Abstract

Neoliberalism and financialization are not synonymous developments. Financialized nations are directed by particularly financialized epistemologies, cultures, and practices, not only neoliberal ones. In examining the financialization of the UK economy since the mid-1970s, this study discovers a socio-economic shift beyond the broad transition from Keynesianism towards free-market fundamentalism. Economic developments were guided by the very particular economic paradigms, discursive practices, and financial devices of the City of London, as financial elites became influential in the Thatcher governments. Five epistemological elements specific to finance are discussed: the creation of money in financial markets, the transactional focus of finance, the centrality of financial markets to economic management, the orthodoxy of shareholder value, and the intensely micro-economic approach to financial calculation. Identifying these distinctions creates new possibilities for understanding financialization, elites, and the neoliberal condition that brought about both the financial crash of 2007–8 and the political and economic crises that have followed.

This article contributes a new perspective on how ‘financialization’ and ‘neoliberalism’, though related, are different. As concepts they appear very complementary, a pair of socio-economic phenomena that can seem almost interchangeable. Both terms can be found across multiple academic disciplines in critical accounts of contemporary capitalism. Financialization is the lesser-employed of the two. Neoliberalism is both the older by several decades and of more widespread interest to politics. But the financial crash of 2007–8 and the political and economic repercussions that have followed have piqued interest in financialization. In part, this is because of the pressing need to think clearly about how finance influences public policies, so many of which have been termed ‘neoliberal’. However, as this piece argues, while the two have their correlatives, they also have significant differences. These are structural-economic but also, as highlighted here, cultural and epistemological. Drawing on evidence gathered from the nexus of UK political and financial elites, this article offers an exploration of these differences, thus clarifying the distinctions between the two concepts.

What are the epistemological and cultural foundations of financialization, and how do these foundations distinguish it from neoliberalism? This article identifies five important areas of difference in the way financial actors think and behave in relation to ‘the economic’: the creation of money in financial markets, the transactional basis of finance, the centrality of financial markets to economies, the orthodoxy of shareholder value, and the intense microeconomic focus of investors. Each of these creates a microclimate for financialization in which cultures, epistemology, and practices develop autonomously from neoliberalism. Such differences are further emphasized by the reliance of neoliberal theory upon a neoclassical economics that has never come to grips with the role of finance nor the growing primacy of financial markets to the exclusion of so much else.

Those states which have acted as path-breakers of financialization have done so, in part, because such financial elites and epistemologies have had a greater influence on state institutions. They have driven financialization’s expansion with its particular set of structural and economic characteristics. Beneath these contingent characteristics have lain specific cultural and epistemological foundations unique to financialization. These owe relatively little to the older concept of neoliberalism.

The following study describes these differences through the exploration of the UK state-finance nexus. The UK was one of the earliest adopters of financialization and has one of the most financialized economies in the world. The findings suggest that historical shifts in UK economic policy were driven not simply by a broad neoliberal political and economic agenda imported from the corporate sector. Nor were they only about the conflict between capital and labour, or free market policy and Keynesian welfare state institutions. Transformation was also facilitated by a new alliance of financial and emerging state elites against industrial and established state elites. The Thatcher government imported personnel and thinking from the financial sector and placed them in charge of the Treasury and Department of Trade and Industry. They bought with them a very particular financial-market economic philosophy, tools, and disciplinary practices developed from a set of cultural and epistemological foundations. This amalgam of individuals, ideas, and economic mechanisms – underpinned by cultures and epistemologies – then provided the roadmap by which Britain pursued a more financialized economic policy pathway.

This historical single-nation account has wider significance as it provides a theoretical explanation for why two key phenomena cannot be described as an identity. In so doing, it opens up new possibilities for understanding financialization, elites, and the neoliberal condition that has left us with so many political challenges. As it makes clear, financialization rests on a set of knowledges and practices that have constructed and been constructed upon epistemological and cultural foundations. Fundamental aspects of these foundations are explicitly not shared by neoliberal theory.

The remainder of this article is in four parts. The first explores some of the literature pertaining to these two concepts, their similarities and differences. The second part briefly makes the case for scrutinizing the UK and explains the methods employed: in-depth interviews with key government actors of the period, historical and biographical accounts, and a close reading of annual budgets, going back to the 1970s. The third section documents the changes in personnel and thinking in the UK state’s main departments of economic management following the 1976 IMF crisis. The fourth shows how a financialized economic paradigm, as much as a general neoliberal one, then guided the reshaping of core parts of the UK’s economy.

Financialization Understood Against the Background of Neoliberalism

Neoliberalism is a wide-ranging concept with multiple interpretations (see accounts and definitions in Larner, 2000; Harvey, 2007; Mirowski and Plehwe, 2009; Peck, 2010; Crouch, 2011; Davies, 2014). It has emerged as both a political project, enacted through state institutions, and as a broader set of ideas and values, such as individualism, laissez faire and free choice. In addition, neoliberalism has been built on a broad economic paradigm closely tied to principles of neoclassical economics and economic liberalism, in direct opposition to the Keynesian welfare state economic paradigm before it. Economies are believed to best operate through market mechanisms rather than state management, and anything hindering the smooth operation of markets should be removed. Thus, as Larner (2000) states, it is simultaneously a broad ideology, a form of ‘governmentality’ and a policy framework. In practice, neoliberalism has directed a set of economic policies across the world: supply-side measures such as low taxes and less regulation, monetarist policy levers over fiscal ones, programmes of privatization and state withdrawal from industry, the marketization of state functions, weakening employee rights and welfare state provision, market deregulation, open trading borders, low inflation and price stability.

