Abstract

The present research article is an attempt to add something new and revalidate the influence of already existing corporate governance dimensions related to the board of directors on listing-day performance of the Indian initial public offering (IPO) firms measured through underpricing. Like other emerging market economies, firms in the Indian economy are also characterized by concentrated ownership held by an owner or a promoter in the context of the Indian corporate environment. In the backdrop of this concentrated complex ownership structure, the present study analyses the influence of the board of directors on underpricing when the appointment of such directors is largely an affair handled by such owners, whom they are given the task to monitor. The sample consists of 471 IPO firms which went public during the time period from January 2003 to December 2017. Results obtained from the regression analysis show that the board size and board committees act as information signals for Indian IPO firms having a significant and negative relation with listing-day initial excess returns. Other board-related dimensions of governance do not have significant influence on underpricing. Overall board variables have a very miniscule contribution in explaining the underpricing in Indian IPO firms.

Introduction

An initial public offering (IPO) is probably one of the most important decisions taken in the life cycle of a firm (Pagano, Panetta, & Zingales, 1998), representing its transition from formerly a privately owned company to becoming a public one (Certo, 2003) with a highly dispersed ownership. An IPO indicates an opportunity for initial investors or founders of a firm to sell their shares held to the public at large in the market (He & Wan, 2013). Dilution of the owner’s holding results in agency conflicts between those who manage the firm and outside shareholders (Jain & Kini, 1994). For these agency conflicts taking place with separation of ownership and control, Young, Peng, Ahlstrom, Bruton, and Jiang (2008) have differentiated the case of the emerging economies which are characterized by principal–principal conflicts from the developed economies which are characterized by principal–agent conflicts. Lin and Chuang (2011) in their study on the emerging market economy of Taiwan presented a view that principal–principal conflicts occur when there is a risk of expropriation of minority shareholders’ interests by the controlling shareholders.

La Porta, Lopez-De-Silanese, and Shleifer (1999) in their comprehensive study found the concentrated ownership in the hands of the founder family a common sight in many developed as well as developing economies, giving the controlling shareholders of such firms a significant say in the management of the firm. Claessens, Djankov, and Lang (2000) in their study on nine East Asian countries found high family ownership concentration and subsequently controlling shareholders or other persons related to him in the management of the firm. The Indian economy, similar to a majority of East Asian countries’ economies and some of the developed economies like France (Roosenboom & Schramade, 2006), is one such economy having highly concentrated and promoter-controlled ownership structure. For such concentrated ownership structures, Shleifer and Vishny (1997) contend that there exists a risk of expropriation by the large investor or the controlling shareholder who can redistribute the wealth in his own favour, which may or may not be aligned with the interests of minority shareholders. Drawing support from these arguments, there exists a situation of uncertainty for potential outside investors with regard to the return on investment to be made by them. This uncertainty, arising out of an information asymmetry among an IPO firm, its underwriters and outside investors, results in the underpricing of the issue with more established firms evidencing lesser uncertainty among investors regarding its actual intrinsic value and thereby resulting in lower underpricing (Ibbotson, Sindelar, & Ritter, 1988). Among theories that try to answer the question of why IPO firms put a lower price tag on their issue, one widely referred theory by Rock (1986) contends that two categories of investors exist, informed and uninformed; to keep uninformed investors too with the firm and ensure their participation in the issue, it is priced at a discount. Another probable reason of underpricing is given by Allen and Faulhaber (1989) and Welch (1989) which suggests that IPO firms use underpricing as a signal showing their good quality as only high-performing firms can bear excess initial costs and will recoup this expense by seasoned offerings marked at a higher price.

Many previous studies have validated and revalidated the existence of the inherent anomaly of underpricing across different economies of different countries, though with variation in its quantum (Loughran, Ritter, & Rydqvist, 1994). Underpricing which is considered as a performance indicator of an IPO affects the interests of initial investors or owners of firms as it results in lesser funds generated for the firm (Daily, Certo, & Dalton, 2005). The phenomenon of underpricing occurs when the issue is offered at a discount, that is, a price lower than its intrinsic value due to the uncertainties associated with agency problems (Chahine & Filatotchev, 2008). Although probably due to aforementioned reasons the offer is made at a discounted price, yet in a perfect market setting or in an efficient market, the price of stock reaches its intrinsic value (Nafid, 2014; Walker, 2008), resulting in underpricing or overpricing of the issue. When it is underpricing, it is an indirect cost (Chahine, 2004) to be borne by the firm which is associated with the process of going public, representing direct transfer of wealth from original shareholders to new investors (Chahine & Filatotchev, 2008). Underpricing is also referred to as ‘money left on the table’ resulting in lesser amount accumulated by the process of IPO to be employed in activities of the firm (Howton, Howton, & Olson, 2001). Previous studies have established a positive relation among information asymmetry, ex ante uncertainty and resulting underpricing—with more the information gap prevailing between the IPO firm and external investors, more the difficulty in firm valuation and more the underpricing (Beatty & Ritter, 1986; Lowry, Officer, & Schwert, 2010). Information asymmetry is the result of the fact that firms going public are relatively lesser known to investors as these firms lack publicly available history of their operations and trading records (Zimmerman, 2008). Certo (2003) contends that these firms suffer from ‘liability of market newness’. Like many previous studies drawing support from the signalling theory (Spence, 1974), firms need to send signals of their good quality to external investors to show that the firm is worth their investment (Xu, Wang, & Long, 2017). Some of the information signals under the wide umbrella of corporate governance studied for their impact on underpricing by inhibiting information asymmetry include auditor reputation (Beatty, 1989), underwriter reputation (Carter & Manaster, 1990), venture capitalist association (Megginson & Weiss, 1991), anchor investors’ participation (Sahoo, 2017), IPO grading (Chhabra, Kiran, & Sah, 2017) and so on.

