Abstract

Using the Self-exciting Threshold Autoregressive Model (SETAR_M) and linear models such as the vector error correction model (VECM), and univariate models, this article specifies forecasting models for exchange rate volatilities in Ghana and compares their forecasts accuracy using Diebold–Mariano and Pesaran-Timmermann tests statistics. The relevance of this research is to equip business owners and businesses on managing forex losses and to reduce their impact on profits, productivity and employment in high volatile and unstable currency environments. The research concludes that the non-linear SETAR model is superior to the linear models in predicting short-term volatilities in exchange rates, while the fundamentally based linear model is superior for predicting long-term volatility in exchange rates. Therefore, short-term business commitments or transactions such as raw material purchases, cash expenses or incomes in foreign currencies should be planned or managed using SETAR or a non-linear model, whereas long-term contractual obligations like futures and forward contracts should be planned with a fundamentally based multivariate linear model.

Introduction

Exchange rates have a significant influence on production decisions and investment plans, as well as on the countries’ prices and competitiveness. Ghana’s exchange rates have been marred with frequent fluctuations leading to loss of business confidence, and obstructions in monetary policy transmissions (Abdul-Rasid & Yao, 2018; Abradu-Otoo et al., 2003; BoG, 2017). Mensah et al. (2013) revealed that exchange rate volatilities have substantially impeded employment growth in the manufacturing sector of Ghana, and it is one of the most unstable rates in the sub-region. To protect businesses and stop the decline in the macro economy, many researchers have proffered improvement in the macroeconomic fundamentals, increased policy transparency and the independence of monetary authorities (BoG, 2017). While these recommendations are likely to stabilize the macro-economy over the long term, businesses in the micro-sector need to manage the short-term effects of the transformational phase on business profits, productivity and employment. For this purpose, businesses, mostly affected by exchange rate volatilities, should have in their toolkit a framework or model which will assist them in planning and predicting exchange rates. The objective of this article is to specify forecasting models for exchange rate volatilities in Ghana and also to compare the forecast accuracy of these alternative models. The absence of this kind of research in Ghana will increase forex losses and put pressure on business profits, productivity and employments. These will result in hyperinflation and a high cost of living in the country.

The literature on specifying or modelling the volatilities in foreign exchange is vast and significant to reducing losses in the forex market (Abbate & Marcellino, 2014). Many researchers have classified these literatures into fundamentally based models and random-walk models. The fundamentally based models are exchange rate models specified or modelled on macroeconomic variables. These models could either be univariate models or multivariate models. The plethora of exchange rate models in research has shifted the focus of recent empirical works to comparing the statistical prediction of the models. For example, Rossi (2013), Carriero et al. (2009) and Cheung et al. (2005) compared the mean square forecast errors of fundamentally based models and random-walk models. The comparison revealed that the fundamentally based models are statistically superior to the random-walk models. This finding, however, contradicts the investigation in Abbate and Marcellino (2014) which supports the superiority of the random walk models over the fundamentally based models. These varying results have led Hauner et al. (2011) to conclude that there is no one superior model and that these mixed results or outcomes are due to differences in economic structures of countries. It is for this reason that Bléjer et al. (2000) emphasized for a country-specific study of exchange rate models rather than a panel study of the problem. Also, Petruccelli and Davies (1986) and Tsay (1991) have drawn a comparison between the linear and non-linear models and found that the non-linear models, as against linear models, are able to capture the dynamics and time irreversibility of a time series better than the linear models. Researchers such as Lee and Chen (2006), Sarno et al. (2004), Granger and Andersen (1978), Maravall (1983) and Tong (1983) have all written extensively on the superiority of the non-linear models in forecasting time series data. Therefore, researchers appear to build consensus on the superiority of non-linear models in forecasting exchange rate volatilities over all class of linear models. Accordingly, this article also intends to model exchange rate volatilities using Ghanaian data and to compare the forecasts or predictions of competing models. The approach adopted in many research works on this topic has been to employ traditional tools such as the mean square errors (MSEs) to compare between the forecasts of different models. These tools are, however, heavily criticized for their lack of economic meaning and unreasonable forecasts (Granger & Pesaran, 2000; Pesaran & Skouras, 2002). This research, besides using the MSEs, also employs Diebold–Mariano (DM) test statistics and the Pesaran-Timmermann (PT) test statistic to compare the forecast performance of the competing models. This approach ensures that business owners and businesses are able to manage (with minimum forex losses) the increasingly unstable and volatile currency in the country.

The objective of this article is to specify forecasting models for exchange rate volatilities in Ghana, and also to compare the forecasts accuracy of competing models. The research concludes that the non-linear model is superior to the linear models in predicting short-term volatilities in the exchange rate, whereas the linear model (the fundamentally based model) is superior for predicting long-term volatility in exchange rates. This result confirms the assertion in Abbate and Marcellino (2014) that the linear models added with macroeconomic differentials have higher predictive likelihoods at long horizons and during periods of recession. Therefore, short-term business commitments or transactions such as raw material purchases, cash expenses or incomes in businesses should be planned or managed using SETAR or a non-linear model, whereas long-term contractual obligations like futures and forward contracts should be planned with a fundamentally based multivariate linear model. The research also made recommendation for future research into determining the avoidable forex losses in the financial statements of a panel of businesses using the conclusions in this research.

The rest of this article is organized as follows: The second section is on the literature review, the third section is the methodology of the study, the fourth section is results and discussions, and the fifth section is conclusions.

Literature Review

This research studies one of the most volatile currencies, which have undergone several redenomination in Africa. The most recent redenomination that marks the start of the third cedi regime from 2007 has led to the taking off of four zero digits that brought the Ghana cedi on equal footings with the pound sterling of the fourth phase (Bank of Ghana Statistics and Reports Office, 2018). These exercises made Ghana cedi the highest denominated currency unit issued in Africa by 2007. The decision to redenominate the currency was to ensure ease of carrying the cedi. The redenomination did not have much to do with the value of the cedi relative to other currencies. Therefore, the ‘free fall’ of the cedi continued eventually, leading to a depreciation of 516% by May 2018. This rapid depreciation of the Ghana cedi and the occasional small appreciations distort trade and businesses in the country (International Monetary Fund, 2017).

Theories on Exchange Rates Determination

Exchange rates refer to the relative value of a country’s currency against the currencies of other countries. The value of a country’s currency could be a product of the outcome of monetary policy and market forces. Most countries today have entrusted the function of deciding monetary policies in the hands of Central Banks (Blinder, 1998; De Rosa et al., 2009). In determining relative values, the foreign exchange market sets the current market price of the value of one currency as demanded against another. These transactions are catered for globally between banks and are under the supervision of the Bank of International Settlements.

There are several theories or models on the determinants of relative prices of currencies in a free-float economy. Among these determinants are the international parity condition models, the balance of payment models, and asset prices models. These models are termed as fundamentally based models because they predict exchange rates with changes in economic fundamentals.

International Parity Condition Model

Hill (2006) acknowledged a general consensus in literature on the significance of prices, interest rates and market psychology in determining exchange rates. This subsection reviews the literature and data on the influence of prices and interest rates on Ghana’s exchange rates.

Purchasing Power Parity (PPP)

This theory or model of exchange rates assumes equal prices for identical goods in different countries under conditions of no transport cost and barriers to trade. In this model, exchange rates are determined by comparing prices of equal goods across countries. This is known as the Absolute PPP model and is expressed as

where yt is the price of an item or a basket of items in the home country’s currency at time (t), xt is the price of an item or a basket of items in the foreign country’s currency at time (t), ExRt is the relative price or exchange rate at time (t).

The absolute PPP model in Equation (1) neglects the effects of inflation on prices. However, relative PPP model incorporates these effects into the computation of exchange rate in Equation (2)

where INFA(t) is home country’s inflation, INFB(t) is foreign country’s inflation. The effect of inflation on the exchange rate will depend on the magnitude of INFA(t) and INFB(t), that is, inflation differential (INFA(t) – INFB(t)).

Hill (2006) mentions that the PPP model is best in producing results in countries with high inflation and under-developed capital markets. To test the predictive power of the relative PPP on Ghana’s exchange rates and market expectations, we regressed the exchange rates with the inflation differentials as follows:

If relative PPP holds, β will be negative, implying a depreciation in the exchange rate of the home country.

Theoretically, the β will be equal to one (1) if the whole basket comprises of only traded goods, and less than one (1) if non-traded goods are included in the basket. This will also mean that the α will be zero (0) if the whole basket comprises of only traded goods. The PPP theory was first proposed by Cassel (1918).

