Abstract

Microcredit programs usually target poor rural women to reduce poverty and empower the women involved. The general body of existing research provides conflicting evidence, depending on context, poverty reduction and empowerment may or may not be partially achieved. Research on the effects of context on microcredit is limited in Ghana. Based on focus group discussions and in-depth interviews with stakeholders, the contextual factors that affect microcredit for poverty reduction among women are explored. The findings of this study suggest that the orthodox use of social collateral through group lending doesn’t fully account for why some microlending programs are effective, and others are not. Contextual factors appear to make the difference.

Introduction

Since the Beijing Platform for Action in 1995, the gender dimension of poverty has received increased attention, as has the need for specific strategies in support of women who are living in poverty. Among these strategies, those that enhance women’s access to financial services and resources as means to improving their livelihoods have received particular attention in sub-Saharan Africa. In many countries in Africa, poor people, especially women, are generally excluded from the financial services sector (World Bank, 2012). For instance, only about 22 percent of women and 27 percent of men in sub-Saharan Africa have a bank account with a formal financial institution (World Bank, 2012). Limited savings and lack of access to credit make it difficult for many women in Africa to become self-employed and to undertake productive employment and income-generating ventures (Ganle, Afriyie, & Segbefia, 2015). Microcredit programs for women have thus emerged and are currently being promoted as both a solution to women’s limited access to credit, a strategy for poverty reduction and women’s empowerment (Afrane, 2002; Arku & Arku, 2009; Ganle et al., 2015; Haile, Bock, & Folmer, 2012; Schindler, 2010).

Microfinance is a broad term encapsulating a package of financial services including loans, savings, insurance, leasing, transfers, and forms of social intermediation such as non-financial support provided by formal, semiformal, and informal institutions to prospective borrowers to help them acquire through skills and values which they need to initiate and sustain microenterprises (Ngo & Wahhaj, 2012). For the purposes of this study, the term microcredit is used, because the microlending organizations we studied only provided small loans, with limited emphasis on savings, insurance, leasing, transfers, and social intermediation. By microcredit, we mean the extension of a small amount of collateral-free institutional loans to jointly liable group members or in some cases individuals for their self-employment and income generation (Rahman, 1999).

There are arguments that microlending to poor women holds the key to twenty-first century sustainable economic and social development (Kamau, Kimani, & Wamue-Ngare, 2014; Norwood, 2005; United Nations [UN], 2011). According to this argument, the biggest promises of microcredit are to reduce poverty and empower women (Banerjee, 2013; Norwood, 2005). A number of authors have particularly noted the critical role of microcredit in achieving the Millennium Development Goals (Kamau et al., 2014; Littlefield, Morduch, & Hashemi, 2003; Makina & Malobola, 2004; Simanowitz, 2003). In fact, Mohammed Yunus, founder of the Grameen Bank’s microcredit program in Bangladesh, has suggested that microcredit is one simple idea that could eradicate global poverty among women (Hulme, 2000).

In Ghana, as in many sub-Saharan African countries, microentrepreneurs constitute about 66 percent of the labor force (Adjei, 2010). Microfinance institutions (MFIs) provide financial services to an estimated 15 percent of the country’s total population compared to the 10 percent for the commercial banking sector (Adjei, 2010). In recognition of the growing importance of microfinance in poverty reduction, the Government of Ghana (GoG) in 2006 established the “Microfinance and Small Loans Centre” (MASLOC). Currently, MASLOC operates as a microfinance apex body responsible for implementing the GoG’s microfinance programs targeted at poverty reduction, and job and wealth creation. It also provides business advisory services, training, and capacity building for small- and medium-scale enterprises.

Despite the growing importance of microcredit in the development of African economies, evidence from several impact assessment studies has generally revealed mixed results (Adams & Von Pischke, 1992; Copestake, 2002; De Haan & Lakwo, 2010; Ganle et al., 2015; Imai, Gaiha, Thapa, & Annim, 2012; Rooyen, Stewart, & De Wet, 2012; Sigalla & Carney, 2012; Zaman, 2001). In fact, a recent systematic review on the impact of microcredit on income, savings, expenditure, and the accumulation of assets as well as non-financial outcomes including health, nutrition, food security, child labor, education, women’s empowerment, housing, job creation, and social cohesion concluded that the true impact of microcredit in sub-Saharan Africa is decidedly mixed (Rooyen et al., 2012).