The aim of this empirical study is to add to this existing literature an important dimension of corporate governance, that is, the structure of the board of directors for IPO firms of India. Whenever corporate scandals occur in any economy of the world, the trust of investors present globally gets a jolt. Satyam computer service scam was one such scam which took place in the Indian market economy that robbed domestic as well as foreign investors (Singh, 2011) to the tune of 70,000 million (Kota, 2018). Other global scams include Enron and WorldCom in the USA, HIH in Australia and so on. In the backdrop of these scams, corporate governance of a firm assumes much more importance. La Porta, Lopez-de-Silanes, Shleifer, and Vishny (2000) define corporate governance as a set of mechanisms put in place by the firm to protect interests of external minority shareholders from the risk of expropriation by controlling shareholders who are apparently insiders. The board of directors of a firm constitutes an internal corporate governance mechanism (Chahine, 2004), entrusted with the task of monitoring the top management of the firm (Peasnell, Pope, & Young, 2005). Hillman and Dalziel (2003) study the role of the board under both the agency theory in which the board provides monitoring on behalf of shareholders and the resource dependence theory in which the board provides resources external to the firm. Previous literature has studied some of the aspects of the structure of the board which include board size, busyness of members, that is, their interlocking and their independence for its impact on the performance of firms. But since going public necessitates a firm to fulfil new investors’ expectations while simultaneously complying with legal and regulatory guidelines according to the legislature of a country (Thorsell & Isaksson, 2014), this study captures the relationship among various dimensions of the board structure and underpricing, that is, how much value potential investors attach to corporate governance mechanisms adopted by IPO firms. Studying this relationship assumes more importance for firms going public as contended by Gouldey (2006) that in an entrepreneurial setting surrounded by uncertainty, investors tend to evaluate the same piece of information differently.

Review of Literature and Variables’ Development

Independent Variables

La Porta et al. (2000) put forward the view that in economies with good investor protection, insiders expropriate minority shareholders’ interests by overpaying themselves, by putting their relatives in the management of the firm or by undertaking some wasteful projects. The Indian economy is in its developing stage since the introduction of reforms of 1991 that led to globalization of the economy. Since then, the Indian market has received enormous investments from around the world in addition to domestic investment. Attempts have been made by the Indian legislature to protect investors’ interests from time to time, starting from the inception of the capital market regulator SEBI in 1992 to making various committees recommend norms for disciplining the market, the latest development being the introduction of the new Companies Act 2013 and SEBI’s panel on corporate governance led by the banker Uday Kotak recommending steps for a stronger governance mechanism. The protection of interests of minority outside shareholders in the promoter group held complex and concentrated ownership in the Indian corporate structure which creates agency problems unique to such ownership structures and makes monitoring of such firms a challenging task (Jackling & Johl, 2009). In such an environment of concentrated ownership in few hands, the role of the board of directors assumes greater importance for protecting minority investors’ interests.

Board Size

Size of the board which represents the number of directors employed on the board of the firm has been one of the most important dimensions of corporate governance studied for its impact on firm performance, as well as for its role in inhibiting information asymmetry in an environment of uncertainty for a firm going public. Large size of the board can have two implications, either it can enhance monitoring efficiency or it can make decision-making rigid and slow, which necessitates striking a trade-off between these two extreme implications (Harford, Mansi, & Maxwell, 2008; Mishra & Kapil, 2017). Prior research has given ambiguous results for the impact of size of the board (Xu et al., 2017). Yermack (1996) in his study on US firms found that a smaller size of boards had a positive impact on overall performance of the firm. Similar findings were reported in a study on the UK firms by Guest (2009) which established a negative relation between the board size and the firm performance citing poor communication and decision-making in larger boards as the reason. Validating the result for the developing Indian economy too, Sriram (2018) found that the smaller size of the board is better for improved performance of firms. Past studies have also found support in favour of larger boards. Jackling and Johl (2009) in their study on Indian firms found evidence in support of larger board size impacting the performance positively suggesting under-resource dependence theory, the more the board members, the more the resources and the better the performance. Another study by Johl, Kaur, and Cooper (2015) is in favour of large board size for Malaysian firms. In the context of IPO firms where primary considerations are signalling of information and then its evaluation by potential investors, Certo, Daily, and Dalton (2001) found a negative relation between size of the board and underpricing, suggesting that investors see large board size as a means of acquiring more resources. In their study on the emerging economy of Indonesia, Darmadi and Gunawan (2013) also found a negative relation between the two, contending that a larger board enhances the monitoring ability resulting in lower information asymmetry. In contrast, Hearn (2011) in his study in sub-Saharan Africa found a positive impact of the size of the board on underpricing, indicating the communication gap due to the larger board and resulting increased information asymmetry; results obtained similar to results of Bathula (2008) in New Zealand and Mnif (2009) in France. Also, an insignificant relation was reported by Howton et al. (2001) and Xu et al. (2017). These mixed results across various economies call for studying this governance mechanism of Indian IPO firms which are largely dominated by promoter ownership and their subsequent control over appointments of directors.

