Abstract

The growing activity of foreign banks in most European countries may increase financing constraints by intensifying the problem of borrower discouragement. We provide new evidence of this association by analysing a sample of small and medium-sized enterprises (SMEs) operating in 25 developed and developing European countries. We find that financing constraints increase with foreign banks for those SMEs operating in countries where the share of banking assets owned by foreign banks is above 34%. Our results also show that borrower discouragement may decrease, or increase less, with the presence of foreign banks for SMEs operating in countries with high income, with cheap debt enforcement mechanisms, or having a private bureau that provides credit information about firms and individuals. These results suggest that unification towards better institutions needs to occur in Europe before the banking union progresses to a more open banking system.

Keywords

Introduction

The process of the liberalisation of European financial markets has been influential in changing the structure of the banking system (Padoa-Schioppa, 2004). Data obtained from the World Bank show that the presence of foreign banks in most European Union (EU) 28 member states has increased from 1995 to 2014, with Eastern European countries such as Estonia (from 8% to 75%), Croatia (from 6% to 52%) and Lithuania (from 0% to 75%) experiencing the highest increase. In addition, this process is likely to continue in the future as the European Central Bank (ECB) recognises that completing the banking union is not a long-term project because leaving the banking union unfinished would be the opposite of risk reduction . . . We need a deeply integrated financial system with well-capitalised intermediaries that are active across borders and benefit from the risk diversification options that the economic diversity of the euro area offers. (Praet, 2016)

However, a higher presence of foreign banks may increase financial constraints upon small and medium-sized enterprises (SMEs). The aim of this article is to shed additional light on this problem by examining the association between the presence of foreign banks in a country and borrower discouragement for SMEs, and how this relationship might be affected by the strength of a country’s institutions.

The presence of foreign banks may bring benefits to a country’s banking system by introducing new skills, facilitating the access of firms to international capital markets and increasing competition in the market for large companies. However, from the theoretical point of view, we may expect a less positive effect of foreign banks on smaller firms and varying effects across firms operating in different institutional environments. These variations are likely to arise because informational asymmetries influence the borrower–lender relationship and, therefore, the demand for and access to debt financing. This is especially true for the relationship between foreign banks and SMEs. On the one hand, foreign banks usually have a disadvantage in offering relationship lending to opaque and risky firms because they have less access to soft information or they are either less willing or less able to process it along their hierarchical organisational structures. On the other hand, SMEs are characterised by high informational asymmetries and lack of assets to pledge as guarantees to reduce risk (Hanedar et al., 2014). Consequently, we analyse whether the liberalisation of the banking system affects the access of SMEs to debt financing through changes in the presence of foreign banks and whether the strength of a country’s institutions produces different results across countries. We explore such issues using a survey data set of 2582 firms operating in 25 developed and developing European countries.

Our article offers several contributions. First, we analyse if the share of foreign banks in a country’s banking sector influences financing constraints upon firms. We do so by analysing the intensity of discouraged borrowers, who are quality firms that choose not to apply for the financing they need (Kon and Storey, 2003). This form of financial restriction is more frequent than credit denial (Levenson and Willard, 2000), with an economic impact twice the size of rejected borrowers. 1 Second, we contribute by allowing for a greater flexibility in the estimation of our model in order to identify a heterogeneous relationship between foreign banks and borrower discouragement. Existing literature suggests that positive and negative effects of foreign banks may coexist, but they dominate at different ranges of foreign banks penetration in a country (Claessens and van Horen, 2014; Cull and Pería, 2008; Gormley, 2011). Using a zero-truncated Poisson count model, our results show that a higher presence of foreign banks in a country reduces the intensity of borrower discouragement when their share of assets in the banking sector is below 34%, the point at which foreign banks have a detrimental effect on SME access to debt. Moreover, acknowledging that we do not have the ideal risk measures, we are able to show that more intensely discouraged borrowers are not riskier firms.

Finally, we also allow for the possibility that the effect of foreign banks on borrower discouragement could be moderated by the strength of a country’s institutions. Informational asymmetries are lower in more developed economies (Claessens and Laeven, 2004), which is likely to influence the association between foreign banks and borrower discouragement. Our results show that a higher presence of foreign banks produces a lower increase in the intensity of borrower discouragement for firms operating in countries with high income, with low cost of enforcing debt contracts, or having an information infrastructure. These differences in the level of institutional development also explain why borrower discouragement in our sample appears to be higher for SMEs operating in the 10 newer Member States (EU 10) compared to the 15 old Member States (EU 15) of the EU. These results could help to understand why previous studies find that the overall size of the banking sector of developing countries decreases with the presence of foreign banks, even if these credit institutions offer loans to SMEs (Claessens and van Horen, 2014; Detragiache et al., 2008).

The remainder of the article is organised as follows. First, we discuss previous literature and develop the hypotheses. We then present the variables, data and methodology, followed by the results. Finally, we present the summary and conclusions.

Theory and hypothesis development

The liberalisation of the European financial landscape has facilitated the development of cross-border activity (Padoa-Schioppa, 2004). However, changing the structure of a country’s banking sector influences the flow and use of soft information (Berger et al., 2004), which, in turn, might exacerbate the problem of borrower discouragement for SMEs. Soft information has a key role in lending to SMEs because the scale and scope of hard information are usually limited (Grunert and Norden, 2012).

According to Kon and Storey (2003), imperfect information is the primary source of discouraged borrowers, who are good quality firms that choose not to apply for a loan due to bank screening errors, the existence of application costs and the availability of alternative funding from moneylenders. Therefore, the existence of discouraged borrowers reflects a market failure because quality firms choose not to apply for bank funding even though they are in need of financing. We expect a non-linear relationship between the presence of foreign banks in a country and borrower discouragement. We argue that the level of foreign bank penetration per se is likely to change the marginal effect that foreign banks have on the balance among screening errors, the scale of application costs and the extent to which interest rate differs from that charged by moneylenders.

On the one hand, foreign banks with a low presence in a country may incur high screening errors because the availability of soft information about SMEs is scarce. Yet, at the same time, poorly informed foreign banks impose low costs to applicants because any requirement for additional information can be easily met (Kon and Storey, 2003). In addition, the relative cost of loan applications could decrease with the initial presence of foreign banks offering better skills and services, diversification of risks and access to international capital markets (Berger et al., 2000). As for the interest rate charged to SMEs, the gap between banks and moneylenders is likely to increase with the initial presence of foreign banks if domestic banks increase their focus on SMEs. According to the cherry-picking effect (Degryse et al., 2012), foreign banks grant most credit to more transparent and less risky firms so less likely to develop relationship lending to SMEs (Berger and Udell, 2006). By cherry-picking, foreign banks increase the competition in the market for large companies and force domestic banks (see segregation effect in Dell’Ariccia and Marquez, 2004) to increase the share of SMEs in their portfolios. Therefore, we expect that borrower discouragement decreases with the initial presence of foreign banks in a country if lower costs of loan applications and higher cost of alternative funding compensate for higher screening errors.

