Abstract

The expansion of shale gas extraction has been supported by the UK national government because of predicted economic benefits. However, what is largely missing from this analysis is an estimation of local and regional economic impact. This paper seeks to contribute to the deliberations of local stakeholders by outlining current estimates of local multiplier effects and indicating where policy initiatives could be targeted to maximise local economy benefit. This advocates a reorientation of public policy support for the shale gas industry to focus upon the development of educational partnerships, enhancing skills development and attracting inward investment through spillover effects, thereby enhancing local economic impact.

Introduction

The expansion of the shale gas industry has been encouraged by the UK government due to its potential economic benefit. Considerations around energy security, the wealth generating capacity of an emerging energy industry to counterbalance declining North Sea production, potential reductions in energy prices for consumers and enhanced tax revenues have all generated noticeable support in government circles. Indeed, the Prime Minister has stated government strategy is ‘going all out for shale’ (House of Lords Economic Affairs Committee, 2014a: 9).

At the time of writing, however, there is considerable uncertainty over the future of the industry due to concerns raised about the extent of negative environmental externalities (Green et al., 2012; Wood et al., 2011: 7). 1 Indeed, as this paper is being completed, Lancashire County Council planning committee has deferred a decision on further shale gas extraction in the Bowland Basin for a further eight weeks, pending public consultation on new sound deadening proposals put forward by Cuadrilla to avoid planning permission refusal on grounds of noise and disturbance. 2 Moreover, a recent House of Commons Environmental Audit Committee (2015) report has raised serious concerns over the regulation of shale gas extraction, the viability of it being developed to meet short-term energy requirements and the compatibility of using shale gas within current emissions targets without a simultaneous introduction of carbon capture and storage technical solutions. 3 The Committee recommended a moratorium on shale gas extraction pending detailed consideration of these issues, but this was defeated in a House of Commons vote on an amendment to the proposed Infrastructure Bill. Hence, it would appear that national public policymakers have concluded that, properly regulated to prevent the worst effects, the expansion of the shale gas extraction industry would produce positive net economic benefit for the UK economy. Accordingly, a programme of tax reliefs and other fiscal incentives have been announced to stimulate the development of this industry (HM Treasury, 2014: 35, 58).

What is largely missing from this analysis, however, is consideration of potential local and/or regional economic impact, if the shale gas industry should expand as national policymakers and industry sources seem to assume. As the UK is more densely populated than those US areas in which shale gas extraction currently occurs, local acceptance of the industry is considered to be essential for its long-term successful development. Indeed, the International Energy Authority (IEA) is explicit in its conclusion that the large-scale expansion of shale gas extraction is dependent upon whether government and industry is able to (i) devise robust environmental regulation and (ii) secure public acceptance in order to ‘earn’ the industry a ‘social license to operate’ (IEA, 2012b: 142).

Yet most studies have either neglected to estimate potential local impact or else have assumed that regional benefit will be fairly automatic (House of Lords Economic Affairs Committee, 2014a: 29, 35, Ev 139; IOD, 2013: 8). 4 This omission is all the more surprising because it would seem logical for supporters of the shale gas industry to attempt to mollify local opposition through evidence-based analysis demonstrating the benefits, as well as the costs, which may derive from the expansion of the industry. Since most costs will be experienced most drastically at local level, it would seem reasonable to expect local economic benefit to exceed externalities if local communities are to acquiesce to the expansion of the industry.

This conclusion is reinforced by a recent survey of residents in Blackpool, Fylde and West Lancashire, carried out by the Britain Thinks (2013) polling agency, which has identified that support for the expansion of the shale gas industry is finely balanced, as concerns over environmental externalities are largely negated by anticipation for employment opportunities and benefits for the local economy. 5 However, this potential level of support, or perhaps more passive acquiescence, requires the realisation of these potential economic benefits. This, in turn, emphasises the importance of a detailed consideration of the distribution of costs and benefits deriving from any expansion of shale gas exploration and extraction.