Board Independence

Fama (1980) termed ‘board of directors’ as ‘internal monitors’ whose job is to scrutinize the work of highest decision-makers within an organization. Weisbach (1988) in his empirical study found the evidence that outside board members played an important role in ameliorating firm performance by removing weak managers, in comparison to inside directors. A recent study in New Zealand by Li and Roberts (2018) present an opposite result demonstrating a negative influence of outside board members on performance of a firm, a view common with a past study by Baysinger and Butler (1985). Regarding the role of independent directors in curbing information asymmetry, Howton et al. (2001) and Darmadi and Gunawan (2013) found a positive relation between independent directors’ dominated boards and their proportion, respectively, and the IPO underpricing. A positive relation shows failure to inhibit information asymmetry on the one hand and high valuation in the market by investors on the other. Mnif (2009) in a study on concentrated ownership structure in France (Roosenboom & Schramade, 2006) and Lin and Chuang (2011) in their study in the emerging economy of Taiwan found that the proportion of independent directors on the board negatively impacted underpricing and thus controlled the principal–principal conflicts common in emerging economies. Laws and regulations related to corporate governance of various countries recommend employing a combination of both inside and outside directors on the board (Jackling & Johl, 2009). The aim of incorporating this variable is to capture the perception of investors towards the independence of outside directors of Indian IPO firms where their appointments are made by inside owners whom they are supposed to monitor to protect minority shareholders’ interests (Hora, 2017).

Board Committees

Another dimension of the board of directors given under the ‘management’ section of Indian IPO firms, along with directors’ information, is various committees of the board. These committees arrange their meetings separately from the full board, comprise subsets of directors in the board and clearly carve out functions to perform (Klein, 1998). The Indian listed firms are required to make these committees such as audit committee, nomination and remuneration committee and stakeholders’ relationship committee as per the provisions of Companies Act, latest being the act of 2013, and SEBI’s Listing Obligations and Disclosure Requirements. Companies going public can frame more such committees to indicate their stronger governance mechanisms, as evidence given by Handa (2014) shows that more committees result in better monitoring and lesser information asymmetry and underpricing. In his study of the sub-Saharan African region of West Africa, Hearn (2011) found a positive relation between the board committees and the IPO underpricing, indicating their failure to curb information asymmetry and the lack of trust in investors regarding independent working of such committees in weak governance environment. Very few such studies exist measuring the impact of various committees of the board on underpricing. The aim here is to fill this gap and see whether such committees are able to meet the investor’s expectations of stronger governance.

Female Directors’ Proportion

Companies Act, 2013, of the Indian legislature though it modified many existing governance mechanisms also added a whole new dimension of having at least one female director on the boards of listed firms; otherwise, that has largely been a male bastion. Many studies conducted in different countries have pointed towards their low presence on corporate boards. Kang, Cheng, and Gray (2007) demonstrated a low number of female directors on the Australian corporate boards for top 100 companies where a majority of them had only one woman director, showing their low percentage. Bathula (2008) in a study in New Zealand found a positive influence of female directors on performance of the firm, while putting forward the fact that 70 per cent of firms did not have any female director on their boards. Another study conducted by Banerji, Mahtani, Sealy, and Vinnicombe (2010) demonstrated low numbers of board positions held by women in different countries: in Canada it stood at 15 per cent; in the USA, women occupied 14.5 per cent board positions and 8.3 per cent in Australia. For the Indian BSE-listed, the leading 100 companies of BSE100 figure stood abysmally low at 5.4 per cent. Moreno-Gómez and Calleja-Blanco (2018) found a positive relation between women directors and the performance of firms in Colombia. Regarding the consequences of introducing quotas for women directors, Adams and Ferreira (2009) presented different results for US firms with weak and strong governance mechanisms. Weak governance firms having female directors improved performance due to their better monitoring abilities, but for strong governance firms it resulted in negative influence on firm performance because of over-monitoring by female directors. Very few studies have captured the perception of investors towards female board members in IPO firms. One such study by Reutzel and Belsito (2015) in the US IPO firms found reduced biasness of investors towards female presence on the board as a result of the introduction of corporate governance reforms. The aim of incorporating this variable is to check how much value investors attach to diversified Indian boards and how does the presence of female directors help IPO firms in curbing information asymmetry.

Directors’ Interlocking

Interlocking represents a number of board positions held by directors in other firms. It acts as a proxy for their reputation in the corporate world. Having such reputed board members result in prestige for directors and legitimacy to the employing firm (Certo et al., 2001). Hillman and Dalziel (2003) also lend support to the argument and discuss the role of the board under resource dependence theory where the board provides advice and counsel and links with the external environment to the firm. But presenting an opposite impact, Hamdan (2018) in a study in Saudi Arabia found that employing directors with several interlocks resulted in a negative impact on performance of firms. Other studies supporting this busyness hypothesis include Santos, Da Silveira, and Barros (2012) in Brazil and Fich and Shivdasani (2006). Although previous studies have examined the impact of interlocking on performance of firms, very few studies have captured the relation between directors’ interlocking and underpricing. Certo et al. (2001), Arthurs, Hoskisson, Busenitz, and Johnson (2008) and Thorsell and Isaksson (2014) are some of the researchers whose studies that have established a negative relation between interlocking of directors and underpricing, showing that interlocking acts as an information signal considered by investors.

Dependent Variable

Since the aim of the present study is to measure the influence of various dimensions of the board of directors of IPO firms on underpricing, it is taken as a dependent variable which is considered after making adjustments for movements of the market between the issue close date and listing of IPO date (Chen & Yang, 2013). The resulting adjusted underpricing so obtained is referred to as the market-adjusted excess return. To adjust initial returns for market movements, BSE Sensitive Index has been used. Myriad studies conducted in the past on Indian IPO firms have used Sensex to adjust for market movements. BSE Sensex as mentioned on BSE’s official website is based on free-float capitalization methodology on par with other major index providers such as Dow Jones and Financial Times Stock Exchange (FTSE) and so on. With a long history and broader acceptance, this benchmark index is unmatched in reflecting market movements and sentiments.