On the other hand, foreign banks with a high presence in a country may achieve more autonomy and deeper knowledge about SMEs, which eventually may result in lower screening errors. However, soft information is difficult to transmit in the large and hierarchical structures of foreign banks with their headquarters at a considerable distance from small and local businesses and used to operating in a different economic, institutional and cultural environment (Berger et al., 2001; Jiménez et al., 2009). This is supported by Beck et al., (2011) showing that foreign banks do not rate soft information as an important factor in evaluating loans. Therefore, there is a high probability that if foreign banks continue cherry-picking large and transparent companies achieving an increasing number of viable SMEs will use alternative lenders; this will in turn, reduce; this extent to which the bank interest rate differs from that charged by the alternative lenders. Finally, the cost that foreign banks impose upon applicants is expected to rise because firms have more difficulties in fulfilling the information requirements of better informed banks (Kon and Storey, 2003). Accordingly, we expect that, at some point, borrower discouragement increases with the presence of foreign banks if higher application costs and lower cost of alternative funding overcome lower screening errors.

Based on the above arguments, our first hypothesis is as follows:

Hypothesis 1. The association between the presence of foreign banks and the intensity of borrower discouragement for SMEs follows a U-shape.

There appear to be few previous studies focused on the association between borrower discouragement and foreign banks. Related works suggest that there could be a non-monotonic association between foreign banks and borrower discouragement due to the existence of differences in the level of development of the institutional environment. Theoretical models by Boustanifar (2014) and Gormley (2014) show that the strength of a country’s institutions is important in determining the effect that foreign lenders may have in their economy and financial sector. There are also studies that find a reduction in the amount of bank credit to the private sector (as a percentage of gross domestic product (GDP)) as a consequence of a higher presence of foreign banks in low-income countries, whereas this effect disappears for developed countries (Detragiache et al., 2008; Gormley, 2014). The underlying argument is that rich economies and strong institutions may ameliorate informational asymmetries and reduce screening costs (Claessens and Laeven, 2004), making SMEs lending more feasible or desirable for foreign banks. This would mean that borrower discouragement is determined by a combination of foreign bank presence and institutional development. Following this argument, our second hypothesis is as follows:

Hypothesis 2. The existence of more developed institutions ameliorates the intensity of discouragement that SMEs could experience due to the increased presence of foreign banks.

Data and method

Dependent variable

We consider discouraged borrowers to be those firms which have not applied for a loan but would have been encouraged to resort to a loan if one or several of the following factors had been more advantageous: (1) interest rates, (2) procedures for granting loans, (3) guarantee requirements, (4) delays in granting loans and (5) other reasons. Using these answers from the survey question, we build the variable discouraged counting (adding) each one of the reasons that would have encouraged firms to apply for a loan. Therefore, the variable discouraged proxies for the intensity of borrower discouragement ranging from 1 to 5, where higher scores indicate higher discouragement intensity. 2

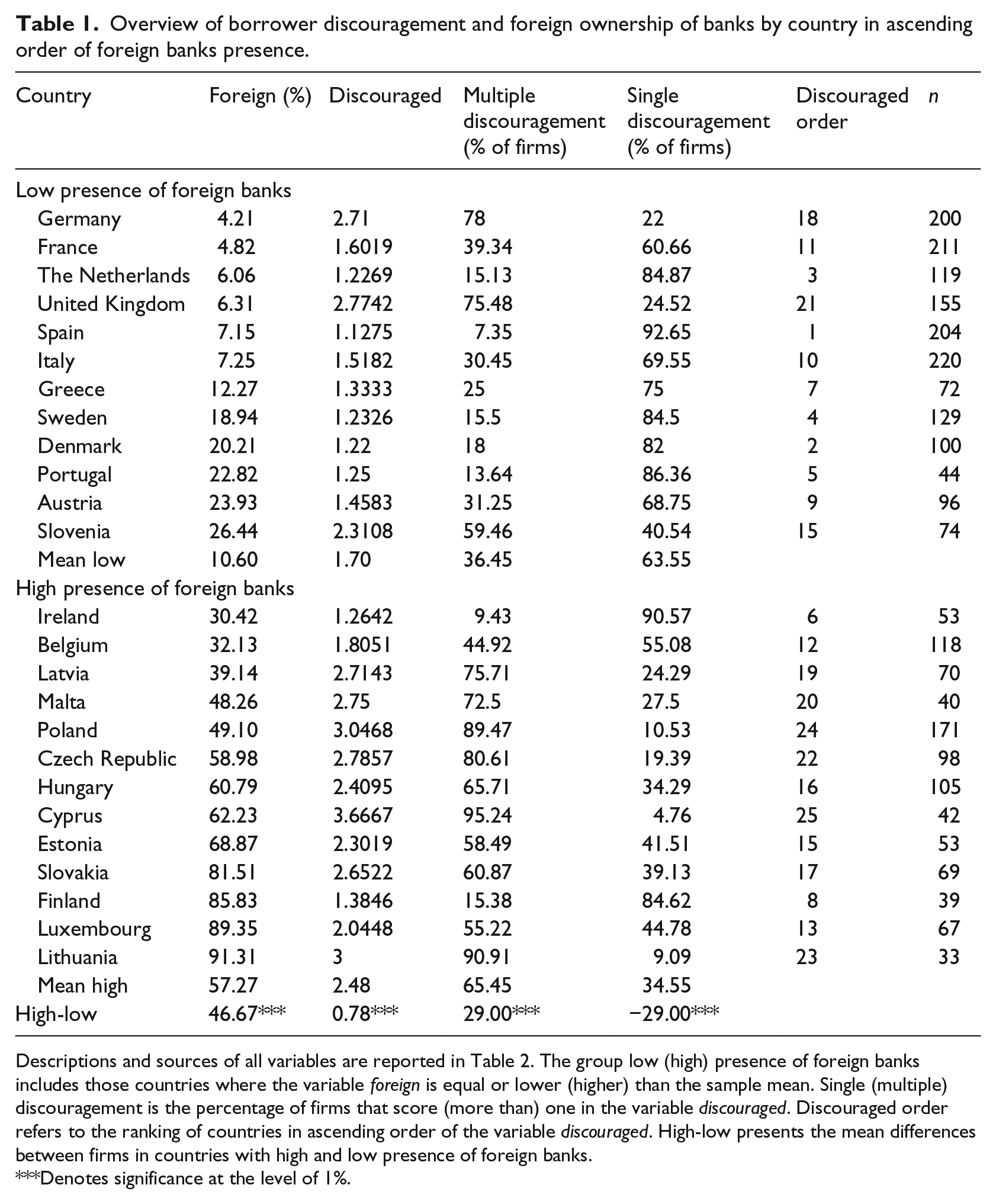

The so-called ideal comparison, undertaken in previous research, would be between applicants and non-applicants, taking account of a range of risk factors, and then analysing how the presence of foreign banks influences that relationship. However, going beyond this traditional approach, we follow Mol-Gómez-Vázquez et al. (2018b) and only focus on those borrowers who are discouraged, analysing whether the presence of foreign banks intensifies or ameliorates the magnitude of their discouragement. 3 The argument for this approach is that the more reasons discouraged borrowers have for their behaviour, the more complicated the solution to their discouragement will be. This is especially important in light of the statistics shown in Table 1, where we observe the existence of a large variation in the intensity of borrower discouragement. For example, in 13 out of 25 countries in our sample, more than 50% of firms experience what we call multiple discouragement, which are firms having two or more reasons for being discouraged from applying for a loan. Overall, our sample contains 1219 SMEs (47.21% of the observations) suffering multiple discouragement.

