Abstract

Loans from international organizations impose large costs on the receiving nation. The decisions to accept such loans and then whether or not to implement the prescribed reforms are made with high stakes in mind. Domestic leaders are most likely facing punishment for the current economic crisis, but what is their incentive to implement the arrangements if the costly reforms associated with the loans may reduce their ability to satisfy their supporters? To fully understand this relationship, I develop a theory that explains leader tenure in the post-reform period as a function of the rational decision to accept a loan. Leaders who expect to be secure in the adjustment period are more willing to accept the conditions that accompany loans rather than attempt to withstand the crisis on their own. With the use of a selection duration model, I examine the interplay between electoral incentives and institutional dynamics to show that leaders governing under different institutional arrangements are affected differently for involvement in IMF loans. Since leaders choose when to accept IMF loans based on their own expectations of post-reform tenure, democratic leaders are less likely to participate in loans. Authoritarian leaders, on the other hand, are more likely to participate in agreements because their hold on power in the post-reform period is stronger.

Keywords

Introduction

When leaders are faced with balance-of-payments problems and rampant inflation, they are often limited in the range of policy options that they can take. On the one hand, they can attempt to handle the economic crisis on their own. On the other hand, the alternative is to approach the International Monetary Fund (IMF) and receive a much-needed boost in foreign reserves to help them weather the storm. However, even if the loans help the leader survive the crisis, the difficulties are not over. IMF loans with stringent austerity programs may constrain the abilities of leaders to distribute goods in the form of government expenditures that are often necessary for the leader to maintain backing of his key supporters and stay in power. In this sense, leaders are picking their poison, between economic crisis and costly adjustment.

In this paper, I address whether leaders are able to withstand the pressures of IMF loans in ways that differ based on their regime type. Since the choice to participate in an IMF arrangement is a political one in which leaders weigh the costs against the benefits, only politically secure leaders will accept the conditions associated with the loans. I extend a theory of Smith and Vreeland (2006) that suggests that leaders of different regime types participate in IMF agreements to varying degrees because of the anticipated consequences of those agreements on their post-reform tenure. Unlike Smith and Vreeland (2006), I find that authoritarian leaders are not only more likely to participate in loans (controlling for economic performance), but that they remain in office for longer periods because they have a stronger hold on power in the post-reform period. Leaders from both democracies and authoritarian regimes pick their poison, adjustment or crisis, based on the probability of their survival: authoritarian leaders are more likely to choose adjustment while democratic leaders are more willing to face crises on their own.

Democratic characteristics provide incentives for leaders to be responsive to the preferences of the electorate. I theorize that those same institutions also make democratic leaders more likely than autocratic leaders to lose office following receipt of IMF loans. Somewhat counter-intuitively, the political institutions that are intended to make democratic leaders more representative actually make politically motivated leaders more likely to forgo the most appropriate policy in an effort to remain in office. This dilemma also has implications for the use of IMF loans to address balance-of-payments problems. Since leaders are reluctant to participate in loans when their post-reform tenure is unsure, studies of the consequences of IMF loans risk misleading conclusions if they fail to incorporate this choice.

In the first section, I examine the effects of economic crises on political stability and the incentives that leaders have to accept IMF loans. In the next section, I review why leaders have the incentive to implement economic reforms even though the reforms are likely to be unpopular and may create short-term economic disturbances. I then use Smith and Vreeland’s theory of differing effects as the logical foundation to suggest that leaders’ concerns about maintaining office drive their decisions to participate in IMF loans. I illustrate the importance of this strategic choice by using a selection duration model simultaneously to model both the leader’s decision to accept a loan and then that loan’s effect on leader tenure. I conclude by illustrating the bias that non-random sample selection imposes and by providing the implications for such bias in the study of IMF arrangements on leader survival.

International Monetary Fund Loans and Leader Survival

The decision to enter into an IMF arrangement is a political decision, with commensurate costs and benefits for the leader. Executives are political actors who are held accountable for their policies. Debt crises can exacerbate the already asymmetric power distribution between multinational lenders and poor debtors. This limits the range of acceptable policy options for a leader and increases the incentive for accepting an IMF arrangement. Though balance-of-payments problems have costly effects on political stability, leaders may still be hesitant to pursue Fund agreements because of the political costs of the agreements themselves. Although the costs of the agreements are certain, the benefits from the arrangements are often couched in uncertainty (Bienen and Gersovitz, 1985).

What is the incentive to seek IMF loans if the chances of repairing the economy are relatively slim but the costs are definite and most likely severe? First, leaders may want to enact economic reforms in the pre-adjustment stage, but be unable to do so because of strong opposition groups. Since these loans decrease the amount of government spending, they often entail slashing subsidies and limiting the number of government jobs. Such reforms are likely to be met with strong opposition, especially by those groups that are affected the most. IMF agreements therefore allow leaders to enact reforms that they would otherwise be unable to enact (Przeworski and Vreeland, 2000; Vreeland, 2002). By tying the leader’s desired policies to the policies of the IMF, the costs of rejecting the conditions of the loan are increased, thereby reducing the chance that the loan will be unsuccessful (Vreeland, 2002).

Leaders may also implement IMF agreements to obtain additional loans or financing support from other institutions (Fischer, 1997). The presence of an IMF agreement brings in more aid from outside sources that wait for the IMF to make the first move and attach needed conditions. Thus, IMF agreements act as a ‘green light’ for investors, thereby indicating that reforms are taking place to provide a friendlier investment environment (Bird and Rowlands, 2001; Bird and Rowlands, 2002). In addition, by providing accurate information regarding the state of the economy, IMF agreements do a great deal to ‘facilitate reputation-building on the part of post-stabilization governments’ (Collier and Gunning, 1999: F649). 1 The post-adjustment levels of transparency are much higher, which helps to restore investor confidence.

It is a reasonable assertion, then, that the IMF also makes decisions partly based on the economic viability of the structural adjustments demanded by the loan (Haggard et al., 1995) and whether the loans will help correct the balance-of-payments crisis. The strongest determinant of whether the IMF chooses to provide a loan is the extent to which the state is experiencing balance-of-payments problems. Conway (1994) argues that the rate of economic growth and the state of the current account are the most substantively important factors causing participation in loans. Other balance-of-payments conditions strongly affect the supply side of IMF arrangements, including the real effective exchange rate, level of external debt, gross domestic product (GDP) growth, GDP per capita and whether the state was previously involved in an IMF loan (Knight and Santaella, 1997). Contrary to the IMF’s ‘Doctrine of Economic Neutrality,’ scholars find that political calculations may affect the decision to lend, primarily because the weighted voting scheme provides the US with a virtual veto on all lending decisions. Scholars have also considered political influences on the provision of loans (e.g. Thacker, 1999; see Steinwand and Stone, 2008, for a review).