The formula employed to calculate MAER is the following:

Adj. Underpricing = [(P1-P0)/P0 – (M1-M0)/M0]*100 P0: Offer price P1: Closing price on the first day of listing M0: Closing value of the BSE Sensitive Index on the issue closing date M1: Closing value of the BSE Sensitive Index on the issue listing day

Control Variables

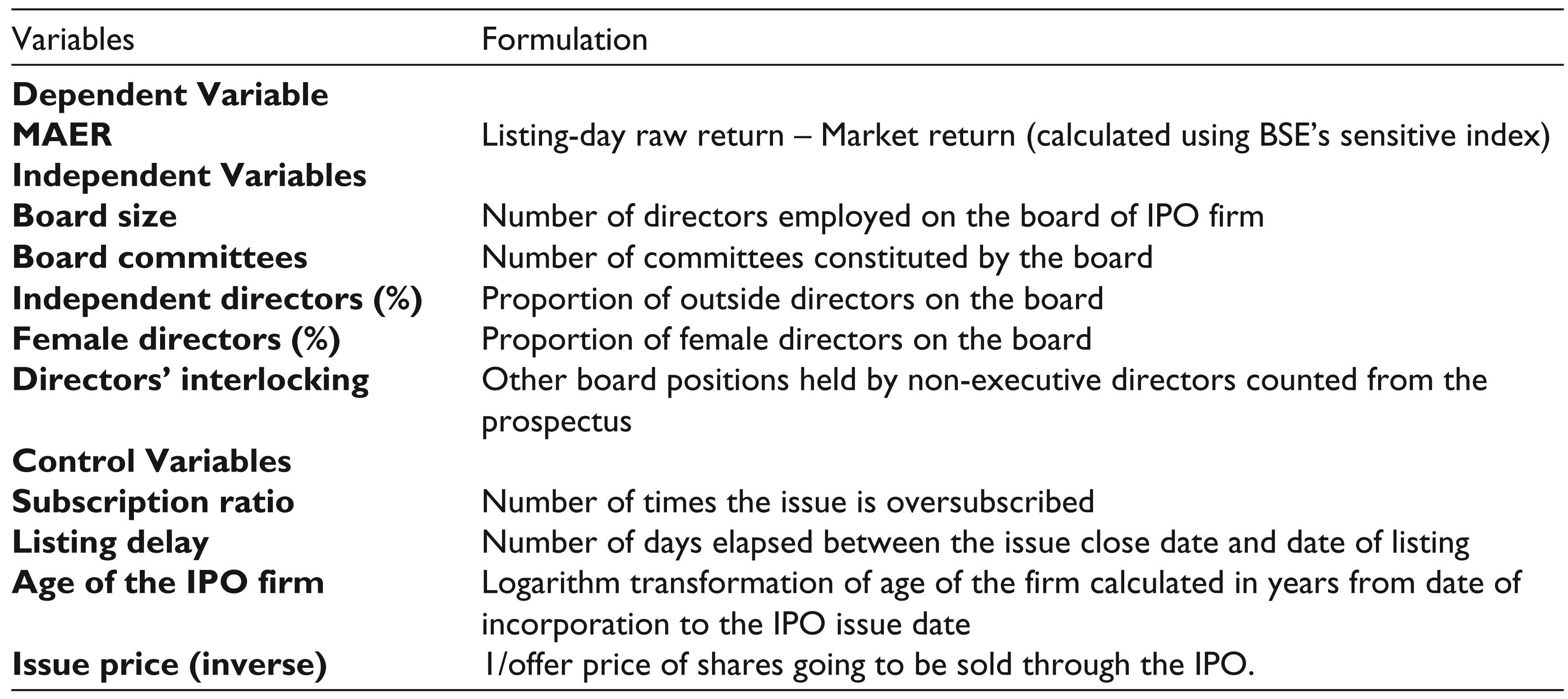

Since previous literature shows this internal control mechanism of governance, that is, that the board of directors are not the only variables influencing underpricing, some other IPO-related and firm-related control variables have also been included in the study for their possible influence on underpricing. The first IPO-related control variable added is the subscription ratio which represents response of investors to the issue offered through the IPO in terms of the number of times the issue is oversubscribed (Chahine & Tohme, 2009). Previous studies have established a highly significant positive relation between the subscription ratio and underpricing (Agarwal, Liu, & Rhee, 2008; Vong, 2006). Another IPO-related variable included is the listing delay as Baluja and Singh (2016) established a link between listing delay and survival of IPO firms, giving the argument that with greater time gap in listing, investors get more time to gather critical information about the firm, which subsequently reflects in the IPO’s performance. Fama (1980) contends that investors invest at a particular offer price when it reflects its inherent risk and will get rewarded for undertaking this risk by realizing investment in the capital market after its listing. Guenther and Willenborg (1999) and Bédard, Coulombe, and Courteau (2008) are some of the researchers whose studies controlled the influence of the issue price by taking its inverse transformation. Among firm-related controls, many studies related to IPOs have also controlled the influence of age of the firm at the time of going public (Reutzel & Belsito, 2015; Xu et al., 2017), for its probable influence on underpricing as mature firms are relatively less impacted by the liability of market newness (Singh, Tucker, & House, 1986). Table 1 presents the composition of variables included in the study. The final regression model employed is as follows:

Formulation of Variables Under Study

Sources of Data and Research Methodology

Data for the present empirical investigation include 471 IPO firms which went public from 1 January 2003 to 31 December 2017 and got listed on the Bombay Stock Exchange. IPOs of 2003 and beyond have been considered because this was the time when SEBI’s Committee on Corporate Governance under the Chairmanship of Shri Kumar Mangalam Birla submitted its recommendations based on which amendments were made in listing agreement, and the new Clause 49 was added and was wholly implemented post-2002. Board-related data were collected from the ‘management’ section of prospectuses of IPO firms, which were procured from the official website of SEBI. 1 Unavailability of final prospectuses for some firms resulted in reduction of sample size. Listing-day close prices for respective stocks and Sensex values were obtained from the official website of BSE. 2 Delisted firms during the sample period have not been included in the study. Further, incomplete information in prospectuses of some firms resulted in reduced firms in the final regression model. Hierarchical ordinary least square regression tool has been used to analyse the influence of internal corporate governance mechanisms of the board of directors on adjusted underpricing.

