Abstract

The credit crisis has led to tightened bank so lending to smaller firms it is no surprise that the debate concerning the re-introduction of regional stock exchanges into the UK has received fresh impetus. This article analyses all UK based Initial Public Offerings (IPOs) on the Alternative Investment Market (AIM) to contribute to this debate and the small firm funding literature. The results indicate that London has dominated IPO activity on the AIM; this reflects the dynamism of this local economy rather than differential funding across the regions. A more fruitful approach than developing regional stock exchanges might be for the current stock exchange to develop stronger links with small business advice and networking organizations working with these existing mechanism/structures to enhance the supply of equity and debt finance to suitable firms much earlier in their life-cycles.

Introduction

The supply of, and demand for, small firm finance remains a critical issue for researchers, policy makers and practitioners (Fraser, 2005). However, it is now recognized that the funding needs of small firms are diverse and complex given their heterogeneity (Cumming, 2006; Franke et al., 2006). This article contributes to the small firm funding literature through an analysis of the potential for Regional Stock Exchanges (RSEs) to offer finance for those ventures who require additional funding to support growth but for whom debt funding is unlikely to be suitable, in either terms of scale or cost, and for those where conventional venture capitalist and business angel funding is unappealing given the potential loss of entrepreneurial and managerial control. Accordingly, RSEs could be a mechanism to support local enterprise and fuel recovery whilst challenging the tendency for the natural conservatism of existing funding institutions to withdraw to the South East when markets contract, which in turn further embeds regional disparities.

Potentially, RSEs might also have strong multiplier and accelerator effects such that they could generate and strengthen regional focus helping to address some of the regional weaknesses in local labour markets and high growth sectors. In turn, this would help maintain successful firms in the regions. Hence, such stock exchanges might offer a potential solution to regenerating and rebalancing the UK economy; but to what extent this may be borne out in reality depends on the interplay of a range of influences – in particular, the current lack of RSEs may simply reflect a lack of sufficient demand for market-based equity in the regions. This article contributes to the small firm funding debate through an analysis of the potential offered by RSEs to support firm growth whilst stimulating regional development; to achieve this objective we analyse, using publicly available data, the regional disparities in Initial Public Offerings (IPOs) on the UK Alternative Investment Market (AIM). We conclude that such disparities are more a reflection of the different regions than the differences in market-based equity funding.

The remainder of the article is organized as follows. The next section uses existing literature to draw out theoretical insights as to how access to equity finance might be affected by location. Section three describes the research question, the sample and the research methodology. Section four presents empirical results and the final section discusses the results and considers their implications for the debate on small firm funding and regional stock exchanges.

Accessing equity finance: Theoretical insights into the importance of location

It is a long and widely held view (from Macmillan, 1931, to Klagge and Martin, 2005) that whatever the structure of the UK capital markets at the time, both financial institutions and markets have not provided smaller growing firms with the required amounts and types of capital. Furthermore, another perennial complaint is that the UK financial system generally, and the equity markets in particular, are very ‘London-focused’ and as a consequence, even very successful small firms in the regions are unable to raise funds to the same degree as similar firms located in the South East (Bank of England, 2001, 2003; HM Treasury, 2003a, 2003b; Wojcik, 2009). It is not surprising therefore, that there have been contemporary calls to investigate the re-introduction of some form of RSEs to address the perceived equity gap (Huggins et al., 2003). To investigate whether the spatial structure of the financial markets affects accessibility to equity finance, it is important to consider how the financial markets are conceptualized. In a perfect capital market where there are no transaction costs, no bankruptcy costs, information is costless and symmetric, and there is perfect competition, spatial proximity to the stock exchange does not matter. However, given these conditions are unlikely to hold, it is suggested that the location of firms influences their access to and success in securing equity funds (Klagge and Martin, 2005) so, RSEs might helpfully address the perceived failure of the equity market for smaller growing companies (Huggins et al., 2003).

The basic premise that a centralized stock exchange may be undermining the prospects of successful smaller growing companies in the regions can be broken down into two arguments, a basic ‘supply of finance’ and a ‘cost of supply’ argument (Christensen, 2007; Grinblatt and Keloharju, 2001; Huberman, 2001; Pollard, 2003). First, the investors in a centralized exchange do not invest in regional businesses to the same degree as those close to the centralized exchange due to a lack of information and familiarity (Coval and Moskowitz, 1999). Thus, there is a basic shortage of equity finance due to informational asymmetries. In essence, regions could have the same dynamics within their economies but their effective separation from the centralized exchange means that fewer successful small firms achieve the equity finance they need via an IPO. To overcome this problem, RSEs could potentially encourage local investors to invest in local small growing firms and so, local funds would be released to support smaller growing firms within the regions.

A second argument being that a centralized exchange imposes higher costs (both tangible and intangible) 1 on small firms in the regions (Wojcik, 2009). As a consequence, smaller growing firms will have to be relatively more profitable, ceteris paribus, to take equal benefits from a centralized exchange. In other words, while there might be the same supply of equity finance across the regions, the cost of this type of financing has a regional dimension. Accordingly, smaller growing firms are more likely to access funds from the equity market via RSEs because the costs of raising initial funds (direct transaction costs) and ongoing funds (asymmetric information and low liquidity) are likely to be lower (Klagge and Martin, 2005). Both of these arguments point towards a centralized exchange constraining the supply of suitable equity funds to regional businesses.

