Abstract

Leveraged finance is an important market for professional advisory firms such as investment banks, financial sector law firms and the ‘Big 4’ consultancies. As such, researchers and information professionals in these firms are often asked to research the market. This may be to produce a list of leveraged finance deals in a particular industry or jurisdiction, to find the size or composition of the market or to find expert commentary, including predictions for the future. In this article, Ian Hunter explains the ways in which leverage finance is defined, describes the leading sources and highlights some caveats to bear in mind when relying on the sources.

Introduction

Researchers and information teams in professional advisory firms are often asked to research the leveraged finance market. This may be to produce a list of leveraged finance deals in a particular industry or jurisdiction, to find the size or composition of the market or to find expert commentary, including predictions for the future. In this article, Ian Hunter describes the components of the leverage finance market and the leading sources for researching the market, with some caveats.

What is leveraged finance?

At its simplest, leveraged finance is using borrowed money for an investment. In the corporate world, this could be to buy more physical resources in order to increase output, restructure existing debt on more favourable terms or even to acquire another company. All are done in the expectation that the profit made will be greater than the interest payable on the borrowed money. In the same way, a private individual may take out a mortgage to purchase a residential property in the expectation that the property will increase in value over the lifetime of the mortgage, resulting in a profit.

In the world of finance, most commentaries on the leveraged finance market break the market down into two parts: high yield bonds and leveraged loans.

A bond is a promise by a company (the issuer) to pay an interest rate usually over a set period of years to the buyers of the bond (the bondholders). Governments may also issue bonds, traditionally known as gilts in the UK. A high yield bond is one paying a higher rate of interest. This can be for a number of reasons, including the financial health of the issuer or the characteristics of the bond itself, but essentially because the bond comes with higher levels of risk for the bondholders: if the company goes bust, the bondholders may not get their money back.

A leveraged loan is usually a form of syndicated loan, a loan made to an organization by a syndicate or ‘club’ of lenders. Within the leveraged finance market, leveraged loans are usually identified by either the credit rating of the borrower or the loan itself or the ‘pricing’, the interest rate the company has to pay on the loan. The lower the credit rating or the higher the price, the more likely the loan is to be considered ‘leveraged’. Credit ratings are assigned based on the financial health of an organization, or the loan in question, and generally given by one of the ‘Big 3’ ratings agencies, Standard & Poors (S&P), Moodys and Fitch. A leveraged loan is a loan with a credit rating of Ba1/BB+/BB+ or below, where the Ba1 is the Moodys rating, the first BB+ is the S&P and the second BB+ is Fitch. Ratings are usually written in this format (S&P and Fitch do not always use the same codes for their ratings, but they are the same at this particular level).

Pricing is usually expressed as LIBOR+130, being the number of points above the LIBOR rate. This is the interest rate the company will have to pay. The lower the financial health or credit rating of the company, the more interest it is likely to have to pay. Standard & Poors, for example, would class any loan with a price of LIBOR+125 or above as leveraged (it is possible for the company to be in good financial health but for the characteristics of the loan to make it a riskier proposition for the lenders).

Bonds involving borrowers or issuers in good financial health or loans with a credit rating above Ba1/BB+/BB+ are known as investment grade.

As well as, the overall size of the market researchers may need to know the breakdown by reason for the financing, usually known as ‘use of proceeds’. A company may take out a loan or issue a bond in order to acquire another company (acquisition finance), to refinance its existing debt (refi) or to fund general corporate activities (general corporate purposes). These categories will often appear in reports on the leveraged finance market and are highly valued by practitioners such as law firms and investment banks.

Why research the leveraged finance market?

The leveraged finance market is an important market for professional advisory firms such as investment banks, financial sector law firms and the ‘Big 4’ accountancy firms. Much of the work of these firms is arranging leveraged finance for companies or advising them on the terms. Many companies will want to invest in the leveraged finance market in times of low interest rates as the returns on conventional investment products will be unattractive.

Leveraged finance has arguably been especially important in the years following the global financial crisis of 2008 onwards. Mergers and acquisitions activity (M&A) is usually the key barometer of the health of the global financial economy and reviewing the market size over the last 10 years, leveraged finance recovered more quickly: the low point for both leveraged finance and M&A was 2009, but in both the US and Europe, the leveraged finance market was very healthy by 2013, and in the US, even surpassed the pre-financial crisis high point of 2007. 1 This was probably due to companies restructuring their existing debt in the face of challenging market conditions, and the relative attractiveness of leveraged finance products in an era of very low interest rates.

