Abstract

Previous studies provide suggestive evidence that entrepreneurship varies with the state of the business cycle. This article extends the knowledge base by exploring whether the rate of self-employment – a widely used measure of entrepreneurship – is a lagging or leading indicator of the business cycle. The study, which utilizes time series UK data on aggregate output, unemployment and self-employment rates, is robust to structural breaks in the cyclical relationships between these variables. The study finds evidence of significant bi-directional causality: that is, entrepreneurship both causes and is caused by business cycles. The covariance of entrepreneurship is positive with respect to output and negative with respect to unemployment.

Introduction

Entrepreneurship is widely linked to long-term increases in living standards, via wealth and job creation, innovation and growth (Audretsch and Keilbach, 2004; Parker, 2009). Yet, less is known about the relationship between entrepreneurship and the business cycle, including whether entrepreneurship is pro-cyclical or counter-cyclical, and whether it lags or leads business cycles. This is unfortunate given the importance of this issue from a policy perspective. If, for example, policymakers knew that shocks to entrepreneurship preceded business cycles, there might be a better intellectual case for entrepreneurship promotion policies than if entrepreneurship merely responds passively to cycles in output.

This issue is closely related to another important question: namely, the dynamic macro relationship between rates of entrepreneurship and unemployment. The extant literature (Parker, 2009; Storey, 1994) has tended to approach this question from a static viewpoint, for example by examining relationships between these variables at snapshots in time. Prior work has generated mixed and inconclusive estimates of this relationship and in any case, has focused more on growth issues (e.g. van Stel and Carree, 2004; van Stel et al., 2005; Wennekers et al., 2010) than on cyclical covariations in these variables. Nevertheless, the entrepreneurship–unemployment relationship remains of central policy interest, especially as entrepreneurship is often seen by policymakers as a way to combat unemployment (Congregado et al., 2010). Transitions into entrepreneurship can reduce unemployment rates, both directly (since each self-employee creates their own job) and indirectly, if entrepreneurs create additional jobs for others (Haltiwanger, 2006; Pfeiffer and Reize, 2000).

Throughout this article, entrepreneurship is operationalized as self-employment. This is consistent with the majority of studies of cyclical variations in entrepreneurship conducted to date. It is also consistent with some, although not all, of the theoretical analysis of this issue – including the link with unemployment which, like self-employment, is the subject of analysis by labour market economists. Furthermore, this operationalization is dictated by data availability considerations. Of course, entrepreneurship is a multidimensional construct and, arguably, self-employment captures only a partial and incomplete representation of it (Parker, 2009).

With this caveat in mind, this article explores whether the entrepreneurship rate co-varies with output and the unemployment rate. Using an unusually large sample of quarterly UK data (by the standards of prior research) from 1978 to 2010, we examine whether the self-employment rate is a leading or lagging indicator of these variables. Our empirical strategy proceeds in several steps, using multiple empirical methods for robustness. First, after extracting the cyclical components of these variables using a Hodrick-Prescott filter, we compute cross-correlation coefficients to identify any lagging or leading relationships between them. Second, we estimate a vector auto-regression (VAR) between these variables and perform Granger causality tests to establish causal links between them. An advantage of the VAR approach is that bi-directional, as well as uni-directional, causality is possible. Third, we re-estimate the VAR model to obtain results that are robust to structural breaks in the series. Fourth, we perform forecast error variance decompositions to gauge the relative strength of the impact of each variable on the others. Thus we are interested not only in the statistical but also in the economic significance of the cyclical relationships analysed.

Our findings confirm the value of a multi-method approach. The simple cross-correlations and VAR models based on the full sample (steps 1 and 2) imply simple uni-directional causality, with self-employment rates being a leading indicator of output and unemployment cycles. However, the structural break tests and re-estimations of the VAR model at step 3 show that the full sample masks several different outcomes that prevail in different periods. In the longest coherent sub-period, namely 1993−2010, we uncover bi-directionality between self-employment rates on the one hand, and output and unemployment rates, on the other. These results are confirmed by estimates using forecast error variance decomposition analysis (step 4).

The remainder of this article is structured as follows: The next section briefly summarizes some theoretical perspectives about entrepreneurship and the business cycle, as well as empirical evidence on the relationship. The third section describes the data. The fourth presents the methodology and results and finally, we discuss some implications of the results, together with some potential avenues for future research.

Entrepreneurship and the business cycle

Theory

One of the earliest theories of entrepreneurship and the business cycle appears in Josef Schumpeter (1911). According to Schumpeter, business cycles occur because entrepreneurs are heterogeneous, with the most able commercializing inventions at roughly the same time thereby, generating cyclical fluctuations in innovation and output. Although Schumpeter did not explain precisely why entrepreneurs choose to commercialize simultaneously, the idea that endogenous innovations by entrepreneurs drive cyclical variations has proven to be an enduringly popular one, which continues to influence economic theories of business cycles (e.g. Corriveau, 1994).

Arguably, Schumpeter’s theory has less to say about high-frequency business cycles than about ‘long wave’ cycles. The latter are characterized by major disruptive innovations whose effects unfold over many decades, and which tend to be followed by long periods of hiatus. As Simon Kuznets pointed out, only ‘the most momentous innovations such as steam power, electricity, etc’ (1940: 264) follow this kind of pattern, which is more akin to ‘long waves’ than to conventional notions of the business cycle. In fact, most innovations tend to arrive continuously over time, rather than being bunched in a way that gives rise to business cycles. So overall, Schumpeter’s theory of entrepreneur-driven business cycles does not seem to match the evidence very well.

Shleifer’s (1986) theory of implementation cycles addresses some of the limitations of Schumpeter’s theory. Shleifer argued that although major inventions may arrive in a steady stream over time, entrepreneurs optimally choose to implement them simultaneously to take advantage of high aggregate demand. The result is implementation cycles, in which innovations (rather than inventions) are bunched in particular periods. The reason is that, anticipating future imitators eroding their profits, exceptional entrepreneurs do best by delaying their innovations until times when profits are the highest, which is during a boom. The clustering of innovations then generates a boom in labour demand, which in turn generates the high demand for output needed to support the boom. Conversely, when entrepreneurs expect a boom only in the distant future, they may choose to postpone implementation, consigning the economy to a recession. The duration of a recession depends on entrepreneurs’ (self-fulfilling) expectations. Whereas Schumpeter viewed innovations as essentially autonomous, i.e. independent of demand, Shleifer explicitly linked innovation with expected (and actual) demand. Hence, entrepreneurs play a central role in driving business cycles; an implication of Shleifer’s theory being that entrepreneurship varies contemporaneously and positively with the business cycle.