Interest Rate Parity Condition Model

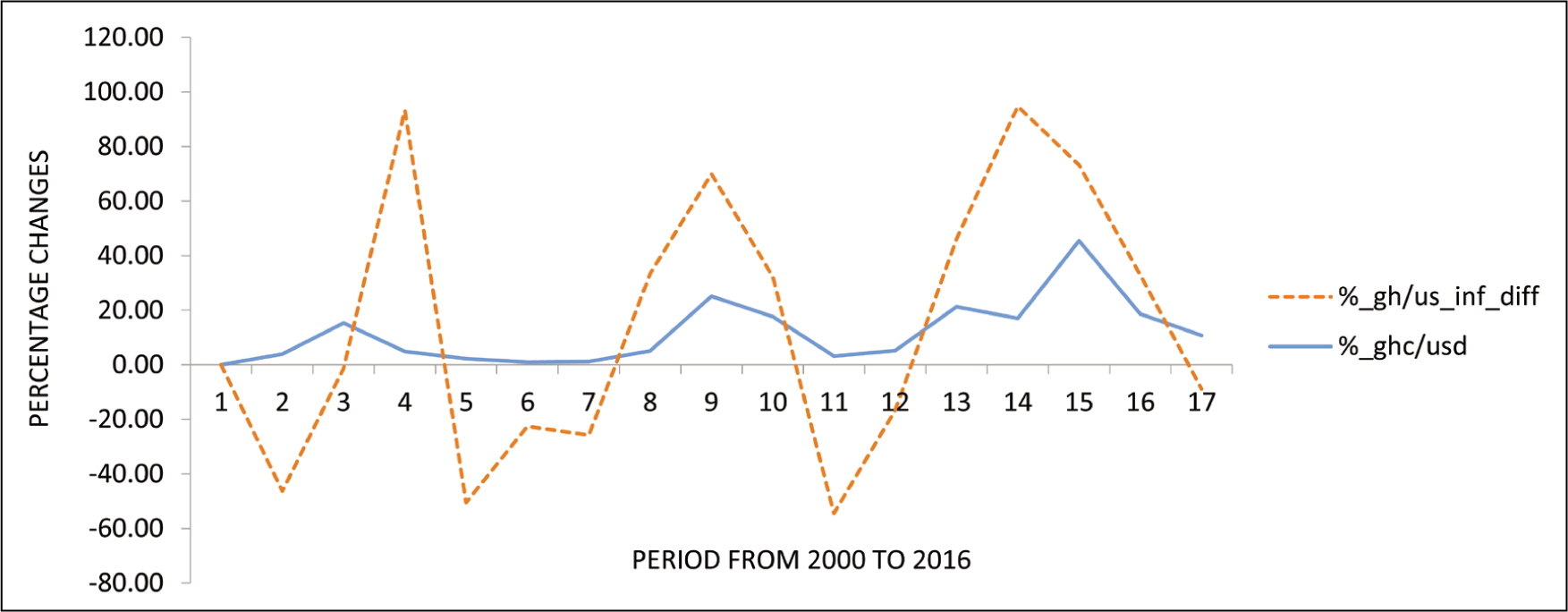

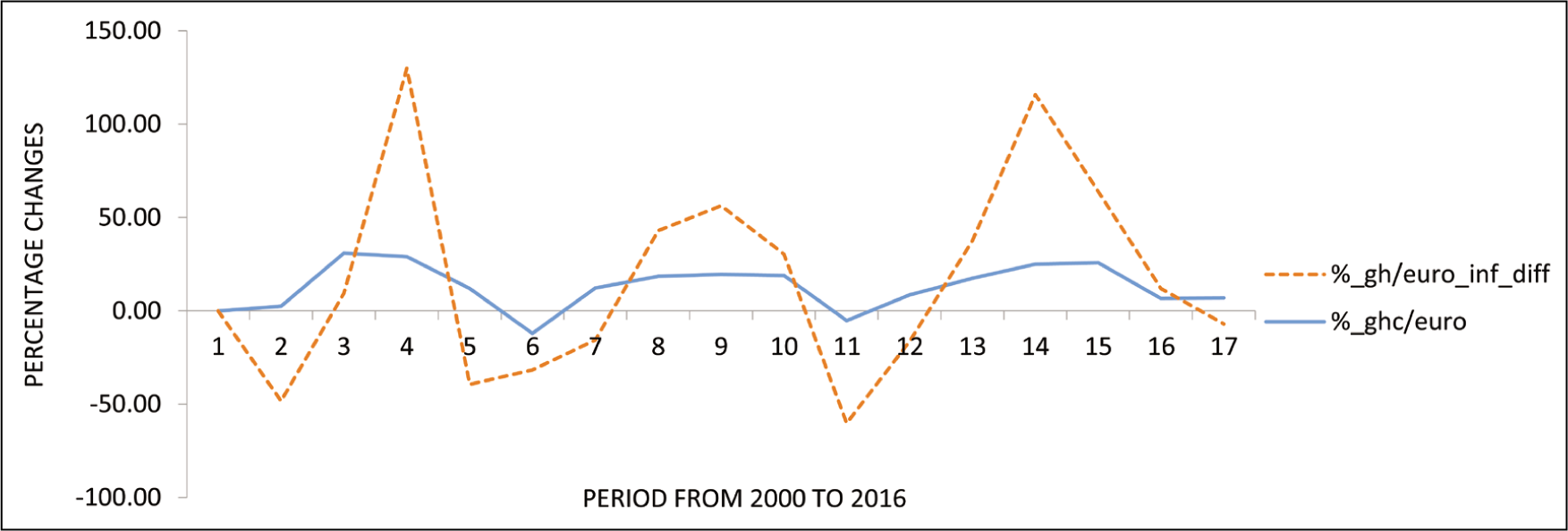

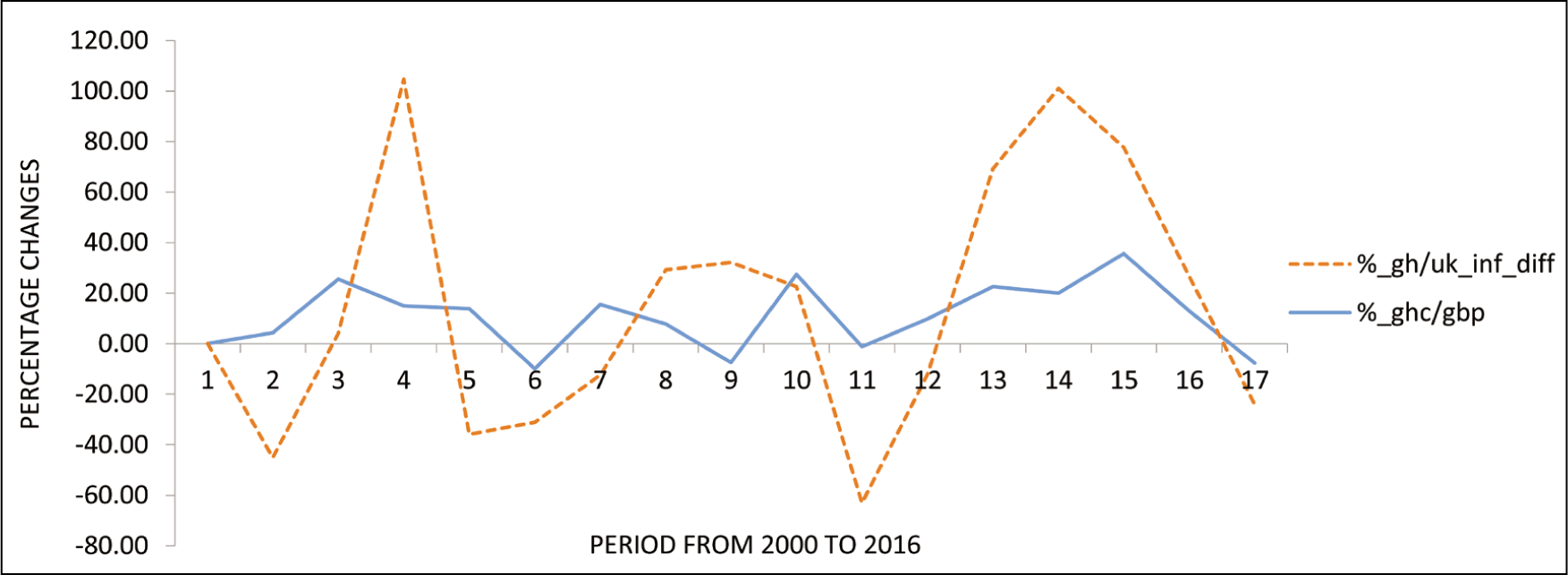

The interest rate rule operates on the basis of the Taylor principle which suggests a positive relationship between interest rates and inflation. The rule states that for every 1% increase in inflation, interest rates should be increased by more than 1%. The Taylor rule or principle is depicted in Figures 1–3. These figures show a positive general trend between the differential series. The Taylor rule is consistent with the International Fisher effect theory. This theory suggests that investors expect increase in interest rates when inflation increases as a compensation for the lost in value of their investment. The Fisher effect shares similarities with the Taylor rule, and was first formalized by Irwin Fisher (Hill, 2006). The Fisher effect considers high interest rates as a premium on inflationary risk. This is expressed as

Cedi–Dollar Exchange Rate and Inflation Differential Plot.

Cedi–Euro Exchange Rate and Inflation Differential Plot.

Cedi–Pound Rate and Inflation Differential Plot.

where It is the nominal interest rate, rt is the real interest rate and INFt is the inflation.

The Taylor rule is preliminary to the success of uncovered Interest rate parity (UIRP). The UIRP suggests that a currency with a higher interest rate is expected to depreciate by the amount of interest rate differential. This depreciation will make up for the gain in interest which will therefore prevent arbitrage profit in the foreign exchange market. The Taylor rule recommends a high nominal interest rate when inflation is above its target and output is above full employment. This is a case of monetary tightening. However, during periods of stagflation, where inflation is above its target and output is below full employment, the goals of monetary policy may conflict. The IMF Article IV Consultation Report (International Monetary Fund, 2017) recognizes this is the situation seldom experienced in Ghana. The remedy specified under the Taylor rule in this circumstance is to specify some relative weights for reducing inflation and some for increasing output. The IMF under the same report has also noted Ghana’s increasing desire to populate domestic output instead of bring inflation within target (Bhattarai & Armah, 2005; International Monetary Fund, 2017).

The interest rate parity is stated formally as the change in the spot exchange rate between two currencies A and B. This is expressed as

where S1 is the spot rate at the beginning of the period, S2 is the spot rate at the end of the period.

Balance of Payment Model

This model assumes exchange rate to be caused by tradable goods and services. It ignores the role of global capital flows in exchange rate determination. Exchange rate appreciations are linked to current account surplus and transactions in the model.

Asset Prices Model

This model views currencies as an important class of building investment portfolios. Asset prices or exchange rates are influenced mostly by peoples’ willingness to hold the existing quantities of assets or currencies which in turn depends on their expectations of the future worth of these assets. This model states that the exchange rate between two currencies represents the price that just balances the relative supplies of and demand for assets denominated in those currencies.

Empirical Review of Literature

Modelling and predicting Ghana’s exchange rate movements will need a decision to be made on model specifications. Work on exchange rate models, especially in an open economy, has evolved from specifying and comparing the forecast evaluation measures of models to now testing and comparing the significance of forecast evaluation measures. The empirical works of Rossi (2013), Carriero et al. (2009) and Cheung et al. (2005) have specified and compared the mean square forecast errors of fundamentally based econometric models such as the univariate models, error correction models, multivariate models and panel models with the mean square errors of random-walk models. These works have found the fundamentally based models to be statistically superior to the random-walk models. However, the conclusion reached by these researches is in sharp contrast with the view held in Abbate and Marcellino (2014), who believe most empirical studies support the superiority of the random walk models over the fundamentally based models. These differences in empirical works have led Takizawa et al. (2011) to assert that it is challenging to anticipate a likely winner between these competing exchange rate models and therefore different methodologies have produced mixed results and outcomes.

Petruccelli and Davies (1986), Yao and Rahaman (2018) and Hansen (1999, 2011) mentioned the significance of forecasting with non-linear models in another related development. They assert that non-linear models, as against linear models, can capture the dynamics and time irreversibility of a time series better than linear models. Additionally, it is also a well-known fact that the Gaussian linear time series models have failed to capture many phenomena commonly observed in practice (Tsay, 1991). This has led many researchers to propose non-linear specification of exchange rate modelling and that the non-linear models consistently outperform their linear counterparts in many respects (Ben Aïssa et al., 2004; Granger & Andersen, 1978; Maravall, 1983; Tong, 1983). For instance, in terms of forecasting accuracy and reliability, Tsay (1991) asserts that the non-linear models have moved time series analysis a step closer to reality. However, despite what has appeared to be a consensus of the non-linear models’ superiority, there is also general recognition of their difficulties and sophistication. We review a few of the literature on the difficulties in specifying a non-linear model and the methodologies in detecting non-linearity in time series data.

Many studies have shown that the BDS test, developed by Brock et al. (1987), has power against several ranges of linear and non-linear phenomena. The BDS test was developed to test the null of independent and identical distribution (IID) in time series and help detect non-random and chaotic dynamics. The strength of the BDS test is its ability to test for both non-linearity and model misspecification, which are the two main issues challenging non-linear analyses. Also, another equally relevant approach for testing non-linearity in a time series is the Tsay F-test statistic. The Tsay F-test approach or statistic detects a wide range of non-linear phenomena in time series data. For instance, the Tsay test is good in detecting bi-linearity. It can also detect threshold non-linearity and exponential non-linearity in a time series (Tsay, 1991). However, this test has a slight shortcoming in its approach to determining threshold non-linearity. The disadvantage of using the Tsay test (1986), including the test proposed by Petruccelli and Davies (1986), is the use of arranged autoregressive model in determining the thresholds that generally require knowledge of the threshold variable. Tsay (1989) asserts that the arranged autoregression only becomes useful for the threshold models when arranged according to the threshold variable. Our experience of the literature on threshold regression reveals that this threshold variable is primarily unknown by researchers. This, therefore, complicates Tsay’s approach in detecting threshold non-linearity, but it is still an essential tool in detecting non-linearity and widely used by researchers. Finally, an alternative test to the Tsay’s test and the Petruccelli and Davies approach is the Bai–Perron test. This test is equally good in detecting thresholds in times series and does not determine thresholds based on an arranged regression. This test is, therefore, functional even if the threshold variable is unknown. The procedure is based on multiply structural changes and allows one to test the null hypothesis of say i changes versus the alternative hypothesis of i + 1 changes. This is useful because it allows a specific-to-general modelling strategy to consistently determine the appropriate number of changes (Bai & Perron, 1998).

