Abstract

This paper considers the significance of the newly conceived Canada Infrastructure Bank in relation to the political economy of settler colonialism in Canada. I argue that the Canada Infrastructure Bank is a fundamentally colonial institution that marshals private capital to reproduce and extend the jurisdictional power of the setter state. The Bank is an arms-length financing institution whose purpose is to leverage private and institutional capital for investment in large scale, nation-building infrastructure, including infrastructure that supports resource extraction in remote and northern Canada. The first section of the paper examines the specific configuration of the Canada Infrastructure Bank. I suggest that the need to attract private investment into certain kinds of infrastructure development must be understood in relation to state struggles to exercise territorial jurisdiction over Indigenous lands and resources. This struggle is reflected in the specific configuration of the Canada Infrastructure Bank. The second part of the paper focuses on some of the implications of pension securitization. The Canada Infrastructure Bank has deliberately been designed to leverage Canadian pension fund capital; I ask what it means to grow settler workers’ savings through investment in privatized, resource development infrastructure.

Introduction

“The Mining Association of Canada (MAC) applauds the federal government’s nation-building infrastructure plan, including the creation of a new Canada Infrastructure Bank … The Government of Canada’s visionary infrastructure plan is going to set Canada on a path of long-term, sustainable growth. The government’s bold actions on infrastructure will help get Canadian goods to market, address the unique challenges in remote and northern communities … Such strategic leadership by Prime Minister Trudeau and his government should be commended … government has communicated an unprecedented vision for how infrastructure will transform remote and northern Canada—regions that are critically important to, and reliant on, Canada’s mining sector … The acute lack of infrastructure in Canada’s remote and northern regions is inhibiting further sustainable mineral development due to the high costs of exploring, building and operating in these regions”. (MAC, 2016, online).

“It is through our use and occupation of our lands and going out onto our territory and actually living and using our land that is going to stop [this pipeline]. That is the power that we stand on as Secwepemc … and that is what Canada is scared of” (Kanahus Manuel in Beaumont, 2018).

In their 2016 and 2017 federal budgets, the Government of Canada announced a 180 billion-dollar wave of infrastructure investment aimed, in the words of the finance minister, at “build[ing] the Canada of tomorrow” (Morneau, 2017: 33). Federal representatives billed this “unprecedented investment” to the business and finance sectors (Morneau, 2017: 33–34) as an “opportunity”; on the one hand to make Canada more competitive, increase trade and access to markets, unlock investment in energy resources, and develop northern resources, and on the other hand to offer public infrastructure to private investors on a scale never before seen in Canada (Sohi, 2017: 37–48). The “centerpiece” of the so-called Investing in Canada Plan (2017) was the establishment of the controversial Canada Infrastructure Bank (CIB), first introduced in the 2016 Fall Economic Statement (FES) released in the runup to the 2017 budget (Sohi, 2016: 34).

Back-drop to this initiative was a report published in October 2016 by the Finance minister’s Advisory Council on Economic Growth that presented the Bank as the solution to “Canada’s infrastructure imperative”, a narrative that first appears in (heavily redacted) interim materials prepared by the Council and circulated mid-2016 to ministers and senior government officials (e.g. ACEG, 2016a: 69–90). The “imperative” (which reads as a justification and rational to both industry (for a government-backed institution) and parliament (for privatization of public infrastructure)) appears as a three-part narrative in which it is claimed on one hand that Canada faces several medium- to long-term threats including significant decline in economic per capita GDP growth, and on the other, that as a “massive northern territory” heavily dependent on trade in energy and natural resources Canada faces a considerable “infrastructure gap”—a gap, they note which would be particularly well filled by large scale “nation building projects”. Massive investment (upwards of several hundred billion dollars) in productivity-enhancing infrastructure is, they suggest, “imperative” in order to avoid disastrous economic consequences. Noting in particular Canadian pension funds’ appetite for investment in infrastructure and the trillions of dollars (globally) sitting in negative yield bonds, the narrative concludes Canada must “innovate in infrastructure financing”: greatly increase the participation of institutional capital (from Banks, pension funds, insurance companies, sovereign wealth funds, and other long-term investors) “as a national priority and as a condition for success” (ACEG, 2016b: 56).

The purpose of this Bank is to use billions of dollars of treasury money to harness private capital to federal infrastructure policy objectives. In its current configuration, the Bank anticipates leveraging at least 140 billion dollars of private capital for new “nation building”, “productivity enhancing”, “national economic development infrastructure” (ACEG, 2017: 1, 8), a significant portion of which is directed toward the so-called natural resource infrastructure (NRI) and specifically prioritizes investments that move resources and energy more efficiently (ACEG, 2016b: 59–62; ACEG, 2017: 8; Infrastructure Canada, 2018: 50). The CIB will be capitalized up to 35 billion dollars, 15 of which will be available for direct investment in infrastructure projects and up to 20 to invest in assets that would result in the Bank holding debt or equity (the 35 is a balance sheet figure since the value of an asset may change over time).

NRI is defined by the Prospectors and Developers’ Association of Canada (PDAC) as “infrastructure that supports resource development”, especially in “northern” (north of 60 degrees latitude) and “remote” (51 or more Km from established transportation infrastructure) regions of Canada (2015: 1). This includes “infrastructure that decreases the costs of resource extraction and development” and that “contributes to opportunities for greater wealth discovery and production” (CMIF, 2017: 13, see also PDAC, 2016a). PDAC (2016b) identifies road (including transportation corridors, highways, and all-weather roads); energy (including power plants, electrification, and grid access); broadband connectivity; rail; port; and airport infrastructure as essential to cost-effective resource development and extraction. Industry experts suggest that investment in NRI will “unlock” remote and northern Canada, “enhance investment competitiveness” of the Canadian economy”, and generate national wealth (CMIF, 2017: 13; PDAC, 2015, 2016a, 2016b). The CIB explicitly supports NRI from across two of its three five billion-dollar funding streams. These include Green Infrastructure and Trade and Transportation Infrastructure which together target: large-scale rural and northern electrification projects and replacement of transportation infrastructure vulnerable to climate change (such as ice roads with all-weather infrastructure) under the guise of climate change mitigation, resilience, and reduction in green house gas emissions; development and enhancement of new trade and transportation corridors; increased remote access to existing transportation infrastructure; broadband internet connectivity; and development or expansion of new ports and airports.