Francois and Lloyd-Ellis (2003) criticized Shleifer’s model for assuming drastic but costless imitation and the impossibility of storing output. For example, if entrepreneurs could store their output, they would do best by producing when costs are low (i.e. during recessions) and selling when demand is high (i.e. during booms). Obviously, this would undermine the existence of cycles. Francois and Lloyd-Ellis relaxed the assumption of drastic imitation and non-storage, yet were still able to show that entrepreneurs choose to release paradigm-shifting innovations together in good times, à la Shleifer. Entrepreneurs devote effort to developing, but not to implementing, new innovations in recessions because implementation would reveal valuable proprietary information to rivals, thereby reducing entrepreneurs’ competitive advantage – as a result, recessions are prolonged. However, ‘eventually it becomes profitable to implement the stock of innovations that have accumulated during the downturn, and the cycle begins again’ (Francois and Lloyd-Ellis, 2003: 532). For their part, booms come to an end because wage costs rise so much that new entrepreneurial activities become less profitable. As a result, entrepreneurs have incentives to divert effort away from production and towards new innovations instead, so the economy slows. Effectively, the opportunity cost of investing in innovation, and thereby enhancing future productivity growth, is lower in recessions. An implication of Francois and Lloyd-Ellis’ model, in slight contrast to Shleifer’s, is that entrepreneurship is pro-cyclical and leads output.

Another model which focuses on the demand side of the market is Caballero and Hammour (1994). These authors ask whether recessions result in fewer entries by entrepreneurs using the latest technology, or whether they accelerate the exits of incumbents who use old technologies. The former case is referred to as an ‘insulating’ effect, since it protects incumbents. Caballero and Hammour’s model predicts that the insulation case arises when firm entry costs are linear. This implies contemporaneous pro-cyclicality of entrepreneurship, as entry rates decline in recessions and recover in booms. In contrast, if firm entry costs are increasing in the number of firms looking to enter, entrepreneurial entry can occur at the same time as incumbents exit. In which case, entrepreneurship could be less pro-cyclical, and possibly even acylical.

Several other models explore the links between entrepreneurship, output and unemployment. Bernanke and Gertler (1989) stress the importance of entrepreneurs’ balance sheets. In boom times, entrepreneurs find it easy to obtain funds from lenders, which they use to invest in capital and labour. This enables them to increase output, keeping the good times going. The opposite process occurs in recessions: entrepreneurs exacerbate business cycles, implying a lagged pro-cyclical mechanism running from output to entrepreneurship. Hiring by entrepreneurs is also pro-cyclical, meaning that the unemployment rate is counter-cyclical: causality is predicted to run from entrepreneurship to unemployment. A second model by Rampini (2004) generates similar predictions, but in Rampini’s model greater wealth not only releases funds from lenders, but also decreases risk aversion, amplifying the effects emphasized by Bernanke and Gertler.

A third model by Ghatak et al. (2007) devotes the most attention to entrepreneurship as an occupational choice. Ghatak et al. argue that because wages and employment fall in recessions, less able individuals (including the unemployed) are encouraged to become entrepreneurs. The phenomenon of transitions into entrepreneurship increasing when the opportunity cost of entrepreneurship is low is known as a ‘recession push’ effect, implying a positive (i.e. counter-cyclical) relationship between unemployment and entrepreneurship (Parker, 2009). The causal relationship at this point in the cycle runs from unemployment, U, to entrepreneurship, E: U → E. Ghatak et al. (2007) go on to argue that if lenders apply a common interest rate to a mixed pool of entrepreneur borrowers, competitive pressures force them to respond to a reduction in the quality of the borrower pool in recessions by increasing interest rates. This reduces entrepreneurs’ resources and hence, their ability to hire, which in turn reduces wages and demand while increasing unemployment even more. At the same time, some entrepreneurs are forced to exit the market. The phenomenon of increasing transitions out of entrepreneurship when returns there are low is known as a ‘prosperity pull’ effect, implying a negative (i.e. pro-cyclical) relationship between unemployment and entrepreneurship. The causal relationship at this point in the cycle runs E → U. Hence Ghatak et al’s model implies two-way causality between cycles in entrepreneurship, on the one hand, and output and unemployment, on the other: entrepreneurs both affect and are affected by business cycles. Faria et al. (2009) propose a similar mechanism yielding two-way cyclical causality between entrepreneurship and unemployment, in which the number of firms increases in booms, reducing profits and causing a recession. The recession push effect then kicks in, with the number of firms and aggregate labour demand from entrepreneurs increasing, starting a new boom.