Research Methodology and Empirical Testing

Research Variables and Data

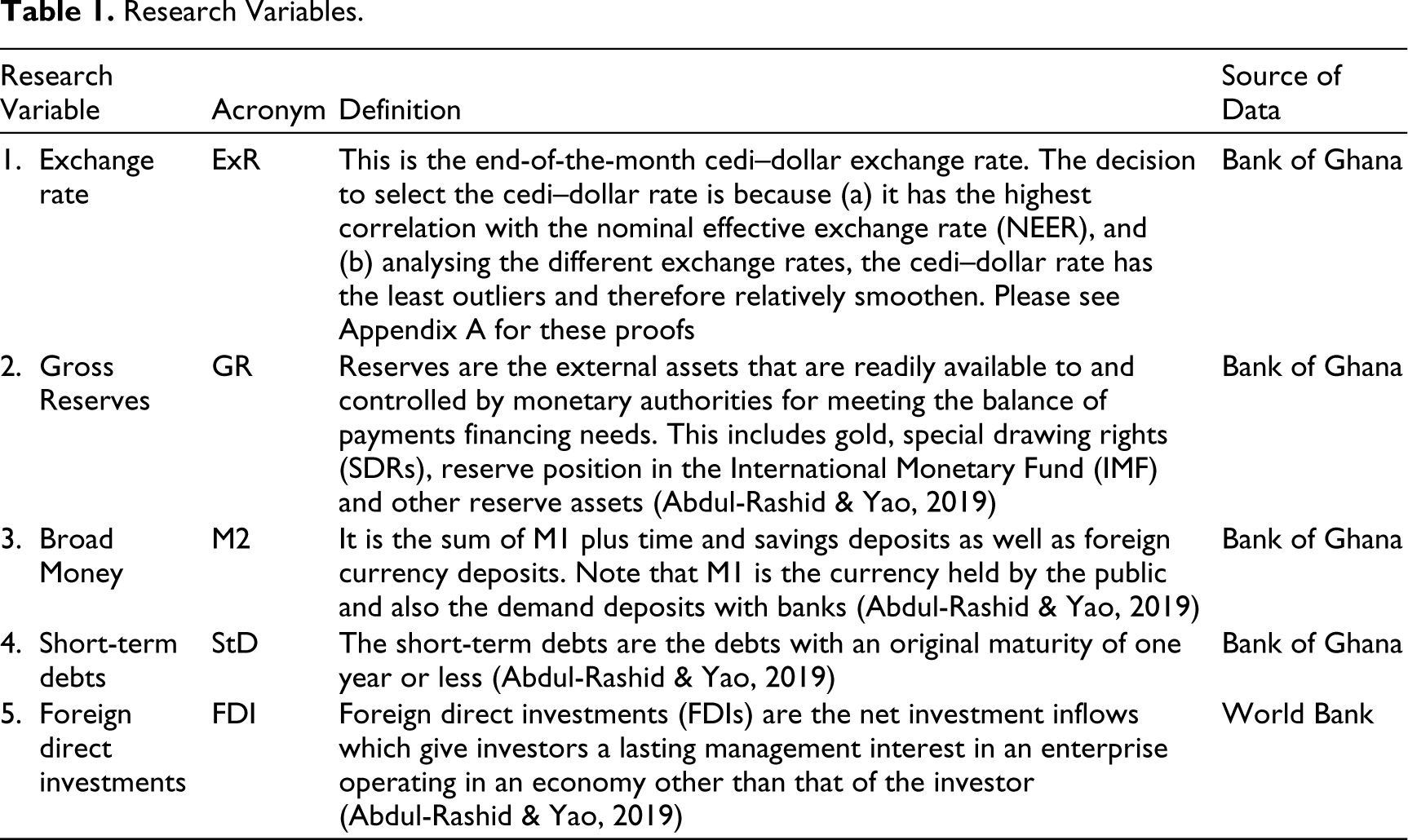

Molodtsova and Papell (2012) find that the predictions of Taylor rule models can be improved when supported with credit spread or measures of financial conditions. Sarno et al. (2004) also show evidence of the relationship between exchange rates and monetary fundamentals, and Lossifov and Loukoianova (2007) proved the prices of main export commodities also have an impact on Ghana’s exchange rate. Also, a report from the Bank of Ghana (May 2017) asserts that to reduce the cedi exchange rates’ volatilities, Ghana’s government has sought to reduce its external exposure by changing its debt structure to include more domestic debts. For these reasons, the research variable used in this research are carefully selected to include: exchange rates, gross reserves, broad money, short-term debts, and foreign direct investments.

The data for the research is a monthly time series data taken from the Central Bank of Ghana’s database and from the World Bank database from the years 2000 to 2018. Table 1 shows the research variables and the sources from which data were taken.

Research Variables.

Specification of Linear Models and Test Outputs

Preliminary Testing

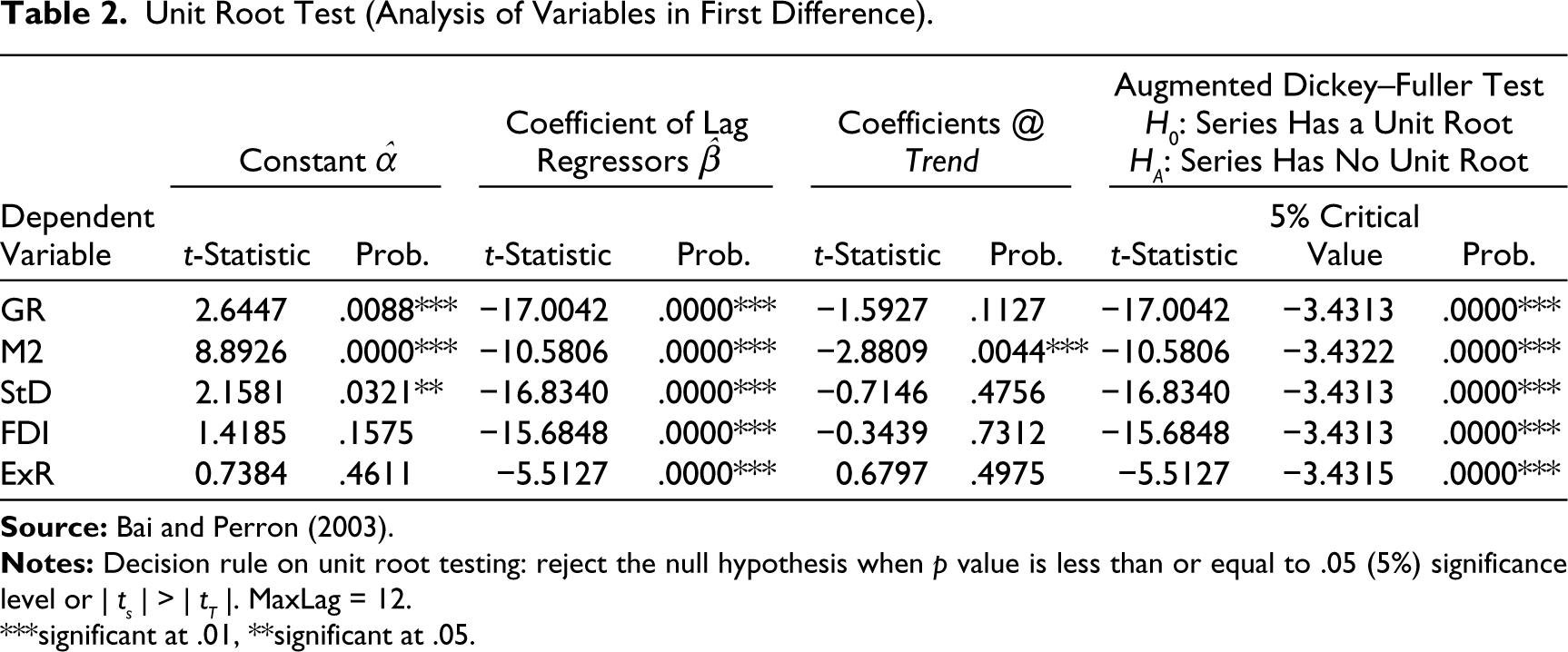

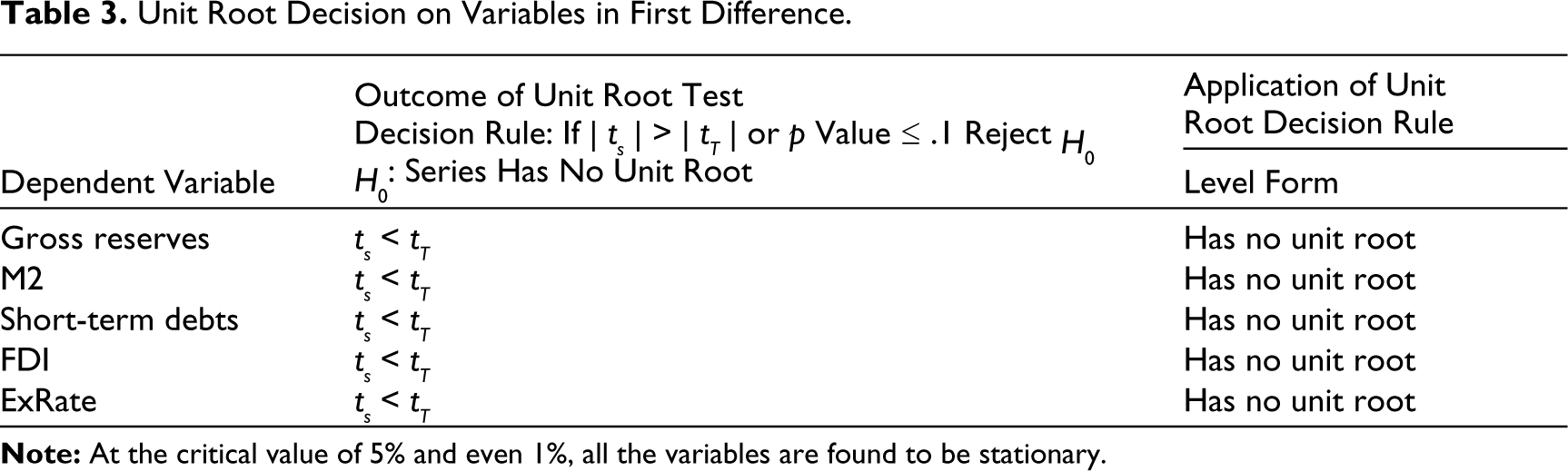

The variables were tested for stationarity or unit root. Tables 2 and 3 show the results of the unit root test. The test shows all the variables as stationary [I(0)]. Also, we found the variables gross reserves, broad money and short-term debts to have significant constant terms. We also found broad money to have a significant trend. We, therefore, specify and estimate the linear models with these deterministic features.