While research and debate on the development impact of microcredit remains largely unsettled, what is emerging is that the impact, success, or failure of microcredit schemes usually depend on contextual factors such as the target group, the type of lending model or strategy, attitudes about debt, group cohesion, financial literacy, the presence of regulatory institutions, and other sociocultural factors (Cull, Asli, & Morduch, 2011; D’Espallier, Guerin, & Mersland, 2011; Ganle et al., 2015; Haile et al., 2012; Hermes & Lensink, 2011; Karlan & Zinman, 2010). This literature, as Tchouassi (2011) argues, is an emerging trend in the mainstream literature. As such there is limited direct empirical studies addressing this issue in the context of Africa more generally and Ghana in particular (Ngo & Wahhaj, 2012). The few studies that have indirectly examined how contextual factors influence the outcomes of microcredit schemes have, however, reported interesting findings. For instance, Hartarska (2005), Hartarska and Nadolnyak (2007, 2008), and Caudill, Gropper, and Hartarska (2009) have identified efficient contract design, good lending methodology, and corporate governance as important contextual success factors. In Ethiopia, Haile et al. (2012) studied the role of formal and informal institutions in facilitating or hindering the ability of microfinance schemes to empower women. They find that variations in formal and informal rules matters for how microfinance programs work out. Ngo and Wahhaj (2012) also studied microcredit and gender empowerment and found two instances in which women are most likely to benefit: when there is scope for investing the loan profitably in a joint activity, and when a large share of the household budget is devoted to household public goods. Another recent study also suggests that microcredit schemes that have a high degree of outreach assistance are most efficient and successful (Bos & Millone, 2015).

While the above studies have been important in providing insightful pioneering evidence, they have generally fallen short of identifying and elaborating the specific contextual determinants of microcredit success or failure. In particular, borrowers’ and lenders’ perspectives on what contextual factors are important for microcredit’s success have not been fully explored. This lacuna could potentially inhibit evidence-based decision-making in the African developmental space more generally, and the microfinance sector in particular. This knowledge and evidence gap could also breed unnecessary speculation. Against this background, this article qualitatively explores the contextual factors that affect the success or failure of microcredit for poverty reduction among women in Ghana. Findings, which are presented and discussed below, suggest that the popular orthodox explanation of effective use of social collateral through the group lending methodology does not fully account for why some microlending programs for poverty reduction among women in Ghana are effective and others are not. Rather, our results suggest that the initial decision-maker on joining a microcredit scheme, type of investment, lending methodology used, business literacy skills of borrowers, borrower’s ability to control loan funds and returns from investment made with borrowed funds, and ability to keep transaction costs low, matter most for how microcredit programs affect women borrowers’ poverty in Ghana. The implications of these findings for policy are discussed below.

Methods

This study forms part of a larger mixed methods study that sought to understand the contextual determinants of microcredit success or failure in Ghana and Kenya between November 2015 and March 2017. The results reported in this article are based on the qualitative component of this larger study in Ghana, which aims to explore the perspectives of various stakeholders on the contextual determinants of microcredit effectiveness among women borrowers. The benefits of qualitative research in understanding the contextual determinants of the success of microcredit have long been acknowledged in literature. For instance, both Mayoux (1998) and Sinha and Matin (1998) think that it is unlikely that existing quantitative methods can realistically assess the impact of women’s access to credit on their empowerment. However, qualitative research, which attempts to provide access to people’s opinions and aspirations, and power relationships, has the potential to help explain how people, places, and events arise in identifiable local contexts, with privileged individual’s lived experiences (Karnieli-Miller, Strier, & Pessach, 2009). The qualitative methods used in this study generated rich, contextually detailed, and valid process data that left the perspectives of research participants minimally altered.

Empirical field research was conducted in 3 of the 10 administrative regional capital cities of Ghana. These were Tamale, Kumasi, and Ho. These capital cities were purposively selected to represent the different parts of the country. Specifically, Tamale was selected to represent the northern part of Ghana; Kumasi was selected to represent the middle part of Ghana; while Ho was chosen to represent the southeastern part of the country.

The microcredit industry in Ghana has varied actors. Based on literature and discussions with key stakeholders in the sector, including the Ghana Association of Microfinance Companies and the Ghana Microfinance Institutions Network, we grouped microcredit institutions (MCIs) into three. These were private-for-profit MCIs, private-not-for-profit MCIs, and state/government-operated microcredit schemes. Based on this broad typology, we selected, in each capital city, one private-for-profit MCI, one private-not-for-profit MCI, and one state/government-operated microcredit scheme (i.e., MASLOC). A total of nine MCIs were, therefore, included in our study. The main participants in our qualitative study were staff of the nine MCIs and their respective women borrowers. Cognizant of the multiplicity of actors in the microcredit sector in Ghana, however, we also interviewed staff of regulatory institutions and apex organizations such as the Ghana Association of Microfinance Companies, the Ghana Microfinance Institutions Network, the Money Lenders Association of Ghana, and the Ghana Co-operative Credit Union Association. In all, there were 146 participants. This comprised 11 participants from MCIs and related organizations, and 135 women borrowers (15 each from the 9 MCIs). Our specific sampling methods are discussed below.

Our sampling and recruitment strategy involved both probability and non-probability sampling procedures. For women borrowers, a simple random sampling procedure was used. This involved a four-stage procedure. First, we obtained a register containing names and personal records of each of the women borrowers from the nine selected MCIs. Second, we listed the names of all the women borrowers in excel. Third, we used a Google-based random number generator to randomly select the required number of participants (15 for each selected MCI) from the pool of names compiled in excel. Finally, we contacted each of the randomly selected women through contact information provided by their respective MCIs. The study was discussed with each randomly selected woman. Where any of the randomly selected women was not available or declined to participate in the study (and there were only five such cases), we repeated the sampling process to get replacement. For those who agreed to take part in the study, they were informed about the purpose of the study and the other women borrowers who were taking part in the study. A date for a focus group interview was then proposed by the researchers, and each woman indicated their availability for the group discussions. Those who were unable to come to the group discussion were individually interviewed at a later date (see data collection methods below).