In contrast to the arguments in favour of RSEs, it is suggested that RSEs would do little to alter the regional variation in IPOs because of the lack of demand for such a type of financing across the regions (Mason and Harrison, 1992). A lack of demand for market-based equity in the regions could result from a number of arguments. First, it could simply be the case that there are fewer small firms in the regions which reach the point of maturity to warrant an IPO; in other words, the relative lack of regional IPOs reflects the lack of entrepreneurial dynamism in the regions. Second, while there may be regional small firms which could achieve an IPO, the entrepreneurs choose not to pursue this route due to the lack of a demonstration effect and/or a higher preference to keep control of the business. Moreover, the higher potential personal cost of going public for regional entrepreneurs in a small labour market could make them less willing to take their firms public as if they were unsuccessful, they would lose their firm and reputation (Wojcik, 2009). Third, it could be the case that venture capital institutions have become regional alternatives to capital markets for those small firms which are located in peripheral regions. However, the results of a survey conducted by Martin et al. (2005) show that proximity to investee companies is an important factor for venture capital firms, as the UK venture capital market is highly concentrated in London and the South East (Martin et al., 2003, 2005; Mason and Harrison, 1991, 2002) venture capital firms are more likely to focus investments in their own region hence, causing a South-East bias in the regional distribution of investment (Jones-Evans and Thompson, 2009; Martin, 1992).

Evidence on the regional dimension of venture capital activity in other countries is mixed. For instance, Avdeitchikova (2009) finds a heavy concentration of informal venture capital in metropolitan areas and the university cities of Sweden. Christensen (2007) documents that Danish venture capital funds confine themselves to investments within a closer geographical distance as competition increases. In contrast, Griffith et al. (2007) find that Silicon Valley venture capital firms are only interested in the best deals and the location of the investee does not matter. Moreover, Fritsch and Schilder (2007), investigating German data, find that spatial proximity is far less important for venture capital investment than is often believed.

Over the past couple of decades, policy makers have tried to solve the perceived equity gap problem in the UK through establishing government-backed Regional Development Agencies (RDAs) in 1999 and Regional Venture Capital Funds (RVCFs) in 2002. However, evidence shows that RVCFs in Northern regions find it difficult to raise private finance and so, mainly rely on government, European Union and local authority funding rather than local investors (Klagge and Martin, 2005). Moreover, Murani and Toschi (2010) report that public venture capital programs in the UK have been more effective in high-tech regions. Mason and Pierrakis (2009) argue that public sector venture capital in the UK is unable to create entrepreneurial regions and as such, suggest that a new approach is required which puts greater emphasis on the demand side. In addition, there have been other attempts to narrow the equity gap across the UK. For example, the Alternative Investment Market (AIM) was established in 1995 for listing successful smaller businesses. By September 2009, 3080 firms had been admitted to trade on the AIM and more than 63 billion pounds had been raised. In addition, the OFEX market was created in 1995 to provide a more cost effective and less regulated alternative to the AIM. Although the development of these exchanges has clearly been helpful, there are dramatic regional disparities regarding the businesses listed. In response to this issue, the London Stock Exchange (LSE) introduced its landMARK market in 2001 designed to meet the requirements of regional companies establishing landmark offices and regional advisory groups (RAGs) across UK regions. Nevertheless, landMARK does not seem to have resolved the funding gap problem given the LSE bias towards large companies and that many of the RAGs managers and advisors are based in London thus, not lack knowledge regarding the regional trading context for smaller firms (Klagge and Martin, 2005).

In spite of the above developments, there is still considerable variation in entrepreneurial success across the regions; hence, it is not surprising to see the regional stock exchange debate being given fresh impetus. Historically, there was a dense network of regional stock exchanges in the UK (Huggins et al., 2003) but these exchanges ceased operating in the early 1970s following the changing industrial scene. Although the integration of RSEs might seem inevitable as a consequence of globalization and changing industrial structures, it is worth noting that regional exchanges have become embedded in the economies of many other developed countries such as the US, Japan and Germany (Huggins et al., 2003). So far, we have argued that the spatial structure of finance across the UK may be affecting access to equity finance in the regions and furthermore, the growth of regional venture capital funds has not completely filled the gap. However, to better understand the impact of regional funding effects, it is important to pay attention to the literature which documents the impact of regional location on small firm formation and performance (see, for example, Anayadike-Danes and Hart, 2006).

