Abstract

This article presents a process-model for the abandonment of a practice. This complements earlier research on adoption and abandonment by allowing for fluctuations in the level of commitment across time and by demonstrating the persistent role for both institutional pressure and performance-based concerns on the maintenance of a practice. It also provides a novel means for identifying differences in the method of abandonment through the introduction of a concept of decommitment. Further, it helps resolve the question of how firms respond when faced with conflicting internal and external evidence of the success of an adopted practice. Using the divestiture of unrelated business segments by 100 U.S. firms between 1970–96, I estimate post-adoption commitment to a practice and the likelihood of a given firm decommitting. I find that treating abandonment as a process clarifies the evolving role of institutional and performance-based concerns and helps identify when a given firm is more subject to either source of pressure. The implications of this approach and these findings for current research on resistance to adoption and de-institutionalization are explored in the conclusion.

Keywords

Introduction

There is an increasing interest in the question of how practices evolve after the initial wave of adoption (Fiss, Kennedy, & Davis, 2012; Terlaak & Gong, 2008; Westphal & Zajac, 2001; Zeitz, Mittal, & McAulay, 1999). This includes research on diffusion that considers the influence of resistance (Fiss & Zajac, 2004; Marquis & Lounsbury, 2007), and research in institutional theory on the effect of practice variations (Ansari, Fiss, & Zajac, 2010; Jonsson, 2009; Okhmatovskiy & David, 2012) or the prevalence of symbolic adopters (Park, Sine, & Tolbert, 2011; Weaver, Trevino, & Cochran, 1999). However, because these investigations focus upon the early stages of institutionalization, we still lack a clear response to Oliver’s (1992) call for investigations into the conditions under which an institutionalized practice collapses.

The prevailing explanations reflect the belief that when there is uncertainty institutional pressure stimulates adoption (DiMaggio & Powell, 1983) but effectiveness determines abandonment (Davis, Diekmann, & Tinsley, 1994; Rao, Greve, & Davis, 2001). Adoption is therefore driven by “social proof” and abandonment by the accumulation of evidence (Greve, 1995, 2011a). These findings treat managers as instrumentally-rational actors whose susceptibility to normative pressure declines as the quality of their information on the practice improves (Abrahamson & Fairchild, 1999). Under these assumptions, effective practices may fail to spread, but ineffective practices cannot persist as any normative pressure to maintain a practice loses influence when ineffectiveness becomes evident.

Despite the cogency of this argument, managers often exhibit an inability to abandon a practice they adopted. This can be seen in cases as disparate as NFL coaches making 4th down decisions (Romer, 2006) to hedge fund managers who discount the positive performance of deviant practices to avoid switching (Jonsson, 2009). In each setting the actors have strong incentives to maximize their returns and clear evidence of how to do so, but they cannot escape the pressure to act as expected. Staw (1981, 1997) explains that these “escalations of commitment” often occur because the initial returns to a practice are rarely unambiguous and negative early returns are as likely to be seen as evidence of insufficient commitment as they are of excessive commitment. But even in situations where the returns are unambiguously negative, social pressure can enforce commitment (Teger, 1980).

Research at the organizational-level provides comparable evidence that practice abandonment does not indicate the triumph of rationality over institutional pressure. First, studies of decoupled adoption find that institutional pressure can increase over time, even for firms that adopted symbolically to avoid performance decline, leading to “recoupled” adoption (Hallett, 2010). Second, because organizations adopt practices for a variety of reasons (Green, 2004), performance changes may not be interpreted as challenging the practice. Davis et al. (1994) find that institutional pressure remains so influential that practices die not because adopters abandon the inefficient ones, but because adopters inability to abandon them begets the end of the organization. These responses point to a central tension in accounts of the abandonment of a practice between the assumption that institutional pressure is strong and persists even when challenged by evidence of ineffectiveness, and the assumption that it is strong under initial uncertainty, but weakens rapidly as evidence accumulates.

A possible resolution exists in redefining the abandonment of a practice as a process rather than single act. While research on the diffusion of innovations and practices acknowledges variations in the degrees and kind of adoption (Ansari et al., 2010; Fiss et al., 2012; Jonsson, 2009; Terlaak & Gong, 2008; Westphal & Zajac, 2001; Zeitz et al., 1999), abandonment, when studied at all, is assessed as a one-time act (Burns & Wholey, 1993; Greve, 1995). I propose that re-characterizing abandonment as a process rather than a moment helps address two of the main issues that constrain past efforts to explain the decline of a practice.

First, this approach allows us to study the changing influence, and interaction, of normative pressure and practice efficiency. Rather than treating one as subordinate to the other, or both as locked into monotonic patterns, treating abandonment as a process allows the strength of each factor to vary across time and across organizations. Most importantly, this approach recognizes the potential for contestation that arises when an institutionalized practice collapses and it allows us to estimate the conditions under which performance concerns reduce normative pressure and when normative pressure remains resolute.

Second, it allows for the fact that managerial interest in abandoning may fluctuate with time. This permits clearer distinctions between firms that adopt symbolically and those that adopt to gather information. It also allows for the possibility that managers navigate tensions between social and performance-based factors by reducing commitment without abandoning. In general, redefining abandonment as a process accepts that the transition from excited to rational is not smooth, nor is information always clear or consistent. Instead, managers engage in a continual process of sense-making, where both the manner in which they interpret information and the degree of pressure it exerts evolve. In contrast, by focusing on adoption and then abandonment individually most past research fails to address the space between these points and therefore impedes attempts to understand how a practice evolves once adopted. The object of this article is to introduce a multi-stage theory of abandonment and to estimate whether the relevance of institutional and performance-based factors differ between the penultimate decision (to decommit) and the final act (to abandon).

Specifically, I use the adoption and abandonment of unrelated diversification by 100 U.S. firms between 1970–96 to estimate the role of social, organizational, and financial factors on the decision to abandon a practice. This provides a comparison to past studies that have also used forms of diversification to examine the adoption or abandonment of a practice (Davis et al., 1994; Fligstein, 1985; Haveman, 1993; Palmer, Friedland, Devereaux Jennings, & Powers, 1987; Zuckerman, 2000) while also providing a practice that was widely adopted and abandoned across multiple industries between 1970–96.

Using Heckman models with selection effects to estimate both the degree of commitment and the likelihood of decommitment, I find evidence that abandonment is driven by a combination of institutional and financial pressure but that the influence of either factor is moderated by the features of the organization. Specifically, I find that recent adopters are particularly sensitive to the behavior of their peers, that firms operating below the industry average are more sensitive to both performance changes and peer behavior, and that the size of the organization determines the direction of its response. I also find that when the two principal sources of information on a new practice conflict, organizations are quick to decommit but slow to abandon. These results provide evidence in support of the claim that treating abandonment as a process allows us to more accurately identify how organizations shed institutionalized practices and contribute to the collapse of a popular practice.

These findings offer several contributions to extant research on the diffusion of practices and institutional theory. First, the findings offer a way to reconcile the frequent expectation that institutional factors influence abandonment with the lack of evidence for their role in the final act (Greve, 1995; Rao et al., 2001). Treating abandonment as a process reveals the persistent role of both institutional pressure and performance on the decision to reduce commitment that precedes abandonment. Second, it extends the recent stream of research on the significance of variations in an adopted practice (Ansari, Reinecke, & Spaan, 2014; Fiss et al., 2012; Westphal, Gulati, & Shortell, 1997). Previously, these studies focused on the resilience of institutions; however, the findings here suggest that variations in commitment—both initially and subsequently—may also explain the decline of a practice. In addition, the model proposed here offers a method to explore whether initial variations influence subsequent patterns of commitment or abandonment.

Finally, the findings suggest the possibility of decoupled abandonment, where firms adopt in earnest, but then maintain only a vestige as a way to symbolize compliance. This is substantively different from the notion of decoupling at adoption, where the intent is to resist. Here firms initially act in good faith but find themselves pressured into maintaining elements of a practice they want to abandon. These contributions are explored more fully in the discussion.

The Value of Decommitment

Currently, in place of an account of the process of abandonment, we have studies of: the creation of new organizational routines (Dobbin & Sutton, 1998), their adoption (David & Strang, 2006; Tolbert & Zucker, 1983), and their abandonment (Davis et al., 1994). These studies focus on one act at a time, examining each action independently rather than as part of a process. Greve (1995) details the replacement of one radio station format with another, but does not examine why or for how long this new format persists. Davis et al. (1994) explain the de-institutionalization of diversification but do not compare these factors to those that first brought about diversification. Only theoretical accounts offering a more comprehensive view suggest a complicated process where rationales evolve after the practice is adopted (Abrahamson & Fairchild, 1999). However, even these more comprehensive accounts are limited by their characterization of a lifecycle as two extreme events with nothing in between.

Consistent with this, empirical studies treat abandonment as a simple binary function—organizations either maintain the practice or they do not (Burns & Wholey, 1993; Greve, 1995; Rao et al., 2001). Yet it is not hard to imagine situations in which abandonment occurs as a lengthy process. For instance, Scott Paper (Figure 1) spent 12 years pursuing forms of unrelated diversification before deciding, in 1981, to shift tactics. But overcoming the resistance of managers committed to the old plan, finding buyers for the assets the company sought to divest, and persuading analysts and shareholders that this was a proactive and not reactive decision took four years. Defining “abandonment” as solely the final sale in 1985 distorts the portrait of what occurred.

The trajectory of Scott Paper.

Thus far there has been little interest in whether an organization abandons quickly or slowly, in small steps or all at once, in how their level of commitment varied before abandonment. The focus has been on when or whether they abandon and not on how. But how is of central importance to managers and deserves greater attention from scholars. In particular because how an organization abandons often explains both whether and when they do so. For example, empirical studies of abandonment reinforce the claim that it is a rational process, as opposed to the excited process of adoption. These claims are based on the finding that declining performance, not the action of similar firms, predicts final abandonment. But what if a firm begins abandoning before their performance declines? What if the decision to abandon precipitates a decline in performance? We’d still find that declining performance precedes the final abandonment, but the causality would be reversed. At present we can predict the act, but not explain the mechanism; full understanding requires a model of the process.

