Abstract

This article analyzes the relationship between the shadow economy and tax evasion in order to verify if their dynamics are substantially identical or may present elements of differentiation, even though the two aforementioned phenomena appear (on the basis of certain statistical definitions) to overlap in terms of economic values. To this end, the article proceeds by providing a series of terminological definitions that are useful to properly classify these phenomena and then it lists the main methodologies used for their quantification. Although such methods and their strengths and weaknesses are well known in economic studies, it is useful to recall them in order to underline some questions connected with the development of a model aimed at describing the approach to the shadow economy and tax evasion from a microeconomic perspective. The first question is if the underground economy can exist in absence of tax evasion and, in that case, which are the factors that allow it. A related question is how is it possible from a microeconomic perspective to estimate in percentage the overall disadvantage (fiscal and non-fiscal) deriving from the total declaration of economic activities to public authorities compared to firms that work in the underground economy? On this matter, reference to case law and regulatory measures, performed in order to create an economic-juridical parallel on the shadow economy and tax evasion, has been made with regard to the Italian legal system, so as to fit the mathematical model as much as possible to observed facts.

Introduction: The Shadow Economy and Tax Evasion

The shadow economy can be defined as that part of the legal economy that escapes direct statistical observation because the public administration is not aware of both tax and social security contribution evasion and inobservance of employment regulations. In this regard, the classifications made at international level, with the System of National Accounts SNA93 (published by the United Nations and updated in 2008) and with the European System of Accounts ESA95 (adopted by European Union in line with the SNA93 and updated in 2010), are of fundamental importance even though for statistical purposes.

According to the two above-mentioned systems of national accounts, the set of economic activities, for which the statistical survey presents problems, is called ‘non-directly observed economy’. Within such macrocategory it is then possible to define:

‘underground’ (also called ‘hidden’ or ‘shadow’) economy, as legal production activities of goods and services voluntarily concealed from public administration in order to avoid tax payments and social security contributions and the observance of labour legislation; ‘illegal’ economy, as productive activities to which the legal system assigns a negative social value; these activities are not admitted by law and their commission involves the infliction of a criminal penalty or an administrative fine; ‘informal’ economy, as legal productive activities that are difficult to survey from a statistical point of view due to their particular structural characteristics; and ‘statistical underground’, as legal productive activities that are not surveyed due to the inefficiency of the statistical data collecting system.

In general, we could plainly assert that tax evasion is a peculiar component of the widest set of behaviours that constitute the shadow economy. Nevertheless, given the commonly accepted definition for statistical purposes of this magnitude, it is possible to consider that the underground economy—as a set of incomes or, however, taxable products concealed from taxation—tends to coincide with tax evasion and evasion in social security contribution. In this regard, a recent article by Buehn and Schneider (2016, p. 2) has cited the two following definitions of the underground economy:

the first being ‘those economic activities and the income derived from them that circumvent government regulation, taxation or observation’ and the second being ‘the shadow economy includes unreported income from the production of legal goods and services–either from monetary or barter transactions–and so includes all the economic activities that would generally be taxable were they reported to the tax authorities’.

1

In practice, the second definition states a sort of de facto overlapping—in terms of quantity—of the phenomena of the shadow economy and tax evasion. Having established that, it can be said that the underground economy—as a set of incomes or, however, taxable products concealed from taxation—coincides with tax evasion. With reference to this concept, it is necessary to make further technical and juridical considerations to understand the nature of tax evasion and, consequently, the complexity of the corresponding estimates. In fact, tax evasion can be defined as the violation of fiscal rules relating to each specific tax, in order to conceal, either entirely or partially, taxable facts or taxable amounts from tax administration so as to reduce the tax burden (Adinolfi et al., 2015, p. 517).

On a juridical level, the distinction between ‘tax evasion’ and ‘tax avoidance’ is important. Tax avoidance is a behaviour that does not violate tax laws, but which—being devoid of appreciable economic reasons—aims to circumvent the fiscal rules in order to obtain undue tax advantages. 2 Conversely, ‘tax compliance’ can be defined as the spontaneous fulfilment of tax obligations. Essentially, tax evasion is a phenomenon that has peculiar characteristics in relation to different types of tax revenue and, for this reason, it should be estimated in reference to each of them. For statistical purposes, however, it may be useful to consider tax evasion as a macro-phenomenon that requires a conceptual delimitation. To give a general legal definition of tax evasion that is useful to make an estimate of it on a national level, it is necessary to consider the constitutional foundation of the tax levy. In this regard, the Italian constitutional principle of ability to pay is relevant, according to which ‘All are required to contribute to public expenditure by reason of their ability to pay’ (Italian Constitution, Article 53). In its turn, such contribution to public expenditure must be seen as one of the imperative duties of political, economic and social solidarity which must be fulfilled according to Article 2 of the Italian Constitution.

Starting from these premises, as well as from other Italian constitutional principles, such as the one which states that the tax system shall be based on criteria of progressiveness (criteria that ascribe a wealth redistribution function to taxation), the Italian Constitutional Court defined tax evasion in each of its manifestations as the breach of the bond of minimal loyalty that binds citizens, thus leading towards the violation of the imperative duties of solidarity on which a civil coexistence based on the values of individual freedom and social justice is founded according to Article 2 of the Italian Constitution. Additional points of contact between the definition of the underground economy developed in the economic field and general legal concept of tax evasion can be found in the Italian constitutional jurisprudence (where social security and health contribution is equated to tax levy) and in the fact that the income tax bases may coincide, tendentially, with those concerning the determination of contributions for social security.