Bearing in mind that the economic outcomes of a region are the result of a complex intermingling of variety of factors (see, for example, Wagner and Sternberg, 2004), the main reasons for the observed regional disparity in new firm formation have been documented to be demand, financial, cost, human resource, and industry agglomeration and structure (Okamuro and Kobayashi, 2006). In terms of demand factors, it has been found that new firm formation is influenced by previous local population growth (Armington and Acs, 2002), increased local income, and business activity (Acs and Armington, 2004b). It has also been found that new firm formation in different regions is positively related to regional economic diversity and greater regional/personal wealth (Sutaria and Hicks, 2004) while it is negatively related to high prices of land (Wagner and Sternberg, 2004). In terms of human resource factors, it is reported that new firm formation is negatively related to the proportion of manual workers in the industrial population (Garofoli, 1994), while positively related to a high self-employment environment, entrepreneurial and educational experience (Acs and Armington, 2004b), and entrepreneurs’ social relationships (Shane and Cable, 2002). The birth rate of firms is also affected by regional agglomeration advantages (Fotopoulos and Spence, 2001), a tradition of smaller scale firms in the regions (Acs and Storey, 2004), and industrial density (Armington and Acs, 2002).

Given the above evidence, the regional performance literature has provided suggestions on how to reduce regional diversity. For instance, Roper (1998) suggests that policymakers should attempt to improve the structural mix within regions as well as the competitive position of the existing plants. Moreover, Roper et al. (2000) suggest that promoting R&D as well as technology transfer and networking by regional development agencies will yield significant positive benefits by directly increasing the level of innovative activity. Finally, Anyadike-Danes et al. (2005) suggest that policy makers should not only focus on increasing the birth rate of new firms but also have to pay attention to the growth of the existing small businesses and to reducing their death rate. However, it needs to be noted that relationship between small firm enterprise and regional characteristics is not uni-directional as there is also a literature (for an informative discussion see Acs and Armington, 2004a) which relates the growth rates of regions to entrepreneurial activities.

Sample, research question and methodology

Sample

The initial sample of this study is the population of British companies that have gone public on the AIM market from June 1995 to the end of 2008. Although there have been 1751 IPO flotations on the AIM market in the investigation period, only the 1429 companies which are incorporated in the UK are of interest.

Research question and methodology

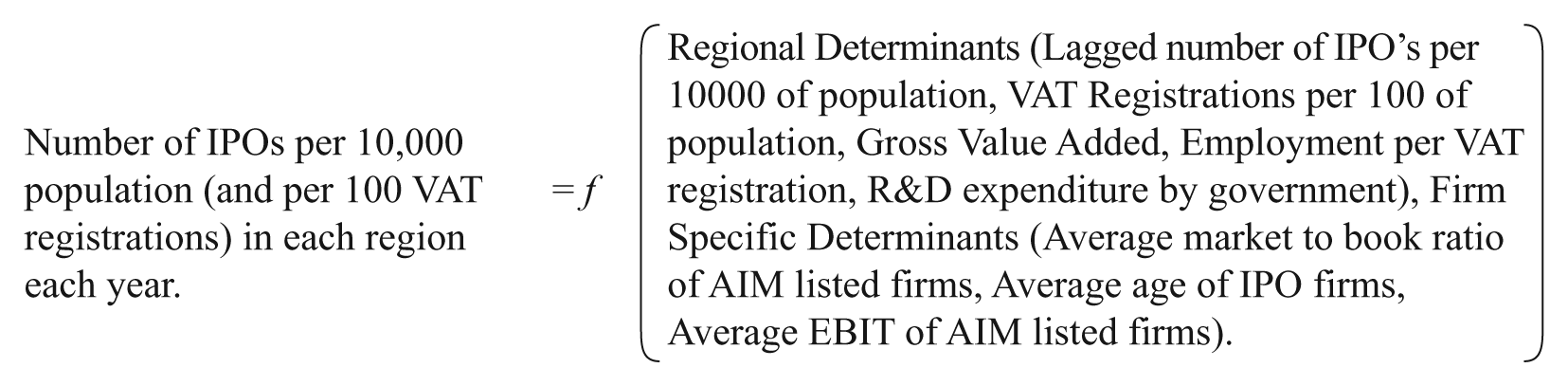

To offer insight into the question as to whether RSEs might improve the flow of equity funds to small growing companies, this article analyses regional and firm-specific determinants of the regional disparities in AIM IPOs. As the use of publicly available data does not permit the separate identification of the supply and demand of fund factors (any actual outcome being the result of the interplay of supply and demand conditions), the methodological approach adopted here is to use established regression techniques and acknowledge limitations of this approach in the discussion and interpretation of the empirical results. More specifically, empirical support for firm-specific determinants of regional disparities in AIM IPOs will suggest that the re-introduction of RSEs might have a useful role to play in the equity funding of smaller growing firms; whereas, support for regional determinants will suggest that more might be gained from a renewed emphasis on improving the entrepreneurial dynamism of regions.

Consequently, the approach adopted here is to analyse whether the number of businesses achieving an IPO in a region in a given year depends on the characteristics of the region and firm-specific factors. The firm-specific factors have been included to proxy for finance arguments; in general, if these factors are found to be significant then different types of firms are being funded via an IPO across the different regions – these, of course, reflect the interplay of both demand and supply factors and it is impossible to reach a conclusion solely on the significance of these variables. However, positively significant regional determinants (signalling the impact of regional dynamism) coupled with a lack of significant firm-specific factors would tend to rule out the argument that the disparity in IPOs across the regions is a reflection of funding supply arguments.