For social historians tracing its evolution (Harvey, 2007; Mirowski and Phehwe, 2009; Van Horn et al., 2011), individuals and ideas have nurtured neoliberalism’s development through institutions. Neoliberal economists built from their Mont Pèlerin and Chicago School bases, aided by wealthy donors and think tanks, to mount a forceful challenge and takeover of government institutions from the 1970s onwards. For Mirowski (2009: 426), neoliberalism ‘was an intricately structured long-term philosophical and political project … a “thought collective”, that slowly penetrated national institutions of economic management’. Ironically, while driven by a much diminished role for the state within its liberalizing project (Peck, 2010), neoliberalism’s success has depended on states adopting and sponsoring it.

One cannot be totalizing about neoliberalism, which is in its expression contingent on its circumstances and thus different everywhere. Indeed, some authors (Larner, 2000; Mitchell, 2002; Fourcade, 2009) emphasize the significant variation in the ways state institutions have adopted, interpreted, and then implemented neoliberal ideas. In Larner’s words (2000: 12): we have different configurations of neo-liberalism, and close inspection of particular neo-liberal political projects is more likely to reveal a complex and hybrid political imaginary, rather than a straight-forward implementation of a unified and coherent philosophy.

So too, there are structural and institutional differences in nations which are more financialized, as opposed to being simply more neoliberal. In such nations there has been a rapid growth of financial markets relative to both the state and material, productive economy of goods and services (Epstein, 2005; Palley, 2007, 2013; Krippner, 2011). Financial institutions manage larger amounts of capital, provide a greater percentage of corporate profits, and make a greater contribution to national GDP growth. Part of this is traced to the ability of banks and financial institutions to create money equivalents far in excess of sovereign funds, through debt creation, shadow banking, derivatives and other means (e.g. Dodd, 2005; Pettifor, 2014). Banking is less about capital investment in non-financial companies, or ordinary savings and loans; instead, it is more about short-term profit-seeking through activity within financial markets. Large NFCs (non-financial corporations) are increasingly run to create ‘shareholder value’ by any means, including through purely financial activities (see Crotty, 2005; Froud et al., 2006).

At another, mass-consumer level, financialized economies are more active in enrolling citizens into finance (see Seabrooke, 2006; Leyshon and Thrift, 2007; Lazzarato, 2012) through a mixture of personal credit card and mortgage debt, investment of public pension funds, and securitization. Related to this transfer of capital into financial markets are the issues of growing inequality, ‘rentier behaviour’, and global tax avoidance and evasion (Epstein and Jayadev, 2005; Shaxon, 2011; Piketty, 2014). Finally, financialization also involves a growing influence over the state through the funding and rating of government debt as well as general influences over economic activity (e.g. Krugman, 2008; Lazzarato, 2012). Most developed economies are now touched by some or all of these aspects of financialization. However, some nations have been rather more embracing of such activities, and actively promoted them beyond their borders, too.

When considering how they each manifest in the real world, financialization and neoliberalism are clearly related but different. The ways and degrees to which neoliberal economies have become financialized have varied considerably, as some states have much larger financial centres, relative to their industry and state sectors, than others. Some national economies are more active instigators of financialization (Epstein, 2005; Shaxon, 2011), in terms of creating debt, shadow banking structures, complex financial products and foreign investment vehicles (e.g. the US, the UK, Holland, Switzerland). On the other hand, some are more passive adopters (Krugman, 2008; Lazzarato, 2012) of such products and fluid investments (e.g. Greece, Italy, Thailand, Argentina). While almost all states may now be affected by financialization, some nations have been rather more instrumental in nurturing it and facilitating its expansion.

How neoliberalism and financialization are seen to relate to each other varies across the literature, and the distinctions between them are not always clear. For many scholars they appear as elements of the same emerging political economic configuration, and are frequently discussed in such terms (e.g. Crotty, 2005; Epstein, 2005; Bresser-Pereira, 2008; Fine, 2012). Some see financialization as a character in a neoliberal drama, whether as an ‘apparatus’ (Lazzarato, 2009) or a ‘central project’ (Tomaskovic-Devy, 2015) of neoliberalism. Kotz (2010) has argued that neoliberal restructuring caused financialization. Duménil and Lévy (2004) posit that financial restructuring was central to creating neoliberalism.

Clearly, there is also overlap when it comes to comparing some of the core ideas of neoliberalism and financialization. At a general ideological level, neoliberal economists and financiers agree on a range of economic measures, from low taxes and market deregulation to free trade and free movement of capital. When comparing the core economic principles and intellectual paradigms of the two, both are in favour of markets and advocates of global free trade.