For the 11 participants from the MCIs and related organizations, a purposive sampling technique was used. Specifically, the selection was based on the participant’s perceived role or knowledge of the subject of study and availability and willingness to take part in the study. Usually, institutional heads were approached by the researchers, and requests were made to interview personnel (mostly loan managers) who were directly involved in managing loans. In few instances, however, institutional heads either volunteered to be interviewed or nominated another person other than the loan manager who the researchers had originally requested. These decisions—as we were told—were largely based on either the absence of a loan manager at the time of the study or the loan manager being relatively new to the organization.

Focus group discussions (FGDs) and in-depth interviews (IDIs) were the main data collection methods. Nine FGDs (one for each category of MCI in the three cities and involving a total of 95 women borrowers) and 40 IDIs were conducted. These were, however, complemented with in-depth case studies of few women borrowers and lenders. In each study city, 3 FGDs were conducted in addition to at least 10 IDIs. Focus groups consisted of 8–12 women, and all discussions were held in places within the city that were proposed by researchers and agreed upon by women. Focus groups were conducted using mixed interview languages depending on the city: English and Twi in Kumasi; English and Dagbani in Tamale; and English and Ewe in Ho. Focus group discussions lasted between 60 and 90 minutes. Generally, group discussions were ended when saturation levels were attained for the main topics of discussion. Saturation was attained on different issues at different points in the discussion and also varied from one FGD to another. Before discussions in all groups, participants’ verbal consents were gained, and the discussions were audio recorded using a digital voice recorder alongside handwritten field notes.

Individual IDIs were also conducted with a total of 40 women borrowers across the three cities who either could not take part in the FGDs or specifically indicated their preference to be interviewed individually. Similar to the FGDs, IDIs were held in places within the city and at times convenient to both women borrowers and the researchers. Also, IDIs were conducted using mixed interview languages similar to the FGDs. Interviews lasted between 20 and 35 minutes, and the interviews were ended when saturation levels were attained for the main topics of discussion. Each participant’s verbal consent was sought and obtained, and the interview was audio recorded using a digital voice recorder in addition to handwritten field notes.

For the focus groups with women borrowers only, and IDIs with women borrowers and staff of MCIs, an open-ended thematic topic guide and question guide, respectively, were designed and used to collect data. While the same themes were covered in each FGD or IDI, the instruments were designed to allow questioning and discussion to flow naturally while permitting the researchers to probe more in depth on certain pertinent issues. The instruments focused primarily on documenting and identifying potential contextual factors that affect effectiveness or ineffectiveness of microcredit for poverty reduction among women from the perspectives of both borrowers and lenders. Specific questions explored included: what contextual factors affect the effective operations of microcredit schemes among women? What would you think are the most important contextual factors that underlie the success or failure of your loan-funded enterprise? How do contextual factors such as the target group, the type of lending model, the presence of regulatory institutions and regulatory supervision, and sociocultural factors impact the poverty reduction benefits of microcredit schemes for women? Do variations in the sociocultural, economic, and microcredit organizational contexts explain why some programs are more successful than others? Other issues explored included the role of social networks among small borrower groups, the importance of active borrower participation in loan management, the role of interest rates, transaction costs, loan repayment schedules, managing borrower default, the role of loan managers and field staff, clients’ needs assessment and redress, gender norms, and business literacy skills among borrowers.

Data Analysis

Following the completion of interviews, the data were thematically analyzed. The data analysis process comprised several steps. To begin with, all tape-recorded interviews were transcribed verbatim in the original interview language. Non-English transcripts were then translated into English by three independent language specialists (one each for Twi, Ewe, and Dagbani). All the authors then read and reviewed the transcripts for overall understanding. This first step was completed by separately summarizing the key points participants made in each transcript. We then exported all transcripts into NVivo 9.0 qualitative data analysis software, where the data were coded both deductively and inductively. As defined by Miles and Huberman (1994) and used in this study, codes are labels, which we assigned to whole or segments of transcripts and interview notes to help catalog key concepts and points participants made during the interview.

We continued coding the data until theoretical saturation was reached (i.e., when no new concepts emerged from further coding of data). Once data coding was completed, we applied the code structure to develop and report themes. Themes in this context represented some level of patterned response or meaning within the data set (Boyatzis, 1998). Following from this, all the themes identified were collated into a thematic framework, which was then used to guide the reporting and discussion of our findings. Finally, we went through all the data segments related to each theme to ensure that individual themes and the thematic framework reflected the data. Necessary refinements were made where needed and appropriate. In many instances, verbatim quotations from interview transcripts were used to illustrate relevant themes. Qualitative responses were also aggregated and presented in a quantitative fashion in some instances to facilitate easy understanding.

