Abstract

Despite predictions to the contrary, institutionally contested practices are sometimes disseminated broadly. Does diffusion indicate they have achieved legitimacy in the eyes of key constituents? The conventional view regards diffusion as a process of legitimization and suggests that unconventional practices gain legitimacy following diffusion. Building on recent studies that view diffusion as an outcome of political struggle, we instead argue that political contestation ramps up as controversial practices are disseminated, making it difficult for them to gain wide acceptance. Their diffusion threatens the stability of preexisting institutional arrangements, and constituents who remain supportive of the status quo react negatively. We test our argument by examining shareholders’ response to downsizing in Japan, a practice that is highly controversial given the deeply entrenched norm of lifetime employment. Our analysis of panel data on 1,791 Japanese firms between 1973 and 2005 shows that neither domestic financial institutions nor foreign investors responded positively to downsizing as it became broadly disseminated. Domestic financial institutions actually responded in increasingly negative ways in the 1990s, while they did not in the 1970s when downsizing was conducted within the framework of the long-term relationship between Japanese firms and their main banks. These results suggest that the relationship between diffusion and legitimacy can be contingent, in that the diffusion of institutionally contested practices can trigger reactions that differ from those of institutionally supported practices.

Introduction

Organizational institutionalists posit that organizations adopt new practices congruent with the broad cultural beliefs and norms shared by key constituents (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). Such practices, they argue, are seen as legitimate and thus rapidly diffuse across organizations (DiMaggio & Powell, 1983; Dobbin & Sutton, 1998; Edelman, 1990; Ruef & Scott, 1998); in contrast, practices that conflict with widespread beliefs and norms are seen as illegitimate and fall into disfavor (Davis, Diekmann, & Tinsley, 1994; Oliver, 1992). In this respect, the diffusion of institutionally contested practices, which are “new practices that face stiff opposition from key constituents in potential adopters’ primary institutional environment” (Sanders & Tuschke, 2007, p. 34), poses an intriguing theoretical challenge. Organizations that adopt contested practices can be seen as challenging shared beliefs and norms and thus face negative sanctions (Meyer & Rowan, 1977). Nevertheless, many examples of such diffusion exist. A timely example, which we will investigate in this paper, is the diffusion of the Anglo-American, shareholder-oriented system of corporate governance into countries with stakeholder-oriented systems (Aguilera & Cuervo-Cazurra, 2004; Ahmadjian & Robbins, 2005; Fiss & Zajac, 2004; Sanders & Tuschke, 2007).

Previous studies have demonstrated that the diffusion of institutionally contested practices is not unusual and have described how such diffusion can occur. However, they have left unexamined an important question: Does diffusion legitimize those practices in the eyes of key constituents? The conventional, cognitive view regards diffusion as the process of legitimization and thus suggests that even an unconventional practice may achieve legitimacy once it is widely diffused (Scott, 1995). In contrast, an alternative, political view suggests that diffusion can also be a contentious process where certain actors and groups attempt to promote practices that defy the preexisting institutional arrangements (Ahmadjian & Robbins, 2005; Briscoe & Safford, 2008; Dobbin & Dowd, 2000; Fiss & Zajac, 2004; Schneiberg, 2013). Further developing this political view on diffusion, we argue that the diffusion of institutionally contested practices can trigger reactions that differ radically from those of institutionally supported practices. The diffusion of controversial practices can intensify political contestation over their legitimacy, because their growing prevalence can be seen as a threat to preexisting institutional arrangements; as a result, it becomes difficult for them to gain broad acceptance from institutional constituents.

We test our argument by analyzing shareholder responses to downsizing in Japan. During the prolonged economic slowdown in the 1990s, even prominent Japanese firms began to engage in downsizing (Ahmadjian & Robbins, 2005). Downsizing, however, was at odds with the overarching stakeholder-oriented system of corporate governance, particularly Japan’s much vaunted practice of lifetime employment (Ahmadjian & Robinson, 2001; Dore, 1973; Ono, 2010). Downsizing defied not only the widespread public sentiment that companies should take care of their employees throughout their work lives, but also the firmly rooted belief that superior human resources nurtured through lifetime employment were a core strategic asset of Japanese firms (Aoki, 1988; Koike, 1995; Nitta, 1988). Downsizing was tolerated only when either the firm or the economy as a whole was in deep trouble (Kang & Shivdasani, 1997; Usui & Colignon, 1996). The question is whether the diffusion of downsizing in the 1990s helped mitigate the skepticism that prevailed against it. We examine how shareholders responded to downsizing and further investigate whether and how the diffusion of downsizing changed shareholders’ perceptions of it.

Japan provides us with a unique historical and political-economic setting in which to examine how contestation around a practice shapes the relationship between its diffusion and legitimacy. There were two waves of downsizing in postwar Japan, the first in the 1970s during the recession caused by two consecutive oil shocks and the second in the early 1990s during the economic slowdown after the bubble economy burst. During the 1970s, downsizing was adopted as an emergency measure and was implemented under the oversight of the main banks of companies who had cultivated long-term relationships with companies (Aoki & Patrick, 1994; Gerlach, 1992). Conducted within the framework of the Japanese system of corporate governance, downsizing in the 1970s was seen as necessary for the retention and revival of the traditional system. In contrast, during the 1990s, downsizing was seen as a challenge to the system. It was often conducted under pressure from foreign investors seeking enhanced profitability through reform of the traditional Japanese system (Ahmadjian & Robbins, 2005; Desender, Aguilera, Lópezpuertas-Lamy, & Crespi, 2016; Jacoby, 2007). Comparing these two periods, we examine the change in shareholder response to downsizing as it became increasingly widespread among Japanese firms.

In Japan two groups of shareholders had distinctive preferences: domestic financial institutions and foreign investors each supported opposing systems of corporate governance. Domestic financial institutions had long been integral to the stakeholder-oriented system, which promoted lifetime employment (Gerlach, 1992; Gilson & Roe, 1999; Sheard, 1994). They remained largely attached to the system even after the economic bubble burst (Hoshi, 1994; Jackson, 2003; Vogel, 2006). Hence, they were more likely to see downsizing as an institutionally contested practice. In contrast, foreign investors had no particular allegiance to the Japanese system. Instead, they promoted an alternative, the shareholder-oriented system (Ahmadjian & Robbins, 2005; Davis, 2009) and were less likely to worry about whether downsizing would be locally accepted.

Using data on 1,791 publicly traded Japanese firms, we analyze the responses of domestic and foreign investors to downsizing during the period between 1973 and 2005. Our results generally support our argument that diffusion may reinforce the legitimacy of only institutionally congruent practices but not institutionally contested ones. Although downsizing became more common among Japanese firms in the 1990s, it failed to gain acceptance, either from domestic financial institutions or from foreign investors. In the case of the former, their response actually became more negative as downsizing became more prevalent. These results suggest that institutionally contested practices must overcome considerable barriers to be accepted by key constituents, even after their widespread adoption.

Competing Views on the Relationship between Diffusion and Legitimization

Diffusion and legitimization, although sometimes treated as equivalents in empirical research, indicate distinct processes, and one does not necessarily lead to the other (Colyvas & Jonsson, 2011). Following Suchman (1995, p. 574), legitimacy is defined as “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions,” and legitimization is defined as the process through which a given practice attains legitimacy. Following Strang and Soule (1998, p. 266), diffusion is defined as the spread of a practice—a behavior, strategy, structure, or technology—within a social system. Studies have shown that a practice that conforms to prevailing norms, values, or belief systems is more likely to be diffused, and that in turn its diffusion can reinforce its legitimacy, thereby continuing a recursive cycle (Barley & Tolbert, 1997; Edelman, Uggen, & Erlanger, 1999; Haveman & Rao, 1997; Scott, 1995). It remains unclear, however, whether this kind of recursive dynamic between diffusion and legitimization also occurs for institutionally contested practices.