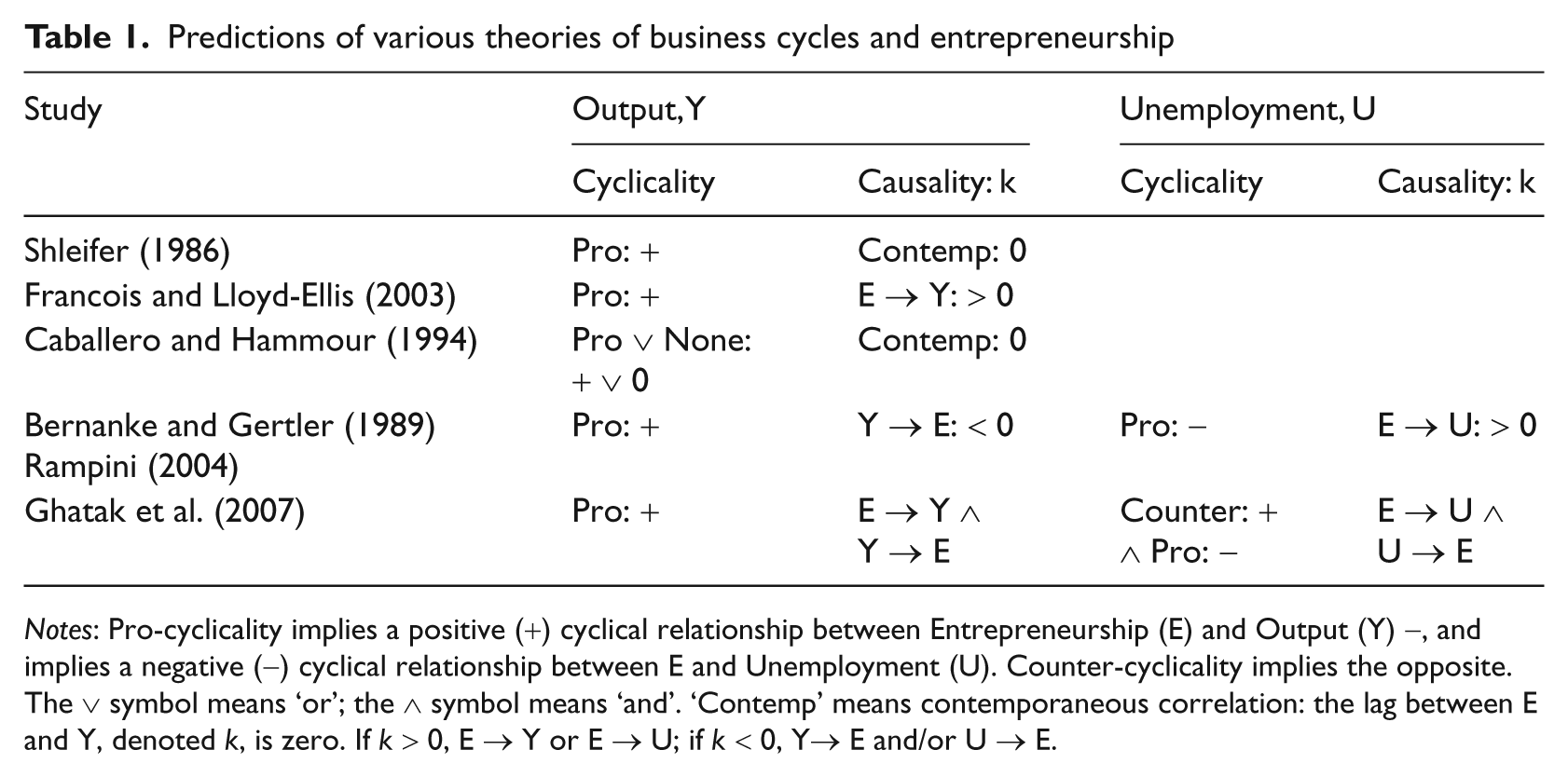

In summary, different theories predict a range of different possibilities, including uni-directional and bi-directional relationships between cycles in output, entrepreneurship and unemployment. Moreover, the temporal structure of these cycles could be contemporaneous or operate with a lag. Our interpretation of the different predictions associated with each model is summarized in Table 1. It should be noted that the Shleifer and Francois and Lloyd-Ellis entries are predicated implicitly on a definition of entrepreneurship as an innovative activity; the Caballero and Hammour entries are predicated more on entrepreneurship as entry; Bernanke and Gertler (1989) and Rampini (2004) are predicated on entrepreneurship in terms of borrowing and production activities by the existing stock of small businesses; and the Ghatak et al. (2007) entry conceives of entrepreneurship more in terms of occupational choice in the labour market and borrowing in the credit market. Thus, in a sense, the self-employment definition of entrepreneurship used in the empirical part of this article would seem to be most consistent with the final entry of Table 1. In which case, one might hypothesize pro-cyclicality with bi-directional causality as the most plausible theoretically-grounded outcome when entrepreneurship is operationalized in terms of self-employment rates. Before testing this empirically, we next review the extant empirical evidence on the cyclicality of entrepreneurship, under a variety of operationalizations as used by prior researchers.

Predictions of various theories of business cycles and entrepreneurship

Notes: Pro-cyclicality implies a positive (+) cyclical relationship between Entrepreneurship (E) and Output (Y) −, and implies a negative (−) cyclical relationship between E and Unemployment (U). Counter-cyclicality implies the opposite. The ∨ symbol means ‘or’; the ∧ symbol means ‘and’. ‘Contemp’ means contemporaneous correlation: the lag between E and Y, denoted k, is zero. If k > 0, E → Y or E → U; if k < 0, Y→ E and/or U → E.

Evidence

A handful of studies claim that rates of venture formation and transitions into entrepreneurship among individuals are higher on average in good economic times and lower on average in bad ones (Audretsch and Acs, 1994; Carrasco, 1999; Grant, 1996). While this suggests that entrepreneurship is pro-cyclical, and is consistent with many of the theories outlined previously here, this evidence is rather informal in nature, being based on estimates of the sign of time dummies in cross-section studies, rather than derived from careful analyses of time-series data.

To the best of our knowledge, one of the few previous studies to use time series methods to study entrepreneurship and output cycles is Congregado et al. (2011). Using an ‘unobserved components’ time-series model, Congregado et al. found evidence of business cycle-induced influences on self-employment rates in Spain, but not in the USA. Faria et al. (2009) also used time series data to establish the periodicity of entrepreneurship cycles in the USA, UK, Spain and Ireland as between five and 10 years, although whether the cycles are persistent or decay over time depends on the properties of the error term in their specification.

Other studies have explored cyclical variations in firm entry rates. One of the first of these was Highfield and Smiley (1987), whose temporal cross-correlation analysis associated growth in US company incorporation rates with higher unemployment and interest rates in the preceding year, and with lower unemployment and interest rates in subsequent years. This suggests that firms enter or expand to seize opportunities created during recessionary times, and thereby stimulate increased economic activity in later periods − consistent with Ghatak et al’s (2007) theorizing of bi-directionality between rates of unemployment and entrepreneurship. In contrast, Campbell (1998) obtained evidence (also in the form of cross-correlations) of straightforward pro-cyclicality in the US manufacturing plant entry rate, while Audretsch and Acs (1994) produced regression results showing that the industry-level rates of firm entry in the USA respond positively to both macro-economic growth and high unemployment rates.

In short, the evidence about the cyclicality of entrepreneurship and causality between business cycles and entrepreneurship is mixed. Consensus is also lacking about the relationship between entrepreneurship and unemployment (Parker, 2009; Storey, 1991). At the individual level of analysis, several studies have linked unemployment or redundancy with transitions to self-employment (Alba-Ramírez, 1994; Cowling and Mitchell, 1997; Evans and Leighton, 1990; Johnson, 1981). Many of these transitions appear to be of low-ability workers who have made poor job matches in paid employment in the past (Carrasco, 1999). As a result, many of these transitions are unsuccessful, culminating in speedy exit. At the aggregate level of analysis, Acs et al. (1994) reported a significant and positive correlation between aggregate self-employment and unemployment rates among a group of Organisation for Economic Co-operation and Development (OECD) countries. However, this correlation disappeared when additional variables such as gross domestic product (GDP) were controlled for (Parker and Robson, 2004). In addition, while Koellinger and Thurik (2009) found evidence of a recession push effect from unemployment to self-employment by using a panel of data from 22 OECD countries, Faria et al. (2010) reported a bi-directional relationship between unemployment and self-employment rates. So did Thurik et al. (2008), who embedded both recession-push and prosperity-pull mechanisms in a VAR model, which was estimated using aggregate data from 23 OECD countries from 1974–2002. Thurik et al. reported that prosperity-pull effects seemed to dominate recession-push effects, with a negative causal effect running from self-employment to unemployment rates. However, this mechanism seemed to operate with very long time lags of eight years and more in duration. Unlike the present article, Thurik et al. (2008) did not focus on the cyclical relationship between self-employment and unemployment; neither did that study address business cycle (output) effects.

In summary, the available evidence paints a mixed and inconclusive picture. There are several likely reasons for this, including the use of different measures of entrepreneurship and the different types of data and econometric methods deployed in prior work. We believe this warrants a new empirical analysis, which uses a consistent measure of entrepreneurship and is based on a multi-method approach. We also believe that it is important to recognize the possibility that different relationships prevail over different periods of time, even within the same country. We now describe the dataset on which our empirical analysis will be based.

