Abstract

Highlights

Content budgets are stable with only 15 per cent of respondents suffering significant reductions (5 per cent or more).

Great majority interested or have an early involvement in big data and data analytics initiatives. But uncertainty whether and how the information service quite fits in. Can this only be ‘analysis-lite’.

Major potential new role in curating big data and analytics.

Global operations for many services, with varying central control and a mix of organizational models.

Pressures on staff headcount as 35 per cent lose posts and others appointed on temporary or fixed term contracts.

A commitment to outsourcing by some 50 per cent of respondents, some very mature arrangements, with a shifting balance of responsibilities between onshore and offshore staff.

Whether to embed information staff in business units is still a big decision point for managers.

Technical, analytics and personal skills development needs of IS staff is widely recognized.

Continuing doubts about adequacy of professional education given these changing business and technology environments.

Many positive developments in knowledge sharing, social media, the use of stories and growing use of enterprise-wide collaborative systems.

Relationships with information vendors and managing local access to data products still a high profile and sometimes a contentious issue.

Introduction

This is the 24th year of the Business Information Survey, the longest continuous survey of the delivery and use of business information services and sources in the UK. With the Eurozone crisis on the back burner if not resolved, unemployment dropping across Europe and North America, and some economies such as the UK’s showing positive if patchy growth, the conditions for business look much more positive as we near the second quarter of 2014. Despite worldwide political uncertainties and concerns over energy prices, the S&P & FT share indices are riding high.

Whilst competition in many industrial and service sectors is fierce, there is a guarded sense of optimism that the global business environment is on the up. If so, what is the position of corporate information services in this climate?

Last year’s Survey 1 asked some fundamental questions about the present and future of these services, or at least as we have traditionally known them. Some of the responses gathered in early 2013 raised major doubts about the ability of conventional information and research services to survive changed user demands, disruptive technologies, managerial scepticism about the value being added by professional information managers and their services, let alone the ever increasing pressure on costs and central overheads. If not apocalyptic, these forces seemed to be shaking many services to their core.

When these findings were published a year ago and in successive presentations I made at professional meetings, I received a mixed response. I have never claimed that this tiny survey population could ever be statistically valid so I was always nervous about how far these worries could be generalized. Some audiences thought that these were far too gloomy and did not represent the reality at that time. Others said that it coincided with their experiences, personally or from observing events in other companies. I argued that there were too many worrying signs that cast doubts over the long-term survival of traditionally organized, centralized information services to simply ignore this admittedly partial evidence from the coal face.

I suspect that if anyone senior in the professional associations had read the article then it would have sent a shiver up their collective spines. Maybe, in retrospect, I was too pessimistic. Maybe I did misread some of the signs. But, actually, I doubt either of these.

I asked ‘what if anything, in this world of uncertainty and change, could be done to preserve some information services organizational models which quite evidently are worth defending.’ I suspect that was only part of a key question. Perhaps more positively I should have added ‘and what new and innovative models can be developed to meet future needs and circumstances.’

I hope that you will find that much of what follows is interesting as a conspectus of current information management issues. For instance, the trajectories of budgets, utilization of staff, outsourcing, service development, vendor management, the traction of social media and knowledge management in companies and the development of metrics are all important factors which rightly preoccupy senior information managers. However, these are not ‘the big question’.

The key issue is finding a way that information managers can exploit existing competencies and to develop new skills to enable organizations to make better decisions, achieve greater profitability and in a socially responsible way. If this territory is moving information management away from the conventional exploitation of external information and the piecemeal processing of internal data then that is where we need to be.

Methodology

The Survey methodology is simple and straightforward. I interview a panel of senior information managers from a range of industry sectors. Seventy-six per cent of them, 16 of this year’s sample of 21, have been involved in the Survey in previous years, some for many years. The rest are newly recruited on the basis of their sectoral involvement, their expertise and, of course, their willingness to be open and honest with me. It is my intention to try to retain this core group for a number of years in order to provide continuity and a longitudinal element to the Survey, a kind of panel study. The new participants bring a freshness, varied perspectives and different practices to the Survey findings.

The interviews last between 30 and 45 minutes, sometimes longer, and concentrate on developing a narrative about their role in the company, the key issues they face and their strategic priorities for the next two to three years. The interviews are totally confidential – no one else knows the identity of the participants – and the data I obtain is aggregated so as to disguise the identity of the respondents. Sometimes comments made in the discussion have to be omitted in the writing up because otherwise it can become obvious which company is involved.

This is a kind of ethnographic methodology, charting the development of these services, returning year on year and trying to understand the dynamics by close analysis and discussion. The interviews have over the years developed into a number of long conversations with trusted colleagues. This is the complete obverse of a tick box questionnaire. Twenty-five information managers were approached in December 2013 and January 2014 and 21 agreed to take part.

We gave up many years ago any claim to the statistical validity of this small population in relation to the totality of business information managers in the UK. The Business Information Survey 2014 is no more or less than a detailed look at 21 information services and how they are resourced, managed and financed. In fact, there is quite a good mix of sizes of services (measured by extensiveness of budget or numbers of staff), of industry sector, of philosophy and of their approach to the utilization of certain technologies.

The value of the Survey rests on the seniority and authority of the chosen respondents. It uncovers examples of different strategies and practices – whether these are good, bad or indifferent is for the reader to judge. But there is more agreement than divergence on many of the questions. We believe that a picture of the state of such corporate business information services has emerged, though less clearly than in the past, and a number of generalizations and trends are visible. This Survey gives an interesting account of how these very professional services have been repositioning themselves to serve their companies more cost-effectively in the face of transformative financial, technological and social change.

It is appropriate here to record our thanks to the respondents who, through the generous donation of their time and even more through their frankness have once again made this year’s Survey interesting. It hardly needs to be stressed that the confidential nature of the interviews are an essential reassurance to senior corporate staff who have been extraordinarily honest with their views on their business situations. Even more plaintive are our thanks to those colleagues who have helped us over the past 23 years, yet have themselves become casualties of the cataclysmic forces and fragilities of economic and business cycles, or of changing corporate fashions and views about the value for money that these services bring.

Big data, analytics and the managerial challenge for information leaders

How is the information profession preparing people for the new information/knowledge roles that are emerging in areas such as big data and analytics? The competition for these roles is coming from a number of other professional fields and it is far from certain that the traditional information community can get a significant share of these jobs, or indeed take leadership roles. Senior knowledge functions are often undertaken by IT professionals or, in the legal sector, practice lawyers. Sometimes these roles are re-cast as Chief Knowledge Officers, Chief Information Officers or, even more fashionably at the moment, Chief Digital Officers. Access to senior management, at board level is fundamental. Are IM professionals up to this competition?

