Abstract

We examine how gender inequalities are reproduced through categorization processes in mainstream discourse. Drawing from an analysis of six years of US media coverage of credit card borrowers throughout the recent financial crisis, we show how categorization processes facilitate gender-based status differences by categorizing male and female credit card borrowers based on competence. We find that three dimensions of competence—savviness, responsibility, and agency—are constructed through two discursive mechanisms: accounts and vocabularies. Additionally, we highlight how vocabularies work to amplify stereotype-consistent accounts, yet undermine stereotype-inconsistent accounts. We contribute to research on institutional maintenance by highlighting the role of categorization processes in the reproduction of institutionalized relations of inequality. Further, we contribute to research on gender inequality by offering an in-depth examination of the micro-processes involved in the social construction of gender-based status differences. In this way, we shed new light on the cultural means through which gender inequalities are reproduced.

Introduction

In the aftermath of the global financial crisis and with the emergence of the Occupy movements worldwide, inequalities within the current economic system have re-entered the public debate (Oxfam, 2014; UN Women, 2014; United Nations, 2013). Research has pointed to the negative societal outcomes associated with inequality such as crime, political dysfunction, and social unrest (Neckerman & Torche, 2007; Stiglitz, 2012; Wilkinson & Pickett, 2009). In spite of these negative outcomes, inequality within the economic system—related to gender, race, ethnicity, and class—persists and is highly resistant to change (Castilla & Benard, 2010; Gray & Kish-Gephart, 2013; Putnam, 2015; Ridgeway, 2011; Tilly, 1999).

All durable relationships of inequality are rooted in institutions (Tilly, 1999). We view institutions as “rules and shared meanings that define social relations, help define who occupies what position in those relations, and guide interaction by giving actors cognitive frames or sets of meanings to interpret the behavior of others” (Fligstein, 2001, p. 108). Unequal social relations are therefore defined by societal rules, norms, and understandings. Thus, in order to understand how inequality persists, it is necessary to examine how the institutional underpinnings of inequality are reproduced. Indeed, as Lawrence and Suddaby (2006) note, “the real mystery of institutions is how social structures can be made to be self-replicating and persist beyond the lifespan of their creators” (2006, p. 234).

At the heart of institutionalized relationships of inequality is the privileging of one group of social actors over another (Ridgeway, 2011). Accordingly, understanding inequality and its persistence involves examining how social actors are categorized in a way that privileges certain groups over others in an ongoing manner. Though existing research on institutional maintenance has shed new light on the means by which institutions are reproduced through, for example, rituals (Dacin, Munir, & Tracey, 2010), rhetoric (Riaz, Buchanan, & Ruebottom, 2016), and narratives (Zilber, 2009), there has been limited attention to categorization processes, which may constitute another means through which institutional maintenance takes place (e.g., Martí & Fernández, 2013). In this paper, we unpack categorization processes critical to understanding the reproduction of institutionalized relationships of gender inequality.

The link between categorization and inequality has been highlighted in a growing body of research on the symbolic and cultural reproduction of gender inequality (Acker, 2006; Fenstermaker & West, 2002; Lorber, 1994; Ridgeway, 2011). As Butler (1990) states, categories of gendered social actors exist in a discrete “relationship of difference”: characteristics belonging to the category of men stand in direct opposition to characteristics belonging to the category of women (Schippers, 2007). These characteristics include gender-based stereotypes portraying men as “more proactive and agentically competent” and women as “more reactive and emotionally expressive” (Ridgeway, 2009, p. 149). Categorization formed on stereotypes of this nature works to reproduce gender inequality by creating gender-based differences in social status (Correll, 2004; Ridgeway, 2001; Ridgeway & Correll, 2006). Social status refers to “shared beliefs about the social categories or ‘types’ of people that are ranked by society as more esteemed and respected as compared to others” (Ridgeway, 2014, p. 3). We suggest that categorization processes are crucial to understand the reproduction of gender inequality since it is through these processes that status differences between genders are socially constructed and reproduced (Acker, 2006; Ahl, 2004; Ridgeway, 2011).

Though a large number of studies examine why categorization based on gender stereotypes creates gender-based status disparities, there has been much less research on how this occurs (Ridgeway, 2011, 2014). As Ridgeway (2014) argues, in addition to describing inequality, “we want to understand the deeper problem of how inequality is made and, therefore, could potentially be unmade” (2014, p. 1). Specifically, there is a need for analysis of the micro-processes and mechanisms underlying stratification (Reskin, 2000; Ridgeway, 2014; Roscigno, Garcia, & Bobbitt-Zeher, 2007). In this study, our objective is to address this gap in the literature.

We situate our study in the financial realm of the United States. The financial realm is a critical aspect of socio-economic life for most people (see Dymski, Hernandez, & Mohanty, 2013; Espino, 2013; Floro & Dymski, 2000; Fukuda-Parr, Heintz, & Seguino, 2013; Lee, 2014; Roberts, 2015). Research in the area suggests that in an increasingly “financialized” economy (Davis & Kim, 2015), understanding how inequality is manifested in the financial realm—including spending, credit, and debt—can offer substantial insights into inequality’s persistence (Fligstein & Goldstein, 2015; Mahmud, 2012; Rajan, 2012). In particular, consumer debt is a focal point for studying issues of inequality because terms of debt contracts and access to debt are closely linked to underlying societal inequalities (LeBaron, 2014; Riaz, 2016; Roberts, 2014). Research on gender inequality in the financial realm has focused on structural and material aspects but has given limited attention to cultural aspects. Building upon insights on the importance of credit and borrowing in this literature, we examine media discourse surrounding consumer debt over a six-year period across the recent financial crisis in the US as a means to investigate the cultural reproduction of gender inequality.

Our findings elucidate how categorization processes in media discourse about consumer borrowing construct gender-based status differences in the financial realm. In particular, we illustrate how categorization processes dichotomize male and female credit card borrowers according to their competence through two micro-discursive mechanisms: (1) accounts of savviness and accounts of responsibility, and (2) vocabularies of agency. In doing so, we make two major contributions. First, we contribute to research on institutional maintenance by uncovering the key role of categorization processes in the social construction of gender hierarchies. In this way, we shed new light on how institutionalized relations of inequality are reproduced and open up new avenues for research in the area. Second, we contribute to research on gender inequality by elucidating mechanisms through which status-based gender differences are discursively constructed and reproduced. In doing so, we extend the body of research that has recently turned to the cultural processes involved in the persistence of inequalities.

Categorization, Gender Stereotypes in Media, and Inequality

Categories are culturally grounded cognitive schemas that are socially constructed through discourse (Cornelissen, Durand, Fiss, Lammers, & Vaara, 2015), operate as “prototypes or causal models” (Ocasio, Loewenstein, & Nigam, 2015, p. 31), and “furnish a repertoire of meanings” (Glynn & Navis, 2013, p. 19) to actors. Categories shape what is socially valued and create boundaries that “demarcate who and what is included or excluded within a category” (Jones, Maoret, Massa, & Svejenova, 2011, p. 1524). Stable category meanings can operate as “constructs of comparability” (Khaire & Wadhwani, 2010, p. 1283), where some categories are deemed more legitimate and socially powerful than others (Glynn & Navis, 2013). As such, we follow Keller and Loewenstein (2011), who argued that categories are “generated by cultural groups for labeling and grouping sets of objects, material practices, social actors, and other socially-experienced examples” (2011, p. 299). For instance, mutual funds are categorized into high and low risk (Lounsbury & Rao, 2004), films are categorized into genres and sub-genres (Hsu, 2006), and architecture is categorized into different styles (Jones et al., 2011). Such categorization adds a sense of organization and coherence to the world by “partitioning items into groups” (Vergne & Wry, 2014, p. 58).

As scholars of gender have observed, social actors are also subject to categorization processes. In particular, a large body of research describes gender stereotypes and the role of media in the employment of stereotypes in the categorization of men and women (e.g., Chavez, 1985; Coltrane & Adams, 1997; Gauntlett, 2008; Jones, Murrell, & Jackson, 1999; Vincent, 2004). Media is important for understanding the reproduction of gender inequality because of its influence in shaping public opinion (Clemente & Roulet, 2015). Media outlets “make sense of ‘realities out there’” (Risberg, Tienari, & Vaara, 2003, p. 123) and play a central role in “sensegiving” since they report on and offer commentary on these realities for their audiences (Gioia & Chittipeddi, 1991).

The literature on gender stereotypes in US media is wide-ranging and striking. For example, Coltrane and Adams (1997) analysed television advertisements and found that women were less likely to exercise authority or display active/instrumental behaviors and more likely to be portrayed as sex objects. Jones, Murrell, and Jackson (1999) examined print media coverage of Olympic athletes and found that female athletes were often portrayed based on physical appearance whereas males were portrayed based on degree of strength or power. In Chavez’s (1985) analysis of comic strips, she found that both women and men were presented in stereotypical roles that privileged men. These studies show that US media reproduces socially constructed, categorical differences between males and females.