Data

The first task is to measure entrepreneurship. Entrepreneurship is known to be a multifaceted concept which encompasses a range of roles and activities, including risk-bearing, coordination, arbitrage and Schumpeterian innovation (Iversen et al., 2008). Therefore, any single measure of entrepreneurship is unlikely to do justice to all of these different facets. In cross-country comparisons, by far the most common measure of entrepreneurship used in practice is self-employment (Iversen et al., 2008; Parker, 2009). This chiefly reflects the widespread availability of aggregate self-employment data for a range of countries. As noted by entrepreneurship scholars, the self-employment definition has the merit of inclusiveness and convenience. It also has a theoretical rationale: by being residual claimants of their own ventures, the self-employed correspond to the risk-bearing arbitrageur entrepreneur emphasized in the writings of Knight, Say and Kirzner (Iversen et al., 2008; O’Kean and Menudo, 2008).

However, self-employment has its limitations as a measure of entrepreneurship. For example, it includes numerous casual businesses as well as long-established enterprises. Self-employment data also typically under-sample Schumpeterian innovative entrepreneurs relative to ‘replicative’ businesses (Audretsch, 2002; Baumol et al., 2009). However, we were unable to find an alternative (or supplementary) measure to self-employment for a sufficiently long period to conduct time series analysis. Hence, the theoretical and empirical ability to interpret our results is likely to be restricted to the specialized domain of entrepreneurship operationalized in terms of self-employment. This limitation should be borne in mind when interpreting the results below.

We use seasonally adjusted data on UK self-employment (S t ) and unemployment rates (U t ), where seasonal adjustment was performed using the X-12 ARIMA algorithm. The self-employment rate is defined as the share of employed people that is self-employed. The source of the data is Work Force Jobs, which is part of the Labour Force Survey collected by the UK Office for National Statistics. The longest available span of data available commences in 1978(II) and ends in 2010(III). Data on real GDP, denoted by Y t , are taken from the Quarterly National Accounts database. These data are also seasonally adjusted and are expressed in billions of chained 2006 pounds sterling.

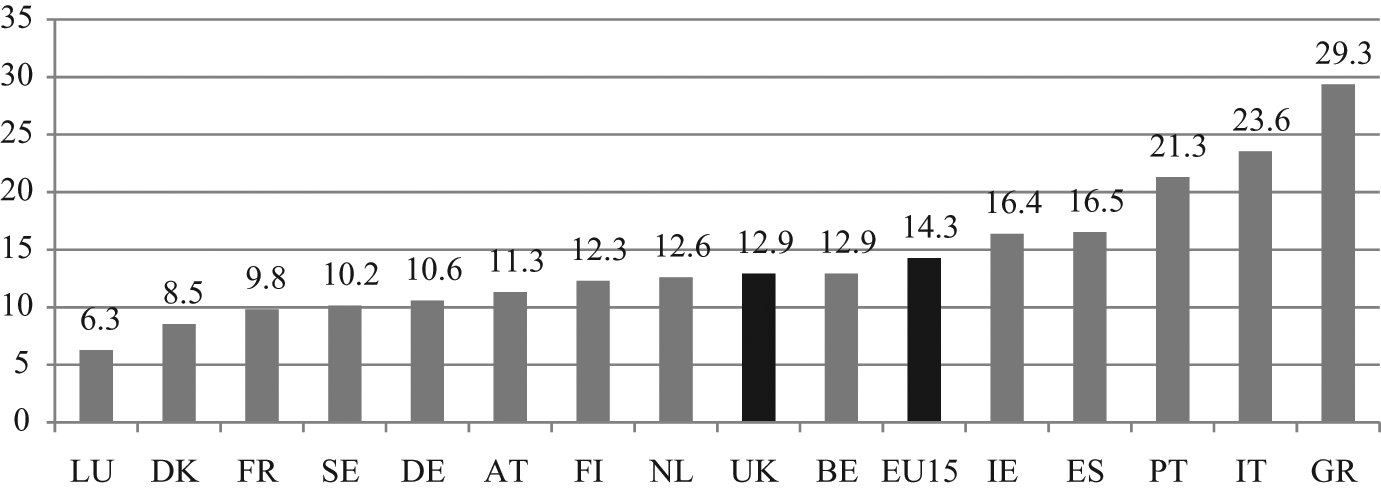

In total, 3.8 million people were self-employed in the UK in 2008. The UK self-employment rate is similar to that in Belgium and the Netherlands, and is in the mid-range for the EU-15 (see Figure 1).

Self-employment rates in the EU-15

Results

This section presents the empirical results in several steps. First, we report the results of analysing co-movements between entrepreneurship cycles and the output and unemployment cycles. Second, we move from correlations to Granger causality, estimating a VAR structure over the full data sample. Third, we allow for the possibility of structural breaks in cyclical relationships at different points of time. Thus, we re-examine causality for different subsamples identified from a structural break analysis. Finally, we report results from forecast error variance decompositions, which allows us to test the forecast power of each variable on the others.

Bivariate correlations

We first estimate the co-movements between self-employment, output and unemployment. We follow the empirical business cycle literature by applying the standard methodology developed by Burns and Mitchell (1946). This methodology interprets the correlation coefficients cor(k), k∈{0, ±1, ± 2, ± 3, ± 4} as measures of the degree of co-movement between each pair of time series. As is standard in the business cycle literature, and following the practice of the US Census Bureau, we apply the Hodrick-Prescott filter to X11-SA series to de-trend the data. Experimentation with alternative filters, including a modified Hodrick-Prescott filter applied to the trend-cycle component of the series (as used by the Bank of Spain in its Signal Extraction in ARIMA Time Series method) yielded virtually identical results. This suggests that our results are not sensitive to the filtering method used to obtain the cyclical component of the series.

The following summary may help interpret the correlations reported below. First, the contemporaneous correlation coefficient, cor(0), describes the degree of contemporaneous co-movement. Second, the cross-correlation coefficients, cor(k), describe the phase shift of one series relative to another. Thus a large correlation at t+k (respectively, t-k) indicates that a series lags (respectively, leads) the cycle by k years. If the variable’s value of the cross-correlation is highest at k = 0, then the variable is taken to move contemporaneously with the cycle.

