Abstract

Infrastructures are never neutral; they reflect social priorities, institutional silences, and unequal entitlements to safety. This article explores how disaster governance practices contribute to the differentiated distribution of vulnerability and the systematic neglect of marginalised lives. Through a comparative case study of the Grenfell Tower fire in the United Kingdom and the Grand Kartal Hotel fire in Turkey, we examine how institutional breakdowns interact with austerity, outsourcing and technocratic accounting regimes to both produce harm and obscure responsibility. Grounded in critical urban theory and interpretive approaches to accounting, we propose the framework of Inequality-Responsive Accounting, which conceptualises accounting as a spatial and political instrument shaped by broader power relations. The framework introduces five interrelated tools: vulnerability mapping, accountable regulation tracking, chain of responsibility audits, spatial equity budgeting and redistributive risk accounting. These tools enhance institutional responsiveness to marginalised groups and disrupt procedural routines that displace substantive accountability. Our analysis shows how accounting systems act as selective mechanisms of recognition and exclusion, influencing whose lives are safeguarded and whose are treated as expendable. By tracing the political geographies of disaster governance, the article highlights how infrastructural inequality is sustained through ostensibly routine institutional operations.

Keywords

Introduction

On 14 June 2017, a fire engulfed Grenfell Tower, a high-rise social housing block in West London, resulting in the deaths of 72 residents (MacLeod, 2018). Less than a decade later, on 21 January 2025, a fire swept through the Grand Kartal Hotel in Bolu, Turkey, claiming the lives of 78 individuals, many of them workers and local tourists (De Ruiter, 2025). Although occurring in distinct socio-political contexts, both disasters share troubling similarities: they exposed systematic failures in regulation, the hollowing out of safety regimes, and the devastating consequences of institutional neglect. Crucially, they also revealed how risk and vulnerability are disproportionately distributed, affecting those already marginalised by race, class, political ideology, migration status and spatial disadvantage.

Disasters are often misrecognised as natural or technical occurrences. Yet, there is a growing recognition that their human toll is shaped less by the hazards themselves than by the pre-existing inequalities into which they erupt (Reid, 2013; Wisner et al., 2004). Grenfell and Grand Kartal illustrate what happens when the burden of safety is offloaded onto structurally disadvantaged populations, and when governance systems fail to see and account for the unequal social conditions that determine who is protected and who is exposed. In such settings, traditional forms of accounting, which focus on financial compliance, asset-liability management, or post-event cost assessment, prove woefully inadequate in revealing or addressing the deeper structural inequalities and global challenges that shape vulnerability (Carnegie et al., 2024). Although conventionally reduced to financial reporting, compliance, and the reconciliation of accounts, critical accounting perspectives reframe accounting as a broader set of practices that extend beyond the ledger. Audits, inspections, and regulatory reviews can all be understood as expressions of accounting logics, insofar as they constitute mechanisms that render activities visible, attribute responsibility, and selectively conceal breakdowns or failures (Hopwood and Miller, 1994; Özbilgin et al., 2016). Rather than existing outside the domain of accounting, these practices exemplify its reach: they inscribe what counts as evidence, whose accounts are acknowledged, and how accountability is distributed. Recognising this expanded remit underscores the entanglement of accounting with accountability, and explains why such procedures are theorised here as accounting devices rather than merely regulatory instruments.

We argue that accounting plays a central yet under-examined role in the governance of disaster risk. By deciding what to measure, disclose and prioritise, accounting practices can either challenge or reinforce the unequal distribution of risk. Yet, in both cases examined here, these accounting processes persistently failed to register the multiple and intersecting vulnerabilities of the affected populations. In Grenfell, these included working-class families, minoritised groups, people with disabilities and undocumented migrants (Gohil, 2024). In Grand Kartal, the victims were primarily precarious workers and transient populations rendered invisible by informal labour markets and opaque governance structures (Karşı Mahalle, 2025). These omissions were not accidental; they reflect what Cooper (2015) refers to as the politics of what is accounted for. This article situates accounting within the infrastructures of urban inequality, showing how it shapes differential exposure to harm through mechanisms of visibility, omission and selective valuation.

In response to the structural failures identified in both cases, we propose a conceptual model, Inequality-Responsive Accounting (IRA), that reconceptualises accounting not as a neutral technical instrument but as a mechanism with the potential to either reproduce or redress vulnerability. The IRA framework comprises five interrelated interventions that position accounting within the spatial logics of disaster governance: (1) accountable regulation tracking examines how safety regulations are implemented, bypassed or selectively enforced across uneven regulatory geographies, revealing jurisdictional gaps and enforcement disparities; (2) co-designed vulnerability mapping integrates disaggregated sociodemographic data into risk assessments to expose how vulnerability clusters in specific places, making visible the demographic geographies of harm; (3) chain of responsibility audits clarify lines of accountability within multilevel and spatially fragmented governance arrangements, where diffusion of responsibility often coincides with spatial distancing from sites of risk; (4) spatial equity budgeting evaluates how resources for risk mitigation and safety infrastructure are distributed across territory, interrogating whether these allocations reproduce or challenge spatial inequalities and (5) redistributive risk accounting calls for equity-based principles in the distribution of protection, recovery and resilience measures, attending to how spatial and social asymmetries shape both exposure to harm and access to institutional response. Together, these interventions advance an approach to accounting that is ethically informed and transformation-oriented, seeking not only to make inequality visible but to disrupt the institutional practices through which it is maintained (Dillard and Vinnari, 2019; Neu et al., 2018).

To ground the IRA framework empirically, we present a comparative case analysis of the Grenfell Tower and Grand Kartal Hotel fires. Drawing on public inquiry reports, planning and audit documents, survivor testimonies, and secondary data, we demonstrate how accounting failures were central to both the production of vulnerability and the erasure of responsibility. While the two cases differ in institutional form and national context, both illustrate how formal systems of governance and accountability can bypass the lives and needs of those most exposed to harm. We argue that disaster governance without an explicit accounting for inequality is ineffective and complicit in the perpetuation of harm.

Accounting practices in disaster governance often appear as technical oversights or isolated failures. We frame these failures as systemic expressions of infrastructural violence, manifested through accounting practices that selectively register risk, obscure inequality and institutionalise disregard for marginalised lives. In this article, we make three key contributions. First, we conduct a comparative case analysis that reveals how institutional neglect is reproduced across contrasting political and regulatory environments. Second, we develop a conceptual framework, IRA, that redefines accounting as an instrument for confronting structural inequality within disaster governance. Third, we propose a set of actionable accounting interventions, including co-designed vulnerability mapping and spatial equity budgeting, that offer concrete pathways for advancing more inclusive and justice-oriented approaches to disaster risk management.