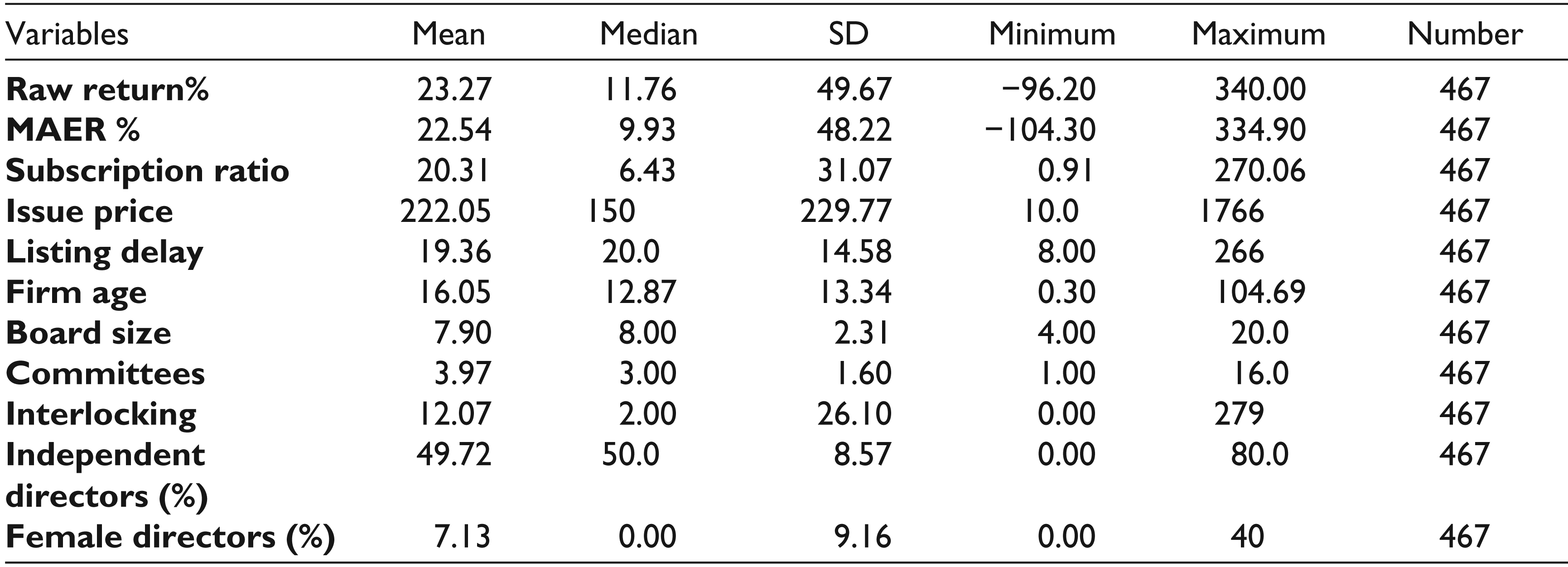

Descriptive Statistics

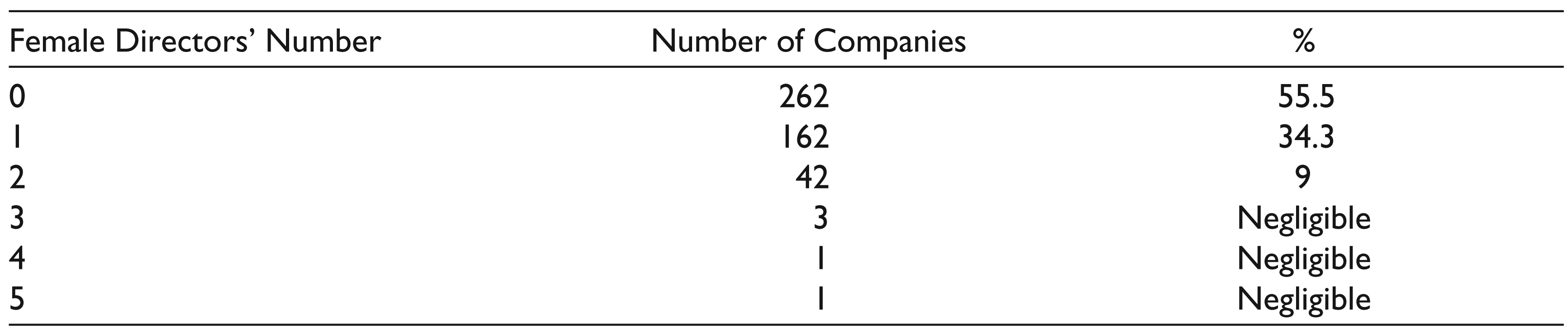

Descriptive statistics of the variables incorporated in the study are given in Table 2. The mean value of approximately 23 for the initial excess return during the sample period for Indian IPO firms is an evidence of the presence of anomaly of underpricing, that is, money forgone needlessly by firms going public (Arthurs, Busenitz, Hoskisson, & Johnson, 2009), although large variations in the spectrum beginning with a negative value of 96 show the existence of overpricing in some issues too. Variations in the subscription ratio indicate the existence of informed demand made by investors with better issues attracting more demands from investors. Like many previous studies, to standardize large variations in ages of firms going public as can be seen from descriptive statistics, the logarithm transformation of this variable has been taken. The IPO is an event for a firm where the board of a firm is subjected to scrutiny by the public for the first time (Certo et al., 2001). With regard to the proportion of independent board members, mean value of approximately 50 and maximum value of 80 show the majority of firms abiding by this dimension of corporate governance very well. Another important observation for the Indian IPO firms is the abysmally low proportion of female directors on boards of such firms as shown in Table 3.