Thus, broadly, tax evasion can be considered as one or more conducts of taxpayers aimed to reduce the due tax burden on the basis of the fiscal system. On the matter, the official statistics tend to normally indicate the amount of taxes assessed or collected without drawing a distinction between the different objections addressed to taxpayers.

Methods to Estimate the Size of Tax Evasion

Performing a precise and reliable estimate of tax evasion is a very complex task because it requires assigning a measurement as accurate as possible to a phenomenon that, by its own nature, tends to avoid any forms of survey or observation. Nevertheless, different estimating methods have been developed over time, although they present specific limitations that could affect their accuracy. In this regard, the first distinction can be made between direct and indirect methods. 3

Direct estimation methods have a microeconomic nature and may include: (i) anonymous questionnaires for individuals and businesses and (ii) analysis of the results of tax assessments and social security contribution audits conducted by tax authorities and other public bodies in charge of performing inspections. Indirect estimation methods aim at obtaining an aggregate value of the phenomenon using available statistical and administrative sources. These are essentially empirical methods. The increased availability and improved quality of statistical data compared to the past, together with the refinement of estimation methods, have led to a strong focus on these procedures, which proceed to the quantification of the magnitude based on economic variables which are available thanks to periodic surveys or administrative records collected. Finally, in order to make estimates on the shadow economy and tax evasion, these procedures can also be combined, giving rise to mixed methods.

The direct methods and the main indirect methods are briefly described hereafter.

The method based on sample surveys is a direct method. Its estimates are the result of the sample surveys that may be carried out on businesses, families, individuals, etc. Its main advantage is that it allows to break down the different categories of unreported incomes in detail and also to quantify unpaid taxes. Despite this merit, the method presents some critical issues in terms of reliability. In fact, estimates may be utterly marred by reluctance of respondents or by the selection of inadequate or unrepresentative statistical samples.

The method based on tax assessments is a direct method that reconstructs the volume of tax evasion starting from a comparison between declared fiscal data and data resulting from fiscal assessments on a sample basis. In addition to unreported taxable bases, this approach allows estimating unpaid taxes. Although the method in question is theoretically valid, it is necessary to take into account the possibility it may lead to unreliable results, given that: (i) at first, taxpayers subjected to control can be unproperly selected and, thus, the results of the subsequent process of taxation are really insignificant; (ii) the sample of notices of tax assessment (on which the estimates will be operated) can be selected in a wrong way and, in this case, the information will not be representative; and (iii) after the statistical survey, fiscal assessment may be followed by a contentious phase which can modify the elements taken into account to estimate fiscal evasion.

Methods based on monetary indicators (also known as currency demand approach) lead to an indirect estimate of the shadow economy, through the reconstruction of real economy on the basis of the extent of currency in circulation. These methods are based on the assumption that irregular transactions generally take place under cash payments; therefore, the dynamics of the underground economy should be monitored based on the demand for currency. In addition, the actual size of the real economy should emerge on the basis of the quantity of currency.

In practice, tax evasion could be estimated by measuring the gap between the GDP and the total value of monetary transactions. This procedure is often bound by a set of basic assumptions, which means: (i) the amount of currency attributable to tax evasion can be determined as the difference between the demand for cash, which is estimated on all the explanatory variables, and the simulated one which is obtained considering the cause variable (i.e., the tax levy, without which there would be no tax evasion) as equal to zero or to its historical minimum in the reference time period; (ii) tax evasion essentially takes place with cash transactions; and (iii) the velocity of currency circulation is the same both in official and underground economy.

Even though the demand for currency can be a valid indicator of overall real economy (and, thus, also of non-directly observed economy), it is possible to formulate some doubts about the ability of this approach to measure tax evasion. In particular, the method is based on a set of assumptions that may also deviate from reality: for instance, it is not necessarily true that unlawful or undue reduction of the tax levy is always performed through cash transactions; if this can be considered true for the so-called ‘widespread fiscal micro-evasion’, these types of transactions are more unlikely in the case of big tax evaders, given the frequency with which tax fraud or tax avoidance phenomena occur. Moreover, the demand for currency is certainly strongly influenced not only by tax evasion, but also by illegal economy, which is a distinct phenomenon from tax evasion.

The national accounting method is based on macroeconomic analysis aimed at comparing the total amount of reported taxable incomes with an estimate of potential ones which are calculated thanks to national accounting aggregates (i.e., production, value added, etc.). To fully understand the potential of this method, it must be noted that the shadow economy must necessarily be included in the national accounts. Data collected from businesses represent the observed economy, while the national accounts data contain an integration due to the underground economy. However, the comparison can only be performed in relation to tax bases (and not in relation to taxes). The national accounting method is certainly one of the most reliable and, therefore, considerably widespread. Nevertheless, it presents some critical issues due to the impossibility of estimating—inter alia—the loss in tax revenue following tax evasion and the serious difficulty connected to the disaggregation of the estimates beyond the broad categories of income (e.g., income from employment, self-employment income, business income).

The ‘total income

Another important indirect method is the so-called ‘model approach’, which is aimed at creating a structural econometric model in which the underground economy (or tax evasion) is considered as a latent variable, that is, an unobservable theoretical construct that is linked to a set of observable indicators that reflect its changes, and to a series of observable variables that are considered the cause of the phenomenon to be measured. With this method, we also refer to multiple-indicators multiple-causes (MIMIC) or dynamic multiple-indicators multiple-causes (DYMIMIC) procedures. Unlike other methods, this approach provides a model of factorial analysis that does not discriminate a priori between causes and indicators. The procedure in question is very complex and shows a serious weakness because it is characterized by a discretionary interpretation of the identified factors and the way they interact. Thus, potentially, the model approach may give rise to non-univocal estimates.