Throughout this article, we refer to visibility, representation and recognition as interrelated yet analytically distinct dimensions of inequality. By visibility, we mean the extent to which marginalised groups and their risks are made legible within accounting systems and institutional discourse. For example, in the aftermath of the Grenfell Tower fire, official accounting systems focused on the number of confirmed deaths and the financial costs of rehousing survivors, while largely obscuring the long-term health, trauma and community displacement experienced by residents. By privileging what could be numerically tallied, these accounting practices shaped the public narrative of the disaster and the distribution of institutional responsibility (Funnell and Jupe, 2022). Representation refers to how these groups and their experiences are portrayed or categorised, often reductively, within official records and regulatory frameworks. Recognition, drawing on Fraser (2000) and Bhattacharyya (2018), captures the normative and political imperative to affirm the dignity, agency and structural positioning of those rendered vulnerable. Where visibility without recognition may lead to surveillance or tokenism, and representation without visibility may result in symbolic inclusion, we argue that inequality-responsive accounting must integrate all three to disrupt structural erasure and promote justice.

The article proceeds as follows: first, we review existing literature on accounting and vulnerability, highlighting the limits of current accounting frameworks in addressing structural risk differentials. We introduce the Grenfell and Grand Kartal cases, providing context and rationale for their comparative analysis. Then, we present the theoretical underpinnings and components of the IRA framework. Applying this framework empirically to the two cases, we illustrate the consequences of accounting absence and distortion. The article discusses the broader implications of the IRA for accounting research, policy and practice. We call for a more just and inclusive approach to accounting in disaster and risk governance.

Accounting and the social production of vulnerability

Critical accounting has long been positioned as a tool for rendering visible operations of organisations, institutions and states, interrogating what, and who, gets counted (Cooper, 2015; Miller and Power, 2013). In contexts of risk, safety and disaster governance, accounting can either illuminate structural inequalities or obscure them through selective valuation and omission. Increasingly, scholars in critical accounting and adjacent fields have begun to interrogate how accounting practices contribute to the social production of vulnerability: that is, how marginalised populations are made more precarious through the very systems that purport to measure and manage risk (Dillard and Vinnari, 2019; Neu et al., 2018; Walker, 2016). Urban political geography deepens this critique by analysing how governance structures obscure structural risks through spatial and institutional practices. Pile et al. (2023) demonstrate that post-political regimes sustain appearances of openness while instituting forms of closure that suppress contestation and depoliticise harm. Instruments such as accounting and audit functions within these regimes are not neutral devices, but as mechanisms that selectively distribute visibility and defer political accountability. Critical accounting scholarship builds on comparable concerns, showing how accounting practices are embedded in broader configurations of power that determine which harms become institutionally intelligible and which are excluded from recognition. Recent critical accounting literature challenges the idea that accounting is an objective or apolitical practice (Tanima et al., 2024). Instead, it situates accounting within broader structures of power and inequality, arguing that accounting systems often reflect and reproduce dominant social logics, particularly those aligned with neoliberal governance, marketisation and managerialism (Arnold and Cooper, 1999; Spence, 2009). In disaster settings, this manifests in multiple ways. For instance, public audits of disaster response may focus on the cost-efficiency of emergency interventions, while remaining silent on the unequal precarity of those who suffered most. Similarly, building safety inspections may confirm regulatory compliance without accounting for the racialised geographies of housing degradation or the long histories of tenant disempowerment that shape everyday risk exposure (Graham, 2012).

Recent scholarship in disaster governance has moved beyond simply establishing that disasters are socially constructed, to interrogating how risk and emergency are performatively constituted through discourses, practices and institutional arrangements. Adey et al. (2015) and Anderson (2017) showed how naming an event as an emergency is not neutral, but mobilises specific state capacities while foreclosing others, shaping both visibility and response. O’Grady's work (2016, 2018, 2025) demonstrates how fire risk is assembled through technologies, protocols and security practices, producing particular logics of preparedness and neglect. Similarly, Simon (2016) and Eriksen and Simon (2017, 2025) highlight how fire risk is entwined with processes of urban development and socio-spatial inequality, generating what they call an affluence–vulnerability interface. Cooper and Whyte (2022) extend this critique to Grenfell, framing austerity and neglect as forms of slow institutional violence that accumulate into catastrophe. Bringing these insights into conversation with critical accounting underscores how accounting devices do not merely record risk but participate in constructing emergencies, distributing accountability, and shaping whose vulnerabilities are acknowledged.

The failure to embed sociodemographic dimensions into accounting systems has particular implications for disaster governance. Vulnerability to disasters is not randomly distributed; it is shaped by factors such as income, race, gender, immigration status, disability, age, proximity to power and geography (Cutter et al., 2003; Wisner et al., 2004). In addition to these structural determinants, from a social–ecological perspective, community cohesion is a key determinant of preparedness and adaptive capacity, shaping how hazards translate into harm (Prior and Eriksen, 2013). Yet traditional accounting systems, particularly those oriented towards compliance or performance management, rarely engage with these axes of inequality (Agyemang et al., 2024). As Shaw (2019) argues, austerity enacts a form of spatial violence through the gradual dismantling of public infrastructures and the displacement of care. This perspective helps illuminate how disasters like Grenfell and Grand Kartal were abrupt anomalies and outcomes of a slow erosion of state responsibility and spatial justice. Instead, they often treat populations as homogeneous units, such as households, residents or occupants, thereby erasing the differentiated capacities of individuals and communities to prepare for, respond to or recover from disasters (Neu et al., 2022). This is what Bhattacharyya (2018) terms the violence of abstraction: the rendering of difference illegible in the name of bureaucratic order.

Recent advances in feminist, post-colonial and decolonial scholarship on accounting have brought much-needed attention to these silences (Kyriakidou et al., 2016; Manning, 2021). Feminist scholars, for example, have argued that accounting must contend with the gendered and racialised division of care and risk, particularly in households and communities where women and girls shoulder disproportionate burdens in the wake of disaster (Dambrin and Lambert, 2008; Haynes, 2008). Others have highlighted the coloniality of accounting systems that fail to recognise the knowledge, practices, and needs of indigenous, migrant, or stateless populations (Gallhofer and Haslam, 2019). These critiques underscore a growing consensus: that the marginalisation of vulnerable groups is not simply a failure of implementation but a feature of accounting design itself.

Within the domain of public sector accounting, this omission is further exacerbated by a reliance on performance metrics that prioritise fiscal control and service delivery over social equity or distributive justice (Broadbent and Laughlin, 2005; Ezzamel et al., 2004). Disasters are therefore assessed in terms of whether response budgets were met, shelters were opened, or compensation was disbursed in aggregate figures, while questions about whose lives were rendered most precarious are sidelined. These approaches flatten differences and obscure how the very systems intended to prevent harm, such as fire safety inspections, housing audits and regulatory controls, are often designed and implemented in ways that exclude those most at risk.

Calls for a critical and inclusive accounting have begun to emerge in response. Dillard and Vinnari (2019) advocate a shift in accounting from simply representing stakeholder interests towards a more inclusive and ethically informed approach to accountability, which engages actively with social, ecological, and moral concerns and resists reinforcing dominant power structures. Neu et al. (2018) argue for accounting practices that attend to the marginalised needs, seeking out the voices and experiences that standard systems of measurement render invisible. In the context of disaster governance, this means moving beyond post hoc evaluations of response and towards a proactive engagement with the systems that produce differential risk exposure.