Findings and Discussion

The ages of participants in this qualitative study ranged from 21 to 56 years. While all the 11 participants from the MCIs and related organizations were highly educated (the minimum level of education among this group was higher national diploma), the majority of the women borrowers had no formal education. Several of the women were married or living with a partner, while the majority of the women also had between one and four surviving children. The duration of women’s involvement in the various microcredit schemes ranged from 1 to 15 years. Many of the women identified themselves as petty traders.

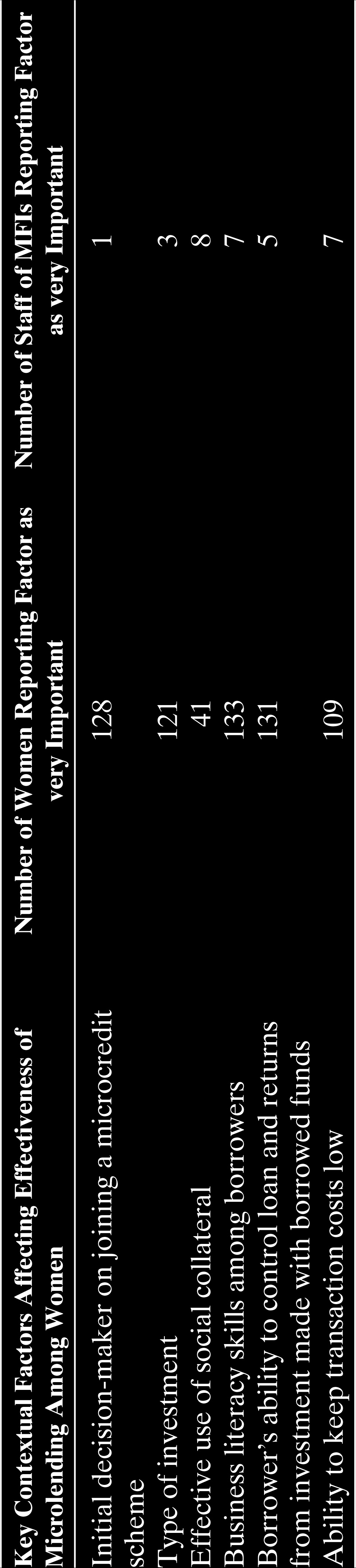

Participants’ perspectives and narratives on contextual factors that affect effectiveness of microcredit for poverty reduction among women in Ghana converged on a number of common themes (see Table 1). A total of six main contextually relevant factors were identified. However, women borrowers and lenders valued the relative importance of each factor differently, and in some instances, some factors that promote lenders’ success directly or indirectly inhibit borrowers’ success. These factors are discussed below in detail.

Contextual Factors Affecting Effectiveness of Microlending Among Women

One of the contextual factors that most women identified as important for success or otherwise of microcredit schemes for poverty reduction among women is the person who makes the initial decision for a woman to join a microcredit scheme. While the issue of the initial decision-maker may be irrelevant in many Western contexts, in many Ghanaian communities where men’s domination over women is strongest within the household, it has a considerable bearing on whether borrowed funds are invested in productive ventures. This issue was particularly highlighted in Tamale, where patriarchal gender norms generally favor men as key decision-makers, both within the public and private sphere.

As one woman in Tamale narrates:

One of the things that negatively affected my loan investment was my husband. You know he was the one who asked me to join and to take the loan. So, when I got the loan, he asked me to give part to him to repair his bicycle and pay other debts. I couldn’t say no…because he is the head of the house and I had no option. Because of this, it is hard for me to make good profit and pay the interest since the amount left was very small. (Borrower, IDI, Tamale)

Similar accounts were given in Ho and Kumasi, although women in Kumasi appeared to be less constrained by patriarchal gender norms partly because matriarchy is the dominant sociocultural organizational ideology in Kumasi. For example:

One thing I think is important is the person making the initial decision. I say this because I know some women whose husbands asked them to join and collect the money…so as soon as they received the loan, their husbands took part of the money…it became difficult for such women to make profitable investment. (Borrower, FGD, Kumasi) What my sister is saying is really true…but for me personally, I didn’t have such issues…I made the decision myself and so my husband could not ask me for any money unless I voluntarily gave him part. (Borrower, FGD, Kumasi)

While several women reported the importance of initial decision-makers, this did not appear relevant to many of the staff of the nine MFIs studied. Only one loan manager in Ho acknowledged this issue.

I think a key issue we have realized is the person asking the woman to join. What we have realized is that women who decide to join on their own with the consent of their husbands do better. Those who are either asked by their husbands to join or do not receive the support of their husbands always have problems managing the loan and paying the interest. (Lender, IDI, Ho)

Taken together, women’s collective and individual accounts here suggested that the benefits to be had from access to microcredit are likely to be better if women themselves made the decision to join and receive loans. This is particularly relevant in contexts where gender norms disproportionately favor men as household heads, decision-makers, and controllers of household resources. In such contexts, it is critical that efforts are made to understand what drives women to join microcredit schemes before loans are granted. This is important for preventing both loan fungibility and indebtedness of women.