These categorical differences are important because once categories or “types” of people are established and certain categories are privileged over others, it can lead to durable differences in social status between groups (Correll, 2004; Eagly & Steffen, 1984; Ridgeway, 2011, 2014; Rudman, Moss-Racusin, Phelan, & Nauts, 2012). Scholars have recently suggested that research on inequality needs to examine status in more detail since doing so can provide insights into the cultural reproduction of gender inequality that more structural accounts cannot capture (Ridgeway, 2011, 2014). Status beliefs essentialize differences between categories of social actors, thus drawing more focus toward these simplistic differences, and in some cases, amplifying them (Tilly, 1999). Even when men and women occupy the same material position (e.g., job, income, athletic position), gender-based status differences allow men to still exert more influence than do women (Eagly & Carli, 2007).

A central reason why differences in social status are important to gender inequality is that actors in high-status categories are likely to be viewed as more competent than actors in low-status categories (Fiske, Cuddy & Glick, 2007; Fiske, Cuddy, Glick & Xu, 2002; Foschi, 1992; Wood & Karten, 1986). Competence focuses on the degree to which an individual possesses the ability, knowledge, and skill to successfully complete a task (Fiske et al., 2007). Since men enjoy a higher social status than women, they are perceived as being more competent (Biernat & Kobrynowicz, 1997; Wood & Karten, 1986). Though research has established that status is associated with perceptions of competence, what is less understood is how status and competence-based differences between men and women get reinforced and reproduced (Ridgeway, 2011, 2014). Our study builds on calls for ‘“mechanism-oriented’ analyses of gender stratification and its origins (Reskin, 2000), and explorations of the micro-processes that reinforce gender inequality” (Roscigno et al., 2007, p. 18). Specifically, we ask: How do categorization processes in mainstream discourse reproduce gender-based status differences? We explore this question in the context of media coverage of consumer debt in the United States.

Research Context and Methods

Research context: Credit card borrowers in US newspapers, 2005–2011

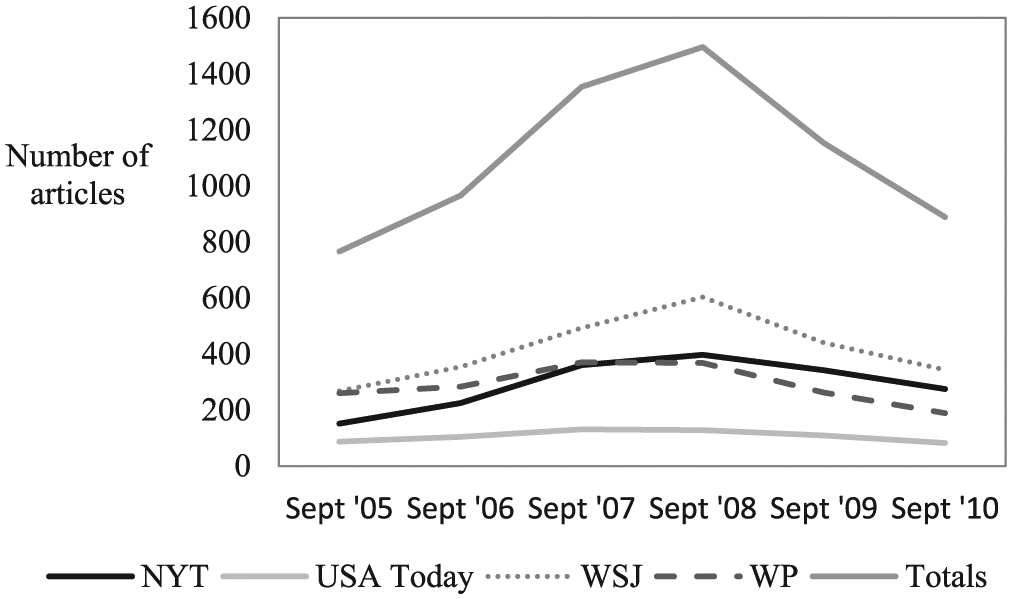

Consumer debt has become a taken-for-granted part of American life over the last 40 years (Davis, 2009). In 1970, only one sixth of US households had bank-issued credit cards as compared to two-thirds of households in 1998 (Hyman, 2012). However, with the onset of the recent financial crisis, there has been increasing public attention on consumer debt and borrowing as central components of the crisis (Hodson, Dwyer, & Neilson, 2014; Davis, 2009; Soederberg, 2013). During this period, stories about credit cards and credit card borrowers became a dominant part of mainstream discourse surrounding the crisis. Figure 1 shows the increase in media coverage of credit card debt during this period.

Coverage of credit cards in selected outlets.

This context provided us with an ideal opportunity to study portrayals of gender in mainstream discourse in an important socio-economic context. An emerging body of research focuses on gender inequality in the financial realm (Dymski et al., 2013; Espino, 2013; Floro & Dymski, 2000; Fukuda-Parr et al., 2013; Lee, 2014; Roberts, 2015). While this literature primarily focuses on the broad implications of financialization on gender inequality, we extend this literature by focusing specifically on how portrayals of actors—namely, credit card borrowers—reproduce gender inequality. Managing debt in the current financialized economy is a key attribute for socio-economic success (Davis, 2009; Mahmud, 2012). Accordingly, the status of actors in the realm of debt and credit is likely to impact both access to credit as well as the terms of contracts (LeBaron, 2014; Riaz, 2016; Roberts, 2014). In this regard, how male and female credit card borrowers are portrayed in the media with respect to their competence in managing debt can compound gender inequality.

The specific time frame for our analysis is appropriate for a number of reasons. Our focus on the issue of consumer debt is a particularly good fit with the context of the financial crisis, when media discourse on this topic increased substantially. From a practical standpoint, the increase in media coverage of credit card borrowers during the crisis provides us with an opportunity to see how categorization processes reproduce gender stereotypes in and around the issue of consumer debt, with important implications for gender inequality in the financial realm and beyond.

Importantly, this time period allows us to examine gender inequality in the background of the broader crisis. Faced with the immediate task of reporting on a complex unfolding crisis about debt and financial institutions, there would be little time or motivation on the part of journalists to recognize and question implicit biases about gender status. This is advantageous for our purposes since stereotypes are more likely to be employed in cases when the object of the stereotype—in our case, gender—is not the primary focus. While there may be explicit attempts to understand or question long-standing assumptions regarding debt during the crisis, gender-based explanations were not part of the larger story during this period. However, gender is still present as an orienting variable to “categorize and make sense of one another” (Ridgeway, 2009, p. 146) that is written into our language system (i.e. through use of gendered pronouns, he or she). Thus, reporting on gender occurs at an implicit level through the use of pronouns, without the need to bring it into the realm of the explicit. Implicit biases and stereotypes would therefore be retained in reporting on gender and our context is well suited to study these.

Research design and data

We use qualitative content analysis (Krippendorff, 2004; Suddaby & Greenwood, 2005) to explore the link between mainstream discourse and gender inequality, analysing media texts about credit card debt from 2005 to 2011. We also take cognizance of key ideas from critical constructivism (e.g., Holstein & Gubrium, 2011; Zilber, 2006), albeit in a manner limited to the focus of our study. The primary insight from critical constructivism that we draw upon is that existing institutions (i.e. taken-for-granted rules, norms, and assumptions) and power relations in the US context play a key role in how gender is socially constructed in mainstream discourse (Kincheloe, 2005). This line of thinking informed how we engaged with the data throughout the analysis. Specifically, we recognized the continued stereotypes in the early 21st century US society related to gender and a simultaneous attempt at political correctness that prevents invoking gender and other demographic stereotypes (e.g., race, class, age) in an explicit manner when talking of competence and status. However, many norms and assumptions surrounding gender still operate implicitly and can be revealed through a systematic analysis of language and discourse. Examining categorization processes of gender in mainstream media thus allows us to observe societal rules, norms, and understandings about inequality that may not be immediately visible, and thereby helps us reveal processes through which institutionalized relations of inequality are maintained.

We analysed texts from four mainstream US news outlets that each have national coverage: New York Times, USA Today, Wall Street Journal, and Washington Post. Our six-year time frame allowed us to explore mainstream discourse starting two years before the crisis emerged and until two years after the peak of the crisis. See Table 1 for an overview of the news outlets included in the sample.

Overview of data.

Weekday circulation as of March 2013, including both print and digital subscriptions.

Using the Factiva database, we searched the keywords “credit card” and “consumer” or “borrower” in order to find relevant articles that focused not only on credit cards, but also on individuals who use credit cards. We started with an initial sample of texts from the six-year period surrounding the crisis (five articles per month per outlet, September 2005–August 2011) and observed that earlier years had limited media discourse on consumer and credit card debt. The discourse became more salient during the years of the crisis; accordingly, we collected more articles for this time period to capture the most relevant discourse (100 articles per year per outlet, September, 2009–August, 2011). One outlet had fewer than 100 articles per year that met our search criteria, giving us a total sample of 2,623 articles.

Data analysis

Our analysis unfolded in three inductive and iterative phases. In the first phase, we isolated text segments where individual borrowers were mentioned in the media. During this phase we coded borrowers on any demographic dimensions mentioned, including gender, race, age, and class. Gender was observable on a large scale because of the required use of pronouns (e.g., he/she, him/her), while other demographics were silenced likely because of the emphasis on political correctness at this time in US history, which prevents explicit attribution of circumstances to gender, race, class or age. We ended up with 1,621 instances where individual borrowers were discussed. We then inductively coded these borrower segments for several variables that seemed to differ based on gender, keeping in mind the work of Fiske (1993) and colleagues (Fiske et al., 2002, 2007), as well as Connell (1987, 1995, 2002) on gender stereotypes. Specifically, we focused on attributions of blame or praise, coding for the reasons given for the borrower’s situation. For example, “She’d blow her tax refunds on shoes or a vacation to Miami—and wonder, a couple of months later, where all the money had gone” cast blame on the woman for “non-essential purchases” and “lack of knowledge”. Whereas, “When Peter Means returned to graduate school after a career as a civil servant, he turned to a debit card to help him spend his money more carefully” praised the borrower for their “responsibility”. We coded various borrower behaviors (e.g., “making timely payments on a Wells secured credit card” and “made a lot of poor financial decisions”) or traits (e.g., “one of the savviest card users I know”) and the way situations were characterized (e.g., “was a victim of a debt settlement company”).