Unit Root Test (Analysis of Variables in First Difference).

***significant at .01, **significant at .05.

Also, a co-integration test was performed on the first difference of the variables, and the test revealed no co-integration existed in the transform state of the variables. Therefore, this output is withheld.

Unit Root Decision on Variables in First Difference.

Specifying Linear Models (i.e. a VAR Model and an ARIMA Model)

First, we specify a VAR model. Note that because there is no long-term relationship among the variables, we do not add an error term to the model. Therefore, we only specify a VAR(p) model, and impute into the model both trend and constant terms. These variables are added to the model because of the significant constant and trend in the unit root test table. In the final estimate of the VAR(p) model, we introduce a lagged exogenous variable into the model which is petroleum prices. This approach is to capture the research finding of Lossifov and Loukoianova (2007) that prices of main export or import commodities also have an impact on Ghana’s exchange rate.

The general VAR(p) model is therefore expressed as

where Yt is a (k × 1) vector of endogenous variables; X is a (k × 1) vector of exogenous variables, that is, change in petroleum prices; α0 is a (k × 1) vector of constant terms; θi is a (k × k) matrix of coefficients; δi is a matrix of exogenous coefficients; εt (k × 1) vector of error terms.

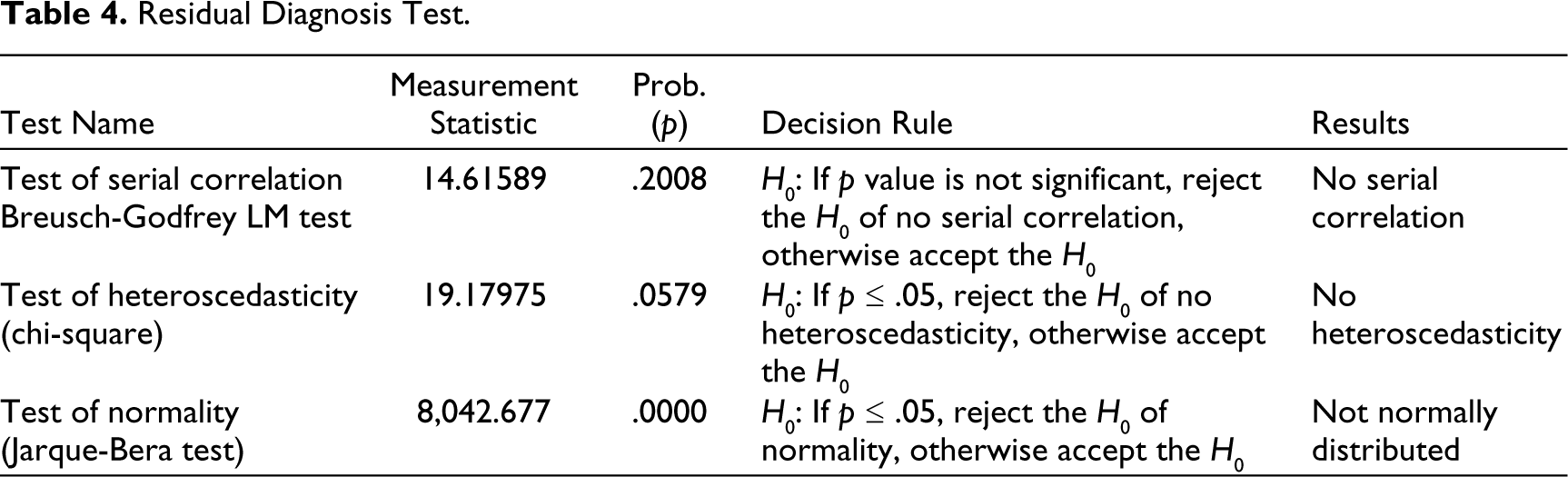

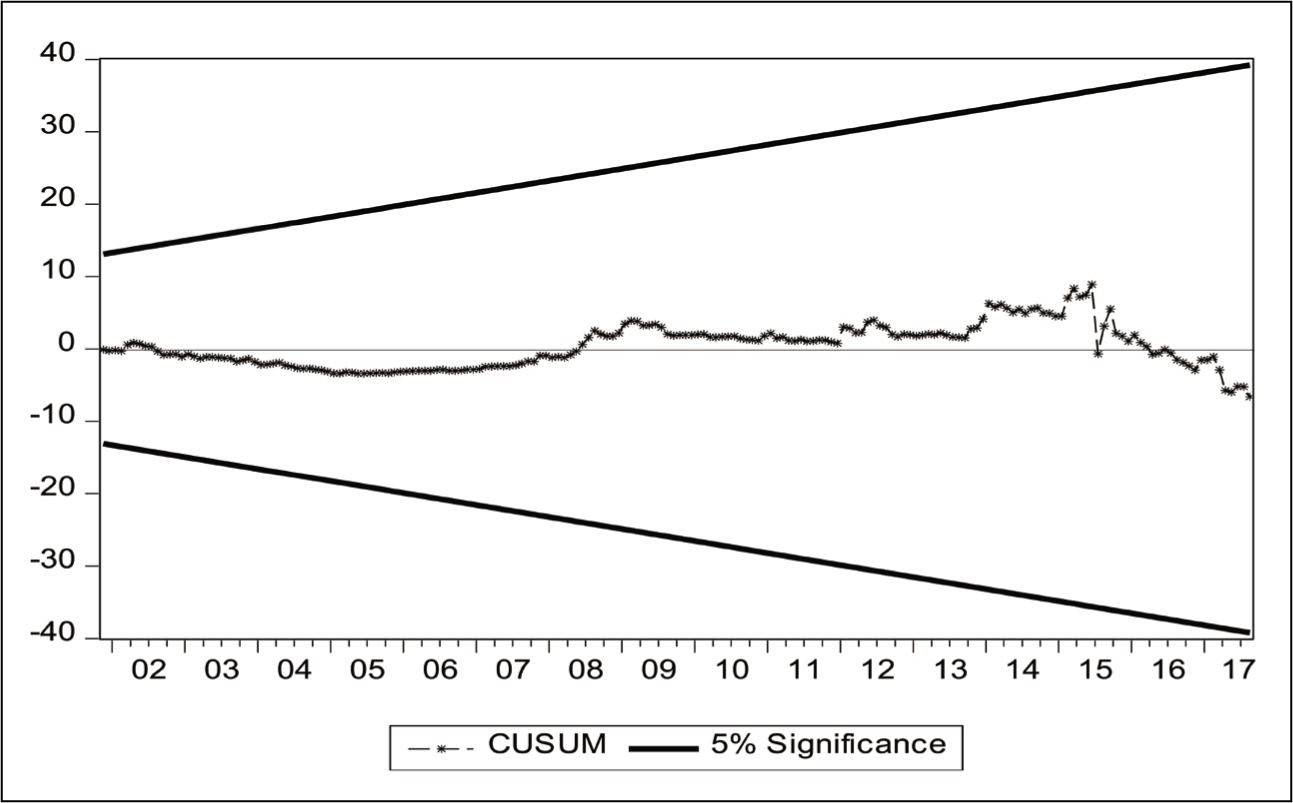

The model was tested for serial correlation, heteroscedasticity and normal distribution. Table 4 shows these residual diagnosis tests, and Figure 4 shows the parameter stability test of the model.

Residual Diagnosis Test.

Parameter Stability Test.