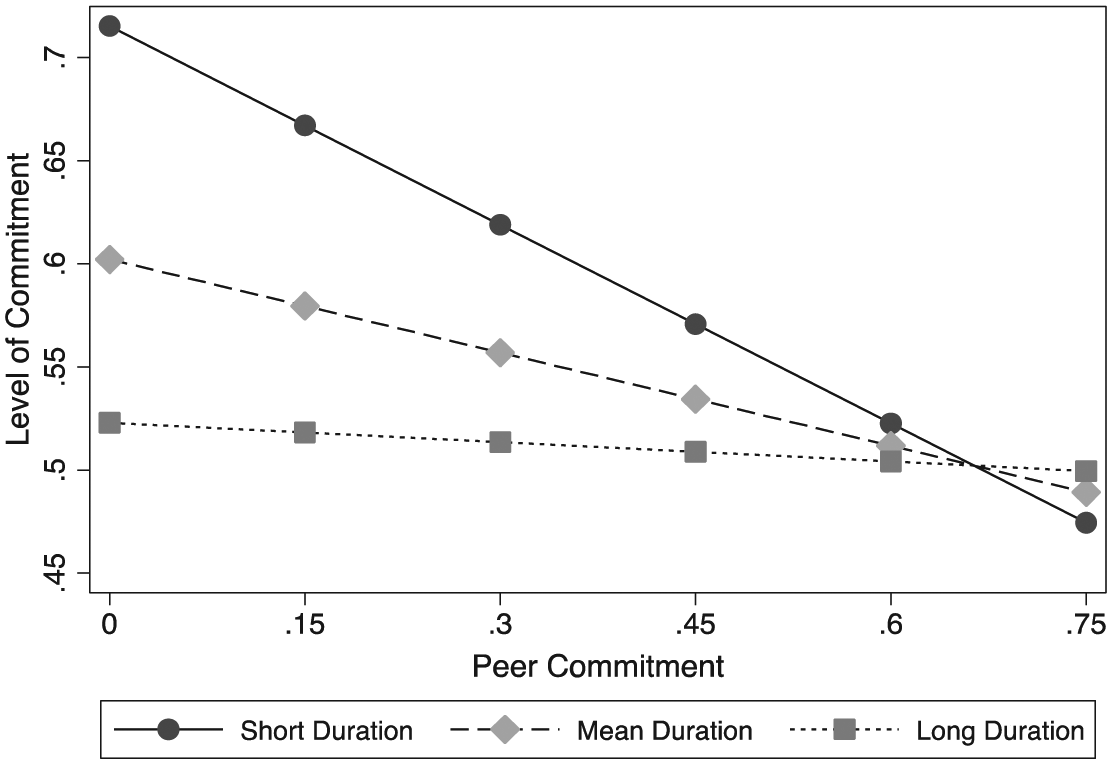

Consider the history of two diversified firms (Figure 2). A conventional account would indicate solely that General Foods abandoned faster. But the significance of this finding is difficult to interpret; faster could reflect managerial hesitancy to commit or the failure of a full-scale commitment. A study that only focuses upon the end date cannot identify which of these contradictory factors motivated the decision. It treats Tenneco’s gradual increase and decrease as no different than General Foods’ constant commitment and abrupt end. Identifying the point of decommitment and assessing variations in the level of commitment help establish the different paths the two firms took to reach the same decision and the factors that precipitated it.

Comparison of two commitment trajectories.

The benefits to theory parallel the methodological gains. First, this approach builds on the growing number of inquiries into why adopted practices vary (Ansari et al., 2010; Boxenbaum & Jonsson, 2008; Colyvas & Jonsson, 2011). These studies document the role of competing institutional logics (Marquis & Lounsbury, 2007), cultural differences (Fiss & Zajac, 2004), managerial opposition (Jonsson, 2009), and the availability of alternative schema (Okhmatovskiy & David, 2012) in predicting the form of adoption. However, because these studies focus on variations that occur at t0, they leave unanswered how those practices become more or less varied by tn. A study of subsequent variation allows us to connect these initial deviations to the persistence or decline of a practice to assess the consequence of deviance rather than its likelihood. At present, we cannot distinguish under which conditions these initial variations collapse from those in which the variations contribute to the practice’s collapse.

The significance of this is clearest if we consider a classic question in institutional theory (Oliver, 1992): what explains the decline of an institutionalized practice? Two of the most compelling answers are that decline is caused by resistance from actors pressured to adopt (Marquis & Lounsbury, 2007) and that it is caused by the ineffectiveness of the practice (Davis et al., 1994). Both potential answers benefit from reimagining abandonment as a process.

A focus on initial variations implies that it is the decision to decouple that merits attention and leads to the assumption that this decoupling weakens norms and hastens collapse. But it is hard to distinguish between decoupling and testing, and firms that appear to decouple may in reality soon surpass the commitment of more “genuine” adopters. In this situation, apparent decoupling would not instigate the collapse of a practice but may even serve to reinforce it. A focus upon performance assumes that the rationale and degree of adoption are ancillary to evidence of effectiveness. But this is hard to extend to settings where performance did not drive adoption or where the performance data is contested.

For example, in Maguire and Hardy’s (2009) study of the abandonment of DDT, we see that interest in abandoning DDT fluctuated across time and within subfields. Abandonment cannot be understood in this case without examining the development of an oppositional consensus that preceded the act. In essence, for DDT, abandonment was just the final stage in which the successful problematization of chemical pesticides was the equally critical prior moment. Studies of the rise of nouvelle cuisine in France (Rao, Monin, & Durand, 2003) offer similar evidence of the importance of these prior erosions of a practice in understanding the decline of haute cuisine. Reimagining adoption as a process of fluctuating commitment that eventually ends rather than merely two points with a space between them allows us to test these alternatives and to more precisely capture the effect of social and performance-based factors on the path of a practice.

Theory and Hypothesis

If abandonment is a process more than a moment, the question becomes: what determines the shape of the process? The conventional answer, offered by Abrahamson and Fairchild (1999), is that while adoption of a practice is irrational and excited, driven by normative pressure like any fad, abandonment occurs as a reasoned response to accumulated evidence. Therefore, we would expect any abandonment process to be predominantly influenced by the availability of new information on the costs and benefit of the practice. This assumption is reinforced by multiple studies (Ahmadjian & Robinson, 2001; Brauer & Wiersema, 2012; Davis et al., 1994; Greve, 1995) that find both inferred and direct information increase the likelihood of abandonment across a wide range of organizations. The belief in a rational process of abandonment suggests a null where there is little distinction between a point of decommitment and a subsequent point of abandonment. Once the practice is recognized as deleterious to the operation of the organization both decommitment and abandonment should follow rapidly, there is no reason to assume any motivation to decommit would not also motivate abandonment.

The two central forces in abandonment are therefore (1) peer influence, through external pressure to imitate similar organizations or from vicarious learning, and (2) an organization’s direct experience. Independently, the expectations are not particularly surprising, evidence of declining performance along either dimension should drive firms to both decommit and abandon. However, there is reason to question the universality of these claims as timing, organizational features, and the potential for contradictory information moderate these general effects and produce distinct paths to abandonment. I will briefly highlight the rationale for an indirect relationship between performance, peer commitment, and firm abandonment before investigating the moderating factors that create variations in the process.

Information and abandonment

One of the central findings of research on the diffusion of practices is that experiencing performance declines motivates the replacement of a practice. Given that managers are evaluated based upon performance goals, and organizations are subjected to countless forms of performance assessment, it is not surprising that managers are sensitive to evidence of decline. For instance, in a study of radio format change, Greve (1998) shows that it is failure to meet performance aspirations that motivates mangers to adopt new practices. Similarly, Palmer et al. (1987) found that the adoption of the multi-divisional form was driven by the belief that performance was lagging. Even if the organization is not presently struggling, Kraatz (1998) finds that increased uncertainty about future performance can drive organizations to adopt new practices. Across nearly all studies of the collapse of a practice the central story revolves around internal assessments of performance. Therefore, evidence of diminished performance should uniformly predict an increase in the likelihood of decommitment, the rate of decommitment, and the likelihood of abandonment.

However, because claims about the performance of a unit are often contested and ambiguous it can take time before firms have the confidence that what they see is evidence and not an aberration. As a result, organizations often examine the behavior of related organizations (similar in size and focus) to gain complementary evidence of costs and benefits. This information can function, as in the case of Rogers’ (1962) seminal study on the adoption of hybrid corn, as vicarious learning. Or, as in the evolution of physician’s prescribing behavior (Coleman, Katz, & Menzel, 1957), it can occur in imitation of higher-status actors. Irrespective of whether the mechanism is functional—managers act upon new data—or ceremonial—they mimic industry leaders, evidence of diminution in commitment from similar organizations should generate pressure on the focal organizations to reduce their commitment as well. This helps explain why, in studies of diversification trends, Markides (1992, 1995) finds that companies that begin with high degrees of diversification move to conform with industry averages. And, in their research on how analysts perceive abandonment timing, Brauer & Wiersema (2012) show that practices are abandoned in waves as managers imitate each other.

Length of practice and abandonment

While performance concerns motivate abandonment decisions (Abrahamson & Rosenkopf, 1993; Lieberman & Asaba, 2006), time mediates the value of both direct and indirect information in multiple ways. First, the less experience an organization has with a practice the less able they are to determine whether or not it is succeeding or failing. Adoption of a new practice can require substantial changes across the organization and introduce new coordination costs, the resulting liability can be difficult to separate from the returns to the new practice (Haveman, 1992). In addition, new practices are rarely assumed to be instantaneously beneficial, making it difficult for managers to determine whether a new practice is failing or still transitioning. Further, managers may discount post-adoption declines rather than face the costs of changing course again, or of admitting to having adopted erroneously (Staw, 1981, 1997). In each case, while performance changes exert an influence, the uncertainty attendant to a recent change creates incentives to read the performance data selectively, mitigating the effect.

At the same time, if adoption is a method of information gathering—firms adopt new practices on a trial basis and then adjust their commitment according to the returns—the effect of performance on the degree of commitment might increase as the quality of information improves and the uncertainty diminishes. Abrahamson (1991) argues that this type of managerial updating helps explain the decline of fads as managers continually assess the post-adoption performance, consistent evidence takes time to accumulate, but once gathered abandonment swiftly follows. Scholars draw on the value of this internal information to propose that abandoning firms are less prone to herding behavior than adopting firms (Terlaak & Gong, 2008).