Response to the Bank from the mining and exploration industry was remarkable. Lauding the Federal government’s “visionary”, “nation building” leadership (above), the Mining Association of Canada (MAC) called the 2016 announcement of the CIB “bold”, “essential” to the future of the mining economy in Canada, and sure to attract new investment to the sector (MAC, 2016: online). The PDAC declared the Bank would “unlock natural resources in remote and northern Canada” (PDAC, 2017a: online) and in an effusive post-budget editorial proposed “the stars [had] align[ed] … [for the] Billions of dollars in mineral wealth [that] lay stranded across northern Canada due to inadequate infrastructure” (2017b: 22–23). The federal government, according to the editorial, was “literally paving the way” toward an improved “economics of underdeveloped mineral deposits and exploration” in Canada (PDAC, 2017b: 22–23).

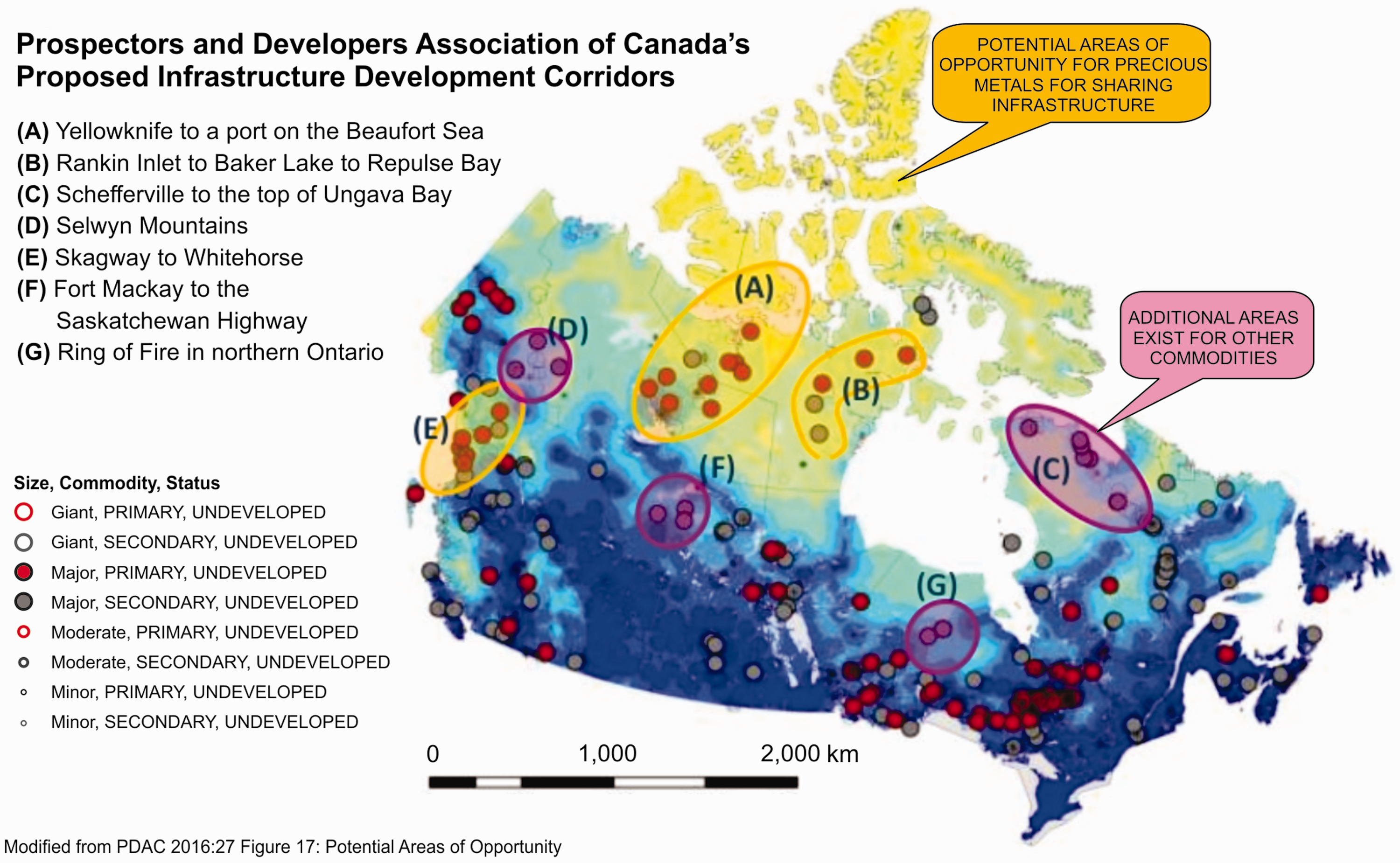

NRI has become an increasingly significant policy concern of the Canadian mining industry who have long campaigned in favor of a federal institution to finance resource development infrastructure (CCC, 2016a; CMIF, 2016, 2017; Pagnan, 2017). According to PDAC: only 12% of known discoveries lie above 60 degrees of latitude despite it representing 40% of Canada’s landmass (PDAC, 2016b: 5); and in the territories, the vast majority of mineral potential remains “untapped” (of existing discoveries in the Yukon, Northwest Territories, and Nunavut, 77%, 69%, and 85%, respectively, remain undeveloped) largely due to their remoteness from existing infrastructure (2016b: 21). Indeed, lack of access to energy and transportation infrastructure, they suggest is the diver of mining and exploration costs in remote locations (PDAC, 2015, 2016b). To lower the prohibitive costs of exploration and extraction, and “capitalize on the economic potential of remote and northern Canada”, PDAC are campaigning for construction of seven “infrastructure development corridors” (shown in Figure 1) linking major geologic structures to markets (2016b: 27).

Infrastructure corridors.

