correlation shows the same results as the Pearson correlation, with small differences. In the case of the relationship between FDI and external public debt, the monotonic correlation is weaker than the linear correlation. But in relationship with net exports, the positive monotonic correlation is strong compared to the linear correlation. Regarding the relationship between net export and GDP, the result shows a higher negative monotonic correlation than the linear correlation (Table 2).

Spearman’s Rho Correlation

To test the presence of autocorrelation in the errors of the regression model, we performed the Durbin–Watson statistic. This statistic (Durbin–Watson statistic = 1, 55) shows that the adjacent observations errors are not correlated. Thus, we can conclude that standard errors seem not underestimated, and the predictors appear significant because the statistical test value remains within a relatively normal range. The variance inflator factor (VIF) shows no significant multicollinearity in the regression model. Since this indicator remains very low, the contribution of each variable to the standard error in the regression is not significant.

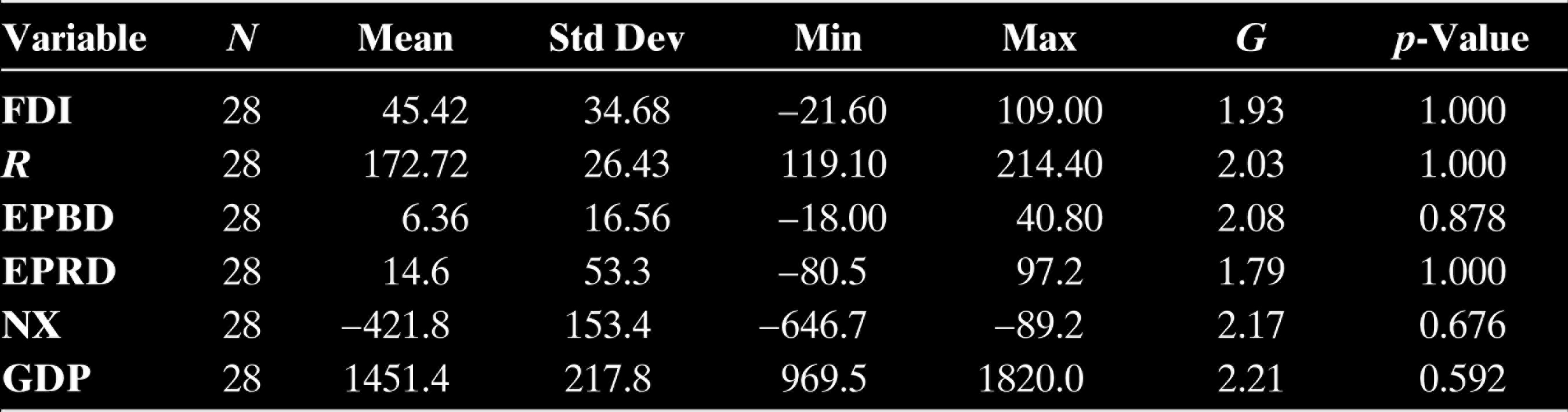

With regard to the strength of the relationship between the model and the dependent variable (GDP), the distance between data and fitted values (S) is around 99.8371, and the model explains 82.88 percent of the variation in GDP. The percentage of variation in response explained by the model, adjusted for the number of predictors relative to the number of observed values, is 79 percent, and the predictive ability of the model is around 70 percent (Table 3). Mallows’ Cp equals the number of independent variables plus the constant, indicating that the model is unbiased and fits the data well. The p-value for the regression as a whole is significant with p-value < 0.05 (Table 4). The Grubbs’ test shows no outlier at the 5 percent level of significance (Table 5).