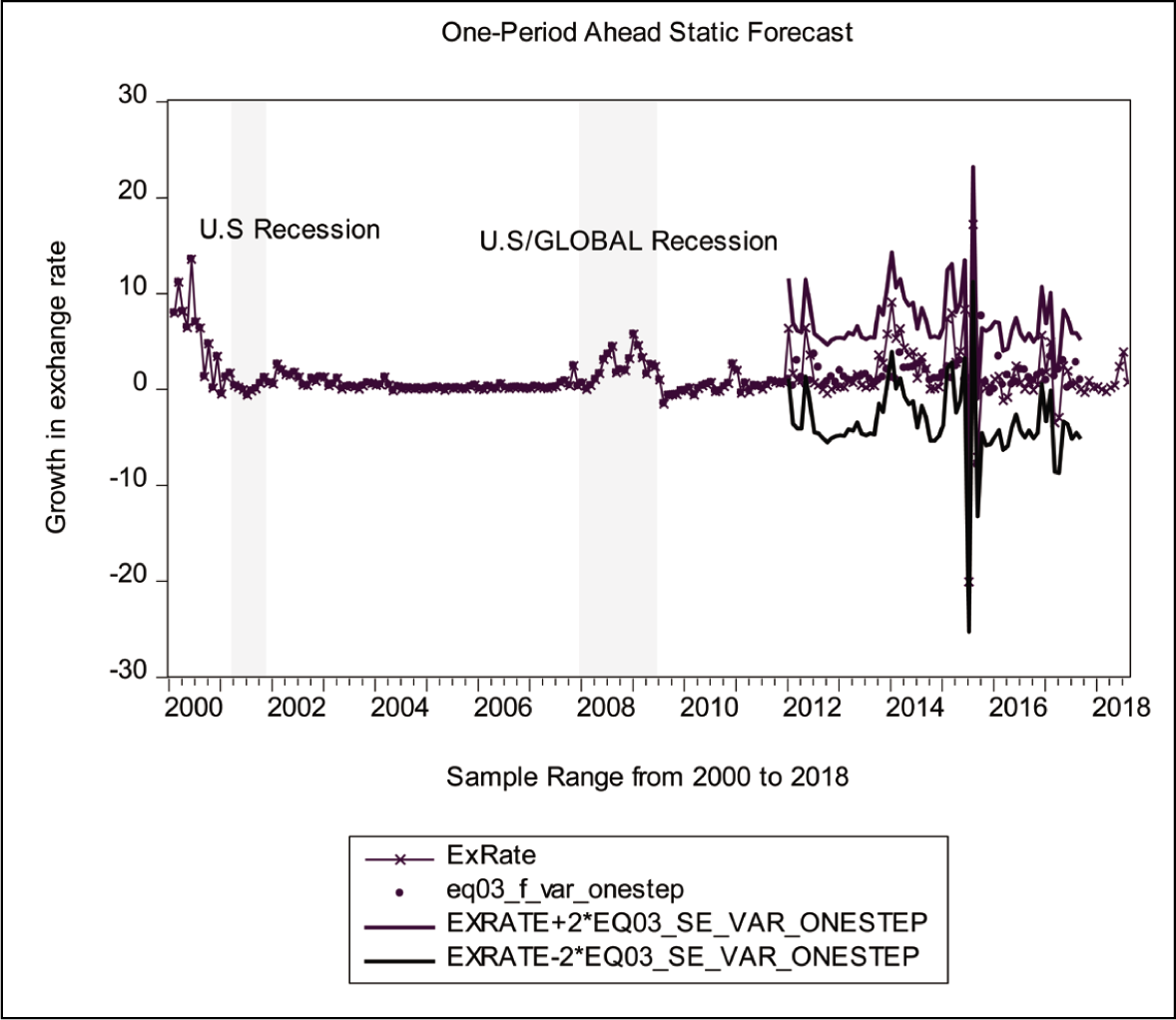

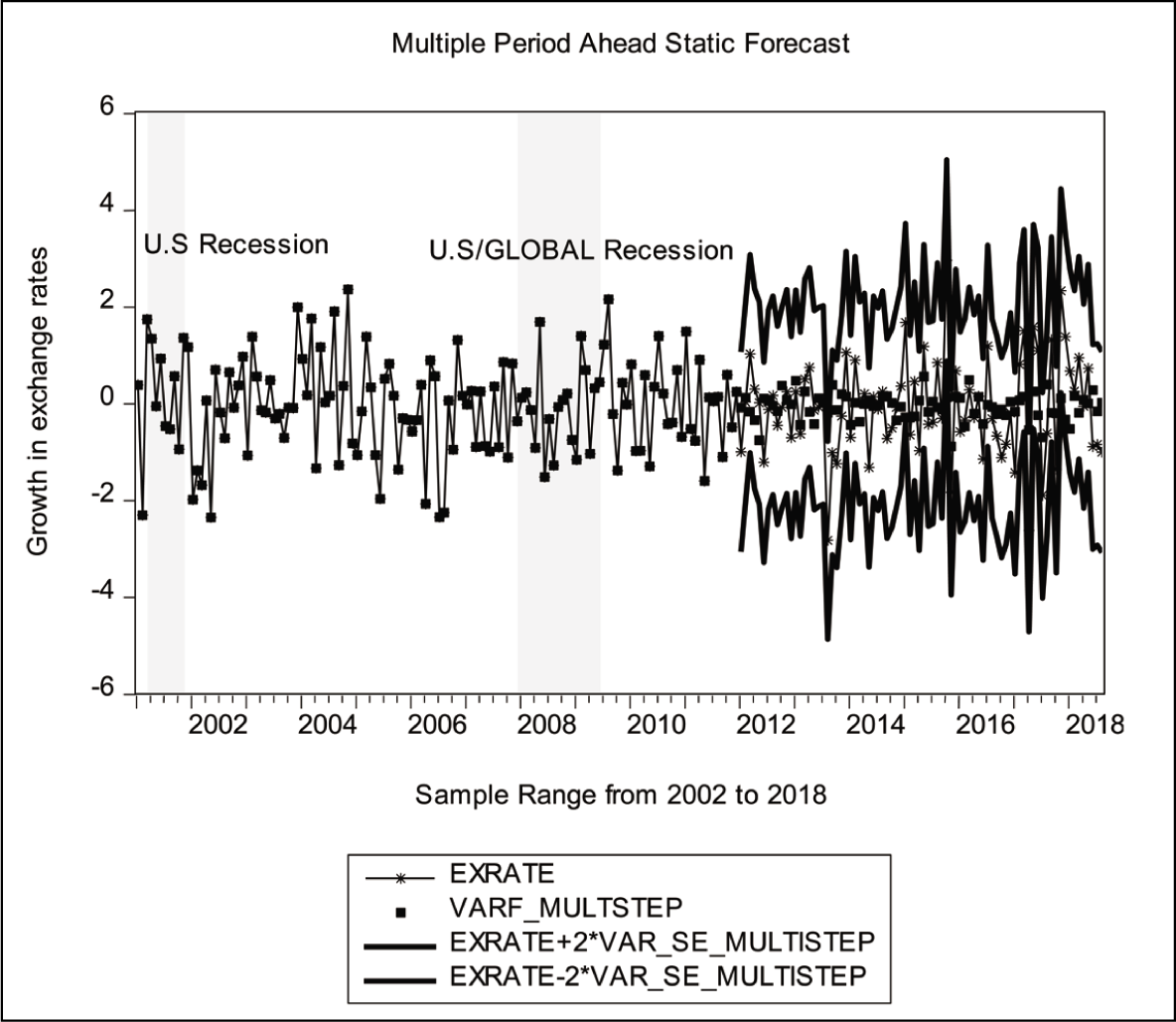

The forecast measures of the VAR model are summarized in Table 5. The root mean square error (RMSE) and the Theil inequality coefficient are lesser for the one-period ahead forecast than the multiple-period ahead forecasts. This result means the prediction for the one-period ahead forecast is more accurate for the VAR model than the prediction of the multiple-period ahead forecast. Figures 5 and 6 show the forecast graphs of the VAR model.

Forecast Performance Evaluation Measures of the VAR(11) Model.

One-period Ahead Forecast Graph_VAR Model.

Multiple-period Ahead Forecast Graph_VAR Model.

ARIMA Model

Second, we specify an autoregressive integrated moving average (ARIMA) model by following the BJ (Box–Jenkins) methodology. In the BJ methodology, the first approach is to identify the appropriate values of the autoregressive lags (p), the number of times the series is differentiated (d), and the number of moving average terms (q).