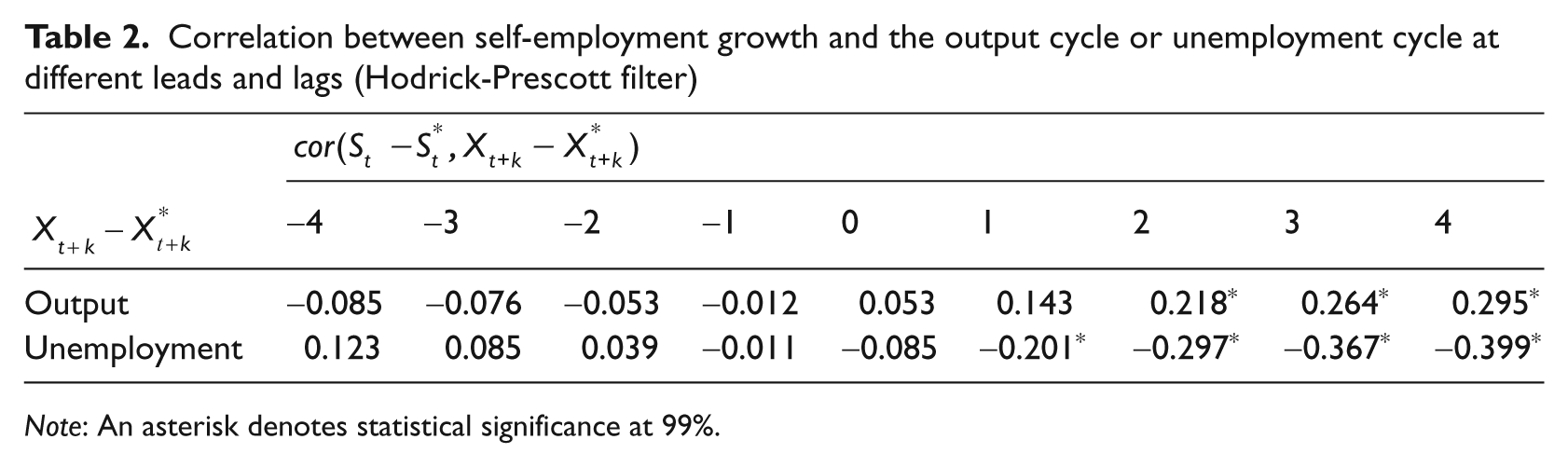

Table 2 reports estimated correlations for up to four leads and lags between the Hodrick-Prescott-filtered series for self-employment and output: denoted by St-St* and Yt-Yt* respectively, and between self-employment and unemployment, Ut-Ut*. The first row of Table 2 indicates that cycles in entrepreneurship are also significantly associated with cycles in output up to four quarters later. Furthermore, the relationship is one of pro-cyclicality. The second row of Table 2 indicates that cycles in entrepreneurship are significantly associated with cycles in unemployment up to four quarters later. Here the relationship is negative, suggesting that positive upswings in the cyclical component of entrepreneurship are associated with downswings in the cyclical component of unemployment. This also implies pro-cyclicality (see the notes to Table 1).

Correlation between self-employment growth and the output cycle or unemployment cycle at different leads and lags (Hodrick-Prescott filter)

Note: An asterisk denotes statistical significance at 99%.

Granger causality tests

The purpose of this section is to establish Granger causality in the relationships under study. Granger causality is tested using the estimates of two VAR models, each comprising two equations. The first model contains equations explaining self-employment cycles and output cycles. The second model contains equations explaining self-employment cycles and unemployment cycles. Since Ng and Perron (2001) tests have established that the three cyclical variables are stationary, 1 we can estimate the two VAR models, which are written as follows:

As in Table 2, the differences

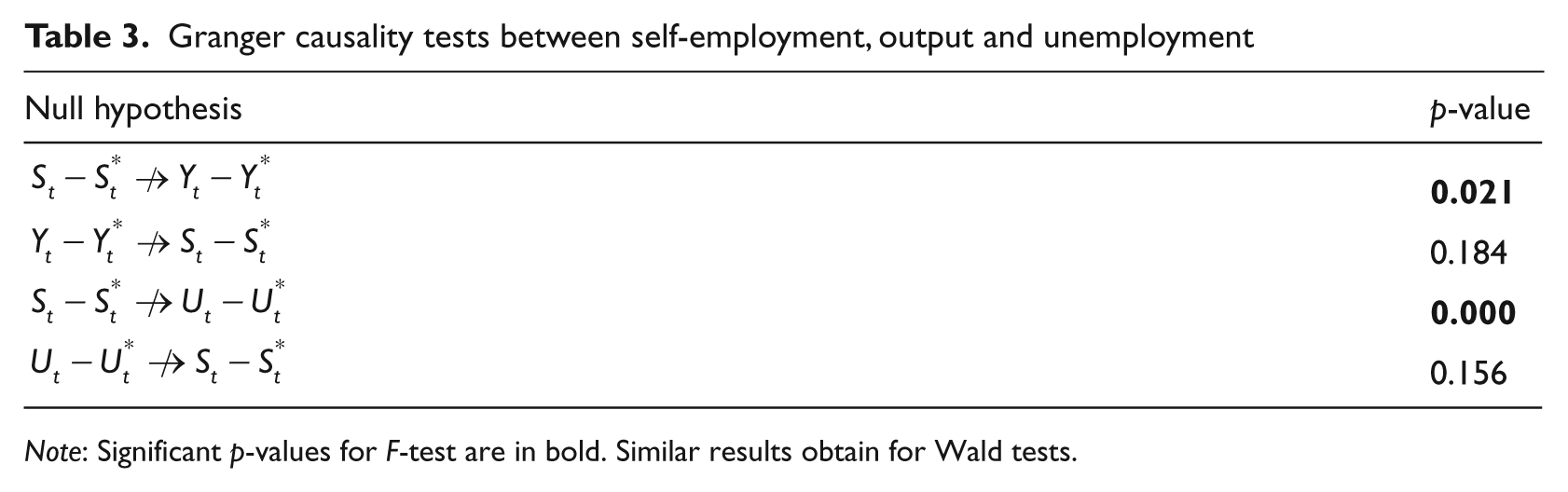

Table 3 reports the results of Granger causality tests based on these VARs, where the null is the hypothesis of no causation. In all cases and for any relationship, null hypotheses allow causality to run in either direction. The first row of Table 3 indicates a significant causal relationship running from self-employment variations to output variations, consistent with row 1 of Table 2. Reverse Granger causality (row 2 of Table 3) is not supported at conventional levels of significance. The third row of Table 3 indicates a significant causal relationship running from self-employment variations to unemployment variations, also consistent with the findings in Table 2 (row 2). Here too, we cannot reject the null hypothesis of no reverse causation running from unemployment variations to self-employment variations. Hence overall, Granger causality tests confirm the findings in Table 2; moreover, they suggest that these associations also capture causality, in Granger’s (1969) sense.

Granger causality tests between self-employment, output and unemployment

Note: Significant p-values for F-test are in bold. Similar results obtain for Wald tests.

Structural breaks: causality reconsidered

Since we are considering a long period of time (1978–2010), it is possible that the two relationships under consideration have undergone some structural shifts. Because the existence of structural shifts would bias the results, leading to incorrect inference about cyclicality, we checked for (possibly multiple) structural breaks in the relationships estimated in the previous subsection, using a methodology proposed by Bai and Perron (1998, 2003a, 2003b). In the absence of structural breaks, the inferences made earlier remain valid; however, in the presence of structural breaks, the causal relationships estimated in the previous subsection need to be re-estimated for each sub-period determined by the breaks. In this way we can avoid drawing spurious conclusions from an inappropriately conjoined set of sub-periods.