While important contributions have explored the intersections of accounting and crisis (Bhimani, 2008; Leoni et al., 2021), existing approaches often focus on the wider impact of crises rather than on how accounting practices participate in the reproduction of structural and sociodemographic inequalities. In this article, we advance an alternative approach that foregrounds the role of accounting in rendering certain populations invisible and unaccounted for in disaster planning, risk assessment and post-crisis evaluation. This approach provides both conceptual and practical tools for developing a more politically attuned and socially responsive form of accounting. In the sections that follow, we draw on prior scholarship to show how conventional accounting practices contributed to the marginalisation of structurally vulnerable groups in the Grenfell and Grand Kartal disasters. We then outline a normative intervention aimed at reimagining accounting in ways that are sensitive to the politics of inequality, difference and voice.

Case contexts: Two fires, shared patterns of neglect

The Grenfell Tower fire in the United Kingdom and the Grand Kartal Hotel fire in Turkey unfolded in different geographical, political and regulatory settings. Yet both disasters illustrate how socio-spatial inequality, deregulation and institutional neglect coalesce to produce lethal outcomes, particularly for minoritised and economically disadvantaged populations. These cases provide a fertile empirical foundation for examining how accounting practices (and their silences) intersect with the social production of vulnerability.

Grenfell Tower: Neglect in the heart of the metropolis

Grenfell Tower stood in North Kensington, one of the most deprived wards in London, surrounded by extreme affluence. Originally built in 1974 as social housing, the tower was home to over 300 people from more than 20 nationalities. Many residents were racialised minorities, migrants or recipients of state assistance. They lived within a local authority, Kensington and Chelsea, that had increasingly outsourced housing management and embraced austerity measures that undermined investment in building safety (Hodkinson, 2020; Ministry of Housing, Communities & Local Government, 2018). Between 2012 and 2016, Grenfell Tower underwent a significant refurbishment project led by the Kensington and Chelsea Tenant Management Organisation (KCTMO), which had been delegated responsibility by the Royal Borough of Kensington and Chelsea (RBKC), which is one of the wealthiest neighbourhoods in the world (Grenfell Tower Inquiry, 2025). Central to the refurbishment was installing aluminium composite cladding with a polyethene core, an inexpensive yet highly flammable material. The cladding's use was justified through questionable certifications, insufficient oversight and a cost-cutting logic prioritising appearance and efficiency over safety (Booth, 2017). Alongside cost-cutting on cladding, the RBKC simultaneously invested in other highly visible local projects, such as the renovation of a nearby church site (Bulley et al., 2019). This contradictory allocation of resources reflects what Collier (2025) terms the disaster contradiction of contemporary capitalism, where austerity and neglect in some domains co-exist with selective investment in others, producing uneven geographies of care, visibility and abandonment.

The catastrophic result of intersecting failures unfolded on the night of 14 June 2017: inadequate fire safety regulations, a fragmented inspection regime and a governance structure that insulated decision-makers from accountability. More than 70 lives were lost. In subsequent public inquiries, it became clear that residents’ warnings, many of which explicitly raised concerns about fire risks, had been ignored or dismissed as administrative nuisances. Furthermore, post-disaster audits and official reports frequently referred to residents in generic terms, such as occupants, tenants and households, failing to reflect the demographic complexity and vulnerability of those affected (Shildrick, 2018).

The Grenfell Tower case illustrates how risk governance in neoliberal urban regimes operates through the individualisation of responsibility, whereby institutions shift the burden of risk onto individuals under the guise of compliance and market rationality (Shamir, 2008). It also highlights how accounting for safety and risk, via building inspections, compliance documents and regulatory filings, can simultaneously obscure the racialised and classed geographies of hazard exposure. Moreover, this logic of responsibilisation extends beyond risk governance, as neoliberal regimes consistently displace structural accountability onto individuals, thereby deflecting attention from systemic causes and limiting the scope for collective remedies (Vincent et al., 2024). Yet reading disaster governance solely through the lens of responsibilisation risks oversimplifying a more contradictory landscape. As Collier (2025) argues, contemporary capitalism produces a disaster contradiction, in which austerity and neglect in some areas co-exist with targeted investments that bolster state visibility, legitimacy or selective publics. O’Grady and Shaw (2023) similarly show how resilience discourses simultaneously mobilise responsibility and enact abandonment, producing uneven relations between government agencies and affected communities. Overall, these insights suggest that the politics of disaster governance cannot be reduced to individualisation alone but must be understood as a dynamic interplay of retrenchment, selective investment, and differentiated forms of care and neglect.

Grand Kartal Hotel: Precarity at the urban periphery

Originally built in 1978, the Grand Kartal Hotel was established in the late 1990s, during a period of rapid expansion in Turkey's tourism sector, particularly in regions promoted for their natural beauty and seasonal appeal (Gazete Oksijen, 2025). Located in Kartalkaya, a ski resort area within the Bolu province, the hotel became a central part of local winter tourism infrastructure. Over the years, the region witnessed intensified commercialisation and deregulation, with hotel operators capitalising on rising demand while public oversight mechanisms remained weak and fragmented. Much like broader trends in Turkey's neoliberal transformation, public functions such as safety inspections, licensing and oversight were increasingly outsourced or rendered symbolic, often serving more to legitimise development than to ensure public safety.

On 21 January 2025, a fire broke out at the Grand Kartal Hotel in Bolu, a Turkish city known for its winter tourism. The fire, which began in the hotel's basement and quickly spread through poorly compartmentalised upper floors, resulted in the deaths of 78 people and injured many others. Among the victims were foreign tourists, internal migrants working in the service sector, and undocumented hotel staff who had been housed informally in unsafe quarters. Despite previous fire safety warnings and reports of illegal modifications to the building, no substantive regulatory intervention had occurred before the disaster (Cursino and Armstrong, 2025; Giuffrida, 2025). Post-disaster investigations revealed a pattern of institutional abdication. Hotel owners exploited regulatory loopholes and relied on a patchwork of fire inspection reports, many of which had been falsified or outsourced to private firms with minimal oversight. Emergency exits were blocked, smoke detectors were non-functional, and combustible materials were widely used in renovation works, all contravening safety codes (Gürbüz and Göder, 2025; Öztürk, 2025). Yet state actors and regulators engaged in public performances of compliance rather than substantive enforcement, mirroring trends of deregulatory statecraft seen elsewhere in the Global South (Dubash and Morgan, 2013). Drawing on Anderson's (2021) analysis, such performative governance may be sustained through affective atmospheres like boredom, an ambient disengagement that both registers public disaffection and blunts collective critique. In this way, institutional neglect becomes routinised, rendered unremarkable through the very affects it provokes. Austerity does not function as a neutral fiscal tool; it spatialises harm by disproportionately withdrawing public care and resources from already marginalised communities (Shaw, 2019).

What distinguishes Grand Kartal is the informal and precarious status of many of the deceased (Karşı Mahalle, 2025). Because of their undocumented or temporary employment status, many were not initially listed among official victims. Media and official discourse tended to focus on visitors rather than workers, erasing the intersecting vulnerabilities of those killed. This disrupted identification and compensation processes and also pointed to a broader problem: the absence of demographic data collection and reporting systems capable of recognising and addressing structural risk inequalities.