Early coding included borrowers’ culpability, degree of self-control, responsibility, savviness, self-sufficiency, whether the borrower was portrayed as a victim, and the nature of purchases, all of which were prevalent themes in the media sensemaking to explain borrower debt during the financial crisis. Through discussions, self-control and the nature of purchases were combined with “responsibility,” and culpability, being a victim, and self-sufficiency were combined with “savviness” because of conceptual overlap between the labels. Similarly, we resolved all other disagreements in coding through a series of discussions. What became evident through these conversations is that relevant codes for understanding credit card borrowers in the financial crisis were dichotomous: borrowers were presented either as responsible or irresponsible, savvy or unsavvy. We then re-coded text segments to flesh out these emerging themes.

In phase two of the analysis, we explored differences between themes for men and women. Common to all descriptions of individual borrowers in our data were brief details that explained the particular circumstances along with some biographical information. Following other studies (e.g., Elsbach, 1994; Khan, Munir, & Willmott, 2007), we labeled these as “accounts.” These accounts primarily consisted of a quote from the consumer with surrounding text inserted by the journalist. In most cases, the quote and surrounding text supported the same theme and thus there were very few instances where we needed to tease out what theme was dominant in a particular account. Similar to Riad and Vaara’s (2011) study of the media accounts of international mergers and acquisitions, we calculated the frequencies of the types of accounts used in relation to each gender, for savviness and responsibility, to uncover differences between men and women. We found that differences were consistent throughout the time period of our sample. We then checked to see if the differences identified were related to journalist gender and found that male and female journalists both stereotyped consumers. 1

In phase three, we delved further into the emerging categories using an inductive analysis of vocabularies used to construct various subject positions (Alvesson & Karreman, 2000; Foucault, 1972). We coded account segments (excluding direct quotes from the consumers) for the types of verbs, adjectives, and emotion words used in reference to borrowers, comparing between genders. We bolded all strong, active words (e.g., “negotiating,” “decided,” “runs,” “demands”) and underlined weak, passive words (e.g., “trying to,” “had to,” “fell behind,” “concedes,” “took a hit”). It became immediately apparent that the strength of verbs, adjectives, and emotions presented another type of difference between men and women. For example, the vocabulary in descriptions of male borrowers more often used strong action verbs, while female borrowers were more often described using passive verbs. We then compared vocabularies within the categories of savviness and responsibility and found that gender differences appeared even within the same category (e.g., comparing between savvy men and savvy women). We aggregated verbs, phrases, and emotions under the label “vocabularies of agency.” We then calculated the ratios of “strong-form: weak-form” agency for both men and women and compared strong-form agency versus weak-form agency within each type of account: savvy, responsible, unsavvy, and irresponsible. 2 By doing so, we found that stereotype-consistent accounts (such as savvy men and unsavvy women) were amplified, and counter-stereotypical accounts (such as unsavvy men and savvy women) were undermined through vocabularies of agency.

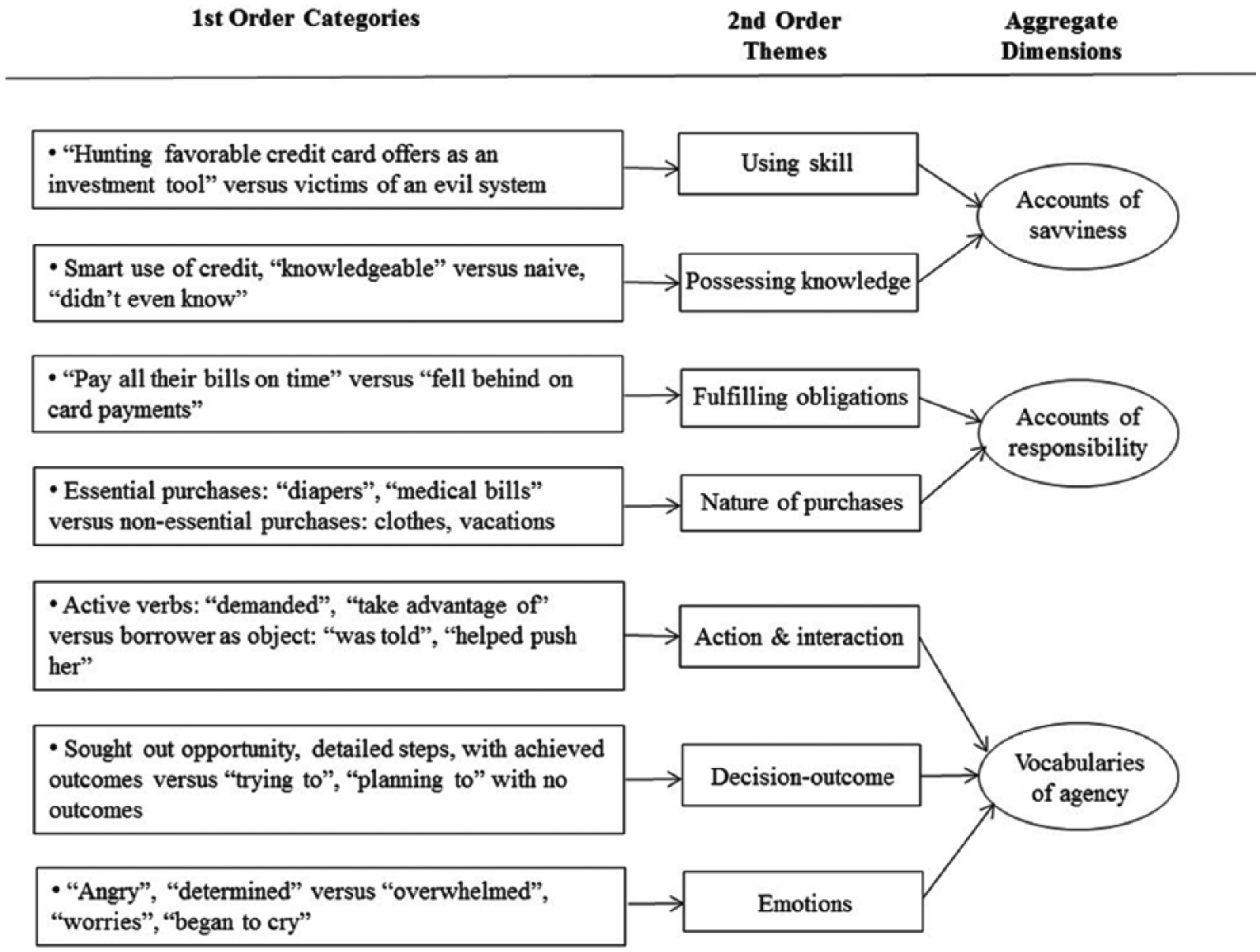

In sum, our analysis revealed three aggregate dimensions of borrower competence—accounts of savviness, accounts of responsibility and vocabularies of agency—that differed along gender lines. Figure 2 displays our final data structure.

Data structure of borrower competence: savviness, responsibility and agency.

Findings: Categorizing Competence in Media Discourse

Our findings reveal how categorization processes in mainstream discourse constructed the competence of borrowers in managing credit card debt. We specifically uncover the way different dimensions of borrower competence—savviness, responsibility, and agency—are constructed in media discourse and differentially patterned along gender lines. We reveal two mechanisms through which this competence was constructed: accounts and vocabularies.

