Abstract

Purpose

The purpose of this article is to explore the disclosure of corporate sustainability (CS) practices and to examine the association between sustainability performance and financial performance in Asian context considering firms from India and Japan.

Design/methodology/approach

The present study is based on secondary data collected from annual reports and CS reports of 28 and 35 listed non-financial firms from India and Japan from 2009 to 2014. Content analysis (binary coding system) is employed to calculate the sustainability disclosure score based on Global Reporting Initiatives (GRI) framework. Market-to-book ratio is used to measure the financial performance. These scores are further used to examine the impact of CS performance on financial performance employing both the panel data model and logit regression model.

Findings

The study finds that the average level of disclosure is more in case of Japanese firm as compared to Indian firms. Using both the regression model, the study finds the influence of CS performance on financial performance is positive and significant for both the nations. However, the influence of CS performance is more in case of Japan than that of India. Moreover, the study also reveals that environmental factor is more dominating in influencing the financial performance in Japan. Whereas, in India, it is the social factor that dominates the financial performance.

Originality/value

It is the first comprehensive study in Asia analyzing the CS practices using both the panel data regression model and logit regression model.

Keywords

Introduction

With the growing environmental and social concerns worldwide, the present decade has witnessed a paradigm shift of the business firms from the traditional financial expectations to corporate sustainability (CS). The publication of ‘Brundtland Report’ of World Commission for Environment and Development (WCED) in 1987 along with increasing demand of the ‘voice of society’ (Warhurst, 2000) has encouraged corporate firms to bring a strategic change in the management process by focusing on triple bottom line in a balanced manner. According to the concept of triple bottom line, every organization must put an effort to give equal importance to society, environment and economy (Elkington, 1994) and such performances must be communicated in the form of a report known as Sustainability Report or Business Responsibility Report. The broad concept of CS encompassing short-term and long-term economic, social and environmental performances has emerged as a strategic weapon for a firm to maintain healthy relationship with the stakeholders (Cortez & Cudia, 2011; Lopez, Garcia & Rodriguez, 2007) and eventually to fulfil the broad dimensions of sustainable development (Gladwin, Kennelly & Krause, 1995). The fulfilment of the needs of the society helps firm to reduce cost through efficient utilization of scarce resources, increase revenue through sale of social-environmental friendly products, improves transparency, reduces conflict of interest and finally enhances firm value (Lo & Sheu, 2007; Matjaz, Damjan, Jens, Su & Boštjan, 2014; Ngwakwe, 2008). The growing importance of CS in the recent times has attracted the interest of researchers to investigate empirically the association between sustainability performance and firm performance (Cho & Patten, 2007; KPMG, 2011).

According to various survey reports, there is an increasing trend of publishing sustainability report around the globe, although the quantum of publishing report is very high in developed countries like USA, UK, Japan, France, Germany and many other European countries (Carrot & Stick, 2013; KPMG, 2011, 2013). Consequently, most of the studies relating to the CS issues are concentrated in those developed economies (Isabel, Castelo, Curto & Teresa, 2012; Lo & Sheu, 2007; Lopez et al., 2007; Tracy, Lee, Nelson & Walker, 2010). However, the researchers have mainly focused on the overall aspects of CS and have ignored in most of the cases the contribution of the components of CS on firm performance. Likewise, there are some studies where the researchers have addressed any one of the components of CS as the indicator of sustainability to find out the association between CS and firm performance (Hillman & Keim, 2001; Waddock & Graves, 1997; Wagner & Wehrmeyer, 2002). On the other hand, a few empirical studies have investigated the influence of overall CS and its components on firm performance (Ameer & Othman, 2012; Burhan & Rahmanti, 2012; Ho & Taylor, 2007; Krishna & Lucus, 2010). However, the findings of these studies are inconclusive, encompassing positive association (Lo & Sheu, 2007; Isabel et al., 2012; Tracy et al., 2010), negative association (Ho & Taylor, 2007; Lopez et al., 2007) and insignificant association (McWilliams & Siegel, 2000; Ullman, 1985; Wagner & Wehrmeyer, 2002).

In Asian context, the survey reports of KPMG (2008, 2013) and Carrots and Sticks (2013) have demonstrated that the concept of CS is highly developed in Japan and Korea. The reports also reveal that Japanese firms produce highest number of sustainability report in Asian context, while the concept of CS is still evolving in India. Nevertheless, the empirical studies relating to the association between corporate sustainability performance (CSP) and financial performance in developed nations of Asia in the matter of publishing CS report are very limited (Choi et al., 2010; Cortez & Cudia, 2011; Hidemichi et al., 2012; Ho & Taylor, 2007) to the best of our knowledge, and the results are inconclusive. On the other hand, in Indian context, most of the studies are descriptive in nature focusing on the disclosure of CS (Aggarwal, 2001; Bhatia & Chander, 2014; Ghosh, 2002; Murthy, 2008). Further, there is no comparative study relating to the association between sustainability performance and firm performance between the developed and developing countries. To address the above research gaps, the present study is a modest attempt to explore the sustainability reporting practices and to investigate the association between CSP and financial performance for the Indian and Japanese firms.

We select India and Japan for the following reasons. First, only a handful of empirical studies relating to the CSP and financial performance are conducted in India and Japan. Second, the concept of CS is highly developed in Japan, thus, providing highest number of sustainability report in Asia. On the other hand, the concept of CS is still in its nascent stage in India (Carrot & Stick, 2013). Third, there is a lack of comparative study relating to CSP between these two countries. In Asian context, most of the studies are descriptive in nature (Belal, 2001; Bhatia & Chander, 2014; Ghosh, 2002; Imam, 2000). There are some studies, where only one component is used as a proxy for CS (Cortez & Cudia, 2011; Hidemichi et al., 2012). Only a few studies considered all the components (Ameer & Othman, 2012; Burhan & Rahmanti, 2012; Ho & Taylor, 2007) and the results are inconclusive. This study contributes to the existing literature by providing information relating to the impact of overall as well as component-wise disclosure score of CS on the market-to-book ratio (MBR) from two countries–Japan and India, where the former is more advanced in publishing sustainability reporting as compared to the later. The outcome of the study is expected to be useful for both corporate firms as well as other stakeholders relating to the influence of publishing sustainability report on the market value (MV) of the firm. Further, a comparative study may be helpful to the corporate managers for investment decision making towards CS and may help the policymaker in formulating policy for contributing towards sustainable development.

The rest of the article is organized as follows. The second section presents literature review and development of hypotheses. The third section discusses data and methodology adopted in this study. The fourth section is devoted to the results and discussion followed by practical implications in the fifth section, and concluding remarks are presented in the sixth section.

Literature Review and Development of Hypotheses

Disclosure of Corporate Sustainability

The publication of the ‘Our Common Future’ report of the WCED in 1987 is regarded as the landmark for the growth of sustainable development all over the world ‘that meets the needs of the present without compromising the ability of future generations to meet their own needs’. (WCED, 1987: p. 43) The increasing demand of the stakeholders relating to the contribution of firms towards sustainable development has considerably changed the attitude of firms towards publishing sustainability report and consequently, measuring firm performance employing only economic indicators is regarded as insufficient (Ho & Taylor, 2007). To facilitate such reporting, several frameworks like GRI, The UN Global Compact (UNGC), United Nation Principle for Responsible Investment (UNPRI), Organization for Economic Co-operation and Development (OECD), etc. have been developed.