The diffusion of institutionally contested practices has recently drawn much attention because scholars recognize that it can be an important mechanism of institutional change. They are new or unconventional practices that defy preexisting, institutionalized prescriptions of what organizations should or should not do. Because organizational practices tend to organically evolve in such a way as to work hand in hand within a particular institutional context (Aguilera & Jackson, 2003), a new practice that does not follow prescriptions is likely to conflict with other practices and thus undermine their efficient operation. Hence, institutionally contested practices are vulnerable to challenges about their viability. Despite their lack of cognitive legitimacy, scholars show that such practices can be disseminated for various reasons. For instance, institutional entrepreneurs and social movements may promote innovative but controversial practices in order to challenge the status quo (Briscoe & Safford, 2008; Campbell, 2004; King & Pearce, 2010). In addition, powerful interest groups can pressure organizations to adopt practices that serve their special interests even when doing so goes against prevailing institutional arrangements (Ahmadjian & Robbins, 2005; Fiss & Zajac, 2004).

How then does the diffusion of institutionally contested practices improve their legitimacy in the eyes of key institutional constituents? There are competing views. A conventional view regards diffusion as a process of legitimization. Scott (1995, p. 114) suggests that diffusion of a given practice can be regarded as “increasing institutionalization” of the practice. Pushing this idea further, Haveman and Rao (1997) suggest that a duality exists between the diffusion of a new organizational practice and the strength of its underlying institutional arrangements, such that changes in one lead to changes in the other in a virtuous cycle. According to this view, the diffusion of an initially controversial practice can eventually enhance its legitimacy, by nurturing a sense of taken-for-grantedness for the new practice and by strengthening the alternative institutional arrangement that underlies the practice.

Evidence is mixed for the conventional view. On the one hand, studies of innovation provide supportive evidence. Organizations that adopt an innovative practice can initially suffer from penalties and negative evaluation from external constituents, but they subsequently experience fewer penalties and more positive evaluation once the number of defectors reaches a certain mass (Dobrev, Ozdemir, & Teo, 2006; Rao, Monin, & Durand, 2005; Sine, Haveman, & Tolbert, 2005). This suggests that diffusion of an unconventional practice can help external constituents overcome their initial suspicion and gradually embrace it. On the other hand, studies on the global diffusion of shareholder-oriented practices provide opposing evidence. Despite being widely diffused, such practices often fail to achieve legitimacy in the eyes of local constituents and remain controversial (Ahmadjian & Robbins, 2005; Fiss, Kennedy, & Zajac, 2012; Sanders & Tuschke, 2007; Zelner, Henisz, & Holburn, 2009). These latter studies suggest that when externally imposed practices directly challenge local norms, their diffusion may not attain broad support from local constituents and thus may fail to achieve legitimacy.

We argue that in the case of institutionally contested practices, their widespread diffusion can also intensify political contestation, by arousing negative reactions from groups that benefit from the status quo. Diffusion of organizational practices may not simply indicate acceptance of those practices, as had been suggested by earlier studies of diffusion. Instead, more recent studies show that diffusion can occur due to the political mobilization of an interest group attempting to institutionalize their preferred practices despite resistance from others (Ahmadjian & Robbins, 2005; Briscoe & Safford, 2008; Dobbin & Dowd, 2000; Fiss & Zajac, 2004; Schneiberg, 2013). When the latter is the case, wide diffusion may exacerbate political tension over the practices, making it difficult to achieve broad social support for them. If such practices are adopted by only a small number of organizations, they are unlikely to be seen as threatening and thus likely to be tolerated. Once a sizable number adopt them, however, they can be seen as posing a significant threat and trigger counter-mobilization from those groups aiming to maintain the status quo. The research on social movements provides many examples that show how the rise of social movements triggers counter-mobilization by groups that support the status quo (Ingram & Rao, 2004; McAdam, 1982; Meyer & Staggenborg, 1996; Schneiberg & Bartley, 2001). Such political struggle and tension may prevent institutionally contested practices from gaining legitimacy, particularly from those constituents who remain supportive of the preexisting institutional arrangements.

Diffusion of Downsizing and Shareholder Response in Japan

Downsizing in Japan provides a useful case to study how the institutional standing of a given organizational practice can affect the relationship between diffusion and legitimacy. We first describe two waves of downsizing, one in the 1970s and the other in the 1990s, and then provide our hypotheses regarding how domestic and foreign investors responded to the diffusion of downsizing during each wave.

Historical context: Two waves of downsizing in postwar Japan

Workforce downsizing contradicted the stakeholder-oriented system of corporate governance in postwar Japan, particularly the norm of lifetime employment. Japanese firms hired fresh high school or college graduates, trained them, and retained them until retirement. Employees, in return, invested in firm-specific skills (Aoki, 1988; Dore, 1973). Despite the norm of lifetime employment, particularly in large firms, downsizing was not uncommon in times of economic hardship (Usui & Colignon, 1996). During the two consecutive oil shocks in the 1970s, many Japanese firms engaged in downsizing under the guidance of their main banks (Sheard, 1985). During postwar economic development, major commercial banks served as stable shareholders who had a long-term commitment (Aoki & Patrick, 1994; Gerlach, 1992; Hoshi, 1994). This unique firm–bank relationship granted banks considerable input into managerial decision-making. During the oil crises, the main banks of struggling firms actively supported restructuring efforts (Kang & Shivdasani, 1997; Kaplan & Minton, 1994).

As an example, Pascale and Rohlen (1983) provide a detailed description of how the Sumitomo Bank guided the restructuring of Toyo Kogyo, the manufacturer of Mazda automobiles, from 1974 to 1980. The bank first announced that it would carry any new loans that Toyo Kogyo needed to support its restructuring; subsequently, it dispatched one of its executives, who assumed the title of executive vice president and oversaw the implementation of restructuring plans. The bank’s deep involvement reassured Japanese shareholders of Toyo Kogyo’s viability. Another study shows that when facing financial problems, Japanese firms with a strong relationship with their main banks were less likely to go bankrupt than those without such a relationship (Suzuki & Wright, 1985). Hence, although downsizing in the 1970s represented a significant departure from the highly regarded practices of lifetime employment and human capital investment, it was subject to little controversy because it was implemented within the framework of the traditional Japanese system of corporate governance, with the hope that firms would restore lifetime employment once the hard times ended.

Many Japanese firms turned again to downsizing when the economy stagnated during the 1990s, but this time the practice became highly contested. Unlike during the earlier wave, now downsizing was seen as a drastic departure from the traditional Japanese system rather than as a temporary deviation. Most importantly, many Japanese firms began to engage in downsizing without much support from the main banks. The complementary firm–bank relation significantly weakened over time, particularly after the real-estate market collapsed in the early 1990s, as banks were forced to sell off shares due to financial pressures (Hoshi & Kashyap, 2004; Jackson & Miyajima, 2007). New regulations further induced selloffs. The Act on Limitation on Shareholding by Banks and Other Financial Institutions, passed in 2001, limited a bank’s total shareholdings to an amount equivalent to its equity capital. 1 As a result, the percentage of shares held by Japanese financial institutions steadily decreased throughout the 1990s. In this process, banks lost their ability to monitor management, and the mutual commitment between banks and firms slowly shifted to a rational, financially motivated relationship (Schaede 2008). Reflecting this shift, bank interventions in financially distressed firms declined significantly, from 34 percent in the 1970s to 16 percent in the 1990s (Vogel, 2006, p. 128).