Overview of borrower discouragement and foreign ownership of banks by country in ascending order of foreign banks presence.

Descriptions and sources of all variables are reported in Table 2. The group low (high) presence of foreign banks includes those countries where the variable foreign is equal or lower (higher) than the sample mean. Single (multiple) discouragement is the percentage of firms that score (more than) one in the variable discouraged. Discouraged order refers to the ranking of countries in ascending order of the variable discouraged. High-low presents the mean differences between firms in countries with high and low presence of foreign banks.

Denotes significance at the level of 1%.

Independent variables

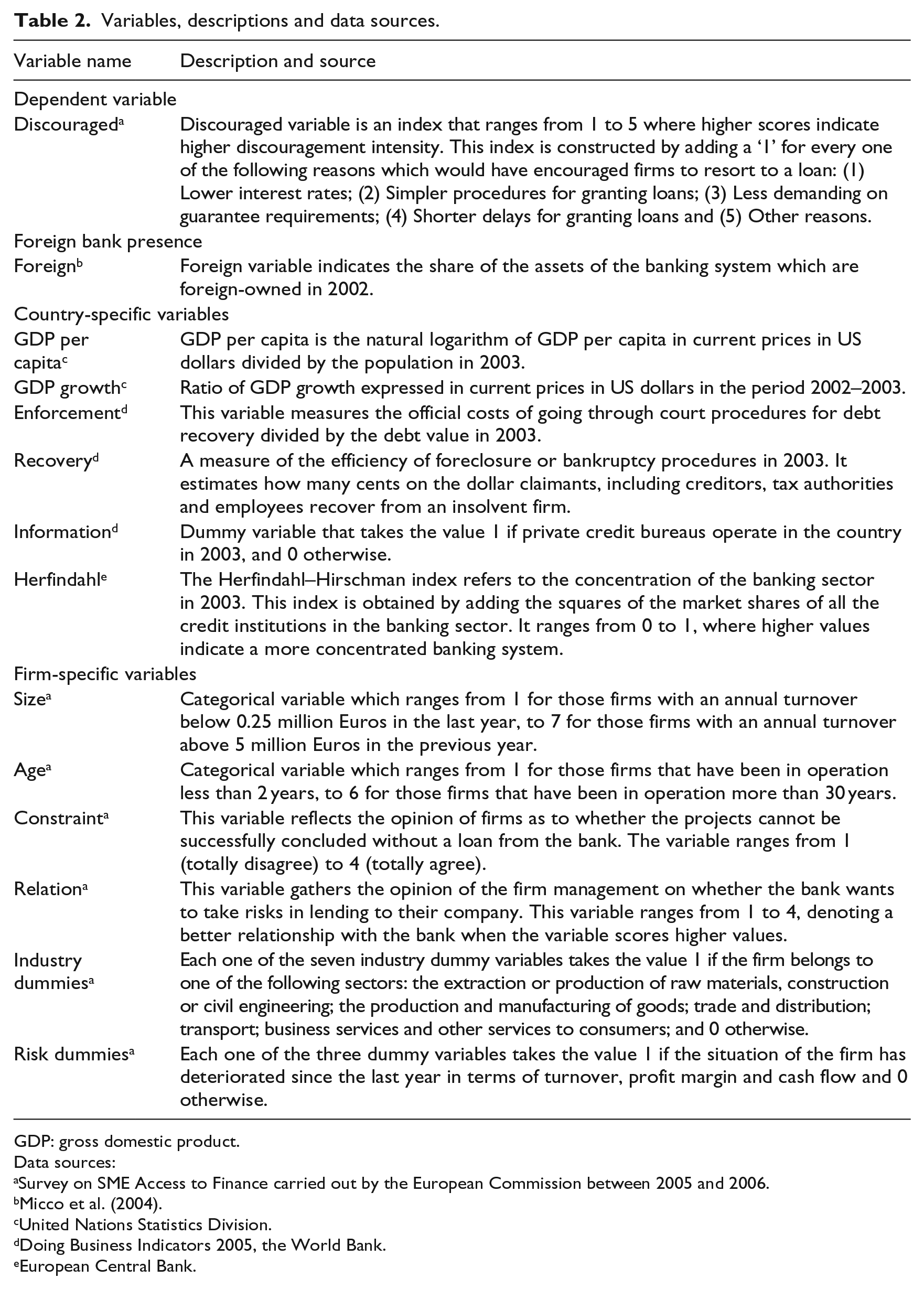

This section describes the explanatory variables used in our empirical study. Table 2 provides detailed definitions of all the variables.

Variables, descriptions and data sources.

GDP: gross domestic product.

Data sources:

Survey on SME Access to Finance carried out by the European Commission between 2005 and 2006.

United Nations Statistics Division.

Doing Business Indicators 2005, the World Bank.

European Central Bank.

Foreign bank presence

We measure the presence of foreign banks in a country banking system using the variable foreign. This variable equals the share of the banking system assets that are owned by foreign banks. Higher values for the variable foreign indicate the existence of a wider and stronger participation of foreign banks in the banking system of a country. This measure has been widely used in the financial literature (Claessens and Laeven, 2004; Claessens and van Horen, 2014; Clarke et al., 2006).

Table 1 shows large variations across countries in the participation of foreign banks in the banking system, from Germany with 4.21% of banking assets held by foreign banks, to Lithuania with 91.31%. Dividing the countries into two groups according to the mean value of the variable foreign, we can also observe that 11 out of the 12 countries with a low presence of foreign banks belong to the EU 15, while 9 out of the 13 countries with a high presence of foreign banks belong to the EU 10. Finally, Table 1 contains mean comparison tests between firms in both groups, which are statistically significant at the 1% level. Results indicate, for example, that firms in countries with a high presence of foreign banks are more intensely discouraged (2.48) and more commonly affected by multiple discouragement (65.45%) than firms in countries with low presence of foreign banks (1.70% and 36.45%, respectively).