This paper, therefore, seeks to highlight the factors that local stakeholders and their representatives should consider when seeking to maximise the potential economic benefit arising out of the possible expansion of the shale gas industry in their region. It does not, therefore, seek to assess the broader environmental or social impacts of shale gas extraction, but rather focuses upon the issue of, if shale gas extraction occurs in a given location, how might the local community best generate an optimal economic benefit to set against inevitable externalities caused by the activity. The paper focuses upon the Bowland Basin, situated in Lancashire, but which is part of the more extensive Bowland-Hodder unit encompassing Cheshire, parts of Derbyshire around Edale, Cleveland and the Humber regions. This has been identified by the British Geological Survey as having the greatest potential shale gas reserves in the UK (Andrews, 2013).

Background

Shale gas is a form of natural gas contained within a commonly occurring shale rock formation. The low permeability of shale rock creates the possibility for shale gas exploration, due to the preservation of the oil and gas reserve, but it creates difficulties for the extraction process. One solution has been horizontal drilling, where the drill shaft represents an ‘L’ shape, in order to gain better immediate access to gas pockets. A second is to use hydraulic fracturing to enhance flow rates (Rogers, 2011: 121). This process involves pumping a fluid at high pressure through the well and into the surrounding target shale rock, thereby creating fractures or fissures a few millimetres wide in the rock, for a radius of perhaps hundreds of metres away from the well bore. To prevent these fractures closing, once the pressure is released, small particles, such as sand or ceramic beads, are added to the fracturing fluid in order to infill the small fractures in the rock. These ‘propanants’ quite literally ‘prop open’ the fractures and, due to their greater permeation, facilitate the escape of the gas into the well. It is the ‘fracking’ process that raises particular environmental concerns (Wood et al., 2011).

Unconventional gas resources, such as shale gas, remain largely untapped and, indeed, it is only really in the USA, in recent years, where a rapid expansion in shale gas extraction has occurred. From representing only 1% of the total US gas market at the turn of the century, shale gas has grown to represent one-fifth of the US market in 2009 (Stevens, 2010: vi). The International Energy Agency predicts that gas will form a rising share of world energy demand for the next two decades, as coal and oil experience a modest decline and, moreover, potentially two-thirds of this increase in gas supply may derive from unconventional gas sources (IEA, 2012a: 79–81; IEA, 2012b: 125–154). Consequently, it is proposed that unconventional gas has the potential to become a vital part of an increasingly important energy resource at the global level.

Potential significance of shale gas in the North West

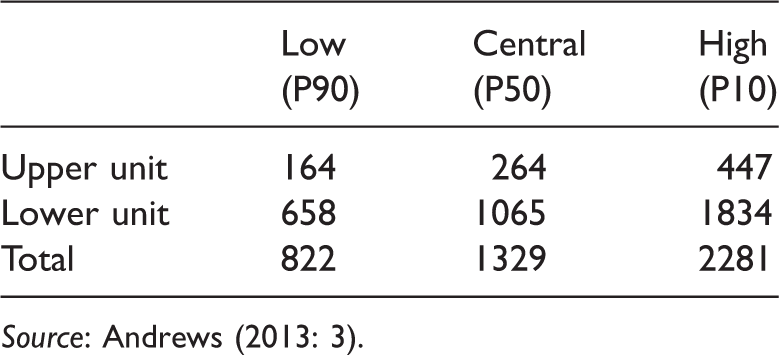

Total gas in place estimates (trillion cubic feet, tcf).

Source: Andrews (2013: 3).

When attempting to place a value upon the size of the potential shale gas industry, there are significant barriers, since estimates of ‘gas in place’ (GIP) do not, however accurate, closely reflect technically or economically recoverable gas reserves. Indeed, the latter are likely to be only a very small proportion of the GIP forecasts. There is evidence to suggest that drilling costs may be higher in the UK than the USA, albeit that higher European gas prices may offset higher cost factors (House of Lords Economic Affairs Committee, 2014a: 40; IOD, 2013: 114, Ev 179).

One estimate assumes that the upper (more mapped) element of the Bowland field might be similar to that of Barnett Shale in Texas, in which case the economically recoverable yield would be around 4.7 tcf (or 4.7bn mmbtu) (Andrews, 2013: 3; DECC, 2011). 6 At a current European wholesale price for gas of around US$10 per mmbtu, this would value an equivalent economically recoverable shale gas reserves in the Bowland field to be in the region of £28bn (US$47 billion).