More specifically, to examine the regional disparity in IPOs, we estimate regression models where the dependent variables are the number of IPOs per 10,000 of population and the number of IPOs per 100 of Value Added Tax (VAT) registrations in each region for each year and where the explanatory variables comprise regional determinants and firm specific factors.

Regional determinants of IPO activity

Lagged number of IPOs per 10,000 of population

According to market timing theories there are some periods when firms are more likely to go public. For example, Subrahmanyam and Titman (1999) point out that raising capital from the public market is preferred when investors can get valuable information cheaply. Brau et al. (2003) document that more IPOs are conducted in favourable market periods when there is less information asymmetry and investors are overly optimistic about investing in IPOs. Given the market timing theories, the lagged number of IPOs per 10,000 of population, calculated for each region in each year, is expected to positively affect the current number of IPOs.

VAT registrations per 100 of population

This variable measures the number of enterprises registering for VAT each year per 100 of population for each region and is therefore, an indicator of the number of business start-ups – allowing for the fact that it will not capture the very smallest businesses that operate beneath the VAT threshold. According to Ciccone and Hall (1996) a higher number of new business establishments facilitates more spillovers in regions. Using this ratio as a measure of spillovers, it is expected that the dependent variables of regional IPO activity will have a positive relationship with it.

Ln (GVA)

This variable measures Gross Value Added (GVA) generated in each region for each year. Lowry (2003) provides evidence that there is a positive relationship between growth in the economy and the probability of an IPO. Thus, it is hypothesized that regions with higher generated GVA should experience a higher number of IPOs. In order to run the regressions the natural logarithm of GVA has been used.

Employment per VAT registration

This variable is calculated by dividing the total number of people in employment by the number of VAT registrations in each region for each year. This ratio gives an estimate of the degree of dominance by large firms in each region. It has been suggested that firms that are larger are more likely to go public (Chemmanur et al., 2009; Shen and Wei, 2007). Therefore, it is expected that more IPOs occur in regions dominated by larger firms.

R&D expenditure by government

The variable is the amount of R&D expenditure by government in each region for each year. Fischer (2000) documents that firms with high R&D intensity are more likely to go public. Therefore, R&D expenditure affects the going public decision and we test whether regions with higher R&D expenditure by government experience a higher number of IPOs.

Firm specific determinants of IPO activity

The variables described below are included to proxy for the possibility that different types of firms achieve an IPO in different regions as a result of funding not being equivalent across the regions. For example, if lower valued, younger and less profitable firms were more likely to achieve an IPO in London than in the other regions, this would tend to suggest a different funding regime in the capital which could reflect a different attitude to market-based equity amongst London-based firms and/or a different attitude to supplying such firms with market-based equity.

Average market to book ratio of AIM-listed firms

This variable is the average of the market to book ratio of already listed AIM firms in each region for each year. It has been documented in the literature that more firms go public when market valuations are high. For example, Lerner (1994) finds that venture capital-backed firms go public at market peaks when equity valuations are high and choose private financing when market valuations are lower. Ritter and Welch (2002) suggest that entrepreneurs are more willing to go public after valuations in the public market have increased. If the market values firms locating in certain regions more than other firms, more firms from those favourable regions will decide to go public. Thus, it can be hypothesized that there are more IPOs in regions which have a higher average market to book ratio for their listed firms.

Average age of IPO firms

This variable shows the average age of the firms at the time of flotation on the AIM market in each region for each year. According to life cycle theories, firms stay private at the early stages of their life cycle and decide to go public later when they are sufficiently mature (see for example, Ritter and Welch, 2002). This variable is included to proxy, albeit weakly, for the notion from life cycle theories that firms are more likely to go public later on in their development.

Average earnings before interest and tax (EBIT) of AIM-listed firms

This variable is the average EBIT of the already listed AIM firms in each region for each year. It has been documented by Shen and Wei (2007) that more profitable firms are more likely to go public. Here, more profitable small listed firms in a region have been considered as a proxy for more profitable small firms in a region. Therefore, it is expected that more IPOs will occur in regions where already small listed firms have a higher EBIT on average.

Empirical results

The empirical analysis begins by examining in detail the dependent variable and then proceeds to examine the strength of the various determinants of regional IPOs.

Regional location of AIM IPOs

The exact locations of IPOs have been examined in depth, with location being defined as a measure of their economic centre of gravity rather than their registered office address or headquarters’ address. 2 The procedure followed was that the location of the companies was cross checked using different data sources such as the LSE website, the ICC PLUM database, the Thomson One Banker database, the websites of the companies, the prospectuses of the companies, and the Lexis Nexis database. The following rules have been applied to determine the location of companies at the time of their IPO:

The original place of operation at the time of the IPO rather than the registered address or head office address has been considered as the location of a company.

If the place of operation of the firm was not clear, the head office address rather than registered office address was considered to be the location of the company.

In the case of a merger and acquisition the location of the dominant party was considered. The dominant party is usually the acquiring firm except in reverse takeovers when the dominant party is the acquired firm.

Companies located in Isle of Man, Jersey, and Guernsey have been excluded due to having different regulatory environments from the rest of the UK.