This suggests that the influence of experiential information increases with time, while the influence of vicarious information declines. Thus analysts who recently adopted coverage of a stock are more responsive to other analysts dropping coverage than those with long-held positions (Rao et al., 2001). And firms begin abandoning high-speed ferries because they witness others doing so, but accelerate the abandonment once they have their own reliable information (Greve, 2011a). By contrast, vicarious information is often described as operating as a complementary good (Bresman, 2010), whose significance depends upon the quality of direct information. As a result, we would expect the value of this inferred knowledge to be highest early in the process and to decline as the quality of the direct information increased:

H1: The influence of performance declines on decommitment will increase with time, while the influence of peer actions on decommitment will decrease with time.

Organizational characteristics and abandonment

While performance may serve as a general motivator for most firms, several features of the organization can moderate these effects in distinct ways, even reversing the direction of the influence and helping to establish unique paths to abandonment. For example, studies of abandonment have been particularly sensitive to the performance of both small and “underperforming” firms. Both internal and external assessors rarely consider the performance of a firm in isolation; therefore, an absolute decline in performance is less problematic for managers than a decline relative to the performance of peer organizations. As a result, Montgomery and Thomas (1988) found that firms divested not because performance fell, but because it fell relative to the average firm in their industry.

Underperformers presumably enjoy fewer margins for error and are therefore more responsive to changes in performance that result from their new strategy. For instance, in an analysis of the shipping industry Greve (2011b) finds that small firms and firms falling below their “aspiration level” exhibit less positional rigidity. In other words, these firms are more likely to abandon a strategy than larger rivals even if the practice is worse for the rival. This complements earlier work by Greve (1998) on the decision to change formats by radio stations, in which he demonstrates that falling below their aspiration level increases the likelihood that an organization will pursue a change. Together these suggest a potential moderating effect of relative performance on changes in performance, leading to the next hypothesis:

H2: The influence of peer commitment and performance declines on decommitment is stronger for organizations below their aspiration level.

Similarly, multiple studies document the moderating role of firm size in determining sensitivity to normative pressure (Kraatz, 1998) and performance declines (Freeman, Carroll, & Hannan, 1983). Size, in general, creates a paradox for firms, where larger firms are both more financially able to pursue change and absorb any losses that follow but are also more visible when deviating from norms. For example, in her study of diversification rates in the savings and loan industry, Haveman (1993) found that large organizations possessed both the resources necessary for change and an ability to withstand the risk of performance declines. Their greater insulation to loss leaves the large firms less sensitive, relative to small and medium-sized firms, to performance declines, and therefore less apt to change course if the returns are not positive. By contrast, small firms can escape notice if they violate a norm, allowing them great latitude in experimentation and making them less subject to reduce commitment simply to match peer behavior.

These findings suggest that the influence of performance and peer commitment will vary with the size of the organization. More precisely they suggest that larger organizations are more likely to respond to divestments by their competitors, but less likely to respond to changes in performance than small organizations:

H3a: The influence of peer actions on decommitment will be greater for large organizations than for small organizations.

H3b: The influence of performance declines on decommitment will be greater for small organizations than for large organizations.

Conflicting accounts and abandonment

The emphasis on abandonment as a rational act reinforces the need for unambiguous information as a precondition of change. As a result, when there is a consensus that a practice is problematic it is not hard to predict the organizational response. However, two distinct paths to abandonment emerge in situations where experienced and inferred knowledge contradict each other. For example, when an organization believes the practice is succeeding but witness their peers abandoning or when they believe it is flawed but see others increasing commitment. In these situations, as shown below, the direction of the tension predicts the process of abandonment.

In the first situation, peer commitment can moderate the influence of negative direct experience by reinforcing the impression that the practice is typical. Abandonment of a widespread practice risks drawing extra negative attention upon managers who must now explain why they failed to do what others managed successfully. To prevent these challenges organizations often seek to maintain an appearance of similarity and refrain from engaging in overtly deviant action (DiMaggio & Powell, 1983). Studies have repeatedly shown that the adoption and redefinition of practices are strongly motivated by these legitimacy-based concerns (Burns & Wholey, 1993; Deephouse, 1996). The tension between the impetus to abandon and to maintain the practice requires that managers strike a balance between decommitment and the need to retain some element of the practice. At a minimum, rather than risk penalties, managers might circumscribe the scope of their abandonment, retaining a symbolic element of a practice to indicate normative compliance, while still reducing the extent of the damage from maintenance.

The emergence of the opposite situation, in which again the information signals conflict, with organizational performance unaffected but abandonment spreading across an industry, motivates a second path to abandonment. Here the social pressure operates not as a constraint but as an enabler, pushing organizations to adopt replacement practices or abandon existing ones. For example, Zuckerman (2000) shows that security analysts pressured firms to resemble the typical firm in their industry, penalizing firms that remained diversified as the norm in the industry shifted to concentration. While managers traditionally demonstrate reluctance to adapt when performance is stable (Miller & Chen, 1994), there is equal evidence that they adopt some elements of a practice, despite ambiguous benefits, in order to meet external expectations (Meyer & Rowan, 1977). This suggests a slower path to abandonment with organizations ceremonially reducing commitment while maintaining as much of the practice as possible.

In either situation the optimal response is to reduce costs by limiting the internal losses and the potential for external penalties. This creates a tension between the need to decommit while simultaneously not abandoning, leading to the final hypothesis:

H4: When internal and external signals conflict, organizations will be more likely to decommit but less likely to abandon.

Data and Methods

To test these hypotheses, a sample of 100 firms was randomly selected from the 1970 Fortune 500 list. As past research on diversification and divestiture frequently draws their samples from the same pool (Davis, 1991; Markides, 1992; Palmer & Barber, 2001) the use of this sample facilitates comparisons with existing research. 1970 was selected because it preceded the wave of de-diversification (Davis et al., 1994; Fligstein, 1985) and was the first year in which firms were required to report business segment data. 1996 was chosen as the final year of observation because it was the last year in which data were categorized using the SIC codes.

During this period of observation 80 firms adopted the practice, 48 abandoned it, and 10 exited through bankruptcy or acquisition prior to abandoning, resulting in an imbalanced panel with 2698 firm-year observations. Seven of the adopting firms were left-censored, adopting before 1970 and were therefore dropped from the event history analyses (of those seven, four abandoned the practice, and three were right-censored). As the sample suffers from incidental truncation, where some firms adopted the practice while others did not, one must model the possibility of sample selection bias. Heckman’s (1979) maximum-likelihood estimation with selection offers a viable means to treat this concern. The model conducts a two-stage estimation to predict the degree of commitment not only as a function of the independent variables but also based upon the likelihood that an organization adopted the practice at all. The descriptive statistics for all variables are provided in Table 1.

Descriptive statistics.

Note: This table presents pairwise correlations based on 2698 observations of 100 publically traded American firms between 1970 and 1996.

Dependent Variables

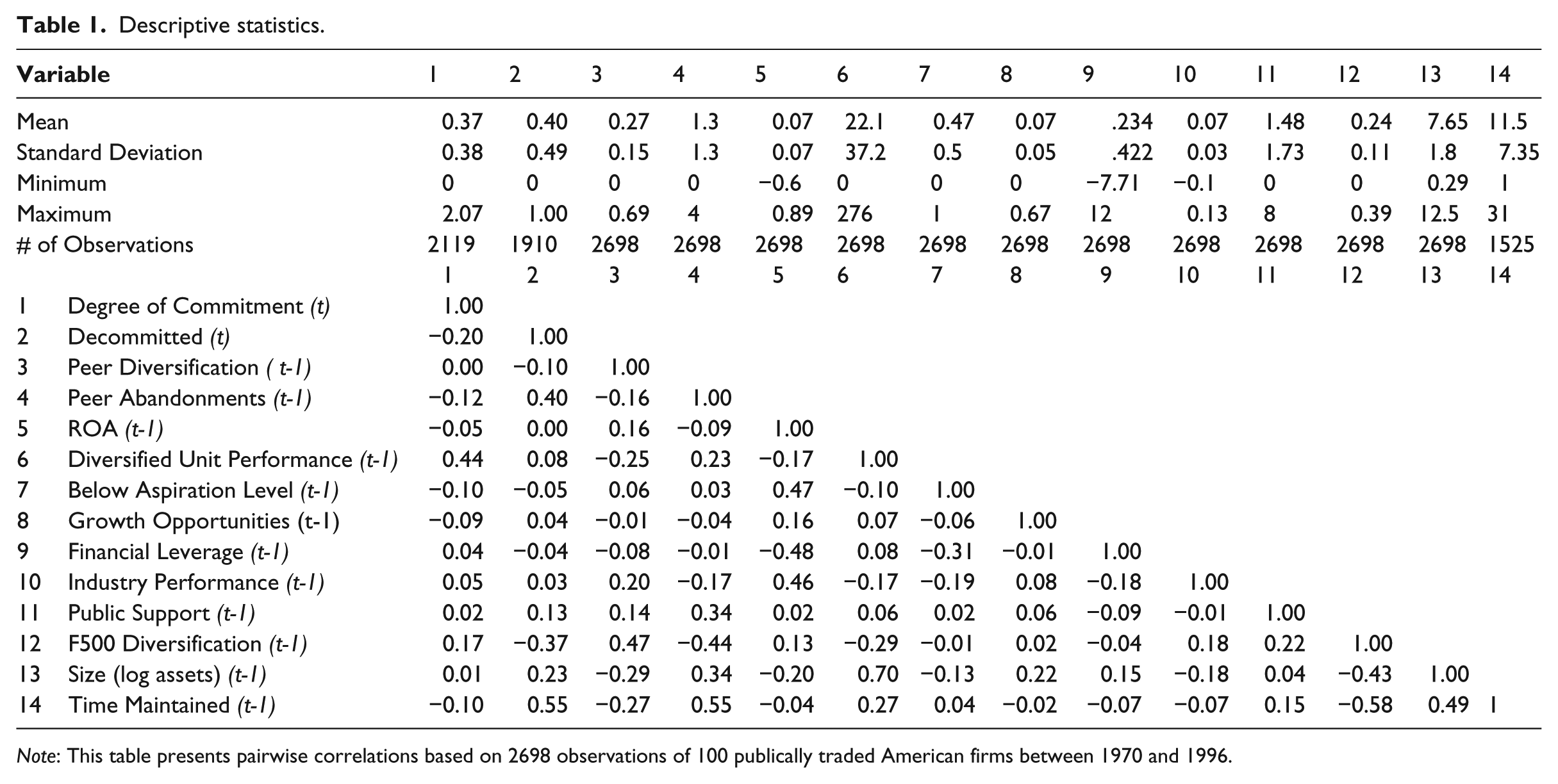

Commitment

Testing the hypotheses requires a method for measuring the level of commitment and a means of identifying when a firm has decommitted. For the first, to establish a continuous measure of commitment, I use an entropy measure of unrelated diversification (Jacquemin & Berry, 1979) that follows the formula:

Where D is the level of unrelated diversification, Pi is the proportion of total sales in segment i. and Ui is an indicator for whether segment i is unrelated to the core business of the firm (1 = outside 2-digit primary SIC code, 0 = inside). By this measure firms with no sales outside of their primary 2-Digit SIC receive a score of 0, with the score increasing as unrelated diversification increased.

