Abstract

This article examines the role of strategic intensity or commitment to a chosen course of action, and the impact of pure versus hybrid competitive strategies on competitive performance in transition economies, using survey data (N = 333) from Bulgaria. We find that strategic intensity is positively related to performance; firms that deviate from pure cost leadership or differentiation and achieve a balance on both dimensions report superior performance. In a post hoc analysis of our data, we find preliminary evidence that strategic intensity may act as a mediator of the relationship between strategic type and performance.

Introduction

The dominant paradigm of mainstream strategy research, developed in the context of established businesses in advanced market economies, has coalesced around Porter’s (1980, 1985, 1996) argument that strategic purity, or the clear choice of one generic competitive strategy (either low cost or differentiation), contributes to better performance. The ‘pure’ strategy argument is predicated on the assumption that competitors are operating at the productivity frontier. The productivity frontier constitutes ‘the sum of all existing best practices at any given time’ (Porter, 1996: 62), so that the points along the frontier represent all combinations of delivered customer value and relative cost position that render superior economic performance. In other words, Porter’s theory is a theory of competitive advantage (i.e. above industry average performance) for capable competitors operating at the productivity frontier in the relatively efficient markets of an advanced economy.

This article examines a very different population: new firms 1 at a stage of initial competitive positioning, operating in transitional economies, 2 characterized by resource scarcity and inefficient markets. These firms are not likely to operate at the productivity frontier (Deliktas and Balcilar, 2005; Sabirianova et al., 2005). Instead, their goal is to improve operational effectiveness and reach competitive parity with industry incumbents (i.e. attain industry average performance) before they can aspire for competitive advantage in industry rivalry. Currently, we do not know if the dominant theoretical paradigm linking competitive strategies and performance persists in the case of new ventures in transition economies. With the notable exception of Lyles et al.’s (2004) and Danis et al.’s (2010) studies of the competitive strategies and performance of new and small ventures in Hungary, there is a dearth of empirical research in this area. This is the knowledge gap this article explores; thus, we use the context of our study to extend the boundaries of Porter’s theory of competitive advantage. More specifically, we seek to provide a theoretical explanation regarding the optimal competitive trajectory toward the productivity frontier that Porter characterizes as ‘improving operational effectiveness’ (Porter, 1996: 62).

We complement the industrial organization economic theory of competitive advantage (Bain, 1956; Porter, 1980, 1985, 1990) with the concept of strategic intensity, defined as managerial and resource commitments applied to a strategic imperative (Hamel and Prahalad, 1989; Reitsperger et al., 1993, 1994; Thornhill and White, 2007). As such, we develop a two-stage argument; first, we argue that new ventures in transition economies need to move toward the productivity frontier, or ‘catch up’ with capable competitors, making the intensity of strategic commitment an important factor in explaining new venture performance. Second, we argue that in the movement toward the productivity frontier in transition economies, a hybrid strategy, or a combination of low cost and differentiation positioning, is most likely to maximize performance. In a post hoc examination, we link strategic intensity and strategic positioning and present an innovative and intriguing analysis which explores how strategic intensity may act as a mediator in the relationship between strategy and performance.

Empirically, our analysis draws on the modeling method developed by Thornhill and White (2007) in their study of the competitive strategies and performance of Canadian businesses. These authors measured the firm’s competitive strategy as the angle of the deviation of the firm’s strategy vector in a two-dimensional orthogonal strategy space delineated by ‘pure low cost’ and ‘pure differentiation’ axes. In their study, Thornhill and White (2007) found that irrespective of industry-specific success factors, a pure strategy (either low cost or differentiation) generally outperforms a hybrid strategy. Although we follow their modeling approach, our results are markedly different.

The article proceeds as follows. After a review of the theoretical perspectives that guide the study, we formulate and test two hypotheses using survey data from 333 new and small Bulgarian private ventures. We discuss our findings and interpret them in light of the institutional and competitive conditions in a transitional economy context. We conclude by outlining the implications for research and practice.

Theory development

The productivity frontier

The concept of a productivity (or efficiency) frontier is similar to the concept of production possibility frontier applied in macroeconomics. The productivity frontier (commonly represented visually as a curve in a two-dimensional space) represents ‘the maximum value that a company delivering a particular product or service can create at a given cost, using the best available technologies, skills, management techniques, and purchased inputs’ (Porter, 1996: 62). Firms that are operationally effective are said to operate on the frontier, based on their pursuit of strategies that utilize state-of-the-art operational best practices and technologies. Firms that are not optimally effective exist within, or below, the frontier to the degree they do not utilize existing best practices and/or technologies.

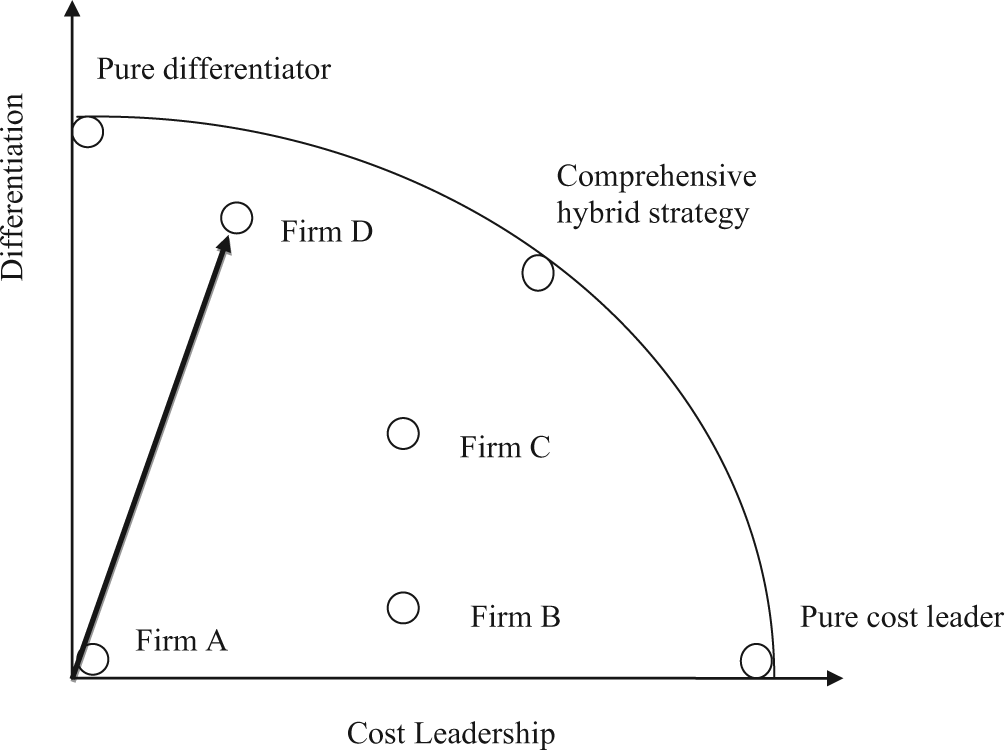

Firms move toward the productivity frontier by choosing a strategic orientation and committing resources toward the implementation of the chosen strategy. We illustrate different strategic positions as they relate to the productivity frontier in Figure 1 which situates firm strategies in a two-dimensional space defined by cost leadership and differentiation, an approach similar to that used by Reitsperger et al. (1994) and Thornhill and White (2007). For capable, operationally effective competitors, the goal of competitive strategy is to identify a product/market positioning that maximizes the value created at a given cost and thus, to gain competitive advantage resulting in superior performance relative to the industry average. These positions are represented in Figure 1 as the firms operating on the productivity frontier in a pure low cost, pure differentiation, or hybrid competitive positioning. In contrast, Firm A does not emphasize any strategy and makes little progress toward the productivity frontier, whereas Firms B, C, and D illustrate various degrees of commitment to improving their operational effectiveness and consequently, move toward the productivity frontier. The direction of the strategy vector in relationship to the two axes (low cost and differentiation) represents the strategic orientation of the firm (i.e. pure low cost, pure differentiation, or various combinations of the two). The length of the strategy vector indicates the firm’s strategic intensity. Accordingly, Firm D is situated closer to differentiation than to hybrid strategy and is characterized by relatively high strategic intensity (i.e. the length of the vector is close to the longest one possible to the productivity frontier).