We give a brief description of the Bai-Perron methodology before turning to the results (further details can be found in the Appendix). The Bai-Perron methodology comprises a sequence of tests of the following form. First, the null hypothesis of no structural breaks is tested against the alternative of an unknown number of breaks. If the null is rejected, one proceeds to the second step, which contains a set of tests of no breaks against an integer number l of breaks. If these tests show evidence of at least one break, at the third step a further set of hypotheses of l breaks is tested against the alternative of l +1 breaks. This identifies the precise number of structural breaks, as well as break points, in the data.

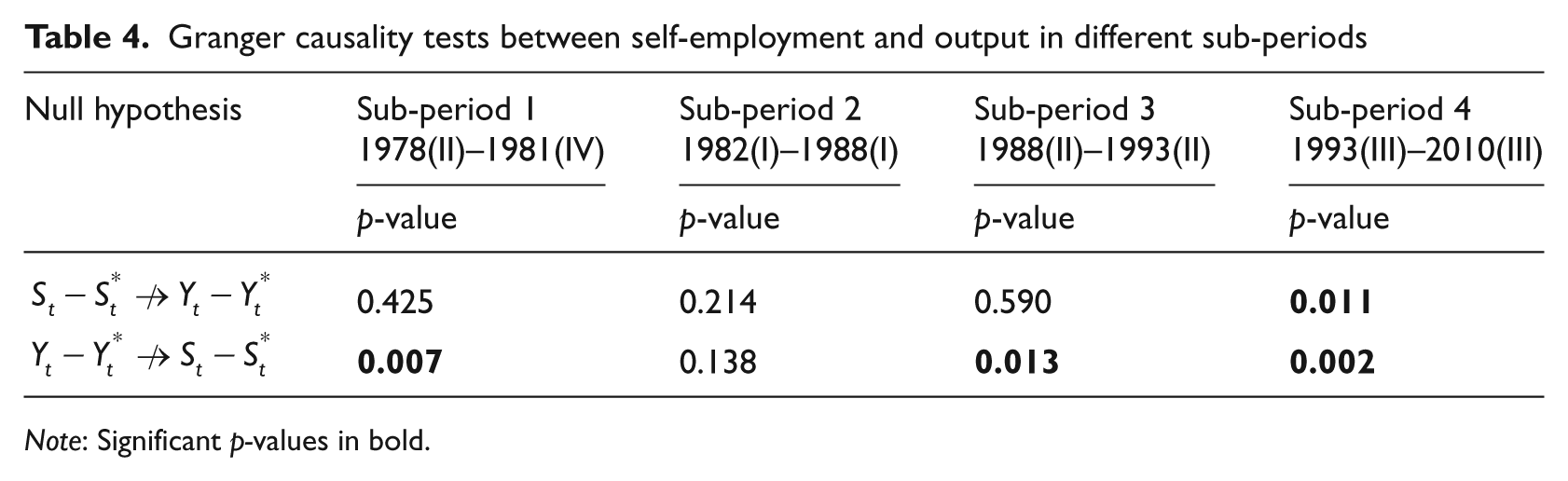

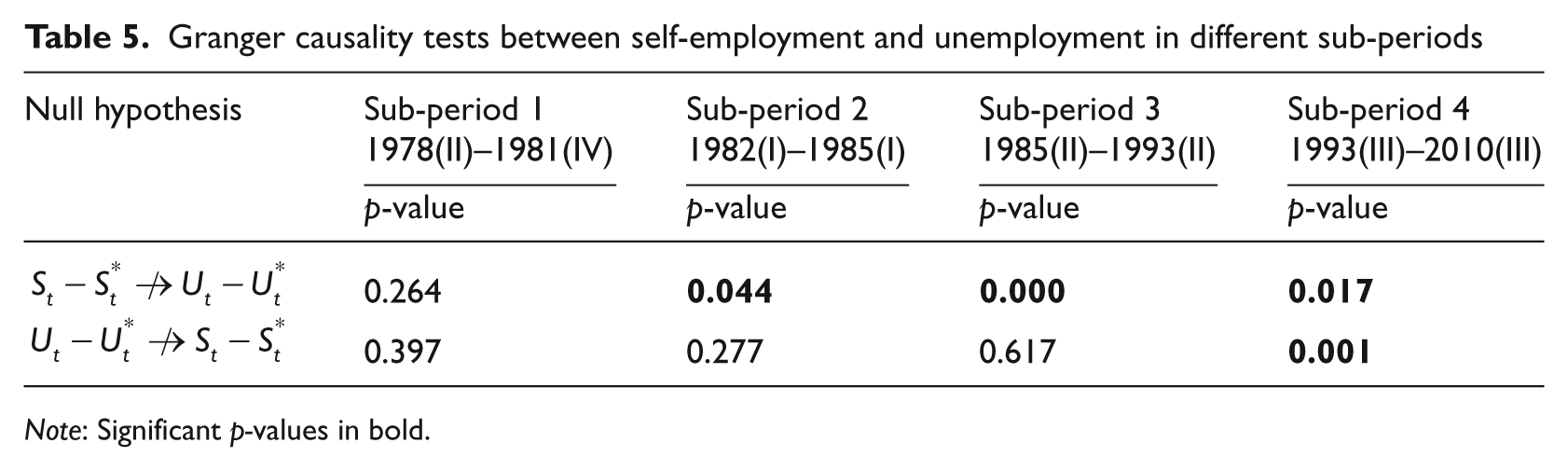

As Table 7 in the Appendix shows, the S-Y relationship is subject to three structural breaks, with break points 1982(I), 1988(II) and 1993(III). This implies four sub-periods over which the S-Y relationship can exhibit different cyclical relationships: 1978(II)−1981(IV); 1982(I)−1988(I); 1988(II)−1993(II); and 1993(III)−2010(III). Strikingly, as Table 8 in the Appendix shows, the S-U relationship is also subject to three structural breaks, with similar break points as for the S-Y relationship: 1982(I), 1985(II) and 1993(III). This implies four sub-periods in which the S-U relationship can exhibit different cyclical relationships: 1978(II)−1981(IV); 1982(I)−1985(I); 1985(II)−1993(II); and 1993(III)−2010(III).

Given the existence of structural breaks in both the S-Y and S-U relationships, we re-estimate the VAR models (1) and (2) for each sub-period separately, and the results are summarized in Tables 4 and 5. Looking at Table 4 first, it is immediately clear that different sub-periods exhibit different cyclical relationships, and that these differ from those reported for the full-sample analyses in Tables 2 and 3. In particular, the first three sub-periods, each of which is relatively short, do not exhibit causality running from self-employment cycles to output cycles; if anything, the reverse is true. However, the longest sub-period, 1993(III)−2010(III), exhibits pro-cyclical bi-directional causality between entrepreneurship and output. The latter finding is consistent in principle with Ghatak et al.’s (2007) model, reviewed previously in this article.

Granger causality tests between self-employment and output in different sub-periods

Note: Significant p-values in bold.

Granger causality tests between self-employment and unemployment in different sub-periods

Note: Significant p-values in bold.