Descriptive Statistics

Female Directors on the Indian IPO Firms

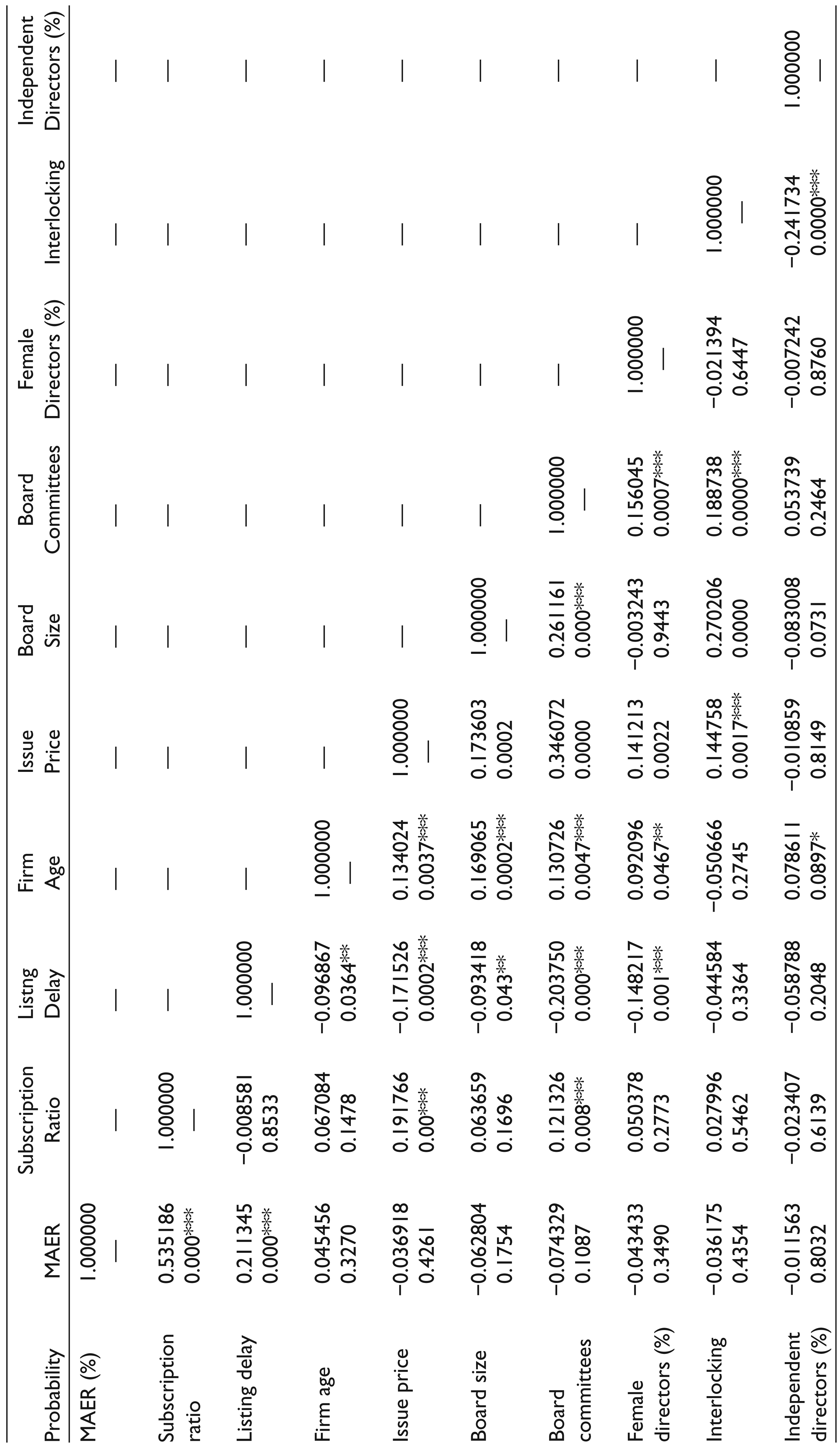

Correlation among variables has been given in Table 4. Results of the correlation matrix show that listing delay, subscription ratio and age of the firm while going public have a positive relation with the market-adjusted excess return. Rest all, the control and independent variables incorporated in study, have a negative influence on underpricing.