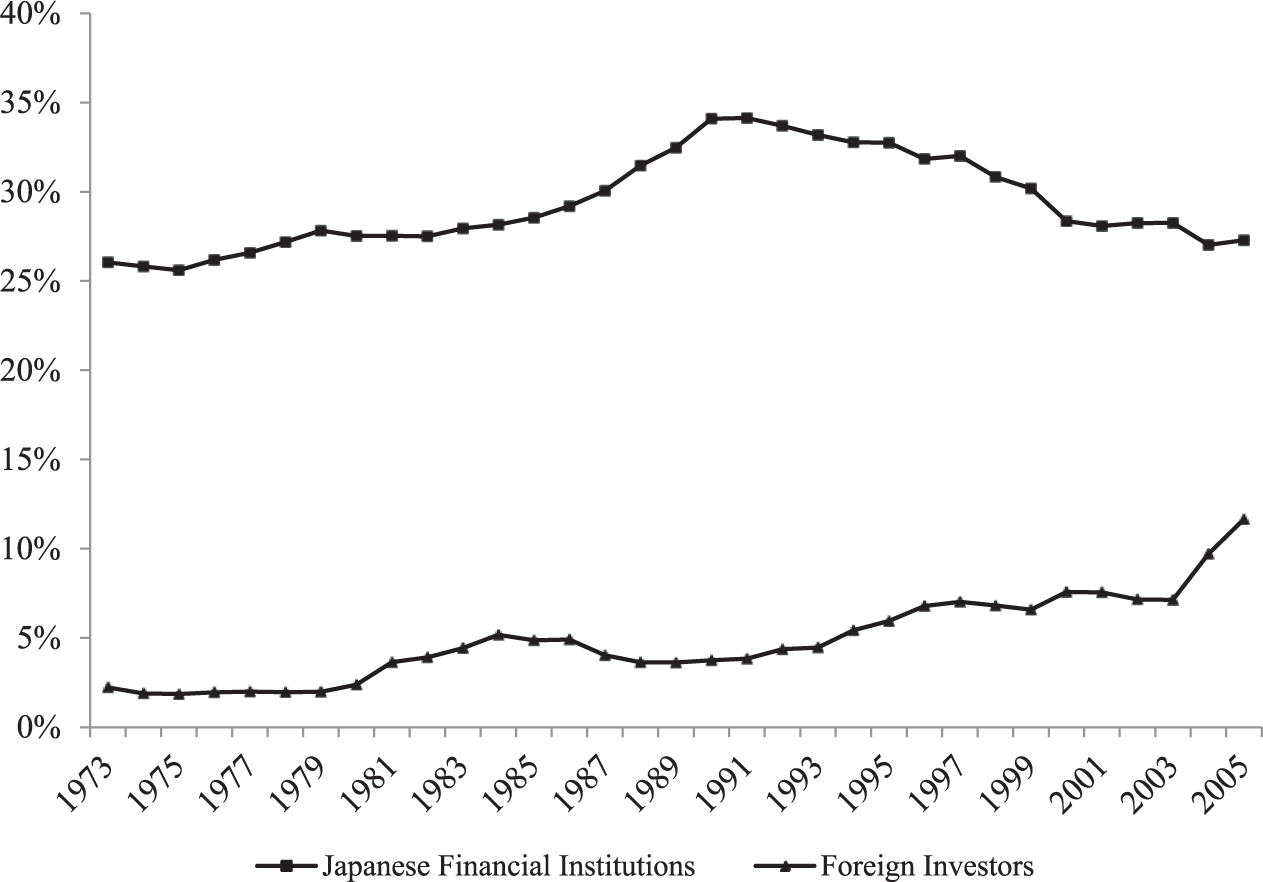

Downsizing was further contested because of the growing influence that foreign investors held over Japanese firms (Ahmadjian, 2007; Gedajlovic, Yoshikawa, & Hashimoto, 2005; Jacoby, 2007). Foreign ownership, having long been negligible in Japan, significantly increased beginning in the 1990s. Most foreign investors came from countries where a shareholder-oriented system of corporate governance prevailed, such as the United Kingdom or the United States, and did not share the stakeholder orientation of Japanese management that valued long-term commitment to and from employees. Some foreign investors pressured Japanese firms to downsize in order to enhance profitability (Ahmadjian & Robbins, 2005). Figure 1 presents average share ownership by Japanese financial institutions and foreign investors, respectively, for the firms in our sample during our observation period.

Average Share Ownership by Japanese Financial Institutions and Foreign Investors.

In this changed environment, downsizing was seen as a challenge to the traditional Japanese economic system. Conducted without active support from the main banks and under pressure from foreign investors, downsizing was perceived as a practice borrowed from the US-style liberal economy playbook, a practice based on the shareholder value ideology. It thus remained highly controversial, particularly among local constituents who were attached to the Japanese system and ambivalent about the shareholder-oriented system (Jacoby, 2005; Nitta & Hisamoto, 2008; Ono, 2010). Employees and labor unions were clearly against downsizing in general and layoffs in particular (Vogel, 2006), and even some business leaders were critical of the practice. Okuda Hiroshi, former president of Toyota and Japan Employers’ Association (Keidanren), publicly criticized layoffs and defended the virtues of lifetime employment; in his interview with Bungeishunjū, a popular monthly magazine that publishes political as well as literary commentary, in October 1999, he said to top managers, “If you axe your employees, you must kill yourself by seppuku 2 [Keieisha yo, kubi kiri suru nara seppuku seyo].”

Shareholder responses to downsizing

The distinctive historical contexts of the two waves of downsizing, as well as the contrasting roles played by domestic financial institutions and foreign investors, allow us to test the competing views on the relationship between diffusion and legitimacy in the case of institutionally contested practices. We first explain why we expect domestic financial institutions and foreign investors to respond differently to downsizing. We then discuss how their responses would be affected by the diffusion of downsizing during the 1990s, a period of institutional contestation.

Response of Japanese financial institutions

Japanese financial institutions had previously played a major role in guiding corporate restructuring. By the 1990s, their role weakened as the bank–firm relationship shifted. Due to the shift in their role in corporate restructuring, we expect that during the 1990s domestic financial institutions would be more wary of the viability of downsizing. Without financial support from the main banks, corporate restructuring might just fail. Downsizing could also hurt a firm’s long-term productivity by disrupting the unique Japanese system of human capital development. Moreover, most Japanese firms reactively engaged in downsizing (Lee, 1997). It is well known that reactive downsizing, downsizing after performance has declined, is likely to fail (Cascio, Young, & Morris, 1997; Flanagan & O’Shaughnessy, 2005; Guthrie & Datta, 2008; Love & Nohria, 2005). Investors were concerned that downsizing might be an act of desperation after other, less controversial, cost-cutting measures had been attempted. When Fujitsu (one of Japan’s leading manufacturers of personal computers, semiconductors, and communication equipment) announced its plan to eliminate 16,400 jobs, or nearly 10 percent of its global workforce, an analyst in Tokyo noted that the plan “smacked of an emergency evacuation” (Asahi Newspapers, 2001). We expect that domestic financial institutions responded negatively to downsizing in the 1990s when it was rare for the main banks to be deeply involved in firms’ restructuring efforts.

Hypothesis 1 (H1): Japanese financial institutions’ response to downsizing will be negative in the 1990s.

Response of foreign investors

We expect that foreign investors responded differently to downsizing. Before the 1990s, foreign investors were marginal players in the Japanese stock market, and thus had little influence over Japanese management. Since the 1990s, however, foreign investors have come to play a more prominent role, thanks to their increased ownership in Japanese firms (Ahmadjian, 2007; Desender et al., 2016). Unlike domestic financial institutions, they were not committed to the Japanese system of corporate governance or to the practice of lifetime employment. Most foreign investors came from liberal market economies such as the US, where the practice of cutting jobs to boost profits was an accepted business strategy (Budros, 1997; Jung, 2015; Lazonick & O’Sullivan, 2000). In fact, pressure from foreign investors to enhance profitability helped popularize downsizing by Japanese firms (Ahmadjian & Robbins, 2005). Hence, foreign investors were likely to respond positively, or at least not negatively, to downsizing, particularly during the 1990s.