An analogy can be made between the current situation in corporations and that of the information agenda in universities in the mid-1990s. Many universities realized that in order to get libraries, IT and other learning/research support properly recognized and up the senior management agenda then it should integrate these previously independent services and make a senior appointment to head up this new function. Such ‘directors of information’, analogous to Chief Information Officers in the corporate sector, were to become members of senior management teams and to provide strategic leadership. In that capacity they sat alongside directors of finance, human resources, and academic affairs, with the same status and authority. So the universities who ventured down this path of ‘convergence’ then started recruiting to these new roles. Eighty per cent of these appointments turned out to be library and information professionals rather than IT directors or from other backgrounds. The reasons were, generally speaking, straightforward. The librarians were well connected across their institutions, they had acute political antennae, they were closely aligned and in tune with the overall corporate objectives, they had managerial ability, they were bright and had strategic insight on higher education. Most outshone the technically oriented IT directors. Is it possible for senior information management personnel to rise to the current challenge in companies in the same way, to take on senior leadership roles?

Some of our respondents are well aware of this challenge to the information profession generally as well as that in their own organizational environments:

We have to be careful that we don’t spend all our time trying to justify information and research services that we provide through ROI (return on investment) calculations, through cost savings and so on as this can become far too introspective. Librarians and information management is a famously conservative profession. The window is open to the wider world and it’s getting rather draughty! I believe we must be more aggressive and expansionist both in investing in new products and replicating the confidence that other areas show, such as Business Development which has grown by about 25 per cent in the last year or two. Perhaps it is easier for them to justify their existence with revenues climbing in such a fashion and hence they can show very good return on investment. But such areas do constitute a serious threat and I believe commandeer resources that previously the Information/Research service would have deployed and managed. Perhaps the relative success of Business Development is about them being better in arguing the case. Information/Research has been more cautious and, I think, has suffered because of that. Part of that caution is because we tend to look long-term, say five years and in terms of what we’re doing with information collections and research tasks. Whereas other departments such as Business Development are probably only looking 18 months ahead. Ultimately, though, it’s because Business Development have been a lot more focused on growth. One of the problems is, I think, that we’re in a vice, squeezed between tradition and new roles. We are fighting to keep some contracts whereas perhaps we ought to walk away from some of our activities. As a profession I don’t think we have taken sufficient ownership of some of the content that we manage. We have to find new roles because we will not survive as a profession as a body of people on the current basis. Even outsourcing isn’t too clear at the moment. Some work goes out to offshore locations, some comes back. It’s interesting to observe that our US colleagues seem to be more effective and they don’t seem to attract the ‘taken for granted’ label. I think we need a paradigm shift. We have to create the new norm by reinventing ourselves and developing new business skills. Or do we simply go back to established core practices? We have to establish the information research service as part of a convincing business narrative. This is a lot easier to say than to achieve. (Legal) The workload has continued to grow, both in volume and sophistication. We have moved into more ‘advisory’ roles rather than just data retrieval and delivery. Some of this work involves large client-facing projects. For instance, we contribute to the work of the Corporate Finance team on major disposals. In terms of sectoral capability, we have become more knowledgeable. This is a constant challenge but, generally speaking, most of our users think we’re great! We have also been contributing to the forward planning of the Leadership Team in their construction of future scenarios that might face the company. The contribution of a strong research function here is appreciated. We are using the Jive collaboration software to assist this process. It’s very important as this group is led by the Chief Executive and five partners who make up the executive. Sometimes, we have problems because the embedding of our staff in business units and projects is so successful that they can ‘go native’, for instance in the Business Development team. But this is a compliment to the quality of my staff and shows how important it is to work closely with the business and be aware of business objectives. The more access to data and human resources we provide, the more demand we create and the higher the value that we are seen to be adding to the company. But we have to be aware of the danger of trying to be all things to all men. It can be exhausting but, ultimately, I believe we are providing the right services to the right customers. (Financial Services) The recent report by the SLA/FT

2

emphasized the information profession’s dilemma between traditional values and roles and moving into new areas and adding more value to the business. As a profession we must go beyond finding and disseminating information into a more analytical form of work. To illustrate this in our own company we undertake lots of searches and recently we have been pulling out themes and summarizing these important issues for the company. These summaries have gone down very well around the company and have generated a lot of good will for us. This is a step well beyond the past practices of the information department here. The company is interested in process mapping, that is how we actually undertake our research programme. Up to now the Information Department has been pretty invisible in this exercise. This is interesting because our services are well used and we are highly valued within the business. Yet being marginal in a major project such as process mapping shows that we are sometimes bypassed and, like fresh air, rather taken for granted. We must be much more explicit about our contribution to the business and more visible within the company. (Technology) The service offering from Information Services is pretty much unchanged. We continue to look for new opportunities to develop services, to capitalize on the intellectual assets of the business. We continue to try to exploit the demand for advanced research work which gives our organization a competitive edge. With the focus continuing on cost management, we are also keen to ensure we engage the organization more effectively to support the broader discipline of information management. We have to be clearer about the needs of the business which, inevitably, are changing. In developing our service offering we’re unsure about the receptivity of this strategy. The Bank has tried knowledge management programmes in the past but these on the whole have disappointed. There are significant opportunities to partner with IT to support their information management strategies but the critical question remains, of course, ‘what value can we add?’ and how are we perceived by our colleagues to support these initiatives? (Bank)

According to Viktor Mayer-Schönberger and Kenneth Cukier, authors of a useful recent book on the subject,

3

‘Big Data’ refers to the burgeoning ability to crunch vast collections of information, analyse it instantly, and draw sometimes profoundly surprising conclusions from it. This emerging science can translate myriad phenomena – from the price of airline tickets to the text of millions of books – into searchable form, and uses our increasing computing power to unearth epiphanies that could not have been seen before. Big Data will change the way we think about business, health, politics, education, and innovation in the years to come. It also poses fresh threats, from the inevitable end of privacy as we know it to the prospect of being penalized for things we haven’t even done yet, based on Big Data’s ability to predict our future behaviour. [The data scientist is] a high-ranking professional with the training and curiosity to make discoveries in the world of big data. The title has been around for only a few years. (It was coined in 2008 by one of us, D.J. Patil, and Jeff Hammerbacher, then the respective leads of data and analytics efforts at LinkedIn and Facebook.) But thousands of data scientists are already working at both start-ups and well-established companies. Their sudden appearance on the business scene reflects the fact that companies are now wrestling with information that comes in varieties and volumes never encountered before. If your organization stores multiple petabytes of data, if the information most critical to your business resides in forms other than rows and columns of numbers, or if answering your biggest question would involve a ‘mashup’ of several analytical efforts, you’ve got a big data opportunity. The computer engineers who mine the enormous pools of data being collected about our lives to predict things like which Netflix movie you want to watch next and what your social media connections say about your ability to pay back a loan.