Correlation Matrix

Results and Discussion

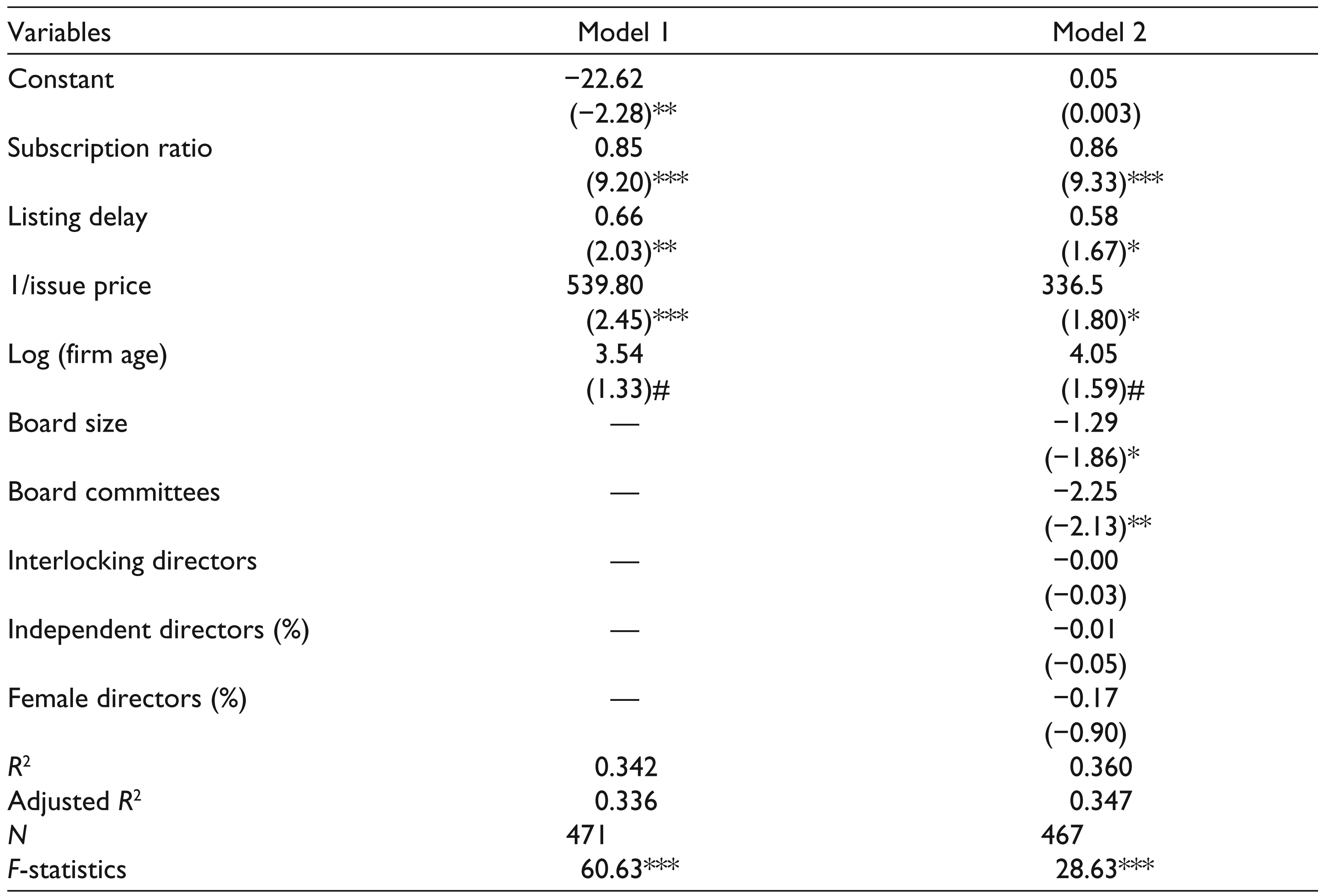

Results of the cross-sectional regression analysis are run to measure the influence of various board-related corporate governance mechanisms on adjusted underpricing that are given in Table 5. Both the regression models have been tested for existence of problems of multicollinearity and heteroskedasticity. Existence of multicollinearity among variables was checked by computing variance inflation factor. As all the values computed were less than the acceptable limit of 10, no problem of multicollinearity existed among variables. The problem of heteroskedasticity was found to exist, and to solve it White’s test of consistent standard errors was used. Results of IPO-related and firm-related control variables for their impact on underpricing are presented in Model 1. Model 2 reports the influence of board-related independent variables in addition to control variables on adjusted underpricing. Taking a glance at both the models makes this thing very much evident that board-related governance variables do not constitute a very major part of the investor’s consideration for taking investment decisions in Indian IPO firms as the fact can be gauged from the very negligible increase in the adjusted R2 of Model 2 in comparison to the previous model.

Regression Analysis

# symbol represents loose significance at 20% level.

The subscription ratio significantly and positively influences underpricing in both models. This highly significant relation is in line with findings of Chahine and Tohmé (2009), Singh and Kumar (2012) and Vong (2006) who suggested that oversubscribed issues indicate the good quality of the firm going public. Investors, who do not get subscription of such a high-quality firm, go for the secondary market believing that sooner they get the subscription, the more beneficial it will be. This excess demand on the listing day pushes the close price up and hence the excess initial return. For both models, listing delay has a positive significant influence on the adjusted underpricing, common with findings of Chen and Yang (2013), Chahine and Tohmé (2009) and Shah (1995), which explain underpricing as compensation or reward for taking risk of investing in a new firm and parting with their invested money. Similar to findings reported by Su and Fleisher (1999), the issue price negatively influences underpricing in both models, with this relation more pronounced in the first model. It shows that a higher issue price attenuates the prevailing information asymmetry and as put by Krishnamurti, Thong, & Vishwanath (2009), resulting in the higher issue price and subsequently lower underpricing. Age of the firm at the time of going public with loose statistical significance has a positive relation with underpricing similar to findings of Mitchell Van der Zahn, Singh, and Singh (2008) in Singapore and Hearn (2012) in sub-Saharan Africa. This shows that older the firm more the positive value associated with the market reflected in excess initial returns.