Hypothesis 2 (H2): Foreign investors’ response to downsizing will be positive in the 1990s.

Diffusion of downsizing and shareholder responses

Finally, we examine how the diffusion of downsizing affected the responses of Japanese financial institutions and foreign investors. As for Japanese financial institutions, two competing predictions are possible. According to the conventional view that regards diffusion as a process of legitimization, the diffusion of an institutionally contested practice can gradually improve its legitimacy in the eyes of constituents who were initially skeptical. Therefore, the widespread adoption of downsizing by Japanese firms in the 1990s could improve local investors’ perception of the practice. Even if the diffusion failed to reverse the expected negative response from domestic financial institutions, it could mitigate their initial hostility by encouraging a sense that downsizing had become inevitable.

Our political view instead suggests that the diffusion of downsizing as an institutionally contested practice might not necessarily enhance its legitimacy. Rather, rapid diffusion can disrupt preexisting institutional arrangements and even trigger hostile reactions by groups who feel threatened (Ingram & Rao, 2004; Marquis & Lounsbury, 2007). Indeed, tension erupted as downsizing became pervasive among Japanese firms in the 1990s. For instance, when Nissan Motor Company, the third largest auto maker in Japan, announced that its 1999 restructuring plan would include plant closures and 21,000 job cuts worldwide, after a series of similar announcements by other major Japanese firms, then Prime Minister Obuchi Keizō and his cabinet members publicly chided the company for reneging on its obligations to employees, suppliers, and communities from areas surrounding the plants facing closure (Strom, 1999). Such tension would prevent downsizing from gaining support from Japanese financial institutions that were already worried that downsizing could hurt the long-term prospects of firms by undermining their human-resource-based competitive advantage (Aoki, 1988). Hence, the hypothesized negative response of domestic financial institutions in the 1990s is likely to become more negative as downsizing is diffused. This negative interaction effect, however, is unlikely to be observed for the 1970s when downsizing was not seen as contested.

Hypothesis 3-1 (H3-1): The expected negative response of Japanese financial institutions to downsizing in the 1990s will become more negative as the number of Japanese firms that engage in downsizing increases.

Foreign investors, on the other hand, might view the diffusion of downsizing in a different way. Unlike domestic financial institutions, foreign investors were supportive of neither the Japanese system of corporate governance in general nor the practice of lifetime employment in particular. The institutionally contested nature of downsizing in the Japanese context was unlikely to be a serious concern for them (Shimogori, 1999). Instead, they might see its diffusion as evidence of its effectiveness. As proponents of the norm of shareholder primacy, they favored downsizing as a means of maximizing shareholder value (Lazonick & O’Sullivan, 2000). Therefore, we expect that foreign investors’ response to downsizing would become more positive when downsizing became prevalent in the 1990s.

Hypothesis 3-2 (H3-2): The expected positive response from foreign investors to downsizing in the 1990s will become more positive as the number of Japanese firms that engage in downsizing increases.

Data and Method

We examine the responses from domestic financial institutions and foreign investors to Japanese firms’ downsizing. We present pooled cross-sectional time series models of share ownership by the two groups, using fixed-effects analysis. Our data cover a long span of time from 1973 to 2005, and thus include two waves of downsizing. Following our historical account of the two waves, we split the period into three subperiods—the period of the first wave during the oil shocks (1973–81) 3 , the boom period before the economic slowdown of the 1990s (1982–91), and the period of the second wave after the bursting of the bubble economy (1992–2005). We run separate sets of models for these three historical periods. Our primary interest is in comparing shareholders’ reactions in the first and the third periods, but we include the intervening period for comparison.

Sample

Our sample consists of all non-financial firms ever listed in the first section of the Tokyo Stock Exchange (TSE) between 1973 and 2005, for a total of 1,791 firms. This sample includes most major Japanese firms. The size of the sample differs each year because some firms entered after 1973 (typically because they were founded or went public after 1973), and others exited from the sample during the observation period (typically because they failed, were delisted, or were acquired during the observation period). Ultimately, 40,616 firm-years were used for analysis after cases with missing values were dropped; on average, firms in our sample contribute 23 years of data during the 33 years we observe. Our primary source of information for the sampled firms is the Nikkei NEEDS database, which provides financial information as reported in securities filings by all listed firms in Japan. This database has been widely used in previous studies (e.g., Ahmadjian & Robbins, 2005).

Variables

Dependent variables

To capture the evaluation of downsizing by domestic financial institutions and foreign investors, we analyze changes in share ownership by each group after downsizing. A growing body of research has shown that major institutional shareholders tend to sell shares when dissatisfied with the management (Admati & Pfleiderer, 2009; Chung & Zhang, 2011; Edmans & Manso, 2011; Parrino, Sias, & Starks, 2003). Our dependent variables are the percentages of shares of a given firm owned by Japanese financial institutions and those owned by foreign investors. Japanese financial institutions include commercial banks, trust banks, and insurance companies. As for foreign investors, we do not have information on their nationalities, but Ahmadjian and Robbins (2005, p. 456) report that foreign investors in Japan are mostly large American, European, or Australian corporations or institutional investors. 4 We acknowledge that changes in share ownership may not directly measure legitimacy; shareholders may liquidate their investment for various reasons other than legitimacy considerations. Nevertheless, studies on symbolic management have demonstrated that shareholders positively react when firms symbolically embrace institutionalized practices (Fiss & Zajac, 2006; Westphal & Zajac, 1998; Zajac & Westphal, 2004). Changes in share ownership can thus at least partly capture how different shareholders evaluate the legitimacy of downsizing.

Independent variables

Our main independent variable is a binary variable that indicates whether or not a company reduced the size of its workforce by more than 5 percent the previous year. 5 Hence, we define downsizing events as an actual decrease in the firm’s total workforce. Alternatively, one may use announcements of downsizing plans, as is common in other studies (e.g., Budros, 1997; Jung, 2015). Ahmadjian and Robinson (2001, p. 632), however, suggest that using public announcements may not capture actual downsizing rates by Japanese firms. Their investigation of downsizing announcements described in a major Japanese newspaper shows that such announcements refer mostly to proposed labor force reductions rather than actual downsizing events. Therefore, they suggest that counts of real reductions in a firm’s total workforce are a better measure than downsizing announcements.

In addition, we include a measure of downsizing density among all firms in our sample each year and its interaction with the indicator variable of downsizing events. This allows us to test H3-1 and H3-2 regarding how the diffusion of downsizing moderates the effect of downsizing events. Following Ahmadjian and Robinson (2001, p. 633), we measure downsizing density as the percentage of sampled firms, minus the focal firm, that engaged in downsizing during the previous three years.