Unfortunately, the remedy for economic problems may be as harmful as the problems themselves. IMF agreements may generate many sources of political instability. While different types of loans offer various short- and long-term goals, they generally demand that future funds be made available only when four broad conditions attached to the loans have been met (Biersteker, 1990). 2 First, the IMF demands that the country devalue its currency and allow for market-determined exchange rate adjustments. This is aimed at correcting short-term balance-of-payments problems by making imports more costly and making exports more attractive. The second condition is an anticipatory reaction to the inflation that traditionally follows devaluation. In order to manage demand, the IMF suggests slowing the rate of growth in money supply, government fiscal adjustment and wage restraints. The government’s deficit is reduced by limiting current government spending and increasing revenue through improvements in the collection of income and corporate taxes, and the selling of public enterprises. The third condition is premised on restoring market mechanisms. This includes the reduction of price controls (ending subsidies), increasing interest rates and liberalizing trade through lowering tariffs, eliminating trade licensing and phasing out export incentives. All of these policies are aimed at increasing competition and improving the efficiency of domestic production. The final condition of adjustment loans includes privatization, which helps generate revenue and improves the efficiency of production (Biersteker, 1990).

Yet, there is some evidence to suggest that not all IMF loans are alike. Copelovitch (2010) shows that the level of conditionality – measured by the number of conditions included in the loan – varies across countries and across time. Empirical analysis has been limited to examining the number of conditions because of the difficulty in ascertaining the ‘relative stringency’ of the conditions as well as the content of the conditions across states (Copelovitch, 2010: 59–60). On the other hand, there are quite a few commonalities across loans. Another in-depth study of the structural conditions attached to IMF arrangements from 1995 to 2004 found that two-thirds of all the conditions were concentrated in areas such as taxation, financial sector reform and public expenditure management (Independent Evaluation Office of the IMF (IEO), 2007: 5). 3 In an effort to make my findings directly comparable to those of Smith and Vreeland (2006), I aggregate all IMF programs.

The IMF often demands a reduction in the budget deficit, which entails improving tax collection, wage restraints, subsidy removal and constraining the size of the public sector (Fischer, 1997). Political instability flows directly from the distributional impacts of stabilization policies, because the reforms impact various groups in different ways. IMF arrangements can directly lead to riots and political unrest due to changes in redistributive policies, as shown in the cases of Venezuela, the Ivory Coast and Ecuador (Bienen and Gersovitz, 1985). Since some disadvantaged groups are likely to hold the government accountable for their economic situation, IMF arrangements have the potential to threaten the leader’s hold on power. Thus far, the literature has largely failed to take into account the fact that IMF arrangements do not comprise a random sample, but instead are a function of choices made by both the leader and the IMF. An exception is Copelovitch (2010), who uses propensity score matching techniques to control for the possibility of selection bias. Unfortunately, by treating the selection process as a ‘nuisance’, one loses valuable information about how the selection process influences leader duration. In the next section, I build upon previous work on the consequences of IMF loans by Smith and Vreeland (2006) and directly test the importance of the choice to participate in IMF arrangements.

Self-Selection and International Monetary Fund Loans

I assume that a leader’s fundamental goal is to stay in office (Downs, 1957). Although leaders may have other goals (improving their legacy, implementing their policy preferences, etc.), these goals are best served if the leader remains in office. This argument suggests that leaders will try to resolve any problem that threatens their ability to maintain office, of which economic crisis is a prime example. Although economic crises affect most areas of society in some way, there are certain groups that are especially vulnerable to crises. Increasing budget deficits encourage leaders to produce money supply growth at a rate faster than the income growth rate, resulting in inflation. On the other hand, the costly austerity conditions also demand drastic reductions in government programs. These consequences damage key groups within the leader’s core supporters because the leader may be unable to shield completely those groups from the negative effects.

Will the public blame the leader for poor economic conditions? In order to answer this, one must first look at the idea of legitimacy. For the most part, democratic citizens view their leader as legitimate because he or she came to power through free, fair and competitive elections. Legitimacy not only means that the leader can act in the interests of the citizens, but also that he or she will be accountable. The shadow of an upcoming election 4 means that the public can threaten to remove the leader from office because of policy failures. Because there is a strong relationship between economic conditions and accountability (see Lewis-Beck and Paldam, 2000, for a review), I argue that citizens in a democracy will hold their leader accountable for economic crises.

In the only analysis of its kind, Smith and Vreeland (2006) develop a theory that explains the varying effects of IMF loans on leader survival as a result of both regime type and leader motivations. They find that the effects of loans on leader survival depend on domestic institutions and the motivations for leaders seeking these loans. Key to their theory is Bueno de Mesquita et al.’s (2003) ‘selectorate theory,’ which offers a simple explanation for the differences in expected responses by leaders from different regimes to adjustment. In their work, Bueno de Mesquita et al. (2003) examine why particular policy failures dramatically reduce leader survival while others do not. This relationship is conditioned by the size of the ‘winning coalition’ and the selectorate. The ‘selectorate’ is the subset of the population that has the ability to participate in choosing the leader of the country, while the winning coalition is the group of individuals whom the leader depends on for support in order to maintain power. In democracies, the size of the winning coalition is functionally tied to the size of the selectorate through the electoral rules. Leaders maintain support through the provision of public and private goods. The larger the winning coalition, the more difficult it is for the leader to maintain their support through the provision of a finite set of private goods. As the winning coalition approaches the size of the selectorate, the leader depends on public goods, which ‘affect the welfare of everyone in the state,’ and can include ‘political freedoms, national security, [and] general economic growth policies that lift the total size of the pool of resources of the state’ (Bueno de Mesquita et al., 1999: 149).

Policy failures are more dangerous to the leader’s survival when there is a large winning coalition. Holding the selectorate constant, ‘decreasing the size of the winning coalition increases the loyalty of members of a leader’s winning coalition because the chance that a defector will be left out of the rival’s winning coalition is greater’ (Bueno de Mesquita et al., 1999: 153). The most stable system is one in which there is a large group of potential supporters (selectorate), with a small number of supporters needed to maintain power (winning coalition) (Bueno de Mesquita et al., 1999). Based upon these assertions, they argue that policy failures will not impact survival rates in states with large selectorates and small winning coalitions, because their core constituents demand private, not public, goods. Democracies traditionally have large selectorates and large winning coalitions, while autocracies intrinsically have small winning coalitions (with varying sizes of the selectorate). Reform is likely to reduce the ability to provide public goods but not necessarily private goods.

On the other hand, authoritarian leaders do not have the same sense of election-driven legitimacy as democratic leaders. Traditionally, authoritarian leaders do not need to have electoral legitimacy in order to maintain power, as long as they have support from the key groups within their ruling coalition. With a finite set of resources, the leader is faced with the choice of spending government revenue on investment, public welfare and development projects, or patronage to his coalition of key supporters. The general public will be hurt by reductions in subsidies, elimination of price ceilings or implementation of wage restraints, meaning that the leader will choose to focus his limited resources on shoring up support for his administration. Because of the ways in which IMF loans affect the ability to distribute public and private goods, Smith and Vreeland (2006) suggest varying reasons why IMF loans might influence tenure. When faced with severe economic problems, leaders of democracies (with large coalitions) may be reluctant to pursue a loan because it is indicative of a policy failure, but at the same time the loan might alleviate some economic problems and provide the leader with a scapegoat. When democracies pursue loans when there is no pressing financial need, Smith and Vreeland expect that they will benefit because the leaders can possibly overcome domestic veto players. For autocratic leaders (with small coalitions), pursuing a loan is a mixed blessing: the loan provides another source of patronage and gives the option of scapegoating, but the conditions that accompany the loan might restrict funds to be used solely for public goods. They find that democratic leaders are generally benefitted by loans while autocratic leaders are hurt if they accept loans when economic conditions do not warrant them.