Country-specific variables

We include a set of country factors to control for additional heterogeneity across European countries. By influencing the willingness to establish close banking relationships, the market power of banks may affect the problem of borrower discouragement (Mol-Gómez-Vázquez et al., 2018b). Following previous financial literature (Claessens and Laeven, 2004; Cole and Sokolyk, 2016), we control for bank market power using a measure of concentration, the Herfindahl–Hirschman index. As the Herfindahl variable increases, the market power of banks increases. Previous evidence also shows that borrower discouragement decreases with the existence of better institutions (Chakravarty and Xiang, 2013; Mac an Bhaird et al., 2016). We include the variables GDP per capita and GDP growth to control for the level of economic development and the growth rate of the economy, the variables enforcement and recovery to measure the efficiency of the legal environment when enforcing debt contracts and dealing with credit recovery after bankruptcy and the variable information to control for the existence of an information infrastructure in a country.

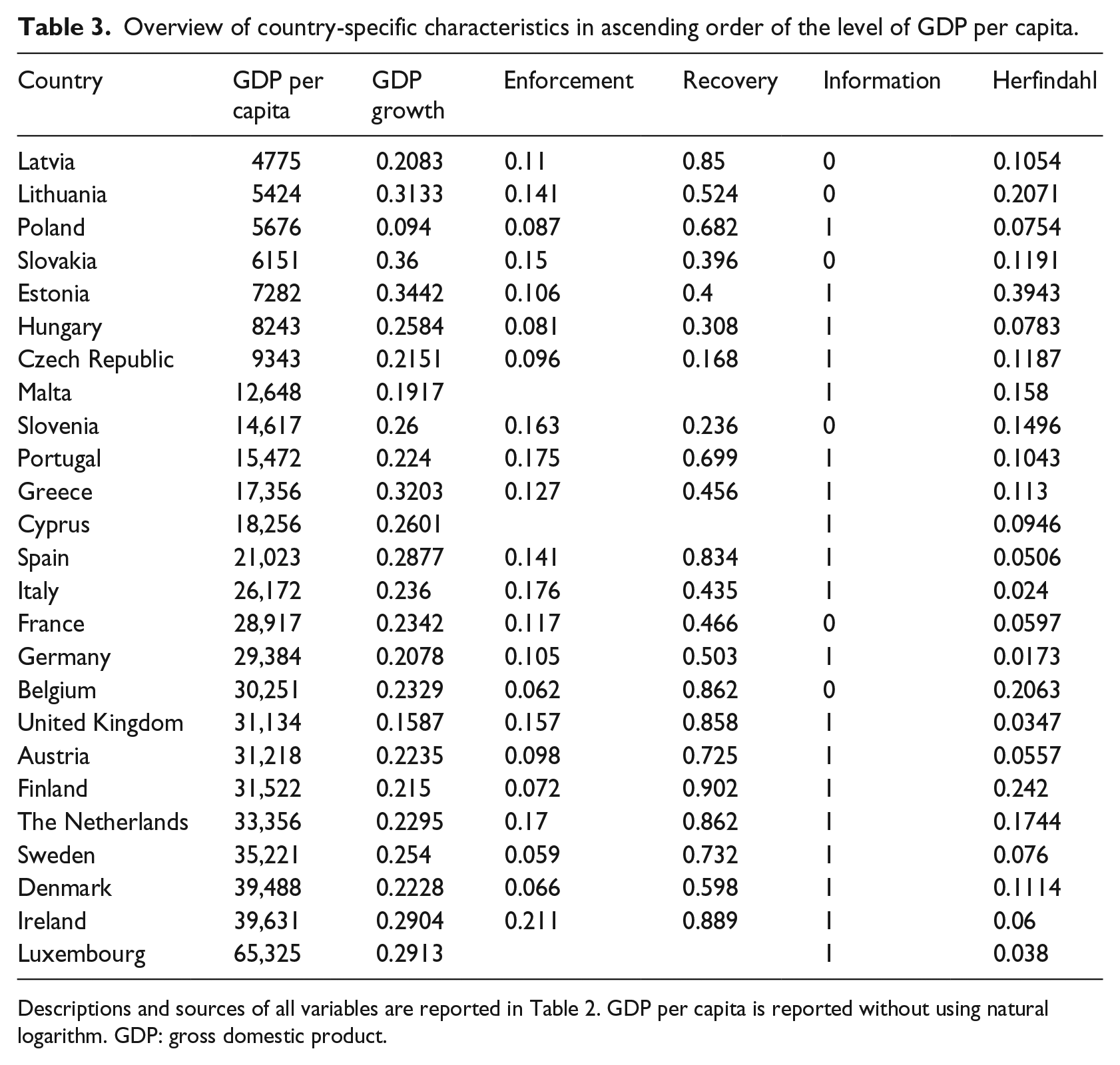

Table 3 shows the existence of large differences across countries in the level of concentration of the banking sector and the strength of institutions, and how they are related with the level of economic development. It reveals that rich and poor countries may differ in aspects such as the recovery rate, which has an average value of 0.7847 for the high-income countries and 0.4754 for the low-income countries, or the level of concentration of the banking system, which achieves an average value of 0.1082 for the high-income countries and 0.1569 for the low-income countries. 4 However, it also happens that for other characteristics of the institutional environment such as the cost of enforcing debt contracts, the mean values for high- (0.1127) and low-income (0.1101) countries are quite similar.

Overview of country-specific characteristics in ascending order of the level of GDP per capita.

Descriptions and sources of all variables are reported in Table 2. GDP per capita is reported without using natural logarithm. GDP: gross domestic product.

Firm-specific variables

The firm-specific variables size, age, constraint and relation have been included in order to control for firm heterogeneity in our sample. 5 Due to the existence of longer track records, wider public presence, and larger availability of assets to pledge as collateral, larger and older firms are expected to suffer less from borrower discouragement (Chakravarty and Xiang, 2013; Mac an Bhaird et al., 2016; Xiang et al., 2015). We also take into account that borrower discouragement may decrease if firm managers have a better perception of their credit situation (Mac an Bhaird et al., 2016), that is, perceiving less financing constraints or the existence of a better relationship with their banks. Finally, we control for differences across industries in the amount of fixed assets, which is likely to influence discouraged borrowers (Freel et al., 2012), creating seven industry dummies. 6

Methodology and data

Due to the discrete and non-negative count nature of the dependent variable discouraged, we estimate a zero-truncated Poisson count model regression to analyse how the intensity of borrower discouragement is influenced by the presence of foreign banks. 7 The model presents the following form

where i represents the ith firm in the sample; discouragedi is the dependent variable for the firm i; foreigni is our main variable measuring the presence of foreign banks in a country’s banking system; CSCi is the vector of country-specific control variables; FSCi represents the set of firm-specific control variables and εi is the residual. 8

Our sample is based on the Flash Eurobarometer Survey on SME Access to Finance carried out by the European Commission between 2005 and 2006. From this survey, we obtain the data regarding borrower discouragement and the remaining firm-specific variables for 4583 SMEs in the EU 25. Unfortunately, the period used in this article is limited by data availability. As such, we cannot take into consideration a longer period or attempt to implement the analysis with more current data. However, our empirical contribution, previous to the financial crisis, will allow future contributions to compare the impact of foreign banks on discouraged SMEs across different economic and financial scenarios. Moreover, this survey data set has been used in articles recently published in reference journals (Canton et al., 2013; Mol-Gómez-Vázquez et al., 2018a, 2018b).