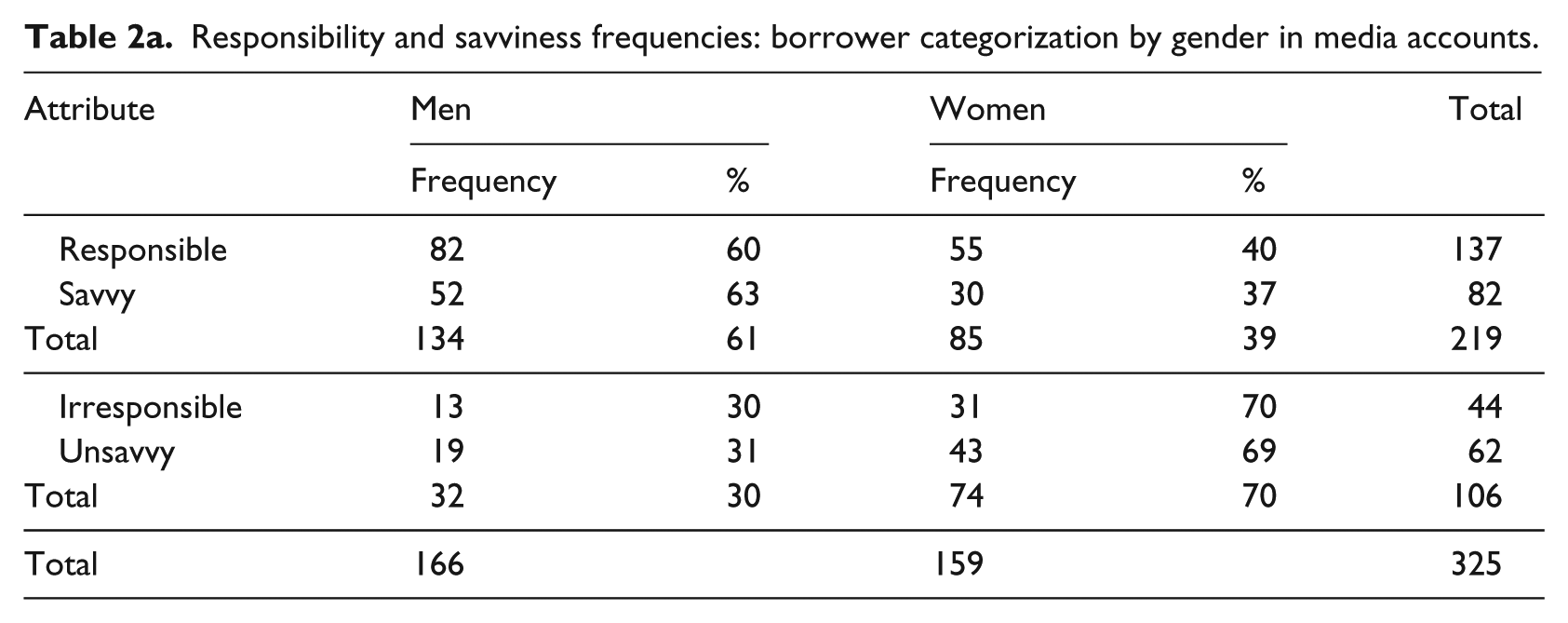

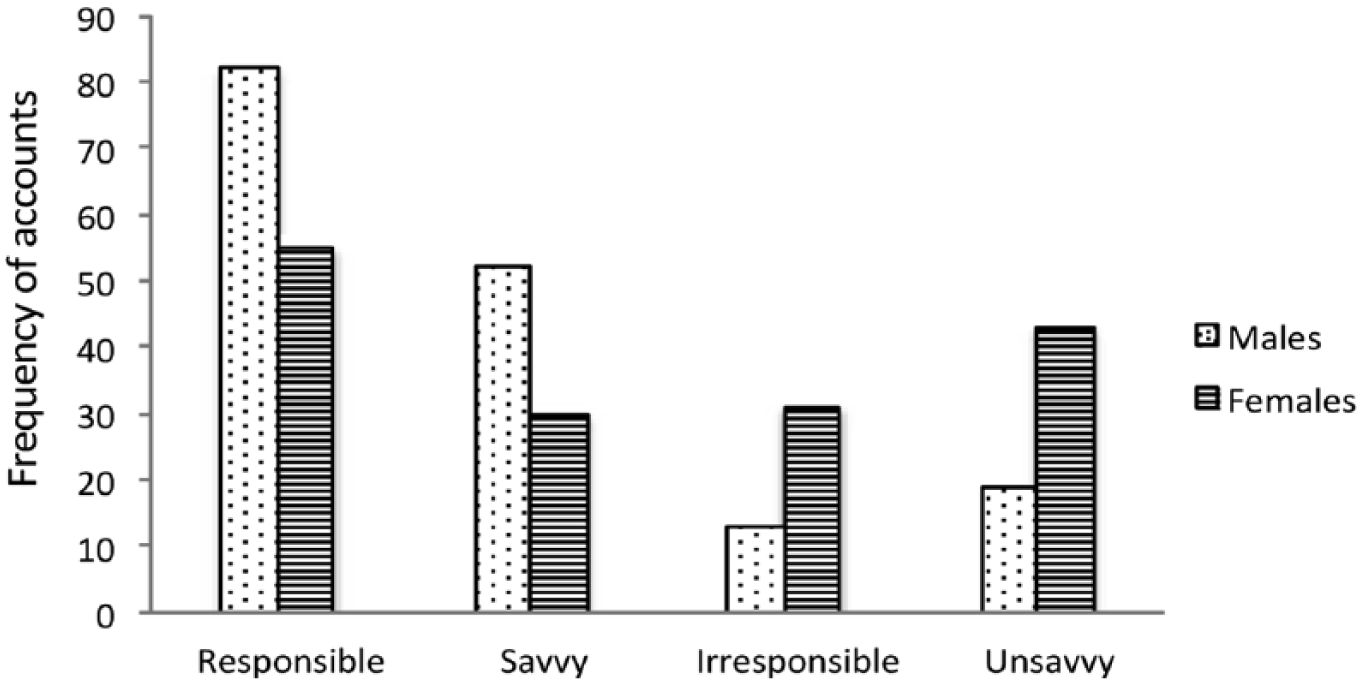

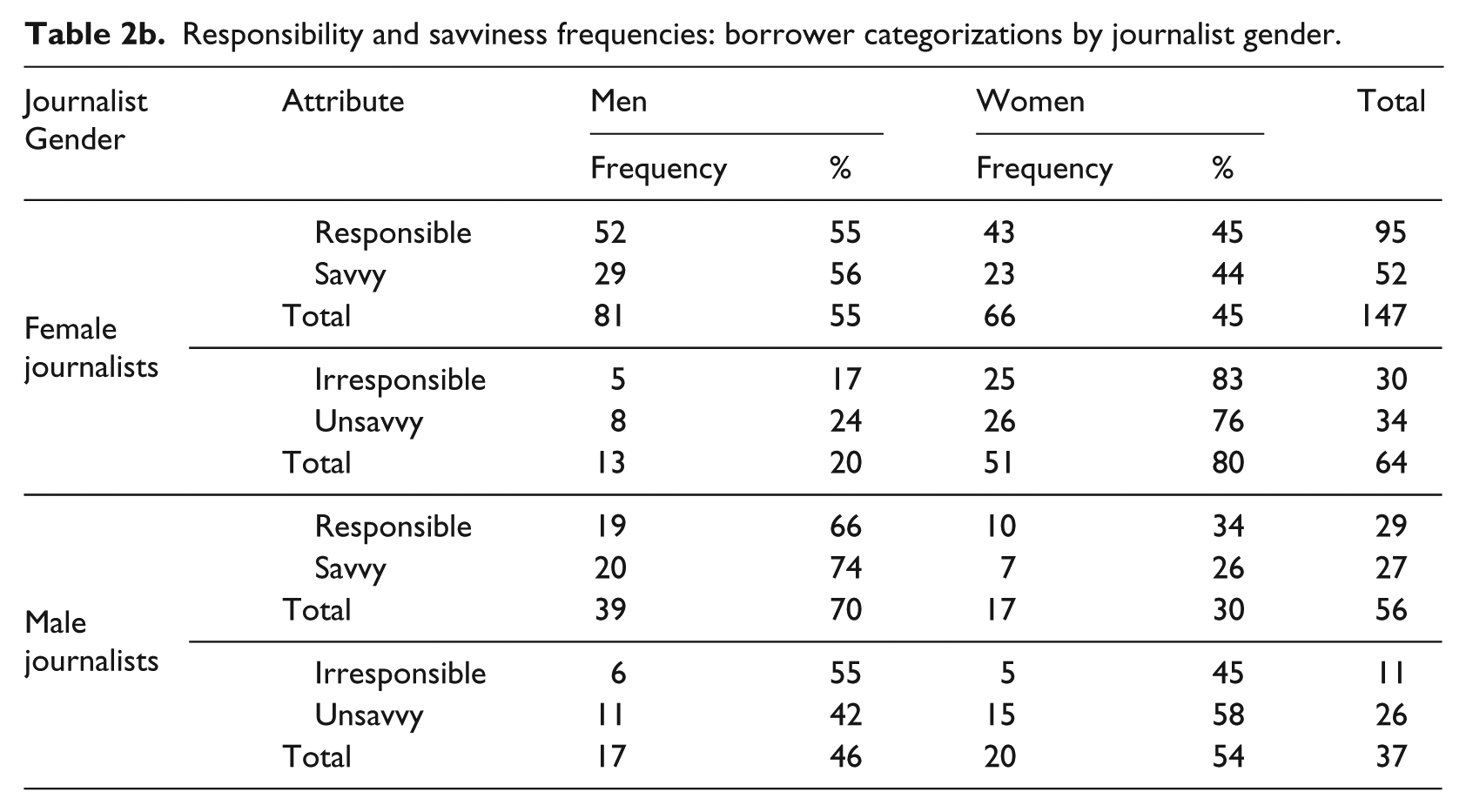

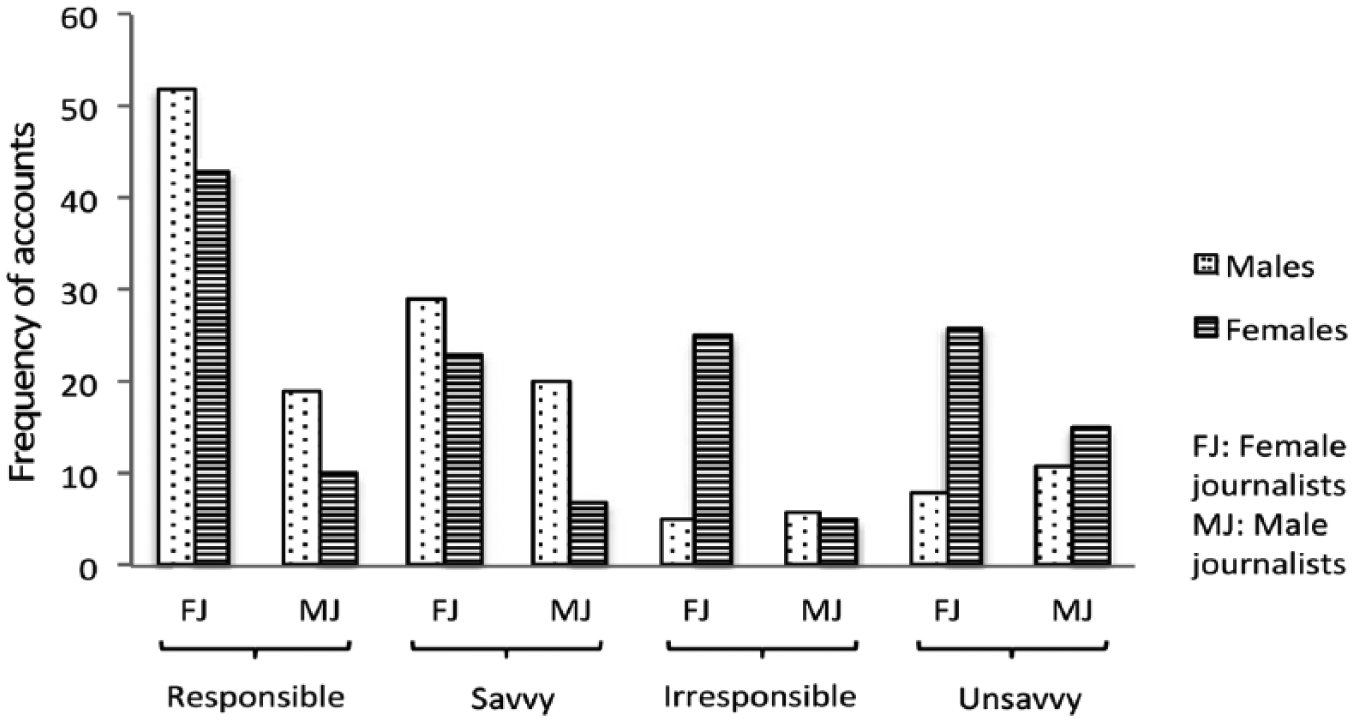

The media relied on “accounts” (Elsbach, 1994; Khan et al., 2007) to categorize the competence of borrowers. Accounts of savviness and accounts of responsibility describe the extent to which borrowers skillfully navigate, and dutifully meet their obligations to the credit card system. Table 2a and Figure 3a display the frequency with which males and females were portrayed as savvy and unsavvy, responsible and irresponsible in our sample, and Table 2b and Figure 3b show the frequencies separated by journalist gender. Though men and women were almost evenly represented in media coverage (166 and 159 respectively), we observed large differences in the number of men and women presented as (ir)responsible and (un)savvy. While we expected to find that male journalists were more likely to use stereotyped accounts than female journalists, what we found was a more nuanced picture of stereotyping used by journalists of each gender. Female journalists were more likely than male journalists to critique female borrowers, portraying greater discrepancy between men and women who were irresponsible/unsavvy. Male journalists, on the other hand, were more likely than female journalists to praise men, portraying greater discrepancy between responsible/savvy men and women.