Extant literature reveals that large number of research studies has been carried out both in developed and developing countries relating to CS disclosure practices. For instance, Guthrie and Parker (1990) studied the corporate social reporting practices in the UK, USA and Australia. The study indicated that the overall level of disclosure was 98 per cent in USA, followed by 85 per cent in UK and 56 per cent in Australia. Similarly, Thom and Decoutere (2009) found such level of disclosure to be around 81 per cent in Belgium. While analysing the sustainability reporting practices in case of eight Latin American companies, Carvalho and Siqueira (2007) observed that the overall level of disclosure was 50 per cent. On the other hand, Lungu, Carauabu and Dascelu (2011) found the extent of such disclosure to be around 88 per cent in case of leading companies from Global Fortune 500. However, the review of literature from developing countries reveals lower level of CS disclosure. In Malaysia, the level of disclosure was found to be lower than 26 per cent (Ahmed et al., 2003; Andrew et al., 1989), followed by 41 per cent in Bangladesh (Belal, 2001; Imam, 2000), 26 per cent in Singapore (Andrew et al., 1989; Tsang, 1998) and around 46 per cent in India (Aggarwal, 2001; Ghosh, 2002; Murthy, 2008). Similarly, Bhatia and Chander (2014) found that the extent of overall responsibility disclosure varied between 8 per cent and 52 per cent for 30 SENSEX companies in India in 2009–2010. Furthermore, among the three components of CS the review of literature indicates that the environmental aspect is the most favoured category of disclosure in developed countries (Carvalho & Siqueira, 2007; Ho & Taylor, 2007; Lungu et al., 2011; Thom & Decoutere, 2009). In contrary, social aspects of CS are mostly reported in developing countries (Bhatia & Chander, 2014; Murthy, 2008; Tsang, 1998).

Sustainability Performance and Firm Performance

Apart from studies relating to the analysis of sustainability disclosure practices, researchers also focused on its association with firm performance. Corporate sustainability is a broad societal guiding model that incorporates the three concepts (economy, society and environment). However, there are studies where researchers considered either one or two of the component(s) to examine the association with firm performance. On the other hand, there are only few studies where researchers included all the three components to investigate the association with firm performance.

Studies relating to sustainability performance and firm performance have been carried out mostly in the developed market. For instance, on studying the association between sustainability performance and MV of the firms in US market, researchers have found positive and significant association (Isabel et al., 2012; Lo & Sheu, 2007) and concluded that firms with better sustainable strategy were more likely to be rewarded by the investors. Likewise, the outcome of the study conducted by Isabel et al. (2012) also revealed that investors tend to penalize firms with lower level of sustainability performance, irrespective of their profitability. While examining the factors affecting sustainability performance in case of US firms, Tracy (2010) observed that investment towards sustainability principles leads to significantly higher firm size, high growth potential and profitability. Again, Laskar and Maji (2016) examined the CS reporting practices in India. The study found an increasing trend in disclosing information related to CS. Moreover, the study also encountered positive and significant association between CS reporting and firm performance. Ameer and Othman (2012) also found similar results for top 100 global sustainable companies from both developed and emerging nations. Likewise, Krishna and Lucus (2010) investigated the association of sustainability reporting and financial performance in case of 68 listed companies from New Zealand and Australia. The study observed that the association between sustainability reporting and MV of the firm was positive and significant only in the case of Australian firms. However, only social reporting was found to be significant in case of companies selected from New Zealand. Similarly, the findings of Burhan and Rahmanti (2012) indicated that among the three components of sustainability, only social performance was found to have positive and significant influence on firm performance in Indonesia. In contrary, there are studies where the researchers observed significant negative association between sustainability performance and firm performance in case of USA and Japan (Ho & Taylor, 2007; Lopez et al., 2007). On the other hand, Maji and Laskar (2014) found insignificant association between sustainability performance and firm performance, in the context of 18 listed non-financial companies from India. According to their study, the main plausible reasons for insignificant association were limited study period (i.e., four years) and less number of companies studied.

Dobbs and Staden (2016) examined the motivation for CS reporting in the context of 122 companies listed in New Zealand Stock Exchange. The outcome of their content analysis indicated that community concern and shareholder rights were the important drivers of CS reporting. According to this study, CS reporting was used as tool to legitimate their actions with a range of stakeholders. However, the study did not examine the impact of such reporting on the firm performance. On the other hand, Ortas et al. (2015) investigated the association between companies’ financial factors and CS reporting for 3,931 companies operating in 51 industries from 59 countries. Employing content analysis technique to measure CSP (i.e., CS reporting) based on GRI framework, the outcome of the study indicated that firms’ financial performance served as a driver of CS reporting only for those companies who were active in disclosing sustainability information. The outcome of quantile regression model further revealed that the impact of CS reporting on firm performance was significant at upper quantiles of the distribution of the response variable. The results clearly demonstrate that the MV of company and sustainability reporting practices are positively associated only for those companies that are particularly active in such practices. Using a sample of 141 respondents distributed across Anambra state in south-eastern Nigeria, Ekwueme et al. (2013) examined the association between CS reporting and firm performance. The results of the study showed a significant positive association between CS reporting and corporate performance. The study revealed that investors and consumers were inclined to purchase the products of green companies, which positively influences the MV of the companies. The study further reported that the companies must adopt CS reporting practices for attaining competitive advantage. Similarly, Hussain (2015) examined the impact of sustainability performance on financial performance by employing content analysis technique on the CS reports of Global Fortune N100 firms from 2007 to 2011. The outcomes of their fixed effect regression models revealed a positive and significant association between CS reporting and the different measures of financial performance i.e., ROA (Return on Assets), ROE (Return on Equity) and MBR. While conducting a systematic review using 316 articles related to CS reporting published in English journals between 2000 and 2015, Dienes et al. (2016), however, reported inconsistent and ambiguous findings with regard to the impact of firm’s profitability and leverage on CS reporting. The findings are consistent with the exploratory study of Hahn and Kuhnen (2013) for 178 articles published between 1999 and 2011. In another study, Zhao and Patten (2016) conducted an exploratory analysis of managerial perceptions of CS reporting in China. The outcome of the study indicated that managers considered CS reporting as a tool to enhance firm’s image.

The extant literature also reveals that social dimension of sustainability helps in attracting socially responsible consumer, increasing returns, satisfying stakeholders’ needs that eventually leads to better firm performance (Clarkson, 1995; Lev et al., 2008). Chen et al. (2015) examined the relationship between corporate social performance and financial performance in the context of 75 manufacturing companies collected from GRI website. The outcomes of the study indicated that the human rights, society as well as product responsibility were positive and significantly correlated with the financial performance. Employing Kinder, Lydenberg and Domini (KLD) index, a multidimensional measure of social performance, Hillman and Keim (2001) examined the influence of corporate social performance on financial performance. The findings of the study revealed that employees and customers were having a positive and significant influence on the financial performance of the firm. Such positive association tends to be negative when social performance involves high costs than the derived benefits (Boyle, Higgins & Rhee, 1997; Brammer, Brooks & Pavelin, 2006). On the other hand, there are some studies where the researchers found insignificant association between social performance and firm performance (Garcia-Castro et al., 2010; McWilliams & Siegel, 2000).