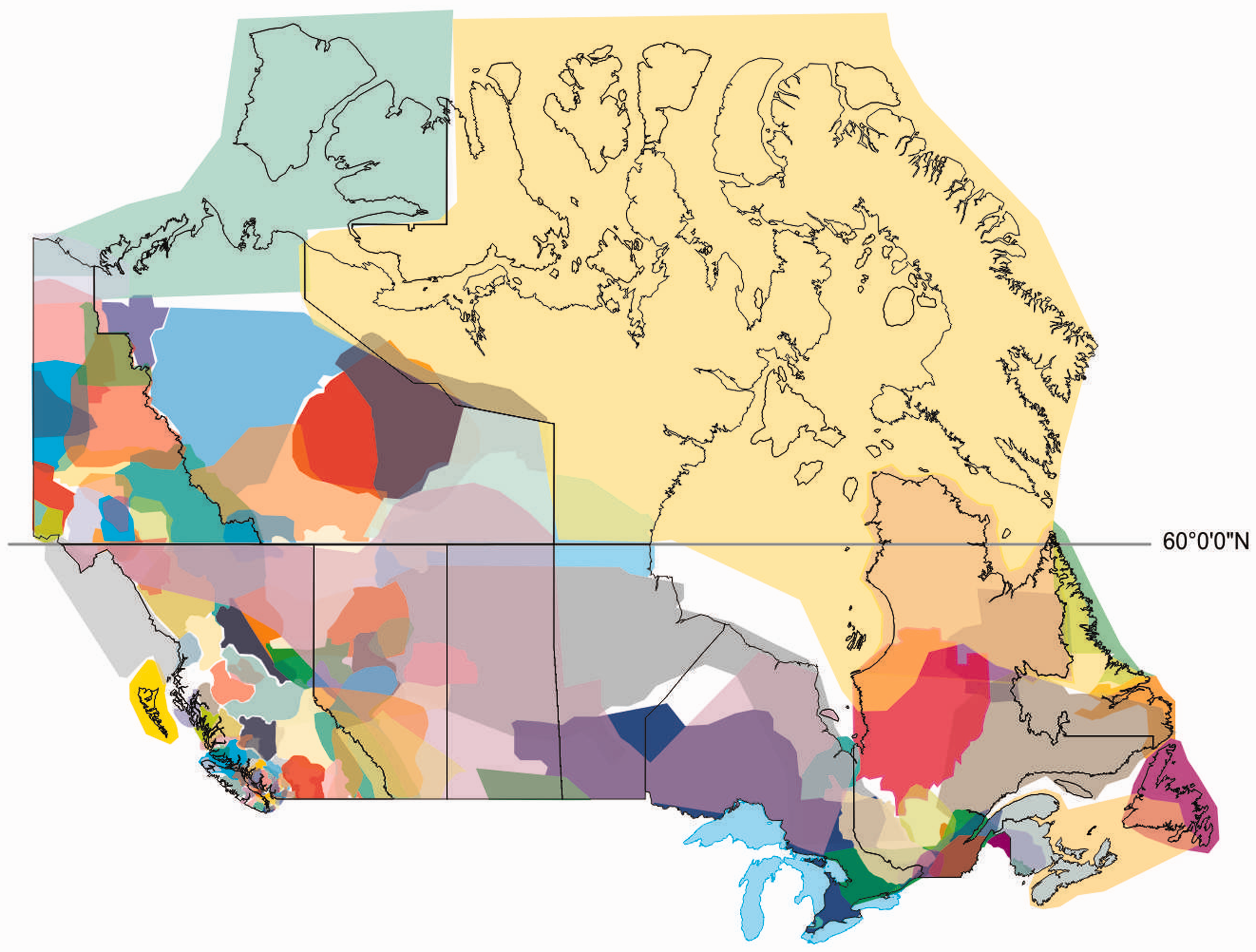

The purpose of this paper is to consider the significance of the CIB in relation to the political economy of settler colonialism in Canada. Deb Cowen and Shiri Pasternak remind us that infrastructure is a materialization of the settler state’s jurisdictional claims (2018). As the map in Figure 2 indicates mining plays and mineral claims, particularly in “remote” and northern regions, inscribe Indigenous lands and must increasingly confront the “deepening problem of Indigenous jurisdiction” (Cowen and Pasternak, 2018). Following its announcement, think tanks, media, and other left-wing commentators decried the privatization of public infrastructure projects the Bank would entail as a “cash grab” and “sell off” of Canada’s collective, public wealth (Frie, 2017; Mcquaig, 2017; Sanger, 2017a, 2017b). Without disparaging these critiques, I want to insist that neither the significance of the CIB, nor what is at stake in privatizing infrastructure can be fully understood outside the context of settler colonialism and the ongoing project of producing colonial space in what is now Canada.

Indigenous territorial jurisdiction in Canada.

This paper is divided into two main parts. In the first section, I draw from access to information and privacy (ATIP) requests, media articles, Hansard transcripts, and mining industry publications to examine the specific configuration and mandate of the CIB. I suggest that the need to attract private investment (and in particular, large-scale institutional investment, including from Canadian pension funds) into certain kinds of infrastructure development must be understood in relation to state struggles to exercise control over Indigenous lands and resources, particularly in northern and remote areas of what is now called Canada; a project that increasingly relies on private finance. This struggle is reflected in the specific configuration of the CIB whose unstated aim is to bring the aspirations of corporate capital and the settler state into functional alignment. I propose that the CIB is a fundamentally colonial institution that marshals private capital to produce and extend state jurisdiction through infrastructure development and, relatedly, accelerated resource development. In the second part of the paper, I focus on some of the implications (for settler colonialism) of pension securitization in relation to infrastructure development. In the run up to the FES, the federal government actively courted Canadian pension funds, who, sitting on trillions of dollars of unproductive assets were looking for stronger returns. The CIB has deliberately been designed to attract Canadian pension fund capital and to respond to what Canadian pension investors have identified as a lack of infrastructure “opportunities” in Canada (O’Reilley, 2017; see also GoC, 2016: 26). While the Bank has yet to make any investments in NRI projects, 1 its configuration raises important questions about what it means to grow settler wealth through investment in privatized NRI. Drawing on Susanne Soederberg’s concept of “cannibalistic capital”, I argue that, if successful, the CIB will effect another set of strategic alignments, this time between the interests of what I inadequately term “settler-workers” and investors (capitalists) and against Indigenous jurisdiction on Indigenous lands.