Responsibility and savviness frequencies: borrower categorization by gender in media accounts.

Responsibility and savviness frequencies: borrower categorization by gender in media accounts.

Responsibility and savviness frequencies: borrower categorizations by journalist gender.

Responsibility and savviness frequencies: borrower categorizations by journalist gender.

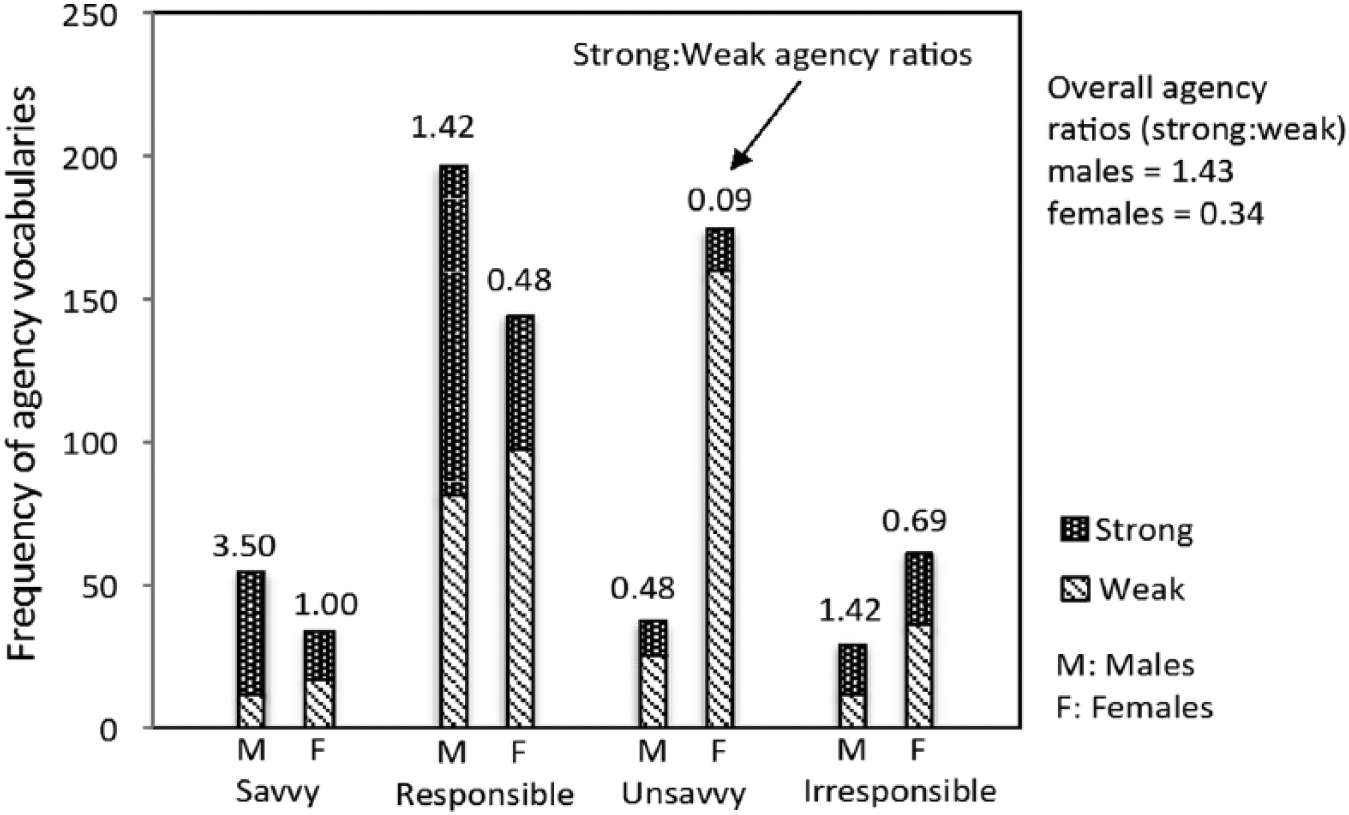

Further, we find that media used “vocabularies” (Loewenstein, Ocasio, & Jones, 2012) to depict the agency of borrowers, that is, the extent to which the borrower can act to achieve desired outcomes. We find that men were presented as more strongly agentic than weakly agentic (strong-form agency to weak-form agency ratio of 1.43) in contrast to women who were much more weakly agentic (strong-to-weak ratio of 0.34). Figure 4 provides an overview of the frequencies of vocabularies. 3

Agency frequencies: borrower categorization by gender in media vocabulary.

Together these frequencies indicate a dichotomous pattern of categorization for men and women, where men are more often portrayed as savvy, responsible, and strongly agentic, and women are unsavvy, irresponsible, and weakly agentic. We now discuss how the underlying mechanisms create these discrepancies, showing each of the three dimensions of borrower competence that differed along gender lines.