The review of literature also indicates that some researchers considered only environmental aspects of sustainability to investigate its association with firm performance. For instance, Hidemichi et al. (2012) investigated this association in case of Japanese manufacturing firms. The study indicated a significant positive association between environmental performance and firm performance, which is consistent with the study of Cortez and Cudia (2011) in the case of Japanese firms. Considering environmental performance as a proxy for CS, Russo and Fouts (1997) examined the relationship between environmental performance and financial performance in the context of 243 firms from USA. The results of the pooled data regression model revealed that environmental performance was significant and positively related with the financial performance of these firms. On the other hand, Wagner and Wehrmeyer (2002) examined the relationship between environmental performance and firm performance in case of European firms. However, the study failed to disentangle any significant association between environmental performance and firm performance.

The extant review of literature relating to the empirical association between CSP (including its three components) and firm performance indicates mixed result. These differences in findings may be ascribed to differences in methodology adopted (Wagner & Wehrmeyer, 2002), study period examined, discontinuation in reporting and the wide variation in variables used to measure sustainability performance and firm performance. However, theoretically there is positive association between sustainability performance and firm performance (KPMG, 2008). Sustainability reporting helps in maintaining healthy relation with stakeholders, reduces risk of boycott from society and attracts socially responsible investments (SRI), which ultimately enhances firm’s overall performance. Thus, based on the theoretical association between CSP disclosure and firm performance, the present study intends to test the following alternate hypotheses:

H1: There is a positive association between CSP and firm performance. H2: There is a positive association between corporate economic performance and firm performance. H3: There is a positive association between corporate environmental performance and firm performance. H4: There is a positive association between corporate social performance and firm performance.

Developed countries support the development of sustainability strategies by providing legal safeguard to firms because such strategies help in boosting the economic development (Ho et al., 2012). According to Porter and Kramer (2006) developed countries have better resources like advanced technology, skilled labour, etc., to deploy towards sustainable development. Bhatia and Chander (2014) in the context of 25 leading Indian companies indicated that the responsibility behaviour of the firm was very poor in India. On the other hand, such behaviour was found to be much advanced in developed countries. The findings are in line with the survey reports of KPMG (2008, 2016) and Carrots and Sticks (2013). These survey reports have demonstrated that in Japan, being a developed country, the concept of CS is much advance as compared to India, which has recently started such practices. Thus, in terms of the influence of CSP on firm performance, it is legitimate to expect that there is a significant difference between the firms from developed and developing countries. Accordingly, the following hypothesis is formulated for testing:

H5: The association between CSP and firm performance is significantly different between Japan and India.

Data and Methodology

Source of Data, Study Period and Sample

The present study is based on the secondary data collected from the published annual reports and sustainability or responsibility reports of the listed non-financial companies from India and Japan for a period of 6 years from 2009 to 2014. Non-financial companies are considered because the study is based on the GRI reporting guideline in which all the items specified in the framework might not be applicable for financial companies to report. Although there are different platforms (like company’s respective website, Corporate Registrar website, UNGC website, GRI website, etc.) where companies are publishing their respective CS report, but the present study is relying on the respective company’s website to collect the sample due to easy availability. Initially all the non-financial firms listed in Bombay Stock Exchange (BSE) for India and Tokyo Stock Exchange (TSE) for Japan are considered. While publishing annual reports is mandatory for both the nations, publishing CS report is voluntary. Thus, the study has developed three distinct criteria in order to select the sample: (i) a listed non-financial company must publish its CS report in the respective website; (ii) a company must publish its CS report in English language; and (iii) a company must publish its CS report on a continuous basis. Continuous reporting displays a sense of responsibility towards the society and environment at large (Carrots and Sticks, 2013). From the available number of listed non-financial companies, only 28 from Indian and 35 from Japanese non-financial companies could fulfill these criteria. Thus, the final sample of the present study consists of 28 non-financial companies from India and 35 from Japan. Moreover, it is also worth noting that there are many companies who are publishing their CS report in different places like Corporate Registrar website, UNGC website and GRI website; however, these companies are outside the purview of this research.

Measurement of Variables

Dependent Variable

In this study, financial performance is the dependent variable that is measured by MBR. The extant literature indicates that the researchers have used market-based measures of firm performance (Lo & Sheu, 2007; Marti et al., 2015). MBR is calculated by dividing the MV by book value (BV) of common stock. Market value of common stock is the product of the number of outstanding equity share and share price at the end of each financial year.

Explanatory Variables

Corporate sustainability performance and its three components, such as social performance (SOP) environmental performance (ENVP) and economic performance (ECOP) are used as explanatory variables in this study. For measuring CSP, researchers have widely adopted the common methodology of content analysis (Aggarwal, 2001; Ahmed et al., 2003; Belal, 2001; Guthrie & Parker, 1990; Lungu et al., 2011; Murthy, 2008; Thom & Decoutere, 2009). Thus, the present study has also employed content analysis technique based on GRI framework to calculate the disclosure score. GRI framework is found to be most suitable for the study because majority of the sample companies have adopted this framework for publishing their respective sustainability reports. For content analysis, either of the two versions of GRI framework, that is G3 and G3.1, is considered as per their applicability in the report. Because there are few sample firms who were using G3 version continuously for reporting, until new version G3.1 was released. G3 version was published in 2006 with 79 indicators altogether, and G3.1 was released in 2011 with an additional five indicators for social component. Thus, the total number of items in G3.1 version increases from 79 to 84. It is also worth noting that if the sample firm does not follow either of the versions, then content analysis is made on G3 version. To calculate the overall level of disclosure score, binary coding system is used, that is 1 if the indicator is disclosed or 0 for not disclosed. After obtaining the item/indicator-wise score, overall disclosure score for CSP and its three components (S) are computed by:

where, nj is the maximum expected score for each category, j is the company, i is the item and Xij is the estimated score of firm j at period t. Xij assumes 1 or 0 value, respectively, for disclosed and not disclosed.

Control Variables

To control the influence of firm size on financial performance as a continuous variable (Choi et al., 2010), firm size (SIZE) is used as control variable, which is computed by the natural log of total sales. The extant literature shows that financial leverage has an influence on the firm’s value (Ho & Taylor, 2007; Lo & Sheu, 2007). To control the effect of capital structure, debt-to-equity ratio (DER) is used as the indicator of leverage.

Empirical Models

Extant literature reveals that plethora of empirical studies employed classical linear regression model to investigate the association between sustainability performance and firm performance (Ho & Taylor, 2007; Hussain, 2015). In order to identify appropriate panel data regression model for the present data set, Breusch–Pagan test and Hausman test are employed. The outcomes of these two tests advocate in favour of random effect model (test results are shown in Table 1). Additionally, the variances of the random effects are more than zero and also chi-square statistics are significant (results are shown in Table 1), which clearly indicates that the random-effect models applied in the present context are appropriate.

The general form of the random effect model is:

where, Xl is the number of covariates and ωit is the composite error term.