With regard to board-related independent governance variables given in Model 2, only size of the board and committees constituted by the members of the board have significant influence on the investment decision of potential investors. Similar to the results obtained by Certo et al. (2001) for developed economies and Darmadi and Gunawan (2013) for the emerging market economy of Indonesia, the board size has an inverse relation with underpricing, which shows that larger the size of the board, lesser will be underpricing. This ability of a larger board in curbing the information asymmetry surrounding the IPO firm is the result of better monitoring expected from the larger board (Boone, Field, Karpoff, & Raheja, 2007) and more resources to be provided by a greater number of directors on the board, a role often discussed under resource dependence theory (Jackling & Johl, 2009). This result obtained also lends its support to recent recommendations of a panel by SEBI on corporate governance to increase the minimum number of directors to six from current requirement of three, given in Companies Act 2013 (Upadhyay & Laskar, 2017). Since the listing-day close price reflects private information of those small and retail investors who do not obtain any allocation of shares prior to listing (Walker, 2008), another justification for inverse relation of board size can be due to the reason that such investors do not highly value IPO firms with large sizes of boards and thus low demand and lesser initial returns. Committees constituted by board members share a significant and negative relation with adjusted underpricing in contrast to the result of Hearn (2011) obtained for West African IPO firms. An inverse relation between the number of board committees (both required by law and voluntarily made committees) and under- pricing shows the importance of constituting such committees in addition to minimum and mandatory required by law, in containing the information asymmetry and subsequent underpricing. The number of committees act as an information signal for efficient monitoring mechanism put in its place.

Rest all, other board-related governance variables, have an insignificant relation with adjusted underpricing. Similar to the inverse relation established by Arthurs et al. (2008) and Thorsell and Isaksson (2014), in the present study also the negative relation is evidenced between the director interlocking and adjusted underpricing, although this relation lacks statistical significance for Indian IPO firms. Another negative but insignificant relation is witnessed between proportion of independent directors on board and adjusted underpricing, consistent with direction of relation established by Lin and Chuang (2011) for the emerging Taiwanese economy. Lack of statistical significance shows that though board independence reduces the quantum of dependent variable, that is, underpricing, these fail to act as an important information signal for investors of Indian firms. This can be due to the complex concentrated ownership structure of firms in the Indian corporate environment. Kota (2018) explains the difference of ownership patterns of developed economies like the USA and emerging economies represented by India with a classic example of corporate giants like Apple where 60 per cent ownership is held by various institutional investors and rest by top leadership of the company including its CEO, Tim Cook. The case for India on the other hand is the opposite where in Wipro, 76 per cent of ownership is held by the promoter and promoter group. In such family-controlled firms, where appointment of independent directors and quantum of information provided to them depend on will of promoters (Hora, 2017), their independence becomes dubious. Reports on governance often point towards lesser independence of independent directors and them being more of friends and acquaintances of the promoter group, making their presence redundant.

Women directors on boards of Indian firms also have an insignificant but a negative impact on quantum of underpricing. Table 3 presenting the number of female directors on IPO firms’ boards shows their very low presence and biased attitude prevailing against them in Indian corporations. A majority of IPO firms have no female directors on their boards. Their continuous presence and increasing numbers can be seen only after the introduction of Companies Act, 2013, which mandated the presence of at least one woman director for listed firms.

Conclusion

The present empirical analysis sheds light on the board of directors’ related corporate governance mechanisms adopted by IPO firms and their influence on underpricing. Results achieved through regression analysis show that governance mechanisms do not form a significant part of investors’ consideration as can be gauged from a very less increase in the adjusted R2 from Model 1 to Model 2. Among board variables, board size and board committees act as information signals for Indian IPO firms. Both variables have negative coefficients which mean that larger board and more number of committees both result in lesser underpricing and vice versa. Independent board members who hold their importance because of their role in safeguarding the interests of outside minority shareholders do not have any significant influence on investors’ decision-making and thus underpricing. Their partial independence can be a reason of this insignificant relation. SEBI introduced the concept of independent directors in India by Clause 49 of the Listing Agreement, 2000. But scams like that involved Satyam and top management spats like that of Tata-Mistry and Infosys keep on reminding that much more needs to be done. Recently, a SEBI’s 23-member panel on corporate governance led by banker Uday Kotak has advocated more powers for independent directors which include their minimum compensation, meetings, an increase in their accountability and so on (Vardhini, 2017). To increase the number of female directors on boards of Indian firms, the same panel of SEBI on corporate governance has recommended mandating the presence of at least one ‘independent’ female director on boards of listed firms. Adhering to this recommendation is expected to improve monitoring efficiency of the board by ensuring diversity in the board. Incorporating these developments in the prevailing legislature will ensure that these governance measures are considered by potential outside investors in their decision criteria followed while taking investment decisions, ensuring them of better performance of the firm and a return on their investments.

Implications of the Study and Scope for Future Research

The present study has been conducted for the concentrated and pyramidal ownership structure of Indian IPO firms. Results can be generalized to other developing and developed economies which have characteristic of concentrated family ownership common with that of the Indian economy. Since initial return is a measure of compensation for initial investors for investing in the firm (Hanafi & Setiawan, 2018), adhering to the results of the study by firms going public can result in lesser need of compensating investors, resulting in more funds collected for the activities of the firm. Large board size, institution of board committees and having a gender diverse board can largely help IPO firms checking information asymmetry and uncertainty surrounding the IPO. Another important task at hand for policymakers as well as for firms going public seems to be ensuring independence of independent directors. Although a sufficiently large number of board positions are held by independent directors in Indian firms, their insignificant impact on underpricing asks for more to be done. Lin and Chuang (2011) have also favoured employing stringently defined independent outside directors for checking principal–principal conflicts of developing economies. The new Companies Act of 2013 has given some regulations regarding proportion of independent directors on boards of Indian firms. Investors can immensely benefit by keeping the results of the present study and adherence of regulatory practices by the IPO companies in mind while making investment decisions.

Future researches focusing on the board of directors can measure the impact of their other characteristics on the perception of potential outside investors which may include their qualification, compensation, age and dual role as the chairman and CEO, among others.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.