While Turkey's regulatory context differs from that of the United Kingdom, the underlying dynamics, outsourcing of public functions, inadequate enforcement and the marginalisation of vulnerable groups, resonate strongly with Grenfell. In both cases, institutional records, audits and compliance regimes failed to register the presence and precarity of those most at risk.

Comparative insight: Risk, inequality and the silence of accounting

The juxtaposition of these two cases reveals a shared architecture of neglect across political and economic systems. Both disasters occurred not in the absence of regulation, but amid an abundance of technical documentation, risk assessments, safety certificates and audit trails that were either falsified, gamed or rendered irrelevant by structural disregard for inequality. Formal accounting systems in both contexts privileged material traceability while sidelining broader forms of social responsibility, emphasised compliance in ways that displaced substantive care, and elevated metrics that obscured rather than illuminated meaning.

Crucially, neither case included a systematic account of the populations most affected. In the Grenfell case, some demographic information was available. For instance, RBKC records acknowledged that more than 20 nationalities were represented in Grenfell Tower, and accessibility requirements were part of public housing regulations. Yet, there was no consolidated or mandated system for integrating such data into safety planning, resident registries or evacuation strategies. As the Inquiry highlighted, there was no single record of who lived in the building at the time of the fire (Grenfell Tower Inquiry, 2019: 20), meaning that migration status, disability and other relevant indicators were not systematically captured or operationalised in ways that could have informed risk management or emergency response. Ideally, such a mandate would have applied to the building owner or delegated management body, such as the Tenant Management Organisation in the case of Grenfell, with an obligation to submit this information to local housing authorities and national regulators. Embedding such reporting within official registries and oversight mechanisms would have ensured that the sociodemographic vulnerabilities of residents were made institutionally visible rather than remaining unrecorded. In the Grand Kartal case, hotel management prioritised residents of executive suites, who were alerted and other residents were not alerted to leave their rooms. In this context, a comparable mandate would have required hotel operators to keep accurate registries of all residents and staff, including those in informal accommodation, and to submit these to municipal authorities and fire safety regulators. Further, fragmented subcontracting and informal housing arrangements made it nearly impossible for state officials to identify who had died in the immediate aftermath. These omissions were not simply technical or administrative lapses; they illustrate how institutions can acknowledge inequality in discourse while failing to take meaningful action to address it (Puwar, 2004). We develop the IRA framework as a response to these failures. The IRA framework seeks to embed sociodemographic visibility, redistributive logic and intersectional ethics at the heart of accounting for risk and disaster.

Methods

We use a comparative case study approach (Bartlett and Vavrus, 2016) to explore how accounting systems engage with structural inequality in the context of disaster governance. This approach helps reveal convergent mechanisms of symbolic compliance and institutional neglect across divergent regulatory regimes. Following their emphasis on tracing power across scales and contexts, we examine how similar logics of institutional neglect and symbolic compliance emerge in distinct regulatory and political settings. Rather than treating Grenfell and Grand Kartal as isolated cases, we approach them as sites through which to trace institutional rationalities that travel across space through models of governance, audit cultures and managerial abstraction. We build on the interpretive tradition in accounting research, which seeks to understand how accounting operates within broader social and institutional contexts, rather than as a neutral technical practice (Chua, 1986). Comparative case studies provide a robust methodological lens for uncovering how conflicting institutional pressures and accountability failures manifest across contexts that are structurally different, yet functionally comparable (Rautiainen, 2010). Our focus is on two major fire disasters: the Grenfell Tower fire in the United Kingdom and the Grand Kartal Hotel fire in Turkey. We chose these cases not because they are rare or extreme, but because they are disturbingly representative. Both reveal how deregulated risk regimes, the invisibility of vulnerable populations in formal accounting systems, and systemic failures of accountability can converge to produce deadly outcomes.

Case selection and comparative strategy

Our comparative strategy is grounded in the principle of structured, focused comparison (George and Bennett, 2005), which enables us to examine how similar patterns of inequality and erasure manifest across distinct governance systems. Rather than seeking statistical generalisability, we aim for theoretical generalisability: the development and testing of a normative accounting framework, the Inequality-Responsive Accounting (IRA) model, capable of illuminating shared mechanisms of risk, exclusion and institutional denial.

By juxtaposing a high-income welfare state (the United Kingdom) with a middle-income emerging economy (Turkey), the study examines how accounting's role in risk governance travels across contexts and is shaped by national variations in law, regulatory culture and political economy. Both cases reveal different forms of failure, outsourced housing management in Grenfell, and informality and inspection capture in Grand Kartal, but similar logics of neglect and invisibilisation.

Data

Between February and April 2025, we identified and reviewed 127 unique documents, of which 71 are on Grenfell and 56 on Grand Kartal which will be placed on an open electronic repository. We targeted publicly accessible materials that offered insight into five key domains of disaster risk governance: regulatory oversight, legal proceedings, spatial and planning documentation, policy and budgetary instruments, and media reports or survivor testimonies. We sourced these documents from government websites, court archives, urban planning portals, independent inquiries, news databases and non-governmental organisation (NGO) repositories. Our review included official inquiry reports (such as the Grenfell Tower Inquiry Phase 1 (2019) and Phase 2 (2025) reports, the Grand Kartal public investigation and expert reports), fire service and regulatory agency documentation, legal texts including building codes, fire safety legislation, housing acts and civil contingency frameworks from both jurisdictions, as well as policy reports from governmental and NGOs. We also incorporated media and professional associations’ investigations and survivor testimonies where they featured in legal or inquiry processes, alongside relevant academic and grey literature on disaster governance and regulatory failure. We excluded brief news announcements, duplicate entries and opinion pieces lacking evidentiary support.

We used a structured analytical guide to code each document. This guide helped us trace patterns of regulatory neglect, demographic invisibility, institutional outsourcing, spatial marginalisation and policy austerity. We developed these categories based on our interest in how accounting mechanisms often fail to register, and sometimes erase, the risks faced by marginalised communities. To verify our findings, we cross-checked key claims across different document types, for instance, comparing official statements with court filings and survivor testimonies. We also created detailed timelines for both disasters to situate key events within their political and regulatory contexts. This allowed us to uncover how accounting failures emerged not only during the crisis response, but also through long-standing patterns of institutional neglect. Through this approach, we aimed to show how accounting practices actively shaped conditions of vulnerability, before, during and after the disasters.

Analytical approach

In our comparative analysis of the Grenfell Tower and Grand Kartal Hotel fires, we applied Lindsay Prior's (2002, 2008) documentary analysis method to interrogate how institutional texts produce, reproduce or obscure systems of accountability. Following Prior's conceptualisation of documents as active agents in the construction of organisational meaning rather than passive containers of information, we examined inquiry reports, legal and planning documents, and survivor testimonies as socially situated artefacts. This approach allowed us to explore not only the content of the documents but also their institutional authorship, circulation and silences, thereby revealing how accounting omissions and demographic erasures are embedded within bureaucratic routines and governance logics.