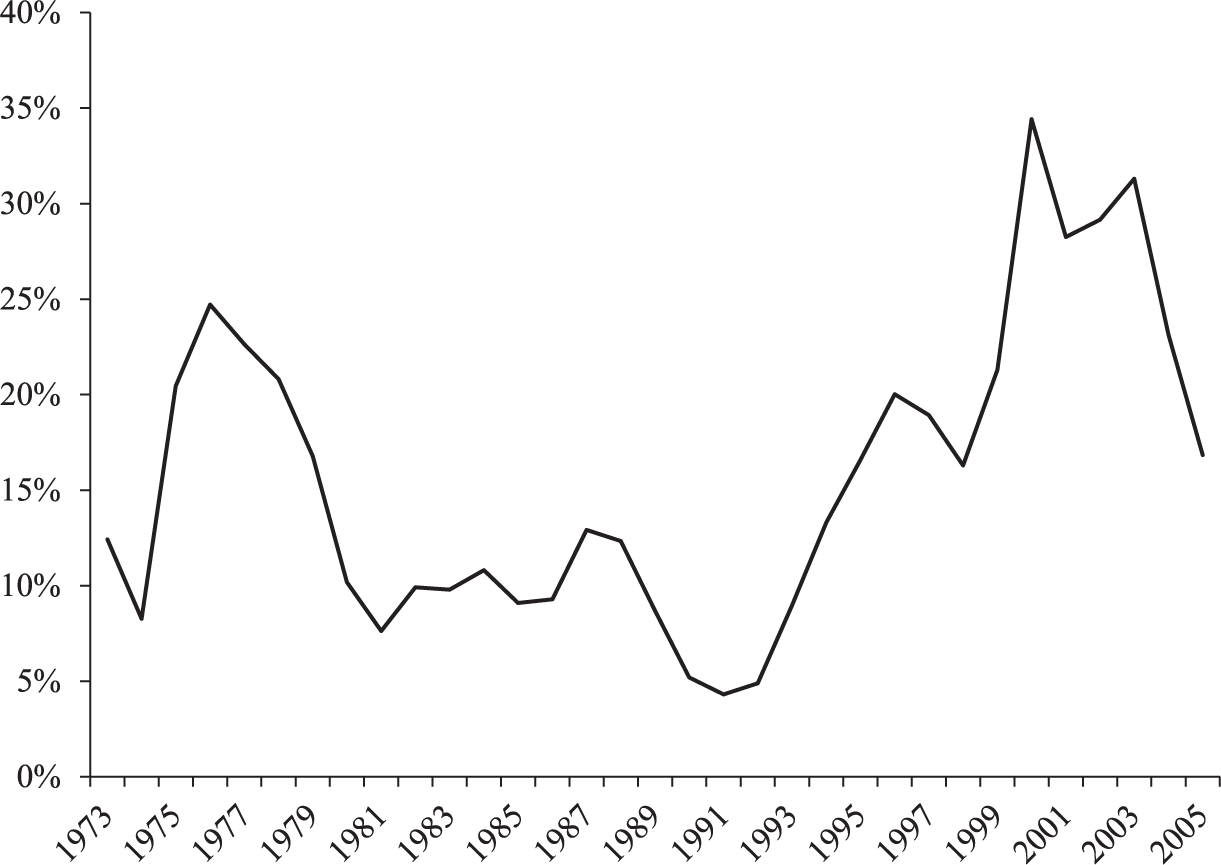

Figure 2 shows annual rates of downsizing from 1973 to 2005. As previously mentioned, two waves of downsizing occurred—one after the first oil shock in the early 1970s and the other after the bursting of the bubble economy in the early 1990s. During the 1980s, about 10 percent of firms in our sample engaged in downsizing; the increase in downsizing activity was striking after the early 1990s, surpassing the rate of the 1970s. It peaked, reaching almost 35 percent, in 2000, and then declined thereafter.

Annual Rate of Downsizing (5% or More Employees).

Control variables

We control for other factors that may affect both a company’s decision to downsize and shareholders’ decision to stay with or leave a given firm. Many of them measure pre-downsizing performance and financial conditions of the firm, and controlling for them helps mitigate the concern that shareholders withdraw their investment for reasons other than legitimacy considerations. Unless otherwise noted, all control as well as explanatory variables are lagged by one year.

First of all, we control for firm performance. Return on assets (ROA) is a widely used measure of operating performance and is defined as profits before taxes and extraordinary items divided by total assets. In order to account for industry-wide effects, we adjust the ROA variable by subtracting each company’s industry median in a given year. Industry-median ROA measures industry-wide performance; structural issues at the industry level may affect both a given firm’s decision to downsize and its attractiveness to shareholders. Volatility in firm performance, measured as the standard deviation of the ROA variable for the previous three years, is also included; volatility in performance may lead to a firm’s decision to downsize as well as to a reduction in ownership by risk-averse shareholders. Profit per employee measures the productivity of a firm’s workforce and is calculated as the ratio of a firm’s net profits to total employees. Finally, annual rate of sales growth is included; growth-oriented firms are unlikely to downsize.

We also include a set of measures of a firm’s capital and cost structure. Debt-to-equity ratio is a commonly used measure of a firm’s leverage structure and is calculated as total debt divided by total equity. Bank loan ratio is the ratio of bank loans to total debt and measures the extent to which a firm relies on bank loans. Self-financing ratio measures the proportion of fixed investment financed by retained earnings. Labor cost per employee measures the average labor cost of a firm, and is defined as the ratio of a firm’s total labor cost to total employees.