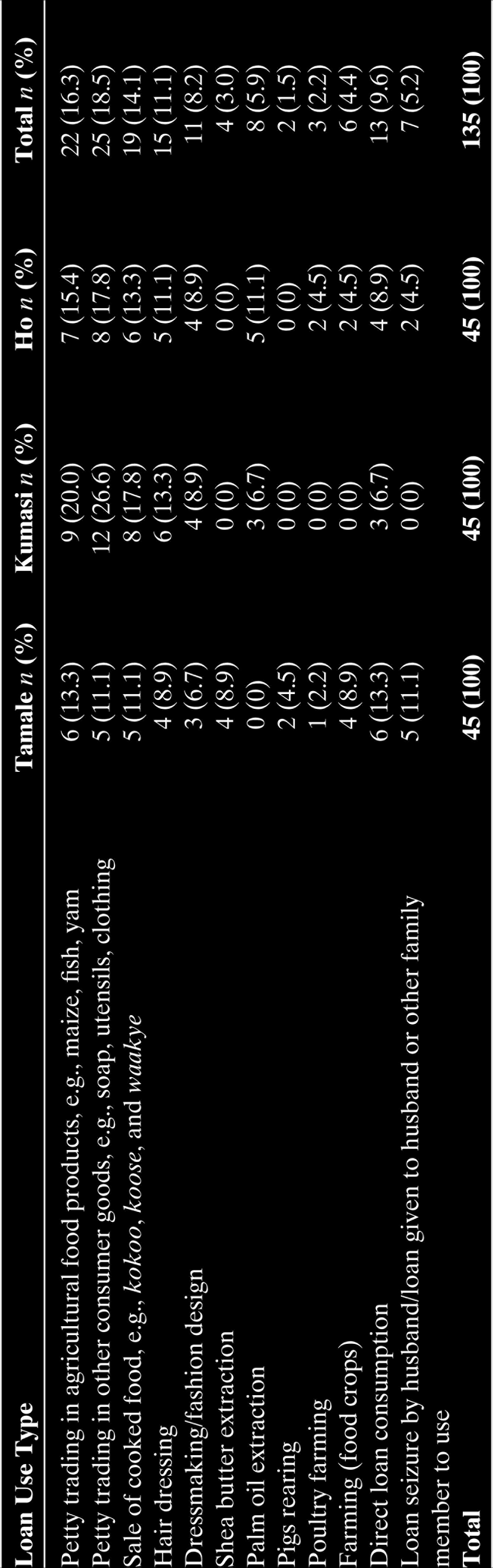

But it is not only initial decision-maker alone who determines whether women benefit from access to microcredit. In addition, the type of investment borrowed funds are put to was reported to determine whether borrowers will succeed or fail. Table 2 shows the patterns of loan utilization among the 135 women borrowers interviewed. Most women borrowers invested their loan funds in 1 of 12 different economic activities (see Table 2). While this is very positive, further analysis of the data showed a number of problematic issues.

Loan Investment Patterns

First, about 14.8 percent of the women interviewed lost their loan funds to either direct consumption or seizure by husband and/or another family member. Several narratives were given about how loan funds were used to meet immediate household needs like purchase of food and medicine, and payment of children’s school fees. Several of these women came from Tamale, whereas noted earlier, male dominance is rife. While using loan funds for direct consumption is a form of benefit, it was widely reported that losing the initial loan capital either through direct consumption or seizure by male partners often initiates a process of dispossession and indebtedness that results in socioeconomic disempowerment as many such women struggle to pay the interest on their loans. This result is indeed consistent with previous research in Ghana, where a substantial number of women borrowers used their loan funds for purposes other than investment in income-generating activities, and where such women were found to struggle to repay their loans (Ganle et al., 2015). In terms of policy implications, our findings here would suggest that microcredit schemes that are targeted at women already engaged in some business venture stand a better chance of success than those who seek to create entirely new enterprises.

Second, most women who invested their loan funds in one form of income generating activity or the other invested in activities that reportedly yielded little profit.

My problem is that the profit I make is so small…and also because I sell vegetables in the market, sometimes they can all go bad because of their perishable nature, and this can create problems for me. (Borrower, FGD, Kumasi)

Generally, most women and few of the loan staff interviewed agreed that for women to benefit from microcredit, they ought to be investing in income generating activities that are profitable.

I think the type of investment women engage in matters … the investment must be profitable, otherwise how will they pay the interest. (Lender, IDI, Tamale)

While there is widespread recognition that successful microcredit schemes for women are those who are driven by profitable individual investments, the data from our qualitative study suggest many women indeed struggle to find highly profitable investment in practice. Discussions with women borrowers suggested that male dominance in the local economic sphere often push many women into less profitable income generating activities. Some women also reported that they invested their loan funds in such low-profit-earning activities because of the small size of the loan they received. Interviews with both women and lenders suggested that loan managers, especially government and private not-for-profit ones, rarely pay attention to whether borrowers have profitable enterprises into which loan funds may be invested. Rather, the focus is on increasing clientele base.