These differences in responses to adjustment are largely supported by the literature on the ability of authoritarian leaders to withstand adjustment to a greater extent than democratic leaders (Bienen and Gersovitz, 1985; Remmer, 1986; Haggard and Kaufman, 1992; Nelson, 1990). IMF agreements are conditioned on fiscal adjustment, which often includes decreasing government spending through expenditure reduction and expenditure switching, both of which will damage the leader’s ability to provide public goods (van de Walle 2001). ‘Expenditure reduction’ involves contractionary measures (cuts in the rate of growth of the money supply) that indiscriminately affect all parts of the population. On the other hand, ‘expenditure switching’ entails redistributing income within the economy to increase incentives for market operations; oftentimes, this involves switching funds traditionally spent on consumption over to investment. These types of reform are the most likely to target specific groups, but they also give the leader the most leverage in deciding which groups to target (van de Walle, 2001). A key difference is that loans affect the provision of public goods more than private goods, allowing leaders with smaller winning coalitions (autocracies) to fare better in the post-reform period. Further, authoritarian leaders have another option that democratic leaders do not have. In those cases where the loan is met with domestic unrest, they are able to maintain a more stable political environment through the use of repression (Gelpi, 1997).

An under-emphasized part of Smith and Vreeland’s theory is the notion that leaders make these decisions based on their incentives to remain in office. They suggest that democratic leaders can benefit from pursuing discretionary loans because they select themselves into the agreement. It is unclear, however, why the benefits of self-selection do not apply to leaders of other regime types who also make a rational decision whether to participate in a loan. It is more reasonable, then, to suggest that leaders of all regime types are unlikely to pursue loans if this threatens their tenure. The IMF loans that occur, then, occur because the leader anticipates that participating in the loan leaves him or her in a better position than the alternative. If authoritarian leaders are better able to withstand the post-reform period, then scholars may see different patterns of loan-participation based on regime type.

It is perhaps helpful at this point to provide an empirical example of this selection procedure at work. In 1980, Ghana was a fledgling democracy facing major socioeconomic decline (with a Polity score of 6). President Dr Hilla Limann recognized that reform needed to occur, but also realized that his hold on power was tenuous because of the multiple coups in the years before he came into office. Although he secretly held meetings with the IMF to push for desired reforms, no action resulted from the negotiations. ‘Factional disputes within the government and fears of popular opposition to stabilization measures’ meant that his already tenuous hold on power in the fledgling democracy would be pushed to the limits by enacting the adjustment reforms (Nelson, 1990: 273). Although Limann incorrectly assumed that the costs of adjusting would outweigh the dangers of the economic crisis, 5 he selected himself out of an IMF arrangement. He avoided the IMF because, in his judgment, ‘devaluations cause coups’ (Nelson, 1990: 326).

An interesting empirical puzzle arises from this discussion. On the one hand, studies have demonstrated that IMF loans may be more beneficial to the stability of authoritarian leaders than democratic leaders (e.g. Haggard and Kaufman, 1992). On the other hand, democratic leaders may benefit more from the loans than authoritarian leaders: ‘not only does the IMF program provide a loan but also a convenient scapegoat for the economic pain that economic reforms may bring’ (Smith and Vreeland, 2006: 268). At its very foundation, choosing whether to participate in an IMF agreement represents a political decision with accompanying consequences, both beneficial and destructive. First, leaders are significantly more likely to halt structural adjustment loans immediately before an election (Dreher, 2003), even though the loan may increase their probability of reelection (Dreher, 2004). Also, governments that delay reforms are predominantly from politically fragile systems, while governments implementing reforms tend to have the support of wide coalitions (Nelson, 1990). Adjustment loans that require a high number of structural reforms risk damaging democratic practices within the country (Brown, 2009). Together, these different findings help paint a picture of a leader evaluating the domestic environment before selecting himself into a potentially politically tenuous situation. I propose a solution to this puzzle that is based on the idea that leaders are rational office-seekers who are unwilling to choose policies that put their own tenures at risk. Only those leaders who feel that IMF arrangements may improve their position will agree to the loan in the first place. Authoritarian leaders will be more likely to accept agreements because they have greater capacity to withstand the shocks of adjustment and may be in a better position to benefit; since democratic leaders are more vulnerable to removal after a loan occurs, they will be more hesitant to accept a loan. This leads me to my two-part hypothesis:

Hypothesis 1a: The more democratic a leader is, the lower the probability of participating in an IMF arrangement.

Hypothesis 1b: The effect of IMF arrangements on leader tenure is conditional on regime type, with democratic leaders facing higher hazards than autocratic leaders.

Data and Methods

In order to test these hypotheses, I use a data set originally created by Bienen and van de Walle (1991) and updated to 2000 by Bueno de Mesquita et al. (2003). The unit of analysis is the leader-year and the data set extends from 1970 to 1999. 6 Because the dependent variable is the amount of time that a leader has stayed in power, I use a duration analysis, which will be expanded upon later in this section. IMF agreements are operationalized as three dummy variables, indicating whether an IMF agreement occurred (IMF) or began (IMF Onset) during that leader-year, or was signed by the previous leader (Previous Leader). 7 Since the four types of IMF loans have varying substantive goals but the same battery of conditions, they are aggregated into one measure. 8 I expect that the decision to participate in an IMF arrangement is a function of institutional arrangements, economic conditions and political considerations:

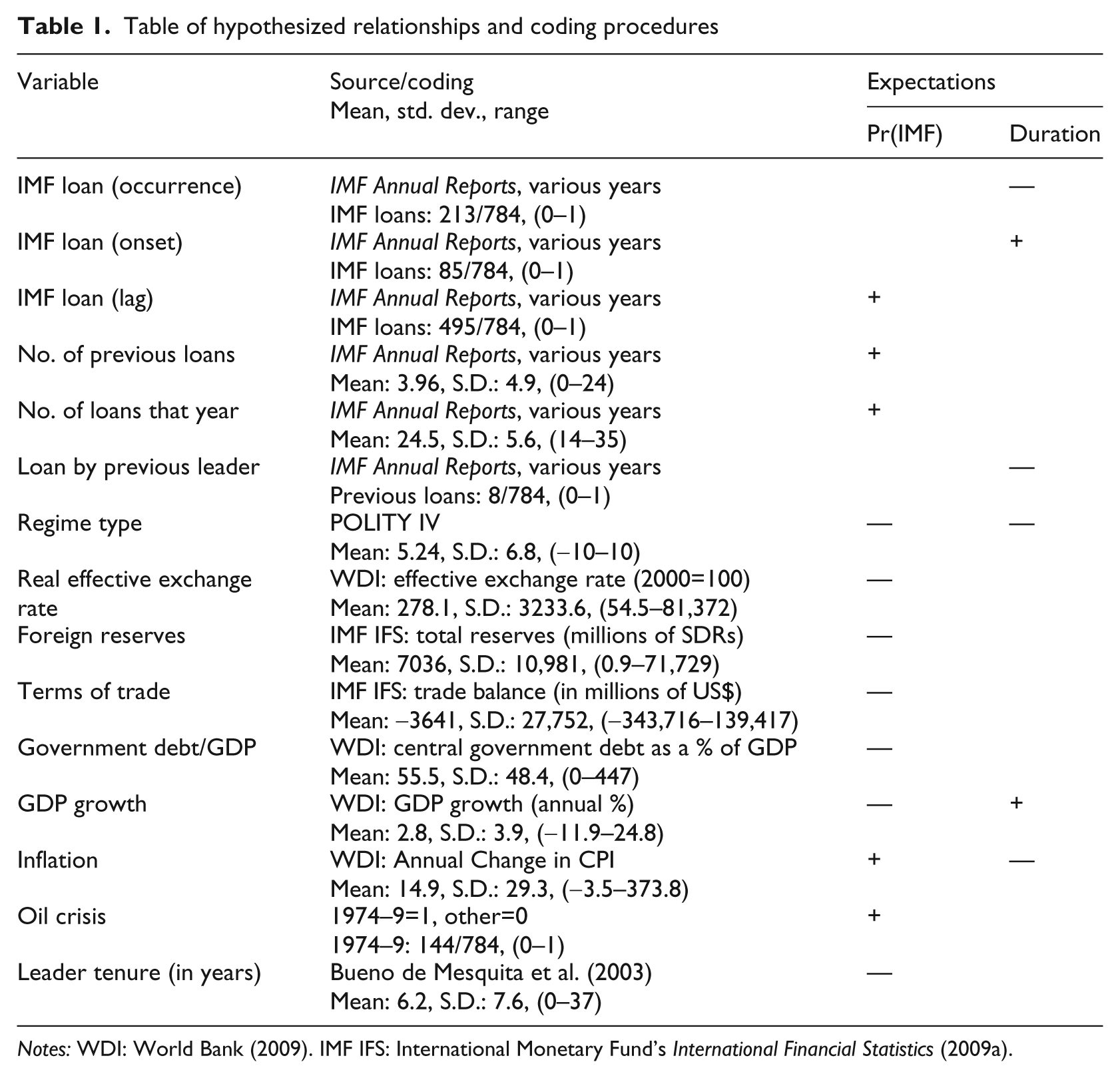

Data sources, theoretical expectations and summary statistics for the variables used in the selection equation are provided in Table 1.

Table of hypothesized relationships and coding procedures

Notes: WDI: World Bank (2009). IMF IFS: International Monetary Fund’s International Financial Statistics (2009a).

There are a number of variables that have been theorized to have an effect on the survivability of leaders, including regime type (R.T. in the above model specification). Democratic leaders are subject to periodic elections that produce a risk that the leader will be removed by the citizenry. Alternatively, autocratic leaders are largely not threatened by the prospect of election, either because there is no election, or because the government has reduced political opposition to a level where the outcome of the election is predetermined. Regime type is measured with the 21-point index from Polity IV, ranging from −10 (full autocracy) to 10 (full democracy). By including regime type in the duration model, I can determine whether the effects of loans on leader survival vary across regime types.

The desire for an IMF loan is largely a result of balance-of-payments problems; if a state has a low level of international reserves, it is less able to minimize balance-of-payments crises by using its own stock of foreign reserves (Knight and Santaella, 1997). Foreign reserves (F.R.) is measured in millions of SDRs (IMF, 2009a). Other economic conditions affecting the balance of payments will also influence the decision to participate, including the real effective exchange rate (E.R.), total terms of trade (T.B.), inflation (I.), GDP growth (GDP), and the level of external debt (Debt) (Conway, 1994; Knight and Santaella, 1997; Vreeland, 2002). IMF agreements are not solely the result of economic conditions, as various scholars have identified the importance of political considerations (e.g. Thacker, 1999; Stone, 2004). Some political determinants of IMF loans include the oil crisis of 1974–9 (Oil), leader tenure in years (Ten.), whether the state had an IMF agreement in the previous period (Loant-1), the number of previous loans (Prev. Loans) by that state, and the total number of loans made by the IMF in that year (#Loans) (Knight and Santaella, 1997; Bird, 1996). 9 These variables are all included in the selection equation, and the sources and theoretical expectations are described in Table 1.

The process of choosing between continued economic crisis and the costly austerity programs that accompany IMF loans is the political equivalent of picking one’s poison. In the next section, I simultaneously model the decision to accept a loan and that loan’s effects on leader tenure.

The Process of Picking the Poison

To begin, I intend to show that the effects of loans on leader survival depend on the leader’s regime type. Since the selection duration model estimates leader survival given the occurrence of a loan, it can directly test my theory of selection effects, but it cannot provide a full test of the conditional nature of regime type. In order to test the hypothesis that the effects of IMF loans on leader tenure are conditional on regime type (Hypothesis 1b), I estimate a simple Weibull duration model (without modeling the selection procedure). I choose to parameterize the underlying hazard rate as a Weibull distribution because of my strong theoretical expectation that the hazard of leader removal decreases over time (e.g. Smith and Vreeland, 2006).

I argue that leader tenure is a function of the following covariates:

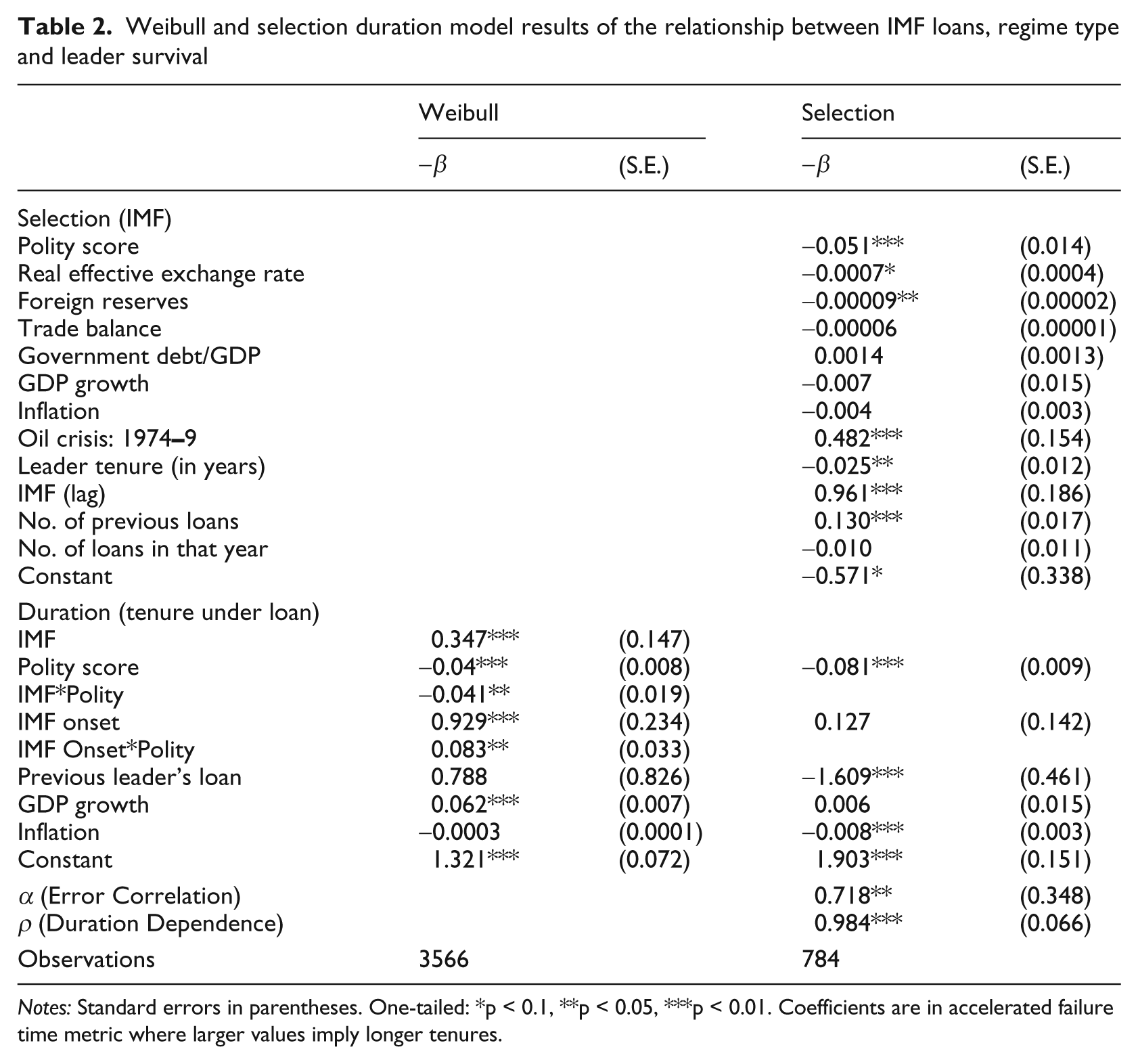

I explicitly test two interactive relationships: whether a loan occurred (IMF) and whether the onset of a loan (IMF Onset) interacted with regime type (R.T.) to create two interaction variables (IMF × R.T. and IMF Onset × R.T., respectively). While the onset of a loan may actually benefit the leader by initially creating the appearance that the leader is addressing the balance-of-payments problems, I expect that the influence of loans will be felt as the austerity measures are implemented over time (thus, when the loan is ongoing). In other words, early on, the leader can receive the political benefit for addressing the problems without yet paying the costs of adjustment. I therefore expect to find that the marginal effect of an ongoing loan – controlling for the onset of a loan – is more positive for authoritarian leaders than democratic leaders. I also expect that higher GDP growth and lower inflation, respectively, will increase leader tenure. I present these results in the first column of Table 2.

Weibull and selection duration model results of the relationship between IMF loans, regime type and leader survival

Notes: Standard errors in parentheses. One-tailed: *p < 0.1, **p < 0.05, ***p < 0.01. Coefficients are in accelerated failure time metric where larger values imply longer tenures.

Recall that there are two interactive relationships in the Weibull model: the effects of IMF loans on leader survival conditioned on regime type, and the effects of the onset of loans on leader survival conditioned on regime type. We can gain a few inferences from the coefficients of the lower-order and interactive variables in Table 2. First, let’s examine the effects of onset. For mixed regime types (i.e. when Polity = 0), the onset of an IMF loan lengthens tenure, and the positive interactive variable (IMF Onset×Polity) shows that this beneficial effect increases as the regime becomes more democratic. On the one hand, this lends support to the idea that the onset of an IMF loan may help the leader by appearing to address the problems. On the other hand, this result may be a function of the coding procedures. More specifically, since IMF has to equal 1 for IMF Onset to equal 1, it may be difficult (if not impossible) to isolate the true effects of onset, controlling for the occurrence, with a Weibull duration model. Later on, I introduce an empirical test that distinguishes between these two possibilities.

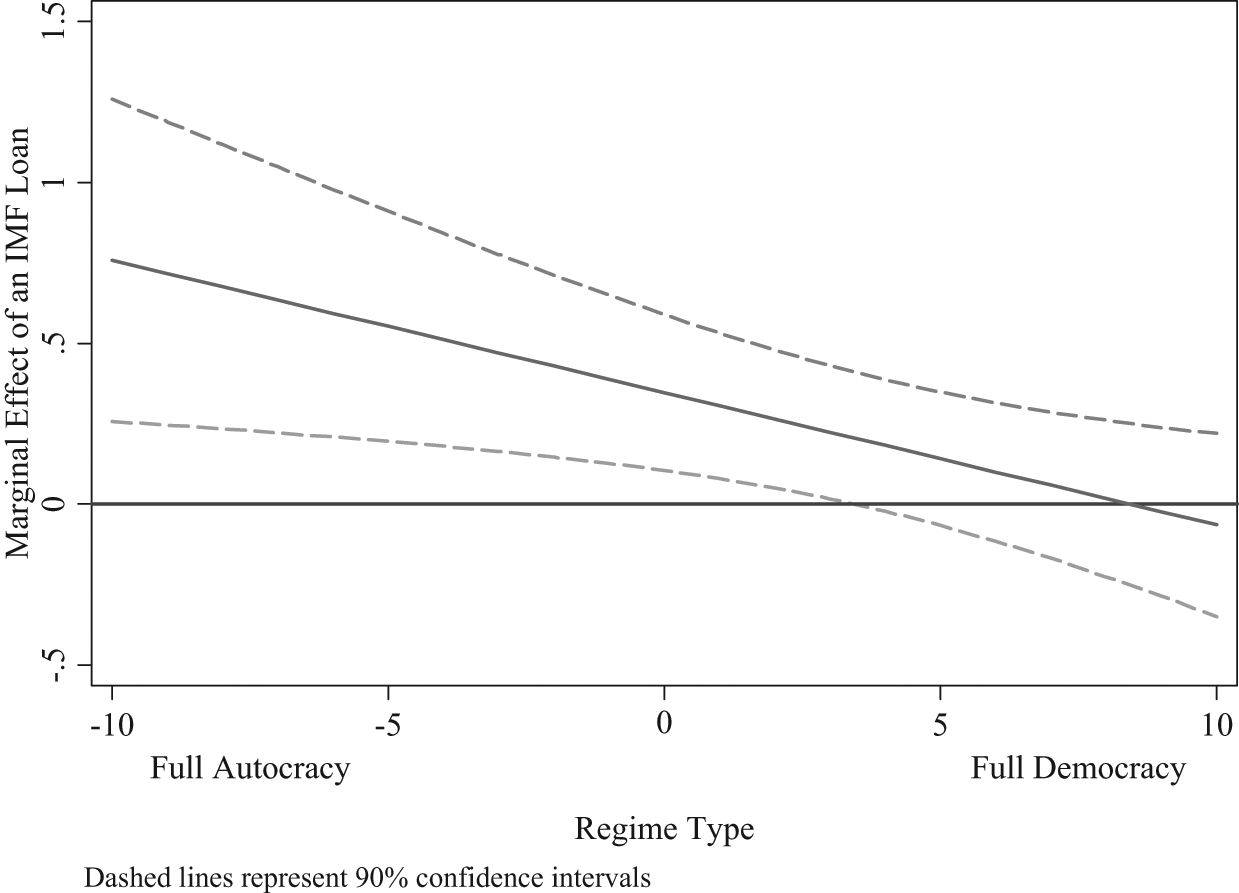

The coefficients for the occurrence of an IMF loan support Hypothesis 1b. 10 Figure 1 shows the marginal effect of an ongoing loan (and 90 percent confidence intervals) across the sample range of regime type (e.g. Brambor et al., 2006).