Strategic intensity and productivity frontier.

New ventures typically operate below the productivity frontier facing face significant cost disadvantages as they cannot generate learning curve economies (because of their young age) or economies of scale (because of their relatively small scale of operations). Neither do they wield significant bargaining power because of their small market share. New industry entrants need to absorb significant sunk costs in establishing brand presence and shifting customer preferences, and may be preempted in their access to superior locations, raw materials, credit, and/or distribution channels (Bain, 1956; Porter, 1980). Newness and smallness do confer some advantages in competitive rivalry; new firms are not entrenched in a dominant logic (Bettis and Prahalad, 1995), and do not have to make trade-offs with existing activity systems allowing them to explore novel combinations of low cost and value creation (Porter, 1996). Smallness helps if large and rigid rivals can be outmaneuvered through: ‘speed, stealth, and selective attack’ (Chen and Hambrick, 1995). Empirical evidence from frontier analysis studies across diverse institutional and industry contexts, however, (Caves, 1998; Sutton, 1997; Taymaz, 2005; Tybout, 2000) suggests that new entrants, on average, are less efficient than large established competitors. Relatedly, research, particularly in the population ecology tradition (Aldrich, 1990; Geroski et al., 2010; Wiklund et al., 2010), has shown that new firms are highly susceptible to institutional and competitive pressures and exceedingly prone to organizational failure and death. Thus, before they can aspire for competitive advantage, new players need to ‘race to the frontier’ and reach competitive parity (industry average performance) in order to ensure their competitive viability.

The challenge of meeting industry levels of operational effectiveness is a particularly arduous task for new firms in transition economies. Regarding the cost dimension, achieving low costs in transition economies is critical because of price sensitivity driven by relatively low disposable incomes. 3 Unfortunately, in addition to the cost disadvantages common to ventures across market and institutional contexts (discussed above), the voids in the underdeveloped institutional environment (Khanna and Palepu, 1997) and infrastructure deficiencies (Hitt et al., 2006) are particularly detrimental to new and small ventures (Doern, 2009). For example, the institutional barriers to entry in transition economies are disproportionately high for new entrants (Chang and Wu, 2014); opportunistic government officials often take advantage of obscure regulatory regimes to exploit new and small firm vulnerabilities for personal gain (Manolova and Yan, 2002; Smallbone and Welter, 2001). These deficiencies lead to the new ventures experiencing higher costs of doing business relative to both foreign competitors, hailing from countries with more favorable institutional regimes, and established domestic firms that may enjoy preferential regulatory treatment.

On the differentiation dimension, new ventures in transition economies encounter further challenges. As Murray (1988: 396) noted, a product differentiation strategy will be viable only if customers attach value to product attributes other than price. Unfortunately, transition economy markets are still relatively underdeveloped, thereby not yet deep (or segmented) enough to allow meaningful targeted differentiation, especially for products directed to affluent or sophisticated consumers (Cui and Liu, 2001; Manrai et al., 2001). In addition, new and small players in transition economies are less resource-endowed relative to their counterparts from developed market economies (Aulakh et al., 2000), so for example, there is a lack of managers with market economy experience (Lyles et al., 2004; Wright et al., 2005). In other words, new ventures in transition economies lack the organizational arrangements fostering innovation, marketing orientation, or exploitation of information technologies that may serve as a basis for creating superior customer value. The incomplete and inefficient factor markets (Luo, 2003) further constrain access to resources, which is particularly disadvantageous to creating value through a resource-intensive strategy such as differentiation.

Not surprisingly, empirical research indicates that firms in transition economies generally operate below the productivity frontier. For example, Sabirianova et al. (2005), in their comparative analysis of the productive efficiency of domestic and foreign-owned industrial firms in the Czech Republic and Russia, found that during the 1998–2000 period, the efficiency of the median domestic firm was 37.4% of the frontier in the Czech Republic and only 14.6% in Russia. The frontier in their study was defined as the mean productive efficiency of the top third of foreign-owned firms in the corresponding industry. Similarly, in their stochastic frontier analysis of the productive efficiency of 8341 large- and medium-sized enterprises in China, Zhang et al. (2003) found that within the private sector, foreign firms had higher R&D and productive efficiency than domestic collective-owned enterprises and joint stock companies.

To summarize, new firms in transition economies still have substantial progress to make in order to move toward the productivity frontier and improve their chances of success in market-based rivalry with established domestic players and capable competitors from developed economies. In the following section, we argue that strategic intensity, or the level of commitment to a strategic course of action, drives new venture progress toward the productivity frontier and so enhances their competitive performance.

Strategic intensity and new venture performance

The concept of strategic intensity and its association with performance was suggested by Lawless et al. (1989) and Reitsperger et al. (1994), but has so far received limited attention in the literature, as acknowledged by Thornhill and White (2007: 555). In the empirical work to date, which examines the association of strategic intensity and firm performance, results are mixed. Recently, Thornhill and White (2007), in their large panel data study of Canadian firms, found no significant relationship between strategic intensity and performance. Others, however, have found that strategic intensity affects performance, for example, Reitsperger et al. (1993) in their study of Japanese electronics manufacturers, Kim and Choi (1994) in the context of Korean small businesses, Spanos et al. (2004: 145) in their study of the competitive strategies of established Greek firms, and Acquaah and Yasai-Ardekani (2008) in their study of established Ghanaian firms.

Drawing on Reitsperger et al. (1994), we define strategic intensity as the level of commitment to a chosen strategy. Our definition is consistent with that of Acquaah and Yasai-Ardekani (2008: 349), who noted the need for a coherent strategy, involving high levels of emphasis, and with Kim and Choi’s (1994: 22) conclusion that ‘firms should focus on keeping a coherent pattern of their strategy’. We propose that when a firm prioritizes a strategic course of action, this strategic emphasis is expressed in both the level of managerial commitment and the level of resource commitment to the chosen course of action, resulting in improved competitive performance. We discuss each mechanism in turn, combining behavioral and economic theoretical lenses.

We commence with the role of managerial commitment. The distribution of managerial attention to particular types of activities is driven by firm-level priorities (Ocasio, 1997). Managers budget their time and energy in response to the objectives they need to accomplish and the incentives to do so. When the strategic priorities of the new venture emphasize improving operational efficiency, managers will likewise focus upon the implementation of these priorities. As one example, managerial commitment to export strategies has been positively linked with export performance (Shoham and Albaum, 1994). In a related stream of research, studies on the role of strategic planning have shown that when managers engage in the process with some intensity, strategic planning results in improved performance (Hopkins and Hopkins, 1997; Mintzberg, 1994). Thus, in line with the behavioral strategic management perspectives, we argue that strategic intensity leads to better performance through managerial commitment.

The strategic role of resource commitments is explored in various economic models; Dixit’s (1980) pioneering work on strategic behavior toward entry examines the manner in which rival firms’ payoffs (performance) in some future period can be influenced by strategic commitments (making investments or incurring sunk costs) made in an earlier period. For example, a firm pursuing a differentiation strategy through superior customer service may decide to invest in a sophisticated customer relationship management system or extensive training for its employees, while a firm pursuing a cost leadership strategy may invest in a highly efficient production line. When a firm commits durable, costly, and difficult-to-transfer resources to a chosen strategy, it sends a clear signal that it intends to remain as exit is costly and impractical (Ghemawat, 1991). This allows a firm to exploit early-mover advantages, deter imitation, and blunt substitution (Ghemawat, 1991; Raynor, 2007), improving its competitive performance.

Our arguments above rest on an important assumption, namely, that new firms intentionally commit to a strategic course of action. This is subject to debate. While some scholars (e.g. Jansen et al., 2013; Storey, 1994) describe most entrepreneurs as ‘muddling through’ strategic decision making, others (Ackelsberg and Arlow, 1985; Hansen and Hamilton, 2011) suggest that at least the best, and probably most, firms engage in intentional efforts to position themselves, even if they are not always effective. In further support of intentionality, Brinckmann et al. (2010) found a positive relationship between planning and performance for both new and small businesses in their meta-analysis.