Categorizing borrowers through accounts of savviness

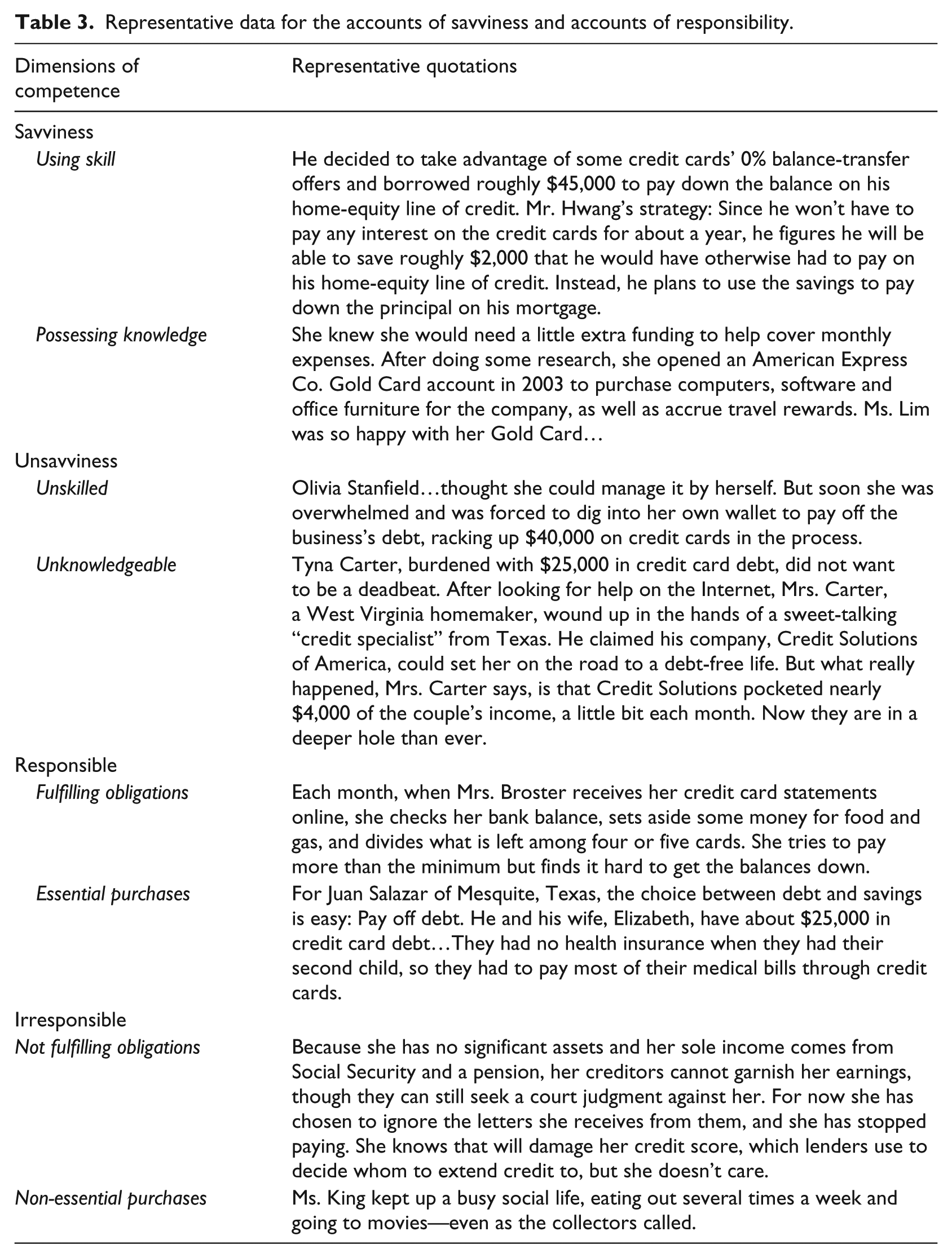

The accounts of savviness presented a dominant picture of male borrowers as both skillful and knowledgeable, using their expertise to improve their financial situations, while female borrowers were uneducated and naïve in their credit card use. Table 3 shows representative examples of these borrower categorizations.

Representative data for the accounts of savviness and accounts of responsibility.

Savvy male borrowers were more often able to find ways to gain from their credit cards, while unsavvy female borrowers often experienced negative consequences because of their poor credit management, as these selections show: This year, Lee Dunham… halved his annual fees on two cards and lowered the variable rates on the same accounts to 12.9%, from 20%, for three months. It took just one call to his card company. …her credit problems began…when she opened a Visa account in return for the campus signup premium, a large candy bar. Since then, she said, she has rarely made more than minimum payments. As credit card companies offered her more cards and deeper credit lines, she said she kept her balance close to the maximum, eventually topping $37,000. Even as her credit card debt surpassed her annual income, she assumed that someday she would make more money and pay it off.

In these data excerpts, the savvy male borrower was able to reduce expenses with one phone call. The female borrower accepted a credit card because she wanted a candy bar and was unable to handle credit, assuming she would deal with the large amount of debt “someday”.

It was common for unsavvy female borrowers to think they knew what they were doing, but instead end up with large, unmanageable debt due to their attempts to benefit from the system. Savvy male borrowers, in contrast, were more often able to benefit from their knowledge and expertise. However, even when both men and women faced negative circumstances beyond their control, women were more likely to be portrayed as unsavvy victims while men were still able to adapt their behavior in order to minimize negative consequences: Gloria Snowden thought she had found a way out from under her $10,000 credit card bill when she signed up with a company that promised to negotiate with creditors to settle the debt for less than she owed… Snowden said she didn’t realize she had been swindled out of her deposits until the Maryland attorney general’s office called to let her know it had nailed the firm’s leaders. Mr. Allen said he has also scaled back travel because credit was tight and business was slower than normal. “You’ve got to play a balancing act,” Mr. Allen said. “This is going to be a moving target.”

When the male borrower’s cards were denied without notice, he was able to “scale back” and play the “balancing act.” The female borrower, on the other hand, did not even know she was a victim until someone else informed her that she “had been swindled.”

Overall, media accounts of savviness offer one dimension of what is a competent borrower. Our findings suggest that, through these accounts, a dichotomy is created between savvy and unsavvy borrowers and that males tend to be more often categorized as savvy while females tend to be more often categorized as unsavvy.

Categorizing borrowers through accounts of responsibility

Accounts were also used to present a dominant picture of male borrowers as responsible and female borrowers as irresponsible. Responsibility does not involve using the system for personal advantage in the same way as savviness; instead, responsibility focuses on simply adhering to the rules of the system. Responsible borrowers were the ones who made credit card payments on time, met their obligations to the credit card company, and focused on essential purchases. Irresponsible borrowers on the other hand failed to meet their financial, ethical or legal obligations to the credit card companies and often made non-essential purchases. The first segment demonstrates this difference between the responsible male borrower and irresponsible female borrower: Mr. Sack, who says he makes sure to never miss a payment to keep his credit scores up, says his reliance on credit cards dates back to 1985, when he founded his company using about a dozen of them. For most of her 20s, Valerine Conerly followed a financial philosophy of sorts: “Spend now, figure out how to pay later.” She’d blow her tax refunds on shoes or a vacation to Miami—and wonder, a couple of months later, where all the money had gone.

In these examples, borrowers are shown to follow a long-term pattern of behavior. The male borrower has a history of responsible credit card management, whereas the female borrower has long been irresponsible with her credit, not taking her responsibility seriously.

A second theme we observed in accounts of responsibility related to the nature of the purchases being made. Specifically, we found borrowers portrayed as responsible were often shown to be making essential purchases whereas borrowers portrayed as irresponsible were more likely shown to be making non-essential purchases. Essential purchases refer to those that are considered necessary, such as groceries, home and auto repairs, gasoline, health bills, etc. Non-essential purchases are those that can be considered superfluous such as new clothes, eating out, and taking vacations. The selection below highlights this pattern of irresponsible female borrowers who are making non-essential purchases: Ms. Ebben, who has maxed out 15 credit cards and racked up more than $80,000 in debt, says she vowed to stay away from stores. Still, she couldn’t resist the temptation of e-commerce, particularly the appeal of 30% off and free shipping. While her husband was gone, she spent $400 at Toysrus.com and Target.com, using money from the couple’s joint bank account.

Female borrowers were often not able to “resist the temptation” of shopping. The connection between irresponsibility and excessive consumptive debt is common in accounts of female borrowers. Male borrowers are more likely to be portrayed as able to resist temptation and focus on essential forms of consumptive debt, taking ownership for their financial situations: Ignacio Vasquez, a Houston plumber, is among those who are planning a leaner Christmas this year. Mr. Vasquez says he typically buys presents for his nine brothers and sisters, as well as for his parents. But this year it will be just mom and dad. “We’re budgeting. I’ve always used coupons, but now it’s a way of life,” he said as he piled into his pickup truck with some diapers purchased at Wal-Mart.

In the above quote, being a responsible consumer is tied to items purchased. In this case, diapers are presented as an example of the borrower’s essential purchases, as he also describes his plans for “a leaner Christmas” and his practice of using coupons.

Overall, we found the dominant portrayal of men was that of responsible borrowers who ensured they were able to pay their bills consistently and make only important purchases. The dominant portrayal of women was that of irresponsible borrowers unable to responsibly manage their bills due to forgetfulness and excessive unnecessary purchases.