The regression model employed in this study to examine the impact of CSPL on MBR is:

Corporate sustainability performance including its components has been measured using content analysis technique considering the published sustainability reports as the base. Although, the observed scores are quantitative in nature, basically qualitative indicators are converted into numerical terms. Considering the qualitative nature of CSP, the present effort has also employed logit model to examine the association between CSP and firm performance of select countries. For employing logit model in the present context, the outcome variable (MBR) which is metric in nature, is segregated into two groups using median value as the threshold limit (δ). Median is used as the threshold limit instead of mean to safeguard the effect estimates from the influence of the outliers present in the data set. The application of logit model along with appropriate panel data regression models would also be helpful to examine the robustness of the results. In the logit model, the log odds of the outcome are modelled as a linear combination of the predictors. Mathematically, let π be defined as:

π = P[MBR ≥ δ], then a logit model can be written as

where, X1, …, Xk are various predictors and control variables of interest, β1, …, βk are the parameters to be estimated as the effects of the predictors, and β0 is a constant. The specific logit models used in this study are:

where, CSPL is the overall level of CSP, ECOL is the level of economic performance, ENVL denotes level of environmental performance, SOL indicates level of social performance, DER is the debt-equity ratio and SIZE denotes the size of firm.

In order to test the relative impact of CSPL on firm performance between India and Japan, following logit model is employed for combined data set:

where, Dummy is a dummy variable that represents 1 for Japan and 0 for India. The sign and significance level of dummy variable after controlling the influence of CSP indicate the relative difference of the influence of CSPL on firm performance between the two counties.

Results and Discussion

Disclosure Trend

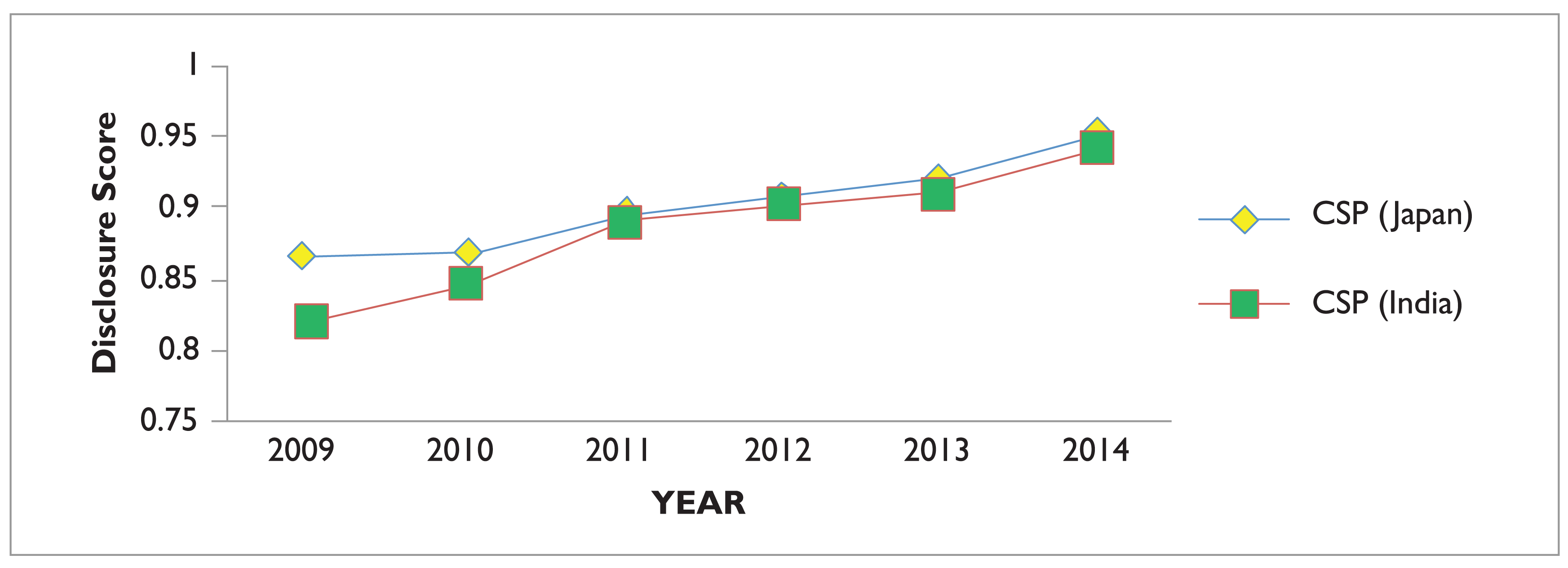

To analyze the sustainability disclosure practices of the firms selected from India and Japan, year-wise disclosure scores relating to overall CSP as well as its components are computed. These scores are shown graphically in Figures 1–3.

Overall CSP Disclosure

Figure 1 reveals the year-wise average disclosure of the overall sustainability performance by Indian and Japanese firms. The figure shows that the Japanese firms disclose more information than the firms selected from India. The disclosure scores of both the nations also indicate that there has been a continuous increase in level of disclosure. For instance, Japanese firm discloses nearly 87 per cent of items indicated in GRI reporting framework in 2009, which increases to 95 per cent in 2014. On the other hand, Indian firms disclose 82 per cent in 2009, which increases to 94 per cent in 2014. A closer look into Figure 1 further reveals that the rate of change in disclosing information is found to be more in case of Indian firms. The reason for such increase in rate may be due to the fact that Japanese firms are already disclosing large number of items than Indian firms and thus there is a little scope for improvement for Japanese firms.