Overall, managerial and resource commitment to a chosen course of action are important for improving new venture operational effectiveness and thus, enhancing competitive performance. Formally,

Hypothesis 1. In a transition economy, there is a positive relationship between strategic intensity and performance.

Hybrid strategies and new venture performance

In his theory of competitive advantage, Porter (1980, 1985, 1996) postulates that competitive strategy involves the choice of clear positioning in the product-market space based on either low cost or differentiation. While Porter (1980) states that neither pure strategic approach is inherently superior or inferior, he does argue that failing to make a choice, or trying to achieve a competitive advantage through every means, renders a firm ‘stuck in the middle’, which is usually a recipe for below-average performance.

Some theorists have argued that cost leadership strategies, which require substantial economies of scale or experience curve effects, are beyond the means of new and small ventures, while focus differentiation strategies involving product innovation, creative design, or high quality are more viable (Miller and Toulouse, 1986; Rugman and Verbeke, 1987/1988). Empirical evidence is mixed. Some studies find that any pure strategy improves new and small venture performance (Ebben and Johnson, 2005; Lechner et al., 2014). Others, however, find that different generic strategies are linked to different aspects of performance (Baum et al., 2001; Chandler and Hanks, 1994), or that one generic strategy is superior to another (Dowling and McGee, 1994; Lyles et al., 2004). Finally, some find that hybrid strategies, combining elements from both generic competitive strategies, lead to better performance (Carter et al., 1994; Kim and Choi, 1994; Parnell, 2013). Thus, while early prescriptions suggested that new and small firms would be advised to follow a focused differentiation strategy (Miller and Friesen, 1986a, 1986b; Miller and Toulouse, 1986; Rugman and Verbeke, 1987/1988), empirical evidence is largely inconclusive and results are influenced by a number of contextual factors, such as industry conditions (Escribá-Esteve et al., 2008; McDougall et al., 1992), entrepreneurial orientation (Lechner et al., 2014), or strategic intensity (Kim and Choi, 1994).

We argue that in their progress toward the productivity frontier, new ventures in transition economies will benefit most from pursuing a hybrid strategy, or a simultaneous emphasis on cost containment and value creation. We highlight three reasons why a hybrid strategy will be associated with better competitive performance: (1) the need to improve on multiple fronts, (2) the entrepreneurial legacy, and (3) the need to balance efficiency and flexibility.

First, as discussed in the preceding section, new ventures in transition economies are most likely to operate below the productivity frontier. For firms seeking to make progress toward the frontier by improving their operational effectiveness, it is not only possible, but appropriate, to improve on multiple fronts in order to ‘catch up’. The simultaneous improvement on both fronts matches well the competitive environment in transition economies. The price-sensitive nature of demand in transition economies, coupled with the need for some (but not extreme) level of differentiation, makes hybrid strategies (or a balance between low costs and differentiation) a preferable strategic orientation relative to pure generic strategies. This argument has been suggested by other researchers exploring the link between strategies and performance in the context of transition economies or the broader context of emerging markets (Acquaah and Yasai-Ardekani, 2008; Gopalakrishna and Subramanian, 2001; Hlavacka et al., 2001). A similar argument has been advanced in recent theorizing about organizational ambidexterity. Gulati and Puranam (2009) and Birkinshaw and Gupta (2013) suggest that the simultaneous pursuit of exploitation (efficiency) and exploration (differentiation) is positively associated with performance, particularly when firms are far from the productivity frontier.

Second, a balanced positioning may be more realistically obtainable in view of the predominant types of new ventures in transition economies and the entrepreneurial legacy from the early stages of the reform. As reported in the 2013 Global Entrepreneurship Monitor report, over 40% of the early-stage entrepreneurship in transition economies such as Poland, Slovakia and Bosnia and Herzegovina was driven by necessity, compared to less than 10% in developed market economies such as Sweden, Norway, Luxembourg, and Switzerland (Amorós and Bosma, 2014). As a case in point, the overwhelming majority of small businesses in Bulgaria are very small in size. Microenterprises that employ between one and nine employees represent 89.2% of the total number of small- and medium-sized enterprises (Ministry of Economy, Energy and Tourism, 2008). In the initial stages of the reform, characterized by extreme uncertainty, institutional hiatus, and resource scarcity, entrepreneurs succeeded by ‘self-help’ (McMillan and Woodruff, 2002), relying on personal connections to navigate the hostile institutional maze (Puffer and McCarthy, 2001) and gain access to information, resources, and markets. Given the entrepreneurial legacy of opportunistic, exploratory, or guerrilla strategizing (Peng, 2003; Wright et al., 2005) of these players, a hybrid strategy appears to be a natural choice as these firms work toward the productivity frontier.

Finally, a balance between low costs and differentiation allows new actors to maintain a requisite level of strategic flexibility (Wright et al., 2005) in the context of the evolving competitive environments of transition economies. Strategic flexibility depends on the inherent flexibility of resources available to the organization plus manager flexibility in applying these resources to alternative courses of action. As such, it helps firms take advantage of existing and new strategic opportunities and respond quickly to environmental threats (Sanchez, 1995; Wright et al., 2005: 8). This argument is consistent with recent work on the microfoundations of competitive performance (Eisenhardt et al., 2010), which calls for an effective balance between efficiency and flexibility, particularly in dynamic environments.

Formally,

Hypothesis 2. In a transition economy, there is a positive relationship between hybrid strategy and new venture performance. Specifically, we expect a curvilinear, inverted U-shaped relationship between strategic purity and performance, in which firms with hybrid strategies have stronger performance than firms with pure strategies of cost leadership or differentiation.

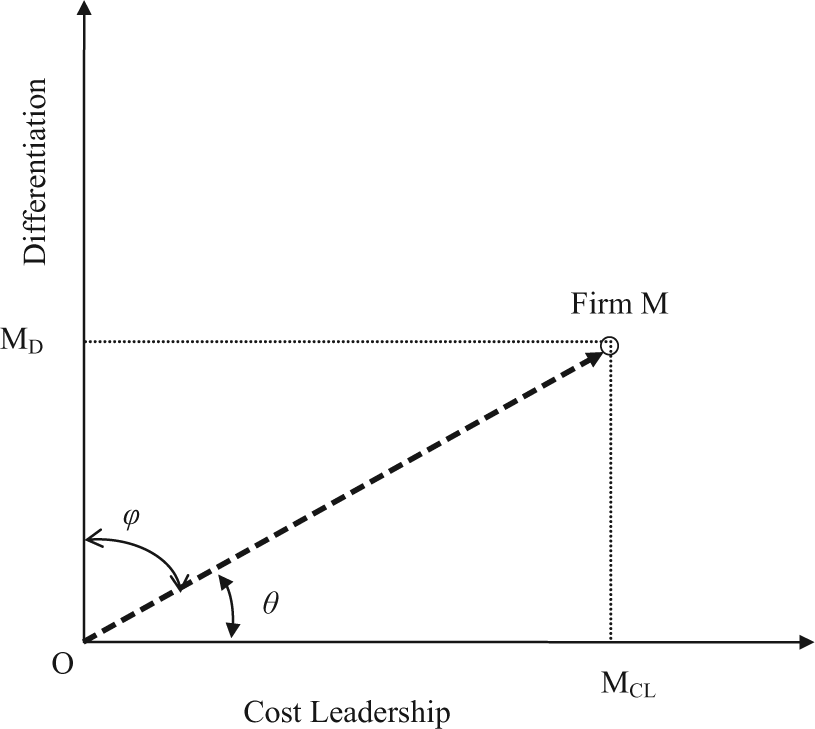

We illustrate our argument regarding hybrid strategies in Figure 2. In the two-dimensional strategy space from Figure 1, a firm’s strategy can be presented as a vector. The length of the vector represents the intended managerial and resource commitment, or strategic intensity, while strategic orientation is indicated by the direction of the vector. In Hypothesis 1, we argued that the further away from the origin (e.g. the closer to the productivity frontier) a firm is, the higher its performance. In Hypothesis 2, we argue that the best positioning is near the diagonal of the strategy space.