However, while the cultures and epistemologies of neoliberalism and financialization show similarities, there are significant differences too. Financial elites have particular views on markets and their place in the economy that are generated within finance-centred ‘epistemic communities’ (Haas, 1992). These form a set of practical concerns that are quite distinct from those of neoclassical economists and neoliberal politicians. Such differences can be observed within professional finance textbooks (Brealey et al., 2011; Bodie et al., 2013; Golding, 2003). They also register in sociological studies of finance (Lazar, 1990; Abolafia, 1996; Knorr Cetina and Preda, 2005; Davis, 2007) and critiques of finance by heterodox economists (Keen, 2011; Palley, 2013; Pettifor, 2014). Across these varied literatures, five areas of difference in economic perspective can be noted.

First, neoclassical economics ignores the ability of the financial sector to create money equivalents and the influence of finance capital in the rest of the economy (Keen, 2011, Pettifor, 2014). Monetarism is focused on controlling the money supply but ignores the fact that far more capital, and its equivalents, are created in the financial system through debt-credit creation and financial engineering. For example, while in the US in 2007 the money supply was $9.4 trillion, securitized debt had reached four times that level, and the total value of derivatives in the economy ten times that (Bresser-Pereira, 2010: 9). Non-financial economies use simple currency exchange but financial markets use multiple equivalents instead, with ever-changing relative values (derivatives, bonds, shares, etc.). For financiers, then, generating capital and its equivalents, as well as their relative stabilities, risks and ‘liquidity’, are primary concerns (Golding, 2003). Neoliberal theory’s reliance on neoclassical economics means that these primary concerns of financiers are bracketed out, and this begins to explain the divide in epistemologies.

Second, in financial-market thinking the key focus is on transactions – not production or consumption – and the best conditions for those transactions to take place. According to the Efficient Market Hypothesis (Fama, 1970; Bodie et al., 2013), all markets should be as frictionless and liquid as possible with transaction costs made as small as possible. Theoretically, multiple anonymous buyers and sellers will then produce an efficient market, and equilibrium prices, provided each has access to all price-relevant information. In this view, many of the factors and costs that concern actual businesses and markets, as well as the material economy, are removed from consideration. Changes in raw commodity prices, consumption trends, labour and land price fluctuations, as well as the political decisions and social issues which affect these, are of secondary concern to the conditions and shifts of a financial market itself. This transactional focus of finance creates another significant point-of-difference between neoliberal accounts of what is important in an economy and the informed priorities of finance.

Third, financiers do not believe just that economic management works best through markets, they also allot financial markets the key role as the best way to allocate capital across an economy (Hutton, 1996; Golding, 2003; Davis, 2007). Theoretically, rational investors ensure that money is moved from poor and declining firms, economic sectors and national economies to good and growing ones. Globalization does not just facilitate neoliberalized free trade, it frees international financial markets which, in turn, create larger, better capitalized, more liquid and free-flowing market conditions. Where neoliberal economists and politicians embrace the broadening of markets and marketization of so many aspects of life, financiers remain relatively fixated on financial markets – another importance difference between them.

Fourth, in financial markets the primary (usually only) stakeholders are considered to be shareholders and investors (Froud et al., 2006). For political institutions and non-financial companies there is a much wider set of stakeholders, including employees, communities, consumers, suppliers, and owners of businesses that are not necessarily financialized. For neoliberal economists these wider stakeholders still matter, but perhaps the most specially considered in neoliberal analyses are (overburdened) taxpayers. Where corporations and governments become beholden to share and bond investors, they are influenced to behave in ways that suit those investors rather than doing what is best for companies and multi-stakeholder economies. Shareholders are increasingly interested in short-term and higher returns than many companies can achieve under normal business conditions, very often putting their desires in conflict with those of other constituencies. While also keenly interested in efficient return-on-capital, neoliberal economists and politicians do hold a larger basket of concerns beyond pleasing shareholders/financiers, and this again drives a distinction between neoliberal and financialized cultures.

Fifth, financial market participants tend to think in microeconomic terms, with their preferred theories focusing on discrete markets, firms and individuals, even if global investment decisions look at macroeconomic data. Trades, hours, days, weeks, quarters, firms, funds, sectors, exchanges: in a fast-paced, highly variable set of systems, the minute details must capture participants’ attention as much as any ‘bigger picture’. In contrast, national economic policies – including those used by neoliberal politicians – rely on macroeconomics and consider general aggregate trends that often ignore financial activity. For example, GDP and CPI calculations of inflation exclude what happens in financial markets, ignoring rises in values of property and finance (e.g. bonds, derivatives and share prices). Thus, there can be huge growth in activities and values in finance, but they may not feature in key macroeconomic indicators or economic policy. Similarly, a strong currency encourages greater foreign investment in national financial markets but weakens exports. These effects may look very different from the points-of-view of financiers and free-market economists. Furthermore, material economies are affected by a series of taxes (such as VAT, fuel duties, etc.) which minimally affect the workings of financial markets. Material economies need large investments in physical plants and machinery, which depreciate, but financial services much less so.