2015 and 2016 have seen a reduction in the size of the market, possibly due to continuing sluggish activity in the global economy and therefore lack of demand for finance.

Knowledge of the market size and trends allows professional services firms to advise their clients on business strategy, and even to inform their own, for example, should a law firm have more leveraged finance partners based in New York, London or Frankfurt?

Market figures published after each year end by the major publishers such as Thomson Reuters, Dealogic and Bloomberg are therefore eagerly awaited.

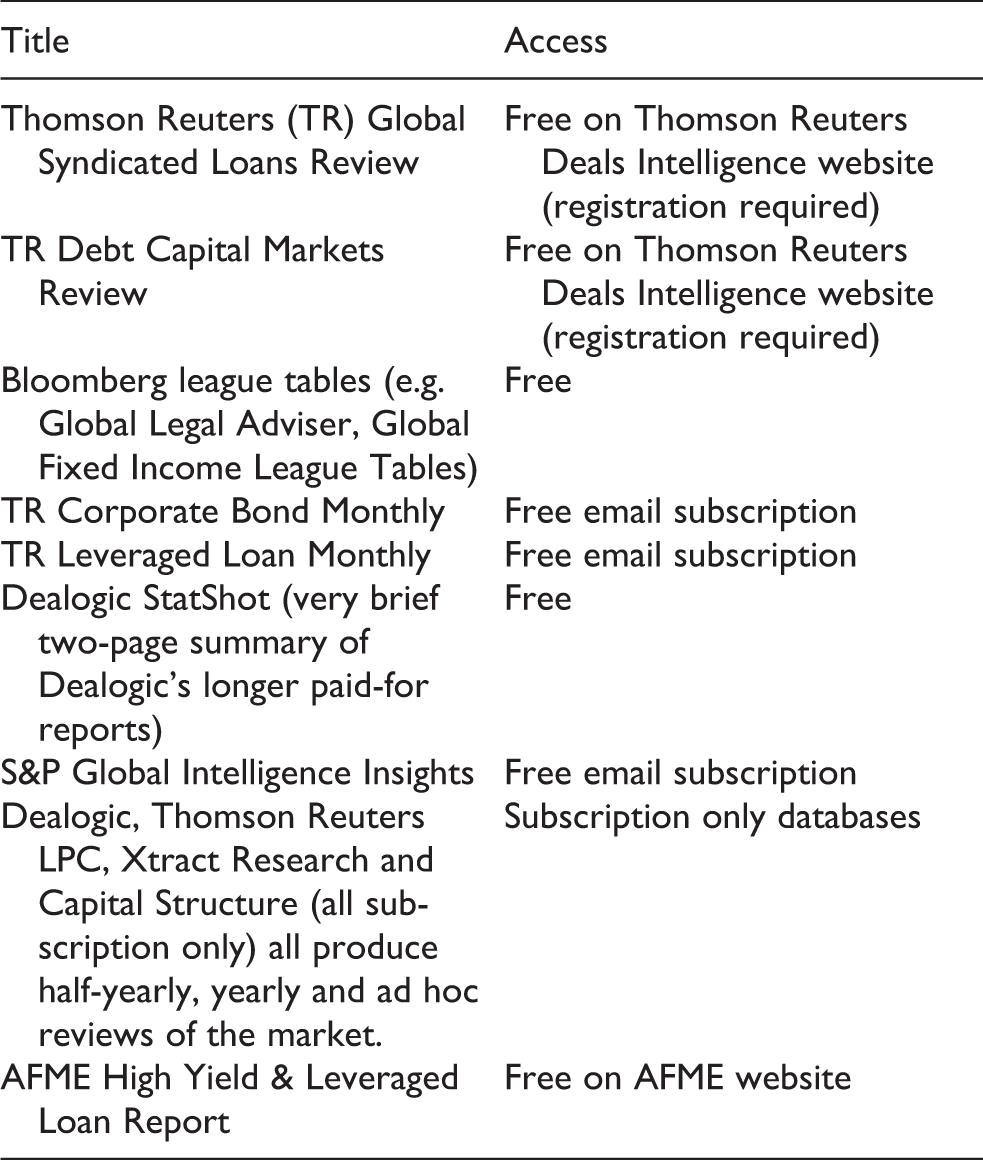

Researching the market size and composition

Publishers such as Thomson Reuters, Dealogic and Bloomberg publish quarterly or monthly reviews, often based around league tables, free of charge on their websites. The league tables show which advisers have advised on most deals. These reviews typically contain a one-page introduction to the league tables for each region which states whether deal levels are up or down on the previous year.