Marginal effect of an ongoing loan on leader survival across regime type: Weibull duration model

A positive marginal effect means that the loan has a positive (i.e. lengthening) impact on the leader’s tenure. For leaders of autocratic and mixed regimes (i.e. when Polity < 5), being under a loan (controlling for its onset as well as whether the loan was agreed to by the previous leader) increases their predicted tenures. For more democratic leaders, being under a loan has a negative – but not statistically significant – impact. The marginal effect of a loan for a full autocracy (Polity = −10) is statistically higher than the marginal effect for a full democracy (Polity = 10). 11 This is the case even when I control for the actual onset of the loan, the effect of which is more positive for democratic leaders. 12 This would suggest that early on in the process democratic leaders are aided by agreeing to a loan, but as time goes on, the benefits disappear because of the costly implementation. The other variables perform as expected (with GDP growth improving tenure), except for the previous leader and inflation variables (which are not statistically significant).

In order to account for non-random sample selection caused by the decision to participate in these loans, I use a selection duration model that simultaneously estimates the selection outcome (participation in an IMF agreement) and the duration outcome (length of leader tenure given an IMF agreement). 13 Similar to Smith and Vreeland (2006), I theorize that the effects of IMF arrangements on leader survival depend on the leader’s regime type. We differ in our empirical expectations because I propose that leaders choose whether to participate in IMF loans with their expected post-reform tenures in mind.

I therefore expect to find three empirical results from the selection duration model (Boehmke et al., 2006). First, I expect to find that, given an IMF agreement, the more democratic a state is, the shorter that leader’s tenure will be. Second, I theorize that because of their shorter post-reform tenures, democratic leaders will be less likely to participate in IMF loans, all else being equal. Finally, since leaders ‘pick their poisons’ based partly on their likelihood of surviving the necessary reforms, I expect to find a positive correlation between the likelihood of accepting an agreement and the leader’s post-reform tenure. The results of the simultaneously estimated selection equation and the duration model are presented in the second column of Table 2.

The selection equation in the second column predicts whether a loan occurs in that leader-year. 14 Similar to either a logit or probit, positive coefficients indicate that the variable increases the probability of an IMF loan. As hypothesized, the polity regime type variable is negative, indicating that the more democratic a country is, the less likely it will be to accept an IMF loan. I argue that this is because authoritarian leaders are in a better position to benefit, so that they are more likely to participate in these loans. Many of the economic variables in the selection model are not significant, which is not surprising given that previous studies have found that ‘many key macroeconomic variables have weak or indeterminate effects on IMF lending’ (Copelovitch, 2010: 53; see also Joyce, 2004). 15 The real effective exchange rate and total foreign reserves variables are statistically significant and in the expected direction. This finding makes sense, as the larger reserves a state has, the less they need an IMF loan. The other economic variables are not statistically significant, possibly because the level of reserves is the most important factor in accepting a loan. Moreover, the oil crisis dummy variable is statistically significant, indicating both an increase in demand for IMF loans and a subsequent decrease in alternative lenders. States that have previously had IMF arrangements are likely to receive another loan. This is shown by the positive and statistically significant coefficients for both the lagged dependent variable (IMFt-1) and the number of previous loans by that country. The negative coefficient for leader tenure indicates that leaders early in their tenures are also more likely to accept an IMF arrangement.

The duration equation in the selection duration model estimates the tenures of leaders under IMF agreements. It is important to note that the coefficients in Table 2 are in accelerated failure time (AFT) metric, which implies that larger coefficients indicate longer durations and smaller hazards. Given that it is a selection model, the coefficients represent the effects of the variable on leader duration given the occurrence of an IMF agreement. In a sense, these coefficients are limited interaction terms in that they represent the effects of the variables on leader tenure given the occurrence of an agreement (or when IMF = 1). 16

To test my hypothesis, I include regime type with the expectation that the coefficient will be negative. The regime type variable is statistically significant and negative, which implies that, given an IMF agreement, the more democratic a nation, the shorter the leader’s tenure. The dummy variable indicating whether the IMF loan began in that year (IMF onset) is not statistically significant, indicating that there is no statistical difference between whether the occurrence or onset of loans affect leader tenure.