Our analysis proceeds in two stages. First, we constructed individual case narratives for Grenfell and Grand Kartal, guided by three central questions: Who was rendered vulnerable, and how was this reflected (or omitted) in institutional data? How were resources for safety and risk management allocated, and to whom? What forms of public disclosure and post-disaster accounting occurred, and how did they represent affected populations? These questions directly map onto the three pillars of the IRA framework: accountable regulation tracking, vulnerability mapping, chain of responsibility audits, spatial equity budgeting and redistributive risk accounting. Second, we applied the IRA framework comparatively, identifying patterns of convergence and divergence across the two cases. This allowed us to test the framework's capacity to illuminate institutionalised inequality, its potential for cross-contextual application, and its contribution to rethinking accounting's role in disaster governance.

While we rely primarily on public inquiry reports, legal documents and regulatory filings, we recognise that these state-authored documents are not neutral accounts but are shaped by institutional interests, legal constraints and political agendas. As Prior (2002, 2008) cautions, documents must be understood not only for what they contain but for how they function within systems of power. Accordingly, our analysis treats these texts as partial and situated artefacts that reflect dominant logics of risk, responsibility and visibility. This positionality is crucial in interpreting the silences, abstractions and omissions that pervade official narratives, particularly concerning marginalised groups whose experiences are often underrepresented or selectively framed. Documentary analysis may exclude informal, oral or undocumented knowledge, particularly from minoritised or undocumented populations (Prior, 2002). However, in both cases, survivor testimonies were embedded within formal inquiries, allowing some of these perspectives to inform our analysis. Additionally, while media sources can introduce bias, we mitigated this by focusing primarily on documents produced through legal, regulatory or parliamentary processes.

Comparative analysis: Shared architectures of institutional neglect

Despite their divergence in geographic, political and regulatory settings, the Grenfell Tower and Grand Kartal Hotel fires manifest a striking convergence across five interrelated domains: regulatory neglect, demographic invisibility, institutional outsourcing, spatial marginalisation and policy austerity. Each domain operates not in isolation but as part of an overlapping architecture of institutional abandonment, whereby formal mechanisms of risk governance obscure, rather than address, the structural vulnerabilities of minoritised and precarious populations.

Regulatory neglect

In both cases, regulatory neglect was not a matter of legal absence but of active disengagement and performance-based governance. At Grenfell Tower, the cladding materials used during refurbishment, specifically, the polyethylene-cored aluminium composite material, were known to be flammable, yet were approved due to failures of due diligence and cost prioritisation. The Inquiry noted, ‘Nobody at Rydon [the main contractor] appears to have given any thought to whether the materials…met the requirements of the Building Regulations’ (GTI Phase 1, 2019: 582). Certification processes failed to account for material variations in fire safety, deferring risk assessment to contractors: ‘Arconic had chosen to withhold the results of Test 5B from the BBA (British Board Agreement) … As a result of its decision not to do so, the BBA certificate was thoroughly misleading, because it failed to draw a distinction between the two fixing systems in relation to fire performance’ (GTI Phase 2, 2025, Vol. 2, 19.5: 27). Moreover, regulatory bodies relied on manufacturers’ self-reported data, resulting in certifications that ignored critical safety distinctions: ‘The BBA certificate was … issued on the basis that it applied generically to the product, despite significant evidence that fixing methods altered fire performance’ (GTI Phase 2, 2025, Vol.2, 19.4: 27).

Similarly, in Grand Kartal, investigators found that mandatory fire inspections were either falsified or bypassed entirely. Court investigations revealed that fire safety reports were prepared without field inspection and only on paper, with GPS tracking data confirming that inspection vehicles never visited the hotel on claimed inspection dates, while official reports documented that ‘the inspection method has been carried out as a customary practice since the establishment of Bolu Provincial Special Administration’ (Bölükbaş, 2025; Özalp, 2025). These were not simply failures of enforcement; they reflected deeper logics of deregulatory governance, where the appearance of compliance supplanted substantive oversight (Power, 1997; Shamir, 2008).

Demographic invisibility

The governance void was compounded by demographic invisibility. In both disasters, those most affected were already marginalised within dominant social hierarchies. At Grenfell Tower, tenancy data was patchy and failed to include crucial demographic variables. The Inquiry found ‘no central record of who was living in the building at the time of the fire’ (Grenfell Tower Inquiry, 2019: 20). Here, ‘central’ referred not to the national government, but to the absence of a consolidated resident registry at the level of the RBKC and its delegated housing manager, KCTMO. Responsibility for tenant and safety records rested with these local bodies, yet the fragmented governance structure meant that no single organisation held accurate demographic information. This omission meant that many residents, including undocumented migrants and persons with disabilities, were effectively unseen by the very institutions tasked with protecting them.

At Grenfell, demographic invisibility was compounded by the disproportionate number of disabled residents, many of whom were unable to self-evacuate. Although the official stay put policy presumed individual mobility, there was no evacuation strategy from the London Fire Brigade for high-rise buildings with significant numbers of residents with vulnerabilities, further exposing the fatal consequences of failing to integrate disability into risk governance (GTI Phase 1, 2019). In Grand Kartal, a similar dynamic played out. Post-disaster investigations revealed that evacuation procedures were unevenly applied: hotel managers and residents in executive suites were alerted early and evacuated, while many guests in other rooms, as well as staff housed in basement dormitories, received no warnings (Hürriyet, 2025). This selective recognition of whose safety mattered underscores the stratified nature of risk governance. In line with Bhattacharyya’s (2018) notion of the violence of abstraction, those in less visible or less valued spaces were effectively erased from institutional protection, demonstrating how vulnerability was actively produced through unequal evacuation practices rather than merely through technical oversight.

Institutional outsourcing

Institutional outsourcing further entrenched this invisibility by creating fractured chains of responsibility. In Grenfell, the RBKC outsourced housing management to the KCTMO, effectively creating an accountability buffer. The Inquiry observed that RBKC ‘treated KCTMO as a separate entity … and failed to hold it accountable for lapses in safety governance’ (GTI Phase 2, 2025, Vol. 2: 123).

The process of outsourcing, coupled with regulatory withdrawal, fosters a system where visibility is simulated through formal procedures while substantive protections are eroded. Austerity, far from being a neutral policy choice, operates as spatial violence, producing uneven infrastructures of vulnerability and abandonment (Shaw, 2019). Without systematic checks, contractors frequently deferred safety compliance to others. For instance, Rydon, the company appointed to carry out the refurbishment of Grenfell Tower, oversaw the project's execution, left the selection of compliant materials to subcontractors, leading to significant gaps in fire safety. The Inquiry criticises Rydon for its failure to clearly identify responsibilities. The absence of checks allowed the use of combustible cladding and insulation that did not meet safety standards. This hands-off approach contributed to what the report calls a ‘merry-go-round of buck-passing’, undermining accountability (GTI Phase 2, 2025: Vol.4, Chapter 67, 320). Fragmentation within regulatory systems created gaps in accountability, leaving no single authority to oversee fire safety comprehensively. This fragmentation produced what Hodkinson (2020) describes as a systematic accountability vacuum, where layers of delegation and outsourcing created gaps that insulated both public authorities and private contractors from responsibility. This dynamic transferred risk management to individual actors within the construction industry who lacked coordination or oversight: ‘The TMO… failed to inform RBKC of fire safety reports’ (GTI Phase 2, 2025: Chapter 5, 16). Further: ‘The regulatory arrangements… had become too complex and fragmented’ (GTI Phase 2, 2025: Chapter 113, 31).