International companies registered in the UK but operating overseas were excluded.

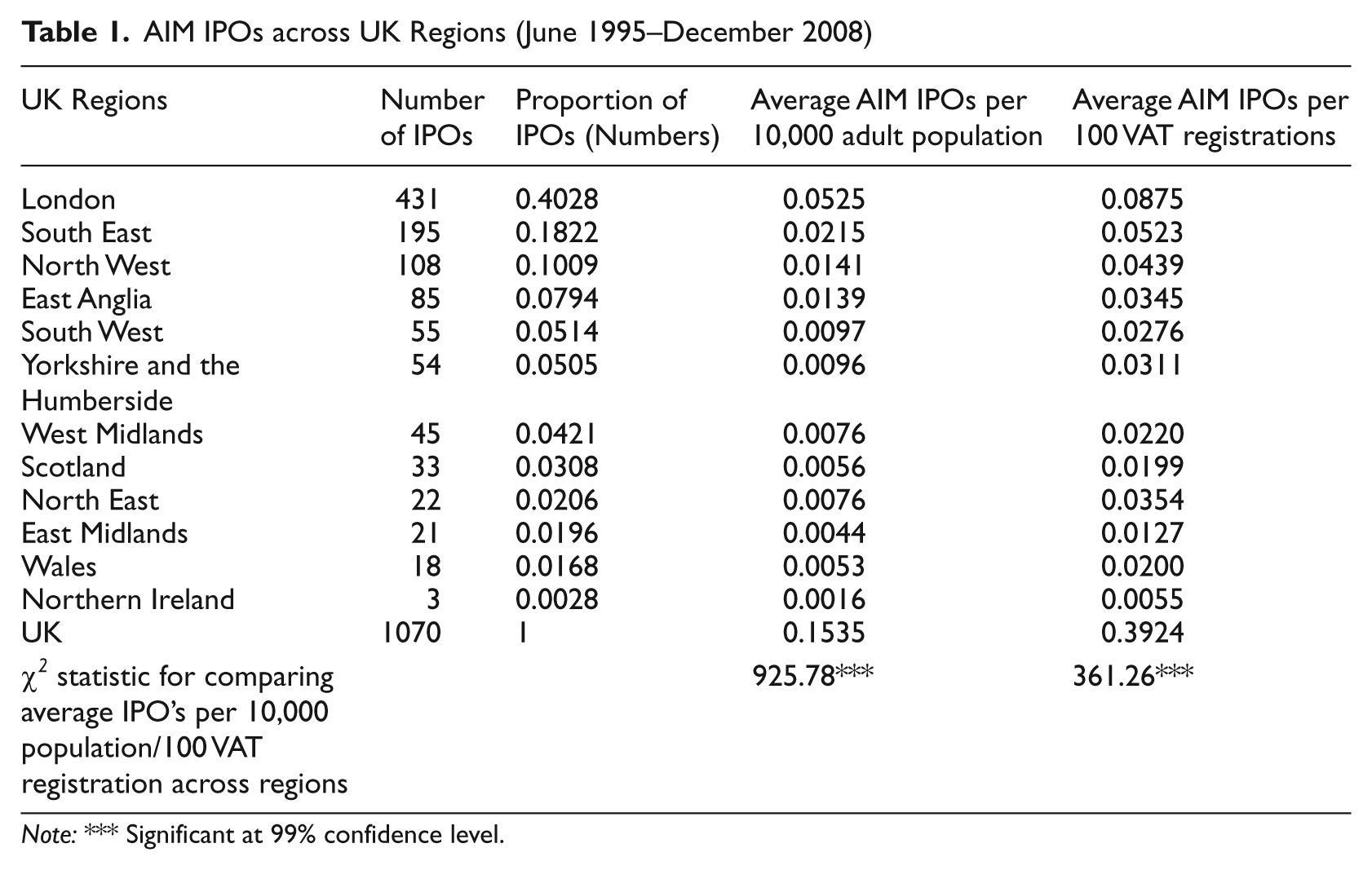

Examining the location of the companies applying above rules the final sample of the study consists of 1070 companies. 3 Table 1 shows the number of IPOs in the regions and the proportions of IPOs compared to the overall total number of IPOs. It can be seen that London has 40.28 per cent of the UK AIM companies and is the region with the highest number of IPOs by quite a margin, with the second placed South East having 18.22 per cent of the IPOs. In contrast to this domination of London and the South East (having together approximately 60 per cent of the IPOs), Northern Ireland and Wales together have less than 2 per cent of the total number of IPOs.

AIM IPOs across UK Regions (June 1995–December 2008)

Note: *** Significant at 99% confidence level.

Nevertheless, the simple comparison of the number of IPOs across regions can be misleading as regions are not similar in terms of size. To control for this factor, the number of IPOs relative to the population in each region and relative to VAT-registered firms in each region has been standardized (Armington and Acs, 2002). The number of IPOs per 10,000 of adult population and per 100 VAT registrations during the analysis period is shown in Table 1.