In order to understand the mandate and configuration of the CIB, I explicitly foreground Canada’s settler colonial context by situating my analysis in what Shiri Pasternak describes as a “dynamic of governance” wherein “state jurisdiction over Indigenous lands is an object of constant struggle to exercise effective sovereign control” (2017: 4). This tension is particularly well illustrated in the second opening passage where Secwepemc activist and warrior Kanahus Manuel describes active use and physical occupation by Indigenous peoples of Indigenous territories as a source of Secwepemc authority and jurisdiction in Secwepemc lands and as a disruption of the jurisdictional claims of the settler state. What is so insightful about her statement is its insinuation that it is likewise for the state. Jurisdiction, Pasternak reminds us, does not emanate from the presumption of state sovereignty (2017: 3). Rather, she writes, it is the apparatus through which sovereignty is rendered meaningful, because it is through jurisdiction that settler sovereignty organizes and manages authority. In the settler colonies in particular, sovereignty is asserted against the legal and political authority of Indigenous peoples over their lands and nations; in the absence of legal agreement a perpetual struggle over jurisdiction defines the terrain. (Pasternak, 2017: 3)

Existing as it does in relation to this gap, I argue the CIB is closely linked to the (unfinished) project of perfecting settler sovereignty, of—in Pasternak’s words: “fusing of sovereignty claims with the effective exercise of territorial jurisdiction over Indigenous lands” (2017: 14–15). This means, I propose, that we need to understand the CIB as a series of interventions that on the one hand work toward the goal of asserting settler jurisdiction over Indigenous lands and resources (and replacing Indigenous jurisdiction), and on the other of “risk managing” liabilities associated with extraction of corporate and settler wealth given the operational confines of imperfect settler sovereignty (Dafanos and Pasternak, 2018; Stanley, 2016).

I also explicitly foreground Canada’s settler colonial context by situating my analysis of the Bank (ostensibly a privatization Bank) after Dene scholar Glen Coulthard’s insistence that the dynamics of accumulation in settler colonies are best understood through analysis of what he refers to as the “colonial [rather than capital] relation” (2014). The CIB has been predominantly read as a neoliberal story about privatizing public infrastructure under pressure of the financial sector (for an exception see Curry, 2017). Digging deeper into the public record, however, suggests reticence on behalf of investors and reveals significant efforts taken by the ministry of finance to engage and attract the private sector. It matters how, why, and under what circumstance private capital and the state align. Foregrounding the colonial relation, so that Indigenous dispossession becomes the central analytic feature of critical engagements with capitalism (Coulthard, 2014) at once broadens and deepens the analytic perspective on this alignment.

How the CIB aligns the interests of capital and the setter state

Left accounts of the genesis of the CIB overwhelmingly suggest the Bank came about in large part as a result of pressure from private finance (especially pension funds) seeking the growth opportunities provided by private investment in public infrastructure in an investment context that economist Toby Sanger (2017a, 2017b) has aptly described as a classic crisis of overaccumulation. Indisputably, infrastructure assets are increasingly attractive to institutional investors because they offer stable, predictable, and growing returns and are a good match for defined-benefit pension liabilities, endowment and foundation obligations, and annuity and life insurance liabilities (Bahceci and Leh, 2017; JP Morgan Asset Management, 2015). The Ontario Teachers’ Pension Plan (OTPP) earned above 18% on their infrastructure portfolio in 2017, Ontario Municipal Employees Retirement System (OMERS) slightly over 12%, and Ontario Public Services Employee Union Trust (OPTrust) 11% (OMERS, 2017: 9; OPTrust, 2017: 27; OTPP, 2018: online). And certainly, pension funds and other long-term institutional investors are eagerly switching into infrastructure. Canada’s five largest pension funds have significant exposure to direct private equity investment in public infrastructure (approximately 76 billion dollars collectively) and have become market leaders in public infrastructure acquisition as a central component of their investment strategies— foremost amongst them, the Ontario Teachers’ with almost 19 billion currently invested in infrastructure and OMERS with nearly 17 billion (OMERs, 2017: 34; OTPP, 2018: online; Sekerrett, 2018, see also Sabia, 2016: online). The top four Canadian funds rank among the world’s top 10 infrastructure investors, and Canada’s top 10 amongst the top 200 in the world (Whiteside, 2017).

Yet, despite the reality of increased investor appetite for infrastructure, close examination of the genesis of the CIB suggests, in fact, that the objectives of institutional investors and the settler state did not map neatly onto one another. Rather, a significant amount of time, energy and effort was spent on behalf of the federal government to shape an institution in which these interests might productively entwine. Others have extensively documented the months long array of consultative processes with private sector stakeholders, through which the CIB was developed and implemented (see Curry, 2017; Mcquaig, 2017; Sanger, 2017a, 2017b; Whiteside, 2017). Following a brief summary of pension fund involvement in the design and implementation of the Bank, I examine some of the ways in which this process and the resulting financial configuration of the Bank sought to achieve alignment. These initiatives detail the significant lengths undertaken by the state (including handing over the design of the Bank to the private sector) to recruit institutional capital to the task of national infrastructure development.