Component-wise Disclosure

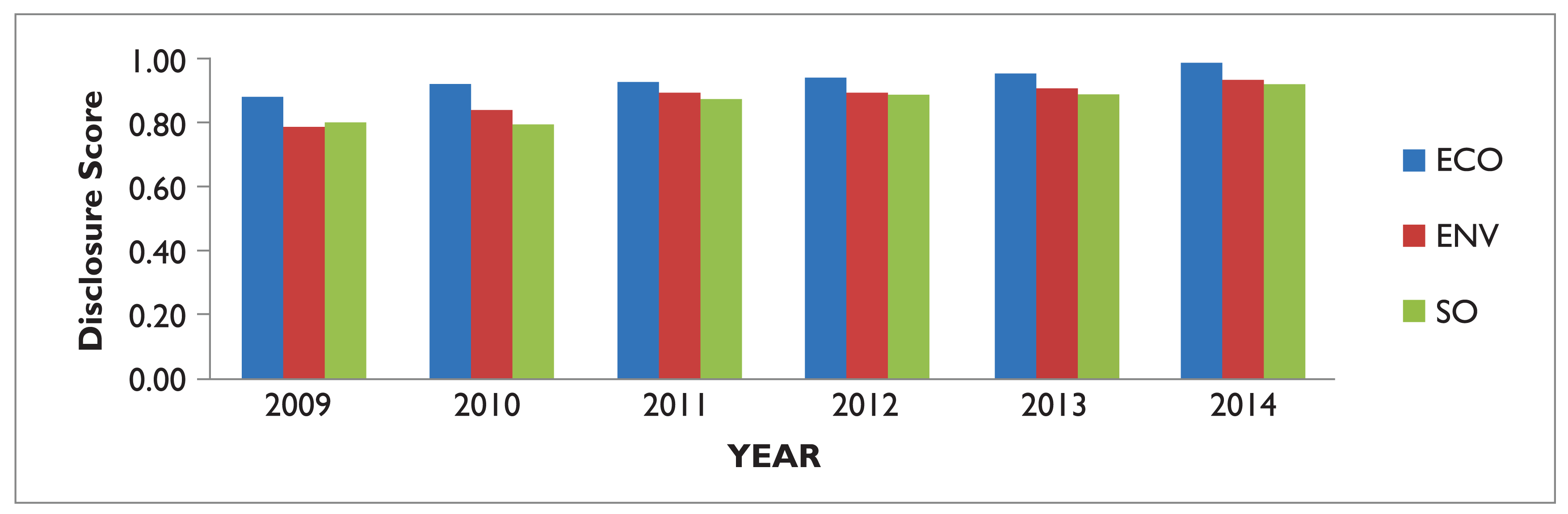

Figures 2 and 3 reveal the component-wise disclosure of sustainability performance by Japanese and Indian firms, respectively. The component-wise score reveals that the economic aspects are disclosed more followed by environmental and social aspects by both the nations. During 2009, the average level of environmental and social disclosure in the case of Japanese firms is nearly 88 per cent, while in the case of Indian firms, the level of disclosure is nearly 79 per cent. Moreover, from 2009 to 2010, unlike Indian firms, non-financial disclosure is found to be more than economic disclosure in the case of Japanese firms. These indicate that Japanese firms are more inclined towards non-financial disclosure than Indian firms, which can be visible from Figures 2 and 3. However, the rate of change in the level of non-financial disclosure in the case of Indian firms is found to be more as compared to Japanese firms. For instance, the rate of change in the disclosure of social information in 2014 is more than 4 per cent in case of India, where it is only 2.8 per cent in case of Japan. Similarly, in case of environmental aspects, it is 2.7 per cent in India as compared to 2.5 per cent in Japan. A general look into the table reveals that there has been a steady growth in component-wise disclosure of CSP for both the nations.