Standardizing IPOs respecting size does not substantially alter the patterns already observed in the non-standardized figures; we also test whether the differences in proportions across regions are statistically significant; using a chi-square test, we found the differences in the proportions across regions to be statistically significant. Therefore, controlling for the differences in regions’ size, it still emerges that they vary significantly in the number of smaller firm IPOs. Moreover, since the highest proportion of IPOs is observed in London, we tested whether the difference in the proportions across regions remains significant when London is excluded. Results of the chi-square test reveal that, excluding London, the proportion of IPOs per population/VAT registration across regions is still significantly different. Accordingly, Table 1 shows two major results; first, London has clearly dominated the IPO activity on AIM and second, even after allowing for the dominance of London there is still significant variation in IPO activity across the other regions. 4

Regional and firm-specific determinants of regional variation in AIM IPOs: Descriptive statistics

Table 2 presents the descriptive statistics for the regional and firm-specific variables across the UK regions during 1995 to 2007. Panel A of Table 2 shows that London and the South East are the prominent regions with respect to four of the five regional determinants of IPO activity. Regarding the lagged number of IPOs per 10,000 population, on average London has the highest number followed by the South East. With respect to VAT registrations per 100 of population and GVA, again London dominates; concerning employment per VAT registration however, it shows that London has the lowest employment per VAT registration suggesting that the average size of the firms is smaller than the rest of the UK regions. This confirms the fact that London is a fertile region for the growth of small firms. Regarding R&D expenditure by government, Panel A of Table 2 shows that the highest amount is in the South East and the lowest amount is in Northern Ireland. Overall, the above descriptive statistics show the dynamism of London and the South East.

Panel A. Descriptive Statistics for Regional Variables

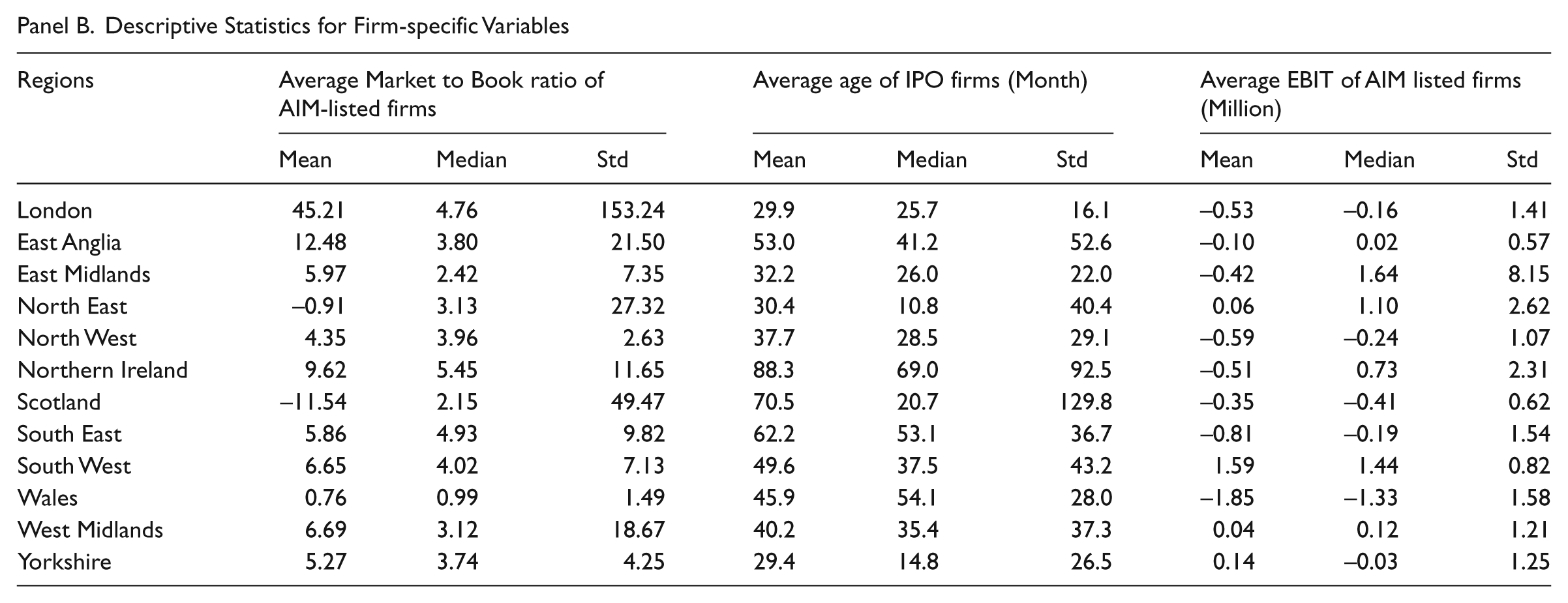

Descriptive Statistics for Firm-specific Variables

In terms of the firm-specific variables, Panel B of Table 2 shows that the highest average market to book (M/B) ratio is for London firms, suggesting that the market has priced, in general, the AIM-listed firms located in London higher than firms located in any other region of the UK. Table 2 also shows that average age of IPOs at flotation in London (29.9 months) is only slightly higher than the lowest average age (29.4 months) which is observed in Yorkshire. Finally, regarding the EBIT of AIM-listed firms. Table 2 shows that London IPOs have on average a lower EBIT with respect to most of the regions, suggesting that these are some of the least profitable IPOs.