In sum, financial market considerations and economic thinking can be markedly different from concerns of neoclassical economists and neoliberal economic policy-makers. Financiers create and deal with multiple capital equivalents that are ignored by economists. They focus on market transactions and liquidity, not production/consumption, traditional supply/demand factors. They elevate financial markets over non-financial markets, states and traditional banking for capital allocation in economies. They consider investors over other stakeholders. Their day-to-day decision-making most often is on microeconomic terms rather than macroeconomic, and tends to exclude a whole set of material economy factors. These differences in priorities create ‘blind-spots’ between the two, leading to divergent epistemological and cultural communities. For all their complementarity, neoliberal thinking and financier thinking are not entirely synonymous.

Investigating the UK Case

This article now turns to the case example of the UK state. Since the late 1970s, the UK government has become a leading proponent of financialized capitalism. This shift took place on a similar level and timescale to that of the US, and like the US it can be traced in simple economic indicators. In the century prior to the 1970s, UK bank assets had been equal to roughly half the value of UK GDP, but by the mid-2000s these rose to five times the value of GDP (Haldane, 2010). In 1980, the equity value of the stock market (£30.8 billion) was roughly 40 per cent of government income (£76.6 billion), but by 2012 it was worth £1.76 trillion, or nearly three times government income (£592 billion) (HMSO, 2013/14). At the same time, UK industry suffered a decline more pronounced than any other G7 economy. In 1970, 30 per cent of UK GDP came from manufacturing and accounted for 16.3 per cent of total world exports (Coates, 1995: 7) but, by 2010, 13 per cent of GDP came from manufacturing and the UK was running a manufacturing trade deficit of 2 to 4 per cent (Chang, 2010: 90). And the population also financialized. By the end of 2004, UK households owed approximately one trillion pounds to financial firms, £867 billion of which was mortgage borrowing (Langley, 2008: 139). By 2002, British citizens held approximately £1.2 trillion in shares through mutual funds and occupational and personal pensions (Langley, 2008: 60).

The question is: How exactly did this state-facilitated shift toward financial market thinking and practice, as opposed to general neoliberal free-market thinking and practice, permeate through the institutions of the UK state?

This article concentrates specifically on those institutions and policies that propelled UK financialization, leading to the rapid growth of the financial sector and its increasing dominance vis-à-vis industry and the state itself. To this end, it looks at the individuals, cultures and practices of the two key departments involved in UK economic management: the Treasury and Department of Trade and Industry (DTI). From the late 1930s onwards, both the Treasury and the various departments of trade and/or industry had been accommodated by successive UK governments relatively equitably. This was despite the fact that they operated with quite different economic paradigms and links to the wider economy. The economic shocks of the 1970s upset this equilibrium. In different ways, both departments were subjected to powerful exogenous shocks in 1976 (the IMF bailout) and 1979 (the new Thatcher government). While the Treasury was strengthened by events, the DTI was destabilized. Such developments resulted in increased Treasury and financial market influences over industry and the institutions of economic management. Ultimately, DTI culture was reshaped to reflect the economic epistemological framework that the Treasury and City of London held, to subsequently be relayed to the real, material economy. In the process both industrial and political elites became more subordinated to financial elites.

Evidence was collected from the following sources: 1) a series of 20 in-depth interviews with ministers, senior officials and advisors of the DTI and Treasury in the period, 2) a close reading of the annual budgets and aggregation of budgetary shifts between 1976 and 2007, 3) several biographies, Who’s Who entries and insider accounts, 4) the collection of socioeconomic data from reports and other secondary sources.

The Influx of Financial Market Personnel and Knowledge into Government

In the middle decades of the 20th century, both the Treasury and the various departments of trade and/or industry played key roles in economic management. This was despite their functions, economic world views, practices and external elite network links being remarkably different. The Treasury was a more inward-facing department that primarily communicated with other government departments. Its primary operational role involved controlling public spending, so Treasury officials rarely dealt with actual industry (Pliatsky, 1989; Lipsey, 2000). Distinct social, class and geographical divisions between Treasury civil servants and industrialists also hindered social relations. Instead, officials had far more formal and social contact with the City of London and Bank of England (Ingham, 1984; Theakston, 1995). By the 1970s Treasury staff had become fairly critical of the large, inefficient nationalized industries, which often demanded money and were also associated with the ongoing industrial relations problems of the time (see also Hall, 1995; Jenkins, 2006).

Consequently, the Treasury shared an economic perspective that had much in common with the financial institutions of the Bank of England and the City. This perspective, typical of a more widespread (and neoliberal) economic view that was emerging, was anti-state intervention and spending, critical of large public industries, in favour of free trade and international markets. It was also particularly supportive of UK financial services. This translated into lowering taxes and regulations on corporations and markets, and encouraging international trade and inward investment. However – and crucially for the discussion here – Treasury thinking was very much detached from the conditions of production, product markets and the wider economy operating across the regions.