Strategy in a cost leadership/differentiation space.

Methods

Research context

We tested the theoretical model with data from a broad study of entrepreneurship in Bulgaria, a lower–middle income country in Eastern Europe. Socialist central planning virtually eliminated the private sector of the economy for more than 40 years (from the late 1940s to 1989). Large-scale institutional and economic reforms began after the fall of the Berlin Wall (1989), when the country set on a road of democratization and market liberalization.

The number of private businesses in Bulgaria has grown rapidly since they became legal in 1989. More than 99% of private businesses in the country are classified as small businesses with not more than 250 employees; indeed, about 88.5% of them are microbusinesses, with fewer than nine employees (Ministry of Economy, Energy and Tourism, 2008). In 2007, small and medium enterprises (SMEs) contributed 37.8% of the total gross value added and 38% of the total employment in the economy (Ministry of Economy, Energy and Tourism, 2008). Plagued by inconsistent and oftentimes arbitrarily enforced regulations, limited access to growth financing, and skeptical societal attitudes toward entrepreneurship, the majority of new ventures in Bulgaria have maintained a predominantly no-growth or low-growth orientation (Manolova and Yan, 2002; Williams and Vorley, 2014).

Although still lagging behind the transition economies in Central Europe (the Czech Republic, Hungary, Poland, the Slovak Republic, and Slovenia), by 2007 Bulgaria successfully fulfilled the market-liberalization and institutional-reform criteria for joining the European Union (EU). The country has demonstrated about average macroeconomic efficiency compared to other transition economies. 4 As it occupies somewhat of a mid-point on the scale of market and institutional development in transition economies, it offers an opportunity for broader generalizations of the study’s findings.

Data collection

Data were collected in September 2006, using a quota sampling approach. The basic goal of quota sampling is the selection of a sample that is a replica of the population to which one wants to generalize (Judd et al., 1991; Neuman, 2003), that is, new and small ventures in Bulgaria, with respect to a particular category, such as industry composition or owner’s gender. Graduate students in a research-methods course at a local university were trained to administer the survey to entrepreneurs who satisfied the following two conditions: the businesses had to be started in the preceding six years and have fewer than 250 employees, and the cutoff for small- and medium-sized enterprises in the EU. Respondents were founders and CEOs of the firms, and each of them described a single business. Businesses were based primarily in the capital Sofia (about 61%) and other urban areas with more than 100,000 inhabitants (11%), while 23% were located in cities with less than 100,000 inhabitants, and the remaining 5% came from rural areas.

The survey instrument was based on published research (Baum et al., 2001; Chandler and Hanks, 1994; Gartner et al., 2004) and included sections on the enterprise, owner’s background, firm strategy and resources, performance, and the entrepreneurial environment. The final instrument was forward and backward translated to ensure semantic consistency.

We obtained a usable sample of 333 surveys, for which we report descriptive statistics and the results from hypothesis testing. These were predominantly small businesses, averaging 19.8 employees, with about half having seven or fewer. The sample also exhibited a higher annual rate of growth (on the average 7.1%) than the average for the country (0% for 2010, according to Bulgarian SME Promotion Agency (2012: 21)). The sample comes from a variety of industries that broadly approximate the distribution of small businesses across industries in the country: about one-third (33.0%) in retail, 19.6% in manufacturing, 12.3% in wholesale, 8.2% in construction, 5.3% in transportation and storage, 7.6% in financial services, and the remaining 14% in other sectors. 5 One-third of the business owners in the sample had college degrees, and a little over half were women. 6

Measures

We measured performance, the dependent variable, by self-reported evaluations of firm cash flow, market share, and sales growth. We chose a perceptual index over objective data for two reasons. First, small firms are often reluctant to provide financial data (Fiorito and LaForge, 1996). Second, financial data on small privately held businesses were not publicly available for Bulgaria, which would have made a cross-validation with published data impossible. That is why we used a subjective measure used in prior research (Baum et al., 2001). The three items (firm cash flow, market share, and sales growth) loaded on a single factor whose scores we used for the analysis (Cronbach’s alpha = .82).