In Grand Kartal, compliance was outsourced to private contractors hired by the hotel itself. One inspection company, under investigation for issuing fraudulent certificates, had also provided services to five other hotels in the region without state audit for over 4 years (Gürbüz & Göder, 2025). This system of delegated compliance allowed both public and private actors to disclaim knowledge and responsibility, enabling what Roberts (2009) refers to as organised irresponsibility.

Spatial marginalisation

The spatial dynamics of both disasters illustrate a geography of abandonment. Spatial marginalisation refers to the ways in which certain populations are excluded from safe and well-resourced spaces, often relegated to areas where their physical environment reflects, reinforces and perpetuates their social invisibility and risk. Grenfell Tower exemplifies this through its degraded infrastructure, governance failures and the systemic dismissal of residents’ voices (Danewid, 2020; MacLeod, 2018; Waine and Chapman, 2022).

Grenfell stood in North Kensington, a site of extreme inequality, juxtaposed with some of the most affluent postcodes in Europe. Yet the building's refurbishment prioritised aesthetics over safety, as ‘aesthetic considerations … influenced the decision to install ACM cladding’ (GTI Phase 1, 2019: 582). The material used was £300,000 cheaper than non-combustible alternatives (GTI Phase 2, 2025: Volume 4, 214).

Grenfell residents were not only physically marginalised in a high-rise structure, but also socially and politically marginalised. Their efforts to raise concerns were actively resisted or ignored by those in power: ‘Some, perhaps many, occupants of the tower regarded the TMO as an uncaring and bullying overlord that belittled and marginalised them, regarded them as a nuisance, or worse, and failed to take their concerns seriously…“The TMO lost sight of the fact that the residents were people who depended on it for a safe and decent home and the privacy and dignity that a home should provide”’ (GTI Phase 2, 2025: Chapter 2, 15).

Grand Kartal's staff dormitories were located in converted storage rooms lacking proper ventilation or fire exits, described in one media report as windowless concrete units tucked behind the boiler room (De Ruiter, 2025). These were the consequences not just of hotel negligence, but of wider urban exclusion, where migrant workers were denied access to formal housing markets and emergency planning systems.

Policy austerity

Finally, policy austerity intensified these dynamics by normalising disinvestment as fiscal prudence. At Grenfell, fire safety investments were constrained by budget cuts: ‘fire doors failed, alarms were absent, and the stay-put policy had not been updated in over a decade’ (GTI Phase 1, 2019: 30). The Inquiry confirmed that building control officers were under-resourced and unable to verify fire safety during the cladding installation phase.

Testing and product certification bodies prioritised commercial interests over public safety, shifting responsibility for product safety to the industry itself: ‘Senior BRE staff gave advice to customers such as Kingspan and Celotex on the best way to satisfy the criteria for a system to be considered safe, thereby compromising its integrity and independence … we saw evidence of a desire to accommodate existing customers and to retain its status within the industry at the expense of maintaining the rigour of its processes and considerations of public safety’ (GTI Phase 2, 2025: Chapter 2, 9).

The fiscal re-prioritisation left mid-tier and staff-heavy hotels under-regulated, reinforcing what Soja (2010) calls ‘spatial injustice’. Taken together, these five domains illustrate a shared paradigm in which accounting systems, far from being neutral or technical, actively participate in the production of risk and reproduction of inequality. They obscure whose lives are made vulnerable, whose deaths are considered regrettable but unremarkable, and whose suffering is quietly absorbed into the background noise of institutional life.

In both Grenfell and Grand Kartal, what was most damaging was not only the presence of risk, but the absence of recognition. These absences were not passive. They were structured through accounting silences, governance design and political choice.

Toward an IRA framework

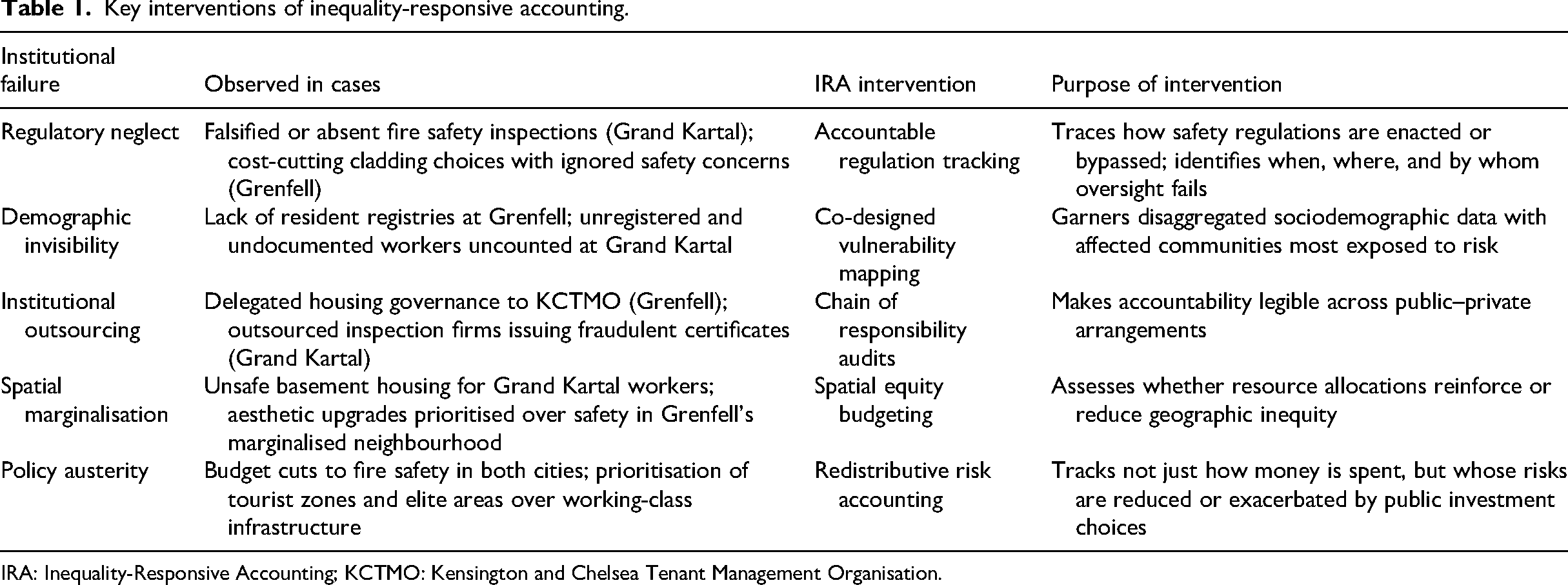

The Grenfell Tower and Grand Kartal Hotel disasters were not simply failures of fire safety, they were institutional failures of accounting that rendered precarity invisible and allowed known risks to culminate in mass fatality. While these cases unfolded in vastly different regulatory and socio-political settings, their comparative analysis reveals five recurring institutional deficits: regulatory neglect, demographic invisibility, institutional outsourcing, spatial marginalisation and policy austerity. These failures were not incidental but patterned, systemic and accountable to specific decisions and omissions. To address this, we propose an IRA framework, built around four transformative themes: (1) accountable regulation tracking, (2) vulnerability mapping, (3) chain of responsibility audits and (4) spatial equity budgeting (see Table 1).