In stark contrast, the departments of trade and industry were largely outward-facing. Their economic remit was directed towards managing and boosting UK-based industries at home and abroad. Officials had strong links with leaders of industry across the regions of the UK, far beyond London (Middlemas, 1991; Pollard, 1992; Theakston, 1995). The departments were central to the tripartite politics and Keynesian economic framework that had directed UK state policy from the late 1930s onwards. Having direct management of many nationalized industries and links with both business and union leaders, they had become fairly central to the running of large parts of the UK economy. These differences, in terms of elite group networks, institutional links and economic outlooks were apparent to those involved: Margaret Beckett, former Secretary of State for DTI: you are talking different worlds quite often … John Smith gave a talk in the City at one point, reasonably close to the 1992 election, and it was almost like the bride’s side and groom’s side. There were the people from the financial world who were there and there were the people from the industrial world who were there and they almost kind of weren’t talking to each other, and literally almost sitting on different sides of the room with different interests and concerns.

1

After 1979, the Treasury was given a more prominent role in developing macroeconomic policy in the larger economy, as opposed to merely managing the government’s finances (Pliatsky, 1989; Theakston, 1995; Lipsey, 2000). With its new powers, it began exerting control through a series of new disciplinary mechanisms and procedures for managing department spending (Chapman, 1997, Thain and Wright, 1995). The DTI was one of its immediate targets as it suffered some of the harshest budget cuts across government in the 1980s (Mullard, 1993). The Treasury was also given far greater control over the rest of the civil service and government departments, and this included power to manage civil service personnel (Pliatsky, 1989; Johnson, 1991; Theakston, 1995; Hall, 1995; Chapman, 1997; Lipsey, 2000). In 1981, it began managing the appointment of other department permanent secretaries, senior appointments, and civil service pay.

Key to what took place during this period was a dramatic shift of senior personnel at all levels. Rarely noted, but equally crucial, was that many people coming in to occupy ministerial and civil service roles had spent considerable time working in the City. They were very much linked to financial elite networks and guided by a financialized economic knowledge framework.