A correlation matrix between the dependent variable of the IPOs per 10,000 population and the independent variables is shown in Appendix Table A1. The correlations with the other dependent variable – IPOs per 100 VAT registrations – are essentially similar and not shown here for reasons of brevity. The correlation matrix suggests that correlation between some of the explanatory variables is more than 30 per cent. Although these correlations are not considered high for the panel data methodology used in this article, in the next section the robustness of the regression results will be checked by excluding the variables with more than 30 per cent correlation. Finally, the sign of the correlations between the dependent and explanatory variables are as expected for most of the variables but this is not the case for employment per VAT registration and average EBIT which have a small insignificant negative correlation with the dependent variable.

Overall, the descriptive statistics suggest that the regional determinants are stronger for London-based IPOs whereas firm-specific determinants are greater for IPOs in the regions other than London. In addition, the correlation matrix shows that regional variables have high significant correlation with the dependent variable whereas the firm-specific variables have low insignificant correlation with the dependent variable.

Regional and firm-specific determinants of regional variation in AIM IPOs: Regression results

The results of the random effect panel data regression analyses of the determinants of the regional variations in IPO activity are presented in Table 3. 5 Although the majority of the analyses use data from the 12 UK regions for the time period from 1995 to 2008, some of the regional data for GVA, employment, or population were not available (at the time of the analysis) for 2008; therefore, 2008 has been excluded from the regression analyses. Moreover, due to the use of a lagged dependent variable as an explanatory variable, 1995 data have also been excluded. Therefore, the estimations are based on a panel of 12 regions over 12 years. 6 Furthermore, to test whether the centralized LSE has a London bias, the model has been estimated including and excluding the London based IPOs.

Estimates of Effects of Regional Characteristics on IPOs of UK AIM Firms using 1996 to 2007 data

Notes: R2 has not been reported due to the fact that in panel data analysis the explanatory power of the model cannot be obtained. This is because the error term is transformed to control for unobserved heterogeneity, R2 therefore, which is calculated based on the errors is not reliable anymore.

Significant at 90% confidence level. ** Significant at 95% confidence level. *** Significant at 99% confidence level.

Comparing the regressions of all regions (columns 2 and 3) with the regressions after excluding London (columns 4 and 5) indicates that the observed results for all regions are very much dominated by London. Therefore, the variables which are statistically significant in columns 2 and 3 in Table 3 are largely a result of a ‘London effect’. More specifically, IPO activity in London is explained by its past history/persistence of flotations (lagged number of IPOs per 10,000 of population), the dynamic nature of its new enterprise environment (VAT registrations per 100 population) and the dynamism of its economy (Gross Value Added). The significance and size of the coefficient for the employment per VAT registration are similar for regressions both including and excluding London, and so, the explanatory power of this variable is seen as being determined by regions outside London.

In contrast to the strongly significant results for London, the results for the other regions (columns 4 and 5) have few strongly significant explanatory variables. There is weak evidence in column 4 that IPO activity outside London is explained by the nature of the enterprise environment in a region (VAT per 100 of population) and stronger evidence (column 5) that the size of businesses in a region (employment per VAT registration) have a positive impact on the IPO activity. This latter result is consistent with the previous literature (Chemmanur et al., 2009; Shen and Wei, 2007) which confirms a positive relationship between the regional dominance by large firms and the likelihood of going public.

The regression results for government R&D expenditure are rather more complicated – with the London-dominated results of columns 2 and 3 showing a significant, negative coefficient, while the results for the rest of the regions indicate a positive relationship between IPO activity and government R&D expenditure in a region. Analysis of the descriptive statistics in Table 2 indicate that for regions outside London there is a positive relationship between government R&D expenditure in a region and IPO activity. In contrast, while London has the highest level of IPO activity, it only comes sixth in terms of government R&D expenditure. Therefore, excluding London, a higher amount of R&D expenditure by government in a region assists more firms to go public. In contrast to the results for the regional determinants of IPO activity, the results for the firm-specific determinants (average market to book ratio, average age and average EBIT) are all statistically insignificant.

To test the robustness of the results reported in Table 3, the regressions have been re-estimated excluding lagged variables and after controlling for potential multicollinearity. More specifically, the sign and significance of the results reported in Table 3 do not change qualitatively after the exclusion of the lagged variables. In terms of multicollinearity, the regression models are re-estimated after excluding variables with more than 30 per cent correlation. For this purpose VAT per 100 of population and GVA variables have been excluded from the model and the regression analysis has been repeated. The result suggests that excluding these variables, either one by one or at the same time, does not qualitatively change the results and the coefficients of the variables remain virtually unchanged.