A more recent estimate, however, suggests that shale gas extraction could represent a larger percentage of GIP, perhaps 10–30% (House of Commons Energy and Climate Change Committee, 2013: Ev 132–133; House of Lords Economic Affairs Committee, 2014a: 33, Ev 124–125; IOD, 2013: 112). Taking the more conservative figure, this would equate to between 26.4 tcf for the upper unit central estimate and 132.9 tcf if including the more uncertain lower unit forecasts. At current wholesale gas prices, this would value potential upper unit recoverable reserves at approximately £157.1bn (US$264bn), rising to £791.1bn (US$1329bn) if lower unit predictions are added. If this is accurate, then the stock of potential shale gas in the Bowland Basin could contain as much value as that previously extracted from the North Sea (House of Lords Economic Affairs Committee, 2014a: 33, Ev 124–125). Furthermore, over the forecast two decade shale gas industry lifespan, this would generate between £7.9bn and £39.6bn per annum.

Cuadilla Resources, the company licensed to explore the larger part of the Bowland shale, originally estimated that there is 200 tcf of GIP in their exploration field, although the most recent estimate forecasts possibly as much as 330 tcf, thereby suggesting potential reserves may be 65% larger than first estimated. 7 The former is close to the central upper unit forecast made by the BGS, whereas the latter is far higher (Andrews, 2013: 3). Assuming 10% can be economically recovered, and at current European gas wholesale prices, this would equate to a value of approximately £119bn (US$200bn) for the lower forecast and £196bn (US$330bn) for the most recent estimate. Averaged over a 20-year extraction cycle, this would represent between £5.95bn and £9.6bn per annum. To place this into context, in 2009, the 12 district Lancashire economy is worth approximately £18.3bn, representing one-fifth of the economy of the North West of England. 8 Therefore, if this industry prediction is accurate, shale gas could add as much as an additional 32.5–52.4% to the current size of the Lancashire economy over this two-decade period.

Cuadrilla Resources have advanced a slightly higher estimated market value of £136bn, presumably by employing a more generous assumption as to the proportion of reserves that can be economically recovered. 9 Using Cuadrilla cost and volume estimates, alongside DECC price predictions, Deloitte (2013) estimates that Bowland shale production could generate tax revenues of £580 million per annum by 2020 and sustain peak level employment of between 6900 and 23,600, depending upon assumptions made in calculations. If the most recent forecasted reserves are accurate, both of these figures could rise substantially.

Assessment of national economic impact

The significance of the conventional North Sea oil and gas industry can be represented by its balance of payments contribution, accounting for approximately 68% of UK oil and 58% of gas demand, alongside its contribution of one quarter of all corporation tax revenues and support for approximately 440,000 jobs in the UK, whether directly, through the supply chain or induced through income multiplier effects (Oil and Gas, 2012). Shale gas development has the potential to make a contribution in each of these areas. For example, the Institute of Directors and DECC have forecast that shale gas could offset otherwise rising energy imports, as North Sea gas output falls in the future, thereby strengthening the balance of payments and providing enhanced energy security (House of Lords Economic Affairs Committee, 2014a: 17, 2014b: Ev 24–31; Huppmann et al., 2011; Rogers, 2011: 118). It has the potential to generate significant revenue for the government (EY, 2014: 31).

In terms of employment opportunities, AMEC (2013: 65–66, 83–84) forecasts between 2600 and 5300 total full time equivalent (FTE) jobs generated, Ernst and Young (EY) (2014) predicted 39,000 jobs throughout the supply chain at peak production, whilst the IOD (2013: 130), using a different set of assumptions around the number of wells drilled at each site, forecasts a peak level of employment of 74,000 supported by the industry. A separate study, examining the potential employment effect upon the coastline of the North West, forecasts a peak year impact of 15,500 jobs (AMION, 2014). In addition, an industry-sponsored study forecasts 6500 new jobs, based upon the assumption of 10 wells per drilling site (Regeneris, 2011: 47–48). Current industry plans have extended to proposing up to 20 wells per site; however, the considerable economies of scale, witnessed in the US industry, imply that employment creation will not increase in proportion (i.e. constant coefficients) to any increase in production, but at a slower rate. Thus, if predictions assume a similar level of technical efficiency to US shale gas operations, should the Bowland field expand to 800 wells, the total workforce requirements would be likely to rise to 7858 FTEs, at an average of 9.82 per well (MSETC, 2011: 29).