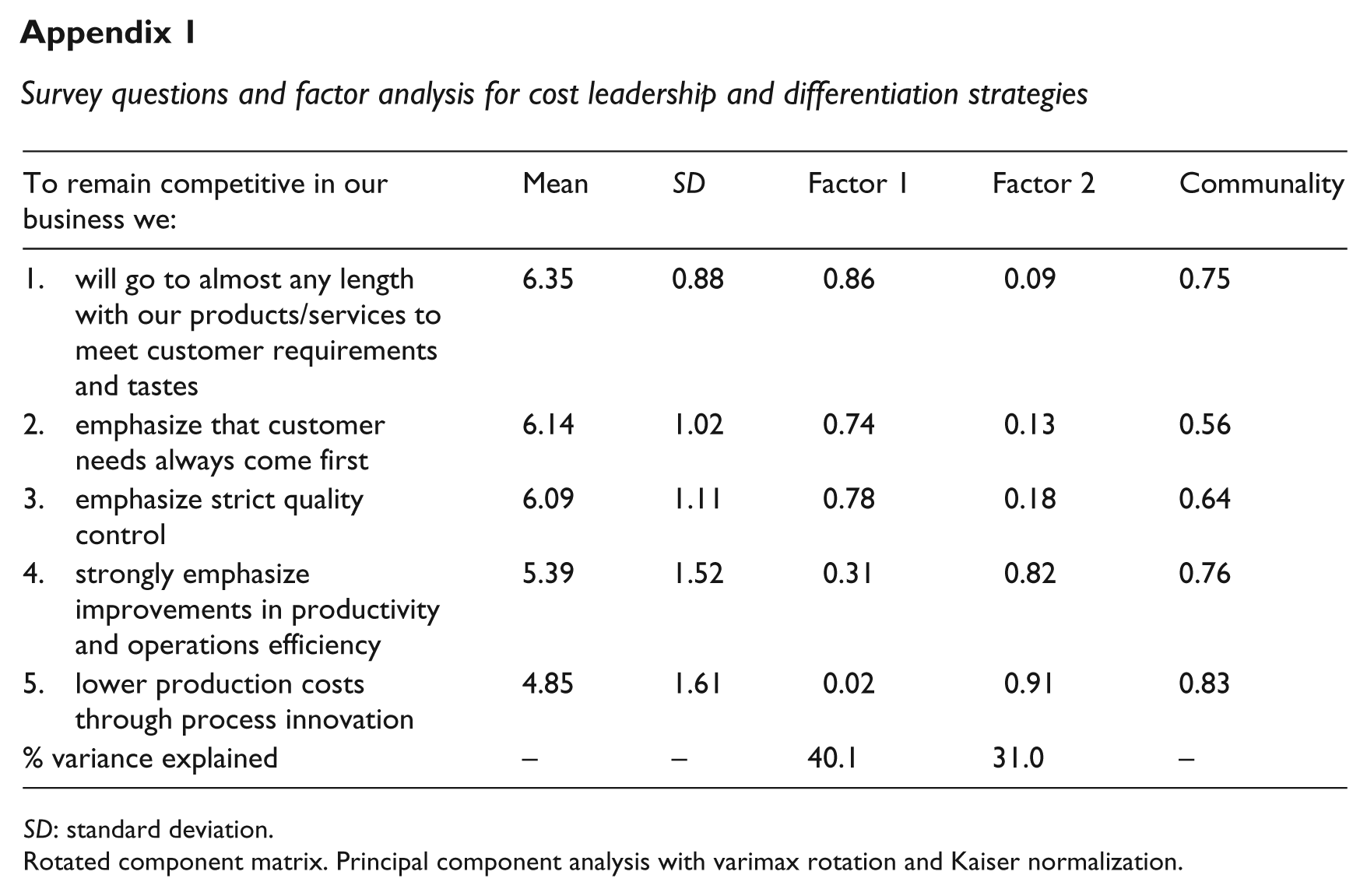

To measure the effect of strategic intensity and hybrid strategy, we followed Thornhill and White’s (2007) method of measuring the length and angle of a strategy vector. To measure the generic strategies of cost leadership and differentiation, we used an adapted Chandler and Hanks’ (1994) instrument. Cost leadership was measured by two questions about emphasizing improvement in productivity and operational efficiency and lowering production cost through process innovation (Cronbach’s alpha = .71). Differentiation was measured by three items: emphasizing strict quality control, meeting customer requirements and tastes, and emphasizing that customer needs come first (Cronbach’s alpha = .72). In a principal components analysis with varimax rotation, these items produced satisfactory loadings (between .74 and .91; highest crossloading .31) on two factors (please see Appendix 1). The scores of these factors (to which the absolute values of their respective minima were added, so that all values are nonnegative as represented in Figure 2) were used to define a firm’s strategy, positioning it in the two-dimensional space defined by cost leadership and differentiation. Strategic intensity was measured as the Euclidean distance between the origin and the point of a focal firm’s strategy. Furthermore, a pure cost leadership strategy would have an angle θ of 0, while a pure differentiation strategy would have an angle ϕ of 0 (Figure 2). Firms characterized by hybrid strategies would lie in the middle. Following Thornhill and White (2007), we computed the angle of deviation from pure cost leadership (in radians) as

where OMD is the differentiation component of the strategy of firm M, and OMCL is the cost leadership component of firm M’s strategy.

As the representation of the one axis as horizontal and the other as vertical is arbitrary, we repeated the analysis with the deviation from pure differentiation

We controlled for the effect of the entrepreneur’s personal background, characteristics of the firm, and industry. At the level of the individual entrepreneur, we used age (in years), gender (0 male, 1 female), and education (in years). At the firm level, we controlled for firm size (natural logarithm of the number of employees) and firm age (in years). At the industry level, including multiple control variables for different sectors was not practical with a sample size of a few hundred; thus, we followed previous studies in controlling for industry effects in a parsimonious way. In the first place, we included a dummy variable for manufacturing, as Acquaah and Yasai-Ardekani (2008) did, because the distinction between manufacturing and services obviously has a major effect on firm strategy. Second, we followed Sharfman and Fernando’s (2008) empirical approach in evaluating which industries are likely to impact firm strategies in our sample. Using the seven major industry groups listed previously, we conducted an analysis of variance (ANOVA) with performance as the dependent variable. The analysis showed a statistically significant effect; thus, we performed a post hoc analysis using Dunnett’s T3 test, a relatively sensitive (i.e. nonconservative) test for differences. Notably, even if the test does not assume equal variances across groups, in fact there was no statistical difference between these variances. The Dunnett’s T3 test showed only one marginally significant difference, between the wholesale and retail sectors (.31 vs −.20, respectively, s.e. = .17, p < .08). Thus, in the regression analysis, we included a second industry dummy variable to control for the effect of the wholesale sector. 7

We performed Harman’s (1967) single-factor test to check for common method bias. All self-reported measures were entered into a principal components factor analysis with varimax rotation, which showed that there was no single or general factor that would account for most of the covariance in the variables. Thus, common method variance was not evident.

Results

Descriptive statistics

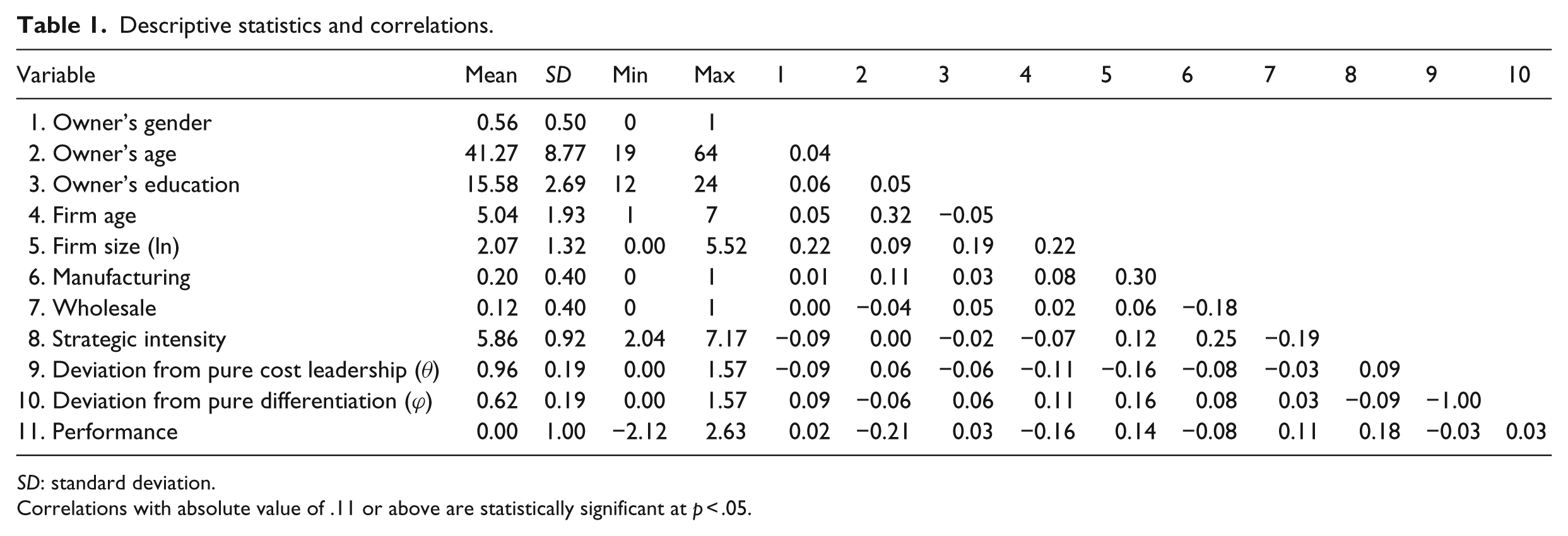

Descriptive statistics and correlations are presented in Table 1. Notably, the mean angle from pure cost leadership θ is .96 radians or 54.8°, and the standard deviation is .19 radians or 11.1°. This means that the majority of the business in the sample emphasize differentiation somewhat more than cost leadership (i.e. θ > 45°), but their strategies are best described as hybrid.

Descriptive statistics and correlations.

SD: standard deviation.

Correlations with absolute value of .11 or above are statistically significant at p < .05.

Hypotheses testing

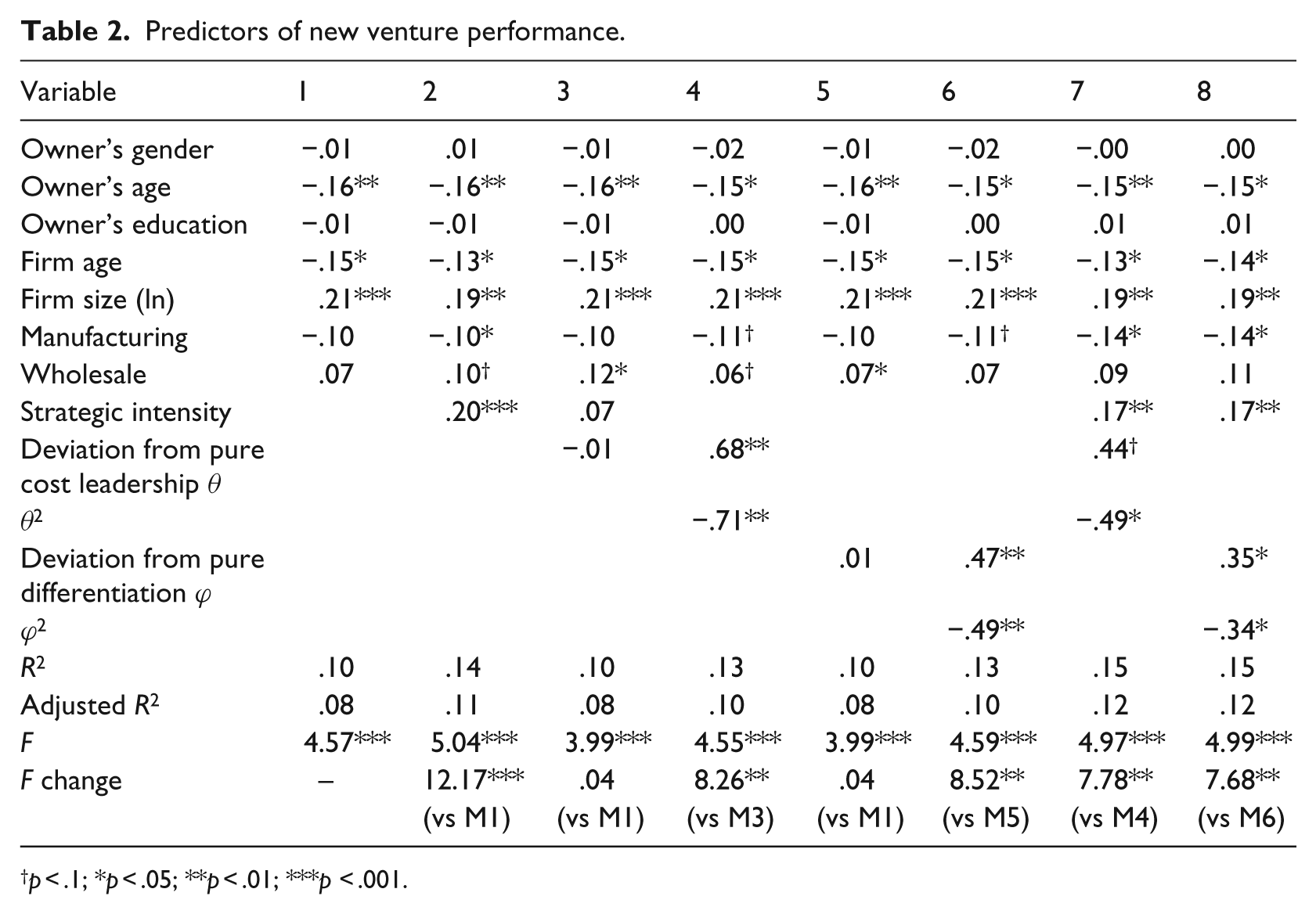

We tested the two hypotheses through ordinary least squares (OLS) regressions of new venture performance (Table 2). Model 1 presents the regression on the control variables only. Model 2 adds strategic intensity. Model 3 reports the results for the control variables plus the deviation angle from cost leadership θ, and Model 4 adds the squared term θ2. Similarly, Models 5 and 6 report the results for the deviation angles from differentiation ϕ and the squared term ϕ2. Finally, Models 7 and 8 report the regression results for strategic intensity together with the respective deviation angles and squared terms. 8

Predictors of new venture performance.

p < .1; *p < .05; **p < .01; ***p < .001.

Younger entrepreneurs, younger firms, and larger firms were more likely to report higher performance as were firms in wholesale or otherwise outside manufacturing, although these industry effects were not always statistically significant. Hypothesis 1, which focuses on strategic intensity, was supported (betas .20, p < .001 in Model 2 and twice .17, p < .01 in Models 7 and 8). Hypothesis 2, which focuses on the relative benefit of a hybrid strategy versus a ‘pure’ strategy, was supported too: the squared terms in Models 4, 6, 7, and 8 are all statistically significant and negative (−.71, p < .01; −.47, p < .01; −.49, p < .05; and −.34, p < .05, respectively). These coefficients denote an inverted U-shaped relationship between a pure strategy and performance, with firms with hybrid strategies near the maximum for performance. More precisely, the maximum for performance is reached for an angle θ from pure cost leadership equal to .89 radians or 51° (please see Appendix 2 for calculations on estimating the quadratic function).

Post hoc analysis

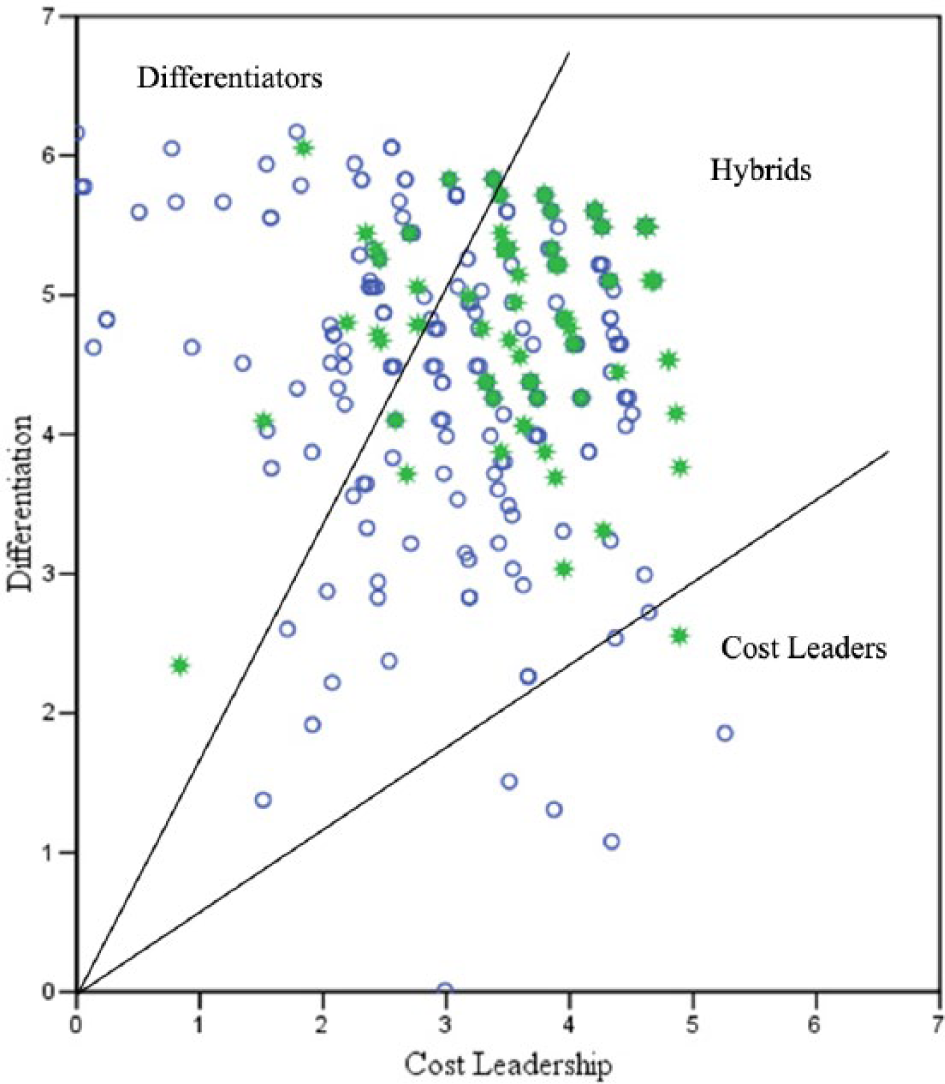

A scatterplot of strategies for firms in our sample along the cost leadership and differentiation dimensions is shown in Figure 3. Firms with performance in the upper quartile of the sample are shown with stars. Most high-performing firms tend to be farthest away from the origin, that is, have high strategic intensity, and a cluster of them have clearly hybrid strategies. That prompted additional post hoc analyses. First, as shown in Figure 3, we divided the sample in three segments on the basis of the deviation angle θ from pure cost leadership, each of which spans 30°: cost leaders, hybrids, and differentiators, counterclockwise from the lower right, respectively. Second, we ran an ANOVA of firm performance on these three strategic groups. The analysis indicated that the hybrid group had the highest mean on performance, though the F-test was only marginally statistically significant (p < .065). Third, as most high-performing firms appeared to be closer to the productivity frontier, we ran an ANOVA of firms’ strategic intensity on the three strategic groups. This analysis showed clear differences between the three groups: the F-ratio of 11.848 was statistically significant at p < .001, and post hoc tests showed statistically significant (at least at p < .05) differences between the means of all three groups: hybrids (highest strategic intensity), differentiators, and cost leaders (lowest).

Scatterplot of firms’ strategies.