Association between Sustainability Performance and Financial Performance

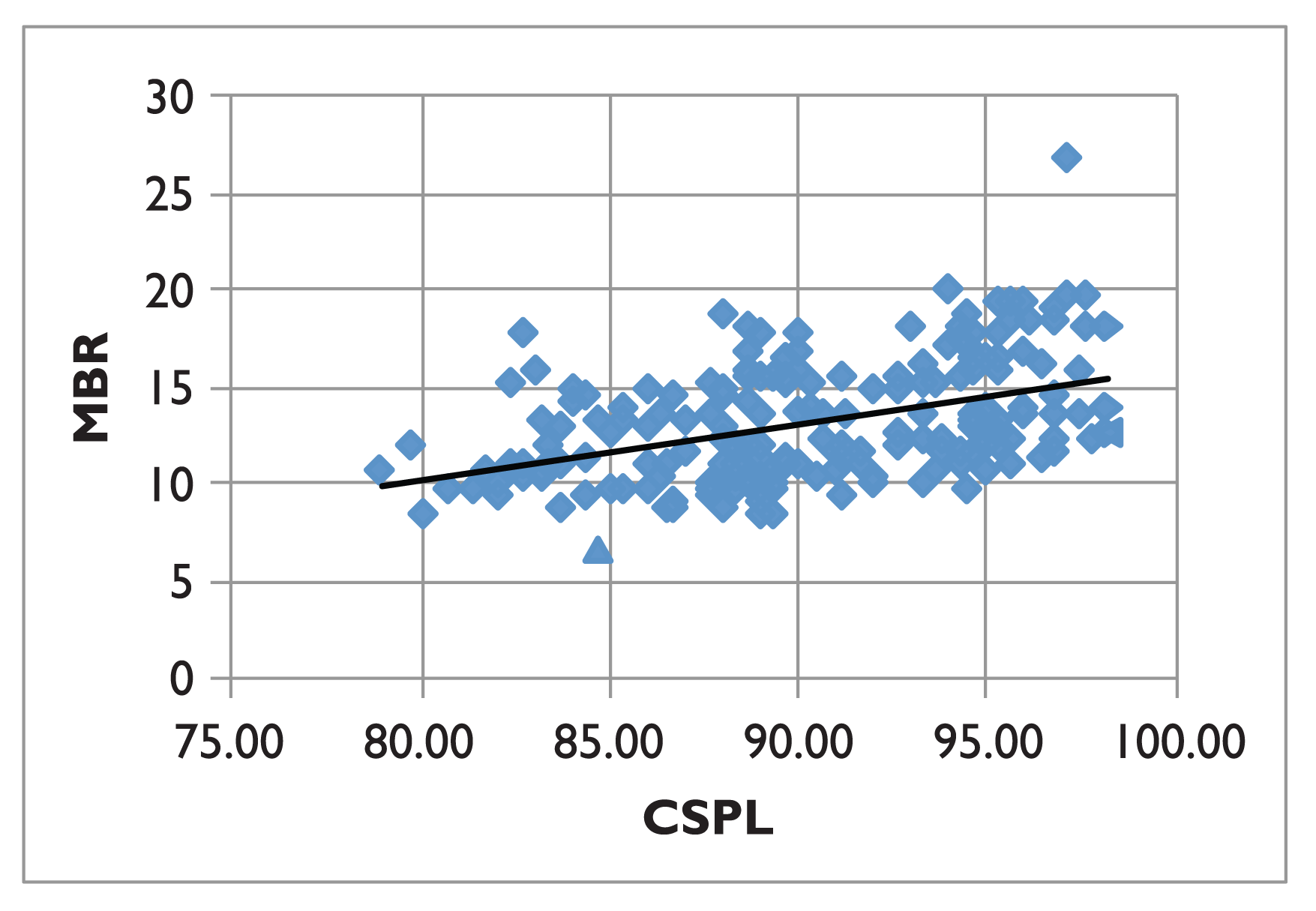

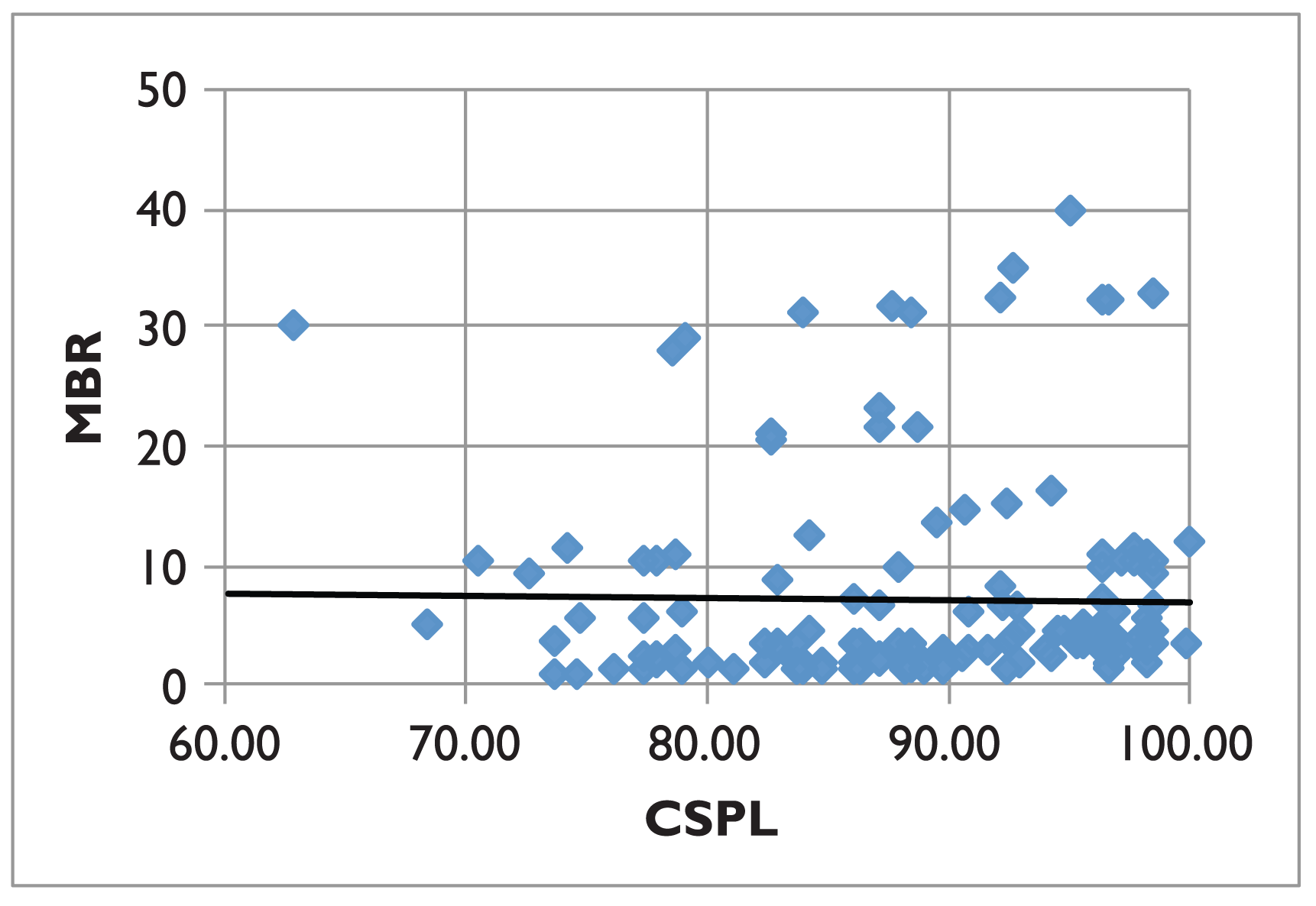

We have carried out exploratory analysis to have a primary impression of overall association between CS and financial performance using bivariate and matrix scatter plots for both the countries. The results of bivariate scatter plots are shown in Figures 4 and 5, respectively, for Japan and India. While a slow but steady increase in the slope of the linear relationship is apparent in case of Japan, but such an impression is not very obvious in case of India. The overall relationship between the study variables is significantly linear in Japan, as depicted by the scatter plot, since all except only one point is along the fitted/estimated line. In case of India, a handful of firms have found their places on the top right-hand corner on the plot in comparison to a large number of these lying much below along the horizontal axis. It is interesting, however, to ponder upon why only a handful of performing firms could achieve a high score on sustainability scale, while others do miserably low.