It is important to note that employment rates vary considerably, within the shale gas extraction industry, between the labour-intensive, but relatively short-lived drilling phase, and the longer term gas extraction and maintenance phase, where far fewer people are employed. Moreover, shale gas wells tend to deplete faster than conventional gas comparators, having a life of perhaps 8–12 years rather than a more typical 30–40 years (Stevens, 2010: 11). Thus, the production profile depends upon the ability to continually expand the industry, through the drilling of new wells; a fact that necessitates continuing public acceptance (Rodgers, 2013: 5–6). Consequently, the IOD forecast, employment peaks approximately 10 years after the start of expansion, and reaches a stable state at around 17,000 after an additional decade, whereas, for AMEC, this maintenance stage might employ as few as 200–1152 workers. Thus, without further data concerning the number of wells to be drilled, estimates of employment potential are considered to be unclear (House of Lords Economic Affairs Committee, 2014a: 42, Ev 191–193).

An additional potential benefit, for the UK economy, might derive from reductions in price resulting from an increased supply of gas from shale reserves. In the US, a rapid expansion in shale gas production resulted in a decline in gas prices of around 20%, to the benefit of domestic customers but also enhancing the international competitiveness of energy-intensive industries (Huppmann et al., 2011: 72). 10 This might assist in the retention and/or ‘re-shoring’ of firms in these sectors (House of Lords Economic Affairs Committee, 2014b: Ev 61). Whilst predictions on the impact of shale gas on UK prices are indeterminate, it has been noted that low-cost supplies of shale gas have resulted in a cost advantage over Chinese competitors exceeding the disadvantage in labour costs (House of Commons Energy and Climate Change Committee, 2013; House of Lords Economic Affairs Committee, 2014a: 15, 2014b: Ev 11–14)

Studies of economic impact are inevitably limited in terms of the scope of their analysis, due to the difficulty inherent in incorporating dynamic effects, such that the displacement costs of other industries or externalities (i.e. environmental damage or the cost to other industries and the local community of rising costs of living and/or higher housing costs) tend to be left out of the equation (Weinstein and Partridge, 2011). Nevertheless, input–output modelling (Leontief, 1986) for 2005, the latest year when data are available, suggests that an increase in activity in the oil and gas sector will result in an output multiplier of 1.321 (ONS, 2005). Thus, a £28bn increase in oil and gas production would be anticipated to result in an estimated total benefit to the nation as a whole of some £37bn, after the beneficial impact on supply chains has been taken into consideration. Alternatively, the forecast made by Cuadrilla Resources for potential economically recoverable shale gas reserves might signify a national economic impact of £157bn.

There are a number of reasons to be cautious about the precise national economic impact which may arise from the expansion of the shale gas industry, not the least of which derives from the considerable uncertainty involved in identifying the size of recoverable reserves. Moreover, access to these reserves is likely to prove more complicated in the UK than in the US, because the former is a more crowded island, with proportionately less land available for drilling without generating significant disruption externalities for established communities. Moreover, UK landowners do not own the rights to minerals and hydrocarbons beneath their land – this belongs to the Crown – and therefore there are fewer incentives for landowners to cooperate in the exploration and extraction process (White et al., 2014).

Local economic impact

For the US studies, a commercially developed IMPLAN input–output model has typically been used to generate a multiplier estimate for regional economies. 11 The most prominent amongst the work in this area has been Considine and his team, from Pennsylvania State University, whose estimates of output multipliers have generated a fairly consistent 1.9–1.94 range, whilst employment multipliers have been estimated to lie between 2.03 and 2.05 (Considine, 2010; Considine et al., 2009, 2010; Snead and Barta, 2008; Weinstein and Partridge, 2011). In the UK, however, the Office for National Statistics does not produce input–output tables on a regional basis, and whilst devolved (Scottish, Welsh and, to a lesser extent, Northern Irish) governments have produced their own disaggregated models, this does not provide an adequate basis for a study seeking to estimate the more localised impact of an industry moving to a specific English region.