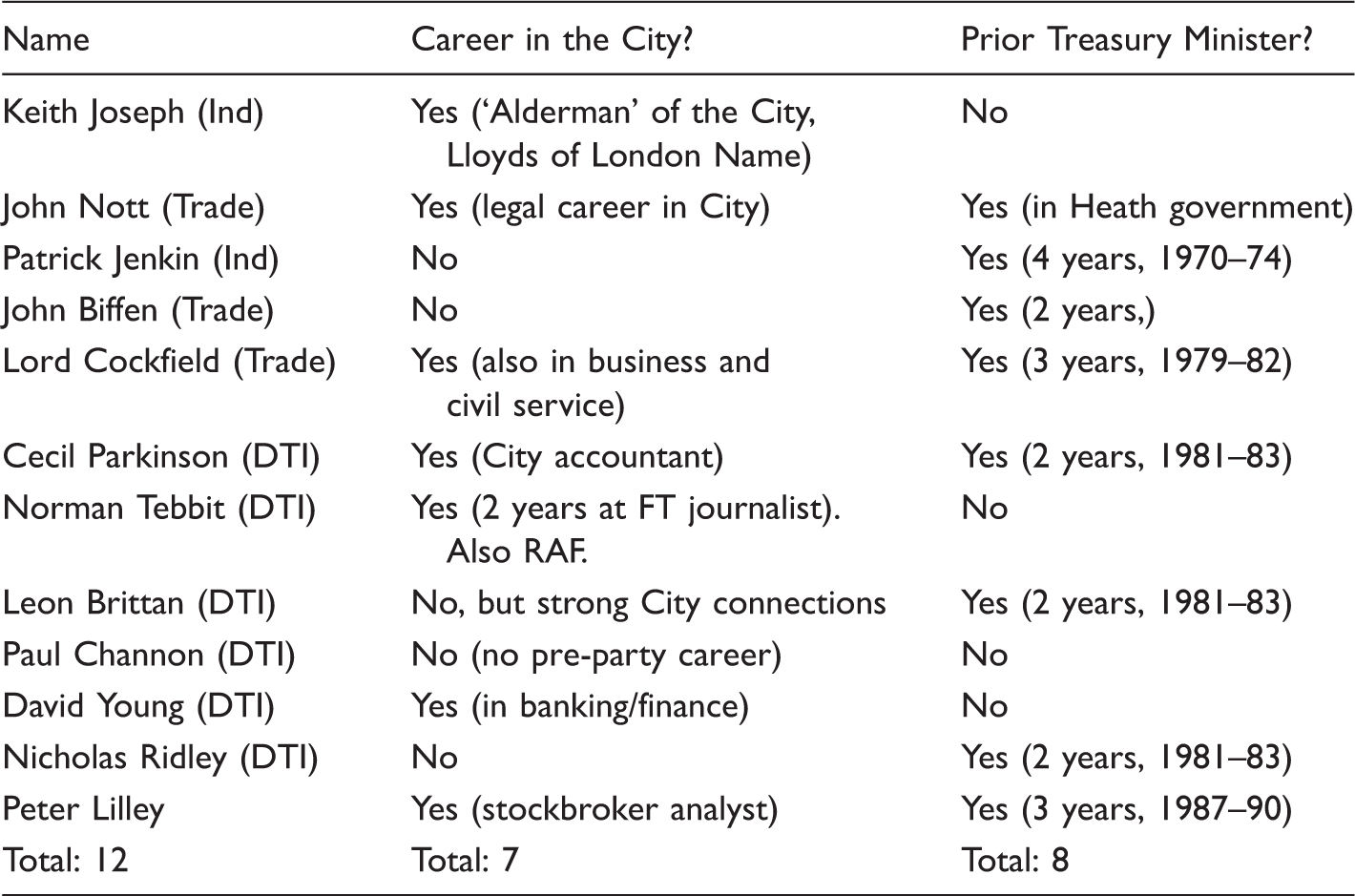

The senior ministerial positions in the Treasury were taken by a succession of politicians with City backgrounds and/or networks. Nigel Lawson, Thatcher’s second chancellor and the widely-acknowledged intellectual economic force of the period, had spent many years in the City. His successor chancellors, John Major and Norman Lamont, as well as several junior Treasury ministers (Cecil Parkinson, Lord Cockfield, Nicholas Ridley and Peter Lilley), also had established City careers before entering Parliament. In fact, several interviewees stated that many of their ideas for reform came from their experiences working in the City: Nigel Lawson, former Chancellor: I think everybody agreed that the nationalised industries were a problem … I had the advantage I suppose initially of particularly a financial dimension. In 1959/60 I was the senior writer of the Lex column on the Financial Times and therefore I got to know the City of London very well and I got to know how companies report to the marketplace, how new issues worked and all that practical stuff and so I think that was helpful in thinking, trying to think how you would set about getting rid of state ownership. Norman Lamont, former Chancellor: My time in the city did inform my disillusionment with the policies pursued by Heath because I could see, you know, I worked as an investment manager and I could see the problems that were building up and the harm that was being done, and the distortions that were being created by the policies. Secretaries of State in the DTI, 1979–1990.

Similar changes were made across the civil service as the new Thatcher government also set about ‘purging’ the top ranks of officials, first in the Treasury and then the DTI. Any senior Whitehall mandarin associated with the IMF debacle and Keynesianism was pushed out, and a mid-ranking neoclassical economist, Peter Middleton, was suddenly promoted several ranks to become Permanent Secretary at the Treasury. One former Treasury official recalls the great shift in personnel through the early 1980s: John Gieve, senior Treasury civil servant: In the Treasury as a whole, the IMF episode, the loss of control of spending, was a traumatic event … there was a major, major shift when Howe came in with Lawson … And there were some big shifts in personnel in those years … everyone was called Douglas I seem to remember when I arrived at the Treasury, and most of them left. Anonymous senior former DTI civil servant: The direction was set in those very early years by Sir Keith and Mrs Thatcher. If you didn’t like that, that was pretty tough if you had a different view as an official. But, if you were in one of those pockets where you were dealing with the big privatizations it was an extremely exciting time with a very clear sense of direction of what needed to be done and a lot of energy around those particular activities … the best people were directed to these big privatization activities on the industry side of the department. Dan Corry, Labour Economic Advisor: [The City] was probably too influential. I think the big bank leaders were, you know, they were much more into the Treasury than they were, and into Number 10. And I was aware in Number 10 that the banks had a strong line into the place, not only to the prime minister.

The next section explores how specific financial-market epistemologies – norms, discursive practices and mechanisms – drove changes to the UK economy as much as simple free-market neoliberal ideology. Three knowledge-areas are discussed: taxation, privatization and trade deregulation. Through each of these policy areas, the tools and discourses adopted had a very strong element of financialized-market thought. Blunt free-market ideas united the government managers of economic policy, but financial market discursive practices and devices provided the route map.

Financialization as an Epistemological Framework for Policy-Making

Starting with fiscal policy, since 1979 the Treasury has made a series of changes to the tax regime aimed at liberating markets and industries of all kinds (see also Cairncross, 1992; Pollard, 1992; Jenkins, 2006; Toynbee and Walker, 2010). For example, between 1979 and 2015, corporation tax has been steadily reduced from 52 per cent to 20 per cent (with 15% possible). It, along with the standard rate for business assets, has continued to drop in every Parliament since. These cuts, along with those in business assets and higher rates of income tax, amongst others, have provided ample evidence of the kind of government fiscal policy underpinning neoliberalism: one contributing to the expansion of multinationals and inequality.

However, further details also reveal that this new thinking about the tax regime more often worked to benefit financial markets over industry. Stamp duty on the purchase of shares and bonds was cut in stages from 2 per cent in 1979 down to 0.5 per cent. Dividend payment controls were abolished in 1982. Although corporation tax was cut for all businesses, this was paid for by removing capital investment allowances for machinery and plants – measures which hit industry, not finance. For Nigel Lawson, these decisions came back to his view that reducing transaction costs would boost the economy far more than encouraging industrial investment. There was little recognition that financial markets would be the main beneficiaries: Nigel Lawson, former Chancellor: Transaction taxes do a particular harm because you need to have transactions, that’s how markets work. If there are no transactions there’s no market, so you don’t want to put barriers in the way of transactions … that was entirely my own thinking [cutting tax relief on capital investment], obviously having decided that I wanted to reform, right at the beginning, corporation tax, and to have a lower rate of tax on profits, offset by a gradual winding down of all these reliefs, which had no economic rationale.