Key interventions of inequality-responsive accounting.

IRA: Inequality-Responsive Accounting; KCTMO: Kensington and Chelsea Tenant Management Organisation.

First, accountable regulation tracking addresses what we term regulatory neglect. In both cases, safety protocols and regulatory tools were present, yet they failed to function as safeguards. At Grenfell, combustible aluminium composite material (ACM) cladding was approved and installed despite clear warnings about its risks, and despite statutory obligations to ensure fire-resistant materials. The Grenfell Tower Inquiry explicitly noted that nobody at Rydon appears to have given any thought to whether the materials met the requirements of the Building Regulations (GTI Phase 2, 2024). Similarly, in Grand Kartal, fire safety inspections were either falsified or ritualised. Court records revealed that critical fire safety reports were prepared without field inspection and that inspection methods had become a customary practice with no meaningful oversight (Bölükbaş, 2025). These are more than technical failures; they exemplify how compliance is enacted symbolically, with little substantive engagement. Accountable Regulation Tracking, as proposed under IRA, requires that safety inspections, certifications and risk assessments be audited not just for presence but for veracity, tracing which actors upheld or undermined regulatory intent. It brings transparency to how and why regulations fail in practice and links compliance efforts to actual protection for vulnerable groups.

Second, co-designed vulnerability mapping is a response to demographic invisibility, the failure to record and consider those most at risk. This theme is rooted in Bhattacharyya’s (2018) notion of the violence of abstraction, whereby institutions erase complexity in the name of administrative efficiency. While vulnerability mapping has often relied on indices such as the UK's Index of Multiple Deprivation, which already incorporate certain sociodemographic dimensions, this approach remains limited in two key respects. First, as Eriksen and Simon (2017, 2025) and Simon (2016) note, such metrics tend to treat populations as homogeneous units, masking the intersecting vulnerabilities that emerge through race, migration status, disability and spatial marginalisation. Second, these maps are typically produced in technocratic ways, privileging administrative categories over lived knowledge. In contrast, our proposal for inequality-responsive vulnerability mapping calls for co-production with affected communities, ensuring that the maps not only register deprivation but also reflect how residents themselves understand and navigate risk. This extends beyond existing models by embedding recognition and accountability into the very process of generating visibility. At Grenfell, the lack of a central resident registry made it impossible to know who lived in the building at the time of the fire (GTI Phase 1, 2019: 20). This omission meant that key vulnerability indicators, such as disability, immigration status and language proficiency, were unknown to first responders and uncounted in disaster preparedness plans. In Grand Kartal, 78 fatalities could be matched to formal identities in the first 72 hours (ivme, 2025). The undocumented, informally employed and precariously housed were quite literally unaccounted for. As an accounting tool, co-designed vulnerability mapping would require disaggregated sociodemographic data, garnered through participation of affected communities, to be integrated into disaster planning, ensuring visibility of the differentiated risks borne by groups defined by race, gender, class, age, disability or legal status. Such mapping could have flagged the elderly and disabled residents on Grenfell's upper floors or the basement-dwelling hotel staff in Grand Kartal as high-risk long before tragedy struck.

Third, chain of responsibility audits confronts the issue of institutional outsourcing and the diffusion of accountability across fragmented governance structures. Both disasters illustrate how decentralised or privatised management can produce what Roberts (2009) calls organised irresponsibility. At Grenfell, the RBKC outsourced housing management to the KCTMO, and in doing so, distanced itself from the everyday governance of building safety. The Inquiry found that RBKC ‘treated KCTMO as a separate entity … and failed to hold it accountable for lapses in safety governance’ (GTI Phase 2, Vol. 2, 2025: 123). In Grand Kartal, hotel management outsourced compliance to private inspection firms, several of which had provided fraudulent reports without a state audit for years (Turkish Regulatory Report, 2025). In both cases, accountability dissipated across actors, none of whom could be held singularly responsible. Chain of Responsibility Audits would require a comprehensive mapping of contractual, managerial and regulatory relationships across actors, public and private, clarifying who is accountable for which decisions and outcomes. This would prevent accountability from being buried under layers of delegation and allow for institutional ownership of failure. By engaging with these debates, the IRA framework can be seen as a way to cut through contradictions. Rather than presuming a uniform process of individualisation, IRA foregrounds who is rendered visible within accounting systems and whose safety is prioritised or neglected by selective investments. In doing so, it provides tools such as co-designed vulnerability mapping and spatial equity budgeting to interrogate how resources are differentially distributed, and how accountability can be redirected towards those most at risk.

Finally, spatial equity budgeting responds to both spatial marginalisation and policy austerity by demanding that accounting systems attend to where and for whom resources are spent. Grenfell was located in a socially deprived part of one of the UK's wealthiest boroughs, yet refurbishment decisions privileged aesthetic value over safety, with the flammable cladding chosen in part for its visual appeal to neighbouring elites (GTI Phase 1, 2019: 582). The cheaper ACM option saved £300,000 compared to safer alternatives (GTI Phase 2, Vol. 1, 2025: 214). In Grand Kartal, fire inspection budgets were slashed by 18% over 4 years, with funds reallocated to tourist zones, leaving staff-heavy working-class hotels under-regulated (Bolu Budget Report, 2024). Spatial equity budgeting introduces tools that measure the distributive effects of public investment, asking: Whose risks are being reduced? Whose safety is being deprioritised? It makes spatial injustice, as described by Soja (2010), quantifiable and challengeable through fiscal accountability.

Each of these four IRA themes is designed to confront a specific institutional pattern of neglect identified through comparative analysis. But beyond their technical role, they represent a shift in the ethics of accounting from a backwards-looking, metrics-driven tool of post hoc justification to a proactive, justice-oriented mechanism of care. They help reconfigure accounting as a moral as well as methodological practice, one that renders inequality visible, traceable and addressable before harm occurs. IRA interventions would fall to regulators, fire services, municipal authorities, housing bodies and contracted firms to implement, with governments and treasuries responsible for reporting through audits, registries and budget statements. In this way, public agencies and private contractors are made visible as accountable actors.

Taken together, the IRA framework contributes to a broader reimagination of accounting within disaster governance. It moves beyond critique to provide concrete, actionable strategies for embedding equity into how risk is measured, resourced and reported. As climate change, austerity and forced migration continue to produce overlapping crises, such a transformation is not merely desirable but essential. By aligning each of the five domains of failure with a targeted IRA intervention, the framework offers a roadmap for rebuilding institutional accountability on the foundations of recognition, redistribution and representation.