Internal documents obtained through ATIP reveal the excessive lengths to which government went to consult and address private sector concerns. Guided extensively by Blackrock (the world’s largest asset manager) and the finance minister’s industry-led Advisory Council, development of the CIB consisted of extensive discussions with private and institutional investors including about: how Canadian infrastructure could be made more attractive to long-term private sector investment; obstacles to long-term investment in privatized public infrastructure; and approaches to incorporating private sector financing into infrastructure deals (ATI 2016-142, 2016). Of particular note were the months of bi-weekly meetings beginning in the early summer of 2016 between Blackrock, federal ministers, and the Privy Council Office to shape infrastructure policy and inform the Bank’s mid-November debut with leading global investors, including Canadian pension funds. 2 In what appear to be a series of parallel efforts (starting as early as January 2016), the Federal government also began closed door consultations with Canadian pension funds (including Canada Pension and Investment Board (CPPIB), Ontario Teachers Pension Fund (OTFund), OPTrust, Onatio Municipal Employees Retirement System (OMERS), and the Caisse de Depot et Placements de Quebec (CDPQ) to solicit involvement in the Bank (Ljunggren and Scuffham, 2016). According to Heather Whiteside, the ministry of finance also hired consultants from the Bank of America, Meryl Lynch, Morgan Stanley, and Credit Suisse, to help enlist the support of large Canadian pension funds (2017: 226).

The Advisory Council (who for all intents and purposes were handed the task of singlehandedly drafting federal infrastructure policy) was for its part heavily weighted toward financial and private sector interests with significant representation from the pension sector. 3 This was a deliberate strategy to court private and, in particular, institutional capital to infrastructure and to ensure infrastructure policy reflected their objectives. 4 The Council met several times over the summer with senior government officials, including for “deep dives” on what would become the Infrastructure Bank. The stated purpose of these meetings was to ensure alignment with federal policy objectives (ATI 2016-142). Unsurprisingly, the Council’s final report, entitled “Unleashing Productivity Through Infrastructure”, spelled out a national infrastructure strategy focused in its entirety on attracting private and institutional capital into large scale, “productivity enhancing”, “economic development” infrastructure (2016b). The role of the Bank, as outlined in the report, was to deliver on these objectives by curating attractive investment opportunities and brokering the privatization of new (greenfield) infrastructure assets.

“Risk managing” private equity investment

There’s lots of … projects, but they’re all greenfield. So you have this situation where I’ve got huge demand and I’ve got huge supply but I feel like I’ve got an extension cord and I’m a foot and a half short … I can’t plug one end into another because of the risk profile of the eligible investments. (Leech in Porado, 2017: online)

Immediately following the passage of the 2017 budget, and amidst debate about its governing legislation, the Bank was presented to parliamentarians as a way to “risk manage” the development of infrastructure by taking on its financial liabilities to the point where it would become attractive to private capital. In the words of the senior civil servant overseeing its legislative implementation: the Bank is a “risk bridge” (Campbell, 2017: 59), “[ … It is] designed to take the risk and to manage the risk” (Campbell, 2017: 54–57). Borrowing from the Council’s “infrastructure imperative”, this financial configuration was presented to parliament and the public as essential to leveraging financing for projects private investors otherwise “just can’t invest in” (Campbell, 2017: 59); a message quickly reinforced by pension fund investors who insisted that in order for the Bank to attract private capital, it “must … earn a lower rate of return than investors” (Claerhout, 2017: 88).

Indeed, despite their ongoing involvement in the development of the Bank, leading Canadian pension funds consistently expressed significant concern with the “risk and return characteristics” of greenfield infrastructure investment (Machin, 2016) and over the resulting need for “government and institutional investor capital and risk sharing” (Mock, 2016b see also: CPPIB, 2016; Simmons in Scuffman, 2017). Typically, pension funds prefer to invest in infrastructure that is already fully operational with sustainable, proven revenue streams, and well-known liabilities. Greenfield investments, according to analysts, face considerable “front end” liabilities associated with permitting, regulatory issues, initial cost outlays, policy cycles, construction, contracting, and eventual “bankability” that pension funds and other investors typically wish to avoid (Beckers and Stegemann, 2013; Marsh and Mclennan, 2015; Webster, 2017). These in addition to what the pension sector insist is a lack of in-house institutional capacity to administer the front end of infrastructure development, and a distinct lack of confidence in government to oversee these in a timely, cost-effective manner.

Interim materials prepared and circulated (in May, June, July, and August 2016) by the Council suggest particular consideration was given to liabilities associated with investment in new, nation building infrastructure projects, and that the Bank’s design was specifically tailored to reconcile the growth and investment objectives of pension funds with the nation building, extractive objectives of the liberal government (e.g. ATI 2016-142, 2016: 80). To begin, governance of the Bank was deliberately configured to minimize exposure of private capital to the liabilities associated with state involvement in infrastructure planning and development (including threats posed by its regulatory frameworks). Internal documents suggest the Council insisted upon an independent governance structure completely removed in its operations and financial leadership from government (ACEG, 2016b). 5 Claiming that governments lacked the sophistication, directional continuity, and know-how of the private sector, particularly in relation to finance and risk planning, the Council also recommended that Bank leadership be recruited from amongst the elite of the private sector. The Bank was crafted as a private institution with exclusively private sector leadership that takes responsibility for creating and supporting construction and development of national infrastructure opportunities—privatized delivery of national infrastructure projects subsidized by government.

Second, the Bank was explicitly configured such that the state assumes the (financial) liabilities associated with development and early-stage operation of infrastructure projects. On this, the council (and later, the department of finance) could not have been more clear: the Bank’s transactions, as set out in the final report (and subsequently enshrined in legislation), have been deliberately structured to address “early-stage risks” associated with large infrastructure projects (ACEG, 2016b: 63). Consistent with the Council’s proposals, the Bank adopted a wide range of “innovative” financing techniques meant to “share” and “distribute” the “risks” associated with national infrastructure projects, and to offer investors highly tailored, bespoke management of project liabilities (ACEG, 2016a: 80, 85). These include: upfront equity investment to address regulatory requirements (specifically those associated with “risk assessments, social impact analyses, [and] early permitting” (ACEG, 2016b: 63)); adoption of first loss and subordinated equity and loan positions; acceptance of below market returns to enable institutional investors to clear the market; revenue floors beneath which revenue would accrue to private investors; performance bonds; loan guarantees; repayable (and non-repayable) loans; and a host of other credit-enhancement mechanisms to reduce the cost of private sector borrowing.