While useful, much of this freely available information is in snippets, for example, a report will break down the totals into high yield and investment grade bonds for the US but not Europe, so trying to get the whole picture from one report can be frustrating.

For more detailed analysis or lists of individual deals, a subscription to one of the publishers’ databases is usually required (e.g. Thomson LPC, Dealogic, Bloomberg, S&P LCD, Thomson One).

The best free source is probably the European High Yield and Leveraged Loan Report. This quarterly report by the AFME, formerly the High Yield Association, contains very detailed data for the European market, including breakdown by use of proceeds. The AFME reports are published later than those by the commercial publishers, however, up to eight weeks after the end of the quarter and cover the European market only.

The table below contains a list of the key sources. These are free unless otherwise stated.

Researching leveraged finance deals

While news on significant individual deals may be freely available via specialist news websites, lists of deals, and the ability to run bespoke lists in a particular industry or region, are generally not. In this case, a subscription to a database is usually necessary.

Thomson One and Bloomberg are possibly the most comprehensive deal databases on the market, containing many thousands of leveraged finance, M&A and other deals. The criteria for inclusion are often loose; however, so many leveraged finance deals included in these databases would not be included in the published reports. This can result in inaccurate numbers of deals and inaccurate figures for market size when using the databases.

It may be safer to use one of the specialist leveraged finance databases such as Dealogic Loan Analytics, Thomson LPC or S&P LCD, where the criteria for considering a deal ‘leveraged’ tend to be stricter. There are also smaller, but often very useful products such as Capital Structure and Xtract Research, which usually contain fewer deals in their database but more information on each one. As a result, they are generally less reliable for market size but useful when searching for examples of specific types of deal.

Reliability of the market data and deal numbers

Publishers differ in their valuations of the market and numbers of deals. This can be frustrating if one publication does not contain all the data required: effectively, it is not possible to use, for example, the European data from the AFME and the US data from a Thomson Reuters publication as total market sizes provided will not be consistent.

More surprisingly, total values obtained from a database search (e.g. Bloomberg, Thomson, Dealogic) often do not match those in the published reports by the same publishers, due to all the editing that goes into the latter. It is not therefore advisable to rely on the market total from a published report and then obtain the country or use of proceeds breakdown from the database, even if the database is produced by the same publisher.

Finally, we have already noted that the more generalist databases such as Thomson One and Bloomberg are almost too comprehensive: they can be useful for generating lists of deals but should be used with caution when looking for market size.

Researching market trends – Finding commentary and analysis

Among the leading journals in this area are International Financial Law Review, International Financial Law Review and thirdly Global Capital (formerly Euroweek; all subscription only). These journals include news on significant deals and trends in the market, and in some cases, reviews of the year. The subscription databases such as Xtract Research and Capital Structure usually include analysis in their annual reviews of the market sent to subscribers.

Standard & Poors offer a free email update in the form of a blog on various aspects of the market: search for S&P LCD Insights.

The AFME, Bloomberg and Thomson Reuters league tables and annual reviews do not usually include analysis of trends in the markets or predictions for the future.

Fortunately, for non-subscribers, many professional services firms publish analysis of the leveraged finance market in the form of ‘thought pieces’. While not as detailed as the other publications in terms of data, these reviews usually offer predictions for the future and reasons for trends in the market. As in any other text-based research, traditional information retrieval skills around the use of selecting search terms, Boolean operators and a critical approach to sources come to the fore here. It may be useful to specify the name of a preferred author-firm when searching online for these to avoid too much lower quality content, usually one of the Big 4 consultancy firms or large international law firms.

Conclusion

Leveraged finance has been an important market for many professional services firms and despite the apparent downturn in 2015–2016 is likely to continue to be so, particularly with the current low level of interest rates. At the time of writing, there is no significant data available since the EU referendum of 23rd June so the effects of Brexit remain unclear. The third quarter reports from the big publishers should contain early indications.

While market size is widely reported in free publications from Thomson Reuters and Bloomberg among others, with the exception of the AFME High Yield & Leveraged Loan Report, there is not usually sufficient detail for the needs of most professional services firms. For detailed global comparable figures broken down by region or use of proceeds, a subscription to one of the key databases is usually needed.

Most surprisingly, consistency is an issue: estimates of market size often vary between publishers, and even when using figures from the same publisher, totals may differ in the published reports and the database.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.