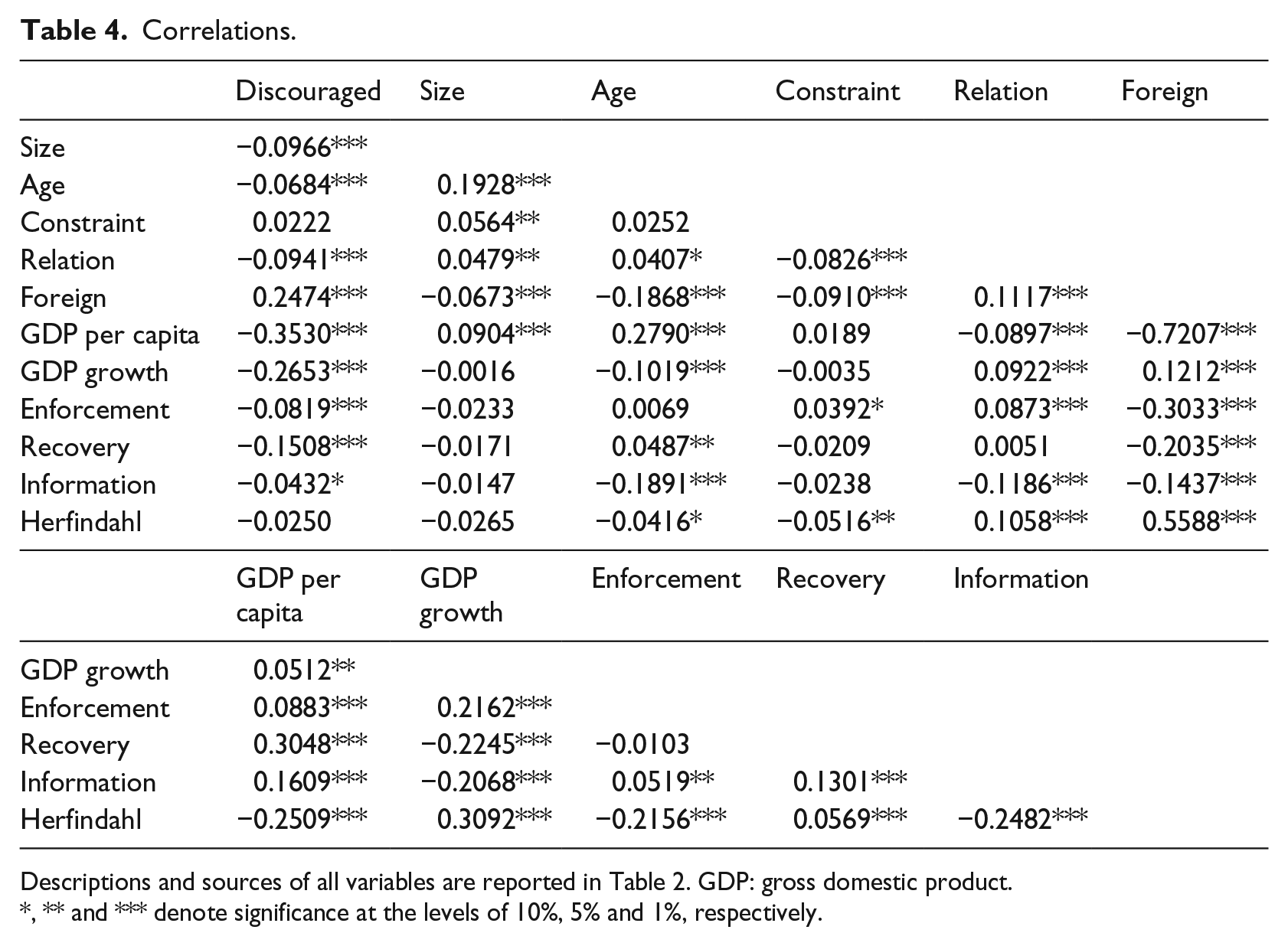

In our sample, 3047 firms (66%) belong to the EU 15 and the remaining 1536 firms (34%) belong to the EU 10 (Bulgaria, Romania and Croatia are not represented because they joined the EU after 2006). Interviews were conducted in September 2005 in the EU 15 and between April and May 2006 in the EU 10. After dropping 125 firms operating in the financial sector, we keep 2582 observations which contain information about borrower discouragement. 9 Finally, we lose 526 observations due to missing values in one or several of the independent variables, arriving to a final sample for our regressions made up of 2056 observations from 22 countries (14 old Member States and 8 new Member States). Variables describing the presence of foreign banks and country-specific variables are obtained from Micco et al. (2004), the European Central Bank, the United Nations Statistics Division and Doing Business Indicators. Table 4 reports the correlations, where no collinearity problems are detected.

Correlations.

Descriptions and sources of all variables are reported in Table 2. GDP: gross domestic product.

, ** and *** denote significance at the levels of 10%, 5% and 1%, respectively.