By the time of New Labour, with financial services flourishing, fiscal policy now positively aimed to support the sector. In 1998 Gordon Brown announced that capital gains tax for investors holding non-business assets for 10 years would fall from 40 p to 24 p in the pound, and 10 p ‘for those who build businesses or stake their own hard-earned money’ (Hansard, 17 March 1998). In his 2000 budget he changed the tax regime on bonds for the sake of ‘the international competitiveness of the bond market in the City of London’ (Hansard, 21 March 2000). When he reduced capital gains tax he made buying stocks and shares yet more profitable. Interviews with former ministers from the Blair years confirmed what the budget analysis suggested: that is, that finance was now a key ‘industry’ that needed to be supported because of its contribution to the UK economy: Stephen Byers, former DTI Secretary of State: It came very clear that London was going to be the sort of financial capital of Europe and a major global financial player. So I think we got the benefits of that and it became a very attractive destination, we had the right tax regime and I think it was a combination of factors … we didn’t want to do anything that would kind of cross it.

This became increasingly clear with the evolution of ‘good corporate governance’. Financial market thinking from the 1970s onwards emphasized ‘shareholder value’ as central to good corporate governance (see Hutton, 1996; Froud et al., 2006; Davis, 2007). These principles of ‘shareholder value’ clearly influenced government policy and regulation in relationship to corporate governance and takeovers. Each new committee on corporate governance (Cadbury, Greenbury and Hampel) was dominated by financial institutions, and each further decreed that the first obligation of company boards was to satisfy their shareholders. Responsibility for enforcement was then placed with the London Stock Exchange and Financial Reporting Council (FRC), both of which were dominated by City representatives. The 2000 Financial Services Act and 2006 Companies Act, produced by the DTI, then officially sanctioned these regimes (see Seely, 2012; Davis et al., 2013).

A similar process took place in regard to takeover policy. After 1979, the tests and scope for government intervention during takeovers were steadily weakened by DTI Secretaries of State. In 1984, Norman Tebbit made clear that referrals to the then Monopolies and Mergers Commission would be made primarily on ‘competition grounds’. In the 2002 Enterprise Act, Patricia Hewitt took further powers away from ministers to intervene. Such changes, along with general trade liberalization policies (see below), left UK companies extremely vulnerable to takeovers. Accordingly, the UK became the easiest of all the major economies in which to do takeovers (Jackson and Miyajima, 2007). Thus, once again, the Exchange was given greater influence over capital allocation in the economy.

A third area of policy shift which depended on a financialized epistemology was in international trade deregulation. Much of this process, as discussed by critics of neoliberalism, has been recorded as enabling large corporations and the super-rich to gain the upper hand (e.g. Crouch, 2011; Shaxon, 2011). Thus, industrial production has shifted towards countries with cheap labour, tax avoidance opportunities have increased, and nations have joined a race-to-the-bottom in an attempt to attract corporate investment. However, once again, the other side of the story is that trade liberalization and competition policy has enabled the huge growth of the financial sector, with all sorts of international financial flows and exchanges coming to dwarf those of the real, material economy.

Legislation in 1979 and 1980 brought the release of international exchange and credit controls and thus initiated a new credit boom. This also meant that big UK-based banks and institutional investors started switching far more of their funds abroad rather than into the UK economy. At the same time, the DTI and Lord Cockfield, with long experience at the Treasury and in finance, led the way in negotiations for the liberalization of international trade, within the EU and beyond. Many other states agreed to such trade liberalization policies, but most also maintained more protections and support for key industries (Hall, 1995; Hutton, 1996; Coates, 2000; Hall and Soskice, 2001). Each of these changes left the UK’s industry more open to international financial influence and the threat of foreign takeovers: Terry Burns, former Treasury Permanent Secretary: There was a very conscious programme of removing obstacles like, for example, not favouring British institutions over American or European institutions … I think very few countries probably would have tolerated that, but again there was quite a long tradition of London being a relatively open system … I think the UK is probably less protectionist than almost anywhere of the major countries. Cecil Parkinson, former DTI Secretary of State: We were bidding to become a world financial centre … And so we set out to open the thing up, it wasn’t an accident … we wanted the big players to come into our market. That was, if we were going to compete with Wall Street, if we were going to have a role as a world class financial centre then you couldn’t have a little local centre and securities market. Andrew Turnbull: The Treasury is an anti-mercantilist place. It doesn’t believe that there is something magic about the production of goods. It believes there is, what matters is value added … This process has gone further in Britain partly because the financial services sector has been so powerful. Probably the financial services sector almost certainly has over-expanded.