In summary, the large number of London-based IPOs and the strength of the regional determinants of such IPO activity tend to suggest that London provides many opportunities and positive role models for raising capital via an IPO. Whereas, in contrast, the regions tend not to have such concentrations of small growing firms and hence, there is likely to be much lower demand for IPO finance irrespective of the amount and ease of access to available equity capital. Moreover, the strength of the regional determinants of IPO activity and the lack of significance of firm-specific variables suggest that IPO activity is not different across regions due to having different types of firms in terms of profitability or age or because the market places a higher value on firms from specific regions. Whereas, the significance of regional variables suggests that it is the regional dynamism which makes IPO activity different across regions. We argue therefore, that different regional dynamism causes different demand for market-based equity finance. Thus, the regional variation in AIM IPO activity is not so much a reflection of an equity supply constraint but more likely, a result of very different levels of demand for market-based equity across the regions. The results suggest, therefore, that unless RSEs are prepared to increase demand for a public listing then they are unlikely to appreciably increase the number of regional IPOs simply by having a physical presence in regional business capitals.

Discussion and conclusions

By analysing the regional and firm-specific determinants of the incidence of IPOs within regions for the population of UK-based AIM IPOs, this paper offers two insights: first, London has clearly dominated AIM IPO activity with over 40 per cent of all IPOs; second, London IPO activity clearly reflects the past history/persistence of flotations (lagged number of IPOs per 10,000 of population), the dynamic nature of its new enterprise environment (VAT registrations per 100 population) and the dynamism of the economy (GVA) in London. These results suggest that London’s domination of IPO activity reflects the dynamism of the London economy as compared to other regions. Moreover, the lack of significance of firm-specific factors adds to the relative importance of the regional determinants.

The results provided here show that the scaled number of IPOs is more a reflection of regional characteristics than firm-specific factors; this suggests that more work is required on the inter-linkages between the real economy and the financial system on a regional basis. Nevertheless, even allowing for the limitations of the current results, they suggest that the re-development of RSEs will do little to alter the current picture of IPO activity unless they increase the demand for IPO financing in the regions. Given that this seems unlikely with the current institutional focus, a more fruitful approach than developing RSEs might be for the current stock exchange to develop stronger links with public and private small business advice and networking organizations to enhance the supply of equity and debt finance to suitable firms much earlier in their life-cycles, i.e. at the start-up, informal venture capital and pre-listing stages. While such linkages could take many forms, one obvious possibility would be listed regional development funds that have the express remit of investing in pre-IPO ventures. The investors in such funds would then have first call on further investment opportunities emanating from the fund. Given the likely future cuts in public funds for small firm support, the development of this new market-based asset class might be very much needed if the regions and the economy are to be rebalanced.

The above results taken in their entirety (the significance of the regional determinants and the insignificance of the firm-specific factors) suggest that the disparities of AIM IPOs across regions are more likely to be a reflection of demand than supply conditions. The results, therefore, complement the available evidence on debt finance that small firm funding is now less a problem of supply but more an issue of entrepreneurs being aware of the differing characteristics of alternative sources of finance and choosing the capital mix which best suits their purpose – such awareness and appreciation is unlikely to be achieved without substantial investment in educating entrepreneurs and finance suppliers on the importance of different capital structures. However, a word of caution is required here. The available evidence on small firm debt finance precedes the current financial crisis and anecdotal evidence suggests that matters may well have changed. First, the banks seem to be rebuilding their balance sheets by restricting loans to individuals and companies with less than perfect borrowing records and limited collateral (Ivashina and Scharfstein, 2009). Second, the large number of small companies going into insolvency across 2008 and 2009 through being unable to meet the demands of banks for repayment (see Wilson and Altanlar, 2010) may well have changed the appetite for equity as compared to debt capital.

Finally, the results are not without limitations. First, they are based on published data and because of this they should only be seen as an initial attempt to get to grips with the topic of small firm market-based equity. Further work will require other empirical approaches – survey work and case studies – to add to the detail of the supply of and demand for market-based equity across the regions. This will involve discussions with a range of stakeholders if the detail of this segment of small firm financing is to be explored more fully. Second, there is no escaping the fact that the world seems to be changing in response to the financial crisis and there is a need to examine what these changes mean for the important topic of the financing of small firms.

Footnotes

Appendix

Pearson Correlation Coefficients between Variables

| Correlation | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. IPO per 10,000 of population | 1 | ||||||||

| 2. Lagged number of IPOs per 10,000 of population | 0.61 | 1 | |||||||

| 3. VAT per 100 of population | 0.55 | 0.51 | 1 | ||||||

| 4. Ln (GVA) | 0.55 | 0.57 | 0.58 | 1 | |||||

| 5. Employment per VAT registration | −0.15 | −0.12 | −0.48 | −0.03 | 1 | ||||

| 6. R&D expenditure by government | 0.21 | 0.24 | 0.34 | 0.62 | 0.04 | 1 | |||

| 7. Average market to book ratio of AIM-listed firms | 0.09 | 0.03 | 0.20 | 0.15 | −0.06 | 0.03 | 1 | ||

| 8. Average age of IPO firms | 0.01 | −0.02 | 0.15 | 0.12 | 0.00 | 0.12 | 0.02 | 1 | |

| 9. Average EBIT of AIM listed firms | −0.03 | −0.03 | −0.03 | 0.05 | 0.06 | −0.01 | −0.01 | −0.02 | 1 |

Acknowledgements

We would like to express our appreciation and thanks to the editor and the referees for their support and valuable comments.