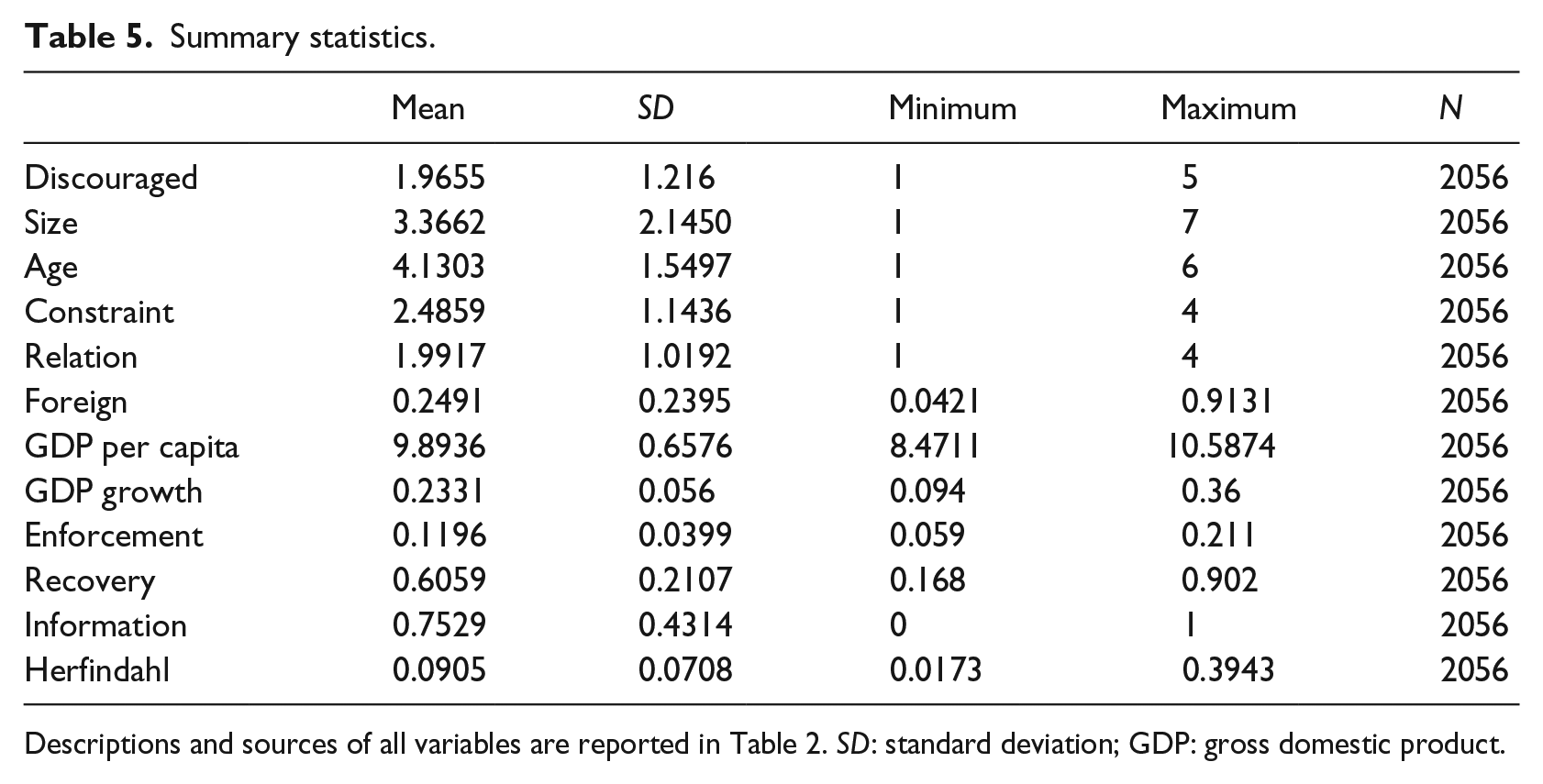

Table 5 shows a summary of statistic for the variables used in our regressions. The first thing we notice is that the variable size shows a mean value of around 3, which in our categorical classification places the average observation in our sample into the group of micro firms, with an annual turnover below 2 million Euros. This is important because most empirical research in the financial literature neglects such firms due to the lack of data. In spite of their reduced dimension, managers have a moderate perception about the existence of financial constraints (2.4589) and the strength of their banking relationships (1.9917). As for the institutional environment, enforcing debt contracts has an average cost of 11.96% and ranges from a minimum of 5.9% to a maximum of 21.1%, the recovery rate from insolvent firms ranges from 16.8 to 90.2 cents on a dollar with a mean value of 60.59, and around 25% of firms operate in countries without private credit registries about firms and individuals. This indicates that European countries still have an important task in trying to improve the strength and efficiency of their institutions.

Summary statistics.

Descriptions and sources of all variables are reported in Table 2. SD: standard deviation; GDP: gross domestic product.

