Abstract

Transformation of cultural markets is a complex development that relates to both the audience and the industry. During the last decade, domestic popular films in Turkey increased their share of box office significantly. This study analyses socio-economic developments along with monopolization of exhibition sector to understand the change. While factors such as higher income level, relatively lower ticket prices, higher proportion of population in education and urbanization created a new potential audience for domestic films, rise of a dominant player in exhibition sector broke the hegemony created by foreign distribution companies.

Introduction

Domestic film production in Turkey made a great leap in 2000s. Box-office numbers increased dramatically for domestic films starting from 2005 and made a further surge after 2010s, reaching a stable market share above 50%. In the meantime, total movie audience and number of movie theatres grew larger.

This article aims to analyse the socio-economic developments in the background along with the change in the industry structure to explain the surge in domestic film production. It will be argued that both the audience and industry-related factors played a role. Throughout this time period, due to economic and sociological developments, a new audience interested in watching domestic films at movie theatres emerged. Yet, this was not sufficient for the domestic films to flourish since distribution companies associated with Hollywood-dominated industry. The change came with monopolization of the exhibition sector which targeted profit opportunity in domestic films.

Discussion requires an understanding of how the content of cultural products is determined. Adorno and Horkheimer (2002) point to the industry’s determinant role which eventually reproduces capitalistic order serving the ruling class ideology, homogenizing mass audience. Content determined from the top, in a top-to-bottom framework, however, does not necessarily result in dominance of Hollywood cinema in a framework where there are domestic actors in the industry who need not favour Hollywood products over domestic ones as long as they are compatible with ruling class ideology. Hegemony of Hollywood follows, according to Miller etal. (2005), from the role of international organizations which impose rules and conditions favourable for Hollywood products. These result in gains for Hollywood cinema internationally at the expense of domestic production.

Another view on Hollywood dominance is in economic terms. Cultural barriers create a disadvantage to foreign films, also called cultural discount in the literature. This works at the disadvantage of countries with smaller markets since they have a limited audience to finance production. Countries like the United States, which has a large population, benefit from scale economies in film production, attract more investment, produce films with higher technical quality using generous budgets and dominate other markets (Hoskins and Mirus, 1988; Wildman and Siwek, 1988).

While this reasoning applies well with smaller countries, for more populous ones with an audience capable of financing film production, such as Turkey, it does not necessarily hold true. Furthermore, cultural discount limits dominance of Hollywood cinema as well. Hollywood films are in a foreign language for most other countries and often incorporate cultural codes that are foreign to at least part of the audience in countries outside the United States. Although Hollywood strives to produce films that have a potential to reach a wide and diverse audience (Hoskins and Mirus, 1988; Waterman and Jayakar, 2000), local audiences usually have familiarity with local content and hence value foreign products less.

It could be argued that repeated exposure and consumption may reduce cultural discount and result in new cultural codes (Park, 2005, 2015). Having a hegemony on theatre screens for long time, Hollywood might over time have conditioned audiences in a particular way that reflects its particular needs and interests. Yet, this is a time-taking process. Bourdieu (1986) defines cultural capital as long-standing dispositions and habits formed over a long period of socialization. The length of time it takes for this capital to form makes it stable and resistant to change. Anderson (1983), among others, notes the slow pace of national culture construction. In the case of Turkey, as will be discussed later in detail, such exposure was largely restricted to a certain part of the population who have frequented movie theatres rather than large segments of population. The fact that foreign films are shown with subtitles further limited its audience.

Imposition of foreign films through means described in Miller etal. (2005) may result, as we argue was the case in Turkey, in exclusion of certain parts of audience from movie theatres. Yet, it is difficult to sustain this dominance due to the presence of a large potential audience for domestic films alienated from movie theatres who are keeping their distance to Hollywood products.

Given this framework where Hollywood hegemony is established through near monopoly of distributors closely associated with Hollywood, how could it be possible to understand the recent upheaval of domestic production? Fiske (1989) points to the power of consumer as the purchaser of the cultural product and hence determinant of what is popular. Ang (1990) recognizes the importance of consumer but notes its limitations. Harrington and Bielby (2001) state that the ‘discussion on the extent which “people make the popular” has yet to be resolved’. While Adorno and Horkheimer (2002) argue that industry shapes the cultural product for certain objectives, film industry is a complex structure formed by the uncertainties inherent in film production due to the lack of an intrinsic quality or utilitarian value (Hirsch, 1972). As Curtin (2007) argues, ‘globalization theories point to messy and complicated interactions but cannot identify the forces’.

A change in socio-economic conditions may force the industry to evolve, and DiMaggio (1977) directs researchers to focus on industry structure which at times may change due to competition. Indeed, Peterson and Berger (1975) find that vertical integration plays an important role regarding homogeneity of the product. The change in potential audience may result in a change in cultural product through certain parts of the complicated industry structure. It may as well lead to changes in the industry, and further change in product may be initiated by those which are better positioned to observe change in consumer preferences and which are likely to increase their profits by adopting to change.

This study, therefore, looks into developments on both sides, consumers and producers, of the popular cinema industry to explain the rise of domestic cinema in Turkey. On the audience side, with increasing income, lower relative prices and a young population, of which a higher share are educated, demand for movies, especially domestic ones, in theatres surges. In the meantime, on the industry side, a vertically integrated industry that brings dominance of foreign films and less diversity is being challenged on the exhibition side. We argue that monopolization of movie theatres, not integrated with Hollywood majors, created a window of opportunity for diversity in cinema production, not necessarily in terms of the content but in terms of source of production.

To summarize, we adopt a framework which emphasizes the role of intermediaries in the industry. A change in external environment, need for products appealing to a new group of spectators, has been met with new productions because movie theatre sector which has over time monopolized favoured these new products which gave an upper hand in its bargaining with foreign movie distributors and later establishing itself as a competitor in the distribution sector. While the shift to domestic movies hurt Hollywood producers and distributors, the same cannot be argued about theatre owners. Limiting the industry largely to Hollywood products at the expense of losing audience was detrimental for movie theatres and it helped fuel domestic production once they had the means for it.

The next section will provide an analysis of the change in movie audience and factors that contributed to its change. This will be followed by an analysis of film industry in Turkey and empirical analysis of box office data from 2005 to 2018.

Socio-economic developments – A new audience emerging

We argue that the fundamental change driving increase in domestic film box-office numbers is the change in potential audience of movie theatres. Audience studies are rare in Turkish cinema. It is generally accepted that there has been a significant shift in 1970s with the introduction of TV and then video players, worsening economic conditions and political developments that culminated in disturbances in public space. These drove away families from theatres to their homes (Çağlayan, 2004). According to a media professional Nizam Eren, before TV emerged, movie theatres were frequented by everyone, including uneducated and rural populations. This has changed over time, and audience profile was tilted towards young, educated, urban households (Sabah, 2016). Erkılıç (2009) discusses the change in audience quoting from Ayça (1993) and Zileli (2007). Film audience became younger and urban, and had higher income. He also presents film audience surveys by Fida Film and AC Nielsen. In 1994, 80% of the audience are 15–30 years old and 14% are 30–50 years old. Seventy-eight per cent have high school or more education. Forty-six per cent are students. AC Nielsen’s survey in 13 provinces in 2006, with 3652 people, finds 62% to be from upper- and upper-middle-income groups, followed by 9.2% from the middle-income group. Almost 90% of the total was made up of 8- to 24-year-olds (40.1%) and 25- to 39-year-olds (47.8%).

Urban audience profile was also reflected in the location of movie theatres after 1980s. According to Turkstat, in 2004, there were 424 movie theatres, and in 15 of 81 provinces there were none. In 2008, 11 provinces did not have a movie theatre and 6 had only one. In contrast, five largest provinces had half of the theatres.

A reflection of high-income, educated, and urban audience was foreign films shown with subtitles in movie theatres. While most foreign films were dubbed in 1960s, when audience was more composite, starting from 1980s foreign films were not dubbed but subtitled. It is clear that this is likely to create a barrier for a large part of population. Indeed, in television, subtitles were rare. An exception was the television channel CNBC-E that emerged in 2000 that appealed to higher income groups.

Cinema audience has been subject to two types of transformation in 2000s. First, the group that makes up the majority of audience, young and educated population has increased due to extension of compulsory education and increasing university education opportunities. Second, new audiences were added due to high economic growth and settlement of early migrants in urban centres where new socialization venues with movie theatres emerged.

In 1998, Turkey extended compulsory education from 5 to 8 years. This was observed to have a significant impact on high school as well as on university graduation rates. According to the Ministry of Education statistics, net enrolment ratio for secondary school was 36.52% in 1999–2000, 50.51% in 2004–2005, 62.71% in 2009–2010, and 79.26% in 2014–2015. For higher education, ratios were 10.52%, 26.63%, 29.55%, and 41.10%, respectively. In the meantime, Turkey’s young age population of 15- to 24-year-olds fluctuated, being 13.4 million in 2000, 12.5 million in 2010 and 12.9 million in 2015.

Another important development was the striking increase in the number of universities and university students. The number of public universities increased from 53 in 2000, to 102 in 2010, to 109 in 2015. Private universities increased from 20 in 2000, to 54 in 2010, to 84 in 2015 (Günay and Günay, 2011). The number of students who have been placed to a university for the freshman class increased from 414,647 in 2000, to 763,516 in 2010, to 983,516 in 2015. In 2008, universities were opened in nine additional provinces which previously did not have a higher education institution, and each one of the 81 provinces had at least one university. The impact of universities may be observed in the example of Siirt, for example, where the first movie theatre was opened in 2012, 5 years after the university was founded.

The profile of university student has necessarily changed, with a larger part of the population getting into universities. Although university enrolment increased, the quality of education was rather lacking, especially in new universities in small provinces. With this new student body, likely in search of entertainment opportunities in their spare times, domestic cinema had a new potential audience who was not well served by the subtitled Hollywood films.

Another factor for favouring domestic products over foreign ones, when it comes to younger population, may be related to speed of availability of pirated copies in Internet. As some foreign films have been occasionally screened later in Turkey and their DVD copies are available earlier, time to reach illegal Internet market may be shorter for foreign films. Unfortunately, we do not have data to inquire this mechanism.

Another development to be noted is the rise in incomes and drop, in real terms, in cinema ticket prices. Especially during the period 2002–2006, the average annual growth rate in real gross domestic product (GDP) reached 6% (Acemoglu and Ucer, 2015). There has also been slight improvement in income distribution, with Gini coefficient improving from 0.42 to 0.38 from 2003 to 2008.

Regarding university students, the number of scholarships through the government agency for student loans and scholarships, Kredi ve Yurtlar Kurumu, has more than tripled, and the number of education credits doubled from 2005 to 2015. The monthly scholarship payment increased from 45 TL in 2002 to 330 TL in 2015, an increase that exceeded general inflation. Starting from 2012, tuition payments for higher education at public universities have been lifted.

In the meantime, cinema ticket prices stayed rather constant after accounting for inflation. While the average ticket price in 2003 was 5.89 TL in 2003, according to Turkstat, it increased by 64% to 9.68 in 2010 and by a further 38% to 13.38 in 2015. The inflation rate was 161% from 2003 to 2013, exceeding the ticket price increase of 127%. Hence, cinema tickets have been cheaper in real terms and especially so considering the real change in incomes. In 2003, a ticket cost 2.61% of monthly net minimum wage but less than 1% in 2015. We should also add that while the ticket prices went down on average, films were projected in better theatres, mostly in shopping centres which have been frequented by middle-class households. It should also be noted that foreign film ticket price is 18% higher than the domestic films in 2013, mostly due to lower ticket prices outside metropolitan locations where domestic films are more popular (Kanzler, 2014).

Shopping centres have been an important part of the story since they all had multiplex movie theatres. The urbanization of provinces has been rather quick and disorganized, resulting in little public space available for new urban middle-class families to socialize. Shopping malls, then, took this role, providing space for families to spend time in an environment that felt secure. That was particularly the case for neighbourhoods in metropolitan areas that housed first- and second-generation migrants from rural areas or small provinces. Started with Galleria Shopping Center in Istanbul in 1988, 368 shopping malls were operational by 2013, with an increase in the number by 47.6% between 2010 and 2013 (Erkip and Ozuduru, 2015). Only 21 of 81 provinces had no shopping mall by 2015 (Habertürk, 2015). These became an attraction point, especially for the middle-class households, and a new audience emerged for Turkish cinema as these shopping malls have been built all around the country.

Finally, we should note the impact of television on the new audience. Starting from mid-1990s, Turkish television productions made a big leap and gradually took a larger part of the screen time. Turkish TV serial production boomed. In 2013/2014 season, according to an analysis by Deloitte (2014), domestic television series made up almost half of the programming of the top six television channels in prime time. Foreign films, on the other hand, took 10% of the screen time. The same analysis found domestic series and their repeat screenings to make 52% of top five programmes in TV, while foreign films took only 5%.

The surge of domestic television series production was reflected in film production, with Turkish films taking the top box-office figures in 2000s, yet the number of films stayed largely limited to high-grossing films (Çetin-Erus, 2007a). Familiarity with Turkish television programmes would make television viewers a potential audience for Turkish films. As noted, cinema products cannot be experienced prior to consumption, leading to the choice of familiar products. As the new audience’s earlier experience with visual media was mostly through television and as television programmes have been dominantly domestic productions in the last two decades, new audience members would be attracted to domestic films which usually employed acting crew from TV production sector.

All these developments made cinema within reach of a new potential audience. While not exactly similar to the audience in 1960s which was formed of families, this audience shared some of the qualities with them. They were from relatively lower income groups compared to the audience of 1990s and they had less education. Most importantly, they had familiarity with Turkish productions through television, but they were not used to subtitled foreign films.

It should also be noted that starting from 1990s, Turkish political landscape has been significantly transformed. In 2002, following the economic crisis of a year earlier, religious conservative party, Adalet ve Kalkinma Partisi (Justice and Development Party), gained a large majority in the parliament and has been ruling the country since then. This long period of political dominance was reflected in society, with Turkey becoming more religious, conservative and nationalist. Kaya (2015) reports education policies, such as changes in curriculum, that emphasized Islamic values, resulting in, with the contribution of policies in other areas, a ‘subtle’ Islamization of society. Lüküslü (2016) points to policies and discourse directed to youth aiming at an Islamized version of Turkish nationalism, situated in conflict with Western values and civilizations, based on pre-Republican history. Apparently, this new mind-set should have also been influential in the rise of domestic films.

Transformation of film industry

Following regulation that opened Turkish film distribution sector to foreign firms in the late 1980s, Warner Bros. and UIP entered the market as major distributors and established their dominance (Kalemci and Özen, 2011). The presence of Hollywood-affiliated firms in the distribution sector created a serious barrier for domestic products. The remaining major distributor, although local, survived with the rights to 20th Century Fox films (Özen Film until 2012 and Tiglon/Fida after that). The market share of these two foreign distributors has been over 70% for the period 2007–2013, with the exception of 2009 (57%) and 2010 (65%). In 2013, UIP had 46% of box office, followed by Tiglon/Fida and Warner Bros totalling another 43% (Kanzler, 2014). These three companies’ portfolio was largely shaped by Hollywood films, and other countries’ share was less than 10%. Their interest in domestic productions was limited to those expected to bring high box-office revenues.

The role of distributors in Turkey is limited to connecting the producers to exhibitors, as distributors often did not contribute to advertisement and promotion expenses. This created a further obstacle for domestic producers who already had limited financial resources. Other distributors were small and did not have a chance to affect the market. Facing an exhibition sector which was composed of small-scale theatre owners until late 2000s, the distributors had an upper hand in bargaining. These firms could dictate the theatres to limit their exhibition capacity to the films they distribute. It is likely that distributors have been pushing films with less of interest to audiences along with popular ones, and their connection with Hollywood likely made them favour foreign products over domestic ones (Çetin-Erus, 2007b; Ulusay, 2005).

In this setting, unsurprisingly, domestic film production was largely absent. While foreign films always had a significant share in Turkey, this reached its peak in 1990s. In the period 1990–2005, domestic production was limited to an annual average of 15 films, a significant drop relative to 1980s with annual average of 112 (Çetin-Erus, 2005; see Arslan, 2011; Esen, 2000; Kırel, 2005 for cinema industry in Turkey from 1960s on).

It should be noted, however, that the popularity of domestic products in television gradually created a number of production firms and a talent pool that is associated with that. Occasionally, these firms would attempt to convert this popularity to movie theatres by producing a limited number of films (Çetin-Erus, 2007a). As a result of this, the market share of domestic products increased gradually in the first decade of 2000s, reaching 50% in 2006 and staying close to or above that in the following years. It is worth noting that Behlil (2010) finds emergence of a film industry less related to television sector after 2005. She also points to the role of state support incentives for film production which intensified in the second half of 2000s.

Kanzler (2014) reports that in the period 1990–2013, 68% of 358 production firms had only one film produced. The number of films increased rapidly but was still low with 56 in 2009 and 68 in 2010. In the following years, the number of films and box-office revenues stagnated, only to make a further jump starting from 2013. While domestic films reached a considerable market share by 2012, there still were few regular producers, and 79% of the box-office revenue for domestic films in 2009–2013 came from the top 10 films.

The change in post-2013 period, which constitutes the focus of this work, came with the monopolization of exhibition sector. Going back to the 1980s, with the decline in audience, the number of screens dwindled. 1990s was not any better, but recovery started by 2000. From 1990 to 2000, the number of screens doubled from 299 to 606, and in the following decade it further increased to reach 1674 in 2010 and exceeding 2000 by 2012. The annual average growth rate in the number of theatres was 12.3% from 2007 to 2012 (Kanzler, 2014). It is to be noted that the increase in the number of screens has been supported by foreign distributors who needed more outlets to show their movies (Tüzün, 2013).

Movie theatre chains started to flourish especially with screens in new shopping centres, and they quickly reached a high market share. Mars Entertainment Group which operates screens under the name of Cinemaximum is exceptional in the crowd, in that it reached the market share of 52% in terms of box office with 26% of all screens and two-thirds of digital screens in 2013 (Kanzler, 2014). Closest competitors had 5%–6% of the market in 2013. While Mars has been in the sector since 2001, it became a significant player gradually. It first expanded in newly constructed shopping malls. Its dominance was established in 2011 when it acquired another major exhibition chain, AFM, and has been the most important player. In certain neighbourhoods with high-income level, the dominance of Cinemaximum approached the status of a monopoly (Tüzün, 2013).

One factor in the emergence of chains was the change in technology. With digital screening, small theatre owners who failed to secure funds to invest in new technology dropped out of the market. Chains with capacity to invest played an important role, and digital screen penetration which lagged behind until then increased from 11% to 48% from 2012 to 2013 (Kanzler, 2014).

With this development, Turkish cinema sector had two major distributors connected to Hollywood producers and a dominant player in the exhibition sector. This was received negatively by the domestic sector as independent movie theatres have been their only outlet to reach the audience, especially for art films. Tüzün (2013) reports sector representatives’ discontent of disappearance of independent theatres. Yet, Mars Entertainment Group had different priorities compared to foreign-based distributors. For the distributors, films from the studios that they are attached to had low marginal cost. Facing single and powerless theatres, they could easily bundle films. For Mars Entertainment Group, on the other hand, to show a movie with relatively low audience did not make sense and it had the power, in 2010s, to avoid this. It was clear that domestic productions with their potential audiences were more profitable to theatres but not necessarily to Hollywood-based distributors.

We claim that this resulted in an increase in the number of domestic products. A new growth spurt started after the merger of Cinemaximum with AFM in 2011, and from 2011 to 2014 the number of domestically produced films almost doubled again, reaching 110 in 2014. Box-office revenues have also doubled in the same period. Gradually, Cinemaximum decreased its dependence on distributors further by starting to distribute films itself.

Analysis of box-office data from 2005 to 2018

Empirical work is based on the analysis of box-office data for all films screened from 2005 to 2018 obtained from Box Office Türkiye. Data include both the number of ticket sales and ticket revenues. Also available are the date of initial screening, duration of screening and number of theatres at the initial screening.

As we argue that the rise in domestic film box office is based on a new audience, our hypothesis is that new domestic films compete with other domestic products rather than foreign films. We expect this to be reflected in two ways in the data. First is the initial screening time. Hollywood blockbusters are usually screened in late spring, summer and end-of-year holiday months. January to early April and August to early November are usually weaker months in terms of expected box-office figures. In most countries, these times are seen as more favourable times for domestic films.

We use this characteristic as an indicator of the surge in domestic films. We argue that as the domestic films gain a momentum and compete with each other, the initial screening times would move to the months initially occupied by the Hollywood films.

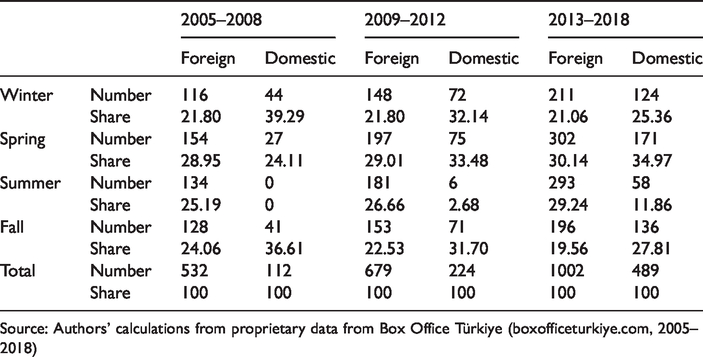

Number and seasonal share of films screened by origin and years.

Source: Authors’ calculations from proprietary data from Box Office Türkiye (boxofficeturkiye.com, 2005–2018)

Results are in line with our expectations. In the early period, until 2013, most Turkish films are screened from October to February. In late spring, we observe smaller number of domestic products, and in the summer months it decreases further. From 2005 to 2008, there were no domestic films screened during the summer months, and in 2010, 2011 and 2012, there was only one. The change in the distribution of films in the period 2013–2018 is clear, with summer season getting 10% of the films and other seasons having a more balanced distribution.

This supports the hypothesis that with new audience and accessible theatres, Turkish films competed more with each other than with Hollywood films, making it more profitable for some to be launched in times where few domestic films are screened.

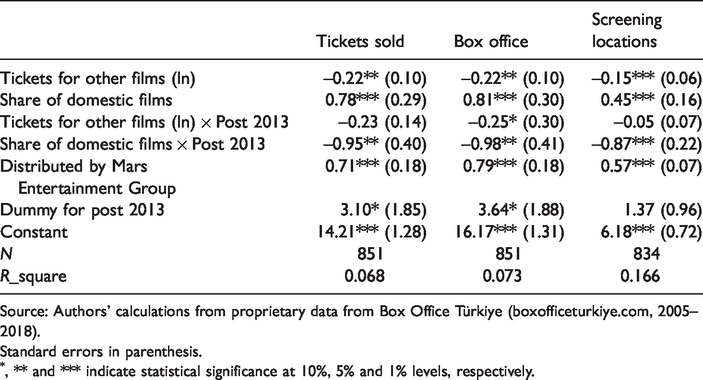

To further evaluate the hypothesis, we next perform a regression analysis. The dependent variables, considered in the study, are number of tickets sold, box-office receipts and number of locations in the first week of screening for domestic films. To estimate competition faced by the film, we consider the box-office figures of other films that were screened the same week. To address non-linearities in the relation, we use natural logarithms of these variables and the dependent variable in the regression. To measure competition against domestic films, we also include the share of domestic films. We create a variable that indicates whether the film is screened before or after 2013 and interact it with independent variables. Finally, we include a dummy variable for films distributed by Mars Entertainment Group to assess the impact of entry in distribution by the major player of exhibition sector. To exclude films with very low ticket sales, we consider only the domestic films that had more than 5500 tickets sold, the figure which sets the limit for the bottom quartile of the films in terms of their ticket sales.

Regression results.

Source: Authors’ calculations from proprietary data from Box Office Türkiye (boxofficeturkiye.com, 2005–2018).

Standard errors in parenthesis.

, ** and *** indicate statistical significance at 10%, 5% and 1% levels, respectively.

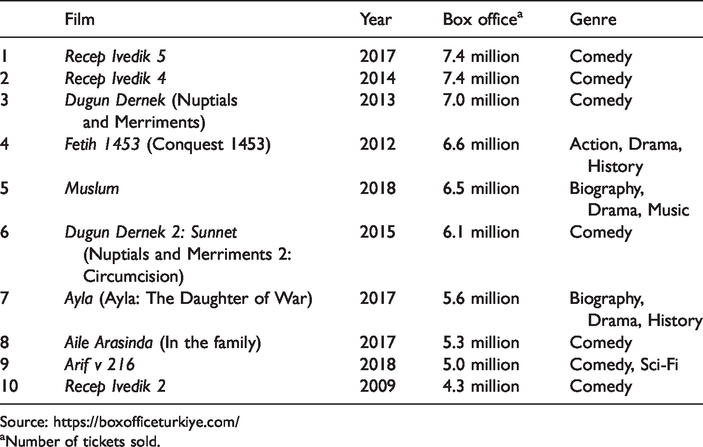

Films with top box-office figures in Turkey (2009–2018).

Source: https://boxofficeturkiye.com/

Number of tickets sold.

Comedies dominate the list of top 10 films as seven of the top 10 can be classified as comedies (Recep Ivedik 2, 4 and 5, Dugun Dernek 1 and 2, Aile Arasinda, Arif v. 216). There are two historical films (Fetih 1453 and Ayla) and one biopic film (Muslum). It is often argued that comedy is the genre that is the most difficult to translate across cultures, giving domestic films an advantage. A second important feature is the presence of well-known stars. This reflects to some extent the impact of popular domestic television sector on film industry. It is to be noted that films are made with moderate budgets. Special effects are rather rare and observed only in two of the top 10 films, Fetih 1453 and Arif v 216. While there is no dominant theme in the movies, traditions and their place in modern world come to the fore in most comedies. The presence of two historical movies, both displaying heroism, is to be noted.

Conclusion and discussion

The study provides an analysis of the surge in domestic cinema in Turkey in 2010s. How the cultural production is made and the dynamics involved in determining its content has been shown to be a complicated process. In this case, we show that two factors played an important role. First, socio-economic developments brought about a potential movie theatre audience for domestic films. Yet, the conditions were not suitable due to the dominance of Hollywood-connected firms in distribution. This has changed with the rise of Mars Entertainment Group as a dominant player in the exhibition sector with its Cinemaximum brand. In the following period, domestic products found more place in movie theatres.

The case of Turkey is interesting since the rise of domestic cinema occurred with little government intervention. Market conditions and profitability of domestic production, under suitable market conditions, resulted in the increase in production.

This finding is of importance to policy makers. Ministry of Culture has been providing incentives for domestic film production since 2006. While these had an effect on film production, most producers had been single film producers, not continuing film production. In contrast, the change after that period, argued here to result from the characteristics of industry structure, had been more dramatic. In that sense, the article displays the importance of distribution and exhibition sectors in domestic production.

The work is also important for future policy choices in Turkey. In 2016, Mars Entertainment Group was acquired by South Korean firm CJ CGV. It is interesting to see how this will affect domestic production in the future. In fact, in the end of 2018, there has been a showdown between the Group and domestic producers regarding sharing box-office revenues. While the issue was resolved with government intervention slightly favouring domestic producers, it is yet to be seen whether this would change the approach of the Group to domestic production. This development does also remind us that the producers face a monopoly-like structure in the exhibition sector.

Finally, it should be noted that there have also been other factors in place during the time period studied. The maturing domestic film sector through 2000s clearly played a role in the process. Government subsidies, although limited and at times leading to single film production companies, contributed to the success of domestic cinema. Our work does not assume away these developments but emphasizes importance of industry structure.

Footnotes

Acknowledgements

Zeynep Cetin-Erus thanks the Scientific and Technological Research Council of Turkey, Postdoctoral Research Scholarship Programme (BIDEB-2219) for funding her sabbatical year at Comparative Media Studies/Writing at MIT where part of this research was conducted. The authors also thank Tolga Akıncı for data used in the article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.