So how can information professionals, as we traditionally know them, get a piece of this action? Or perhaps they cannot or should not and will be by-passed by these developments. In fact, the majority of our respondents (80%) believe that they should get involved in their companies big data and analytics projects, in some way or another, even if they are not sure how. Some of the dilemmas are very well described by one respondent:

We are interested in the big data issue and, in terms of our involvement, it’s very much on the cusp at the moment. We’ve spent the last twelve months trying to understand what the term will mean to us and what contribution we can make. I’m sure that big data and greater analytical capability will contribute to the company’s growth agenda. Part of our role is ‘analysis’ and we have benefited from some training by our software providers to be able to use some analytical tools along with the retrieved data. But we are still exploring what the Information/Research team can bring in areas such as data visualization. I’m sure that we have to go further in developing these analytical capabilities to enhance our service offering but we have to define boundaries. Some of this discussion is about the bringing together of external information, our traditional territory, and internally generated data. We are domain agnostic and there is a need for a more forensic type of analysis. Developing some of our people as data analysts will enhance our capability and has to be part of our future. But it is difficult to make a formal proposal to the company at the moment to achieve this transformational move without more insight and there’s a danger in biting off more than we can chew, over-engineering our services. (Financial Services) This is a big area for the company which has been expanded through acquisition. We procure a great deal of data of all kinds. There are a host of data analytics companies around such as Axion & Comscore who will provide outsourced services and software. I’m not personally sure where it all fits together. The consultants in the company are leading this area but there is involvement from risk people, IT, Marketing and ourselves who have an interest. My counterpart is head of market analytics and is obviously equally keen to contribute. There seem to be two ways in. There’s the number crunching element and there are some very bright people already very good at that. The other angle is to ensure that it’s the right data that is being worked on and that suitable insight is being gained as a result. Another later stage is the communication of the analysis into actionable decision-making. So there’s a lot of cross-overs of skills and competence. We’ll have to see how it all shakes down and what our role becomes. (Business Services) This is important for the business. Indeed, it was part of the reason for the changes in organizational structure and the compilation of the five-year plan. This is one of the crucial business touchpoints and will affect the company strategically. (Pharma) I think there are important developments in this area and there are some initiatives with which we are involved in the company. A number of students from the local information studies department have gone into data analytics in the last five years. Our technology management team are taking the lead in this area. Initiatives such as web scraping have big risks associated with them. There are lots of North American examples which we’re following to see whether we can learn from them in the areas of big data. The information services group have an involvement in some of these schemes, albeit a peripheral one. (Technology) We have an increasing interest in data analytics alongside existing services. One of the biggest challenges facing the company is the management of the mass of internal data, not the external information with which we are primarily concerned. Text and data mining are important applications which are relevant here. Although we’re not driving these developments, we partner with the data analysts and take part in the nascent groups starting to form around the big data agenda. The term ‘integrative analytics’ is being used by some people. It seems to me that the leadership of this new area is up for grabs. (Pharma) I believe that there may be a role here for Information Services but we haven’t seen it clearly yet. Getting heavily involved in these areas would be a major step change in our activities and services and at the moment we’re trying to do this through advice and guidance. I think our service development will evolve rather than be made in one massive step. The Bank does have an analytics team of around 60 people who are offshored but who are not part of Information Services. This is the kind of work Information Services undertakes but the analytics groups provide additional ‘bells and whistles’. Their work contributes to pitch books, annual reports, investment reports and so on. For instance, they’ll produce big sets of presentation slides for use by senior Bank staff providing a one-stop shop to support the bankers’ requirements. (Bank) The IS isn’t directly involved in any Big Data projects in the Company. We are a very small team which concentrates on being efficient and customer centred, with no capacity, in terms of skills or time, to venture substantially outside our conventional information supply and management mission. Our structure within the KM function doesn’t really enable us to get involved with Big Data. The IT people see it as their domain. However, I am interested in general developments in this area and am keeping a watching brief. (Energy) We don’t really do much analytical work. This is done by the lawyers themselves. We are mainly concerned with enquiry work and coping with the number of these we receive is taxing. We don’t undertake interpretive work but concentrate on providing access to sources of information and data retrieval. (Law) The company is looking at the issue of big data at the moment. I don’t think that either I or the company is quite equipped yet to take this development on as a major project. Some of the added value work that I carry out might be called ‘analysis-lite’. (Technology) I think our major contribution in this field may be around the custody of data. There are clearly emerging needs for the curation of the Bank’s intellectual property. This is not widely recognized. (Bank) A real challenge is to work out in this information management landscape, what actually belongs where for maximum effectiveness. Analytics people are more expensive so we have to manage costs carefully. We need to maximize the value we provide from each of our business and service lines. More generally, the information industry as a whole needs to step up and be less apathetic in this new world. But this is easier to say than to do. The low hanging fruit have already gone, so future benefits/wins will be harder to come by and require more innovation and effort to deliver. (Bank) In terms of information use generally I think there is a real problem that people do not see themselves as owners. There seems to be no inbuilt responsibility for ownership. I would call this ‘information apathy’ – an inherent laziness by users. This seems to offer a major opportunity for information professionals but I’m not entirely sure how we exploit this. I believe that it has a material effect on the way that we manage our information assets. (Bank)

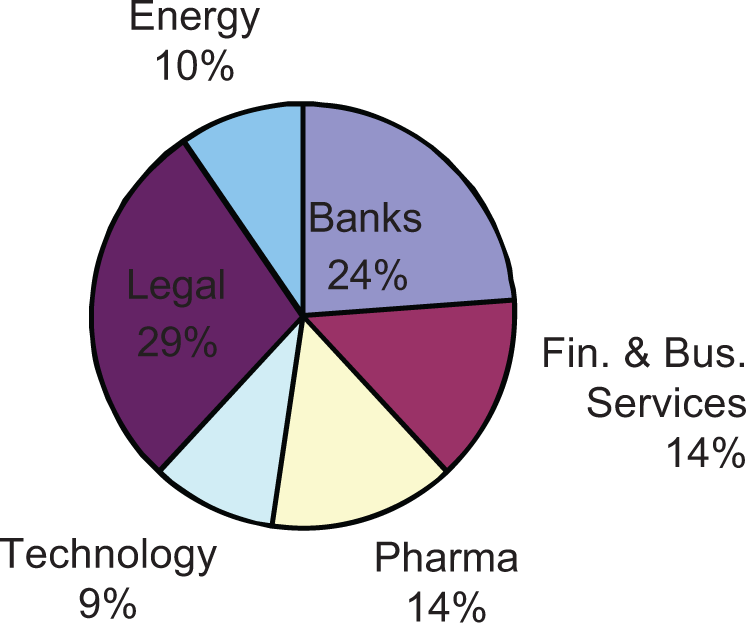

Industry sector breakdown

Question 1: Which industry sector is your Company in?

Respondents by sector (n = 21).

Question 2: Where is your information/research service positioned in the Company?

This question is designed to probe the way in which the Information/Research service is located in the organizational structure. The range of responses in 2014 exemplifies the highly varied organizational models into which information services fit in the wider world driven by a host of factors. One of the interesting observations to anyone looking in from outside is that few companies with global reach and distributed information services seem willing to establish an executive and integrated structure to bring these services together.