The CIB has been explicitly configured to risk manage threats to the private sector so as to activate their capital for investment in infrastructure—an arrangement that involves a complicated re-organization of exposure to devaluation of capital invested and to the possibility of below-market returns between the settler state and finance capital. The flipside, of course, to providing what essentially amounts to a massive subsidy to the financial sector is that government can harness private capital to achieve its policy objectives. As one senior pension executive noted: this subsidy makes perfect sense, because unlike the financial sector, “government is not in the business of investing … they are in the business of providing critical infrastructure to their citizens and making sure that the society they create supports growth” (Claerhout, 2017: 92). Privatization of nation-building infrastructure requires nationalization of exposure to capital’s financial liabilities

Materializing jurisdictional entitlement to Indigenous lands

The financial innovations of the CIB are an attempt by the liberal government to secure the extractive economic future of the settler state through legislated, institutional commitment to in their terms “de-risk” infrastructure investment. Settler colonial space, legal scholars suggest, is at best described as a “variegated legal space” of “enclaves and corridors” where colonial authority (the aim of which is territorial acquisition for settlement and extraction (Wolfe, 2006)) remains a work in progress (Benton, 2010: 37–38). Not least due to the countless acts of refusal (such as the long-standing Blockade movement) continually enacted across what is now Canada wherein Indigenous nations repeatedly assert jurisdiction (Simpson, 2017: 35) and strategically and effectively resist imposition of state jurisdiction and extractive projects.

NRI, for its part, materializes a jurisdictional entitlement to Indigenous lands. Greenfield NRI (particularly as cartographed by PDAC) thus epitomizes the production of settler colonial space. Its expansion (which the CIB has been explicitly crafted to encourage) quickens the unidirectional flow of wealth that underwrites the settler state and bears energetically on the state’s ability to make good on its sovereign territorial claims. PDAC analysts, for instance, predict a “twofold impact” if strategic investments in infrastructure are made. First, the costs of exploration would decrease significantly leading to more exploration and more economically viable discoveries. Second, the cost of developing existing “stranded” discoveries (including those not currently viable due to grade) would decrease making their development and production economical (2016b: 5). New mining plays, infrastructure installations, investment activities, enhanced circuitries of trade and transportation, and the proprietary claims that go with them enliven myriad jurisdictional practices and administrative authorities (including federal, municipal, provincial and territorial laws policies, regulations, and processes) on Indigenous lands and help to steadily undermine the ability of Indigenous people to govern their lands. NRI development focuses the authority of the settler state.

Positioning the CIB as an agent in the constant struggle waged by the settler state to exercise sovereign control of Indigenous lands and resources clarifies the political economy of settler colonialism in Canada. Specifically, it provides a window into how the divergent imperatives of the state and private capital are brought into functional alignment given the imperfections of settler colonialism. Sovereign power is organized though jurisdiction and jurisdictional enactments order settler colonial space (Pasternak, 2017: 15). The CIB, whose primary function is to structure private financing and curate national infrastructure deals, works to amplify and produce state jurisdiction; and in so doing, to produce Indigenous lands (for settlers, resource firms, and investors) as singular, sovereign territorial space. It represents a corporate–state–finance modality of risk management that nationalizes exposure to institutional capital’s financial liability while positioning investors (including pension workers) as direct beneficiaries of Indigenous dispossession. Privatized infrastructure development (as I will show in the following section) profitably mobilizes increased forms of economic precarity that link income security and interest income with Indigenous dispossession.

Pension securitization: How the CIB aligns setter workers and investment capital against Indigenous control of Indigenous lands

“Pension securitization” describes the pronounced shift in pension fund investment strategy across the OECD toward ever-deepening exposure to financial markets to “grow” retirement savings—the upshot of which (according to Heather Whiteside) is that pension funds have become “more than just repositories for worker savings, they are private capital actors and major institutional investors within financial markets” (2017: 232), Canadian pension funds foremost amongst them. Beginning primarily in the 1980s and 1990s, and coincident with initial waves of state neoliberalization, pension funds moved away from their initial reliance on non-market investments into capital (and other financial) markets, significantly increasing their investments in corporate equity, stocks, and bonds as well as more complex financial instruments. In the Canadian context, government reforms in the early- to mid-1990s to the pension sector restructured pension funds as arms-length investment boards and mandated funds to invest retirement savings in financial markets. Changes to the Canada Pension Plan Act in 1993, for instance, created the Canada Pension Plan Investment Board (CPPIB) and instructed it to grow plan savings by investing broadly in capital markets so as to seek higher long-term returns than were previously realized (CPPIB, 2018: 12). Until 1999, CPPIB was invested exclusively in non-marketable government bonds. It now invests all net cash flows into the fund and income generated by it in financial markets. As of March 2018, the fund was valued at 365 billion CAD (up from 36.5 billion in 1999) and is invested in Canadian and global equities, fixed income instruments, and real assets (including infrastructure) (CPPIB, 2018: 19). Canada’s top five pension funds (including OMERS, CPPIB, OPTrust, OTPP, and CDPQ) have ballooned in size (in some cases nearly 10-fold) since the early 2000s and hold assets of nearly one trillion CAD.

Perhaps the most significant repercussion of this shift is that, as Suzanne Soerderburg notes, “workers have become increasingly dependent on the economic performance of corporations [in financial markets] for the value of their retirement savings”—and by extension capitalist accumulation and the neoliberalization of relations of production (2011: 224). This dependence dovetails with a neoliberal discourse of workers’ empowerment and the worker/owner (also known as “workers’ capital”) where workers-cum-shareholders/owners of equity seize the opportunity to harness the power of pension funds for the advancement of their (class based) goals as workers and to advance worker welfare through investment in capital markets (Sekerrett, 2018: 22; for a critique see also See also Soerderburg, 2010, 2011; Whiteside, 2017). Despite this discourse, the observed reality of pension securitization has been the mobilization of worker savings on capital markets (as part of an overall redistribution of wealth to the wealth-owning classes (Mahmud, 2015: 73)) and emergence of public pension funds as “active agents and opportunity takers in a world being reconfigured by neoliberal restructuring” (Sekerrett, 2018: 20–21).