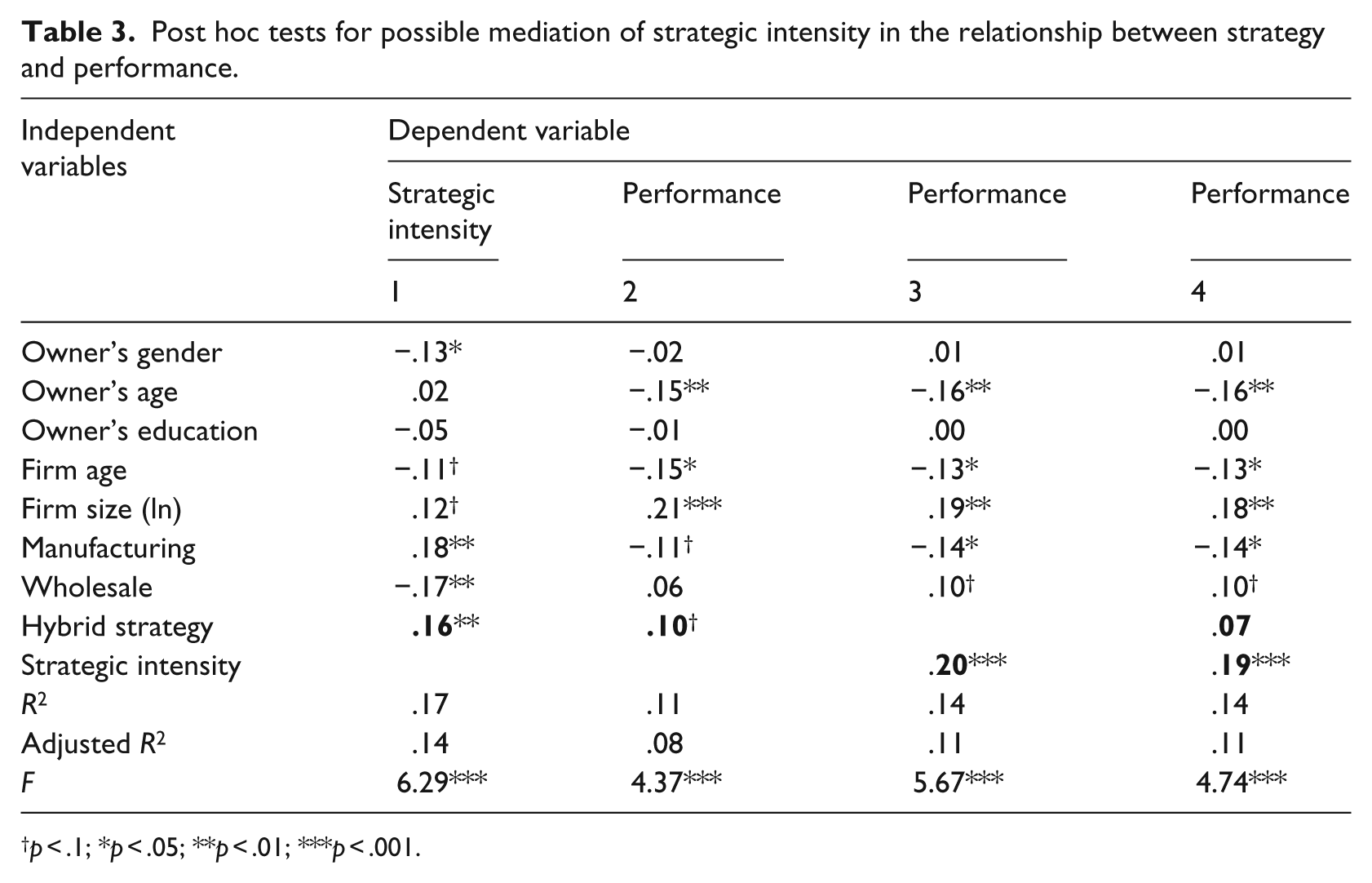

Taken together, these post hoc tests pointed to a possible mediating effect of intended strategic intensity between strategy and performance. This is not a relationship that we could deduce on the basis of extant theory. To investigate further, we repeated the regression analyses from Table 2 with a binary variable for hybrid strategy instead of the quadratic term for deviation from pure strategy: on the basis of our previous analysis, one would expect hybrids to have higher performance than the other pure strategy groups. In addition, we ran OLS regressions with intended strategic intensity both as a dependent variable and as predictor of performance. These analyses are shown in Table 3.

Post hoc tests for possible mediation of strategic intensity in the relationship between strategy and performance.

p < .1; *p < .05; **p < .01; ***p < .001.

These results are generally indicative of a likely mediating effect of strategic intensity in the relationship between strategy and performance. Firms with hybrid strategy were more likely to have greater strategic intensity (beta .16, p < .01 in Model 1). In turn, firms with greater strategic intensity tended to report better performance (beta .20, p < .001 in Model 3). The direct effect of hybrid strategy on performance was marginally significant (beta .10, p < .09 in Model 2) and dropped below statistical significance (beta .07, not significant (n.s.) in Model 4) when controlling for strategic intensity, which in itself was statistically significant (beta .19, p < .001, again in Model 4).

Discussion

In this article, we extend the boundaries of Porter’s theory of competitive advantage in the context of new ventures in transition economies, whose strategic priority is to improve their operational effectiveness and reach competitive parity with industry incumbents. We developed and tested a theoretical prediction regarding optimal competitive trajectory toward the productivity frontier. Our analysis suggests three main findings.

In the first instance, the strategic intensity with which firms in transitional economies pursue a chosen strategy is positively related to performance. This is consistent with a stream of research on transitional economies which suggests that the pursuit of market-based sources of competitive advantage becomes increasingly important with the advancement of reforms (Danis et al., 2010; Lyles et al., 2004; Peng, 2003). In the more stable institutional environment, characteristic of a later stage of reform, competition increases and firms increasingly, and purposefully, search for cost savings and/or sources of differentiation. At the same time, most firms in transitional economies still lag behind major world-class competitors (Sabirianova et al., 2005), opening up diverse possibilities for improvement. As Porter (1996) suggests, when companies have not reached the productivity frontier, they benefit from any effort to improve their operational effectiveness and move toward the frontier, regardless of direction. Greater strategic intensity, characterized by a better defined strategy in the form of greater managerial and resource commitments toward a strategic position, is likely to lead to better performance, regardless of whether the strategy is pure (cost leadership or differentiation) or a hybrid.

Second, our results demonstrate that the majority of small and new firms in our transitional economy context adopt hybrid strategies and even more importantly hybrid, rather than pure, strategies are associated with superior performance. This supports a long-held view in entrepreneurship research in general that new and small firms usually follow mixed or multifaceted strategies (Carter et al., 1994; McDougall et al., 1992). Outside the field of entrepreneurship, our results are consistent with studies reporting that emerging market firms following hybrid strategies outperform those with pure strategies (Kim and Choi, 1994; Parnell, 2013).

Finally, our post hoc analysis suggests fruitful new ground for research on strategic types by finding that strategic intensity acts as a likely mediator in the relationship between strategic type and performance. This indicates that a complex relationship may be in play in which hybrid firms are more likely to pursue their strategies intensely, and that intensity rather than positioning is most closely associated with performance. While some research in the context of transition economies (e.g. Acquaah and Yasai-Ardekani, 2008; Spanos et al., 2004) and newly industrialized countries (e.g. Kim and Choi, 1994) has found that firms pursuing more intense strategies outperform firms ‘stuck in the middle’, to our knowledge, this is the first time that strategic intensity has been evaluated as a potential mediator. Strategic intensity holds promise for explaining the inconsistent results in prior research that studies the effect of strategic type on performance. Our findings are consistent with Cronshaw et al.’s (1994) interpretation of Porter’s argument, according to which the ‘stuck in the middle’ position is different from the successful pursuit of a hybrid strategy: such firms do not achieve competitive advantage because they fail to execute, rather than because they do not pursue, a pure strategy.