Greater similarity between the full-sample and sub-period findings characterizes the cyclical S-U relationships reported in Table 5. Causality running from the self-employment to the unemployment cycle is statistically significant in all but the first period in Table 5; but in the final, longest, sub-period we have (as in Table 4) significant bi-directionality in the relationship. This too is consistent with our interpretation of the Ghatak et al. (2007) model. It is also consistent with some prior evidence, discussed previously, of bi-directionality between self-employment and unemployment rates (Faria et al., 2009, 2010; Highfield and Smiley, 1987; Thurik et al., 2008).

Forecast error variance decomposition

The results obtained so far have clarified the existence and significance of causal cyclical relationships between entrepreneurship, on the one hand, and output and unemployment, on the other; but it has not established the strength of these relationships. Thus we can ask: how much of the variance in cyclical variations in these variables is accounted for by the others? The greater the variance accounted for by entrepreneurship, for example, the greater the importance of this variable for driving business cycles.

A method know as the forecast error variance decomposition technique enables us to answer this question. This technique identifies the relative importance of one variable’s shock in explaining the predictive error variability of another at different time leads. If the forecast error variance of a variable at a given horizon is explained entirely by an idiosyncratic shock, then its forecast at that horizon does not improve when considering the behaviour of the other variable’s shock.

To see how the technique works, the forecast error variance of GDP is decomposed into two proportions: one attributed to self-employment and one attributed to itself. The bivariate VAR used for this end, can be expressed as follows:

where A(L) is a kth-order matrix polynomial in the lag operator L, and.

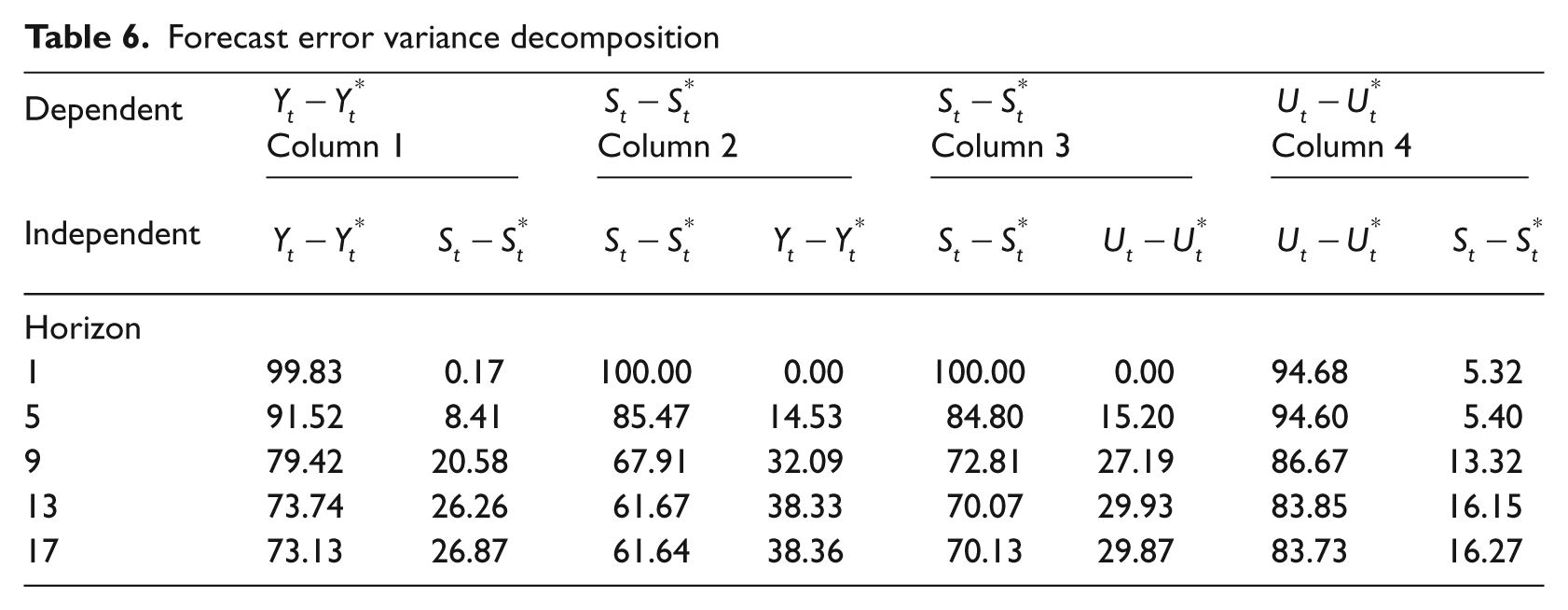

This system is estimated for the longest sub-period available in the data, namely 1993(III)−2010(III); using data from the other periods yields similar results. 2 Results are summarized in the first column of Table 6. The second and third columns of this table decompose the forecast error variance of self-employment into one proportion attributable to itself, and another attributable to GDP and unemployment, respectively. The final column of Table 6 decomposes the forecast error variance of unemployment into two proportions: one attributed to self-employment and one attributed to itself, using the VAR:

where

Forecast error variance decomposition

The various rows of Table 6 give the cumulative impact of cyclical variations in entrepreneurship and the other variables. One would expect that as shocks die away, the cumulative impacts from any variable would converge. That is exactly what we see in Table 6. Thus, for example, at the foot of column 1, the results show that 17 quarters out from an initial set of shocks, 26.87 percent of the variation in the error variance of cyclical output is accounted for by the entrepreneurship cycle. Convergence can be seen by looking down the columns.

Output variations have an even stronger effect on the entrepreneurship cycle: at the foot of column 2, we see that the forecast error variance of GDP explains more than 38 percent of the forecast error variance of entrepreneurship. Taken together, these results confirm bi-directionality of the cyclical relationship between entrepreneurship and output, while also demonstrating that the impacts of these variables on each other are sizeable in economic terms. In a similar way, columns 3 and 4 of Table 6 demonstrate bi-directionality between entrepreneurship and unemployment, with a stronger effect of the latter on the former (29.87%) than vice-versa (16.27%). To summarize, even though entrepreneurship is an important driver of cyclical variations in output and unemployment over the period 1993−2010, its own cycle has been even more strongly affected by cyclical variations in output and unemployment.

Conclusion

This article has examined the cyclical relationship between self-employment, output and unemployment by using a sample of more than three decades of quarterly time series data from the UK. The analysis applied a novel multi-method empirical approach to a relatively long span of quarterly time series data. Another novelty is allowing for structural breaks. The latter turned out to be an especially important issue, having a major bearing on the qualitative nature of the results. Without taking structural breaks into account, we found a pro-cyclical relationship with entrepreneurship cycles driving cycles in output and unemployment. However, when we relaxed the assumption of common relationships over the sample, a different picture emerged. In particular, several distinct sub-periods were detected, which each exhibited different cyclical relationships. Over the longest sub-period for which a common relationship could be sustained, namely 1993–2010, we found strong evidence of bi-directionality, with cycles in entrepreneurship causing and being caused by cycles in output and unemployment. Throughout, the dominant pattern was of pro-cyclicality in entrepreneurship.