A Possible Equation on the Shadow Economy

After this brief description of the concepts of the shadow economy and tax evasion, now it is necessary to examine them from a microeconomic perspective. The purpose is to build a mathematical model aimed at measuring the potential economic advantages deriving from being part of the hidden economy and, then, at trying to describe an individual approach to the shadow economy and, in particular, to tax evasion.

The discussion on the underground economy and its estimation methods reveals that sometimes, on the base of certain statistical definitions, the size of the shadow economy and tax evasion (in terms of not reported taxable bases) could overlap. This possibility stimulates some questions and, in particular, if the underground economy and tax evasion coincide from a quantitative point of view, can the shadow economy exist in the case of absence of tax evasion? And in this case, which are the factors that make it possible?

Tax evasion has been the subject of study in economics. In literature, several factors are considered its causes, among which, undoubtedly, there are: (i) high pressure of taxation and social security contribution (it is understood that the higher the tax evasion, the higher the tax burden only for the taxpayers who fulfil their fiscal obligations); (ii) diffusion and regularity of institutional controls, since the lower the probability of being subjected to a fiscal audit, the greater the propensity to escape taxation; (iii) complexity of tax legislation and fiscal fulfilments required to taxpayers; (iv) expectation of tax amnesties, which increases the propensity to evade taxes in view of a future fiscal amnesty; (v) structure of the economic system, as its fiscal control is more difficult to apply in case of ‘informal’ or ‘volatile’ activities; and (vi) cultural attitude of taxpayers, given that tax compliance of citizens will be higher if tax evasion is diffusely felt as a negative social issue; however, it is necessary to point out how this cultural attitude is greatly influenced by the perception of the efficiency (or inefficiency) of the public services which are supplied thanks to the tax levy.

On this matter, it is worth mentioning a decidedly significant model created by Allingham and Sandmo (1972) and, then, developed by Bernardi and Franzoni (2004). 4 In practice, tax evasion is seen as a portfolio choice that is based on the following assumptions: (i) a taxpayer acts rationally and selfishly in order to maximize—under uncertainty—his utility and shows a certain degree of aversion to the risk of being discovered and punished; (ii) a taxpayer knows his actual income Y, unknown to tax authorities, of which he declares only part Yd = Y – Ye (where Ye is the tax evasion); (iii) there is a simple proportional tax on income, with a constant rate t that is applied to the reported income Yd = Y – Ye; (iv) a taxpayer knows the probability p [0,1] that the income tax return can be assessed and, simultaneously, that tax authorities can apply an administrative fine proportional to the evaded tax according to factor m; and (v) d is the taxpayer’s discomfort related to the interference of the fiscal investigation into his business.

Given these circumstances, a taxpayer decides the amount of tax evasion that maximizes his expected utility. In practice, without tax assessment, tax evasion is a benefit, while in the case of a fiscal audit, it causes a loss. The expected utility will be given, therefore, by the combination of assessed income and non-assessed income, according to the following function:

If there is no tax assessment, the net income will be equal to the total income Y minus the tax on the reported income tYd. In case of tax assessment, the net income will also be reduced by the payment of the evaded tax tYe and the fine mtYe and by the cost of discomfort d. Now, coming back to the possibility of existence of the shadow economy in absence of tax evasion, it should be noted that the aforementioned theory explains tax evasion from an essentially economic perspective and, on that level, shows that, on one hand, it is determined by the will to achieve savings on due taxes and, on the other hand, that the phenomenon is reduced according to the likelihood of a fiscal audit.

In this perspective, tax evasion and the underground economy, as magnitudes, seem to have a single logic of functioning. Nevertheless, in reality, tax evasion cannot be described as a mere economic phenomenon, but rather as an economic-juridical one. According to this perspective, it is worth analyzing the relationship between the dynamics of the shadow economy and tax evasion. In this context, it is evident that if taxpayers and, in general, citizens did their best for a total emersion of economy, there would not even be tax evasion, because each tax base would be reported. Perhaps the opposite would not occur if tax evasion ceased, and this would be due to the dual juridical and economic nature of the considered phenomenon.

In fact, supposing all tax rates were set at zero by law (thus t = 0 in the aforementioned equation), tax sanctions would have no reason to exist (mtYe) as well as tax evasion because of the absence of its legal requirement. 5 Nevertheless, the underground economy may still subsist since it allows to obtain—in any case—further economic utilities. For example, the shadow economy may have its own logic in the violation of labour legislation or regulations on the safety of products or, again, in the violation of the rules regarding the protection of trademarks. In these cases, in fact, being part of the underground economy determines more competitive prices and, then, greater profits to the detriment of other competitors in the market.

This concept may be represented by an equation aimed at expressing, in percentage, the overall disadvantage (or the overall missed advantage) deriving from the total declaration to public authorities of economic activities compared to those firms that work in the underground economy. However, the construction of such a model involves the overcoming of some difficulties. First of all, in order to be as close as possible to a real situation, it is necessary to individuate a single economic magnitude on which, in a first time, the overall incidence of the aforementioned competitive disadvantage (CD) and, in a second time, the overall tax burden have to be calculated (the tax burden is given by different forms of taxation that hit taxable bases often different from income). Moreover, there must be found a way to isolate the economic incidence of legal prescriptions in non-fiscal fields.