Our results regarding hybrid versus pure strategies run exactly contrary to those in Thornhill and White’s (2007) study. This is intriguing, especially as we replicated their method of measuring hybrid and pure strategies. These contrasting results can be attributed, above anything else, to the difference in context. Apparently, firms in Canada, a developed Western economy, can gain superior performance through pure strategies, in a classic application of Porter’s (1985) argument about strategic purity. In contrast, firms in countries that are only catching up in economic development and are peripheral in the world economy appear to embrace more opportunistic, day-to-day strategies (Spanos et al., 2004). Furthermore, small, often family-owned firms are likely to make incremental changes in their strategies, rather than adopt bold and expensive changes in their strategic postures. In an emerging transition economy such as Bulgaria, with little institutional tradition, a hybrid strategy may provide the requisite flexibility to ensure survival.

While initially our results that hybrid rather than pure strategies are associated with superior performance appear to be at odds with the mainstream Porterian view, they are however, to the contrary, actually consistent with it. As discussed, the call for ‘pure’ strategy argument is grounded in an assumption that competitors are operating at the productivity frontier. Most new firms lag behind incumbents in operational effectiveness, and the suboptimal efficiency of new ventures in transition economies is particularly acute (Deliktas and Balcilar, 2005; Narayanan and Fahey, 2005; Sabirianova et al., 2005). In such conditions, it is not only possible, but appropriate to pursue both cost leadership and differentiation as firms try to catch up (Porter, 1996; Raynor, 2007). In other words, as firms in transition economies move toward the productivity frontier, they adopt hybrid strategies, including elements of more than one generic strategy (Kim et al., 2004; Kim and McIntosh, 1999). Accordingly, the conflicting findings in the literature on the role of strategic purity may be a function of the strategic intensity of firms. If businesses operate below the productivity frontier, then the best strategy would be the one that is farthest from the ‘no strategy’ position (cf. Spanos et al., 2004).

Our research invites at least three questions for further research. First, transition economies have certain characteristics that are common for most emerging economies, such as underdeveloped institutions, incomplete and inefficient factor markets (Hoskisson et al., 2000), and a large number of firms operating below the productivity frontier (Minniti and Lévesque, 2010). At the same time, the transitional economy context has certain specific features, for example the strong legacy of central planning and the decades of suppression of private initiative, which have resulted in the relative shortage of managers with market economy experience (Lyles et al., 2004) and the reliance on personal connections in the initial stages of market reforms (Peng, 2003; Wright et al., 2005). Accordingly, the setting for this study invites the question of how generalizable the findings are in the broader context of emerging markets. We contend that to the extent firms in emerging markets operate below the productivity frontier, strategic intensity would be positively associated with performance. At the same time, emerging markets are very diverse with respect to market size, resource endowments, level of economic and market development, and institutional sophistication. All of these factors may influence the nature of competition and, hence, optimal competitive positioning and its effect on performance. Future research should extend and generalize the findings from our study in other emerging economy contexts. Similarly, the contingent effects of industry structure need further exploration. For example, a study of the strategic types and performance of small firms in Korea (Kim and Choi, 1994) identified five different strategic types of small businesses (innovative, efficient, versatile, marginal, and reactive), each dominating a different industrial setting. Across industries, the firms reflecting the dominant strategic type were also the highest performers. We call on future research to extend and generalize our findings across different industry contexts.

The second question for future research is how the strategies of new and small firms compare with those of established firms in the same transitional economies context. New ventures are characterized by greater strategic flexibility but lack slack resources; this leads to increased volatility and threatens survival (Short et al., 2009). A plausible surmise is that established firms, especially those that benefit from links with and investment from established competitors, would be more likely to pursue pure rather than hybrid strategies as the benefits from flexibility are lower. A study that compares these two groups of firms is necessary to clarify this.

And third, how do the hybrid strategies of small and new firms evolve? Do they evolve in an incremental, muddling through manner, as day-to-day responses to evolving strategic challenges, or are they a result of a firm starting with one strategy and then gradually adopting elements of another (e.g. starting with cost leadership and then differentiating because economies of scale cannot be attained given the small size of the firm)? Recent case-based work on emerging economy ‘copycats’ (Luo et al., 2011) documents the evolution of emerging economy enterprises from low-cost imitators to novel innovators.

Limitations

Our article is not without limitations that need to be considered when interpreting the results from hypothesis testing and their implications. First, we studied new and small ventures in a single country in transition, a small, efficiency-driven, lower–middle income economy. It is likely that competitive positioning may affect new venture performance differently in a different institutional and cultural setting. As discussed in the previous section, further research is warranted in the context of other transition economies and emerging markets, in general. A second limitation is the cross-sectional design which does not prove causality. Third, we could only study those new businesses that survived the perilous years of their initial histories, which can create survivor bias. Survivor bias is particularly problematic for new and small ventures because of the inherent vulnerability caused by the liabilities of newness and smallness. Ideally, a research design should be longitudinal, allowing researchers to track survival and explore lagged effects on performance. In addition, we used perceptual measures of performance. While performance measurement presents a challenge for all entrepreneurship research (Murphy et al., 1996), and prior studies have established a good correlation between perceptual and actual competitive performance (Brush and Vanderwerf, 1992), multiple measures of performance, including actual accounting and financial results, would be preferable. Finally, while quota sampling rendered a preset number of cases in each of several predetermined categories (new venture size and age, and industry distribution) that reflect the diversity of the population (Neuman, 2003: 211), it can introduce some selection bias (Judd et al., 1991: 135). A future study based on pure random or stratified random sampling would permit robust statistical corroboration and generalization of the study results.

Conclusion

Our study has implications for future research, managerial practice, and managerial training. We demonstrate that the development of a more intense strategy is beneficial for small and new firms in the context of transition economies. Consistent with a number of recent studies that emphasize the need for strategic flexibility, we find strong support for the role of hybrid strategies for competitive performance. Further research can examine in greater depth the boundaries of the Porterian theory of competitive advantage, which may be less appropriate for small and new ventures operating within institutional uncertainty.

The results of this study have important implications for managerial training, both in formal university courses and seminars for practicing managers. Often instructors of strategic management call for strategic purity as a generic recipe based on a narrow reading of mainstream strategy theory. We call for more precision in drawing conclusions about strategic management and paying more attention to context. When competition is not developed, market institutions are not fully functioning, and corporate traditions are not established, as is the case in transitional economies and, likely, emerging economies in general, most firms operate within, rather than at the productivity frontier. In this context, in the race to the productivity frontier, strategic intensity may be more important than competitive positioning in predicting performance.

New firms led by owner-managers are often governed using more personal control (Bhalla et al., 2006), focusing on efficiency rather than the development of a consistent strategic orientation (Woods and Joyce, 2003). Our advice to entrepreneurs and managers in transition economies, therefore, would be to develop strategies to reach the productivity frontier in the first instance. For that, the pursuit of a hybrid strategy may be fully adequate and perhaps preferable to a pure strategy. Entrepreneurs and managers in transition economies would be well advised to seek ways to meet the seemingly divergent pressures for cost reduction and differentiation into an integrated strategy that carefully calibrates and aligns with firm resources and activities.

Footnotes

Appendix 2

Appendix 1

Survey questions and factor analysis for cost leadership and differentiation strategies

| To remain competitive in our business we: | Mean | SD | Factor 1 | Factor 2 | Communality |

|---|---|---|---|---|---|

| 1. will go to almost any length with our products/services to meet customer requirements and tastes | 6.35 | 0.88 | 0.86 | 0.09 | 0.75 |

| 2. emphasize that customer needs always come first | 6.14 | 1.02 | 0.74 | 0.13 | 0.56 |

| 3. emphasize strict quality control | 6.09 | 1.11 | 0.78 | 0.18 | 0.64 |

| 4. strongly emphasize improvements in productivity and operations efficiency | 5.39 | 1.52 | 0.31 | 0.82 | 0.76 |

| 5. lower production costs through process innovation | 4.85 | 1.61 | 0.02 | 0.91 | 0.83 |

| % variance explained | – | – | 40.1 | 31.0 | – |

SD: standard deviation.

Rotated component matrix. Principal component analysis with varimax rotation and Kaiser normalization.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.