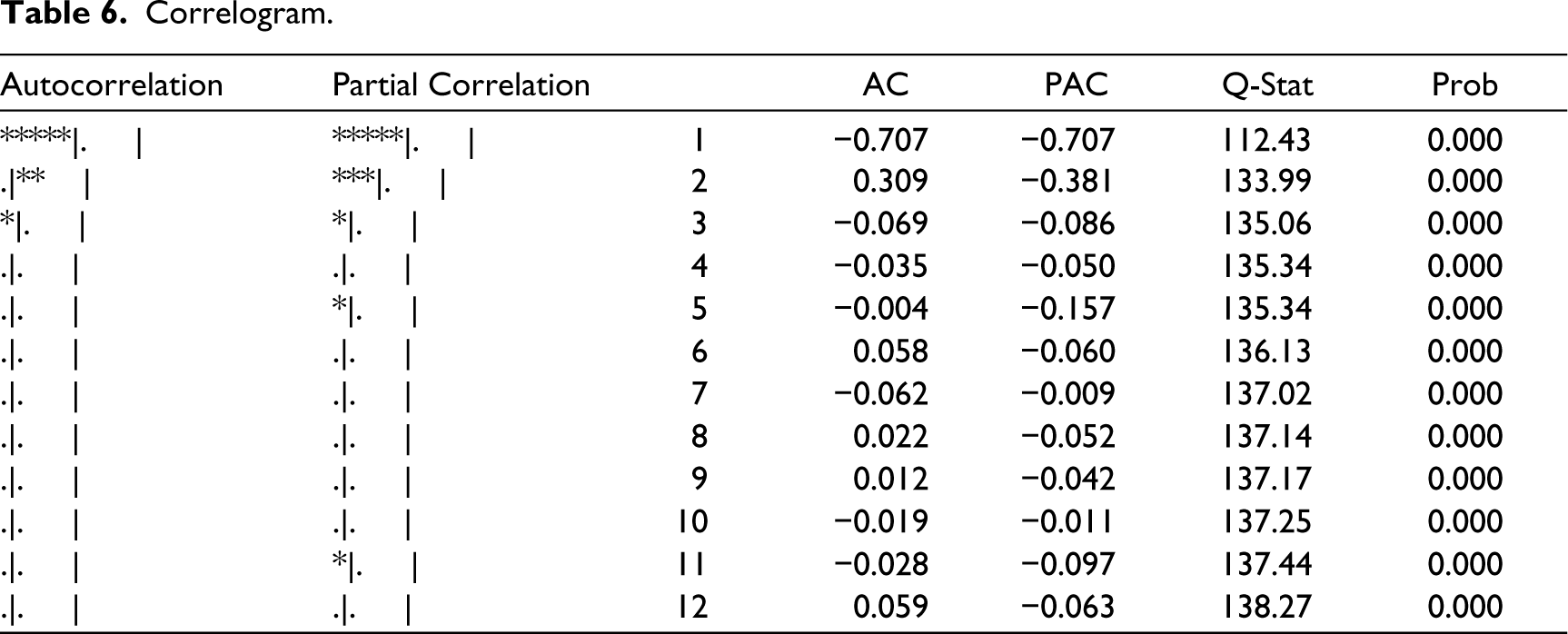

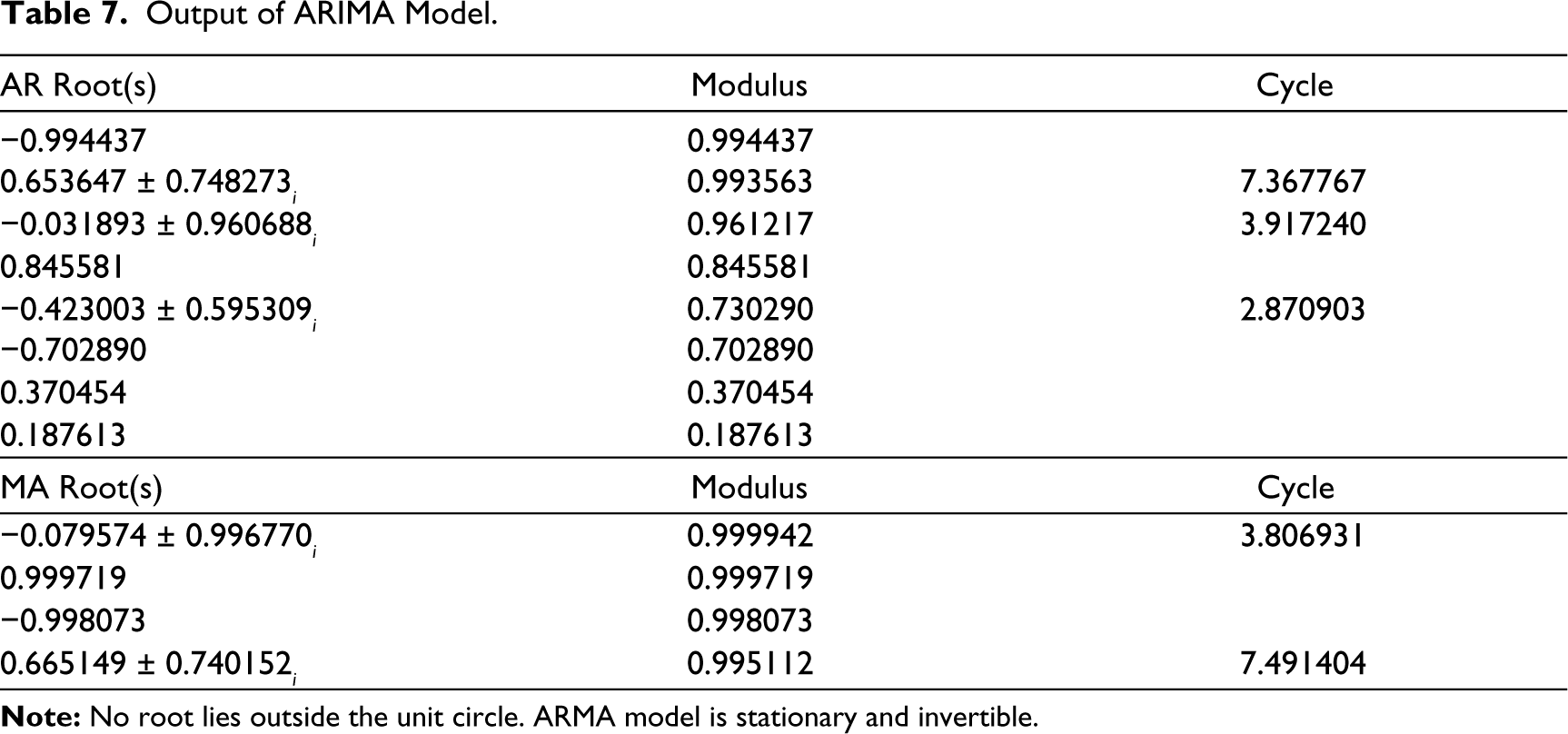

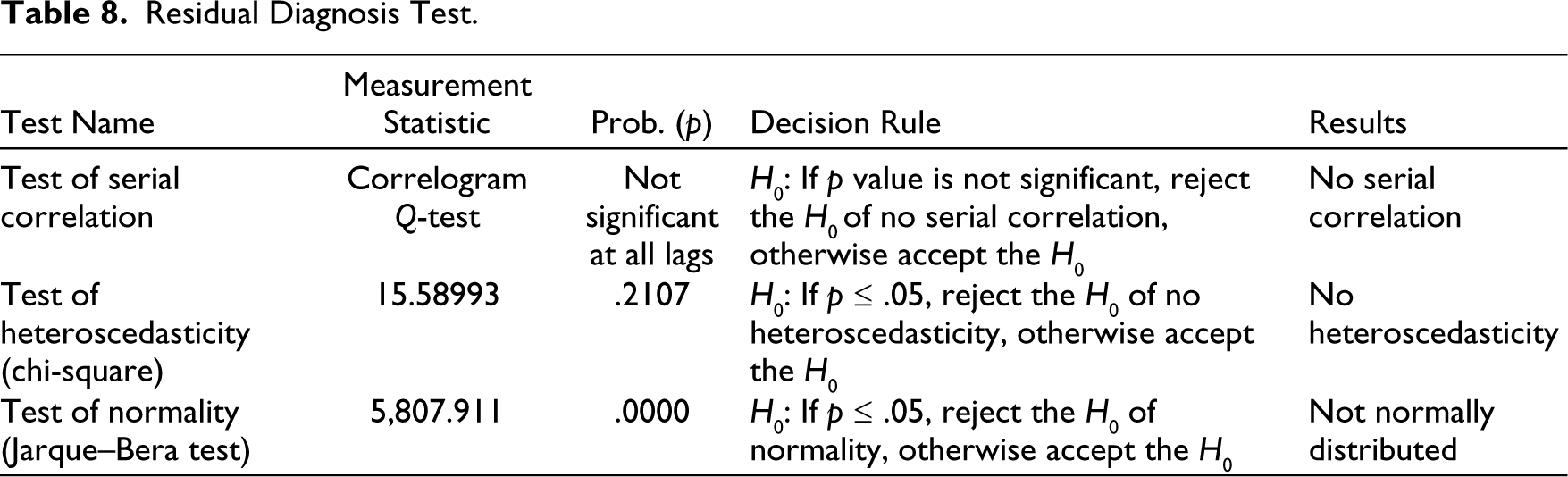

For the order of integration (d), we have shown in the VAR model that the cedi–dollar exchange rate is an integration of order 1, that is, [I(1)]. Table 6 shows the correlogram which will enable us to determine the values of p and q. From the correlogram, we observed that the PACF is significant up to the 11th lag and the ACF has only two significant lags. The outlook of the table gives an ARIMA (11, 1, 2); however, the final fitted model is an ARIMA (11, 1, 6). The estimated output of this model is presented in Table 7. Also, the residual diagnosis test of this model is shown in Table 8.

Correlogram.

Output of ARIMA Model.

Residual Diagnosis Test.

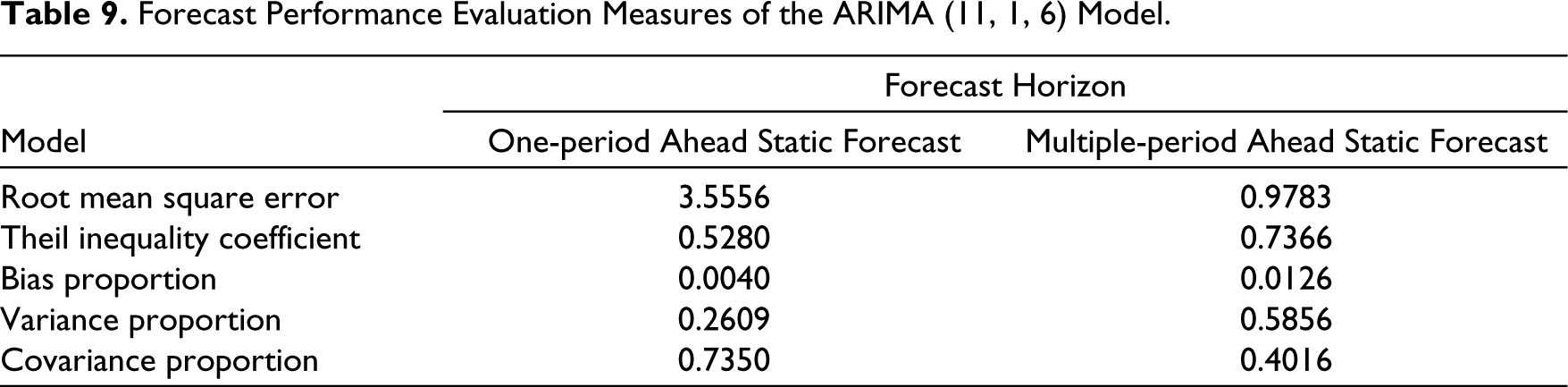

The forecast measures of the ARIMA (11, 1, 6) is that the RMSE and the Theil inequality coefficient are lesser for the one-period ahead forecast than the multiple-period ahead forecasts. This is shown in Table 9. The result, again, shows that the one-period ahead forecast prediction of the ARIMA model is more accurate and closer to the actual values than the multiple-period ahead forecast prediction. Figures 7 and 8 show the forecast graphs of the ARIMA model.

Forecast Performance Evaluation Measures of the ARIMA (11, 1, 6) Model.

One-period Ahead Forecast Graph.

Multiple-period Ahead Forecast Graph.

Specification of a Non-linear Model and Test Output

Before we proceed with estimating a non-linear model, we need to establish that (a) the cedi–dollar exchange rate is non-linear and (b) which type of non-linear series is the cedi–dollar exchange rate?

To address these issues, we employed the Brock, Dechert and Scheinkman (BDS) independence test and the Bai–Perron test statistics, respectively. Tables 10 and 11 show the test output of the BDS test and Bai–Perron test statistics, respectively. The BDS test output shows the cedi–dollar rate series is non-linear, and therefore, predictions of the series values are better captured by a non-linear model. Also, the Bai–Perron test results show the presence of thresholds in the cedi–dollar rates and therefore specifying a self-exciting threshold autoregression (SETAR) model fits the data correctly (Gibson & Nur, 2011; Gyamfi & Kyei, 2016; Haggan et al., 1984; Lossifov & Loukoianova, 2007). The SETAR model is specified below:

BDS Independence Test of Non-linearity.

Bai–Perron Test of L + 1 Versus L Sequentially Determined Thresholds.

*Significant at the 0.05 level; **Bai–Perron (Bai & Perron, 2003) critical values.

A time-series data is said to follow a j-regime self-exciting threshold autoregressive (SETAR) model with a threshold variable Zt– 1 if it satisfies:

where θ is the autoregressive parameters; σ is the standard noise deviation; Γ is the threshold parameter; ε is a sequence of IID random variables with mean 0 and variance 1.

The general form of the SETAR model is

From the general model, the parameters are in the lower regime if the threshold variable (Zt– d) is lower than the threshold value (Γ) and in the upper regime, if the threshold variable (Zt– d) is greater than the threshold value (Γ). This process is the regime-switching process between linear models and is dependent on the position of the threshold variable (Zt– d). Our fitted SETAR (5, 11) model is therefore:

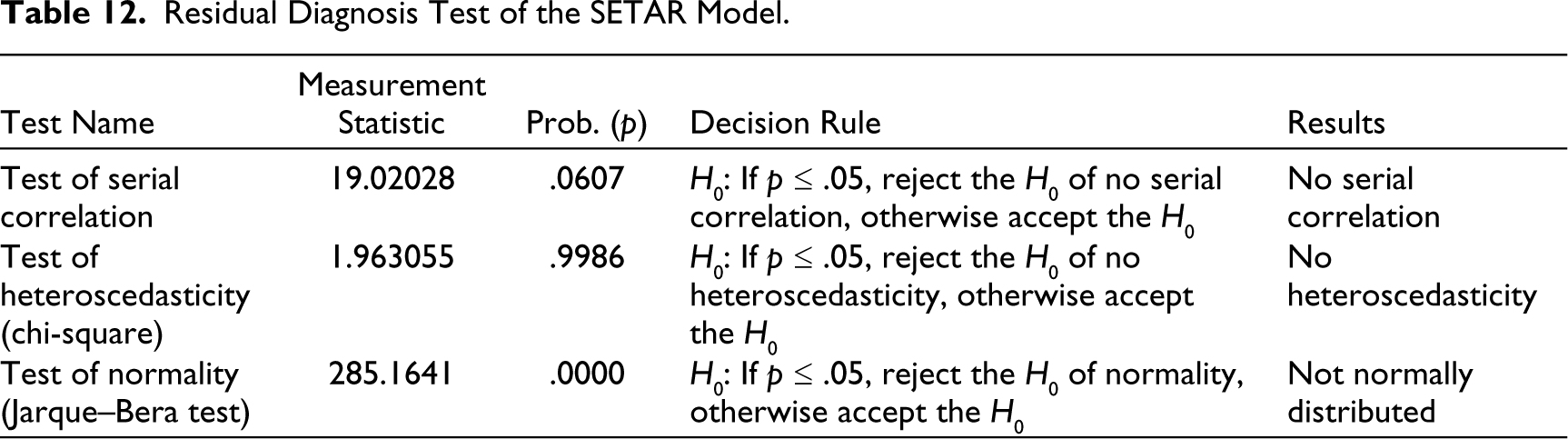

Table 12 shows the residual diagnosis of the SETAR model. The Jarque–Bera test statistic indicates the residuals of the series are not normally distributed, but this condition can be improved with data additions.

Residual Diagnosis Test of the SETAR Model.