In this regard, it is necessary to consider the total wealth that an economic operator (which is identified as an enterprise in the first part of this section) can produce not only without any kind of tax levy (given that tax rate ‘t’ is assumed equal to zero), but also at gross of all sort of contractions resulting from non-fiscal normative constraints related to the regulation of markets and production activities. From a certain point of view, isolating the impact of the legal factor may seem impossible with regard to the economic cost of each individual normative prescription. But an easier way to achieve this result may consist in hypothesizing the zero setting or the inexistence of the sanctions provided by the legislation now in question. In fact, if normative prescriptions remained in force but were not associated with sanctioning rules, de facto the economic operators would be free to carry out their businesses with the only limit of maximum profitability; thus, the well-known maxim ‘laissez faire, laissez passer’ would be practically implemented’. In this perspective, the shadow economy would have reason to exist not for escaping public sanctionary activities (which are supposed inexistent), but rather for avoiding civil suits due to commercial or industrial practices qualified—in any case—as unfair.

Once the maximum producible wealth is assumed in the hypothesis of absence of non-fiscal sanctioning rules, we could use this magnitude to evaluate the potential economic advantages deriving from the concealment of economic activities taking into account the real existing non-fiscal sanctions. Thus, in order to evaluate the hypothetical convenience of being part of the underground economy (in absence of taxation, but in presence of non-fiscal sanctions related to the market regulation), the overall wealth that can be produced and accumulated by the economic operators (where they were left free to pursue only the maximum profit) should be taken as base theoretical magnitude. It may be defined as the difference between the net assets remaining at the end of a given time period and the net assets held at the beginning of such a period. In this regard, the definition of income used in business economics (and, among other things, diffusely accepted) may be relevant. According to this definition, the produced income is considered as the increase or decrease of a firm’s net assets that takes place during a business year, due to business management.

Hence we have that:

∆

In this regard, only the positions of economic operators that, potentially, are able to produce and accumulate wealth can be considered relevant (i.e., it is assumed that ∆NA is a positive quantity). In fact, this magnitude, as conceived, expresses the maximum patrimonial growth that can be attained by an economic operator, taking into account that this one might also not comply with the rules. In practice, ∆NA is suitable to intercept also those situations in which the fulfilment of legal obligations determines, in a given business year, a decrease of net assets or an increase equal to 0, but which are able to lead to a patrimonial increase by exploiting unfair competitive advantages and without taxation. Therefore, the economic operators in deficit are excluded from the hypothesized model. However, in the medium/long term, they would probably come out of the market or, in any case, would be forced to ‘emerge’ before the public administration for civil suits due to indebtedness.

Having said this, it is possible to assume that, also in the absence of taxation (and, therefore, in the impossibility of evading or avoiding taxes), there are still some economic advantages in concealing the production of wealth. If we indicate with ‘CD’ the competitive disadvantage that an enterprise declaring its economic activities expects to sustain in comparison with another one that operates in the shadow economy, we will have:

Briefly, the competitive disadvantage derives from the following variables:

co, that is, a pecuniary value given by the organizational cost sustained for the accounting of the economic activities and their communication to the public authorities, which has a negative influence on the propensity for being part of the official economy; mac, that is, a pecuniary cost given by the missed advantage in terms of competitiveness, given that the declaration to the public administration of all economic activities carried out does not allow to make use of supplies which violate the regulations on the safety of products, to practise wages policies that do not respect labour legislation, to avoid expensive organizational procedures in the sector of workplace safety or, again, to realize industrial and commercial practices that violate the rules on the protection of trademarks, etc.; this variable is given by the sum of the costs sustained in the application of the cited normative prescriptions and has a negative influence on the propensity for being part of the official economy; NFS, that is, the pecuniary value given by the non-fiscal sanctions that the legislation provides for behaviours to which the legal system assigns a negative social value; p1

The equation has the following condition:

CD cannot be:

higher than the producible and accumulative wealth, at most it can be equal to DNA; negative, if we assume that the economic operator acts rationally, the same will not have any interest in concealing the economic activities, where—in the presence of a serious sanctionary system—there is such a high probability of a control to make the overall burden resulting from application of non-fiscal sanctions higher than the achieved competitive advantage.

6

Then, it would not make any sense to consider negative values of CD, as we would refer to cases in which the shadow economy could not exist, as it would determine an economic loss (i.e., the contraction of the wealth that can be accumulated) rather than an advantage. Therefore, given the assumed rationality of the economic operator, being subjected almost certainly to sanctions that frustrate the aforementioned potential competitive advantages does not fall within its business decisions.