Conclusions: Distinguishing the Cultures and Epistemologies of Financialization from Neoliberalism

Although financialization has much overlap with neoliberal economic thinking and practice, there are also clear differences, and these can be seen at work in the case of the UK. The findings here, put alongside a disparate range of studies of finance, have helped identify five elements of distinction between financialization and neoliberalism. What these five elements have in common is that they stem from a different set of assumed knowledges about what is important, and a different set of cultures that arise from practices that both created these knowledges and are perpetually remade by them. The creation of money, the transactional basis of finance, the reductive power of financial markets, the orthodoxy of shareholder value, and the intense micro-economic focus of finance create a micro-climate particular to financialization. These are some key epistemological and cultural foundations of financialization, and excavating them makes clear how they are not shared by neoliberalism but are unique to financialization as a socio-economic phenomenon. In addition, the reliance of neoliberal theory upon neoclassical economics, and the primacy of financial markets for financiers, has created adjoining but distinct sets of knowledge and social practice as well as experiences. For all their complementarity, neoliberal thinking and financier thinking never have been entirely synonymous.

The case presented here has focused on the key state institutions of economic management, as Britain shifted towards its own particular form of financialization. Specifically, it has examined the dramatic changes that took place after 1976 in the Treasury and DTI. This shift over several decades increased the influence of financial elites relative to non-financial corporate and political elites. Key to the transformation was an influx of politicians and civil service personnel whose previous professional employment had been in the City of London. These actors bought with them not just a pro-market, anti-state economic management and low tax perspective, but an ‘ideal’ understanding of ‘the economy’ centred on finance. They also increased links and exchanges with the financial sector, thus strengthening the elite networks forming between government and finance.

With this change new parameters were established, not only around monetarism and free markets but also around uniquely financial concerns: the primacy of markets, transactions, shareholders, and money, and this had serious consequences for the UK economy. Over the decades, reconfigured state institutions then strongly shifted political and economic conditions in favour of finance and against industry via fiscal policy, privatization, corporate governance regulation and international trade liberalization. Changes in taxation, following a financial market logic, focused on reducing market transaction costs, but paid for by cutting tax incentives to non-financial industries. Privatization did more than withdraw the state from economic management. Most industries were floated on the London Stock Exchange rather than moved into the private sector using other financial and ownership structures. Corporate governance regulation removed state and other stakeholders from management consideration, making international shareholders the only ‘regulators’ and stakeholders that mattered. Thus, the City was considerably strengthened as a hub for capital allocation in the UK economy. Lastly, trade deregulation did far more to free global finance and financial markets than it did international trade itself. Transnational investors were given the freedom to create and transfer capital in much larger quantities than nation-bound political and corporate elites and industries. These policy changes were dependent on knowledge and culture that were not just neoliberal: they were specifically financialized.

This case and the arguments drawn from it have wider implications, suggesting that other financialized national economies have been similarly influenced by finance-based elites and their respective financial market logics. Broader free-market goals may have been set, but the means for achieving those goals had a distinctive financial market logic, and thus financial economic paradigm principles have the power to structure neoliberal political-economic objectives. Financial elites can and do export discourses, tools and mechanisms of economic management to state elites, and the frameworks explored here – specifically epistemological and cultural ones – could be applied to similar transformations all over the world.

This historical account is also significant when looking at the causes and consequences of the global financial crash of 2007–8, the world-wide recession that followed, and the sense of political instability experienced in many nations since then. It is pertinent to both the recent UK vote to leave the European Union and Trump’s electoral victory in 2016, as well as to growing political and economic instability elsewhere. All these developments have revealed the new schisms that have opened up between business, political and financial elites. To date, much of the critical debate about causes and alternative future pathways that has followed has been centred on the policies and histories of neoliberalism. However, financialization – its systems, institutions, and practices – also require further scrutiny, both in relation to neoliberalism and as an independent phenomenon. So, too, interrogation should include a focus on financialization’s cultures and epistemologies.

Footnotes

Note

Interviewees cited

Anonymous former Senior Civil Servant, various positions at the DTI: 10 December 2013.

Dame Margaret Beckett, Labour MP, 1974–, various cabinet and shadow cabinet posts, 1989–2006, including Secretary of State for DTI, 1997–8: 26 June 2013.

Lord Terry Burns, Chief Economic Advisor to Treasury/Head of Government Economic Service, 1980–91, Treasury Permanent Secretary, 1991–8: 15 July 2014.

Stephen Byers, Labour MP, 1992–2010, various cabinet posts including Secretary of State for DTI. 1998–2001: 4 September 2013.

Dan Corry, Economic Advisor to Labour in DTI, (Shadow) Treasury and No. 10 Policy Unit, 1989–2010: 5 August 2013.

Sir John Gieve, Senior Treasury Civil Servant, 1978–2001, various senior posts elsewhere, 2001–9: 11 July 2013.

Lord Norman Lamont, Conservative MP, 1972–97, various ministerial positions in government, in Treasury, 1986–93, including Chancellor of the Exchequer, 1990–93: 28 June 2013.

Lord Nigel Lawson, Conservative MP, 1974–92, Chancellor of the Exchequer, 1983–9: 20 June 2013.

Lord Cecil Parkinson, Conservative MP, 1970–92, various cabinet positions, 1983–9, including Secretary of State for DTI, 1983: 1 August 2013.

Lord Andrew Turnbull, Treasury Civil Servant, 1970–94, Permanent Secretary to Treasury, 1998–2002, Cabinet Secretary, 2002–5: 18 September 2013.