Model Summary

Analysis of Variance

Method

Null hypothesis: All data values come from the same normal population

Alternative hypothesis: Smallest or largest data value is an outlier

Significance level: α = 0.05

Grubbs’ Test

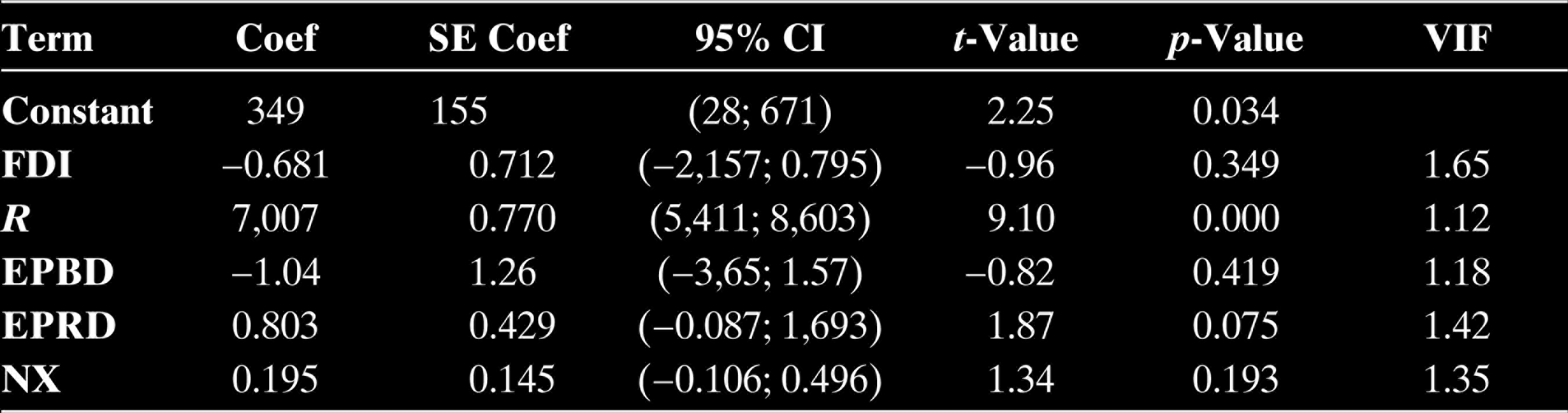

With regard to coefficients (Table 6), the standard error of the remittance coefficient and the coefficient value itself vary widely (t-value 9.1). So, the model was able to estimate the remittance coefficient with great precision. The remittance coefficient value resulted in 7,007, signifying a high positive impact on GDP. That is, for each unit increase in remittances, the GDP increases by seven units. Unlike in other countries where remittances have shown negative or mixed effects on GDP and economic growth (Caceres & Saca, 2006) (Hassan & Shakur, 2017) (Singh, Haacker, Lee, & Le Goff, 2010), in the case of Kosovo, the effects are positive. As remittances represent a significant percentage of GDP, they produce multiplier effects that lead to economic growth. They have considerably improved the living standard of the recipient households of Kosovo, and as such, remain stable regardless of the economic conditions (Duval & Wolff, 2016). The contribution of remittances to GDP depends on how these funds are handled.

Coefficients

In the case of Kosovo, remittances are used as follows: current consumption = 35.4 percent, other expenditures = 24.8 percent, residential investment (acquisition or renovation) = 19.6 percent, education or health-care spending = 10.6 percent, business investment = 3.9 percent, and savings = 3.7 Percent (Ministry of Economic Development, 2018). The contribution of remittances to economic growth would most likely be greatly enhanced if used in the form of direct investment in sectors that will generate benefits such as profits, dividends, interests, commissions, etc. (Govori, 1997).

Regarding EPbD, the standard error of the coefficient and value of coefficient itself do not have large difference (t-value 0.82; p-value 0.419), indicating a negative effect of external public debt on GDP. That is, for every unit increase in EPbD, the GDP decreases by about 1.04. At the end of 2018, external public debt accounted for around 38 percent of total public debt, which represents about 6.27 percent of GDP. Projects financed by external public debt include road infrastructure, water infrastructure, and public sector services (Debt Management Division, 2019). Investing these funds mainly in these nonproductive sectors had a negative effect on the GDP.

On the contrary, the external private debt shows positive effects on GDP. External private debt accounts for around 75 percent of total external debt and is mainly short-term debt. The difference between the external private debt coefficient and SE coefficient is small (t-value 1.87, p-value 0.075). The regression coefficient shows that for each unit increase in external private debt, GDP increased by 0.803.

The regression coefficient of the net exports relates positively to the GDP, which indicates that the GDP increases by 0.195 for each unit increase in net export. The trade deficit in Kosovo remains roughly 30 percent of GDP. Imports have continued at close to 50 percent of GDP (International Monetary Fund [IMF], 2018a). Although exports increased steadily over the last 3 years (raw materials, agricultural and food products, and services), the trade deficit still remains large. This deficit is due to the faster growth of imports of goods and the much slower growth of exports of goods.

There is evidence of a small difference between the SE coefficient and the FDI coefficient, which resulted in a t-value of −0.96 and a p-value of 0.349. The negative regression coefficient of FDI indicates that for every unit increase in FDI, there is a decrease in GDP by about 0.681 units. Generally, FDIs in Kosovo have declined in recent years. This decline was evident in 2018 and was enough to finance the current account deficit (World Bank, 2019). The negative effect of FDI on GDP may be a result of FDI inflows into the primary sector during the observed period. Recent FDIs focused mainly on real estate. Positive effects cannot be expected as long as these investments are not concentrated in the manufacturing industry sector (Alfaro, 2003).

Conclusions

As in many other developing countries, remittances in Kosovo play a vital role in the economy. From the view of the family members who receive them, remittances increase the well-being of these families by supporting their consumption of goods and services, enhancing education, and assisting in their investment activities (business, real estate, savings, etc.). Remittances also play a vital role in economic growth. Depending on the way remittances are used, they induce different effects on macroeconomic conditions and their indicators.

We found that from the view of the macroeconomic effects, remittances have a positive impact on GDP. Less favorably, their use mainly relates to consumption and expenditures by about 60.2 percent, and only a small portion of these funds are used for business investment purposes. The usage of remittances for investments in the manufacturing sectors would create benefits for both the investors and the economy as a whole.

According to empirical findings, the results show that external public debt has negative effects on GDP growth, while external private debt has positive effects. The negative effects of external public debt on GDP, as well as the positive effects of external private debt on GDP, are based on the fact that projects financed through external public debt belong to the nonprofit sectors, while external private debt is associated mainly with the financing of business projects that can produce profits.

Empirical evidence regarding the impact of FDI on GDP growth indicates mixed effects. Some research has shown that FDIs’ impact on GDP is greater in export-oriented economies (Iqbal, Ahmad, Haider, & Anwar, 2014). However, other research shows no significant positive effects of FDI on GDP growth (Carbonell & Werner, 2018). Our study shows that FDI negatively impacts GDP growth. This result may be due to the country’s trade deficit and concentration of FDI in nonmanufacturing sectors.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.