“Cannibalistic capitalism” denotes some of the predatory dynamics of pension securitization, and is a concept that “captures the processes by which workers savings in the form of pension funds, feed off both their own indebtedness and that of other workers” (Soerderburg, 2011: 224). Within the context of the neoliberal assault on workers and restructuring of labor markets in the US in which rising rates of poverty have forced new segments of the population into poverty and forced workers to turn to credit to meet the needs of social reproduction, Soerderburg uses this concept to capture the extent to which worker savings (in pension funds) are increasingly dependent on interest income generated through investment in debt instruments that bundle a stream of future re-payments on loans or debt. Pension funds, in her words, literally “prey on those dispossessed workers who, in the absence of a safety net, strive to maintain basic standards through the credit system” (Soerderburg, 2010: 8).

Investment in privatized public infrastructure—in particular, the recent shift by many of Canada’s largest pension funds toward direct (private equity) investment in public infrastructure (documented by Sekerrett, 2018) is an instantiation of cannibalistic capital (see Whiteside, 2017 for a similar assessment), particularly because worker savings are being fueled by investment in privatized public assets, increasingly made profitable by the retrenchment of labor rights. As Whiteside (2017) and others note privatized infrastructure: is more expensive to finance (for taxpayers, since the costs of private borrowing are higher than for governments); involves regressive taxation through profit leaching, tolls, and other income-deflating user fees; threatens the jobs, working conditions, and livelihoods of workers; derives profits and efficiencies from labor cost savings (often involving downsizing, union busting, and sub-contracting); and often results in reduced public access to the services the infrastructure provides. The returns achieved by private investment in public infrastructure are not so much created by the market, as extracted from the populations and workers that depend on them (Sekerrett, 2018: 32).

Here, I explore the dynamic of cannibalistic capital as apolitical opening for thinking through the complex linkages between value extraction, interest income, and Indigenous dispossession. Acknowledging that the CIB (at the time of writing) has yet to make any investments in NRI, I ask what it means to grow settler wealth through investment in privatized NRI? My premise is two-fold. First, the way in which (settler) labor is exploited under capitalism has bearing on how capital and processes of accumulation in turn confront and extract value from Indigenous life. The extreme violence done to Indigenous peoples notwithstanding, the extent to which settler workers are subject to cannibalistic violence makes their stake in the reproduction of the system (including in the success of infrastructure plays and the extractive industries that sustain their value) all the more dangerous to Indigenous peoples and useful to the settler state. Second, pension fund investment embodies not only class power but colonial power too. Property rights and the legitimacy of market rates of return (for instance) that underpin the capitalist accumulation and pension fund securitization (Ghilarducci in Sekerrett, 2018: 33) are as much a product of colonialism as capitalism in Canada and other settler states. Cannibalistic capital (and pension securitization more broadly) considered in light of the “constitutive and continuing role of…colonization … for capitalism” (Byrd et al., 2018) directly links struggles for income security to settler colonialism and interest income to colonial violence.

Value extraction, interest income, and Indigenous dispossession

I begin by highlighting two aspects of cannibalistic capital. First is the paradoxical and deeply pernicious way in which pension securitization (as exemplified by private investment in public infrastructure) configures competing class interests. Neoliberal discourses of worker empowerment notwithstanding common concern with achieving the maximal rate of return on investments and increased dependency of workers on interest income for the security of their retirement has the practical effect of uniting workers (as shareholders and owners) with capitalists. As Sekerrett puts it: in practice “workers capital operates no differently than regular capital, and the workers on whose behalf it is invested are being integrated into the normal process of capturing financial profits out of capitalist production and circulation” (2018: 30). The power of pension funds, he reminds us, is a function of their character as capital (not as the property of workers), 6 the upside of which is that: privately invested pension funds have come to embody—not working class power—but the power of the capitalist class “whose business it is to make the accumulation process work” (2018: 33).

Second, the process of expanding and reproducing capital (worker savings) through the financial system also works to obfuscate the linkages between (class) exploitation and interest income. As capital, tout court, worker capital “shares with regular capital [and the culture of the financial system] an interest in obscuring the underlying social relations of exploitation and expropriations from which financial profits are derived” (Sekerrett, 2018: 30). Cannibalistic capital denotes financial fetishism; a “reification of the social relations that comprise the financial system” (Soerderburg, 2010: 12) that masks the structural violence (of labor) in financial markets including in the ways in which value is extracted and re-distributed as interest income. According to Soerderburg, this involves the production of the financial system as abstract space wherein: “people relate to each other through commodities treated as neutral objects devoid of social power and human content” (2010: 12); social relationships appear as relationships between things (e.g. labor power and money); and financial markets appear as “un real”, wholly separate from the “real” economy (Soerderburg, 2011: 225). Finance, and its products (the revenue it generates for instance) are thereby abstracted from the wider processes involved in their creation and re-creation, including class struggle (Soerderburg, 2011: 225). This abstraction for Soerderburg works to obscure extant linkages between (class) exploitation and interest: “investments are assumed to increase in value over time through a momentum all their own” (2010: 13) and financial markets are purged of class power and social content (2011: 225). Expunged from view are the ways in which both securitization of pension savings, and increased worker reliance on financial markets result from “complex historical forms of struggle between labour and capital” and “intensifying attempts to discipline workers” (Soerderburg, 2010: 12).

The growth of settler savings (wealth) through institutional investment in the type of privatized public NRI favored by the Bank will mean increased reliance of settler workers on the circulation of value in privatized corporate infrastructure ventures and increased dependence on the market value of infrastructure equities and securities. Settler workers, as a result, will have a stronger, deeper (and more pernicious) dependence on the success of infrastructure plays and on the underlying conditions that make them valuable—including the repression of Indigenous jurisdiction over profitable lands and resources. 7 This is especially so considering that the kind of infrastructure ventures targeted by the Bank (all season roads, airports, ports, rail, or the PDAC’s proposed transportation corridors for instance) are a form of fixed capital. The profitability of investment in this type of infrastructure depends on expanded flows of capital around it, otherwise sunk capital becomes devalued and lost (Scott, 2013). Settler workers thus become structurally more invested in, and dependent upon, the expansion and success of the resource extraction economy required to support and fortify their fixed capital.