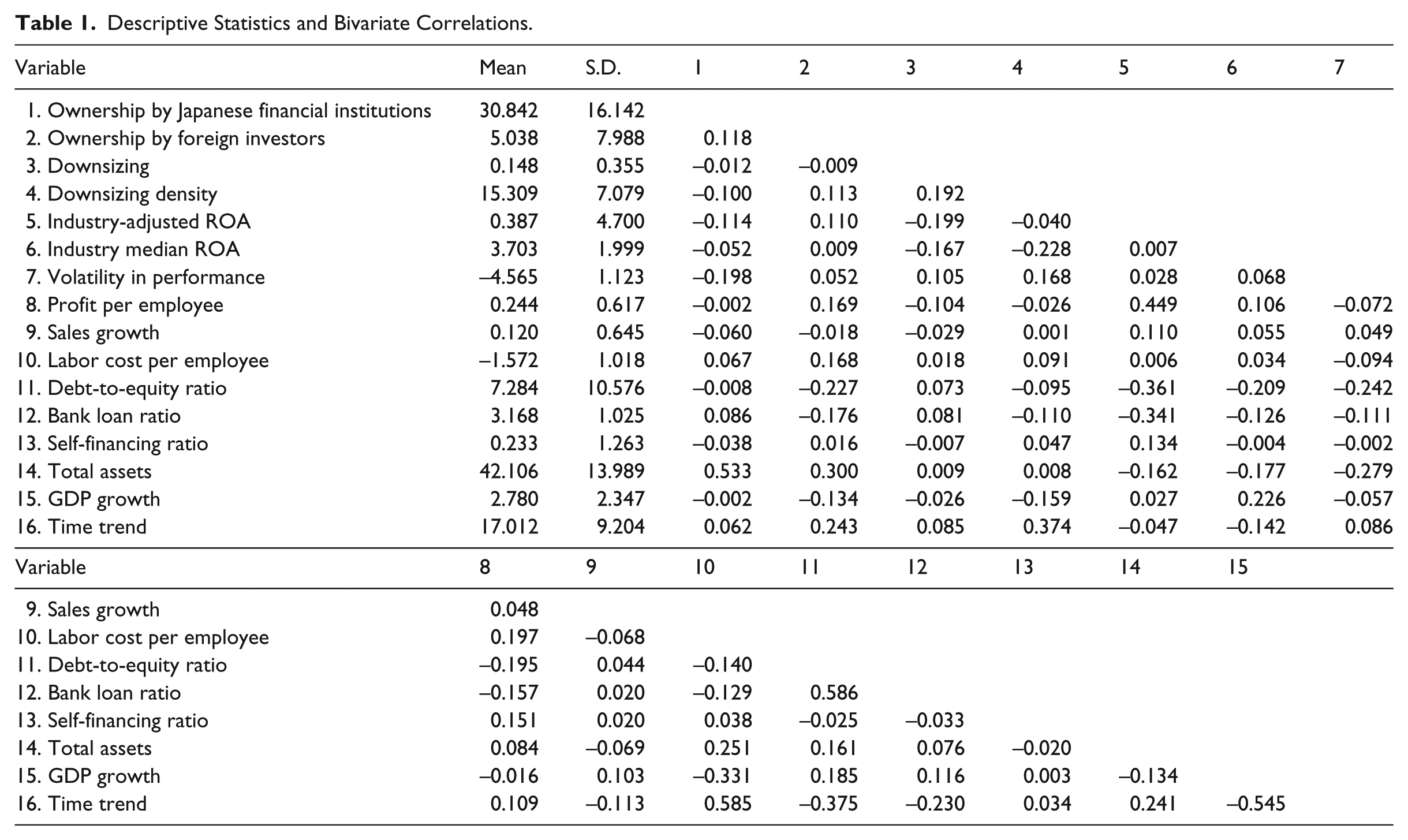

Firm size is measured by total assets. It is log-transformed because of its highly skewed distribution. Annual GDP growth rate is included to account for macroeconomic conditions that may affect both downsizing rates and ownership levels. Finally, we include a time trend variable to capture any unobserved historical trend in ownership by the two shareholder groups. Table 1 presents descriptive statistics and bivariate correlations.

Descriptive Statistics and Bivariate Correlations.

Estimation

We conduct fixed-effects analysis of share ownership by domestic financial institutions and foreign investors, respectively, with robust standard errors. The fixed-effects specification employs large numbers of parameters, rendering models less efficient than similar models without fixed effects, but it provides more stringent tests of hypotheses, because the firm fixed effects account for any time-invariant unobserved firm-specific characteristic (Allison, 2005). A significant coefficient suggests that a change in the independent variable (i.e., the occurrence of a downsizing event) is followed by a change in the dependent variable, the percentage of shares owned by either domestic financial institutions or foreign investors. In addition, the specification also offers an efficient means of dealing with non-constant variance of the errors, which derives from our use of multiple observations of each firm. Because our outcome variables are measured as proportions of the entire ownership, there can be interdependency between the two. In other words, their error terms are likely to be correlated. Seemingly unrelated regression accounts for interdependency among outcome variables and provides unbiased, efficient estimates (Zellner, 1962). Fixed-effects models of both domestic financial and foreign ownership are simultaneously estimated using seemingly unrelated regression.

Results

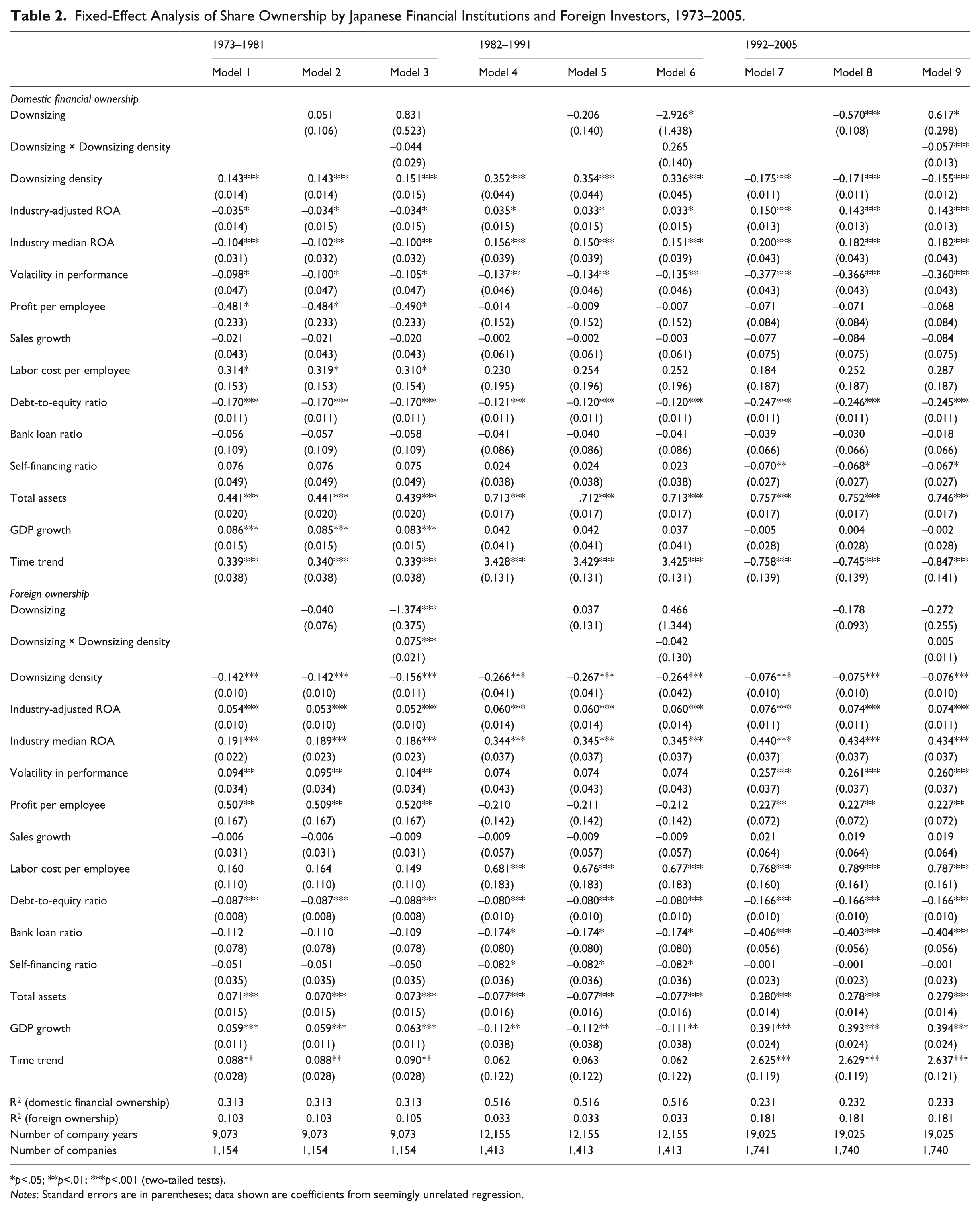

In Table 2, we present coefficient estimates from the fixed-effects analysis. For each model, the upper section presents the equation for domestic financial ownership; the lower section, the equation for foreign ownership. There are three sets of models for the periods 1973–81, 1982–91, and 1992–2005. For each set, the first model contains only control variables, the second adds the main term of the indicator variable of downsizing events, and the third adds its interaction with the downsizing density variable. Our models explain a considerable portion of within-firm variation in our dependent variables, especially in the last period; the explained variation increases from 32 to 52 percent for Japanese financial ownership and from 3 to 18 percent for foreign ownership.

Fixed-Effect Analysis of Share Ownership by Japanese Financial Institutions and Foreign Investors, 1973–2005.

p<.05; **p<.01; ***p<.001 (two-tailed tests).

Notes: Standard errors are in parentheses; data shown are coefficients from seemingly unrelated regression.

Concerning the response from Japanese financial institutions, we expected that they negatively responded to downsizing in the 1992–2005 period (H1). The results in Table 2 support this prediction; Japanese financial institutions significantly reduced their ownership stakes after downsizing. This result is compatible with our account that downsizing during this period was seen among local constituents as a highly contested practice. It was not the case in the previous two periods. During the oil crises in the 1970s and also during the 1980s, downsizing was not seen as contested because of the heavy involvement of the main banks. In contrast, during the 1990s and the early 2000s, firms engaged in downsizing without support from their main banks, leaving domestic investors wary of its effectiveness.

As for foreign investors, we expected that they positively responded to downsizing during the 1992–2005 period, given that they promoted downsizing in that period (H2). Our results do not support this hypothesis. Contrary to our prediction, foreign investors also significantly reduced their ownership stakes after downsizing.