There remain three information centres based in mainland European capitals. Between them they subscribe to some very expensive databases including Standard and Poor’s, Moody’s and so on. There has still been no substantial coming together of information staff distributed around these offices despite my keenness over many years to achieve greater integration. (Bank) The Information/Research service has had more global exposure and use by the ‘distributed’ member firms. The UK-based service has the most developed service offering so this is hardly a surprise. Some of these other firms have their own information presence locally and we try to help and influence them when we can. This doesn’t amount to any kind of centralized management. We accept that different markets have differing needs. I continue to report to a Board Member and therefore have very senior access. (Financial Services) My management team is made up of myself plus seven regional managers. Most of our communication is virtual because we are distributed around the globe. The bulk of it is via a blog. Of course, there is a lot of face-to-face contact as well and twice yearly I do a ‘state of the nation’ session with all staff. The blog is an open one, not only to Information and Knowledge staff but also users around the company. (Legal) This corporate law company is, by turnover, one of the top 20 in the UK. The library and information service sits within a wider knowledge group. This includes various support services including IT and know-how/professional support lawyers who make up the team. This is a global group working across offices around the world. The library and information service has repositioned itself, more closely aligned with our knowledge management colleagues. There is far greater collaboration between information and knowledge professionals across the company. This has improved our visibility within the business but this still is a work in progress. Global communication between us all is achieved by a variety of methods and technologies including WebEx. Because of time differences, collaborative meetings have to be split between time zones. Our services are becoming more integrated in areas like current awareness and generally there is a healthy attitude to sharing. But there isn’t much global procurement at the moment. (Legal) There’s been no significant change in the organization arrangements this year except in one respect. This is the first time we’ve brought the global team under one group structure. My management reporting lines have changed. Now it is to the Head of Knowledge & Information who is a partner based in London. He looks after online content, social media, document automation and various other matters. One of the major challenges is communication to all these information professionals and support staff across these time zones. To tackle this communication process we use blogs, communities of practice and a whole variety of ways to bring people together. Clearly, we use teams, bringing individuals together for specific projects. An example is a project on document automation for which we needed to set up templates, biographies and company profiles. It’s reassuring that there’s really no significant cultural differences across this information community in these various, widely distributed geographical areas. We’re hanging a lot of the conversation between all staff on the concept of working smarter, not longer. Much of this is about establishing best practices that we use throughout the company and disseminating these and encouraging others to follow them. (Legal) I run a primarily scientific and technical information service which supports the company globally. The Information Service was formed in 2001 as a mainly virtual library and information service, consolidating a number of small physical libraries. Four small physical libraries remain – in the UK, France and two in the US. There is a matrix management system where the information staff in the non-UK locations report into their local managements as well as to me in the UK. There are seen to be major advantages in this degree of decentralization, with the staff embedded in the business units. (Energy) I’m the manager of the Information Centre in London. We’re part of the Bank’s investment banking division and I’m responsible to the global information head who is based in New York. We also have teams in Japan, China and Australia. Up to 12 months ago we also had small hubs in two mainland European cities but these have been closed, partly because the overall number of bankers employed has dropped. I don’t think that our workflow processes between the various offices and hubs on the information side are very integrated. I’m responsible for the licensing of market data globally and we manage the contracts for this out of New York and London as a shared responsibility. (Bank) There are major cultural differences between us and our US colleagues. In our US parent company there seems to be a perception shift to taking sectors seriously. They have huge practice groups and are open to different kinds of management approaches. We have to behave strategically. Whilst we’ve nailed the cost side down on a budget of some $8M overall, the practice in the US and in the UK on recharging differs. Most costs are recharged in the US but we do not recharge legal stuff in the UK. We have to look at the charging model much more closely because clients are now examining their billed charges much more assiduously. (Legal) My reporting line has been changed during the year. A year ago my manager was the Head of Quality & Compliance. But this has reverted once more to be the Managing Partner. The company has become a LLP, partly as a result of the preparatory work we did in advance of the ultimately failed merger in 2012. This corporate legal status makes future mergers easier to achieve. In fact, during the past year we’ve merged with a very small and sound London practice whose Managing Partner is about to take retirement. It has 10 good staff and a strong client list. The merger was smooth and everything came across in apple pie order. A previous merger was chaotic and we’re still trying to sort out issues. We’ve also absorbed a small, specialized service office which undertakes a lot of government and public sector work. It’s worth re-stating that the company doesn’t employ professional support lawyers (PSLs). The Knowledge & Information Team fulfils this role. It used to be common for law companies to have a number of PSLs but this is much less fashionable now and more difficult to justify in cost against value added. The lawyers we employ are expected to be fee earners. (Legal) In this global banking and financial services company there has been significant change in the organization of the information services function during the year. It has been split into two areas. My function now is to lead on market data procurement, primarily for content for our London office but also with some global contracts. I now report to the Chief Procurement Officer and have joined an eclectic team of support staff. Our Information Centre consists of just three staff members who are responsible for research and information seeking in various ways. This is partially outsourced now. These staff now principally serve the Compliance Team through their research efforts. (Bank) There’s been a major structural change in the organization of the information service. This is proving a real challenge to the operations of the group. There are now two parts to the information service. Firstly, the research team continue to be focused on ‘information discovery’. This is a blend of onshore and offshore capability, with embedded teams in some locations. Their work continues to be broken down into tiers with the heavy lifting associated with the less complex tasks executed offshore: high volume/quick turnaround requests. The other main group now, which is split off is concerned with vendor management. This is the team that handles all content management matters although negotiating with vendors continues to be handled by the procurement group. This has always been a distinct group of staff but the focus has now shifted. This is because it’s so large an area that a new management team and a new approach has been necessary. All transactional work will be undertaken by supplier staff, both onshore and offshore. A small group of employees (onshore and offshore) provide the oversight and governance of the function and associated management software. Managerially, this activity is the responsibility of the global head of vendor management. That person then reports to me, the head of the information service overall. There is no doubt that this change has improved our level of capability. We are managing a large content portfolio involving hundreds of contracts for thousands of products. This is a complex task. Given the level of spend, there is significant focus on managing these costs proactively. Our relations with this third-party supplier are good but we do realize that we have to manage the concentration risk, through dealing with one particular supplier. This doesn’t make me comfortable so we’re looking for another partner to undertake some of this work. This will be offered out to tender in 2014. (Bank) As head of the unit I wouldn’t say that I provide directorial leadership. Someone has likened it to more than 50 people in a boat rowing without a cox. It’s a kind of bottom-up management where the regional managers distributed across these offices have a lot of autonomy and report to me by exception. We use a global standards service model to guide us in the direction of the service. (Legal) Personally, in the interests of succession, I’m stepping back a little from the hands-on leadership of Information Services and my management team are increasingly taking some of this responsibility. (Bank) The research team remains within the research department of the Bank and has the same management as last year. Compared with past organizational homes, this continues to give us a higher image profile and we’re associated with a positive brand. Most of our users are internal within the Bank but we also serve some external users. There’s somewhat more of a regional focus which means that needs are more scattered and somewhat less obvious. (Bank) We are still located within the R&D function. This is a very creative environment and a suitable one in which to provide information services. In terms of hierarchy, we are one step down from the research leadership team. The Info Service operates globally and supports offices across time zones. We’re now leaner and more process oriented. The Competitive Intelligence function has shifted out of the Information Centre and is now outsourced. (Pharma) My work is now undertaken as part of the Marketing team which has been my organizational home now for three years. This grouping is very effective for me in that I can keep abreast of the important business development in the business and contribute my own information skills as well as tapping into a number of other discussions about the development of the company. (Technology) The place of the Information/Research Service is stable, sitting alongside Marketing & Business Development. This is functional and as good an organizational home as any other we’ve tried over the years here. There are synergies and commonalities between customer relationship management (CRM), market research and analysis and information/research functions. (Business Services) The last 12 months have been very busy but, in some respects, in terms of the Information & Knowledge service, somewhat calmer. Following the implosion of the KM/Information team a year ago, this has been a period of stabilization and regrouping. I was the only survivor of the cull of staff, had become a ‘one man information band’ and was located in the Human Resources Department. A review of support staffing in April 2013 led to a re-think and a restructuring of the support services. I was moved to the Compliance Team and this has been a great improvement. Information sits much more comfortably there and I’m directly responsible to the director who is in charge of risk matters. Whilst he isn’t particularly interested in information management or KM, I do get on with him at a personal level (he was a director of the company I worked for before the merger) and through him have more direct access to the senior management of the company. (Legal) We used to be located alongside the small training function and there were some synergies. The trainers have now gone and that leaves a gap for me in helping to deliver user training and ‘legal information literacy’. There are some 400 professional lawyers in the company and training is an important need. The Risk team is made up of six of us and we work well together. But I remain as the only information person and there’s no one to assist or mentor me in a professional sense. The company has established a new marketing team but they’ve yet to make any great impact as far as I can see. This is perhaps, once again, because of the difficulties of merging the fragmented elements of the previous four or five companies. (Legal) I am unsure about the long-term viability of the information function. The hangover from the 2012 review still affects us. Despite trying to turn the service around, the situation is still very difficult. (Bank)