The primary SIC code, or core industry, was defined in keeping with past research (Berry, 2012; Palepu, 1985) as the largest 2-Digit SIC business in terms of total sales. Firms that had not yet diversified received a “0” entropy score and firms were dropped from the sample they year after they abandoned (entropy = 0).

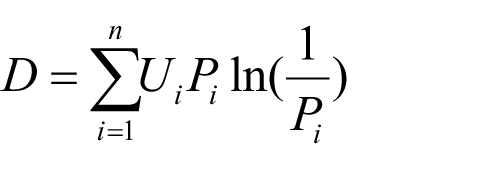

The entropy score is a frequently used measure of diversification (Davis et al., 1994; Palepu, 1985; Prechel, Morris, Woods, & Walden, 2008) and has the advantage of being easily separable into related and unrelated components. It offers an annual measure for the degree of unrelated diversification for a given firm, which forms a suitable proxy for the degree of commitment to the practice of unrelated diversification. Figure 2 displays the mean level of unrelated diversification for the sample and the annual count of committed firms over time.

Decommitment

Decommitment is defined as the point after which the entropy measure of diversification neither increased, nor remained constant for any two-year period. It is recorded as a “1” from this point until abandonment and as a “0” for prior years. This definition limits “decommitment” to the firms that are actively and routinely reducing their commitment. The two-year period was selected because the complexity of divesting meant that some transactions took more than a year to complete, creating episodic pauses in a general downward trend.

To prevent right-censored firms from being mistakenly identified as decommitted, only firms that abandoned the practice during the period of study were eligible to be considered decommitted. This produces a more conservative estimate of the firms that decommitted, but analyses done on the larger sample of firms produced no statistically significant differences in the results.

It is worth asking if the point of demonstrated decommitment accurately reflects the point managers consciously chose to decommit, or if alternative definitions better capture the concept. For instance, returning to Figure 3, it is plausible to claim 1978 or 1983 as the true points of “decommitment.” These points clearly capture additional moments of interest and could be argued to indicate the time managers elected to decommit. However, each suffers from its’ own limitations. Selecting 1978 ignores the four years of nearly constant commitment between 1979–83, while selecting 1983 arbitrarily defines the reduction from 1981–82 and 1982–83 as less significant than subsequent reductions. Therefore, to best introduce the concepts I have sought the most easily defined and identified points. There is only one earliest point after which commitment continually declines, and that is 1981.

Unrelated diversification over time.

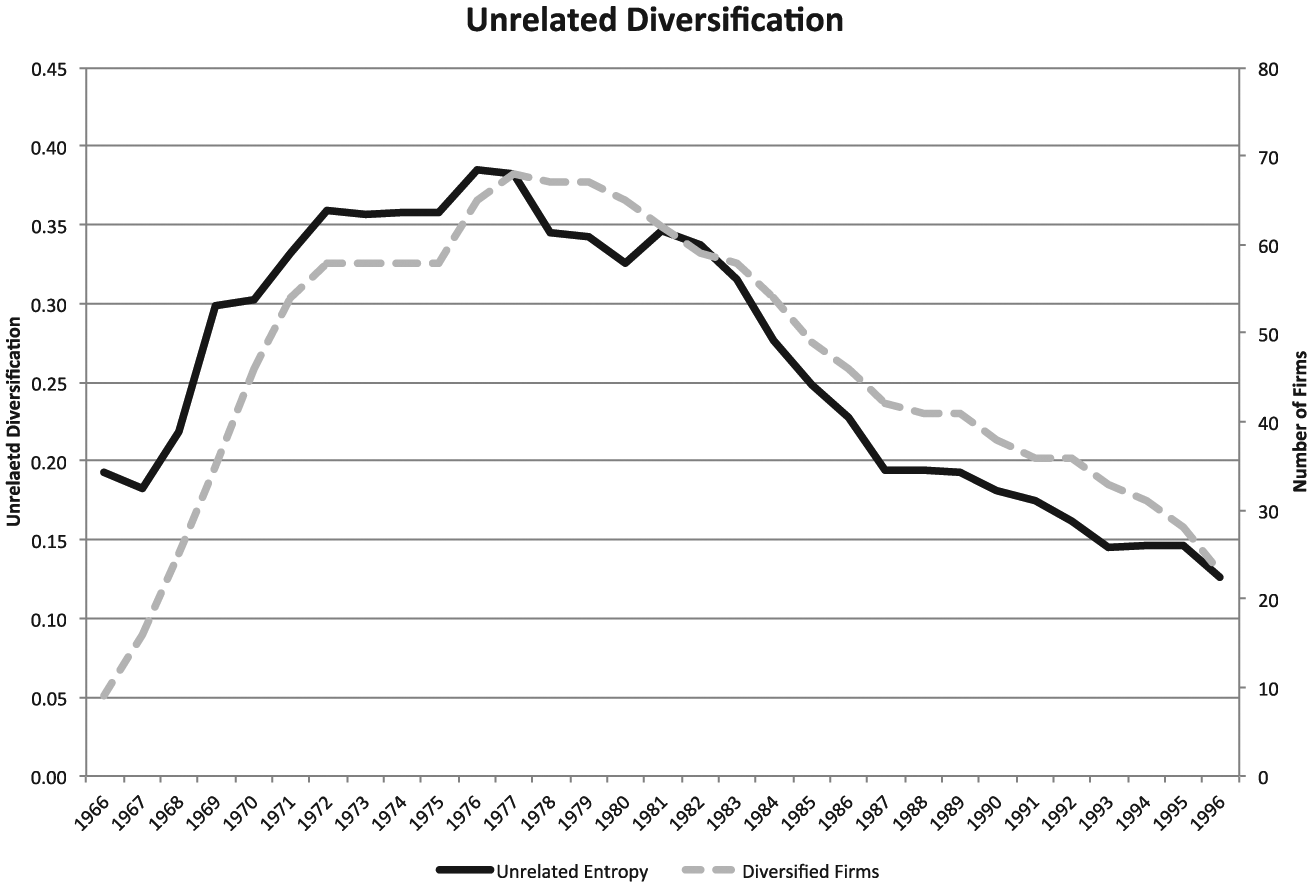

Analysis of the annual reports found that a majority (~60%) of companies self-identified their year of abandonment as the same year found here (Figure 4). The remaining firms either did not discuss the change in strategy or did not identify a specific year. Although not definitive, this offers some qualitative support both for the notion that decommitment is an event worth capturing and that the definition identifies a time consistent with the experience of the managers.

Declaring decommitment.

Data on firm sales by business segment were taken from Compustat Industry Segments (post-1976) and directly from firm 10-K reports (pre-1976). Critically, this data distinguishes between vertically-integrated segments and unrelated forms of diversification. In the event that a company did not identify their segments or failed to assign their business segments SIC codes, data for that year was not included. To reduce the likelihood of errors caused by a change in SIC schema, each business segment was identified in firm 10-K reports to determine if the same segment was given a different 2-Digit SIC designation after a change in the regulatory standards. For the 100 firms included in the study only six had at least one division reclassified. Removing these six firms from the study did not alter the results (Appendix B). It was therefore possible to use the Census correspondence tables (which explained how categories were redefined) and firm 10-Ks to construct a consistent code for each segment for the duration of the study and include all 100 firms in the tables presented. Additional sensitivity analyses are explained below.

Independent Variables

Peer commitment

For the purpose of this study, a peer is defined as a firm that shares the same 2-digit SIC classification and is within one standard deviation of the focal firm’s size (log(assets)). For each focal firm there is therefore a set of alters that form their “peers” composed of a subset of the firms within their industry. I measure peer diversification as the mean annual level of unrelated diversification (entropy score) by a focal firm’s peers, by year. In addition, peer abandonments were measured with an annual count of firms in the peer group to have abandoned within a given year. As an annual rather than cumulative count, this captures how a mass of abandonments influence the remaining firms rather than the aggregate pressure of total abandonment. Additional analyses estimated with a cumulative count instead of an annual count or a broader definition of peer (i.e. shared SIC class) produced comparable results.

Although comparable, these two variables capture different aspects of the pressure faced by firms. The first measure is commitment-related, capturing the pressure faced by firms as their rivals increase their attachment to a given practice. The second measure accounts for the pressure faced by a firm to conform as an increasing percent of the industry abandons a new practice. Variations in their effects indicate the degree to which focal firms respond to the general (adopt/abandon) or specific (degree of adoption) patterns of their peers.

Performance

To measure the performance of the firm I use the return on assets and the square root of sales within diversified units. This distinguishes between the effect of overall firm performance and the performance of the unit to be divested. Both are among the most common and widely accepted measures of performance, have a high degrees of correlation with alternatives (Berry, 2010), and have been used to explain firm divestment in prior research (Berger & Ofek, 1999; Bergh, 1997; Park, 2002). ROA was calculated using EBIT/assets as reported in Compustat Fundamentals Annual and updated annually. The square root of within unit sales was used to control for positive skew, the data were derived from Compustat Industry Segments.

In addition, as Greve (2011b) has shown that the effect of performance on abandonment decisions varies depending upon whether that performance exceeds or falls below industry averages, I include his measure of the performance aspirational level. This is a binary measure of whether a given firm exceeded the average ROA of similar sized firms within their industry, by year.

Control Variables

Given that the practice under study here was the adoption and abandonment of unrelated diversification by U.S. manufacturing firms, it is prudent to include financial measures found to have been influential in the rise and fall of diversification more generally. Therefore I include a measure of the growth opportunities (capital expenditures to sales), financial leverage (total debt to equity), industry performance (median Tobin’s q), and firm size (log assets) all updated annually. These measures are frequently used in financial studies of divestment decisions (Chatterjee & Wernerfelt, 1991; Markides, 1995; Rumelt, 1982). And is in keeping with multiple past studies that found a relationship between debt ratios and firm diversification activities (Berry, 2010; Hoskisson & Johnson, 1992; Hoskisson, Johnson, & Moesel, 1994).