Results

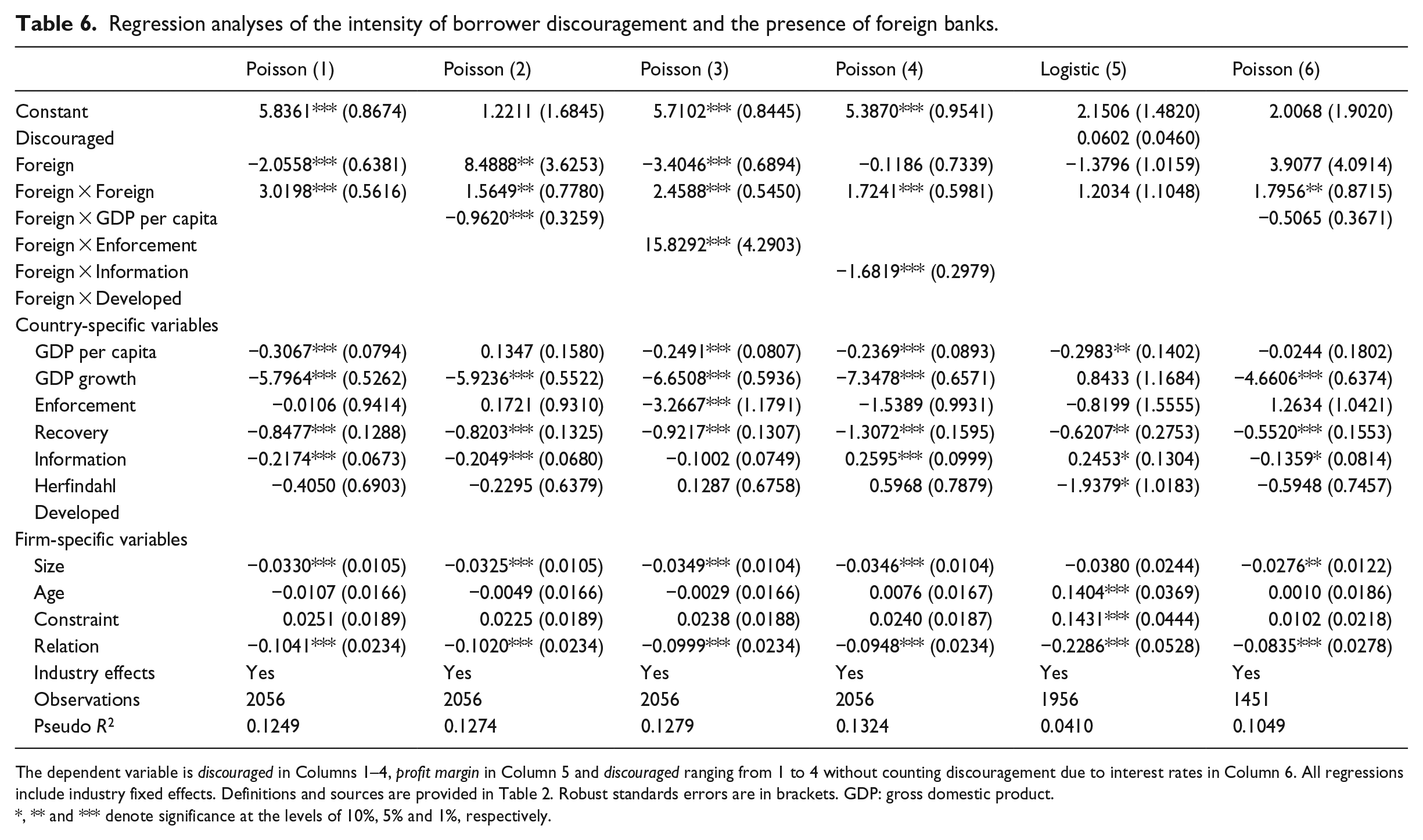

Table 6, Column 1, contains the non-linear specification, which includes the quadratic term of the variable foreign, aimed at testing our first hypothesis. The coefficients for the variables foreign and foreign × foreign are statistically significant (at the 1% level), with a negative and positive sign, respectively. This confirms hypothesis 1, indicating that the association between the presence of foreign banks in a country and the intensity of borrower discouragement follows a U-shape. The minimum of this relationship is achieved when foreign banks own 34.04% of the banking system assets, which is around the 75th percentile for the variable foreign. This means that around 25% of firms in our sample are, compared to the remaining 75%, more discouraged from applying for a loan as the presence of foreign banks in the banking sector increases. Even if the number of firms affected by the presence of foreign banks is smaller than those that benefit, the economic impact of the former is much more significant. The intensity of borrower discouragement increases around 170% (from 1.23 to 3.3) if the variable foreign increases from a value of 34.04% (where the U-shape reaches its minimum) to 91.31% (the sample maximum), whereas it decreases less than 25% (from 1.60 to 1.23) if the share of assets owned by foreign banks goes from 4.21% (the sample minimum) to 34.04%.

Regression analyses of the intensity of borrower discouragement and the presence of foreign banks.

The dependent variable is discouraged in Columns 1–4, profit margin in Column 5 and discouraged ranging from 1 to 4 without counting discouragement due to interest rates in Column 6. All regressions include industry fixed effects. Definitions and sources are provided in Table 2. Robust standards errors are in brackets. GDP: gross domestic product.

, ** and *** denote significance at the levels of 10%, 5% and 1%, respectively.

Next, in Columns 2–4, Table 6, we introduce the interaction terms of the variable foreign with the variables GDP per capita, enforcement and information, respectively. We do this to test, in our second hypothesis, whether the effect of foreign banks on borrower discouragement depends on the development of a country’s institutions. 10 The coefficients for the three interaction terms are statistically significant (at the 1% level), confirming hypothesis 2. The negative sign for the coefficients on the variables foreign × GDP per capita and foreign × information and the positive sign for the coefficient on the variable foreign × enforcement indicate that better institutions can mitigate the harmful effect that foreign banks have on discouraged borrowers. 11 This also means that borrower discouragement may decrease (or increase less) with the presence of foreign banks in countries with high income, with cheap debt enforcement mechanisms, or by having a private bureau providing credit information about firms and individuals. For example, for firms operating in the country with the most expensive (cheapest) debt enforcement mechanism, a one standard deviation increase in the variable foreign induces an increase of 52.04% (decrease 14.55%) in the intensity of borrower discouragement. The same variation in the variable foreign originates that the intensity of borrower discouragement decreases 12.17% (increases 43.01%) for firms operating in the richest (poorest) country in our sample.

However, we cannot fully rule out that the non-monotonic association between foreign banks and borrower discouragement is also due to the degree of presence of foreign banks per se. In Columns 2–4, Table 6, we also obtain the U-shaped relationship between borrower discouragement and foreign banks. The coefficient on the variable foreign × foreign remains positive and statistically significant, while the coefficient on the variable foreign becomes negative for those firms operating in countries with stronger institutions. As a consequence, we believe that the level of institutional development and the share of foreign banks in the banking system are both important in explaining the influence of foreign banks on borrower discouragement.

Regarding the control variables, results across the different specifications of Table 6 remain consistent with the existing literature (Freel et al., 2012; Leon, 2015; Mac an Bhaird et al., 2016; Xiang et al., 2015). Borrowers operating in more developed countries or in economies which are growing at a higher rate are subject to lower levels of discouragement. Our results also show that a more efficient legal environment when dealing with bankruptcy procedures helps to reduce borrower discouragement. We find that the existence of a private registry that provides information about individuals and firms also proves to be important in ameliorating the problem of discouraged borrowers. As for the firm-specific variables, our results seem to suggest that borrower discouragement is associated with the existence of informational asymmetries. We find that borrowers of smaller size or having a worse relationship with their bank are more discouraged.