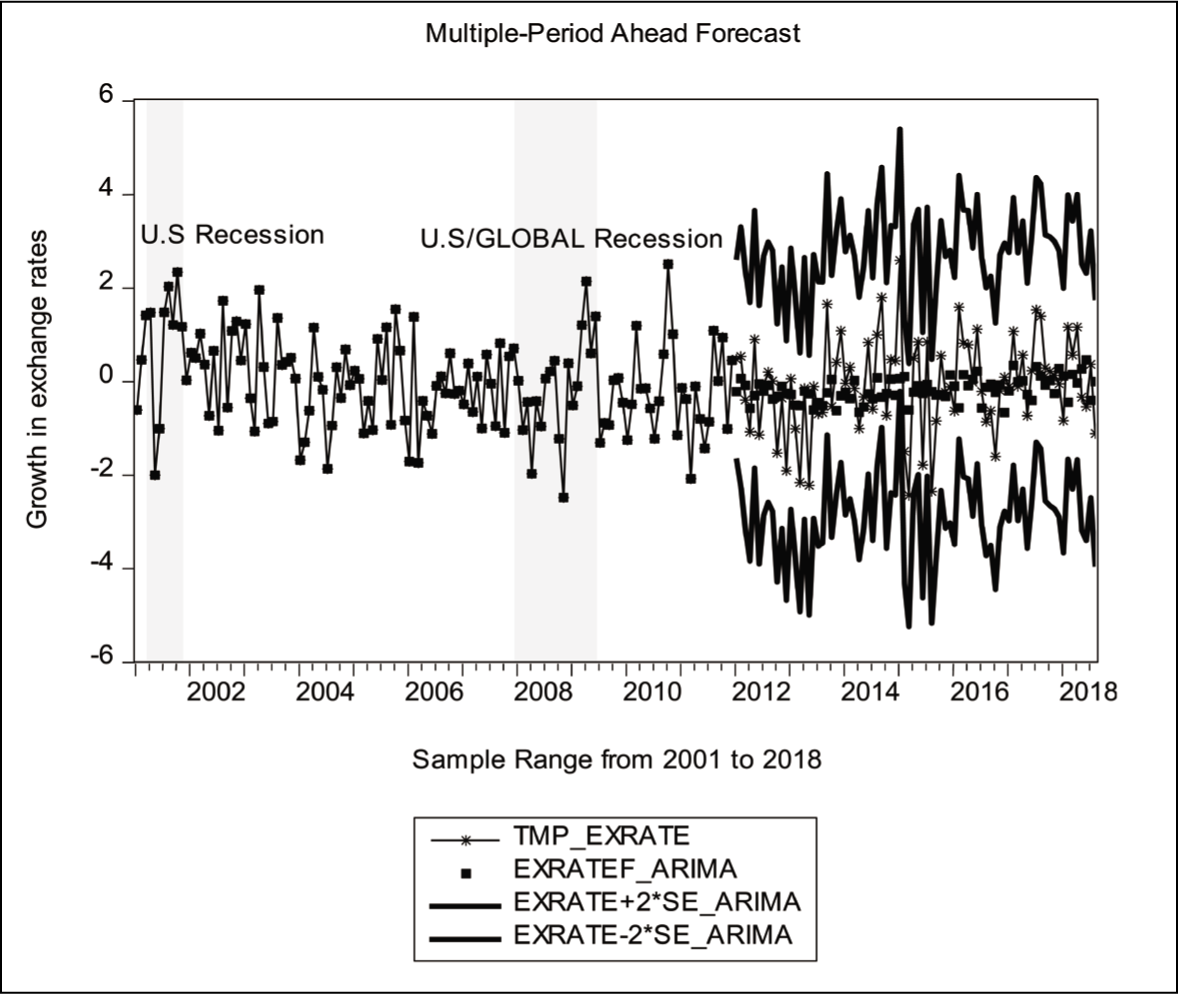

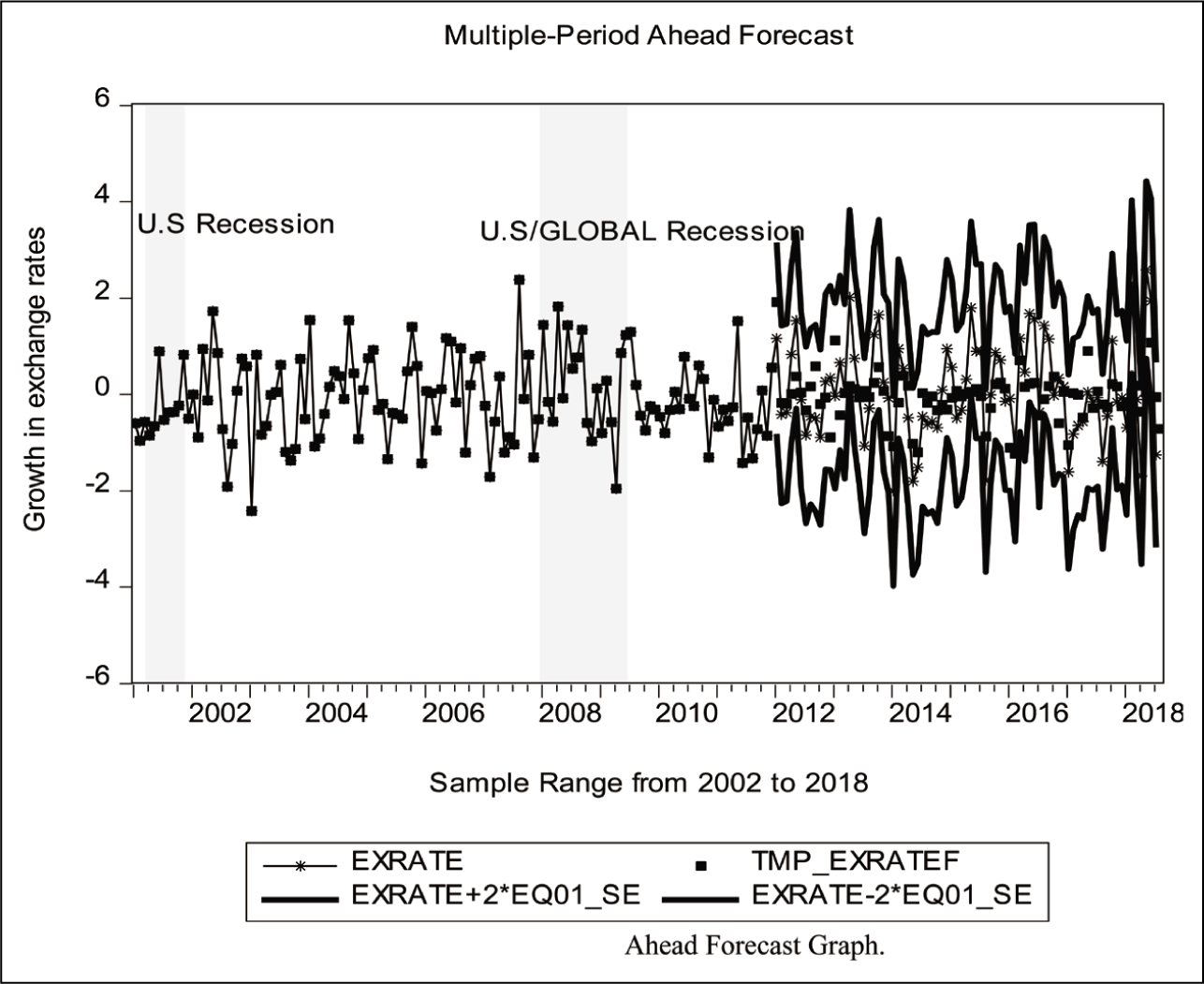

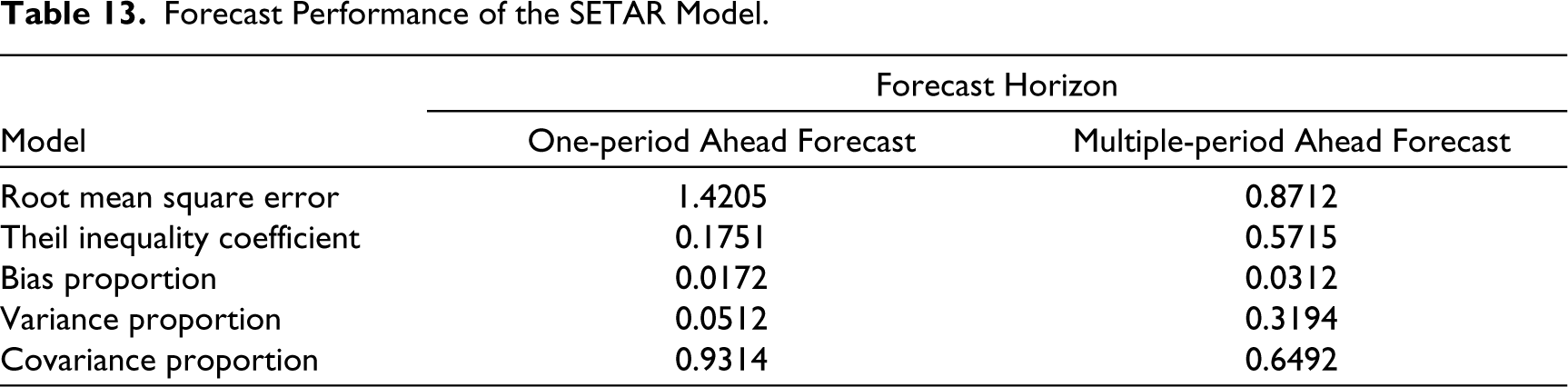

Figures 9 and 10 show a one-period ahead forecast and a multiple-period ahead forecast of the SETAR (5, 11) model. These figures marked the United States’ low economic periods, that is, the recession of 2001 and the global financial crisis from late 2007 to early 2009. The plot of the actual rates (represented by an asterisk line x) and the forecasted rates (represented by a square box) from 2011 to 2018 shows a relatively narrow gap than the plots in Figure 10 (the multiple-period ahead forecast). This narrowing gap shows that the forecasts produced in Figure 9 are superior and better than the forecasts in Figure 10. The results in Table 13 confirm the observations from the figures. Table 13 shows the forecast evaluation measures of the SETAR non-linear model. The RMSE of the SETAR model is lesser for the multiple-period ahead forecast. This lesser value of 0.8712 means the predicted values of the non-linear model for the multiple-period ahead forecast are superior to a one-period ahead forecast. The other measurements, that is, the Theil inequality, the Bias proportion, variance proportion and the covariance proportions, are sub-measures or components of the RMSE. We will discuss these sub-measures in the ‘Results and Discussions’ section.

One-period Ahead Forecast Graph.

Multiple-period Ahead Forecast Graph.

Forecast Performance of the SETAR Model.

Comparison between the Forecast Evaluation Measures

The forecast evaluation measures of the competing models are compared using both the traditional forecast evaluation measures and the advanced forecast evaluation measures.

Traditional Forecast Evaluation Measures

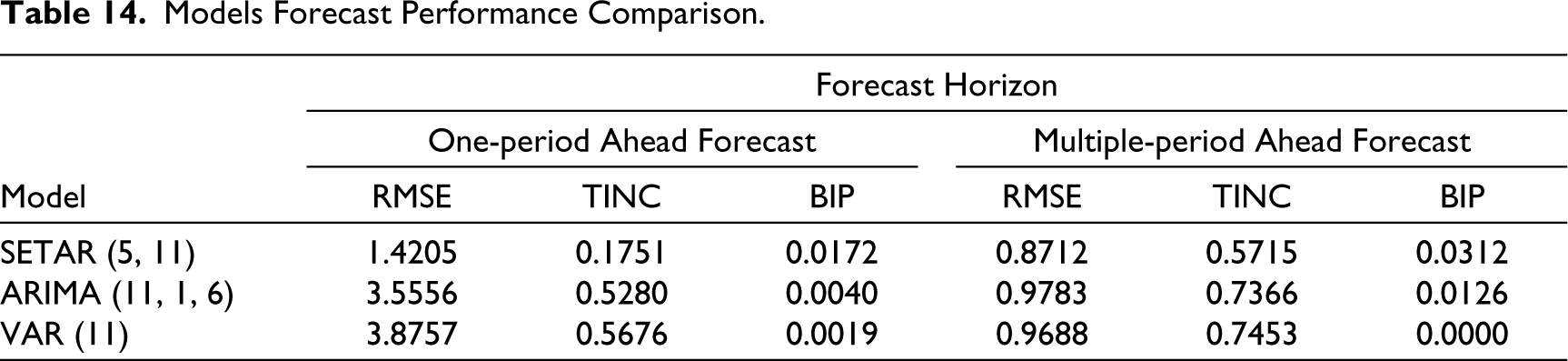

According to the RMSEs and the Theil inequality coefficients, forecasting with the non-linear SETAR model returns better predictions of the actual values in both the single-period ahead forecasts and the multiple-period ahead forecasts, while the ARIMA model produces better superior predictions among the linear models over a shorter horizon. These statistics are shown in Table 14.