To assess the role of broader public support, a count was made of articles in the New York Times supporting unrelated diversification as a strategy. Two independent coders read and analyzed New York Times articles between 1970−96 that mentioned some variant of “diversification” (diversif*: diversification, diversified, diversify, diversifying). These articles were coded according to whether they discussed related or unrelated diversification, and whether they were positive or negative about the practice. The analysis of inter-rater reliability showed high levels of agreement (>90%). In cases of disagreement, raters reviewed their analysis and reached a consensus. To account for the overall popularity of the practice among managers, I include the average sample diversification, by year, across all sample firms.

As multiple studies have used the qualities of a firm at the origin of the study as controls, the models were also estimated with initial diversification level, peak commitment level, and age as control variables but the results were not significant. Debt ratio (total debt/total assets) and common liquidity measures (e.g. current assets/current liabilities) were also tested for inclusion but not found to be significant and therefore excluded. In all the regressions all of the independent variables are lagged one period.

Sensitivity Analyses

A modified Wald test for panel data showed no group-wise heteroskedasticity and diagnostics using a variance inflation factor suggested no problems with multicollinearity as all of the VIF values were below 10. In addition, I conducted multiple sensitivity analyses to verify the robustness of the results (Appendix B). The first model presents a complete case random effect model with errors clustered by firm. To test errors in the coding of commitment, the second presents the results only using post-1976 data; the third presents a Heckman model excluding firms that reclassified a business unit, and; the fourth measures diversification by a count of the 3-Digit SIC categories in which a firm reported sales (data from Dun & Bradstreets Million Dollar Directory 1968–96) as an alternate to the entropy score. Finally, as discussed in Appendix A, a secondary analysis was conducted on a single industry, pharmaceuticals, to test alternate means of defining the moment of abandonment and a firm’s peers, the results of all tests do not vary significantly from those presented in the primary tables.

Data Analysis

I utilize Heckman’s (1979) model with selection to estimate the degree of commitment to the practice over time and a Heckman probit model to estimate the likelihood that a firm had decommitted. The Heckman model was chosen to address the possible sample selection bias arising from the fact that not all the firms adopted the practice. The model used here assumes that the likelihood of adoption is a function of an organization’s size (log asset), performance (ROA), debt ratio (debt/equity), capital expenditures, and the percent of other firms in their industry that adopted. Appendix C provides the estimates including the selection model results.

Results

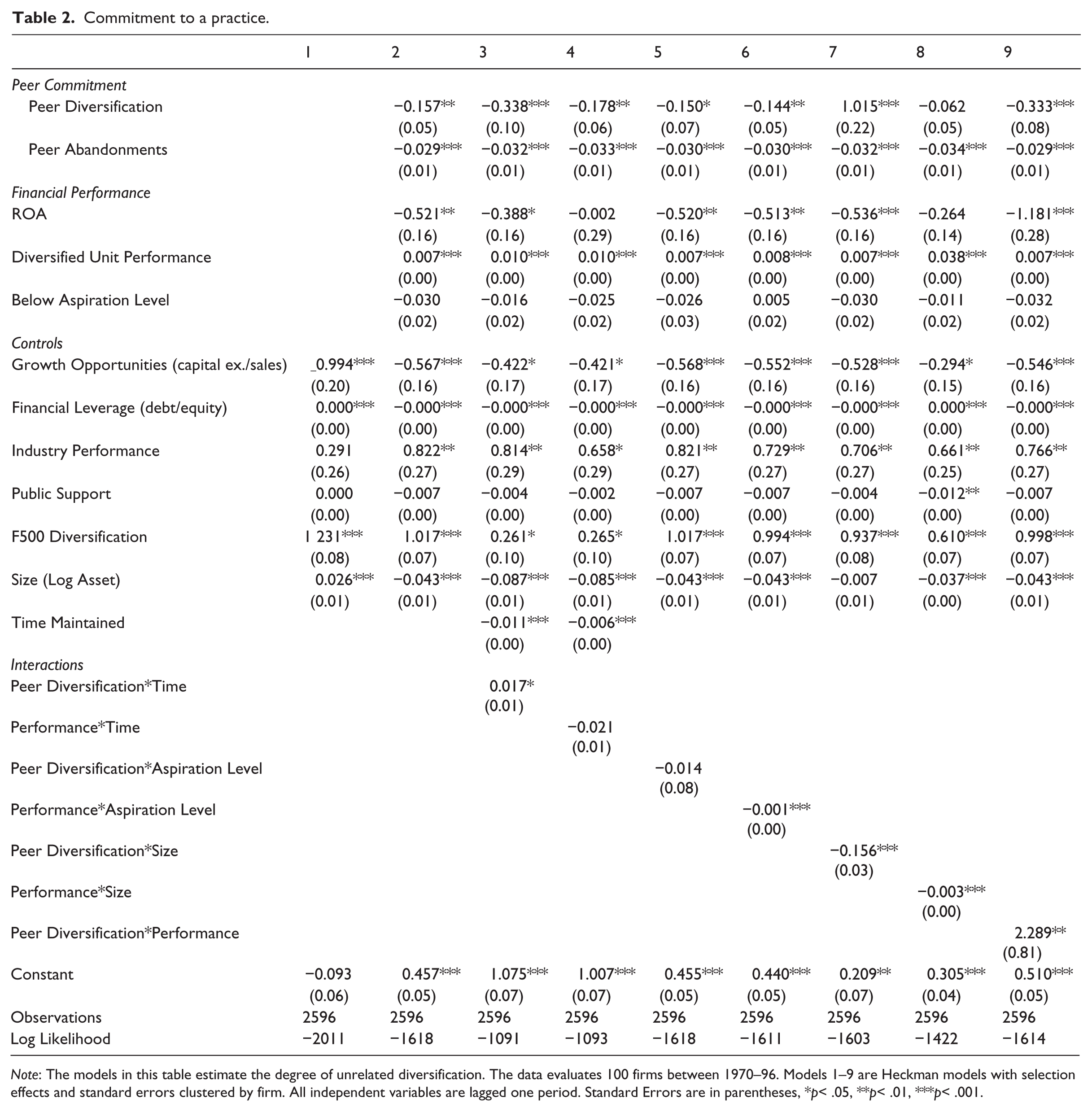

Table 2 presents the result of estimating the effect of external and internal signals on the degree of commitment to a practice. Model 1 presents a baseline with the controls, model 2 offers the complete model, and models 3−9 introduce interaction terms to test the specific hypotheses.

Commitment to a practice.

Note: The models in this table estimate the degree of unrelated diversification. The data evaluates 100 firms between 1970–96. Models 1–9 are Heckman models with selection effects and standard errors clustered by firm. All independent variables are lagged one period. Standard Errors are in parentheses, *p< .05, **p< .01, ***p< .001.

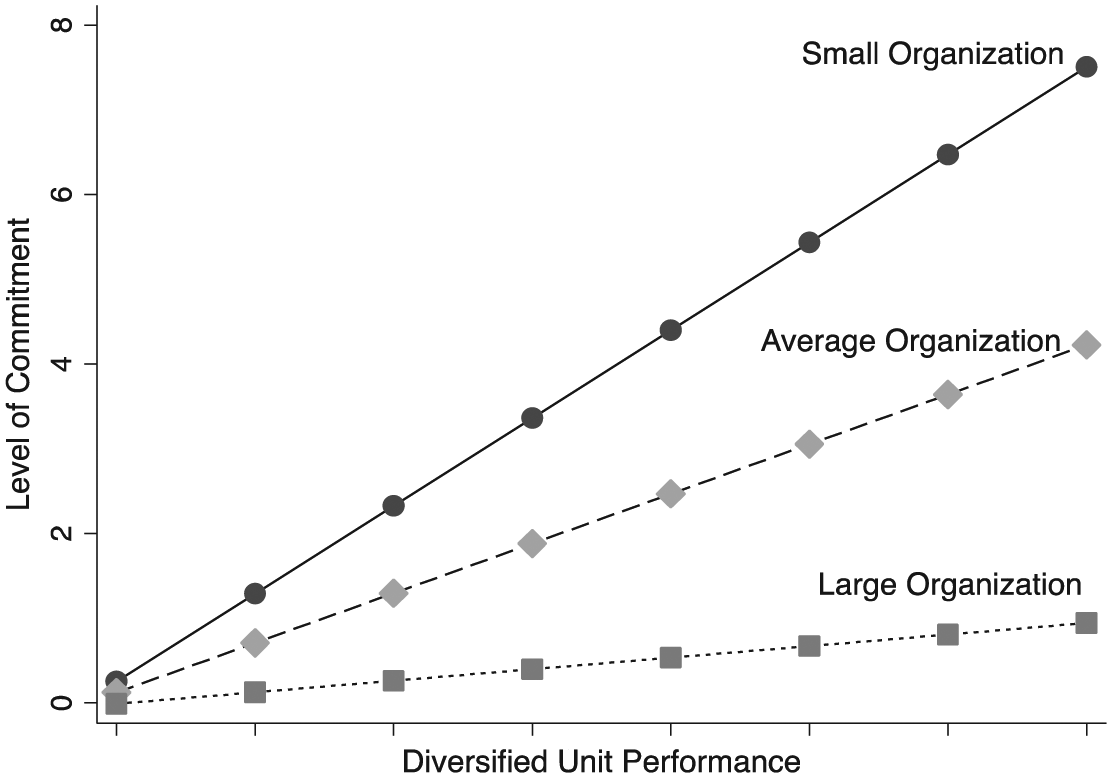

The first hypothesis proposed that the influence of peer commitment is inversely, and performance directly, related to the duration of the practice. To estimate this I include, in model 3, an interaction term between the level of peer commitment and the number of years since a focal firm began pursuing unrelated diversification, and in model 4 an interaction between performance and duration. The results offer modest support for the hypothesis, showing that the influence of peer commitment is greatest for recent adopters, but that this effect is reduced the more pervasive the practice becomes. Figure 5 shows that firms that recent adopters respond more strongly to changes in peer commitment than other firms. However, the effect declines as the practice becomes embedded within an industry, and in industries with extremely high levels of commitment there is no difference between recent and long-time adopters. In addition, there is no evidence that the effect of performance varies with time.

Interaction effects of time and peer commitment on firm commitment.