Estimates for the impact experienced in specific regions or localities in the UK would be expected to be smaller, as benefits leak out of local economies to benefit firms and employees located elsewhere in the UK and, indeed, abroad; presumably the latter is one of the reasons why national UK multiplier estimates are smaller than regional American comparators. The fact that approximately 45% of total oil and gas employment in the UK is located in Scotland, with a particular concentration in and around Aberdeen, indicates the existence of a successful cluster of energy supply companies, whereby an expansion in shale gas exploration may rely upon the skills and technical machinery derived from this region (Aberdeen City Council, 2012; Oil and Gas, 2012). Agglomeration effects may, therefore, require significant incentives or market rewards to consider significant relocation closer to the point of shale gas drilling sites.

The absence of a local or regional input–output method of calculation resulted in the industry consultancy group, Regeneris (2012), adopting a forecasting methodology utilising input–output estimates for the UK economy as a whole (1.3) and supplementing this with data derived from industry sources. Thus, Regeneris (2011: 37) notes that, in the initial test well phase of exploration within the Bowland region, only 15% of jobs were taken by Lancashire residents, whereas around 17% of industry expenditure could be identified as being spent upon local employees and suppliers. This gave rise to multiplier estimates of 2.1 at national level, and 1.5 locally, with peak level job creation of between 1700 and 2500 in Lancashire, incorporating those employed directly, sub-contracted via agency or consultancy, employed by one of the shale gas supply chain or induced elsewhere in the region (Regeneris, 2011: 37–48; Regeneris, 2012). Unfortunately, this methodology suffers from two weaknesses, in that, firstly, input–output estimates should have been used from the oil and gas industry rather than the average for the UK economy as a whole, and secondly, these should have been substituted (not augmented) by data drawn from supply chain calculations and second stage multiplier effects deriving from employee expenditure (Regeneris, 2012). This double-counting over-inflated multiplier estimates.

An alternative forecast for employment creation, in the Ocean Gateway (coastline) area of the North West, is based upon the twin assumptions that a significant proportion of the supply chain relocates to the area and that local residents are equipped with the necessary skills to work in the industry. On this basis, the report predicts a peak year total is some 3500 jobs (AMION, 2014). This would represent around 23% of all jobs predicted to be created by the industry.

Local economic impact depends upon the size of the initial boost to the local economy, through direct expenditure by the emergent industry (whether through the consumption patterns of employees or expenditure through the supply chain located within the area), multiplied by indirect (subsequent supply chain expenditure) and induced (multiplier) effects. Consequently, even if the multiplier estimate is found to be in the region of 1.3 if regional benefit mirrored national impact calculated by input–output analysis, or 1.5 as estimated by industry consultants, if the initial expenditure located within the local economy is small, the ultimate effect upon the local economy will remain relatively small even after inflated by the multiplier effect.

The evidence, obtained from industry sources, operating within the Bowland field at this early stage of exploration, would suggest that only 1.94% of supply chain value is allocated to firms based in the Lancashire area, and 4.12% in the North West as a whole, compared to just over one-tenth of the total flowing to firms based overseas. The latter may be an underestimate given that predictions, made by AMEC (2013: 69) and Regeneris (2011: 36), suggest that 29% and one-third of supply chain expenditure will be located overseas. Moreover, Regeneris (2012: 37) found that, in the initial test well phase of exploration within the Bowland region, only 15% of jobs were taken by Lancashire residents. Consequently, it would appear that the key factors, determining the size of local economic impact, derive from the extent to which the advent of the new industry impacts upon the local labour market, through employment of local residents and enhancing human capital formation, together with the development of a local cluster of firms servicing the industry.

This conclusion confirms similar findings from previous studies. Local companies tend to possess extensive local linkages resulting in stronger local multiplier effects than large companies doing business in many different regions and countries. Moreover, local supply-side effects are associated with different company and city-regional characteristics. Thus, indirect multiplier effects are typically stronger with companies which have been operating in a specific location for a lengthy period of time. Similarly, service sector firms tend to have a higher local impact than manufacturing companies, largely because employment costs are a more significant proportion of expenditure for the latter than the former, thereby anchoring a greater share of initial expenditure in the local economy. Furthermore, the larger the city region, the less significant are the leakages from a given economic boost, and therefore the greater the resulting local income multiplier (Domanski and Gwosdz, 2010). Finally, the interrelationship between firms has been found to be highly significant, in terms of delivering regional multiplier effects, as agglomeration effects, through the growth of clusters and resultant informational flow between firms, tend to spillover into skills development and local income growth (McCann, 2013: 169; McCombie and Thirwall, 1994).