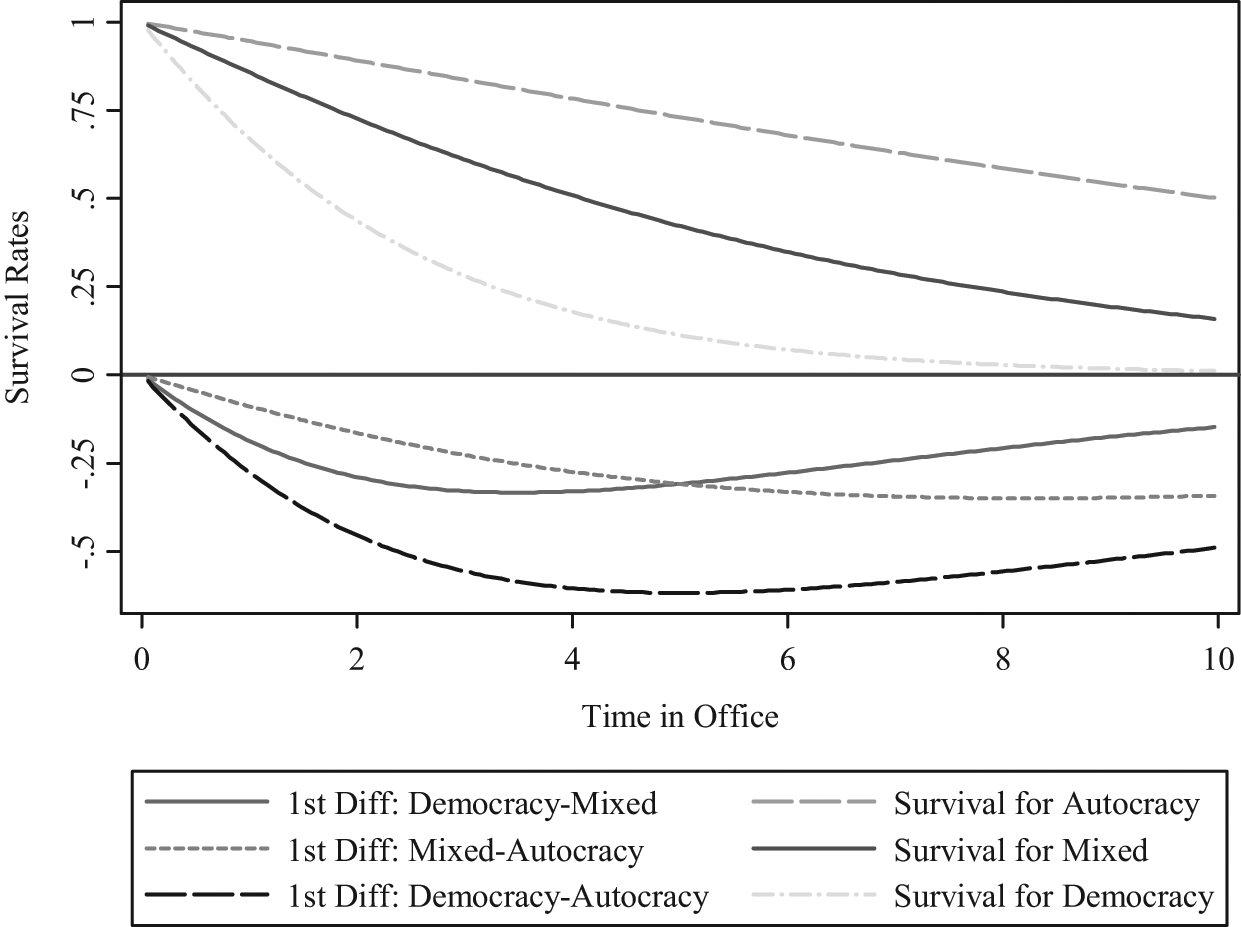

One way to view the conditional relationship between regime type, IMF loans and leader tenure is by presenting the survival rates of three leaders of different regime types facing identical conditions. The top panel of Figure 2 provides the predicted survival rates for three types of governments under an ongoing IMF agreement, holding all other variables constant. 17 The top half shows the predicted survival rates for the three regime types while the bottom half (below 0) shows the first differences in predicted survival rates. As expected, the effects of IMF loans on survival depend on the leader’s regime type. Authoritarian regimes are much more likely to withstand the costs of structural adjustment and maintain their position than leaders of either mixed regimes or democracies. The survival rates for authoritarian leaders decrease slowly over time in office, while the survival rates for democracies decline exponentially. This is to be expected, as the vast majority of democratic leaders do not last more than 10 years in office. It is interesting to note, however, that it is during their first four to five years in office that the first differences between the survival rates for various regimes are the greatest in magnitude. For all leaders, the first few years in office have high survival rates. However, when under an IMF agreement at year t + 5, survival rates for authoritarian leaders (about 0.75) and for democratic leaders (about 0.10) are vastly different. As expected, the first difference from democratic and autocratic leaders is the largest of any of the first differences, with the difference the greatest at about year t + 5. Regardless of the political, economic and social circumstances, authoritarian leaders have much higher survival rates than leaders of both mixed and democratic regimes when faced with an IMF arrangement. This buttresses my theory that democratic leaders’ hold on power will be more tenuous after an IMF loan. In fact, robustness checks indicate that this conditional relationship holds even when the size of the loan is taken into account. 18

Survival rates for leaders of various regime types under ongoing structural adjustment loans: selection duration model

The rest of the control variables perform as expected, except for GDP growth (which is not statistically significant) and the dummy variable measuring whether the current loan was signed by a previous leader (which is negative and significant). The latter result indicates that there is no ‘scapegoating’ benefit, contrary to what has been previously suggested by scholars (e.g. Remmer, 1986). Rather than increasing a leader’s duration by allowing the leader to blame the previous leader for the difficult adjustment, being under a previous leader’s arrangement decreases the current leader’s tenure. Inflation is negative and statistically significant, indicating that domestic economic problems increase the hazard for termination.

The selection model’s ancillary parameters also provide vital information about the underlying hazard rate and the importance of the selection equation. The first parameter, α, provides the correlation between the error components of the two models with the null hypothesis that the non-random sample selection is ignorable. The positive and statistically significant α parameter indicates that there is unignorable selection bias because the decision to participate in an IMF loan creates non-random sample selection in the analysis of their effects on leader survival. The positive correlation is generally consistent with my hypothesis regarding the danger of loans for leaders. It indicates that the higher the expected post-reform tenure, the more likely the leader will accept an IMF arrangement. This also provides support for the third component of my theory, mainly that there is positive correlation between the decision to enter into an agreement and the leader’s anticipated survival rates. Also, the statistically significant ρ parameter points to a rejection of the null hypothesis of duration independence. This is shown by Boehmke et al. (2006) to be a result of estimating a naive model in the face of non-random sample selection. They show that this can bias the duration dependence parameter (ρ) in the same direction as the error correlation (α). More substantively, this finding echoes Smith and Vreeland’s (2006) finding that the underlying hazard of losing office decreases the longer the leader is in office (because ρ < 1).

To what extent does the selection bias inherent in the choice to accept a loan actually affect the estimation of the survival rate? Estimating a Weibull model in the face of selection bias has been shown to bias the constant downward in Monte Carlo simulations. Since a higher constant indicates a smaller hazard rate and longer leader tenure (when all the variables are held constant at 0), by comparing the constants from the Weibull and selection duration model in Table 2, one can see that the Weibull model artificially inflates the risk of leader termination because it ignores the selection procedure (Boehmke et al., 2006). More importantly, selection bias ‘attenuates estimates of causal effects on average’, which produces numerical estimates that are closer to zero than they actually are (King et al., 1994: 130).

Figure 3 further addresses this question by providing both the Weibull (shown in the first column of Table 2) and the selection duration model estimated survival rates for leaders under an ongoing IMF arrangement signed by the current leader, for four different regime types. 19 Recall from Figure 1 that the marginal effect of an IMF loan is positive for autocratic leaders and negative for democratic leaders. The similarity in survival rates between the two models varies as a function of regime type. For fully autocratic leaders, the Weibull duration model actually under-predicts the survival rates of leaders principally because it underestimates the positive effects of IMF loans. Though the lines appear close because of the scale of the figures, in some cases the Weibull model predicts a much lower survival rate than the selection duration model. For example, during the sixth year of the autocratic leader’s tenure, the Weibull survival rate is 0.17 lower than the selection duration model. When the selection procedure is taken into account by the selection model, the estimates of autocratic leader survival rates are actually higher than the Weibull model would predict.