We now turn to the interaction effect of downsizing and downsizing density and examine the relationship between diffusion and the legitimacy of downsizing. In the case of Japanese financial institutions, there is strong evidence to support our hypothesis that their response to downsizing became more negative when more Japanese firms engaged in downsizing in the 1992–2005 period (H3-1). Specifically, domestic financial ownership significantly decreased when downsizing density is high. A similar negative interaction effect was not observed for other periods. In fact, the interaction effect is positive for the 1982–91 period. The diffusion of downsizing in that period seemed to have triggered a legitimization process among domestic investors because downsizing, often supported by the main banks, was not seen as being in conflict with the traditional Japanese system of corporate governance. Also note that the main effect of downsizing density on domestic financial ownership became significantly negative during the last period. This implies that Japanese financial institutions generally reduced their ownership stakes when downsizing became widespread. This is another indication that downsizing was seen as institutionally contested among local institutional constituents in the 1990s.

Finally, contrary to our prediction in H3-2, there is no evidence to support our hypothesis that the response of foreign investors to downsizing would be positive when more Japanese firms engaged in downsizing during the last period. The null interaction effect in the final column of Table 2 indicates that foreign investors were unwilling to accept the legitimacy of downsizing when its legitimacy was contested by local actors. Although their response did not become more negative when downsizing became widespread, the null effect implies that there are considerable barriers that can prevent institutionally contested practices from achieving legitimacy even among institutional outsiders.

Control variables

As expected, both performance and financial status variables explain share ownership for both categories of shareholder. But the results reveal markedly different preferences between the two categories across the three periods. For instance, foreign investors strongly preferred firms whose profitability, measured as return on assets, increased. Japanese financial institutions appeared to have changed their preference over time; while they tolerated declines in profit during the 1970s, in subsequent periods they preferred firms with increasing profits. Domestic financial institutions avoided firms that demonstrated volatile performance, whereas foreign investors preferred such firms. Sales growth had little effect on either investor category. Interestingly, in the last period, foreign investors preferred firms with large labor cost per employee. These firms were likely to be firms that maintained well-paid workers with firm-specific skills. This pattern may suggest that even foreign investors favorably evaluated those Japanese firms that continued to invest in human capital development. Finally, both domestic and foreign investors preferred large firms and firms with less debt.

Robustness checks

We conduct several supplementary analyses to test the robustness of our findings. First, our measure of downsizing density treats all downsizing events as of identical importance. But downsizing by certain firms, such as large or profitable ones, may draw more attention from investors. In order to see if this is the case, we modify our density measure by counting downsizing events only by largest or most profitable firms, which are defined as firms within the top 10 percent in terms of either asset size or returns on asset, each year. Using these two modified measures of downsizing density, we find that the results are qualitatively the same as those in Table 2 (see appendices A and B). The response from domestic financial institutions for the 1992–2005 period became more negative when downsizing density increased among large or profitable firms.

Second, we predicted that domestic financial institutions responded negatively to downsizing during the 1992–2005 period, assuming that downsizing during that period occurred under pressure from foreign investors and therefore signaled firms’ departure from the traditional Japanese system of corporate governance. It is hard to directly test this assumption; we conduct an indirect test by considering the level of foreign ownership before downsizing events. We include foreign ownership in models of domestic financial ownership with two years’ lag and its interaction term with downsizing events. The results are consistent with our prediction: the response of domestic financial institutions was more negative for firms with sizable foreign ownership before downsizing (see appendix C). This finding suggests that domestic investors became skeptical about downsizing when it occurred, or appeared to occur, under pressure from foreign investors. Interestingly, the opposite was the case with foreign investors: their response was less negative for firms with sizable domestic financial ownership before downsizing. This suggests that foreign investors became less skeptical about downsizing when it was conducted within the framework of the long-term relationship between Japanese firms and their main banks.

Finally, we check for the possibility of reverse causality where changes in both domestic financial ownership and foreign ownership encouraged Japanese firms to engage in downsizing. To address the problem, we adopt an instrumental variable approach (Bascle, 2008). We utilize the longitudinal structure of our data to construct a set of reliable instrumental variables. We adopt as our instrumental variables downsizing events in the distant past, six to ten years before the observation point, assuming that investors responded to most recent downsizing events. The results show that the negative responses of domestic financial institutions and foreign investors in the last period, 1992–2005, remain significant (see appendix D).

Conclusion

For employees of major Japanese firms, employment used to last a lifetime. Many believed that this signature practice was the key to Japan’s postwar economic miracle (Aoki, 1988; Ouchi, 1981). As a prolonged economic stagnation followed the bursting of the bubble economy in the 1990s, however, this practice was increasingly criticized for being inflexible and hindering the recovery of the Japanese economy. Thus, although many Japanese firms initially held on to the practice, they began to depart from it one after another in the 1990s. One clear indicator was the spread of downsizing. According to Ahmadjian and Robinson (2001), one out of every two publicly traded Japanese firms, including prominent companies such as Fujitsu, Hitachi, and Nissan, engaged in some form of downsizing activity during the 1990s. The diffusion of downsizing among prominent Japanese firms, however, did not lead to a change in its perceived legitimacy in the eyes of significant local constituents. Our analysis demonstrates that, reflecting the institutionally contested nature of downsizing, domestic financial institutions responded negatively when Japanese firms engaged in downsizing. Strikingly, their response became even more negative as downsizing became more widespread in the 1990s.

Our findings contribute to the literature of diffusion, by revealing the gap between diffusion and legitimization of an organizational practice. Although these two processes are distinctive, they have often been conflated and treated as interchangeable (Colyvas & Jonsson, 2011). What makes it difficult to disentangle the two is the underlying assumption that they strengthen one another. Organizations try to adopt widely accepted practices to achieve legitimacy in the eyes of external constituents (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). Their adoption, then, further reinforces the legitimacy of those practices because their prevalence can be interpreted by other organizations as evidence of their legitimacy (Deephouse, 1996; Scott, 1995). In this diffusion-as-legitimization framework, failed or partial institutionalization—diffusion that did not achieve legitimacy—has been overlooked. Legitimacy-seeking may not be the only motivation for organizational adoption, and controversial practices can be widely diffused for political reasons (Ahmadjian & Robbins, 2005; Briscoe & Safford, 2008; Fiss & Zajac, 2004; Sanders & Tuschke, 2007). Thus, diffusion does not guarantee legitimacy. Our study shows that in the case of practices that remain controversial in the given institutional context, diffusion does not necessarily improve the cognitive legitimacy of the practices but can trigger even more negative reactions from key institutional constituents.

Our study demonstrates that the response of institutional constituents is an important missing link in previous diffusion studies that attended mostly to organization-side dynamics. There are many studies about how and why organizations adopt certain practices in order to achieve legitimacy from key constituents, but there are far fewer studies about how those constituents interpret and respond to the diffusion of practices. This gap is unfortunate because legitimization requires interaction between organization- and constituent-side processes. For instance, Johnson, Dowd, and Ridgeway (2006) propose a process model in which a practice gains legitimacy through four stages that include innovation, local validation, diffusion, and general validation. By including two validation stages, this model emphasizes the crucial role of the response from external constituents. Furthermore, by placing general validation as the last stage of legitimization after diffusion, their model also suggests that the relationship between diffusion and legitimacy depends critically on the response of diverse groups of constituents. In the case of downsizing by Japanese firms, its diffusion suggests that it gained local acceptance among similarly situated firms; without earning a positive response from domestic financial institutions, however, it seems to have failed to achieve wide acceptance.