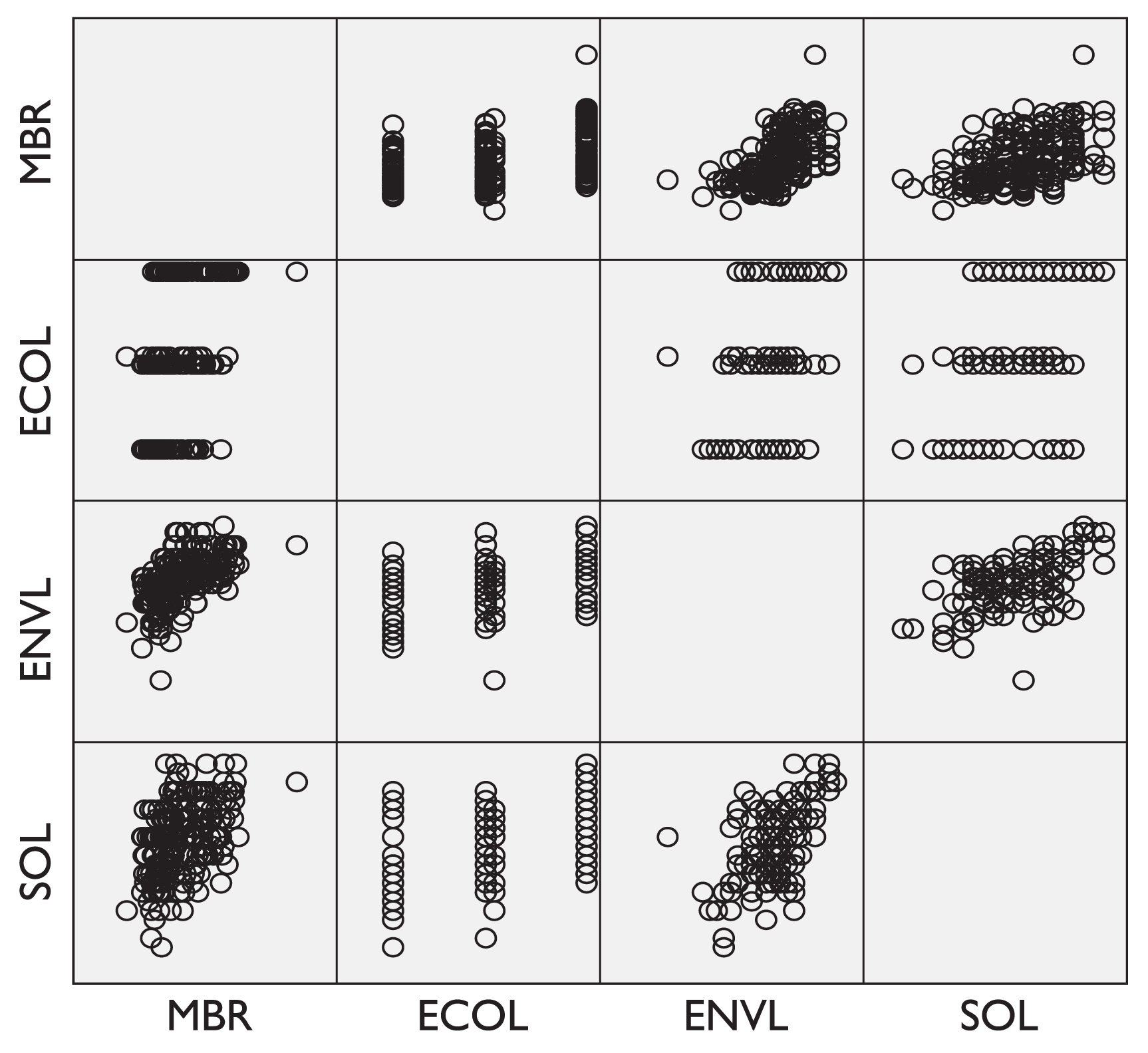

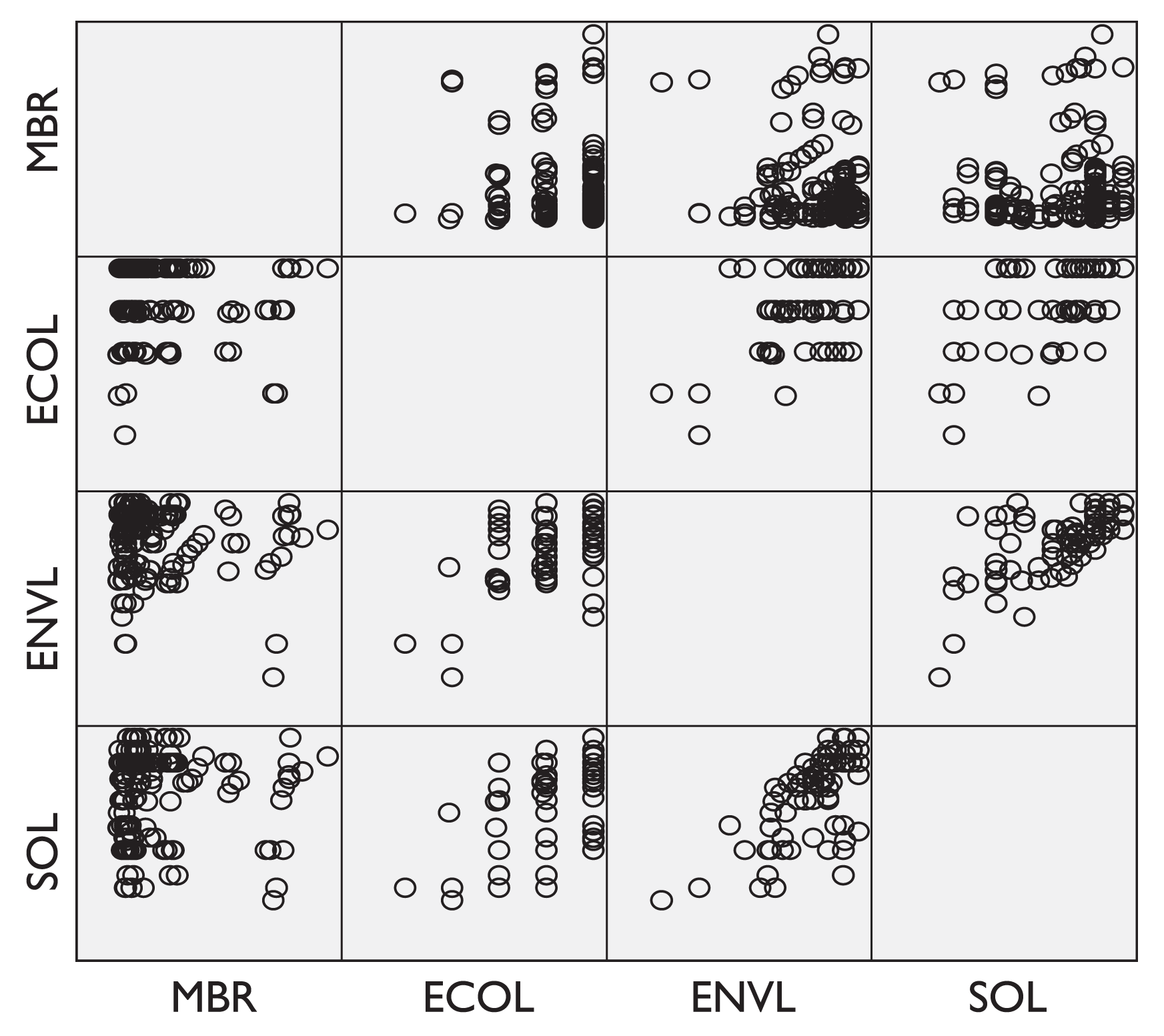

Matrix scatter plots (Figure 6 for Japan and Figure 7 for India) show the extent of linearity in relationship between pair of variables without adjusting for the confounders. In case of Japan, the linear association of MBR with all the three economic, environmental and social variables is obvious except for one and only one outlying firm. All these relationships have remained obscured and not interpretable for India due to a similar reason as described earlier. However, the strength of bivariate relationship between MBR and SOL dominates the overall association.

The outcomes of the random-effect regression models (Model 1a) are shown in Table 1. The impact of CSPL on MBR is found to be positive and statistically significant after adjusting the effects of DER and SIZE for Japan and India. The outcomes reveal that the sustainability performance-related disclosures play an important role in enhancing the MV of the firm. Among the two control variables, DER is found to be negative and significant in the case of Indian firms only. This indicates that Indian firms are generally more inclined towards the use of internal funds rather than the debt capital, which is consistent with the packing order theory of capital structure. The outcomes of random-effect model are consistent with the results of logit model (shown in Table 2). In Table 2, the results of Model 1b clearly show that the effect of CSPL is positive and statistically significant ( p = 0.013 and p = 0.000 for India and Japan, respectively) after adjusting for the effects of DER and firm size (SIZE). The results indicate that with one unit increase in CSPL, it is expected to see about 18 per cent and 5 per cent increase in the odds of being in the class of performing firms for Japan and India, respectively. Hence, the alternate hypothesis H1 is accepted for both the countries. Moreover, the outcomes of the logit model (Model 1b) not only indicate the positive impact of CSPL on MBR but also show the extent of the impact of CSPL on MBR. Pseudo-R2, which exhibits an approximate strength of the model, is not very pronounced for either of the two countries.

Random-effect Regression Results of CSPL and MBR

Japan: [Breusch–Pagan test–Chi-square (1) = 235.747 (000), Hausman test–Chi-square (3) = 2.106 (0.550)].

India: [Breusch–Pagan test–Chi-square (1) 362.091 (000), Hausman test–Chi-square (3) = 1.638 (0.650)].

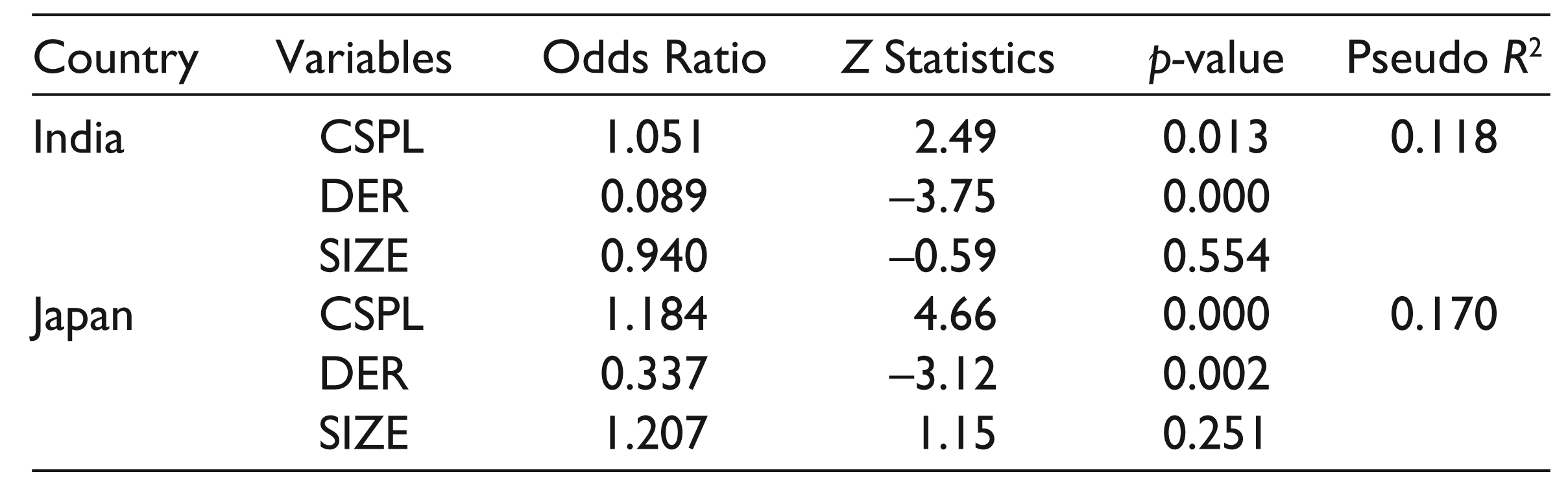

The influence of the components of CS (economic, environmental and social) on the response variable (MBR) is estimated using the logit model (Model 2), as it is assumed to be more appropriate than the panel data model in the present context. The outcomes of Model 2 are shown in Table 3. Model 2 finds the effect of levels of social/environmental performance statistically significant while adjusting for environmental/social performance and economic indicators along with the other two predictors used earlier. While the effect of social performance is significant ( p = 0.000) in India, the effects of social ( p = 0.04) as well as environmental performance ( p = 0.00) are significant for Japan. It is worth noting that for Japan, with one unit increase in the level of environmental performance we expect to see about 67 per cent increase in the odds of being in the class of performing firms, and for social performance, it is about 15 per cent. Whereas, in case of Indian firms, the extent of impact of social performance on the MV of the firm is 8 per cent only. Therefore, our results support the alternate hypotheses H3 and H4 in case of Japan and only H4 in case of India. Of the two control variables, the influence of leverage (DER) is found to be significant for all the cases. However, the effect of firm size on financial performance is found to be insignificant for both Japan and India.

Logit Regression Results of CSPL and MBR

In case of Model 2, pseudo-R2 value has substantially improved for Japan (but not for India) establishing the link between social and environmental links with firm performance. However, in Indian context only a handful of firms publish sustainability report. The findings of the study in case of Japan support the results of Carvalho and Siqueira (2007), Thom and Decoutere (2009) and Lungu et al. (2011), where the researchers have found environmental parameters as the most dominating among the components of sustainability. In contrary, the observed significant influence of the social aspects of CS on financial performance in India demonstrates the findings of Tsang (1998), Murthy (2008) and Bhatia and Chander (2014) in the context of developing nations.

Logit Regression Results of the Components of CSPL and MBR

Relative Impact of CSP on Firm Performance in Japan and India

The regression results of Model 1 depict positive and significant influence of CSPL on MBR in case of both the countries. In order to examine whether the positive influence of CSPL on MBR is significantly different between the two countries, the regression Model 3 is employed for the combined data set. The results in Table 4 show that the odds ratio of CSPL for the combined data set is positive and significant at 1 per cent level. Further, the odd ratio of the dummy variable is positive and significant at 1 per cent level, which clearly demonstrates that there is a significant difference between the two countries. The result indicates that the influence of CSPL on MBR in Japan is significantly higher than that of India. The results are, thus, sufficient to accept the alternative hypothesis H5.

Relative Impact of CSP on MBR

Practical Implications

The outcomes of the study are useful for many policy implications. The findings of the study indicate that non-economic disclosure plays a significant role in influencing the firm performance in case of both the countries. In case of Japanese firms, environmental and social indicators are found to be the most crucial for enhancing the MV of firms. However, in Indian context, only the social factor is the most influential factor in enhancing firm performance. Thus, the findings revealed that CSP helps to engender the stakeholders’ trust in companies. Companies could make use of these findings as a tool to legitimize their actions in the society and attract ethical investors. The findings of the study also indicate that traditional financial reporting cannot help in assessing the value of the firm. Hence, stakeholders should consider CS report as a tool to value the firm, which ultimately boosts the importance of overall sustainable development. Presently, the corporate managers are facing challenges to develop effective sustainability related strategy. This study can be helpful for firms to understand the importance of CSP that can lead to a sustainable competitive advantage. Effective integration of sustainable activities into the management strategy helps a firm to improve its overall performance.

The study provides an empirical support that CS reporting can help in improving the MV of the firm, which indicates that a firm can improve its performances through efficient utilization of resources. This is consistent with the resource-based view of the firm, which states that the performance of a firm depends upon the efficient utilization of both tangible and intangible resources. However, in the knowledge-based economy, many researchers have advocated that intangible resources are creating the significant gap between BV and MV of firms (Clarke, Seng & Whiting, 2011; Lev, 2001; Stewart, 1997). Since most of the indicators of CS are non-financial in nature, the outcomes of the study clearly demonstrate the relevance of disclosing non-financial information or intangible resources in enhancing the MV as well as competitive advantage. The findings of the study also supports the notion of WCED (1987) that every firm must make an effort to meet the needs of the present generation while maintaining the resources not only for the present but also preserving such resources for the future generations. Thus, the findings of the study may stimulate the corporate managers to make an effort for efficient utilization of resources, which will not only help in improving the firm performances at present but also can help in continuing such performances in future as well. Moreover, the significant positive association between CS reporting and firm performance also reveals that CS reporting plays an important role in enhancing transparency by legitimizing firm’s activities in the society. Therefore, the study further suggests the corporate managers to reorient their strategies towards CS, which will help them in fulfilling the increasing demand of the ‘voice of society’ (Warhurst, 2000).

Concluding Remarks

The present study is a modest attempt to explore the sustainability disclosure practices and its association with financial performance of two Asian countries–Japan and India. We find that level of disclosure (overall as well as component-wise) is marginally higher for Japanese firms as compared to Indian firms. However, a steady growth in component-wise disclosure of CSP for both the nations is revealed. By employing bivariate scatter plots, our results depict that a slow but steady increase in the slope of the linear relationship between overall sustainability performance and financial performance is apparent in case of Japan, but such an impression is not very obvious in case of India. Similar results are found for the relationship between the components of sustainability performance on financial performance. While in case of Japan, the linear association of MBR with all the three economic, environmental and social variables is obvious, all these relationships have remained obscured and not interpretable for India.

The results of the random-effect model and the logit regression model also demonstrate the same. In case of the logit model, the results show that with one unit increase in CSPL, we expect to see about 18 per cent and 5 per cent increase in the odds of being in the class of performing firms for Japan and India, respectively. The results, thus, support the hypothesis H1 for both the nations. However, regarding the influence of the components of CSP on financial performance some contradictory results are found. While ENVL and SOL positively and significantly influence financial performance in the case of Japan, such significant association is found to be significant only in case of SOL in India. Thus, our results support hypotheses H3 and H4 in case of Japan and only H4 in case of India. The plausible reason for insignificant impact of economic indicators on financial performance for both the nations may be that all the firms mandatorily disclose the economic indicators in the published annual reports over the years. Hence, further disclosure of the same information in the sustainability report may not add much value to the firm. Additionally, the regression results also reveal that the positive influence of CSP on Japanese firms is significantly higher than that of Indian firms.

The present study is based on GRI reporting framework. Despite having global acceptability of this framework, it is not free from limitations. It is a general framework used equally by both developed and developing countries in respect of different industries and different needs. For instance, the information needs of the stakeholders from developed and developing countries are primarily different. Additionally, the activity levels of different industries are different from one another, as activities in service industries are different from manufacturing industries. Being a common framework, it is very difficult to consider all these differences. Thus, the combination of other frameworks like UNGC, Carbon Disclosure Project, etc., along with GRI may be very effective in assessing the sustainability related activities of the firm. Additionally, the present study is limited to only two countries from Asia. Thus, the outcome of the study cannot be generalized. Considering this limitation, future work can be done by considering some other developed and developing countries from Asia.