Essentially, the propensity to be part of the official economy, even without taxation, is strongly influenced by the existence of potential economic advantages resulting from the concealment of economic activities. In particular, in percentage on the potential wealth that can be accumulated, the expected total competitive disadvantage (ETCD), 7 deriving from being part of the official economy, can be expressed by the following equation:

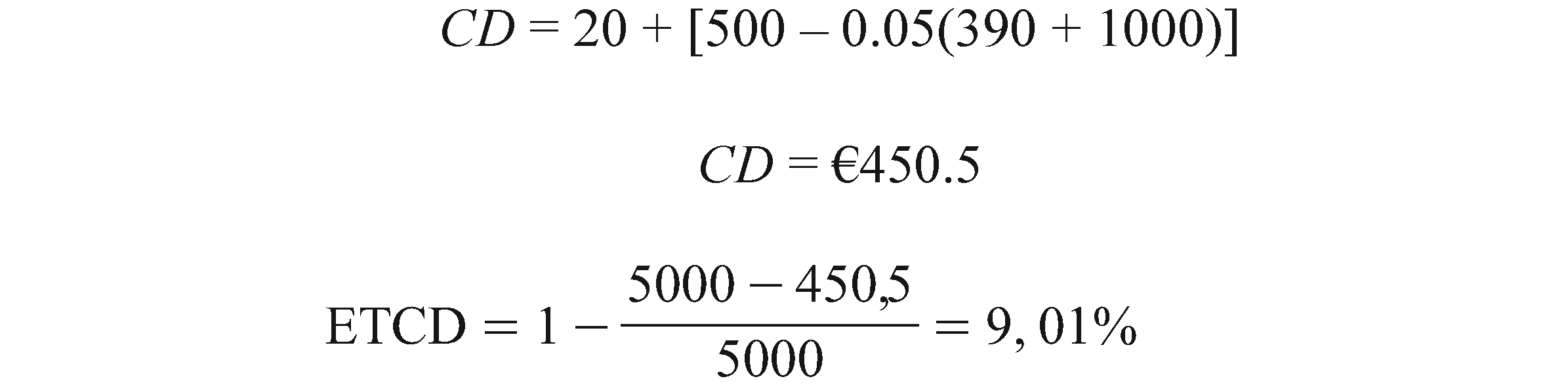

For example, let us consider the case of an enterprise that, in order to make a profit through the payment of lower wages compared to those provided by the trade-union bargaining and the cost-cutting related to the organizational procedures pertaining the workplace safety, conceals its activities from public authorities. In this regard, we assume that:

∆ co: €20. mac: €500 (€300 given by the cost necessary to conform the wages to those provided by the trade-union bargaining and €200 given by the cost necessary to respect the workplace safety rules). NFS

NFS

p

In practice:

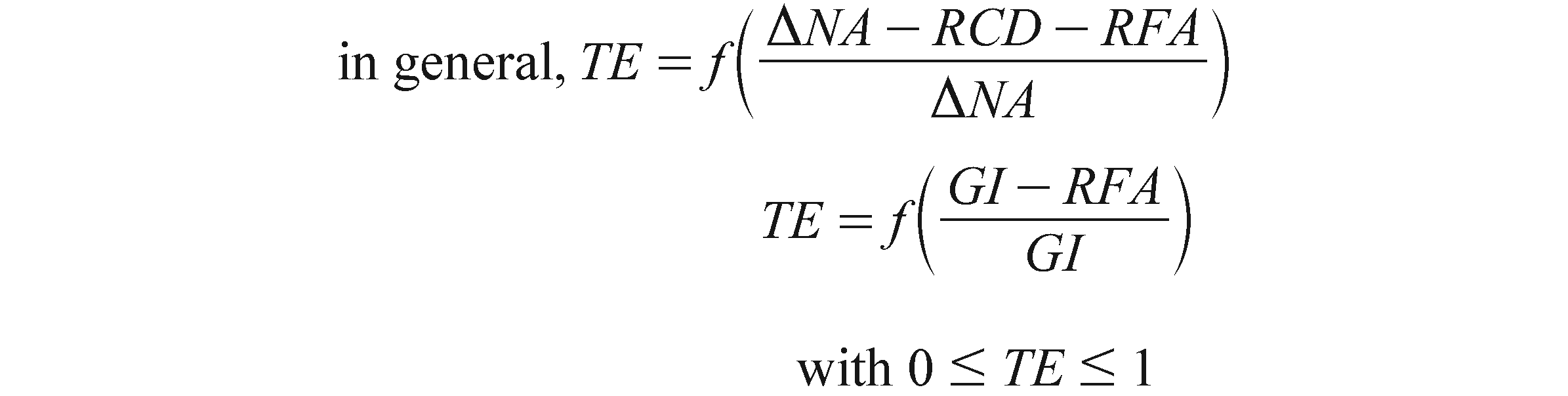

Moreover, it is possible to determine a further indicator that we can conventionally call ‘TE’ (tendency to emersion), which directly depends on the ratio between the potential wealth net of CD and the same full potential wealth. On the base of the specific economic activities carried out by a determined economic operator, the ratio in question tends to measure—in percentage—how much potential wealth that can be produced in the shadow economy is not affected by unfair competitive advantages. So that, ‘TE’ will express a higher propension to become part of the official economy (in other words, a higher propension to comply with rules) as the ratio gets closer and closer to 1:

Obviously, we have that 0 ≤ TE ≤ 1, because the tendency to emerge may not exceed the 100 per cent of the producible wealth (i.e., 1), nor to be less than the 0 per cent (i.e., 0) in the case of total concealment of economic activities.

Conclusively, since the shadow economy can exist also in the hypothetical case of absence of taxation, it is possible to say that the underground economy, even if it coincides—in absolute values—with tax evasion, has autonomous dynamics in respect to the latter.

A potential example of this logic of functioning might be found in the so-called ‘ten-year Imposta sul Reddito delle Persone Giuridiche (IRPEG) (corporate income tax) exemption’, which was provided, several years ago, for businesses that opened production plants in Southern Italy (according to Italian law 64/1986). In fact, the income tax exemption did not exclude the economic advantage of tax evasion in relation to the payment of VAT, because the concealment of tax bases, even if totally irrelevant for income tax (given the IRPEG exemption), was still able to give rise to an unlawful saving of VAT on not reported taxable transactions.