Our study has implications for the recent debate regarding the role of institutional pluralism. The presence of competing institutional demands creates latitude for organizations to exercise some level of strategic discretion (Dhall & Oliver, 2013; Greenwood, Raynard, Kodeih, Micelotta, & Lounsbury, 2011; Pache & Santos, 2010; Quirke, 2013; Seo & Creed, 2002). Indeed, many Japanese firms could continue to engage in donwisizng throughout the 1990s despite mounting criticism, thanks largely to the increased stock ownership by foreign institutional investors who, unlike Japanese institutional investors, lacked a long-term, stakeholder orientation (Ahmadjian & Robbins, 2005). In this more complex institutional environment, Japanese firms seemed to have more leeway to embrace previously taboo practices in their bid to regain profitability during the prolonged economic slowdown. Nevertheless, our study also suggests a potential limitation of institutional pluralism. Although it may allow firms to have more leeway, the strategic choice made by firms may remain controversial and fail to be institutionalized (Besharov & Smith, 2014). In this case, greater leeway seems to come with the need to constantly justify the legitimacy of the chosen action.

Given the gap between diffusion and legitimacy reported in this study, more research is warranted regarding the mechanisms that may facilitate or inhibit the transition from mere diffusion to legitimacy. Our study suggests that there can be multiple possibilities in the case of controversial or unconventional practices; the diffusion of such practices may improve their initially weak legitimacy and lead to wider acceptance, but at the same time their diffusion can further expose their controversial nature and lead to more challenges to their legitimacy. It is beyond the purview of this paper to provide a complete list of possible mechanisms; instead, we highlight two factors based on our findings. One is the visibility of the given practice (Briscoe & Murphy, 2012). Downsizing was always a highly visible practice in Japan and received much (mostly negative) media coverage. We suspect that the rapid diffusion of downsizing in the 1990s further increased its visibility, and that the increased attention it received from the media intensified the political tension over its widespread use by Japanese firms. Another is the stance of dominant resosurce providers (Baum & Oliver, 1992). Downsizing was always highly controversial in Japan, but Japanese investors tolerated the practice before the 1990s because of the active involvement of the main banks, who were a major source of stability for Japanese firms. Their involvement in effect endorsed downsizing efforts by companies and helped give investors confidence in the practice.

There are several limitations of our study that warrant future research. We do not directly measure legitimacy; we infer it from shareholder reactions. Future research may develop more direct measures of legitimacy. Shareholders or other constituents may express their approval or disapproval of corporate decisions through other channels. In addition, focusing on shareholders and their relationships with firms, we do not consider other important constituent groups, such as employees and subcontractors. Analyzing their roles would provide a more comprehensive picture of the process of institutionalization described in this study. Finally, there can be an issue of generalizability. Some of our findings, especially the negative response of both foreign and domestic investors to downsizing, might reflect the unique historical and institutional context in Japan. Nevertheless, we believe that our findings can still provide useful insights for the development of future research. Even in countries where downsizing is considered an accepted business strategy, it is rarely welcomed by the public. The pervasive use of downsizing as a way to increase profit may thus invite backlash. Our discussion about diffusion as a process of political contestation can provide a useful theoretical lens to examine the dynamic relationship between diffusion, legitimacy, and resistance.

Footnotes

Appendix

Instrumental-Variable Regression.

| Domestic financial institutions |

Foreign investors |

|||||

|---|---|---|---|---|---|---|

| 1973–81 | 1982–91 | 1992–2005 | 1973–81 | 1982–91 | 1992–2005 | |

| Downsizing | 0.393 | −1.890 | −2.780*** | −2.311* | −2.169 | −2.216** |

| (1.273) | (1.378) | (0.799) | (1.047) | (1.300) | (0.702) | |

| Downsizing density | 0.151*** | 0.379*** | −0.167*** | −0.100*** | −0.305*** | −0.090*** |

| (0.019) | (0.051) | (0.013) | (0.015) | (0.048) | (0.011) | |

| Industry-adjusted ROA, t–1 | 0.023 | 0.009 | 0.086*** | −0.025 | 0.111*** | 0.035* |

| (0.030) | (0.023) | (0.017) | (0.024) | (0.022) | (0.015) | |

| Industry-adjusted ROA, t–2 | −0.016 | 0.007 | .067*** | −0.025 | −0.032 | 0.043** |

| (0.017) | (0.019) | (0.015) | (0.014) | (0.018) | (0.013) | |

| Industry median ROA | −0.060 | 0.134* | 0.093 | 0.039 | 0.342*** | 0.416*** |

| (0.069) | (0.059) | (0.054) | (0.057) | (0.055) | (0.048) | |

| Volatility in performance | −0.014 | −0.091 | −0.236*** | 0.223*** | 0.101* | 0.341*** |

| (0.060) | (0.053) | (0.048) | (0.049) | (0.050) | (0.042) | |

| Profit per employee | −0.596 | 0.467* | 0.136 | 1.437*** | −0.391* | 0.207* |

| (0.507) | (0.209) | (0.103) | (0.417) | (0.197) | (0.090) | |

| Sales growth | −0.045 | 0.097 | 0.061 | 0.008 | 0.022 | 0.082 |

| (0.055) | (0.079) | (0.089) | (0.045) | (0.075) | (0.078) | |

| Labor cost per employee | −0.127 | 0.532* | 0.904*** | 0.345 | 0.304 | 0.798*** |

| (0.259) | (0.254) | (0.218) | (0.213) | (0.240) | (0.191) | |

| Debt-to-equity ratio | −0.110*** | −0.061*** | −0.189*** | −0.112*** | −0.030* | −0.160*** |

| (0.016) | (0.013) | (0.013) | (0.013) | (0.013) | (0.012) | |

| Bank loan ratio | 0.108 | 0.075 | 0.094 | −0.069 | 0.017 | −0.550*** |

| (0.150) | (0.102) | (0.079) | (0.123) | (0.096) | (0.069) | |

| Self-financing ratio | 0.113 | 0.036 | −0.033 | −0.058 | −0.080* | −0.011 |

| (0.063) | (0.043) | (0.032) | (0.052) | (0.040) | (0.028) | |

| Number of employees | 2.612** | 0.550 | 1.239*** | −2.041** | −3.544*** | −1.809*** |

| (0.797) | (0.491) | (0.353) | (0.656) | (0.463) | (0.310) | |

| Total assets | 0.237*** | 0.643*** | 0.641*** | 0.243*** | −0.085*** | 0.335*** |

| (0.047) | (0.026) | (0.029) | (0.039) | (0.024) | (0.025) | |

| GDP growth | −0.043 | 0.020 | 0.047 | −0.006 | −0.104* | 0.451*** |

| (0.045) | (0.046) | (0.034) | (0.037) | (0.044) | (0.030) | |

| Time trend | 2.991*** | 3.687*** | −0.706*** | 0.015 | 0.038 | 2.829*** |

| (0.428) | (0.153) | (0.156) | (0.352) | (0.144) | (0.137) | |

| Constant | 5.936* | −4.959** | 5.443*** | 4.676* | 21.576*** | −3.975*** |

| (2.540) | (1.750) | (1.328) | (2.090) | (1.651) | (1.165) | |

| R2 | 0.223 | 0.481 | 0.221 | 0.046 | 0.040 | 0.136 |

| Number of company-years | 6,425 | 10,758 | 16,946 | 6,425 | 10,758 | 16,946 |

| Number of companies | 1,071 | 1,253 | 1,578 | 1,071 | 1,253 | 1,578 |

p<.05; **p<.01; ***p<.001 (two-tailed tests).

Note: Standard errors are in parentheses.

Acknowledgements

We thank Christina Ahmadjian, Frank Dobbin, Kim Pernell-Gallagher, Dan Schrage, Sameer Srivastava, Andras Tilcsik, and Hugh Whittaker.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.