While a focus on greater outreach means that many more women are likely to benefit from these microcredit schemes, the fact that several women are losing their loans through direct consumption or struggle to find profitable ventures to invest loan funds does raise questions about the prospects of borrowers realistically raising sufficient cash to pay the interest on loans. It also does suggest that perhaps many MFIs do not adequately appreciate what women’s access to microcredit can do or not do in a context where economic opportunities for women are limited and where women face other economic necessities such as poverty and hunger (Ganle et al., 2015).

Another contextual determinant relates to the type of lending methodology an MFI adopts to lend money to women. Among the MFIs we studied, their lending methodologies are generally modeled around the Grameen Bank approach, where no individual collateral proprietary arrangements are required, and where lending is group-based and where MFIs rely on what has been described as the joint-liability condition (Rooyen et al., 2012). Under this condition, no group member is allowed to borrow again in the event of any group member defaulting, and group members are also collectively responsible for paying up the debt of any single group member in case of default (Ganle et al., 2015). This contrasts many formal sector credit arrangements, which have traditionally been organized around two principles: loan is given only if a borrower is considered to have adequate future earnings to permit loan repayment, and conditional proprietary rights created on the borrower’s assets in the form of collateral (Banerjee, 2013).

Majority of the MFIs studied (8 out of 11) favored the group lending approach because it supposedly limited high-risk lending by placing the responsibility on group members to self-select only credit-worthy individuals, thereby allowing MFIs to both address the problem of information asymmetry often common in individual-based lending schemes, and to recover loans at minimum costs.

We prefer the group lending approach … it is the real secret behind our organization’s success. (Lender, IDI, Kumasi)

We largely use the group lending methods … it allows us to take advantage of group solidarity or social collateral so that group members actually do the work of getting their members to pay their loan interest on time. (Lender, IDI, Ho)

However, many women borrowers expressed discontent with many aspects of this lending approach, arguing that it has often inhibited their success. This was reflected in the relatively low number of women (see Table 1) who mentioned effective use of social collateral as an important determinant of their success. This argument was particularly common among borrowers who had joined microcredit schemes for relatively longer periods.

The problem I have is this group thing … I have joined the scheme for long so I don’t see why I need a group to access the loan. I believe I can pay back my loan with the interest, so why must my progress depend on whether other group members are able to pay? (Borrower, IDI, Tamale)

Personally, I prefer the individual one…my business suffered some time ago when one of us had problems paying. In fact, some friends of mine left the group to join another company that gave individual loans. (Borrower, FGD, Kumasi).

These concerns were complicated by the exigencies of contemporary urban living in Ghana, where poor personalized addressing systems, combined with individual mobility, often create information asymmetry even among group members.

In this city, it is really hard to say that you know people very well. People also change their living places…and because the addressing system is not good, how will you know where a group member has moved to if they take the loan and decide to relocate to another place? This is why the group thing is not good for some of us. (Borrower, IDI, Kumasi)

Indeed, some of the private-for-profit MFIs studied reported how they initially started with the groups but found it problematic.

The issue of lending methodology is important. Most MFIs think the group approach is better. But our experience is that, it is rather the individual lending method that helps both us and women borrowers to succeed. We used to do group lending but now we focus on individuals as long as we are satisfied that they can pay back the loan. We only do group lending in rural areas where social relations are still very tight. That probably explains much of our success today. (Lender, IDI, Kumasi)

Clearly, there is disagreement not just between borrowers and lenders but also among lenders as well as among borrowers about which lending methodology is appropriate in helping women maximize the potential gains of microcredit. This would suggest that rather than just following popular orthodoxy, there is a need for MFIs in our study context to be more innovative and dynamic in their lending methodology, such that different lending approaches are chosen to suit the needs and capability of clients.

For instance, an individual lending approach could be applied to borrowers who have demonstrated capacity to independently manage their loans and pay the required interest and who may prefer such an individualized system. However, group methods could be applied to starters who may have a higher chance of defaulting in loan repayment due to difficulties in managing and paying off their loans. Similarly, and as shown above, group lending may also be appropriate in rural or contexts where social relations and networks are high compared to urban settings where these relations are mostly fragmented. Such a targeted approach stands a better chance of addressing individual borrowers’ needs while potentially maximizing investment returns for both lenders and borrowers.

The business literacy skill, especially financial literacy and education of borrowers, is one of the factors that was identified by both lenders and borrowers in our study.

MFIs must understand that it is a waste to lend money to women who have no idea how to do basic book keeping or even calculate profit and loss. So for us, before we give out loans, we train all borrowers in basic loan management and book keeping. This is a critical component of our business and I believe any microcredit scheme that aims to be sustainable must do this. (Lender, IDI, Ho)

I think one thing that has helped me personally is the training they gave me before I received the loan. It really helped me to manage my loan and business…I think I would not have succeeded without this training. (Borrower, FGD, Ho)

Generally, our discussions with women borrowers, lenders, and regulators suggest that it makes business sense in contexts such as Ghana, where both general and financial literacy among women are relatively low to invest in developing the business management capacities of borrowers before loans are granted. While many participants agreed that this potentially increases the cost of borrowing to poor women, it was equally acknowledged that the long-term gain for both lenders and women borrowers are much greater. Therefore, it is critical that in contexts such as Ghana, microcredit operators actively assess the financial literacy of their clientele and develop appropriate and supportive financial literacy and investment education programs to help borrowers profitably manage their loan-funded enterprises.