Policy implications

The size of the local economic impact, arising from the expansion of the shale gas exploration and extraction industry, will largely depend upon the proportion of employees to be drawn from the local region and the relocation of a sizeable share of the supply chain within the local economy. These conclusions have implications for local and national policymakers. For example, the Lancashire Local Economic Partnership City Deal has outlined ‘significant opportunities’ deriving from shale gas expansion in the region, with the energy sector being identified as a key component for growth, jobs and skills development. 12

Skills formation

There is some evidence, drawn from industry predictions and US studies, that the share of employment taken by local residents will expand over time, as the industry becomes more established in the region (Regeneris, 2011: 41). Indeed, there are limited but encouraging signs to indicate that entry-level vacancies are actively marketed to the local labour force. 13 Nevertheless, a more substantive shift in spatial employment patterns will depend crucially upon the development of the skills required within the local labour force. Hence, AMEC (2013: xiv, 50, 83–84) argues that maximising local economic impact is dependent upon local labour market training and the establishment of apprenticeship schemes.

In the absence of a tailored skills training programme, and even at this early stage of development, industry sources have already expressed concern over skills shortages and labour force bottlenecks. Thus, the IOD (2013: 18) found that 68% of offshore contractors and 75% of operators had experienced problems in recruiting suitable employees in particular occupations within the industry. Moreover, within the oil and gas industry more generally, an EY survey found that a majority of respondents raised concerns that attracting suitably qualified individuals was the primary factor limiting growth in their organisation (IOD, 2013: 144).

One possible response to this skilled labour supply bottleneck might involve the continued use of short-term contracts and the development of a dual labour market. Hence, it may prove to be cost effective to import and adapt an existing highly skilled workforce, from Scotland and the shale gas fields currently being worked in the USA, rather than invest in the training of local residents. This cost–benefit calculation is unlikely to encompass lesser skilled occupations, as these will require less training investment and generic equivalent skills amongst the local labour force are likely to be more plentiful. Nevertheless, there would be a smaller local economic impact if a dual labour market emerged, with better paid, high skilled jobs to be imported for a transitory period whilst lower skill, lower paid jobs were more easily accessible by the resident labour force.

In the US shale gas industry, similar labour supply constraints were experienced (MSETC, 2011: 28) and various skills training programmes were developed as a result. The most notable of these are the Petroleum Services Programme (Nicholls State University, Louisiana) and the Shale training and Education Centre (ShaleTec), formerly the Marcellus Shale Education and Training Centre (MSETC); the latter was formed out of a partnership between Pennsylvania College of Technology and Penn State Education, with some smaller initiatives investigated in the New York State (Jacquet, 2011: 1–2, 15–16). These initiatives provide bespoke training for the shale gas industry and were formed at least partly to coordinate curriculum development and to overcome a high spatial distribution of workers and training providers. To facilitate this supply-side development, these centres received significant public as well as industry financial investment. Indeed, ShaleTec/MSETC alone benefitted from Federal and State grants totalling £10.5m (US$17.6m) (MSETC, 2011: 52).

The need for skills training and academic research focused upon the needs of the shale gas industry has been noted by the House of Commons Energy and Climate Change Committee (2013: 38), which emphasised the importance of the establishment of partnerships between the shale gas industry and local educational providers, particularly universities, in reducing these labour supply constraints. However, aside from industry-funded small-scale initiatives, there has been nothing comparable to the US education and training centres in the UK. This may be one area where a public–private partnership may be able to facilitate the development of an emerging industry, whilst simultaneously attempting to increase the local economic impact arising out of its expansion. It might be one area where local stakeholders and their representatives might engage with national government to seek pump-priming investment with the dual purpose of resolving skills bottlenecks whilst simultaneously enhancing local economic gain.