Models Forecast Performance Comparison.

Advanced Forecast Evaluation Measures

Having analysed the linear and non-linear models’ forecast measures using the traditional methods, we go a step further by determining whether this difference is significant or simply due to specification error. In this research, we used the DM test statistic to check the comparison made between the forecasts of the linear and non-linear models. We also used the PT test to determine whether the models’ forecasts are accurate in predicting changes in the direction of the exchange rates. According to Ince and Molodtsova (2017), Haggan et al. (1984) and Aïssa and Jouini (2003), the latter approach is vital because of hyper-inflation, high-interest rates, political instability and growing external exposures which often cause a sudden change in the direction of the exchange rates in developing countries. Also, for market participants whose sole aim is to maximize gains and reduce losses in the foreign exchange market, knowing the direction of the change is significant to decide whether to buy (take a long position) or sell (take a short position) in the market.

The DM test makes use of the differential loss function (d) of two forecasts residuals, that is, e1t and e2t. The DM test is

where

For h ≥ 1, define the Diebold–Mariano statistic as follows:

The hypotheses test of the Diebold–Mariano test statistics is H0: E(dt) = 0, that is, the two forecasts have the same accuracy; H1: E(dt) ≠ 0, that is, the two forecasts have different levels of accuracy.

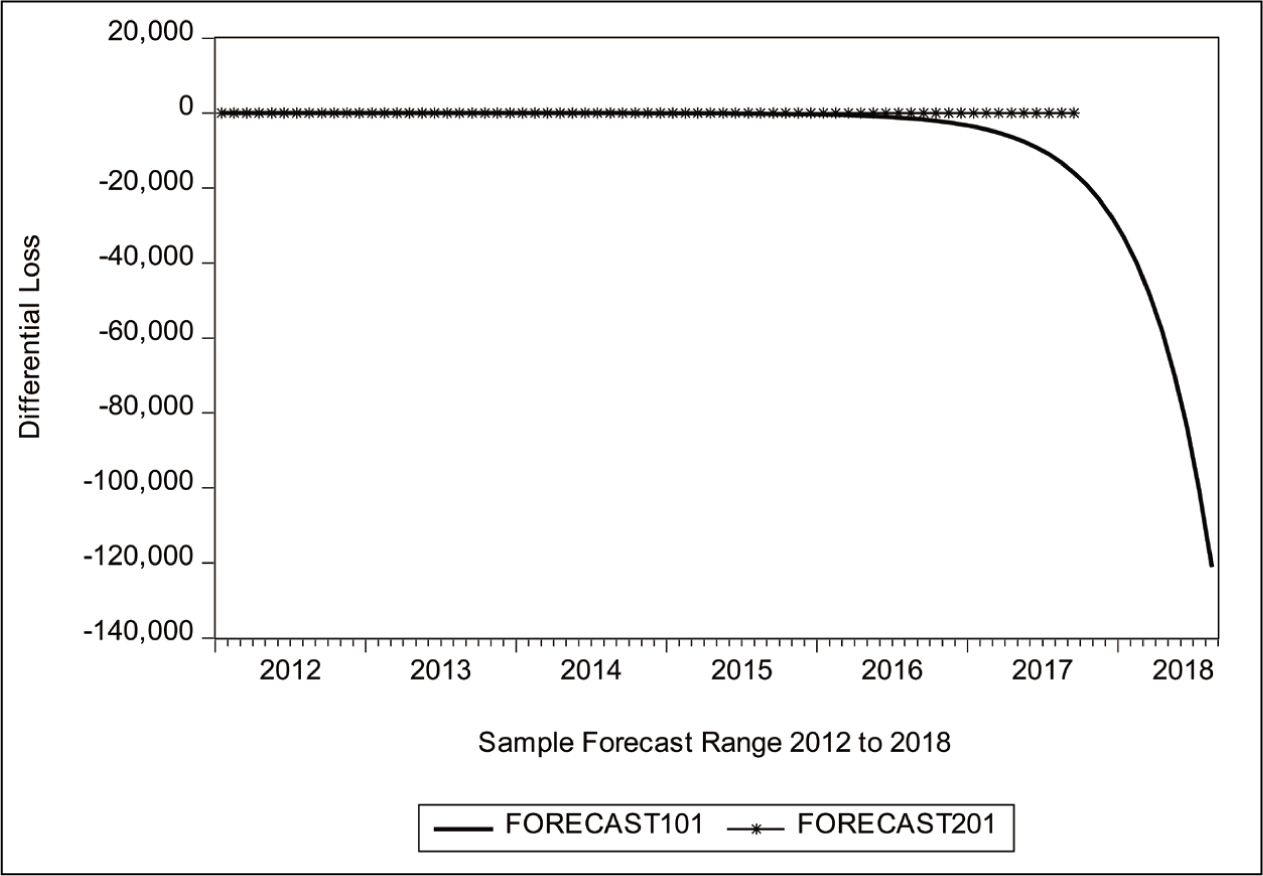

Table 15 and Figures 11 and 12 show the linear and non-linear models’ DM test statistics in both one-step and multiple-step forecast horizons. Note here that the VAR model represents the linear model because it has a better prediction than the ARIMA model. Therefore, the actual comparison of the models is between the VAR model and the SETAR model. The DM test statistics return a significant p value in the one-period ahead forecast horizon, implying that the differences between the models are significant and merit attention in a one-period ahead forecast horizon. For the directional forecasting accuracy, Pesaran and Timmermann (1992) used a non-parametric test to examine the effectiveness of a forecast to predict the direction of a change in a series of interest. This approach computes the proportion of the forecast values with the same sign as the actual series data. Assume we denote the series of interest as yt and its forecasts are xt, the PT test is defined as

DM Test Statistics.

DM Test Statistic One-step Ahead Forecast Graph of the Linear and Non-linear Model.

DM Test Statistic Multiple-period Ahead Forecast Graph of the Linear and Non-linear Models.

where

Under the null hypothesis of xt not been able to predict yt. Note that Sn also follows the standard normal distribution. Table 16 shows the PT test statistics for the various models.

Directional Forecasting: Pesaran-Timmermann Test.

Results and Discussions

The models’ forecast evaluation measures return lower comparative RMSE and Theil inequality coefficient values for the non-linear SETAR model for both the one-period ahead forecast and the multiple-period ahead forecasts. These statistics imply that the non-linear SETAR model’s forecast values are closer and nearer to the actual exchange rate values than the comparable linear models. This finding confirms the findings in Granger and Andersen (1978), Maravall (1983), Tong (1983) and Tsay (1991). However, the comparison between the linear models, that is, the ARIMA and VAR model, reveals some slight advantage of the ARIMA model over the VAR model in a one-period ahead forecast, but the VAR model also has the advantage in a multi-period ahead forecast.

The research on comparing the forecast accuracy of econometric forecasting models has now gone beyond the mere comparison of forecast evaluation measures. Recent empirical works now move the comparison a little higher to comparing the statistical significance of these forecast evaluation measures. For this reason, we have computed the DM test statistics to improve the level of our comparison. The DM test statistics have found that the differences in the linear models’ forecast performance measures and the non-linear model is statistically significant. This result means that the predictions of the models are significantly different and merit attention by businesses in forecasting the cedi exchange rates in a one-period ahead forecast. However, the significance test was rejected in the multiple-period ahead forecasts, meaning the models do not perform differently in the long run.

For forecasting the directional movements of the cedi exchange rate, the PT test statistics have found that the non-linear SETAR model is superior for forecasting the exchange rate movements in one-period ahead forecasts. However, the VAR model produces a better prediction of the direction of change in the cedi exchange rate for a multiple-period ahead forecast despite it having a relatively higher mean square error than the non-linear model. This result confirms the assertion in Abbate and Marcellino (2014) that the linear models added with macroeconomic differentials have higher predictive likelihoods at long horizons and during periods of recession. Ince and Molodtsova (2017) and Engle and Hamilton (1990) highlight the relevance of testing the econometric models for directional accuracy, especially in developing nations characterized by high inflationary figures, high interest rates, political instability, and high external exposures, which often causes swift changes in the directional movement of the exchange rates. Also, for market agents who operate to profit from exchange rate movements, predicting the directional movement of the exchange rate is essential to reducing forex losses (Abdul-Rashid et al., 2022; Cook, 2014; Leitch & Tanner, 1991; Pesaran & Timmermann, 1992).

Conclusions

The SETAR model produces better forecasts in terms of relative magnitude and directional trends of the exchange rate in a one-period ahead forecast horizon. The SETAR model is also superior in multiple-period ahead horizon forecasts, but the precision is only in predicting the magnitude of the change (and not in predicting the direction of the change). For predicting the directional change in exchange rates, in multiple-period ahead horizon forecasts, the VAR model has a better precision of the volatilities in exchange rate. These conclusions have insight for business owners or businesses whose operations are affected by forex movements. For short-term business commitments or transactions such as raw material purchases, cash expenses or incomes, business owners should plan or predict exchange rate movements using the SETAR or a non-linear model. However, for long-term contractual obligations like futures and forward contracts, the VAR or a multivariate linear model should be used in planning the management of forex losses.

Also, businesses which are established to trade in the cedi forex market or on the larger capital market with cedi-denominated securities can benefit from these research conclusions to minimize losses in the capital market.

Bléjer et al. (2000), Lossifov and Loukoianova (2007), Salachas et al. (2017) and International Monetary Fund (2017) provide technical advice to independent policymakers to wrap up any process of successful implementation of monetary and fiscal policy framework by having reliable forecasts of target variables (in this case the exchange rates). This research, especially the aspect of the directional prediction of the exchange rate, will also help policymakers in adjusting the policy tools in efforts to stabilize the economy.

Recommendation for Future Research

Further research can consider a panel study of businesses in Ghana by analysing their financial statements and reporting the losses that these research conclusions could have helped save.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix A. Choice of Research Variable

According to BoG (2018), the nominal effective exchange rate (NEER) provides a much more comprehensive assessment of the cedi than any exchange rate series of key trading partners. However, this research intends to use Ghana’s exchange rate with one of its key trading partners, but this rate should also be a good proxy to the NEER. This approach is to enable us benefit from the analysis with single exchange rate data whiles at the same time not losing the benefits of the composite effect in the NEER.

This research has therefore used three strategies to select the exchange rate that can be a good proxy to the NEER in the analysis.

First, the research analyses the correlations of each key partner’s exchange rates with the NEER in ![]() .

.

The cedi-dollar exchange rates were found to have the highest correlation with the NEER, and can be a good proxy to the NEER with this strategy adopted.

Secondly, the research looked at the strategy of outliers, and again choosing the right exchange rates with the least outliers. The box plot of the various exchange rates series is shown below:

The cedi-dollar rates series were again found to have the least outliers and was again chosen by this strategy as the right proxy for the nominal effective exchange rates.

Therefore, concluding on the two strategies, the research has selected the cedi-dollar rates as the best proxy for the NEER series.