Another determinant is whether women borrowers are able to exercise control over their loans and returns from investment made with borrowed funds. Generally, the MFIs we studied grant women credit based on assumptions that women will exercise full control over the loan and loan-funded enterprises. This assumption, however, does not apply to all women borrowers. Similar to previous research in Ghana (Ganle et al., 2015), we found that several women are unable to exercise full control over both the initial loan capital and funded enterprises. The issue of ownership and control of loan-funded enterprises was particularly pronounced in Tamale and Ho.

I believe the loan is helpful. The only issue is that it is largely beneficial for women who are able to control the loan funds. I say this because not all of us who take the loan can decide on our own how to use it…I personally do not control what the loan should be used for…I have to consult with my family… my husband usually controls things and determines how I should use it. (Borrower, IDI, Tamale)

Focus group discussions with women and IDIs with staff of not-for-profit MFIs revealed that although women receive the loans and therefore bear all liabilities, decisions about how these loans are used and who might exercise control, usually occur within the household economy, where decisions including economic decisions are made and power is exercised. In this way, it was widely reported that some women exercised very little control over the loans they receive and the enterprises they fund with the loans. Rather, their husbands or male partners usually control the loans and funded enterprises either fully or partially.

Several narrative accounts from FGDs with women as well as IDIs with loan managers suggested that some women are unable to exercise control over how their loan funds are utilized precisely because either their husbands or other male relations in the household made the initial decision for such women to join and receive the loan, or existing patriarchal and sociocultural norms often make it hard for women to own or exercise control over assets. In particular, married women are generally viewed as the property of their husbands while unmarried daughters belong to their fathers in patriarchal contexts like Tamale and Ho. This explains why husbands feel entitled to control loan funds once the money enters the household economy.

What we have realized is that if the husband made the initial decision for the woman to join, they usually want to control the money as soon as the women receive it. But this often does not help the women in their investments. (Lender, IDI, Ho)

This situation is, however, less pronounced in Kumasi, whereas reported earlier, matriarchy provides the dominant sociopolitical organizational framework for household and community level decision-making. In such a context, some women rather talked about voluntarily handing over their loan funds to their male partners. Such voluntary ceding of the right to manage loan funds was reported to be underlined by beliefs that men are better handlers or managers of monetary transactions.

Indeed, Todd (1995) has brilliantly provided a logical justification of why some women may hand over loan funds to their husbands. Todd argues that since men’s enterprises are often more profitable than women’s, investing loan funds in men’s activities may make more business sense. Although this could potentially be a good rational business strategy, many of the participants in our study admitted that such women often do not benefit much from accessing microcredit. Consequently, both women and lenders underscored the need for microcredit schemes to pay attention to how much control women have over personal decisions within the domestic sphere before granting loans. While this could potentially further disfavor women who already have weak bargaining power at the household level, our qualitative narrative accounts of women and lenders suggested that lending to women who already have full or significant control over some essential household level decisions and resources, including their loans and proceeds from enterprises funded with their loans, was more likely to be beneficial and successful.

The ability of both lenders and borrowers to keep transaction costs to the minimum was also identified as an important determinant of effective microlending.

Like any business, one of the important things we do at our organization is put emphasis on low transaction cost. As soon as our cost of transaction goes up, it has trickle down effects … we pass it on to the borrowers by way of interest, and this creates profitability and loan repayment problems … sustainability even becomes a big challenge … so every microcredit scheme must watch the cost of lending money to borrowers. (Lender, IDI, Kumasi)

In MASLOC, one of the key challenges we had was high operational cost … we spent a lot of resources chasing women, especially those who became insolvent, to pay. So though our average loan repayment rate was about 90-95%, sometimes the cost of recovering the loan was even more than the recovered loan funds. This really created sustainability challenges for us, and central government had to come in and subsidize our operations. But now we have learnt to keep cost down. So, I think ability to lower cost of lending is critical to the success of any microcredit scheme. (Lender, IDI, Ho)

Women borrowers also reported how important it is for loan-funded enterprises to keep cost low.

I agree with what my sister said… One thing is that, if you do not know how to reduce costs, it will be difficult for you to make profit and repay your loan. I say this because of my own experiences. When I joined the credit scheme and started my Kokoo and koose business, I was making huge losses. I didn’t use to plan well… I use to go to the market several times just to buy all the things I needed to prepare the kokoo. Later on when I sat down and thought about the issue, I realized I was spending a lot of money on transport. So I decided that I will plan well by listing all the things I needed, then go to the market and buy everything at once. When I started doing that, then I realized I was reducing cost … and that really helped. Now I even have farmers in the villages who bring me the millet to buy … it is much cheaper when you buy directly from the village farmers. So I think it is important to reduce your business costs, otherwise it will collapse. (Borrower, FGD, Tamale)

Thus, among both lenders and borrowers, keeping lending and/or production costs low was deemed necessary for reaping the full benefits of microcredit. While the issue of reducing lending and production costs has always been an important consideration for formal and/or large firms, participants in this study argued that it was even more important for small businesses funded through microcredit schemes to be extremely cost-effective. This is precisely so not only because interest rates are typically higher and repayment periods are also shorter but also because most microcredit-funded enterprises are typically organized as family businesses. Therefore, the potential for inefficiencies and cost-ineffectiveness is higher than formal and large-scale enterprises.