General management issues

Question 3: How do you describe the current business conditions in which you are operating?

The business climate, obviously, has a huge effect on the operations of all companies, one way or another. Industry sectors also can vary in fortunes and direction. This in turn will set the context in which all parts of business are operating including the information service. So what has the last year brought our respondents and how do they look currently?

Overall the business conditions for the bank have improved. However, the investment banking arm has had a particularly difficult time and has shifted its priorities towards wealth management rather than investment banking. The investment banking division embraces corporate finance mergers and acquisitions capital markets. Our workloads have fluctuated somewhat because there are less bankers employed by the Bank than in the past. (Bank) I’m head of the information research function for a medium-size firm of lawyers. The key change during this last year is the considerable easing in the economy and there is no doubt that the pressure on us has slackened, to some extent at least. The major change is that there is less oversight on spending. There are still cost pressures but these are not as onerous as in the last few years. (Legal) We are operating in quite a good business climate at the moment, certainly better than last year. Cost control is tight but this isn’t such a bad thing. We are certainly doing more with less than in the past. (Legal) The business conditions for the institution have been mixed in the last year. We are certainly going in the right direction and the overall strategy is paying dividends. The recovery is patchy and in a rather stop-start fashion. There are many regional differences of course, with the American market showing the most resilience. The institution has a particular focus now on wealth management, on building reserves, and also generating customer deposits. This is a search for stability as well as new markets. (Bank) The company is going through an aggressive expansion phase. During the year we have acquired a specialist company in the oil and gas industry and we’re looking for growth in various other sectors. In fact, this growth is coming through both acquisition and internal expansion of our products, services and consultancy. Our presence in the health technology and scientific markets through product development is growing significantly. The economic climate appears right for this rather bullish expansion although in some sectors there have been delays on specific projects. (Technology) We are a technology consulting company. Our principal areas of activity are published research, bespoke consultancy, business support, sales and marketing. The business environment is tough but we are growing and taking market share from our competitors. However, we are not growing as fast as the company management requires. We are owned by a private equity company and we have an ambitious growth strategy. But everybody is aware of the competitive nature of the market. (Technology) The general business conditions are somewhat easier than expected. Of course, as a global bank there are different issues in various regions which preoccupy us. (Bank) Multiple products to the oil and gas sector. Generally good, growing in turnover and profitability. (Energy) The merged company has settled down somewhat and there seems more stability and mutual understanding. It continues its quite aggressive strategy of acquiring smaller practices, increasingly the norm in the legal sector. Size is critical, or so it seems, and the company is in a good business position as a result. (Legal) We have a global presence in 40 countries. The company has a strong portfolio of pharma products, with expansion in Asia-Pacific markets. Very competitive conditions elsewhere. (Pharma) The growth of the company globally is going ahead but is rather a slow burn. The member firms around the world have a great deal of autonomy in their strategy and operations. (Financial Services)

Information resources budgets

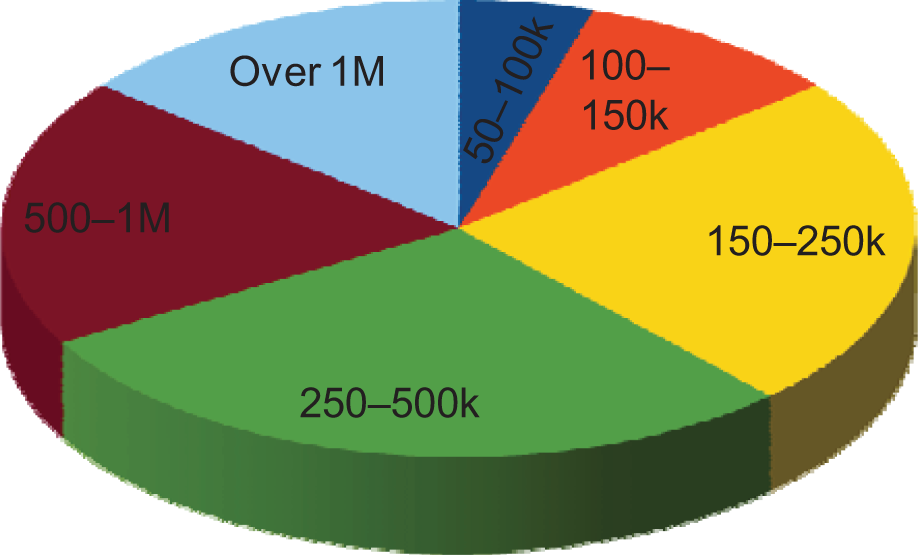

Question 4: What is your information department’s annual budget for business information resources?

Below £5000 [ ] £5000–£49,999 [ ]

£50,000–£99,000 [ ] £100,000–£149,999 [ ]

£150,000–£249,999 [ ] £250,000–£499,999 [ ]

£500,000–£999,999 [ ] £1 million plus [ ]

How has this changed from the previous year: Increased? Decreased? Stayed the same?