Our findings are consistent with some previous empirical research as well as one of the theoretical frameworks proposed by previous researchers. In terms of theory, Ghatak et al.’s (2007) occupational choice model predicts bi-directional pro-cyclicality, which is also what we found to hold empirically. It is probably no coincidence that this theory, which matches our results most closely, emphasizes the role of labour markets which in turn matches the self-employment operationalization of entrepreneurship. In terms of prior empirical literature, our findings relating to the impact of entrepreneurship on the rest of the economy are broadly consistent with previous studies which have related self-employment rates to subsequent aggregate economic performance (Fritsch and Mueller, 2004; Koellinger and Thurik, 2009; Thurik et al., 2008). At the same time, our findings are consistent with evidence that business cycle fluctuations in output and unemployment rates lead fluctuations in self-employment rates (Carmona et al., 2010; Congregado et al., 2011). In addition, pro-cyclicality has been found using cross-section data and regression methods in prior work (Audretsch and Acs, 1994; Carrasco, 1999; Grant, 1996). However, perhaps most striking is our finding of bi-directionality between cyclical variations in self-employment and unemployment rates. Other than Faria et al. (2010), few researchers have paid much attention to this issue. Arguably, bi-directionality magnifies the role of entrepreneurship in a policy setting, relative to one-way causality: not only is entrepreneurship affected by the economic cycle, but it also seems to affect it.

Does evidence of pro-cyclicality of entrepreneurship matter? Compared with studies of entrepreneurship and growth (van Stel et al., 2005; Wennekers et al., 2010), much less is known about cyclical relationships. Yet these are also important, as business cycles have real effects on living standards and spur the involvement of central banks and politicians in efforts to ameliorate their effects. A better understanding of the empirical structure of business cycles is clearly important in its own right, and our findings of a central role for entrepreneurship add to the growing consensus that important macro-economic trends and fluctuations cannot be fully understood without comprehending the role of entrepreneurship. More broadly, recent work is beginning to uncover the centrality of entrepreneurs in aggregate wealth accumulation (Cagetti and de Nardi, 2006), as well as innovation and economic growth (Audretsch, 2006; Fritsch and Mueller, 2004).

Implications for policymaking and practice

Some tentative policy recommendations can be advanced on the basis of our research. It may be advisable, for example, to frame a different set of counter-cyclical policies that boost entrepreneurship during downturns, while curbing incentives for market entry during upturns. So, for example, the British Small Firms Loan Guarantee Scheme and Enterprise Allowance Scheme (Parker, 2009) were both launched during the recessions of the early 1980s which, according to our reasoning, would be the best time in the cycle to do so. During booms, such as the one running from the mid-1990s through to the mid-2000s, it would have been advisable to roll back pro-entrepreneurship programmes: for example, this could involve reducing tax relief for small businesses and restricting access to the Small Firms Loan Guarantee Scheme. Whether by luck or design, the British government of the day did both of these things thereby, potentially smoothing out the entrepreneurship and business cycles. Of course, this could not avert the financial crisis of the late 2000s which had its roots elsewhere: namely, the widespread construction and dissemination of toxic bank loan portfolios.

Our findings also add to the debate in the scholarly literature, where they may even help reconcile some disparate prior empirical findings. For example, as noted in our review of the evidence on entrepreneurship and the business cycle, some previous researchers have detected causality running from entrepreneurship to output and/or unemployment cycles, while others have recorded the opposite − and others still have claimed to find evidence of bi-directional causality. Our results show that the dominant pattern depends in part on the period under investigation, since the cyclical relationship between entrepreneurship, output and unemployment seems to vary over time. The disparate findings obtained in previous research were all replicated in our UK study, albeit in different sub-periods. Nevertheless, the predominant pattern seems to be one of pro-cyclical bi-directionality, which strikes us as an exciting and intriguing characterization of the relationship between entrepreneurship and the business cycle.

Recommendations for future research

To conclude, we believe the present article advances our understanding of the role of entrepreneurship in the context of macro-economic business cycles. However, more research remains to be done. One important avenue for future work is to obtain time series data for different measures of entrepreneurship, for example Schumpeterian innovation. Alternative measures of entrepreneurship might exhibit different cyclical relationships with output and unemployment, consistent with alternative theories about how entrepreneurs propagate and respond to the business cycle fluctuations. Other useful tasks for future work include analysing data for countries other than the UK, and pioneering theories which are suitable for different types of cycle. For example, the origins and nature of the Great Recession of 2007–2008 appears to be different from the recession of 1991–1992, which begs the question of whether entrepreneurs played different roles in each of these episodes. While the current article has made a start in demonstrating the power of suitable econometric techniques to uncover the role of entrepreneurs in these events, more fine-grained analysis would be well suited to open the ‘black box’ and shed more direct light on the precise mechanisms at play. This, in turn, could highlight the value of fresh theorizing along possibly new dimensions of analysis.

Footnotes

Appendix

At the first step, the structural break statistics are termed UDmax and WDmax. These are double maximum tests, where the null hypothesis of no structural breaks is tested against the alternative of an unknown number of breaks. At the second step, the statistics are termed SupFt(l)for up to l breaks. These are Wald tests for the hypothesis of 0 breaks vs. l breaks. The maximum number of breaks l is set at 8. At the third step, the statistics are termed the SupFt(l + 1/l). If this test is significant at the 1 percent level, then l+1 breaks are chosen. We used a testing specification where S−S* is the dependent variable and either Y−Y* or U−U* is the dependent variable. We account for potential serial correlation via non-parametric adjustments. We allowed for different distributions for the data across segments and different variances of the residuals across segments.

The results of applying Bai-Perron tests to the relationship between output cycle and self-employment cycle, i.e. S-Y, are shown in Table 7. Table 8 does the same for the relationship between the unemployment cycle and the self-employment cycle. In both Tables 7 and 8, the UDmax, WDmax and the SupFt (l) statistics indicate that at least one break is present in our series. Moreover, the SupFt(l + 1/l test is significant for l = 3, indicating three breaks at the dates given in the lower panels of the tables. It is unclear what ‘caused’ the observed structural breaks; they may reflect changes in overall market conditions, for example, but it is impossible to tell without more information.

Acknowledgements

The authors would like to thank the three anonymous reviewers for their insightful and constructive feedback.

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Notes

Simon C. Parker is an associate professor at the Ivey School of Business, University of Western Ontario. He researches the economics of entrepreneurship.

Emilio Congregado is Associate Professor of Applied Economics at the Department of Economics, University of Huelva. His areas of research include the economics of entrepreneurship, labour economics and regional economics.

Antonio A. Golpe is Lecturer in Economics at the Department of Economics, University of Huelva. His main research interest is in the area of macroeconometrics applied to the analysis of entrepreneurship.