If the shadow economy is possible in the hypothetical absence of taxation, then it is needful to consider what role tax levy plays in the real case in which the wealth produced is subjected to one or more forms of taxation. Previously, it has been assumed that if an enterprise declares its economic activities to the public authorities, even in absence of taxation it is possible to identify a competitive disadvantage (CD) due to certain variables. Adding the element of tax levy, it is necessary to consider further variables that affect the taxpayer’s tendency to become part of the official economy. However, before trying to integrate the preceding equations, it is indispensable to formulate some specifications of methodology.

In the equation of Allingham and Sandmo, as developed by Bernardi and Franzoni, only one form of levy on income Y is hypothesized, with a proportional tax rate t, and only one type of sanction proportional to tax evasion m. Nevertheless, the fiscal legislation normally provides different forms of tax levy that—depending on the rules on taxable bases and tax rates—will be able to assume alternately a regressive, proportional or progressive connotation.

With the intent to hypothesize a mathematical model that expresses this situation, first of all, we have to define the economic magnitude on which taxes will burden all in all and concretely. In this case as well, it is relevant the wealth produced by the taxpayer that can be accumulated, which is given by the increase of net assets at gross of all taxes that must be paid in a specific tax period. In fact, if in a given business year a taxpayer was exempted from any form of tax levy, the sum of net taxes (payable under conditions of normal taxation) would increase the accumulative wealth at the end of the considered time period.

The economic magnitude that has to be taken into account is, once again, the produced and accumulative wealth, which is expressed by the changes of net assets between the end and the start of the business year matching the aforementioned specifications.

Taxation, in all its forms, will reduce—for an amount equal to the overall tax burden—the wealth that the taxpayer can potentially accumulate at the end of the business year. In this regard, the overall tax burden can be calculated with reference to a given taxpayer on the base of certain specific conditions. First, a normal fiscal system provides various forms of taxation. Then, tax rates and tax bases are extremely different and depend on each specific tax structure. It is impossible to relate all taxes to the income; however, it is possible to calculate the overall incidence of the tax burden on the wealth that can be accumulated by the taxpayer at the end of the year. Therefore, by adding the amount of all taxes to the wealth that has been produced and accumulated in a given year, we obtain the wealth that would have been theoretically accumulated in absence of taxation, that is, DNA. However, this result requires to relate the different forms of taxation, that normally provide various proportional or progressive tax rates, to a single type of structure. This aim involves the consideration, for each specific form of taxation, of the following variables:

Consequently:

With reference to a given period and in relation to each specific form of taxation, the overall due net tax will be equal to:

Thus, if we wanted to determine the taxpayer’s overall tax burden in a given tax year, we should consider the following summation:

However, a consideration of legal character on the overall tax burden has to be made, given that this article aims at examining the possible influences that the legal system can exercise on the choices of individual economic operators. In a legislation that is inspired to the protection of citizens’ rights and economic development, the overall tax levy can never be higher than the total wealth that can be produced and accumulated. Economic and legal considerations support this statement.

On an economic level, if a productive activity was subjected to a tax burden higher than the produced wealth, it would determine the end of the business in question or, if possible, its transfer abroad, without counting the boost in tax evasion and tax avoidance. Based on these considerations, the legislator should feel inhibited to impose such a high tax burden which would generate similar consequences.

On a juridical level, however, such a possibility must be considered precluded because in any democracy, although the pressure of taxation can be high, the fundamental legal principles tend to safeguard the freedom and the affluence of citizens and, more specifically, the freedom of enterprise. The best example is given, perhaps, by the Italian legal system, where, in spite of a very high pressure of taxation, it can be certainly excluded that the overall tax burden exceeds the produced wealth, because this situation is prevented by specific constitutional provisions, which have a higher level than the tax laws in the hierarchy of the legal rules.

Let us consider, in this regard, the constitutional principle of ability to pay, according to which, for constant jurisprudence of the Italian Constitutional Court, the taxable facts shall consist in direct or indirect demonstrations of wealth which can be selected by the legislator with the limit of non-arbitrariness. Moreover, there is a limit in the size of the tax levy which must be compared with the taxpayers’ possibility of depriving themselves of part of their assets to finance the public expenditure once they have satisfied their basic needs. Thus, the overall tax burden cannot exceed the wealth that is produced by an economic operator and, therefore, the following condition can be considered a juridically (and economically) well-founded hypothesis:

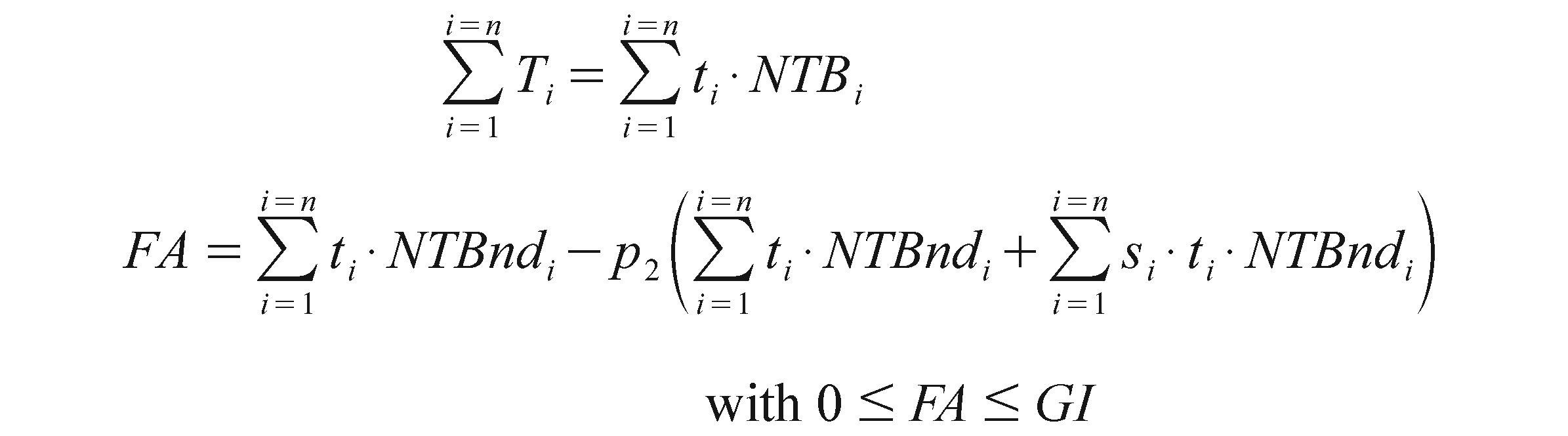

Hence, in the case of tax evasion, the expected overall fiscal advantage (FA)—that the dishonest taxpayer can achieve compared to those who regularly fulfil their tax obligations—may be expressed, taking into account the non-declared net tax bases (NTBnd), by the following equation:

FA derives from the following variables:

The equation aimed at determining FA has the following condition:

FA cannot be:

negative, as if it is assumed that the taxpayer acts rationally, the same will not have any interest in evading taxes in presence of such a high probability (p2) of a fiscal audit to make the consequent overall payment of the taxes plus the fiscal fines higher than the unlawful fiscal saving achieved at the beginning; hence, it would not make sense to take into consideration negative values of FA, as it would refer to cases in which—due to the taxpayer’s choice—tax evasion could not exist as it would determine an economic loss rather than a fiscal advantage, thanks to the probable subjection to tax assessment and to the infliction of fiscal fines; higher than ∆NA, because at most FA can be equal to the overall tax burden, which, in turn and for the abovementioned reasons, cannot be higher than the produced and accumulative wealth:

Given the above outlined hypotheses, we might represent an equation aimed at expressing, in percentage on the potential wealth that can be accumulated, the expected total competitive disadvantage deriving from not being part of the shadow economy and the expected missed fiscal advantage deriving from paying taxes regularly (ETCFD) in the following way:

Although in theory, in particular circumstances, the combined individual values of CD and FA might even exceed ∆NA, the above-mentioned condition appears to be appropriately imposed, because, even if DNA < CD + FA, the final value of ETCFD will be equal to 1. Instead, in case of CD and FA both equal to 0, the value of ETCFD will be equal to 0.

Also in this case, the indicator ‘TE’ depends on the ratio between the potential wealth affected by CD and FA and the same full potential wealth:

As above, the more the ratio is close to 1, the lower the overall size of the competitive disadvantage and the missed fiscal advantage resulting from the observance of all the regulations in force. It is clear that values of the ratio close to one underline the presence of efficient non-fiscal market regulations and incisive tax evasion law enforcement strategies that make tendentially fruitless the unfair advantages resulting from being part of the shadow economy and evading taxes.

Determining the advantages due to concealment of economic activities by individuals that carry out self-employment activities (without the contribution of specific organizational structures) or subordinate employment deserves some slightly different considerations compared to those that have been set out so far in relation to enterprises. 9 By making use of a non-basic organizational structure, broadly speaking comparable to a firm, 10 it is possible to allocate the produced wealth just on the same structure that might be considered, de facto, as a sort of distinct entity from the ultimate beneficiaries of the income. This consideration allows to define the overall produced and cumulative wealth as the ∆NA of an enterprise. Then, this patrimonial increase, which constitutes income in a company-oriented perspective, will be distributed at the end of the year of reference or, on the contrary, will be paid as advances or withdrawals during the same year. In any case, the competitive disadvantage (CD) and the missed fiscal advantage (FA) can be compared with the ∆NA of the enterprise.

But, the same conclusions cannot be formulated with reference to the wealth produced by subordinate employment and self-employment carried out substantially by individuals. As a matter of fact, if part of the produced wealth is consumed during the year in order to satisfy the worker and his family’s needs—as normal—at the end of the considered period it will not be possible to calculate the incidence of CD and FA on the patrimonial increase, because this one might not exist or only coincide with a part of the personal income. Consequently, as far as subordinate employment and self-employment are concerned, the overall wealth produced in a given year must not be compared with a patrimonial increase, but with the total gross income received (GI), which will necessarily have a positive relative value because it consists in the salary received that can not be negative or equal to 0.

In this regard, it is difficult to recognize hypotheses of competitive disadvantages with reference to incomes deriving from self-employment activities and subordinate employment carried out by individuals. Therefore, in this case, the fiscal advantage seems to be the only factor which is able to encourage the concealment of economic activities from public administration.

Thus, the following equations will also be relevant for these types of taxpayers:

So, we might express, in percentage on the total gross income received, the expected total fiscal disadvantage deriving from paying taxes regularly (ETFD) in the following way:

Workers’ tendency to emersion (TE) will be only influenced by the fiscal advantage deriving from the unreported tax bases and directly depends on the ratio between the total income net of FA and the total gross income received.

Also in this case the more the ratio is close to one, the higher the tendency to emersion (TE). Unlike what might happen in the case of enterprises (where CD is relevant), this ratio cannot assume negative values, given that:

The topic of the shadow economy (and tax evasion) has been approached so far only under the perspective of the economic advantages that can be attained through the concealment of the productive activities. Actually, personal choices are also guided by subjective, psychological or even ideological reasons, which can be foreseen with considerable difficulty. If, on the basis of the mere economic convenience, the probability of being subjected to a control for fiscal purposes or for other aims is the main deterrent that induces to pay taxes or, in any case, to observe the legal fulfilments, from a subjective point of view certainly there are at least two other determinant factors that must be considered, namely, (i) the perception of the ‘functionality to aims of solidarity and social character’ of compliance with the legislation applicable to the economic activities and (ii) the personal propensity or aversion towards risk, with reference to the probability (p) of being subjected to a control by the public administration.

Although the above-mentioned factors do not have an economic nature, they cannot be underestimated because such factors are able to affect the tendency to emersion (TE). In fact, it can not be excluded that, even if there is a considerable advantage in becoming part of the underground economy, the economic operator may be convinced of the importance of compliance with the rules because the observance of legal prescriptions determines, even indirectly, more guarantees for everyone in the rights protection. Moreover, with specific reference to the tax levy and the social security contribution, the compliance with the rules allows the state and other public bodies to supply important public services. Thus, the economic operator can decide to observe the legislation also in spite of a low risk of control. Vice versa, it may happen that the economic operator does not perceive the importance of compliance with the legal rules, maybe due to the lack of confidence in the quality of public services or in the fairness or efficiency of the public administration, and, thus, he might decide to become part of the shadow economy. Hence, it is possible to indicate with A the subjective propensity to observe the rules, which can be considered as a function of the personal perception of the quality and importance of the services provided by the public administration. It follows therefore that:

‘A’ will be equal to 0 in the worst case, that is, when the individual does not have any stimulus to emerge in the official economy, whereas, at most, it will be equal to 1 when the economic operator is intimately convinced of the usefulness and importance of a full emersion through the observance of the legal prescriptions. Instead, if we consider the personal propensity to risk, it is needful to identify an additional factor, that is ‘r’ (which is a corrective factor of p) that precisely expresses that propension. Therefore, we will have that 0 ≤ r ≤ p, because the absence of personal propensity to risk will assign to ‘r’ a value equal to 0 (and in this case, acting rationally, the economic operator will decide only on the mere probability of a control, without any ‘psychological’ interference), whereas the maximum propensity to risk can not be higher than p (i.e., the effective probability of a control) and will induce the economic operator not to be worried at all about such an eventuality. This approach leads to calculate the increase of CD and FA due to the propensity to risk.

The rectified competitive disadvantage (RCD) will be equal to:

The rectified value of the fiscal advantage (RFA) will be equal to:

The propensity to risk tends to increase the expected unfair advantages, because such a propension limits the perception or relevance of p. So, on the base of r, we might correct the equation that expresses ETCFD in the following way:

The equation, as before, is subjected to the following condition

For workers, we similarly have that:

Consequently, having regards to the psychological factors, first of all we will have that the individual tendency to ‘emersion’ will directly depend on the aforementioned ratios, so that:

In conclusion, considering also the subjective propensity to respect the rules (A), it is possible to say that the overall rate of emersion (RE) is given by the following equation:

RE is given by the tendency to emersion TE (corrected with the propensity to risk ‘r’) increased by a percentage ‘A’ (i.e. the subjective propensity to observe the legislation) of the rate of non-emersion (1 – TE).

Conclusions

This article hypothesizes some indicators that might be useful to analyze the shadow economy and tax evasion with reference to the motivations and advantages related to the choice of concealing the economic activities from the public authorities. First of all, it has been considered the maximum potential wealth that can be produced in the shadow economy, that is, the increase of net assets (‘∆NA’) for firms and the total gross income (‘GI’) for workers. This economic magnitude is suitable to be compared with the real costs arising from the compliance with non-fiscal market regulations and tax legislation. Then, the indicator called ‘tendency to emersion’ (‘TE’) has been conceived on the basis of this magnitude. In particular, the ‘tendency to emersion’ derives from the following ratios (where ‘CD’ stands for ‘competitive disadvantage’ and ‘FA’ stands for ‘missed fiscal advantage’):

The ‘tendency to emersion’ can be considered under an interdisciplinary (legal and economic) perspective. In fact, from an economic point of view, it may express the individual tendency to be part of the official economy, since the more the ratio is closer to one, the lower the overall disadvantage resulting from the observance of the rules. From a legal perspective, the ‘tendency to emersion’ may highlight the efficiency of the legislation in force, because ratios close to one underline efficient non-fiscal market regulations and incisive tax evasion law enforcement strategies.

Finally, in order to highlight the effort aimed at fitting the models as much as possible to reality, case law and regulatory measures of the Italian legal system have been taken into account. However, it is possible that the proposed equations are valid also for the legal system of other countries. In fact, given that what distinguishes one unobserved economy from another is the particular rule being violated (Feige, 2016a), the proposed models try to capture the different kinds of concealed economic activities that combine to determine the underground economy, since the ‘competitive disadvantage’ considers the violations of non-fiscal market regulations, while the ‘missed fiscal advantage’ attempts to express the economic advantage arising from the violation of tax rules. 11