The following views represent the mixed picture of budgets generally and content budgets in particular. Ten per cent of our respondents have enjoyed budget increases of 5 per cent or more. Twenty-five per cent have had stable budgets, with purchasing power more or less maintained. Fifty-five per cent have flat budgets which have reduced in terms of what they can buy. And 15 per cent have suffered real reductions of 5 per cent or more. The hardest hit information manager reported a 25 per cent cut in the content budget (Figure 2). Here are the detailed responses:

Business information budgets £ per annum (n = 21). Information services staffing (n = 21). We have a four-year budget cycle and we’re about to start the third year. We are likely to have the same base budget in 2015. This predictability is important. The content budget has increased by around 5 per cent plus and we have built somewhat deeper sector resources to meet changing needs. There are still major challenges to face given the overall demands on us on the one hand and the resources on the other. The ‘integrity’ element of our service is as important as ever and involves compliance checking, an onerous but necessary task for the business. A recent compliance audit reaffirmed the value of our contribution to these processes. We are concerned about the changes made to and by Factiva as this is an important product for us. We can provide some substitution through One Source but this doesn’t replace the need for Factiva. It looks as though multiple subscriptions will be necessary. Our content management is carried out by manual methods but there are some useful systems available such as Research Monitor from Priory Solutions. (Bank) We’re holding our costs steady, flat in fact, and are trying to establish more standardized provision across all information services in all domains. This encompasses 26 offices in 31 countries. There has been tight cost control but somewhat more relaxed than the previous year. However, we have to be very vigilant as we use a zero-based budgeting model across information services globally. We set budgets each January and start the financial year in May. The process involves close questioning of requirements internally plus involvement of the local business finance manager in the distributed offices in London or New York then the budget is built up from local agreements. (Legal) Resource conditions are tight though stable. There have had to be reductions in content expenditure but ultimately the subscriptions renewals aren’t significantly different. We’ve had to adjust the content portfolio but did this in good time so as to ensure a smooth transition and avoid a sense of crisis. We have maintained a ‘business as usual’ approach, been ahead of the game and are now working to a three-year plan. (Pharma) We’ve been out to the business to check out those services which are seen as essential and those that are dispensable. It’s transpired that some of the cancelled material hasn’t made a difference in terms of information support to our users. For instance, we subscribed to three expensive, specialist pharma sources covering competitive drugs in the development pipeline. None of the three were error free but we felt in the past that we needed to combine all three to get an overall view. We took the decision to cancel two of them and none of our users has batted an eye since then. So there was surplus in the content collection but after this round of cuts then we are down to the bone. I’ve worked hard to convince both my management and user community that we’ve reached the limits. I have to say that the senior management of my division, Business Services, has given me great support. (Pharma) For some data resources we act as gatekeepers, as middlemen, as we can’t afford the licensing costs of putting it on desktops. The company is extremely dispersed, with 26 offices globally. Obviously, with this degree of distributed staffing, we have to keep data licensing costs within reason. This is down to hard negotiations with the vendors. In terms of resources we have enjoyed an increased content spend in this last year. However, we have to be very precise in business planning and in drawing up budgets which are realistic. (Technology) We overspent our budget last year but no one seemed overly concerned given that the data was needed for the business. We keep our content under close review and this has been a year of big changes exemplified by the Factiva situation. News aggregation is important for us and we keep in close touch with ongoing developments and professional communities of practice discussions such as instigated by Freepint. A global business has to be concerned with global news, and not just from Anglo-American sources. (Business Services) The content budget is stable, with a 3 per cent increase for inflation. I never submit an inflated budget, only bidding for what is needed, and I always work within that budget envelope. We have a new Head of Finance so it remains to be seen how this new broom looks at our operation. (Legal) The content budget has increased slightly with a rather new emphasis on ‘intelligence’ type products. I’m coaching my team to review content constantly. A number of aggregators have sprung up in recent years and we deal with them. However, there is a countervailing move for some publishers to withdraw their material from the aggregators and serve it themselves directly. News aggregation is an issue for us as we subscribe to Factiva. We’re not certain about the middle- to long-term option or if we should move to another supplier. E-books are important and are still much debated between the LIS and our users who need some of them. The publishers seem to take very different approaches to making these available and to use varied business models. We are quite happy to buy access to a number of key books for our users but don’t want a huge bundle of irrelevant material. This model may be quite appropriate for an academic library but not for us. It’s quality rather than quantity that is important in our case. (Energy) There’s strong pressure on costs and this obviously led to the staffing reductions over a year ago. Yet despite the damage to my professional pride and the limited budgets we have, I think there is a greater understanding of the information management/KM agenda than 18 months ago. The content budget is stable, some £500k, and has actually increased by 3 per cent. I don’t have input to the budget setting process and am just told by our Finance people what has been allocated. Lexis-Nexis is the major single item of expenditure and is obviously an essential tool for our lawyers. I completed a very time consuming, thorough essential audit of information resources in the new merged company in July. From a situation of confusion about these resources immediately post-merger, the position now is much clearer. One of our book suppliers helped in the process by assisting me in tracking content, clarifying subscriptions and creating a spreadsheet. The company is very keen on digital resources rather than print and in the circumstances we now face with staffing and space then this is obviously a sensible strategy. We’ve made strenuous efforts to reduce duplicated paper subscriptions to standard works that are usually around in law firm offices. We merged with two small legal practices in the autumn, taking on another 100 staff in all, and have encountered more duplicates, a number of which we have been able to cancel in favour of networked digital equivalents. (Legal) Our content budgets have been reduced and this has meant we’ve had difficult choices to make. The cuts have been in the order of 10 per cent during this last year and have meant difficult negotiations with vendors. The possibility of substituting one product for another is difficult because often we are served by niche providers who are most aggressive in their pricing strategies. The reality of the situation is that we have fewer licences than we had before and less desktop machines which are authorized to access these various data resources. We are a second-tier investment bank and therefore don’t have the budgets of the giant banks with whom we compete in certain markets. (Bank) The resource climate in the last year has been very tough, with a 25 per cent reduction in our content budget. It’s too early to assess the impact of such a draconian cut on the support of R&D and other aspects of the business. We’ve not been singled out as other areas of the company have been similarly affected. Our users were prepared for this, so haven’t protested too much. (Pharma)

Information services staffing

Question 5: How many staff are there in your library/information/KM service? In the past two years has this increased, decreased or stayed the same?

The pressure to control staff numbers and costs has continued pretty much across all our respondents. Thirty-five per cent have suffered losses of one or more staff, 45 per cent have the same headcount and 20 per cent have gained one or more. This is less serious than the situation described in the 2013 Survey for which we must be grateful (Figure 3). But even those respondents who have steady numbers may have had to change the employment conditions of their workforce:

The pattern now is to use many more fixed term contracts for staff and there are very few permanent positions. Whilst these and other temporary contracts are unfortunate, they are a sign of the times. Staffing is more favourable in North America than in the UK, both in number and in levels. The staffing pressures have led us to pare back certain services and also find new ways of doing things. This is illustrated, for instance, by the development of automated press searches which we now run. Some of these work well, some don’t. We have an enquiry service rota system. This used to be paired up with two staff but no longer. We are running at capacity, and illness and holidays do cause problems. (Legal) In terms of staffing numbers we now have nine members of the information team. This was 10 but we lost a post. Some staff have reduced their hours but we’re hoping that they will come back to full-time and therefore increase our capacity. (Technology) We’ve increased our headcount by two posts, up to 12 FTEs, during the year following a review. This is a small step recognizing the pressure we have been under given the growing workloads. We appointed these new staff via an employment agency and they are on rolling contracts. We are thin on the ground at the centre in terms of what we’re trying to do. (Business Services) IS is made up of four staff manning the four service points globally. We have lost two staff in the past couple of years because of company-wide pressures on headcount but made up some of this capacity by increasing the hours of some of the part-time staff. But staffing is down a little overall. This doesn’t reflect doubts about the efficiency and importance of the Information Service which is highly regarded throughout the Company. The service delivery has been impacted by this reduction in capacity. We have had to make decisions on priorities and find smarter ways of doing things. But I am concerned about the long-term effects on the service and have made this clear to my management. (Energy) I have five staff, as last year, but we have added a three-days a week administrator. I’m really pleased with this development and it has made a big difference. The company lost an IT trainer a few years ago and now this post has been filled by a two-days a week trainer and a precedent administrator in K&I. We justified this by a KM argument about capturing more efficiently the internal know-how. Labelling it ‘information’ would have made the task of getting it approved much harder. Compliance work is important for us but I have only a day a week input from a compliance officer. (Legal) I have no staff so I continue to work as a ‘one man band’. Just one good additional person would make a huge difference. There’s a real growth in the demand for business information and if I had the time and the tools then I could make a real impact. Every day I feel that I’m working out of my comfort zone. (Legal) I have 11 staff in London and there are 30 in the information centre in New York. In addition, of course, we have the offshore operation. The focus in London and New York is the more complex, non-standard work (20 per cent of the total) whereas the high volumes are handled offshore by the outsourcing company. The latter makes up around 80 per cent of the overall volume of our work. (Bank) We lost posts a couple of years ago and the remaining staff have had to pick up the extra work. This has rather stunted personal development as there is no time left for this. But the streamlining of processes in the last 24 months is beginning to free up time. Our staffing is very stable with most of the incumbents being here for many years. This obviously has major benefits but it would be healthy to inject a new freshness with a new professional or two. (Pharma) One of the principal ways that we add value for the Bank is through deep integration of our information staff. Pretty much everybody is embedded in business units or associated closely to business teams. Most of our staff have been here with us for a long time and there are very good team affiliations. They are also well connected into the business which can never be underestimated. However, we do have to be mindful of the problem of these staff ‘going native’ but in practice that hasn’t happened. (Bank) A large chunk of our work has been to embed information staff in the business function. The analyst is a real asset and part of the research process, a core function of the company. We need to proceduralize this embedding and although we’ve gone some way this is not as extensive as I would want. A big concern for us is that the staff might go native in the business/research/consulting units. (Technology) Half of my staff are out in business units. We’re keeping this under review as there is a business case for keeping them there and another for centralizing them more fully. The more experienced staff are embedded. There’s always a danger of them ‘going native’ so we have to manage that issue by keeping them involved in more centralized projects and developments. If we incorporate them in mixed teams then it’s less likely that they’ll be lost to us. (Business Services) We’ve been rather successful in increasing the headcount in this last year. It’s modest but there are three more posts globally in Information and Knowledge Services. Our staff are based in central locations rather than embedded in business units. It is the responsibility of our engagement managers to work with business units to ensure that we supply the right services to them. We believe that the centralized model works best for us because it allows us to process higher volumes of work and it’s of a higher quality. (Legal) On the resources front we have done well overall with budgets, 10 per cent up over the previous year. The staffing is stable and, apart from a current maternity cover, the numbers are even and sustainable. Of course, there is a phenomenal difference in the costs between staff in regional cities on the one hand and in London on the other. There is a rebalancing of the job market going on. We have to pay a lot more money now for good people. Perhaps inevitably there is a flow of jobs and people to London so attracting good candidates in the regional offices is much harder. (Legal) There’s no particular pressure on my staff numbers and this is very stable. Personally, I’m still involved in the quite separate ‘people development’ initiative. [This is part of my exit strategy and succession planning as I have been able to progress the leadership development of other LIS staff]. The project is currently a two-year half-time secondment and is likely to be renewed. Part of my role in this is to ensure that staff are engaged with the company’s R&D strategy. I run engagement sessions, meeting with globally distributed staff face to face to discuss the company’s overall strategy. These are then cascaded down through the company. The assessment of this programme has been very positive, with 80 per cent of participants rating it as such. (Pharma)

Skills development

Question 6: When considering the present and future of your information service, how are you addressing the need for new skills in your staff team?

In this year’s Survey we added a new question to specifically address the skills area. Of course, this interest is partly generated by service developments, partly by the speculation about more work in analysis and big data projects.

We have stable numbers of staff. The skills requirements are changing somewhat and it will be increasingly necessary to embrace more analytical skills in the digital library world. This is possibly our biggest challenge to update skills in preparation for a rather different role in the future. In fact, I believe that we’re quite good at identifying and responding to skill gaps. We’ve developed capacity and expertise in patents, chemicals and bio fuels – and these areas require different expertise. We have to become less reactive and more proactive. The Library Services here have already made that switch through the use of digital techniques and tools. The research area needs to follow. (Energy) The skills requirement has changed and will continue to change. For instance, we run the corporate intranet which is a good thing but takes up a lot of time. This may or may not stay with the information team long-term. It might be more sensible to deploy a technical person in this role in the future. We invest heavily in technology, for instance in cloud-based CRM systems. We have a content management system made up of mainly our own publications. We have the intranet which is less key than it was previously. So we need a range of technical skills to be able to maintain these systems and develop them in the future. Any new recruit has to be able to communicate well. We use interns, new graduates, but they are often poor in certain respects. We need our staff to be confident in meetings, to be able to express themselves clearly. We have one very competent member of staff who is pretty much mute in meetings. We need staff who will raise their heads above the parapet. So information management graduates who are attracted to a company like ours have to have lots of skills not covered in the conventional information science/management curriculum. I become very dispirited when I look at the products of information management courses. Recently we appointed two interns from one of the major schools. They showed little interest in the commercial world even though if they had proved themselves in our environment they would have put down a marker for possible employment in the future. Many graduates from the schools seem locked into a public or academic library career. It seems extraordinary to me that in a regional business centre which has relatively few large information teams there aren’t more candidates with the necessary commercial skills mix that we need. Many seem utterly unprepared for this business world. (Technology) On the skills front I think we have to revisit professional education. Whilst the products of our postgraduate courses in information work are competent at traditional information skills, they lack the capacity for real critical thinking. (Legal) The types of professionals that we now appoint are non-traditional. Many of them are embedded in business units and need to be very commercial, confident, outgoing and can market themselves within the company. These are not easy to find in the current recruitment market. (Business Services) We are interested in the very fashionable role and function of ‘data scientist’. We do need to enhance our analytical skills. We are responsible for a massive amount of data in our online library. We might be able to handle this more effectively with enhanced data analytic and maybe some rudimentary programming skills. This would at least enable us to have more confidence and influence when working with our IT colleagues. (Energy) The information service has embraced global tasks including, for instance, producing sector newsletters, the kind of work that was undertaken in the past by analysts. The skill mix in London has to be carefully balanced but there is no doubt that this needs to change. We need to upskill some of our staff, particularly in sectors specialisms. This is hard stuff because they need in-depth sectoral knowledge to add real value. It has to be remembered that we are a small team in a big operating bank. We don’t have ‘data geeks’ in the information centre. We have to be careful about what work we can sensibly expand into, what skills we have and what skills we don’t have nor could ever have. (Bank) There has been a delay in recruiting these [two new] posts, but that is because we have struggled to find appropriate people. I’m not sure if this is because we’ve been too fussy or maybe we’re not paying enough. My general observation is that good people are tending to stay in their posts rather than looking for moves. Or perhaps there are ‘pipeline’ issues given the loss of so many information sector posts in the past five years. We look for professionals who are very commercial in their outlook, interpersonally confident people who can easily make connections across the business. (Financial Services) Traditional library/information skills of the staff were adequate in the past. But the game has changed in the last 18 months. We need staff now to be more creative and with greater analytical skills if we are to meet our five-year plan. We have made an investment in text and data mining and we need to do more of this in the future. The competitive intelligence work is now outsourced and is produced in packaged form. In this context the primary research is wholly outsourced whilst some secondary analysis is carried out internally. (Pharma) In terms of the skills that I require for this new procurement job, all I can say is that I’ve been willing to embrace this difficult transition and to find interest in it. Managing subscriptions with lots of variables make the job interesting, more interesting than many I have done. (Bank) The last information officer whom we recruited had experience in legal information but not in a corporate context. Legal experience is certainly useful and is more important than information searching skills. These can be learnt on the job. As you would expect, we work under acute time pressures. (Legal) If and when I’m in a position to recruit staff I will be looking for a broad range of skills. Whilst some background in the legal sector would be useful, that isn’t critical. Personal skills are much more important – speed, accuracy, commercial awareness and, increasingly, analytical skills. (Legal) There is a very close connection now between investment banks and risk management. This has never been more sensitive. And the role of information in decision-making is particularly interesting in this climate. For instance, there was a recent multi dollar deal that the Bank was involved in negotiating, that only a handful of people knew about what was going on. So we have a regular tension between transparency and high commercial sensitivity and security. This creates another level of complexity for anybody involved from the information research side who is caught up in contributing to such deal making. (Bank) We do need to enhance the skills of our staff and a major investment in our people is needed. The biggest challenge is a cultural one. We used to focus on operational work but we have to raise our aspirations beyond day-to-day targets. We need a different mindset if we’re to cope and flourish in this changed environment. For instance, there is increased pressure on embedded information and research staff as bankers in the business units face their own changing demands. In summary then we need both to develop skill sets in staff and secondly to implement cultural change. (Bank) There’s no perceived need for a substantially changed skill set in our staff. But we could always do with more sector-specific resource support. (Bank)