Robustness checks

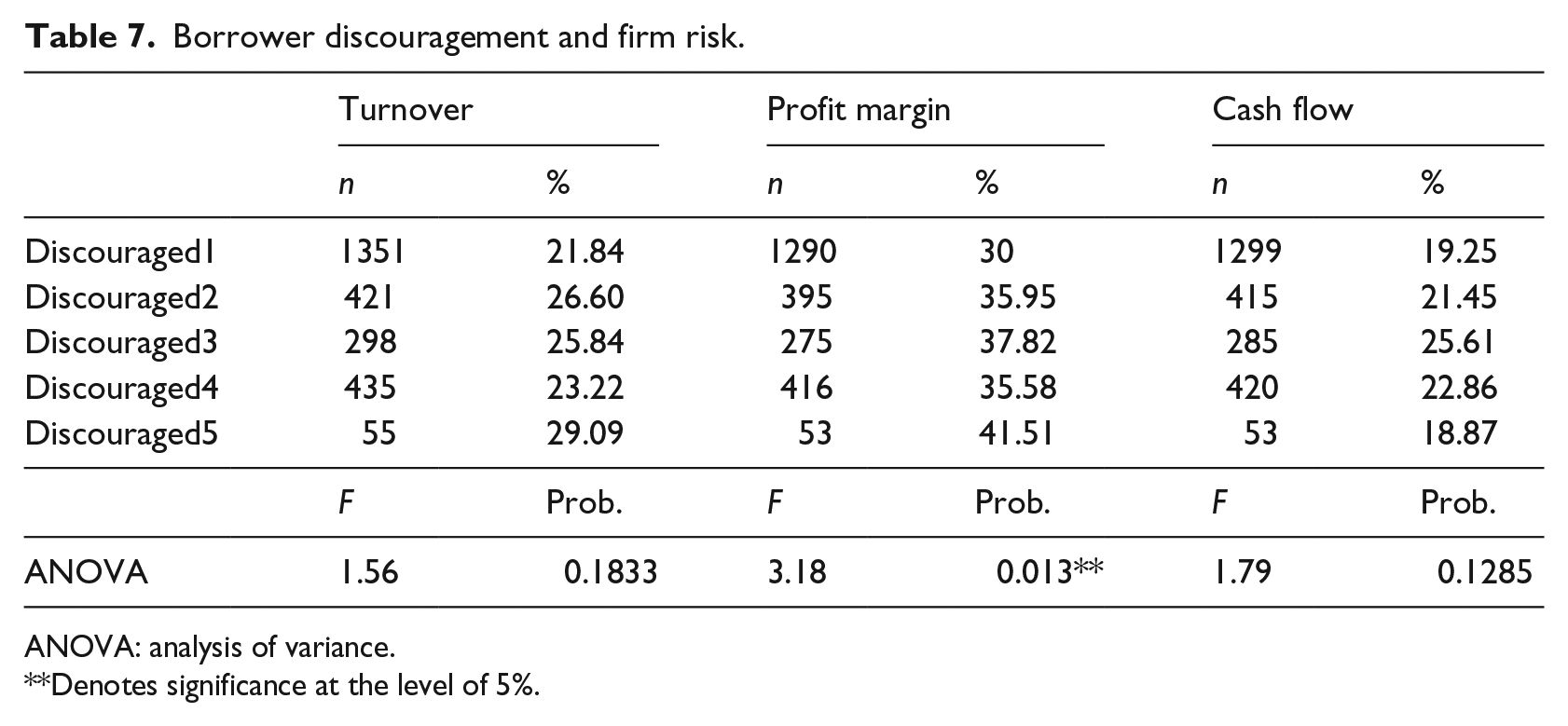

One limitation of our dependent variable is that there is no distinction between good and bad borrowers. So, one could wonder whether more intensely discouraged borrowers are actually riskier or worse firms and therefore, discouragement would be seen as desirable. Unfortunately, our data set does not provide detailed financial information in order to make a comprehensive assessment of the quality of borrowers and its association with their discouraged level. We can only create three dummy variables that take the value 1 if the firm’s manager recognises that the situation of the firm has deteriorated since the last year in terms of turnover, profit margin and cash flow, respectively, and 0 otherwise. Using these risk indicators, we try to address this issue empirically following Ferrando and Mulier (2015). 12

First, Table 7 contains a one-way analysis of variance (ANOVA) that tests for differences in the variables turnover, profit margin and cash flow broken down by the levels of the variable discouraged. We observe that profit margin is the only variable where the mean differs significantly among the levels of borrower discouragement. However, in unreported results (available upon request), Bonferroni, Scheffe and Sidak multiple-comparison tests indicate that the differences between the means of these variables for each pair of discouragement levels are not statistically significant.

Borrower discouragement and firm risk.

ANOVA: analysis of variance.

Denotes significance at the level of 5%.

Second, to investigate whether borrowers subject to more intense discouragement are riskier over and above the other factors that drive discouragement, we regress in the following empirical model (2) our risk indicators on basically the same model as in our base model (1) and add the variable discouraged as independent variable

where risk measures are the dummy variables turnover, profit margin and cash flow. For the sake of conciseness and brevity, in Column 5, Table 6, we only report the regression results using the dependent variable that is significant in Table 7, profit margin (results using the other dependent variables remain qualitative the same). We find that the coefficient on the variable discouraged is not statistically significant, indicating that borrowers subject to more intense discouragement are not more likely to have their profit margin deteriorated since the last year. Third, in unreported regressions (available upon request), we find that our results remain the same if we run Columns 1–4, Table 6, on the subset of firms that did not have a deteriorating profit margin, turnover or cash flow over the last year. In light of the above analyses, in our sample, we strongly believe that more intensely discouraged borrowers are not riskier firms.

One could also wonder whether our results are driven by the influence of a single reason such as interest rates or guarantees on the variable discouraged. To check this possibility, we create five alternative definitions of our dependent variable excluding from each counting one of the reasons for borrower discouragement. The five new dependent variables, which now range from 1 to 4, enable us to re-estimate Columns 1–4 in Table 6 five times, thus originating 20 new regressions. The only change in our results is shown in Column 6, Table 6, where the variable foreign × GDP per capita becomes statistically insignificant when interest rate is not taken into account to build the dependent variable. To check the robustness of this result, we follow endnote 10 and substitute the variable GDP per capita by a dummy variable that equals 1 if the country’s GDP per capita is above the sample mean and 0 otherwise. In unreported regression (available upon request), we find that firms operating in richer countries suffer less intense discouragement when the presence of foreign banks increases. This confirms that our main results hold even if we do not count the interest rate reason to build our dependent variable. The above analyses strongly reject the argument that our results are explained by the impact of any single reason on the variable discouraged.

Conclusion

The ongoing and significant process of foreign direct investment in the European banking system, which began two decades ago, continues raising the concerns of policy makers, professionals and academics. The efficiency and international dimension of foreign banks will likely bring benefits for large and transparent companies, while the role of foreign banks in SME financing constraints remains unclear. Existing empirical evidence has largely neglected the demand-side perspective. Besides being rationed, SMEs can suffer financing constraints if they are discouraged from applying for the debt resources they need for their investments.

Extended borrower discouragement could explain, for example, why a higher presence of foreign banks leads to an overall reduction in the amount of credit being granted to the private sector in countries where foreign banks seem to target the market for SMEs. In addition, differences in foreign bank presence and borrower discouragement intensity across countries call for an international analysis of this question. This article provides new insights into this problem analysing the association between borrower discouragement and foreign banks using a sample of SMEs from 25 European countries.

We find that the existence of large differences in the presence of foreign banks in European countries is responsible for the variations in the intensity of discouraged borrowers across European SMEs. Borrower discouragement increases with the presence of foreign banks for firms in countries where more than 34% of the banking system assets are held by foreign banks. This means that once foreign banks control more than one third of the banking system assets, increasing their presence in a country becomes a detrimental aspect of the credit market that intensifies the level of discouraged borrowers. However, the association between foreign banks and borrower discouragement is moderated, to a large extent, by the strength of a country’s institutions. More developed economies, cheaper debt enforcement mechanisms and better private information registries in a country could significantly ameliorate borrower discouragement resulting from a higher presence of foreign banks.

Our study contains evidence with clear implications for firms, financial institutions, policy makers and academics. First, firms should be aware of the ongoing transformation of the banking system triggered by the financial liberalisation. The presence of foreign banks could result in a decline in lending to the most vulnerable firms, which are those of reduced dimension operating in less developed economies. Second, the flow of credit towards SMEs should be of some concern for foreign banks, who should be aware of problems such as borrower discouragement limiting the demand for credit. Third, policy makers should take into account the disadvantageous consequences that our results reveal for the financing of SMEs and, therefore, their growth and survival. Growing financial liberalisation leading to increased penetration of foreign banks may result in more discouraged and constrained SMEs, which hampers job creation and economic growth. Finally, academics could complete our empirical contribution by overcoming the limitations of our sample, that is, using a data set that fully captures the quality of the firms and/or expands over several years. Future contributions could also shed additional light on the market failure represented by discouraged borrowers by comparing them with non-applicants.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Ana Mol-Gómez-Vázquez and Ginés Hernández-Cánovas acknowledge financial support by Santander Financial Institute (SANFI) and Fundación UCEIF.