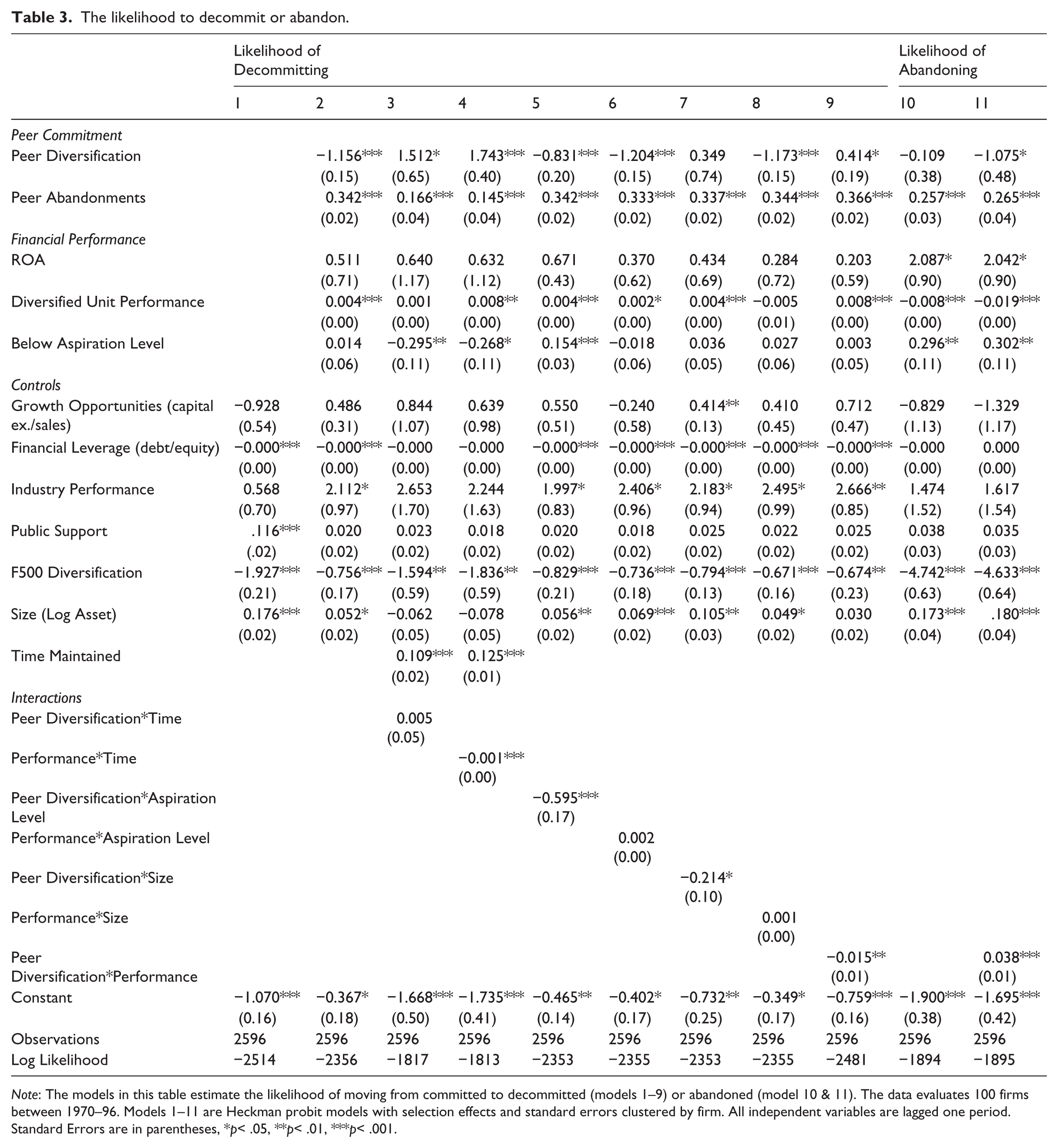

A second way to consider the process of abandonment is to examine the influence of these variables in predicting pre-abandonment shifts in strategy. If the results explain changes in the direction and rate of commitment then it follows that they should also help explain the likelihood that a firm moves from a committed to a decommitted phase in their path to abandonment. To estimate this table 3 presents a Heckman probit method with selection to predict the likelihood that a firm decommitted.

The likelihood to decommit or abandon.

Note: The models in this table estimate the likelihood of moving from committed to decommitted (models 1–9) or abandoned (model 10 & 11). The data evaluates 100 firms between 1970–96. Models 1–11 are Heckman probit models with selection effects and standard errors clustered by firm. All independent variables are lagged one period. Standard Errors are in parentheses, *p< .05, **p< .01, ***p< .001.

The results presented here offer a valuable complement to those in Table 2, as model 4 show that the influence of performance on the likelihood of decommitting changes as the practice is maintained. In contrast to the hypothesis, the longer the practice is maintained the less changes in performance affect the likelihood of decommitting. For practices that have been in place for 20 or more years changes in performance have no significant effect on the likelihood of abandoning, but for practices maintained less than ten years there is an increase in the likelihood as performance improves.

The second hypothesis predicted that firms below their aspiration level are particularly sensitive to the influence of internal and external signals. While there is no evidence between peer behavior and aspiration level in Table 2; model 5 of Table 3 shows that firms below their aspiration level are more sensitive to the changes in peer commitment, with their likelihood of decommitment increasing more rapidly as peer commitment declines.

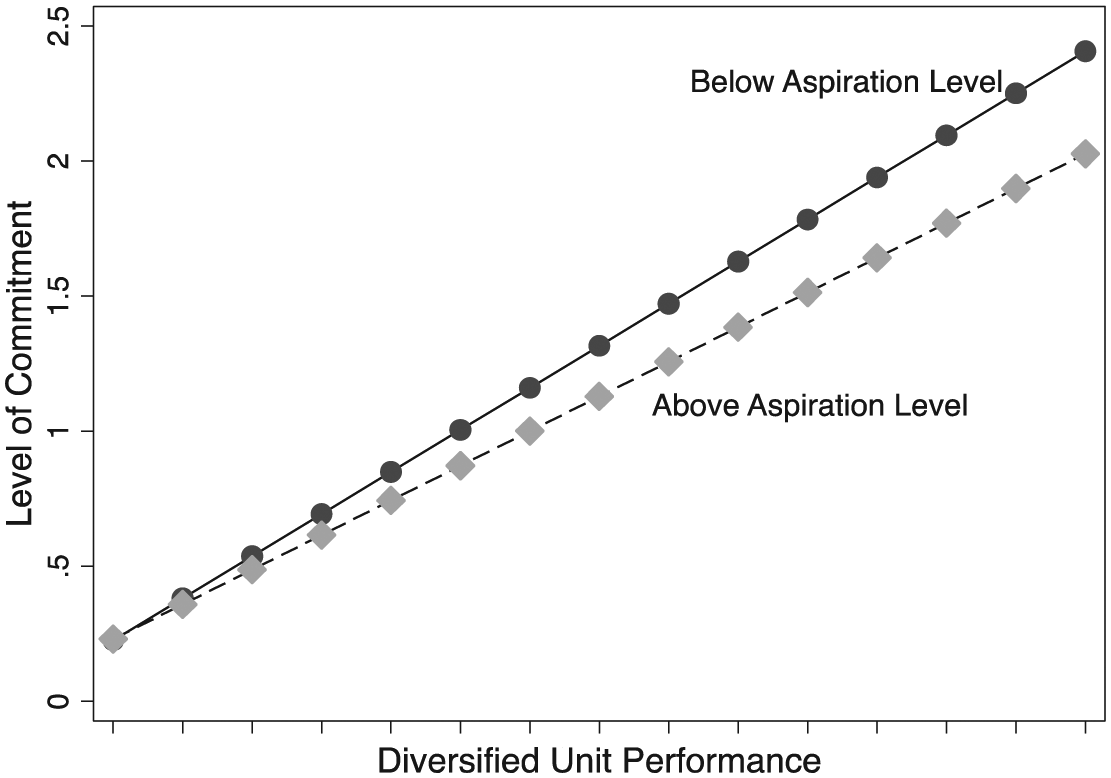

Model 6 tests the second part of the hypothesis and indicates, in Table 2, a significant relationship between aspiration level and the performance of the diversified units. In support of the hypothesis, we see (Figure 6) that firms below their aspiration level increase their level of commitment at a higher rate if performance improves. In other words, firms operating below the level of similar-sized firms within their industry respond to changes in performance by increasing or reducing commitment more than firms above the level of competitors.

Interaction effects of aspiration and performance on firm commitment.

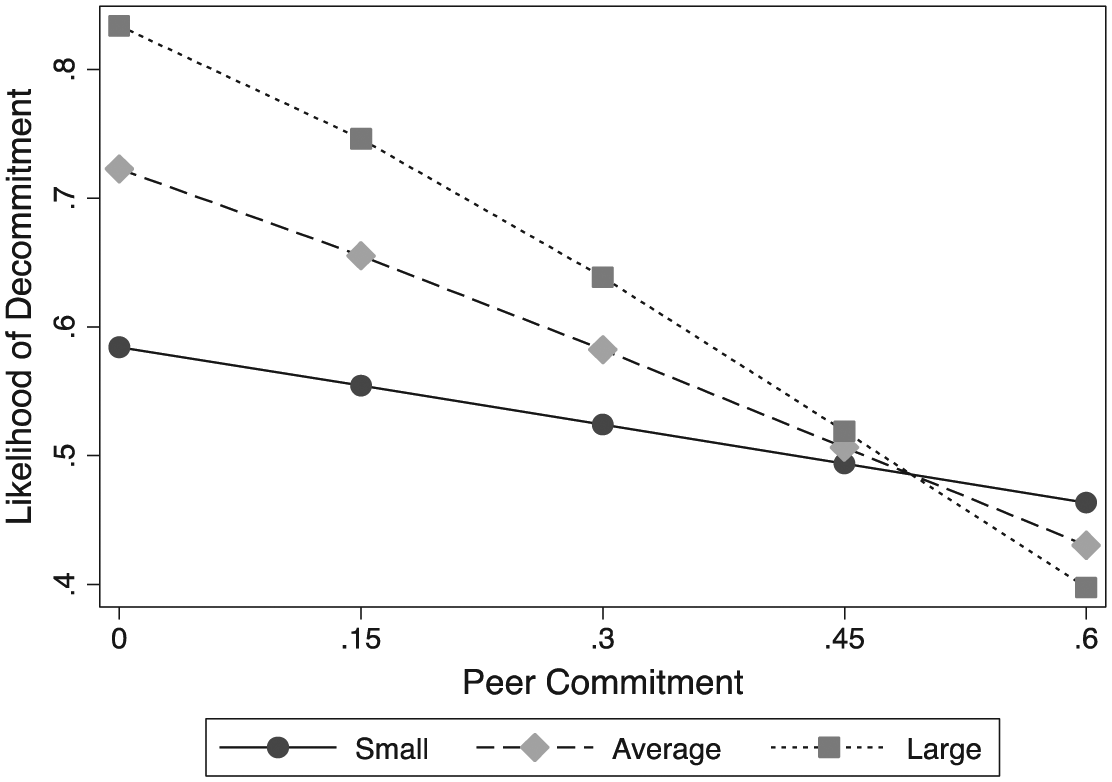

The third hypotheses proposed that the influence of peer commitment would be greater for large firms than for small firms, but that the influence of performance would be greater for smaller than large firms. In support of the hypothesis I find that large firms are both more responsive to peer behavior and that they are differently affected (Figure 7). Small firms exhibit a direct relationship with their level of commitment increasing as the firms around them increase. Moderate sized firms are relatively indifferent to the behavior of their peers and the largest firms display a negative relationship where they reduce their commitment if their peers increase it. Suggesting that while small firms are in a following position here, imitating the behavior of others, larger firms seek out new niches.