The CIB as vehicle through which pension fund investors (in addition to sovereign wealth funds, investment Banks, and insurance companies) can expand and reproduce settler worker capital through investment in NRI extends and deepens the ties that bind Indigenous dispossession and Indigenous life to the wealth of settlers and the valued life of capital. And this wealth is not inconsiderable. The top five plans, who rank amongst the top 10 global investors in infrastructure currently manage just shy of one-trillion CAD and collectively have billions invested in infrastructure (CPPIB alone has nearly 4.5 billion, representing 8% of their 365.1 billion in assets). CPPIB currently manages the assets of 20 million workers, the other top five funds each manage the wealth of hundreds of thousands workers respectively. Riffing off of Soerderburg then, pension fund exposure to privatized NRI will contribute to a social reality in which settler workers will have a deeper, more direct political-economic, and personal stake (in terms the security of their future savings) in the extension and expansion of Indigenous dispossession; a reality in which the interests of settler workers are increasingly aligned with the interests of corporate capital and against Indigenous control of Indigenous lands. This is a social reality that more deeply entrenches workers in a system that (profitably) dispossesses Indigenous peoples and that is antithetical to enactments of Indigenous jurisdictional authority.

These alignments also foretell tighter more direct connections between “growth” of settler wealth (interest income derived from investment in infrastructure) and Indigenous life. Most critiques of financialization involve demonstration of the linkages between circulation in financial markets and production to show that value does not in fact grow on trees, but is extracted and redistributed–forcefully and violently in the material practices of production and exchange (Bryan et al., 2009; Labban, 2010; Mann, 2010; Sekerrett, 2018; Soerderburg, 2010, 2011). Labban has perhaps most convincingly shown how circulation in financial markets is not only linked to the space-time of production and exchange in which the violence of labor occurs but that it in fact intensifies this violence resulting in increased squandering of human material. Circulation in financial markets requires retrenchment in geographies of production from which ever more value has to be squeezed (2010).

The CIB (if successful) will raise settler wealth (by means of workers forced savings, invested by pension fund investors) from an increasingly disciplined labor force in order to finance privatized public infrastructure. Should all go according to plan, investors (pension funds and settler workers) will likewise be extracting value (in interest income and market rates of return) in part from retrenchment of (their own) labor rights, and (their own, and others’) reduced incomes as labor is increasingly disciplined under neoliberalism. But value will also derive in large part from the uncompensated proprietary interests of Indigenous peoples all over Canada—and relatedly the denial and repression of Indigenous jurisdiction and the contemporary social processes, including criminalization of acts of land defense that help to undermine Indigenous jurisdiction. These are the contemporary, continuing conditions of possibility for accumulation in Canada whose reproduction becomes more urgent as investment in privatized NRI increases. So too for the expansion of the resource economy needed to secure and fortify the profitability of infrastructure as an investment. The list of material reconfigurations from which value is violently extracted is long. In addition to those above, value derives from: reduced Indigenous control over treaty and non-treaty lands and resources; destruction of Indigenous economies and systems of social reproduction; theft of the ability to act and govern (Pasternak, 2017: 123); ecological destruction (including toxic contamination, ecosystem disruption, and human and non-human death) in which life processes are put to the task of sustaining the valued life of capital rather than the living beings and economic/ecological systems to which they originally sustained (see Stanley, 2015); dispossession by removal of lands or people (see Pasternak, 2017); militarization of state responses to enactments of Indigenous jurisdiction (including land defense); and in general acts that in Shiri Pasternak’s terms, “dimini[sh] the capacity of [Indigenous] communities to reproduce social, economic and legal orders” (2017: 26).

Concluding remarks: Predatory value and colonial capitalism

Consideration of the often divergent interests of the settler state and private capital and the ways in which they—and the material geographies they bring into play—come into alignment through the creation of the CIB provides an opportunity to examine how colonialism works in Canada, as well as how settler colonial regimes in Canada are coproduced in relation to capitalism and neoliberalism (Dafanos and Pasternak, 2018). This example also provides an opportunity to consider the extent to which producing and asserting jurisdiction and sovereignty exhaustively inflects Canadian financial institutions—especially as Indigenous resistance to infrastructure violence (like the closing of Wet’suwet’en territories against coastal gas link and Secwepemc opposition to the Trans Mountain expansion pipeline) reveal considerable economic consequences for the settler state. These acts of refusal are expressions of Indigenous law, rooted in Indigenous sovereignty and jurisdiction and exemplify the extent to which Jurisdiction in Canada is far from settled. Here, I have argued that the CIB effects a series of alignments between private capital and the settler state and between settler workers and capital and against Indigenous peoples that will help to organize settler state authority and produce colonial space.

On another level, this paper speaks to a growing body of scholarship on racial and colonial capital to suggest that the Canadian economy is an economy of dispossession in the sense that it is configured by “multiple and intertwined genealogies of racialized property, subjection, and expropriation” that co constitute both its material fulcrum (modes and relations of production) and organizational logics (Byrd et al., 2018: 2). Indigenous dispossessions (and related but also different settler possessions), in other words, are constitutive of, not residual to, value formation in the settler state. Colonization serves as a condition of possibility in Canada for the values that circulate in and are extracted from investment in the resource economy (and its infrastructure) and a fulcrum for leveraging value at the expense of Indigenous land and life. If as Byrd et al. (2018: 2) recently suggest: “Indigenous dispossession continues unabated to provide the logics that order power, violence [and] accumulation” then value derived from investment in and through all season roads, expanded trade and transportation corridors and northern electrification schemes accrues first and foremost from subordination of Indigenous life to the pursuit of profit.

Footnotes

Acknowledgements

I am very grateful for the comments of Natalie Oswin and three anonymous reviewers. Many thanks for their helpful suggestions and invitation to improve on the manuscript. All errors and omissions are of course my own.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.