Conclusion and Policy Implications

In many contexts in sub-Saharan Africa, the extension of microcredit to women has been and is still being promoted as a means to reduce women’s poverty and empower them. However, there is growing evidence that poverty reduction and empowerment are not automatic outcomes of women’s access to microcredit, particularly in contexts such as Ghana where gender-based discrimination and power differentials are deeply rooted in the social-structural organization of these societies, and where women still face considerable disadvantages relative to men due to less education, low bargaining power, a greater unpaid domestic work burden, and limited business networks and opportunities. Therefore, the need to focus on examining and identifying the contextually relevant determinants of microcredit success is significant.

In this study, our aim was to explore the contextual factors that affect the success or failure of microcredit for poverty reduction among women in Ghana based on the perspectives of women borrowers and lenders. Our findings show that the popular orthodox explanation of effective use of social collateral through the group lending methodology does not fully account for why some microlending programs for poverty reduction among women in Ghana are effective and others are not. Rather, our results suggest that the initial decision to join a microcredit scheme, the type of investment, the business literacy skills of borrowers, the borrower’s ability to control loan funds and returns from investment made with borrowed funds, and the ability to keep transaction costs low matter most for how microcredit programs affect women borrowers’ poverty in Ghana.

Apart from the fact that our results highlight important contextual factors that both loan scheme managers and borrowers must pay attention to, the results also show how borrowers’ perspectives on relevant contextual factors diverged and converged with those of lenders’ in significantly interesting ways. With regard to convergence, for example, most women and lenders agreed on the need to develop the business literacy skills of credit recipients in order to help borrowers effectively manage loan funds. Similarly, there is a convergence of opinion on the need for both lenders and borrowers to keep business and transaction costs low in order to both sustain microcredit schemes and loan-funded enterprises.

There is also a strong convergence of opinion about the fact that the poverty reduction benefits of microcredit among women are likely to be minimal unless women have significant bargaining power within the domestic economy to exercise meaningful control, both over the initial loan capital and the proceeds/returns from loan-funded enterprises. Convergence in terms of borrowers’ and lenders’ perspectives on the contextual determinants of microcredit success among women clearly provides lessons and opportunities for both loan managers and recipients to take the necessary remedial actions to bring about an improvement in their business operations in Ghana. Indeed, the contextual factors on which the ideas of both women and lenders strongly converged should be the starting point of real solutions to addressing some of the problems affecting the operation of microcredit schemes for women in Ghana and in other similar contexts.

With regard to divergence, many women borrowers believed that the initial decision-maker in relation to access to credit plays an important role in the success or failure of microcredit schemes among women. Fewer of the microcredit scheme personnel we interviewed, however, thought this was an important contextual factor. Similarly, whereas many of the loan managers preferred the group lending methodology, several women decried it and expressed their preference for an individual lending approach. Also, while few lenders paid attention to the type of investment women put their loan funds into, many women underscored the importance of having a profitable economic venture in which to invest loan funds. The seeming divergence in perspectives in terms of what contextual factors are relevant in maximizing the benefits of microlending to women for poverty reduction purposes points to a potential for conflict and policy failure. At best, our discussion here suggests that what loan managers may sometimes value as important to the success of loan recipients may actually be less valued by loan recipients. At worse, the discussion here suggests that policies and strategies that may benefit loan managers in terms of loan repayment and profitability (e.g., group lending) may be detrimental to the success of borrowers.

Therefore, it is important that before credit is extended to individual women or groups, loan managers should undertake a situational analysis of the borrowers to identify potential contextual factors that could support or inhibit effective use and management of loan funds. As shown above, in a context where the initial decision to enroll in a microcredit scheme is not made by a woman or where the woman has little control over initial loan capital and returns from loan-funded investment, it is a singularly poor context to give out credit to women to start new businesses.

In sum, our study provides evidence that illustrates not only the impact of any microcredit scheme depends on the socioeconomic and cultural contexts in which it is implemented but also how the specific ways certain contextual factors operate to either empower or impoverish women loan recipients. While access to cheap credit may be all that is needed on the way out of poverty for many women in contexts where profitable investments opportunities exist, where gender-based discrimination against women is less, and where entrepreneurial skills among women are relatively developed, a good number of borrowers could also be disempowered by accessing microcredit if relevant contextual factors similar to those identified in this study are not considered.

Footnotes

Acknowledgements

The study reported in this article was wholly funded through an Association of African Universities’ Policy Relevant Grant, made jointly to researchers from the Kwame Nkrumah University of Science and Technology, Ghana and Kenyatta University, Kenya. We are grateful to the Association of African Universities for funding our study. We also thank women borrowers and staff of all the MFIs and related regulatory and apex organizations interviewed in this study.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The study was fully funded through an Association of African Universities’ Policy Relevant Grant.