Amplifying and undermining through vocabularies of agency

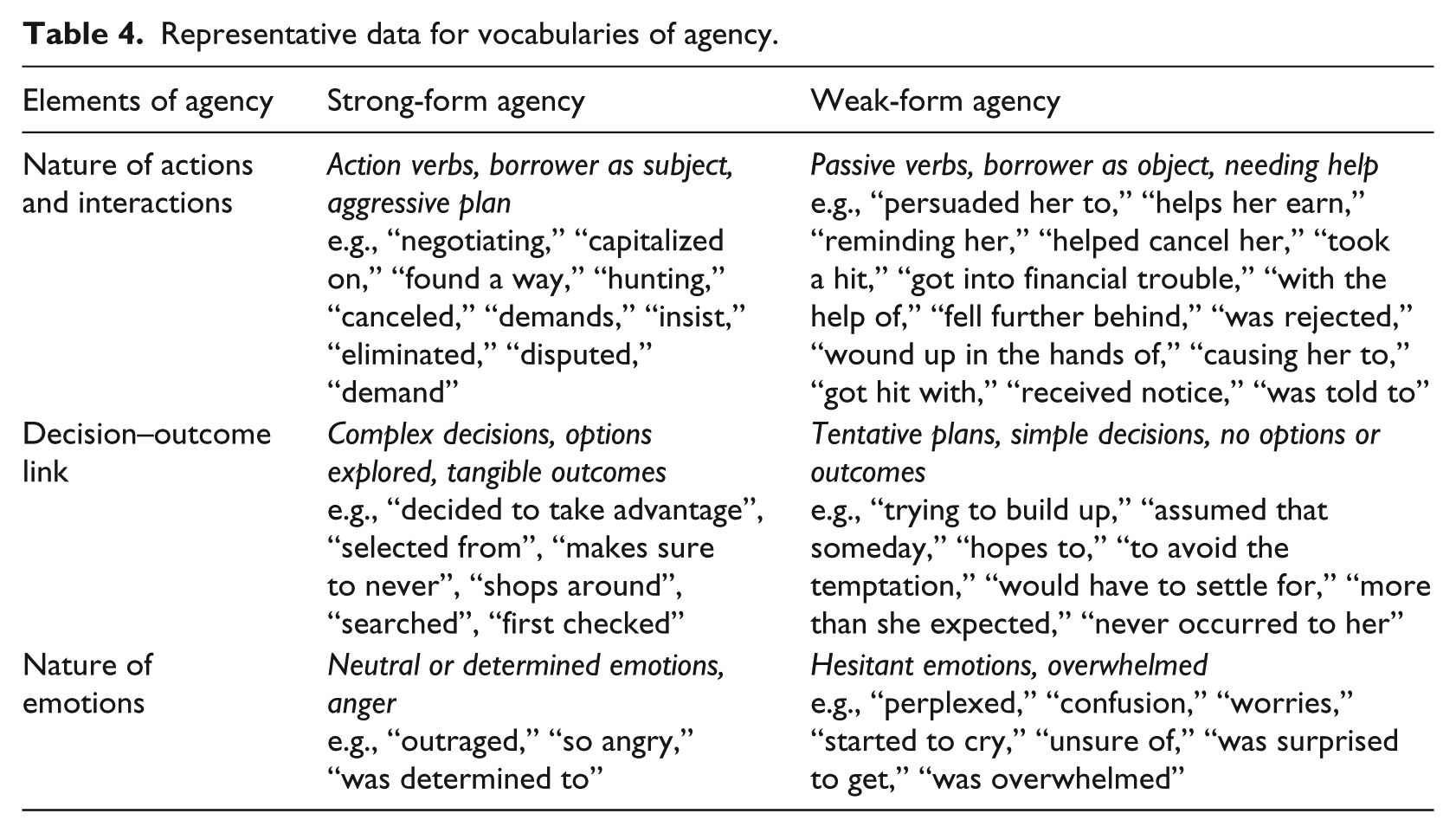

In addition to accounts in the previous section, our findings also reveal a second mechanism of categorization: vocabularies of agency. While accounts told brief stories of male borrowers who were more likely to be savvy and responsible and female borrowers who were more likely to be unsavvy and irresponsible, the language underpinning these accounts also varied by gender. Even in cases where women were portrayed as savvy and responsible, the word choice used to describe the borrower undermined these strengths, articulating a weaker form of agency than that attributed to men. The strong-form agency more often attributed to men included active verbs, aggressive plans, multiple options explored, complex decisions, tangible outcomes, and neutral or determined emotion. The weak-form agency mostly attributed to women portrayed the borrower as the object or used passive verbs, simple decisions, no options considered or outcomes evident, tentative plans, needing help from others, and overwhelming emotions. We disentangled three elements of agency: nature of actions and interactions, decision–outcome link, and nature of emotions. Taken together, these helped portray either strong-form or weak-form agency among the borrowers. See Table 4 for an overview.

Representative data for vocabularies of agency.

First, agency is shown in the language used to describe actions and interactions: active versus passive verbs, borrower as subject versus borrower as object, and aggressive plans versus needing help. Male borrowers were more often shown in media discourse as skillfully negotiating “strategy” despite external forces, where he “takes advantage of” credit card offers to “be able to save.” The language is highly agentic in the purposeful action that male borrowers took. The borrower, as the agentic subject, was not held back by external changes in the system, but instead acted on a plan to improve his situation. On the other hand, media texts about female borrowers more often used passive verbs or presented the borrower as the object in the interaction, with external actors as subjects. Rather than “demanding” or “negotiating,” female borrowers are often described as “accepting,” “being persuaded,” or “needing help” from others. In the end, female borrowers are “pushed,” “forced to,” “hit with” and “fell into” negative situations, using vocabulary to emphasize that it is out of their control.

In the second element of agency, the language used to portray agency differed in terms of the decision–outcome link. Specifically, men’s detailed decision-making processes were linked to tangible outcomes, while women were often shown with minimal details and unclear outcomes. For example, the following male borrower was described using strong-form agency in his planning while the female borrower was described using a much weaker form of agency: Bracher, meantime, is hunting favorable credit card offers as an investment tool. He’s withdrawn money from his home equity line of credit, invested it in the stock market and then pays off his debt with his low-rate credit cards. “I should be able to make more than 2% to 3% in the stock market,” Bracher says. Betsy Olwine, 40, says in the past she held onto her frequent-flier miles up to a year or longer before using any. But now that she’s trying to save and pay down credit card debt, she’s more quickly tapping into her miles for free vacations and trips from her home in Denver to visit her family. “I’m redeeming my miles more often now than in the past,” says Olwine, director of sales recruitment for Hyatt Hotels. She is using 40,000 miles she’s accrued in the United reward program to fly to Hawaii with a friend in September. At the same time, she sees her miles as a safety net for when she needs to fly…

Beyond the active verb “hunting,” the first selection presents steps sequentially, highlighting the numerous calculations made by the male borrower, including a cost/benefit analysis, with a distinct outcome described (even though it is a possible future outcome). In comparison, female borrowers, such as Betsy Olwine above, are “trying to” achieve an outcome by “tapping into” credit card points, without a complex process or reference to steps in the decision-making. Instead of an investment, frequent-flier miles were a “safety net” to support her. Women are often portrayed as more tentative in their planning and the outcomes more modest.

The third and final element of agency is the nature of emotions. Women were more often presented as highly emotional in a way that limited the ability to act. Men, on the other hand, were often presented as neutral, or if emotional, were presented with strong, motivating emotions, such as anger and determination. For example, male borrowers were “so angry” and “outraged on behalf of thousands of people.” In contrast, female borrowers were often worried and overwhelmed by external forces that control the situation. Women required others to “shield her from” when she felt “overwhelmed,” “unsure,” “surprised,” and “started to cry.” Men were not often presented with such weak, incapacitating emotions. In this way, the language used presents a very different picture of the agency of male and female borrowers.

These gender-based differences in vocabulary existed across all categories of accounts. For example, even a woman portrayed as savvy (i.e. using credit for personal gain) was presented as only weakly agentic: Until last month, Jessica Sanner only bought items on eBay. But the sagging economy has forced her to improvise. “I looked around my apartment, took some pictures of some things and listed them” on the online auction site, says Sanner, 20, a college student in Bristol, Conn. She says she couldn’t make ends meet on a part-time job that pays less than $300 a week. To her surprise, her perfume sold for about $25. Within days, she sold five more items. “I get rid of unused items and supplement my paycheck,” she says. “It’s so easy.”

In this example, the female borrower engaged in activities that benefited her personally (savviness), however the vocabulary is passive: the borrower was “forced” by an inanimate object—the economy—much “to her surprise.” Conversely, unsavvy males were often presented using language that denotes strong agency: Mr. Mullaney himself was a victim of a debt settlement company. He was determined, he said, to avoid bankruptcy … He searched online for a debt settlement company run by a lawyer, and by phone closely questioned one based in Anaheim, Calif. As instructed, Mr. Mullaney stopped paying his credit cards, started paying monthly fees and saved aggressively, he recalled. But without warning, three of Mr. Mullaney’s four creditors took legal action. “Finally, the cloud of irrational belief in the concept disappeared, and I realized the scam I’d fallen for,” he said.

Even when unsavvy men are presented as victims, they are still subjects who actively “searched” for and “closely questioned” the options, successfully “eliminating” debt (even though it was through the undesirable outcome of bankruptcy). As such, vocabularies amplified stereotype-consistent categorization of savvy and responsible men and undermined counter-stereotypical categorizations of unsavvy and irresponsible men. Similarly, vocabularies amplified stereotype-consistent categorizations of unsavvy and irresponsible women and undermined counter-stereotypical categorizations of savvy and responsible women. Our findings thus illustrate how accounts of savviness and responsibility, and vocabularies of agency, operate in conjunction with each other to create systematic gender-based differences in competence.

Discussion

We set out to examine how categorization processes discursively reproduce gender-based status differences. Our findings illustrate how media categorization processes construct a gendered hierarchy of credit card borrowers based on competence as they simultaneously explain consumer debt within the context of the financial crisis. In doing so, media coverage systematically assigns women a lower status than men in the financial realm. These gender-based status differences are critical to the cultural reproduction of gender inequality (Correll, 2004; Eagly & Steffen, 1984; Ridgeway, 2011, 2014; Rudman et al., 2012). While resource inequalities are inherently unstable, research has found that status inequalities are often more durable than other forms (Tilly, 1999). This is because once categories or “types” of people are established and certain categories are privileged over others, control of resources becomes consolidated along the lines of a categorical status difference (i.e. gender), exacerbating differences (Ridgeway, 2014). As Ridgeway argues, “when a difference becomes a status difference, it becomes a separate factor that generates material inequalities between people above and beyond their personal control of resources” (Ridgeway, 2014, p. 4). In the realm of finance, if men are systematically given higher status than women, they will continue to wield disproportionate influence in this arena even as material structures of inequality may decrease.