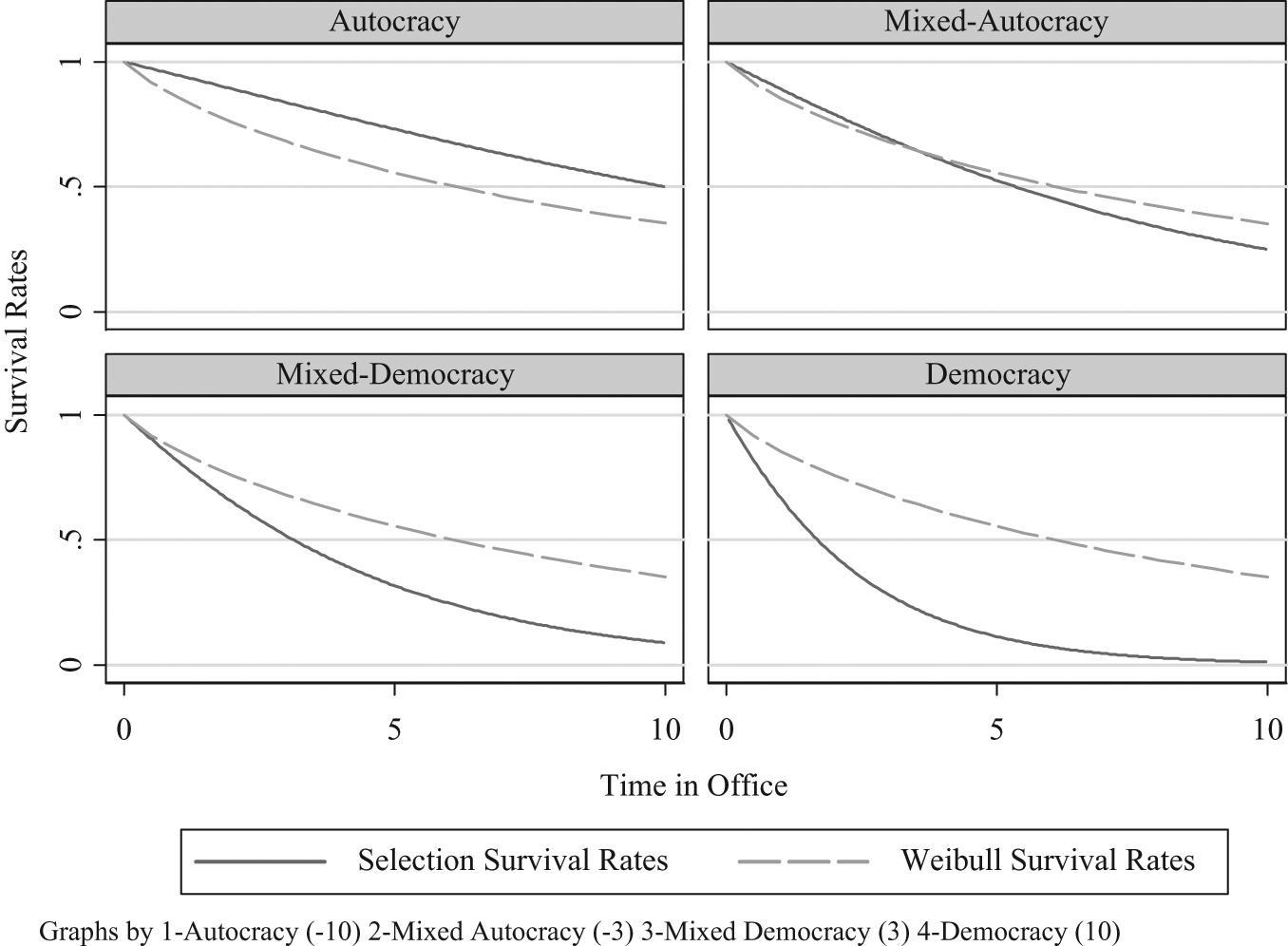

Weibull model’s underestimation of the effect of IMF loans on survival rates of various regime types compared to selection duration model estimates

This bias is particularly important for democratic leaders, where there are larger differences in the predicted survival rates. This makes intuitive sense because democratic leaders have a much more tenuous hold on power, which discourages them from choosing to participate in an IMF agreement (especially given the negative marginal effect of IMF loans for fully democratic leaders in Figure 1). Since the Weibull model is unable to incorporate the selection mechanism, the negative effect of participating in an IMF loan for a fully democratic leader is biased toward zero. Substantively, this means that the Weibull model predicts a much higher survival rate for democratic leaders than it should. Indeed, the direction of bias – as well as the magnitude – is a function of the leader’s regime type, since regime type conditions the effects of IMF arrangements on leader tenure. This figure is further evidence that the Weibull model produces biased results because it is based on a non-random sample of IMF arrangements. This supports my assertion that the selection procedure substantially improves the prediction of leaders’ survival rates in modeling scenarios where leaders are faced with both economic crisis and IMF adjustment.

Conclusion

When examining the options for addressing economic crises, leaders must pick their poison. While some choose to withstand pressure to accept IMF loans, others look to the IMF for help in solving balance-of-payments problems. In this paper, I examine why leaders pick the poison they do. I develop a theory that suggests that the decision to participate in an IMF loan and the loan’s subsequent effects on leader survival are intricately linked. To do so, I build on Smith and Vreeland (2006), who suggest that IMF loans affect survival differently according to the size of the leader’s winning coalition. Autocrats rely on a much smaller segment of the population in order to stay in power. They maintain the support of their winning coalition through the provision of private goods, which can be better insulated by an authoritarian leader in a post-reform environment. Further, autocrats are able to weather the storm of reform more easily because they can repress groups of the public to lessen the risk of political violence from redistributive concerns. My contribution to this literature is that both democratic and authoritarian leaders make a decision whether to approach the IMF for a loan based on their hold on power. In this case, both types of leaders pick their poison. Since democratic leaders have a more tenuous hold on power, they are less likely to open themselves up to the political unrest that accompanies IMF loans, as demonstrated by the negative coefficient for the regime type variable in the selection model. Alternatively, authoritarian leaders are more likely to accept an IMF loan because they know that their hold on power is stronger than that of democrats, so that they are much more likely to benefit from loans, even given the potential for a rough adjustment period.

While I use Smith and Vreeland (2006) as my theoretical foundation, I uncover empirical results that arrive at a conclusion that is far different from their conclusion that democratic leaders’ tenures are lengthened by participating in IMF loans. There are two likely explanations for these opposing conclusions. The first possible explanation is that Smith and Vreeland (2006) argue that loans influence survival rates differently according to whether the loan is need-based or discretionary. While in the abstract this adds a layer of nuance to the argument, in practice it results in more missing data and demands that assumptions be made about the accuracy of the predictive model. As the qualitative data allowing us to identify the ‘discernible causes’ for motivations for accepting loans improves, scholars will be able to revisit their findings and take into account the selection procedure. Until then, scholars have to rely on the variables in the selection equation (such as GDP growth, foreign reserves and debt) that incorporate discretionary and need-based motivations.

Another possible explanation for these contradictory findings is the fact that estimating a model on leader survival rates in the face of non-random sample selection has the potential to bias coefficients (Boehmke et al., 2006). I argue that these counter-intuitive findings are possibly a result of non-random sample selection caused by the politically costly decision for a leader to pull his state into an IMF agreement. As expected, there is a positive correlation between expected post-reform tenure and the decision to accept an IMF loan. For this reason, authoritarian leaders are more likely than democratic leaders to select themselves into IMF agreements because they view their post-reform political situation as much more conducive to their survival in office. Democratic leaders, on the other hand, are more cautious about entering into agreements because they are unlikely to see the political benefits of adjustment. These factors combine to result in the vast differences in expected tenures between authoritarian and democratic leaders when faced with IMF loans under the exact same domestic and international circumstances. The poison leaders pick depends on their assessments of their own post-reform tenure.

By developing a theory that the motivations for participating in loans are a function of the leader’s expected post-reform tenure, the field can gain a better understanding of the politics of IMF lending. This also has implications for the potential success of IMF agreements, as it is important to realize that cases where the loans may be successful may also have leaders who spurn these loans because they anticipate their removal.

Footnotes

Acknowledgements

I would like to thank Glen Biglaiser, Matthew Hoddie, Michael T. Koch, Daniel Morey, Harvey Palmer, Randy Stevenson, Martin Steinwand, Robert Walker, Guy D. Whitten and Byungwon Woo for their helpful comments.