The IRA framework, while conceptually ambitious, is not a naïve suggestion; rather, it is a necessary and timely intervention that reframes accounting as an instrument of social justice. However, operationalising the IRA demands both political will and institutional innovation (Olsen, 2018). Practically, it requires embedding disaggregated sociodemographic data into all stages of disaster governance from risk assessment to resource allocation, through statutory mandates and ethical auditing protocols (Kanbara and Shaw, 2022). Tools such as co-designed vulnerability mapping and spatial equity budgeting must be developed collaboratively with marginalised communities to ensure contextual accuracy and legitimacy (Roy et al., 2024; Sullivan-Wiley et al., 2019). Implementing chain of responsibility audits entails legislative adjustments to enforce traceability across public–private governance arrangements, while accountable regulation tracking may require the redesign of audit systems to evaluate not just compliance, but the intent and outcomes of regulatory practices (Vetterlein, 2018). Nonetheless, caveats abound: institutional inertia, data protection concerns and resistance from entrenched interests may curtail adoption. Moreover, without safeguards, IRA could be co-opted into symbolic compliance rather than substantive reform. Therefore, its success depends on coupling technical interventions with critical reflexivity, participatory governance, and ongoing scrutiny to prevent the very abstractions and silences it seeks to redress.

Conclusion

This article has explored how disaster governance, when filtered through dominant accounting practices, often obscures the very inequalities it ought to address. By examining two seemingly disparate fire disasters, Grenfell Tower in the United Kingdom and the Grand Kartal Hotel in Turkey, it becomes clear that institutional failures are not anomalies but manifestations of systemic practices that neglect the lives and risks of marginalised populations. The comparison has shown that accounting systems, through their silences, omissions and symbolic performances, play a central role in rendering inequality invisible.

We make a simple but urgent claim: we cannot continue to account for disasters without accounting for inequality. Accounting systems that fail to register whose lives are at risk, whose warnings go unheard, and whose losses remain uncounted do more than fall short, they contribute to the perpetuation of harm. Ebbensgaard (2024) highlights how institutional practices of disavowal depoliticise structural harm, allowing responsibility to be deferred under the appearance of technical neutrality. In a world increasingly marked by compound crises such as climate change, pandemics, austerity and displacement, accounting must evolve into a justice-centred practice: one that does not simply document harm after the fact, but actively works to prevent it through the recognition of structural precarity, intersecting vulnerabilities and the politics of omission identified through participatory engagement with affected communities (Bhattacharyya, 2018; Fraser, 2000; Neu et al., 2022; Walker, 2016).

Rather than treating accounting as a neutral administrative tool, this study has shown how it often functions as an instrument through which vulnerability is normalised and institutional failure is concealed. Drawing on a comparative analysis of the Grenfell Tower and Grand Kartal Hotel fires, we demonstrated that these were not isolated tragedies, but outcomes of structural forces including demographic erasure, fragmented governance, spatial injustice and austerity-driven neglect. In doing so, the analysis contributes to the Special Issue's aim of uncovering how accounting shapes the uneven distribution of visibility, protection and legitimacy across different lives and spaces.

The article's central theoretical contribution is the development of the IRA framework, which challenges the presumed neutrality of accounting and redefines it as a relational and political practice embedded in the reproduction or contestation of inequality. By introducing a vocabulary of vulnerability mapping, accountable regulation tracking, chain of responsibility audits, spatial equity budgeting and redistributive risk accounting, IRA offers critical tools for resisting symbolic compliance and institutional neglect (Dillard and Vinnari, 2019; Power, 1997). Accounting processes such as audit trails, checklists and inspection records may create a façade of accountability while concealing institutional inaction. These rituals of compliance, through repetitive bureaucratic acts, perform what Anderson (2021) calls affective closure, producing a sense of resolution while deferring meaningful action. Such symbolic performances contribute to what Pile et al. (2023) describe as post-political spatial closure, wherein the appearance of procedural completeness forecloses contestation and renders certain spaces and subjects politically inert.

Extending critical accounting's engagement with intersectionality (Crenshaw, 2013; Kyriakidou et al., 2016), spatial justice (Soja, 2010) and decolonial thought (Gallhofer and Haslam, 2019; Tanima et al., 2024), the framework positions accounting as a forward-looking instrument of ethical governance. It outlines practical interventions such as mandating sociodemographic data use in disaster risk assessments, embedding redistributive logics in public budgeting, and clarifying accountability within fragmented governance regimes. These are superficial technical adjustments and fundamental shifts in how institutions recognise, value and protect structurally marginalised lives, both in the aftermath of disasters and in the systems that shape their everyday precarity. We contend that visibility, representation and recognition must co-exist in accounting practice to achieve institutional accountability that is both ethical and effective.

Recent reforms, such as the creation of the Building Safety Regulator in the United Kingdom and Turkey's proposed tightening of fire inspection and licensing regimes after the Grand Kartal fire, indicate growing recognition of systemic failures (Grenfell Tower Inquiry, 2025; İvme, 2025). While these measures signal movement towards stronger oversight, their alignment with inequality-responsive accounting remains partial: they emphasise compliance and technical regulation but fall short of embedding vulnerability mapping, chain of responsibility audits or spatial equity budgeting. Without explicit mechanisms to account for marginalised groups and redistribute protection, reforms risk entrenching symbolic compliance rather than delivering substantive accountability. For future research, we invite scholars to apply and extend the IRA framework across diverse geographies and governance regimes, especially in the Global South, where informality and absence from institutional records further entrench vulnerability (Goddard et al., 2016). There is scope for building interdisciplinary and participatory methodologies that develop new modes of visibility, valuation and voice, centred on those typically excluded from accounting's gaze. Further, we encourage engagements with indigenous, feminist and abolitionist ontologies that offer epistemological alternatives to managerialist frames.

This study is grounded in the analysis of two high-profile disasters in distinct national contexts, offering theoretical and empirical insights into the patterned failures of accounting in disaster governance. However, its reliance on documentary data, while analytically rich, necessarily excludes the voices of some minoritised groups whose experiences were not formally recorded, particularly undocumented workers and displaced tenants. Future research could extend the IRA framework by incorporating participatory, ethnographic or co-produced methods to capture these perspectives more directly. Moreover, while this article offers a normative model, further empirical testing is needed to evaluate how IRA interventions perform in real-time crisis planning, regulatory audits or post-disaster reviews. Comparative studies across the Global South, Indigenous communities, or regions with informal governance infrastructures could deepen understanding of how accounting frameworks adapt or fail in varied socio-political terrains. In particular, future work could explore the translation of IRA into practical tools for policymakers and auditors and its integration with decolonial, abolitionist or grassroots accountability practices that resist institutional erasure and centre community resilience. Confronting disposability demands more than institutional reform; it requires transforming how space, risk and care are conceptualised within the everyday infrastructures of governance.

Footnotes

Acknowledgement

We thank the İvme (Turkey) for its support in the systematic collection of media reports related to the Grand Kartal incident.

Ethical approval

This study does not involve the collection or analysis of primary data from human subjects. All empirical materials analysed, including inquiry reports, policy documents and publicly available secondary sources, are openly accessible. Therefore, ethical approval and informed consent were not required.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Declaration of interest statement

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.