Service developments

Question 7: What service developments do you see as particularly noteworthy in the last year?

This question is intended to elicit specific examples of the ways in which our respondents have unveiled new services or are re-thinking previous offerings.

The first of these outlines an important methodological issue:

One of the company’s strategic priorities is to simplify its operating model by reducing complexity and thereby becoming more efficient. I think we’ve gone as far as we can on the consequent ‘simplification’ of processes and services. There is now an increasing emphasis on ‘service management’, a structured methodology used by the company to address key challenges. This brings the service owner together with other stakeholders, especially the customer, backed up by detailed performance metrics. We then take action on the results which may include a serious escalation of change. This is similar to a ‘Gemba’ approach, a Japanese concept that means ‘the real place’ and is intended to get you to the location where something is really going on in the business. It requires a deep curiosity to know what is really going on in the company. Not what you assume is going on, or what you heard is going on, but what is really going on. So we spend time with customers and try to understand the business in much greater depth. I’ve been spending periods of time with each customer group. The core library service can be described as ‘broad and shallow’. The competitive intelligence work has shifted from the Library & Information Service to elsewhere in the business. Some synergies have been lost as a result but, for the company overall, more gained. (Pharma) We issue Westlaw alerts to selected lawyers and used to do more of this. However, we didn’t judge this to be delivering sufficient value to be worth the effort. We have to be strategic and hard-nosed in deciding where to put our limited and precious staff time. For instance, at one stage we carried out a great deal of background work for tenders that the company was bidding for. This proved far too speculative so we’ve rationalized it. The company is much more selective and focused now in such bids. If we don’t think we have a very good chance of winning then we don’t bother. There has to be a serious estimate at the likely return on the investment made. (Legal) I talked last year about ‘matter management’ which is concerned in law firms with the organization of information about documents and email, time worked or billed, people inside and outside the firm associated with case, deadlines, files, and similar. At the moment there is an example of my Knowledge and Information team contributing to a major project for a government agency. This will involve us working directly with the client, constructing a suite of pages on our intranet and then establishing and organizing procedures for the project. This and the central management and quality control of precedent documents for the project will be one of the biggest ventures that my team have undertaken. In another project for an educational agency we are modelling and setting up processes and frameworks which involve a lot of people across the company. We’re getting a solid reputation for undertaking such work and this helps us to be very integrated into the heart of the company’s legal business. Our document standards work in which we invested a great deal of time a couple of years ago has taken a back seat of late. With the company going through re-branding and incorporating these small companies into the mainstream, all the previously established formatting standards and templates have to change to the new house style. This has created a huge backlog of work which is being tackled by our new part-time precedents administrator. This is a big learning curve for her as she’s coming cold to legal documents but she’s progressing well. (Legal) We provide a range of desktop information products to our users covering news, companies, patents, specialist areas like venture capital and so on. I undertake some patent work at the margins but also do due diligence checking and, still, traditional information searching for users. I also try to assist my users by pointing people in directions, mining contacts, for instance searches on LinkedIn. Our senior management used to be rather against social media but these attitudes have changed and these are seen much more positively now. Managing my workflow now is more difficult, I have to say. Another development has been for me to undertake a number of pre-meeting briefings of senior staff. I don’t charge out for this work. In comparison, my fee-based work has dropped off slightly. This work is not as major a commitment for me now as it was in the past. However, I still act as ‘one person information/research band’. (Technology) There has been a growth in the company’s business so with pretty much a static staff the workload has increased. We’re adopting more self-service provision for our lawyers to assist with this position. One of our important projects is to upgrade our intranet news coverage through integrating Linex and Nexis; this is a major piece of work. We have a team of three information scientists and IT people working on this project. SharePoint 13 is still the core infrastructure for our intranet. In terms of other social media we’ve just appointed a social media manager within I&K Services. We have already started a pilot project to use Yammer as a collaborative social media system within the company. (Legal) The real pressure point is how we get the greatest leverage on our technologies. We use a variety of media in this respect, from RSS feeds to cuttings in newspapers, all through a standardized current awareness service. We feel we’re slowly getting there. (Legal) We’re in the final stage of deploying a service desk management system which is rather important to us. Interestingly, we had a proposal to spend 10 times as much to do the same thing by consultants. This kind of project is a way of involving staff globally in a common initiative. (Legal) We assess quality in various ways but we’re keen to maintain at least a base level standard. The quality of the reference interview with users in order to determine their needs is fundamentally important. (Legal) The reference interview needs to be more skilfully undertaken. (Energy) The advisory work can be more or less subtle such as asking questions ‘is there a tax consideration here?’ or ‘have you thought about this matter when discussing this project with your client?’ (Financial Services) Training our end-users has become more important in recent years. (Legal)

KM, social media and collaborative technologies

Question 8: What role does knowledge management and social media have in your company?

Knowledge sharing is an important cultural value in organizations yet difficult to ‘manufacture’. Perry Hewitt in a HBR Blog Network piece (6 December 2013) described cogently the necessity of rewarding digital knowledge sharing, not hoarding: