Abstract

This research attempts to identify the factors leading to the adoption of mobile banking and the degree of influence of each one of the factors in Thailand. It proposes a comprehensive framework that extends the existing UTAUT model with important constructs such as perceived credibility, perceived cost, and perceived convenience. A three-pronged approach, consisting of an extensive review of the literature, expert interviews, and a field survey of mobile banking adoption is put forward. A field survey of respondents was undertaken with both convergent and discriminant validities being conducted. The results of the structural equation modeling show that performance expectancy, effort expectancy, social influence, perceived credibility, perceived convenience, and behavioral intention to use mobile banking posited a positive relationship. Contrary to previous studies, the hypotheses testing perceived that financial cost and facilitation conditions in the adoption of mobile banking were not supported. Discussions and conclusions including academic and practical implications are also presented.

It is important for banks and mobile application developers to understand the behavior of consumers.

Introduction

In recent years, the ease of use and widespread availability of mobile communication has led to its phenomenal growth in both rural and urban areas, especially in many developing countries in Asia (Mishra and Bisht, 2013). Thanks to technological advances in the past few years, the ways that financial services are transacted have changed dramatically. Mobile banking is the latest development in this arena, that allows consumers to check account balances, make payments, transfer money, or even find ATM locations using smartphones or other portable computing devices (Oliveira et al., 2014). This has been possible because of the convergence of several factors such as the Internet, wireless technologies, and mobile devices, which has led to this new paradigm of information technology (Luo et al., 2010).

Market analysis indicates that despite the benefits that mobile phones or tablets offer in conducting mobile transactions and accessing financial information, the use of mobile banking is not as widespread as expected (Dineshwar and Steven, 2013), and that has been documented by reports from Accenture (2013). A recent report by Juniper Reports (2013) predicted that by 2017 more than 1 billion people will use mobile banking. This suggests that there is room for significant growth opportunities as the number of mobile banking users is expected to increase. However, the number of users reported by Juniper Reports represents only 15% of the worldwide mobile subscription base (Shaikh and Karjaluato, 2014). The use of mobile banking services is lower than expected (Cruz et al, 2010) and it remains one of those technologies that are still underused (Huili and Chunfang, 2011). Despite the availability of mobile banking and its potential growth capabilities, the above mentioned figures show that further investigation into the adoption of mobile banking is needed (Shaikh and Karjaluato, 2014).

In Thailand, Bangkok Bank, Krung Thai Bank, Kasikorn Bank, and Siam Commercial Bank, which are the country’s top four banks ranked by assets, have developed mobile banking services . However, the adoption of mobile banking by users (4.5% of the population) is much less than the adoption of mobile instant messaging (40.08%), mobile games (46%) and mobile search (11.44%) (Bank of Thailand, 2014; MarketingOops, 2014; Veedvil, 2013; IT24HRS, 2012). The low rate of mobile banking adoption makes it even more important to understand the reasons why users adopt mobile banking. This paper therefore attempts: to identify the factors leading to the adoption of mobile banking in Thailand to identify the degree of influence of each one of the factors leading to the adoption of mobile banking in Thailand.

An extensive review of the literature found little research on mobile banking in the developing countries that form the Association of South East Asian Nations (ASEAN). There is a lack of research using both qualitative and quantitative methods, as well as a lack of research on mobile banking that compares its adoption from an occupational perspective (e.g., by full-time employees and students). This paper aims to close such gaps in the literature and make the following contributions: a comprehensive model that extends the existing UTAUT model with important constructs such as perceived credibility, perceived cost, and perceived convenience a three-pronged approach, consisting of an extensive review of the literature, expert interviews, and a field survey of mobile banking adoption an empirical view and insight for media companies, banks, and even policy makers into the mobile banking adoption behavior of customers/citizens.

This paper is presented as follows: the next section provides an extensive literature review of the UTAUT model and the extended variables, followed by sections on research methodology – including the proposed research model and hypotheses – data analysis and results, discussions, conclusions and recommendations.

Theoretical background and research model

Unified Theory of Acceptance and Use of Technology (UTAUT)

Users’ acceptance of technology has received a great deal of attention since the introduction of information systems into organizations. Researchers and practitioners alike are interested in determining the factors that affect users’ beliefs, attitudes, and their resistance towards technology acceptance (Lee et al., 2003). The past two decades have seen many studies which have provided theoretical frameworks and models regarding the acceptance of information technology (IT) and information systems (IS). The Technology Acceptance Model (TAM) is the most common theory employed for describing individuals’ acceptance towards information systems (Lee et al., 2003). Other popular predictive models are the Theory of Reasoned Action (TRA), the Theory of Planned Behavior (TPB), Social Cognitive Theory (SCT), and the Extended Technology Acceptance Model (TAM2).

Although these theories have made significant contributions to the study of IT adoption, they have some limitations. First, though the theories use different terminologies, they are basically explaining similar concepts. Secondly, behavioral research is very complex and a single theory that covers all or most of the factors does not exist. This suggests that each of these theories has weaknesses and that they do not complement each other (Qingfei et al., 2008). Researchers tend to pick and choose constructs from different models or choose a model that they favor, ignoring constructs from other models that could contribute to their study. As a result, the existing models need to be reviewed and synthesized so that a unified model can be arrived at (Venkatesh et al., 2003).

The Unified Theory of Acceptance and Use of Technology (UTAUT) shown in Figure 1 was introduced by Venkatesh et al. in 2003. Their objective was to integrate the fragmented theories and research on acceptance of information technology, and on individual acceptance, into a unified theoretical model. This included the study of eight previously established models which were empirically compared using longitudinal data from four organizations over a 6-month period with three measurement points. The UTAUT was then confirmed with two organizations’ data with similar results (Venkatesh et al., 2003). The eight previously established theories included the TRA, TAM, the motivational model (MM) (Davis et al., 1992), a model combining TAM and TPB (C-TAM-TPB), (Taylor and Todd, 1995), the Model of Personal Computer Utilization (MPCU) (Thompson et al., 1991), the Innovation Diffusion Theory (IDT), and SCT. The end result was the formulation of UTAUT, which theorizes that four constructs play a significant role in determining user acceptance and user behavior, namely, performance expectancy, effort expectancy, social influence, and facilitating conditions (Venkatesh et al., 2003). The integration of as many as eight theories makes the UTAUT model one of the most comprehensive and important theories for explaining IT adoption (Qingfei et al., 2008).

Unified Theory of Acceptance and Use of Technology (UTAUT). (Source: Venkatesh et al, 2003)

Of the four predictors, performance expectancy is the strongest predictor of attitude toward use and behavioral intentions (Jeng and Tzeng, 2012). Effort expectancy is vital towards the introduction of new technology. If technology designers fail to take into consideration the factors related to ease of use then the adoption process of the new technology can be constrained (Orlikowski, 1992). In the UTAUT model, social influence acts as a direct determinant towards the use of the system, while behavioral intention represents subjective norm and image (Jeng and Tzeng, 2012). Facilitating conditions have been validated by Venkatesh et al. (2003) as a direct determinant of usage behavior of a new technology.

Performance expectancy, effort expectancy, and social influence each have a direct effect on behavioral intention, while facilitating conditions and behavioral intention have a direct effect on usage behavior. Gender, age, experience, and voluntariness of use form the moderators of the model. Previous models were able to explain approximately 40% of technology acceptance, whereas UTAUT was able to explain 70% of the intention to use technology (Venkatesh et al., 2003).

Although TAM has been used more frequently and more widely, UTAUT has gradually drawn the attention of researchers and has been applied to various technology acceptance studies and different types of users in different countries (Zhou et al., 2010). Examples of these studies include: factors explaining the acceptance, actual use and satisfaction of nurses using an electronic patient record in acute care settings (Maillet et al, 2014); understanding Internet banking adoption (Martins et al., 2014); exploring the determinants of home healthcare robots adoption (Alaiad and Zhou, 2014); understanding website design quality and usage behavior (Al-Qeisi et al, 2014); and investigating the critical factors for cloud based e-invoice service adoption (Lian, 2015). The findings of these studies clearly indicate that the UTAUT model is applicable to people of different genders, levels of IT competency, and cultures, and to a wide variety of technologies, thereby indicating its reliability. The UTAUT model thus provides a useful tool in understanding the possibility of success for new technology introductions. It also helps to understand what the drivers of acceptance are, especially among users who are less likely to adopt and use new technology (Venkatesh et al., 2003).

Mobile banking and the UTAUT relationship

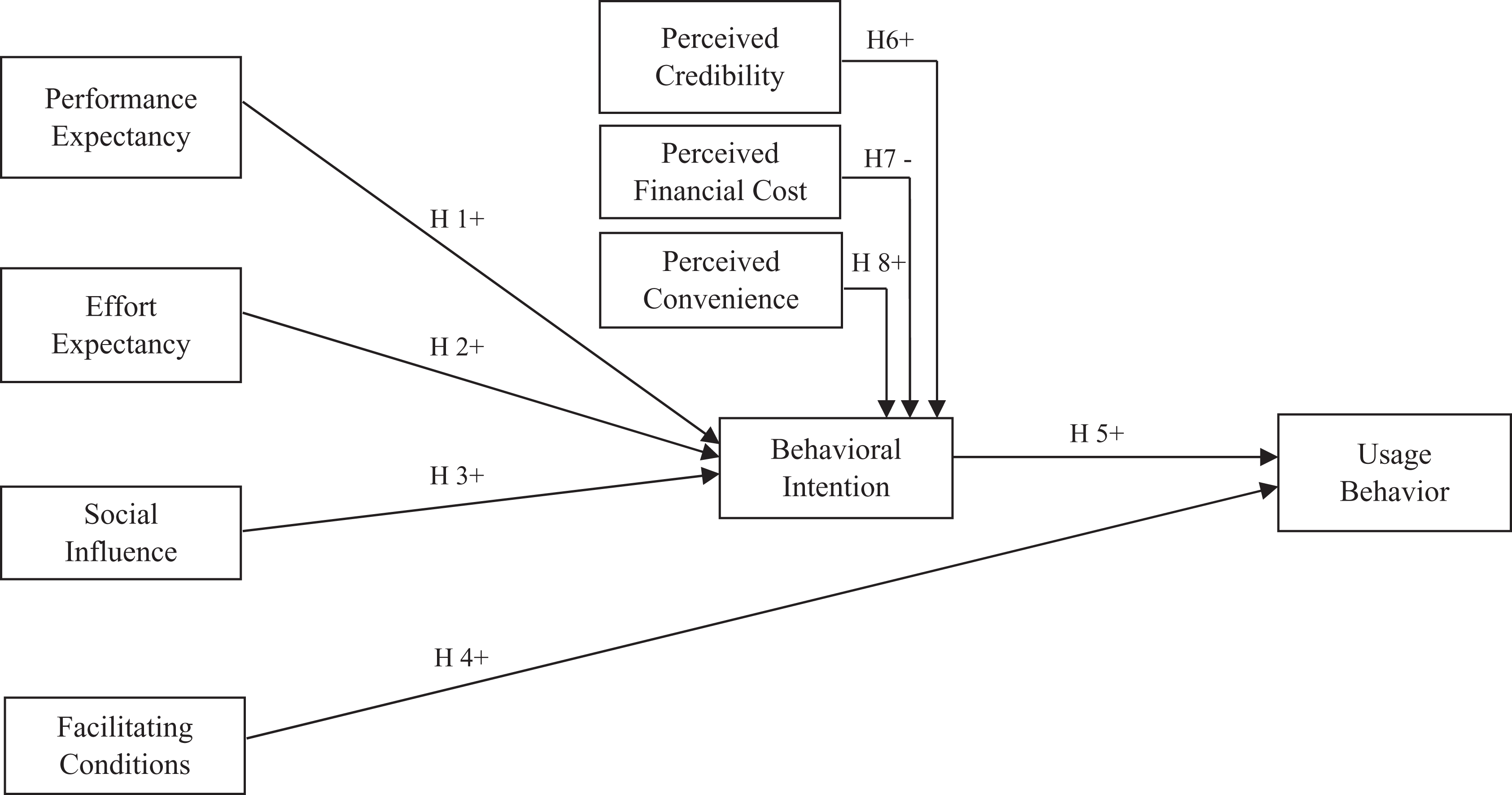

Performance expectancy is defined as “the degree to which an individual believes that using the system will help or her to attain gains in job performance” (Venkatesh et al., 2003). Performance expectancy combines constructs from five different models, namely, perceived usefulness from TAM/TAM2 and C-TAM-TPB, extrinsic motivation from MM, job fit from MPCU, relative advantage from IDT, and outcome expectations from SCT (Venkatesh et al., 2003). In several previous studies, performance expectancy was found to have a positive relationship with behavioral intention. Examples include: predicting uptake of technology innovations in online family dispute resolution services (Casey and Wilson-Evered, 2012); exploring mobile banking adoption (Oliveira et al, 2014); and examining online ticket purchasing for low cost carriers (Escobar-Rodriguez and Carvajal-Truzillo, 2014). The positive relationship was also confirmed by Venkatesh et al. (2003). In the context of mobile banking, performance expectancy reflects the perception of users on convenient payment, fast response, and the effectiveness of the service (Zhou et al., 2010). This study therefore proposes the following hypothesis:

Effort expectancy is defined as “the degree of ease associated with the use of the system” (Venkatesh et al., 2003). Three constructs from three existing models explains the concept of effort expectancy, namely, perceived ease of use from TAM/TAM2, complexity from MPCU, and ease of use from IDT (Venkatesh et al., 2003). A positive relationship between effort expectancy and behavioral intention was confirmed by several studies, such as: predicting the uptake of technology innovations in online family dispute resolution services (Casey and Wilson-Evered, 2012); examining online ticket purchasing for low cost carriers (Escobar-Rodriguez and Carvajal-Truzillo, 2014); and examining the factors that affect the acceptance and use of interactive whiteboard (Tosuntas et al, 2015), as well as by Venkatesh et al. (2003). As regards mobile banking, users will use it if they perceive it to be easy to use and if interacting with it is clear and understandable. The following hypothesis is proposed for this study:

Social influence is defined as “the degree to which an individual perceives that important others believe he or she should use the new system” (Venkatesh et al., 2003). Social influence is characterized as subjective norm in TRA, TAM2, TPB/DTPB, and C-TAM-TPB, as social factors in MPCU, and as image in IDT (Venkatesh et al., 2003). Previous studies by Yu (2012) on mobile banking adoption, Thomas et al. (2013) on mobile learning adoption and Escobar-Rodriguez and Carvajal-Truzillo, (2014) on examining online ticket purchasing for low cost carriers, concluded that there was a positive relationship between social influence and behavioral intention. This was also proposed and confirmed by Venkatesh et al. (2003). In the case of mobile banking, users will use it if they are influenced by environmental factors such as their friends, relatives, or superiors’ opinion (Zhou et al, 2010). Thus, the following hypothesis is proposed:

Facilitating conditions are defined as “the degree to which an individual believes that an organizational and technical infrastructure exists to support use of the system” (Venkatesh et al., 2003). Facilitating conditions combine constructs from four different models namely, perceived behavioral control from TPB/DTPB and C-TAM-TPB, facilitating conditions from MPCU, and compatibility from IDT (Venkatesh et al., 2003). A positive relationship between facilitating conditions and usage behavior was confirmed by several studies, such as the adoption of information services (McKenna et al., 2013), the adoption of mobile banking (Oliveira et al., 2014), and examining factors that affect the acceptance and use of interactive whiteboards (Tosuntas et al., 2015), as well as by Venkatesh et al. (2003). For mobile banking, if users believe they have the knowledge and resources necessary, they will use it. Behavioral intention was also found to have a positive relationship with usage behavior in studies exploring the adoption of mobile banking (Yu, 2012; Oliveira et al., 2014), and technology acceptance by health care professionals (Ifinedo, 2012). Therefore, the following hypotheses are proposed:

Mobile banking and the extended variables

Perceived credibility is defined as the “users’ perceptions of credibility regarding security and privacy issues” (Wang et al., 2003). Previous studies by Dasgupta et al. (2011) on behavioral intentions towards mobile banking usage, Yu (2012) on the adoption of mobile banking and Jeong and Yoon (2013) on acceptance of mobile banking services concluded that there was a positive relationship between perceived credibility and behavioral intention. In the context of this study, users will be more likely to adopt mobile banking if they perceive that it can allow them to securely conclude transactions and also does not reveal their personal information (Luarn and Lin, 2005).

Perceived financial cost is defined as “the extent to which a person believes that using mobile banking will cost money” (Luarn and Lin, 2005). In information systems acceptance studies, economic motivations and outcomes are often the focus (Luarn and Lin, 2005). Previous studies have found that perceived financial cost significantly affects behavioral intentions. Examples of these studies include mobile banking adoption (Sripalawat et al, 2011), factors affecting individuals adoption of mobile banking (Yu, 2012), and adoption of mobile content service in the 3G era (Huang at el, 2012). Users will be reluctant to adopt mobile banking if they perceive that it would cost a lot of money or impose a financial burden on them. The following hypothesis is proposed for this study:

According to Brown (1989), convenience can be proposed to have five dimensions, namely, time, place, acquisition, use, and execution. The time and place dimensions look at the time and place that are convenient for a user to use the product. The acquisition and use dimensions focus on the ease in acquiring the product and the convenience in using it, while the execution dimension looks at providing the user with the product (Brown, 1989). Previous studies by Jih (2007), on convenience on shopping intention in mobile commerce, by Hossain and Prybutok (2008), on consumer acceptance of RFID technology, and by Chang et al. (2011), on continuous English learning intention in a mobile environment, also found a positive relationship between perceived convenience and behavioral intention. Users will be more likely to adopt mobile commerce if they feel that it can help them conclude transactions at any time, in any place, and is easy to acquire and easy to use. Thus, the following hypothesis is proposed for this study:

From the extensive literature review and from the advice from experts in the qualitative interviews, this study proposes the research model and hypotheses shown in Figure 2. The next section provides a detailed explanation of the characteristics of the experts.

Research model and hypotheses.

Research methodology

This study proposes a three-pronged approach comprising (1) an exhaustive review of the literature, (2) interviews with experts from the industry, and (3) field surveys, to propose a model of user adoption of mobile banking in Thailand by integrating the existing UTAUT model with three external variables. The review of the literature offers useful insights, but may contain certain bias that makes it weak. Expert interviews provide an insight on real-world situations that may not be found in the literature (Spiggle, 1994). Even though the expert interview is extremely useful, it may still contain bias as different organizations differ in terms of culture and environment. The interviews were conducted solely for the purpose of verifying the research framework prior to conducting the survey. That is when field studies are important, because they use a large number of respondents who use models and hypotheses that can be verified statistically. The three-pronged approach provides a balanced point of view from different sources that complement each other, thereby aiming to eliminate bias in the study (Chanopas et al., 2006).

Qualitative method

Experts in the field of mobile banking were interviewed in order to gain a better understanding of mobile banking acceptance and usage among users in Thailand. The experts were chosen from the banking sector as well as from universities and research institutions. The rationale was to get a composed view from industry experts as well as experts in academia. The interviews took place between December 2013 and February 2014. Each interview session lasted from 45–50 minutes. The experts were given the questions in advance though email. A standardized open-ended interview approach was used; it is the most efficient qualitative interviewing technique because many interviewers are involved. This interview technique allows for the comparison of the responses from different interviewees (Patton, 1990). Table 1 presents the characteristics and details of the experts.

Characteristics of key experts.

*Large refers to firms that hire more than 200 employees with a fixed asset in excess of $6.25 million

**Medium refers to firms that hire between 51-200 employees with a fixed asset between $1.5 million - $6.25 million

Quantitative method

Instrument

The research model consisted of nine constructs, for each of which multiple items were used for measurement. Six of the constructs reflect the UTAUT model, while the remaining three, perceived credibility, perceived convenience, and perceived financial cost were added to the UTAUT model. The measurement scales for the UTAUT model and the extended variables were adapted and modified from previous studies to fit this study.

For the determinants of UTAUT, performance expectancy is measured by four items (PE1-4), effort expectancy by four items (EE1-4), social influence by four items (SI1-4), facilitating conditions by four items (FC1-4), behavioral intention (BI1-4), and usage behavior by three items (UB1-3), which were adapted from Venkatesh and Davis (2003).

For the extended variables, perceived credibility is measured by four items (PCD1-4) adapted from Luarn and Lin (2005) and Yu (2012); perceived convenience is measured by four items (PC1-4) adapted from Hossain and Prybutok (2008); and perceived financial cost is measured by four items (PFC1-4) adapted from Luarn and Lin (2005) and Yu (2012).

The completed questionnaires were pre-tested among 10 participants to check for language and understanding of the questions. The questions were then modified for clarity as suggested by the participants. Following the pre-test, a pilot test of 24 participants was conducted. A second round of modifications for the questionnaires was made from the pilot test and the reliability of the scales was measured using SPSS 21.

Data collection

Data was collected from two universities in Thailand, Mahidol University International College and Thammasat University, at both undergraduate and graduate levels. In addition, customers at banks and visitors at shopping malls were also approached to complete the questionnaire. The rationale in selecting different types of respondents such as students, retirees, homemakers, and self-employed and part-time or full-time employees was to get a more comprehensive view of the adoption and usage of mobile banking. Convenience sampling was employed in order to gain an adequate sample size for the study. Data was collected from February 2014 to May 2014.

The questionnaire had two sections. Section One contained demographic information about the user, while Section Two asked respondents about their experience in using mobile banking. Respondents were informed that the questionnaire was for mobile banking and not just general Internet banking. The questionnaires took between 10 and 12 minutes to complete. A total of 272 questionnaires were completed. Table 2 presents the descriptive statistics of the respondents.

Demographic data of respondents.

Data analysis and results

The two-step approach recommended by Anderson and Gerbing (1988) was used in analyzing the data. The first step is to perform the analysis of the measurement validity, while the second is to analyze the structural model to test the proposed model as well as the hypotheses.

Analysis of measurement validity

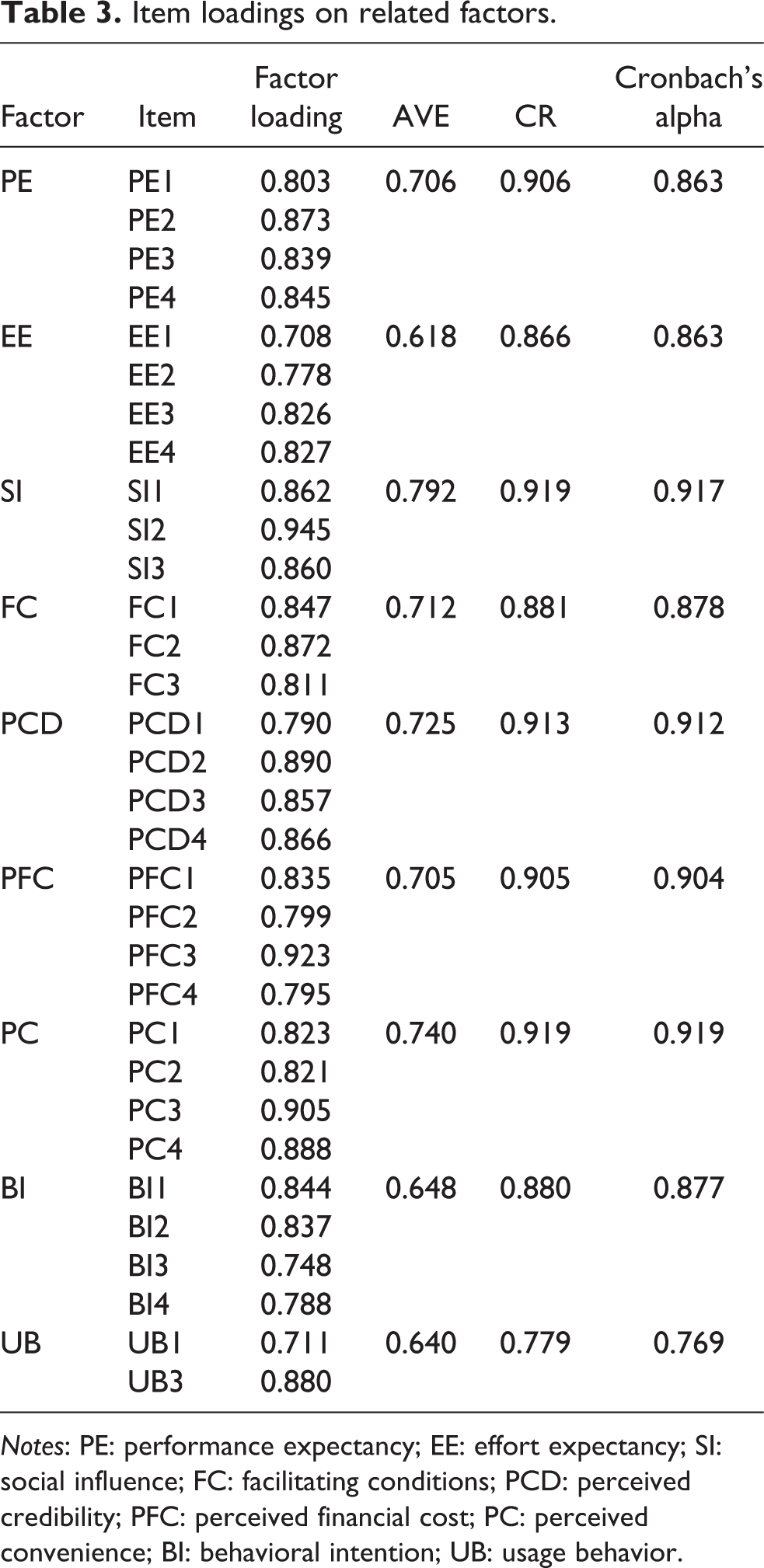

Construct reliability and validity were conducted to test the reliability of the scales using Cronbach’s alpha. The values for Cronbach’s alpha for all the constructs ranged from 0.769 – 0.919, and thus were above the threshold value of 0.70, which indicates the reliability of the scale (Nunally, 1978; Hair et al., 1998). Exploratory factor analysis (EFA) was then undertaken with Principal Component Analysis (PCA) and Kasier’s Varimax Rotation. The Kaiser-Meyer-Olkin (KMO) was found to be at 0.89, which is above the recommended value of 0.80 (Kaiser, 1970).

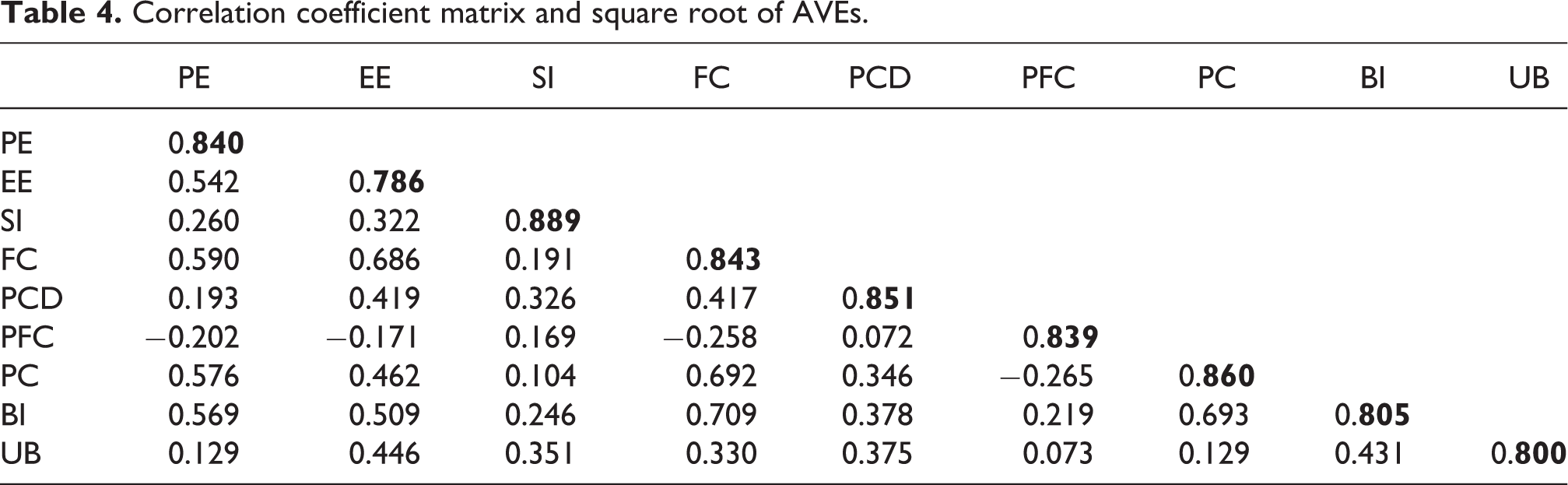

Confirmatory factor analysis (CFA) was then performed. Hair et al. (1998) suggested that factor loadings should be above 0.50. All of the factor loadings except for three items were above the recommended value. These three items, (SI4) from social influence, (FC4) from facilitating conditions, and (UB2) from usage behavior, were removed because of low factor loadings. Furthermore, the composite reliabilities (CR) and average variance extracted (AVE) for each construct were recorded at the recommended value of 0.50, which suggests good convergent validity (Fornell and Larcker, 1981). A summary of the CFA is presented in Table 3. To test for discriminant validity, the square root of the AVE and its correlation with other factors were compared. Table 4 shows that the square root of the AVEs is greater than the correlations between the constructs, suggesting good discriminant validity (Fornell and Larcker, 1981).

Item loadings on related factors.

Notes: PE: performance expectancy; EE: effort expectancy; SI: social influence; FC: facilitating conditions; PCD: perceived credibility; PFC: perceived financial cost; PC: perceived convenience; BI: behavioral intention; UB: usage behavior.

Correlation coefficient matrix and square root of AVEs.

Model testing results

Analysis of Moment Structures (AMOS) 21 was used to test the path as well as the hypotheses proposed in the model. According to Gefen et al. (2000), AMOS is specifically designed for structural modeling (SEM) as well as path analysis. SEM was chosen as the primary tool for testing the model because unlike linear regression or ANOVA, the relationships between multiple independent and dependent variables can be accomplished simultaneously (Gerbing and Anderson, 1988). Table 5 shows the fit indices. The X2/degree of freedom is 1.74, CFI is 0.95, GFI is 0.85, AGFI is 0.82, IFI is 0.95, RMSEA is 0.05, and TLI is 0.94. All the fit indices, except for GFI, are within the recommended values as suggested in the literature. This suggests that the model fits the data well.

Goodness-of-fit measures of the research model.

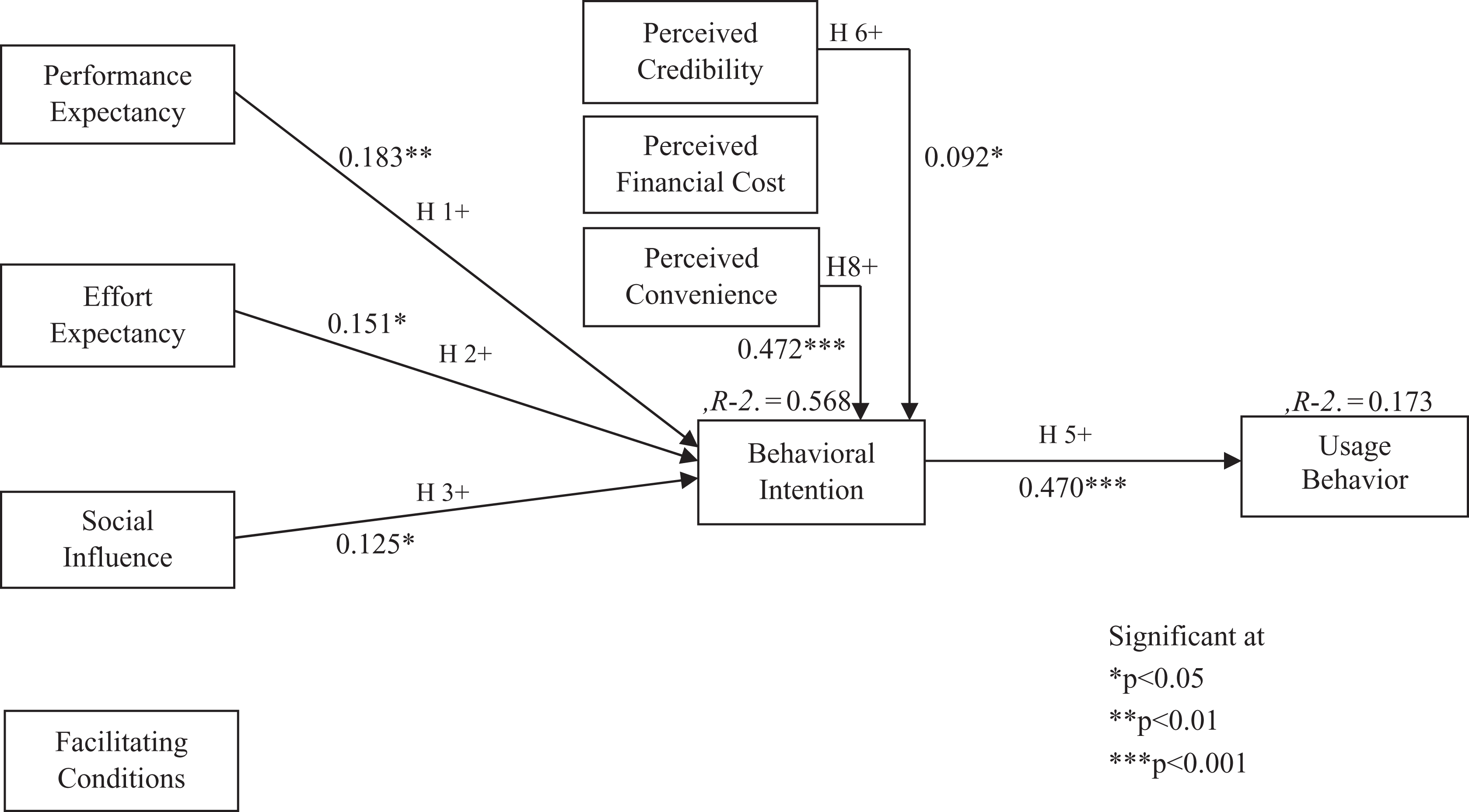

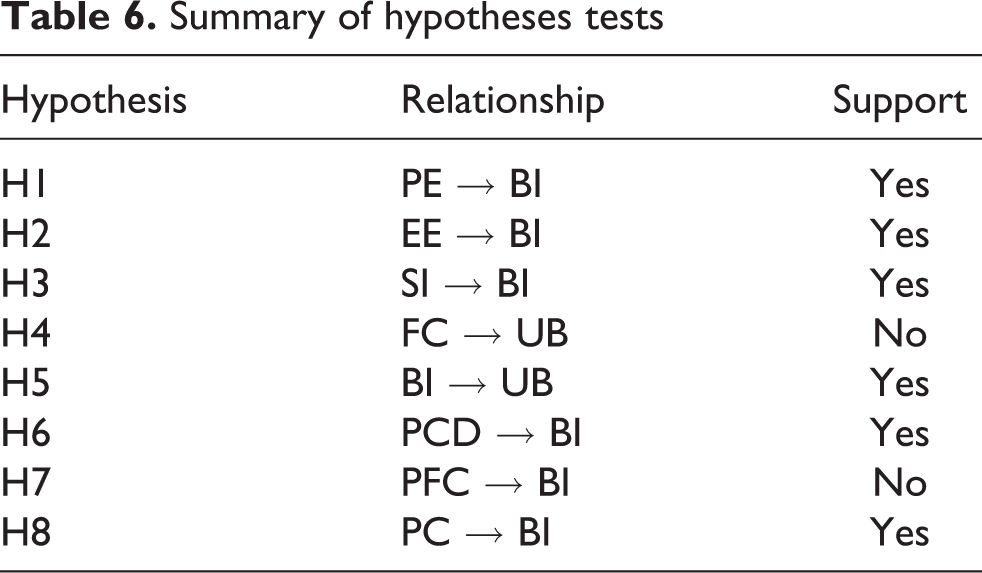

Figure 3 shows the path coefficients (the significant paths are shown) and the significant levels. The model accounts for 57% of the variance in behavioral intention and 17% of the variance in the usage behavior. Six out of the eight hypotheses proposed in the study were supported. Table 6 shows the summary of the results of the hypotheses testing.

Path diagram and hypotheses testing results.

Summary of hypotheses tests

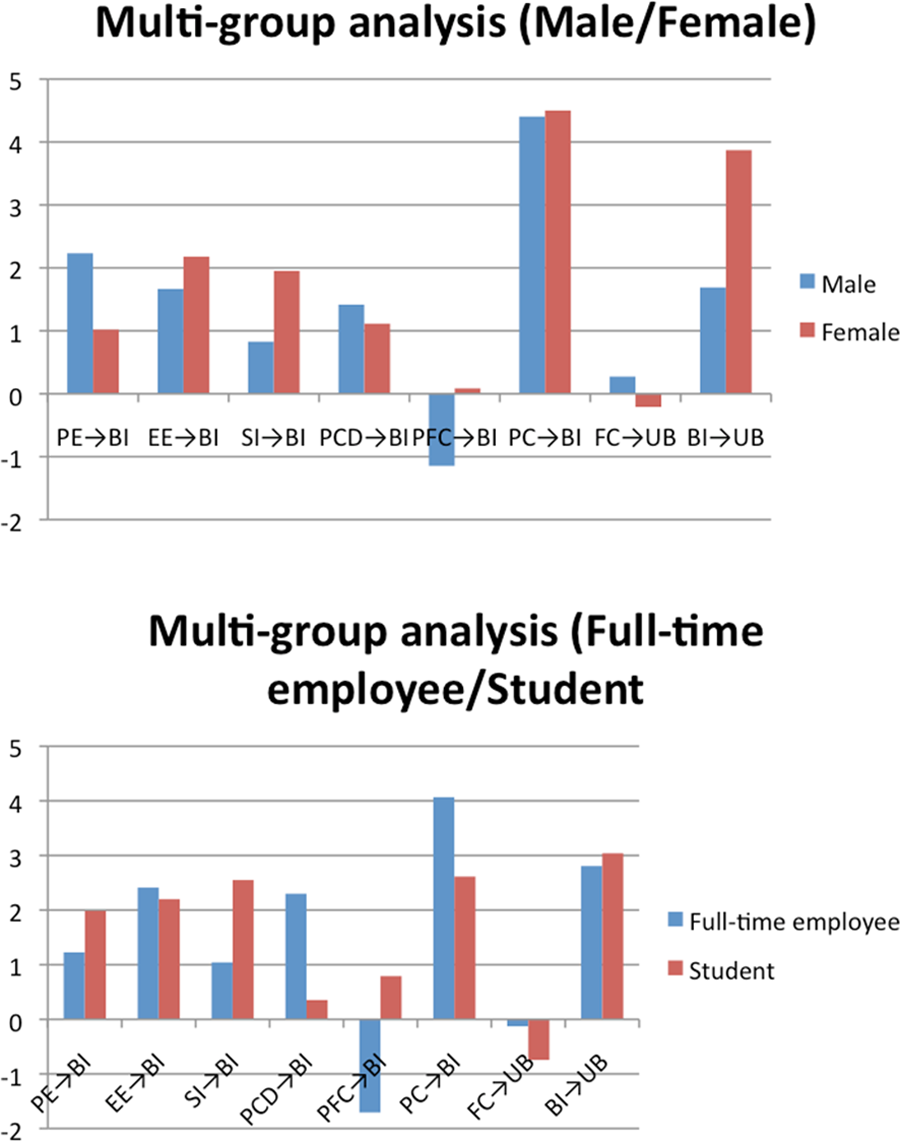

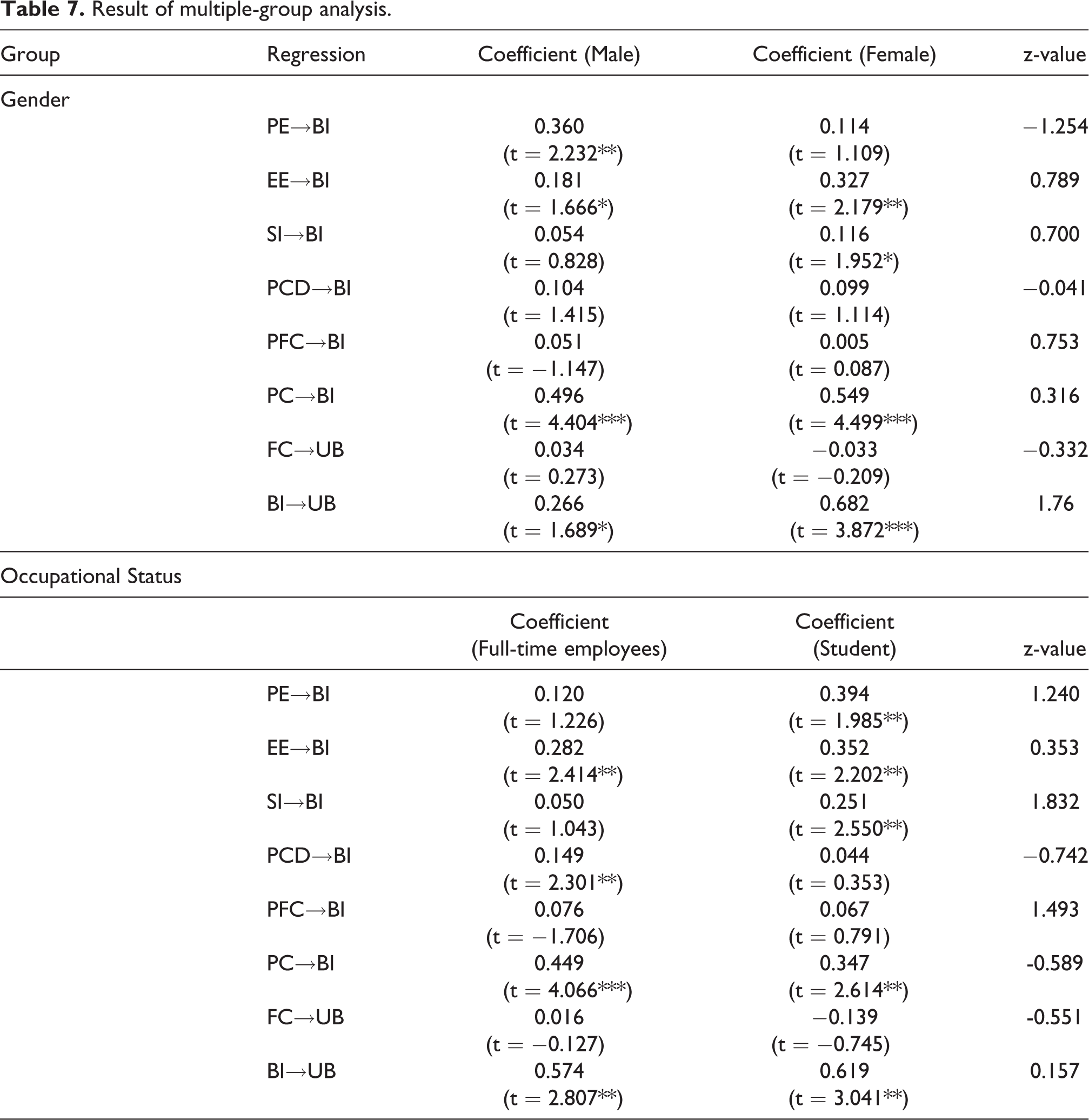

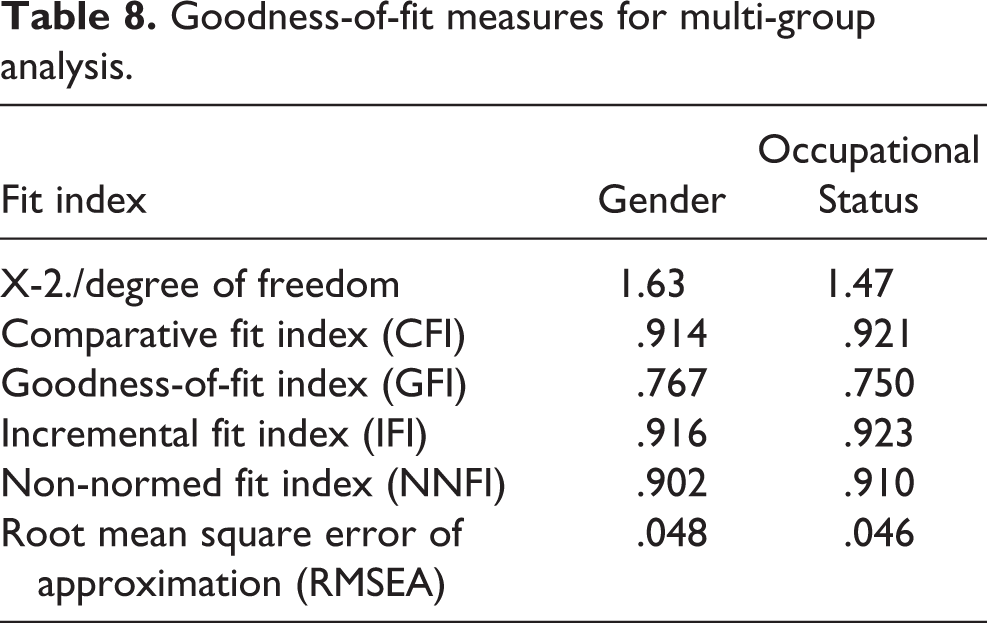

In addition, a multi group analysis using AMOS was performed to test for the differences in the adoption and usage of mobile banking among different genders and occupations, mainly focusing on students and full-time employees as these two represented the highest number of respondents. The rationale was to understand what factors are significant to males and females, students and full-time employees and which construct has a higher impact on their usage of mobile banking. The result of the multi group analysis is shown in Table 7 and Figure 4, as well as the goodness-of-fit measures in Table 8.

Multi-group analysis.

Result of multiple-group analysis.

Goodness-of-fit measures for multi-group analysis.

Discussion

This research is one of the first to propose an extended UTAUT model along with a three-pronged approach in understanding the behavioral aspect of consumers adopting the use of mobile banking. The findings of the study are discussed in this section.

Six out of the total of eight hypotheses were supported in this study. Performance expectancy was found to have a positive relationship towards behavioral intention (β = 0.183, p < 0.01), which is consistent with the findings of Venkatesh et al. (2003), Oliveira et al. (2014) Casey and Wilson-Evered (2012) and Escobar-Rodriguez and Carvajal-Truzillo (2014). A positive relationship was also found between effort expectancy and behavioral intention (β = 0.151, p < 0.05), which is consistent with the findings of Venkatesh et al. (2003), Casey and Wilson-Evered (2012), Escobar-Rodriguez and Carvajal-Truzillo (2014) and Tosuntas et al. (2015). With the increase in the growth of mobile phones and their ubiquitous nature, it is not surprising to note that Thai users expect mobile phones to increase their productivity, save their time, and enable them to accomplish their tasks quickly. This could be a result of heavy reliance on and usage of mobile technology. In terms of effort expectancy, the explanation could be that Thai users have more technical savvy in using mobile technology, hence less effort is required in learning to use mobile banking and at the same they have become quite skillful at using it.

Consistent with the findings of Venkatesh et al. (2003), Yu (2012), Thomas et al. (2013) and Escobar-Rodriguez and Carvajal-Truzillo (2014), this study found a positive relationship between social influence and behavioral intention (β = 0.125, p < 0.05). This is not surprising, as according to Hofstede’s (2001) cultural dimensions, Thailand is a highly collectivist country, which means that individuals are highly committed to families, extended families, and extended relationships. In the context of this study this could mean that users in Thailand who adopt mobile banking do so because they are greatly influenced by people that are close to them. They choose to use mobile banking because they believe that if people who are important or familiar to them think that they should use mobile banking they themselves will indeed use it. They choose to use mobile banking because people around them and in their surroundings use it. The relationship between behavioral intention and usage behavior was also found to be positive (β = 0.470, p < 0.001). This is in line with previous findings of Venkatesh et al. (2003), Yu (2012), Ifinedo (2012) and Escobar-Rodriguez and Carvajal-Truzillo (2014). This positive finding clearly indicates continuous usage of mobile banking among Thai users.

From the three constructs that were added to the existing UTAUT model in this study, two of the findings supported the hypotheses. The first was the positive relationship between perceived credibility and behavioral intention (β = 0.092, p < 0.05). This is consistent with the findings of Dasgupta et al. (2011), Yu (2012) and Jeong and Yoon (2013). This could be interpreted as that, even though Thai users have become more technically savvy and more mobile, they still value their privacy. Even though they use mobile banking, they believe that it should not reveal their personal information and that this should be kept confidential. They also believe that mobile banking is secure in conducting banking transactions and provides them with a secure banking environment. The second added construct that was supported was the positive relationship between perceived convenience and behavioral intention (β = 0.472, p < 0.001). This is in line with previous findings of Jih (2007), Hossain and Prybutok (2008) and Chang et al. (2011).

Of all the hypotheses supported, perceived convenience posited the strongest relationship. This evidently indicates that of all the reasons why Thai users choose to adopt mobile banking, perceived convenience is seen as the most important one. They strongly value the fact that mobile banking allows them to accomplish transactions conveniently, at any time and any place.

Contradictory to previous findings of Venkatesh et al. (2003), McKenna et al. (2013), Oliveira et al. (2014) and Tosuntas et al. (2015), this study did not find a positive relationship between facilitating conditions and usage behavior. This could mean that Thai users believe that they do not have the necessary resources to use mobile banking, and that it is not compatible with their lives. They could also believe that assistance is not available to them when they encounter problems in using mobile banking. This finding comes as a surprise; even though all the major banks provide free mobile apps for customers to connect to their banking services, Thai users still appear to find them to be inadequate.

The second added construct which did not support the hypotheses is the negative relationship between perceived financial cost and behavioral intention. This is not in line with the previous findings of Sripalawat et al. (2011), Yu (2012) and Huang et al. (2012). This could be interpreted as a positive sign for the growth of mobile banking among Thai users, meaning that they do not believe that using mobile banking would cost them a lot of money, nor that they would incur any financial burden if they adopt mobile banking. They also believe that the tools needed to use mobile banking are inexpensive.

In addition, the study also performed a multi-group analysis in order to better understand the adoption of mobile banking in Thailand. The two groups that were further analyzed were gender and occupational status. With gender, there were some similarities and differences in the reasons as to why each gender adopts mobile banking. For males, the significant factors were performance expectancy, effort expectancy, perceived convenience and behavioral intention to use mobile banking, with perceived convenience positing the strongest relationship. As for females, the significant factors were effort expectancy, social influence, perceived convenience, and behavioral intention, with perceived convenience positing the highest influence. The result suggests that both genders are significantly swayed towards the adoption of mobile banking because it requires less effort to use, is convenient, and that they will continue it in the near future. For both genders perceived convenience is the most important factor. As for the difference between males and females it is evident that males use mobile banking because it would increase their productivity, save their time, and enables them to accomplish their tasks quickly. While for females a greater emphasis is placed on the social influence of their families, extended families, and extended relationships.

As for occupational status, the study analyzed the adoption of mobile banking among full-time employees and students, as they comprised the highest number of respondents and users of mobile banking. For full-time employees, the significant factors were effort expectancy, perceived credibility, perceived financial cost, perceived convenience, and behavioral intention to use mobile banking, perceived convenience positing the highest influence. As for students, the significant factors were perceived expectancy, effort expectancy, social influence, perceived convenience, and behavioral intention to use mobile banking, with behavioral intention to continue to use mobile banking positing the strongest influence. Factors that were similar among both groups were effort expectancy, perceived convenience, and behavioral intention. As for the differences, full-time employees pay more importance to perceived credibility and perceived financial cost. Whereas, students give more importance to perceived expectancy and social influence. The surprising elements of the this group analysis are that students are more concerned about performance than full-time employees are and that full-time employees perceive mobile banking to impose financial costs and barriers for them even though they are working and earning while students are not. In addition, full-time employees are much more concerned about the privacy and security aspect of mobile banking compared to students, while students are more likely to be socially influenced by their families, extended families, and extended relationships.

Conclusion

This study extends the existing UTAUT model with three constructs, perceived credibility, perceived cost and perceived convenience, to identify the factors leading to the adoption of mobile banking in Thailand and also to identify the degree of influence of each one of the factors. It also proposes a three-pronged approach, consisting of an extensive review of the literature, expert interviews, and a field survey of mobile banking usage to better understand the adoption of mobile banking among Thai users. The study proposed hypotheses in an attempt to test the key significant paths as follows: performance expectancy → behavioral intention, effort expectancy → behavioral intention, social influence → behavioral intention, perceived credibility → behavioral intention, perceived financial cost → behavioral intention, perceived convenience → behavioral intention, facilitating conditions → usage behavior, and behavioral intention → usage behavior. Eight hypotheses were proposed and six were supported. The two that were not supported were the paths between perceived financial cost → behavioral intention and facilitating conditions → usage behavior. The rest of the above mentioned paths were supported. The study found that the relationship that posited the strongest influence was between perceived convenience and behavioral intention to use mobile banking.

In addition, a multi-group analysis was performed in order to better understand the adoption of mobile banking in Thailand. The two groups that were further analyzed were gender and occupational status. For both males and females, perceived convenience had the strongest influence on behavioral intention to use mobile banking. As for occupational status, among full-time employees perceived convenience posited the most significant factor while for students behavioral intention to continue to use mobile banking did.

The findings of the study have both practical as well as academic implications. For academic implications this study proposes a comprehensive extended UTAUT model for researchers, who can use this framework as a guideline in their future research along the lines of technology adoption in the context of a developing country or countries with similar economic or social characteristics to Thailand, especially countries in the ASEAN region. This study also presented consistencies and contradictions with previous studies on technology adoption, proving the need to conduct research even on popular models that have been used extensively in the past because they tend to yield different results for different types of technology and in different cultures and contexts. In addition, although mobile banking has been studied in the past, using different theories and different samplings from different countries, most such studies did not use a three-pronged approach to strengthen the research framework. By adopting the three-pronged approach this study makes academic contributions as the approach is comprehensive since it includes an extensive review of the literature, expert interviews, and a field survey of mobile banking. In their analysis and synthesis of existing studies on mobile banking, Shaikh and Karjaluoto (2014) discussed the various theories that researchers have used to predict mobile banking adoption. Of the 55 studies they presented, 48 employed theories other than UTAUT, while only seven of the studies used UTAUT. None of the studies proposed perceived credibility, perceived financial cost, and perceived convenience to go along with the UTAUT model. Most studies that have proposed these variables did so by extending it with the TAM model. By extending it with the UTUAT model, this study proposes a comprehensive theoretical framework that integrates eight popular theories in literature.

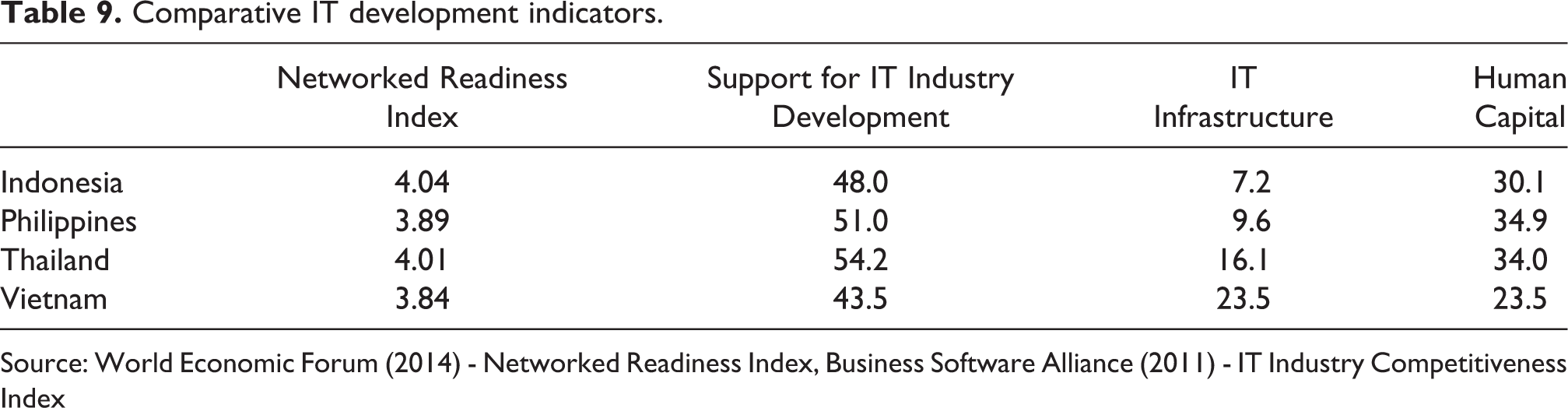

In addition, of the 55 studies Shaikh and Karjaluoto presented, only two were conducted on ASEAN countries, namely, Malaysia and Singapore, which are classified as developed countries. None of the studies were done on developing countries in ASEAN. What this study adds is a potential framework for studying developing countries in ASEAN such as Indonesia, the Philippines, and Vietnam. These countries have a similar technological climate, IT readiness, and IT industry development, as evident from Table 9 below. Besides the countries listed below, this study can also provide a framework for other developing countries in ASEAN such as Cambodia, Laos, and Myanmar. This is extremely important as we near the establishment and integration of the ASEAN Economic Community (AEC) member countries in 2015. The meta-analysis also revealed that most of the studies used either age, gender, or experience in their multi-group analysis. This study extends the theoretical base by adding occupational status such as full-time employees and students as part of the multi-group analysis, which fills a gap in the literature. Furthermore, this study also proposes a trust-based construct (perceived credibility), a financial-based construct (perceived financial costs), and a usability-construct (perceived convenience)

Comparative IT development indicators.

Source: World Economic Forum (2014) - Networked Readiness Index, Business Software Alliance (2011) - IT Industry Competitiveness Index

As for practical implications, this study provides solid empirical evidence as to what factors are taken into account by consumers in their decision to adopt mobile banking. It is especially important for banks and mobile application developers to understand the behavior of the consumers when they develop applications and try to promote its usage and growth among the consumers. For example, this study showed the supported hypotheses which could enable banks to know the reasons for adopting mobile commerce, but also what improvements they need to make. The respondents in this study did not believe that facilitating conditions plays an important role in their mobile banking adoption because they believe that they do not have the necessary resources to use mobile banking, and that assistance is not available to them when they encounter problems in using it. What banks could therefore do is to provide a channel whereby users have access to online help or call in customer service representatives when they have questions or face problems with using mobile banking.

Even though the literature review is extensive and careful attention was taken conducting the expert interviews and in designing and carrying out the field survey, this study has several limitations. Firstly, this was a single study conducted for a group of mobile banking users in Thailand, therefore the results should be considered with caution when applying it to other types of technology or in other countries. Secondly, this study extended the UTAUT model with three additional constructs. Further studies might incorporate other factors that might better explain the adoption of mobile banking. Thirdly, data collected in this study was done at a single point in time making it cross sectional. The longitudinal method of data collection might serve as a better approach of collecting data in the future. Future research could address these issues and extend the model by integrating constructs such as perceived financial risk and enjoyment.