Interaction effects of size and peer commitment on firm commitment.

Model 7 of Table 3 provides additional evidence that the size of the firm influences their interpretation of vicarious information. As predicted we find that larger firms are more sensitive to peer behavior than small firms with their likelihood of decommitting declining at a much higher rate as peer commitment increases (Figure 8).

Firm size and peer commitment on decommitment.

Interactions of firm size and performance return similar results in model 8 of Table 2, with smaller firms responding more strongly to performance feedback than larger firms (Figure 9). However, in Table 3, there is no evidence that size altered the influence of performance on the likelihood of decommitting. This may indicate some heterogeneity in the population of smaller firms, with some seeking to gain an advantage by moving quickly to adopt a new practice while others resist for fear of being perpetual followers. In contrast, large firms are in the position to adopt and slowly increase or decrease as the evidence becomes easier to interpret.

Interaction effects of size and performance on firm commitment.

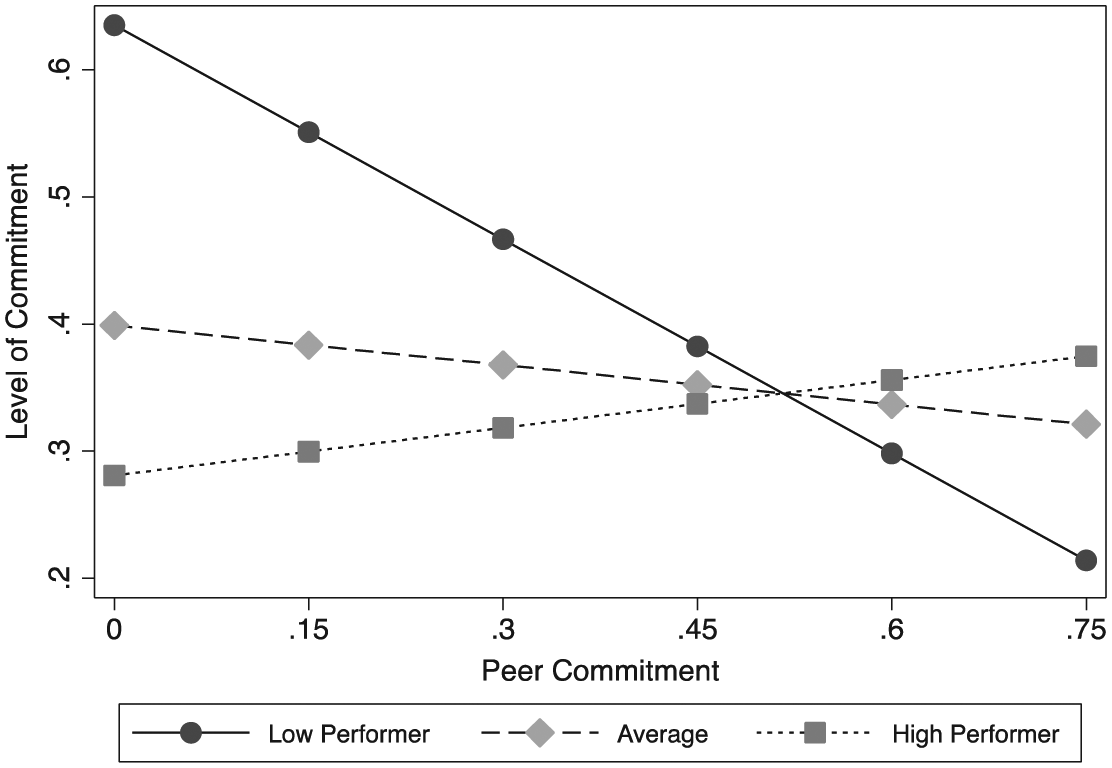

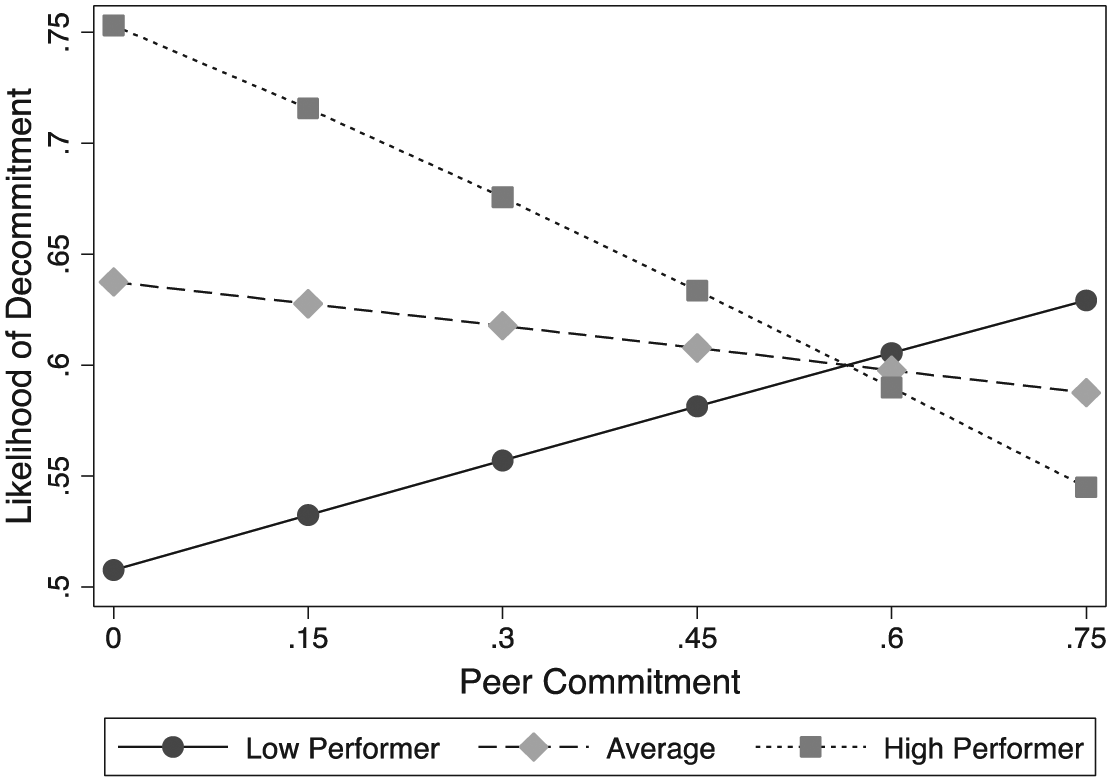

The fourth hypothesis proposed that when the two primary effects are in conflict the firms increase their likelihood of decommitting but not abandoning. Model 9 of Tables 2 and 3 presents evidence in support of this claim, showing that when peer commitment is low but ROA is high firms are at their lowest level of commitment (and actively reduce commitment); when peer commitment is high but ROA is low their likelihood of decommitting is highest and their rate of commitment lowest (Figures 10 and 11). Similar results were returned if we considered the performance of the unrelated divisions.

Interaction effects of performance and peer commitment on firm commitment.

Performance and peer commitment on likelihood of decommitment.

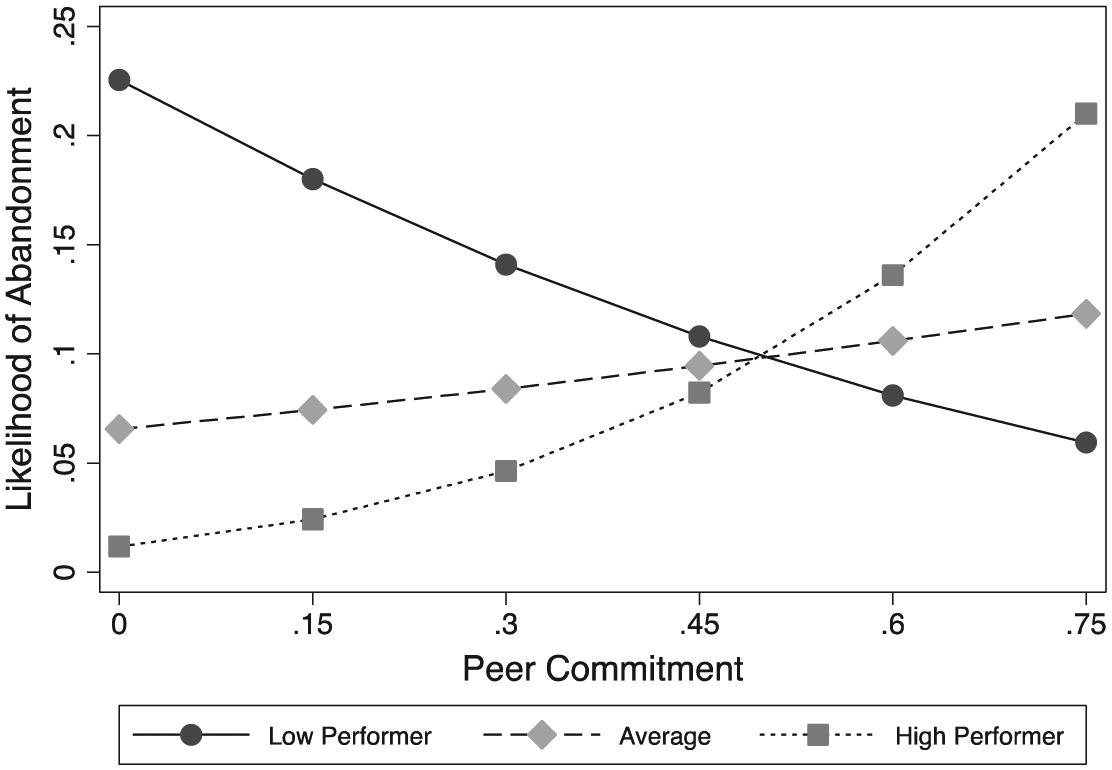

Model 11 of Table 3 confirms the second part of the hypothesis, showing that abandonment is less likely when the sources disagree than when they reinforce one another. For low performers, their likelihood of abandonment declines as peer commitment increases and for high performers it declines as peer commitment decreases (Figure 12). As predicted, when the two sources of information conflict the organizational response is to rapidly decommit but to slowly abandon. By contrast, a concurrence of information, either negative or positive, produces the same results: higher levels of commitment. Low-performing firms in industries with low levels of commitment adopt the same approach as high-performers in industries with high-levels of commitment. This may not be as counterintuitive as it appears, as it may indicate that low-performers adopt high-variance tactics to change their position while high-performers are in position to adopt more conservative plans.

Performance and peer commitment on likelihood of abandonment.

Comparing to abandonment

To suggest that decommitment offers additional value in our understanding of the life of a practice it follows that it should be both an identifiable act and one motivated by distinct factors. To assess the degree to which predictions of decommitment differ from conventional accounts of abandonment I include model 10 which uses a Heckman probit model to assess the likelihood a firm abandoned the practice entirely.

In contrast to the earlier models, and consistent with prior research within industry behavior has no significant effect and all three of the performance criteria are significant. In particular, firms below their aspiration level (.296, .110) and firms whose diversified assets are declining (-.008, .001) are more likely to abandon. This helps highlight the distinctiveness of decommitment, as firms whose unrelated assets were performing well were likely to decommit, but not to abandon. Meanwhile, firms in well-performing industries were likely to decommit, but not to abandon. And while firms were unlikely to abandon or decommit while the practice remained pervasive across the industry, the difference between the effects was substantial.

Together these findings illustrate the evolving value of performance-based and institutional factors in predicting the commitment to an adopted practice. Within industry behavior helps determine the degree of commitment for an adopted practice, but it does not influence the likelihood of ending the practice entirely. Similarly, falling below your aspiration level does not drive a firm to adjust their commitment but it does predict the maintenance or ending of the practice. Including an analysis of commitment and decommitment in studies of abandonment help distinguish between the factors that explain adjustments in a practice and those that explain its demise.

Discussion

The central claim of this article is that there is a difference in treating abandonment as a process rather than a moment. The basis for this claim derives from a tenet of organizational theory: organizations change through the adoption and abandonment of practices, forms, and orientation. And environments—and the taken-for-granted assumptions that govern them—change as these organizations increase or decrease their commitment to those governing beliefs (Tolbert & Zucker, 1983). In order to understand these changes, or the ability of a given organization to change, we need to understand what factors create the space for change. We need to understand not just why a firm adopts a new idea, but why they begin to devalue it, and according to what criteria they measure it (Green, 2004).

The prevailing explanation, that commitment declines and institutions collapse when they prove inefficient, is hard to reconcile with the evidence that practices are often hard to abandon (Davis et al., 1994), managers resist change (Fiss & Zajac, 2004), and performance data is open to interpretation (Jonsson, 2009). By reconsidering abandonment as a process with multiple-stages, I find evidence that both performance-based concerns and institutional pressure motivate commitment decisions, but, consistent with prior findings, that institutional pressure declines the longer a practice is maintained.

Specifically, the results demonstrate that managers navigate conflicting evidence not by addressing either performance or peer influence, but by reducing commitment while maintaining the practice. This offers both the appearance of compliance and a means to mitigate negative returns. Similarly, managers continually adjust commitment and approach the decision to decommit with both sets of factors influencing their decisions. The results do not show the replacement of one strong force by a secondary strong force nor that institutions only operate in the absence of clear performance data, but rather that the life of a practice is consistently shaped by both forces. Further, it suggests that the role of peer influence evolves the longer a practice is maintained, moving from an indicator of what level of commitment to adopt, to an indicator of the minimum amount of commitment required.

The results also show that the interpretation of peer behavior is strongly conditioned by firm size and performance. As a result, higher peer commitment confirms the decisions of high-performers and causes an increase in commitment, but signals to low performers that an area is too competitive. The behavior of peers operated as both a constraint—even low-performing firms maintained a semblance of the practice—and a set of complementary information whose value was filtered through internal biases.

This study recasts abandonment as the final point in a path of fluctuating commitment. While abandonment remains critical to assess, the preceding changes in commitment offer valuable insights into how the practice evolved and why it was eventually abandoned. Trying to describe the end of the practice without looking at these points is like trying to describe what happened in a movie when you only saw the opening and the ending. In this article, I show how investigating changes in the level of commitment prior to abandonment provides insight into how managers navigate when social proof and internal assessments conflict.

Contributions

These findings offer important contributions to extant research on diffusion and institutional theory. First it offers a way to resolve the tension in prior diffusion studies between two competing narratives on the abandonment of a practice. Practices were either abandoned as a result of performance declines (Greve, 1995, 2011a; Rao et al., 2001) or could not be abandoned despite performance declines (Davis et al., 1994). The findings here offer a solution by showing how managers reduce commitment while maintaining a vestige of compliance. The aggregate effect of these reductions is to erode institutional influence so that abandonment is largely ceremonial. This suggests that decommitment must precede abandonment and therefore if firms cannot decommit, they will not erode institutional strength and will appear unresponsive to performance changes. But, if they vary their commitment they create the space for abandonment.

Related to the above, treating abandonment as a process provides a way to reconcile the consistent expectation that abandonment is influenced by social norms with the inability to find evidence of such a relationship. Focusing on the process reveals that social norms influence levels of commitment and the likelihood of decommitment to a practice. As decommitment spreads the relevance of performance concerns increases and allows organizations to make abandonment decisions independent of their peers.

Third, the findings offer institutional theorists an alternate way to consider the contestation of a practice, and to extend research on practice variation. Typically, these studies investigate the variations that occur at adoption, focusing upon how dissenting organizations decouple their adoption or perform symbolic acts of adoption. Here we see that adoption may signal only the first wave of resistance, and that subsequent fluctuations in commitment may provide a greater influence over when and why the practice eventually collapses. In this way, analyzing commitment across time offers a way to unite studies of variations in adoption to recent work on abandonment and allows for a clearer portrait of the paths a practice may take.

Fourth, reimagining abandonment as a process offers us a means to consider the manner of abandonment along with the timing. This methodological refinement allows for a more realistic conceptualization of practice maintenance where managerial support may both rise and fall in response to their environment or internal data, and in non-monotonic patterns. Studying changes in commitment offers a new way to approach the process of deinstitutionalization, where a practice is neither replaced nor defeated but where the meaning of the practice is diluted across time.

Further research on this topic may allow us to identify a typology of abandonment patterns, and to connect the process of abandonment with discrete outcomes. An initial examination of the data included here suggests a relationship between the method of abandonment and ex post performance. For example a chi-square test reveals that firms that exited were committed for shorter durations (m = 8.68) and abandoned more quickly (m = 4.63) than firms that survived (m = 12.5; m = 9.22).

For institutional scholars, these findings help identify the conditions under which institutional pressure remains robust, even as performance signals grow clearer, and the conditions under which they are more readily ignored. This helps answer Oliver’s (1992) call for studies of the limits of institutional pressure, but it also helps to identify how normative pressure to abandon can replace the pressure to adopt or maintain.

For diffusion studies these findings indicate the need for investigation of the points between adoption and abandonment. Here I highlight how examining the decision to decommit separately from the decision to abandon helps explain the shift from institutional to performance based concerns. This suggests the value of further investigation into patterns of abandonment and their relationship to future performance. Finally, for strategy scholars these findings sound a cautionary note that managers, having committed to a practice, exhibit many of the same irrational forms of commitment found elsewhere, even as the performance data becomes clearer.

Historically, there has been more interest in the question of why practices are adopted than in why they are abandoned. If we accept that abandonment is purely rational, driven by an impartial interpretation of evidence of inefficiency, then this imbalance is justified. The results here indicate however that this assumption has led to a misunderstanding of how and why practices are abandoned. Redefining abandonment as a process in which managers adjust their level of commitment based on the confluence of internal and external influences offers a first step towards a remedy.

Limitations

There are a number of potential limitations to the findings at present that indicate the need for further investigation into the process of abandonment. First, the selection of historical data lead to the use of SIC codes to identify the industry in which an organization operated. One helpful reviewer pointed out that this SIC codes may misidentify industry boundaries or misrepresent who an executive considers their peer (Porac & Thomas, 1990). The results may therefore understate peer effects by discounting cross-industry influence.

Second, the inflection points defined above may not align with common understandings of the phrases. For instance, firms may reduce commitment with every intention of staying committed, only to later decide to continue to abandon. In this scenario, the point identified here as “decommitment” reflects a post-hoc characterization rather than the moment managers elected to decommit. Future ethnographic research could reveal how closely the commitment inflection points align with the conscious decisions of managers. At present, I cannot claim that the point captures a conscious shift in strategy but that changes in the direction of commitment provide valuable information about the process of abandoning.

Finally, there are two issues that may reduce the generalizability of the findings. The Fortune 500 is a nonrandom sample of firms and findings that hold in their case may not extend to the behavior of small or private companies. Also, although unrelated diversification is a useful case for the purpose of tying the findings closely to prior studies, the analysis may be limited by unseen peculiarities of the practice. In this case, the high cost and complicated nature of the diversification may reflect some portion of manager’s early reliance upon external cues. And the specifics of the practice—that it was intended as a hedge against regulatory challenges and poor performance in a core business—might explain the direction of the performance coefficients. Additional analyses could determine whether decommitment remains distinct from abandonment in other settings and for other practices. These are beyond the scope of the present article, but offer rich opportunities for future research.

Footnotes

Appendix A

Citations

Acknowledgements

This work benefited from the helpful comments of Lisa Cohen, Robert David, Dror Etzion, Neil Fligstein, and Heather Haveman.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.