One such proposal has been advanced by the Lancashire Local Economic Partnership, whereby £6.2m would be invested in developing Blackpool and Fylde's College facilities in order to meet some of the skill requirements of the shale gas industry. It is proposed that this initiative might dovetail with a new national government proposal, namely to develop specialist colleges delivering the skills training needed for the sector. 14

Supply chain

In terms of supply chain development, the economic benefits derived from agglomeration effects, through the clustering of firms involved in a given industry and resultant R&D spillovers, have been extensively highlighted in the academic and business literature (Audretsch and Feldman, 1996; Cumbers et al., 2003; Porter, 1990, 1998). However, the existence of oil and gas supply chain clusters, focused upon Aberdeen which benefitted from its locational advantages for North Sea offshore exploration, may frustrate the organic development of a shale gas support network in the Lancashire area.

The offshore oil and gas industry supply chain is estimated to account for 1100 companies achieving combined revenues of £27bn in 2011, contributing £6bn in corporation and payroll taxes, and supporting around 440,000 jobs across the UK (IOD, 2013: 59). Approximately 45% of the total oil and gas industry jobs in the UK are concentrated in Scotland (Oil and Gas, 2012). Thus, whilst the location of certain elements of the shale gas supply chain spatially close to the centre of the industry, pre-existing specialisation in Scotland and the South East may draw additional investment outside of the Lancashire area in the absence of policy initiatives to retain significant local benefit. For example, it is anticipated that the shortage of onshore drilling rigs may be met by the Wier Group, which is based in Scotland, rather than via a new manufacturing site established in the North West (IOD, 2013: 143).

Encouragement of a clustering of onshore shale gas supply chain companies, within the Bowland-Hodder field, would not only enhance local economic impact, but would additionally contribute towards the rebalancing of the UK economy – a stated UK government objective (HM Treasury, 2014: 12). 15 Rather than further stimulate existing agglomeration clusters in and around Aberdeen and Greater London – both areas of the UK with above average levels of Gross Value Added (GVA) 16 – the Lancashire area has below UK average GVA and would thereby narrow, rather than exacerbate, regional differentials (ASHE, 2012; LCC, 2009). Policy responses could include targeted fiscal incentives, dependent upon the spatial location of corporate activity by value. Another might be to build up local partnerships between business and universities, to create support networks and R&D spillovers which might attract inward investment.

One recent industry-led initiative has led to the creation of the North West Energy Taskforce, supported by over 100 businesses, largely located within the region, alongside local Chambers of Commerce. 17 One of its most prominent initiatives, to date, has been the organisation of a Shale Gas Supply Chain Conference (Winter Gardens, Blackpool, 24 April 2014), resulting in the participation of more than 300 businesses, to discuss the potential development of supply chain links within the region. The Chair of the Blackpool, Fylde and Wyre Economic Development Company, closed the conference by warning participants that a lack of local support led to Dundee being overlooked in favour of Aberdeen as a base for North Sea oil offshore operations, and expressing the desire that Lancashire did not make the same mistake with an emerging onshore shale gas industry. 18

Fiscal policy

The final aspect of public policy consideration relates to fiscal policy considerations related to the shale gas industry. One element of this arose in response to local opposition to future drilling activities, the shale gas and oil industry developed a Charter whereby it commits to providing £100,000 in community benefits for each well site where fracking occurs, and 1% of revenues to local and regional communities; the latter split two-thirds to local and one-third to county levels (UKOOG, 2014). This revenue stream would be channelled through a newly established Community Foundation for Lancashire, with the stated aim to: work with and for local communities in a robust, effective and fully transparent independent process, supporting local people to define local communities and their priorities, including the appointment of a community panel to recommend how the money will be spent.

19

A similar scheme has operated in Lancashire, as landfill operators have contributed part of their landfill tonnage tax to not for profit bodies such as the Lancashire Environmental Fund (managed by Lancashire Wildlife Trust), and thereby funded projects part compensating the community and environment that have suffered through the negative externalities effects of landfill activity. These community payments, are, naturally, tax deductable (Wood, 2014).

One estimate suggests that this could provide between £3 and £12m of initial benefit to local communities, with a further £0.3–£0.6bn arising from production contributions, depending upon the size and duration of extraction (AMEC, 2013: 84, 122). However, the industry proposal has been labelled ‘derisory’ by Northern Members of Parliament, ‘seriously flawed’ by some of the more vigorous supporters of the shale gas industry 20 and has been rejected as insufficient by the Local Government Association (LGA) (House of Lords Economic Affairs Committee (2014a: 36, Ev 147–148).

This has led, in turn, to consideration as to whether local authorities, in affected areas, might be able to retain 100% (as opposed to the usual 50%) of business rates, for shale gas operations (House of Lords Economic Affairs Committee, 2014a: 38, 2014b: Ev 166). Based upon an assumption, made by Deloitte (2013: 1, 10), that local authorities would receive 2% revenue in the form of business rates, this would equate to in excess of £54.5 million per annum; a total equivalent to 3% of Lancashire County Council expenditure (Deloitte, 2013: 1, 10).

Nevertheless, this proposed distribution of revenues, derived from shale gas extraction activity, remains problematic for two main reasons. Firstly, despite a number of announcements and proposals, emanating from national government and industry sources, the precise magnitude and mode of distribution of the proposed community benefit remains unresolved. Indeed, there have been suggestions that any such arrangements might be open to investigation from the European Commission, pertaining to whether this qualifies as state subsidy, which is prohibited under single market legislation. 21 Secondly, however, the distributional balance of benefits, between industry, national and local stakeholders, would appear to many to remain inequitable.

Pressure for an improved distribution to local communities has included a letter sent to the Prime Minister, written by local Members of Parliament from all three main political parties, alongside the leader of five affected local authorities, 22 arguing that local communities needed to receive more direct benefits to allay concerns over shale gas exploration. The letter argues that shale gas had the potential to produce significant economic benefits – specifically to facilitate ‘a second industrial revolution and to rebalance Britain's economic output’. However, the signatories were united in their opinion that a 1% share does ‘not go nearly far enough’, and that, in the absence of ‘significant retention’ of economic benefits within the local economy, they would ‘find it difficult to support further development in Lancashire’. 23 Suggesting that national taxation may potentially absorb up to a combined 62% of revenues from the industry, Conservative MP for Preston North and Wyre Ben Wallace argued that the proposed distribution of rewards to local communities represented ‘crumbs’ and should be increased substantially. 24 The LGA has made a counter proposal which would involve 10% of revenues from shale gas production being transferred to local communities to secure ‘real strategic and additional advantage for the area’. 25

The national UK budget has identified tax reforms to stimulate the development of the shale gas industry, including a new pad tax allowance of £20m per year (HM Treasury, 2014: 35, 58). Indeed, these fiscal incentives have been identified as providing the UK shale gas industry with the most competitive tax regime in Europe and lower than equivalent rates in the US (UK Treasury, 2013: 49). Set against the rather modest proposals intended to benefit local communities, and it is clear why the conflict over the distribution of shale gas benefits is likely to continue.

Furthermore, the prioritisation of tax incentives for shale gas companies has been challenged as ‘questionable’ by the House of Lords Economic Affairs Committee (2014a: 39, Ev 169–170), given that taxation did not appear to be a significant factor, in evidence put before the committee, in preventing the expansion of the industry. This conclusion would seem to reinforce the other evidence presented in this paper, in that a case could be made for a shift in terms of existing fiscal support for the development of the shale gas industry, away from tax incentives and towards targeted interventions, located within affected communities, intended to enhance local skills and attract large segments of the shale gas supply chain, and thereby maximise local economic benefit.

Conclusion

The proposed expansion of shale gas extraction has been championed at national level, by government and industry sources, but the reaction in communities surrounding the shale gas fields has been markedly less enthusiastic. One reason for this may be that external costs will be likely to be borne by local residents, but the economic advantages, identified by successive reports, may provide more benefit elsewhere in the national or international economy, and thereby generate only modest local gain. Indeed, early studies tend to suggest that this scenario is likely to occur without a substantive shift in employment patterns, to create more job opportunities for local residents and without a marked increase in the proportion of the shale gas supply chain located within the local economy.

The paper has suggested that, although some of this effect may occur organically, the existence of established agglomeration advantages in Scotland and the South East of England, created through servicing offshore oil and gas extraction, may necessitate direct policy intervention to secure the desired level of local economic impact. This may involve the creation of a research and skills educational institution, to reduce labour supply problems for the industry and enhance the employability of the local labour force. It may also require fiscal and/or spillover incentives to attract investment into the local economy to service the shale gas industry. This may, additionally, require central government support for shale gas expansion to be redirected and focused upon these areas of greatest potential.