The dimensions of competence we uncover have important implications for the status of actors in increasingly financialized economies. Savviness has been discussed as a necessary characteristic of consumers; savvy actors are seen as more adept at navigating the increasingly complex financial system, and are more likely to be rewarded by the system than actors that lack savviness (Davis, 2009; Fligstein & Goldstein, 2015). Similarly, those actors categorized as irresponsible are seen to lack what is a necessity in the financial realm: the ability to play within the rules of the game (LeBaron, 2014; Mahmud, 2012; Roberts, 2014). The systematic differences we observe in portrayals of borrower competence place male borrowers in a position of higher status as compared to female borrowers. Such portrayals would set the terms for how actors are perceived by external evaluators and what their roles ought to be in the financial realm, thereby contributing to broader gender hierarchies.

The third dimension of competence, agency, has implications for power and authority in the financial realm. Being agentic through means such as embracing “risk…as an opportunity to be negotiated, cultivated and exploited,” thereby acting as an “entrepreneurial financial subject,” is considered crucial for success in a financialized economy (Mahmud, 2012, p. 483). Yet, in the media articles we examined men were most often represented as subjects acting on the world. Women, on the other hand, were often objects being acted upon by social forces. Even when broad accounts of men and women run counter to stereotypical gender-based differences, this challenge may be undercut through other discursive mechanisms, such as vocabularies.

The vocabularies of agency drew on pre-existing stereotypes of men and women regarding agency (Rudman & Glick, 2001), which was constructed through three elements of the vocabulary: the nature of actions and interactions, the link between decisions and outcomes, and types of emotion. While the nature of actions and interactions, and the link between decisions and outcomes, are often the focus of institutional research on agency, it is interesting to note the role of emotions that were also important for constructing women as less agentic. This finding parallels recent research on the emotions that drive institutional work (Toubiana & Zietsma, 2017). In the present study, paternalistic stereotypes of women’s emotions getting in the way of the ability to act have implications for our understanding of agency. Because the disciplining and dominating power of institutions limits and shapes the possibilities for agency (Lawrence & Buchanan, 2017), vocabulary that portrays strong or weak agency represents a subtle but deeply entrenched mechanism of institutional domination that sustains existing power relations. In media coverage of the financialized economy—including the financial crisis—such mechanisms entrenched within journalistic language serve to maintain gender-based status differences, and can block women from increasing their influence in the financial arena and beyond.

It is important to note that the systematic differences we observed in media portrayals of male and female borrowers cannot be fully accounted for by gender differences in financial literacy that have been found in some studies (Chen & Volpe, 2002; Fonseca, Mullen, Zamarro, & Zissimopoulos, 2012; Lusardi & Mitchell, 2008). Going beyond these studies, our evidence points out how the language used to portray the different status of men and women permeates the entire discourse in a highly systematic manner that transcends and encompasses all sorts of specific cases and situations, including any situation where financial literacy may matter. We argue that the systematic gender-based status differences in media that we observed may work to contribute to broader gender differences. For instance, systematic categorization in media of women as less financially competent may influence how women interpret their own social status, and may prevent women from stepping outside the boundaries dictated by their lower status. Similarly for men, their systematic categorization as being more competent than women may work to boost their confidence and self-efficacy in this area. By impacting the perceptions of both borrowers and other key actors in the financial realm, the reproduction of inequality in media discourse can create a self-reinforcing cycle. In this way, gender differences in financial literacy that have been found (e.g., Chen & Volpe, 2002; Fonseca et al., 2012; Lusardi & Mitchell, 2008) may be facilitated and supported by broader cultural processes uncovered in our study.

Contributions to the literature

Our study sheds new light on the relationship between categorization processes and institutional maintenance. Existing research on institutional maintenance has suggested a number of means through which institutions are maintained, including ritual (Dacin et al., 2010), narrative (Zilber, 2009), and rhetoric (Riaz et al., 2016). However, this research is just beginning to turn its attention to the maintenance of institutionalized relations of inequality (e.g., Dacin et al., 2010; Khan, Munir & Willmott, 2007; Gray & Kish-Gephart, 2013), and does not yet offer insights into the specific processes through which one group of social actors is systematically privileged over another group in an ongoing and routinized manner (Martí & Fernández, 2013). Thus, the persistence of inequality remains an important area yet to be sufficiently explored by institutional theory scholars.

We suggest that categorization processes are a key link between inequality and institutional maintenance. While most literature on categorization focuses on the emergence of new categories (e.g., Kennedy & Fiss, 2013; Jones et al., 2011; Khaire & Wadhwani, 2010; Weber, Heinze, & DeSoucey, 2008), our case demonstrates how categorization serves to maintain institutionalized status differences through creating gender-based dichotomies. Dichotomization has been found to play a role in other institutional processes. For instance, dichotomies such as “winners” and “losers” or “heroes” and “villains” are common in the legitimation of change in media discourse (Hartz & Steger, 2010; Risberg et al., 2003). Indeed, a form of institutional maintenance identified by Lawrence and Suddaby, valorizing and demonizing, suggests that creating dichotomies may be one form of maintenance work that provides “especially positive and especially negative examples that illustrate the normative foundations of an institution” (Lawrence & Suddaby, 2006, p. 232). Martí and Fernández (2013) further suggest that the construction of dichotomies contributed to institutionalized relations of inequality in pre-World War II Germany by creating easily-identified categorical boundaries between Germans and “Others,” which then facilitated the oppression of members of the Other category. We build on work in this area by demonstrating how dichotomies can be socially constructed around competence in ways that reinforce broader gender-based status differences. By creating a dichotomy between competent and incompetent borrowers that systematically draws on stereotypes of male competence and female incompetence (Connell, 1987; Fiske et al., 2002; Ridgeway, 2009), existing institutions that privilege one group over another are reinforced and naturalized. Our study therefore draws a new link between the construction of categories and institutional maintenance, and could be particularly helpful for future research seeking to understand the reproduction of institutionalized relations of inequality.

Furthermore, our focus on processes of categorization also contributes to research on gender inequality by uncovering the discursive mechanisms underlying these processes. In doing so, we shed new light on how status is socially constructed (Ridgeway, 2014). Research on gender inequality is increasingly turning to the importance of status to understand the cultural reproduction of gender inequality (Correll, 2004; Eagly & Steffen, 1984; Ridgeway, 2011, 2014; Rudman et al., 2012) and has found that actors with higher status are perceived to be more competent, which facilitates gender inequalities since men enjoy a higher social status than women (Biernat & Kobrynowicz, 1997; Fiske et al., 2002). Though there is considerable research on the ways in which gender stereotypes are employed in media (Anastasio & Costa, 2004; Chavez, 1985; Coltrane & Adams, 1997; Gauntlett, 2008; Jones et al., 1999; Vincent, 2004), research has yet to explore the social construction of competence and how this works to reinforce and reproduce gender-based status differences (Ridgeway, 2014). Our study advances knowledge in this area by revealing the discursive mechanisms involved in the categorization of competence: accounts and vocabularies. Contrary to prior research that has highlighted the underrepresentation of women in media coverage (Bernstein, 2002; Chavez, 1985; Collins, 2011), there was approximately equal space given to men and women in the media discourse on consumer debt. Yet, the accounts and vocabularies describing these men and women served to reproduce gender inequality based on underlying stereotypes that exist in the current US context (Connell, 1987; Fiske et al., 2002; Ridgeway, 2009). Our findings thus uncover how multiple discursive mechanisms work in conjunction with each other to create gender-based differences, showing how institutionalized relations of gender inequality are maintained through these categorization processes.

Future research

Our findings also suggest avenues for future research in the area. First, though our context of the financial crisis gave us an opportunity to examine categorization processes around gender operating in the background of a larger discussion of credit card borrowers, future research may extend our work to explore possible differences in how stereotypes are employed both in periods of stability and in periods of crisis. Though the systematic reproduction of gender-based stereotypes is likely to occur in both periods, the particular ways in which gender stereotypes are drawn upon in categorization processes may uniquely reflect the broader state of the field. Second, limitations in our data prevented us from systematically exploring how gender intersected with other social categories such as class, age, or ethnicity. However, a more in-depth understanding of how categorizations of gender interact with these other social categories could further advance knowledge in the area by elucidating the complex relationships among social categories and stereotypes. We encourage future research to push forward in this regard. More generally, we hope that our study stimulates further research in organization studies on the cultural mechanisms that underlie the reproduction of inequality in its many forms.

Footnotes

Acknowledgements

We would like to thank Guest Editor Paul Hirsch and three anonymous reviewers for their thoughtful and constructive feedback throughout. We are also grateful to Madeline Toubiana, Maxim Voronov, Banu Özkazanç-Pan, Mary Still, Lukas Neville, Arran Caza, Nicolas Roulin, Wenlong Yuan, Brianna Caza, and participants in the Gender and Inequality paper session at the Academy of Management annual meeting in Anaheim, CA, for their comments on earlier versions of this paper.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.